deutsche bank - l'oréal investisseurs et actionnaires mass market hair & beauty salons...

TRANSCRIPT

Jean-Paul AGON Chairman and CEO

Deutsche Bank JUNE 19th 2014

1 // June 19th 2014

STRONG

STRATEGIC

CONTINUITY

I

2 // June 19th 2014

A PURE PLAYER IN BEAUTY FOR 105 YEARS

3 // June 19th 2014

L’ORÉAL MEETS ALL BEAUTY NEEDS & ASPIRATIONS

ACROSS ALL BEAUTY CATEGORIES

ACROSS ALL DISTRIBUTION CHANNELS

4 // June 19th 2014

TRAVEL RETAIL

BRANDED BOUTIQUES

PHARMACIES DRUGSTORES MEDISPAS

DEPARTMENT STORES PERFUMERIES

MASS MARKET

HAIR & BEAUTY SALONS

MAKE-UP FRAGRANCES HAIR COLOR HAIRCARE SKIN CARE

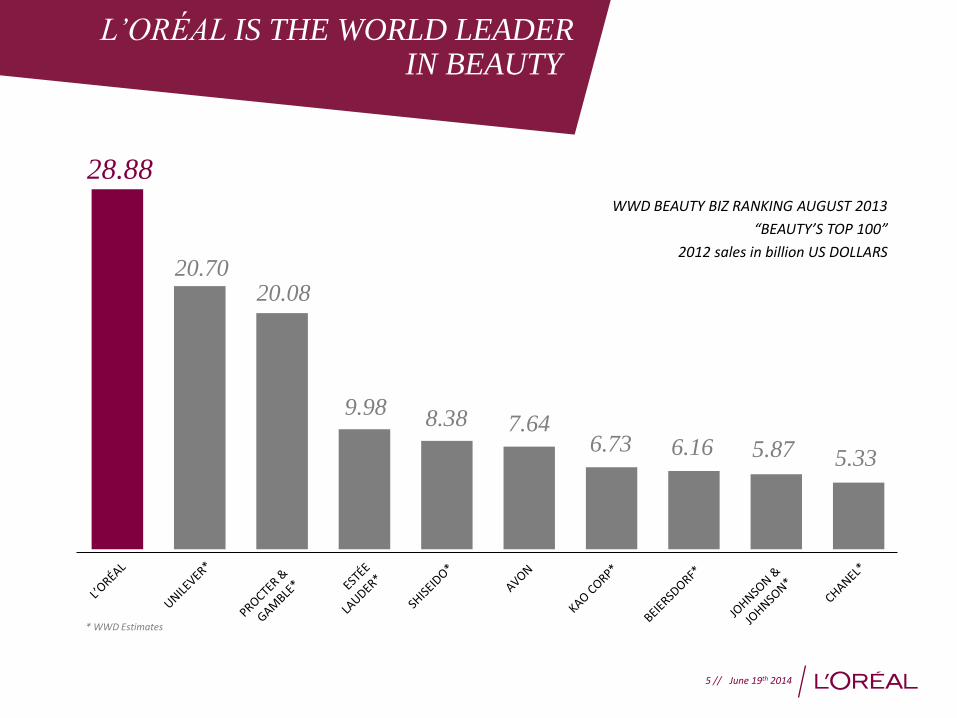

28.88

20.70 20.08

9.98 8.38 7.64

6.73 6.16 5.87 5.33

* WWD Estimates

L’ORÉAL IS THE WORLD LEADER IN BEAUTY

WWD BEAUTY BIZ RANKING AUGUST 2013

“BEAUTY’S TOP 100”

2012 sales in billion US DOLLARS

5 // June 19th 2014

RESEARCH & INNOVATION AT THE HEART OF OUR BUSINESS MODEL

3.4% OF SALES

R&I

6 // June 19th 2014

*

* Pro-forma 2013 – Galderma & Inneov consolidated under the equity method, in application of IFRS 11.

