dg method for the numerical pricing of path...

TRANSCRIPT

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

DG method for the numerical pricing ofpath-dependent multi-asset options

Jirı Hozman 1 and Tomas Tichy 2

1Technical University of Liberec 2VSB-TU OstravaFaculty of Science, Humanities and Education Faculty of Economics

Programy a algoritmy numericke matematiky 18Janov nad Nisou,

June 19 – 24, 2016

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 1 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Outline

1 MotivationFinancial backgroundBasket optionsAsian options

2 Path-dependent multi-asset options

3 Asian two-asset option with floating strikePDE formulationWeak formulationDG discretizationNumerical experiments

4 Asian two-asset option with fixed strikeSimilar approachNumerical experiments

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 2 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

1 Motivation

2 Path-dependent multi-asset options

3 Asian two-asset option with floating strike

4 Asian two-asset option with fixed strike

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 3 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Objects of our interest

to develop efficient, accurate and robust numerical scheme forthe simulation of option pricing problem within DG technique,

to optimize particular steps of the approximation to obtaincorrect results attainable in a reasonable time,

to be robust with respect to various types of options as well asmarket conditions,

to analyze the impact of various approaches

to examine the computational error and demandingness

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 4 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

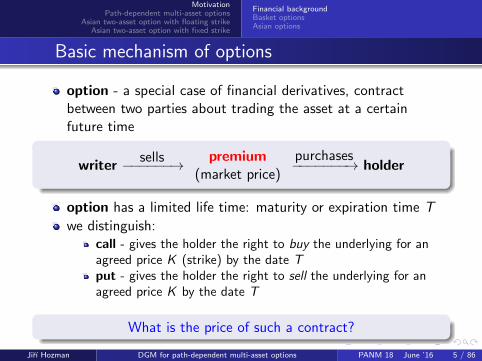

Basic mechanism of options

option - a special case of financial derivatives, contractbetween two parties about trading the asset at a certainfuture time

writersells−−−−−−→ premium

(market price)

purchases−−−−−−−→ holder

option has a limited life time: maturity or expiration time T

we distinguish:call - gives the holder the right to buy the underlying for anagreed price K (strike) by the date Tput - gives the holder the right to sell the underlying for anagreed price K by the date T

What is the price of such a contract?

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 5 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

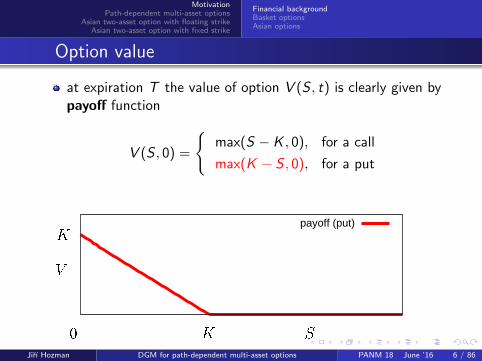

Option value

at expiration T the value of option V (S , t) is clearly given bypayoff function

V (S , 0) =

max(S − K , 0), for a call

max(K − S , 0), for a put

payoff (call)V j0 S K

1

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 6 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Option value

at expiration T the value of option V (S , t) is clearly given bypayoff function

V (S , 0) =

max(S − K , 0), for a call

max(K − S , 0), for a put

payoff (put)K V j0 K S

1

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 6 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Option value

at expiration T the value of option V (S , t) is clearly given bypayoff function

V (S , 0) =

max(S − K , 0), for a call

max(K − S , 0), for a put

But what about now?How much would you pay for such an option?How to calculate a fair value of the option?

Option pricing models

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 6 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Option value

at expiration T the value of option V (S , t) is clearly given bypayoff function

V (S , 0) =

max(S − K , 0), for a call

max(K − S , 0), for a put

But what about now?How much would you pay for such an option?How to calculate a fair value of the option?

Option pricing models

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 6 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Introduction to option pricing

a financial asset with tendency µ and volatility σ

dSt = St(µdt + σdWt), S0 known (1)

µ is drift of St , µ = r , where r is risk-free interest rate

Wt is a standard Brownian motion (BM)

for constant σ and r we have solution of SDE (1) as

St = S0e

(µ−σ2

2

)t+σWt (geometric BM)

option value at t is the expected profit at T discounted to t:

Ct = e−r(T−t) E(max(ST − K , 0)) (call)Pt = e−r(T−t) E(max(K − ST , 0)) (put)

due to the put call parity we can either compute calls or puts

Ct − Pt = St − Ke−r(T−t)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 7 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Numerical techniques for option pricing

1 Monte-Carlo simulations

Snk+1 − Sn

k = Snk (µδt + σ

√δtN (0, 1)), Sn

0 = S0

Ct = e−r(T−t) 1

N

N∑n=1

(max(SnT − K , 0)),

where N (0, 1) is approximated by random function

2 tree methods (Cox, Ross and Rubinstein binomial model)

3 PDE approach within Ito calculus

df (t,St) =∂f

∂tdt +

∂f

∂SdSt +

1

2

∂2f

∂S2(dStdSt)

−→ Black-Scholes (BS) equation

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 8 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

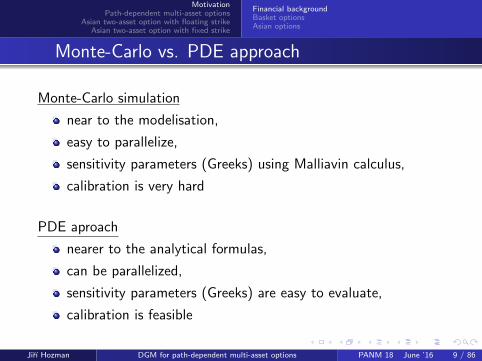

Monte-Carlo vs. PDE approach

Monte-Carlo simulation

near to the modelisation,

easy to parallelize,

sensitivity parameters (Greeks) using Malliavin calculus,

calibration is very hard

PDE aproach

nearer to the analytical formulas,

can be parallelized,

sensitivity parameters (Greeks) are easy to evaluate,

calibration is feasible

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 9 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Derivation of BS equation

We make the following assumptions:

the assets prices follow the lognormal random walk,

the risk-free interest rate r , the volatility σ are constant,

no transactions costs associated with hedging a portfolio,

no arbitrage possibilities,

the underlying assets pay no dividends,

trading of the underlying assets can take place continuously,

short selling is permitted and the assets are divisible.

