design report compilation

TRANSCRIPT

The Wine Mood

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

Millenials

54% of millennials openedtheir own business(or want to)

They link passionwith work.

Professional commitment comes from engaging experiences.

work is present all the time .

They create their own hours so

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

They need a

Break

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

PRESENTS

the wine mood

by

The Wine Mood

Break time doesn’t have be boring.Put yourself and your teammates

in The Wine Mood.

Enjoy this new experience at your workplace in Milano.

Enjoy your break

With qualitywine

Easy to orderapp

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

The App

The Wine Mood

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

Click here to see how the app works

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

The Box

In partnership with

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

Everytime a friend signs up with your invite code, they’ll get their first box free (up to €20). Once they’ve tried The Wine Mood, you’ll also received a free box (up to €20) which will be applied to your account automatically.

Share the Mood

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

Share the MoodNotification after the delivery to share the mood in social media using #thewinemood

The Wine Mood

How?

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

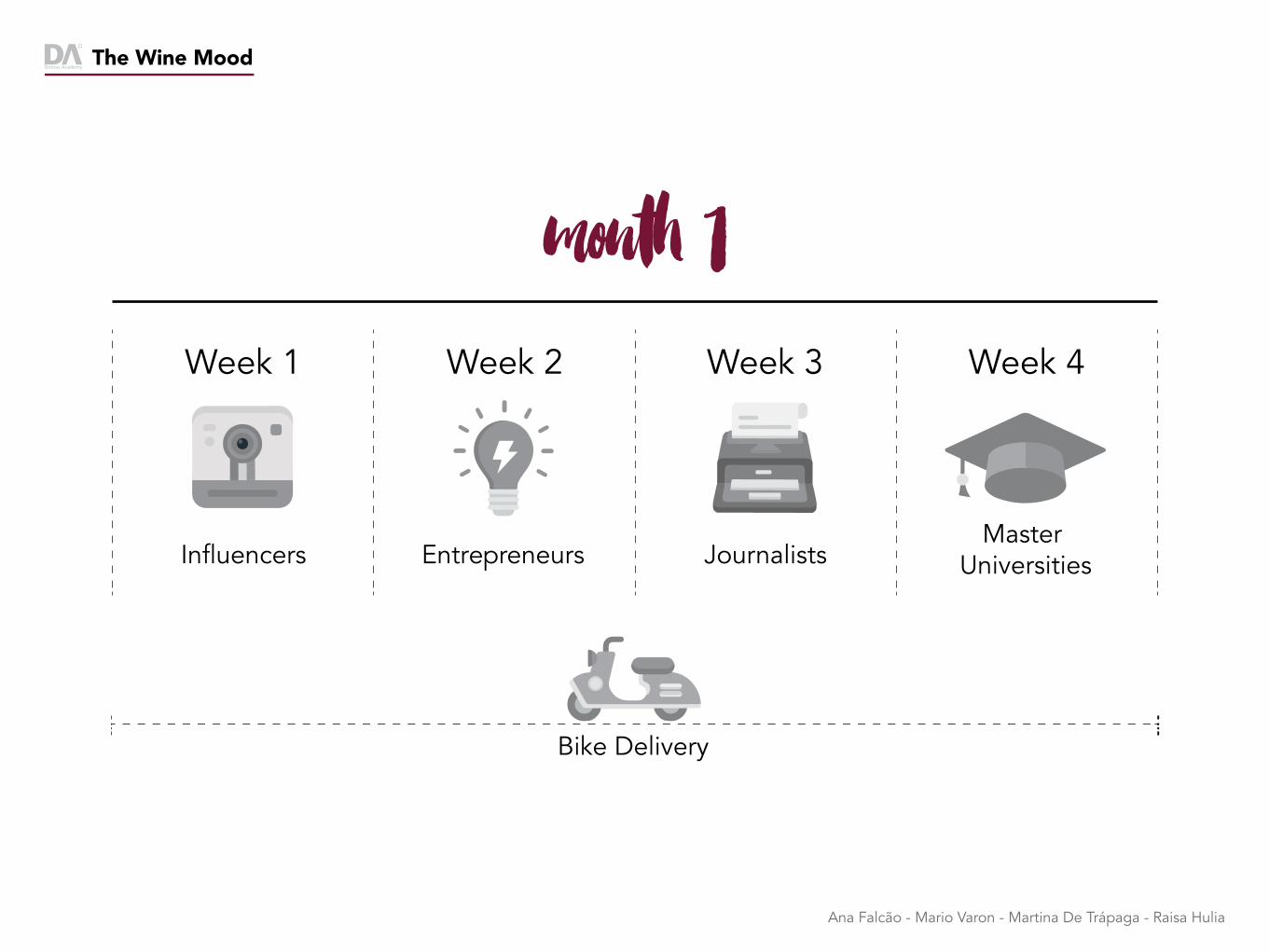

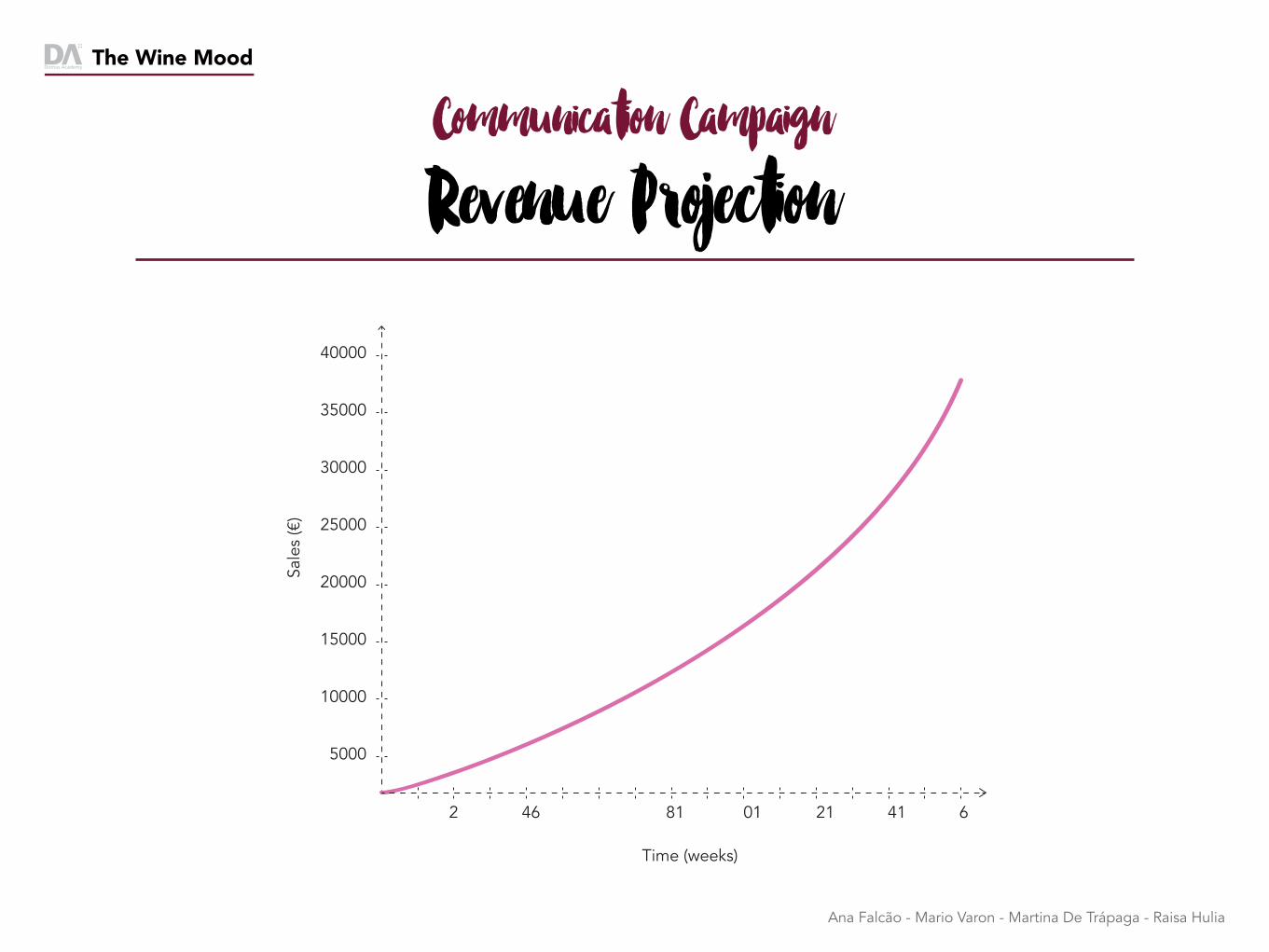

Communication Campaign

4 monthsEvery week 50 boxes will be delivered

for free to different relevant communities.

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

month 1Week 1

Influencers

Bike Delivery

Week 3

Journalists

Week 4

Master Universities

Week 2

Entrepreneurs

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

month 2 month 3month 1 month 4

Total amount:

800 free boxes

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

expected reach

2.099.200

Influencers

800.000 1.280.00016.000 3.200

Journalists Master Universities

Entrepreneurs

TOTAL:

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

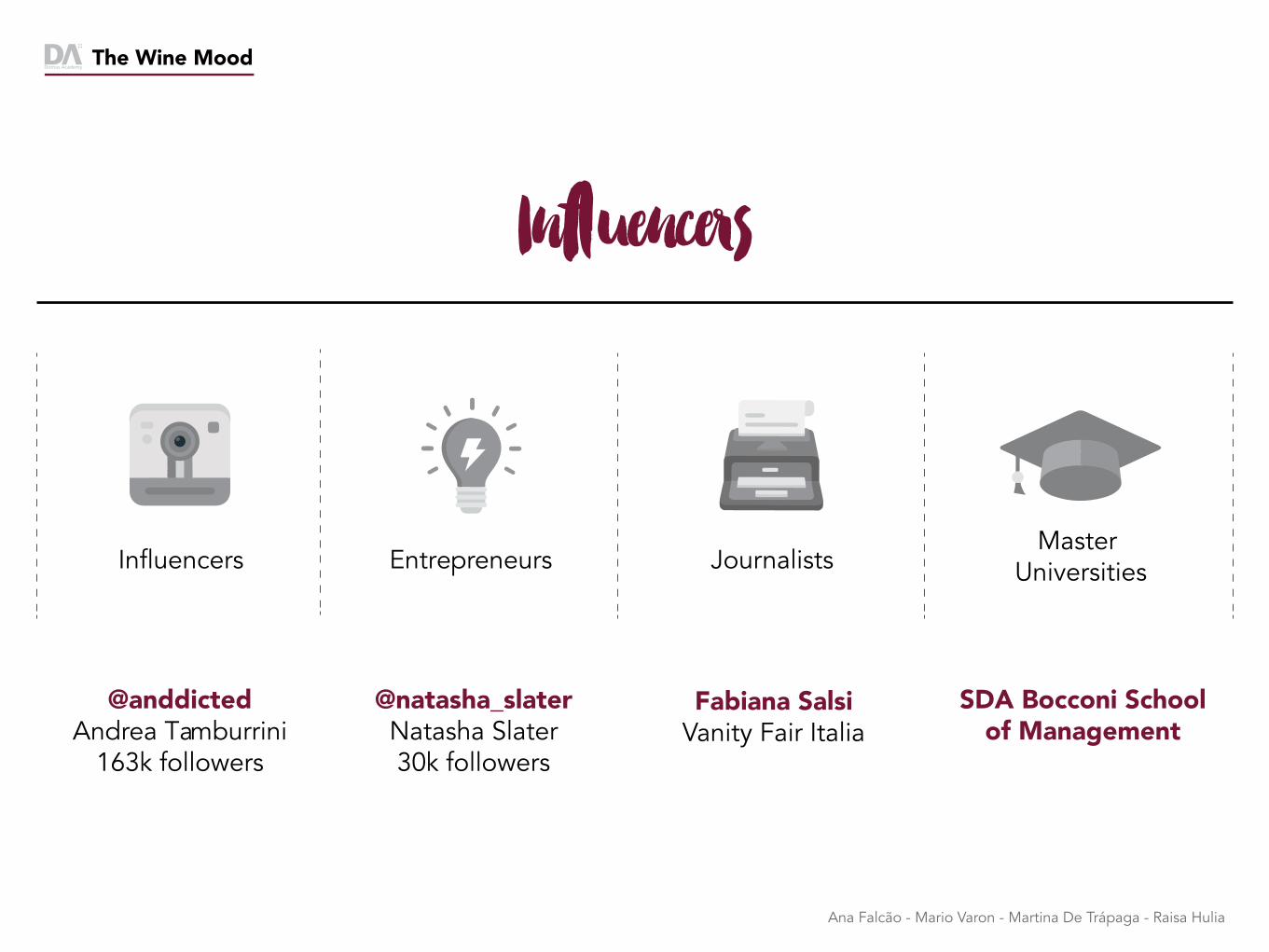

Influencers

Influencers JournalistsMaster

UniversitiesEntrepreneurs

@anddictedAndrea Tamburrini

163k followers

@natasha_slaterNatasha Slater30k followers

SDA Bocconi Schoolof Management

Fabiana SalsiVanity Fair Italia

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

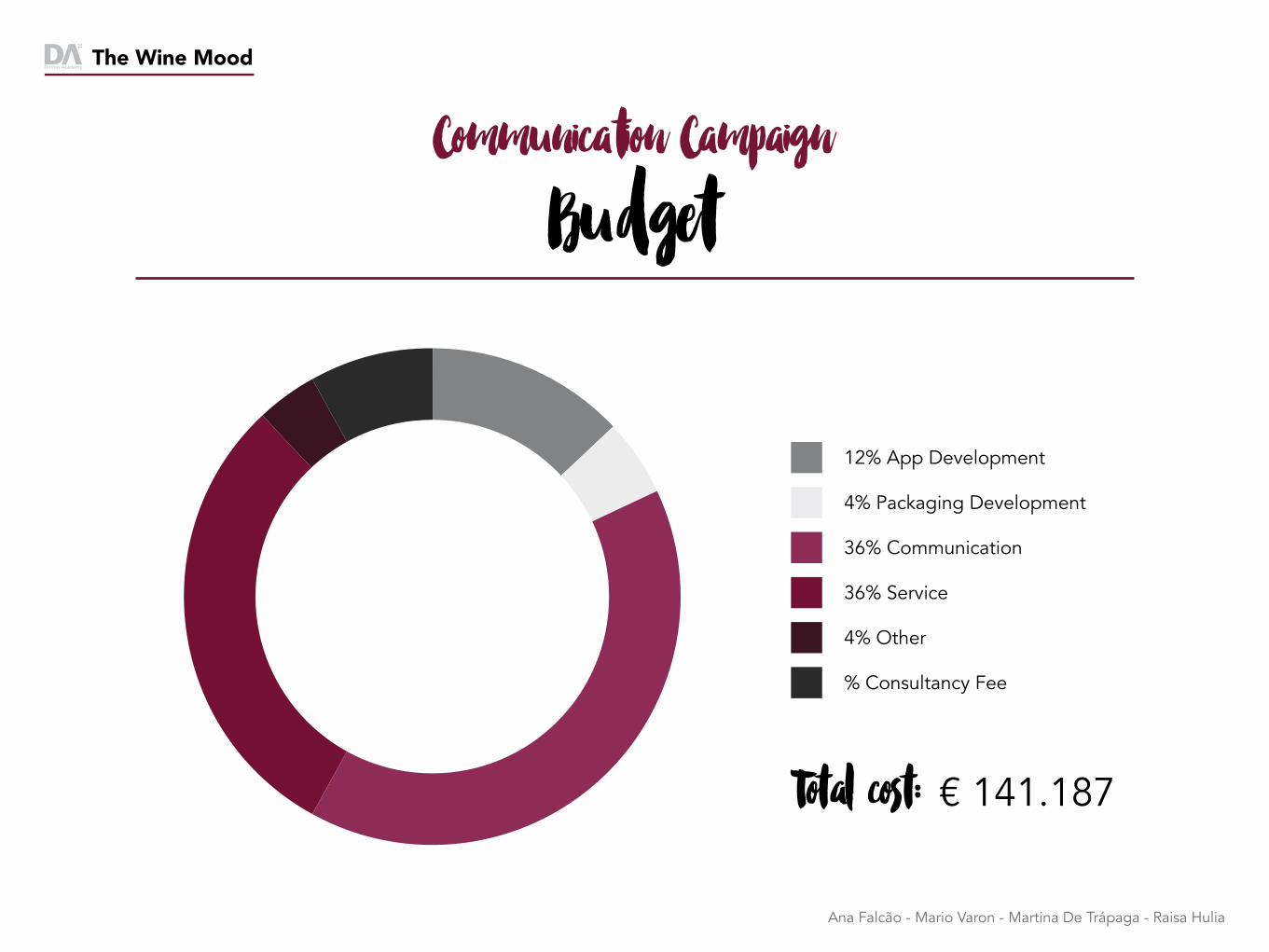

Budget

12% App Development

4% Packaging Development

36% Communication

36% Service

4% Other

% Consultancy Fee

Communication Campaign

Total cost: € 141.187

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

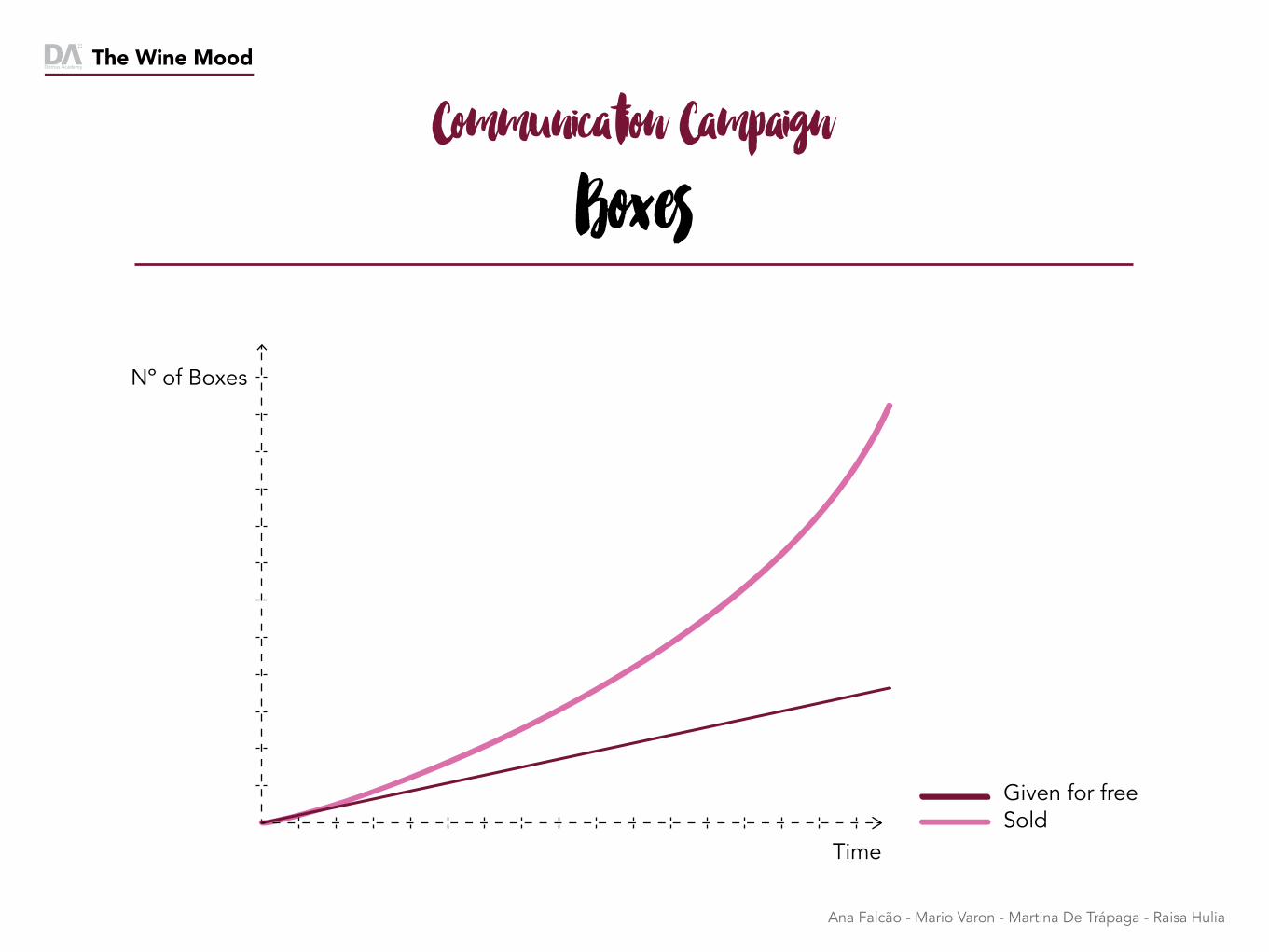

Nº of Boxes

Time

Given for freeSold

BoxesCommunication Campaign

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

Revenue ProjectionCommunication Campaign

Sale

s (€

)

Time (weeks)

2

5000

10000

15000

20000

25000

30000

35000

40000

46 81 01 21 41 6

Ana Falcão - Mario Varon - Martina De Trápaga - Raisa Hulia

The Wine Mood

The Team

Ana Falcão Mario Varon Martina De Trápaga Raisa Hulia

Thank You

AQUOLINA - VIVI NATURABRANDING THROUGH DESIGN

How can we widen the profit margin of Vivi Natura?