A UNIQUE PORTFOLIO OF COMPLEMENTARY BRANDS

7 // June 19th 2014

€ 2 Bn

€ 300 m

2013 1995

€ 530 m

€ 40 m

2013 1999

CAGR 21%

CAGR 12%

8 // June 19th 2014

SINCE ACQUISITION

IN 2011

x2.5 SALES

ACQUISITION IN 2012 +42%

SALES

*2013 Like-for-like sales growth 9 // June 19th 2014

*

WESTERN EUROPE

35.1 %

BREAKDOWN OF 2013 COSMETICS SALES BY REGION

BALANCED GEOGRAPHIC POSITIONS

NEW MARKETS

39.8 %

NORTH AMERICA

25.1 %

10 // June 19th 2014

22.2% 18.7% 19.2%

20.1%**

Western Europe

North America

New Markets

20.5% 19.9% 20.0% 21.2%

20.1%**

Professional Products

Consumer Products

L’Oréal Luxe

Active Cosmetics

BY DIVISION* (as a % of sales)

BALANCED OPERATING PROFIT

BY REGION* (as a % of sales)

* Before central group expenses, fundamental research expenses, stock-option & free grant of shares expenses and miscellaneous items – as a % of total cosmetics sales ** Cosmetics divisions total

11 // June 19th 2014

2013 KEY FINANCIAL FIGURES IN MILLION EUROS

% change

2013 Reported At constant exchange rates***

Consolidated sales 22 977 +2.3% +6.0%

Operating profit 3 875 +4.8% +7.8%

Net profit* 3 117 +4.9% +7.4%

Earnings per share** (in euros) 5.13 +4.4% +7.0%

Net operating cash flow 2 689 +4.4%

*Excluding non-recurring items attributable to owners of the company **Diluted earnings per share based on net profit excluding non-recurring items, attributable to owners of the company *** 2013 figures at 2013 rates / 2012 figures at 2013 rates

12 // June 19th 2014

CONTINUOUS PRODUCTIVITY & EFFICIENCY ENHANCEMENTS

INTEGRATED ON/OFF LINE

MEDIA STRATEGY

ON-GOING OPTIMISATION

OF OUR MEDIA BUYING

ECONOMETRIC MODELING

40 Cosmetics factories worldwide

(excl. Dermatology)

REENGINEERING OF OUR INDUSTRIAL FOOTPRINT & LOGISTICS NETWORK

OPERATIONS GROWTH DRIVERS

OPTIMISATION OF SUPPORT FUNCTIONS AND SYSTEMS

ORGANISATIONS

ON-GOING ASSESSMENT OF OUR PROCUREMENT PERFORMANCE

13 // June 19th 2014

SOLID BALANCE SHEET IN BILLION EUROS

ASSETS LIABILITIES

1.8 2.6 6.2 6.3

6.4 6.7 0.2 0.4

21.3 21.9

2.2 2.0

20.9 22.6

Non-current

liabilities

12.31.2012 12.31.2013 12.31.2012 12.31.2013

Current liabilities

Financial debt (current & non-current)

Non-current

assets

Current

assets

Cash & cash

equivalents

Total Assets 29.5 31.3

Shareholders’

equity

Total Liabilities 29.5 31.3

14 // June 19th 2014

OPERATIONAL & FINANCIAL ROBUSTNESS: A POWERFUL & LONG TERM BUSINESS MODEL

0.008 0.025

0.097

0.44

0.00

0.50

1.00

1.50

2.00

2.50

196

3

196

4

196

5

196

6

196

7

196

8

196

9

197

0

197

1

197

2

197

3

197

4

197

5

197

6

197

7

197

8

197

9

198

0

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

2.50*

1990

1970

2000

1980

2010

1.80

2.00

2.30

*Approved at the shareholders’ meeting held on April 17th, 2014

2013 dividend per share

2.30€ 2.50€*

2012 2013

+8.7%

15 // June 19th 2014

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

48.7%**

30.2%

31.6%

33.6%

35.7% 36.0% 36.6% 36.8%

38.5%

39.6%

41.1% 41.3%

43.9% 44.9%

46.3%

29.1%

* Taking into account the Sanofi history with regards to the dividends. ** Based on the dividend approved at the AGM held on April 17th, 2014

