democratising finance, alternative finance demystified: dealindex research

TRANSCRIPT

DEMOCRATISING FINANCE

AGGREGATING DIGITAL INVESTING MARKETS

Alternative Finance DemystifiedJuly 2015

Volume 1 (Digital Equity Investing): An Overview of the Key Players, Investors and Trends that are Shaping the New Model of Online Collaborative Funding

Prepared in Collaboration with Leading Alternative Finance Players Globally

About This Research While researching and analysing the key players and drivers underpinning the digital investment landscape, the DealIndex team uncovered a whole ecosystem of players that have transitioned into the online investment space. We realised that these players and how they interrelate with one another have not been covered before in a comprehensive manner. As such, we have attempted to capture the interlinkages between the swarm of players in the alternative finance space with this report.

This report covers emerging trends in alternative finance as well as offering an overview of the different areas of the sector, with a focus on equity crowdfunding in Volume 1. In subsequent reports we will cover asset classes including real estate and debt in similar detail. Alternative finance is sometimes seen as a broad and opaque space, through this report we outline how its seemingly disparate parts fit together, and where the sector as a whole is headed. We begin by reporting our key findings and trends, before moving on to describing the diverse array of platforms and services offered. We conclude with an analysis of the changing investor landscape in the sector. This report has been prepared in collaboration with several disruptive and leading alternative finance players across three continents and is furnished with many useful case studies. We hope the report elucidates alternative finance for all who may have an interest in this important and rapidly growing sector.

About DealIndex DealIndex (www.dealindex.co) is an intelligent data and deal aggregator of private companies and assets raising capital across leading alternative finance platforms globally. At DealIndex, we take a global, curated approach to the alternative finance ecosystem. We provide extensive data, research and analytics as part of our service to clients. For this reason, we are able to provide data and context on many different aspects of the market. We can offer as much or as little as is required: from a simple, high-level overview of what’s happening now to deeper insight on longer term trends.

Our flagship product (a global crowdfunding aggregator https://dashboard.dealindex.co/) allows investors to navigate and track deals in real-time, manage their portfolio of private company investments, and is backed by extensive analysis, data and research. The dashboard provides single sign-on access to hundreds of private companies seeking capital, bringing together, for the first time, curated, quality deals from leading equity crowdfunding platforms spanning four continents.

DealIndex is part of The Grow VC Group, a worldwide pioneer and leader in the crowd investing, peer to peer and online investment market.

Authors and DealIndex Research Team

Michael Cameron Edward Flach Research and Investment Associate Research and Investment Associate [email protected] [email protected]

Duncan MacDonald-Korth Neha Manaktala Director, Research and Sales CEO & Co-Founder [email protected] [email protected]

Tom Walker Director, Product and Business Development [email protected]

Acknowledgements Collaboration is a cornerstone of alternative finance, and so for this report we have invited our partners to participate in the production process. Such collaboration will allow our readers unparalleled insights directly from players across the alternative finance value chain and from across the globe. Sincere thanks are extended to our 18 global partners who have contributed to the writing of this report. These industry experts and disruptors are pioneering alternative finance in the markets in which they operate and have contributed truly unique insights. We have received contributions from alternative finance disruptors across Belgium, Canada, France, Germany, Israel, New Zealand, the United Kingdom and the United States.

We are privileged to have first hand insight on the disruption, evolving models and the change each of these players are pioneering in their markets. It is great to be able to bring all this together so our readers can gain a better understanding of the alternative finance ecosystem in markets across the globe: the issuers, the investors, the regulations, the challenges, the similarities, the differences, constantly changing models, collaboration with the financial services industry, and the rapid pace at which this market is evolving. These unprecedented insights from players across the ecosystem, including crowdfunding and M&A platforms, infrastructure, data and technology providers, and advisory firms, have helped us develop a global and more complete picture of the different parts of alternative finance and how they work together. We are overwhelmed with the response and are grateful for the time and effort all of our partners have taken to contribute and participate in this research.

Note From Some of Our Partners

"The digital investing and lending market has grown dramatically in recent years. While the growth is unprecedented, the market is lacking in fundamental data and insight, the type that DealIndex has set out to foster. At Crowd Valley, we believe in universality and transparency in this market and through our digital back office product, we aim at catalysing the markets development through robust middle and back office tools for operators, as well as for the buy and sell side stakeholders. That is why we partner with leading stakeholders in the market that have a digitally native approach to the changes and opportunities in the financial service market." Markus Lampinen, Co-Founder and CEO, Crowd Valley

“I was fascinated to preview this report, shows how new thinking is reframing the finance world, some inspirational stuff and growing scale. Soon, more the new normal than the alternative!” Lin Feng, Founder & CEO, DealGlobe

Contributing Partners

3

4

Note From Some of Our Partners

“FinTECH (Financial Technology) is revolutionising the capital markets! DealIndex provides valued insights regarding how companies and investors are leveraging technology to streamline the investment process. Equity crowdfunding/direct investing has the potential to emulate peer-to-peer lending’s (~Prosper) success as equity investors increasingly migrate online gaining access to premium deal flow at lower costs.” Scott Jordan, HealthiosXchange

"Regulated crowdfunding is the most disruptive form of alternative finance available today. As is the case for any form of alternative or traditional finance to flourish, regulated crowdfunding requires a cohesive eco-system and an integrated infrastructure to bring it all together. Seamless infrastructure technology is the key to integrating the eco-system and ensuring the continued success of regulated crowdfunding. We are delighted to be able to contribute to this Alternative Finance report on how the eco-system works and the importance of proper infrastructure" Oscar A Jofre, Founder, President/CEO, KoreConX

“We are at the forefront of the crowdfunding industry, leading the efforts to democratise capital for all entrepreneurs.” Jeffrey Fidelman, Head of Investor Relations, Onevest

“We were happy to contribute to DealIndex's research, the platform that will become a very useful tool for us." Grégoire Linder, CEO France, Raizers

“While the growth of alternative finance is racing ahead, there has been a dearth of research for those seeking to gain a deeper understanding of the past, present, and future of this market. DealIndex's report sheds light on this dynamic and diverse market, providing insight to the digital investment sector, as well as delving into case studies from various partners in this space. As New Zealand's leading equity crowdfunding platform, we feel that it's important to contribute to this report and help bring alternative finance into sharper focus for global stakeholders.” Josh Daniell, Co-Founder & Head of Platform, Snowball Effect

“As alternative finance increases in size, so does the complexity of its ecosystem. This report is a gold mine for anybody looking to gain an overview of the ecosystem and find out who the main players are in their respective areas.” Gonçalo de Vasconcelos, CEO and Co-Founder, Syndicate Room

"In order for equity crowdfunding to thrive and develop in to a long term and sustainable asset-class, I strongly believe that sound investment principals need to be adhered to and the industry needs to demonstrate that it can consistently deliver returns for its investors in line with the risk they are taking. At VentureFounders we are not going to deviate from our core principals of providing investors with exciting and interesting investment opportunities that are appropriately structured for the risk that investors are taking. This in-depth industry report drills down on various aspects of the alternative finance ecosystem. It is great to be able to feature our unique insights on the fast growing equity crowdfunding industry.” James Codling, Co-Founder, VentureFounders

Table of Contents

Infrastructure: The Importance of a Comprehensive Support System

Investors: A Mix of Both Retail and Institutional

Platforms: The Evolution and Emergence of New Platform Models and Asset Classes

Data and Marketplaces: Shifting Towards a More Data Driven Approach To Investing

Executive Summary: Summary Observations, Key Findings and A Message from the Founders

Issuers: Investment Activity Moving Upstream

09

20

24

31

51

58

65

Introducing the Alternative Finance Ecosystem: Who Are The Key Players and How Do They Interrelate With One Another

Conclusion: Looking Forward74

5

CONTRIBUTING PARTNERS

Crowd Valley powers the future of financial services by providing marketplace technology and API Back Office solutions. The company enables online investment platforms; peer to peer lending, equity and debt marketplaces

Equidam provides a business valuation tool that helps SME’s to manage their value, investors to achieve the required return and invest in the best ideas, and early stage companies to grow and prosper

AgFunder is the world’s first equity-based investment platform created specifically to connect investors with world-class agriculture and agtech investment opportunities from around the globe

Bankless 24 is a German crowd investing platform for the SME sector. Investors can invest in medium-sized companies from 100 euros. Businesses get access to alternative finance

Crowdfundraiser is an expert across the crowdfunding ecosystem, connecting capital between investors and entrepreneurs. It provides services related to both debt and equity alongside liquidity solutions for investors and founders

DealGlobe provides an online platform for investors and corporate professionals seeking investment and partnership opportunities. The company's primary focus is on small and medium sized enterprises with the aim of bridging the information gap between Europe and China

6

US Page 41

GERMANY Page 45

US Page 50

HK, UK, US Page 62

Page 47CHINA, UK

NETHERLANDS Page 60

CONTRIBUTING PARTNERSEquityNet has operated one of the largest business crowdfunding platforms since 2005. The multi-patented EquityNet platform includes over 100,000 individual entrepreneurs and investors, incubators, government support entities, and other members of the entrepreneurial community. EquityNet provides access to thousands of investors and has helped entrepreneurs across North America raise over $330Mn in equity, debt, and royalty-based capital

US Page 35

HK, UK, US Page 64

Grow Advisors is the consulting and advisory unit of The Grow VC Group. Grow Advisors offers professional services aimed at growing crowdfunding, crowd investing and P2P finance around the world

HealthiosXchange is an investment marketplace dedicated exclusively to the global healthcare industry, employing crowdfunding as the cornerstone of a new paradigm in healthcare investing, the company offers direct access to the broadest investment opportunities

