developing and financing ancillary facilities - ihaconnect.org · long term ground lease = 50-75...

TRANSCRIPT

Developing and Financing Ancillary Facilities

2

Agenda• Mixed Use Trends• Development Process / Hypothetical• Own vs Lease• Financing Structures• Case Studies

Ullom’s Rules of Lawyer Competency• There exists in nature an inverse relationship between the number of

syllables used by a lawyer and his/her actual competence.

• The use of citations and references to IRS regulations serves as further evidence of one’s lack of understanding.

• Clients should actually understand their transactions.

• A Lawyer’s goal ought not be to make his/her clients depend upon him/her.

Mixed Use Development Trends• Healthcare

– Shift from Inpatient to Outpatient

– Fewer “Towers”– Ambulatory and Outpatient

Facilities– New Neighborhoods and

Markets– Re-purposing Retail Space

4

Mixed-Use Development Trends• Medical Village

– Freestanding ER– Urgent Care Clinics– Ambulatory Facilities– Imaging– Wellness / Therapy– Medical Office– Apartments / Senior Housing / Assisted Living– Skilled Nursing– Restaurant– Retail– Hotel

5

Mixed Use Implications• Development and Construction Process• Ownership• Taxes • Finance• Operations

6

Hypothetical Project• Non-profit hospital is considering an ambulatory care center

that will include a free-standing emergency department or urgent care center, imaging center, lab and medical office space

• Hospital has identified a site for the project that is located off-campus

• Hospital doesn’t have the expertise to oversee the planning, design and construction of the project

7

Practical Considerations• Site selection • Developer selection• Own vs Lease • Ownership options• Ownership advantages• Leasing advantages

8

Site Selection • Is the site ideal for the proposed use?

– Accessibility– Data analytics – Land cost– Infrastructure

• The one remaining site– Explore all options– On-market vs off-market – Greenfield vs redevelopment

9

Developer Selection• Identifying the right development partners

– Access to capital– Size of project– Provider alignment

• Experience and efficiencies • Fee for service vs developer ownership• Request for Proposals• Asking for incentives

10

Own vs Lease• Now more than ever organizations are struggling with

ownership decisions• Historical policy of owning “core” assets may no longer hold

– Accounting rule changes– Nature of “core” assets– Costs of Capital– Property Tax Implications

• Reverse monetizations make headlines

11

Ownership Options• Traditional ownership options

– Ownership of land and the building• Non-traditional ownership options

– Condominium form of ownership– Ground leasing arrangements– Joint venture with other providers– Excess land held for future development– Hybrid model

12

Ownership Advantages• Lowest Cost of Capital

– Refresher: One may utilize tax-exempt financing to finance capital projects owned and used by a 501(c)(3) organization in furtherance of its charitable purpose

• Control• Clear Balance Sheet Treatment• Property Tax Exemption

13

Leasing Advantages• Flexibility• Some Level of Off-Balance Sheet• Preservation of Capital and Capital Capacity (maybe)• Some level of control through ownership restrictions, use