46.8%

PAY-OUT RATIO: 1997-2013 AS A % OF NET PROFIT*

16 // June 19th 2014

A NEW L’ORÉAL

II

17 // June 19th 2014

1/ NEW STRATEGY

2/ NEW INNOVATION FIREPOWER

3/ RECENT ACQUISITIONS TO COMPLEMENT OUR PORTFOLIO

4/ NEW GEOGRAPHICAL FOOTPRINT

5/ NEW MARKETING MODEL

6/ NEW SUSTAINABILITY COMMITMENTS

7/ NEW SHAREHOLDING STRUCTURE

18 // June 19th 2014

1/ ACCELERATED EXPANSION OF THE MIDDLE CLASS

LATIN AMERICA

8%

NORTH AMERICA

10%

EUROPE

22%

ASIA PACIFIC

54%

MIDDLE EAST AND

NORTH AFRICA

5%

SUB SAHARAN

AFRICA

2%

2020 2009

1.8

3.2

GEOGRAPHICAL SPLIT OF THE GLOBAL MIDDLE CLASS 2020* GLOBAL

MIDDLE CLASS*

(IN BILLION)

*OECD 2010. The emerging middle class in developing countries

19 // June 19th 2014

1/ OUR STRATEGY

UNIVERSALIZATION

OUR OBJECTIVE: 1 BILLION NEW CONSUMERS

GLOBALIZING

WHILE RESPECTING

DIFFERENCES

20 // June 19th 2014

2/ A STRONG CORE AND FIVE REGIONAL R&I HUBS

COUPLED WITH EXPERT MARKETING HUBS

21 // June 19th 2014

Pro-Xylane

2/ MAXIMISE OUR SCIENTIFIC BREAKTHROUGHS

2006

2013

22 // June 19th 2014

2/ LOCAL INNOVATIONS THAT TURN INTO WORLDWIDE BLOCKBUSTERS

23 // June 19th 2014

2/ SPOT, IMPROVE AND AMPLIFY EMERGING IDEAS

Blur Oil BB Cream

24 // June 19th 2014

3/ BRANDS TO CAPTURE NEW CATEGORIES OPPORTUNITIES

25 // June 19th 2014 25 // June 19th 2014

3/ BRANDS TO STRENGTHEN OUR LOCAL / REGIONAL POSITIONS

26 // June 19th 2014

4/ STRATEGIC POSITIONS IN BRIMC COUNTRIES*

No1

MEXICO

BRAZIL

No4

No2

CHINA

INDIA

No3

No1

RUSSIA

*Internal estimates 2013

27 // June 19th 2014

No1

NORTH AMERICA

14.3%

No4

LATIN AMERICA

8.5%

No1

WESTERN EUROPE

19.3%

No1

EASTERN EUROPE

11.8% No8

JAPAN

2.2% No2

AFRICA MIDDLE EAST**

10.2% (in the countries where

L’Oréal is present)

No2

ASIA PACIFIC

10.5% (excl. Japan)

4/ A LEADER WITH HIGH POTENTIAL

L’OREAL MARKET SHARE BY GEOGRAPHIC ZONE 2013*

12.2%

16.9%

8.6%

L’ORÉAL “WORLD”:

“MATURE MARKETS”:

“NEW MARKETS”: * Excluding soaps, razors and toothpastes L’Oréal Estimates BMS ** Perimeter: countries where L’Oréal is present 28 // June 19th 2014

NORTH AMERICA

AFRICA MIDDLE EAST

WESTERN EUROPE

EASTERN EUROPE

SOUTH ASIA PACIFIC

4/ NEW ORGANIZATION 8 STRATEGIC REGIONS

BRAZIL

HISPANIC LATAM

NORTH ASIA

29 // June 19th 2014

5/ DIGITAL REVOLUTION A HISTORIC OPPORTUNITY FOR BEAUTY

RICH CONSUMER DIALOGUE PERSONALIZED SERVICES CONNECTED BEAUTY

E-COMMERCE

+20%*

SALES

DIGITAL MEDIA

12% OF OUR NET MEDIA EXPENSES

*2013

30 // June 19th 2014

31 // June 19th 2014

THE ULTIMATE VIRTUAL BEAUTY ADVISOR

5/ INVENTING A NEW ERA OF DIGITALLY-ENRICHED SERVICES

NEW CONSUMER EXPERIENCES THROUGH VIRTUAL REALITY

SUSTAINABLE INNOVATION 100% of products will have an environmental or social benefit.

