developing the iraqi petrochemical industry critical...

TRANSCRIPT

“Strategy without tactics is the slowest route to victory.

Tactics without strategy is the noise before defeat”

Sun Tzu

Developing the Iraqi Petrochemical Industry Critical Success Factors

Iraq Energy Forum 2017, Baghdad Iraq Energy Institute Research

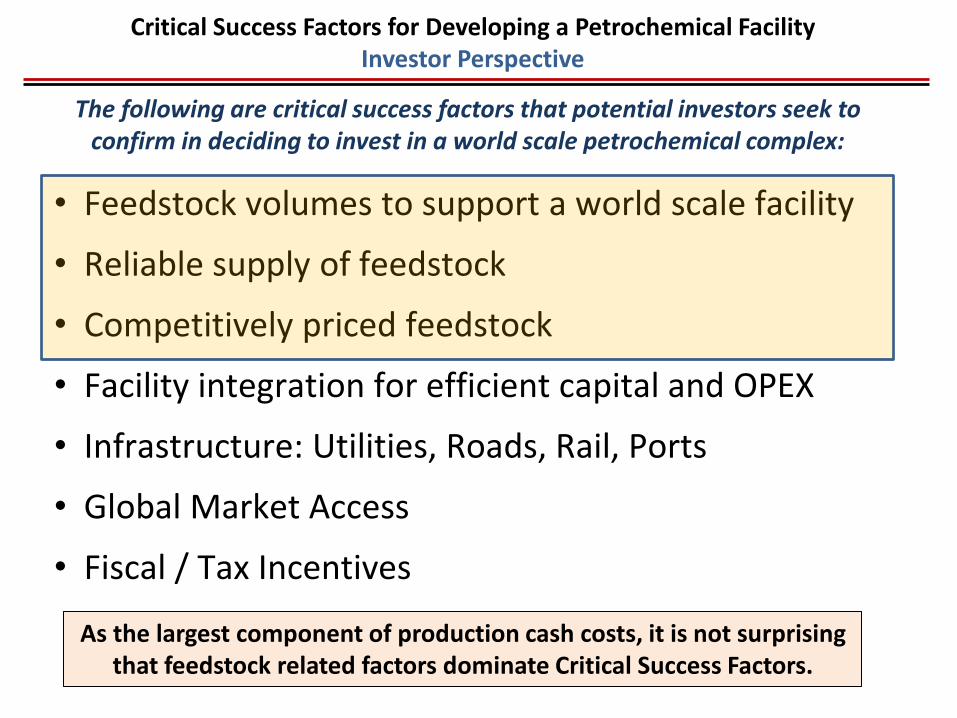

• Feedstock volumes to support a world scale facility

• Reliable supply of feedstock

• Competitively priced feedstock

• Facility integration for efficient capital and OPEX

• Infrastructure: Utilities, Roads, Rail, Ports

• Global Market Access

• Fiscal / Tax Incentives

Critical Success Factors for Developing a Petrochemical Facility Investor Perspective

The following are critical success factors that potential investors seek to confirm in deciding to invest in a world scale petrochemical complex:

As the largest component of production cash costs, it is not surprising that feedstock related factors dominate Critical Success Factors.

• Feedstock type: Ethane – Why? Processing ethane produces ethylene with no byproducts (except fuel gas) to process and manage.

This results in the lowest capital cost to construct a world scale facility and minimizes the complexity of the logistics / distribution requirements. An especially critical factor in early petrochemical industrial development in a country like Iraq. As the industry and corresponding infrastructure develops, subsequent ethylene projects can utilize propane and heavier NGL’s.

• Feedstock: Volume, Reliability and Term – Volume: Sufficient supply of feedstock to establish a world scale ethylene facility. Currently, world

scale range is in the range of 1.0 to 1.5 million tons of ethylene production. A 1.0 million ton per year ethylene facility would require a supply of roughly 1.3 million tons per year of ethane.

