depreciation and expensing opportunities under tax reform€¦ · non-corporate business losses...

TRANSCRIPT

©20

18 C

lifto

nLar

sonA

llen

LLP

CliftonLarsonAllen (CLA)

Depreciation and Expensing Opportunities Under Tax Reform

©20

18 C

lifto

nLar

sonA

llen

LLP

DisclaimersThe information contained herein is general in nature and is not intended, and should not be construed, as legal, accounting, or tax advice or opinion provided by CliftonLarsonAllen LLP to the user. The user also is cautioned that this material may not be applicable to, or suitable for, the user’s specific circumstances or needs, and may require consideration of non-tax and other tax factors if any action is to be contemplated. The user should contact his or her CliftonLarsonAllen LLP or other tax professional prior to taking any action based upon this information. CliftonLarsonAllen LLP assumes no obligation to inform the user of any changes in tax laws or other factors that could affect the information contained herein.

2

©20

18 C

lifto

nLar

sonA

llen

LLP

Housekeeping• If you are experiencing technical difficulties, please dial: 800-422-3623.

• Q&A session will be held at the end of the presentation.– Your questions can be submitted via the Questions Function at any time during the presentation.

• The PowerPoint presentation, as well as the webinar recording, will be sent to you within the next 10 business days.

• For future webinar invitations, subscribe at CLAconnect.com/subscribe.

• Please complete our online survey.

3

©20

18 C

lifto

nLar

sonA

llen

LLP

CPE Requirements• Answer the polling questions

• Remain logged in for at least 50 minutes

• If you are participating in a group, complete the CPE sign-in sheet and return within two business days

– Contact [email protected]

• Allow four weeks for receipt of your certificate; it will be sent to you via email from [email protected].

* This webinar, once recorded, has not been developed into a self study course. Therefore, watching the recording will not qualify for CPE credit.

4

©20

18 C

lifto

nLar

sonA

llen

LLP

About CliftonLarsonAllen

• A professional services firm with three distinct business lines– Wealth Advisory– Outsourcing– Audit, Tax, and Consulting

• More than 5,400 employees• Offices coast to coast• We serve over 5,000 privately held construction contractorsInvestment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC.

5

©20

18 C

lifto

nLar

sonA

llen

LLP

Learning Objectives

At the end of this session, you will be able to:• Recognize key changes to the depreciation and expensing rules under the

TCJA compared to the pre-reform law• Identify techniques to make tax-efficient investments in equipment and

your buildings• Recognize potential technical corrections Congress is evaluating related to

the new depreciation laws• Determine whether opportunities exist to capture benefits for 2017 and

prior years at the higher pre-reform tax rates.

6

©20

18 C

lifto

nLar

sonA

llen

LLP

Speaker Introductions

Dan GreenhagenDan is a Manager within CliftonLarsonAllen’s National Tax Office Team assists clients nationally with technical services, tax law development and planning, cost segregation and fixed asset related projects. With more than 15 years of experience, Dan has supported countless clients through tax law changes. This extensive experience has given him a deep understanding of the issues and concerns tax reform brings to private sector business in today’s challenging environment.

7

©20

18 C

lifto

nLar

sonA

llen

LLP

About Today’s Presenters

Perry McGowan is a professional tax advisor in CLA's Construction and Real Estate group in Minneapolis. He provides advisory services focused on the tax planning issues of construction contractors, real estate owners, and project designers.

Perry applies his 35 years of experience to family-owned businesses and their CPAs, and provides thoughtful tax strategies, transaction design, and tax risk analysis. He serves as a national resource to the industry practice and a tax liaison to industry associations.

8

Perry McGowanTechnical Director, CLA Minneapolis

©20

18 C

lifto

nLar

sonA

llen

LLP

9

The Backdrop of Cost Recovery“What’s the deduction worth to me?

10

©20

18 C

lifto

nLar

sonA

llen

LLP

Tax Cuts and Jobs Act of 2017Signed 12/22/2017

Generally effective 1/1/18Depreciation rules generally effective 9/28/2017

Guidance from the IRSProposed Regulations 8/3/2018 for Asset ExpensingProposed Regulations 8/7/2018 for 199A

