deloitte kenya technology, media & telecommunications (tmt) predictions 2016

TRANSCRIPT

Technology, Media and Telecommunications Predictions 2016

Technology Predictions

2© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

Touch commerce

3© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

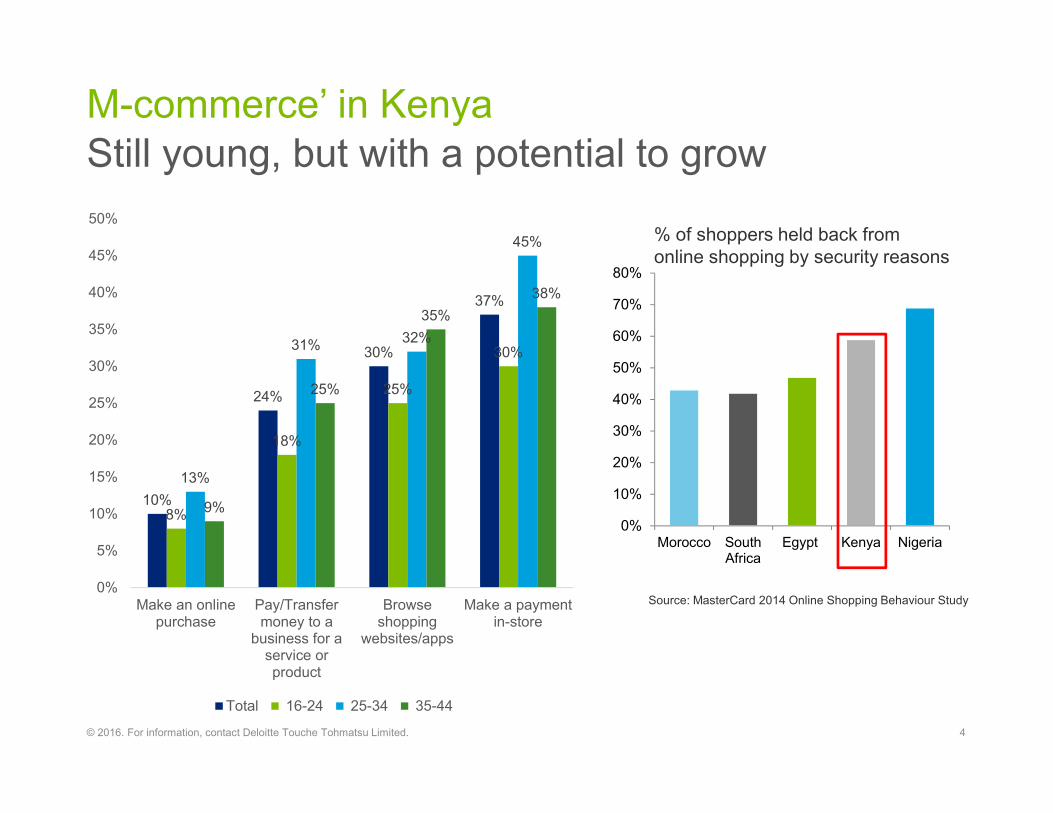

10%

24%

30%

37%

8%

18%

25%

30%

13%

31% 32%

45%

9%

25%

35%38%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Make an onlinepurchase