We construct a portfolio of option and ∆ shares of the underlying

Π = V (S , t)−∆S

where V represents a long position (it is owned) and ∆S a shortposition (it is owed)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 10 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Derivation of BS equation

(A) the change in our portfolio from t to t + dt is completelyriskless (riskless portfolio), described by ODE,

dΠ = rΠdt

(B) equivalently, the change in our portfolio is also equal to

dΠ = dV −∆dS

and using Ito lemma with (dSdS) w σ2S2dt we have

dV =∂V

∂tdt +

∂V

∂SdS +

1

2σ2S2∂

2V

∂S2dt

i.e., the portfolio changes by

dΠ =

(∂V

∂t+

1

2σ2S2∂

2V

∂S2

)dt +

(∂V

∂S−∆

)dS

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 11 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

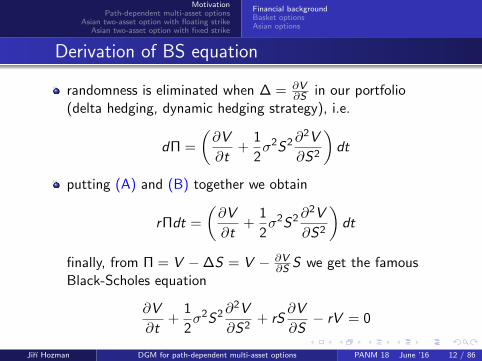

Derivation of BS equation

randomness is eliminated when ∆ = ∂V∂S in our portfolio

(delta hedging, dynamic hedging strategy), i.e.

dΠ =

(∂V

∂t+

1

2σ2S2∂

2V

∂S2

)dt

putting (A) and (B) together we obtain

rΠdt =

(∂V

∂t+

1

2σ2S2∂

2V

∂S2

)dt

finally, from Π = V −∆S = V − ∂V∂S S we get the famous

Black-Scholes equation

∂V

∂t+

1

2σ2S2∂

2V

∂S2+ rS

∂V

∂S− rV = 0

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 12 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Black-Scholes (BS) equation

derivation of BS equation [Black, Scholes, 1973],

a Nobel prize was awarded in 1997

∂V

∂t+

1

2σ2S2∂

2V

∂S2+ rS

∂V

∂S− rV = 0

o V = V (S , t; T ,K , r , σ) - value of optiono t, 0 ≤ t ≤ T - current time, T − t - time time to expirationo S - price of stock at time t, i.e. S = S(t), S ∈ (0; +∞)o r , r > 0 - risk-free interest rateo σ, σ > 0 - volatility of price So K - strike price

backward linear parabolic differential equation

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 13 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Black-Scholes formula

by transforming the Black-Scholes PDE into the heat equationwith reversal time

Black-Scholes formula

Ct = StΦ(d1)− Ke−r(T−t)Φ(d2),

Pt = −StΦ(−d1) + Ke−r(T−t)Φ(−d2)

where

d1 =ln(St/K ) + (r + σ2/2)(T − t)

σ√

T − t, d2 = d1 − σ

√T − t

and Φ denotes the cumulative distribution function of thestandard normal distribution

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 14 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

BS equation – numerical experiments

real data of the DAX on 15SEPT2011 with implied volatilities,

expiration date T = 0.50137 (half year),

risk-free interest rate r = 0.0176,

uniform space-time grid with constant mesh step h andconstant time step τ ,

DG piecewise P3 (cubic) approximations,

sensitivity measures (Greeks):

∆ =∂u

∂xand Γ =

∂2u

∂x2

we investigate the behaviour of approximation values ofoption and Greeks w.r.t. the choice of b.c.

reference DAX data at underlying’s price x = 5508.238(star-symbol in graphs)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 15 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Put options - comparison at expiration date

opt. val. and Greeks (Dirichlet b.c., K = 4000), ref. val.(∗)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 16 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Put options - comparison at expiration date

opt. val. and Greeks (Neumann b.c., K = 4000), ref. val.(∗)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 16 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Put options - comparison at expiration date

opt. val. and Greeks (transparent b.c., K = 4000), ref. val.(∗)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 16 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Limitations and generalizations of the BS model

idealized assumptions are rarely valid in the real world

normal distribution of log-returnsconstant model parameters

important market features are not captured by BSM

volatility clustering and leverage effectvolatility smile

generalizations of BS framework

assumptions of non-constant deterministic (e.g. localvolatility) or stochastic parameters (e.g. Heston model)other models of the price movements instead of diffusion one(in BS model) such as jump-diffusion model (leading to PIDE)or pure jump model (e.g. VG model)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 17 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

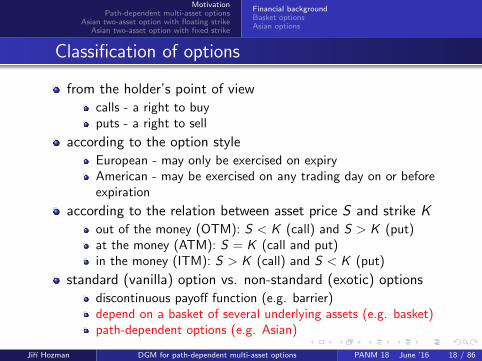

Classification of options

from the holder’s point of viewcalls - a right to buyputs - a right to sell

according to the option styleEuropean - may only be exercised on expiryAmerican - may be exercised on any trading day on or beforeexpiration

according to the relation between asset price S and strike Kout of the money (OTM): S < K (call) and S > K (put)at the money (ATM): S = K (call and put)in the money (ITM): S > K (call) and S < K (put)

standard (vanilla) option vs. non-standard (exotic) optionsdiscontinuous payoff function (e.g. barrier)depend on a basket of several underlying assets (e.g. basket)path-dependent options (e.g. Asian)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 18 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Basket options

generally, dimension d ≥ 2 ⇒ multi-asset options

option depending on a basket of two underlying assets

price of 1st asset S1

price of 2nd asset S2

⇒ value of basket option V (S1, S2, t),

movement of stock prices is driven by SDEs

dS1(t) = rS1(t)dt + σ1S1(t)dW1(t)

dS2(t) = rS2(t)dt + σ2S2(t)dW2(t)

with correlated Wiener processes, i.e., dW1(t)dW1(t) = ρdt,

Sk(t) - prices of stock at time t, 0 ≤ Sk<∞, k = 1, 2,

r , r > 0 - risk-free interest rate,

σk , σk > 0 - volatility of the k-th price Sk , k = 1, 2

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 19 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

2D Black-Scholes equationanalogous approach to 1D BS model with risk-free portfolio

Π = V (S1, S2, t)−∆1S1 −∆2S2

application of multidimensional Ito calculus

delta hedging with ∆1 = ∂V∂S1

and ∆2 = ∂V∂S2

generalization of BS equation into 2D

−∂V∂t

+1

2σ2

1S21∂2V

∂S21

+ρσ1σ2S1S2∂2V

∂S1∂S1+1

2σ2

2S22∂2V

∂S22

+rS1∂V

∂S1+rS2

∂V

∂S2= rV

V = V (S1, S2, t; T ,K , r , σ1, σ2, ρ) - value of optiont, 0 ≤ t ≤ T - time to expiration, T − t - current time

reversal time ⇒ initial condition is given by payoff function

V (S1, S2, 0) = max(α1S1 + α2S2 − K , 0) (call)V (S1, S2, 0) = max(K − α1S1 − α2S2, 0) (put)

, αk > 0, α1+α2 = 1

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 20 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Basket options – numerical experiments

Parameter settings:

basket put option with 60% Allianz (α1 = 0.6) and40% Deutsche Bank (α2 = 0.4), strike at 40 Euro

current date: September 13, 2011 (Tuesday),

piecewise constatnt volatilities σ1 and σ2,

expiration date T = 0.257534 (i.e. 94 days),

risk-free interest rate r = 0.01557 p.a.,

Pearson linear correlation ρ = 0.88

maximal stock prices Smax1 = 130.0 and Smax

2 = 220.0,

two stocks trades at S ref1 = 59.79 and S ref

2 = 23.40

Implementation settings:

adaptively refined grid, constant time step τ = 1/365

piecewise P1 (linear) approximations, sparse solver GMRES

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 21 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Basket options - numerical results

space-time plot of solution at maturity

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 22 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Asian options

be introduced to avoid the manipulation of prices onexpiration date −→ less sensitive to market fluctuations,

a representative of the class of path dependent options,

value of Asian option V = V (S ,A, t) depends also on theaverage A of the price of the underlying assets

we distinguish

fixed strike

floating strike×

continuous

discrete×

arithmetic averaging

geometric averaging

average of the stock price at time t is given by

A =1

t

∫ t

0S(u)du

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 23 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Asian options

movement of the stock price is driven by SDE

dS(t) = rS(t)dt + σS(t)dW (t)

movement of the average-variable is driven by ODE

dA(t) =1

t

(S(t)− A(t)

