deriving value from purpose - building a better working ... · ii deriving value from purpose: ......

TRANSCRIPT

Deriving value from purposeUnderstanding the critical role of the CMO

ii | Deriving value from purpose: understanding the critical role of the CMO

Contents

Foreword 1

Executive summary 2

Methodology 4

Purpose: an idea whose time has come ... 6

Why now? The drivers and returns 9

There’s work to be done 14

The CMO plays a critical role in purpose 20

For the CMO, a new purpose-infused role 25

Acknowledgements 27

1D eriving value from purpose: understanding th e critical role of th e C M O |

T he research that f ol l ow s show s that certain com p anies tak e their purpose significantly more seriously than the rest of the p ack . A grow ing num b er are so f ocused in their ef f orts that al m ost w ithout ex cep tion, k ey stak ehol ders such as w ork ers, m anagers and custom ers are intim atel y f am il iar w ith the organiz ation’ s p urp ose. T he p urp ose is so cl ear and so com p el l ingl y articul ated that p eop l e b oth inside and outside of the com p any understand it and of f er b uy -in, and the host com p any reap s the rew ards.

B ut achiev ing such a state inv ol v es m uch m ore than m erel y ex p ressing p urp ose. T o succeed, p urp ose m ust b e authentic, deep l y ingrained and integrated. Mere sl ogans and m ark eting cam p aigns w il l not achiev e the desired resul ts. R eal p urp ose m ust b egin b y guiding corp orate strategy , and f rom there, ex ecution m ust attain com p l ete al ignm ent. T o b e trul y activ ated, p urp ose m ust inf orm and driv e day -to-day actions. T hroughout the enterp rise, the w ork f orce m ust f eel em p ow ered to m ak e decisions b ased on p urp ose.

G etting there req uires constant com m unication and reinf orcem ent of p urp ose. Perf orm ance ev al uation and ev en com p ensation, b onuses and recognition/ aw ard p rogram s m ust f ortif y the p rem ise of p urp ose. L eaders say that cap ab l y executed, purpose delivers benefits ranging from stronger sales to greater custom er l oy al ty and em p l oy ee engagem ent.

The research also reveals that for chief marketing officers ( CMOs) , p urp ose is b ecom ing a critical p riority , reaching the “ top tw o” l ist at 79% of com p anies. A nd b y no m eans is the p ath f orw ard an easy one. I ndeed, this f ast-ev ol v ing rol e req uires the CMO to lead or influence a wide range of functions and activities ranging f rom p roduct dev el op m ent, to l ogistics, sourcing, H R and ev en M& A .

So does y our com p any hav e a p urp ose? I s that p urp ose cl earl y articul ated and activ ated? A re y ou deriv ing al l of the v al ue there is to b e f ound in com m itm ent to p urp ose? H ow can y ou im p rov e y our p urp ose-driv en resul ts? T hough it w il l rem ain f or each company to find its own answers, we believe the report that f ol l ow s can p rov ide v al uab l e guidance.

— Bruce Rogers, Chief Insights Officer, Forbes Insights

F o r e w o r d

N earl y al l com p anies “ say ” they hav e a p urp ose. B ut do they ?

2 | Deriving value from purpose: understanding the critical role of the CMO

Executive summary1

E x ecutive summary

3D eriving value from purpose: understanding th e critical role of th e C M O |

• Com p anies b ring their p urp ose to l if e through:

• Articulation, the cl ear ex p ression of w hy this b usiness is in b usiness

• Activation, tangib l e p ractices m ak ing p urp ose real f or decision-m ak ers, the w ork f orce, custom ers and al l rel ated stak ehol ders

• Som e com p anies are m ore “ p urp osef ul ” ( p urp ose-driv en) than others: 29% say p urp ose is of p rim ary im p ortance.

• T hese 29% ex hib it a com m itm ent to articul ating and activ ating purpose to a significantly greater degree than others — and are ref erred to as “ p rim ary ” com p anies throughout the anal y sis.

• T he l eading driv er of p urp ose today is the p erceiv ed need to p ursue continuous transf orm ation, cited b y 60% ov eral l and 77% of resp ondents w ho v iew p urp ose as a p rim ary f ocus. Other issues, such as rising consum er p ow er, l eadership concerns or ev en corp orate citiz enship concerns surrounding gl ob al w ork f orce w ork ing conditions or com p ensation, can al so p l ay a k ey rol e.

• Ov er hal f of surv ey resp ondents, 53%, say p urp ose del iv ers significant tangible value to their enterprises, rising to 75% am ong those f or w hom p urp ose is of p rim ary v al ue.

• Over half (51%) say purpose delivers significant intangible v al ue to their enterp rises.

• Com p anies f or w hom p urp ose is of p rim ary im p ortance consistentl y indicate higher l ev el s of f ocus, ef f ort and inv estm ent in its util iz ation, w ith p ositiv e resul ts. Primary firms, in general, tend to report significantly greater p urp ose-rel ated articul ation and activ ation outcom es rel ativ e to the rest of the sam p l e.

• Key challenges inhibiting firms’ abilities to achieve value from p urp ose incl ude:

• Changing em p l oy ee/ organiz ation b ehav iors ( cited b y 39% of resp ondents)

• A chiev ing al ignm ent across al l b usiness f unctions ( 36%)

• A chiev ing b uy -in across the enterp rise ( 34%)

• T he CEO and the CMO m ust w ork cl osel y together on p urp ose:

• Ov eral l , the CEO is m ost f req uentl y cited as b eing the k ey driv er/ decision-m ak er in term s of the dev el op m ent/articul ation of p urp ose ( 79%) .

• T he CMO rank s second ( 53%) , w el l ahead of the CF O ( 37%) .

• N earl y hal f of ex ecutiv es ov eral l ( 45%) say they b el iev e p urp ose is the top p riority f or their CMO:

• This figure rises to 60% at primary companies.

• N inety -f our p ercent of CMOs them sel v es say p urp ose is a top one ( 42%) , tw o ( 24%) or three ( 13%) p riority .

• T he p urp ose rol e f or CMOs is m ul tif aceted:

• Must l ead or col l ab orate on a w ide range of initiativ es ( e. g. , al ignm ent across custom er ex p erience, m easurem ent and m etrics and new p roduct dev el op m ent)

• Must collaborate with a wide array of functions (e.g., finance, H R , R & D)

• Senior executives are likely overconfident in terms of how cap ab l y p urp ose is b eing activ ated:

• The most senior executives in the survey are significantly m ore op tim istic than others ab out the ef f ectiv eness of p urp ose in their organiz ations.

• Confidence declines significantly among mid-level managers.

Purp ose is not a m ission statem ent or a m ark eting sl ogan, b ut an asp irational “ reason f or b eing” that is grounded in hum anity and insp ires a cal l to action.

4 | Deriving value from purpose Understanding the critical role of the CMO

Methodology2

M eth odology

5D eriving value from purpose: understanding th e critical role of th e C M O |

T he insights and com m entary f ound in this rep ort are deriv ed f rom b oth a surv ey and q ual itativ e interv iew s. Partnering w ith EY , F orb es I nsights conducted a gl ob al surv ey of 217 ex ecutiv es. K ey dem ograp hics f rom this f al l 2015 research incl ude:

• Title: CEO ( 26%) , CMO ( 22%) , SVP/ VP ( 17%) , m anaging director ( 8%) , COO ( 6%) , EVP ( 6%) , p resident ( 5%) , CI O/CT O ( 4%) , other C-suite ( 6%)

• Location: North America (30%), Asia/Pacific Rim (30%), W estern Europ e ( 29%) , Central / South A m erica ( 10%)

• Annual sales: $ 5 b il l ion or m ore ( 20%) , $ 1 b il l ion to $ 4. 9 b il l ion ( 51%) , $ 500 m il l ion to $ 999 m il l ion ( 29%)

• Industry: consum er p roducts/ retail ( 20%) , b ank ing and cap ital m ark ets ( 13%) ; tel ecom m unications ( 11%) ; diversified industrial products (7%); health care (6%); insurance ( 6%) ; technol ogy ( 5%) ; oil and gas ( 5%) ; p riv ate eq uity ( 5%) ; real estate, hosp ital ity , construction ( 5%) ; w eal th and asset m anagem ent ( 5%) ; m ining and m etal s ( 4%) ; other ( 8%)

I nterv iew s w ere conducted w ith senior ex ecutiv es f rom f our l eading com p anies. Q uoted interv iew ees incl ude:

• J oey B ergstein G eneral Manager and CMO Sev enth G eneration

• A ndy B urtis SVP Corp orate Mark eting and Com m unications McK esson

• C h ristine M cG rath VP W el l -B eing Mondelēz International

F orb es I nsights ex tends its gratitude to our surv ey resp ondents and interv iew ees.

6 | Deriving value from purpose: understanding the critical role of the CMO

Purpose: an idea whose time has come ...

3

P urpose: an idea w h ose time h as come . . .

