developing a for personal use only -...

TRANSCRIPT

1

Developing a Low Cost Rare Earth Project

NGUALLA RARE EARTH PROJECT, TANZANIA

1st JULY 2014 – GENERAL MEETING

For

per

sona

l use

onl

y

Disclaimer

2

NGUALLA RARE EARTH PROJECT JULY 2014

The information in this document has been prepared as at July 2014. The document is for information purposes only and has been extracted entirely from documents or materials publicly filed with the Australian Stock Exchange and/or the Australian Securities and Investments Commission. This presentation is not an offer or invitation to subscribe for or purchase securities in the Company. The release, publication or distribution of this presentation in certain jurisdictions may be restricted by law and therefore persons in such jurisdictions into which this presentation is released, published or distributed should inform themselves about and observe such restrictions. Certain statements contained in this document constitute “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 and forward looking information under the provisions of Canadian provincial securities laws. When used in this document, the words “anticipate”, “expect”, “estimate”, “forecast”, “will”, “planned”, and similar expressions are intended to identify forward-looking statements or information. Such statements include without limitation: statements regarding timing and amounts of capital expenditures and other assumptions; estimates of future reserves, resources, mineral production, optimization efforts and sales; estimates of mine life; estimates of future internal rates of return, mining costs, cash costs, mine site costs and other expenses; estimates of future capital expenditures and other cash needs, and expectations as to the funding thereof; statements and information as to the projected development of certain ore deposits, including estimates of exploration, development and production and other capital costs, and estimates of the timing of such exploration, development and production or decisions with respect to such exploration, development and production; estimates of reserves and resources, and statements and information regarding anticipated future exploration; the anticipated timing of events with respect to the Company’s mine sites and statements and information regarding the sufficiency of the Company’s cash resources. Such statements and information reflect the Company’s views as at the date of this document and are subject to certain risks, uncertainties and assumptions, and undue reliance should not be placed on such statements and information. Many factors, known and unknown could cause the actual results to be materially different from those expressed or implied by such forward looking statements and information. Such risks include, but are not limited to: the volatility of prices of gold and other metals; uncertainty of mineral reserves, mineral resources, mineral grades and mineral recovery estimates; uncertainty of future production, capital expenditures, and other costs; currency fluctuations; financing of additional capital requirements; cost of exploration and development programs; mining risks; community protests; risks associated with foreign operations; governmental and environmental regulation; the volatility of the Company’s stock price; and risks associated with the Company’s byproduct metal derivative strategies. For a more detailed discussion of such risks and other factors that may affect the Company’s ability to achieve the expectations set forth in the forward looking statements contained in this document, see the Company’s Annual Report for the year ended 30 June 2013, as well as the Company’s other filings with the Australian Securities Exchange and the U.S. Securities and Exchange Commission. The Company does not intend, and does not assume any obligation, to update these forward-looking statements and information.

Competent Person Statement The information in this report that relates to infrastructure, project execution and cost estimating is based on information compiled and / or reviewed by Lucas Stanfield who is a Member of the Australian Institute of Mining and Metallurgy. Lucas Stanfield is the Chief Development Officer for Peak Resources Limited and is a Mining Engineer with sufficient experience relevant to the activity which he is undertaking to be recognized as competent to compile and report such information. Lucas Stanfield consents to the inclusion in the report of the matters based on his information in the form and context in which it appears. The information in the announcement that related to Ore Reserves and estimated mine operating costs was based on information compiled by Mr Ryan Locke, a Competent Person who is a Member of the Australasian Institute of Mining and Metallurgy. Mr Locke is a Principal Planner and is employed by Orelogy Pty Ltd, an independent consultant to Peak Resources. Mr Locke has sufficient experience that is relevant to the style of mineralization and type of deposit under consideration and to the activity being undertaken to qualify as a Competent Person as defined in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Ryan Locke consents to the inclusion in the report of the maters based on his information in the form and context in which it appears. The information in this report that relates to Metallurgical Test Work Results based on information compiled and / or reviewed by Gavin Beer who is a Member of The Australasian Institute of Mining and Metallurgy and a Chartered Professional. Gavin Beer is a Consulting Metallurgist with sufficient experience relevant to the activity which he is undertaking to be recognized as competent to compile and report such information. Gavin Beer consents to the inclusion in the report of the matters based on his information in the form and context in which it appears. The information in this report that relates to Mineral Resources is based on information compiled by Robert Spiers, who is a member of The Australasian Institute of Geoscientists. Robert Spiers is an employee of geological consultants H&S Consultants Pty Ltd. Robert Spiers has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Robert Spiers consents to the inclusion in the report of the matters based on his information in the form and context in which it appears. The information in this report that relates to Exploration Results is based on information compiled and/or reviewed by Dave Hammond who is a Member of The Australasian Institute of Mining and Metallurgy. Dave Hammond is the Technical Director of the Company. He has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves”. Dave Hammond consents to the inclusion in the report of the matters based on his information in the form and context in which it appears.