11

©20

18 C

lifto

nLar

sonA

llen

LLP

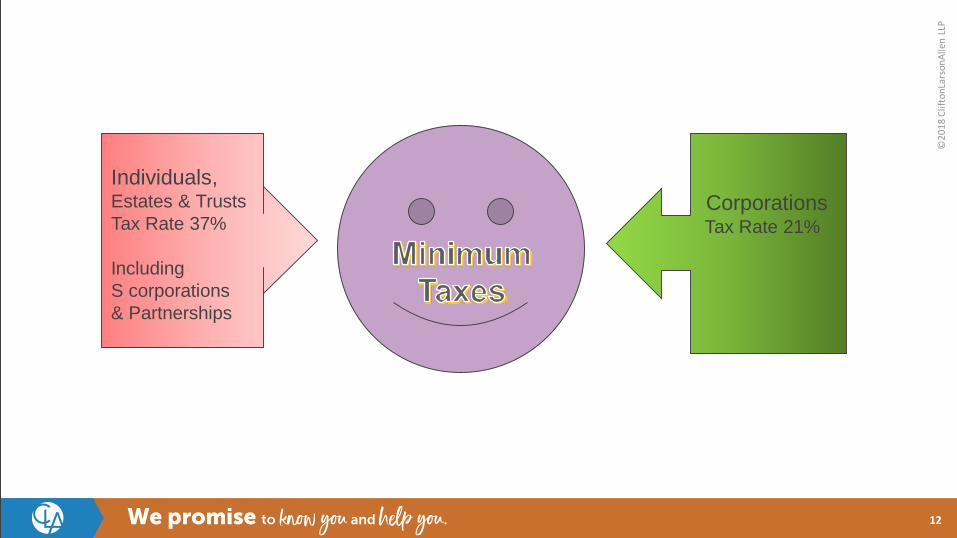

12

Individuals, Estates & TrustsTax Rate 37%

IncludingS corporations& Partnerships

CorporationsTax Rate 21%

©20

18 C

lifto

nLar

sonA

llen

LLP

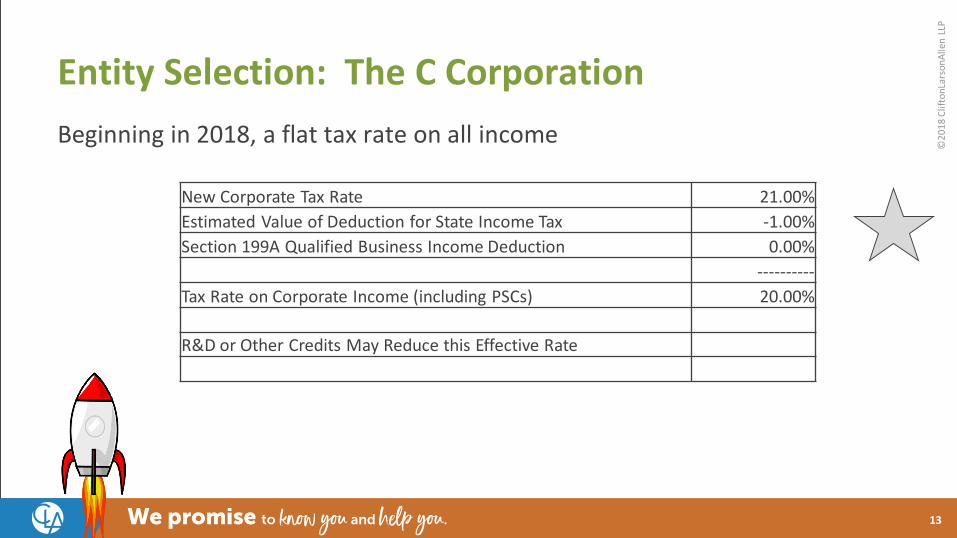

Entity Selection: The C CorporationBeginning in 2018, a flat tax rate on all income

13

New Corporate Tax Rate 21.00%Estimated Value of Deduction for State Income Tax -1.00%Section 199A Qualified Business Income Deduction 0.00%

----------Tax Rate on Corporate Income (including PSCs) 20.00%

R&D or Other Credits May Reduce this Effective Rate

©20

18 C

lifto

nLar

sonA

llen

LLP

Entity Selection: Individuals

14

Taxable Income Post-Reform Tax Average Rate30,000 3,219 10.73%50,000 5,619 11.24%70,000 8,019 11.46%

100,000 13,879 13.88%150,000 24,879 16.59%200,000 36,579 18.29%300,000 60,579 20.19%400,000 91,379 22.84%500,000 126,379 25.28%700,000 198,379 28.34%

1,000,000 309,379 30.94%1,500,000 494,379 32.96%2,000,000 679,379 33.97%3,000,000 1,049,379 34.98%4,000,000 1,419,379 35.48%5,000,000 1,789,379 35.79%7,000,000 2,529,379 36.13%

10,000,000 3,639,379 36.39%

MFJoint Rates

©20

18 C

lifto

nLar

sonA

llen

LLP

Entity Selection: Individuals

15

MFJoint Rates

Taxable Income Post-Reform Tax Average Rate Add Full 199A30,000 3,219 10.73% 8.58%50,000 5,619 11.24% 8.99%70,000 8,019 11.46% 9.16%

100,000 13,879 13.88% 11.10%150,000 24,879 16.59% 13.27%200,000 36,579 18.29% 14.63%300,000 60,579 20.19% 16.15%400,000 91,379 22.84% 18.28%500,000 126,379 25.28% 20.22%700,000 198,379 28.34% 22.67%

1,000,000 309,379 30.94% 24.75%1,500,000 494,379 32.96% 26.37%2,000,000 679,379 33.97% 27.18%3,000,000 1,049,379 34.98% 27.98%4,000,000 1,419,379 35.48% 28.39%5,000,000 1,789,379 35.79% 28.63%7,000,000 2,529,379 36.13% 28.91%