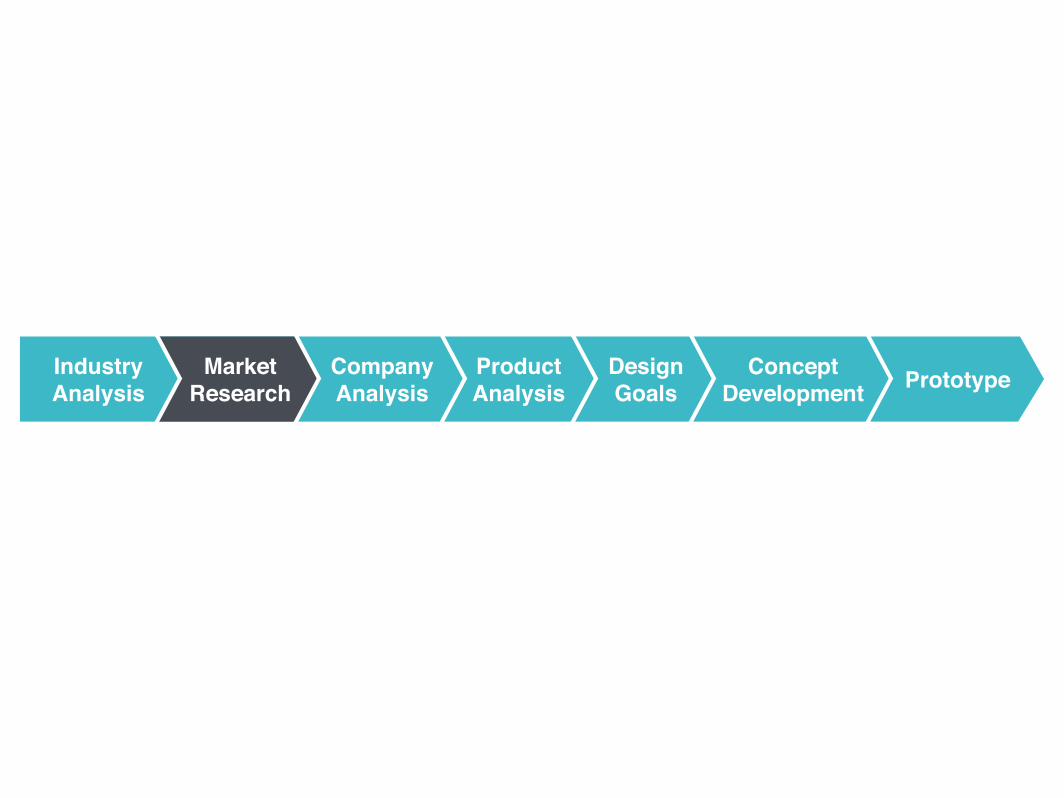

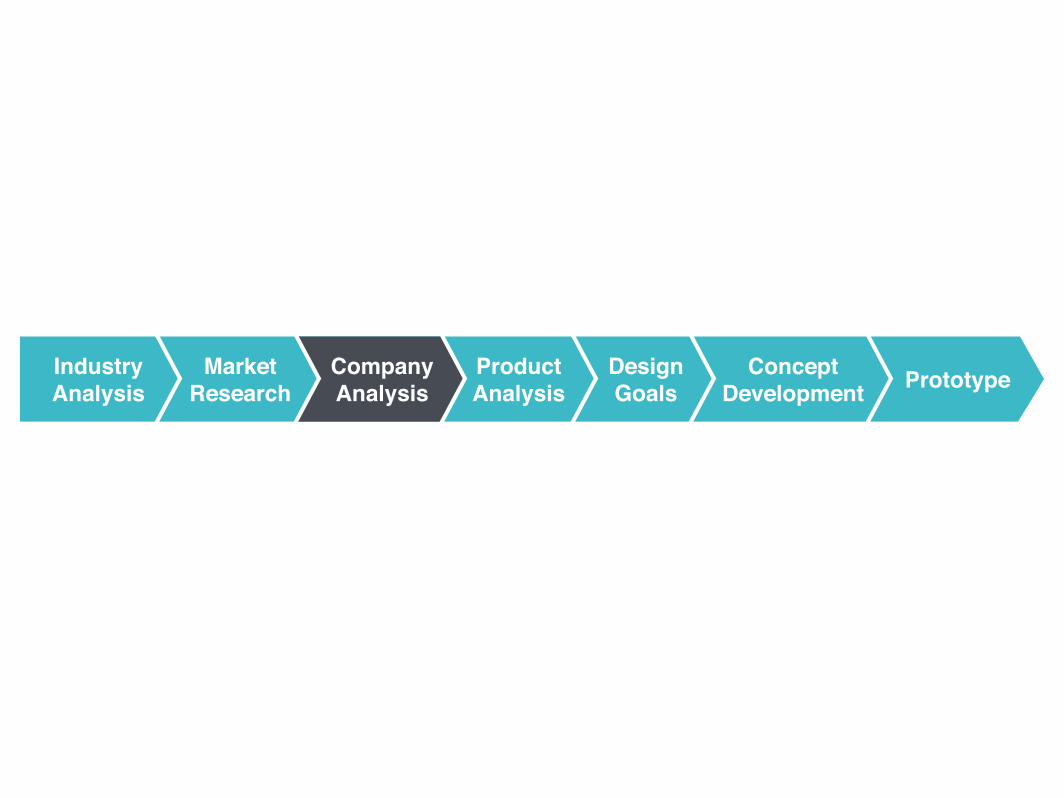

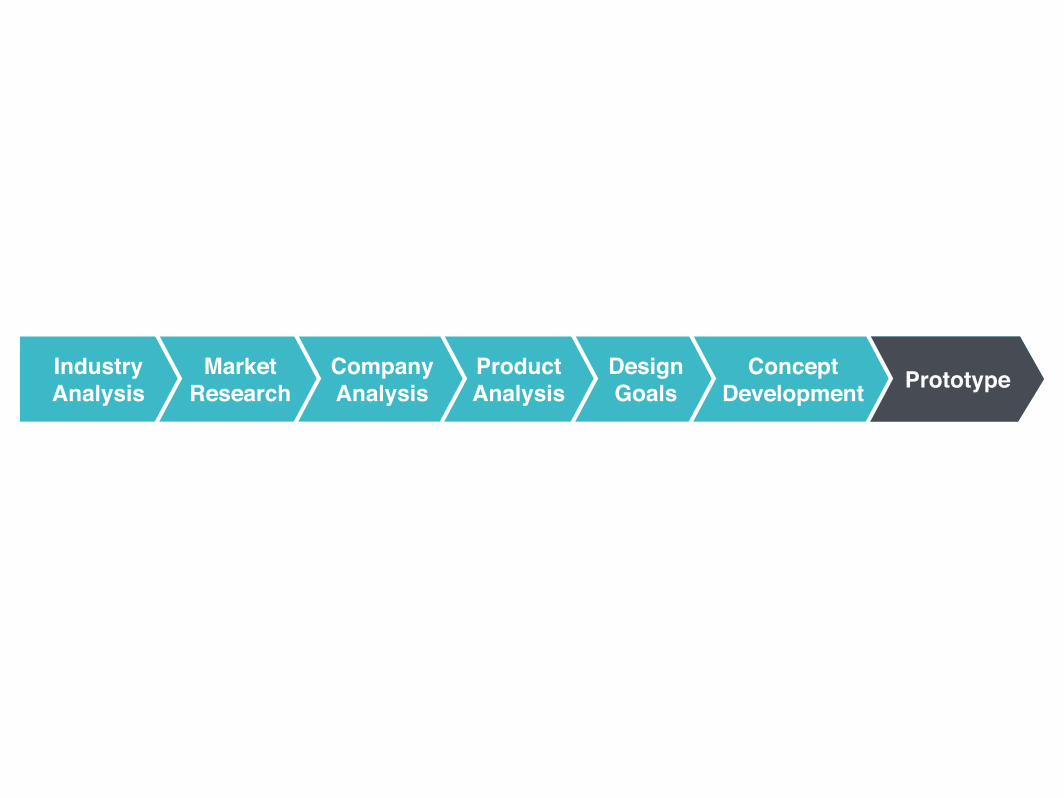

Company Analysis

Product Analysis

Design Goals

ConceptDevelopment PrototypeIndustry

AnalysisMarket

Research

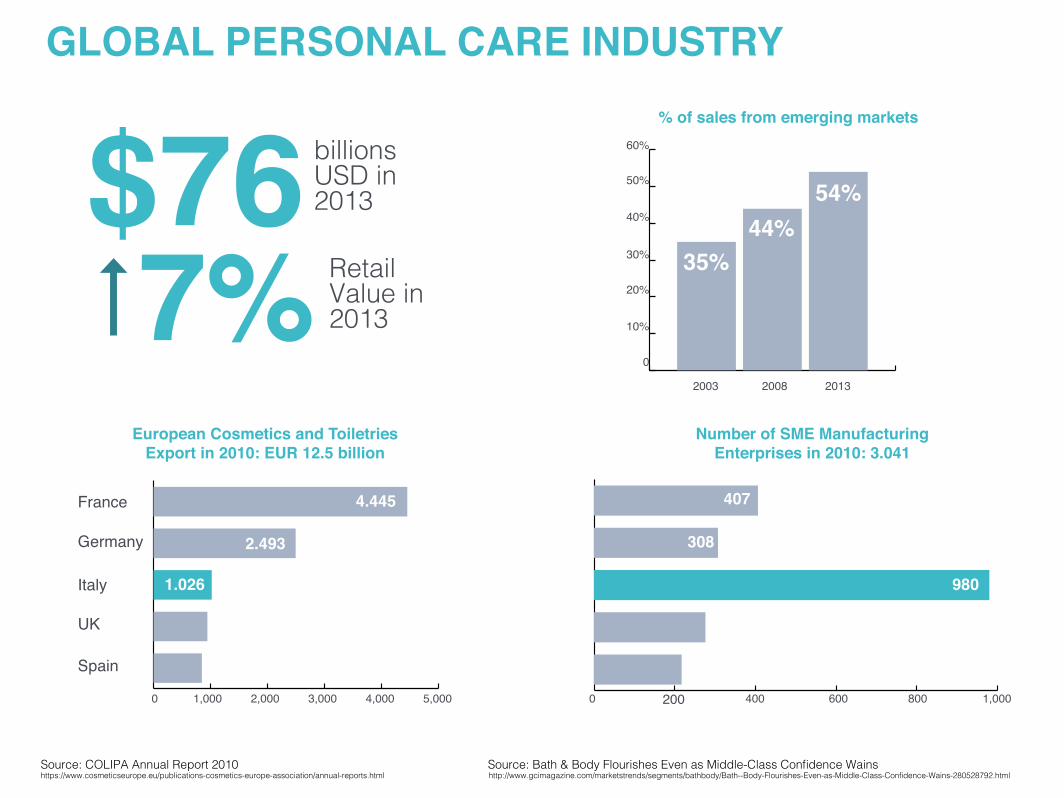

PERSONAL CARE INDUSTRY

% of sales from emerging markets

2003 2008 2013

0

10%

20%

30%

40%

50%

60%

35%44%

54%

European Cosmetics and ToiletriesExport in 2010: EUR 12.5 billion

1,0000 2,000 3,000 4,000 5,000

4.445

2.493

1.026

Germany

France

UK

Spain

Italy

GLOBAL PERSONAL CARE INDUSTRY

Source: COLIPA Annual Report 2010 Source: Bath & Body Flourishes Even as Middle-Class Confidence Wainshttps://www.cosmeticseurope.eu/publications-cosmetics-europe-association/annual-reports.html http://www.gcimagazine.com/marketstrends/segments/bathbody/Bath--Body-Flourishes-Even-as-Middle-Class-Confidence-Wains-280528792.html

1,0008006004002000

980

407

308

Number of SME Manufacturing Enterprises in 2010: 3.041

billions USD in 2013

Retail Value in 2013

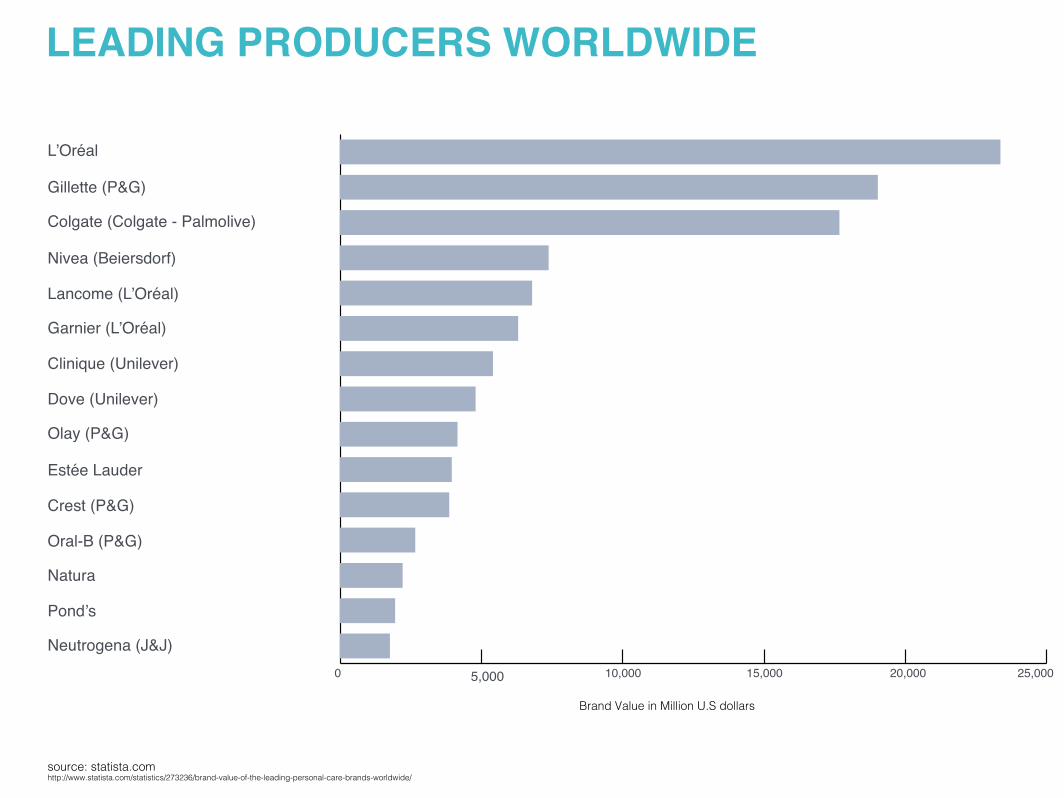

LEADING PRODUCERS WORLDWIDE

L’Oréal

Gillette (P&G)

Colgate (Colgate - Palmolive)

Nivea (Beiersdorf)

Lancome (L’Oréal)

Garnier (L’Oréal)

Clinique (Unilever)

Dove (Unilever)

Olay (P&G)

Estée Lauder

Crest (P&G)

Oral-B (P&G)

Natura

Pond’s

Neutrogena (J&J)

5,0000 10,000 15,000 20,000 25,000

Brand Value in Million U.S dollars

source: statista.comhttp://www.statista.com/statistics/273236/brand-value-of-the-leading-personal-care-brands-worldwide/

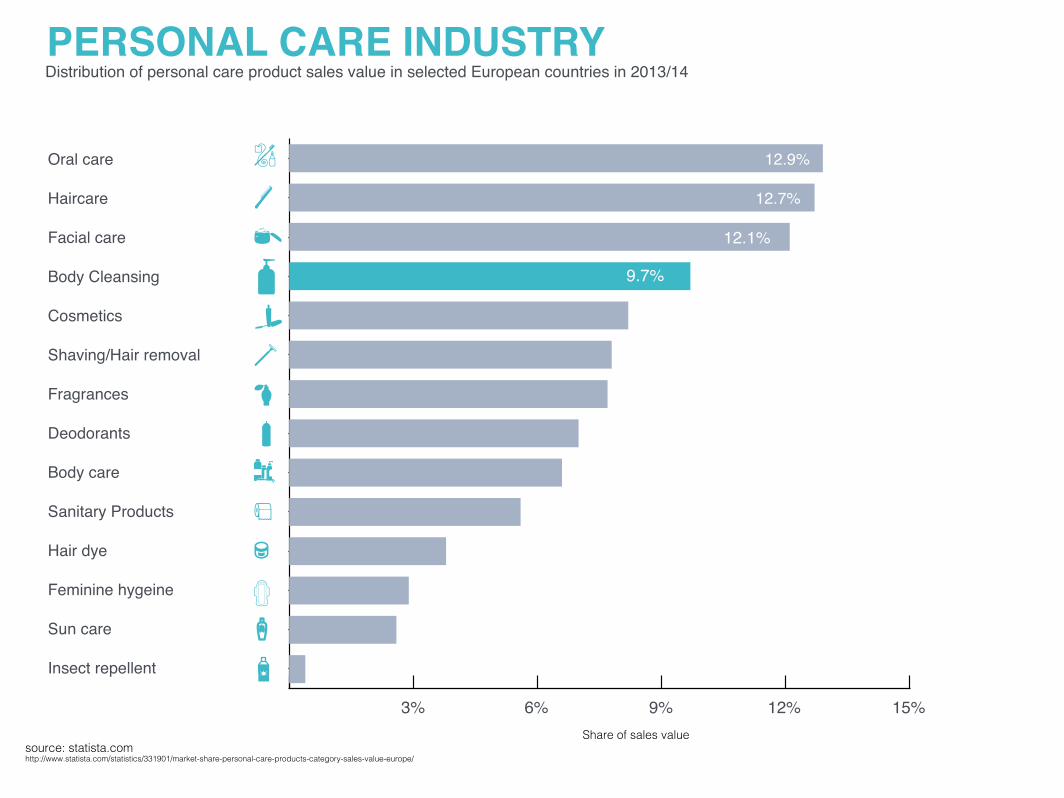

source: statista.comhttp://www.statista.com/statistics/331901/market-share-personal-care-products-category-sales-value-europe/

Distribution of personal care product sales value in selected European countries in 2013/14

