depreciation (as 6) impairment (as 28) · applicable to all assets except: (i) ... (ii) wasting...

TRANSCRIPT

DEPRECIATION (AS 6)IMPAIRMENT (AS 28)

Naina & Co 1

Naina Gadia, ACANaina & [email protected]

4th August, 2009

Applicable to all assets except:(i) forests, plantations and similar regenerative

natural resources;(ii) wasting assets including expenditure on

exploration for & extraction of minerals, oils,natural gas & similar non-regenerative resources;

(iii) expenditure on research and development;(iv) goodwill;(v) live stock.This statement also does not applyto land unless it has a limited useful life .

Applicable to all assets except:(i) forests, plantations and similar regenerative

natural resources;(ii) wasting assets including expenditure on

exploration for & extraction of minerals, oils,natural gas & similar non-regenerative resources;

(iii) expenditure on research and development;(iv) goodwill;(v) live stock.This statement also does not applyto land unless it has a limited useful life .

Naina & Co 2

Depreciation is a measure of the wearing out,consumption or other loss of value of adepreciable asset arising from use, effluxion oftime or obsolescence through technology andmarket changes. Depreciation is allocated so as tocharge a fair proportion of the depreciableamount in each accounting period during theexpected useful life of the asset. Depreciationincludes amortisation of assets whose useful life ispredetermined.

Naina & Co 3

Depreciation is a measure of the wearing out,consumption or other loss of value of adepreciable asset arising from use, effluxion oftime or obsolescence through technology andmarket changes. Depreciation is allocated so as tocharge a fair proportion of the depreciableamount in each accounting period during theexpected useful life of the asset. Depreciationincludes amortisation of assets whose useful life ispredetermined.

Depreciable assets are assets which

(i) are expected to be used during more than oneaccounting period;

(ii) have a limited useful life; and

(iii) are held by an enterprise for use in theproduction or supply of goods and services, forrental to others, or for administrative purposesand not for the purpose of sale in the ordinarycourse of business.

Depreciable assets are assets which

(i) are expected to be used during more than oneaccounting period;

(ii) have a limited useful life; and

(iii) are held by an enterprise for use in theproduction or supply of goods and services, forrental to others, or for administrative purposesand not for the purpose of sale in the ordinarycourse of business.

Naina & Co 4

Useful life

Estimated Residual Value

(i) the period over which a depreciable asset is expected tobe used by the enterprise; or

(ii) the number of production or Similar units expected tobe obtained from the use of the asset by the enterprise.

Useful life is a matter of estimation and is normallybased on various factors including experience withsimilar types of assets. Such estimation is more difficultfor an asset using new technology or used in theproduction of a new product or in the provision of anew service but is nevertheless required on somereasonable basis.

Naina & Co 5

Useful life

Estimated Residual Value

(i) the period over which a depreciable asset is expected tobe used by the enterprise; or

(ii) the number of production or Similar units expected tobe obtained from the use of the asset by the enterprise.

Useful life is a matter of estimation and is normallybased on various factors including experience withsimilar types of assets. Such estimation is more difficultfor an asset using new technology or used in theproduction of a new product or in the provision of anew service but is nevertheless required on somereasonable basis.

Determination of residual value of an asset is normally adifficult matter. If such value is considered asinsignificant, it is normally regarded as nil. On thecontrary, if the residual value is likely to be significant, itis estimated at the time of acquisition/installation, or atthe time of subsequent revaluation of the asset. One ofthe bases for determining the residual value would be therealisable value of similar assets which have reached theend of their useful lives and have operated underconditions similar to those in which the asset will beused.

Determination of residual value of an asset is normally adifficult matter. If such value is considered asinsignificant, it is normally regarded as nil. On thecontrary, if the residual value is likely to be significant, itis estimated at the time of acquisition/installation, or atthe time of subsequent revaluation of the asset. One ofthe bases for determining the residual value would be therealisable value of similar assets which have reached theend of their useful lives and have operated underconditions similar to those in which the asset will beused.

Naina & Co 6

Any addition or extension to an existing assetwhich is of a capital nature and which becomesan integral part of the existing asset isdepreciated over the remaining useful life of thatasset. As a practical measure, however,depreciation is sometimes provided on suchaddition or extension at the rate which is appliedto an existing asset. Any addition or extensionwhich retains a separate identity and is capableof being used after the existing asset is disposedof, is depreciated independently on the basis ofan estimate of its own useful life.

Any addition or extension to an existing assetwhich is of a capital nature and which becomesan integral part of the existing asset isdepreciated over the remaining useful life of thatasset. As a practical measure, however,depreciation is sometimes provided on suchaddition or extension at the rate which is appliedto an existing asset. Any addition or extensionwhich retains a separate identity and is capableof being used after the existing asset is disposedof, is depreciated independently on the basis ofan estimate of its own useful life.

Naina & Co 7

Straight line method

Reducing balance method.

The principle underlying the charge of depreciationto revenue is to match the cost of asset with therevenue it produces. The selection of methoddepends on:

Type of asset

Nature of use

Other circumstances prevailing in business :

Naina & Co 8

Straight line method

Reducing balance method.

The principle underlying the charge of depreciationto revenue is to match the cost of asset with therevenue it produces. The selection of methoddepends on:

Type of asset

Nature of use

Other circumstances prevailing in business :

MethodSelection

Naina & Co 9

MostCommonly

used :SLM/RBM

Combinationis also usedat times

Small valueitems are

depreciatedfirst year

Consistencyto be

maintainedYtoY

Consistency provides comparability of results ofoperations of enterprise from period to period. Achange in Method is made only if the new method is:

Required by statute or

For compliance with an accounting standard or

If it is considered that change would result in a moreappropriate preparation or presentation of financialstatements of enterprise.

Consistency provides comparability of results ofoperations of enterprise from period to period. Achange in Method is made only if the new method is:

Required by statute or

For compliance with an accounting standard or

If it is considered that change would result in a moreappropriate preparation or presentation of financialstatements of enterprise.

Naina & Co 10

depreciation is recalculated – Retrospectively.

The deficiency or surplus - adjusted in the accounts inthe year in which the method of depreciation ischanged.

Deficiency: is charged in statement of profit and loss.

Surplus: is credited to the statement of profit and loss.

Such a change is treated as a change in accountingpolicy and its effect is quantified and disclosed.

depreciation is recalculated – Retrospectively.

The deficiency or surplus - adjusted in the accounts inthe year in which the method of depreciation ischanged.

Deficiency: is charged in statement of profit and loss.

Surplus: is credited to the statement of profit and loss.

Such a change is treated as a change in accountingpolicy and its effect is quantified and disclosed.

Naina & Co 11

Historical cost or other amount substituted forhistorical cost of each class of depreciable asset.

Total depreciation for the period for each class ofassets

Accumulated depreciation for each class of assets

Method of depreciation adopted and applied

Depreciation rates and useful lives if they aredifferent from the principal rates given inschedule XIV

If any depreciable asset is disposed off, discarded,demolished or destroyed, the net surplus ordeficiency, if material, should be disclosedseparately.

Historical cost or other amount substituted forhistorical cost of each class of depreciable asset.

Total depreciation for the period for each class ofassets

Accumulated depreciation for each class of assets

Method of depreciation adopted and applied

Depreciation rates and useful lives if they aredifferent from the principal rates given inschedule XIV

If any depreciable asset is disposed off, discarded,demolished or destroyed, the net surplus ordeficiency, if material, should be disclosedseparately.

Naina & Co 12

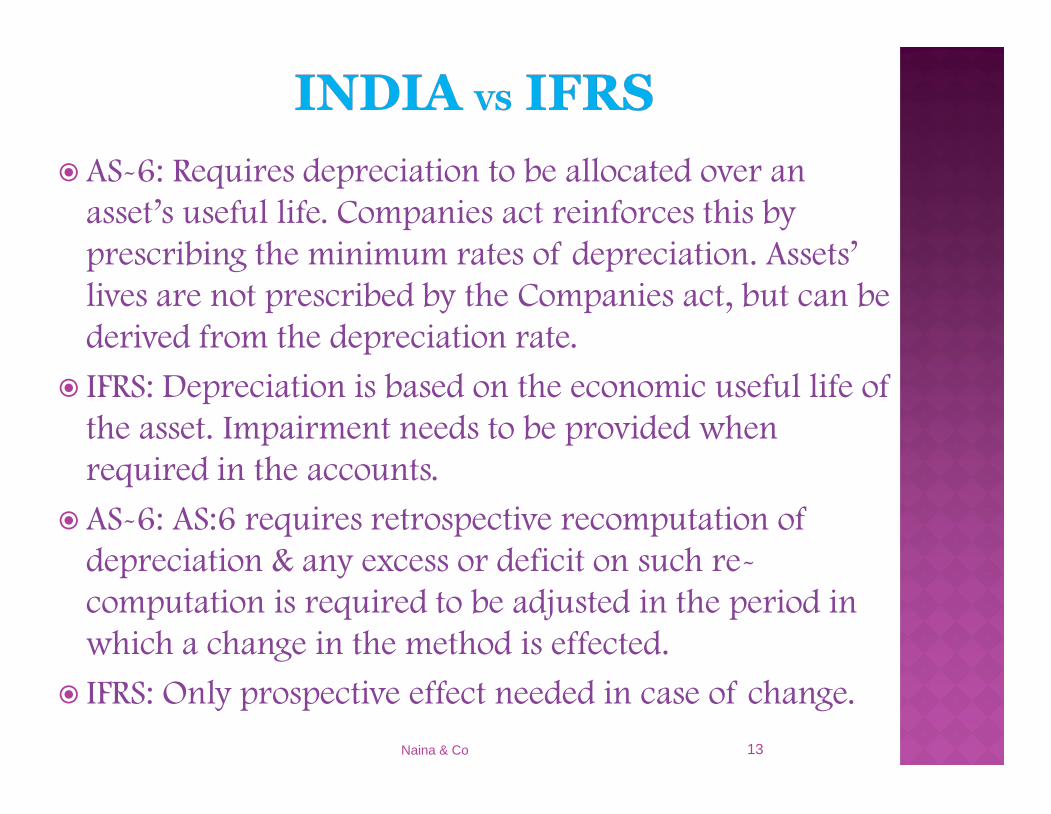

AS-6: Requires depreciation to be allocated over anasset’s useful life. Companies act reinforces this byprescribing the minimum rates of depreciation. Assets’lives are not prescribed by the Companies act, but can bederived from the depreciation rate.

IFRS: Depreciation is based on the economic useful life ofthe asset. Impairment needs to be provided whenrequired in the accounts.

AS-6: AS:6 requires retrospective recomputation ofdepreciation & any excess or deficit on such re-computation is required to be adjusted in the period inwhich a change in the method is effected.

IFRS: Only prospective effect needed in case of change.

AS-6: Requires depreciation to be allocated over anasset’s useful life. Companies act reinforces this byprescribing the minimum rates of depreciation. Assets’lives are not prescribed by the Companies act, but can bederived from the depreciation rate.

IFRS: Depreciation is based on the economic useful life ofthe asset. Impairment needs to be provided whenrequired in the accounts.

AS-6: AS:6 requires retrospective recomputation ofdepreciation & any excess or deficit on such re-computation is required to be adjusted in the period inwhich a change in the method is effected.

IFRS: Only prospective effect needed in case of change.