10,000,000 3,639,379 36.39% 29.12%

©20

18 C

lifto

nLar

sonA

llen

LLP

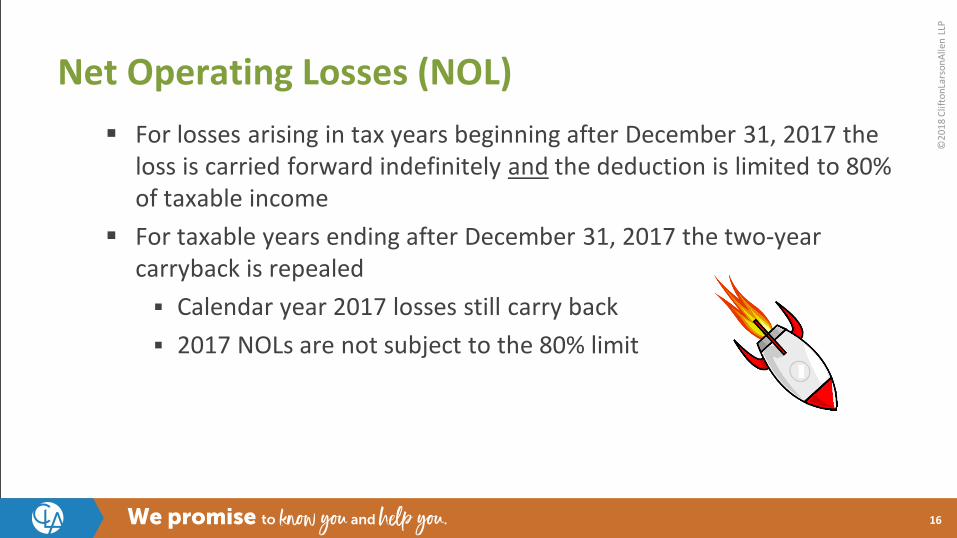

Net Operating Losses (NOL) For losses arising in tax years beginning after December 31, 2017 the

loss is carried forward indefinitely and the deduction is limited to 80% of taxable income

For taxable years ending after December 31, 2017 the two-year carryback is repealed Calendar year 2017 losses still carry back 2017 NOLs are not subject to the 80% limit

16

©20

18 C

lifto

nLar

sonA

llen

LLP

Non-Corporate Business Losses

For years beginning after 12/31/17 and before 1/1/26 an “excess business loss” is a carryforward NOL item

An EBL is the excess of the aggregate business deductions over the sum of gross income or gain from such business plus $500,000 MFJ ($250,000 Single)

Limit is applied at the 1040 level to aggregate losses Compute aggregate losses after passive limits are applied

17

©20

18 C

lifto

nLar

sonA

llen

LLP

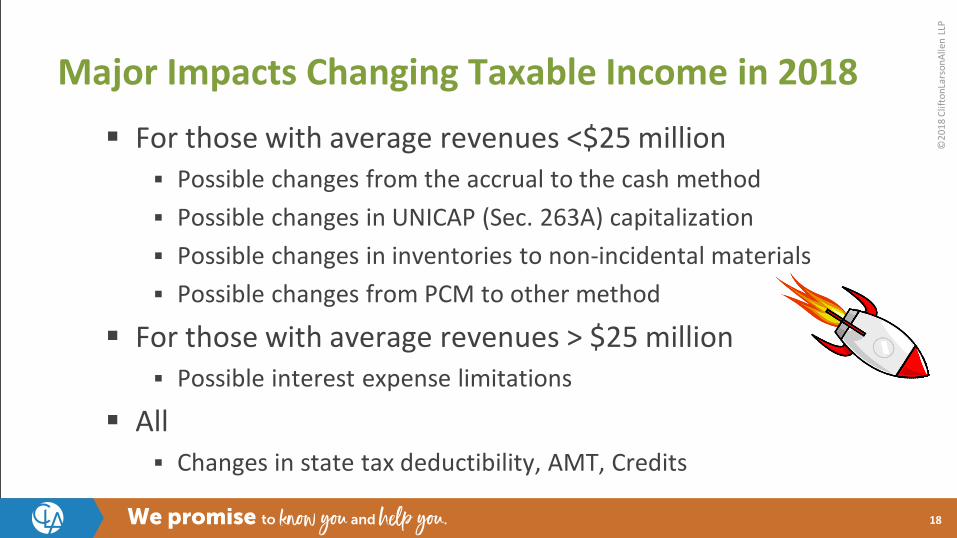

Major Impacts Changing Taxable Income in 2018

For those with average revenues <$25 million Possible changes from the accrual to the cash method Possible changes in UNICAP (Sec. 263A) capitalization Possible changes in inventories to non-incidental materials Possible changes from PCM to other method

For those with average revenues > $25 million Possible interest expense limitations

All Changes in state tax deductibility, AMT, Credits

18

Cost Recovery“Can I write it off?

