did’s specialized solutions mobilizationagriculturaltechnologicaltraining surveillance of...

TRANSCRIPT

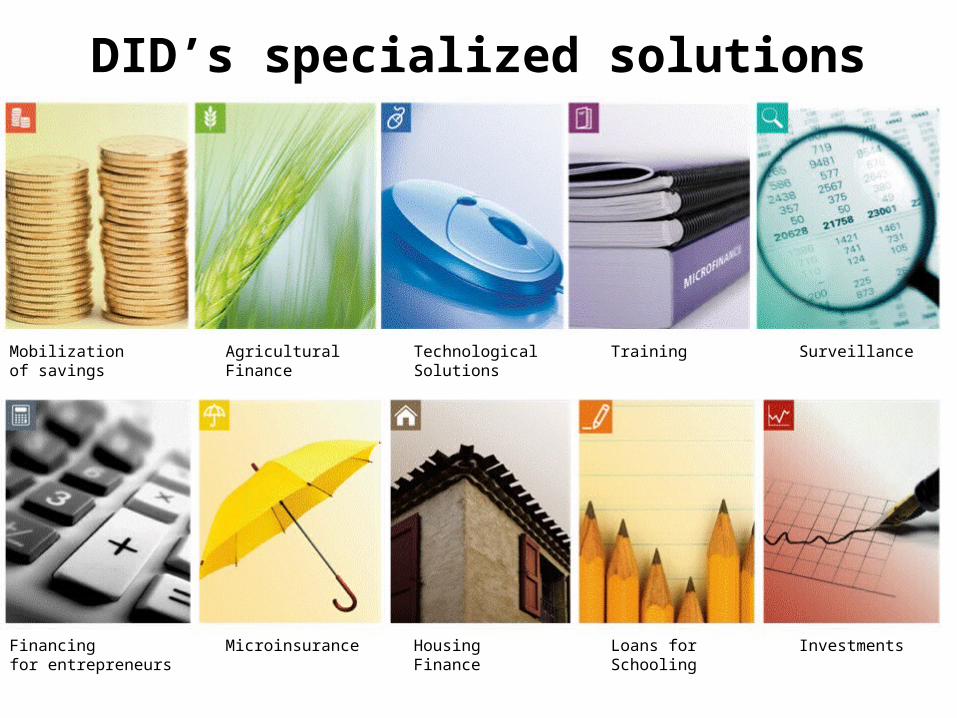

DID’s specialized solutions

Mobilization Agricultural Technological Training Surveillanceof savings Finance Solutions

Financing Microinsurance Housing Loans for Investmentsfor entrepreneurs Finance Schooling

MOBILIZATION OF SAVINGS

Offer leverage for economic development and autonomy

• DID assists its partners (MFI, central banks, etc.) in the design, delivery and marketing of savings products and services

• DID provides MFI the adequate coaching : management of financial risks, technology, training, internal controls and infrastructure

• DID offers education about savings to the population in general

AGRICULTURALFINANCE

Sustain economic development, profitability of agricultural activities and food security

•A diagnostic tool to determine the offer for agricultural credit

•A methodology for analyzing the potential of a supply chain

•Specific training programs for agricultural financing

•Financial services adapted to the various needs of the rural clientele:

-Operating , warehouse, investment credits

-Loan life insurance plan

-Indexed crop insurance

TECHNOLOGICAL SOLUTIONS

Improving performance for financial institutions but also, increasing security and

accessibility of financial services

•SYSDE-SAF transactional program

•Mobile application for information on operations (AMIO)

•Stratego decision-making support system

•Computerized data processing centre (CTI)

•Smart cards

•Intercoop transaction system

•MFI Outlets in town/village market(s)

•Credit+ tool for risk analysis

TRAINING

Develop quality services for members and clients

• Toolkits for setting up a training service within an MFI

•International and institutional seminars (strategic financial management, governance, challenges or training for MFI operators, etc.)

•Specialized international seminars on operational and critical management issues

•Task-based training programs for managers, loan officers and tellers

•Training program for managing and operating savings and credit cooperatives

SURVEILLANCE

Increase the confidence of depositors in microfinance institutions

Our expertise:

Prevention• Legal and regulatory framework

Supervisory activities• Internal control systems• Inspection• External audit

Protection• Security fund

FINANCING FOR ENTREPRENEURS

Supporting the business projects of small and medium entrepreneurs

Two specific business models for SMEs are offered in these two financial institutions models:•EFC Alliance•EFC operator-investor : build, operate and transfer

•Entrepreneurs benefit from sustainable access to financial services adapted to their specific needs.

•Financial institutions gain access to specialized expertise in financing for entrepreneurs

MICROINSURANCE

Reduce the vulnerability of families in the event of unexpected situations

Our adapted tools:

•Loan insurance

•Health insurance

•Indexed agricultural insurance

•Funeral insurance

Desjardins: number one insurer in Québec

HOUSINGFINANCE

Facilitate access for families to healthy and secure housing

Our expertise

•Start up of specialized units dedicated to housing finance within MFIs

•Implementation of decision support systems• •Market analysis and definition of housing finance products and services

•Market positioning, business models and commercialization

•Evaluation of government policies and programs

•Definition of a sector-based approach

LOANS FORSCHOOLING

Facilitating access to education and improving conditions for success

DID helped Haitian financial cooperatives to design, deploy and manage this financial product: schooling loans.