Pay/Transfermoney to a

business for aservice orproduct

Browseshopping

websites/apps

Make a paymentin-store

Total 16-24 25-34 35-44

M-commerce’ in Kenya Still young, but with a potential to grow

4© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

0%

10%

20%

30%

40%

50%

60%

70%

80%

Morocco SouthAfrica

Egypt Kenya Nigeria

% of shoppers held back from online shopping by security reasons

Source: MasterCard 2014 Online Shopping Behaviour Study

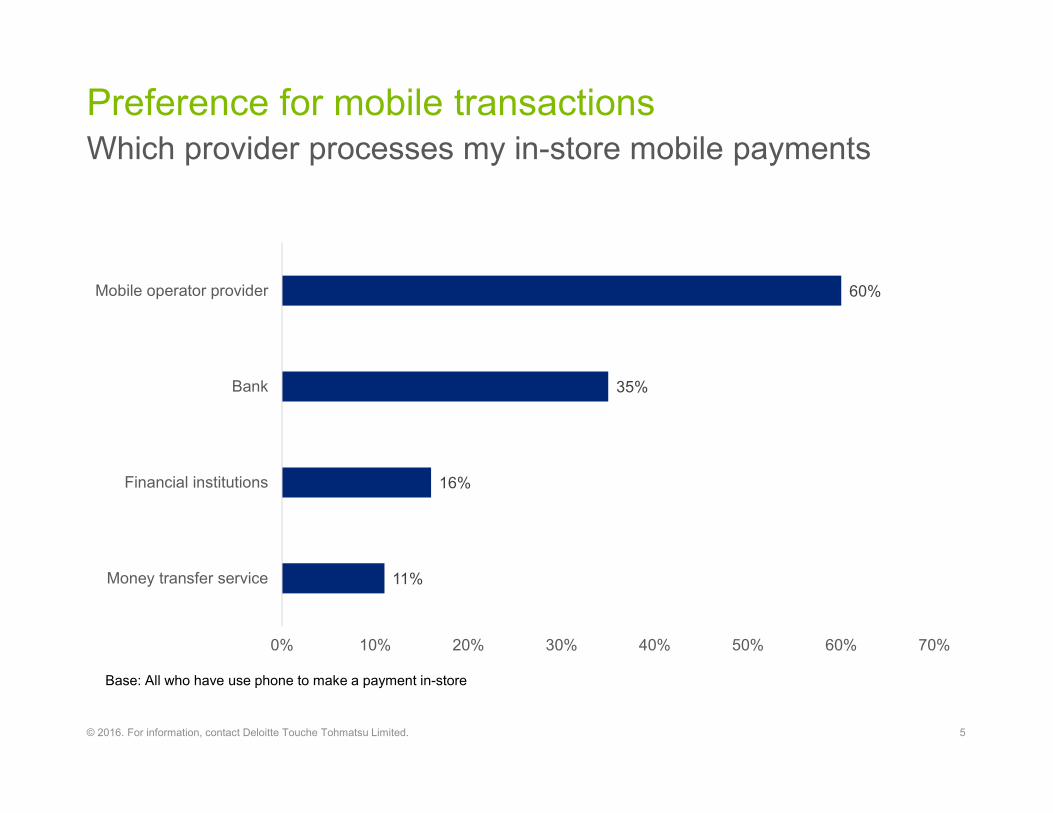

Preference for mobile transactionsWhich provider processes my in-store mobile payments

5© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

11%

16%

35%

60%

0% 10% 20% 30% 40% 50% 60% 70%

Money transfer service

Financial institutions

Bank

Mobile operator provider

Base: All who have use phone to make a payment in-store

Near Field Communications or ‘just’ Biometrics Innovation in Mobile Payment

We predict that the next major shift in preference for MNO or Bank will occur as the result of the next innovation.