Oral care

Haircare

Facial care

Body Cleansing

Cosmetics

Shaving/Hair removal

Fragrances

Deodorants

Body care

Sanitary Products

Hair dye

Feminine hygeine

Sun care

Insect repellent

Share of sales value

3% 6% 9% 12% 15%

12.9%

12.7%

12.1%

9.7%

PERSONAL CARE INDUSTRY

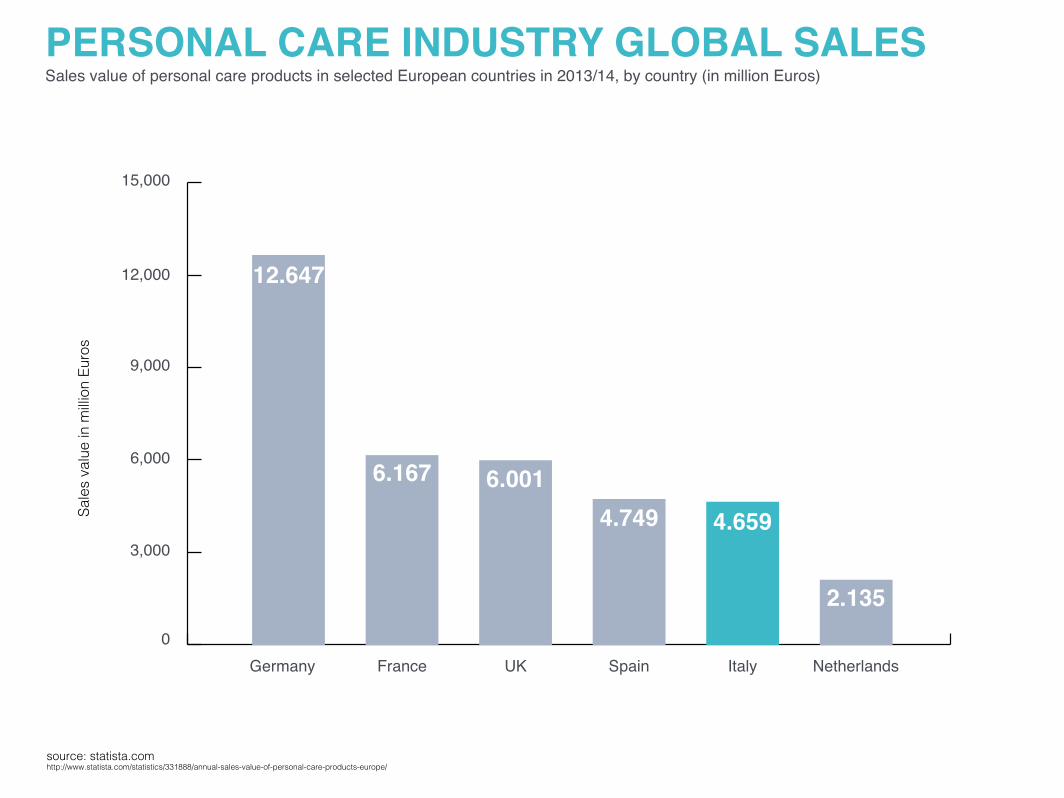

PERSONAL CARE INDUSTRY GLOBAL SALESSales value of personal care products in selected European countries in 2013/14, by country (in million Euros)

15,000

12,000

9,000

3,000

Germany France UK Spain Italy Netherlands

6,000

0

Sale

s va

lue in

mill

ion E

uro

s

source: statista.comhttp://www.statista.com/statistics/331888/annual-sales-value-of-personal-care-products-europe/

12.647

6.167 6.0014.749 4.659

2.135

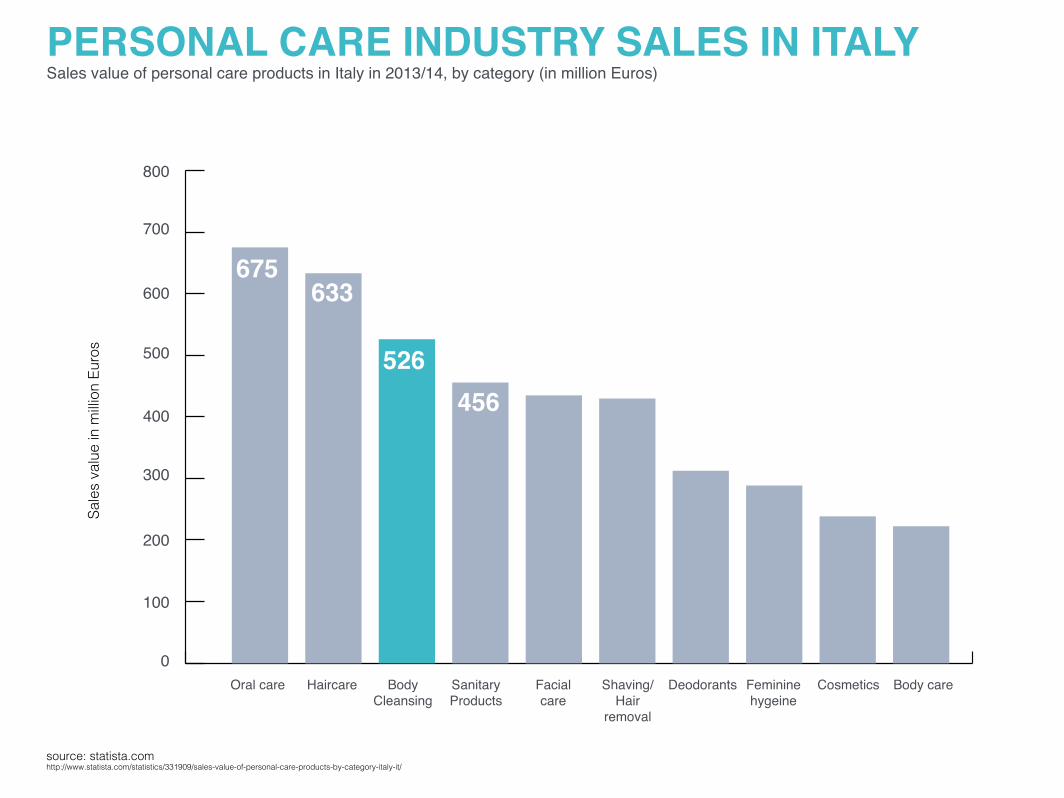

PERSONAL CARE INDUSTRY SALES IN ITALYSales value of personal care products in Italy in 2013/14, by category (in million Euros)

800

700

600

500

400

300

200

100

0Oral care Haircare Body

CleansingSanitaryProducts

Facialcare

Shaving/Hair

removal

Deodorants Femininehygeine

Cosmetics Body care

Sale

s va

lue in

mill

ion E

uro

s

source: statista.comhttp://www.statista.com/statistics/331909/sales-value-of-personal-care-products-by-category-italy-it/

675633

526456

PERSONAL CARE INDUSTRY TRENDS

Natural and Organic products

Multisensorial and Multifunctional

Male Pampering Culture

1 http://www.cosmeticsandtoiletries.com/formulating/category/natural/Demand-for-Organic-Beauty-to-Grow-to-Over-13-Billion-by-2018-Report-Says-213160491.html2 http://www.gcimagazine.com/marketstrends/segments/bathbody/More-Than-a-Feeling-Multisensory-in-Bath-Body-280531752.html3 http://www.gcimagazine.com/marketstrends/segments/bathbody/Bath--Body-Hunts-for-New-Consumers-233364561.html

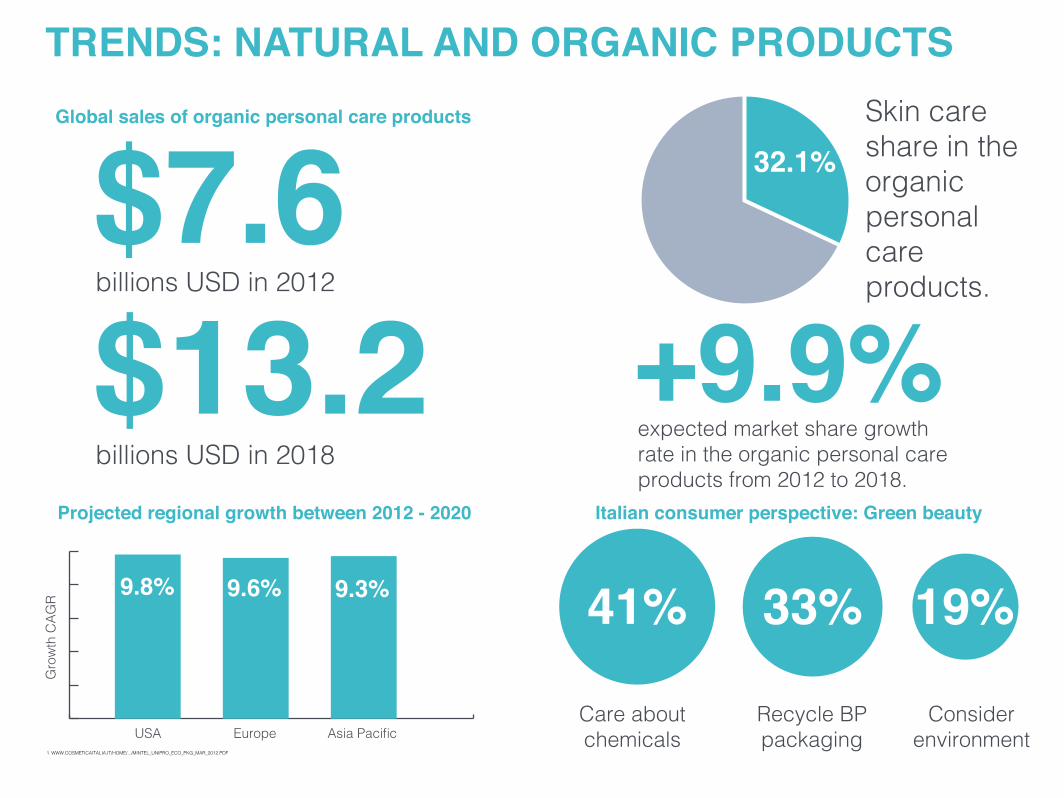

billions USD in 2012

billions USD in 2018

Skin care share in the organic personal care products.

expected market share growth rate in the organic personal care products from 2012 to 2018.

Global sales of organic personal care products

Projected regional growth between 2012 - 2020 Italian consumer perspective: Green beauty

9.8% 9.6% 9.3%

USA Europe Asia Pacific

Gro

wth

CA

GR

Recycle BP packaging

Care about chemicals

Consider environment

TRENDS: NATURAL AND ORGANIC PRODUCTS

1 WWW.COSMETICAITALIA.IT/HOME/.../MINTEL_UNIPRO_ECO_PkG_MAR_2012.PDF

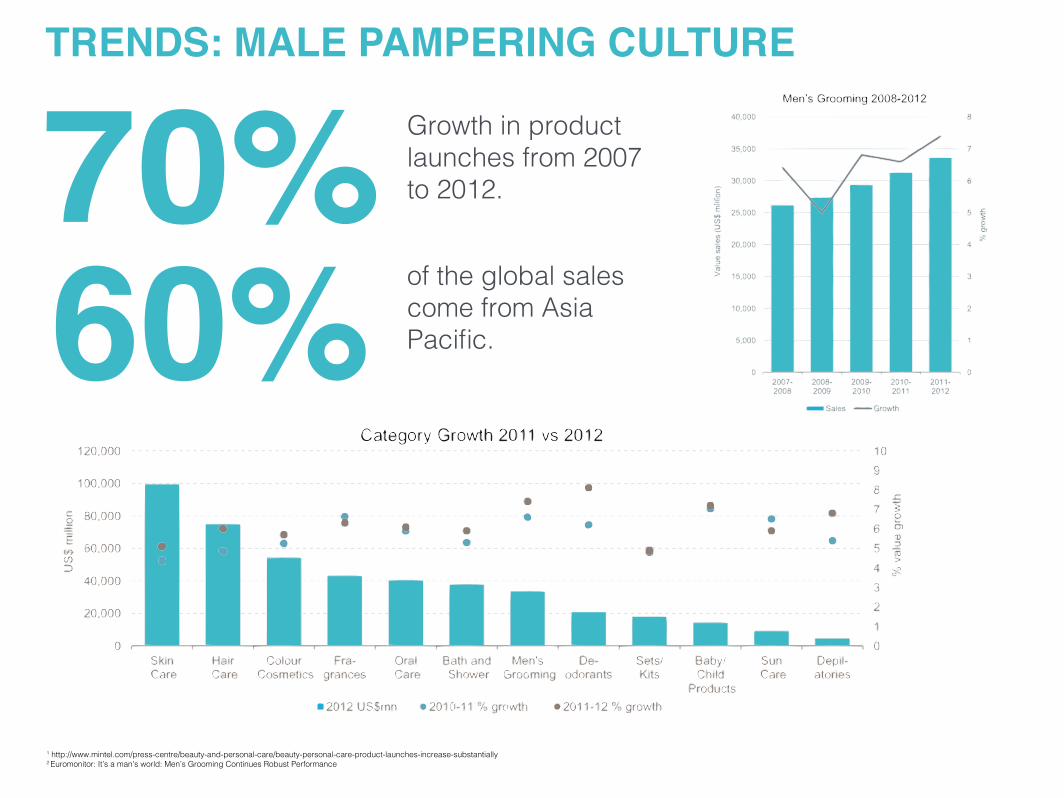

Growth in product launches from 2007 to 2012.

of the global sales come from Asia Pacific.

TRENDS: MALE PAMPERING CULTURE

1 http://www.mintel.com/press-centre/beauty-and-personal-care/beauty-personal-care-product-launches-increase-substantially2 Euromonitor: It’s a man’s world: Men’s Grooming Continues Robust Performance

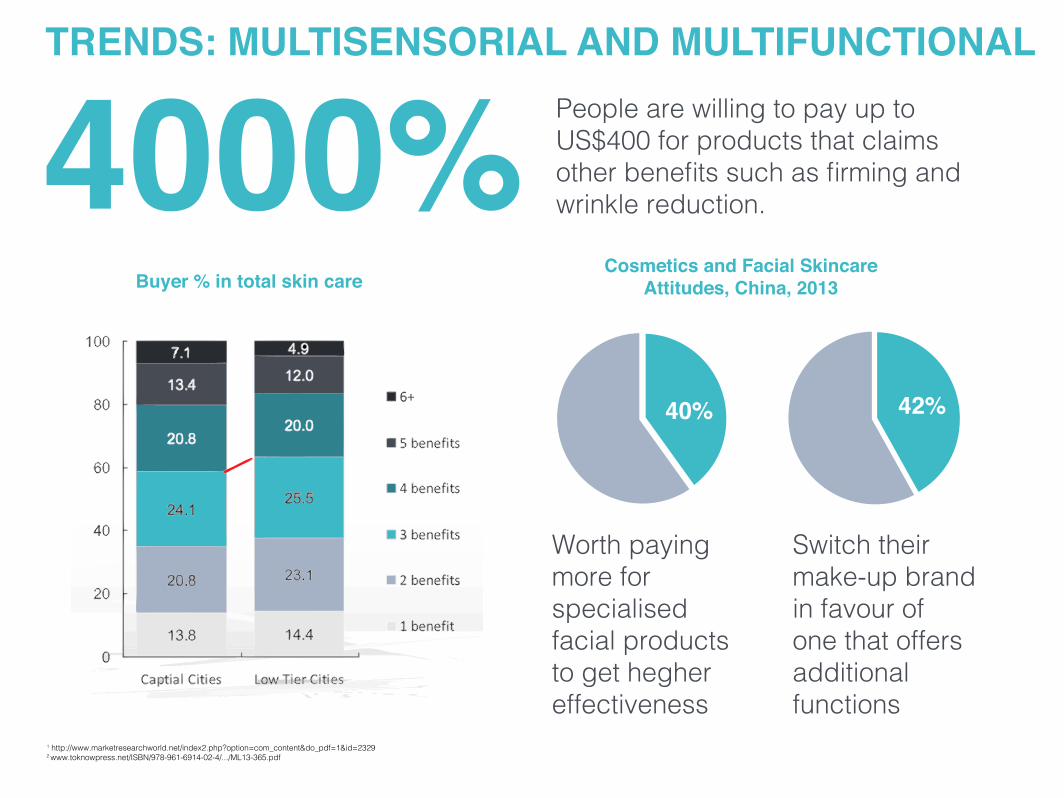

42%40%

People are willing to pay up to US$400 for products that claims other benefits such as firming and wrinkle reduction.

Worth paying more for specialised facial products to get hegher effectiveness

Switch their make-up brand in favour of one that offers additional functions

Cosmetics and Facial Skincare Attitudes, China, 2013Buyer % in total skin care

TRENDS: MULTISENSORIAL AND MULTIFUNCTIONAL

1 http://www.marketresearchworld.net/index2.php?option=com_content&do_pdf=1&id=23292 www.toknowpress.net/ISBN/978-961-6914-02-4/.../ML13-365.pdf

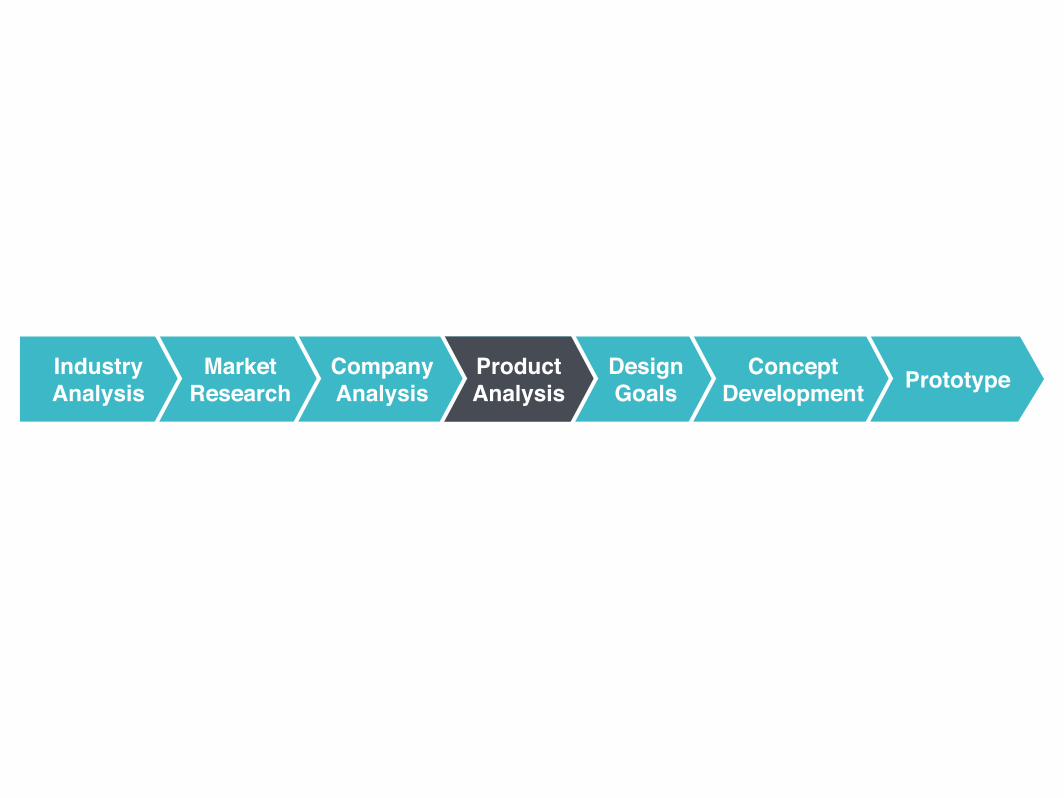

Company Analysis

Product Analysis

Design Goals

ConceptDevelopment PrototypeIndustry

AnalysisMarket

Research

CRITICAL SUCCESS FACTORS

Productinnovation

R&D Fragrances

Multifunctional andMultisensorial

ProductDevelopment

New Trends(organic/green)