– Reliability: An investor would want to ensure that the supply of feedstock is reliable and sustainable (more on this topic later); on-stream factor is a critical variable for economic viability (a world class ethylene plant should run from 4 – 5 years without any planned downtime for maintenance; in addition, frequent unplanned shutdowns result in equipment failures (e.g thermal cycling) and shortened catalyst life resulting in increased operating expense

– Term: An investor would want to secure a feedstock supply contract volume commitment for a minimum of 20 years and more likely in the 25- 30 year range

• Feedstock: Price – The Government of Iraq should to establish a simple, clear and transparent formula for feedstock price.

Given the complexity, risk and lack of infrastructure development, the prices should be competitive with other low cost global regions (i.e. Saudi Arabia & U.S. Gulf Coast). An initial ‘fixed feedstock price’ period (e.g. 10 - 15 years from operational start-up) should be contractually established with agreed upon escalation formula thereafter. Further note that establishing a clear, competitive contractual price would greatly enhance the ability for the investor to secure third party (commercial) financing.

Critical Success Factors Feedstock Related

• Global Market Access: Facility Location – Cost efficient access to global markets is a critical success factor for a petrochemical facility. With ultimate

product production (likely polyethylene plastic) over one million tons per annum for a single world scale plant, Iraq does not have a local market to support a world scale facility and export to global markets is required. Polyethylene markets are highly fragmented with different products (film, containers, packaging, pipe, etc.) requiring different grades and technical specifications further complicating the local demand requirement and necessitating the need for export capability. Therefore, a facility needs to located nears the Um Qasr / Khor al-Zubayr ports in Basra.

• Infrastructure: Utilities, Roads/Rail, Port Facilities – Utilities: Reliable source of utilities (electricity, cooling water, potable water, nitrogen, etc.) Utilities

can be supplied within the petrochemical complex, however, drives up capital costs and not an efficient utilization of capital.

– Road/Rail: A integrated world scale ethylene facility focused on polyethylene production would ship finished product in 20 or 40 ton containers and require an average of 100 – 200 truck shipments per day. A dedicated rail line from plant site to the port would greatly enhance efficiency (lower cash cost) and security.

– Port: The port facilities need to be modern and efficient to handle a steady stream of container shipments. One world scale ethylene-polyethylene facility would generate 50 – 75,000 20 ton containers annually.

• Facility Integration – The Government of Iraq can further enable development by allocating land near the Um Qasr / KAZ ports

dedicated to industrial development (believe this has already been completed).

• Fiscal / Tax Incentives – The Iraqi Investment Law (2006) already provides for a 10 year income tax holiday (as well as other

investment incentives); it would be beneficial if this tax holiday was clearly extended to mid-stream (gas fractionation) operations supporting the development of the petrochemical industry. Such an incentive would incentivize required investment in the midstream sector, a critical ‘condition precedent’ for petrochemical industry development

Critical Success Factors

5

LUKOIL Proposal Simple Model

Development of the Iraqi Hydrocarbon Chain is Stalled in the Upstream (Crude Oil)