Naina & Co 13

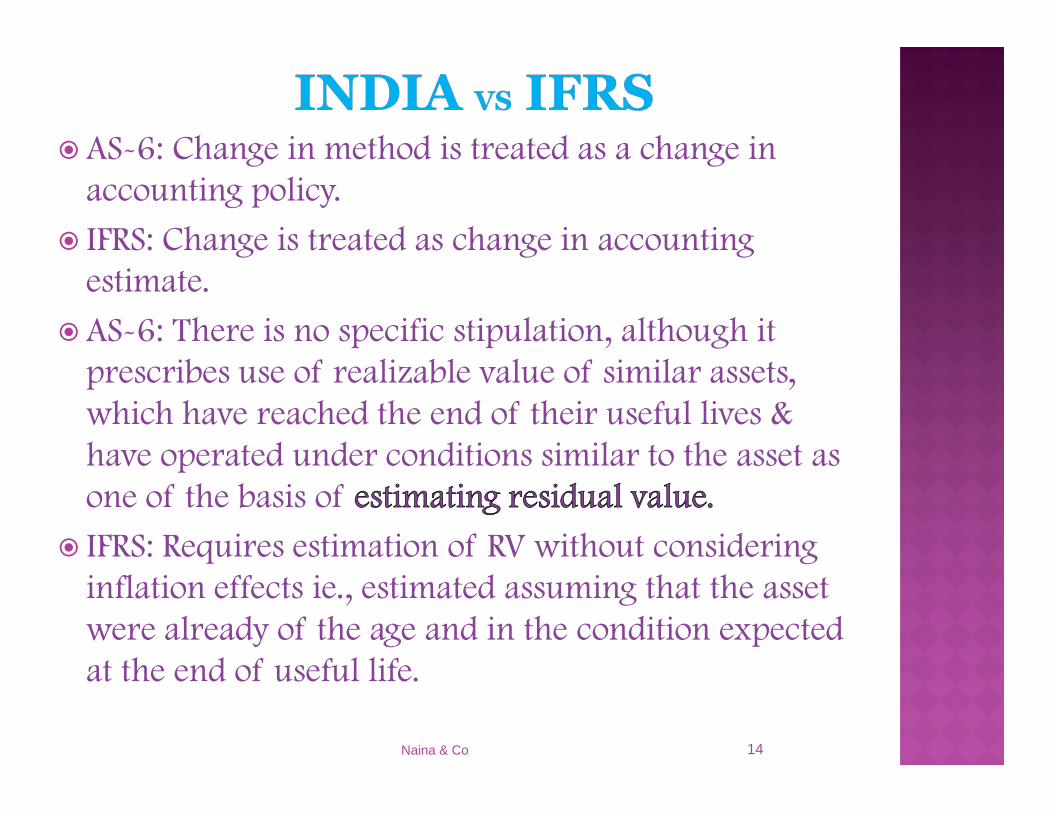

AS-6: Change in method is treated as a change inaccounting policy.

IFRS: Change is treated as change in accountingestimate.

AS-6: There is no specific stipulation, although itprescribes use of realizable value of similar assets,which have reached the end of their useful lives &have operated under conditions similar to the asset asone of the basis of estimating residual value.

IFRS: Requires estimation of RV without consideringinflation effects ie., estimated assuming that the assetwere already of the age and in the condition expectedat the end of useful life.

AS-6: Change in method is treated as a change inaccounting policy.

IFRS: Change is treated as change in accountingestimate.

AS-6: There is no specific stipulation, although itprescribes use of realizable value of similar assets,which have reached the end of their useful lives &have operated under conditions similar to the asset asone of the basis of estimating residual value.

IFRS: Requires estimation of RV without consideringinflation effects ie., estimated assuming that the assetwere already of the age and in the condition expectedat the end of useful life.

Naina & Co 14

OBJECTIVE

SCOPE 1-3

DEFINITIONS 4

IDENTIFYING AN ASSET THAT MAY BE IMPAIRED 5-13

MEASUREMENT OF RECOVERABLE AMOUNT 14-55

RECOGNITION AND MEASUREMENT OF IL 56-62

CASH-GENERATING UNITS 63-92

REVERSAL OF AN IMPAIRMENT LOSS 93-111

IMPAIRMENT IN CASE OF DISCONTINUING OPERATIONS 112-116

DISCLOSURE 117-123

TRANSITIONAL PROVISIONS 124-125

APPENDIX

OBJECTIVE

SCOPE 1-3

DEFINITIONS 4

IDENTIFYING AN ASSET THAT MAY BE IMPAIRED 5-13

MEASUREMENT OF RECOVERABLE AMOUNT 14-55

RECOGNITION AND MEASUREMENT OF IL 56-62

CASH-GENERATING UNITS 63-92

REVERSAL OF AN IMPAIRMENT LOSS 93-111

IMPAIRMENT IN CASE OF DISCONTINUING OPERATIONS 112-116

DISCLOSURE 117-123

TRANSITIONAL PROVISIONS 124-125

APPENDIX

Naina & Co 15

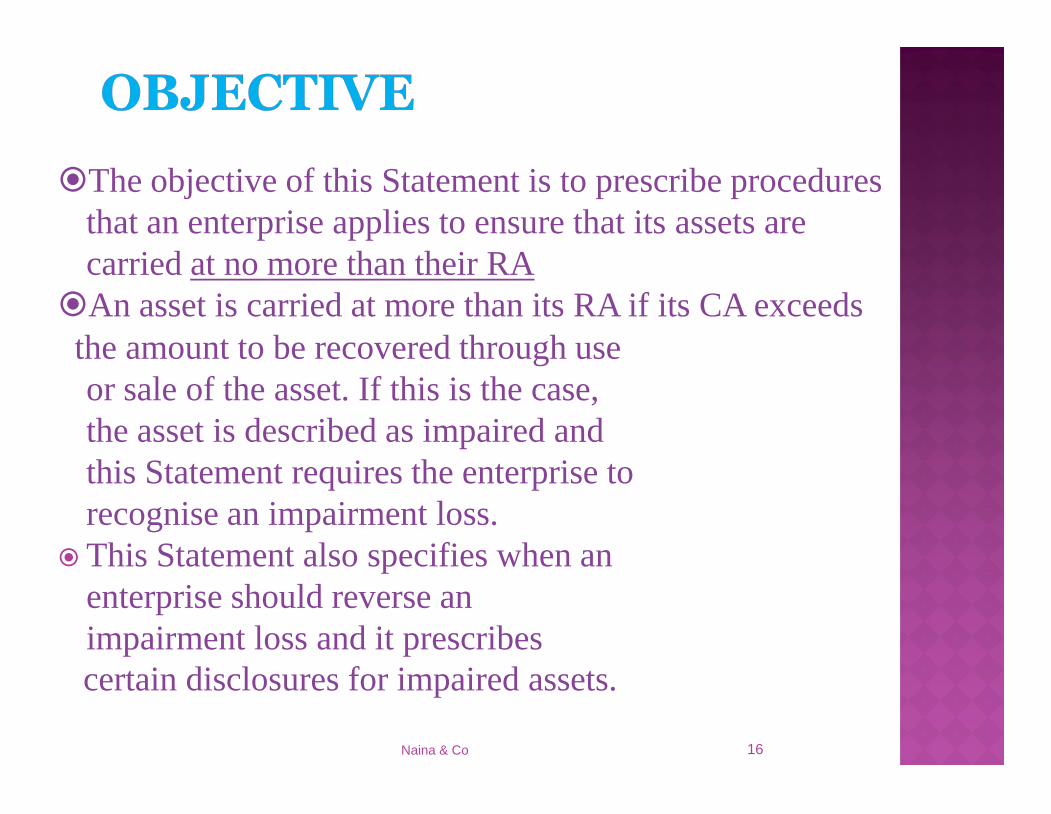

the amount to be recovered through useor sale of the asset. If this is the case,the asset is described as impaired andthis Statement requires the enterprise torecognise an impairment loss.

This Statement also specifies when anenterprise should reverse animpairment loss and it prescribescertain disclosures for impaired assets.

The objective of this Statement is to prescribe proceduresthat an enterprise applies to ensure that its assets arecarried at no more than their RA

An asset is carried at more than its RA if its CA exceeds

Naina & Co 16

the amount to be recovered through useor sale of the asset. If this is the case,the asset is described as impaired andthis Statement requires the enterprise torecognise an impairment loss.

This Statement also specifies when anenterprise should reverse animpairment loss and it prescribescertain disclosures for impaired assets.

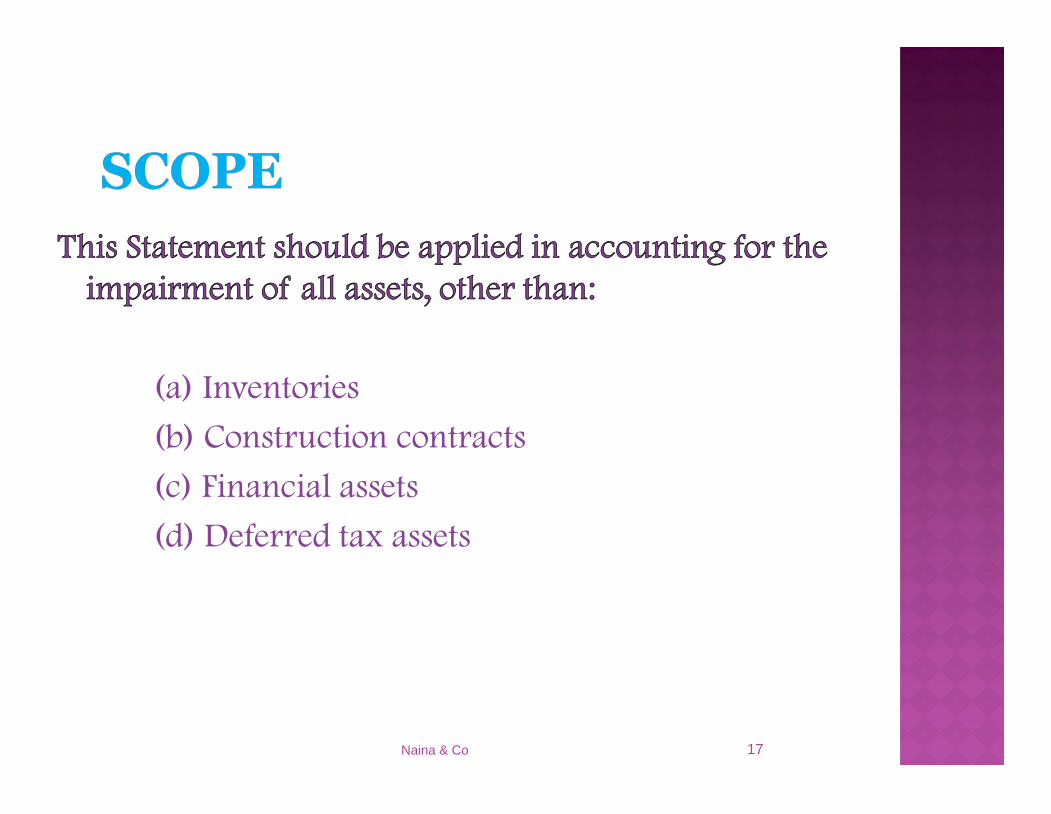

This Statement should be applied in accounting for theimpairment of all assets, other than:

(a) Inventories

(b) Construction contracts

(c) Financial assets

(d) Deferred tax assets

This Statement should be applied in accounting for theimpairment of all assets, other than:

(a) Inventories

(b) Construction contracts

(c) Financial assets

(d) Deferred tax assets

Naina & Co 17

Recoverable amount: is the higher of an asset’snet selling price and its value in use.