restrictions and purchase options

14

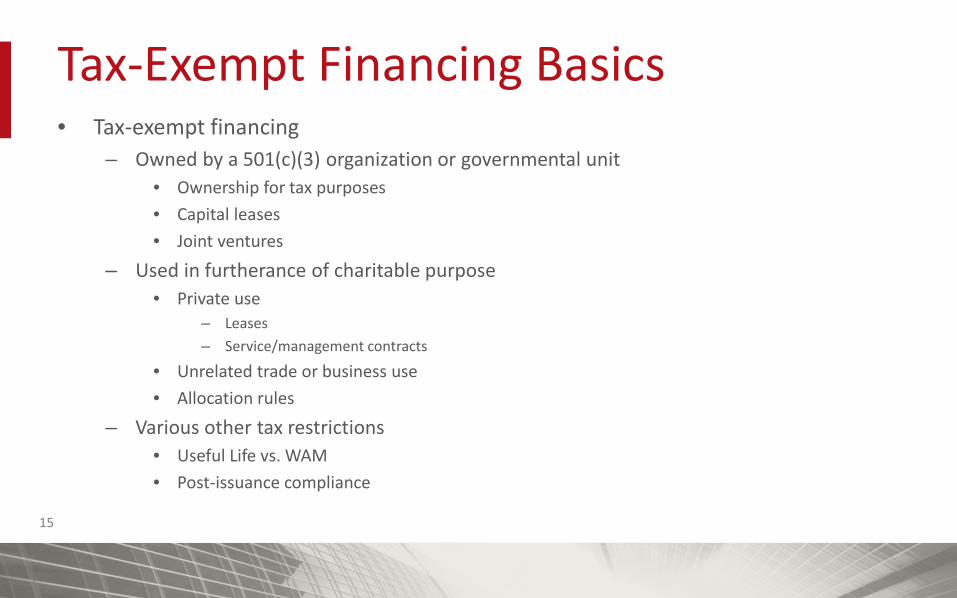

Tax-Exempt Financing Basics• Tax-exempt financing

– Owned by a 501(c)(3) organization or governmental unit• Ownership for tax purposes• Capital leases• Joint ventures

– Used in furtherance of charitable purpose• Private use

– Leases– Service/management contracts

• Unrelated trade or business use• Allocation rules

– Various other tax restrictions• Useful Life vs. WAM• Post-issuance compliance

15

Own and Borrow• Pros

– Lowest cost of capital, if qualified for T/E financing

– Property tax exemption– Project delivery options– Control

• Cons– All on balance sheet– More complicated– Transaction costs– Market disclosure– Split development/financing

501(c)(3) Entity

Fee Developer

Investors / Lenders

T/E or Hybrid Financing

Very traditional structure. Health Care System issues debt (likely tax-exempt bonds) through governmental issuer and engages a

fee only developer to build the building.

16

501(c)(3) Entity

Developer REIT

REIT Investors

Long Term Ground Lease = 50-75 years

Improvements = Operating Lease Back

Build, Monetize, Leaseback

• Pros– Partial off-balance sheet

treatment*– Turn-key development/financing– Greater project delivery control– Simplified execution

• Cons– Property tax– Higher cost of capital/lease rate

Typical Developer/REIT Structure. Health System executes turn-key arrangement with Developer who

sources capital, builds building and sells to REIT. Developer/REIT may be on in the same or separate

entities. Alternatively, Health System may fund construction of building and “monetize” (sell)

building to REIT when completed.

17

*Accounting treatment subject to accounting rules applicable to each health care entity. Consult your accounting advisors for an assessment of accounting treatment.

501(c)(3) Entity Developer

REIT Investors

Long Term Ground Lease = 50-75 years

Non-Qualifying Improvements = Operating Lease Back

Hybrid Solution• Pros

– Lower blended cost of capital– Partially off-balance sheet*– Partial property tax exemption

• Cons– Partially on-balance sheet– Partial property taxes– More complicated– Transaction costs– Market disclosure

Qualifying Improvements = Capital LeaseTri-Party Lease to Include Issuer

T/E Bond Market

Capital Lease Portion Marketedas Tax-Exempt Obligation

Hybrid to take advantage of tax-exempt portion. Health System signs turnkey agreements with Developer. Taxable portion is traditional Developer/REIT lease. Tax-exempt

portion is separated (condo) from remainder and owned by Health System or leased under a capital lease by Health System. Capital for tax-exempt portion sourced at tax-

exempt rates.

18

*Accounting treatment subject to accounting rules applicable to each health care entity. Consult your accounting advisors for an assessment of accounting treatment.

The Best of Both Worlds• Hybrid Solutions for Mixed Use Projects• “Own” the Portion Used by Nonprofit/Gov’t

– Fee Ownership; Condominium; Capital Lease; Installment Purchase

• Lease or Allow Third Party Ownership for Private Portion – Operating Lease– Third Party Ownership