The role of DID consists of:•Establishment of coordination among schools, school officials, parents and the financial cooperatives

•Product design and methodologies to deliver and oversee credit for school fees

•Production of the toolkit related to product design and follow-up

•Training of the staff in the financial cooperatives offering the product

•Monitoring of results

INVESTMENTS

Support the growth and development of microfinance

Our experts analyze applications received, proceed with necessary due diligence, propose terms and conditions for loans or investments and establish partnerships that make it possible to conclude these operations.

The institutions financed receive the support of our experts during investment follow up.

DID manages two funds that promote access to financial resources and thereby provide leverage for development and growth in the microfinance sector.

Partnership Fund(capitalization: CAN$22 million)

Desjardins Fund for Inclusive Finance(capitalization: CAN$10 million)

FINANCING FOR ENTREPRENEURSSupporting the business projects of small and medium entrepreneurs

DID’s Entrepreneurs

Financial Centres (EFC)

How DID contributes to MSME finance and its challenges?

Our answer: Implement business centres specifically for entrepreneurs/MSME, called “EFC”.

• Two business models are offered:

– Affiliated EFC

– EFC operator-investor : build, operate and transfer

• Entrepreneurs benefit from sustainable access to financial services adapted to their specific needs.

• Financial institutions gain access to specialized expertise in financing for entrepreneurs.

What is a EFC?• Entrepreneurs Financial Centres

– Based on Desjardins Group’s initiative– A specialized department within a network of savings

and credit cooperatives– a local microfinance institution offering financial

services for the SME market

• Local and collective ownership• In addition to financial experts (credit, savings)

– Experts in housing finance– Experts in insurance– Etc.

Affiliated EFC EFC operator-investor

Burkina Faso Panama

Mali Tanzania

Senegal Uganda

Zambia

EFC in operation, with DID’s collaboration

DID’s Affiliated EFC

What is an Affiliated EFC ?

• It’s an extension of an already existing financial institution

• It increases the range of services offered to the members and clients

• It maximizes staff performance

• It optimizes the quality of service delivered to entrepreneurs

Sample Organization Chart of an Affiliated EFC

FI FI FIFIFIFI

Coordinating Committee

EFC Technical Director

Personnel

Regional Union

Federation

Hiring and oversightMonitoring of budget, financial results and business plan

Credit Committee

Supervision and support for the financial institutions (FI)

Characteristics of an Affiliated EFC

• The EFC works for and on behalf of its participating financial institutions :– The member can do business with its financial

institution and the EFC at the same time: One financial institution can then respond to its personal and professional needs.

– The EFC’s powers and responsibilities are defined legally and are validated by Board of Directors of the financial institution

– Managers, Union and Federation are all responsible for global management follow-up of the financial institution

Affiliated EFC: Conditions of success

• Continuous commitment of the managers

• Trust relationship between the managers and the supervision structures

• Commitment to action and openness to change

• Common vision and shared business objectives

• Customer-loyalty approach, business development and adequate consulting expertise and techniques

• EFC visibility and its positioning in the market

In the end, the Affiliated EFC is a solution that:

• Reaches the market needs

• Increases financial institutions profitability

• Increases the cooperative character of the network

• Allows the women and the young people to have access to credit

DID’s EFC « operator-

investor »(O/I)

Deployment of CFE-O/I : Prerequisites

Capital and technical

assistance financing

Partnerships

EFC-O/I : DID’s Strategy

• Establish local financial institution with the mission to supply suitable financial products and services to local MSMEs

• Offer financial products adapted to the needs of the local MSMEs

• Encourage the development of the private sector• Community-owned and managed EFCs• Transfer of expertise (build, operate, transfer)• Set-up mechanisms to allow “clients users” of

the EFCs to become owners

EFC O/I vs local ownership: two ways to consolidate

• Employee share ownership programs (ESOP) • Client share ownership programs (CSOP)

The impacts on both EFCs

business models

The EFCs have a considerable impact in their milieu, because they contribute to:• Growth for MSMEs and the feeling of pride that results• Job creation• Economic development in communities• Improved credit management practices in financial

institutions • Increased management capacity• Growth and profitability for financial institutions linked

to the EFC

Lessons learned: Affiliated EFC and EFC-O/I

• To be implemented successfully, the EFCs require:

– A good start-up

– An organizational governance

– An operational governance

– Operations (marketing, credit, administration, management)

– Adequate technological solutions

– A good marketing approach

– Continuous training for officers and managers

Lessons learned: Affiliated EFC and EFC-O/I

• Deploying EFCs take…

– Time • Identify, analyze and conclude in the potential,

install the institutional capacity. • Identify and mobilize resources• Adapt the tools and methodology to the country

– Resources• Human, financial and technological ones

AGRICULTURE FINANCEAccompany farmers facing the challenges of modernization and diversification

Other challenges:

DID’s service offer in

Agricultural Finance

AGRICULTURE FINANCEAccompany farmers facing the challenges of modernization and diversification

What we do…

•Diagnosis the agricultural credit offer

•Analysis of the potential of a supply chain

•Human resource planning

•Specific training programs for agricultural financing

•Financial services adapted to the various needs of the rural clientele:

-Operating credit

-Warehouse credit

-Investment credit

-Loan life insurance plan

-Indexed crop insurance

The equilibrium principle

Fin

anci

al

serv

icesTe

chni

cal

expe

rtis

e

Mar

ketin

g Ris

k m

itiga

tion

AGRICULTURAL DEVELOPMENTEQUILIBRIUM

Agricultural development will be more sustainable if all pillars are strengthened, but also if there are reinforcements of the links between each pillars

The pillar of financial services

The equilibrium principleDID considers that access to adapted financial services must be increased in order to support the development of the agricultural and agri-food sector, but also recognizes that strengthening the financial institutions, albeit essential, cannot support the development of the sector on its own .

The “pillars of equilibrium”

APPROPRIATE LEGISLATION to SECURE ACCESS to LAND and

WATER

Technical expertise

MarketingFinancial services

Risk mitigation

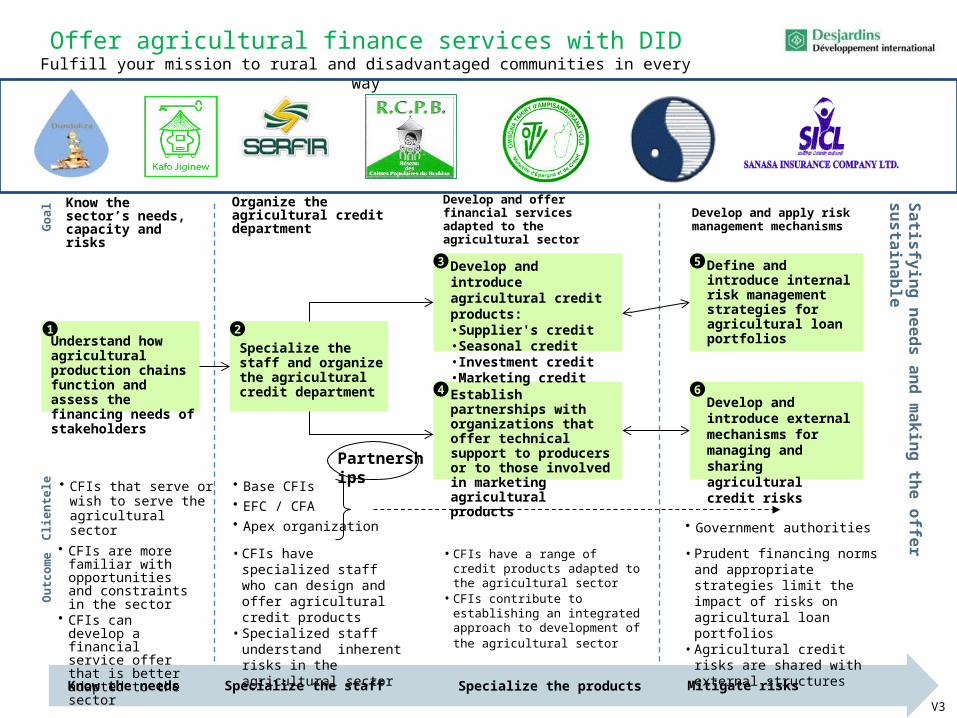

Offer agricultural finance services with DIDFulfill your mission to rural and disadvantaged communities in every way

Know the sector’s needs, capacity and risks

Organize the agricultural credit department

Develop and offer financial services adapted to the agricultural sector

Develop and apply risk management mechanisms

Specialize the staff and organize the agricultural credit department

Understand how agricultural production chains function and assess the financing needs of stakeholders

Define and introduce internal risk management strategies for agricultural loan portfolios

Develop and introduce agricultural credit products:•Supplier's credit•Seasonal credit•Investment credit•Marketing credit

1 2

3 5

64

Go

al

Know the needs Specialize the staff Mitigate risks

• CFIs have specialized staff who can design and offer agricultural credit products

• Specialized staff understand inherent risks in the agricultural sector

Ou

tco

me

• CFIs are more familiar with opportunities and constraints in the sector

• CFIs can develop a financial service offer that is better adapted to the sector

• CFIs have a range of credit products adapted to the agricultural sector

• CFIs contribute to establishing an integrated approach to development of the agricultural sector

• Prudent financing norms and appropriate strategies limit the impact of risks on agricultural loan portfolios

• Agricultural credit risks are shared with external structures

Clie

nte

le • CFIs that serve or wish to serve the agricultural sector

• Base CFIs • EFC / CFA • Apex organization • Government authorities

V3

Establish partnerships with organizations that offer technical support to producers or to those involved in marketing agricultural products

Partnerships

Specialize the products

Sa

tisfy

ing

ne

ed

s a

nd

ma

kin

g th

e o

ffer s

us

tain

ab

le

Develop and introduce external mechanisms for managing and sharing agricultural credit risks

www.did.qc.ca