Quality

Benefits to the skin

Appealing fragrances

Feeling of the product

Brand

Branding and Image

Brand loyalty

Multiple Touchpoints

Marketing strategies

Advertising

Sales and Promotion

Distribution

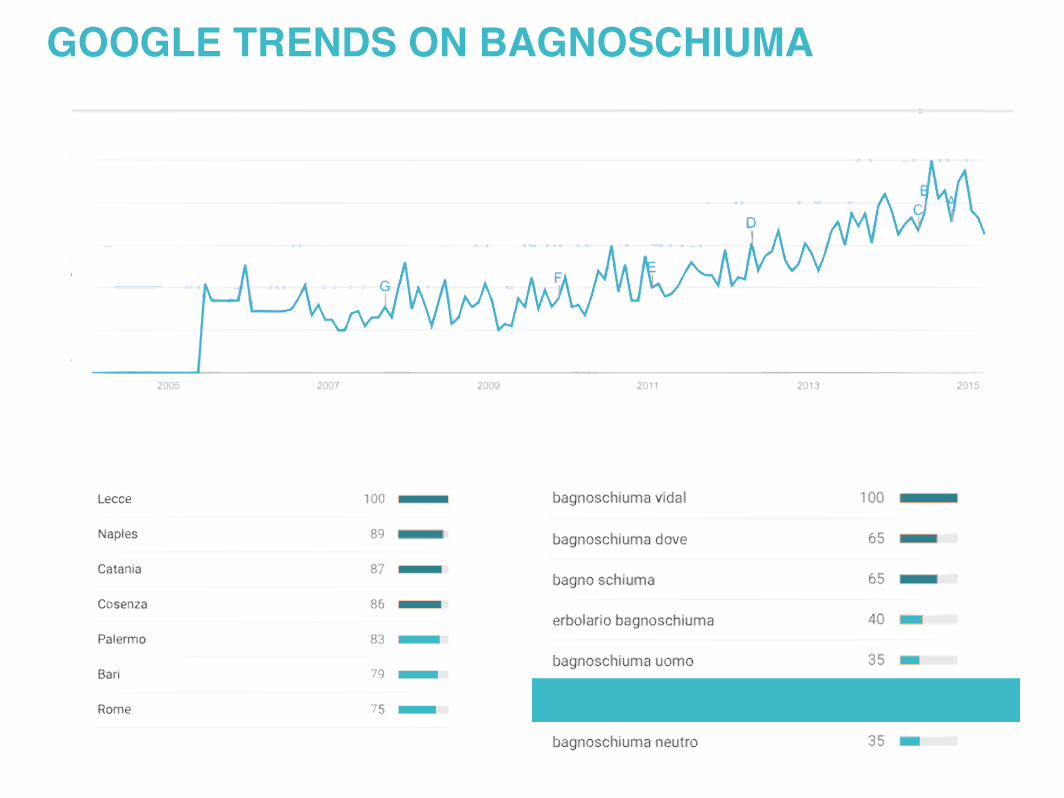

GOOGLE TRENDS ON SHOWER GEL

GOOGLE TRENDS ON BAGNOSCHIUMA

DAILy TIME SPENT ON APPEARANCE, By GENDER

Source: Euromonitor International consumer survey, Personal Appearance Survey 2014http://go.euromonitor.com/rs/euromonitorinternational/images/extract-global-consumer-survey-apparel-beauty-grooming.pdf?mkt_tok=3RkMMJWWfF9ws-Rogv6XIZkXonjHpfsX56eorWaS2h4kz2EFye%2BLIHETpodcMSMZgMk%2BTFAwTG5toziV8R7jFkc1r1d4QXBDr

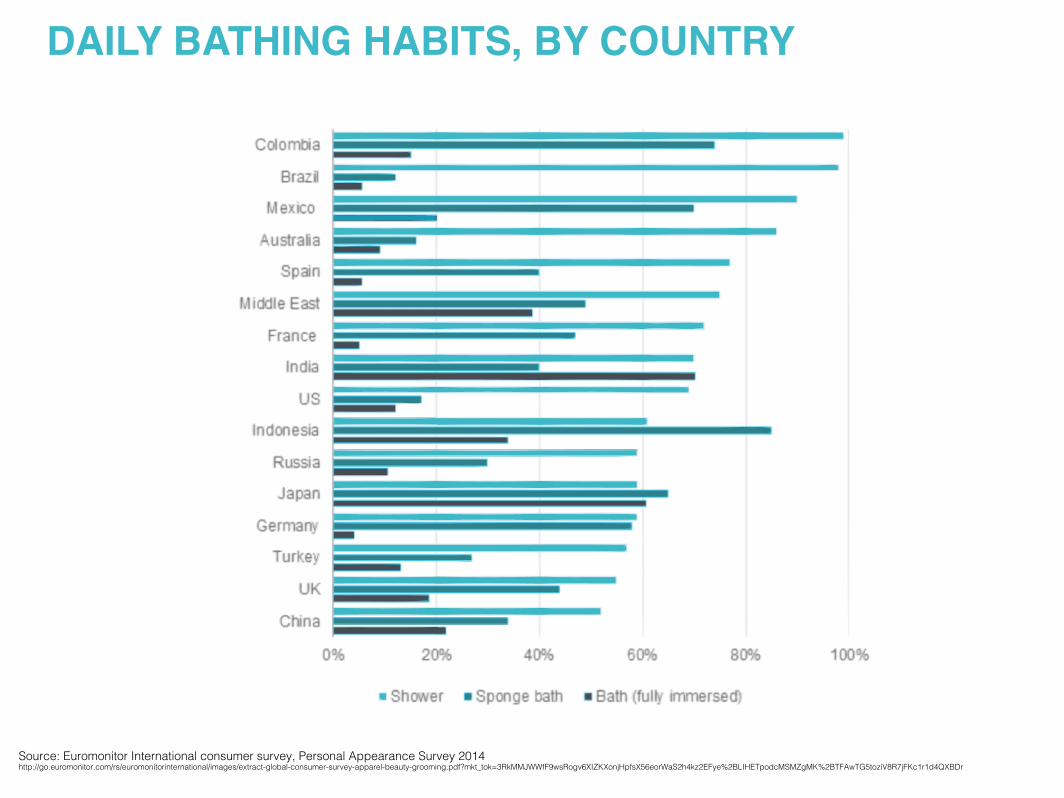

DAILy BATHING HABITS, By COUNTRy

Source: Euromonitor International consumer survey, Personal Appearance Survey 2014http://go.euromonitor.com/rs/euromonitorinternational/images/extract-global-consumer-survey-apparel-beauty-grooming.pdf?mkt_tok=3RkMMJWWfF9wsRogv6XIZkXonjHpfsX56eorWaS2h4kz2EFye%2BLIHETpodcMSMZgMk%2BTFAwTG5toziV8R7jFkc1r1d4QXBDr

ERecession

Made in ItalyGlobalization

Income reductionSharing economyService Economy

Younger purchase powerlow competitive Ability of Italy

Rise of emerging countriesPT

TaxesBureaucracyAgreementsEuropean UnionLegal Framework

Environmental LawItalian political instabilityInternational Trad

AppsDigital

ConnectivitySocial Media

Innovation CultureIncrease of internet sales

Multifunctionality and Multisensorial

SGifts GourmandCustomizationStressful daily lifeLuxury AspirationsOrganic movement

Fast trend generationResponsible consumerismPursuit of youth and beauty

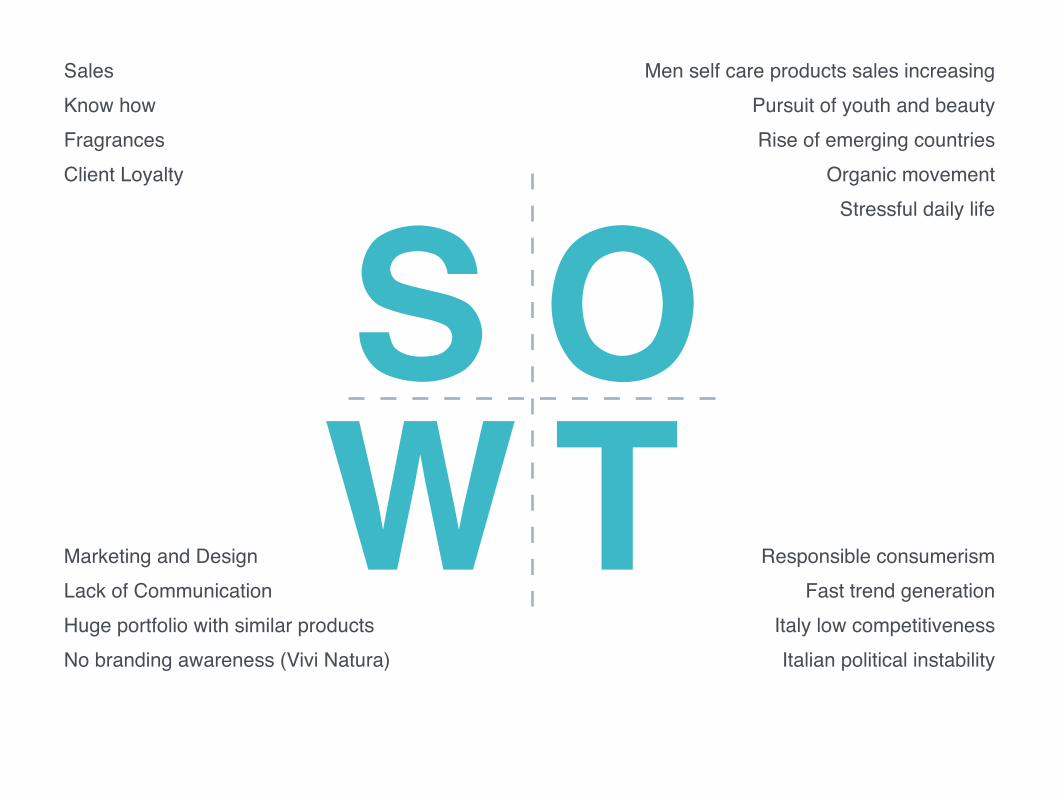

OMen self care products sales increasing

Pursuit of youth and beautyRise of emerging countries

Organic movement

Stressful daily life

ST

Sales Know howFragrancesClient Loyalty

Responsible consumerismFast trend generation

Italy low competitivenessItalian political instability

WMarketing and Design

Lack of Communication

Huge portfolio with similar productsNo branding awareness (Vivi Natura)

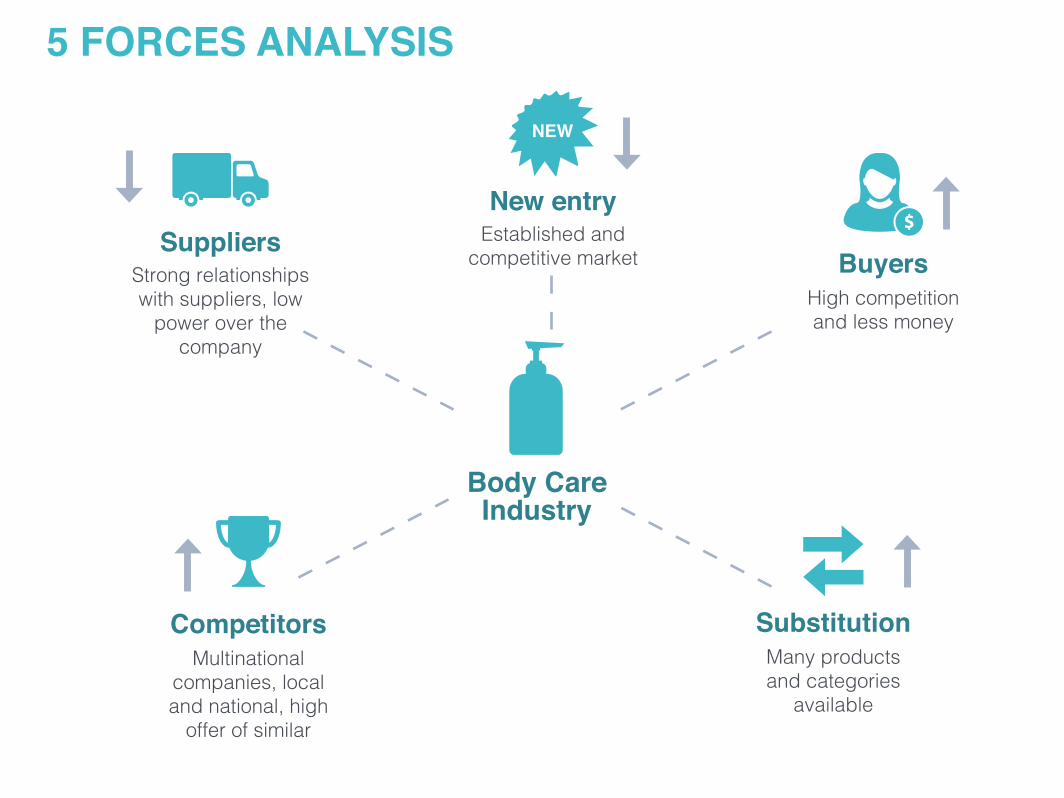

5 FORCES ANALySIS

Body CareIndustry

New entryEstablished and

competitive market BuyersHigh competition and less money

SuppliersStrong relationships with suppliers, low

power over the company

CompetitorsMultinational

companies, local and national, high

offer of similar

SubstitutionMany products and categories

available

Company Analysis

Product Analysis

Design Goals

ConceptDevelopment PrototypeIndustry

AnalysisMarket

Research

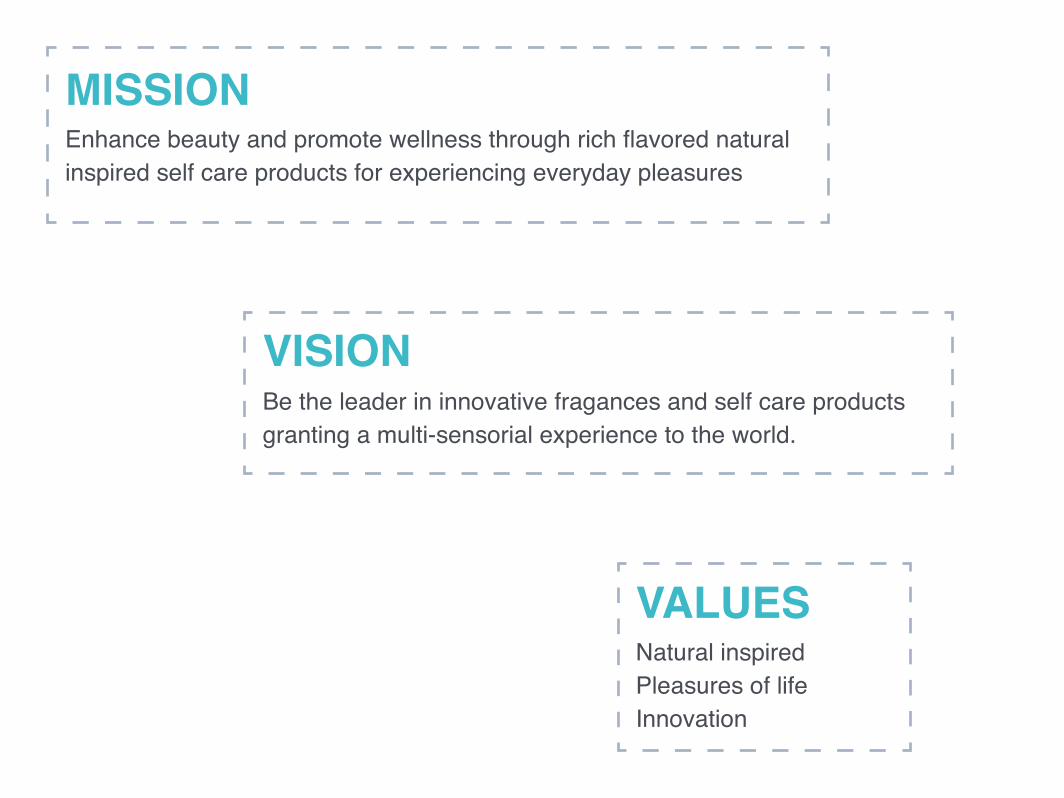

MISSIONEnhance beauty and promote wellness through rich flavored natural inspired self care products for experiencing everyday pleasures

Be the leader in innovative fragances and self care products granting a multi-sensorial experience to the world.

VISION

Natural inspiredPleasures of lifeInnovation

VALUES

BUSINESS MODEL CANVAS

• Fragrance development

• Raw material procurement

• Production

• Quality control

• Packaging

• Distribution

Key Partners

CostStructure

RevenueStreams

Key Activities

Key Resources

Channels

ValuePreposition

CustomerRelashionships

CustomerSegments

• Paglieri USA

• Suppliers

• LLG Group

• Unipro

• DHL

• Fragrance specialist “nose”

• Raw Material

• Production Plant

• Management

• Employees

• Online services

• Strong Brand in Italy

• Shower gel

• Inspired by nature

• Skin-care

• Regenerating effects (antioxidants)

• Argan oil

• Refreshing and relaxing shower experience

• Self-Service web ordering

• In-shop assistance

• Social Media (facebook)

• Customer Engagment

• Auquolina online store

• Online retailers

• Profumerias

(Lagardenia, Limoni)

• Woman

• Middle class

• Upper middle class

• 20 - 50 years old

• Relationships

• Local and International

• Human resource

• Production

• Sales

• Distribution

• Shower Gel

• Gift Package

Classic

Chocolate

A-drops

9 out of the10 Aquolina lines include shower gel.

Fashion

X-moothies

kok-tails

Royal

Fruit Shakes

Vivi NaturaOud

AQUOLINA BRAND LINES

Company Analysis

Product Analysis

Design Goals

ConceptDevelopment PrototypeIndustry

AnalysisMarket

Research

PRODUCT ANALYSIS: VIVI NATURA LINE

Variety of FragrancesInspired by nature / Argan OilLonglasting FragrancesCombine variety of ingredientsGood Feeling

Strong FragancesLook Chemical/ArtificialColors not attractiveLow QualityNot outstanding in generalPo

sitiv

e

Neg

ativ

e

Easy to break

Similar to other brands

PRODUCT ANALYSIS: PACKAGING

Black Cap

Over sized shape

PRODUCT ANALYSIS: LABEL

Informationnot clear

Informationnot clear

Chemical ingredients

“Made in Italywith love”

Plastic wrap

Not attractive

Low Quality Printing

Do not eat

Dark Visual

PRODUCT ANALYSIS: BRAND IDENTITY

Uppercase and Lowercase

Overall Lowquality perception

Lack of product/name coherence

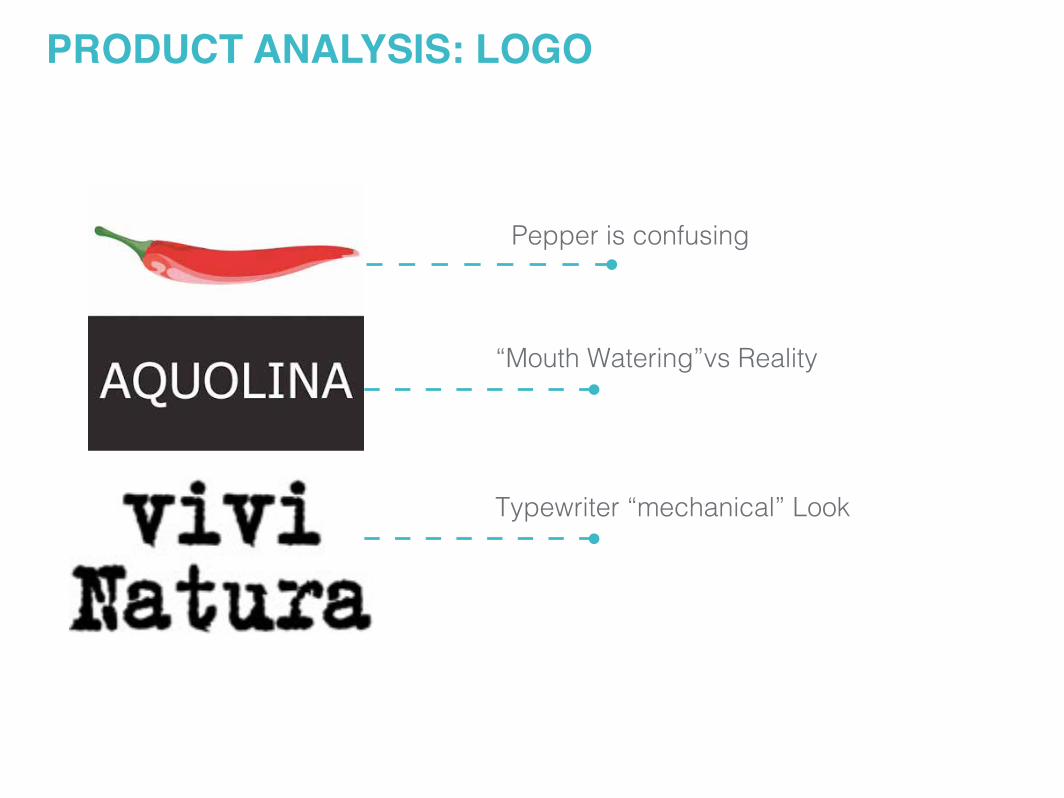

PRODUCT ANALYSIS: LOGO

Pepper is confusing

“Mouth Watering”vs Reality

Typewriter “mechanical” Look

PRODUCT ANALYSIS: SELLING POINT

Hard to recognize

Not visible from distance

Near to Aquolina Fashion Line

Close to the floor

Francesca, 35

Income: mid-class to upper

Location: Milan, Italy

Motivation: Appearance, Social recognition and Financial Incentive

Fears: Financial Unstability, Illness (themselves & family), Aging, Conflicts in family

Hero/ Model: Celebrities, Politician and Business Women

PERSONA“As I’m a busy person, I like to relax and take care of my skin and my body to feel always young and beautiful”

Francesca works as a civil servant and has a busy week. On the weekends she likes to be with her family, her two children, her hus-band Giuseppe and her dog. In her spare time, she likes to watch tv mainly of culinary and beauty programs. Francesca loves to buy and find good prices on her favorite stores. During the holidays she likes to travel with her family for a quiet place near the beach.