19

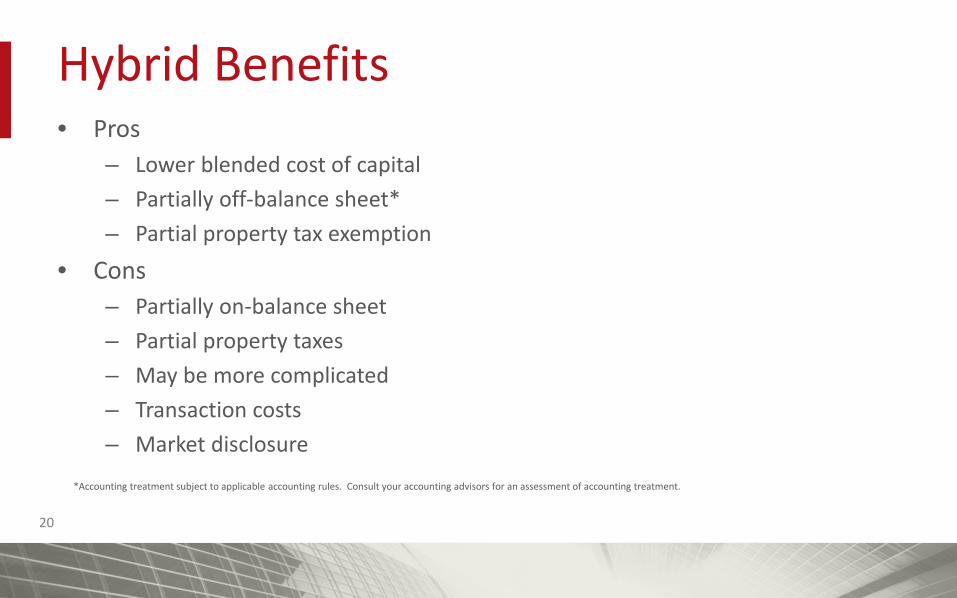

Hybrid Benefits• Pros

– Lower blended cost of capital– Partially off-balance sheet*– Partial property tax exemption

• Cons– Partially on-balance sheet– Partial property taxes– May be more complicated– Transaction costs– Market disclosure

20

*Accounting treatment subject to applicable accounting rules. Consult your accounting advisors for an assessment of accounting treatment.

501(c)(3) Entity

Fee Developer

Conduit Owner

Investor

Long Term Ground LeaseTerminates Upon Repayment

Improvements = Operating Lease BackLease Includes Tax Use Covenants

T/E Obligation• Secured by Lease

Payments & Leasehold Mortgage

• Recourse to Project• Non-Recourse to Issuer

Tax-Exempt Credit Tenant Lease / “Conduit Ownership”• Pros

– Lower cost of capital• Lower than REIT, not as

low as Own and Borrow

– Off-balance sheet*– Property tax exempt

• Dependent on state law

• Cons– Unknown market/

investor reception/funding vehicle– More complicated structure– Market disclosures

Relatively new structure applied in Higher Education, new structure to the Healthcare market. Health System enters into an operating lease with another 501(c)(3) or Governmental Unit that will serve as the owner of the building. Health System manages development and construction in same way as if Health System owned facility. Because both ownership and use are by 501(c)(3) and/or Governmental Unit, building may be financed tax-exempt. Building is on owner’s balance sheet, not Health System’s.

21

*Accounting treatment subject to accounting rules applicable to each health care entity. Consult your accounting advisors for an assessment of accounting treatment.

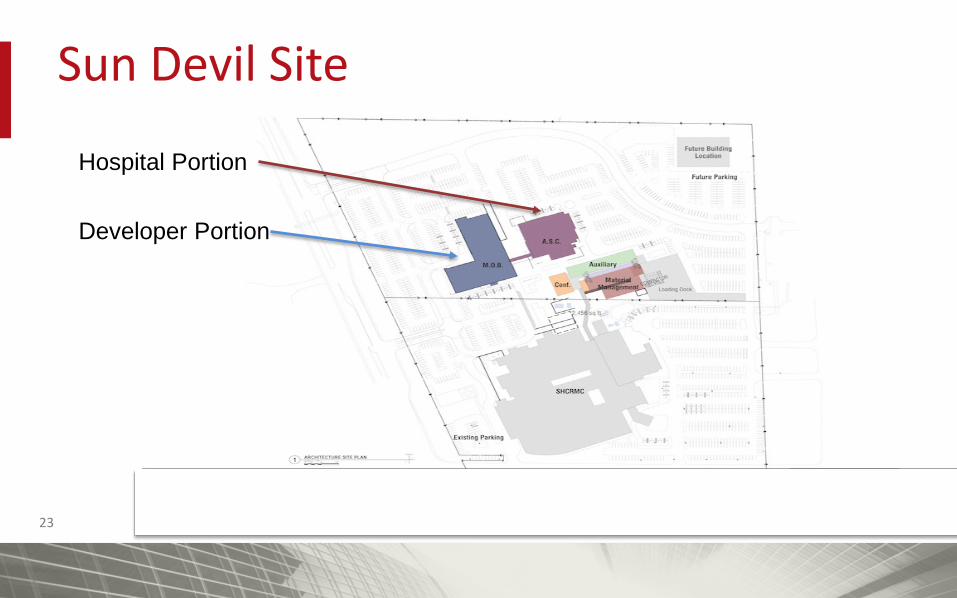

Case Study #1 – Sun Devil• Hospital Campus Development • Two Components

– ASC and Imaging Center (Hospital Portion)– Medical Office Building (Private Portion)