US Page 48

iAngels is an equity crowdfunding platform that gives accredited investors the opportunity to become angels in their own right by investing in technology startups alongside top tier angel investors in Israel

ISRAEL Page 42

KoreConX supports the crowdfunding and capital markets industry by supplying the eco-system infrastructure platform (ESIP). The ESIP is utilised for pre-during-post crowdfunding transactions by facilitating due diligence of issuers, data repository/deal room and shareholder management/communications

Page 63CANADA

MyMicroInvest is a lending and equity based crowdfunding platform in Europe. The platform is based on the co-investment principles between crowd and professional investors and has already facilitated €10Mn investment in over 30 European companies. MyMicroInvest has also developed a system allowing SMEs to make a public offering online by automatising the prospectus redaction and establishing a relationship of trust with the Financial Services and Markets Authority

BELGIUM, EU

7

Page 36

CONTRIBUTING PARTNERSOnevest is reshaping the private equity industry by democratising early stage investing: connecting founders to capital allowing their ideas to transform into successful companies, simultaneously creating new investment opportunities for individual investors

US Page 37

Snowball Effect is New Zealand's leading equity crowdfunding platform, with around 75% of market share. This highly curated platform aims to attract the best quality companies and investors, and is focused on growing carefully to encourage a sustainable equity crowdfunding market over the long term

NEW ZEALAND Page 39

SyndicateRoom is an online equity crowdfunding platform that allows its members to co-invest in exciting companies with seasoned investors. Members co-invest alongside Business Angels

UK Page 43

TradeUp is an equity crowdfunding platform for globalising companies, a rapidly growing and outperforming segment. It helps export-driven companies to connect and transact with accredited investors

Page 45CHINA, UK

VentureFounders is an equity crowdfunding platform with a wealth of investment and startup experience. The company is pushing the boundaries of what can be achieved in the crowdfunding market by presenting investors with a range of curated, structured and diligenced investment opportunities

UKPage 44

FRANCE, SWITZERLAND, DENMARK

Raizers is a crowdfunding platform for entrepreneurs. The Pan-European platform is a collaborative space with innovative features that facilitates the relationship between entrepreneurs and investors

Page 38

8

Private Investment is Moving Online. While

Executive Summary

Private investment is moving online. While alternative finance started off as a seed stage endeavour, more recently platforms have begun to emerge at different stages in the funding cycle, disrupting traditional institutions

“

10

PREFACE: A PARADIGM SHIFT IN FINANCIAL SERVICES

Alternative Finance is a new phenomenon, and it is taking the world by storm. With over 1,250 crowdfunding platforms worldwide, this new model of collaborative funding is breaking boundaries and defying the status quo as to how issuers source capital. In light of this paradigm shift and plethora of platforms, we perceived the need to develop an alternative finance aggregator that would instantaneously display quality private investment opportunities from curated platforms, all in one centralised marketplace.

We embarked on this mission to pioneer an innovative dashboard to address the ‘pain points’ often faced by sophisticated investors who are keen to invest in private companies across all corners of the globe. It is throughout the course of this 12-month journey and vigorous research-driven process that we discovered the relative dearth of information on this burgeoning sector. This industry report thus aims to offer a comprehensive overview of this emerging sector, as well as to provide valuable insights on the complexity of the wider alternative finance ecosystem from various perspectives.

As we set out to develop DealIndex as an alternative finance aggregator, our first port of call was to define the term “alternative finance” and to research the key players underpinning this rapidly evolving sector. While alternative finance is primarily known for crowdfunding and P2P lending, we discovered entire asset classes, important functions of investment banking, including a supporting ecosystem of due diligence, risk management, and infrastructure that had transversed the offline and online world of financial services. We started to see how these seemingly disparate players in alternative finance - involved in different aspects of fundraising, and from all over the world - are interrelated. Assets including alternatives and M&A, represent significantly bigger (albeit challenging) asset classes and have started moving online. More importantly, we learned how these players mirror traditional investment banking services and had already started collaborating with the financial services industry.

Some of the themes underpinning alternative finance include: 1. Increased transparency and access to otherwise closed off asset classes; 2. Redefinition of the term “investor” across the entire spectrum of private and public asset classes. The crowd

gets access to privileged deals and the world’s largest financial institutions have started investing in companies much earlier in the life-cycle of a company;

3. Collaboration is a cornerstone of the industry as the syndication model takes hold with mobile, social media and millennials all generating network effects;

4. Increased volume of funding activity in private companies & assets, and increased amounts of companies getting funded with customers getting involved in product development / playing a role in innovation as investors; and

5. How technology, speed, and data have come together to reduce the inefficiencies in searching and accessing private investment opportunities, thereby saving issuers and investors time in the procurement process.

Alternative finance has already demonstrated its potential to change the way fundraising is carried out by private companies by implementing a much more democratic, transparent and efficient process for both entrepreneurs and investors. Issuers get increased access to diverse funding options, while online platforms alleviate the time, effort and costs associated with fundraising, in addition to generating increased marketing and product awareness.

Democratising Finance Executive Summary

Neha Manaktala CEO and Co-Founder, DealIndex

11

Having been on both sides of fundraising, it is exciting for me to be part of the potential to improve the way different aspects of financial services are performed; all the while deepening collaboration, not just between alternative finance players, but with the financial services industry in general

Democratising Finance Executive Summary

“The definition of investors itself has evolved since the advent of alternative finance and the surge of online platforms. Increasingly, we are witnessing changes to investment behaviour since the start of syndication of investment online. Furthermore, access to global investment opportunities has led to a more data-driven approach to investing.

Despite growing into a $16.4Bn industry in 2014, it is still a drop in the ocean compared to the $3.3Tn addressable market opportunity. Although crowdfunding is still often dismissed as a niche activity associated with rewards or donations, the industry has developed into an entire ecosystem that is constantly evolving. Growth has been exponential with players across the entire funding lifecycle offering diverse and alternative fundraising options. Most of these alternative finance players already have a significant amount of collaboration with the financial services world.

Finance is a singular industry with its ramifications permeating every single part of the economy. As an ex-Lehman Brothers investment banker who witnessed the Great Financial Crisis first hand in 2008, I am constantly reminded of these important principals. With rapid growth in the alternative finance space, comes the need for increased maturity in the industry and systems to contend with the unknown and untested impact of changing credit and interest rate cycles, liquidity squeezes, fluctuating asset pricing and valuations and the impact of the macro economic environment. Moreover, with increased funding rounds, shorter capital raising cycles, diversified and changing investor bases in private companies, structured offerings and more sophistication being applied so early on in the life of a company, comes the need for best practices to be applied from financial services. Due diligence, risk and portfolio management, research, liquidity channels / secondary market - these are all vital parts of finance and are now beginning to permeate alternative finance.

Alternative finance is removing information barriers and information inefficiencies that exist in the private market, opening funding conduits and channeling global liquidity. At DealIndex we take a global, curated approach to the alternative finance ecosystem. We give you a pulse of the market through the provision of data, research, analytics and context on the wider ecosystem. The availability of private company data is a game changer and everyday we are fascinated by the volume of data and patterns that emerge as we observe dealflow going live from different corners of the world across platforms, asset classes and sectors, all in real-time.

Having been on both sides of fundraising including at Morgan Stanley Investment Banking, Actis Private Equity and as an entrepreneur, it is exciting for me to be part of the potential to improve the way different aspects of financial services are performed; all the while deepening collaboration, not just between alternative finance players, but with the financial services industry in general.

I would also like to extend my grateful acknowledgement and appreciation for all our partners and to those who have contributed to this report. It would not have reached you in its present form without them.

Democratising Finance Executive Summary

While alternative finance started off as a seed stage endeavour, more recently platforms have begun to emerge at different stages in the funding cycle, disrupting traditional institutions. Drawn by the increased access to investors that operating online affords, platforms now make it possible for companies to raise capital at every stage of the funding cycle online.

As the market grows in size, so too are more institutions investing in the sector. As much as 66% of the loans originated at Prosper were snapped up by large institutions in the 3rd quarter last year. Similar figures across other P2P platforms highlight an increasingly institutional marketplace. While equity investment remains someway behind the P2P market in this respect, things are beginning to change with more VC’s participating in crowdfunding campaigns. This is expected to only strengthen as more tools for sophisticated investors emerge.

Originally seen as a solution to the long-standing funding gap for early stage companies that appeared in the wake of the 2008 financial crisis, the ability for issuers to raise capital more quickly and at a lower cost than would otherwise be possible at traditional institutions coupled with a host of other benefits such as the increased marketing awareness and customer loyalty has meant that crowdfunding is now seen as an attractive option by many issuers.

ALTERNATIVE FINANCE IS DRAWING MORE ESTABLISHED ISSUERS

As the private investment market moves online, the ability to harvest large quantities of data surrounding investment decisions becomes easier. Furthermore, tools that allow investors to then analyse the data, uncovering trends, are enabling more informed decisions. This is a radical change for the private investment market given its historically closed-off nature.

AVAILABILITY OF DATA IS CHANGING

KEY FINDINGS

Many have wondered if the alternative finance space is set to upend the traditional early stage investing business model. While this angle is hyped, in reality it is emerging that venture capital and alternative finance will work side by side. Rather than disrupting, alternative finance is developing a collaborative and synergistic model. Evidence of this can be seen in the growth of investor-led platforms, as well as the adoption of digital finance by major businesses like Goldman Sachs and Metro Bank.