)dt

r , r > 0 - risk-free interest rate (constant),

σ, σ > 0 - volatility of the price S (constant)

analogous approach to 1D BS model with risk-free portfolio

Π = V (S ,A, t)−∆S

application of multidimensional Ito calculus

delta hedging with ∆ = ∂V∂S

we obtain 2D PDE model of Asian options

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 24 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

2D PDE model of Asian options

continuous arithmetic Asian options with fixed strike

∂V

∂t− σ2S2

2

∂2V

∂S2− rS

∂V

∂S− S − A

T − t

∂V

∂A+ rV = 0

V = V (S ,A, t; T ,K , r , σ) - value of optiont, 0 ≤ t ≤ T - time to expiration, T − t - current time

parabolic PDE degenerated in variable A

reversal time ⇒ initial condition is given by payoff function,

V (S ,A, 0) = max(A− K , 0) (call with fixed strike)

V (S ,A, 0) = max(K − A, 0) (put with fixed strike)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 25 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Asian options – numerical experiments

Parameter settings:

Asian puts on German stock market index DAX,

real data of the DAX on 15SEPT2011 with implied volatilities,

expiration date T = 0.50137 (half year, 183 days),

strike K = 4000,

constant volatility σ = 0.4594,

constant risk-free interest rate r = 0.0176,

maximal stock price Smax = Amax = 2K (usually),

reference node Sref = 5508

Implementation settings:

uniform grid, constant time step τ = 1/365,

piecewise P1 (linear) approximations, sparse solver GMRES

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 26 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Asian options - numerical results (1)

space-time plot of solution at t = 0 days (initial state)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 27 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Asian options - numerical results (1)

space-time plot of solution at t = 92 days (mid state)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 27 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Asian options - numerical results (1)

space-time plot of solution at t = 183 days (final state)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 27 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Asian options - numerical results (2)

isovalues of solution at t = 0 days (initial state)

A

0 S

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 28 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Asian options - numerical results (2)

isovalues of solution at t = 92 days (mid state)

A

0 S

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 28 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Financial backgroundBasket optionsAsian options

Asian options - numerical results (2)

isovalues of solution at t = 183 days (final state)

A

0 S

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 28 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

1 Motivation

2 Path-dependent multi-asset options

3 Asian two-asset option with floating strike

4 Asian two-asset option with fixed strike

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 29 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

General model of path-dependent multi-asset options

combination of basket and path-dependent options

simplification: basket options with 2 assets

price function V = V (S1(t), S2(t),A(t), t) depends on twocorrelated price processes

dSk(t) = rSk(t)dt + σkSk(t)dWk(t), k = 1, 2

and on path-dependent variable (in general form)

A(t) =1

t

∫ t

0g(S1(u), S2(u), u)du (continuous case)

driven by ODE (with drift component only)

dA(t) =1

t

(g(S1(t),S2(t), t)− A(t)

)dt

where g is given according to specific type of option

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 30 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

General model of path-dependent multi-asset options

analogous approach to basket and Asian options with portfolio

application of multidimensional Ito calculus

delta hedging with ∆1 = ∂V∂S1

and ∆2 = ∂V∂S2

3D PDE model of path-dependent two-asset options

∂V

∂t+

1

2σ2

1S21

∂2V

∂S21

+ρσ1σ2S1S2∂2V

∂S1∂S1+

1

2σ2

2S22

∂2V

∂S22

+rS1∂V

∂S1+ rS2

∂V

∂S2+

1

t

(g(S1, S2, t)− A

)∂V

∂A− rV = 0

V = V (S1, S2,A, t; T ,K , r , σ1, σ2, ρ) - value of optiont, 0 ≤ t ≤ T - current time, T − t - time to expiration

parabolic PDE degenerated in variable A

backward PDE ⇒ terminal condition is given by payoff

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 31 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Asian two-asset basket option

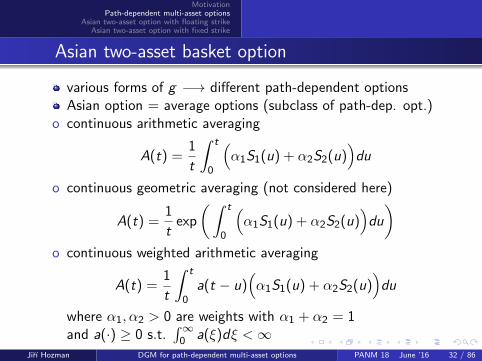

various forms of g −→ different path-dependent optionsAsian option = average options (subclass of path-dep. opt.)

o continuous arithmetic averaging

A(t) =1

t

∫ t

0

(α1S1(u) + α2S2(u)

)du

o continuous geometric averaging (not considered here)

A(t) =1

texp

(∫ t

0

(α1S1(u) + α2S2(u)

)du

)o continuous weighted arithmetic averaging

A(t) =1

t

∫ t

0a(t − u)

(α1S1(u) + α2S2(u)

)du

where α1, α2 > 0 are weights with α1 + α2 = 1and a(·) ≥ 0 s.t.

∫∞0 a(ξ)dξ <∞

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 32 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Asian two-asset basket option: payoff function

function of average over some time period prior to expiry

2 ways how the average is incorporated into payoff

o average strike option (= option with floating strike)

V (S ,A,T ) = max(α1S1(T ) + α2S2(T )− A(T ), 0) (call)

V (S ,A,T ) = max(A(T )− α1S1(T )− α2S2(T ), 0) (put)

o average rate option (= option with fixed strike)

V (S ,A,T ) = max(A(T )− K , 0) (call)

V (S ,A,T ) = max(K − A(T ), 0) (put)

we focus on

Asian two-asset basket option with floating strike Asiantwo-asset basket option with fixed strike

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 33 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

1 Motivation

2 Path-dependent multi-asset options

3 Asian two-asset option with floating strike

4 Asian two-asset option with fixed strike

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 34 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

3D PDE model

continuous arithmetic Asian two-asset basket option withfloating strike

∂V

∂t+

1

2σ2

1S21

∂2V

∂S21

+ρσ1σ2S1S2∂2V

∂S1∂S1+

1

2σ2

2S22

∂2V

∂S22

+rS1∂V

∂S1+ rS2

∂V

∂S2+

1

t

(α1S1 + α2S2 − A

)∂V

∂A− rV = 0

V = V (S1, S2,A, t; T ,K , r , σ1, σ2, ρ) - value of optiont, 0 ≤ t ≤ T - current time, T − t - time to expirationS1, S2,A > 0 - underlying assets and average

backward PDE ⇒ terminal condition is given by payoff,

for t = 0 we obtain 2D Black-Scholes model

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 35 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

3D PDE model - boundary conditions (1)

localization problem on bounded domain

at far-field boundary (from asymptotic behaviour at infinity)

if V is call

limS1→∞

∂V∂S1

(S1,S2,A, t) = α1,

limS2→∞∂V∂S2

(S1,S2,A, t) = α2,

limA→∞ V (S1, S2,A, t) = 0,

and

if V is put

limS1→∞ V (S1,S2,A, t) = 0,

limS2→∞ V (S1,S2,A, t) = 0,

limA→∞ ∂V∂A (S1,S2,A, t) = 1,

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 36 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