Value in use: is the present value of estimatedfuture cash flows expected to arise from thecontinuing use of an asset and from its disposalat the end of its useful life

Net selling price: is the amount obtainable fromthe sale of an asset in an arm’s lengthTransaction between knowledgeable, willingparties, less the costs of disposal.

Recoverable amount: is the higher of an asset’snet selling price and its value in use.

Value in use: is the present value of estimatedfuture cash flows expected to arise from thecontinuing use of an asset and from its disposalat the end of its useful life

Net selling price: is the amount obtainable fromthe sale of an asset in an arm’s lengthTransaction between knowledgeable, willingparties, less the costs of disposal.

Naina & Co 18

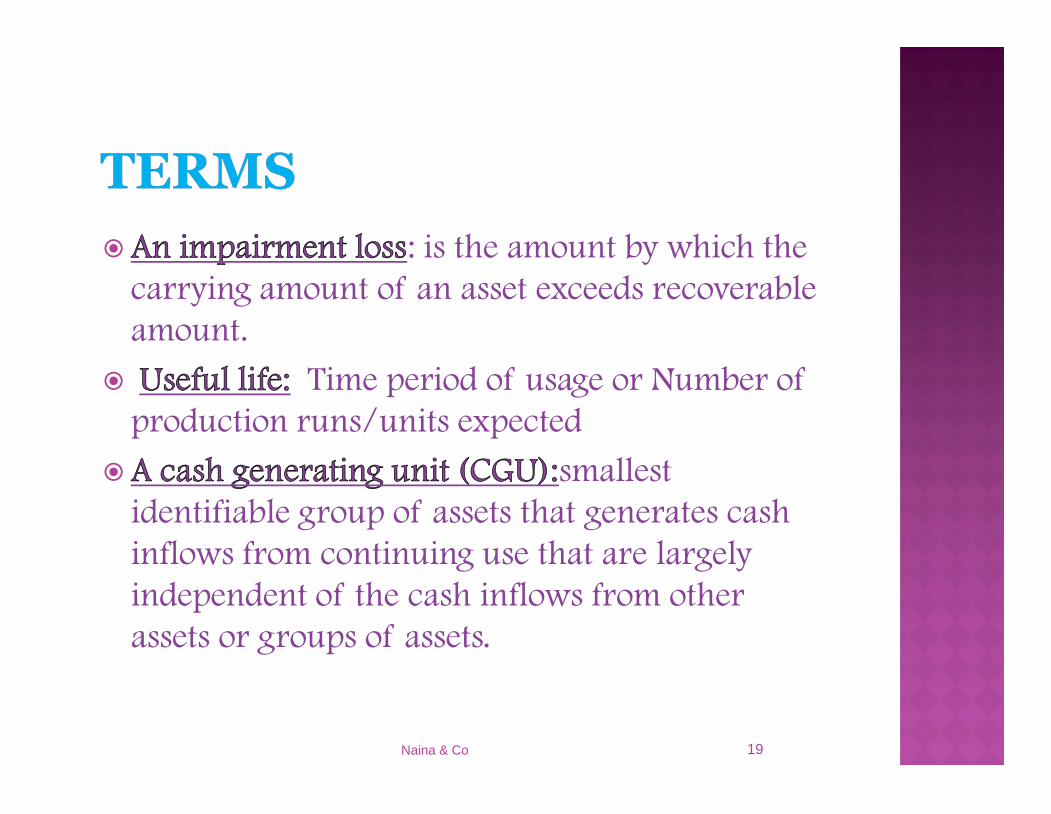

An impairment loss: is the amount by which thecarrying amount of an asset exceeds recoverableamount.

Useful life: Time period of usage or Number ofproduction runs/units expected

A cash generating unit (CGU):smallestidentifiable group of assets that generates cashinflows from continuing use that are largelyindependent of the cash inflows from otherassets or groups of assets.

An impairment loss: is the amount by which thecarrying amount of an asset exceeds recoverableamount.

Useful life: Time period of usage or Number ofproduction runs/units expected

A cash generating unit (CGU):smallestidentifiable group of assets that generates cashinflows from continuing use that are largelyindependent of the cash inflows from otherassets or groups of assets.

Naina & Co 19

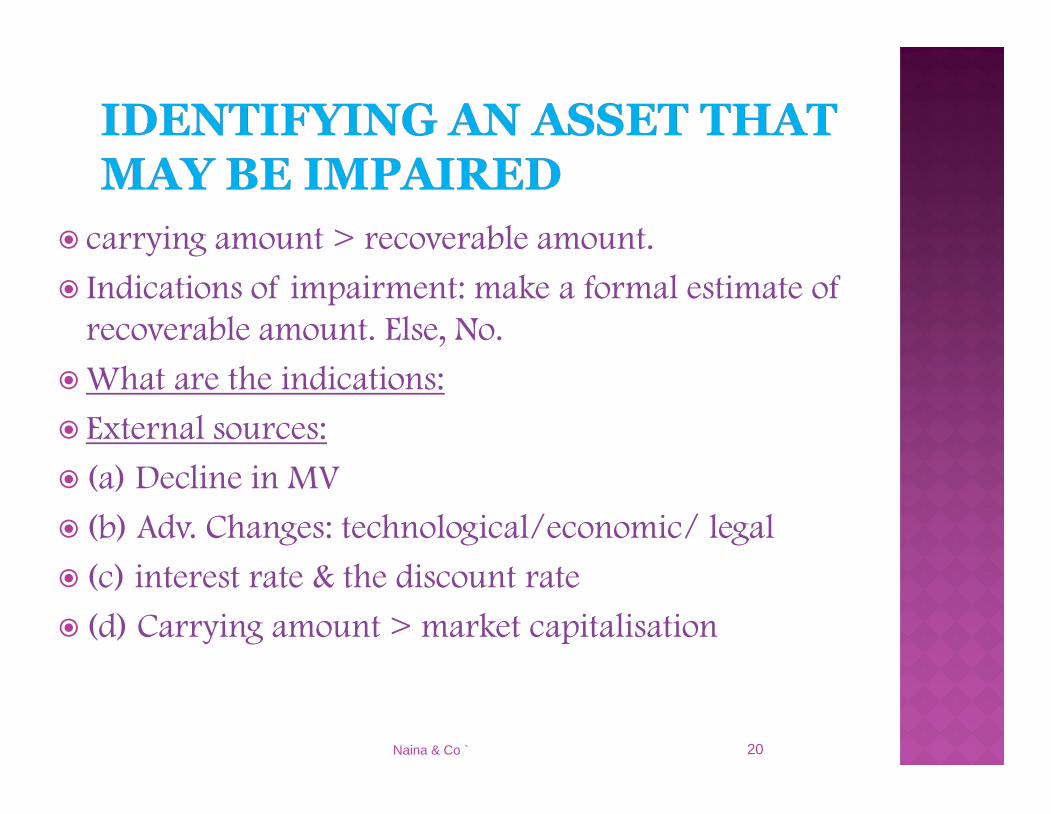

carrying amount > recoverable amount.

Indications of impairment: make a formal estimate ofrecoverable amount. Else, No.

What are the indications:

External sources:

(a) Decline in MV

(b) Adv. Changes: technological/economic/ legal

(c) interest rate & the discount rate

(d) Carrying amount > market capitalisation

carrying amount > recoverable amount.

Indications of impairment: make a formal estimate ofrecoverable amount. Else, No.

What are the indications:

External sources:

(a) Decline in MV

(b) Adv. Changes: technological/economic/ legal

(c) interest rate & the discount rate

(d) Carrying amount > market capitalisation

Naina & Co ` 20

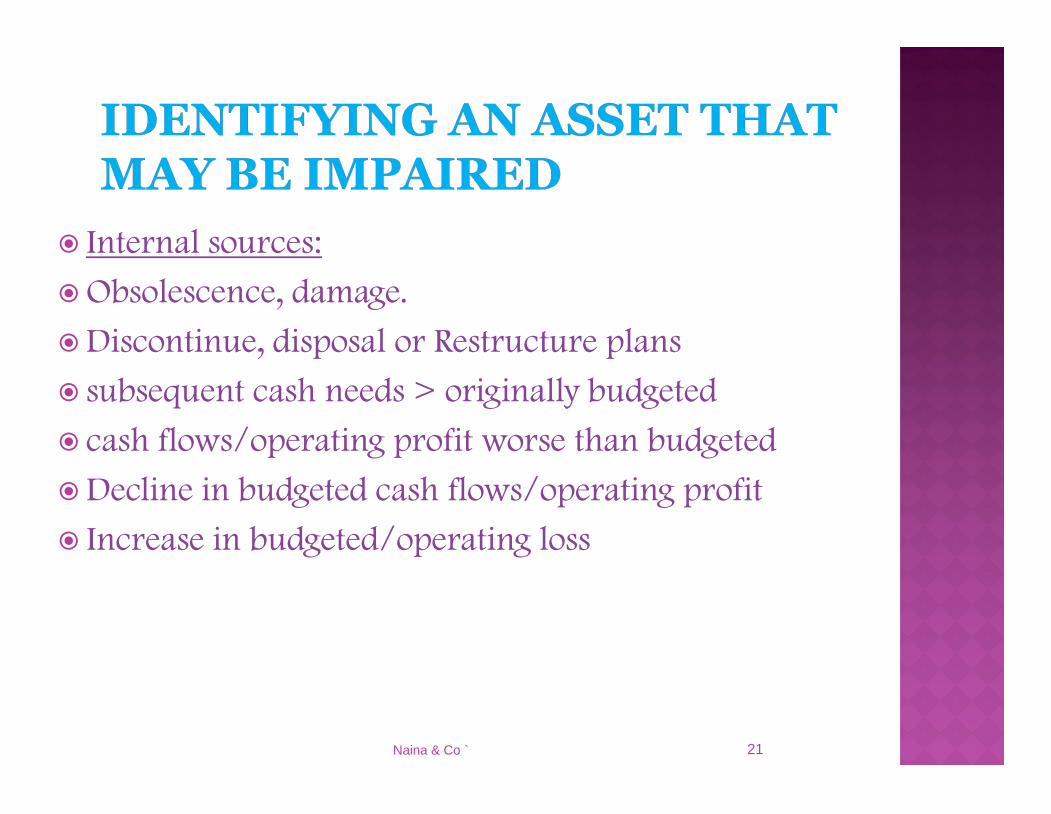

Internal sources:

Obsolescence, damage.

Discontinue, disposal or Restructure plans

subsequent cash needs > originally budgeted

cash flows/operating profit worse than budgeted

Decline in budgeted cash flows/operating profit

Increase in budgeted/operating loss

Internal sources:

Obsolescence, damage.

Discontinue, disposal or Restructure plans

subsequent cash needs > originally budgeted

cash flows/operating profit worse than budgeted

Decline in budgeted cash flows/operating profit

Increase in budgeted/operating loss

Naina & Co ` 21

When no need to estimate recoverable amount?

Net SP/VinU > carrying amount

RA is not sensitive to indications listed

Rise in interest rates still, discount rate unlikely tobe affected by increase or

previous sensitivity analysis of RA shows that:

no decrease in RA because future cash flows arealso likely to increase

When no need to estimate recoverable amount?