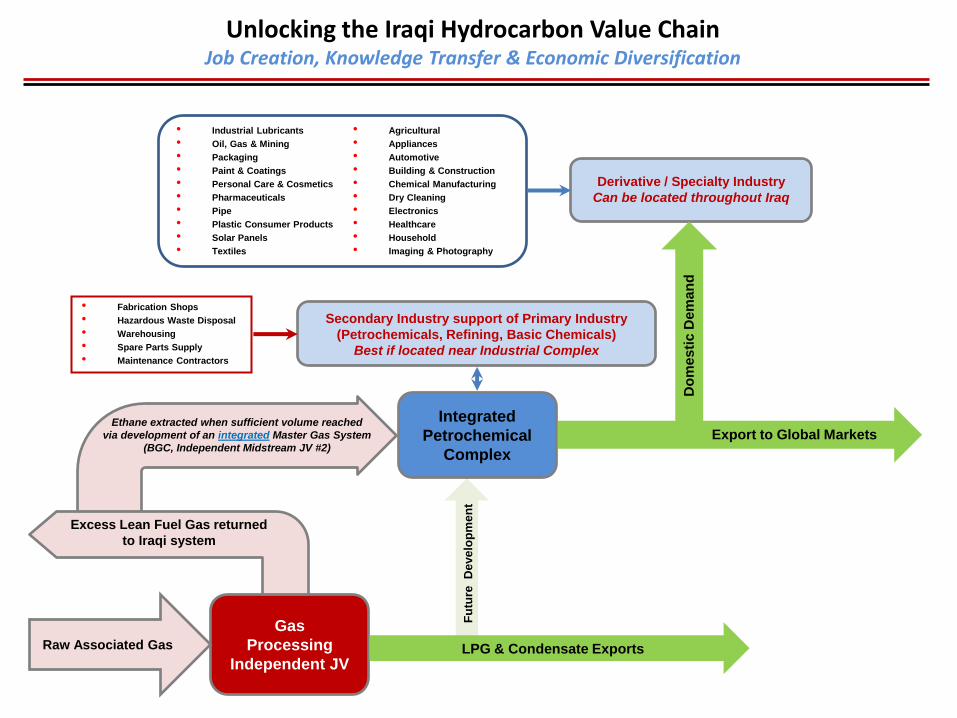

Condition Precedent for petrochemical industry development: Establishing an integrated Master Gas System (midstream) with the objective of providing secure, stable feedstock supply to the petrochemical industry

(This must happen first!)

NATURAL GAS

NATURAL GAS LIQUIDS

(Fractionation Plants)

SECONDARY INDUSTRIES

Domestic Market

PRIMARY

INDUSTRIES

(i.e. Petrochemicals)

Export

to

Global Markets

Crude Oil &

Associated

Gas

Local Manufacture of

Consumer Goods

Focus on midstream to enable petrochemical

development

Capital Intensive

Labor Intensive

F

utu

re D

eve

lop

me

nt

Export to Global Markets

Gas

Processing

Independent JV

Raw Associated Gas

Ethane extracted when sufficient volume reached

via development of an integrated Master Gas System

(BGC, Independent Midstream JV #2)

LPG & Condensate Exports

Excess Lean Fuel Gas returned

to Iraqi system

Integrated

Petrochemical

Complex

Secondary Industry support of Primary Industry

(Petrochemicals, Refining, Basic Chemicals)

Best if located near Industrial Complex

Derivative / Specialty Industry

Can be located throughout Iraq

D

om

es

tic

De

ma

nd

• Industrial Lubricants

• Oil, Gas & Mining

• Packaging

• Paint & Coatings

• Personal Care & Cosmetics

• Pharmaceuticals

• Pipe

• Plastic Consumer Products

• Solar Panels

• Textiles

• Agricultural

• Appliances

• Automotive

• Building & Construction

• Chemical Manufacturing

• Dry Cleaning

• Electronics

• Healthcare

• Household

• Imaging & Photography

• Fabrication Shops

• Hazardous Waste Disposal

• Warehousing

• Spare Parts Supply

• Maintenance Contractors

Unlocking the Iraqi Hydrocarbon Value Chain Job Creation, Knowledge Transfer & Economic Diversification

7

Deep Gas Processing Integrated with World-Scale Petrochemical Facility

Fully Integrated Midstream / Petrochemical Complex

Initial phase designed to process associated gas currently being flared & outside BGC scope (e.g. WQ – 2, Majnoon, Halfaya, Nahr Umr)

To maximize ethane recovery & accelerate petrochemical development, oil producers should supply gas processors full range associated gas and utilize lean fuel (95% methane supplied by gas processors) for internal operational needs

Fully integrated gas processing & petrochemical facility (co-located) would provide opportunity for significant capital and operating cost savings and provide a solid platform for a sustainable, globally competitive facility

Separating oil production from downstream (gas processing & petrochemicals as Independent Joint Venture companies) allows IOCs to focus on their attention and capital on core competencies and primary interest (oil production)

Developing downstream as independent, private sector industry will attract direct foreign investment and reduce the capital burden on the Iraqi budget