For

per

sona

l use

onl

y

Capital Structure

3

NGUALLA RARE EARTH PROJECT JULY 2014

ASX: PEK At 27 June 2014 Ordinary Shares on Issue: 334.2m 1 year range: 5.4c to 16.2c

Market Cap at 0.066c: $22.1m Listed Options: PEKO: 51.7m (25c, expire 31 July 2014) PEKOA: 58.7m (10c, expire 30 June 2015)

Since the discovery of the Ngualla Rare Earth Deposit in August 2010, Peak has only expended AU$16.0m on the Ngualla Project to complete the Resource Drill Out, Scoping Study and Preliminary Feasibility Study (March 2014). This rapid, cost effective progress shows Peak has the deposit and the team to deliver positive results for stakeholders.

For

per

sona

l use

onl

y

Board & Management

4

NGUALLA RARE EARTH PROJECT JULY 2014

Key Senior Staff

Darren Townsend Managing Director

• 20 years mining and corporate experience • Extensive experience in managing ASX and TSX listed

companies • East African experience incl. development of tantalum

mine in Mozambique

Patrick Ochieng Project Manager, Ngualla

James Wheeler Country Manager, Tanzania

Kibuta Ongwamuhana Director, Peak Resources (Tanzania) Ltd.

Gavin Beer Consulting Metallurgist

Lucas Stanfield Chief Development Officer

Alastair Hunter Non- Executive Chairman

Jonathan Murray Non- Executive Director

Dave Hammond Technical Director

Jeff Dawkins CFO/Company Secretary

• 40+ years experience in exploration and management • Formerly a Director of Peninsula Minerals NL, Matlock

Mining NL and Anglo Australian Resources NL

• 25 years technical and management experience • Former Exploration Manager with De Grey Mining

Limited and Sons of Gwalia. Previously with Billiton/Gencor in Africa

• Partner at independent corporate law firm Steinepreis Paganin specialising in equity capital raisings, acquisitions and divestments, governance and corporate compliance

• 20 years in corporate roles in Perth, London and Singapore. Senior Finance experience with listed resource companies F

or p

erso

nal u

se o

nly

Rare Earth Applications

5

NGUALLA RARE EARTH PROJECT JULY 2014

• Green technologies and consumer electronics

• 2013: $3-4B market, ~108,500tpa REO (2014, IMCOA)

• The magnet industry (Nd – Pr) is the largest consumer of rare earths (>35% by value) and is forecast to show the highest growth at 10%pa driven by increasing demand from the wind turbine, automobile and personal electronics sectors

2016 Forecast Consumption by Sector

Lighting / flat panel screens / lasers

Catalytic converters / optical glass

Glass polishing / catalytic converters / yellow ceramics & glass

Portable electronics / magnets for wind turbines & hybrid electric cars

Peak Resources Ngualla Project relative value contributors by product type and constituent REO’s

For

per

sona

l use

onl

y

Rare Earth Magnets

6

NGUALLA RARE EARTH PROJECT JULY 2014

• Growth driven by automotive industry, wind farms and hybrid and electric vehicles

• NdFeB magnets the largest market at 23,000t in 2013 • Hybrid and electric vehicles: 15-20% forecast growth

2012-20 • Direct drive technologies for large new offshore wind

turbines rely on NdFeB magnets

Source: Lynas Corporation Presentation 30 April 2014

Estimated REO demand in magnet industry

For

per

sona

l use

onl

y

Tanzania

7

NGUALLA RARE EARTH PROJECT JULY 2014

• Established mining culture • Third largest gold

producer in Africa

• Politically stable

• Government investment incentives and guarantees

• Transportation infrastructure

For

per

sona

l use

onl

y

Ngualla Resource

8

NGUALLA RARE EARTH PROJECT JULY 2014

• 195Mt at 2.26% REO containing 4.4Mt REO including:

Bastnaesite Zone weathered: 21.6Mt at 4.54% REO for 982,000t contained REO

• One of the highest grade undeveloped Rare Earth projects in the world (See Appendix D for project comparison)

• Open pit mining, low strip

• 58 year mine life in Bastnaesite Zone alone

• Simple logistics- low tonnage high value product

For

per

sona

l use

onl

y

Ngualla Ore Reserve

9

NGUALLA RARE EARTH PROJECT JULY 2014

• 86% of Reserve is highest category of Proved

• Reserve positions Ngualla as one of the largest in the world outside of China

• Reserve represents only 22% of Resource (contained REO tonnes)

Reserve Summary and Classification

Classification Ore Tonnes (Mt)

REO % Contained REO tonnes

Proved 18.0 4.53 817,000

Probable 2.70 4.62 124,000

Total 20.7 4.54 941,000

A 3% cut-off grade is applied. Reported according to the JORC Code and Guidelines in ASX announcement ‘Ngualla Rare Earth Project - Maiden Ore Reserve’ of 19 March 2014.

For

per

sona

l use

onl

y

Ngualla a Giant Deposit

10

NGUALLA RARE EARTH PROJECT JULY 2014

Ore Reserves (blue) or life of mining schedules (grey) from Company filings

For

per

sona

l use

onl

y

Ngualla’s Value drivers – Nd, Pr, Eu

11

NGUALLA RARE EARTH PROJECT JULY 2014

• Aligned with Rare Earth market value, demand and growth

• 83% revenue underpinned by high value Magnet and Critical rare earths

• Increasing demand will support prices

• Rare earth price movements since 1 July 2013

• Ngualla’s main value drivers show large price increases

• Ngualla’s forecast annual production of Nd and Pr is equal to just 73% of one year’s forecast demand growth

Pe

rce

nta

ge C

han

ge 1

Ju

ly 2

01

3 t

o 3

1 M

arch

20

14

(M

eta

l Pag

es)

Recent price movements

For

per

sona

l use

onl

y

Mineralogy – key to low risk and costs

12

NGUALLA RARE EARTH PROJECT JULY 2014

• Weathered Bastnaesite Zone – simple mineralogy

• Host rock leached of carbonates

• No phosphate or monazite

• Non radioactive – U 16ppm, Th 59ppm in Ore Reserve

Mineralogy distinguishes a quality deposit

Enables simple 3 stage metallurgical process F

or p

erso

nal u

se o

nly

Metallurgy - Overview

13

NGUALLA RARE EARTH PROJECT JULY 2014

• Simple three stage process

• Demonstrated, proven metallurgical process from mineralisation to high purity separated products

• Low operating and capital costs

For

per

sona

l use

onl

y

Economic Assessment – (Preliminary Feasibility Study March 2014)

14

NGUALLA RARE EARTH PROJECT JULY 2014

NPV @ 10% discount rate (Post-tax and Royalties) US$ 1.005 billion

IRR (Post-tax and Royalties) 39% NPV & IRR

Capital cost (including 30% contingency) US$ 367 million

Pay back from production start up In 3rd Year

Average (LoM) Cash Cost (FOB) (excluding amortisation, depreciation and royalties)

US$ 11.74 / kg

Average Annual Revenue (after Ramp Up) US$ 295 million

Average Annual Post-Tax and Royalties Cashflow US$ 121 million

In-Ground Basket Price (FOB) US$ 29.29 / kg

Average Annual REO Production 10,069 tonnes

Capital Expenditure

Cash Cost

Financial KPIs

The Economic Assessment assumptions are contained within the ‘Peak Resources Delivers Robust PFS for Ngualla’ ASX announcement of 19 March 2014 Please refer to safe-harbour statement at beginning of this presentation

For

per

sona

l use

onl

y

CAPEX Comparisons – US$M

15

NGUALLA RARE EARTH PROJECT JULY 2014

1. Production of 20,000t of separated rare earth oxides 2. Production of 20,000t of separated rare earth oxides. Uranium, gypsum, phosphate by-products 3. Production of 20,000t of separated rare earth oxides. Zirconium by-product Source: Company filings