Net SP/VinU > carrying amount

RA is not sensitive to indications listed

Rise in interest rates still, discount rate unlikely tobe affected by increase or

previous sensitivity analysis of RA shows that:

no decrease in RA because future cash flows arealso likely to increase

Naina & Co ` 22

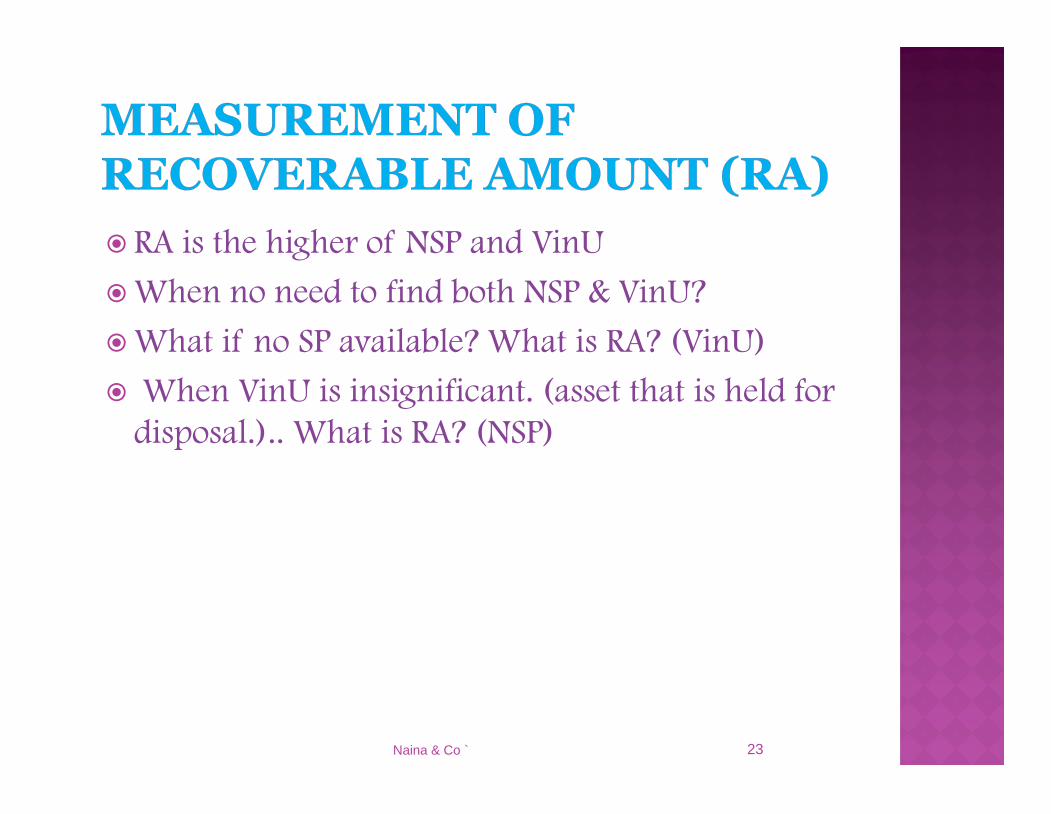

RA is the higher of NSP and VinU

When no need to find both NSP & VinU?

What if no SP available? What is RA? (VinU)

When VinU is insignificant. (asset that is held fordisposal.).. What is RA? (NSP)

Naina & Co ` 23

RA is the higher of NSP and VinU

When no need to find both NSP & VinU?

What if no SP available? What is RA? (VinU)

When VinU is insignificant. (asset that is held fordisposal.).. What is RA? (NSP)

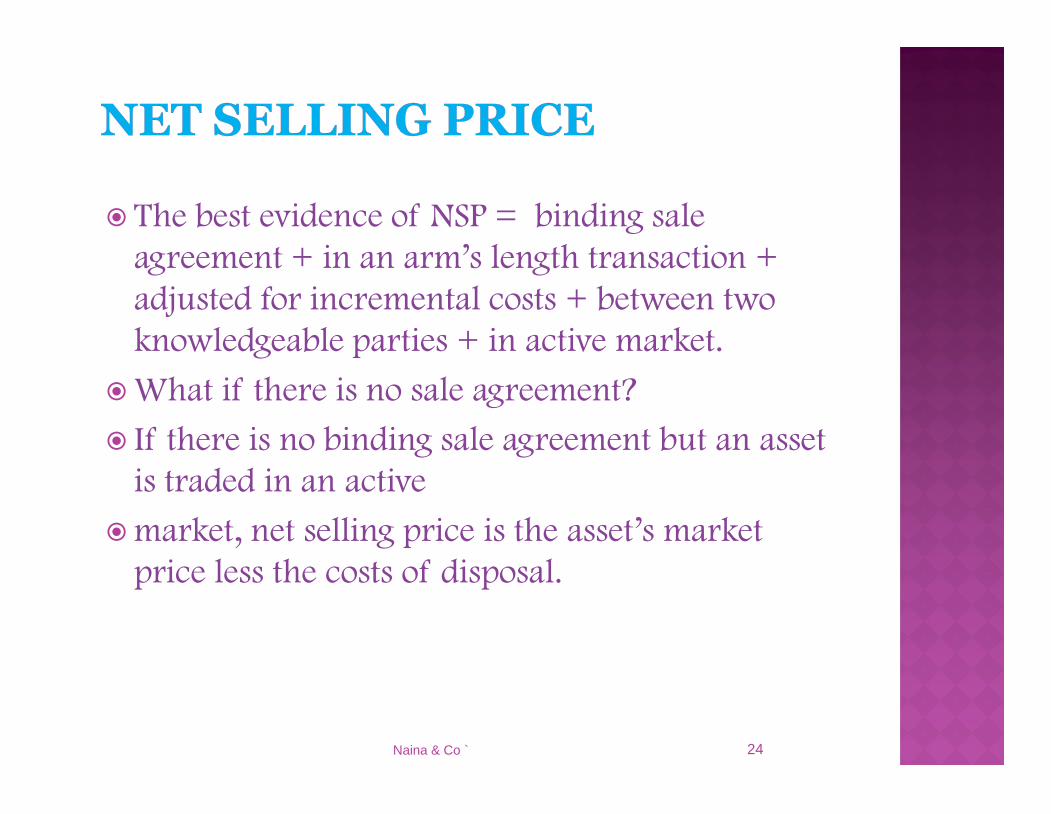

The best evidence of NSP = binding saleagreement + in an arm’s length transaction +adjusted for incremental costs + between twoknowledgeable parties + in active market.

What if there is no sale agreement?

If there is no binding sale agreement but an assetis traded in an active

market, net selling price is the asset’s marketprice less the costs of disposal.

Naina & Co ` 24

The best evidence of NSP = binding saleagreement + in an arm’s length transaction +adjusted for incremental costs + between twoknowledgeable parties + in active market.

What if there is no sale agreement?

If there is no binding sale agreement but an assetis traded in an active

market, net selling price is the asset’s marketprice less the costs of disposal.

What if there is no sale agreement & no active marketavailable?

If there is no binding sale agreement or active marketfor an asset, NSP is based on the best informationavailable to reflect the amount that an enterprise couldobtain, at the balance sheet date, for the disposal of theasset in an arm’s length transaction betweenknowledgeable, willing parties, after deducting the costsof disposal. In determining this amount, an enterpriseconsiders the outcome of recent transactions for similarassets within the same industry.

Naina & Co ` 25

What if there is no sale agreement & no active marketavailable?

If there is no binding sale agreement or active marketfor an asset, NSP is based on the best informationavailable to reflect the amount that an enterprise couldobtain, at the balance sheet date, for the disposal of theasset in an arm’s length transaction betweenknowledgeable, willing parties, after deducting the costsof disposal. In determining this amount, an enterpriseconsiders the outcome of recent transactions for similarassets within the same industry.

Estimating VinU, steps:

(a) estimating the future cash inflows and outflowsarising from continuing use of the asset and fromits ultimate disposal; and

(b) applying the appropriate discount rate to thesefuture cash flows.

Basis for Estimates of Future Cash Flows

(a) Reasonable and supportable assumptions, bestestimate of the set of economic conditions.Greater weight to external evidence;

(b) Most recent financial budgets/forecastscovering max five yrs.

Estimating VinU, steps:

(a) estimating the future cash inflows and outflowsarising from continuing use of the asset and fromits ultimate disposal; and

(b) applying the appropriate discount rate to thesefuture cash flows.

Basis for Estimates of Future Cash Flows

(a) Reasonable and supportable assumptions, bestestimate of the set of economic conditions.Greater weight to external evidence;

(b) Most recent financial budgets/forecastscovering max five yrs.

Naina & Co 26

Beyond five yrs, should be estimated by extrapolating theprojections based on the budgets/forecasts using asteady or declining growth rate for subsequent years,unless an increasing rate can be justified.

This growth rate should not exceed the long-termaverage growth rate for the products, industries, orcountry or countries in which the enterprise

operates, or for the market in which the asset is used,unless a higher rate can be justified.

Where conditions are very favourable… competitorsare likely to enter the market and restrict growth.Therefore, enterprises will have difficulty in exceedingthe average historical growth rate over the long term(say, twenty years)

Beyond five yrs, should be estimated by extrapolating theprojections based on the budgets/forecasts using asteady or declining growth rate for subsequent years,unless an increasing rate can be justified.

This growth rate should not exceed the long-termaverage growth rate for the products, industries, orcountry or countries in which the enterprise

operates, or for the market in which the asset is used,unless a higher rate can be justified.

Where conditions are very favourable… competitorsare likely to enter the market and restrict growth.Therefore, enterprises will have difficulty in exceedingthe average historical growth rate over the long term(say, twenty years)

Naina & Co 27

Estimates of future cash flows should include:

projections of cash inflows

projections of cash outflows

net cash flows, if any, (disposal Cost)

General inflation effects

Overheads

Further Cash Outflows

Estimates of future cash flows should include:

projections of cash inflows

projections of cash outflows

net cash flows, if any, (disposal Cost)

General inflation effects

Overheads

Further Cash Outflows

Naina & Co 28

If the discount rate includes the effect of priceincreases due to general inflation, future cashflows are estimated in nominal terms.

If the discount rate excludes the effect of priceincreases due to general inflation, future cashflows are estimated in real terms but includefuture specific price increases or decreases.

If the discount rate includes the effect of priceincreases due to general inflation, future cashflows are estimated in nominal terms.

If the discount rate excludes the effect of priceincreases due to general inflation, future cashflows are estimated in real terms but includefuture specific price increases or decreases.

Naina & Co 29

33. OVERHEADSProjections include future overheads that can beattributed directly, or allocated on a reasonable &consistent basis, to use of asset.

34. FURTHER CASH OUTFLOWS:The estimate of future cash outflows includes anestimate of any further cash outflow that is expectedto be incurred before the asset is ready for use orsale. For example, this is the case for a buildingunder construction or for a development projectthat is not yet completed.

33. OVERHEADSProjections include future overheads that can beattributed directly, or allocated on a reasonable &consistent basis, to use of asset.

34. FURTHER CASH OUTFLOWS:The estimate of future cash outflows includes anestimate of any further cash outflow that is expectedto be incurred before the asset is ready for use orsale. For example, this is the case for a buildingunder construction or for a development projectthat is not yet completed.

Naina & Co 30

35. Double Counting

To avoid double counting, estimates of futurecash flows do not include:

cash inflows from assets that generate cashinflows from continuing use that are largelyindependent of the cash inflows from assetunder review (receivables); and

cash outflows that relate to obligations thathave already been recognised as liabilities(payables, pensions or provisions).

35. Double Counting

To avoid double counting, estimates of futurecash flows do not include:

cash inflows from assets that generate cashinflows from continuing use that are largelyindependent of the cash inflows from assetunder review (receivables); and

cash outflows that relate to obligations thathave already been recognised as liabilities(payables, pensions or provisions).

