derivatives │ cfa level i derivatives i problem solving session harvard extension school mgmt...

Post on 20-Dec-2015

232 views

TRANSCRIPT

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I

Derivatives I Problem Solving Session

Harvard Extension SchoolMGMT E-2900b

CFA Exam Level IApril 20, 2010

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I

Jeffery LippensLecturer

Tray SpilkerTeaching Assistant

Derivatives I Problem Solving Session

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Derivatives

Topic Area Weights for the CFA ExamTopic Area Level I

Ethical and Professional Standards (total) 15 Quantitative Methods 12 Economics 10 Financial Reporting and Analysis 20 Corporate Finance 8 Investment Tools (total) 50 Equity Investments 10 Fixed Income 12 Derivatives 5 Alternative Investments 3 Asset Classes (total) 30 Portfolio Management and Wealth Planning (total) 5

Total 100

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I

Introduction to Derivative Markets & Instruments

Options Markets, Puts & Calls, & Put-Call Parity

Risk Management Applications of Option Strategies

Derivates I Problem Solving Session

Study Session 17Readings 67,70 & 72

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

1. A derivative security is:

A. a financial asset that bears no risk.B. a financial asset that offers a return

based on the return of another asset or security.

C. a financial asset with no maturity.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

1. A derivative security is:

A. a financial asset that bears no risk.B. a financial asset that offers a return

based on the return of another asset or security.

C. a financial asset with no maturity.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

2. Exchange-traded derivatives:

A. are standardized and backed by a clearinghouse.

B. are largely unregulated and backed by a dealer counterparty.

C. include forwards and swaps.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

2. Exchange-traded derivatives:

A. are standardized and backed by a clearinghouse.

B. are largely unregulated and backed by a dealer counterparty.

C. include forwards and swaps.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

3. A customized, or bespoke, agreement to sell 37,500 pounds of coffee in one month is an example of:

A. a futures contract.B. a swaption.C. a forward commitment.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

3. A customized, or bespoke, agreement to sell 37,500 pounds of coffee in one month is an example of:

A. a futures contract.B. a swaption.C. a forward commitment.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

4. A futures contract is most likely:

A. adjusted daily to account for profits and losses.

B. a contingent claim.C. traded over-the-counter (OTC).

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

4. A futures contract is most likely:

A. adjusted daily to account for profits and losses.

B. a contingent claim.C. traded over-the-counter (OTC).

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

5. A swap is least likely:

A. the exchange of one asset for another.B. a series of options contracts.C. traded over-the-counter (OTC).

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

5. A swap is least likely:

A. the exchange of one asset for another.B. a series of options contracts.C. traded over-the-counter (OTC).

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

6. The right but not the obligation to sell an asset at a particular price in the future is an example of:

A. a short futures position.B. a call option.C. a put option.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

6. The right but not the obligation to sell an asset at a particular price in the future is an example of:

A. a short futures position.B. a call option.C. a put option.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

7. Which of the following could be considered benefits of derivatives: they (1) provide price information, (2) allow investors to manage risk, (3) provide access to leverage, and (4) reduce transactions costs?

A. 2 & 4B. 1, 2, & 4C. All of the above

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

7. Which of the following could be considered benefits of derivatives: they (1) provide price information, (2) allow investors to manage risk, (3) provide access to leverage, and (4) reduce transactions costs?