Capital cost comparisons of major rare earth development and production projects

For

per

sona

l use

onl

y

$6.40 $6.55

$10.93 $11.74

$13.08 $14.06 $14.50

$19.86

0

5

10

15

20

25

Bear Lodge2

Rare Element

Resources

Norra Karr3

Tasman Metals

Ngualla

Peak Resources

Zandkopsdrift4

Frontier Metals

Mt Weld5

Lynas Corp

Nolans Bore

Arafura Resources

Strange Lake6

Quest Rare Minerals

OPEX Comparisons – US$/kg contained REO Product

16

NGUALLA RARE EARTH PROJECT JULY 2014

Green = Lower Value Mixed RE Carbonate/Concentrate Blue = High Value Separated RE Products

US$

/kg

Kvanfjeld1

GreenlandMinerals

1. Mixed rare earth carbonate. After uranium and zinc by product credits ‘Mine and Concentrator Study 26th March 2013’ 2. Mixed rare earth concentrate (+90% REO) ‘Technical Report 43-101 26th June 2013’ 3. Mixed rare earth carbonate, grade unknown (50-60% REO?) ‘PEA 43-101 9th July 2013’ 4. Opex per saleable RE product ‘PEA 30th March 2012’ 5. Production cost target at 22,000tpa REO production rate $14-15/kg ‘Quarterly Reports 2013’ 6. Opex for REO based on relative values of REO to by-products (niobium & zirconium)

Source: Company filings

For

per

sona

l use

onl

y

Development Pathway

17

NGUALLA RARE EARTH PROJECT JULY 2014

• Secure strategic investor, technical and off take partners

- MOU with Chinese end user signed 12 December 2013

- Discussions are progressing positively with a number of potential strategic partners in China, the Middle East, as well as financial institutions in the United Kingdom, Europe and Australia with the objective of funding the development of the Ngualla Rare Earth Project.

- Aim is to secure a Strategic Investor to further enhance project credibility, minimise dilution for existing shareholders.

- Asset retains full strategic appeal with no marketing/off take currently in place.

- Strong expression of interest from a party in relation to a potential off take agreement for a portion of Peak’s planned 10,000 tonne per annum Separated Rare Earth Production.

- Prefer solutions that have strategic benefits such as technical expertise, access to low cost (semi) government debt, cradle to the grave financing solutions.

For

per

sona

l use

onl

y

Current Development Work

18

NGUALLA RARE EARTH PROJECT JULY 2014

• Trenching on site to obtain 16 tonne bulk sample for beneficiation pilot plant operation

• Flotation test work in progress at IMO in Perth targeting increased REO recoveries and concentrate grades to further reduce OPEX

• Baseline environmental surveys commencing to support ESIA for regulatory approvals

For

per

sona

l use

onl

y

Development Pathway

19

NGUALLA RARE EARTH PROJECT JULY 2014

• Metallurgical process optimisation

- Optimisation of beneficiation- A visit to a specialist rare earth mineral processing institution in China was recently completed to investigate the potential to use Chinese technology and experience to further optimise the beneficiation process. This will be completed parallel with further beneficiation work in Australia.

- Acid leach optimisation - Acid recycling

• Definitive Feasibility Study

- Beneficiation and acid leach pilot plants

For

per

sona

l use

onl

y

Investment Highlights of Ngualla Project- Tanzania

20

NGUALLA RARE EARTH PROJECT JULY 2014

Economic Assessment – (Preliminary Feasibility Study) • Magnet and Critical Rare Earths • High value Growth Markets

83% OF

ANNUAL REVENUE

Metallurgical Process Robust Project Economics (Preliminary Feasibility Study)

Large Quality Reserve

• High grade • Mineralisation

at surface

• Low OPEX US$11.74/kg separated rare earth products

• Low CAPEX US$367M (including SX Plant and 30% contingency)

• Average Annual Revenue US$295M Payback in 3rd year

• >50 year mine life

• Demonstrated low cost processing route from mineralisation to high purity separated rare earth oxides

• Favourable Mineralogy • Very low U and Th • Potential to produce non class 7

concentrate

For

per

sona

l use

onl

y

Developing a low cost rare earth project in Tanzania

21

NGUALLA RARE EARTH PROJECT JULY 2014

Thank you Peak Resources Limited

Head Office: Level 2, 46 Ord Street West Perth, Western Australia 6005 Ph: +61 8 9200 5360 Fax: +61 8 9226 3831 ASX Code: PEK [email protected] www.peakresources.com.au

For

per

sona

l use

onl

y

Appendix A – Product and value splits

22

NGUALLA RARE EARTH PROJECT JULY 2014

The value drivers for Ngualla are the Nd- Pr and Mid+HRE >99% purity products

These include the higher value ‘Critical RE’s’ forecast to be in undersupply.