Naina & Co 31

36. Future cash flows should not includeestimated future cash inflows or outflows thatare expected to arise from:

a future restructuring to which an enterpriseis not yet committed; or future capitalexpenditure that will improve or enhance theasset in excess of its originally assessedstandard of performance.

37. Because future cash flows are estimated forthe asset in its current condition, value in usedoes not reflect:

36. Future cash flows should not includeestimated future cash inflows or outflows thatare expected to arise from:

a future restructuring to which an enterpriseis not yet committed; or future capitalexpenditure that will improve or enhance theasset in excess of its originally assessedstandard of performance.

37. Because future cash flows are estimated forthe asset in its current condition, value in usedoes not reflect:

Naina & Co 32

38. RESTRUCTURING: is a programme that is plannedand controlled by management and that materiallychanges either scope of business undertaken by anenterprise or manner in which business is run.

39. When an enterprise becomes committed to arestructuring, some assets are likely to be affected bythis restructuring. Once enterprise is committed torestructuring, in determining value in use, estimates offuture cash inflows and cash outflows reflect the costsavings and other benefits from the restructuring(based on the most recent financial budgets/forecaststhat have been approved by management).

38. RESTRUCTURING: is a programme that is plannedand controlled by management and that materiallychanges either scope of business undertaken by anenterprise or manner in which business is run.

39. When an enterprise becomes committed to arestructuring, some assets are likely to be affected bythis restructuring. Once enterprise is committed torestructuring, in determining value in use, estimates offuture cash inflows and cash outflows reflect the costsavings and other benefits from the restructuring(based on the most recent financial budgets/forecaststhat have been approved by management).

Naina & Co 33

40. Until an enterprise incurs capital expenditure that improvesor enhances an asset in excess of its originally assessedstandard of performance, estimates of future cash flows do notinclude the estimated future cash inflows that are expected toarise from this expenditure

41. Estimates of future cash flows include future capitalexpenditure necessary to maintain or sustain an asset at itsoriginally assessed standard of performance.

42. Estimates of future cash flows should not include: cash inflows or outflows from financing activities; or income tax receipts or payments. The estimate of net cash flows to be received (or paid) for the

disposal of an asset at the end of its useful life should be theamount that an enterprise expects to obtain from the disposalof the asset in an arm’s length transaction betweenknowledgeable, willing parties, after deducting the estimatedcosts of disposal.

40. Until an enterprise incurs capital expenditure that improvesor enhances an asset in excess of its originally assessedstandard of performance, estimates of future cash flows do notinclude the estimated future cash inflows that are expected toarise from this expenditure

41. Estimates of future cash flows include future capitalexpenditure necessary to maintain or sustain an asset at itsoriginally assessed standard of performance.

42. Estimates of future cash flows should not include: cash inflows or outflows from financing activities; or income tax receipts or payments. The estimate of net cash flows to be received (or paid) for the

disposal of an asset at the end of its useful life should be theamount that an enterprise expects to obtain from the disposalof the asset in an arm’s length transaction betweenknowledgeable, willing parties, after deducting the estimatedcosts of disposal.

Naina & Co 34

46. Future cash flows are:

estimated in the currency in which they willbe generated

Discounted using a discount rate appropriatefor that currency.

An enterprise translates the present valueobtained using the exchange rate at thebalance sheet date (AS 11)

46. Future cash flows are:

estimated in the currency in which they willbe generated

Discounted using a discount rate appropriatefor that currency.

An enterprise translates the present valueobtained using the exchange rate at thebalance sheet date (AS 11)

Naina & Co 35

Should be a pre tax rate that reflect current market assessments of time

value of money and the risks specific to the asset. DR should not reflect risks for which future

cash flow estimates have been adjusted.48. This is the return that investors would

require if they were to choose an investmentthat would generate cash flows of amounts,timing and risk profile equivalent to those thatthe enterprise expects to derive from asset.

Should be a pre tax rate that reflect current market assessments of time

value of money and the risks specific to the asset. DR should not reflect risks for which future

cash flow estimates have been adjusted.48. This is the return that investors would

require if they were to choose an investmentthat would generate cash flows of amounts,timing and risk profile equivalent to those thatthe enterprise expects to derive from asset.

Naina & Co 36

When an asset-specific rate is not directlyavailable from the market, an enterprise usesother bases to estimate the discount rate. Thepurpose is to estimate, as far as possible, amarket assessment of:

(a) the time value of money for the periodsuntil the end of the asset’s useful life; and

(b) the risks that the future cash flows willdiffer in amount or timing from estimates.

When an asset-specific rate is not directlyavailable from the market, an enterprise usesother bases to estimate the discount rate. Thepurpose is to estimate, as far as possible, amarket assessment of:

(a) the time value of money for the periodsuntil the end of the asset’s useful life; and

(b) the risks that the future cash flows willdiffer in amount or timing from estimates.

Naina & Co 37

(a) Enterprise’s weighted average cost of capitaldetermined using techniques such as CAPM

(b) Enterprise’s incremental borrowing rate;(c) other market borrowing rates.51. These rates are adjusted:(a) to reflect the way market would assess specific

risks associated with projected cash flows(b)To exclude risks not relevant to projected

cashflows.Risks : country, currency, price & cash flow

risk.

(a) Enterprise’s weighted average cost of capitaldetermined using techniques such as CAPM

(b) Enterprise’s incremental borrowing rate;(c) other market borrowing rates.51. These rates are adjusted:(a) to reflect the way market would assess specific

risks associated with projected cash flows(b)To exclude risks not relevant to projected

cashflows.Risks : country, currency, price & cash flow

risk.

Naina & Co 38

52. To avoid double counting, the discount ratedoes not reflect risks for which future cash flowestimates have been adjusted.

53. DR-Independent of all other rates:The discount rate is independent of the

enterprise’s capital structure and the way theenterprise financed the purchase of the assetbecause the future cash flows expected to arisefrom an asset do not depend on the way in whichthe enterprise financed the purchase of the asset.

54. Pre-Tax RateWhen the basis for the rate is post-tax, that basis is

adjusted to reflect a pre-tax rate.

52. To avoid double counting, the discount ratedoes not reflect risks for which future cash flowestimates have been adjusted.

53. DR-Independent of all other rates:The discount rate is independent of the

enterprise’s capital structure and the way theenterprise financed the purchase of the assetbecause the future cash flows expected to arisefrom an asset do not depend on the way in whichthe enterprise financed the purchase of the asset.

54. Pre-Tax RateWhen the basis for the rate is post-tax, that basis is

adjusted to reflect a pre-tax rate.

Naina & Co 39

57. What is Impairment Loss?If the RA < CA, the carrying amount of the assetshould be reduced to its RA. That reduction is animpairment loss.

58. An impairment loss should be recognised asexpense in the profit and loss A/c immediately,unless: asset is carried at revalued amountHowever, an impairment loss on a revalued asset isrecognised directly against any revaluation surplusfor the asset to the extent that the impairment lossdoes not exceed the amount held in the revaluationsurplus for that same asset.

57. What is Impairment Loss?If the RA < CA, the carrying amount of the assetshould be reduced to its RA. That reduction is animpairment loss.

58. An impairment loss should be recognised asexpense in the profit and loss A/c immediately,unless: asset is carried at revalued amountHowever, an impairment loss on a revalued asset isrecognised directly against any revaluation surplusfor the asset to the extent that the impairment lossdoes not exceed the amount held in the revaluationsurplus for that same asset.

Naina & Co 40

What is a CGU?A cash generating unit (CGU):smallest identifiablegroup of assets that generates cash inflows fromcontinuing use that are largely independent of thecash inflows from other assets or groups of assets.

Identification of the CGU to Which an Asset BelongsEstimating the RA If there is any indication that an asset may be

impaired, the RA should be estimated for theindividual asset. If it is not possible to estimate theRA of the individual asset, an enterprise shoulddetermine the RA of the CGU to which the assetbelongs (the asset’s CGU).

What is a CGU?A cash generating unit (CGU):smallest identifiablegroup of assets that generates cash inflows fromcontinuing use that are largely independent of thecash inflows from other assets or groups of assets.

Identification of the CGU to Which an Asset BelongsEstimating the RA If there is any indication that an asset may be

impaired, the RA should be estimated for theindividual asset. If it is not possible to estimate theRA of the individual asset, an enterprise shoulddetermine the RA of the CGU to which the assetbelongs (the asset’s CGU).

Naina & Co 41

the asset’s value in use cannot be estimated to beclose to its net selling price (for example, when thefuture cash flows from continuing use of the assetcannot be estimated to be negligible);

the asset does not generate cash inflows fromcontinuing use that are largely independent of thosefrom other assets.

In such cases, RA, can be determined only for theasset’s CGU.

Eg: A mining enterprise owns a private railway tosupport its mining activities.

the asset’s value in use cannot be estimated to beclose to its net selling price (for example, when thefuture cash flows from continuing use of the assetcannot be estimated to be negligible);

the asset does not generate cash inflows fromcontinuing use that are largely independent of thosefrom other assets.

In such cases, RA, can be determined only for theasset’s CGU.

Eg: A mining enterprise owns a private railway tosupport its mining activities.

Naina & Co 42

Cash inflows from continuing use are inflows ofcash and cash equivalents received from partiesoutside the reporting enterprise. In identifyingwhether cash inflows from an asset (or group ofassets) are largely independent of the cash inflowsfrom other assets (or groups of assets), an enterpriseconsiders various factors including howmanagement monitors enterprise’s operations (say:product lines, businesses, individual locations,districts or regional areas or in some other way) orhow management makes decisions about continuingor disposing of enterprise’s assets & operations.

Cash inflows from continuing use are inflows ofcash and cash equivalents received from partiesoutside the reporting enterprise. In identifyingwhether cash inflows from an asset (or group ofassets) are largely independent of the cash inflowsfrom other assets (or groups of assets), an enterpriseconsiders various factors including howmanagement monitors enterprise’s operations (say:product lines, businesses, individual locations,districts or regional areas or in some other way) orhow management makes decisions about continuingor disposing of enterprise’s assets & operations.

Naina & Co 43

68. If an active market exists for the output produced byan asset or a group of assets, this asset or group ofassets should be identified as a separate CGU, even ifsome or all of the output is used internally. If this isthe case, management’s best estimate of future marketprices for the output should be used:

(a) in determining the value in use of this CGU,when estimating the future cash inflows that relate tothe internal use of the output; and

(b) in determining the value in use of other CGUsof the reporting enterprise, when estimating the future

cash outflows that relate to the internal use of theoutput.

68. If an active market exists for the output produced byan asset or a group of assets, this asset or group ofassets should be identified as a separate CGU, even ifsome or all of the output is used internally. If this isthe case, management’s best estimate of future marketprices for the output should be used:

(a) in determining the value in use of this CGU,when estimating the future cash inflows that relate tothe internal use of the output; and

(b) in determining the value in use of other CGUsof the reporting enterprise, when estimating the future

cash outflows that relate to the internal use of theoutput.

Naina & Co 44

70. CGUs should be identified consistently from period toperiod for the same asset or types of assets, unless achange is justified.

72. RA and CA of a CGU:

The RA of a CGU is the higher of CGU’s NSP & VinU

73. The carrying amount of a CGU should be determinedconsistently with the way the RA of the CGU isdetermined.

75. CERTAIN ASSETS DIFFICULT TO INCLUDE IN CGU:

In some cases, although certain assets contribute to theestimated future cash flows of a CGU, they cannot beallocated to the CGU on a reasonable and consistentbasis. This might be the case for goodwill or corporateassets such as head office assets.

70. CGUs should be identified consistently from period toperiod for the same asset or types of assets, unless achange is justified.