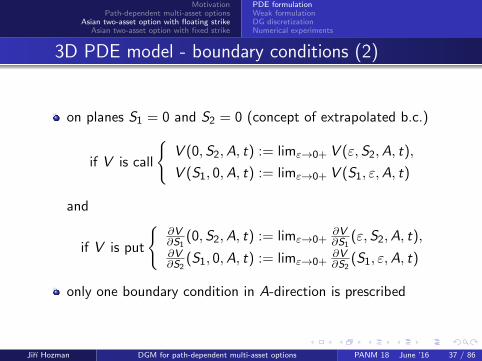

3D PDE model - boundary conditions (2)

on planes S1 = 0 and S2 = 0 (concept of extrapolated b.c.)

if V is call

V (0, S2,A, t) := limε→0+ V (ε, S2,A, t),

V (S1, 0,A, t) := limε→0+ V (S1, ε,A, t)

and

if V is put

∂V∂S1

(0,S2,A, t) := limε→0+∂V∂S1

(ε, S2,A, t),∂V∂S2

(S1, 0,A, t) := limε→0+∂V∂S2

(S1, ε,A, t)

only one boundary condition in A-direction is prescribed

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 37 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Dimensional reduction

to avoid the higher complexity of 3D model

change of variables (approach from [Ingersoll])

x1 =S1

A, x2 =

S2

A, t = T − t

transformation of price function

u(x , t) =1

AV (S1,S2,A, t), where x = [x1, x2]

transformation of payoffs (= initial conditions)

u(x , 0) = 1AV (S1,S2,A,T ) = max(α1x1 + α2x2 − 1, 0) (call)

u(x , 0) = 1AV (S1, S2,A,T ) = max(1− α1x1 − α2x2, 0) (put)

transformation of PDE: homogeneity w.r.t. A−→ separation of variable A −→ dimensional reductionfrom 3D to 2D

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 38 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

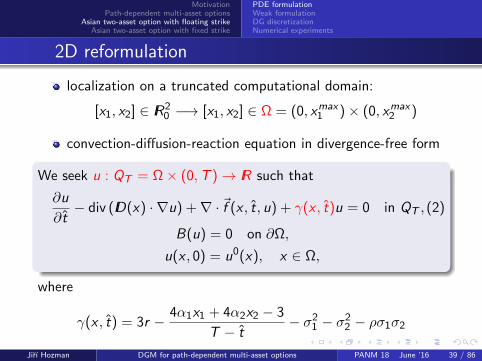

2D reformulation

localization on a truncated computational domain:

[x1, x2] ∈ IR20 −→ [x1, x2] ∈ Ω = (0, xmax

1 )× (0, xmax2 )

convection-diffusion-reaction equation in divergence-free form

We seek u : QT = Ω× (0,T )→ IR such that

∂u

∂ t− div (ID(x) · ∇u) +∇ · ~f (x , t, u) + γ(x , t)u = 0 in QT , (2)

B(u) = 0 on ∂Ω,

u(x , 0) = u0(x), x ∈ Ω,

where

ID(x) ≡ D(x)kl2k,l=1 =

1

2

(σ2

1x21 ρσ1σ2x1x2

ρσ1σ2x1x2 σ22x2

2

),

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 39 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

2D reformulation

localization on a truncated computational domain:

[x1, x2] ∈ IR20 −→ [x1, x2] ∈ Ω = (0, xmax

1 )× (0, xmax2 )

convection-diffusion-reaction equation in divergence-free form

We seek u : QT = Ω× (0,T )→ IR such that

∂u

∂ t− div (ID(x) · ∇u) +∇ · ~f (x , t, u) + γ(x , t)u = 0 in QT , (2)

B(u) = 0 on ∂Ω,

u(x , 0) = u0(x), x ∈ Ω,

where ~f (x , t, u) = (f1(x , t, u), f2(x , t, u))T with

fk(x , t, u) =

(σ2k +

1

2ρσ1σ2 − r +

α1x1 + α2x2 − 1

T − t

)xk ·u, k = 1, 2

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 39 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

2D reformulation

localization on a truncated computational domain:

[x1, x2] ∈ IR20 −→ [x1, x2] ∈ Ω = (0, xmax

1 )× (0, xmax2 )

convection-diffusion-reaction equation in divergence-free form

We seek u : QT = Ω× (0,T )→ IR such that

∂u

∂ t− div (ID(x) · ∇u) +∇ · ~f (x , t, u) + γ(x , t)u = 0 in QT , (2)

B(u) = 0 on ∂Ω,

u(x , 0) = u0(x), x ∈ Ω,

where

γ(x , t) = 3r − 4α1x1 + 4α2x2 − 3

T − t− σ2

1 − σ22 − ρσ1σ2

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 39 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

2D reformulation

localization on a truncated computational domain:

[x1, x2] ∈ IR20 −→ [x1, x2] ∈ Ω = (0, xmax

1 )× (0, xmax2 )

convection-diffusion-reaction equation in divergence-free form

We seek u : QT = Ω× (0,T )→ IR such that

∂u

∂ t− div (ID(x) · ∇u) +∇ · ~f (x , t, u) + γ(x , t)u = 0 in QT , (2)

B(u) = 0 on ∂Ω,

u(x , 0) = u0(x), x ∈ Ω,

t - time to maturity −→ i.c. given by payoffs u0

boundary conditions B(u) specified latter

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 39 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Boundary conditions (1)

Let ∂Ω = Γ1 ∪ Γ2 ∪ Γ3. W.l.o.g. we consider the case of the putoption.

Dirichlet

Neumann Dirichlet

Neumann

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 40 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

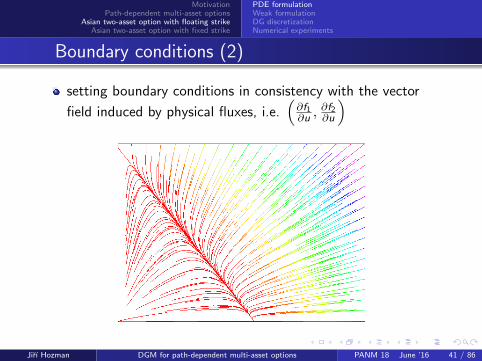

Boundary conditions (2)

setting boundary conditions in consistency with the vector

field induced by physical fluxes, i.e.(∂f1∂u ,

∂f2∂u

)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 41 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Boundary conditions (3)

reformulation of original b.c.

o homogeneous Neumann b.c. on axes x1 = 0 and x2 = 0(ID(x) · ∇u(x1, x2, t)

)· ~n = 0, on Γi , i = 1, 3, t > 0,

where ~n is the unit outer normal vector,

o asymptotic behaviour of options at infinity

u(x1, x2, t) = 0 on Γ2, t ∈ (0,T ).

b.c. for calls follow from put-call parity

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 42 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Weighted Lebesgue space

standard Lebesgue space

L2(Ω) =

v ∈ L1

loc(Ω) :

∫Ω

v 2(x)dx < +∞

with scalar product (·, ·) and induced norm ‖ · ‖:

(u, v) =

∫Ω

u(x) · v(x)dx , ‖u‖ =√

(u, u)

w is weight, i.e. w : IR2 → [0,∞), w ∈ L1loc(Ω) and w 6= 0,

weighted Lebesgue space

L2w = L2(Ω,w) =

v ∈ L1

loc(Ω) :

∫Ω

√w · v ∈ L2(Ω)

,

with scalar product (·, ·)w and induced norm ‖ · ‖w :

(u, v)w =

∫Ω

u(x) · v(x) · w(x)dx , ‖u‖w = ‖√

w · u‖.Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 43 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Weighted Sobolev space

weighted Sobolev space

H1w = H1(Ω,w1,w2) =

v ∈ L2(Ω) :

√wi ·

∂v

∂xi∈ L2(Ω), i = 1, 2

with the norm

‖u‖1,w =

(‖u‖2 +

∥∥∥∥ ∂v

∂x1

∥∥∥∥2

w1

+

∥∥∥∥ ∂v

∂x2

∥∥∥∥2

w2

)1/2

in our case, we take: w1(x) = x21 and w2(x) = x2

2 ,

to treat with b.c., we introduce space:

H1w ,0 =

v ∈ H1

w : v∣∣ΓD

= 0

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 44 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Properties of H1w

The space H1w has the following properties:

(a) H1w is separable,

(b) D(Ω) = v ∈ C∞0 (IR2) : v |Ω is dense in H1w ,

(c) H1w is dense in L2(Ω) with continuous embeding H1

w ⊆ L2(Ω),

(d) the seminorm

|u|1,w =

(2∑

i=1

∥∥∥∥ ∂v

∂xi

∥∥∥∥2

wi

)1/2

is in fact a norm on H1w ,0 equivalent to ‖ · ‖1,w .

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 45 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Variational formulation (1)

we define linear partial differential operator

Ltu = −2∑

i=1

∂

∂xi

(ID(x) · ∇u

)+

2∑i=1

ai (x , t)∂u

∂xi

+

(r − α1x1 + α2x2 − 1

T − t

)u.

where

a1(x , t) =

(σ2

1 +1

2ρσ1σ2 − r +

α1x1 + α2x2 − 1

T − t

)x1,

a2(x , t) =

(σ2

2 +1

2ρσ1σ2 − r +

α1x1 + α2x2 − 1

T − t

)x2.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 46 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Variational formulation (2)

standard approach leads to(∂u

∂ t, v

)+ (Ltu, v) = 0 ∀ v ∈ H1

w ,0, a.e. t ∈ (0,T ),

where

(Ltu, v) =

∫Ω

ID(x) · ∇u · ∇v dx +2∑

i=1

∫Ω

ai (x , t)∂u

∂xiv dx

+

∫Ω

(r − α1x1 + α2x2 − 1

T − t

)uv dx .

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 47 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Weak solution

assume that there exists a function

ug ∈ C 0([0,T ]; L2(Ω)) ∩ L2(0,T ; H1w ),

∂ug

∂ t∈ L2(0,T ; H ′w )

with ug

∣∣ΓD

= g (prescribed Dirichlet b.c.)

Find u: u − ug ∈ L2(0,T ; H1w ,0), u ∈ C 0([0,T ]; L2(Ω)), s.t.

∂u∂ t∈ L2(0,T ; H ′w ) satisfying u

∣∣t=0

= u0 in Ω (u0 ∈ L2(Ω)) and(∂u

∂ t, v

)+ (Ltu, v) = 0 ∀ v ∈ H1

w ,0, a.e. t ∈ (0,T ), (3)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 48 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Properties of Lt

boundedness: ∃CB = CB(t) > 0 s.t.

(Ltu, v) ≤ CB(t)|u|1,w |v |1,w , ∀u, v ∈ H1w ,0, t ∈ (0,T ∗]

Garding inequality: ∃CG = CG (t),Cg = Cg (t) > 0 s.t.

(Ltu, u) ≥ CG (t)|u|21,w − cg (t)‖u‖2, ∀u ∈ H1w ,0, t ∈ (0,T ∗]

Garding inequality ⇒ ellipticity (strict positivity) via easy

transformation u = eλt · z , λ = maxt∈[0,T∗] cg (t), z ∈ H1w , i.e.(

∂z

∂ t, v

)+(Ltz , v)+λ(z , v) = 0 ∀ v ∈ H1

w ,0, a.e. t ∈ (0,T ∗),

with z∣∣t=0

= u0 ∈ L2(Ω) and 0 < T ∗ < T .

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 49 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Unique solvability

Theorem

Problem (3) has a unique weak solution.

Proof (sketch 1/2)

Abstract theory: Let H and V be Hilbert spaces such that V isembedded continuously and densely in H. Let At(·, ·)) becontinuous bilinear form on V × V . The abstract variationalparabolic (AVP) problem associated to the triple (H,V ,At(·, ·)) isthe following: Given f (t) ∈ L2(0,T ,V ′) and u0 ∈ H, findu ∈W (0,T ,V ,V ′) = u ∈ L2(0,T ,V ) : du

dt∈ L2(0,T ,V ′) s.t.

∂

∂ t(u(t), v)H +At(u(t), v) = 〈f (t), v〉 ∀v ∈ V ,

u(0) = u0.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 50 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Unique solvability

Theorem

Problem (3) has a unique weak solution.

Proof (sketch 2/2)

If the form At(·, ·) is coercive, then AVP problem admitsa unique solution for all u0 ∈ H.In our case, we take

T = T ∗

H = L2(Ω), V = H1w ,0

〈f (t), v〉 = − ∂

∂ t(ug (t), v)H −At(ug (t), v),

At(u, v) = (Ltu, v)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 50 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Discontinuous Galerkin approximations

exact solution of (2) is difficult to find,

we construct partitions Th of Ω,

we define space Shp ≈ H1w (Ω) over Th with dim(Shp) <∞

we derive DG semi-discrete formulation,

we discretize in temporal variable,

we obtain fully discrete DG numerical scheme,

we construct basis of space Shp,

we assemble a system matrix and right-hand side,

we solve system of linear algebraic equations,

we obtain DG solution at each time level.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 51 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Triangulations

-1

-0.5

0

0.5

1

-1 -0.5 0 0.5 1-1

-0.5

0

0.5

1

-1 -0.5 0 0.5 1-1

-0.5

0

0.5

1

-1 -0.5 0 0.5 1

1

let Th, h > 0 be a partition of Ω,

Th = KK∈Th , K are polygons (nonconvex, hanging nodes),

hK = diam(K ), h = maxK∈ThhK ,

let Fh = ΓΓ∈Fhbe a set of all edges of Th,

we distinguisha) inner edges F I

h

b) Dirichlet edges FDh

c) Neumann edges FNh

⇒ Fh = F Ih ∪ FD

h ∪ FNh ,

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 52 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Spaces of discontinuous functions

let pK ≥ 1,K ∈ Th be local polynomial degree,

we set vector p ≡ pK ,K ∈ Th,over Th we define:

broken weighted Sobolev space

H1w (Ω, Th) = v ; v |K ∈ H1

w (K ) ∀K ∈ Th,

where

H1w (K ) =

v ∈ L2(K ); x1

∂v

∂x1∈ L2(K ) ∧ x2

∂v

∂x2∈ L2(K )

,

the space of piecewise polynomial functions

Shp ≡ v ; v ∈ L2(Ω), v |K ∈ PpK (K ) ∀K ∈ Th ⊂ H1w (Ω, Th)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 53 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Example of a function from Shp ⊂ H1w (Ω, Th)