12

PRIVATE INVESTMENT IS MOVING ONLINE

INCREASING INSTITUTIONAL INVOLVEMENT

COLLABORATION RATHER THAN DISRUPTION

Democratising Finance Executive Summary

INTERESTING FACTSValue of the Early Stage Investment

Market2

$300Bn

Number of Crowdfunding

Platforms Worldwide4

1,250Estimated Revenue

Crowdfunding Added to the Global Economy in 20143

$65Bn

Alternative Finance Immediately Addressable

Market Opportunity1

$3.3Tn

Equity crowdfunding average growth rate

2012-20145

410%Number of jobs crowdfunding

created in 20143

270,000

VC Industry annual average6

$30Bn Estimated Crowdfunding

Market 20156

$34Bn Angel capital

annual average6

$20Bn > >

100M+Unaccredited

investors in the U.S.

351%Increase in quarterly revenue post equity

crowdfunding

13

What role have governments played in the adoption of digital investing and lending in areas where adoption has been the fastest? Governments play a very important role in digital investing markets, anyone who innovates spends significant effort on doing their own risk assessment and due diligence. While it’s understandable that laws and regulations typically follow innovation, the most important factors for risk assessment are the easy availability of information and the clarity of the regulatory environment. When the rules are less clear, the way the government reacts to innovation is important. For example, in the UK and US, the governments have led and openly communicated their views on innovations in alternative finance and how they plan on acting should the market move adversely. It is important to open a dialogue and build mutual trust between all parties and this approach sends a positive signal to those in this new market.

How do start-up ecosystems across different countries benefit from alternative finance, especially in attracting international investors and how can data on digital investing and lending benefit start-up ecosystems? New digital investing models and related processes accelerate start-up ecosystem knowledge especially with reference to investment processes and investor expectations. In general, they can help a city or country to “skip a generation” of trying to only build or grow traditional “offline” based risk finance models like grants, traditional business angel and venture capital models. Furthermore, in mature markets, business angels and VC’s are already moving onto digital platforms and investing alongside the crowd. In addition by applying digital marketplaces in different countries and cities, one can productively showcase the best regional investment opportunities in the international market, channelling opportunities to different audiences beyond the single marketplace itself.

One of the fundamental differences between digital investing and open marketplace models is that, instead of a company having to limit itself to specific funding instruments rules or limitations, it can freely structure its offering and then let the market decide if it’s interesting.

ALTERNATIVE FINANCE: ROLE OF GOVERNMENTS, STARTUP ECOSYSTEMS AND INVESTORS

Valto Loikkanen Co-Founder & Chairman, DealIndex; Co-Founder & CEO, Grow VC Group

14

Democratising Finance Executive Summary

What has been the evolution and strategy of the Grow VC Group and why did you and Jouko set it up? The idea was to help scale entrepreneurship and identify innovations in the context of the recent financial market failure. We also wanted to harness the power of social networks that brought people to the online world. Both of us have experienced successes and failures in building innovative companies and have learned that market timing is key. We could see we were very early to the market and had difficulty trying to communicate our vision and business model to others. The initial idea for equity crowdfunding was in the summer of 2008, when Facebook only had 100 million users. The name ‘equity crowdfunding’ hadn’t yet been coined and as such we had a hard time explaining it. Initially we called it Venture Capital 2.0. Furthermore, it was hard for many to believe in. It therefore became evident that we would have to commit to a long journey and approach it globally from the start in order to reach the necessary volume of users. Today there is a broad scope of opportunities within various alternative finance sectors.

As an entrepreneur yourself, what are the benefits that alternative finance has for start-ups and founders in the fundraising process? Overall, alternative finance simplifies things and makes the process more transparent. In addition, founders also can gain a lot more knowledge about other companies that have used the process before them. It can be a bit scary to put your business out there as it’s possible that you may not be successful in fundraising, but for any genuinely good deal, with a good valuation, that is well structured and with a good team behind it, it is a very good option. It must be stated that whenever there are more options than before, it is generally a positive thing for everyone and for any company that has high growth ambitions, the digital fundraising process forces them to learn how to communicate with investors early on. This alone is valuable for the future. From a general perspective the digital finance market is all about better access, transparency and efficiency. This, together with the data that this digital market generates, leads to ever faster learning and further development of all areas it spreads to.

The digital finance market is all about better access, transparency and efficiency…..Whenever there are more options, it is generally a positive thing for everyone and for any company that has high growth ambitions, the digital fundraising process forces them to learn how to communicate with investors early on. This alone is valuable for the future…

15

“

1

2

3 4

Democratising Finance Executive Summary

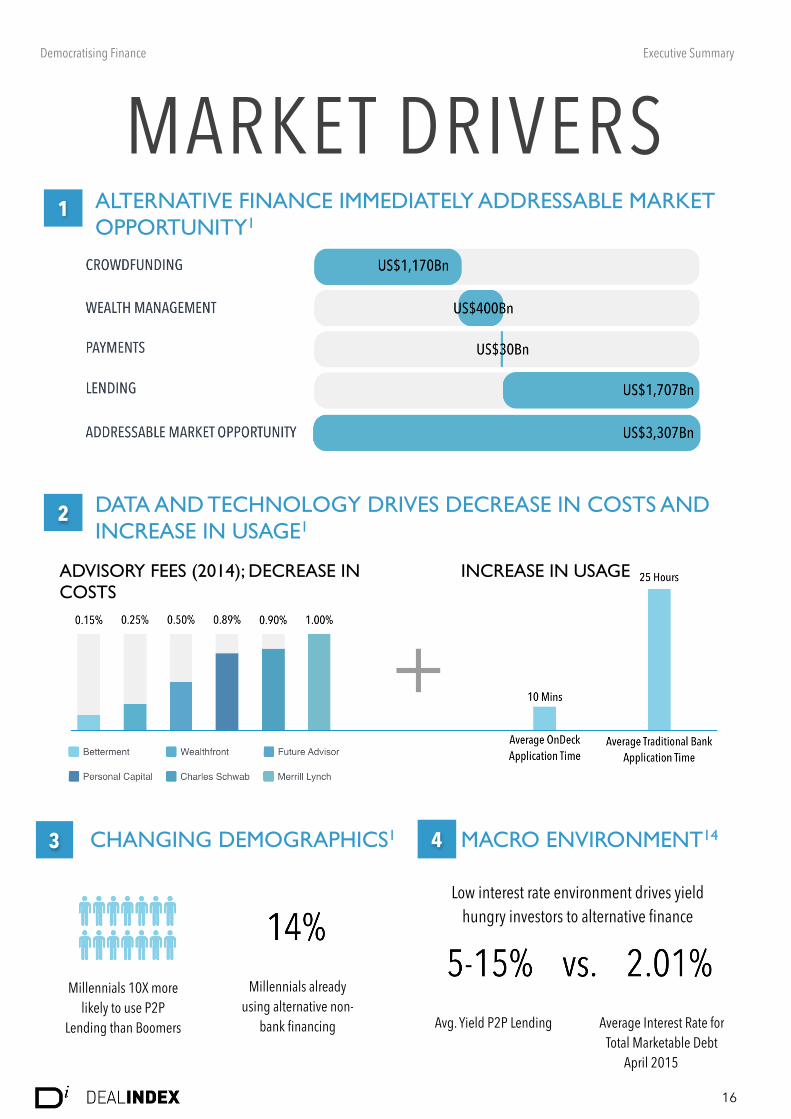

MARKET DRIVERSALTERNATIVE FINANCE IMMEDIATELY ADDRESSABLE MARKET OPPORTUNITY1

DATA AND TECHNOLOGY DRIVES DECREASE IN COSTS AND INCREASE IN USAGE1

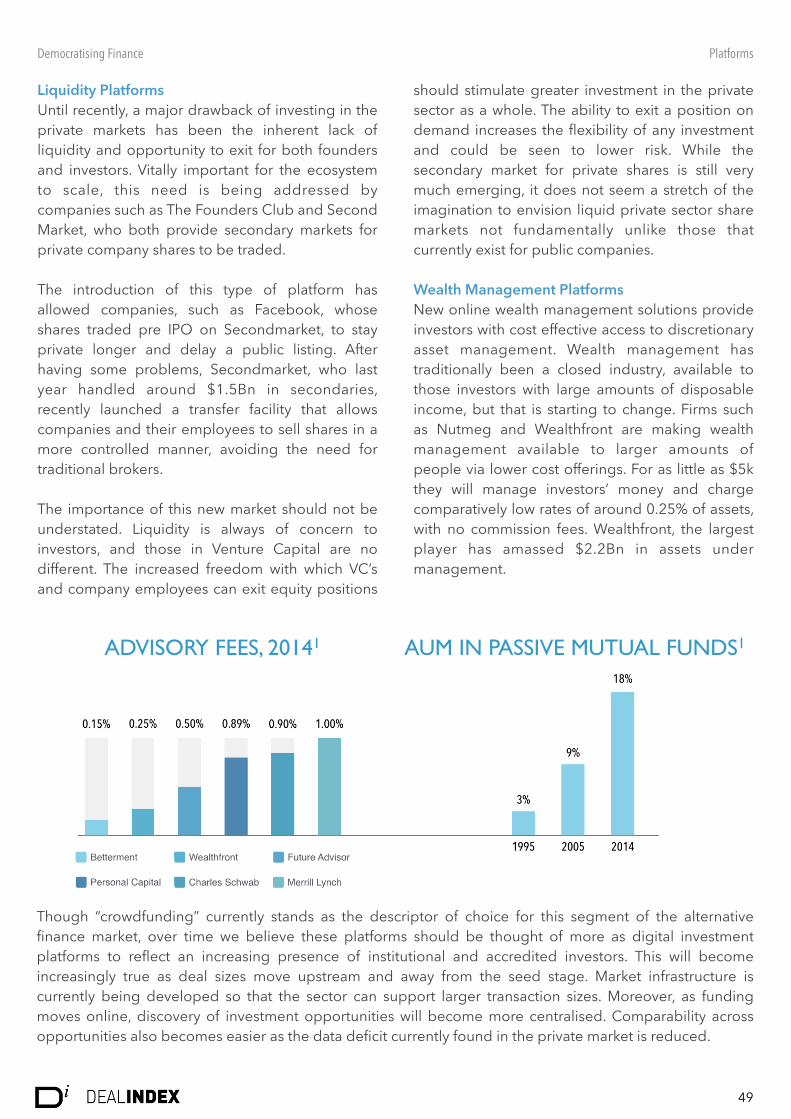

ADVISORY FEES (2014); DECREASE IN COSTS

INCREASE IN USAGE

CHANGING DEMOGRAPHICS1 MACRO ENVIRONMENT14

Millennials 10X more likely to use P2P

Lending than Boomers

Millennials already using alternative non-

bank financing Avg. Yield P2P Lending Average Interest Rate for Total Marketable Debt