Cognitive technologies enhance enterprisesoftware

7© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

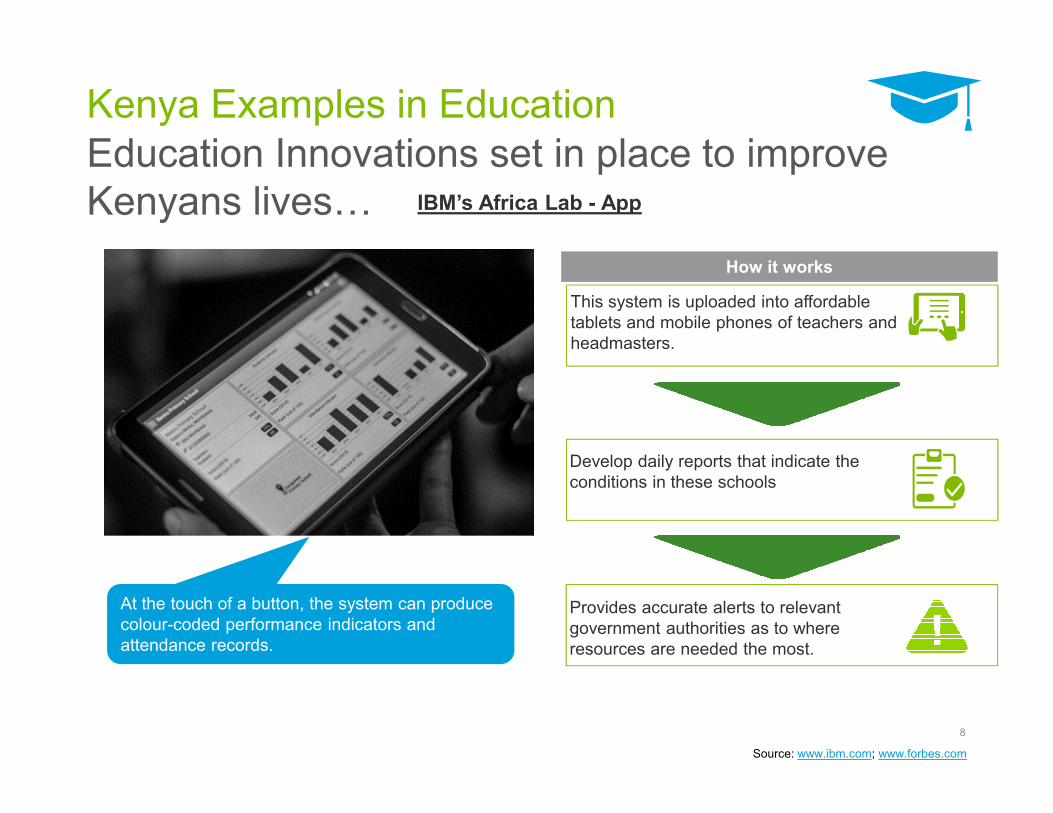

Kenya Examples in EducationEducation Innovations set in place to improve Kenyans lives…

8

Source: www.ibm.com; www.forbes.com

Develop daily reports that indicate the conditions in these schools

This system is uploaded into affordable tablets and mobile phones of teachers and headmasters.

IBM’s Africa Lab - App

Provides accurate alerts to relevant government authorities as to where resources are needed the most.

How it works

At the touch of a button, the system can producecolour-coded performance indicators and attendance records.

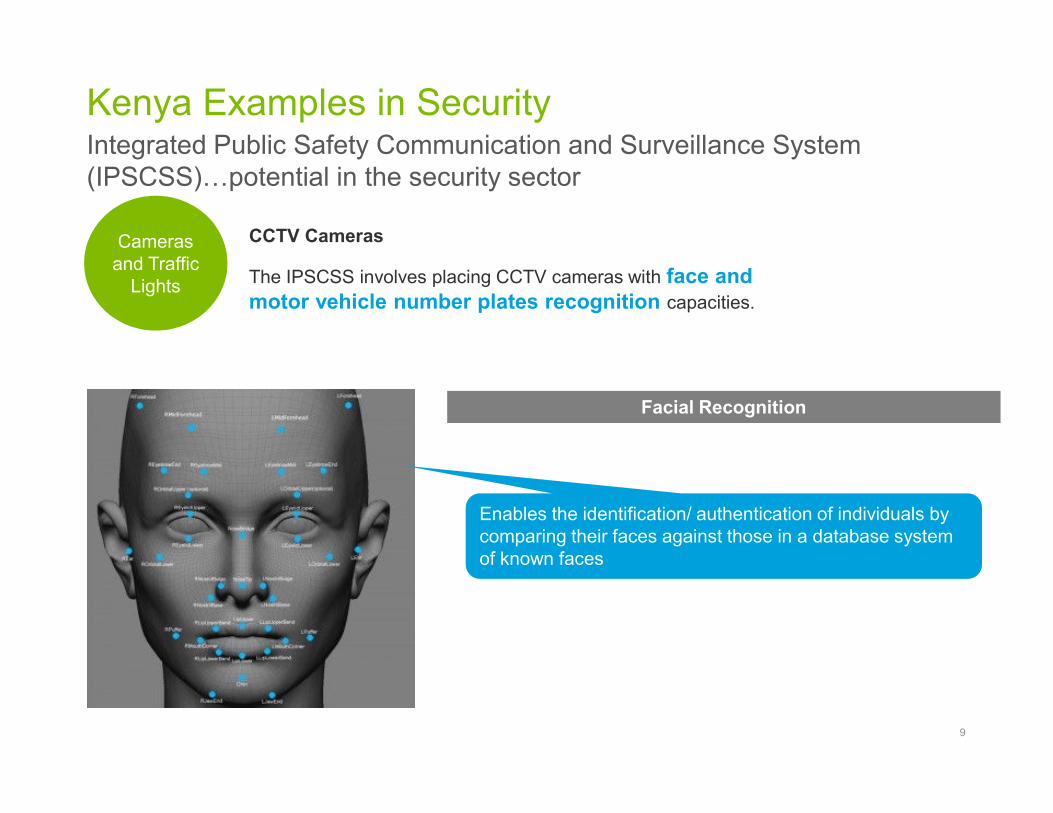

Kenya Examples in Security

9

Integrated Public Safety Communication and Surveillance System (IPSCSS)…potential in the security sector

CCTV Cameras

The IPSCSS involves placing CCTV cameras with face and motor vehicle number plates recognition capacities.