A. 2 & 4B. 1, 2, & 4C. All of the above

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

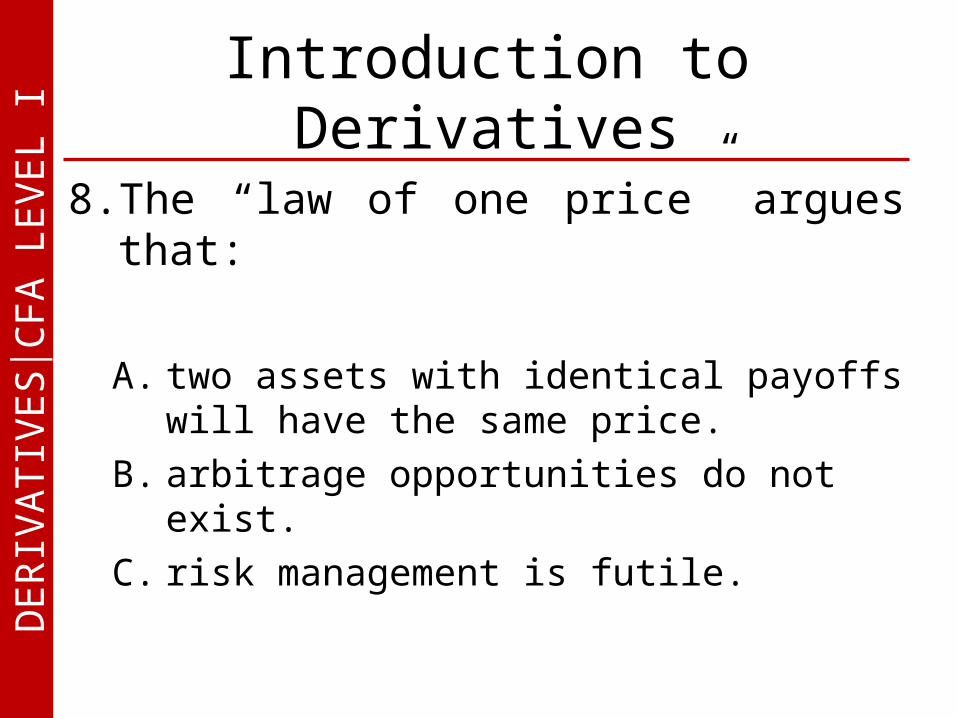

8. The “law of one price” argues that:

A. two assets with identical payoffs will have the same price.

B. arbitrage opportunities do not exist.C. risk management is futile.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

8. The “law of one price” argues that:

A. two assets with identical payoffs will have the same price.

B. arbitrage opportunities do not exist.C. risk management is futile.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Introduction to Derivatives

8. Explained: Arbitrage is the process of creating

“risk-less” profit when assets with identical payoffs become mispriced; buy the lower priced asset and sell (short) the higher priced asset. The Law of One Price enforces this relationship.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts9. Which of the following is in the

money?

A. a put option with S > XB. a call option with S – X > 0C. a put option with S – X > 0

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts9. Which of the following is in the

money?

A. a put option with S > XB. a call option with S – X > 0C. a put option with S – X > 0

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts10.Which of the following is not in the

money?

A. a put option with X – S < 0B. a put option with S < XC. a call option with S – X > 0

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts10.Which of the following is not in the

money?

A. a put option with X – S < 0B. a put option with S < XC. a call option with S – X > 0

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts11.Contrary to European options,

American options:

A. cannot be exercised prior to maturity.B. will always vary in price against a

European option due to exchange rate risk.

C. may have a higher value versus a similar European option.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts11.Contrary to European options,

American options:

A. cannot be exercised prior to maturity.B. will always vary in price against a

European option due to exchange rate risk.

C. may have a higher value versus a similar European option.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts11.Explained:

An American option gives the option holder the right to exercise the option prior to expiration

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts12.Which of the following about puts

and calls is most accurate?

A. Option prices are positively correlated to the time to maturity.

B. The price of the underlying security will exhibit more volatility than the option.

C. An increase in market interest rates will increase the value of a call and decrease the value of a put.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts12.Which of the following about puts

and calls is most accurate?

A. Option prices are positively correlated to the time to maturity.

B. The price of the underlying security will exhibit more volatility than the option.

C. An increase in market interest rates will increase the value of a call and decrease the value of a put.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts12. Five inputs to options prices:

S = price of underlying stockX = exercise price of the optionT = time to expirationRf = risk-free rateV = volatility of underlying stock price Positive Correlation:

Calls S, T, Rf, & V Puts X, T, & V

12.Negative Correlation:Calls X

Puts S & Rf

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts12.Explained (cont)

C = S + P – X / (1+Rf)T

P = C – S + X / (1 + Rf)T

As Rf ↑ X / (1 + Rf )T ↓ Call ↑ Put ↓

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts13.Which of the following is least

accurate?

A. The holder of a put has the right to sell to the writer of the option.

B. The writer of a call has the obligation to buy to the holder of the option.

C. The holder of a call has the right to buy from the writer of the option.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts13.Which of the following is least

accurate?

A. The holder of a put has the right to sell to the writer of the option.

B. The writer of a call has the obligation to buy to the holder of the option.

C. The holder of a call has the right to buy from the writer of the option.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts13.Explained:

Writer: has the obligation to buy from a put holder and sell to a call holder.