April 2015

Low interest rate environment drives yield hungry investors to alternative finance

16

5

6

7

Democratising Finance Executive Summary

MARKET DRIVERSGLOBAL CROWDFUNDING MARKET4,5

Worldwide Crowdfunding in 2014: $16.2Bn YoY Growth 2013/2014

DEMAND FOR DIGITAL INVESTMENT OPERATIONS Q420147

NETWORK EFFECTS YIELD EXPONENTIAL GROWTH1

50% Of all Lending Tree/Prosper loans originated in Q4 2014

17

Over the last few years, much has been made of the potential for alternative finance to disrupt the traditional financial industry, including subverting the established bank loan process with P2P lending. Some may wonder if this will actually be the case, and additionally, whether alternative finance as a whole, will disrupt the traditional early stage investment industry.

Thus far, it appears the alternative finance market is actually moving in the opposite direction. Rather than trying to supplant banking and venture capital, a collaborative model is emerging whereby digital platforms work side by side with traditional investors. This trend is evidenced by a number of developments. There is an increasing trend towards investor-led platforms. Such platforms allow individual investors to follow the lead of an accredited investor, showing how traditional financing and alternative financing can work in harmony.

The emergence of a secondary market for private company shares is making it easier than ever for institutions to participate in the space. According to media sources like the Financial Times, even businesses as regulated and traditional as mutual funds are now investing in private companies, such as Uber and Pinterest. Large institutions are starting to utilise P2P lending as well, with the UK’s Metro Bank announcing that it would start lending customer deposits through P2P platform Zopa. Goldman Sachs itself, widely seen as the pinnacle of traditional investment banking, has even announced that it will start lending through a digital consumer-driven platform. All of these points show how rather than disrupting traditional financing models, alternative finance is developing its own collaborative niche within the industry.

ALTERNATIVE FINANCE: DISRUPTION OR COLLABORATION?

Rather than trying to supplant banking and venture capital, a collaborative model is emerging whereby digital platforms work side by side with traditional investors and financial institutions.

18

“

Global easing of regulations around the world is opening up the private investment market to larger numbers of investors. In the US, changes to legislation allowing for companies to state publicly that they are raising funds meant that the market was opened up to accredited investors in 2013. Regulators recently went a step further and now non-accredited investors have access to the asset class for the first time under Title IV.

REGULATION

Millennials desire for fast, seamless user experience coupled with their preference for online, mobile-first solutions is changing consumer investment behaviour. Furthermore, they are drawn by the greater transparency and increased involvement in the investment process that online funding platforms afford.

CHANGING INVESTMENT BEHAVIOUR

With crowdfunding’s roots in the donation/rewards based category, it did not take long for the sector to evolve and incorporate P2P lending and equity platforms. Furthermore, there are now platforms at every sector of the funding cycle while other online tools such as data providers are evolving to compliment the fast moving sector.

INNOVATION

Investors are incentivised to share campaigns across their network in order that the funding target is reached and as such, alternative finance is an increasingly social market. Furthermore, strong network effects mean that as platforms draw more investors they will draw more issuers and vice versa. All this makes it easier for online platforms to recruit customers than their traditional bricks and mortar counterparts.

CUSTOMER ACQUISITION

Democratising Finance Executive Summary

GROWTH DRIVERS

19

INTRODUCTION

If the Alternative Finance sector does reach its forecasted $34.4Bn in funding in 2015, it will have surpassed the venture capital industry’s $30Bn of annual funding volume6

“

Born out of the ashes of the 2008 financial crisis, alternative finance, which encompasses practices like crowdfunding and peer-to-peer lending, has grown rapidly as a means of financing globally. Beginning as an online extension of traditional financing by friends and family, alternative finance has given rise to truly global online communities of investors and issuers, democratising, globalising and streamlining the capital raising process.

There are many examples of early crowdfunding campaigns, but it has been the combination of a number of factors that has allowed it to grow into the industry that we recognise today. Technological advances, namely the advent of Internet 2.0 has meant that users can enjoy greater interactivity online, while the squeeze on bank lending and low interest rates post 2008 have pushed issuers and investors to explore non-traditional financing and investment models.

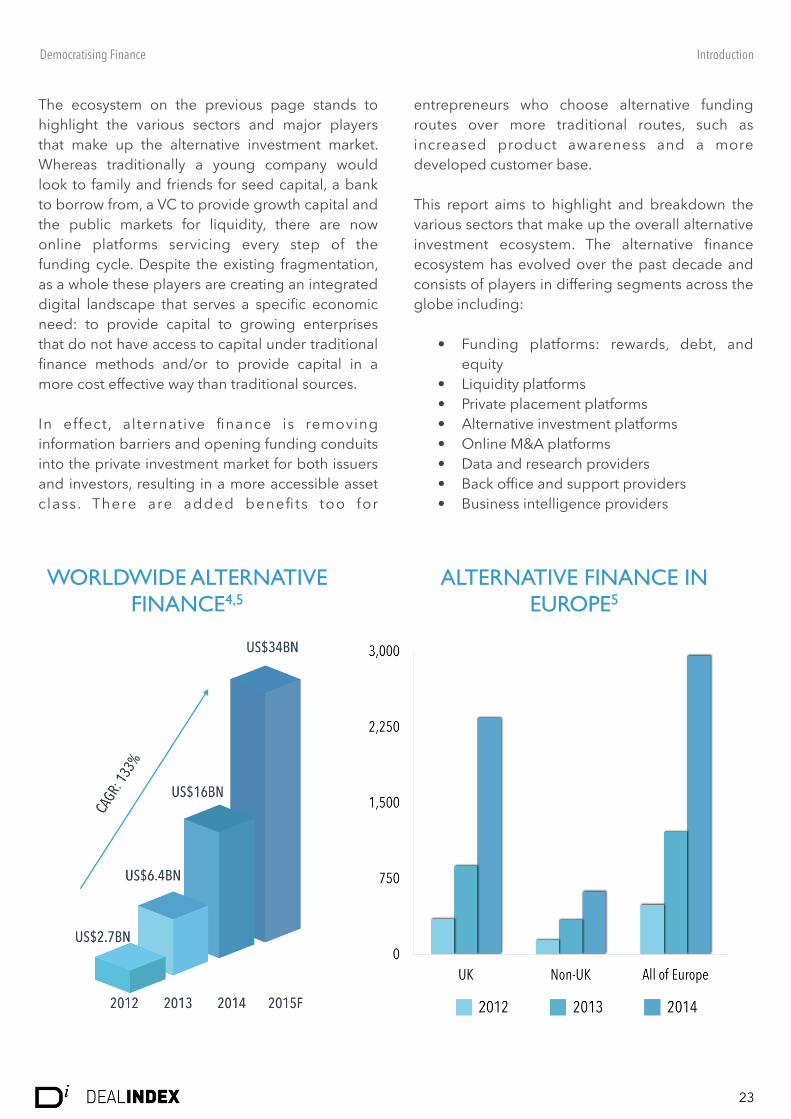

Since 2008, individuals and companies have successfully raised billions of dollars in debt, equity and donations online. Worldwide, some estimates put the total alternative finance market at $16.2Bn in 2014, more than double the $6.4Bn it was in 2013, but still some way short of the $34.4Bn it is expected to reach this year. If the sector does reach its forecasted $34.4Bn in funding in 2015, it will have surpassed the venture capital industry’s $30Bn of average annual funding volume. Such success has given rise to a new, but still nascent, digital investing ecosystem of issuers, investors, funding platforms, marketplaces and information providers that are challenging the traditional players.

Though led by developed nations in a geographic sense, particularly the United Kingdom, the United States and China, which, according to some estimates make up 96% of the financial return crowdfunding market, no single region controls the digital investing landscape as we know it today. It operates on a truly global basis. As with the development of any new financial market, the regulatory environment remains fragmented, differing across geographies not only in a rule-making sense but also in maturity, clarity and relevancy. Moreover, funding platforms, service providers and data availability all remain fragmented as well.

As the Statue of Liberty was being shipped from France, efforts by the US government to raise money for a pedestal for the statue to stand on had stalled. By the summer of 1885 it seemed like all options had been exhausted.

Renowned publisher Joseph Pulitzer took it upon himself to launch a fundraising campaign through his newspaper the New York World. He sought lots of small donations from a large number of people and within 5 months had raised the required $100k from 160k ordinary Americans.

Pulitzer used a single collection point to collect small amounts of money from a very large pool of donors and if this was launched today, the campaign would resemble a reward/donation based crowdfunding campaign similar to those run on Kickstarter and Indiegogo.