1

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 54 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Notation - trace, mean value, jump

Kp

Kn

Γ

~nΓ

1

v∣∣(p)

Γ≡ trace of v |Kp on Γ and v

∣∣(n)

Γ≡ trace of v |Kn on Γ,

〈v〉Γ =1

2

(v∣∣(p)

Γ+ v∣∣(n)

Γ

)and [v ]Γ = v

∣∣(p)

Γ− v∣∣(n)

Γ,

〈v〉Γ ≡ [v ]Γ ≡ v |(p)Γ , Γ ⊂ ∂Ω.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 55 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Space semi-discretization

let u be a strong (regular) solution on Ω,

we multiply (2) by v ∈ H2w (Ω, Th),

integrate over each K ∈ Th,

apply Green’s theorem,

sum over all K ∈ Th,

we include additional terms vanishing for regular solution,

we obtain the identity(∂u

∂ t(t), v

)+ ah(u(t), v) + bh(u(t), v) + Jh(u(t), v) (4)

+γ(t)(u(t), v) = `h(v)(t) ∀v ∈ H2w (Ω, Th) ∀t ∈ (0,T )

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 56 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

DG formulation

(∂u

∂t, v

)+ ah(u, v) + bh(u, v) + Jh(u, v) + γ(u, v) = `h(v)(t)

time derivation, u = u(t) ∈ H2w (Ω, Th), t ∈ (0,T ),

semi-implicit linearization of backward Euler method.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 57 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

DG formulation

(∂u

∂t, v

)+ ah(u, v) + bh(u, v) + Jh(u, v) + γ(u, v) = `h(v)(t)

diffusion terms:

ah(u, v) =∑K∈Th

∫K

ID(x)∇u · ∇v dx

−∑

Γ∈F Ih∪FD

h

∫Γ

⟨ID(x)∇u · ~n

⟩[v ] dS

+∑

Γ∈F Ih∪FD

h

∫Γ

⟨ID(x)∇v · ~n

⟩[u] dS ,

[u]Γ = 0, 〈ID(x)∇u〉Γ = ID(x)∇u|(p)Γ = ID(x)∇u|(n)

Γ , ∀ Γ ∈ F Ih

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 57 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

DG formulation

(∂u

∂t, v

)+ ah(u, v) + bh(u, v) + Jh(u, v) + γ(u, v) = `h(v)(t)

convection terms:

bh(u, v) = −∑K∈Th

∫K~a(x , t)u · ∇v dx

+∑

Γ∈F Ih

∫Γ

H(

u|(p)Γ , u|(n)

Γ ,~nΓ

)[v ] dS

+∑

Γ∈Fh\F Ih

∫Γ

H(

u|(p)Γ , u∗|Γ,~nΓ

)[v ]dS

physical flux ⇔ numerical flux:

~a(x , , t)u · ~n|Γ ≈ H(

u|(p)Γ , u|(n)

Γ ,~nΓ

), Γ ⊂ Kp ∩ Kn.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 57 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

DG formulation

(∂u

∂t, v

)+ ah(u, v) + bh(u, v) + Jh(u, v) + γ(u, v) = `h(v)(t)

numerical flux (concept of upwinding):

H(

u|(p)Γ , u|(n)

Γ ,~nΓ

)=

~a(x , t)u

∣∣(p)

Γ· ~nΓ, if E > 0

~a(x , t)u∣∣(n)

Γ· ~nΓ, if E ≤ 0

where E =∑2

i=1 ai (x , t)ni , ~a(x , t) =(a1(x , t), a2(x , t)

)with

ak(x , t) =

(σ2k +

1

2ρσ1σ2 − r +

α1x1 + α2x2 − 1

T − t

)xk , k = 1, 2,

u∗|Γ is chosen according to boundary conditions.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 57 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

DG formulation

(∂u

∂t, v

)+ ah(u, v) + bh(u, v) + Jh(u, v) + γ(u, v) = `h(v)(t)

interior and boundary penalty:

Jh(u, v)=∑

Γ∈F Ih

∫Γ

ω

|Γ|[u] [v ] dS +

∑Γ∈FD

h

∫Γ

ω

|Γ|u v dS ,

|Γ| is the length of edge Γ,

weighted parameter ω =σ2min4 (1− |ρ|),

u is regular ⇒ [u]Γ = 0 ⇒∫

Γ[u] [v ] dS = 0, ∀ Γ ∈ F Ih.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 57 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

DG formulation

(∂u

∂t, v

)+ ah(u, v) + bh(u, v) + Jh(u, v) + γ(u, v) = `h(v)(t)

reaction terms with factor:

γ(x , t) = 3r − 4α1x1 + 4α2x2 − 3

T − t− σ2

1 − σ22 − ρσ1σ2

(broken) L2(Ω)-inner product

(u, v)=

∫Ω

uvdx =∑K∈Th

∫K

uvdx

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 57 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

DG formulation

(∂u

∂t, v

)+ ah(u, v) + bh(u, v) + Jh(u, v) + γ(u, v) = `h(v)(t)

right-hand-side ⇔ boundary conditions

`h(v)(t) =∑

Γ∈FDh

∫Γ

ID(x)∇v · ~nΓ u∗(t)dS

+∑

Γ∈FDh

∫Γ

ω

|Γ|u∗(t) vdS

o terms from homogeneous Neumann b.c. vanish.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 57 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Semi-discrete DG scheme

Shp ⊂ H2w (Ω, Th) ⇒ (4) makes sense for uh, vh ∈ Shp

we define new bilinear form

Ch(u, v) := ah(u, v) + bh(u, v) + Jh(u, v) + γ(u, v)

Semi-discrete DG solution

We say that uh is a semi-discrete DG solution iff

a) uh ∈ C 1(0,T ; Shp),

b)

(∂uh(t)

∂ t, vh

)+ Ch(uh(t), vh) = 0 (5)

∀ vh ∈ Shp, t ∈ (0,T )

c) uh(0) = u0h, u0

h is Shp-approximation of u0

semi-discrete problem (5) represents ODEs with IC,

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 58 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Existence and uniqueness of semi-discrete solution

Theorem

Problem (5) has a unique semi-discrete solution.

Proof (sketch 1/2)

Let vjDOFj=1 be the standard base of Shp, i.e.

uh(x , t) =DOF∑j=1

ξj(t)vj(x).

We substitute this into (5), choose and set

G (t) = (ξ1(t), . . . , ξDOF (t))T ,

L(t) = (`h(v1)(t), . . . , `h(vDOF )(t))T ,

C(t) = (cij(t))DOF×DOF , cij(t) = Ch(vj , vi ).

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 59 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Existence and uniqueness of semi-discrete solution

Theorem

Problem (5) has a unique semi-discrete solution.

Proof (sketch 2/2)

We rewrite (5) as follows: find G (t), ∀t ∈ (0,T ) such that

G ′(t) = −C(t) · G (t) + L(t),

G (0) = (ξ1(0), . . . , ξDOF (0))T (given by uh(0)).