7D eriving value from purpose: understanding th e critical role of th e C M O |

P urpose is taking h old. C onsider:• C onsumer products: T hink ab out p urp ose-driv en

enterp rises, in consum er goods or otherw ise, and Sev enth G eneration l ands on the l ion’ s share of inf orm ed short l ists. Specifically, says general manager and CMO Joey Bergstein, the com p any ’ s p urp ose is to “ insp ire a consum er rev ol ution that nurtures the heal th of the nex t sev en generations,” a ref erence to the great l aw of the I roq uois. Com m itm ent to these ideas, say s B ergstein, “ is not onl y good f or consum ers and the p l anet as a w hol e, it’ s a v ery sound and sustainab l e b usiness m odel . ”

• F ood and b everage: Sp ringing f rom the 2012 sp l it of K raf t Foods into two independent companies, the Mondelēz I nternational w eb site p rocl aim s its intention to create “ del icious m om ents of j oy ” f or consum ers around the gl ob e. “ W e cal l that ‘ the dream ’ ,” say s VP ex ternal af f airs Christine McGrath, a purpose that eventually cascades into five core strategies, one of w hich is the p ursuit “ of gl ob al w el l -b eing” ( w here McG rath l eads the charge) . N o m ere l ip -serv ice to the cause, the com p any em b eds p urp ose throughout its b usiness p ractices. Ov eral l , say s McG rath, “ our dream driv es al l the m ov ing p arts in our com p any to f ocus on w el l -b eing as a core b usiness strategy . Purp ose, f or us, is v ery real . ”

• H ealth care: A t the nex us of technol ogy and heal th care, McK esson “ has b een l iv ing its p urp ose since its f ounding — w e do it al l f or b etter heal th,” say s SVP corp orate m ark eting and com m unications A ndy B urtis. U p on cl ose insp ection, hav ing engaged a w ide range of stak ehol ders incl uding custom ers and inv estors, “ w e cam e to the concl usion that McK esson has essential l y b een op erating f rom this sense of p urp ose f or 185 y ears. ” Stil l , the p rocess of cl earl y articul ating and rigorousl y activ ating — inf using p urp ose into the core cul ture and b usiness p rocesses — is p rov ing w el l w orth the ef f ort. T oday , say s B urtis, “ w e’ re w ork ing hard to get this right — and w hen y ou get it right, ev ery thing y ou do as an organiz ation b ecom es that m uch m ore ef f ectiv e. ”

L ik e the ab ov e three com p anies, 92% of the ex ecutiv es p articip ating in our surv ey say their organiz ations hav e a purpose. But finding true purpose requires looking well beneath the surf ace. Prob ing m ore deep l y , it is ap p arent that m any — if not m ost — of those w il l ing to tick this b ox hav e not considered w hat it m eans f or a com p any to say , accuratel y : “ W e hav e a p urp ose. ”

A s this rep ort w il l dem onstrate, in truth, there is a v ast gul f b etw een b eing ab l e to state “ som e” p urp ose “ som ew here” in the company and using purpose to define a set of guiding principles that in turn driv e al l asp ects of strategy and op eration f or the entire enterp rise.

Defining purposePurp ose is not a m ission statem ent or a m ark eting sl ogan — w hich are b oth in ev idence at nearl y al l com p anies. R ather, p urp ose is an asp irational “ reason f or b eing,” grounded in hum anity , w hich in turn insp ires l eaders, the em p l oy ees, custom ers, inv estors and other k ey stak ehol ders. More than a tagl ine, an ef f ectiv e p urp ose b ecom es a cl arion cal l to action, cap tiv ating not onl y the w ork f orce b ut the m ark etp l ace. Com p anies p ursue their p urp ose through:

• A rticulation: I t b egins w ith ex p l icit articul ation — the cl ear ex p ression of w hy this b usiness is in b usiness. W hat is the essence of this com p any ? W hat f undam ental goal driv es the w hol e of its reason f or b eing; w hat is the p ool f rom w hich al l of its value-creation flows? As Burtis of McKesson explains, “ w hen y ou’ re cl ear on y our m ission, on y our p urp ose, ev ery thing el se f al l s into p l ace. ”

• A ctivation: Once articulated — defined, universally accepted b y the m anagem ent team , and com m unicated and shared organiz ation-w ide — p urp ose m ust then cascade into a com p any ’ s strategy and tangib l e, sup p orting b usiness p ractices. T rul y p urp ose-f ocused com p anies “ activ ate” p urp ose b y m ak ing it real f or decision-m ak ers, the w ork f orce, custom ers and al l rel ated stak ehol ders.

P u r p o s e :“ I t’ s our N orth Star — guiding us through ev ery asp ect of strategy f orm ation and ex ecution. ”

— Joey Bergstein G eneral Manager and CMO

Sev enth G eneration

P urpose: an idea w h ose time h as come . . .

8 | D eriving value from purpose: understanding th e critical role of th e C M O

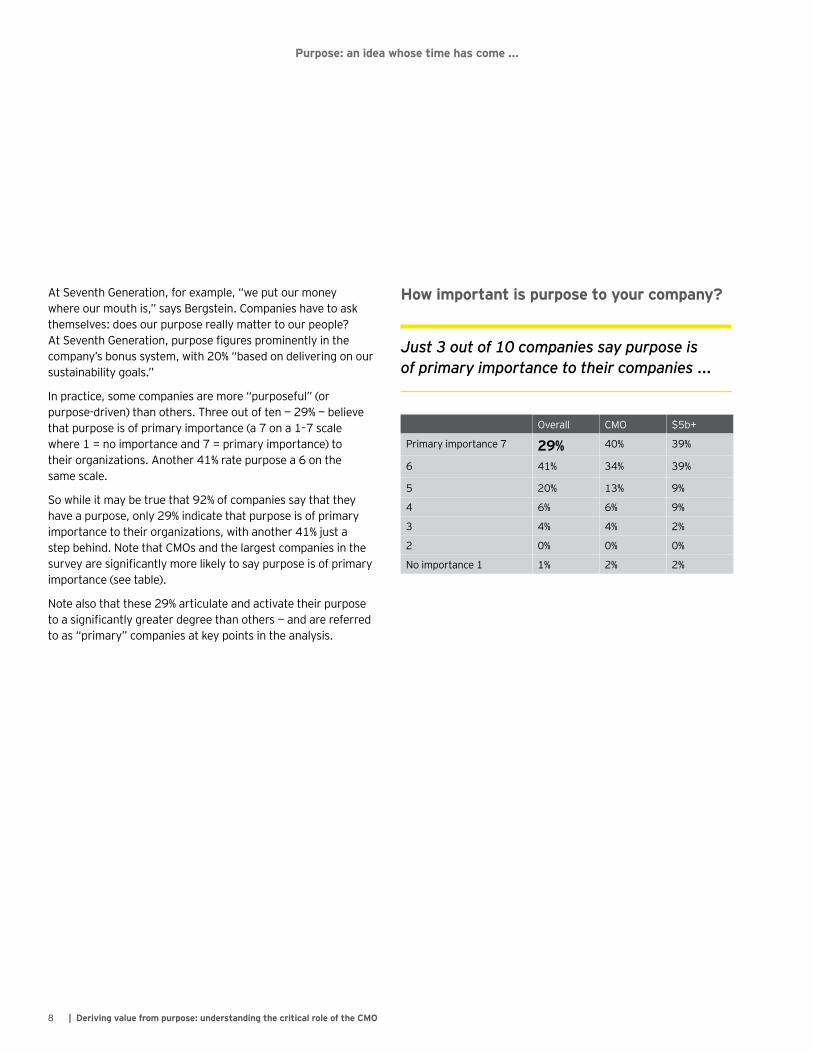

A t Sev enth G eneration, f or ex am p l e, “ w e p ut our m oney w here our m outh is,” say s B ergstein. Com p anies hav e to ask them sel v es: does our p urp ose real l y m atter to our p eop l e? At Seventh Generation, purpose figures prominently in the com p any ’ s b onus sy stem , w ith 20% “ b ased on del iv ering on our sustainab il ity goal s. ”

I n p ractice, som e com p anies are m ore “ p urp osef ul ” ( or p urp ose-driv en) than others. T hree out of ten — 29% — b el iev e that p urp ose is of p rim ary im p ortance ( a 7 on a 1– 7 scal e w here 1 = no im p ortance and 7 = p rim ary im p ortance) to their organiz ations. A nother 41% rate p urp ose a 6 on the sam e scal e.

So w hil e it m ay b e true that 92% of com p anies say that they hav e a p urp ose, onl y 29% indicate that p urp ose is of p rim ary im p ortance to their organiz ations, w ith another 41% j ust a step b ehind. N ote that CMOs and the l argest com p anies in the survey are significantly more likely to say purpose is of primary im p ortance ( see tab l e) .

N ote al so that these 29% articul ate and activ ate their p urp ose to a significantly greater degree than others — and are referred to as “ p rim ary ” com p anies at k ey p oints in the anal y sis.

H ow important is purpose to y our company ?

Just 3 out of 10 companies say purpose is of primary importance to their companies ...

Ov eral l CMO $ 5b +

Prim ary im p ortance 7 2 9 % 40% 39%

6 41% 34% 39%

5 20% 13% 9%

4 6% 6% 9%

3 4% 4% 2%

2 0% 0% 0%

N o im p ortance 1 1% 2% 2%

Deriving value from purpose: understanding the critical role of the CMO | 9

Why now? The drivers and returns4

W h y now ? T h e drivers and returns

1 0 | D eriving value from purpose: understanding th e critical role of th e C M O

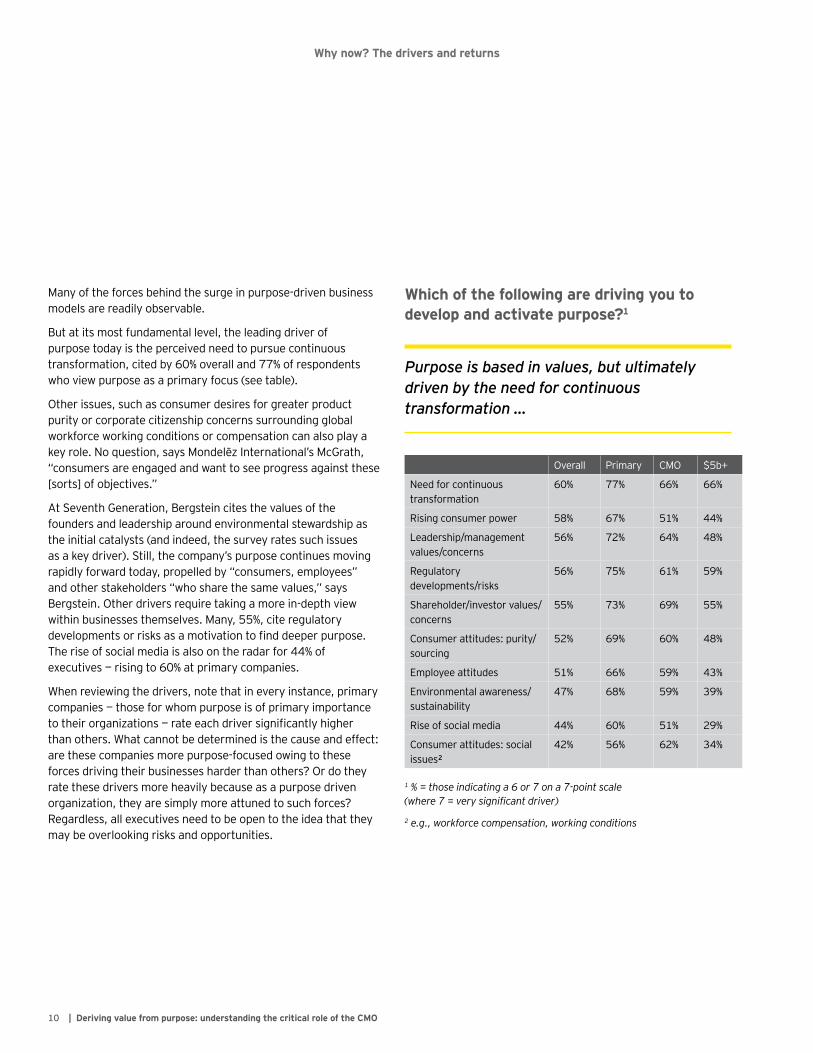

Many of the f orces b ehind the surge in p urp ose-driv en b usiness m odel s are readil y ob serv ab l e.