Ethane

1.3 million tons/year

HDPE

LLDPE

LDPE

Export to Local & Global

Markets

Olefins Cracker 1.O million tons/year Ethylene

De-methanizer

Fuel Gas

LPG

De-butanizer

Residual C3 Extraction

C5+

C3

Fuel Gas (95% C1) to IOCs & Iraqi fuel gas grid

Export via

pipeline

Gas Preparation

Gas Preparation

De-ethanizer

AG from southern oil

fields

Future oil Production

Current Flared

Volume

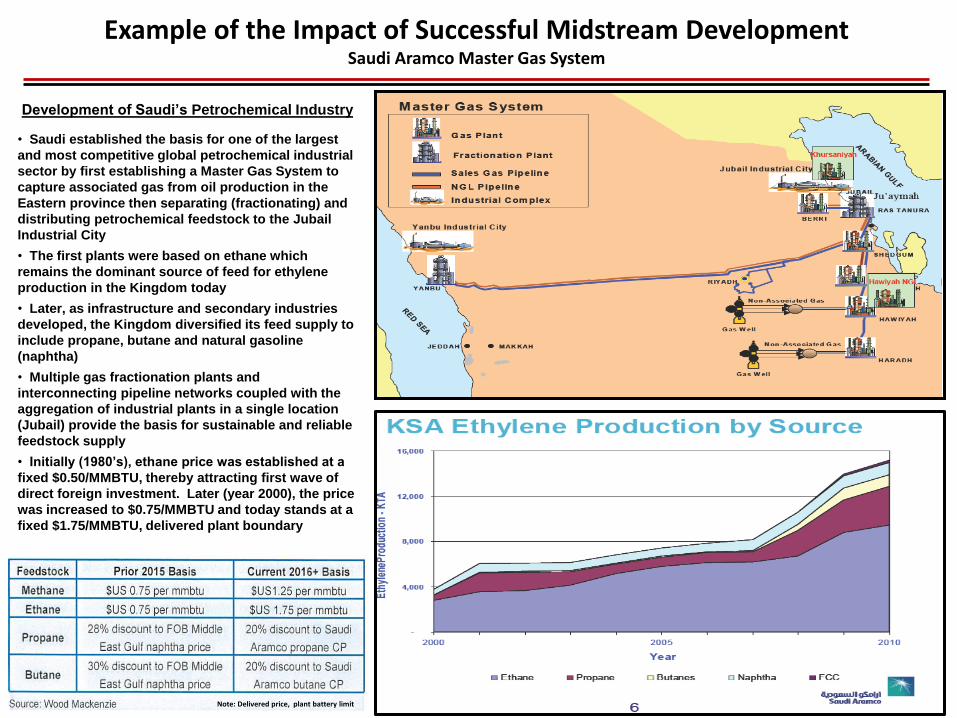

Example of the Impact of Successful Midstream Development Saudi Aramco Master Gas System

Development of Saudi’s Petrochemical Industry

• Saudi established the basis for one of the largest

and most competitive global petrochemical industrial

sector by first establishing a Master Gas System to

capture associated gas from oil production in the

Eastern province then separating (fractionating) and

distributing petrochemical feedstock to the Jubail

Industrial City

• The first plants were based on ethane which

remains the dominant source of feed for ethylene

production in the Kingdom today

• Later, as infrastructure and secondary industries

developed, the Kingdom diversified its feed supply to

include propane, butane and natural gasoline

(naphtha)

• Multiple gas fractionation plants and

interconnecting pipeline networks coupled with the

aggregation of industrial plants in a single location

(Jubail) provide the basis for sustainable and reliable

feedstock supply

• Initially (1980’s), ethane price was established at a

fixed $0.50/MMBTU, thereby attracting first wave of

direct foreign investment. Later (year 2000), the price

was increased to $0.75/MMBTU and today stands at a

fixed $1.75/MMBTU, delivered plant boundary

Note: Delivered price, plant battery limit

Jubail Industrial City A Model for Iraq

Jubail Industrial City (1 & 2)

King Fahd Industrial Port

(1016 km2)

Jubail 1 • Jubail Industrial City was developed in

phases with the objectives of – eliminate flaring (Eastern Province),

– diversify the Saudi economy

– job creation and knowledge transfer

• Jubail Industrial City includes, in addition to

significant petrochemical capacity, a refineries,

steel plant, fertilizers and methanol

• A secondary support industry as well as

derivative production developed an continues

to grow

• Proximity to the King Fahd Industrial Port

(and Jubail Commercial Port) enables access

to global markets.