Numerical flux H is Lipschitz continuous and form Ch(·, ·) isbilinear ⇒ RHS of afore-mentioned ODEs is Lipschitz continuous.The proof is completed by theory of ODEs.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 59 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Time discretization

linearity of form Ch(·, ·) ⇒ implicit treatment,

implicit approach via backward Euler method

let 0 = t0 < t1 < · · · < tr = T be a partition of (0,T ) withconstant step τ = T/r , uh(tm) ≈ um

h ∈ Shp, m = 0, . . . , r

First order implicit scheme(1

τ+ γ

)(um+1h , vh

)+ ah

(um+1h , vh

)+ bh

(um+1h , vh

)(6)

+Jh(um+1h , vh

)=

1

τ(um

h , vh) + `h(vh)(tm+1) ∀ vh ∈ Shp,

problem (6) ⇐⇒ system of linear algebraic equations.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 60 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Existence and uniqueness of fully discrete solution

Theorem

Problem (6) has a unique discrete solution.

Proof (sketch 1/3)

Suppose umh ≡ 0, i.e. `h(vh) = 0, then problem (6) is equivalent to(

1

τ+γ

)(um+1h , vh

)+ah

(um+1h , vh

)+bh

(um+1h , vh

)+Jh

(um+1h , vh

)= 0

Problem (6) is linear algebraic system ⇒ the existence is impliedby uniqueness.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 61 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Existence and uniqueness of fully discrete solution

Theorem

Problem (6) has a unique discrete solution.

Proof (sketch 2/3)

Taking vh = um+1h and neglecting some positive terms, we obtain

1

τ‖um+1

h ‖2 ≤ |bh

(um+1h , um+1

h

)|+ |γ|‖um+1

h ‖2

Since

|bh

(um+1h , um+1

h

)| ≤ C

(Jh(um+1h , um+1

h

)1/2+ |um+1

h |1,w)‖um+1

h ‖

then

‖um+1h ‖2 ≤ τC

(Jh(um+1h , um+1

h

)1/2+ |um+1

h |1,w)‖um+1

h ‖

+τ |γ|‖um+1h ‖2

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 61 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Existence and uniqueness of fully discrete solution

Theorem

Problem (6) has a unique discrete solution.

Proof (sketch 3/3)

For sufficiently small τ , it holds

‖um+1h ‖2 ≤ δ‖um+1

h ‖2, δ ∈ (0, 1)

Then ‖um+1h ‖ = 0, i.e. um+1

h ≡ 0.We prove that exists only trivial solution for homogeneous linearalgebraic system ⇒ existence and uniqueness.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 61 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Linear algebraic problem

standard basis of space Shp: vjDOFj=1 ,

linear algebraic representation:

DOF∑j=1

ξmj vj(x) = umh (x)←→ Um = (ξm1 , . . . , ξ

mDOF )T ∈ IRDOF

sparse matrix equation((1/τ + γ)M + A + B + J

)︸ ︷︷ ︸

C

Um+1 = 1/τ MUm + Fm+1 (7)

Um unknown vector, M mass matrix, A stiffness matrix,

B matrix representing the form bh, J penalty matrix,

Fm+1 = `h(vh)(tm+1) right-hand side vector.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 62 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Fictional triangulation

K1

p1=1

K2

p2=3

K3

p3=1

K4

p4=2

K5

p5=2

K6

p6=1

1

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 63 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Structure of system matrix C

Ck,1,1

12×12

Ck,2,2

40×40

Ck,3,3

12×12

Ck,4,4

24×24

Ck,5,5

24×24

Ck,6,6

12×12

Ck,1,2

12×40

Ck,2,1

40×12Ck,2,3

40×12

Ck,3,2

12×40

Ck,2,4

40×24

Ck,4,2

24×40Ck,4,5

24×24

Ck,5,4

24×24Ck,5,6

24×12

Ck,6,5

12×24

1

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 64 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Freefem++ solver

source: http://www.freefem.org/ff++/,

C++ code and software to solve PDEs numerically,

user friendly input language allows for a quick specification ofany PDE based on a variational formulation,

easy mesh generation/adaptation,

available library of a wide range of finite elements,

implemented sparse solvers,

basic post-processing/vizualization,

for more details see [Hecht].

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 65 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

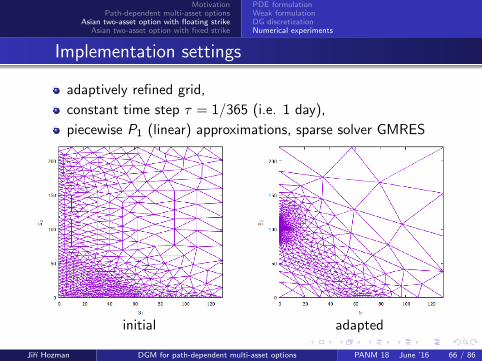

Implementation settings

adaptively refined grid,

constant time step τ = 1/365 (i.e. 1 day),

piecewise P1 (linear) approximations, sparse solver GMRES

initial adapted

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 66 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Parameter settings

basket put option with 60% Allianz (α1 = 0.6) and40% Deutshce Bank (α2 = 0.4),

current date: September 13, 2011 (Tuesday),

volatilities σ1 and σ2 : 4 ways of its determination,

expiration date T = 0.257534 (i.e. 94 days),

risk-free interest rate r = 0.01557 p.a.,

Pearson linear correlation ρ = 0.88,

two stocks trades at S ref1 = 59.79 and S ref

2 = 23.40,

reference point [S ref1 , S ref

2 ,Aref ], where Aref = α1S ref1 +α2S ref

2

maximal stock prices xmax1 = 5.0 and xmax

2 = 7.0.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 67 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Determination of volatility

Real market data of individual options:

(A) constant volatilities σ1 = 0.6392, σ2 = 0.9461,

(B) piecewise constant implied volatility as a function of Si , i.e.σi = σi (Si ), i = 1, 2,

(C) piecewise constant implied volatility as a function of αiSi , i.e.σi = σi (αiSi ), i = 1, 2,

(D) piecewise constant implied volatility as a function ofmoneyness, i.e.

σi = σi

(αiSi

α1S ref1 + α2S ref

2

exp(−rT )

), i = 1, 2.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 68 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Asian basket with floating strike (1)

space-time plot of solution with approach (D)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 69 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Asian basket with floating strike (2)

comparison of approaches, isolvalues of solutions,zoom on (0, 2.50)× (0, 1.80)

(A) (B)

4.08903 (Asian basket) 6.70615 (Asian basket)6.15615 (basket) 8.55314 (basket)

o #Th ≈ 4 000, results at the reference node [1.3218, 0.5173]

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 70 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Asian basket with floating strike (3)

comparison of approaches, isolvalues of solutions,zoom on (0, 2.50)× (0, 1.80)

(C ) (D)

4.08995 (Asian basket) 4.08913 (Asian basket)5.52614 (basket) 5.70892 (basket)

o #Th ≈ 4 000, results at the reference node [1.3218, 0.5173]

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 71 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

PDE formulationWeak formulationDG discretizationNumerical experiments

Asian basket with floating strike (4)

dependency among particular risk sources,basket option value at ref. node vs. correlation plot,approach (D) for volatilities

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 72 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

1 Motivation

2 Path-dependent multi-asset options

3 Asian two-asset option with floating strike

4 Asian two-asset option with fixed strike

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 73 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

3D PDE model

continuous arithmetic Asian two-asset basket option withfloating strike = the same PDE model as for Asian two-assetbasket option with fixed strike,

for simplicity, we consider the case of puts only(the case of calls can be easy derived from put-call parity),

different payoffs (puts): V (S ,A,T ) = max(K − A, 0)

different boundary conditions at far-field boundary (puts)

o no dependency on S1 and S2 for payoffs, i.e.,

limS1→∞

∂V

∂S1(S1,S2,A, t) = 0, lim

S2→∞∂V

∂S2(S1,S2,A, t) = 0,

o zero price for large value of A, i.e.,

limA→∞

V (S1, S2,A, t) = 0

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 74 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