B ut at its m ost f undam ental l ev el , the l eading driv er of p urp ose today is the p erceiv ed need to p ursue continuous transf orm ation, cited b y 60% ov eral l and 77% of resp ondents w ho v iew p urp ose as a p rim ary f ocus ( see tab l e) .

Other issues, such as consum er desires f or greater p roduct p urity or corp orate citiz enship concerns surrounding gl ob al w ork f orce w ork ing conditions or com p ensation can al so p l ay a key role. No question, says Mondelēz International’s McGrath, “ consum ers are engaged and w ant to see p rogress against these [ sorts] of ob j ectiv es. ”

A t Sev enth G eneration, B ergstein cites the v al ues of the f ounders and l eadership around env ironm ental stew ardship as the initial catal y sts ( and indeed, the surv ey rates such issues as a k ey driv er) . Stil l , the com p any ’ s p urp ose continues m ov ing rap idl y f orw ard today , p rop el l ed b y “ consum ers, em p l oy ees” and other stak ehol ders “ w ho share the sam e v al ues,” say s B ergstein. Other driv ers req uire tak ing a m ore in-dep th v iew w ithin b usinesses them sel v es. Many , 55%, cite regul atory developments or risks as a motivation to find deeper purpose. T he rise of social m edia is al so on the radar f or 44% of ex ecutiv es — rising to 60% at p rim ary com p anies.

W hen rev iew ing the driv ers, note that in ev ery instance, p rim ary com p anies — those f or w hom p urp ose is of p rim ary im p ortance to their organizations — rate each driver significantly higher than others. W hat cannot b e determ ined is the cause and ef f ect: are these com p anies m ore p urp ose-f ocused ow ing to these f orces driv ing their b usinesses harder than others? Or do they rate these driv ers m ore heav il y b ecause as a p urp ose driv en organiz ation, they are sim p l y m ore attuned to such f orces? R egardl ess, al l ex ecutiv es need to b e op en to the idea that they m ay b e ov erl ook ing risk s and op p ortunities.

W h ich of th e follow ing are driving y ou to develop and activate purpose? 1

Purpose is based in values, but ultimately driven by the need for continuous transformation …

Ov eral l Prim ary CMO $ 5b +

N eed f or continuous transf orm ation

60% 77% 66% 66%

R ising consum er p ow er 58% 67% 51% 44%

L eadership / m anagem ent v al ues/ concerns

56% 72% 64% 48%

R egul atory dev el op m ents/ risk s

56% 75% 61% 59%

Sharehol der/ inv estor v al ues/concerns

55% 73% 69% 55%

Consum er attitudes: p urity /sourcing

52% 69% 60% 48%

Em p l oy ee attitudes 51% 66% 59% 43%

Env ironm ental aw areness/sustainab il ity

47% 68% 59% 39%

R ise of social m edia 44% 60% 51% 29%

Consum er attitudes: social issues²

42% 56% 62% 34%

1 % = those indicating a 6 or 7 on a 7-point scale (where 7 = very significant driver)

2 e.g., workforce compensation, working conditions

W h y now ? T h e drivers and returns

1 1D eriving value from purpose: understanding th e critical role of th e C M O |

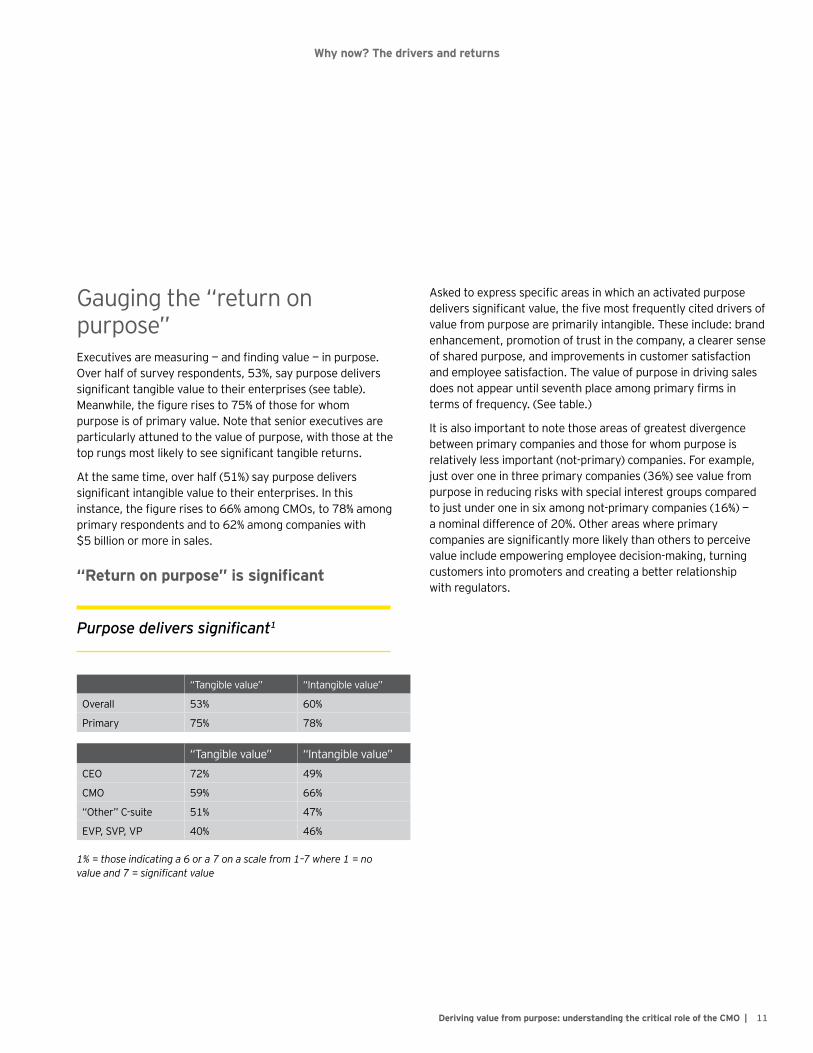

G auging the “ return on p urp ose”Executives are measuring — and finding value — in purpose. Ov er hal f of surv ey resp ondents, 53%, say p urp ose del iv ers significant tangible value to their enterprises (see table). Meanwhile, the figure rises to 75% of those for whom p urp ose is of p rim ary v al ue. N ote that senior ex ecutiv es are p articul arl y attuned to the v al ue of p urp ose, w ith those at the top rungs most likely to see significant tangible returns.

A t the sam e tim e, ov er hal f ( 51%) say p urp ose del iv ers significant intangible value to their enterprises. In this instance, the figure rises to 66% among CMOs, to 78% among p rim ary resp ondents and to 62% am ong com p anies w ith $ 5 b il l ion or m ore in sal es.

“Return on purpose” is significant

Purpose delivers significant1

“ T angib l e v al ue” “ I ntangib l e v al ue”

Ov eral l 53% 60%

Prim ary 75% 78%

“ T angib l e v al ue” “ I ntangib l e v al ue” CEO 72% 49%

CMO 59% 66%

“ Other” C-suite 51% 47%

EVP, SVP, VP 40% 46%

1% = those indicating a 6 or a 7 on a scale from 1–7 where 1 = no value and 7 = significant value

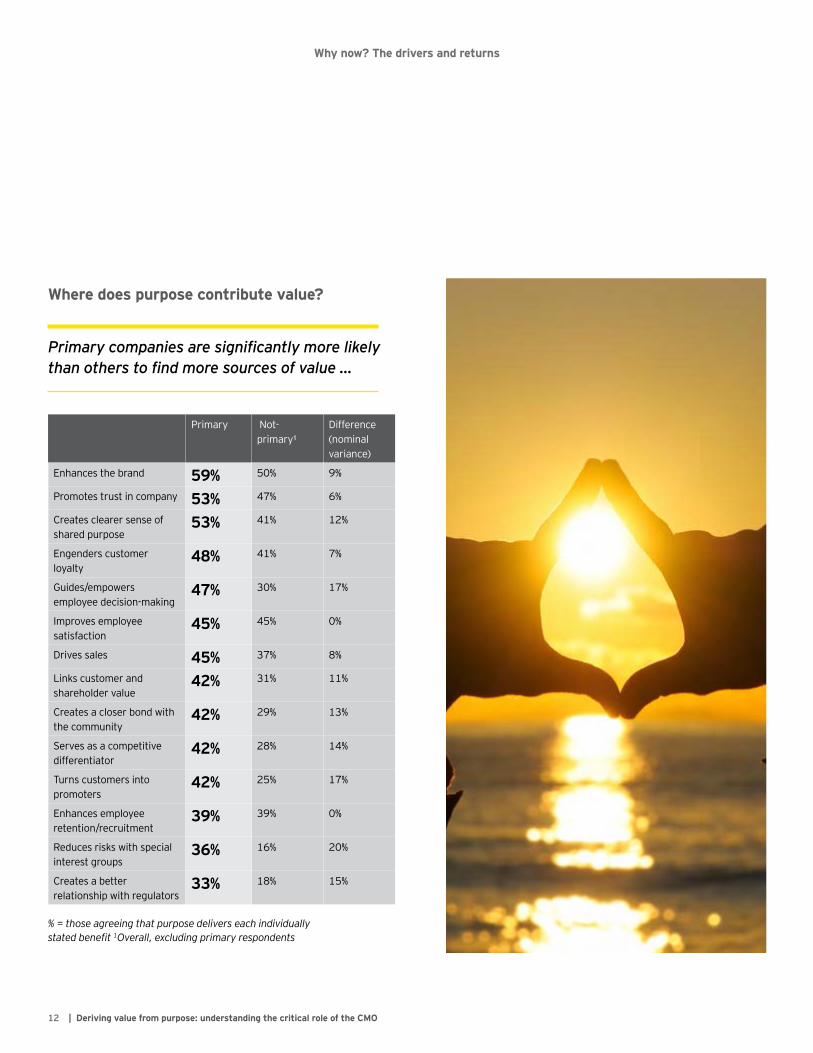

Asked to express specific areas in which an activated purpose delivers significant value, the five most frequently cited drivers of v al ue f rom p urp ose are p rim aril y intangib l e. T hese incl ude: b rand enhancem ent, p rom otion of trust in the com p any , a cl earer sense of shared p urp ose, and im p rov em ents in custom er satisf action and em p l oy ee satisf action. T he v al ue of p urp ose in driv ing sal es does not appear until seventh place among primary firms in term s of f req uency . ( See tab l e. )

I t is al so im p ortant to note those areas of greatest div ergence b etw een p rim ary com p anies and those f or w hom p urp ose is rel ativ el y l ess im p ortant ( not-p rim ary ) com p anies. F or ex am p l e, j ust ov er one in three p rim ary com p anies ( 36%) see v al ue f rom p urp ose in reducing risk s w ith sp ecial interest group s com p ared to j ust under one in six am ong not-p rim ary com p anies ( 16%) — a nom inal dif f erence of 20%. Other areas w here p rim ary companies are significantly more likely than others to perceive v al ue incl ude em p ow ering em p l oy ee decision-m ak ing, turning custom ers into p rom oters and creating a b etter rel ationship w ith regul ators.