19

©20

18 C

lifto

nLar

sonA

llen

LLP

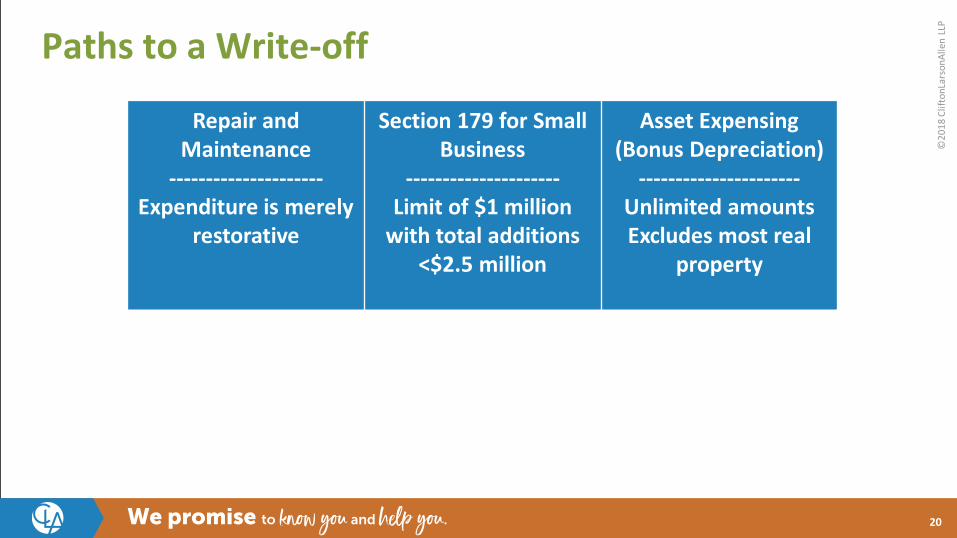

Paths to a Write-off

20

Repair and Maintenance

---------------------Expenditure is merely

restorative

Section 179 for Small Business

---------------------Limit of $1 million

with total additions <$2.5 million

Asset Expensing (Bonus Depreciation)

----------------------Unlimited amountsExcludes most real

property

©20

18 C

lifto

nLar

sonA

llen

LLP

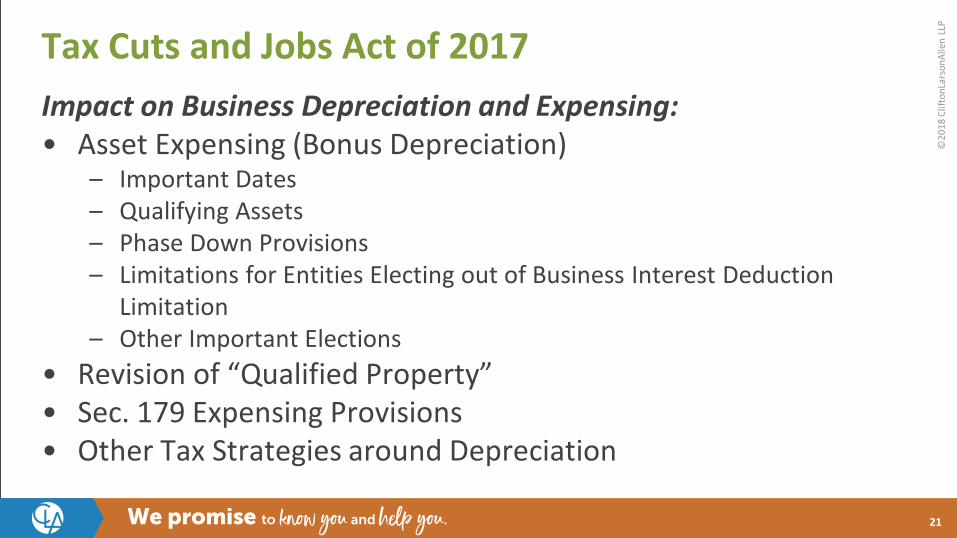

Tax Cuts and Jobs Act of 2017Impact on Business Depreciation and Expensing:• Asset Expensing (Bonus Depreciation)

– Important Dates– Qualifying Assets– Phase Down Provisions– Limitations for Entities Electing out of Business Interest Deduction

Limitation– Other Important Elections

• Revision of “Qualified Property”• Sec. 179 Expensing Provisions• Other Tax Strategies around Depreciation