72. RA and CA of a CGU:

The RA of a CGU is the higher of CGU’s NSP & VinU

73. The carrying amount of a CGU should be determinedconsistently with the way the RA of the CGU isdetermined.

75. CERTAIN ASSETS DIFFICULT TO INCLUDE IN CGU:

In some cases, although certain assets contribute to theestimated future cash flows of a CGU, they cannot beallocated to the CGU on a reasonable and consistentbasis. This might be the case for goodwill or corporateassets such as head office assets.

Naina & Co 45

78. In testing a CGU for impairment, an enterprise

should identify whether goodwill that relates to thisCGU is recognised in financial statements. If yes,enterprise should perform ‘bottom-up’ test, ie:

(i) identify whether CA of goodwill can be allocatedon a reasonable and consistent basis to the CGUunder review; and

(ii) then, compare the RA to CA & recognise anyimpairment loss in accordance with paragraph 87.

The enterprise should perform the step at (ii) aboveeven if none of the CA of goodwill can be allocatedon a reasonable and consistent basis to the CGUunder review;

78. In testing a CGU for impairment, an enterprise

should identify whether goodwill that relates to thisCGU is recognised in financial statements. If yes,enterprise should perform ‘bottom-up’ test, ie:

(i) identify whether CA of goodwill can be allocatedon a reasonable and consistent basis to the CGUunder review; and

(ii) then, compare the RA to CA & recognise anyimpairment loss in accordance with paragraph 87.

The enterprise should perform the step at (ii) aboveeven if none of the CA of goodwill can be allocatedon a reasonable and consistent basis to the CGUunder review;

Naina & Co 46

(b) ‘top-down’ test ie., the enterprise should:

(i) identify the smallest CGU that includes the CGUunder review and to which the CA of goodwillcan be allocated on a reasonable and consistentbasis and

(ii) then, compare the RA of the larger CGU to itsCA (including the carrying amount of allocatedgoodwill) and recognise any impairment loss inaccordance with paragraph 87.

(b) ‘top-down’ test ie., the enterprise should:

(i) identify the smallest CGU that includes the CGUunder review and to which the CA of goodwillcan be allocated on a reasonable and consistentbasis and

(ii) then, compare the RA of the larger CGU to itsCA (including the carrying amount of allocatedgoodwill) and recognise any impairment loss inaccordance with paragraph 87.

Naina & Co 47

79. Goodwill arising on acquisition represents a paymentmade by an acquirer in anticipation of future economicbenefits.The future economic benefits may result from synergybetween the identifiable assets acquired or from assetsthat individually do not qualify for recognition in thefinancial statements.Goodwill does not generate cash flows independentlyfrom other assets or groups of assets and, therefore, theRA of goodwill as an individual asset cannot bedetermined.As a consequence, if there is an indication that goodwillmay be impaired, RA is determined for the CGU to whichgoodwill belongs. This amount is then compared to theCA of this CGU and any impairment loss is recognised inaccordance with paragraph 87.

79. Goodwill arising on acquisition represents a paymentmade by an acquirer in anticipation of future economicbenefits.The future economic benefits may result from synergybetween the identifiable assets acquired or from assetsthat individually do not qualify for recognition in thefinancial statements.Goodwill does not generate cash flows independentlyfrom other assets or groups of assets and, therefore, theRA of goodwill as an individual asset cannot bedetermined.As a consequence, if there is an indication that goodwillmay be impaired, RA is determined for the CGU to whichgoodwill belongs. This amount is then compared to theCA of this CGU and any impairment loss is recognised inaccordance with paragraph 87.

Naina & Co 48

83. What is Corporate Asset?

Corporate assets include group or divisional assets such as thebuilding of a headquarters or a division of the enterprise,EDP equipment or a research centre. The structure of anenterprise determines whether an asset meets the definitionof corporate assets.

85. In testing CGU for impairment, an enterprise shouldidentify all corporate assets that relate to the CGU underreview. For each identified corporate asset, an enterpriseshould then apply paragraph 78, that is:

(a) if the CA of the corporate asset can be allocated on areasonable and consistent basis to the CGU under review, anenterprise should apply the ‘bottom up’ test only; and

(b) if the CA of the corporate asset cannot be allocated on areasonable and consistent basis to the CGU under review, anenterprise should apply both the ‘bottom-up’ and ‘top-down’tests.

83. What is Corporate Asset?

Corporate assets include group or divisional assets such as thebuilding of a headquarters or a division of the enterprise,EDP equipment or a research centre. The structure of anenterprise determines whether an asset meets the definitionof corporate assets.

85. In testing CGU for impairment, an enterprise shouldidentify all corporate assets that relate to the CGU underreview. For each identified corporate asset, an enterpriseshould then apply paragraph 78, that is:

(a) if the CA of the corporate asset can be allocated on areasonable and consistent basis to the CGU under review, anenterprise should apply the ‘bottom up’ test only; and

(b) if the CA of the corporate asset cannot be allocated on areasonable and consistent basis to the CGU under review, anenterprise should apply both the ‘bottom-up’ and ‘top-down’tests. Naina & Co 49

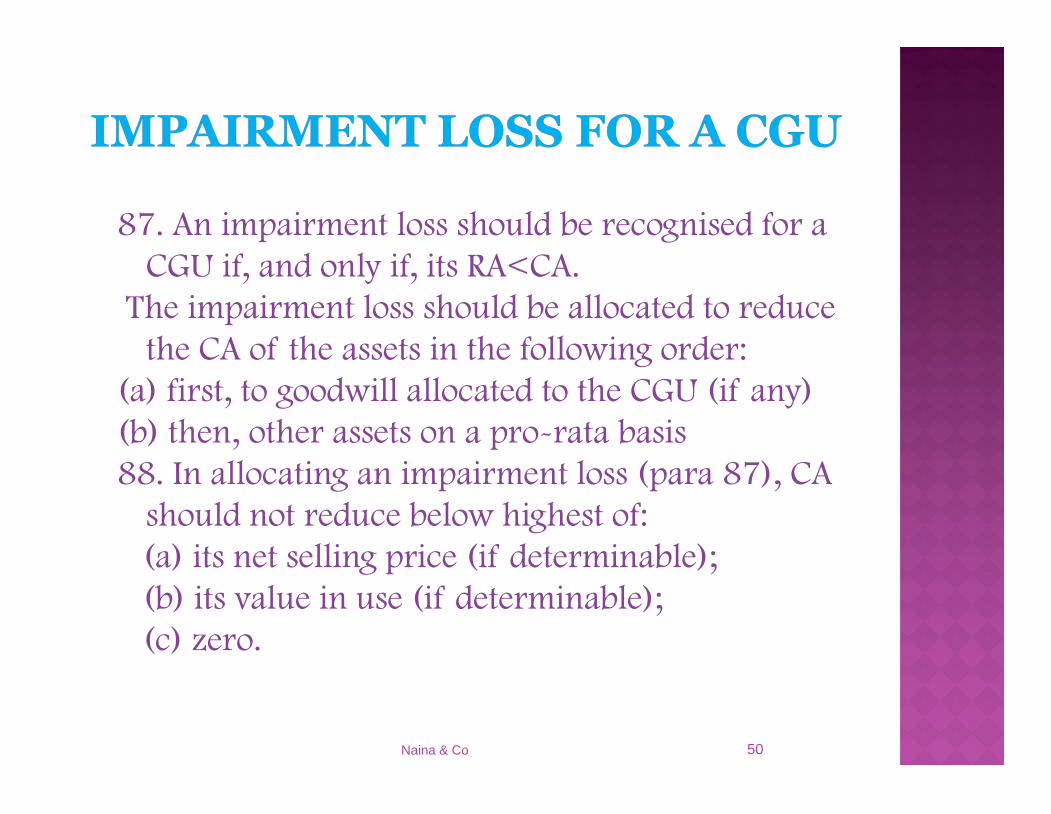

87. An impairment loss should be recognised for aCGU if, and only if, its RA<CA.

The impairment loss should be allocated to reducethe CA of the assets in the following order:

(a) first, to goodwill allocated to the CGU (if any)(b) then, other assets on a pro-rata basis88. In allocating an impairment loss (para 87), CA

should not reduce below highest of:(a) its net selling price (if determinable);(b) its value in use (if determinable);(c) zero.

87. An impairment loss should be recognised for aCGU if, and only if, its RA<CA.

The impairment loss should be allocated to reducethe CA of the assets in the following order:

(a) first, to goodwill allocated to the CGU (if any)(b) then, other assets on a pro-rata basis88. In allocating an impairment loss (para 87), CA

should not reduce below highest of:(a) its net selling price (if determinable);(b) its value in use (if determinable);(c) zero.

Naina & Co 50

94. An enterprise should assess at each B/s date whetherthere is any indication that IL recognised for an asset inprior accounting periods may no longer exist/decreased.If following indication exists, enterprise should estimateRA of asset.

External sources of information

(a) Asset’s MV increased significantly during period

(b) Significant favourable changes on enterprise takenplace in technological/market/economic or legalenvironment

(c) market interest rates decreased during period, andthose decreases are likely to affect DR used in calculatingasset’s VinU & increase RA materially;

Internal sources of information

(d) significant changes with a favourable effect on theenterprise have

94. An enterprise should assess at each B/s date whetherthere is any indication that IL recognised for an asset inprior accounting periods may no longer exist/decreased.If following indication exists, enterprise should estimateRA of asset.

External sources of information

(a) Asset’s MV increased significantly during period

(b) Significant favourable changes on enterprise takenplace in technological/market/economic or legalenvironment

(c) market interest rates decreased during period, andthose decreases are likely to affect DR used in calculatingasset’s VinU & increase RA materially;

Internal sources of information

(d) significant changes with a favourable effect on theenterprise have

Naina & Co 51

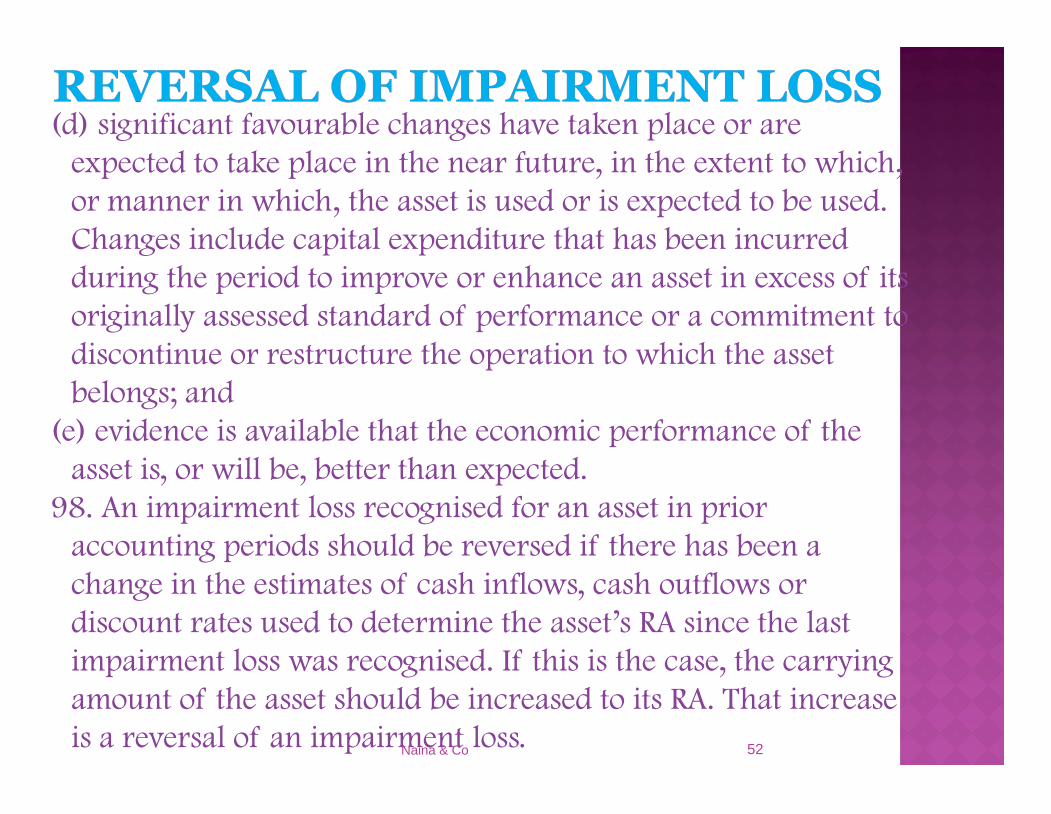

(d) significant favourable changes have taken place or areexpected to take place in the near future, in the extent to which,or manner in which, the asset is used or is expected to be used.Changes include capital expenditure that has been incurredduring the period to improve or enhance an asset in excess of itsoriginally assessed standard of performance or a commitment todiscontinue or restructure the operation to which the assetbelongs; and

(e) evidence is available that the economic performance of theasset is, or will be, better than expected.