Holder: has the right, but not the obligation, to buy when holding a call, or sell when holding a put.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

ContractsQuestion 14 – 16: Consider a call option with a strike of

$42.50, priced at $10, when the underlying stock trades at $50

14. What is the time value of the call?

A. $7.50B. $5.00C. $2.50

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

ContractsConsider a call option with a strike of $42.50, priced at $10, when the underlying stock trades at $50

14. What is the time value of the call?

A. $7.50B. $5.00C. $2.50

Intrinsic Value = S – X = $50 - $42.50 = $7.50

Time Value = $10 - $7.50 = $2.50

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

ContractsQuestion 14 – 16: Consider a call option with a strike of

$42.50, priced at $10, when the underlying stock trades at $50

15. What is the lower bound of the call price?

A. $7.50B. $5.00C. $2.50

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

ContractsQuestion 14 – 16: Consider a call option with a strike of

$42.50, priced at $10, when the underlying stock trades at $50

15. What is the lower bound of the call price?

A. $7.50B. $5.00C. $2.50

Lower Bound of a Call: Ct = max [0, St – X] = max [0, $50 – $42.50]= $7.50

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

ContractsQuestion 14 – 16: Consider a call option with a strike of

$42.50, priced at $10, when the underlying stock trades at $50

16. What is the upper bound of the call price?

A. $10.00B. $50.00C. $42.50

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

ContractsQuestion 14 – 16: Consider a call option with a strike of

$42.50, priced at $10, when the underlying stock trades at $50

16. What is the upper bound of the call price?

A. $10.00B. $50.00C. $42.50

Upper Bound of a Call: Ct ≤ St

Why pay more for the right to buy an asset than the asset is worth?

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts16.What is the lower bound of a

European put option with a strike of $50, when the underlying stock trades at $40, the risk-free rate is 2%, and there is 3 months to maturity?

A. $10.00B. $9.75C. $9.02

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts16.What is the lower bound of a

European put option with a strike of $50, when the underlying stock trades at $40, the risk-free rate is 2%, and there is 3 months to maturity?

A. $10.00B. $9.75C. $9.02

Max [0, X / (1+Rf)T – S]Max [0, 50/(1.02)(.25) – 40Max [0, 9.75] = $9.75

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts17.What is the lower bound of an

American call option on non-dividend paying stocks?

A. Max [0, X – S]B. Max [0, X/(1+Rf)T – S]

C. Max [0, S – X/(1+Rf)T]

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts17.What is the lower bound of an

American call option on non-dividend paying stocks?

A. Max [0, X – S]B. Max [0, X/(1+Rf)T – S]

C. Max [0, S – X/(1+Rf)T]

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts17.Explained: C = Max [0, X – S] c = Max [0, s – x/(1+rf)T] Because the American option has

greater properties than the European option, S – X/(1+Rf)T] must also be the lower bound for an American call option

Thus, C = Max [0, S – X/(1+Rf)T]