• Petrochemical products produced in Jubail

compete worldwide

• Lessons learned from Jubail Industrial City

an be applied to the development of a industrial

complex in southern Iraq.

Location Project

Ethylene

Capacity Feedstock

Estimated Ethane

consumption

(MMSCFD)

Yanbu Yanpet I 875 Ethane 85

Yanbu Yanpet II 780 Ethane/Propane 40

Yanbu Yanpet III 600 Ethane/Propane 30

Yanbu Yansab 1,300 Ethane/Propane 85

Rabigh Petro-Rabigh 1,300 Ethane 95 - 125

Jubail Sharq 1,300 Ethane/Propane 60

Jubail Kemya 810 Ethane/Propane 45

Jubail Petrokemya 850 Ethane 85

800 Propane/Pentanes 0

800 Ethane/Propane 40

Jubail SADAF 1,090 Ethane 105

Jubail Jubail United 1,300 Ethane 125

Jubail Saudi Ethylene & Polyethylene 1,000 Ethane/Propane 50

Jubail Jubail Chevron Phillips 225 Pentanes 0

Jubail Kayan 1,325 Ethane/Butane 45

Jubail Saudi Polymer Company (SPCo) 1,200 E/P 60

Jubail Sadara 1,200 Ethane / C5+ 80

Total 16,755 990 - 1,020

Saudi Arabia's Ethylene Facilities

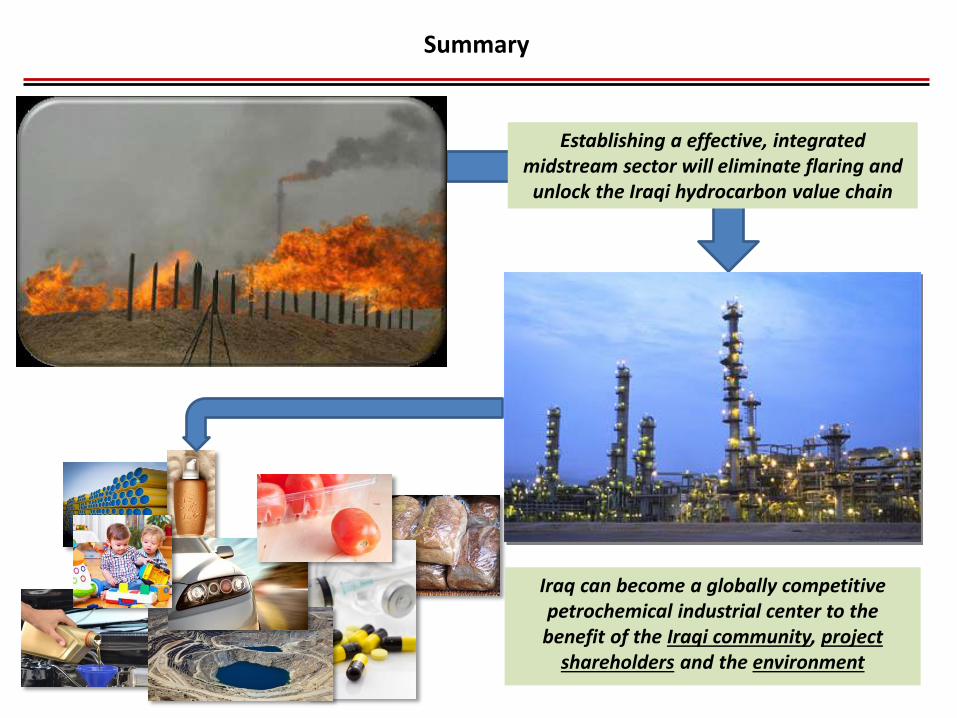

Establishing a effective, integrated midstream sector will eliminate flaring and unlock the Iraqi hydrocarbon value chain

Iraq can become a globally competitive petrochemical industrial center to the benefit of the Iraqi community, project

shareholders and the environment

Summary