STATUE OF LIBERTY

21

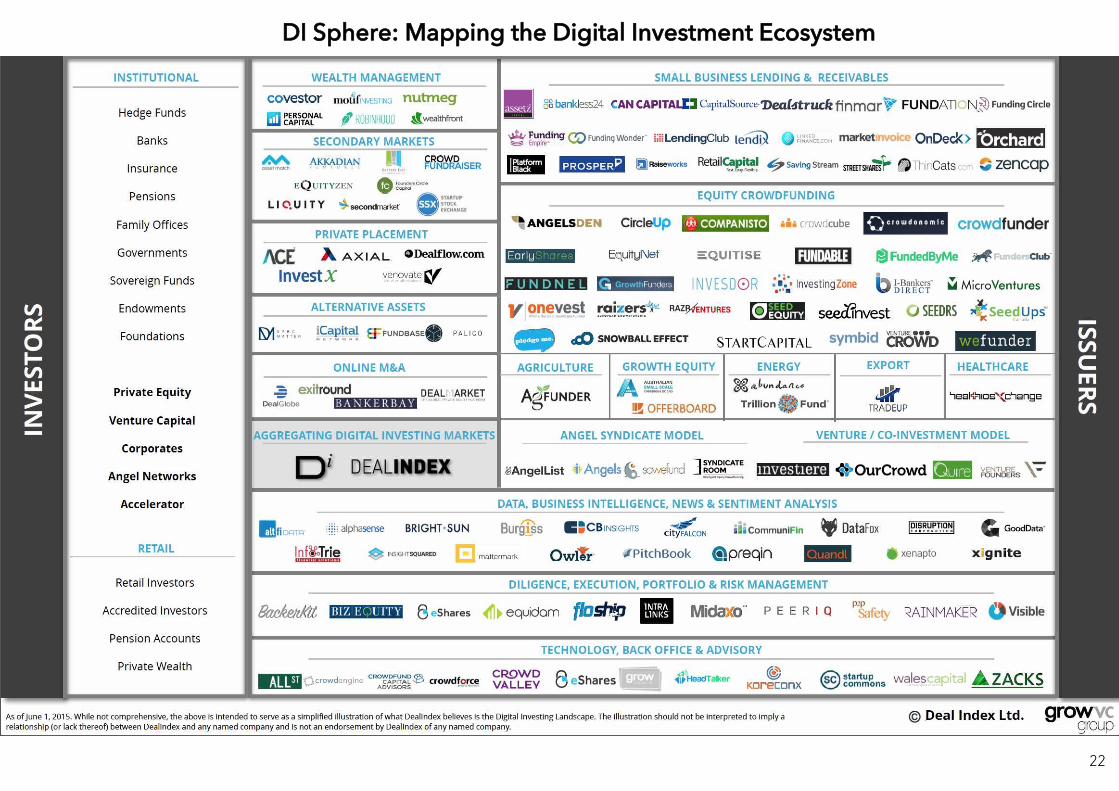

DI Sphere: Mapping the Digital Investment Ecosystem

22

Democratising Finance Introduction

The ecosystem on the previous page stands to highlight the various sectors and major players that make up the alternative investment market. Whereas traditionally a young company would look to family and friends for seed capital, a bank to borrow from, a VC to provide growth capital and the public markets for liquidity, there are now online platforms servicing every step of the funding cycle. Despite the existing fragmentation, as a whole these players are creating an integrated digital landscape that serves a specific economic need: to provide capital to growing enterprises that do not have access to capital under traditional finance methods and/or to provide capital in a more cost effective way than traditional sources.

In effect, alternative finance is removing information barriers and opening funding conduits into the private investment market for both issuers and investors, resulting in a more accessible asset class. There are added benefits too for

entrepreneurs who choose alternative funding routes over more traditional routes, such as increased product awareness and a more developed customer base.

This report aims to highlight and breakdown the various sectors that make up the overall alternative investment ecosystem. The alternative finance ecosystem has evolved over the past decade and consists of players in differing segments across the globe including:

• Funding platforms: rewards, debt, and equity

• Liquidity platforms • Private placement platforms • Alternative investment platforms • Online M&A platforms • Data and research providers • Back office and support providers • Business intelligence providers

WORLDWIDE ALTERNATIVE FINANCE4,5

ALTERNATIVE FINANCE IN EUROPE5

23

ISSUERS

Initially platforms primarily featured young companies raising seed stage capital at a time when it was hard to access traditional funding sources, but now, the industry is moving upstream and is attracting more established businesses, drawn not just by the speed and cost savings but by a host of added benefits too

“

Democratising Finance Issuers

From alternative finance, equity and debt-based crowdfunding emerged to fulfil an important portion of a developing SME’s funding cycle known as the funding or capital gap. Whereas VCs and even angel investors are increasingly looking for businesses with a clear path to exit (somewhat a function of their increasingly traditional investor bases), excluding the majority of young companies f r o m f u n d i n g , e q u i t y a n d d e b t - b a s e d crowdfunding stands to provide capital to businesses that are moving from prototype to start-up to early growth without forcing them to call upon friends or family for capital at a stage that is too early for traditional bank funding. Moreover, requirements for series A rounds are becoming higher, forcing companies to raise prior rounds.

Basel III, resulting in new regulations and capital rules has meant that banks are increasingly strained in their ability to lend to SME’s. This coupled with the fact that even small lines of credit are taking increasingly longer amounts of time to approve has created a funding vacuum. Specifically, in its October 2014 Senior Loan Officer Opinion Survey, the Federal Reserve noted that the majority of respondents indicated that underwriting policies on small business loans were tighter than their average over the last decade. Alternative funding methods stand to reduce this working capital gap. Such reduction in time to funding could have

massive implications for small businesses and overall economic growth.

Alternative finance platforms ability to reduce this working capital gap and time to funding has meant that they are beginning to attract the attention of larger, more established issuers and that has led to investment activity moving upstream in the last couple of years.

In March 2014, Facebook made an announcement that they were taking over Oculus Rift, the virtual reality gaming headset manufacturer, for $2Bn.

What made this exit particularly interesting was that two years prior to the announcement, Oculus Rift raised $2.4Mn via the Kickstarter platform. In return for donations, donors were given T-shirts, posters and for larger donations, developer kits. While the exit did not reap any financial rewards for the donors, it further highlights the potential of investing via crowdfunding.

FACEBOOK ANNOUNCES ACQUISITION OF OCULUS RIFT FOR $2BN

CROWDFUNDING DEALS BY STAGE 2014/155

CROWDFUNDING INVESTMENT BY STAGE 2014/155

25

This year, Lending Club has announced partnerships with both Google and more recently Alibaba, to whom they will provide small business loans of up to $300k to US businesses that are looking to buy inventory from the Chinese eCommerce site. This is of particular note due to the fact that Lending Club is replacing an established, traditional Chinese bank and highlights the threat traditional lenders face from this still infant industry.

LENDING CLUB

Earlier this year, JustPark, previously backed by BMW and Index Ventures, used Crowdcube to raise £1 million of growth capital at a time when it would have usually looked to more traditional funding avenues. JustPark citied one of the key drivers as being the fact that by giving their customers the opportunity to invest in the company it would make them less likely to join competitors in the future.

NEARDESK

NearDesk, who rent desks and meeting rooms by the hour around the UK, recently raised £1Mn via Seedrs. The capital will be used as growth capital and follows previous funding rounds raised online. NearDesk saw VC’s Juno Capital and Renaissance Capital take part in the online round.

In October 2014, UK-based winemaker, Chapel Down Group, raised £3.95 million via Seedrs, making it the first publicly listed company to a c c e s s t h e p u b l i c e q u i t y m a r ke t s v i a crowdfunding. The funds were raised to promote growth and necessary investment to support that growth. Similar to companies raising in the non-public sphere via crowdfunding campaigns, Chapel Down cited the ability to build a significant body of shareholders as a primary reason for using an alternative finance fundraising model.

In 2013, Nicola Horlicks, a highly regarded fund manager, raised £150k via Seedrs. The money was sought to allow her to start raising capital for her first investment fund. Since then, she has raised follow-on investment via Seedrs, to the tune of £450k and increased the fund target from $100 million to $250 million because of investor appetite.

CASE STUDIES

The Mill Residential REIT became the first real estate investment trust to utilise the power of the crowd, when it raised £2.1 million in just three weeks via Syndicate Room last year. In total they raised £3.5 million, with the balance coming from institutional investors. The round preceded a listing on AIM a couple of months later, giving investors immediate access to liquidity and was one of the main reasons that the round was so well received. Furthermore, the structure stands to highlight the increasing sophistication that is becoming prevalent in alternative finance.

CHAPEL DOWN JUSTPARK

MILL RESIDENTIAL REIT

NICOLA HORLICKS

26

Alternative lending has moved on from providing smal l -scale loans to consumers and seen exponential growth since 2010, when the industry self-imposed restrictions to address default rates that were sometimes as high as 30%. Their ability to extend credit in a quicker and more cost effective manner than traditional banks has meant that the industry now encompasses more commercial loans and is providing credit to a growing number of SME’s.

In equity crowdfunding there is evidence of a similar theme developing. Initially platforms primarily featured young companies raising seed stage capital at a time when it was hard to access traditional funding sources, but now, the industry is beginning to move upstream and is attracting more established businesses, drawn not just by the speed and cost savings but by a host of added benefits too.

Aside from the aforementioned benefits, early stage companies have reported seeing increased Angel and VC interest immediately after closing a round through crowdfunding. In a recent study, 71% of businesses reported that within 3 months of closing a fundraising round that they had either taken on investment (or were in discussion to) from Angel investors or VC’s5.

Other reasons private companies are drawn to raising capital online include the increased marketing awareness that engaging with funders brings, from becoming more aware of new market opportunities, to understanding which features resonate with people and gaining insights into competitors. A number of firms are reported to have even scrapped their marketing plans and completely rewritten them subsequently.