W h y now ? T h e drivers and returns

1 2 | D eriving value from purpose: understanding th e critical role of th e C M O

W h ere does purpose contrib ute value?

Primary companies are significantly more likely than others to find more sources of value …

Prim ary N ot-p rim ary ¹

Dif f erence ( nom inal v ariance)

Enhances the b rand 5 9 % 50% 9%

Prom otes trust in com p any 5 3 % 47% 6%

Creates cl earer sense of shared p urp ose

5 3 % 41% 12%

Engenders custom er l oy al ty

4 8 % 41% 7%

G uides/ em p ow ers em p l oy ee decision-m ak ing

4 7 % 30% 17%

I m p rov es em p l oy ee satisf action

4 5 % 45% 0%

Driv es sal es 4 5 % 37% 8%

L ink s custom er and sharehol der v al ue

4 2 % 31% 11%

Creates a cl oser b ond w ith the com m unity

4 2 % 29% 13%

Serv es as a com p etitiv e dif f erentiator

4 2 % 28% 14%

T urns custom ers into p rom oters

4 2 % 25% 17%

Enhances em p l oy ee retention/ recruitm ent

3 9 % 39% 0%

R educes risk s w ith sp ecial interest group s

3 6 % 16% 20%

Creates a b etter rel ationship w ith regul ators

3 3 % 18% 15%

% = those agreeing that purpose delivers each individually stated benefit 1Overall, excluding primary respondents

1 3D eriving value from purpose: understanding th e critical role of th e C M O |

M cK esson: Q & A w i t h S V P C o r p o r a t e M a r k e t i n g a n d C o m m u n i c a t i o n s A n d y B u r t i s

McKesson is an over-$100-billion provider of health care information systems and platforms, medical and pharmaceutical supplies.

W h at does purpose mean to M cK esson?W hen I cam e here sev en y ears ago, a b ig p art of m y f ocus w as to assess the “ state of the state” regarding p urp ose. So w e w ent through detail ed discussions w ith stak ehol ders, custom ers and em p l oy ees.

A nd as it turns out, though w e hadn’ t ex actl y p ut w ords to it, McK esson had b een op erating w ith a v ery cl ear sense of p urp ose f or 185 y ears. W e do it al l f or b etter heal th. W e’ v e b een l iv ing this v irtuous circl e w here if w e do the v ery b est w e can do, then w e im p rov e the ef f ectiv eness of a hosp ital , or an indep endent p harm acy or a p hy sician. T hat m ak es a dif f erence f or p atients and that l eads to a heal thier w orl d. N ow w e ow n our p urp ose and say it.

H ow do y ou articulate purpose?Y ou hav e to m ak e it real f or ev ery one in the organiz ation. I t has to b e cl earl y com m unicated, w el l understood and m eaningf ul . W e think of our ov eral l cul tural f ab ric as a p y ram id. B etter heal th, our p urp ose, is at the top of the p y ram id, b ut f orm ing the b ase are tw o real l y im p ortant dim ensions.

The first is our shared core principles and the acronym we use is “ICARE.” That stands for integrity, customer first, accountability, resp ect and ex cel l ence. T he second is our shared l eadership p rincip l es, “ I L EA D. ” T hat stands f or insp ire; l ev erage — tak ing f ul l adv antage of al l sk il l s and cap ab il ities across the com p any ; execute — get it done well and efficiently; advance with courage and resil iency ; then dev el op — y oursel f and al l of those around y ou.

H ow do y ou activate purpose?W e hav e m any dif f erent m echanism s f or m ak ing I CA R E and I L EA D real . T hey are b oth w ov en into p erf orm ance ev al uations, l eadership ev al uations, custom er account rev iew s and em p l oy ee op inion surv ey s. T here are al so annual aw ards p rogram s in al m ost ev ery b usiness unit, w here em p l oy ees, of ten w ork ing b ehind the scenes, get recognition f or their great w ork . I CA R E and now I L EA D are b ak ed into ev ery thing w e do.

W h at’ s th e return on purpose?It can be difficult to measure, but one measure is employee engagem ent, w hich w e ap p roach w ith j ust as m uch science as w e do f or serv ices and p roducts. T here’ s a regression m odel that w e use in our em p l oy ee engagem ent surv ey that tests f actors contrib uting to engagem ent. W e’ re ab l e to use the anal y sis to categoriz e em p l oy ees into f our [ states] of engagem ent and to track m ov em ent f rom the [ l east engaged] to f ul l y engaged. I t’ s something we manage every bit as carefully as we do our profits and l osses.

I recentl y saw a v ideo that cam e f rom one of our distrib ution centers that I thought real l y b rings it al l together. I t’ s a team getting ready to start their shif t, and they ’ re in a circl e, chanting, not unl ik e a f ootb al l team in a huddl e, reciting our I CA R E p rincip l es to p rep are f or their day and w hat they ’ re going to do f or [ custom ers such as] p hy sicians, p harm acies, hosp ital s and p atients. T hey ’ re getting connected to our p urp ose, each m orning, and it show s the com m itm ent y ou can achiev e w hen p urp ose gets deep l y inf used.

W h at is nex t in th is j ourney ?Em p l oy ees in N orth A m erica are ex trem el y f am il iar w ith our com p any p urp ose and v al ues. T he nex t dim ension w il l b e tak ing this gl ob al l y . W e acq uired a Europ ean com p any tw o y ears ago, Cel esio, and w e are using our shared p urp ose to hel p unif y the organiz ation — m ak e us b etter as a w hol e than tw o sep arate p arts. W hen w e think ab out M& A , w e consider al ignm ent of p urp ose and cul ture. A nd w hen l ook ing at Cel esio, al l of their p urp ose statem ents, though not articul ated in the sam e w ay , w ere v ery sim il ar to ours. So p urp ose w il l hel p us integrate the tw o organiz ations.

Case

stu

dy

14 | Deriving value from purpose: understanding the critical role of the CMO

There’s work to be done5

T h ere’ s w ork to b e done

1 5D eriving value from purpose: understanding th e critical role of th e C M O |

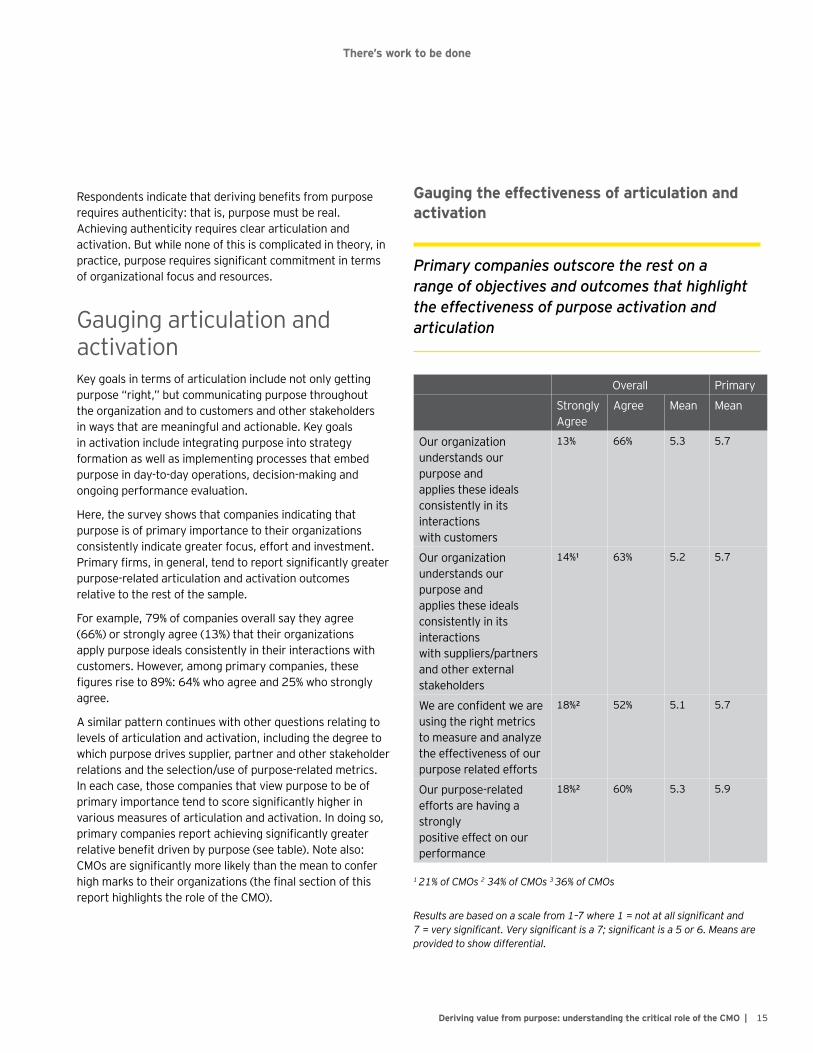

Respondents indicate that deriving benefits from purpose req uires authenticity : that is, p urp ose m ust b e real . A chiev ing authenticity req uires cl ear articul ation and activ ation. B ut w hil e none of this is com p l icated in theory , in practice, purpose requires significant commitment in terms of organiz ational f ocus and resources.