SUSTAINABLE PRODUCTION Environmental footprint:

-60% vs. 2005

SUSTAINABLE CONSUMPTION Empowering L’Oréal consumer to make sustainable consumption choices

SUPPLIERS 100% of our strategic suppliers on our suppliers sustainability programme

COMMUNITIES More than 100,000 people from underprivileged communities, will have access to work.

EMPLOYEES Share & Care: By 2020, health care, social protection and training for all.

32 // June 19th 2014

6/ NEW SUSTAINABILITY COMMITMENTS

7/ STRATEGIC TRANSACTION ANNOUNCED FEBRUARY 11th, 2014

Nestlé

23.29%

Others

Bettencourt Meyers family

Treasury shares

* % of share capital based on a total number of shares of 605,901,887 as of 31/12/2013 ** % of share capital based on a total number of shares of 606,059,384 as of 31/01/2014 - after cancellation of the repurchased shares

New shareholding structure** Buy-back of €6.0Bn L’Oréal shares owned by Nestlé

48.5 million shares

8.0% of L’Oréal’s share capital

124.48€/share

(30.64%*)

(29.44%*)

33.31%

(1.01%*)

1.27%

(38.91%*)

42.13%

BUYBACK Cancellation of the shares EPS enhancement impact: +5% full year est.

33 // June 19th 2014

CONFIDENCE

FOR THE

FUTURE

III

34 // June 19th 2014

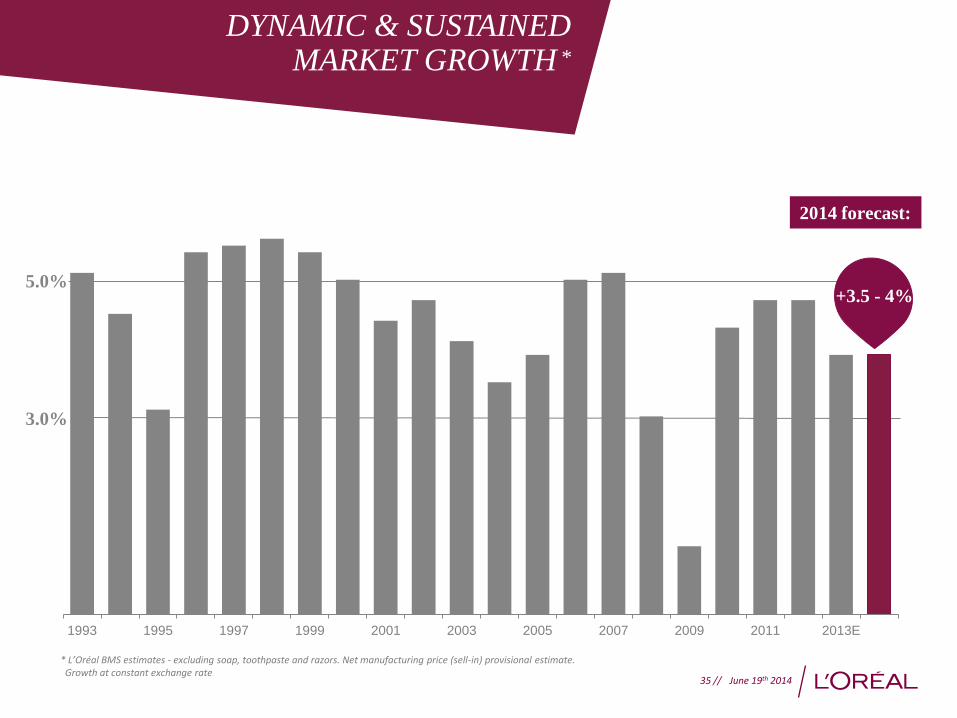

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013E

5.0%

3.0%

+3.5 - 4%

2014 forecast:

* L’Oréal BMS estimates - excluding soap, toothpaste and razors. Net manufacturing price (sell-in) provisional estimate. Growth at constant exchange rate

35 // June 19th 2014

DYNAMIC & SUSTAINED MARKET GROWTH *

L’ORÉAL IS STEADILY OUTPERFORMING THE MARKET

*excluding soaps, razors and toothpastes. 2013 provisional estimates

Source: L’Oréal estimates. Excluding exchange rate impact

+5.6%

+4.2%

2010

+5.0%

+4.6%

+5.5%

+4.6%

MARKET

+5.2%

+3.8%

2011 2012 2013

COSMETICS MARKET GROWTH* AND L’ORÉAL LIKE-FOR-LIKE

COSMETICS SALES GROWTH

36 // June 19th 2014

Like-for-like % change

2013 Q1 2014

Professional Products +2.1% +3.7%

Consumer Products +4.9% +1.2%

L'Oréal Luxe +6.8% +7.2%

Active Cosmetics +7.8% +8.7%

Cosmetics Divisions +5.2% +3.7%

The Body Shop +1.2% -3.4%

Consolidated Total +5.1% +3.5%

* From January 1st 2014, Galderma and Inneov, both 50% owned subsidiaries, will be consolidated under the equity method, in application of IFRS 11.

Like-for-like % change

2013 Q1 2014

Western Europe +1.9% +2.8%

North America +3.8% -0.6%

New Markets +9.4% +7.5%

of which:

- Asia, Pacific +8.4% +6.8%

- Latin America +11.5% +8.2%

- Eastern Europe** +8.2% +6.3%

- Africa, Middle East** +14.3% +14.9%

Cosmetics Divisions +5.2% +3.7%

** As of July 1st, 2013, Turkey and Israel, which were previously included in the Africa, Middle East zone, were transferred to the Eastern Europe zone. All figures for earlier periods have been restated to allow for this change.

AN ENCOURAGING & CONTRASTED FIRST QUARTER

BY DIVISION* BY REGION*

37 // June 19th 2014

38 // June 19th 2014

POWERFUL INNOVATION

HEALTHY MARKET GROWTH

ENHANCED WORLDWIDE LEADERSHIP

MARKET SHARE GAIN OPPORTUNITIES

REGULAR PROFIT INCREASE

DYNAMIC DIVIDEND POLICY

SOLID PROSPECTS

39 // June 19th 2014

-------------------------Avertissement / Disclaimer ------------------------- « Ce document ne constitue pas une offre de vente ou la sollicitation d’une offre d’achat de titres L’Oréal. Si vous souhaitez obtenir des informations plus complètes concernant L’Oréal,

nous vous invitons à vous reporter aux documents publics déposés en France auprès de l’Autorité des Marchés Financiers (également disponibles en version anglaise sur notre site Internet

www.loreal-finance.com).Ce document peut contenir certaines déclarations de nature prévisionnelle. Bien que la Société estime que ces déclarations reposent sur des hypothèses

raisonnables à la date de publication du présent communiqué, elles sont par nature soumises à des risques et incertitudes pouvant donner lieu à un écart entre les chiffres réels et ceux

indiqués ou induits dans ces déclarations.»

"This document does not constitute an offer to sell, or a solicitation of an offer to buy, L’Oréal shares. If you wish to obtain more comprehensive information about L’Oréal, please refer to the

public documents registered in France with the Autorité des Marchés Financiers (which are also available in English on our Internet site: www.loreal-finance.com).This document may contain

some forward-looking statements. Although the Company considers that these statements are based on reasonable hypotheses at the date of publication of this release, they are by their

nature subject to risks and uncertainties which could cause actual results to differ materially from those indicated or projected in these statements."

Françoise Lauvin

Head of Investor Relations

Tel. : + 33 1 47 56 86 82

Fax : + 33 1 47 56 74 93

email : [email protected]

Sophie Gasperment

Group General Manager, Financial Communication

Strategic Prospective

Tel. : + 33 1 47 56 86 22

Fax : + 33 1 47 56 74 93

email : [email protected]