83% of the annual revenue (March 2014 Preliminary Feasibility Study) is from the high purity Nd – Pr and Heavy Rare Earth products.

The lower value Ce and La are relative by-products at only 17% of the total revenue.

Product Status of production of high purity REO products

Total equivalent REO Production t/y*

Relative Value Contribution

Nd – Pr Oxide Completed 2,250 71%

Mid+Heavy Oxide Completed 245 12%

La Oxide Completed 3,042 8%

Ce Oxide Completed 4,542 9%

Total 10,069 100%

For

per

sona

l use

onl

y

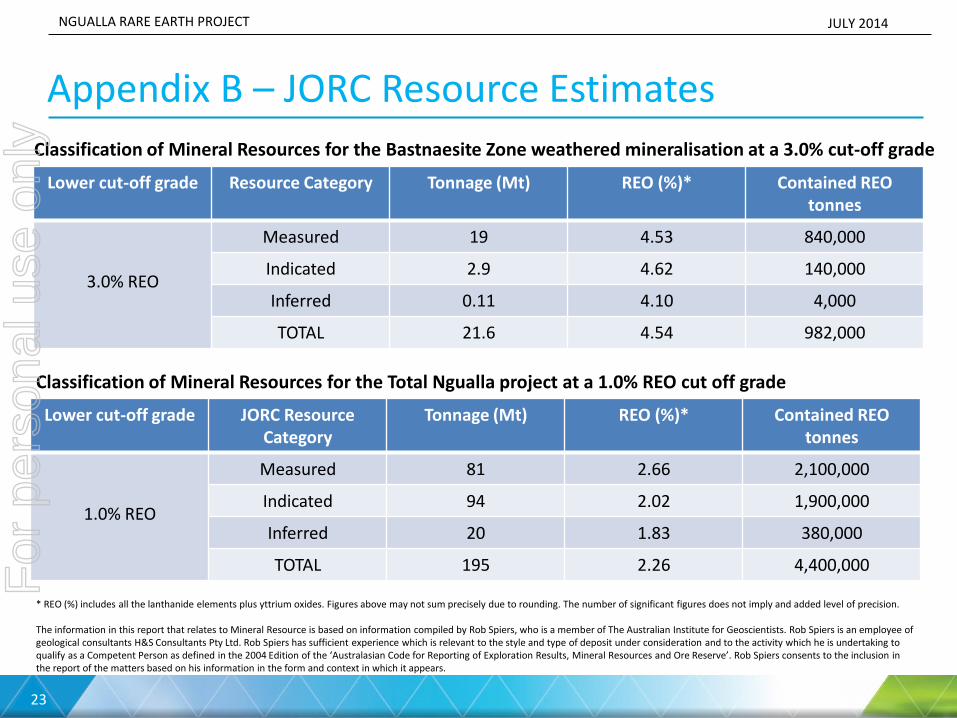

Appendix B – JORC Resource Estimates

23

NGUALLA RARE EARTH PROJECT JULY 2014

Classification of Mineral Resources for the Bastnaesite Zone weathered mineralisation at a 3.0% cut-off grade

Lower cut-off grade Resource Category Tonnage (Mt) REO (%)* Contained REO tonnes

3.0% REO

Measured 19 4.53 840,000

Indicated 2.9 4.62 140,000

Inferred 0.11 4.10 4,000

TOTAL 21.6 4.54 982,000

Lower cut-off grade JORC Resource Category

Tonnage (Mt) REO (%)* Contained REO tonnes

1.0% REO

Measured 81 2.66 2,100,000

Indicated 94 2.02 1,900,000

Inferred 20 1.83 380,000

TOTAL 195 2.26 4,400,000

Classification of Mineral Resources for the Total Ngualla project at a 1.0% REO cut off grade

* REO (%) includes all the lanthanide elements plus yttrium oxides. Figures above may not sum precisely due to rounding. The number of significant figures does not imply and added level of precision. The information in this report that relates to Mineral Resource is based on information compiled by Rob Spiers, who is a member of The Australian Institute for Geoscientists. Rob Spiers is an employee of geological consultants H&S Consultants Pty Ltd. Rob Spiers has sufficient experience which is relevant to the style and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserve’. Rob Spiers consents to the inclusion in the report of the matters based on his information in the form and context in which it appears.