• Hospital Owns All Land – Land Leases Private Portion to Developer

• One Developer; Integrated and Efficient Construction Process• Hospital to Issue Bonds and Own Hospital Portion• Developer to Own Private Portion, Lease Space to Hospital

and Third Parties22

Sun Devil Site

23

Hospital Portion

Developer Portion

Sun Devil Financing• Multiple Lenders

– Bond Purchaser = Bank #1– Developer Lender = Bank #2

• Bank Rights Conflicts Arise on Eve of Closing• Delayed Closing and Nearly Missed Construction Season

• Financing and Use Rights Were Not Coordinated• Development and Construction was Integrated, but not

Financing24

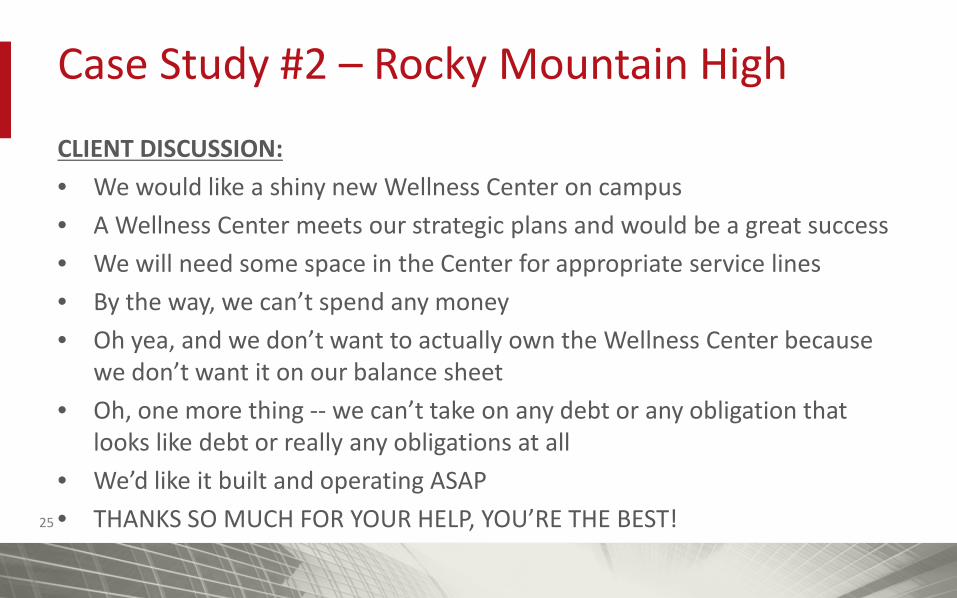

Case Study #2 – Rocky Mountain High

CLIENT DISCUSSION:• We would like a shiny new Wellness Center on campus• A Wellness Center meets our strategic plans and would be a great success• We will need some space in the Center for appropriate service lines• By the way, we can’t spend any money • Oh yea, and we don’t want to actually own the Wellness Center because

we don’t want it on our balance sheet• Oh, one more thing -- we can’t take on any debt or any obligation that

looks like debt or really any obligations at all• We’d like it built and operating ASAP• THANKS SO MUCH FOR YOUR HELP, YOU’RE THE BEST!25

2626

It’s Alive! Creativity to Meet Goals

Nonprofit NewcoHealth System

Developer / Manager PROJECT

Development Agreement

Long TermGround Lease

ManagementAgreement

Condit Issuer

Investors

Loan AgreementPromissory Note

Tax Exempt Bonds1.Senior Series2.Mezzanine Series3.Zero Coupon (“Equity”)

Investment Bankers

Local Government

Community College

Health System

Newco GovernanceNot Controlled nor Consolidated

27

Closing Comments• Mixed-Use Trends Are Real• More Providers are Considering Ownership• Hybrid and Novel Financing Structures = Lowest Blended Cost• Just Like Development and Construction, Financing Must be a

Coordinated Effort• Creativity is Needed

27

Please visit the Hall Render Blog at http://blogs.hallrender.com for more information on topics related to health care law.

Andrew Dick(317) [email protected]

Anchorage | Annapolis | Dallas | Denver | Detroit | Indianapolis | Milwaukee | Raleigh | Seattle | Washington, D.C.

Jerimi Ullom(317) [email protected]