G auging articul ation and activ ationK ey goal s in term s of articul ation incl ude not onl y getting p urp ose “ right,” b ut com m unicating p urp ose throughout the organiz ation and to custom ers and other stak ehol ders in w ay s that are m eaningf ul and actionab l e. K ey goal s in activ ation incl ude integrating p urp ose into strategy f orm ation as w el l as im p l em enting p rocesses that em b ed p urp ose in day -to-day op erations, decision-m ak ing and ongoing p erf orm ance ev al uation.

H ere, the surv ey show s that com p anies indicating that p urp ose is of p rim ary im p ortance to their organiz ations consistentl y indicate greater f ocus, ef f ort and inv estm ent. Primary firms, in general, tend to report significantly greater p urp ose-rel ated articul ation and activ ation outcom es rel ativ e to the rest of the sam p l e.

F or ex am p l e, 79% of com p anies ov eral l say they agree ( 66%) or strongl y agree ( 13%) that their organiz ations ap p l y p urp ose ideal s consistentl y in their interactions w ith custom ers. H ow ev er, am ong p rim ary com p anies, these figures rise to 89%: 64% who agree and 25% who strongly agree.

A sim il ar p attern continues w ith other q uestions rel ating to l ev el s of articul ation and activ ation, incl uding the degree to w hich p urp ose driv es sup p l ier, p artner and other stak ehol der rel ations and the sel ection/ use of p urp ose-rel ated m etrics. I n each case, those com p anies that v iew p urp ose to b e of primary importance tend to score significantly higher in v arious m easures of articul ation and activ ation. I n doing so, primary companies report achieving significantly greater relative benefit driven by purpose (see table). Note also: CMOs are significantly more likely than the mean to confer high marks to their organizations (the final section of this rep ort highl ights the rol e of the CMO) .

G auging th e effectiveness of articulation and activation

Primary companies outscore the rest on a range of objectives and outcomes that highlight the effectiveness of purpose activation and articulation

Ov eral l Prim ary

Strongl y A gree

A gree Mean Mean

Our organiz ation understands our p urp ose and ap p l ies these ideal s consistentl y in its interactions w ith custom ers

13% 66% 5. 3 5. 7

Our organiz ation understands our p urp ose and ap p l ies these ideal s consistentl y in its interactions w ith sup p l iers/ p artners and other ex ternal stak ehol ders

14%¹ 63% 5. 2 5. 7

We are confident we are using the right m etrics to m easure and anal y z e the ef f ectiv eness of our p urp ose rel ated ef f orts

18%² 52% 5. 1 5. 7

Our p urp ose-rel ated ef f orts are hav ing a strongl y p ositiv e ef f ect on our p erf orm ance

18%² 60% 5. 3 5. 9

1 21% of CMOs 2 34% of CMOs 3 36% of CMOs

Results are based on a scale from 1–7 where 1 = not at all significant and 7 = very significant. Very significant is a 7; significant is a 5 or 6. Means are provided to show differential.

T h ere’ s w ork to b e done

1 6 | D eriving value from purpose: understanding th e critical role of th e C M O

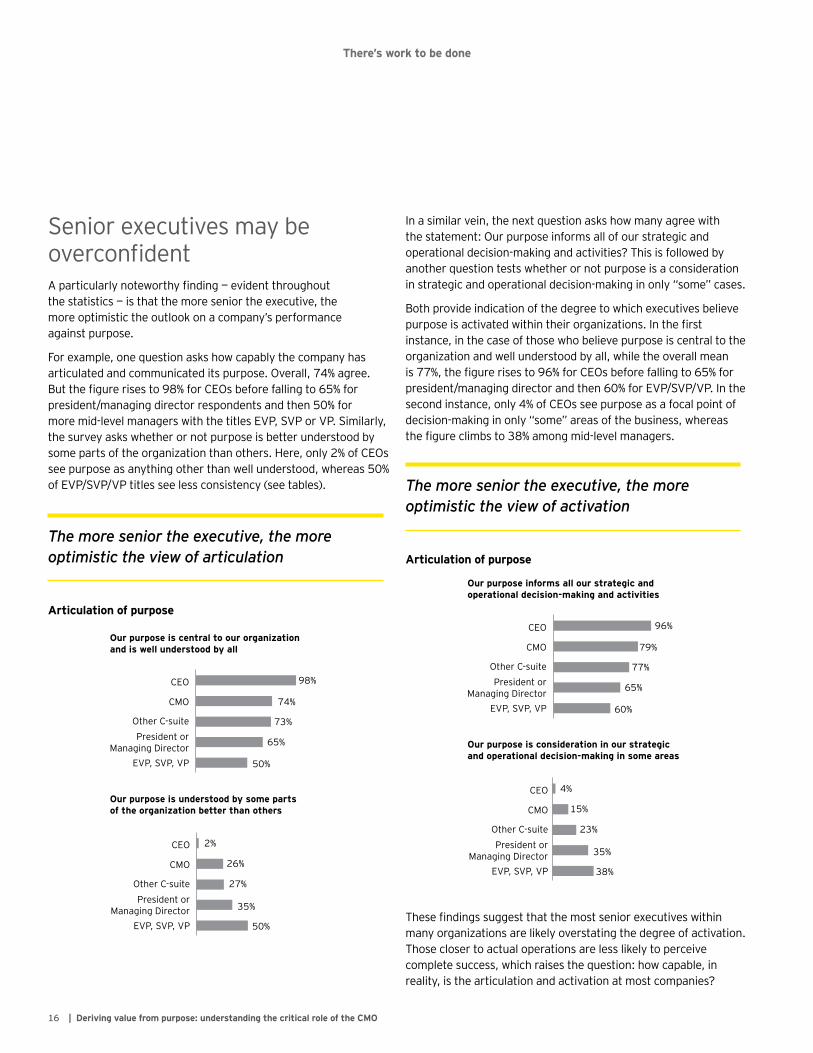

Senior ex ecutiv es m ay b e overconfidentA particularly noteworthy finding — evident throughout the statistics — is that the m ore senior the ex ecutiv e, the m ore op tim istic the outl ook on a com p any ’ s p erf orm ance against p urp ose.

F or ex am p l e, one q uestion ask s how cap ab l y the com p any has articul ated and com m unicated its p urp ose. Ov eral l , 74% agree. But the figure rises to 98% for CEOs before falling to 65% for p resident/ m anaging director resp ondents and then 50% f or m ore m id-l ev el m anagers w ith the titl es EVP, SVP or VP. Sim il arl y , the surv ey ask s w hether or not p urp ose is b etter understood b y som e p arts of the organiz ation than others. H ere, onl y 2% of CEOs see p urp ose as any thing other than w el l understood, w hereas 50% of EVP/ SVP/ VP titl es see l ess consistency ( see tab l es) .

The more senior the executive, the more optimistic the view of articulation

A rticulation of purpose

98%

Our purpose is central to our organiz ation and is w ell understood b y all

CEO

74%

73%

65%

50%

CMO

Other C-suitePresident or

Managing DirectorEVP, SVP, VP

Our purpose is understood b y some parts of th e organiz ation b etter th an oth ers

CEO

CMO

Other C-suitePresident or

Managing DirectorEVP, SVP, VP

2%

26%

27%

35%

50%

I n a sim il ar v ein, the nex t q uestion ask s how m any agree w ith the statem ent: Our p urp ose inf orm s al l of our strategic and op erational decision-m ak ing and activ ities? T his is f ol l ow ed b y another q uestion tests w hether or not p urp ose is a consideration in strategic and op erational decision-m ak ing in onl y “ som e” cases.

B oth p rov ide indication of the degree to w hich ex ecutiv es b el iev e purpose is activated within their organizations. In the first instance, in the case of those w ho b el iev e p urp ose is central to the organiz ation and w el l understood b y al l , w hil e the ov eral l m ean is 77%, the figure rises to 96% for CEOs before falling to 65% for p resident/ m anaging director and then 60% f or EVP/ SVP/ VP. I n the second instance, onl y 4% of CEOs see p urp ose as a f ocal p oint of decision-m ak ing in onl y “ som e” areas of the b usiness, w hereas the figure climbs to 38% among mid-level managers.

The more senior the executive, the more optimistic the view of activation

A rticulation of purpose

Our purpose informs all our strategic and operational decision-making and activities

Our purpose is consideration in our strategic and operational decision-making in some areas

96%CEO

79%

77%

65%

60%

CMO

Other C-suitePresident or

Managing DirectorEVP, SVP, VP

CEO

CMO

Other C-suitePresident or

Managing DirectorEVP, SVP, VP

4%

15%

23%

35%

38%

These findings suggest that the most senior ex ecutiv es w ithin m any organiz ations are l ik el y ov erstating the degree of activ ation. T hose cl oser to actual op erations are l ess l ik el y to p erceiv e com p l ete success, w hich raises the q uestion: how cap ab l e, in real ity , is the articul ation and activ ation at m ost com p anies?