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

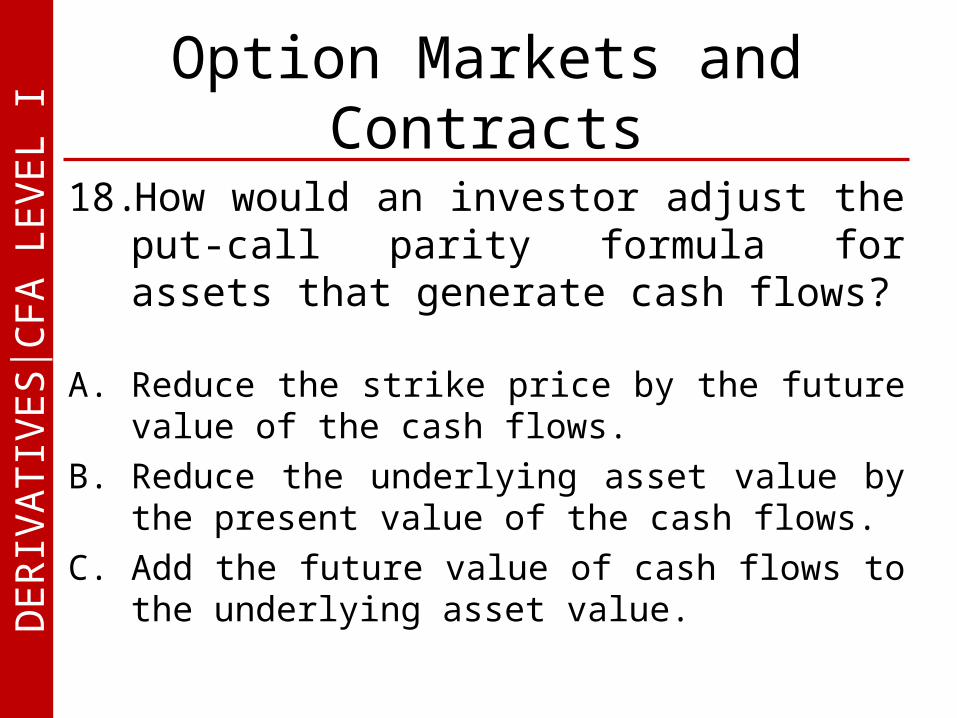

Contracts18.How would an investor adjust the

put-call parity formula for assets that generate cash flows?

A. Reduce the strike price by the future value of the cash flows.

B. Reduce the underlying asset value by the present value of the cash flows.

C. Add the future value of cash flows to the underlying asset value.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts18.How would an investor adjust the

put-call parity formula for assets that generate cash flows?

A. Reduce the strike price by the future value of the cash flows.

B. Reduce the underlying asset value by the present value of the cash flows.

C. Add the future value of cash flows to the underlying asset value.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts19.A forward rate agreement, has the

same payoff as:

A. A long position in an interest rate call option

B. A short position in an interest rate put option

C. A long position in an interest rate call and a short position in an interest rate put option

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts19.A forward rate agreement, has the

same payoff as:

A. A long position in an interest rate call option

B. A short position in an interest rate put option

C. A long position in an interest rate call and a short position in an interest rate put option

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts19.Explained: Assume Libor = 6%,

Fixed = 5% Long call payoff: float–fixed;

Max[0, 6% - 5%] = 1% Short put payoff: fixed–float;

-(Max[0, 6% - 5%]) = 0% FRA payoff: pay fixed, receive float;

= -5% + 6% = 1% = long call + short put = 1%

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts20.From the issuers perspective, an

interest rate floor on a FRN is equivalent to a series of:

A. Short interest rate putsB. Long interest rate putsC. Short interest rate calls

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts20.From the issuers perspective, an

interest rate floor on a FRN is equivalent to a series of:

A. Short interest rate putsB. Long interest rate putsC. Short interest rate calls

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts20.Explained: When market rates falls below the

strike at expiration, the FRN issuers will pay the difference to the put purchaser.

Why would a FRN issuer write an interest rate put option? Don’t they want rates to fall?

To fund an interest rate call purchase / cap; create a collar

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts21.Which of the following relationships

is inaccurate?

A. C = S + P – X / (1+Rf)T

B. P = C – S – X / (1+Rf)T

C. X / (1+Rf)T – P = S – C

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts21.Which of the following relationships

is inaccurate?

A. C = S + P – X / (1+Rf)T

B. P = C – S – X / (1+Rf)T

C. X / (1+Rf)T – P = S – C

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts22.Which of the following will decrease

the value of a put option?

A. A decrease in volatilityB. A decrease in Rf

C. An increase in X

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts22.Which of the following will decrease

the value of a put option?

A. A decrease in volatilityB. A decrease in Rf

C. An increase in X

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts22.Explained: Positive Correlation:

Calls S, T, Rf, & V

Puts X, T, & V Negative Correlation:

Calls X Puts S & Rf

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts23.A put and call option of $40 with 3-

months to maturity is trading at $10 and $2 respectively. The underlying stock is selling at $30 and the risk-free rate is 5%. How much can be made through arbitrage?

A. $0B. $2.36C. $0.24

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts23.A put and call option of $40 with 3-

months to maturity is trading at $10 and $2 respectively. The underlying stock is selling at $30 and the risk-free rate is 5%. How much can be made through arbitrage?

A. $0B. $2.36C. $0.24

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Option Markets and

Contracts23.Explained: Synthetic Stock: S = C – P + X /

(1+Rf)T

$40 = $2 – $10 + $30/(1.05).25

$40 > $37.64

Thus, sell the stock and buy the synthetic for an immediate arbitrage profit of $2.36

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

Applications24.Which of the following poses the

highest risk?