For

per

sona

l use

onl

y

Appendix C – Globally significant RE Deposits – Grade is King

24

NGUALLA RARE EARTH PROJECT JULY 2014

• Critical rare earths and head grade have Ngualla ‘outside the pack’

For

per

sona

l use

onl

y

Appendix D – Demand versus Peak Planned Supply

25

NGUALLA RARE EARTH PROJECT JULY 2014

2013 WORLD MARKET Forecast Peak Planned Annual

Production

Rare Earth Oxide 2013 Demand

(tonnes)^ Price

(US$/kg)* Value

(US$ M)

Average Annual Growth to 2017

(tonnes p.a) (tonnes p.a)

Ligh

t R

are

Eart

hs Lanthanum 31,700 $7.56 240 2,275 3,042

Cerium 39,850 $7.80 311 2,861 4,542

Praseodymium 6,075 $93.96 571 3,081 2,240 combined

Neodymium 18,925 $70.01 1,325

Samarium 730 $14.12 10 168

Hea

vy R

are

Eart

hs

Europium 330 $1,132.60 374

706 245 combined

Gadolinium 1,360 $46.50 63

Terbium 255 $949.04 242

Dysprosium 780 $540.38 422

Erbium 780 $59.50 46

Yttrium 7,585 $25.27 192

Ho-Tm-Yb-Lu 130 - - 34 -

Total 108,500 $3,795 9,125 10,069

* Average Metal Pages Price for Calender Year 2013 except for Erbium which is based on Ngualla PFS Price

^ IMCOA, Rare Earths Quarterly Bulletin 6, 5 February 2014

l Critical Rare Earth, US DoE 'Critical Materials Strategy report, December 2011'

• Light RE: $2.4billion or 65% annual market value. Heavy RE: 35% • Magnet metals: Nd – Pr are 50% of 2013 world market value and forecast to grow to 54% in 2016

For

per

sona

l use

onl

y

Appendix E - Segment Capital and Opex Preliminary Feasibility Study

26

NGUALLA RARE EARTH PROJECT JULY 2014 F

or p

erso

nal u

se o

nly

Appendix F - Economic Sensitivity – PFS

27

NGUALLA RARE EARTH PROJECT JULY 2014

NPV Sensitivities- Opex, Capex, Price

NPV v Basket Price

Change

IRR Sensitivities- Opex, Capex, Price

IRR Sensitivities- Basket Price

Basket Price (USD/kg)

Change

Basket Price (USD/kg)

NP

V (

USD

M)

IRR

%

NP

V (

USD

M)

IRR

%

For

per

sona

l use

onl

y

Appendix G

28

NGUALLA RARE EARTH PROJECT JULY 2014

List of specialist consultants behind the Peak team

Company Responsibility

ANSTO SX pilot plant

Amdel B.V Comminution test work

P.D.C Scoping study project management, infrastructure, tailings, services, environmental, civil engineering, logistics and independent technical report preparation

Hatch Mineral Process engineering, including sulphuric acid plant, comminution and beneficiation circuits, rare earth recovery and solvent extraction plants

H&S Consulting Pty Ltd Independent specialists for Mineral Resource model and estimation

Independent Metallurgical Operations Pty Ltd (IMO)

Beneficiation process design and test work

Met-Chem Consulting Pty Ltd Beneficiation and hydrometallurgical process flow sheet studies and development

Nagrom Beneficiation and metallurgical test work

Orelogy Mine engineering, geotechnical, pit optimisation and scheduling

Roger Townend Mineralogy

Simulus Engineers Process modelling including mass and energy balance

SGS Australia Laboratories Analytical laboratory for drill samples

Dr Wally Witt Geological specialist consultant

For

per

sona

l use

onl

y