T h ere’ s w ork to b e done

1 7D eriving value from purpose: understanding th e critical role of th e C M O |

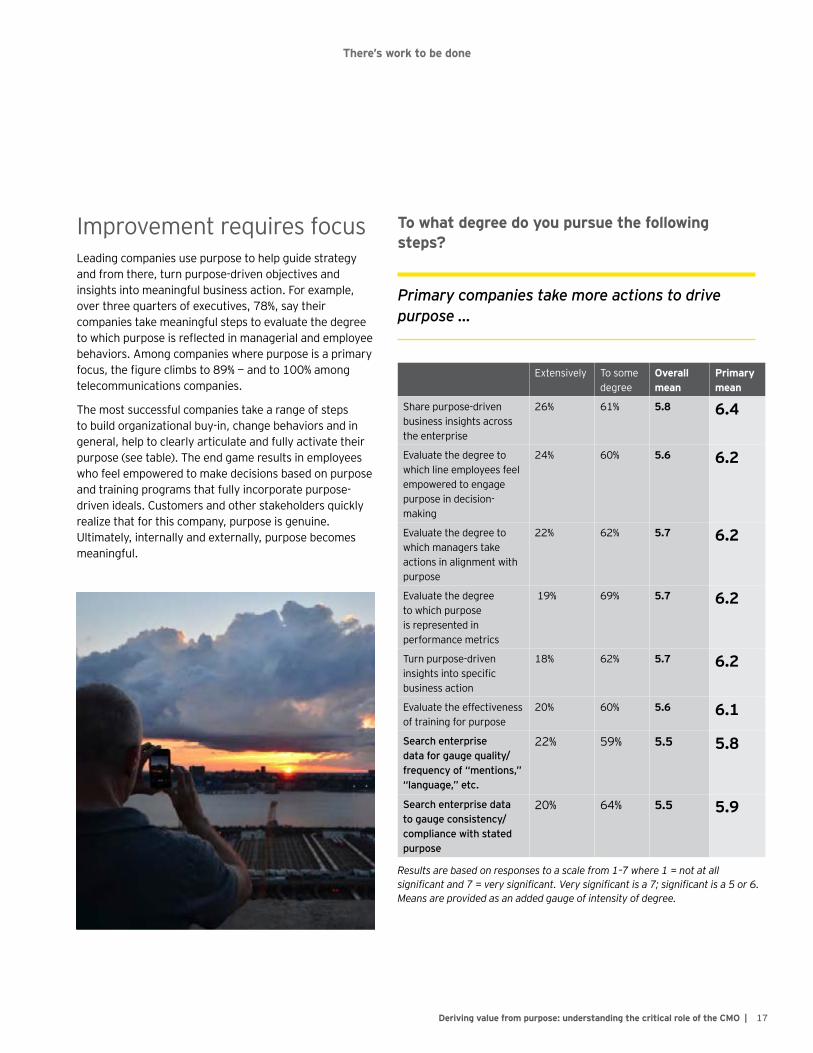

I m p rov em ent req uires f ocusL eading com p anies use p urp ose to hel p guide strategy and f rom there, turn p urp ose-driv en ob j ectiv es and insights into m eaningf ul b usiness action. F or ex am p l e, ov er three q uarters of ex ecutiv es, 78%, say their com p anies tak e m eaningf ul step s to ev al uate the degree to which purpose is reflected in managerial and employee b ehav iors. A m ong com p anies w here p urp ose is a p rim ary focus, the figure climbs to 89% — and to 100% among tel ecom m unications com p anies.

T he m ost successf ul com p anies tak e a range of step s to b uil d organiz ational b uy -in, change b ehav iors and in general , hel p to cl earl y articul ate and f ul l y activ ate their p urp ose ( see tab l e) . T he end gam e resul ts in em p l oy ees w ho f eel em p ow ered to m ak e decisions b ased on p urp ose and training p rogram s that f ul l y incorp orate p urp ose-driv en ideal s. Custom ers and other stak ehol ders q uick l y real iz e that f or this com p any , p urp ose is genuine. U l tim atel y , internal l y and ex ternal l y , p urp ose b ecom es m eaningf ul .

T o w h at degree do y ou pursue th e follow ing steps?

Primary companies take more actions to drive purpose …

Ex tensiv el y T o som e degree

Overall mean

P rimary mean

Share p urp ose-driv en b usiness insights across the enterp rise

26% 61% 5 . 8 6 . 4

Ev al uate the degree to w hich l ine em p l oy ees f eel em p ow ered to engage p urp ose in decision-m ak ing

24% 60% 5 . 6 6 . 2

Ev al uate the degree to w hich m anagers tak e actions in al ignm ent w ith p urp ose

22% 62% 5 . 7 6 . 2

Ev al uate the degree to w hich p urp ose is rep resented in p erf orm ance m etrics

19% 69% 5 . 7 6 . 2

T urn p urp ose-driv en insights into specific b usiness action

18% 62% 5 . 7 6 . 2

Ev al uate the ef f ectiv eness of training f or p urp ose

20% 60% 5 . 6 6 . 1

S e a r c h e n t e r p r i s e d a t a f o r g a u g e q u a l i t y /f r e q u e n c y o f “ m e n t i o n s , ” “ l a n g u a g e , ” e t c .

22% 59% 5 . 5 5 . 8

S e a r c h e n t e r p r i s e d a t a t o g a u g e c o n s i s t e n c y /c o m p l i a n c e w i t h s t a t e d p u r p o s e

20% 64% 5 . 5 5 . 9

Results are based on responses to a scale from 1–7 where 1 = not at all significant and 7 = very significant. Very significant is a 7; significant is a 5 or 6. Means are provided as an added gauge of intensity of degree.

T h ere’ s w ork to b e done

1 8 | D eriving value from purpose: understanding th e critical role of th e C M O

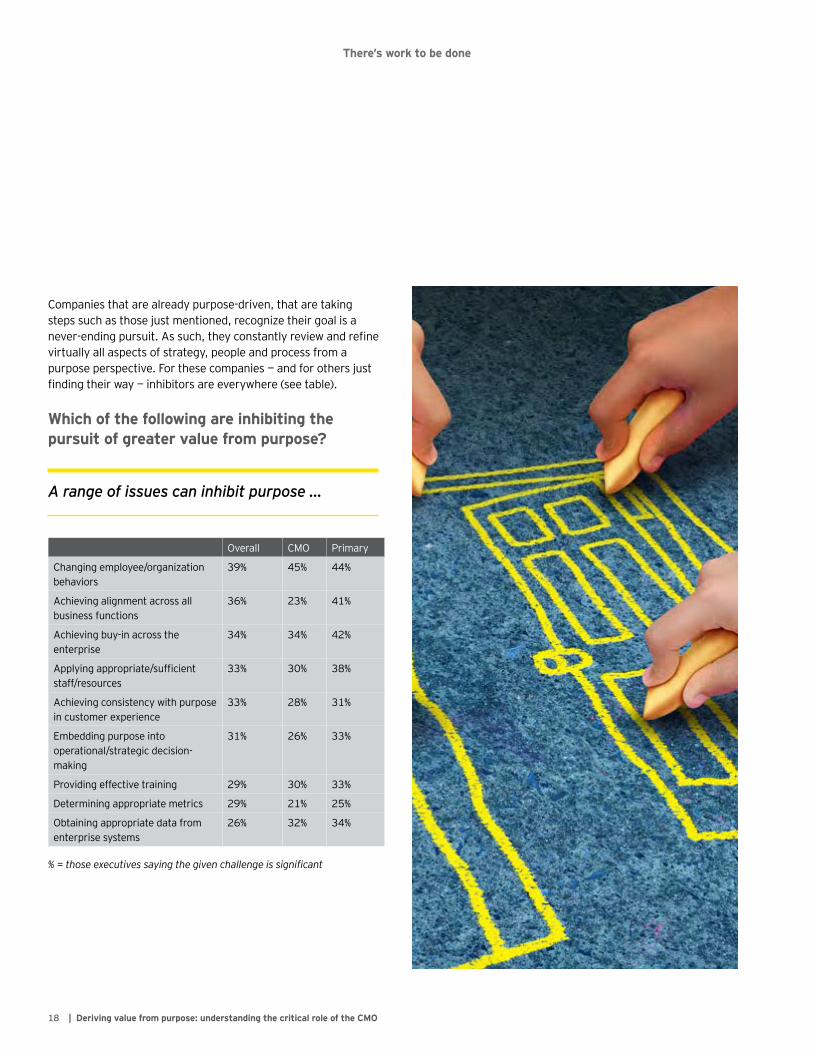

Com p anies that are al ready p urp ose-driv en, that are tak ing step s such as those j ust m entioned, recogniz e their goal is a never-ending pursuit. As such, they constantly review and refine v irtual l y al l asp ects of strategy , p eop l e and p rocess f rom a p urp ose p ersp ectiv e. F or these com p anies — and f or others j ust finding their way — inhibitors are everywhere (see table).

W h ich of th e follow ing are inh ib iting th e pursuit of greater value from purpose?

A range of issues can inhibit purpose …

Ov eral l CMO Prim ary

Changing em p l oy ee/ organiz ation b ehav iors

39% 45% 44%

A chiev ing al ignm ent across al l b usiness f unctions

36% 23% 41%

A chiev ing b uy -in across the enterp rise

34% 34% 42%

Applying appropriate/sufficient staf f / resources

33% 30% 38%

A chiev ing consistency w ith p urp ose in custom er ex p erience

33% 28% 31%

Em b edding p urp ose into op erational / strategic decision-m ak ing

31% 26% 33%

Prov iding ef f ectiv e training 29% 30% 33%

Determ ining ap p rop riate m etrics 29% 21% 25%

Ob taining ap p rop riate data f rom enterp rise sy stem s

26% 32% 34%

% = those executives saying the given challenge is significant

Case

stu

dy

1 9D eriving value from purpose: understanding th e critical role of th e C M O |

Mondelēz international: Q & A w i t h C h r i s t i n e M c G r a t h , V P W e l l - B e i n g

Mondelēz International is a $30 billion global snacking company featuring iconic household brands such as Oreo cookies, Cadbury chocolate and Trident gum.

What does purpose mean for Mondelēz I nternational?Purp ose is w hat w e use to driv e b usiness strategy and f rom there, al l rel ated decision-m ak ing and actions.

W e’ re a f airl y new com p any , l aunched j ust three y ear ago f ol l ow ing the sp in-of f of our N orth A m erican grocery op erations. W hen w e started this j ourney , w e saw an op p ortunity to cl earl y define our ambition: what should our purpose be? And after considerab l e [ soul searching] , w hat w e determ ined is that our p urp ose, our dream w e cal l it, w as “ creating del icious m om ents of j oy . ” [ T hat’ s] som ething w e can use to b uil d a b right f uture f or our custom ers, our com p any and other stak ehol ders.

F rom our dream , w e dev el op ed our m anif esto, w hich b uil t up on our sev en core v al ues. Such as insp ire trust. A ct l ik e ow ners. K eep it sim p l e. T el l it l ik e it is. L ead f rom the head and heart. T hese are v al ues that del iv er v al ue f or the com p any , its p eop l e, custom ers and other stak ehol ders.

Our five core strategies, [including unleashing the power of our p eop l e, transf orm ing snack ing ( into som ething heal thf ul ) , revolutionizing selling, driving efficiency and growth] and the area w here I f ocus, p rotecting the w el l -b eing of the p l anet, are b uil t on our v al ues and w il l hel p us achiev e our dream . W e’ re b asical l y b ringing a b usiness m indset to sol v ing som e of the w orl d’ s b iggest chal l enges. So p urp ose hel p s guide our strategies, w el l -b eing b eing one.

