devaluation risk and default risk: on the costs and benefits of dollarization/euroization andrew...

TRANSCRIPT

Devaluation Risk and Default Risk:Devaluation Risk and Default Risk:On the costs and benefits of On the costs and benefits of Dollarization/EuroizationDollarization/Euroization

Andrew PowellAndrew Powell

Universidad Torcuato Di Tella, Buenos AiresUniversidad Torcuato Di Tella, Buenos Aires

Presentation: London School of EconomicsPresentation: London School of Economics

May 2002May 2002

The Costs and Benefits Depend on Country Circumstances

• Dollarization to consolidate a reform agendaDollarization to consolidate a reform agenda– El Salvador 2001; Argentina 1999?

• Dollarization as an element of crisis resolutionDollarization as an element of crisis resolution– Ecuador 2000; Argentina 2002?

Argentina 1999:Argentina 1999:a short history (1)a short history (1)

• Argentina hit by the attack on Hong Kong (Oct 1997) and the Russian crisis (Mid-1998)

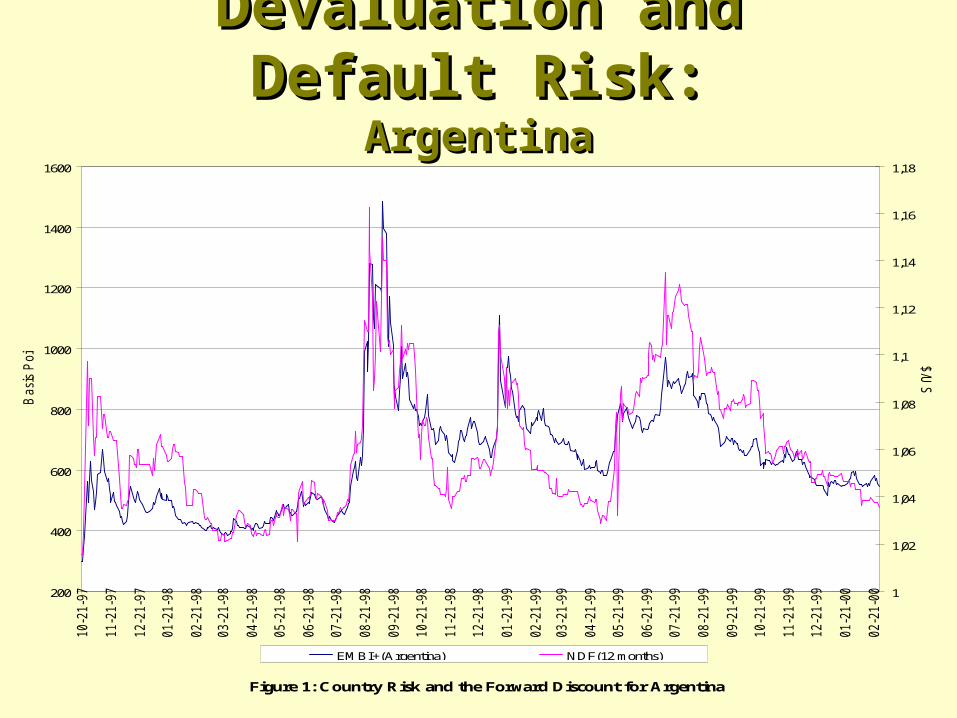

• Under the Currency Board, a strong correlation between devaluation risk and default risk

• Through 1988, a small group in Central Bank and Ministry considered full dollarization

• Informal talks with US authorities in late 1988

Devaluation and Default Risk:Devaluation and Default Risk:ArgentinaArgentina

200

400

600

800

1000

1200

1400

1600

10-2

1-9

7

11-2

1-9

7

12-2

1-9

7

01-2

1-9

8

02-2

1-9

8

03-2

1-9

8

04-2

1-9

8

05-2

1-9

8

06-2

1-9

8

07-2

1-9

8

08-2

1-9

8

09-2

1-9

8

10-2

1-9

8

11-2

1-9

8

12-2

1-9

8

01-2

1-9

9

02-2

1-9

9

03-2

1-9

9

04-2

1-9

9

05-2

1-9

9

06-2

1-9

9

07-2

1-9

9

08-2

1-9

9

09-2

1-9

9

10-2

1-9

9

11-2

1-9

9

12-2

1-9

9

01-2

1-0

0

02-2

1-0

0

Figure 1: Country Risk and the Forward Discount for Argentina

Basi

s P

oin

ts

1

1,02

1,04

1,06

1,08

1,1

1,12

1,14

1,16

1,18

$/U

S$

EMBI+(Argentina) NDF(12 months)