Cameras and Traffic

Lights

Facial Recognition

Enables the identification/ authentication of individuals by comparing their faces against those in a database system of known faces

Nairobi becoming a Smart City?

"A Smart City is an urban area where public and private

entities cooperate in achieving sustainable outcomes through the analysis of real-time

contextual information shared between different expert

systems"

The Singapore of Africa? Maybe not yet ….

Media Predictions

11© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

Sports Rights

12© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

We are contributing

Between 2013/14 and 2015/16 premier league seasons the English Premier League overseas rights were valued at GBP 743.3 million per annum.

English premier league overseas revenuesExpect to pay more for your football viewing

13© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

GBP 55M p.a.

GBP 10M p.a.

GBP 32M p.a.

Sub Saharan Africa’s annual revenue contribution to EPL is valued at GBP 68.3M

>

2016/17 -2018/19 Sub Saharan sports rights are now up to GBP 98M

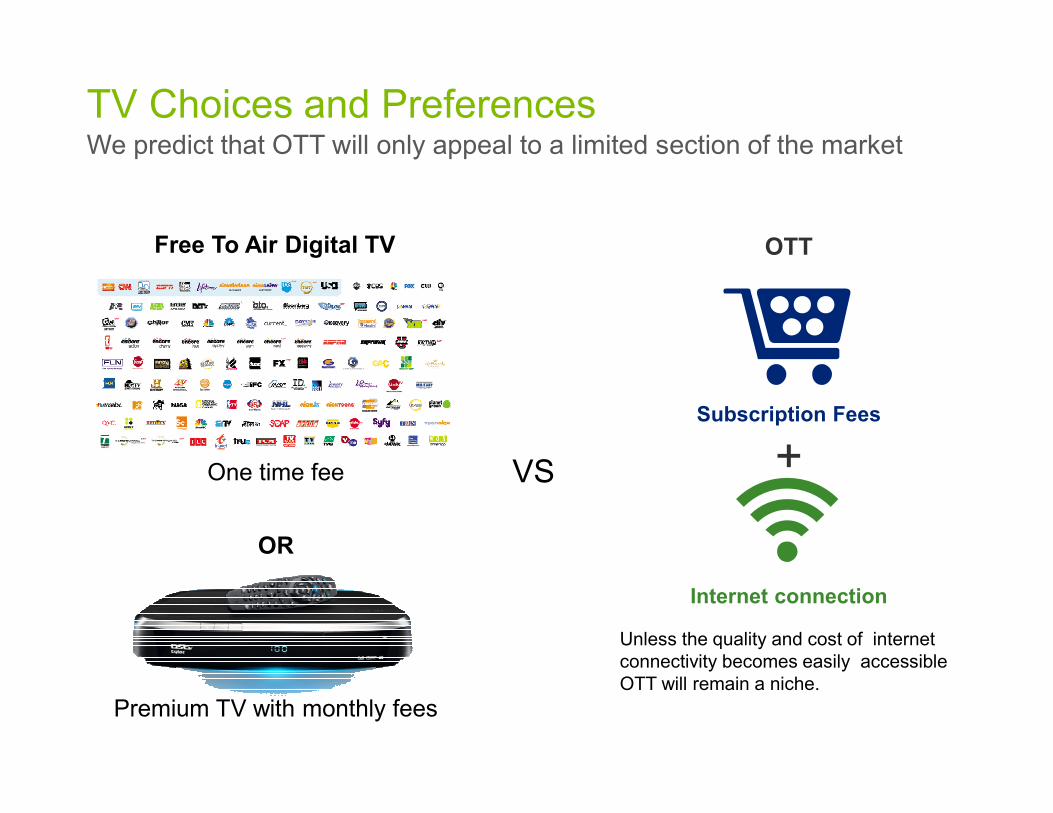

OTT: A Disruptor, but not yet

14© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

OTT

Subscription Fees

+

Internet connection

TV Choices and PreferencesWe predict that OTT will only appeal to a limited section of the market

One time fee

OR

Premium TV with monthly fees

Free To Air Digital TV

VS

Unless the quality and cost of internet connectivity becomes easily accessibleOTT will remain a niche.