Brands Media

Magazines

Newspaper

Beauty Blogs

TV

CUSTOMER JOURNEYTalking to friends about the product

Consumers have a good impression

2

Looking for advertising

There is no advertisement for this line

1

Go to internet

Facebook - Fast replyLimoni | La Gardenia

Online Sales

Go to the shops

Easy to find the shops

Many different brands of the same product

Difficulty to find the product. Last shelf near to the floor

Seller does not suggest the product

Visual attractionThe product is not visual attractive

Other brands are visually attractive Price test

Similar price to other brands

9 Buy the product

2

34

5

6

Smelling testPeople like the smell

87

USER EXPERIENCE

1 Go to the shower

2 Open the water 3 Open the productEasy to open

The bottle shape is not good to hold

4Put the product on the glove or sponge

Use the product on the body

Need to put the product more then one time

6 Wash theproduct

It is not easy to washneed a lot of water

Finish theshowerThe smell stay longer then others brands

5

7

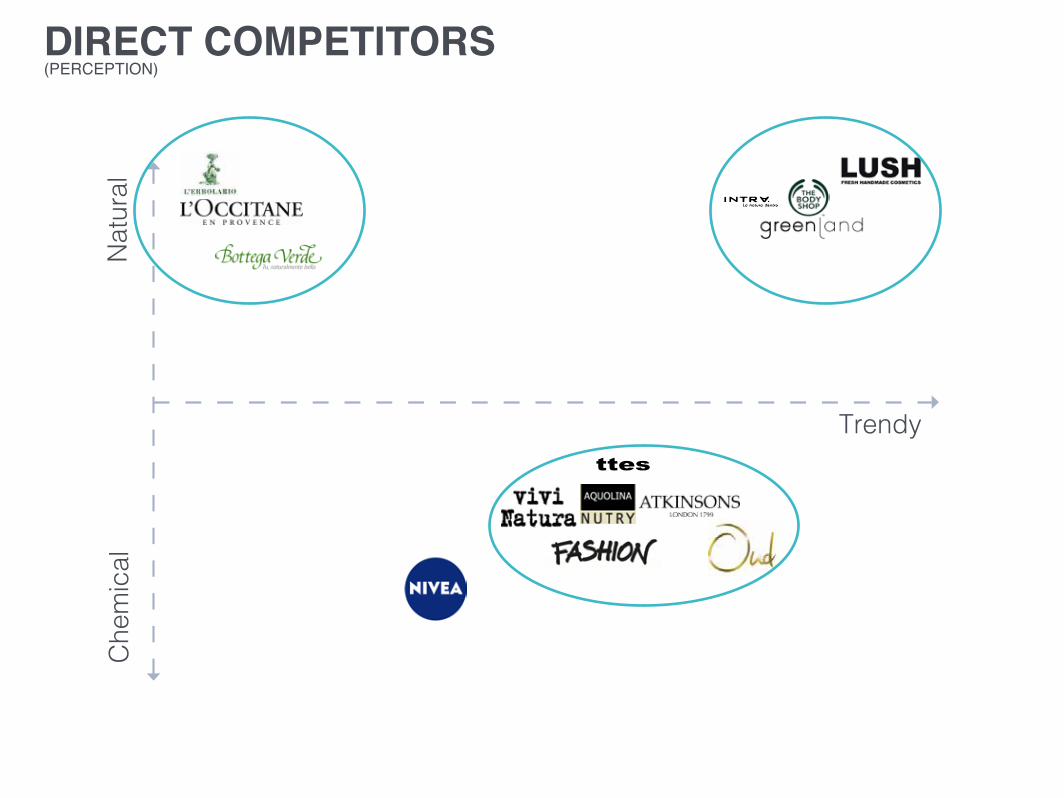

COMPETITORS

DIRECT COMPETITORS (PERCEPTION)

Trendy

Natu

ral

Ch

em

ical

Color

Smell

Packaging and display

Attractiveness

Communication & Storytelling

Natural perception

BENCHMARKING(PERCEPTION BASED)

BRAND PERSONALITy: FLORAL ExTRAvAGANzA

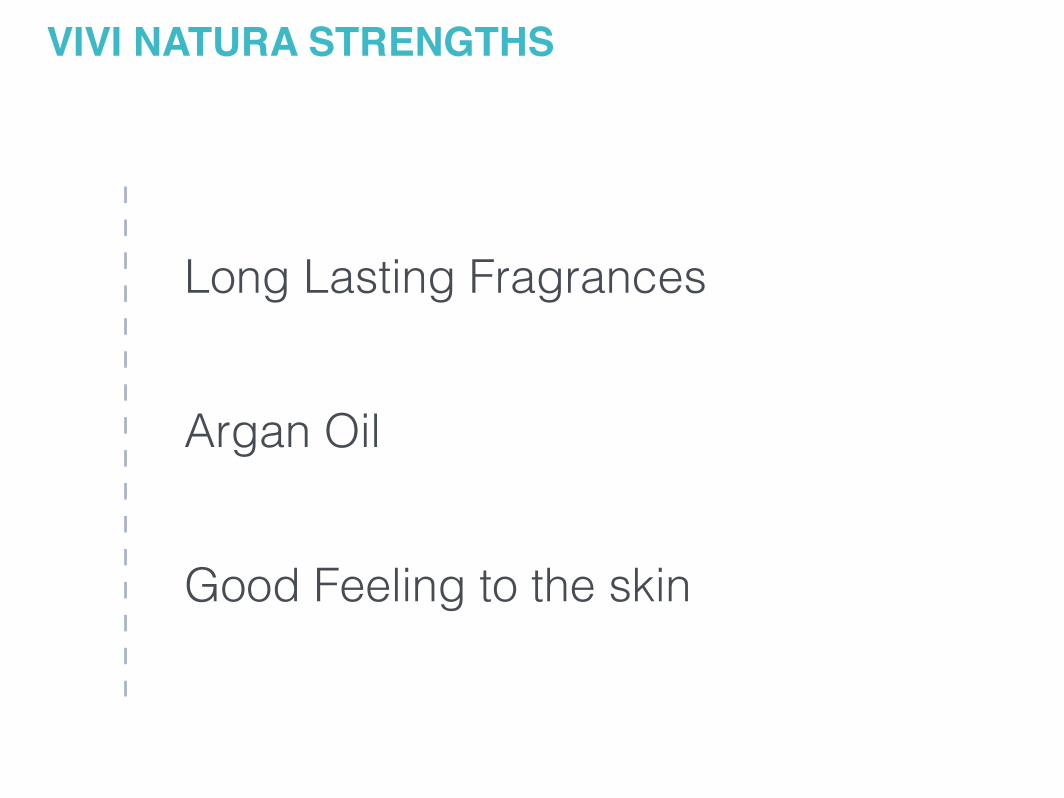

Long Lasting Fragrances

Argan Oil

Good Feeling to the skin

VIVI NATURA STRENGTHS

Company Analysis

Product Analysis

Design Goals

ConceptDevelopment PrototypeIndustry

AnalysisMarket

Research

What if vivi Natura embrace nature?

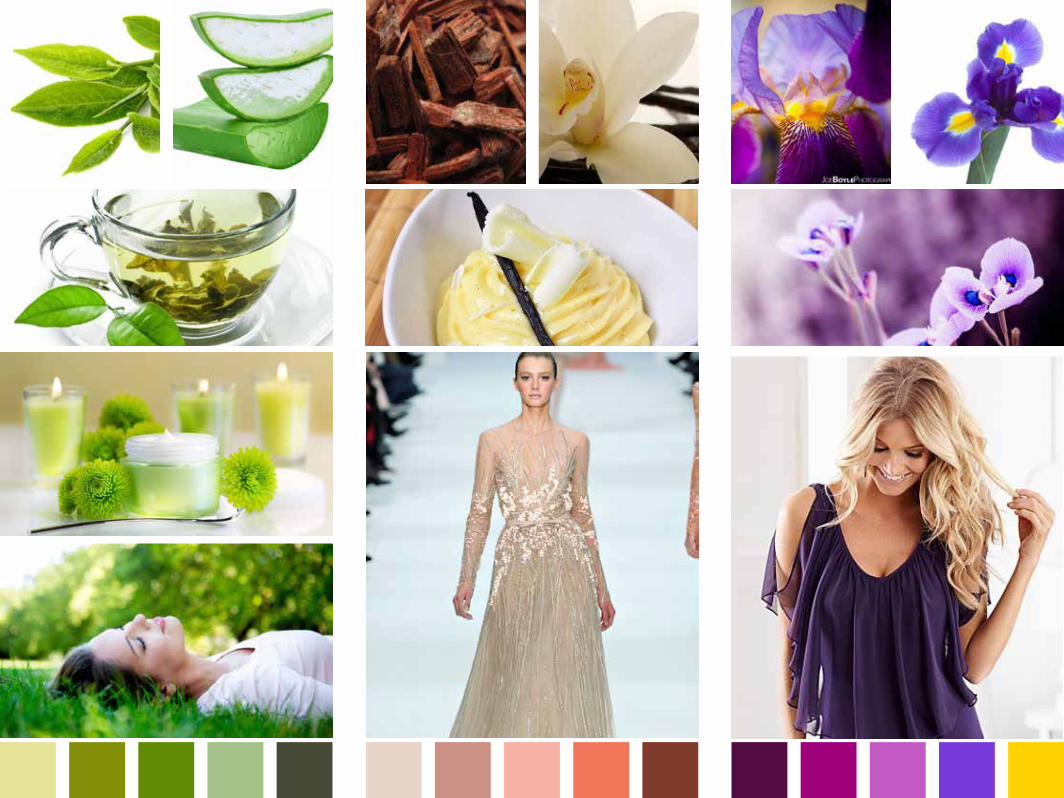

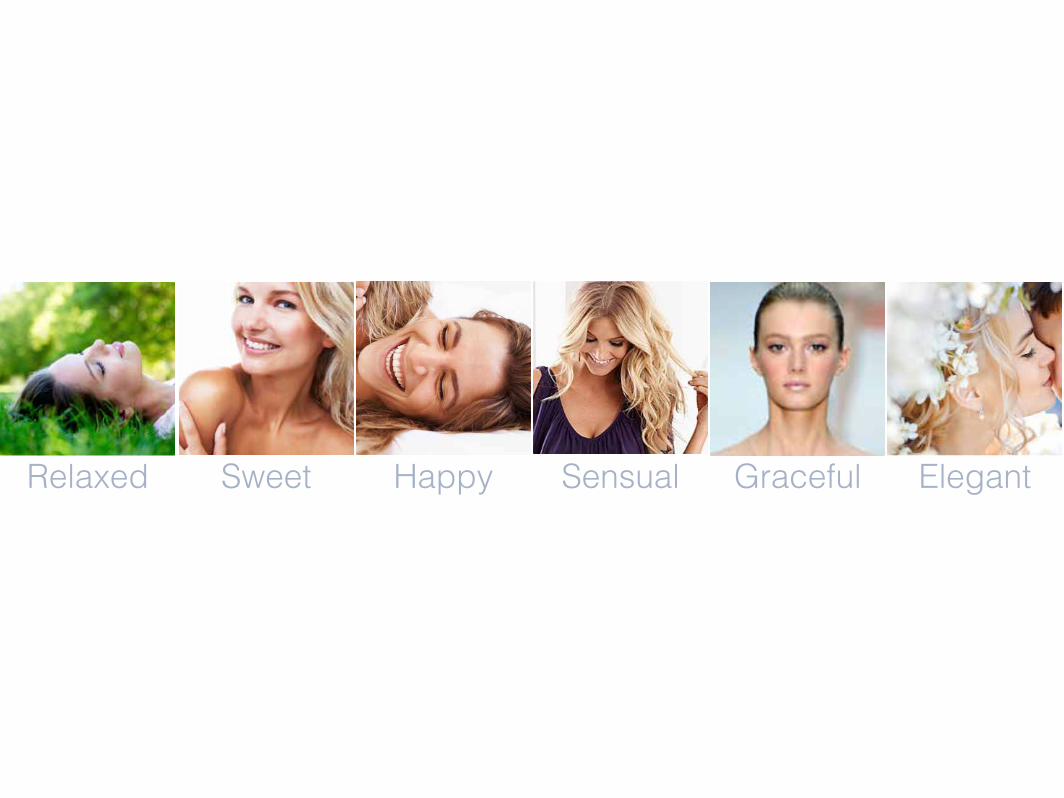

Relaxed GracefulSensualSweet ElegantHappy

Natural Look

Unique Personality

Focus on “Vivi Natura”

DESIGN GOALS

Company Analysis

Product Analysis

Design Goals

ConceptDevelopment PrototypeIndustry

AnalysisMarket

Research

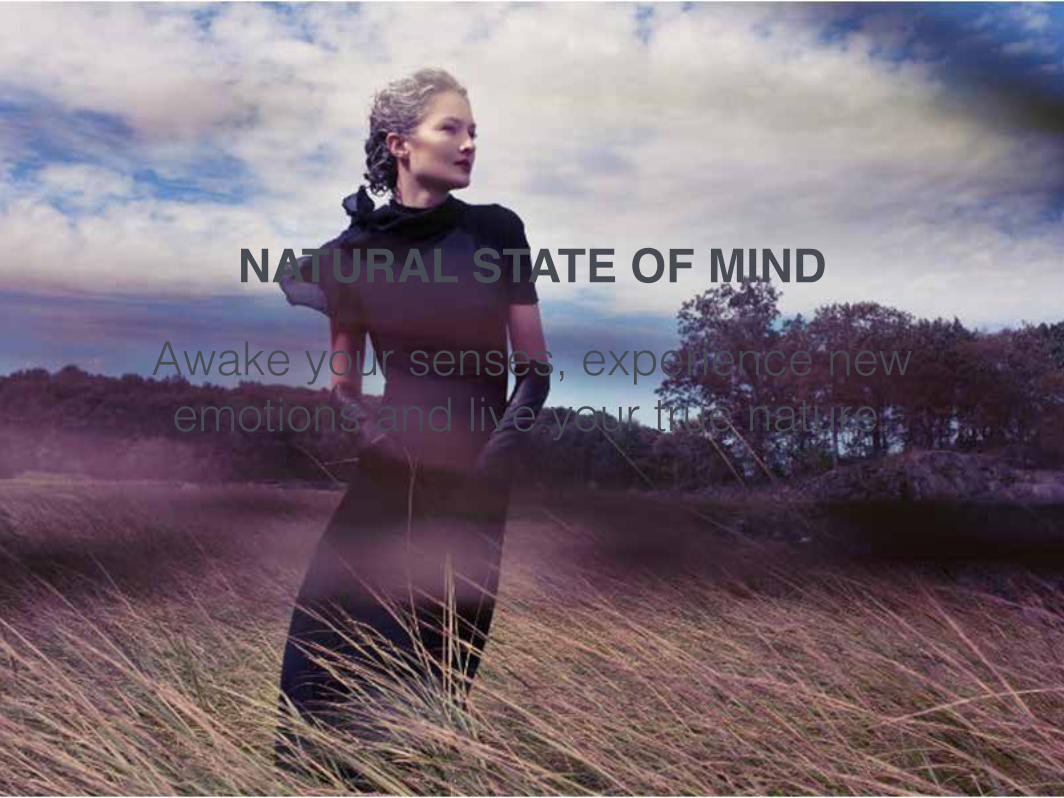

Awake your senses, experience new emotions and live your true nature.

NATURAL STATE OF MIND

movement • shapes • uniqueness

NATURAL STATE OF MIND

Company Analysis

Product Analysis

Design Goals

IndustryAnalysis

MarketResearch

ConceptDevelopment Prototype

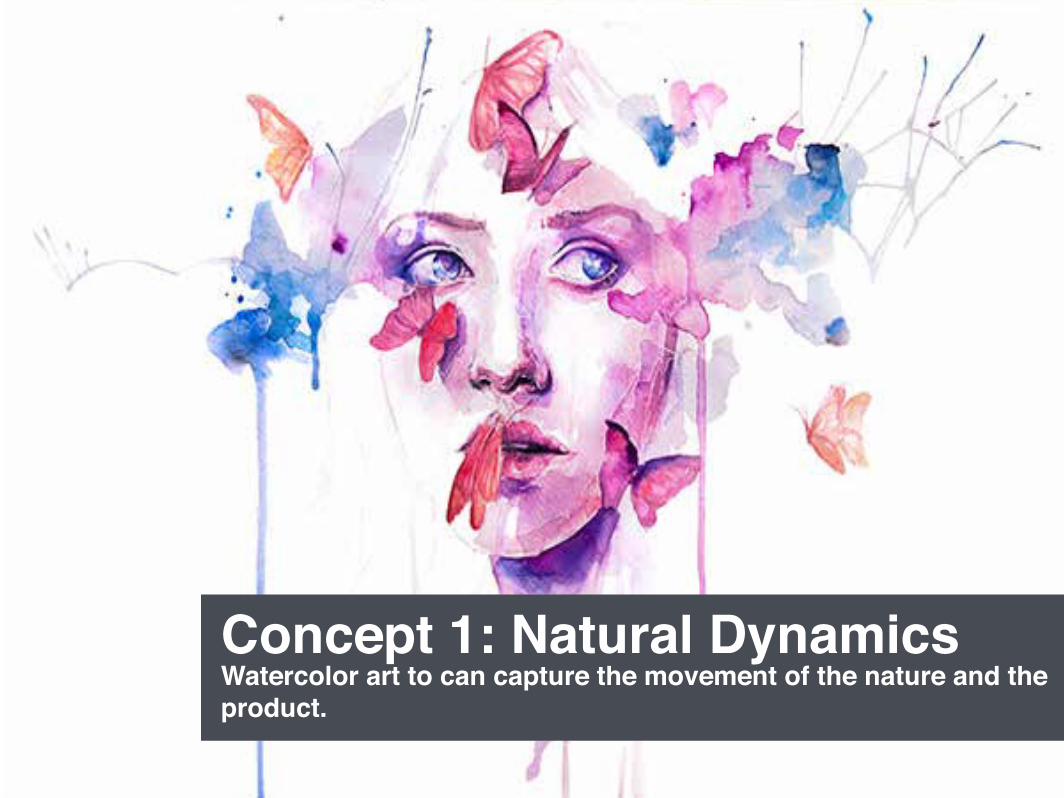

Concept 1: Natural DynamicsWatercolor art to can capture the movement of the nature and the product.

Artistic vision of nature

Fluid sense

Approachable

Concept 2: Emotional MosaicNature shapes are as diverse as each individual’s life experience. Each life is a beautiful unique design similar to a mosaic.

Modern Details

Vibrant shapes

Redifining realness

Concept 3: Discovering Nature

DiscoveringExperience

Modern Look

Unique Product

Nikhil | Rain | Mario | Ulli • Master in Business Design • Domus Academy • 2015

How can we trainLuigi Bianchi Mantova

clients to increasethe company’s export sales?