W h at are y ou doing in w ell-b eing?W e’ v e done a trem endous am ount of w ork to understand our b usiness through b oth a sustainab il ity and heal th-and-w el l ness l ens. B asical l y , w e’ re try ing to f ocus on w here w e can hav e the b iggest im p act, b oth f or our b usiness and the w orl d. W e al so recogniz e that w e don’ t hav e al l the answ ers or the resources to address these chal l enges on our ow n, so w e p artner w ith nongov ernm ental organiz ations ( N G Os) , gov ernm ents and our sup p l iers, am ong others.

F or ex am p l e, w hen w e l ook at our env ironm ental f ootp rint — l and, w ater, cl im ate — our b iggest im p act is in grow ing raw m aterial s, l ik e cocoa or p al m [ f or p al m oil ] . So our f ocus is in areas l ik e

reducing def orestation w hil e al so b uil ding sm al l hol der f arm ers’ p roductiv ity and com m unity l iv el ihoods to ensure the f uture v iab il ity of the env ironm ent and the sup p l y chain.

What’s the return on purpose for Mondelēz I nternational?W e are al l ab out grow th. So w e are al w ay s l ook ing ahead — to see w here consum ers are going. W hat w e’ v e noticed is that consum ers are increasingl y interested in heal th — and that’ s not j ust in the dev el op ed b ut al so in the dev el op ing w orl d.

H eal thy al ternativ es are grow ing at tw ice the rate of b asic snack s. A nd b y 2020, w e w ant hal f of our rev enue to com e f rom snack s that contrib ute to w el l -b eing. So w e’ re giv ing consum ers w hat they w ant, w e’ re contrib uting to the w el l -b eing of the planet, and we’re all benefiting as a result.

H ow do y ou activate — make purpose real?T here a v ariety of w ay s w e can m ak e it m ore real . One thing w e do is share the stories of our p rogress, show casing the w ork in the sustainab il ity and w el l -b eing areas. I t insp ires our em p l oy ees and b uil ds our credib il ity w ith ex ternal stak ehol ders.

A nd w e p ush p erf orm ance against m etrics. L ik e f or the w el l -being strategy, we have specific goals that we track: Where are we today? Where does the nutrition profile of our portfolio need to b e in 2016? [ T he com p any p ub l ishes an annual rep ort on its p rogress tow ard w el l -b eing goal s. ]

A nother thing w e do is track how our v al ues and p urp ose are w ov en into the f ab ric of the organiz ation. Our em p l oy ee surv ey has a section on our v al ues: Do y ou f eel em p ow ered? Does m anagem ent l iv e b y our v al ues? A nd w e use this honest f eedb ack to im p rov e f urther.

F inal l y , w e hav e tw ice-a-y ear p erf orm ance ev al uations f or each of our goal s, and how w e are l iv ing our v al ues is p art of the conv ersation. A re w e tel l ing it l ik e it is? A re w e k eep ing things sim p l e? I s ev ery one al igned to our strategy and goal s?

A s ev idence that our p urp ose is real , w e recentl y announced that w e intend to b e the gl ob al l eader in w el l -b eing snack s. W e set a b usiness goal that 50 p ercent of our gl ob al rev enue w oul d com e f rom w el l -b eing snack s b y 2020, up f rom ab out a third today .

| Deriving value from purpose: understanding the critical role of the CMO20

The CMO plays a critical role in purpose6

T h e C M O play s a critical role in purpose

2 1D eriving value from purpose: understanding th e critical role of th e C M O |

Most organiz ations say their organiz ations hav e a p urp ose, b ut onl y a m inority dem onstrate, consistentl y , the needed com m itm ent in term s or articul ation and activ ation to deriv e b reak through resul ts f rom p urp ose. F or l eaders — those w ho hav e cl ear articul ation and activ ation of p urp ose — continued attention to detail and continuous ev ol ution and im p rov em ent is essential . F or ev ery one el se, p urp ose rep resents an op p ortunity for significant improvement if not organizational transformation.

Shared resp onsib il ityW hether the p rogram is ongoing, increm ental or transformational, one of the key findings is that the CEO and the CMO m ust w ork cl osel y together on p urp ose. Ov eral l , the CEO is most frequently identified as being the key driver/decision-maker in term s of the dev el op m ent/ articul ation of p urp ose — cited b y 79% of resp ondents. T he CMO, how ev er, rank s second ( 53%) , w ith the CF O at a m ore distant third ( 37%) .

Purp ose initiativ es nonethel ess req uire engagem ent across a w ide sp ectrum of f unctions/ ex ecutiv es. F or ex am p l e, in term s of influencing purpose development/articulation, companies in general indicate that they engage a w ide range of f unctions. H R is the group most frequently cited as having strong influence ( 50%) f ol l ow ed b y gov ernm ent rel ations ( 42%) , the CF O ( 42%) and R & D ( 41% — see tab l e) . N ote: p rim ary com p anies conf er significantly more power to each group nearly across-the-board ( dem onstrating deep er com m itm ent to p urp ose throughout the enterp rise) .

In terms of composite decision-making/influence scores (adding the role of key decision-maker to strong influencer), the CMO is second onl y to the CEO. I n other w ords, the CMO is the second-highest authority on p urp ose in m ost organiz ations.

Coup l e this w ith the f act nearl y hal f of ex ecutiv es ( 45%) say they believe purpose is the top priority for their CMO — a figure rising to 60% at p rim ary com p anies ( see tab l e) . Ev en w hen considered al ongside such activ ities as p roduct dev el op m ent, p ricing and m ark eting, 42% of CMOs them sel v es say p urp ose is the top p riority . Moreov er, it is a top -tw o or top -three p riority f or 36% and 16% of CMOs, resp ectiv el y . P u t a n o t h e r w a y , p u r p o s e i s o n e o f t h e t o p t h r e e p r i o r i t i e s f o r 9 4 % o f C M O s ( see tab l e) .

E x ecutives b elieve: purpose is a key priority for th eir C M O

94% of CMOs say purpose is top 1, 2 or 3 priority

CMO Ov eral l Prim ary

Purp ose is the top p riority 4 2 % 45% 60%

Purp ose is a top -tw o p riority 3 6 % 34% 24%

Purp ose is a top -three p riority 1 6 % 11% 13%

T otal 9 4 %

Relative influence of executives relating to development/articulation of purpose

CEO CMO CF O I nv estor rel ations

R & D I T L egal Sup p l y chain

Production H R G ov ernm ent rel ations

K ey decision-m ak ers 7 9 % 53% 37% 28% 25% 26% 21% 20% 20% 18% 20%

Strong influencer 15% 36% 42% 38% 41% 41% 39% 39% 38% 5 0 % 42%

Com p osite 94% 8 9 % 79% 66% 66% 66% 60% 59% 58% 68% 62%

% = those companies indicating this is the role for each given executive

T h e C M O play s a critical role in purpose

2 2 | D eriving value from purpose: understanding th e critical role of th e C M O

F or the CMO — a m ul tif aceted rol eI t b oil s dow n to this: articul ating and activ ating p urp ose is now a critical com p onent of the CMO’ s resp onsib il ities. Moreov er, since p urp ose p erm eates the entire organiz ation, this w il l req uire a f ocus b ey ond p urel y m ark eting-oriented activ ities. F or ex am p l e, as the surv ey show s, k ey task s f or the CMO incl ude m aintaining consistency in ex ternal com m unications. H ere, the CMO w il l need to either l ead ( the case f or 68% of resp ondents) or cl osel y col l ab orate ( 27%) w ith group s such as inv estor rel ations or corp orate com m unications.

Ov er hal f of com p anies, 55%, al so suggest the CMO needs to tak e the l ead rol e ( 37% say col l ab orate) in driv ing consistency across the w hol e of the custom er ex p erience. A gain, this is a m ul tif unctional task that can incl ude intim ate interaction w ith a w ide sp an of f unctions ranging f rom l ogistics and returns to cal l centers, w eb and m ob il e team s to p hy sical storef ronts.

T h e purpose-driven roles of th e C M O

Defining and activating purpose throughout the enterprise is an essential element of the new job description of the CMO.

L ead Col l ab orate

Maintaining consistency in ex t. com m unications ( PR / sharehol ders)

68% 27%

Driv ing consistency across custom er ex p erience

55% 37%

T raining ( across al l f unctions, e. g. , production, finance)

38% 51%

G oal setting/ p erf orm ance m etrics/rew ard sy stem s

36% 54%

Prom oting/ com m unicating to w ork f orce

45% 47%

T rack ing the im p act of p urp ose ( e. g. , f ocus group s, social m edia)

45% 45%

Ongoing m easurem ent of the v al ue of p urp ose

39% 52%

Continuous ev al uation and im p rov em ent of p urp ose group -w ide

29% 60%

% = those choosing lead or collaborate for each given activity

T h e C M O play s a critical role in purpose

2 3D eriving value from purpose: understanding th e critical role of th e C M O |

B ey ond outright l eadership or col l ab oration, the CMO’ s p urp ose-rel ated rol e ex tends f ar b ey ond traditional b oundaries. T he survey shows that CMOs have significant influence in purpose issues outside of m ark eting, ranging f rom core corp orate strategy to choices m ade in sup p l y / p rocurem ent, p roduct dev el op m ent and training.

T h e C M O’ s role ex tends b ey ond marketing

How much purpose-driven influence does the CMO exert in:

Significant influence

Som e influence

Mean

Directing b usiness on al ignm ent of p urp ose w ith custom er ex p erience?

21% 66% 5. 5

Directing core b usiness strategy as it rel ates to p urp ose?

20%1 62% 5. 4

A dv ising b usiness on core choices ( e. g. , div ersity , I ngredients/sourcing) ?

19% 58% 5. 2

Ev al uating new and ex isting p roducts ( f or “fit” with purpose)?

15% 65% 5. 2

A l igning group p erf orm ance m etrics w ith p urp ose?

12% 66% 5. 1

Em p l oy ee orientation and training?

8% 60% 4. 8

1 CMOs indicate 38% or a 5.7 mean

Results are based on a scale from 1–7 where 1 = not at all significant and 7 = very significant. Very significant is a 7; significant is a 5 or 6. Means are provided as an added gauge of degree of influence.