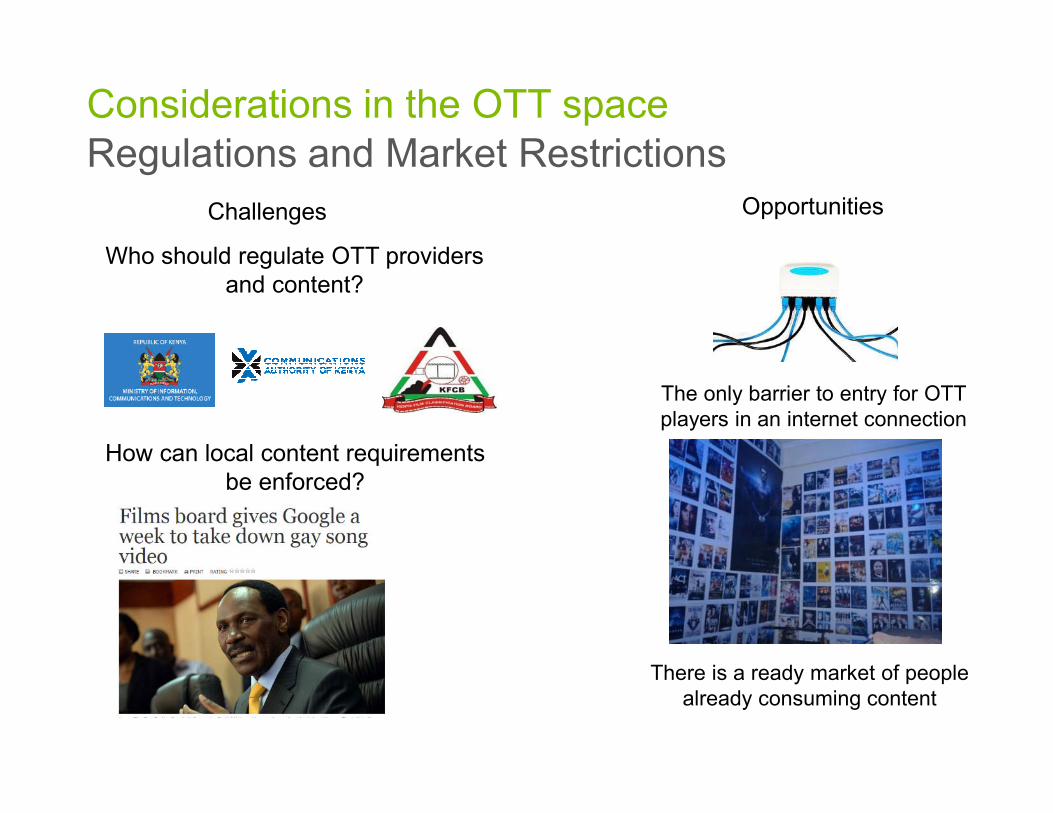

Considerations in the OTT spaceRegulations and Market Restrictions

Who should regulate OTT providers and content?

The only barrier to entry for OTT players in an internet connection

How can local content requirements be enforced?