Industry Analysis

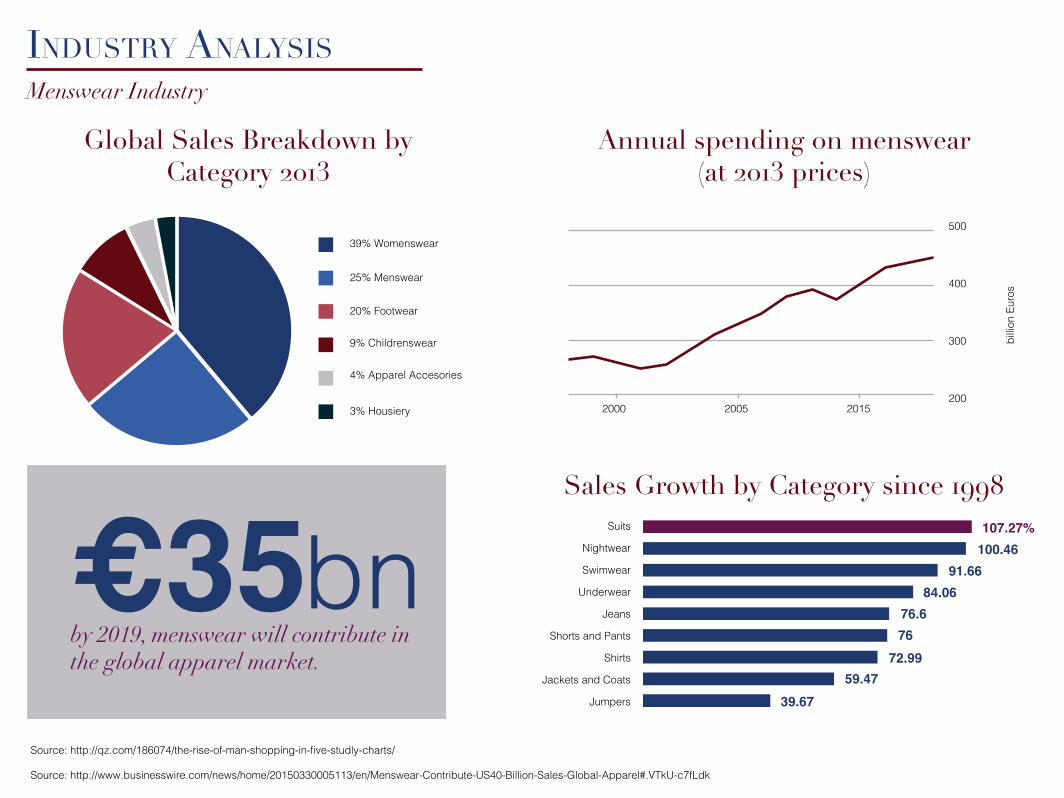

Source: http://qz.com/186074/the-rise-of-man-shopping-in-five-studly-charts/

Source: http://www.businesswire.com/news/home/20150330005113/en/Menswear-Contribute-US40-Billion-Sales-Global-Apparel#.VTkU-c7fLdk

Global Sales Breakdown by Category

Annual spending on menswear(at prices)

Sales Growth by Category since 998

39% Womenswear

25% Menswear

20% Footwear

9% Childrenswear

4% Apparel Accesories

3% Housiery

billio

n Eu

ros

500

400

300

20020052000 2015

by 2019, menswear will contribute in the global apparel market.

Suits 107.27%100.46

91.6684.06

76.676

72.9959.47

39.67

Nightwear

Swimwear

Underwear

Jeans

Shorts and Pants

Shirts

Jackets and Coats

Jumpers

INDUSTRY ANALYSISMenswear Industry

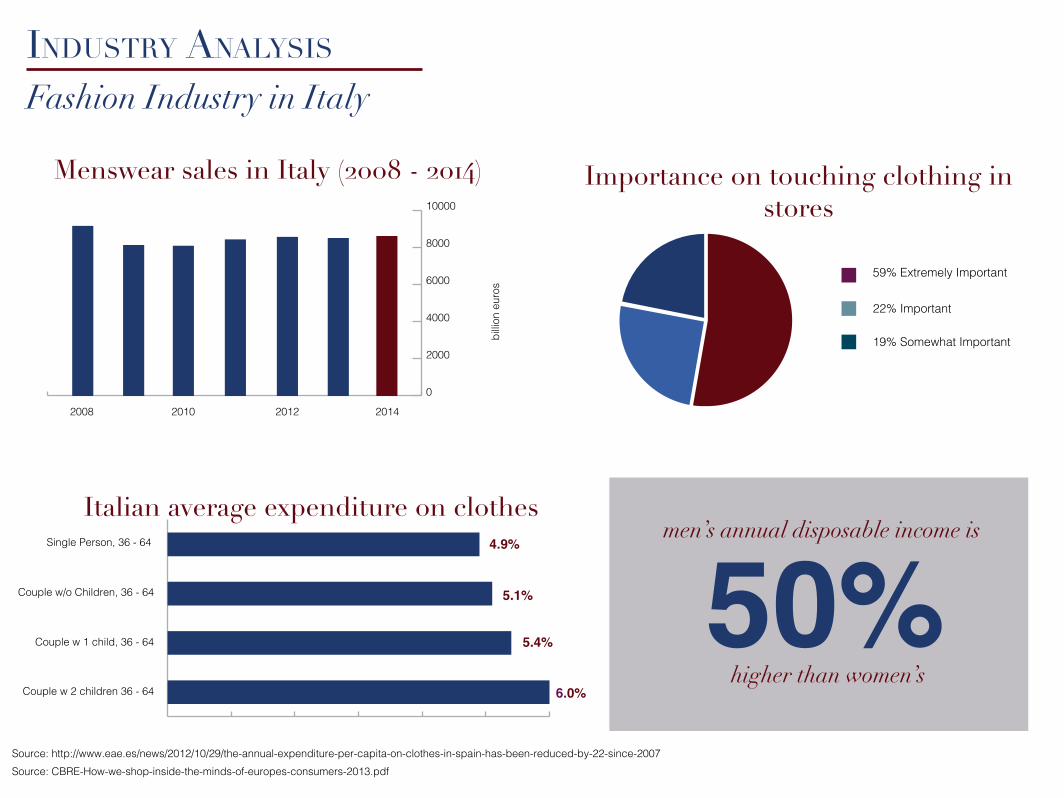

Menswear sales in Italy ( 8 - ) Importance on touching clothing in stores

billio

n eu

ros

10000

6000

8000

4000

2000

0

2008 2010 2012 2014

Source: http://www.eae.es/news/2012/10/29/the-annual-expenditure-per-capita-on-clothes-in-spain-has-been-reduced-by-22-since-2007Source: CBRE-How-we-shop-inside-the-minds-of-europes-consumers-2013.pdf