Argentina 1999:Argentina 1999:a short history (2)a short history (2)

• January 1999: Brazil devalued

• ex President Menem stated Argentina may fully dollarize and asked for opinion

Argentina 1999:Argentina 1999:a short history (3)a short history (3)

• Ex Central Bank President, Pedro Pou, stated there are 3 ways to dollarize and stated:– A) He was against unilateral dollarization– B) That full monetary union was impractical– C) But, Dollarization subject to a “Monetary Treaty”

with the US could be beneficial to Argentina and warranted more serious consideration.

What would be in a Monetary Treaty?What would be in a Monetary Treaty?

• Argentina suggested the Treaty include:– a rule to share seigniorage– a way of using seigniorage flows to

collateralize a liquidity facility– Cf: Central Bank’s Contingent Repo. Facility

(subsequently used successfully in 2001)

• The US ruled out:– changing US monetary policy– being a “lender of last resort”– supervising Argentine banks

Potential CostsPotential Costs• Seigniorage

– with the Treaty, less of an issue– Perhaps not much of an (economic) issue

anyway, more politics than economics

• Lender of last resort– with the Treaty less of an issue

• Main Costs– Notions of sovereignty– Giving up the option of future monetary policy– But Argentina 2002 shows, never say never!

Potential BenefitsPotential Benefits

• Eliminating devaluation risk– Eliminate peso interest rates– Lower default risk: Powell and Sturzenegger (2002)

• Locking in reforms– Argentina: doubling the ‘bet’ of the c. board

• Deeper trade/financial integration into US$ zone– Argentina: already highly dollarized - financially– but tension with Mercosur (cf: UK and EU?)

Powell and SturzeneggerPowell and Sturzenegger

• Eliminating devaluation risk could go either way– balance sheets vs.– inflexibility, inflation tax, seniority arguments

• Standard time series analyses fatally flawed – joint tests of ‘efficiency’ and ‘causality’– peso bond markets less liquid & less efficient

• To avoid this problem, we conducted an ‘event’ study of exchange rate “events” on “default risk”

Powell and SturzeneggerPowell and Sturzenegger

• Latin American Countries

– Lat. Am.: events related to ‘currency risk’– Events Selected by colleagues in the region– Default risk: dollar spreads

• European Countries pre-EMU– Events that altered perception of EMU success– Events from Zettlemeyer (1996)/Ungerer(1997)– Default risk: spreads on DM bonds

Default and “Devaluation” RiskMexico

200

400

600

800

1000

1200

1400

06-0

2-9

7

08-0

2-9

7

10-0

2-9

7

12-0

2-9

7

02-0

2-9

8

04-0

2-9

8

06-0

2-9

8

08-0

2-9

8

10-0

2-9

8

12-0

2-9

8

02-0

2-9

9

04-0

2-9

9

06-0

2-9

9

08-0

2-9

9

10-0

2-9

9

12-0

2-9

9

02-0

2-0

0

Basi

s P

oin

ts

8

9

10

11

12

13

14

15

16

Figure 2: Country Risk and the Forward Discount for Mexico

$/U

S$

EMBI+(Mexico) NDF (12 months)

Event Study: Methodology

Estimation window:

10 days

Event window:

4 days

Post-event window:

5 days

-14

Day of event

The Constant Mean Model

-4 -3 0 1 5

Figure 3: The Setup for the Constant Mean Model

ArgentinaBad News on Currency Risk

Figure 13: Response of Country Risk to bad news on Currency for Argentina

-20

-10

0

10

20

30

40

50

60

70

80

-20 -19 -18 -17 -16 -15 -14 -13 -12 -11 -10 -9 -8 -7 -6 -5 -4 -3 -2 -1 1 2 3 4 5 6 7 8 9 10