Dimensional reduction

to avoid the higher complexity of 3D model

change of variables (approach from [Rogers, Shi])

x1 =K − A(T − t)/T

S1, x2 =

K − A(T − t)/T

S2, t = T − t

transformation of price function

u(x , t) =1√

S1S2V (S1,S2,A, t), where x = [x1, x2]

transformation of payoffs (= initial conditions)

u(x , 0) =1√

S1S2V (S1,S2,A,T ) = max(

√x1x2 · sgn(x1), 0)

transformation of PDE: homogeneity w.r.t.√

S1S2

−→ separation of factor√

S1S2 −→ dimensional reductionfrom 3D to 2D

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 75 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

2D reformulation

localization on a truncated computational domain Ω,

convection-diffusion-reaction equation in divergence-free form

We seek u : QT = Ω× (0,T )→ IR such that

∂u

∂ t− div (ID(x) · ∇u) +∇ · ~f (x , u) + γ(x)u = 0 in QT , (8)

B(u) = 0 on ∂Ω,

u(x , 0) = u0(x), x ∈ Ω,

where

ID(x) ≡ D(x)kl2k,l=1 =

1

2

(σ2

1x21 ρσ1σ2x1x2

ρσ1σ2x1x2 σ22x2

2

),

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 76 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

2D reformulation

localization on a truncated computational domain Ω,

convection-diffusion-reaction equation in divergence-free form

We seek u : QT = Ω× (0,T )→ IR such that

∂u

∂ t− div (ID(x) · ∇u) +∇ · ~f (x , u) + γ(x)u = 0 in QT , (8)

B(u) = 0 on ∂Ω,

u(x , 0) = u0(x), x ∈ Ω,

where ~f (x , u) = (f1(x , u), f2(x , u))T with

fk(x , u) =

(σ2k

2+ ρσ1σ2 + r +

α1

Tx1+

α2

Tx2

)xk · u, k = 1, 2

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 76 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

2D reformulation

localization on a truncated computational domain Ω,

convection-diffusion-reaction equation in divergence-free form

We seek u : QT = Ω× (0,T )→ IR such that

∂u

∂ t− div (ID(x) · ∇u) +∇ · ~f (x , u) + γ(x)u = 0 in QT , (8)

B(u) = 0 on ∂Ω,

u(x , 0) = u0(x), x ∈ Ω,

where

γ(x) = −2r − α1

Tx1− α2

Tx2− 3

8σ2

1 −3

8σ2

2 −9

4ρσ1σ2

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 76 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

2D reformulation

localization on a truncated computational domain Ω,

convection-diffusion-reaction equation in divergence-free form

We seek u : QT = Ω× (0,T )→ IR such that

∂u

∂ t− div (ID(x) · ∇u) +∇ · ~f (x , u) + γ(x)u = 0 in QT , (8)

B(u) = 0 on ∂Ω,

u(x , 0) = u0(x), x ∈ Ω,

t - time to maturity −→ i.c. given by payoffs u0

boundary conditions B(u) specified latter

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 76 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

Boundary conditions (1)

x1 6= 0 and x2 6= 0 −→ domain Ω is a convex quadrilateral

Robin

Dirichlet Robin

Dirichlet

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 77 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

Boundary conditions (2)

setting boundary conditions in consistency with the vector

field induced by physical fluxes, i.e.(∂f1∂u ,

∂f2∂u

)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 78 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

Boundary conditions (3)

reformulation of original b.c.

o non-homogeneous Dirichlet b.c. on axesx1 = k1x2 and x2 = k2x2 (0 < k1 < k2)

u(x1, x2, t) = uD(x1, x2, t), on Γi , i = 1, 4, t > 0,

where uD is the solution of 1D problem on Γi , i = 1, 4,

o Robin b.c. at infinity

1

2u(x1, x2, t)− xi

∂u

∂xi(x1, x2, t) = 0 on Γi , i = 2, 3, t > 0.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 79 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

Weak formulation and DG discretization

standard Sobolev and Lebesgue spaces (no weighted spaces),

existence and uniqueness of weak solution(∂u

∂ t, v

)+ (Ltu, v) = 0 ∀ v ∈ H1

0 , a.e. t ∈ (0,T ),

DG approach analogous to Asian basket with floating strike,

similar numerical scheme(1

τ+ γ

)(um+1h , vh

)+ ah

(um+1h , vh

)+ bh

(um+1h , vh

)+Jh

(um+1h , vh

)=

1

τ(um

h , vh) + `h(vh)(tm+1) ∀ vh ∈ Shp

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 80 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

Parameter settings

basket put option with 60% Allianz (α1 = 0.6) and40% Deutshce Bank (α2 = 0.4),

strike at 40 Euro,

current date: September 13, 2011 (Tuesday),

volatilities: σ1 = 0.6392 and σ2 = 0.9461,

expiration date T = 0.257534 (i.e. 94 days),

risk-free interest rate r = 0.01557 p.a.,

Pearson linear correlation ρ = 0.88,

two stocks trades at S ref1 = 59.79 and S ref

2 = 23.40,

reference point [S ref1 , S ref

2 ,Aref ], where Aref = α1S ref1 +α2S ref

2

maximal values xmax1 = 3.0 and xmax

2 = 3.0.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 81 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

Asian basket with fixed strike (1)

space-time plot of solution at maturity)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 82 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

Asian basket with fixed strike (2)

isolvalues of solutions

#Th ≈ 4 000, results at the reference node [0.6690, 1.7094]2.62975 (Asian basket) 3.56022 (basket)

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 83 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

Asian basket with fixed strike (3)

dependency among particular risk sources,

basket option value at ref. node vs. correlation plot

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 84 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

Conclusion

Achieved results

fundamentals of option pricing,

market models based on Black-Scholes equation (PDE),

combination of Asian and basket options,

2 approaches of dimensional reduction w.r.t. payoffs

nonstationary linear convection-diffusion-reaction problem,

DG space semi-discretization with backward Euler,

promising numerical results

Future work

to add other realistic experiments with real reference values,

to investigate the sensitivity measures (Delta, Gamma, etc.),

to extend the approach to other path-dependent options.

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 85 / 86

MotivationPath-dependent multi-asset options

Asian two-asset option with floating strikeAsian two-asset option with fixed strike

Similar approachNumerical experiments

References

[1ec Y. Achdou and O. Pironneau. Computational Methods for OptionPricing. Frontiers in Applied Mathematics. Society for Industrialand Applied Mathematics, Philadelphia, 2005.

[2ec F. Hecht. New development in FreeFem++, Journal of NumericalMathematics 20, no. 3-4, pp. 251–265, 2012.

[3ec J.E. Ingersoll, Jr. Theory of Financial Decision Making. Rowman &Littlefield Publishers, Inc., New Jersey, 1987

[4ec L. Rogers and Z. Shi The Value of an Asian Option, Journal ofApplied Probability 32(4), pp. 1077–1088, 1995.

[5ec R. Seydel. Tools for Computational Finance: 4th edition. Springer,2008.

Thank you for your attention

Jirı Hozman DGM for path-dependent multi-asset options PANM 18 June ’16 86 / 86