OpportunitiesChallenges

There is a ready market of people already consuming content

Telecommunication Predictions

17© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

Used phones: the market you may have heard of

18© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

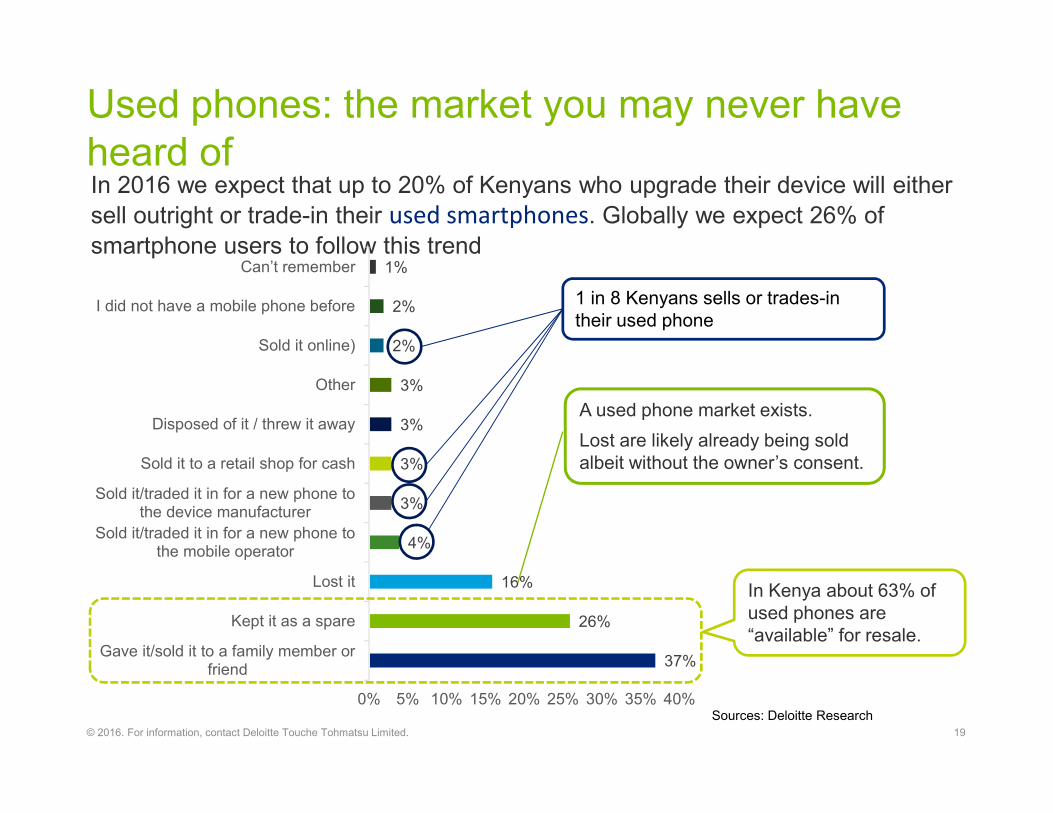

Used phones: the market you may never have heard of

19© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

In 2016 we expect that up to 20% of Kenyans who upgrade their device will either sell outright or trade-in their used smartphones. Globally we expect 26% of smartphone users to follow this trend

37%

26%

16%

4%

3%

3%

3%

3%

2%

2%

1%

Gave it/sold it to a family member orfriend

Kept it as a spare

Lost it

Sold it/traded it in for a new phone tothe mobile operator

Sold it/traded it in for a new phone tothe device manufacturer

Sold it to a retail shop for cash

Disposed of it / threw it away

Other

Sold it online)

I did not have a mobile phone before

Can’t remember

0% 5% 10% 15% 20% 25% 30% 35% 40%

In Kenya about 63% of used phones are “available” for resale.

A used phone market exists. Lost are likely already being sold albeit without the owner’s consent.