21

©20

18 C

lifto

nLar

sonA

llen

LLP

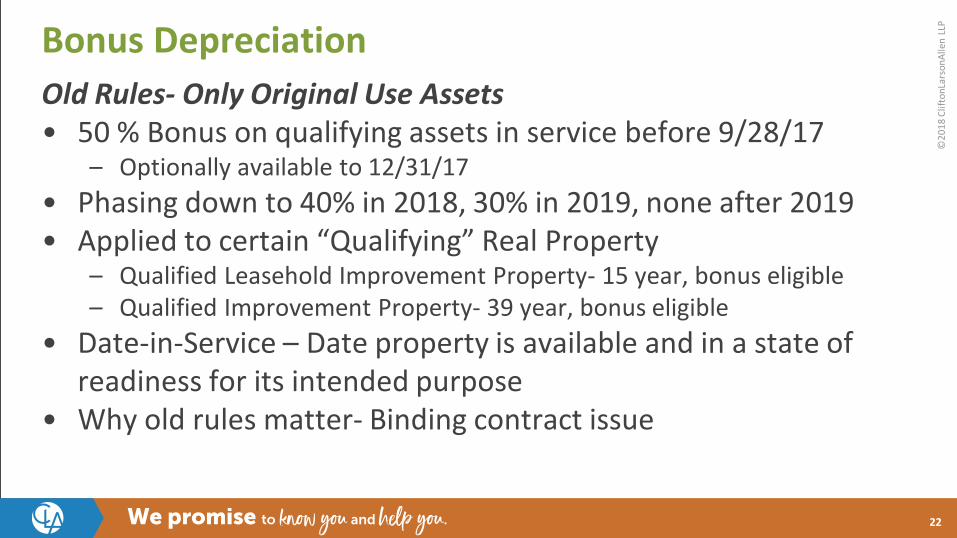

Bonus DepreciationOld Rules- Only Original Use Assets• 50 % Bonus on qualifying assets in service before 9/28/17

– Optionally available to 12/31/17• Phasing down to 40% in 2018, 30% in 2019, none after 2019• Applied to certain “Qualifying” Real Property

– Qualified Leasehold Improvement Property- 15 year, bonus eligible– Qualified Improvement Property- 39 year, bonus eligible

• Date-in-Service – Date property is available and in a state of readiness for its intended purpose

• Why old rules matter- Binding contract issue

22

©20

18 C

lifto

nLar

sonA

llen

LLP

Summary of Old Rules for Building Improvements

Building Improvements- For Additions In 2016 & 2017Recovery

Period50% Bonus as

QIP?Section

179?• Qualified Improvement Property: ‒ Interior Improvements- Not elevator/escalator, or structural 39 yr. Yes No‒ Exterior or Structural Modifications 39 yr. No No

• Qualified Leasehold Improvement Property (Subject to Lease Agreement)‒ Unrelated lessor–lessee (QLIP) & bldg. > 3 yrs. – Interior Only 15 yr. Yes Yes/w limit‒ Related lessor–lessee (QIP) or bldg. < 3 yrs. – Bonus on Interior Only 39 yr. Yes No

• Qualified Restaurant Property:‒ Exterior 15 yr. No Yes/w limit‒ Interior: New construction 15 yr. No Yes/w limit‒ Interior: Bldg. previously in service 15 yr. Yes Yes/w limit

• Qualified Retail Improvement Property:‒ Bldg. > 3 yrs. in service & retailing goods 15 yr. Yes Yes‒ Bldg. < 3 yrs. in service or retailing services 39 yr. Yes No

23

Rev. Proc. 2015-56 Provides Additional Incentives for Retail & Restaurants

©20

18 C

lifto

nLar

sonA

llen

LLPBonus Depreciation- Old Rules

Important Rules on “Qualified Property”• Qualified Leasehold Improvements- 15 year tax life and bonus.

– Building at least 3 years old at time of improvement– Subject to Lease agreement with unrelated party– Interior improvements (cannot be structural or elevators/escalators)

• Qualified Improvement Property- More liberal, plus bonus.– Any interior, non-structural, improvement to a building already placed

into service- 39 year but bonus eligible– Only applicable in 2016 & 2017

24

©20

18 C

lifto

nLar

sonA

llen

LLP

Example – Qualified Improvement Property- Old Rules

25

©20

18 C

lifto

nLar

sonA

llen

LLP

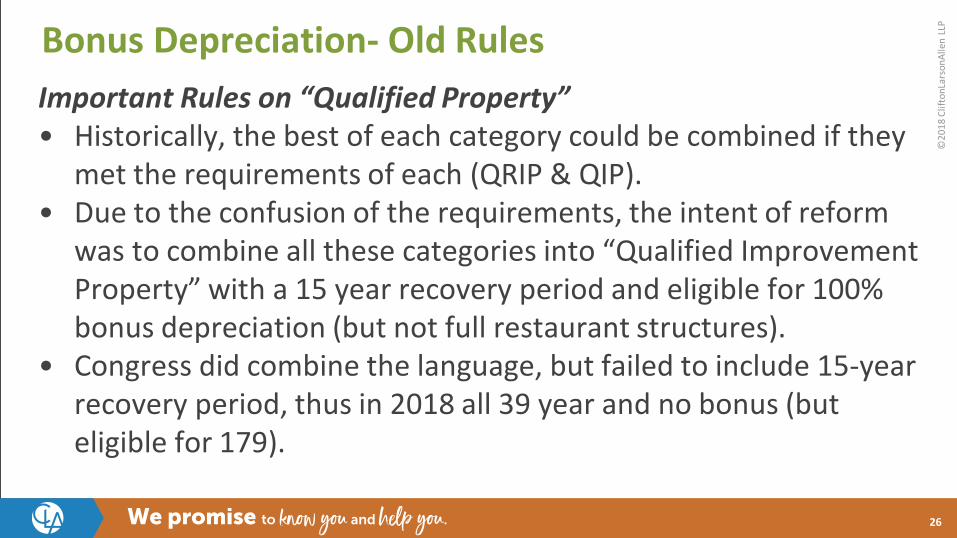

Bonus Depreciation- Old RulesImportant Rules on “Qualified Property”• Historically, the best of each category could be combined if they

met the requirements of each (QRIP & QIP).• Due to the confusion of the requirements, the intent of reform

was to combine all these categories into “Qualified Improvement Property” with a 15 year recovery period and eligible for 100% bonus depreciation (but not full restaurant structures).