Democratising Finance Issuers

CHARACTERISTICS OF UK CROWDFUNDING ISSUANCES5

Summary of benefits for entrepreneurs/issuers of raising money online:

• Efficiency • Access to wider investor base • Marketing/product validation • Democratic process • Newfound comfort with investor structure

now in crowdfunding

27

DEALINDEX DASHBOARD INSIGHTSDemocratising Finance Issuers

DEALFLOW STANDARDISED ACROSS LEADING EQUITY CROWDFUNDING PLATFORMS GLOBALLY

AVERAGE AND MEDIAN DEAL SIZES

28

DEALINDEX DASHBOARD INSIGHTSDemocratising Finance Issuers

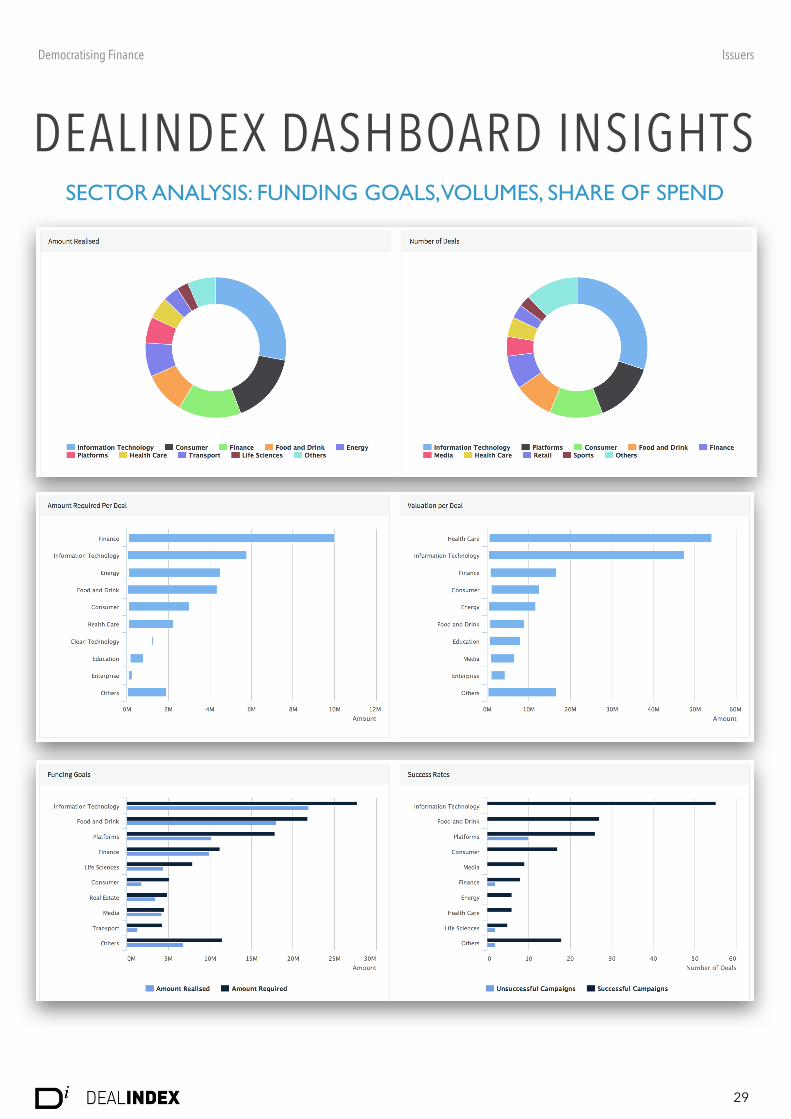

SECTOR ANALYSIS: FUNDING GOALS, VOLUMES, SHARE OF SPEND

29

The race towards embracing crowdfunding has spread globally. Crowdfunding platforms globally raised a total of $16.2Bn last year, according to a recent crowdfunding industry report by Massolution, a research firm. Regulatory reform, international expansion and cross-border deals have helped boost the industry, as has a tide of investors seeking rewards or equity in return for their cash. Among all the regions, Asia is leading the race in terms of growth, with a 320% increase in funding volume. With $3.4Bn raised last year, Asia is experiencing the highest growth in the crowdfunding sector and has surpassed Europe ($3.26Bn raised) to become the second-largest crowdfunding region. In 2015, crowdfunding in Asia is forecast to grow by more than double the rate of that in North America.

What are the Trends Driving this Crowdfunding Revolution in Asia?

First, while rewards and equity-based campaigns typically get the most headlines, it is actually lending-based crowdfunding that dominates the industry: in 2014, it raised $11.08Bn. Part of that, according to Massolution founder and CEO Carl Esposti, is explained by the strong growth of crowd-based lending in Asia: “Surprises materialising from this year’s research included the astounding growth in the P2P and P2B lending market in Asia, stemming largely from the Chinese market.”

Other key drivers underpinning the rampant growth of crowdfunding in Asia can be attributable to the following three factors:

1) Online marketplace popularity (explosion of retail e-commerce). It is estimated for APAC to outspend North American by $40Bn. In fact, 45% of all buyers worldwide on retail e-commerce come from Asia.

2) Social media penetration and savvy. 52% of social media users and 47.6% of mobile users are from Asia. 3) Success and popularity of crowdfunding. Singapore now ranks in the top ten worldwide for crowdfunding.

Compound this by the fact that two thirds of the world’s global middle class will live in Asia by 2030 with $3.5Bn coming from emerging economies; crowdfunding in Asia is clearly here to stay and is poised for even more rapid growth.

Is Asia Ready For Crowdfunding?

Asian markets and regulatory structures are not as sophisticated nor developed as say, the Americas. As such, this naturally begs the question as to whether Asia is really ready to embrace the crowdfunding tidal wave? According to Doctor Jeffrey Chi, Managing Director of Vickers Venture Partners and Chairman of the Singapore Venture Capital & Private Equity Association, the answer is that Asia is absolutely ready to embrace the crowdfunding movement. It is his view that emerging markets are actually more suitable for crowdfunding than mature markets. This is because gaps in the marketplace and lack of access to capital are more pronounced in these markets.

“Crowdfunding in Asia Poised for Rapid Growth”

Director, Marketing & Business Development, DealIndexMICHELLE TANG

30

PLATFORMS

Over time one would expect a broad swath of financial services currently carried out at bricks and mortar institutions to transition to alternative models as business and cultural support is gained

“

Reward Crowdfunding Popularised by Indiegogo and Kickstarter, donation-based funding allows users to make donations to companies or non-profits raising capital in return for an incentive. Those incentives include early access to products, gifts, or an increased sense of self-worth. Compared to equity and debt-based models, rewards based crowdfunding applies mainly to firms in the idea or early prototype phase, or organisations that wouldn’t seek traditional financing like not-for-profits. As recently as July 2015, Kickstarter had $1.8Bn in pledges by 9Mn+ total backers.

Reward based platforms, such as Kickstarter, have proved particularly beneficial to companies who are developing products. The platforms provide an important portal through which issuers can market their product directly to consumers, gain feedback on initial prototypes and validate their ideas, essentially de-risking the process of starting a business. In turn, this makes it more likely that they will go onto raise Angel/VC rounds in the future.

However, with the present capital gap for enterprises in both the start-up and early growth phase discussed above, alternative finance solutions have rapidly moved upstream. No longer are issuers solely looking for seed capital. Companies in the early stage and growth phase are all tapping funding platforms as a means to raise capital.

Democratising Finance Platforms

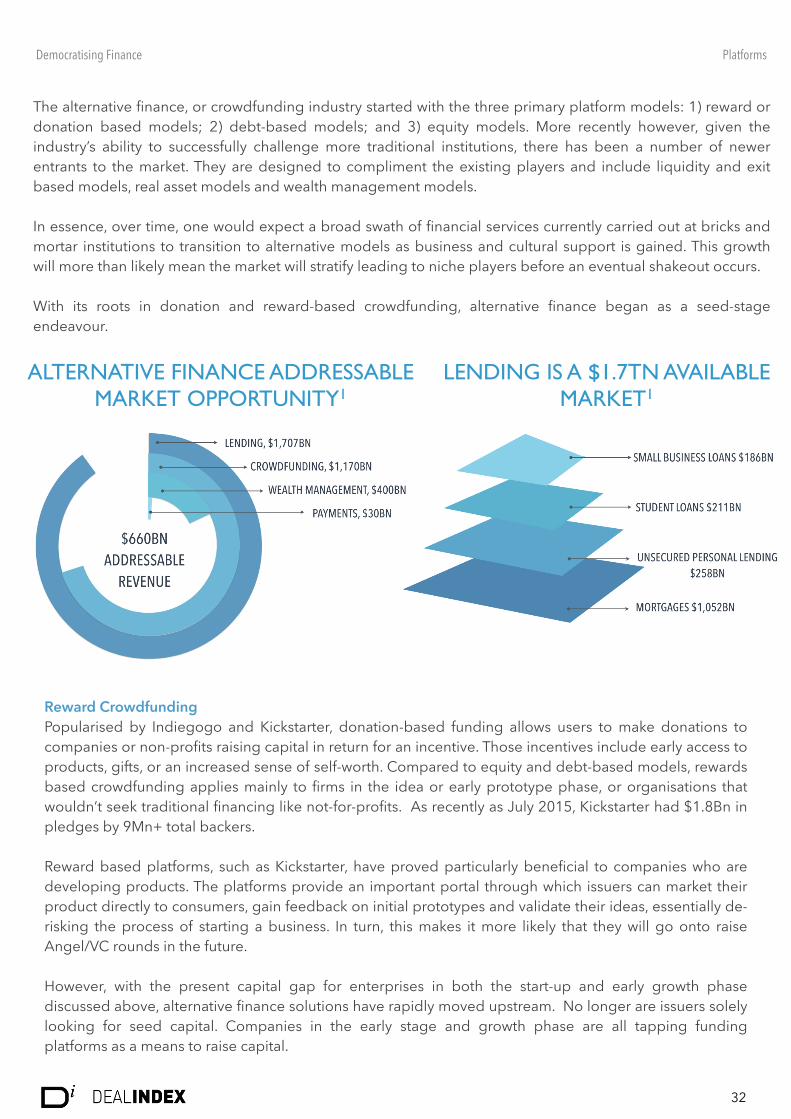

The alternative finance, or crowdfunding industry started with the three primary platform models: 1) reward or donation based models; 2) debt-based models; and 3) equity models. More recently however, given the industry’s ability to successfully challenge more traditional institutions, there has been a number of newer entrants to the market. They are designed to compliment the existing players and include liquidity and exit based models, real asset models and wealth management models.