98. An impairment loss recognised for an asset in prioraccounting periods should be reversed if there has been achange in the estimates of cash inflows, cash outflows ordiscount rates used to determine the asset’s RA since the lastimpairment loss was recognised. If this is the case, the carryingamount of the asset should be increased to its RA. That increaseis a reversal of an impairment loss.

(d) significant favourable changes have taken place or areexpected to take place in the near future, in the extent to which,or manner in which, the asset is used or is expected to be used.Changes include capital expenditure that has been incurredduring the period to improve or enhance an asset in excess of itsoriginally assessed standard of performance or a commitment todiscontinue or restructure the operation to which the assetbelongs; and

(e) evidence is available that the economic performance of theasset is, or will be, better than expected.

98. An impairment loss recognised for an asset in prioraccounting periods should be reversed if there has been achange in the estimates of cash inflows, cash outflows ordiscount rates used to determine the asset’s RA since the lastimpairment loss was recognised. If this is the case, the carryingamount of the asset should be increased to its RA. That increaseis a reversal of an impairment loss.Naina & Co 52

99. A reversal of an impairment loss reflects an increase in theestimated service potential of an asset, either from use or sale.

Eg: (a) a change in the basis for RA (i.e., whether RA is based onnet selling price or value in use);

(b) if RA was based on value in use: a change in the amountor timing of estimated future cash flows or in the discountrate; or

(c) if RA was based on net selling price: a change in estimateof the components of net selling price.

100.WHY NO REVERSAL EVEN IF RA>CA

An asset’s VinU may become greater than the asset’s CAsimply because PV of future cash inflows increases as theybecome closer. However, service potential of asset has notincreased. Therefore, an impairment loss is not reversed justbecause of passage of time, even if RA>CA.

99. A reversal of an impairment loss reflects an increase in theestimated service potential of an asset, either from use or sale.

Eg: (a) a change in the basis for RA (i.e., whether RA is based onnet selling price or value in use);

(b) if RA was based on value in use: a change in the amountor timing of estimated future cash flows or in the discountrate; or

(c) if RA was based on net selling price: a change in estimateof the components of net selling price.

100.WHY NO REVERSAL EVEN IF RA>CA

An asset’s VinU may become greater than the asset’s CAsimply because PV of future cash inflows increases as theybecome closer. However, service potential of asset has notincreased. Therefore, an impairment loss is not reversed justbecause of passage of time, even if RA>CA.

Naina & Co 53

The increased CA of an asset due to a reversal ofimpairment loss should not exceed CA that would havebeen determined (net of amortisation or depreciation)had no impairment loss been recognised for the asset inprior accounting periods.

103. A reversal of an impairment loss for an asset shouldbe recognised as income immediately in the statement ofprofit and loss, unless the asset is carried at revaluedamount in which case any reversal of an impairmentloss on a revalued asset should be treated as arevaluation increase under AS-10.

The increased CA of an asset due to a reversal ofimpairment loss should not exceed CA that would havebeen determined (net of amortisation or depreciation)had no impairment loss been recognised for the asset inprior accounting periods.

103. A reversal of an impairment loss for an asset shouldbe recognised as income immediately in the statement ofprofit and loss, unless the asset is carried at revaluedamount in which case any reversal of an impairmentloss on a revalued asset should be treated as arevaluation increase under AS-10.

Naina & Co 54

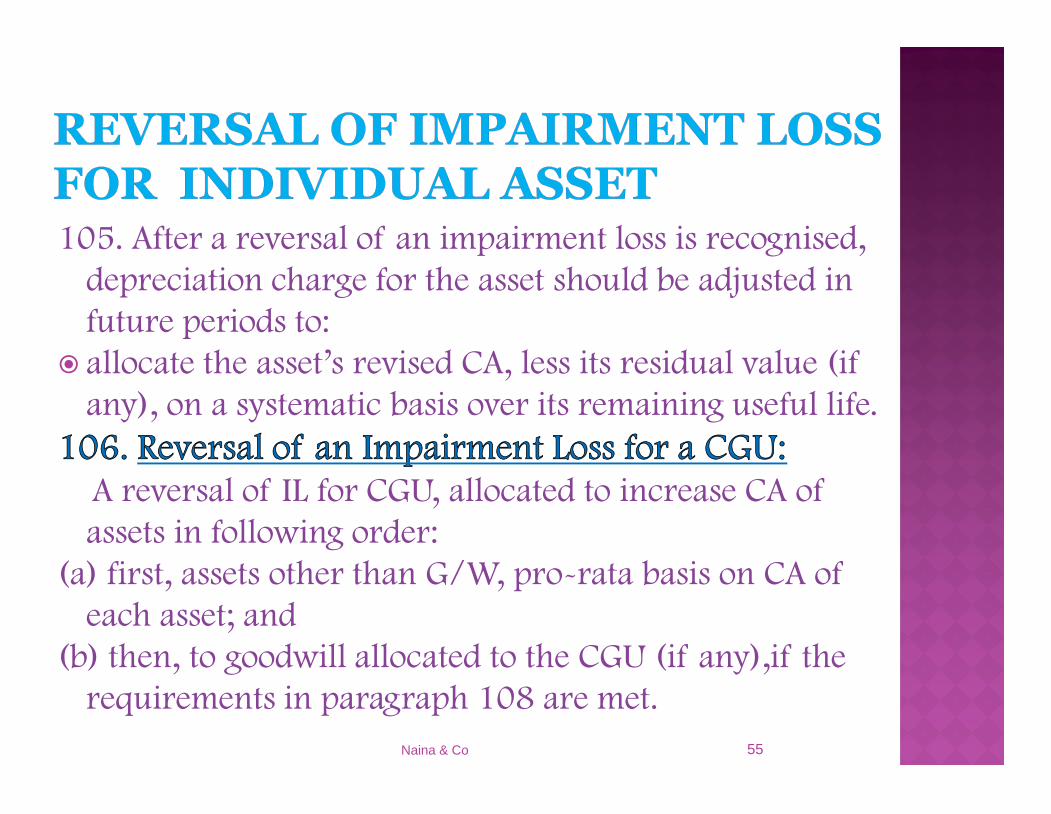

105. After a reversal of an impairment loss is recognised,depreciation charge for the asset should be adjusted infuture periods to:

allocate the asset’s revised CA, less its residual value (ifany), on a systematic basis over its remaining useful life.

106. Reversal of an Impairment Loss for a CGU:A reversal of IL for CGU, allocated to increase CA ofassets in following order:

(a) first, assets other than G/W, pro-rata basis on CA ofeach asset; and

(b) then, to goodwill allocated to the CGU (if any),if therequirements in paragraph 108 are met.

105. After a reversal of an impairment loss is recognised,depreciation charge for the asset should be adjusted infuture periods to:

allocate the asset’s revised CA, less its residual value (ifany), on a systematic basis over its remaining useful life.

106. Reversal of an Impairment Loss for a CGU:A reversal of IL for CGU, allocated to increase CA ofassets in following order:

(a) first, assets other than G/W, pro-rata basis on CA ofeach asset; and

(b) then, to goodwill allocated to the CGU (if any),if therequirements in paragraph 108 are met.

Naina & Co 55

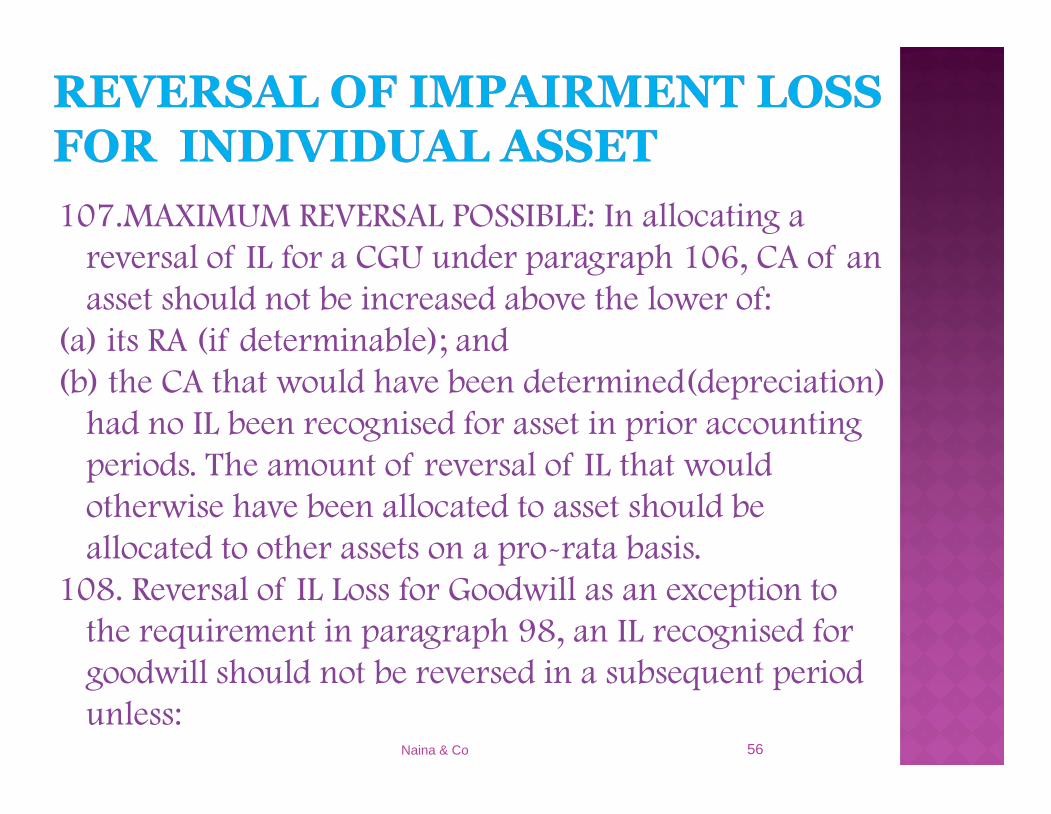

107.MAXIMUM REVERSAL POSSIBLE: In allocating areversal of IL for a CGU under paragraph 106, CA of anasset should not be increased above the lower of:

(a) its RA (if determinable); and(b) the CA that would have been determined(depreciation)

had no IL been recognised for asset in prior accountingperiods. The amount of reversal of IL that wouldotherwise have been allocated to asset should beallocated to other assets on a pro-rata basis.