• Congress did combine the language, but failed to include 15-year recovery period, thus in 2018 all 39 year and no bonus (but eligible for 179).

26

©20

18 C

lifto

nLar

sonA

llen

LLP

Bonus Depreciation- Old RulesImportant Rules on “Qualified Property”• Qualified Retail Improvement Property- Different rules in

different prior years. If qualifying, 15 year tax life, but no bonus.– Building at least 3 years old at time of improvement– Interior improvements (cannot be structural or elevators/escalators)– Must be part of area dedicated to the sales of tangible property

• Qualified Restaurant Property- 15 year tax life, but no bonus– Includes entire building– Includes new buildings and acquisitions

27

©20

18 C

lifto

nLar

sonA

llen

LLP

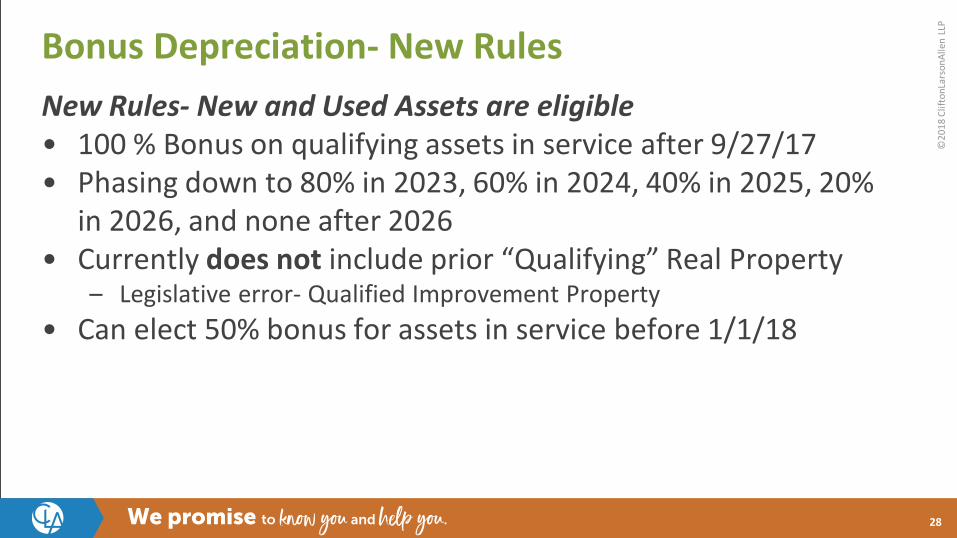

Bonus Depreciation- New RulesNew Rules- New and Used Assets are eligible• 100 % Bonus on qualifying assets in service after 9/27/17• Phasing down to 80% in 2023, 60% in 2024, 40% in 2025, 20%

in 2026, and none after 2026• Currently does not include prior “Qualifying” Real Property

– Legislative error- Qualified Improvement Property• Can elect 50% bonus for assets in service before 1/1/18

28

©20

18 C

lifto

nLar

sonA

llen

LLP

Bonus Depreciation- New RulesSection 754 Step-up May Qualify Under Proposed Regs• Section 743(b) step-ups on partner to partner sales qualify• Section 734(b) step-ups on partnership redemptions do not