1 in 8 Kenyans sells or trades-in their used phone

Sources: Deloitte Research

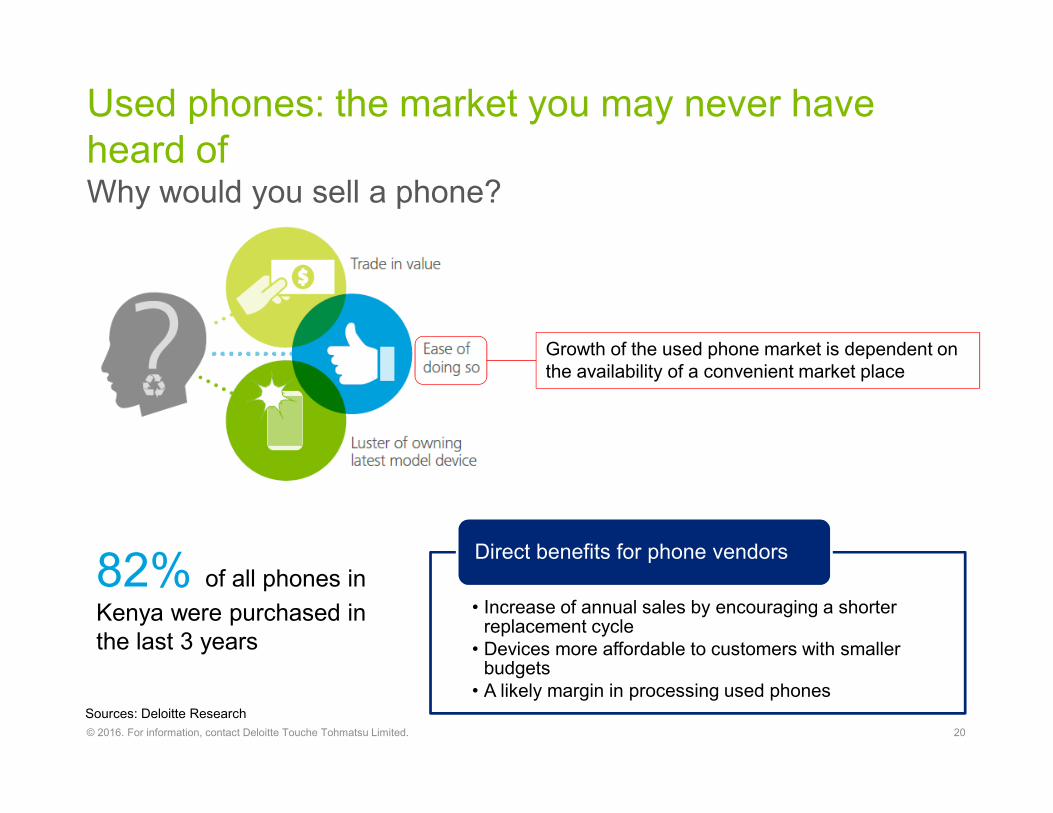

Used phones: the market you may never have heard ofWhy would you sell a phone?

20© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

• Increase of annual sales by encouraging a shorter replacement cycle

• Devices more affordable to customers with smaller budgets

• A likely margin in processing used phones

Direct benefits for phone vendors82% of all phones in Kenya were purchased in the last 3 years

Growth of the used phone market is dependent on the availability of a convenient market place

Sources: Deloitte Research

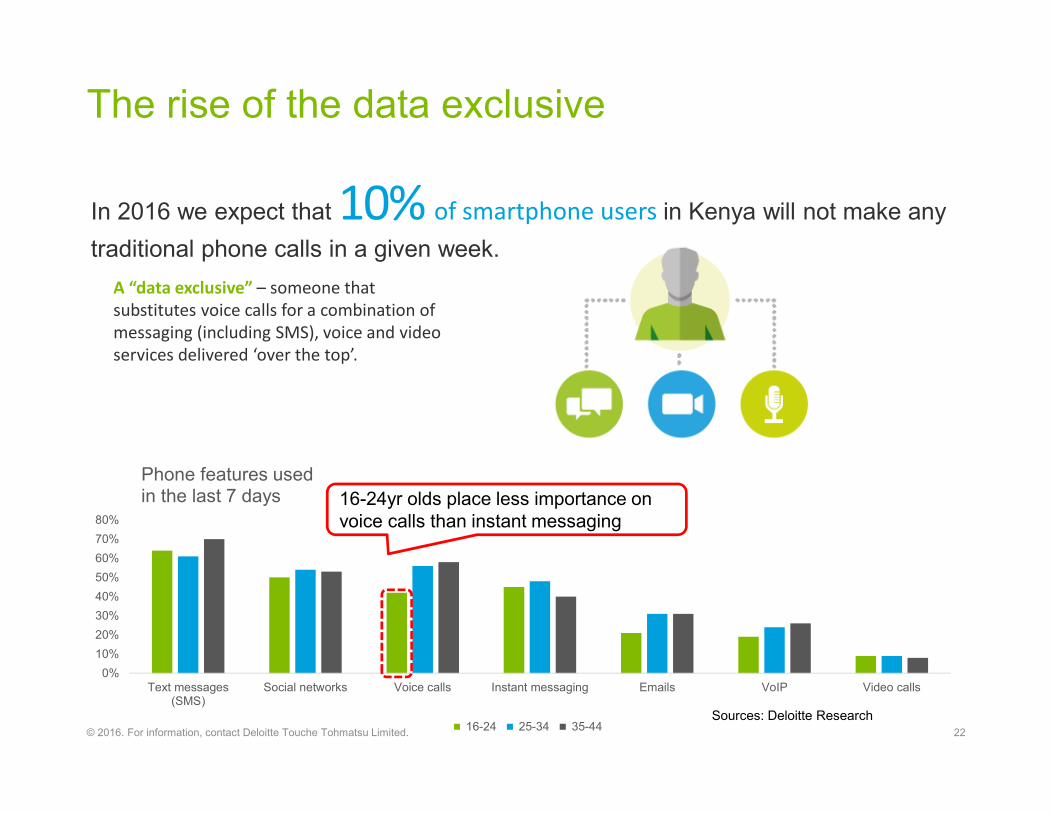

The rise of the data exclusive

21© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

The rise of the data exclusive

22© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

In 2016 we expect that 10% of smartphone users in Kenya will not make any traditional phone calls in a given week.

A “data exclusive” – someone that substitutes voice calls for a combination of messaging (including SMS), voice and video services delivered ‘over the top’.