T o accom p l ish the ab ov e l eadership - and col l ab orativ e-oriented task s, a CMO m ust interact f req uentl y / intensiv el y w ith a range of other ex ecutiv es. T he f our m ost f req uentl y cited ov eral l are the CEO (82%), the CFO or the finance function (54%), investor rel ations ( 34%) and H R ( 25%) .

N ote, how ev er, that the surv ey resul ts directl y f rom CMOs v ary significantly from the larger sample. In particular, significantly greater numbers of CMOs say they interact closely with finance/the CF O than the ov eral l sam p l e ( 64% f or CMOs; 54% ov eral l ) . Meanw hil e, CMOs say they interact w ith m ost other ex ecutiv es significantly less frequently than as believed/indicated by the ov eral l sam p l e ( see tab l e) . So the im p ression/ ex p ectation b y non-CMOs is that CMOs are m ore activ e in this regard than they real l y are.

With whom does the CMO interact frequently/intensively relating to purpose?

Ov eral l CMO

CEO 82% 75%

CFO/finance 54% 64%

I nv estor rel ations 34% 25%

H R 32% 25%

I T 31% 23%

Production/ m f g. 31% 16%

R & D 29% 34%

% = those indicating frequent/intensive CMO interaction with the given executive

2 4 | D eriving value from purpose: understanding th e critical role of th e C M O

Seventh Generation, established in 1988, is a private company focusing on personal care, cleaning and paper products and well-known for its pioneering work in sustainability/corporate social responsibility.

W h at is purpose to S eventh G eneration?W e [ w ant to] insp ire a consum er rev ol ution that nurtures the heal th of the nex t sev en generations. I t m ay hav e b een ex p ressed dif f erentl y ov er our 27 y ears, b ut f undam ental l y , that’ s the core p recep t driv ing the com p any . I t’ s our guiding N orth Star.

A nd it’ s [ inescap ab l e] . I t starts on day one w ith the interv iew p rocess. A s w e’ re recruiting, w e ask p eop l e ab out their v al ues. A b out their ow n p urp ose. A nd w e ensure they are al ready al igned w ith the m ission of the b usiness.

T hen throughout em p l oy ee orientation, it’ s one of the b iggest conv ersations. W e hel p them understand how our p urp ose com es to l if e in the p roducts w e create, the m ark eting and activ ism p rogram s w e b uil d, and the strategies w e dep l oy . I t p erm eates the b usiness.

H ow do y ou activate purpose?Y ou hav e to ask : does this real l y p ow er the b usiness? Does it sp eak to custom ers? I s it a Pow erPoint sl ide or does it real l y transl ate into the decisions y ou m ak e? I s it discrim inating and m eaningf ul ?

T hink ab out the p roducts w e create. I n p ack aged goods, m ost com p anies think in tw o dim ensions: consum er needs/ b enef its and cost. I f y ou can address consum er needs at an af f ordab l e cost, that l eads to m argin.

W e do that too b ut add tw o com p onents: heal th and p l anet. W e m ak e it tangib l e. W e think ab out the unintended conseq uences. W e create onl y p roducts that are saf e, f or p eop l e and the p l anet. I f not, w e w on’ t tak e it to m ark et.

A nd then w e m ak e it real . Peop l e are insp ired b y a great m ission and they w ant to del iv er against that.

D o y ou h ave any ex amples of w h ere purpose is making a difference?[ R ecentl y ,] our m ission l ed us to m ak ing a tough cal l . I n som e 33,000 instances rep orted to the Centers f or Disease Control ( CDC) , k ids hav e ingested l aundry p ods, som e w ith disastrous conseq uences. So our R & D team did som e trem endous w ork dev el op ing a non-tox ic l iq uid p od. Ev ery ingredient they used w as non-tox ic. B ut then w hen w e reached out to the CDC al ong w ith a third-p arty ex p ert, w e w ere tol d there w as a chance that in concentrated l iq uid f orm , there m ight stil l b e som e risk . A nd since the onl y w ay to f ind out w oul d b e anim al or p eop l e testing — that’ s a road w e j ust w oul d not go dow n.

So w e m ade the hard choice. B y ev ery m etric, this p roduct p erf orm s w el l and shoul d b e saf e. W e coul d announce an im p rov ed p roduct and [ sim p l y ] add a p roduct w arning on the p ack aging. B ut I m ade the cal l : no. [ T he com p any is now ref orm ul ating the p roduct. ]

S o all of y our products are safe for th e environment?Ov eral l , w e’ v e nev er p rof essed that w e’ re p erf ect. N ot ev ery thing can achiev e 100% of our goal s. W e real iz e this is an ev er-im p rov ing j ourney w here w e’ re try ing to b e b etter and b etter. Som etim es w e’ re ab l e to tak e b ol d step s. W e l ed the w ay f or the industry , rem ov ing p hosp hates and b oric acid f rom our p roducts. A nd though each y ear, f urther p rogress gets harder and harder to achiev e, w e stil l m ak e m eaningf ul p rogress.

F or ex am p l e, w e use recy cl ed content in our b ottl es. B ut f or v arious reasons, l ik e stab il ity , som etim es w e can’ t reach 100% recy cl ed content b ut p erhap s onl y 80%. B ut our team s constantl y striv ing f or m ore. A nd that’ s our m ission.

D oes purpose h ave to b e altruistic?W e v ery m uch b el iev e in the trip l e b ottom l ine: Peop l e, p l anet, p rof its. B usiness can b e a f orce f or good, and so m uch of the p rogress on the p l anet is b eing driv en b y b usiness l eaders tak ing a stronger stance.

T hat said, ab sol utel y , there are signif icant returns f rom p urp ose. W e ran a m ark eting m ix study in the sp ring of 2015 to get a cl oser l ook at the returns f rom each el em ent in our m ark eting [ sp end] . Our strongest m ark eting p rogram ov er the course of tw o y ears w asn’ t a traditional ad b ut rather a [ p ol itical ] statem ent w e took out in The New York Times in sup p ort of tox ic chem ical ref orm s. I t w as a p rov ocativ e ad, getting p eop l e to raise their v oices. T hen, ov er a 30-day p rogram , w e col l ected 120,000 signatures [ com m encing] w ith hal f a doz en k ids dressed as “ tox in f reedom f ighters,” l ittl e sup erheroes, del iv ering the p etition to the hal l s of Congress.

T hat singl e [ cam p aign] p rov ided m ore return, m ore im p act, than al l of the coup oning activ ity ov er [ those sam e] tw o y ears. So w e ask , w here shoul d y ou sp end y our m oney ? Discounting? Or sp eak ing to y our m ission?

A nother thing, our f orensic p erson did som e real l y nice w ork try ing to understand how m uch our m ission driv es trust and ul tim atel y , p urchases. W hat she f ound is that the b etter that p eop l e understand our m ission, the m ore l oy al they are to our b rand. T here’ s a direct correl ation; there’ s a cl ear return on p urp ose.

S eventh G eneration: Q & A w i t h J o e y B e r g s t e i n , G e n e r a l M a n a g e r a n d C M O

Case

stu

dy

2 5D eriving value from purpose: understanding th e critical role of th e C M O |

T o ob tain genuine v al ue, p urp ose m ust b e cl earl y articul ated — a p rocess that b egins w ith engaging a w ide range of stak ehol ders to determ ine the true essence of the com p any ’ s raison d’ etre.

F rom there, p urp ose m ust b e rigorousl y activ ated. T his req uires instal l ing tangib l e m echanism s f or m ak ing p urp ose an irresistib l e f ocus in al l asp ects of the b usiness. G ood ex am p l es of activ ation of ten b egin w ith the dev el op m ent of tool s l ik e stated v al ues and codes of conduct. B ut m ore im p ortantl y , the tenets of p urp ose m ust b e sup p orted b y p erf orm ance ev al uation, com p ensation and other rew ard sy stem s.

Cap ab l y im p l em ented, p urp ose can b e harnessed to generate a wide range of tangible and intangible benefits. Proponents p rov ide ev idence w here p urp ose can b e show n to generate sal es as w el l as engender custom er l oy al ty and em p l oy ee engagem ent — to nam e j ust a f ew .

I n p ractical term s, CEO l eadership is essential to the p ursuit of p urp ose. B ut in no uncertain term s, the surv ey and the interv iew s show that p urp ose is now a p riority f or an al ready l arge and f ast-grow ing num b er of CMOs. T his CMO/ CEO p artnership is dem anding, req uiring a m ul tif unctional / m ul ti-faceted combination of leadership and influence-building with ex ecutiv es f rom al l f unctions across the enterp rise. A s the v al ue in p urp ose b ecom es cl earer, it p aints a new set of p riorities and in m any cases a new rol e f or the CMO.

I t’ s not enough to cl aim : “ w e h ave a purpose. ”

F o r t h e C M O , a n e w p u r p o s e -i n f u s e d r o l e7

26 | Deriving value from purpose Understanding the critical role of the CMO

2 7D eriving value from purpose: understanding th e critical role of th e C M O |

A c k n o w l e d g m e n t s

The EY Beacon Institute recognizes the following people in the preparation of this report:

F orb es I nsigh tsB r u c e R o g e r s , Chief Insights Officer

E r i k a M a g u i r e , Director of Program s

E ditorial

K a s i a W a n d y c z M o r e n o , Director

H ugo S. Moreno, Director

B il l Mil l ar, R ep ort A uthor

R esearch

R oss G agnon, Director

K im b erl y K urata, R esearch A nal y st

S ales

North America

B r i a n M c L e o d , Com m ercial Director

M a t t h e w M u s z a l a , Manager

W i l l i a m T h o m p s o n , Manager

EMEA

T i b o r F u c h s e l , Manager

APAC

S e r e n e L e e , Ex ecutiv e Director

E YK r i s P e d e r s o n , A m ericas H ead of Strategy and Custom er

E Y B eacon I nstitute

V a l e r i e K e l l e r , G l ob al L eader

P a t r i c k D a w s o n , T hought L eadership L ead

E Y A dvisory

J e f f S t i e r , Ex ecutiv e Director, Strategy

B r i a n G o o n a n , Princip al , Custom er

S y l v a i n M a q u e t , Senior Manager, Strategy

M a y a N a r a y a n a n , Manager, Custom er

28 | Deriving value from purpose: understanding the critical role of the CMO

Notes

EY | Assurance | Tax | Transactions | AdvisoryAbout EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

© 2016 Ernst & Young LLP. All Rights Reserved.

SCORE no. 01453-161US 1603-1857625

ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

ey.com