qualify

29

©20

18 C

lifto

nLar

sonA

llen

LLP

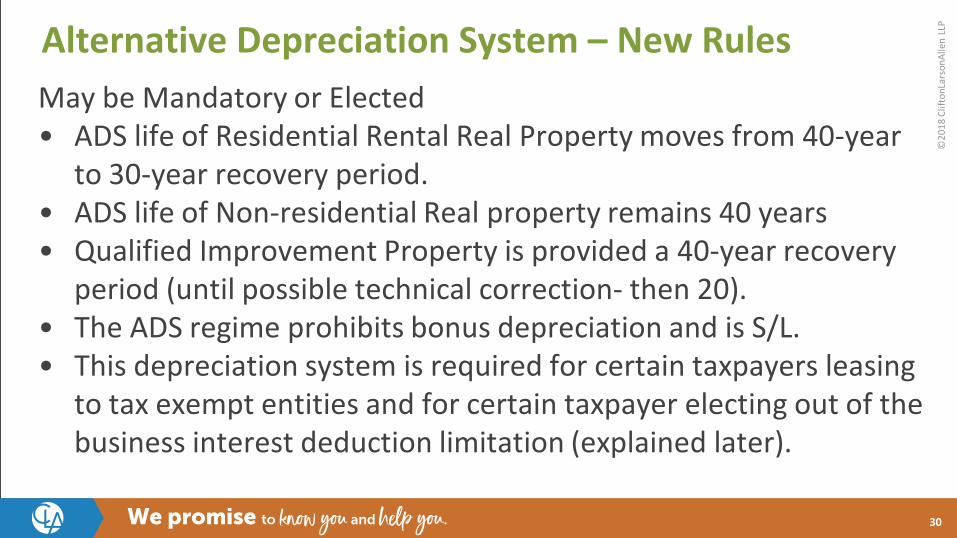

Alternative Depreciation System – New RulesMay be Mandatory or Elected• ADS life of Residential Rental Real Property moves from 40-year

to 30-year recovery period.• ADS life of Non-residential Real property remains 40 years• Qualified Improvement Property is provided a 40-year recovery

period (until possible technical correction- then 20).• The ADS regime prohibits bonus depreciation and is S/L.• This depreciation system is required for certain taxpayers leasing

to tax exempt entities and for certain taxpayer electing out of the business interest deduction limitation (explained later).

30

©20

18 C

lifto

nLar

sonA

llen

LLP

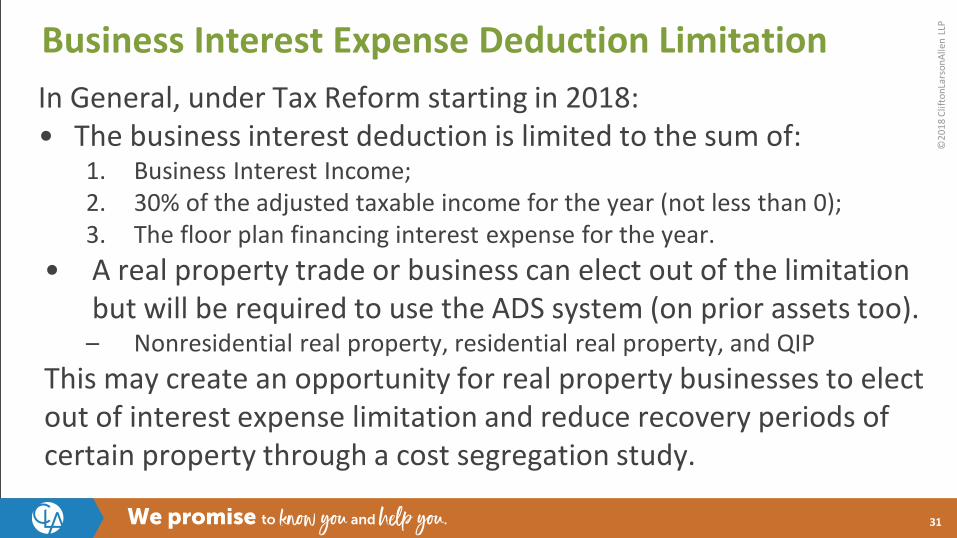

Business Interest Expense Deduction LimitationIn General, under Tax Reform starting in 2018:• The business interest deduction is limited to the sum of:

1. Business Interest Income;2. 30% of the adjusted taxable income for the year (not less than 0);3. The floor plan financing interest expense for the year.

• A real property trade or business can elect out of the limitation but will be required to use the ADS system (on prior assets too).

– Nonresidential real property, residential real property, and QIPThis may create an opportunity for real property businesses to elect out of interest expense limitation and reduce recovery periods of certain property through a cost segregation study.

31

©20

18 C

lifto

nLar

sonA

llen

LLP

• Pre-TCJA: Business interest generally allowed as a deduction• Under TCJA: Interest expense limited to interest income + 30% of

remaining adjusted taxable incomeo Remaining business adjusted taxable income is:

Determined w/o interest income, NOL, 199A, depreciation, amortization, depletion

Determined at tax filer level (1065, 1120-S, 1120)

o Excess (nondeductible) interest carries forward indefinitelyo Businesses with <$25M average annual gross receipts exempt

Disallowed Business Interest Expense

©20

18 C

lifto

nLar

sonA

llen

LLP

Calculation

Adjusted Taxable Income:

Taxable Income $10,000,000

Add: Depreciation and Amortization $3,000,000

Add: Interest Expense Deducted 7,500,000

Subtract: Interest Income Included in Taxable Income (500,000)

Equals: Adjusted Taxable Income 20,000,000

Limitation Calculation:

30% Adjusted Taxable Income $6,000,000

Plus: Interest Income $500,000

Limitation based on ATI $6,500,000

Lesser of Above Limit ($6.5M) or Interest Expense ($7.5M) $6,500,000

• Assumptions:o Average annual revenue $200Mo Taxable income: $10Mo Interest income: $500Ko Interest expense: $7.5M