108. Reversal of IL Loss for Goodwill as an exception tothe requirement in paragraph 98, an IL recognised forgoodwill should not be reversed in a subsequent periodunless:

107.MAXIMUM REVERSAL POSSIBLE: In allocating areversal of IL for a CGU under paragraph 106, CA of anasset should not be increased above the lower of:

(a) its RA (if determinable); and(b) the CA that would have been determined(depreciation)

had no IL been recognised for asset in prior accountingperiods. The amount of reversal of IL that wouldotherwise have been allocated to asset should beallocated to other assets on a pro-rata basis.

108. Reversal of IL Loss for Goodwill as an exception tothe requirement in paragraph 98, an IL recognised forgoodwill should not be reversed in a subsequent periodunless:

Naina & Co 56

(a) the impairment loss was caused by a specific externalevent of an exceptional nature that is not expected torecur; and

(b) subsequent external events have occurred that reversethe effect of that event.

109. EXTERNAL & INTERNAL GOODWILL AS 26, Intangible Assets, prohibits the recognition of

internally generated goodwill. Any subsequent increasein the RA of goodwill is likely to be an increase ininternally generated goodwill, unless the increase relatesclearly to the reversal of the effect of a specific externalevent of an exceptional nature.

(a) the impairment loss was caused by a specific externalevent of an exceptional nature that is not expected torecur; and

(b) subsequent external events have occurred that reversethe effect of that event.

109. EXTERNAL & INTERNAL GOODWILL AS 26, Intangible Assets, prohibits the recognition of

internally generated goodwill. Any subsequent increasein the RA of goodwill is likely to be an increase ininternally generated goodwill, unless the increase relatesclearly to the reversal of the effect of a specific externalevent of an exceptional nature.

Naina & Co 57

112. in accordance with this Statement, an enterpriseestimates the RA of each asset of the discontinuingoperation and recognises an impairment loss or reversalof a prior impairment loss, if any.

113. Firstly, an enterprise determines whether the RA of anasset of a discontinuing operation is assessed for theindividual asset or for the asset’s CGU.

112. in accordance with this Statement, an enterpriseestimates the RA of each asset of the discontinuingoperation and recognises an impairment loss or reversalof a prior impairment loss, if any.

113. Firstly, an enterprise determines whether the RA of anasset of a discontinuing operation is assessed for theindividual asset or for the asset’s CGU.

Naina & Co 58

For example:

(a) Enterprise sells the discontinuing operationsubstantially in Therefore, RA is determined for thediscontinuing operation as a whole and an impairmentloss, if any, is allocated among the assets of thediscontinuing operation.

(b) if the enterprise disposes of the discontinuingoperation as piecemeal sales, RA is determined forindividual assets.

115. A price in a binding sale agreement is the bestevidence of an asset’s (CGU’s) net selling price or valuein use.

For example:

(a) Enterprise sells the discontinuing operationsubstantially in Therefore, RA is determined for thediscontinuing operation as a whole and an impairmentloss, if any, is allocated among the assets of thediscontinuing operation.

(b) if the enterprise disposes of the discontinuingoperation as piecemeal sales, RA is determined forindividual assets.

115. A price in a binding sale agreement is the bestevidence of an asset’s (CGU’s) net selling price or valuein use.

Naina & Co 59

117. For each class of assets, the financial statementsshould disclose:

Amount of impairment losses recognised in thestatement of profit and loss during the period and theline item(s) of the statement of profit and loss in whichthose impairment losses are included;

The amount of reversals of impairment losses recognisedin the statement of profit and loss during the period andthe line item(s) of the statement of profit and loss inwhich those impairment losses are reversed;

Amount of impairment losses recognised directly againstrevaluation surplus during the period; and

Amount of reversals of impairment losses recogniseddirectly in revaluation surplus during the period.

117. For each class of assets, the financial statementsshould disclose:

Amount of impairment losses recognised in thestatement of profit and loss during the period and theline item(s) of the statement of profit and loss in whichthose impairment losses are included;

The amount of reversals of impairment losses recognisedin the statement of profit and loss during the period andthe line item(s) of the statement of profit and loss inwhich those impairment losses are reversed;

Amount of impairment losses recognised directly againstrevaluation surplus during the period; and

Amount of reversals of impairment losses recogniseddirectly in revaluation surplus during the period.

Naina & Co 60

118. A class of assets is a grouping of assets of similarnature and use in an enterprise’s operations.

119. The information required in paragraph 117 maybe presented with other information disclosed for theclass of assets. For example, this information may beincluded in a reconciliation of the carrying amountof fixed assets, at the beginning and end of theperiod, as required under AS 10.

120. An enterprise that applies AS 17, SegmentReporting, should disclose following for eachreportable (as defined in AS 17):

(a) Amount of impairment losses recognised in thestatement of profit and loss and directly againstrevaluation surplus during period; and

118. A class of assets is a grouping of assets of similarnature and use in an enterprise’s operations.

119. The information required in paragraph 117 maybe presented with other information disclosed for theclass of assets. For example, this information may beincluded in a reconciliation of the carrying amountof fixed assets, at the beginning and end of theperiod, as required under AS 10.

120. An enterprise that applies AS 17, SegmentReporting, should disclose following for eachreportable (as defined in AS 17):

(a) Amount of impairment losses recognised in thestatement of profit and loss and directly againstrevaluation surplus during period; and

Naina & Co 61

the amount of reversals of impairment lossesrecognised in the statement of profit and lossand directly in revaluation surplus during theperiod.

121. If an impairment loss for an individualasset or a CGU is recognised or reversed duringthe period and is material to the financialstatements of the reporting enterprise as awhole, an enterprise should disclose:

(a) the events and circumstances that led to therecognition or reversal of the impairment loss;

the amount of reversals of impairment lossesrecognised in the statement of profit and lossand directly in revaluation surplus during theperiod.

121. If an impairment loss for an individualasset or a CGU is recognised or reversed duringthe period and is material to the financialstatements of the reporting enterprise as awhole, an enterprise should disclose:

(a) the events and circumstances that led to therecognition or reversal of the impairment loss;

Naina & Co 62

(b) the amount of the impairment loss recognisedor reversed;

(c) for an individual asset:

(i) the nature of the asset; and

(ii) the reportable segment to which the assetbelongs,

(d) for a CGU:

(i) a description of the CGU (such as

whether it is a product line, a plant, a businessoperation,

a geographical area, a reportable segment asdefined in AS 17 or other);

(b) the amount of the impairment loss recognisedor reversed;

(c) for an individual asset:

(i) the nature of the asset; and

(ii) the reportable segment to which the assetbelongs,

(d) for a CGU:

(i) a description of the CGU (such as

whether it is a product line, a plant, a businessoperation,

a geographical area, a reportable segment asdefined in AS 17 or other);

Naina & Co 63

(ii) the amount of the impairment loss recognisedor reversed by class of assets and by reportablesegment based on the enterprise’s primaryformat (as defined in AS 17); and

(iii) if the aggregation of assets for identifying thecash generating unit has changed since theprevious estimate of the CGU’s RA (if any), theenterprise should describe the current andformer way of aggregating assets and thereasons for changing the

(ii) the amount of the impairment loss recognisedor reversed by class of assets and by reportablesegment based on the enterprise’s primaryformat (as defined in AS 17); and

(iii) if the aggregation of assets for identifying thecash generating unit has changed since theprevious estimate of the CGU’s RA (if any), theenterprise should describe the current andformer way of aggregating assets and thereasons for changing the

Naina & Co 64

way the CGU is identified;

(e) whether the RA of the asset (cash-generating

unit) is its net selling price or its value in use;

(f) if RA is net selling price, the basis used todetermine net selling price (such as whether sellingprice was determined by reference to an activemarket or in some other way); and

(g) if RA is value in use, the discount rate(s) used inthe current estimate and previous estimate (if any)of value in use.

122. If impairment losses recognised (reversed)during the period are material in aggregate to thefinancial statements of the reporting enterprise asa whole, an enterprise should disclose a briefdescription

way the CGU is identified;

(e) whether the RA of the asset (cash-generating

unit) is its net selling price or its value in use;

(f) if RA is net selling price, the basis used todetermine net selling price (such as whether sellingprice was determined by reference to an activemarket or in some other way); and

(g) if RA is value in use, the discount rate(s) used inthe current estimate and previous estimate (if any)of value in use.

122. If impairment losses recognised (reversed)during the period are material in aggregate to thefinancial statements of the reporting enterprise asa whole, an enterprise should disclose a briefdescription

Naina & Co 65

of the following:

(a) the main classes of assets affected byimpairment losses (reversals of impairmentlosses) for which no information is disclosedunder paragraph 121; and the main eventsand circumstances that led to therecognition (reversal) of these impairmentlosses for which no information is disclosedunder paragraph 121.

123. An enterprise is encouraged to disclosekey assumptions used to determine the RA ofassets (CGUs) during the period.

of the following:

(a) the main classes of assets affected byimpairment losses (reversals of impairmentlosses) for which no information is disclosedunder paragraph 121; and the main eventsand circumstances that led to therecognition (reversal) of these impairmentlosses for which no information is disclosedunder paragraph 121.

123. An enterprise is encouraged to disclosekey assumptions used to determine the RA ofassets (CGUs) during the period.

Naina & Co 66

Transitional Provisions

124. On the date of this Statement becomingmandatory, an enterprise should assess whetherthere is any indication that an asset may be impaired(see paragraphs 5-13). If any such indication exists,the enterprise should determine impairment loss, ifany, in accordance with this Statement. Theimpairment loss, so determined, should be adjustedagainst opening balance of revenue reserves beingthe accumulated impairment loss relating to periodsprior to this Statement becoming mandatory unlessthe impairment loss is on a revalued asset. Animpairment loss on a revalued asset should berecognised directly against any revaluation surplusfor the asset to the extent that the impairment

Transitional Provisions

124. On the date of this Statement becomingmandatory, an enterprise should assess whetherthere is any indication that an asset may be impaired(see paragraphs 5-13). If any such indication exists,the enterprise should determine impairment loss, ifany, in accordance with this Statement. Theimpairment loss, so determined, should be adjustedagainst opening balance of revenue reserves beingthe accumulated impairment loss relating to periodsprior to this Statement becoming mandatory unlessthe impairment loss is on a revalued asset. Animpairment loss on a revalued asset should berecognised directly against any revaluation surplusfor the asset to the extent that the impairment

Naina & Co 67

loss does not exceed the amount held in therevaluation surplus for that same asset. If theimpairment loss exceeds the amount held in therevaluation surplus for that same asset, theexcess should be adjusted against openingbalance of revenue reserves.

125. Any impairment loss arising after the dateof this Statement becoming mandatory shouldbe recognised in accordance with thisStatement (i.e., in the statement of profit andloss unless an asset is carried at revaluedamount. An impairment loss on a revaluedasset should be treated as a revaluationdecrease).

loss does not exceed the amount held in therevaluation surplus for that same asset. If theimpairment loss exceeds the amount held in therevaluation surplus for that same asset, theexcess should be adjusted against openingbalance of revenue reserves.

125. Any impairment loss arising after the dateof this Statement becoming mandatory shouldbe recognised in accordance with thisStatement (i.e., in the statement of profit andloss unless an asset is carried at revaluedamount. An impairment loss on a revaluedasset should be treated as a revaluationdecrease).

Naina & Co 68