In essence, over time, one would expect a broad swath of financial services currently carried out at bricks and mortar institutions to transition to alternative models as business and cultural support is gained. This growth will more than likely mean the market will stratify leading to niche players before an eventual shakeout occurs.

With its roots in donation and reward-based crowdfunding, alternative finance began as a seed-stage endeavour.

ALTERNATIVE FINANCE ADDRESSABLE MARKET OPPORTUNITY1

LENDING IS A $1.7TN AVAILABLE MARKET1

32

Since “Star Citizen,” the video game, initially raised $6Mn on Kickstarter and CIG simultaneously in 2012, donations have continued to come from nearly 750,000 ordinary fans at a steady pace of $1-2 million per month. The end result, one of the largest reward crowdfunded project to date at $52Mn. The pledges have ranged in size from $36 – 18k. In return, those making donations get access to special game features, access to unfinished game versions and other merchandise.

Compared to traditional financing, it appears customers, or “fans,” like having input in a finished product. Through their donations, they have a say in development, resulting in a more marketable finished product.

STAR CITIZEN

P2P/Marketplace Lending As it stands, debt-based alternative funding appears more popular with more mature and well-established SME’s, many of whom prefer the cost benefits of an alternative-funding model. Currently, the largest debt-based players include Funding Circle, Lending Club, and Prosper. As evidenced by Lending Club’s recent IPO, this sector of lending continues to gain traction on both the consumer and commercial side. This includes more than $9.2Bn of loans issued by Lending Club and $1Bn issued by Funding Circle. Morgan Stanley estimates that the P2P lending market, which it says is a “misnomer” because of increased institutional activity in the space, will be worth $290Bn in five years12.

As the lending market matures and grows further, drawing in more institutional money such as from pension funds, we expect to see increasing importance placed on good due diligence. This pressure is also likely to come from regulators as the platforms handle larger amounts of capital and appear in the news more.

Democratising Finance Platforms

PROJECTED CROWDFUNDING MARKET GROWTH IN EUROPE4,5

33

GLOBAL CROWDFUNDING MARKET 20144,5

LENDING CLUB IPO

In early December, the peer-to-peer lender, Lending Club, debuted on the New York Stock exchange to strong investor support. On its first day of trading, valuation climbed north of $9Bn, putting it on par with much larger financial institutions by assets. While this is an accomplishment in and of itself for Lending Club, it also serves as a sign that alternative finance has arrived to the mainstream.

Ultimately, it remains to be seen if Lending Club’s goal of transforming the entire banking system from a transparency and efficiency perspective comes to pass, but its IPO certainly added credibility to its cause and the greater cause of alternative finance.

Equity Crowdfunding Equity Crowdfunding has been on the rise for some years, with the UK leading the charge. Other countries, like Australia and New Zealand also made early regulatory moves in the area. Both the US and UK began discussing crowdfunding rules in 2010, but the UK has been faster in allowing broad public access. In 2013, with the passing of the JOBS Act in the United States, equity crowdfunding was made available to accredited investors. Numerous platforms have emerged to serve this market segment and there is now an increasing array of companies at various stages of the funding cycle and operating different business models. These include businesses in the growth equity, private placement, M&A, secondary, and wealth management markets. These platforms are now able to provide a holistic solution for businesses at all stages of the funding cycle. Equity crowdfunding models provide young businesses with a platform that allows them to reach a wide range of investors.

Democratising Finance Platforms

UK MARKET BY TYPE OF PLATFORM 20144,5

UK AVERAGE GROWTH RATE BY TYPE OF PLATFORMS 2012-20144,5

34

What are issuers looking for from crowdfunding providers? What are the key value propositions? Issuers are looking for market appeal and validation. They need crowdfunding providers that can provide them with tools to refine their offerings so they can present them in a manner that is appealing to a large number of investors who may be interested in their companies. Value propositions such as business planning and analysis solutions, document hosting and sharing capabilities, and social media integration methods are vital to accomplish this task.

What has been the feedback from the angel and VC market on your platform? Are there any features you are keen to add, or modify, based on the feedback? Angels and VC’s want the ability to quickly and efficiently screen deal flow. Our system is designed so deals are categorised by automated, unbiased, and patent protected indicators. Angels and VC’s can see a rating of each deal based on dozens of attributes so they can quickly find the ones that meet their investment criteria. They are also provided with data regarding progress towards a company’s funding goal which includes pre-money valuation, funding raised so far, a percentage of how much ownership is for sale, current funding commitments, and funding raised in the past. All investors on our platform can also request any documents that pertain to an issuer’s fundraise at any time. This includes the results from our Enterprise Analyzer software which highlights abnormalities in the company’s business plan, benchmarks the company against its peers within its industry, and provides a host of other financial analytics presented in a standardised format.

What are the current liquidity characteristics of the equity crowdfunding market? How do you see this evolving over the coming months and years? There currently are not any liquidity characteristics of the equity crowdfunding market in the US. Some current regulations require a holding of securities purchased from private placements. Investors can be required to warrant they are not investing for trading purposes, so investments made through crowdfunding are considered long term by many. New regulations, however, may reduce transfer restrictions, which will lead to a general movement towards a secondary market. Companies such as WealthForge have taken great steps towards liquidity by working with CUSIP Global Services to create a standardised database for private investments by issuing unique alphanumeric codes to private securities sold within the crowdfunding industry.

Platform: Equity Crowdfunding Country: United States

Founded: 2005 Funding provided to date: US$330Mn+

EQUITYNETPARTNER CONTRIBUTION

35

What are issuers looking for from crowdfunding providers? What are the key value propositions?Through crowdfunding campaigns, issuers are looking to increase brand awareness, accelerate global fundraising and create communities that can help them to grow their business. Crowdfunding campaigns bring a lot of visibility (press, events and online marketing) to companies. Furthermore, after the campaign finishes, companies can expect the investor community to continue to promote the company, buy the product, advise the entrepreneur and share with their network.

Our key value proposition is to help European SME’s to scale by making pan-European public placement affordable. We are headquartered in Belgium but we operate across the EU and are currently raising funds for French, German, Belgian and Dutch companies.

What are the characteristics of the investors you are, or expect to, work most closely with? We have 3 different types of investors: • Unaccredited investors, who invest on average €700 per transaction. • Business Angels and sophisticated investors who invest an average of €45k per transaction. • VC Funds who invest up to €200k in a deal.

What has been the feedback from the angel and VC market on your platform? Angel and VC’s investors like the fact that MyMicroInvest publishes an information memorandum or prospectus for each new transaction on the platform. Professional investors want to leverage their investment alongside the crowd, who validate the company concept/offer and also like that companies can capitalise on their community to promote the business in the long term. MyMicroInvest offers a simple and efficient crowdfunding solution to issuers by pooling all crowd investors in one single investment vehicle. The simplicity of the structure, whereby all crowd investors are pooled into our investment vehicle instead of investing directly in the target company is an attractive feature.

What do issuers see as the main benefit of listing on your platform? MyMicroInvest actively promotes each company by doing lots of offline and online marketing such as live crowdfunding events. We also have partnerships with major banks such as BNP Paribas, Fortis and KeyTrade Bank. Furthermore, we can help issuers to connect with sophisticated investors such as Angels and VC’s.

What are the current liquidity characteristics of the equity crowdfunding market? How do you see this evolving over the coming months and years? The current liquidity of the equity crowdfunding market is low even though our investors can transfer his/her share(s) to a third party. We believe this situation will quickly evolve since stock markets are willing to list our titles on their market.

Platform: Lending and Equity Crowdfunding Country: Belgium, EU

Founded: 2011 Funding provided to date: €10Mn

PARTNER CONTRIBUTION

MYMICROINVEST

36

Over the past five to ten years the landscape for alternative investing has changed greatly due to technology. Crowdfunding platforms have facilitated a massive influx of capital to early stage/seed stage companies including technology, real estate and everything in between. Traditionally, founders had to approach individual venture capital firms, angel associations and other institutional sources one at a time and wait for a response regarding either the investment size or valuation. What we have successfully done at Onevest is not only enable entrepreneurs to go out and raise money through the traditional sources as mentioned above, but employ fundraising tactics such as equity crowdfunding. At Onevest we do not act as a replacement but as a supplement to their fundraising efforts. Technology has enabled entrepreneurs to reach out to a wider audience in a shorter amount of time to not only showcase their product but to also raise funds.

Issuers look for a platform where they can successfully meet or exceed their fundraising goals. They look to us to perfect their pitch and to understand the general investing landscape. In regards to key value propositions, when it comes to fundraising, the CEO or co-founder has one of two choices, they can either continue to run their business, or go out for 6-9 months and exclusively focus on fundraising. It is near impossible to do both simultaneously and that is why we see such a large value proposition as an equity crowdfunding platform. Digital investment services are not new, there are companies such as, Charles Schwab, E*trade, Fidelity and basic brokerages that offered their services online. What Onevest is doing is democratising private placement capital. What that means is that founders are able to go online and start fundraising ideas. Individuals out there, as long as they are accredited investors or more recently non-accredited with the passing of Title IV, can now participate in those companies that they have been reading about over the past 10-15 years, that have been going public and not been able to participate until they are publicly traded. Onevest focuses primarily on tech enabled companies but there are other crowdfunding platforms that fundraise exclusively for real estate, biotech and other company types. We chose tech companies because we have an advisory base that are well known amongst the early stage investment community and we are therefore able to execute a vigorous due diligence process on each company.