A. Long CallB. Short CallC. Short Put

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

Applications24.Which of the following poses the

highest risk?

A. Long CallB. Short CallC. Short Put

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

Applications24.Explained:

Buying a put or a call exposes you only to the premium.

When writing a put, your loss is limited by the lower bound of a stock price (0) minus the premium you received.

When writing a call, however, your loss potential is unbounded as stock prices can go up infinitely.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

Applications25. A put option with a strike of $25 sells for

$4 while the underlying stock trades at $30. If the option were exercised, which of the following is most accurate?

A. The put writer loses $1 on the transaction.

B. The put buyer loses $4 on the transaction.

C. The put writer gains $5 on the transaction.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

Applications25. A put option with a strike of $25 sells for

$4 while the underlying stock trades at $30. If the option were exercised, which of the following is most accurate?

A. The put writer loses $1 on the transaction.

B. The put buyer loses $4 on the transaction.

C. The put writer gains $1 on the transaction.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

Applications25.Explained:

A. Put Buyer Payoff: Max[0, X-S] – Premium Paid = Max[0, 25-30] – 4 = -$4

B. Put Writer Payoff: Min[0,X-S] + Premium Received = -(Max[0, 25-30]) + 4 = $4

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

Applications26. A call option with a strike of $25 sells for

$4 while the underlying stock trades at $30. If the option were exercised, which of the following is most accurate?

A. The call buyer gains $5 on the transaction.

B. The call writer gains $5 on the transaction.

C. The call writer loses $1 on the transaction.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

Applications26. A call option with a strike of $25 sells for

$4 while the underlying stock trades at $30. If the option were exercised, which of the following is most accurate?

A. The call buyer gains $5 on the transaction.

B. The call writer gains $5 on the transaction.

C. The call writer loses $1 on the transaction.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

Applications26.Explained:

Call Buyer Payoff: Max[0, S-X] – Premium Paid = Max[0, 30-25] – 4 = $1 Call Writer Payoff:

-(Max[0,S-X]) + Premium Received =

-(Max[0, 30-25]) + 4 = -$1

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

ApplicationsQuestion 27 – 28:An investor is long 100 shares of Pfizer

stock at $15. The investor writes one call contract (100 multiplier) at a strike of $25 for $1.

27.What is the maximum result possible for the investor?

A. A gain of $100B. A gain of $1,100C. Unlimited Loss

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

ApplicationsQuestion 27 – 28:An investor is long 100 shares of Pfizer

stock at $15. The investor writes one call contract (100 multiplier) at a strike of $25 for $1.

27.What is the maximum result possible for the investor?

A. A gain of $100B. A gain of $1,100C. Unlimited Loss

100[($25 - $15) + $1] = $1,100

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

ApplicationsQuestion 27 – 28:An investor is long 100 shares of Pfizer

stock at $15. The investor writes one call contract (100 multiplier) at a strike of $25 for $1.

28.What will be the payoff if the stock increases to $30?

A. A gain of $600B. A loss of $400C. A gain of $100

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

ApplicationsQuestion 27 – 28:An investor is long 100 shares of Pfizer

stock at $15. The investor writes one call contract (100 multiplier) at a strike of $25 for $1.

28.What will be the payoff if the stock increases to $30?

A. A gain of $600B. A loss of $400C. A gain of $100

100[($25 - $30) + $1] = $400

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

ApplicationsQuestion 29 – 30:An investor is long 100 shares of Pfizer

stock at $15. The investor buys one put contract (100 multiplier) at a strike of $5 for $1.

29.What is the minimum result possible for the investor?

A. Unlimited GainB. Loss of $600C. Loss of $1,100

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

ApplicationsQuestion 29 – 30:An investor is long 100 shares of Pfizer

stock at $15. The investor buys one put contract (100 multiplier) at a strike of $5 for $1.

29.What is the minimum result possible for the investor?

A. Unlimited GainB. Loss of $600C. Loss of $1,100

100[($5 - $15) - $1] = -$1,100

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

ApplicationsQuestion 29 – 30:An investor is long 100 shares of Pfizer

stock at $15. The investor buys one put contract (100 multiplier) at a strike of $5 for $1.

30.What will be the payoff if the stock increases to $30?