Basis

Po

ints

Estimation window Event window Post-event window

MexicoBad News on Currency Risk

Figure 10: Response of Country Risk to bad news on Currency for Mexico

-100

0

100

200

300

400

500

600

700

-20 -19 -18 -17 -16 -15 -14 -13 -12 -11 -10 -9 -8 -7 -6 -5 -4 -3 -2 -1 1 2 3 4 5 6 7 8 9 10

Ba

sis

Po

ints

Estimation window Event window Post-event window

ChileBad News on Currency Risk

Figure 14: Response of Country Risk to bad news on Currency for Chile

-15

-10

-5

0

5

10

-20 -19 -18 -17 -16 -15 -14 -13 -12 -11 -10 -9 -8 -7 -6 -5 -4 -3 -2 -1 1 2 3 4 5 6 7 8 9 10

Ba

sis

Po

ints

Estimation window Event window Post-event window

Summary of the ResultsSummary of the Resultsfor Latin Americafor Latin America

Powell and SturzeneggerPowell and Sturzenegger

• Highly dollarized countries: strong positive effect from devaluation risk to default risk

• Others: not significant or ‘other way’

Summary of the ResultsSummary of the ResultsEMU CountriesEMU CountriesPowell and SturzeneggerPowell and Sturzenegger

• Countries that entered EMU: strong negative effect from EMU ‘success’ to default risk

• Countries that did not enter EMU initially: not significant or ‘other way’

• Exception: Portugal but not so clear ex ante

Argentina 1999:Argentina 1999:Dollarization, A missed opportunity?Dollarization, A missed opportunity?• Would Argentina have avoided crisis?• Depends on preferred crisis explanation - see

Powell 2002.– Dollarization would have helped

• reducing devaluation risk/default risk

• increasing confidence/investment/growth

– Dollarization would not have helped• problems of ‘competitiveness’

• fiscal problems not related to growth

Would dollarization haveWould dollarization havebeen permanent?been permanent?

• If dollarization had been perceived as permanent, had reduced default risk and enhanced fiscal sustainability sufficiently, then it would have been permanent!

• If dollarization had not been perceived as permanent or competitiveness problems had been paramount then it might not.

• A monetary treaty would have provided some incentives towards permanence

Motives for DollarizationMotives for DollarizationEl Salvador (2001)El Salvador (2001)

• Locking in successful reforms• Deeper trade and financial integration into US

dollar area (70% of trade with US or ‘dollarized’, remittances are 15% of GDP)

• Lower interest rates: but El Salvador was not highly dollarized previously, reduction in interest rates due to replacement of colon with dollar rates and wider credit availability

Dollarization as Crisis Dollarization as Crisis Resolution: Ecuador 2000Resolution: Ecuador 2000

• Main surprise: dollarization helped to stabilise the banking system despite bank resolution process being far from complete

• Seems consistent with empirical results relating exchange rate regimes and financial system size.

• But against some theoretical views; that dollarization implies no lender of last resort so less depositor confidence.

Argentina 2002Argentina 2002• Authorities caught between

– political and economic costs of the financial system restrictions (“el corralito”).

– potential exchange rate instability and inflationary consequences if lifted

• Argentina cannot grow until this solved– if solved without generating an inflationary

spiral, it may be possible to create some monetary instruments and hence an independent monetary policy (a First Best).

– if not, Argentina will most likely have to reinvent Convertibility or Dollarize

Argentina and the IMF:Argentina and the IMF:a game with no solution?a game with no solution?

• The IMF has called for a ‘sustainable plan’• If the IMF Assists, it may fear this reduces

the incentives for prudence (Moral Hazard).• President Duhalde has said it is difficult to

see a ‘sustainable plan’ without the IMF.• But if Argentina had a ‘sustainable plan’,

why would not need the IMF?• Unfortunately Argentina has now wasted 4

months post-default/devaluation

ConclusionsConclusions• Dollarization has been thought of in two ways:

– to consolidate reforms & deepen integration

– as crisis resolution.

• In the case of an El Salvador or Argentina (1999):– the main costs are related to notions of sovereignty and

(possibly) giving up future monetary policy

– the main immediate gain is lower interest rates especially in dollarized economies (Powell & Sturzenegger).

• In the case of Ecuador dollarization helped to stabilise the financial system.

• Argentina 2002: dollarization should not be ruled out, otherwise it may very well still happen!