0%10%20%30%40%50%60%70%80%

Text messages(SMS)

Social networks Voice calls Instant messaging Emails VoIP Video calls

Phone features used in the last 7 days

16-24 25-34 35-44

16-24yr olds place less importance on voice calls than instant messaging

Sources: Deloitte Research

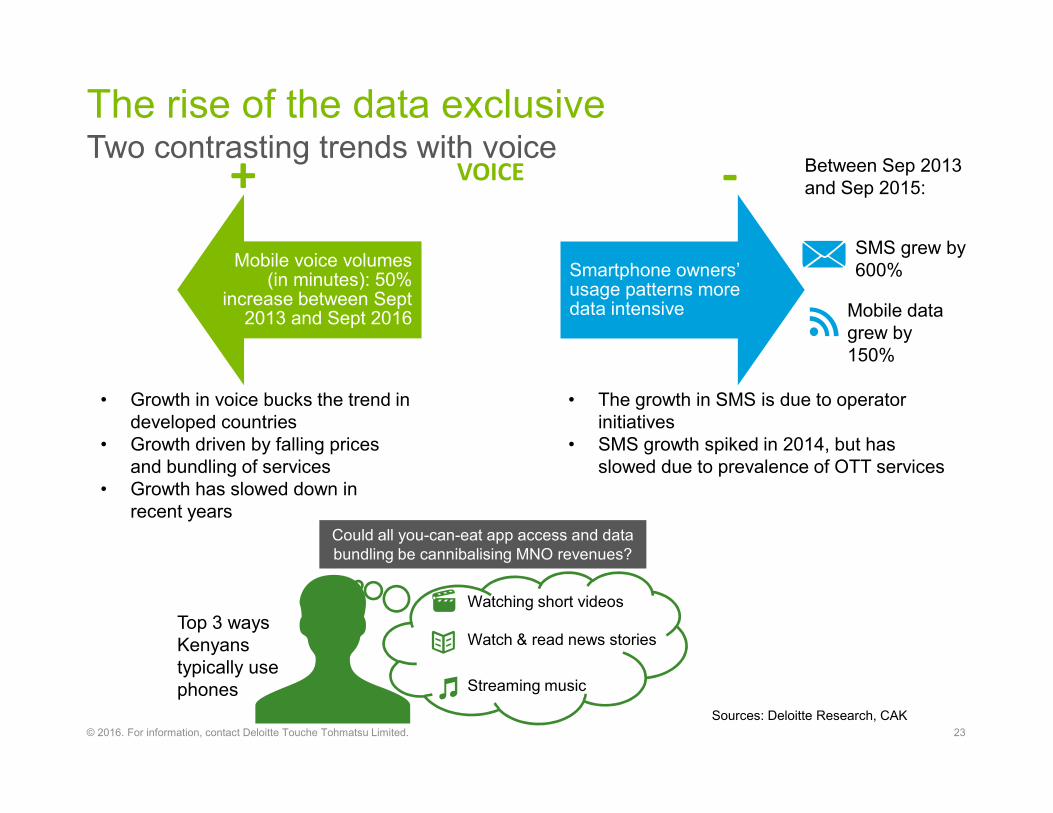

The rise of the data exclusiveTwo contrasting trends with voice

23© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

Mobile voice volumes (in minutes): 50%

increase between Sept 2013 and Sept 2016

Smartphone owners’ usage patterns more data intensive

VOICE+ -SMS grew by 600%

Mobile data grew by 150%

Between Sep 2013 and Sep 2015:

• Growth in voice bucks the trend in developed countries

• Growth driven by falling prices and bundling of services

• Growth has slowed down in recent years

• The growth in SMS is due to operator initiatives

• SMS growth spiked in 2014, but has slowed due to prevalence of OTT services

Could all you-can-eat app access and data bundling be cannibalising MNO revenues?

Watch & read news storiesTop 3 ways Kenyans typically use phones

Watching short videos

Streaming music

Sources: Deloitte Research, CAK

The rise of the data exclusiveData over voice

24© 2016. For information, contact Deloitte Touche Tohmatsu Limited.

3rdoverall in frequency of usage over

seven days after SMS and Social networks.

4thoverall on increase in frequency of

usage in the last 12 months after SMS, Social networks and Instant messaging

In Kenya voice calls were ranked

Voice calls rank SA UG NG ZW

Seven day usage 5th 2nd 3rd 3rd

12 month increase 4th 2nd 3rd 4th

Regional Comparison

Sources: Deloitte Research

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, consulting, financial advisory, risk management, tax, and related services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 210,000 professionals are committed to becoming the standard of excellence.

This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this publication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this publication.

25© 2016. For information, contact Deloitte Touche Tohmatsu Limited.