A. Gain of $1,400B. Gain of $1,500C. Gain of $1,100

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

ApplicationsQuestion 29 – 30:An investor is long 100 shares of Pfizer

stock at $15. The investor buys one put contract (100 multiplier) at a strike of $5 for $1.

30.What will be the payoff if the stock increases to $30?

A. Gain of $1,400B. Gain of $1,500C. Gain of $1,100

100[($30 - $15) - $1] = -$1,400

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

Applications31.Which of the following combination

of options and underlying assets have similar payoff diagrams?

A. Long call combined with a short put vs. a long stock.

B. Covered call vs. a protective put.C. Short put and long call vs. a

protective put

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

Applications31.Which of the following combination

of options and underlying assets have similar payoff diagrams?

A. Long call combined with a short put vs. a long stock.

B. Covered call vs. a protective put.C. Short put and long call vs. a

protective put

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

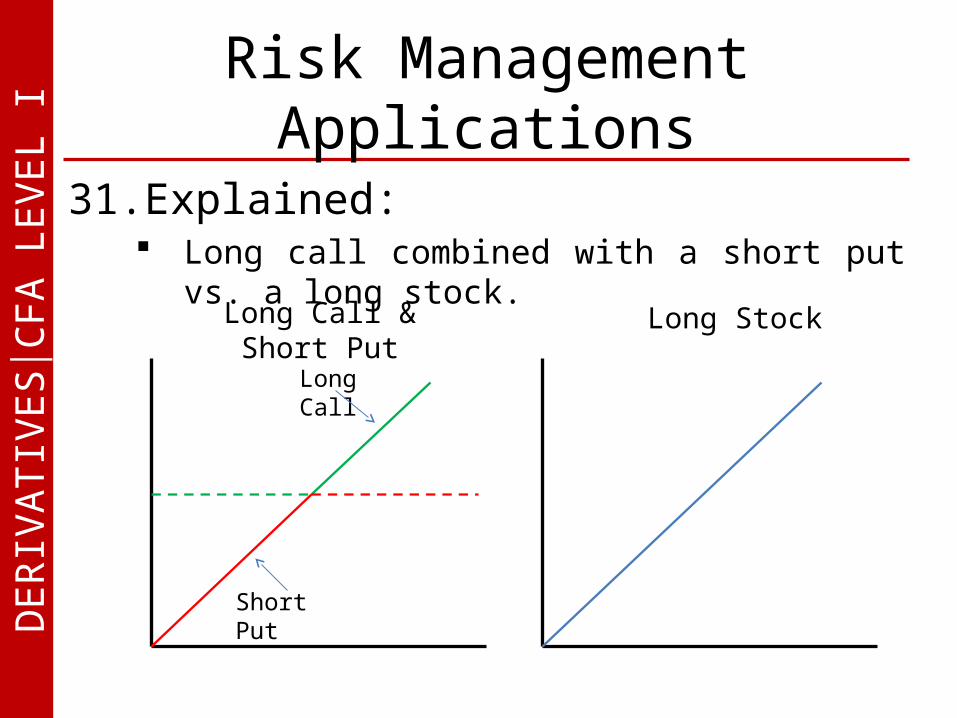

Applications31.Explained:

Long call combined with a short put vs. a long stock.Long Call & Short

PutLong Stock

Long Call

Short Put

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

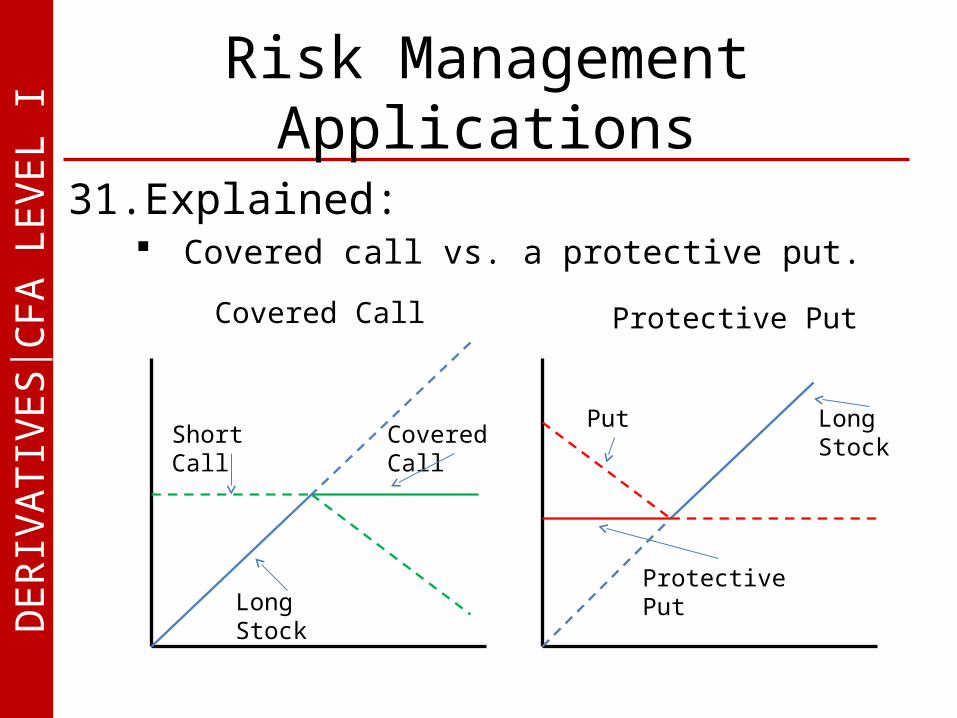

Applications31.Explained:

Covered call vs. a protective put.

Covered Call Protective Put

Short Call

Long Stock

Long Stock

Put

Protective Put

Covered Call

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Risk Management

Applications31.Explained:

Short put and long call vs. a protective put

Protective Put

Long Stock

Put

Protective Put

Long Call & Short PutLong Call

Short Put

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I

Ethics & Professional Standards

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Ethics & Professional

StandardsWhich of the following statements clearly conflicts with the recommended procedures for compliance presented in the CFA Institute Standards of Practice Handbook?

A. Firms should disclose to clients the personal investing policies and procedures established for their employees.

B. For confidentiality reasons, personal transactions and holdings should not be reported to employers unless mandated by regulatory organizations.

C. Personal transactions should be defined as including transactions in securities owned by the employee and members of his or her immediate family and transactions involving securities in which the employee has a beneficial interest.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Ethics & Professional

StandardsWhich of the following statements clearly conflicts with the recommended procedures for compliance presented in the CFA Institute Standards of Practice Handbook?

A. Firms should disclose to clients the personal investing policies and procedures established for their employees.

B. For confidentiality reasons, personal transactions and holdings should not be reported to employers unless mandated by regulatory organizations.

C. Personal transactions should be defined as including transactions in securities owned by the employee and members of his or her immediate family and transactions involving securities in which the employee has a beneficial interest.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Ethics & Professional

Standards“…Employers should compare personal transactions of employees with those of clients on a regular basis regardless of the existence of requirement by a regulatory organization.” - Standards of Practice Handbook, 9th Ed., Pg 153

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Ethics & Professional

StandardsWard is scheduled to visit the corporate headquarters of Evans Industries. Ward expects to use the information obtained to complete his research report on Evans stock. Ward learns that Evans plans to pay all of Ward’s expenses for the trip, including costs of meals, hotel room, and air transportation. Which of the following actions would be the best course for Ward to take under the Code and Standards?

A. Accept the expense-paid trip and write an objective report

B. Pay for all travel expenses, including costs of meals and incidental items.

C. Accept the expense-paid trip but disclose the value of the services accepted in the report.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Ethics & Professional

StandardsWard is scheduled to visit the coprorate headquarters of Evans Industries. Ward expects to use the information obtained to complete his research report on Evans stock. Ward learns that Evans plans to pay all of Ward’s expenses for the trip, including costs of meals, hotel room, and air transportation. Which of the following actions would be the best course for Ward to take under the Code and Standards?

A. Accept the expense-paid trip and write an objective report

B. Pay for all travel expenses, including costs of meals and incidental items.

C. Accept the expense-paid trip but disclose the value of the services accepted in the report.

DE

RIV

AT

IVE

S│C

FA

LE

VE

L I Ethics & Professional

StandardsStandard I(B) Independence and Objectivity: “Members and Candidates must yse reasonable care and judgment to achieve and maintain independence and objectivity in their professional activities. Members and Candidates must not offer, solicit, or accept any gift, benefit, compensation, or consideration that reasonably could be expected to compromise their own or another’s independence and objectivity.”

- Standards of Practice Handbook, 9th Ed., Pg 15