22% Important

59% Extremely Important

19% Somewhat Important

Italian average expenditure on clothes 4.9%

5.1%

5.4%

6.0%

Single Person, 36 - 64

Couple w/o Children, 36 - 64

Couple w 1 child, 36 - 64

Couple w 2 children 36 - 64

INDUSTRY ANALYSIS

Fashion Industry in Italy

men’s annual disposable income is

higher than women’s

Company Analysis

Eleganza maschile da 1911

LUBIAM

COMPANY ANALYSISLubiam Brands

Features

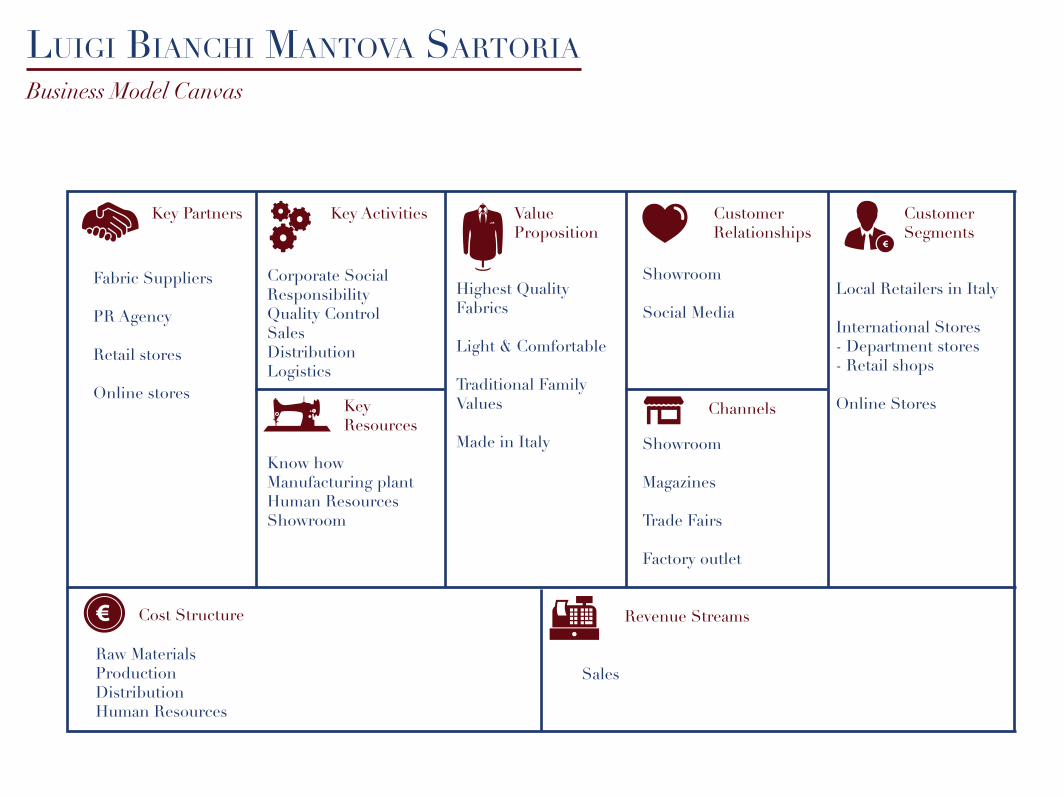

LUIGI BIANCHI MANTOVA SARTORIA

Suits Smokings Coats

VestsTravel JacketBlazer

Products

LUIGI BIANCHI MANTOVA SARTORIA

Elegance Heritage Made in Italy

Traditionalconstruction

Exclusivefabrics

Quality

Brand Values

LUIGI BIANCHI MANTOVA SARTORIA

Target Market

LUIGI BIANCHI MANTOVA SARTORIA

Services

Ready to wear Express Service Su Misura

LUIGI BIANCHI MANTOVA SARTORIA

Business Model Canvas

LUIGI BIANCHI MANTOVA SARTORIA

Key Partners Key Activities ValueProposition

Customer Relationships

ChannelsKeyResources

Cost Structure Revenue Streams

Customer Segments

Fabric Suppliers

PR Agency

Retail stores

Online stores

Showroom

Social Media

Showroom

Magazines

Trade Fairs

Factory outlet

Corporate Social ResponsibilityQuality ControlSalesDistributionLogistics

Highest Quality Fabrics

Light & Comfortable

Traditional Family Values

Made in Italy

Local Retailers in Italy

International Stores- Department stores- Retail shops

Online Stores

Know howManufacturing plantHuman ResourcesShowroom

Raw MaterialsProductionDistributionHuman Resources

Sales

Brand Analysis

RetailersMarketingBrand

Brand AnalysisKey Business Elements

RetailersMarketingBrand

Brand AnalysisBrand

KEY BUSINESS ELEMENTSLogo

KEY BUSINESS ELEMENTSLogo

KEY BUSINESS ELEMENTSLogo

KEY BUSINESS ELEMENTSLogo

KEY BUSINESS ELEMENTSLogo

KEY BUSINESS ELEMENTSLogo

KEY BUSINESS ELEMENTSLogo

RetailersMarketingBrand

Brand AnalysisMarketing

Marketing Campaigns

2010

2013

2011

2014 - 2015

2012

KEY BUSINESS ELEMENTS

Marketing Campaigns

KEY BUSINESS ELEMENTS

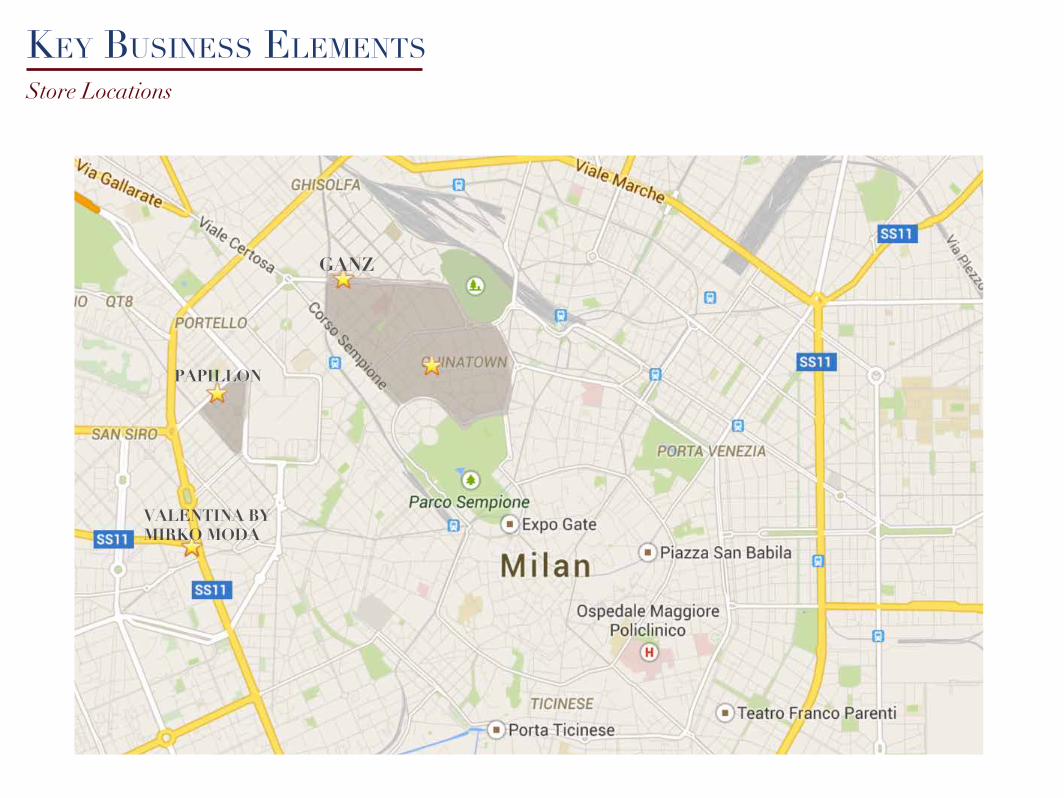

RetailersMarketingBrand

Brand AnalysisRetailers

Neighborhood Shop

KEY BUSINESS ELEMENTS

VALENTINA BY MIRKO MODA

PAPILLON

GANZ

Store Locations

KEY BUSINESS ELEMENTS

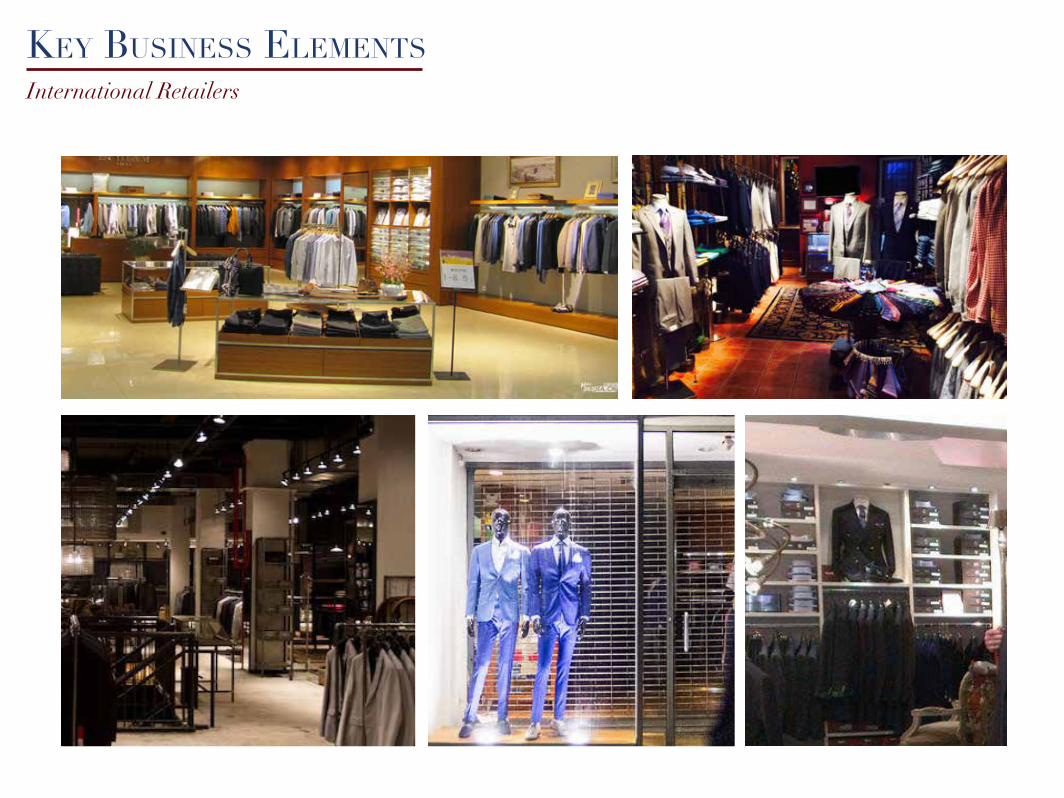

International Retailers

KEY BUSINESS ELEMENTS

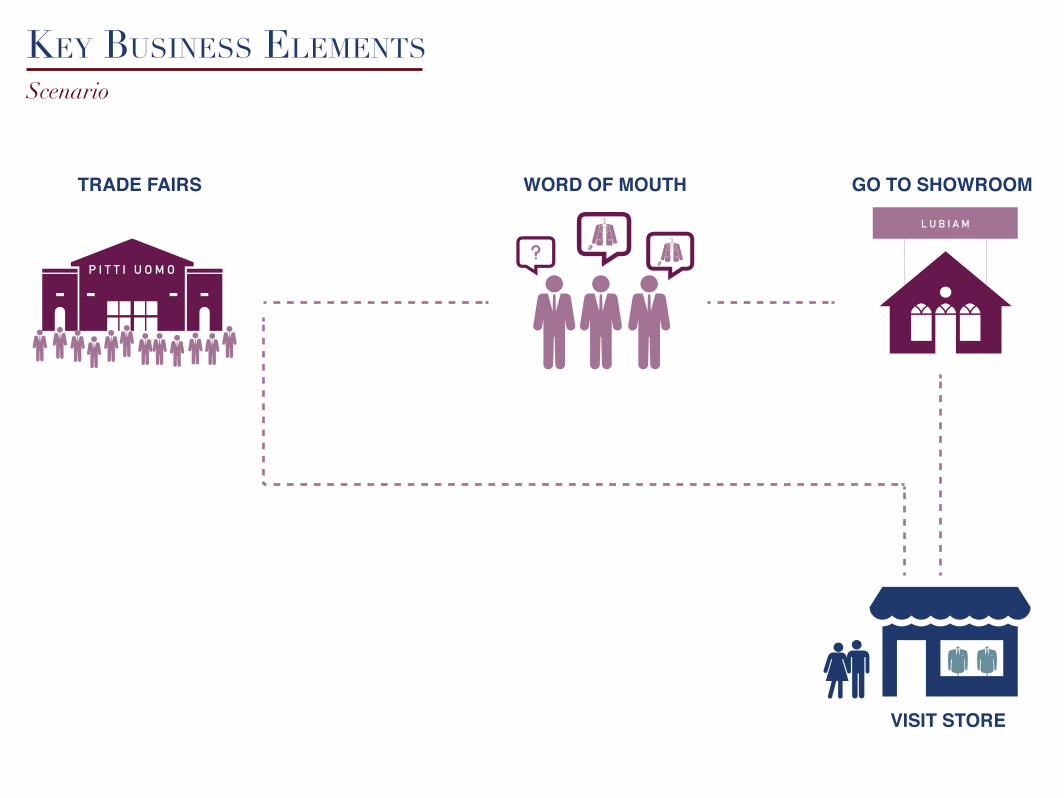

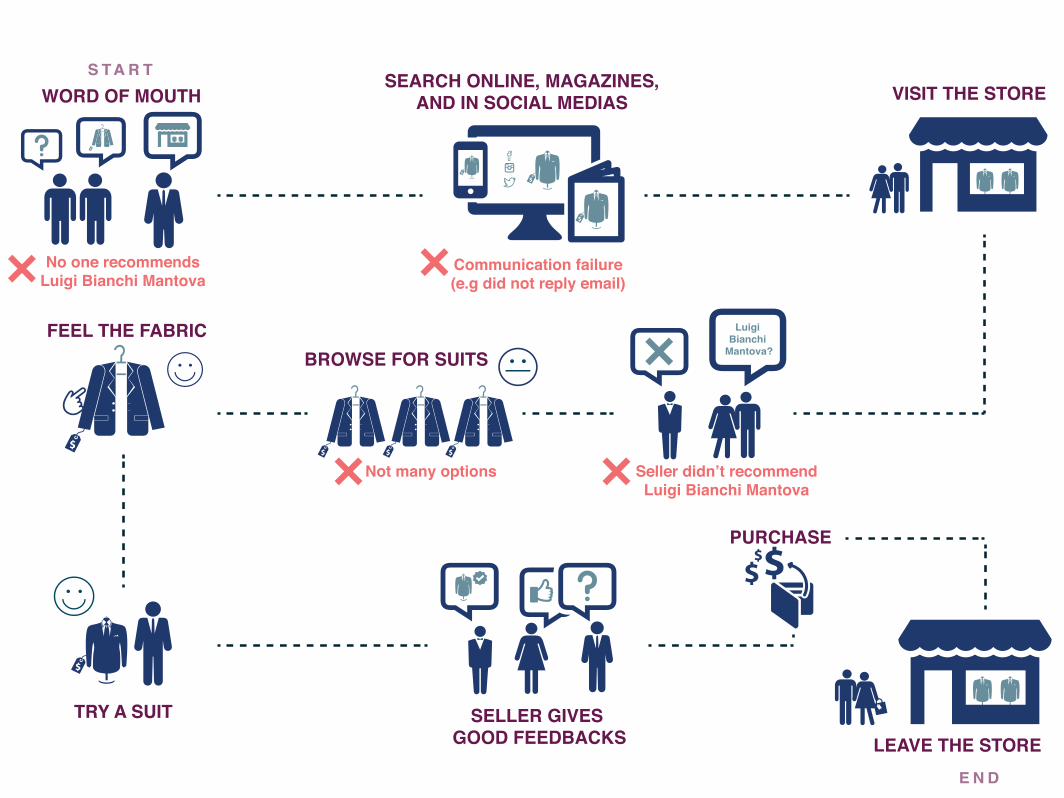

Scenario

KEY BUSINESS ELEMENTS

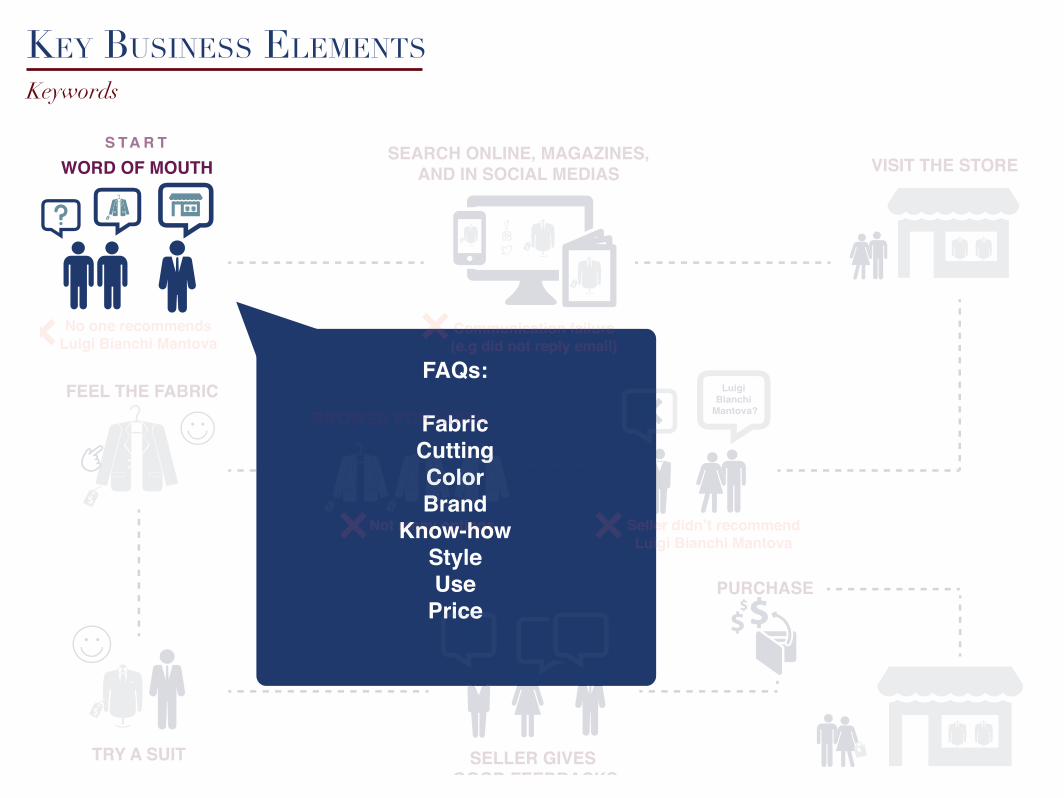

Keywords

KEY BUSINESS ELEMENTS

Social Media

Display

Fabric

Details

Mannequin

Magazines

Survey Results

LUBIAM

L.B.M 1911

Luigi Bianchi Mantova

Felt represented by the Luigi Bianchi Mantova Model. Tailor Made

Neighbourhood Shop

Department Store

Flagship Store

Price

Wearbility

Brand

Fabric

Fit

Preferred place for shopping

Most important criteria when buying a suit

Lubiam’s brands recognition

KEY BUSINESS ELEMENTS

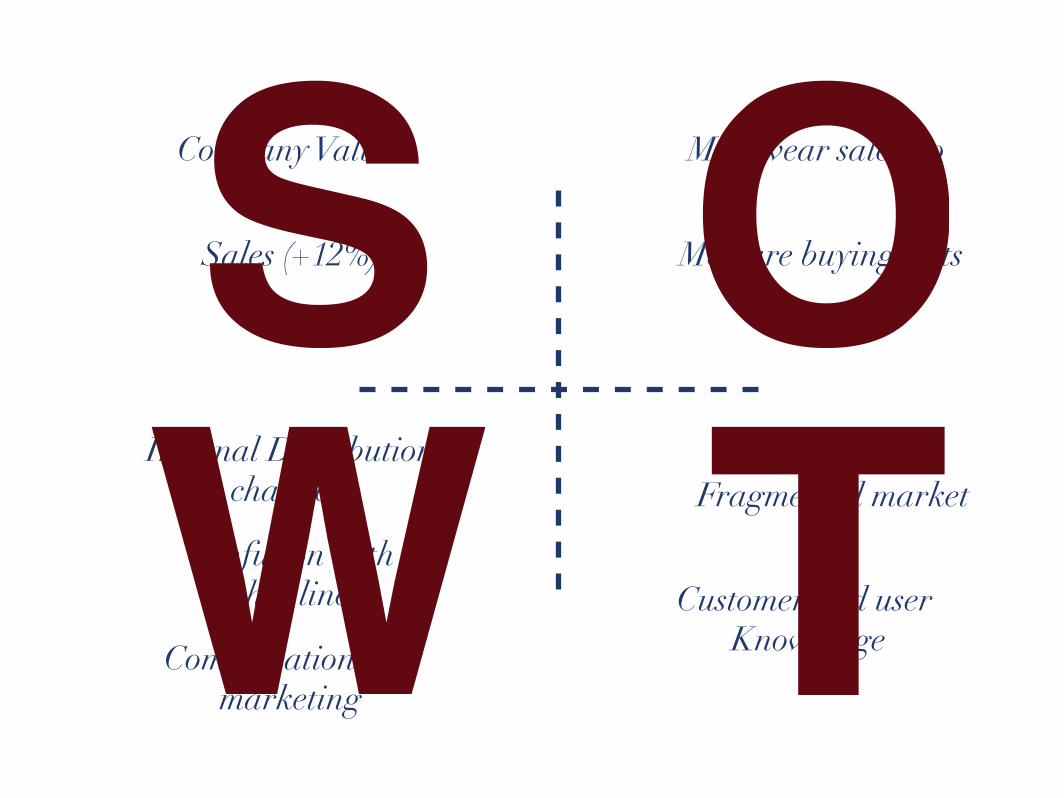

Company Values Menswear sales up

Men are buying suitsSales (+12%)

Internal Distributionchannels Fragmented market

Customer and user Knowledge

Confusion withother lines

Comunication andmarketing

There is a disconnection between the communication

strategy and the brand values.

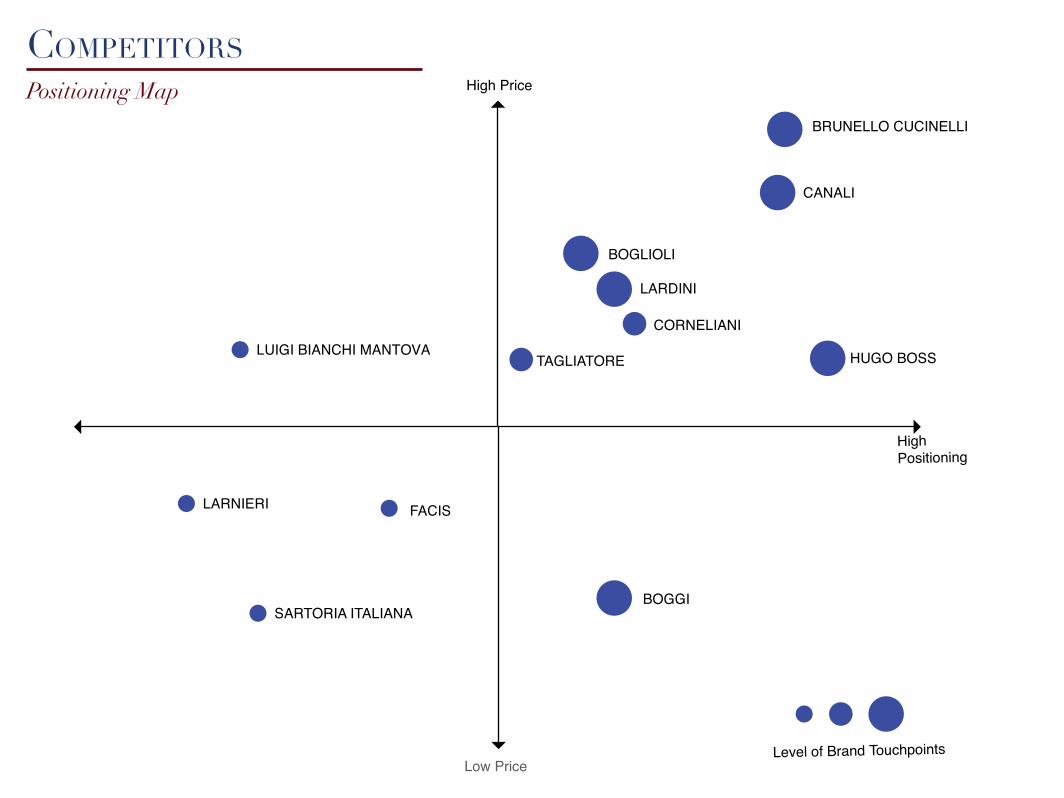

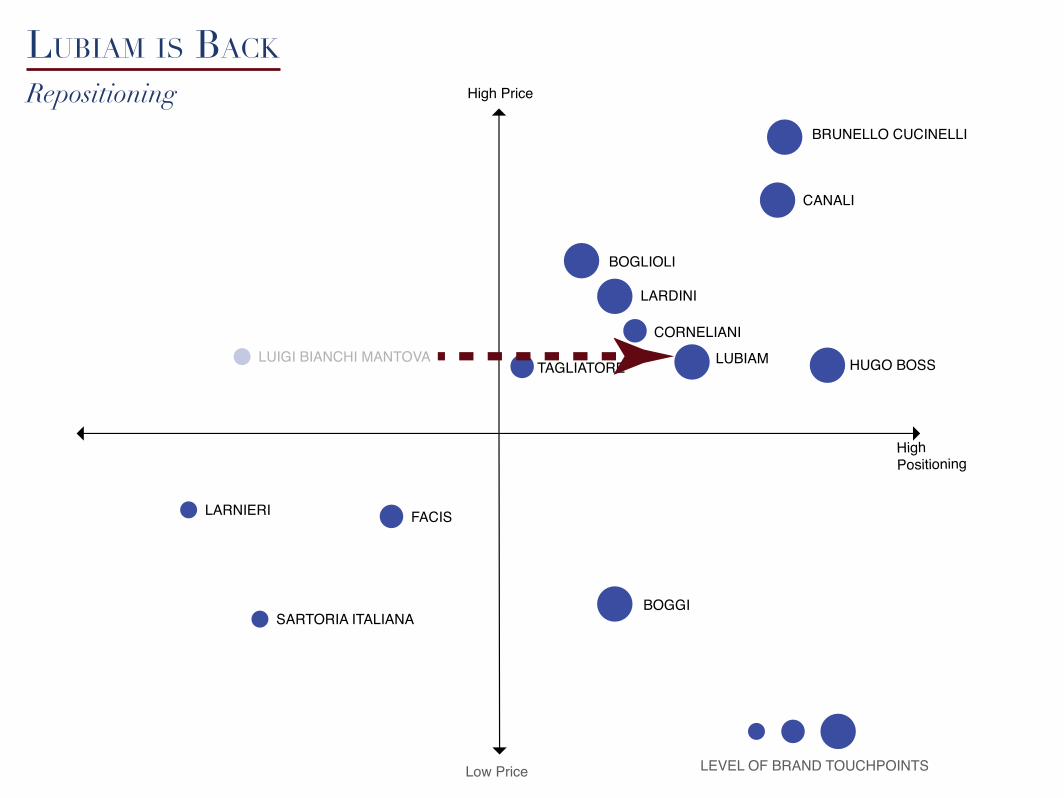

Competitors

High Price

Low Price

HighPositioning

Level of Brand Touchpoints

TAGLIATORE HUGO BOSS

CANALI

BRUNELLO CUCINELLI

CORNELIANI

LARDINI

BOGLIOLI

LUIGI BIANCHI MANTOVA

BOGGISARTORIA ITALIANA

FACISLARNIERI

Positioning Map

COMPETITORS

Well positioned brands have multiple touchpoints with

their customers.

What if Luigi Bianchi Mantova Sartoria embraces

its strengths?

Strategy

Envisioning the ‘dolce vita’ with a bold expresion of sophistication

redifined for the gentleman of today.