Example – Business Interest Expense Deduction Limitation

©20

18 C

lifto

nLar

sonA

llen

LLP

Other Important Elections and Useful Information

34

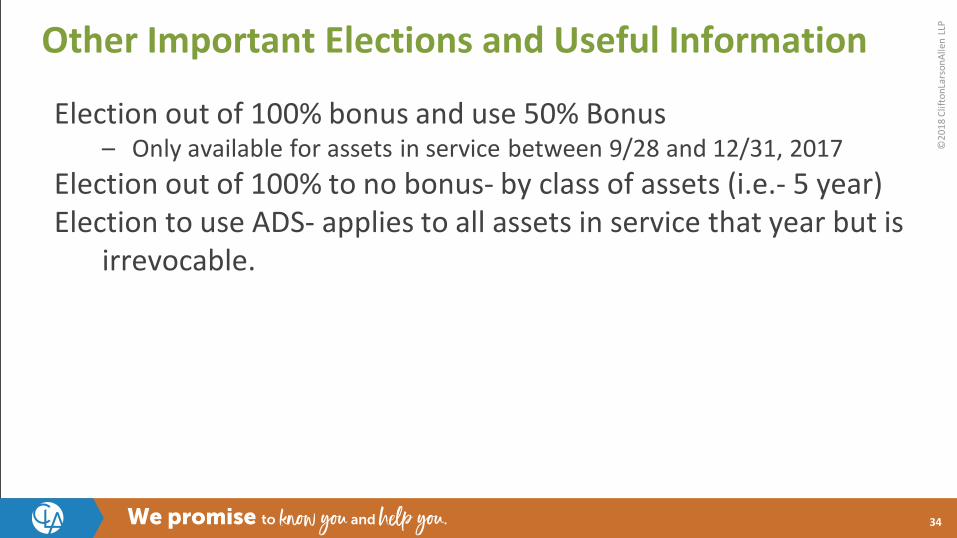

Election out of 100% bonus and use 50% Bonus– Only available for assets in service between 9/28 and 12/31, 2017

Election out of 100% to no bonus- by class of assets (i.e.- 5 year)Election to use ADS- applies to all assets in service that year but is

irrevocable.

©20

18 C

lifto

nLar

sonA

llen

LLP

Sec. 179- Business Expensing

35

Old Rules- Limit was $500k but was phased out dollar-for-dollar for amounts over $2MM– Applies to tangible personal property.– Also to certain “Qualified” real property up to a $500k limit

New Rules- Limit was raised to $1MM with the phase out beginning on amounts over $2.5MM.– Includes tangible personal property– Includes new definition of “Qualified Improvement Property”– Includes assets used in furnishing lodging– Now includes roofs, HVAC, and fire/security alarm systems

©20

18 C

lifto

nLar

sonA

llen

LLP

Procurement Planning for Calendar 2018 Filers

36

Assets placed in service by August 31 represent potential deductions available to reduce tax payments in the third quarter

Assets placed in service by December 31 represent potential deductions available to reduce tax payments in the fourth quarter

©20

18 C

lifto

nLar

sonA

llen

LLP

Last Chance for Adjustments to 2017

37

Depreciation methods can be changed (corrected) for 2017 until the extended due date.

– There should be some consideration for accelerating depreciation deductions into 2017. Not only are rates higher (deduction more valuable) but if a loss is created/increased, the loss can be carried back or can be carried over and utilized at 100%.

– Even if 2017 returns have been filed, there is still an opportunity to review the assets for potential. Amended returns can be completed until the extended due date.

The Tangible Property Regulations still apply– For those that have not reviewed historical assets for the potential immediate deduction,

there is still an opportunity to do so. Especially for the 2017 return (see above).– We can still assist with formal Capitalization Policies and to determine proper de minimis

elections.

©20

18 C

lifto

nLar

sonA

llen

LLP

Cost Recovery Evaluation

An overview of today’s discussion1. A changing tax rate environment, including 199A2. Loss Limitations3. Accounting Method Impacts4. Interest Expense Limitations5. Cost Recovery – Repair, 179, Asset Expensing6. Timing Your Investment Year7. Catching up Missed Deduction in 2017

38

©20

18 C

lifto

nLar

sonA

llen

LLP

For More of the Story

See AlsoFor Construction:Search on Google for “Perry McGowan Tax Reform for Construction”https://www.claconnect.com/resources/articles/2018/reconstructing-taxation-strategies-for-construction-and-real-estate

For Real Estate:Search on Google for “Perry McGowan Tax Reform for Real Estate”https://www.claconnect.com/resources/articles/2018/new-tax-issues-and-strategies-for-real-estate-firms

39

©20

18 C

lifto

nLar

sonA

llen

LLP

National and International Reach

40

CLA has more than 5,400 professionals, operating from more than 110 locations across the country.

twitter.com/CLAconnectfacebook.com/cliftonlarsonallen

linkedin.com/company/cliftonlarsonallen

©20

18 C

lifto

nLar

sonA

llen

LLP

CLAconnect.com

youtube.com/CliftonLarsonAllen

Dan Greenhagen, [email protected]

Perry H. McGowan, CPA [email protected]

41