We have seen investors all across the field from doctors and lawyers to small business owners, former entrepreneurs and real estate developers. Furthermore, the investors that commit the highest level of capital seem to be very knowledgeable about the specific sector that they are investing in. Angel groups often look to us for the due diligence. Every company has a full due diligence report, financial records, pitch deck and all necessary collateral for an angel or an angel group to make an educated decision on whether or not he or she will make an investment into that company. Regarding VC firms, we have been able to form strong partnerships with them due to our vigorous due diligence process. We are able to provide both groups with quality deal flow that they would otherwise not be able to filter through any process.

Platform: Equity Crowdfunding Country: United States

Founded: 2010

ONEVESTPARTNER CONTRIBUTION

37

We recently spoke to Raizers a Pan-European equity crowdfunding platform located across France, Denmark, Switzerland, and with intentions to spread throughout Europe. They help companies to raise between €50k to 1m.

Raizers is the only French crowdfunding platform with a European dimension, with offices located in Paris (France), Lausanne (Switzerland) and in Copenhagen (Denmark). The issuers benefit from this cross-country community through the global vision they have and the help they can give while expanding abroad.

Most of their investors tend to already be consumers of a product, or will be post-investment and act as brand ambassadors who can provide the companies with important feedback. In France a lot of their investors are attracted because of the tax exemptions for equity investors, while debt investors tend to purely be looking for higher returns than other avenues.

VC and Angels are also important to Raizers, who solicit them at the beginning of the round, as the crowd is more likely to invest if the round is subscribed to already. As with many other platforms, Raizers noticed that it was easier to incentivise the crowd to invest when 30% of the financing objective was already realised.

Liquidity still remains a concern for the equity crowdfunding market in Europe, as it does for most people in the sector. Raizers tends do deal with this through tag-along and drag-along clauses, or even calls integrated into the shareholders agreement.

Platform: Equity Crowdfunding Country: France, Switzerland, Denmark

Founded: 2014

RAIZERSPARTNER CONTRIBUTION

38

Previously, we talked with Snowball Effect, a crowdfunding platform based in New Zealand where securities law has been overhauled and a new equity crowdfunding framework was installed in 2014. Now, Kiwi companies can raise up to NZD 2Mn publicly over a rolling twelve month period.

Snowball Effect was one of the first equity crowdfunding platforms in New Zealand to be granted a license in July 2014, and the industry certainly remains in its infancy. However, success has already come for Snowball Effect. To date, issuers have raised in excess of NZD8Mn at an almost 100% success rate via Snowball Effect’s platform. The largest was Invivo, one of New Zealand’s fastest growing wine brands, which raised NZD2,000,000 (maximum possible in New Zealand) through Snowball Effect.

Snowball Effect’s strategy is to showcase a range of companies from New Zealand to test and grow the awareness of equity crowdfunding in its corner of the globe. Other successful raises to date through Snowball Effect include Renaissance Brewing (beverage sector), The Patriarch (first major feature film in the world to be funded through equity crowdfunding), Carbonscape (cleantech sector), Aeronavics (advanced aerial solutions) and Breathe Easy (pharmaceutical company), Red Witch (guitar and bass effects pedals company) and Punakaiki Fund (invests in early/growth stage NZ businesses). Snowball Effect has also raised funds successfully for two private offers and expects private offers to increase over the next 12 months.

Similar to global peers, Snowball Effect takes a multifaceted approach to evaluating issuer applications. Selection criteria includes: (1) performance, (2) markets and product advantage, (3) growth, (4) capability, (5) governance, (6) financials, (7) legal, and (8) pre-committed funds/networks. In its words, companies looking for growth or expansion capital are in its sweet spot, as they can benefit best from the brand exposure and support brought by a public equity crowdfunding offer.

The Executive Director of CarbonScape provided his feedback on the process of raising funding through Snowball Effect:

“Equity crowdfunding has been an absolute life saver for our small start-up CarbonScape Ltd. Despite two distinguished international awards for our technology we could not escape the narrow limits of New Zealand's "eligible investor" criteria. In one of their best moves the Government changed all that with the April 2014 Financial Markets Conduct Act. Suddenly there are platforms like Snowball Effect acknowledging the right and maturity of ordinary mum and dad Kiwis to make their own assessments of commercial risk in equity investments. 207 mostly New Zealanders invested an average of $3,850 and the company raised $764,302, well above our $400,000 target.”

Platform: Equity Crowdfunding Country: New Zealand

Founded: 2012 Funding provided to date: NZD8Mn+

PARTNER CONTRIBUTION

SNOWBALL EFFECT

39

Co Investment Models More recently hybrid, co-investment models focused on early stage issuers have emerged, pioneered by OurCrowd and VentureFounders. These platforms allow investors to co-invest alongside the co-investment funds they manage and more traditional VC investment and differentiate themselves by their level of due diligence and investment management expertise.

OurCrowd, for example, have channelled around $130Mn into 70 companies with plans to invest another $100Mn by the end of 2015. They have a 50 person due diligence team that vets deal before they are presented to investors and invest between 5-15% of the funding in every deal13. They recently invested in ReWalk Robotics, an exoskeleton company that helps disabled people to walk, who having listed recently, have a market cap of around $160Mn.

Investor-Led/Syndicate Models Investor-led platforms, adopted by AngelList in the US and SyndicateRoom in the UK form syndicates around accredited lead investors, whereby the lead investor must invest their own money, negotiate the terms and then invite other investors to join under those same terms, (lead investors also carry out the diligence which provides comfort to the syndicate, this model has resulted in investment from non-traditional sources of private company funding). The idea of both platforms is to open up the deals that the top investors are investing in to the online community and continues our theme of broadening the scope of the private market.

This platform model gives other investors peace of mind by investing alongside professional investors, with the platforms benefiting by taking a slice of the carry on deal. This emerging model also highlights the increasingly collaborative relationship that exists between alternative finance and the traditional investing community. Rather than trying to replace the traditional VC-led funding paradigm, alternative finance is developing a symbiotic and mutually beneficial relationship with the angel and VC community.

Niche Platforms The increasing proliferation of platforms in recent times has meant that a number of new entrants to the market are choosing to specifically target niche sectors. This has been the case with Trillion Fund, who concentrate on clean-tech investment opportunities; AgFunder, who follow a syndicated investment model and operate in the $6.4Tn Food and Agriculture industry and TradeUp, who focus on export driven companies.

40

PARTNER CONTRIBUTION

Agriculture is a $6.4Tn market employing roughly 1.3Bn people around the world. It has outperformed all other sectors but one over the past 15 years, yet there are few avenues for investors to access this asset class and few investors have exposure to agriculture in their portfolio. One reason it’s been so difficult for investors to access agricultural investments is because the industry is highly fragmented. Current investment figures indicate that agriculture needs $200Bn in annual investment in growth and innovation just to keep pace. The lack of funding and cohesiveness across the agriculture industry presents a serious problem because current agricultural production capacity must grow by as much as 70 percent by 2050 in order to supply a global population of over 9 billion people.

The next wave of agriculture will look fundamentally different due to the new technologies now available in this sector, like drones, autonomous vehicles, indoor agriculture operations, and more. Investors looking for exposure to long term trends like population growth, protein consumption, and climate change are increasingly searching for opportunities in pure-play agriculture or in agriculture technology companies.

AgFunder seeks to play a central role in facilitating the funding, access to investment, and ecosystem development for the industry as it enters this next generation. The company has directed nearly $20M in investment into agriculture and agtech companies, with that figure set to double this year.

To help facilitate investment, equity crowdfunding - and technology generally - is key to enabling investment on a global scale. First, crowdfunding offers important procedural benefits. One of the most obvious is the reduction in time that it typically takes to raise funding. A crowdfunding platform offers a much faster way to attract and secure capital. The costs and expenses associated with running a crowdfunding campaign are often significantly less expensive than pursuing funding through a traditional channel. For investors, it offers a shorter investment cycle by providing access to curated deals, transparency, centralising company information and documentation, and enabling electronic investment.

A crowdfunding platform with vertical focus like AgFunder’s allows both companies and investors to self-select around a particular topic and for AgFunder to provide added value and expertise for both parties. Issuers target a curated list of investors who possess industry knowledge, domain expertise, or are simply interested in investing in the space. All of this takes place on a platform that removes key geographical constraints, magnifying the community exponentially.

Currently, AgFunder has over 5,500 registered members. Roughly 1,300 of those members are accredited investors, with over 45% of them coming from venture capital firms, family offices, private equity firms, and even sovereign wealth funds. In addition to pure fundraising functions, AgFunder has also established and continues to cultivate an ecosystem for investment in agriculture. Through its affiliate news site AgFunderNews, investors, partners, experts, corporates, and media outlets interested in food and agriculture technology can learn about new innovations, industry developments, and funding news.

Founded: 2012 Funding provided to date: $20Mn

Platform: Equity Crowdfunding Country: United States

AGFUNDER

41

PARTNER CONTRIBUTION

How have you leveraged crowdfunding in the angel investment market? Equity crowdfunding is the platform that allows us to do our business. It enables us to get our research across to an international community of investors, and provide them with everything they need in order to make intelligent investment decisions in Israeli startups.

What have been the keys to the success of your business model? The key to our model is the alignment of interests between ourselves, our investors, and the lead angel investors we have partnered with. Investing alongside local lead angels with a proven track record and skin in the game, international investors can be assured that they are gaining access to the most exclusive deals the market has to offer and coming in on terms these angels have negotiated for themselves.