RetailersMarketingBrand

Key Components

STRATEGY

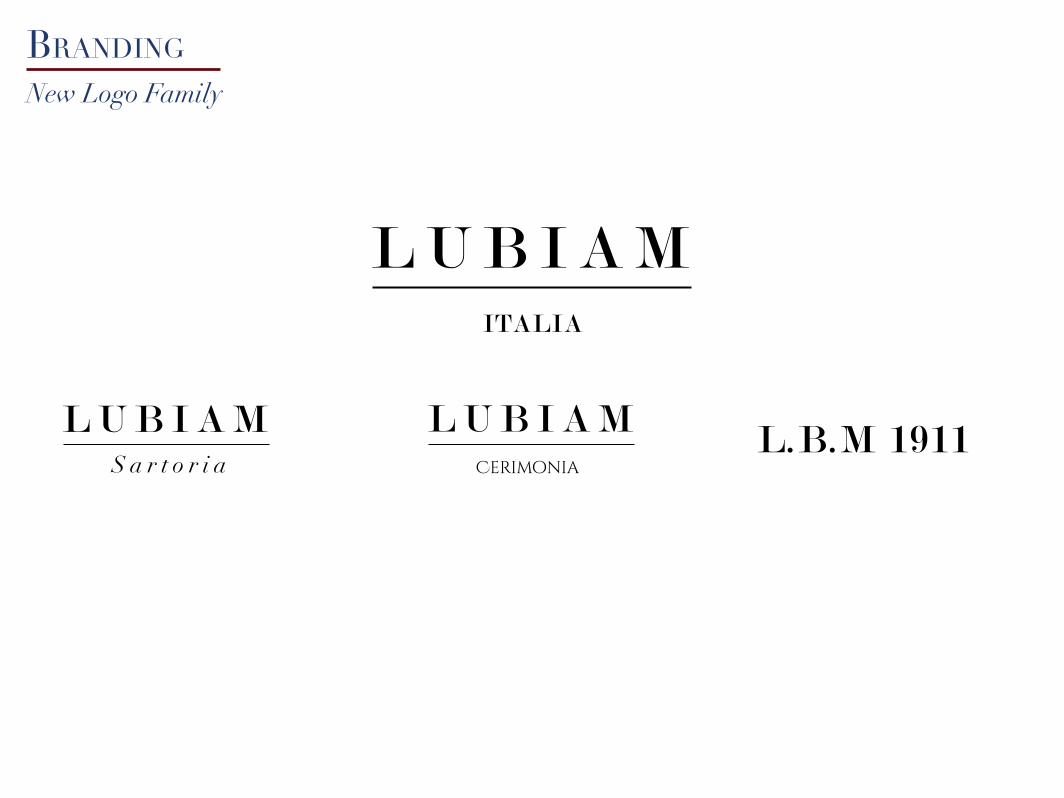

BRANDING

BRANDING

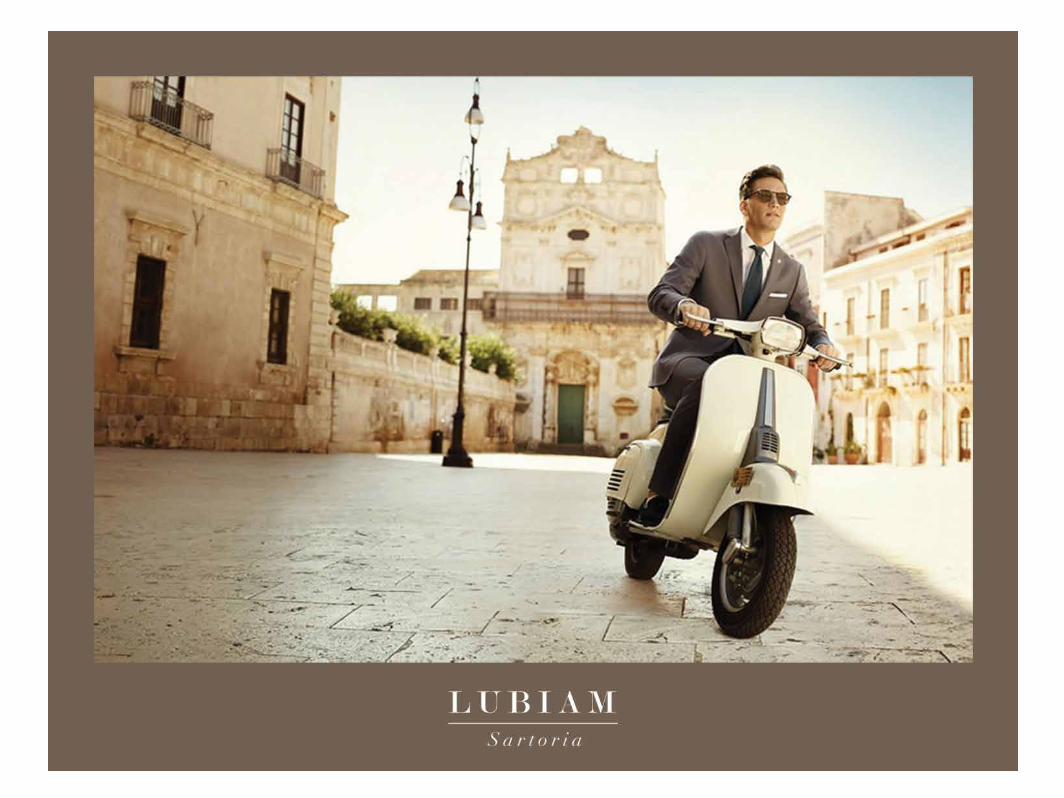

New Logo Family

IN-STORE PRESENCE

IN-STORE PRESENCE

Flipbook

ADVERTISEMENT

CUSTOMER ENGAGEMENT

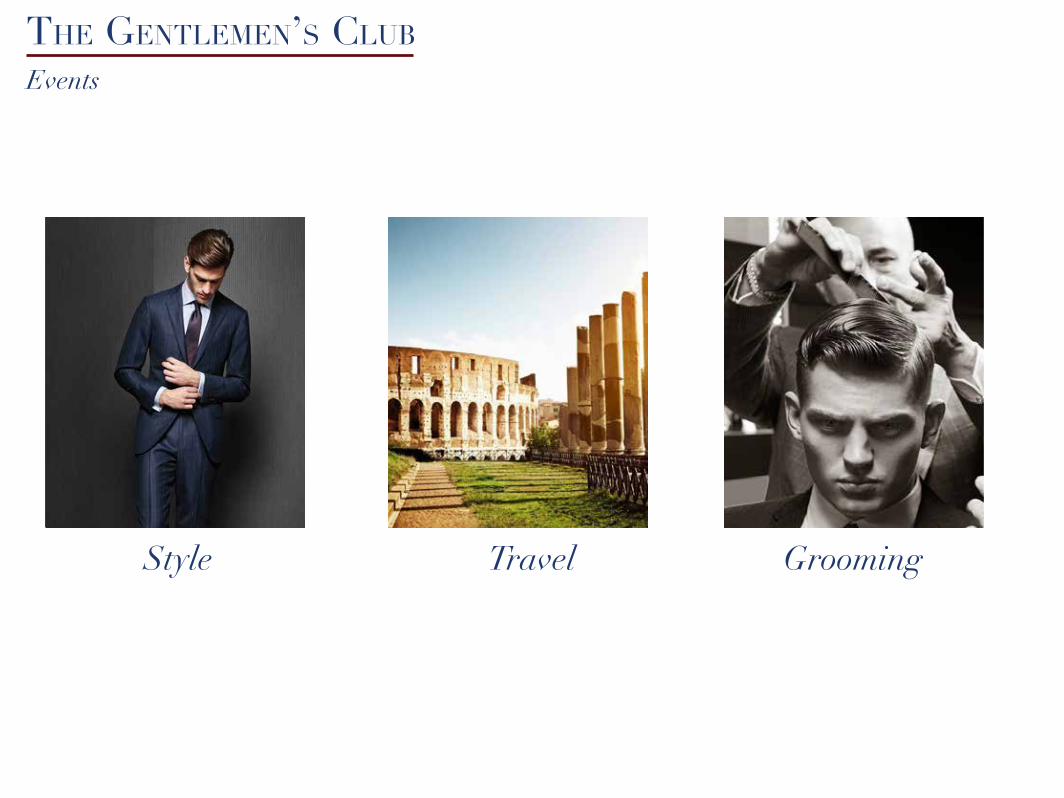

Style Travel Grooming

Events

THE GENTLEMEN’S CLUB

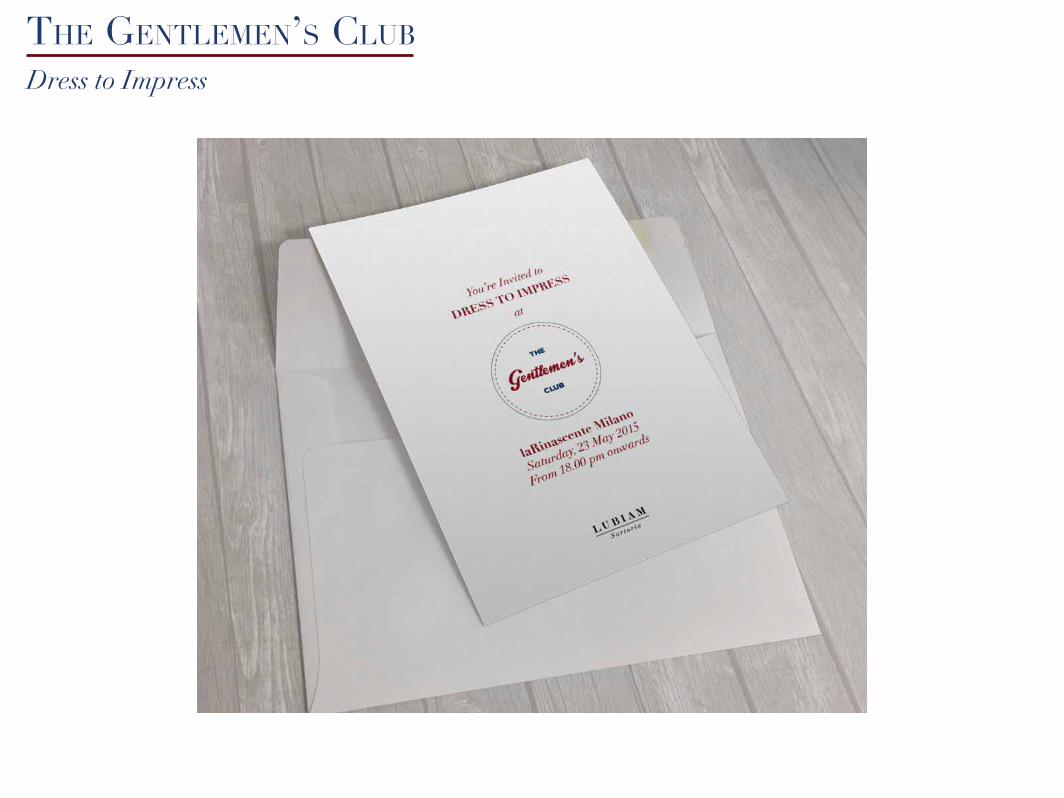

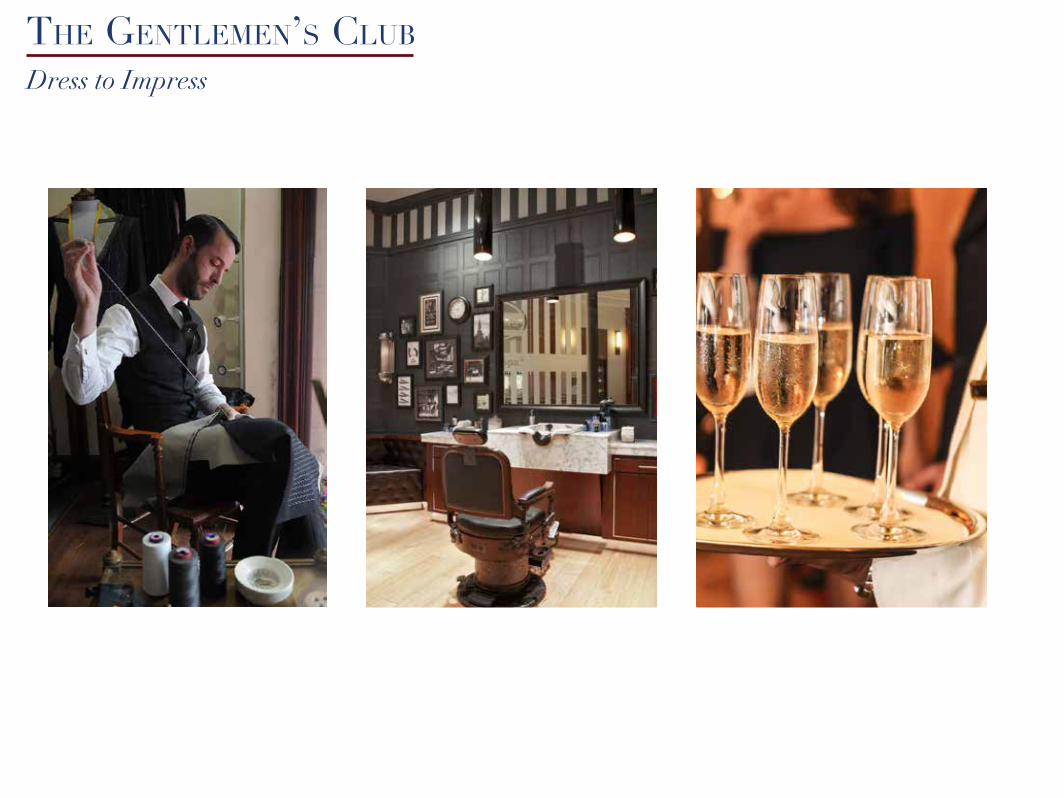

THE GENTLEMEN’S CLUB

Dress to Impress

Dress to Impress

THE GENTLEMEN’S CLUB

Dress to Impress

THE GENTLEMEN’S CLUB

Communications

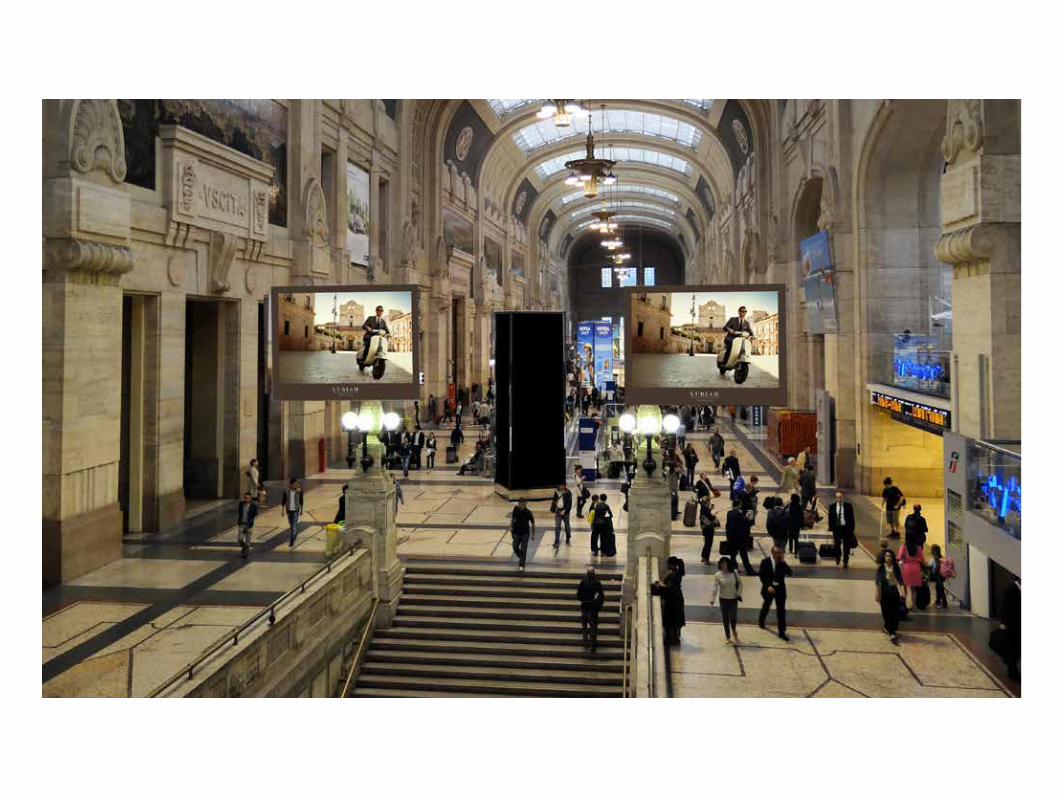

THE GENTLEMEN’S CLUB

Locations

THE GENTLEMEN’S CLUB

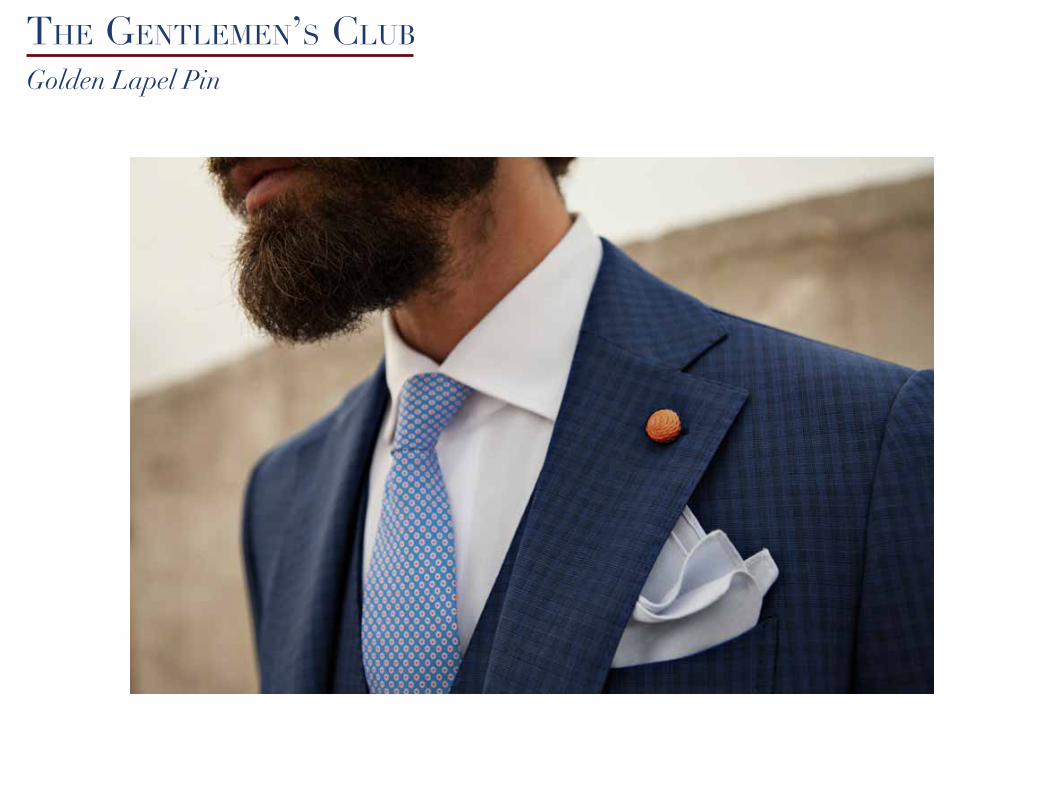

Golden Lapel Pin

THE GENTLEMEN’S CLUB

POP-UP STORE

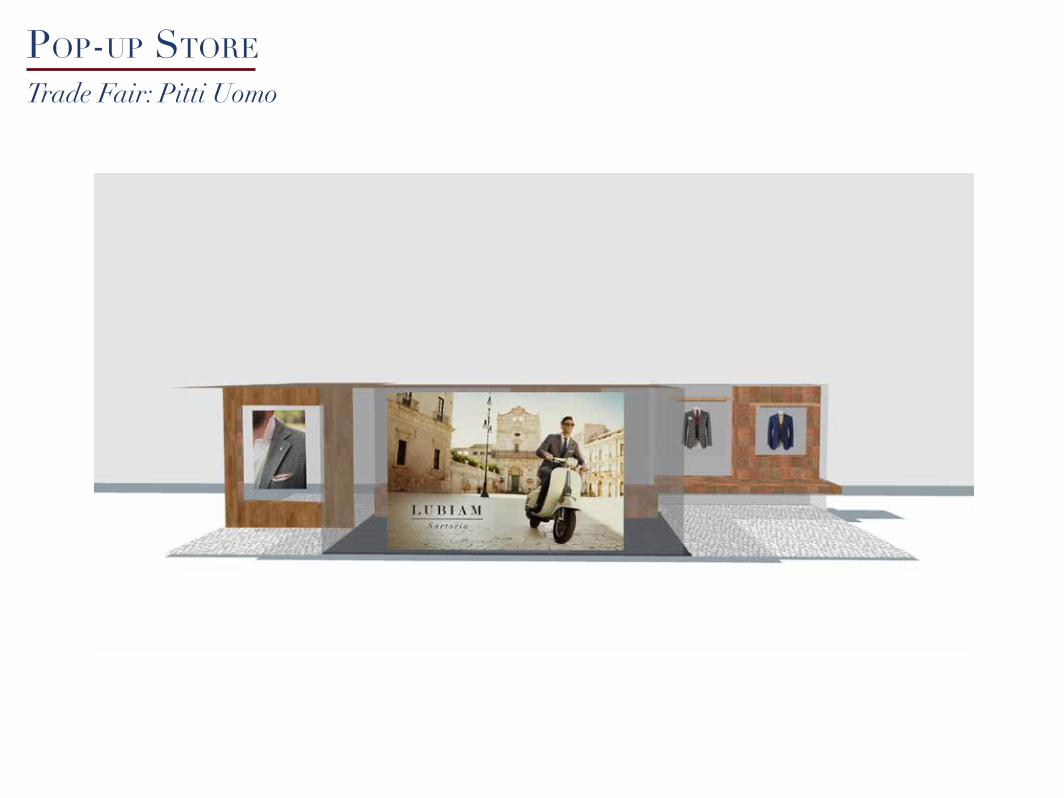

POP-UP STORE

Trade Fair: Pitti Uomo

POP-UP STORE

Trade Fair: Pitti Uomo

POP-UP STORE

Events

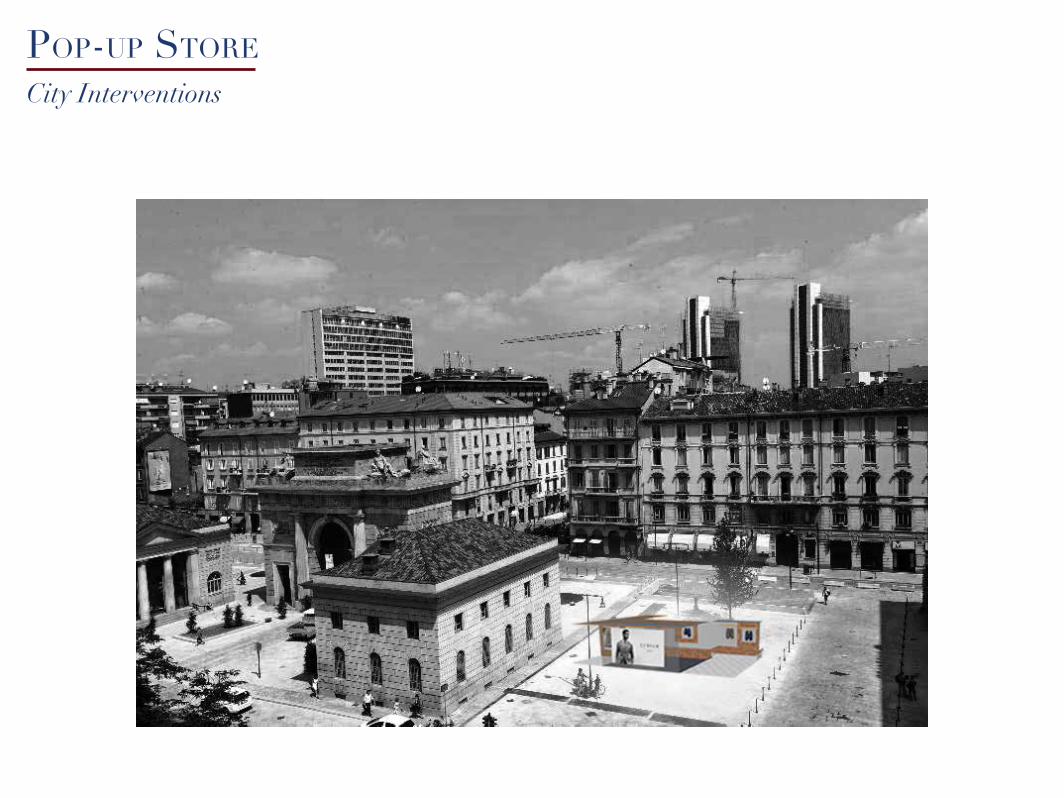

POP-UP STORE

City Interventions

LUBIAM IS BACK

Timeline

LUBIAM IS BACK

Repositioning

Nikhil | Rain | Mario | Ulli • Master in Business Design • Domus Academy • 2015