delivering greater value for shareholders - rio tinto · by reviewing/attending this presentation...

TRANSCRIPT

Delivering greater value for shareholders Bank of America Merrill Lynch conference

13 May 2014

©2014, Rio Tinto, All Rights Reserved

Cautionary statement

This presentation has been prepared by Rio Tinto plc and Rio Tinto Limited (“Rio Tinto”) and consisting of the slides for a

presentation concerning Rio Tinto. By reviewing/attending this presentation you agree to be bound by the following conditions.

Forward-looking statements

This document contains certain forward-looking statements with respect to the financial condition, results of operations and

business of the Rio Tinto Group. These statements are forward-looking statements within the meaning of Section 27A of the US

Securities Act of 1933, and Section 21E of the US Securities Exchange Act of 1934. The words “intend”, “aim”, “project”,

“anticipate”, “estimate”, “plan”, “believes”, “expects”, “may”, “should”, “will”, “target”, “set to” or similar expressions, commonly

identify such forward-looking statements.

Examples of forward-looking statements include those regarding estimated ore reserves, anticipated production or construction

dates, costs, outputs and productive lives of assets or similar factors. Forward-looking statements involve known and unknown

risks, uncertainties, assumptions and other factors set forth in this presentation that are beyond the Rio Tinto Group’s control.

For example, future ore reserves will be based in part on market prices that may vary significantly from current levels. These may

materially affect the timing and feasibility of particular developments. Other factors include the ability to produce and transport

products profitably, demand for our products, changes to the assumptions regarding the recoverable value of our tangible and

intangible assets, the effect of foreign currency exchange rates on market prices and operating costs, and activities by

governmental authorities, such as changes in taxation or regulation, and political uncertainty.

In light of these risks, uncertainties and assumptions, actual results could be materially different from projected future results

expressed or implied by these forward-looking statements which speak only as to the date of this presentation. Except as required

by applicable regulations or by law, the Rio Tinto Group does not undertake any obligation to publicly update or revise any forward-

looking statements, whether as a result of new information or future events. The Group cannot guarantee that its forward-looking

statements will not differ materially from actual results.

2

©2014, Rio Tinto, All Rights Reserved

3

Delivering greater value for shareholders

Consistent execution of a clear strategy

Strong operational performance

Disciplined capital allocation

Transformation underpinned by innovation

©2014, Rio Tinto, All Rights Reserved

4

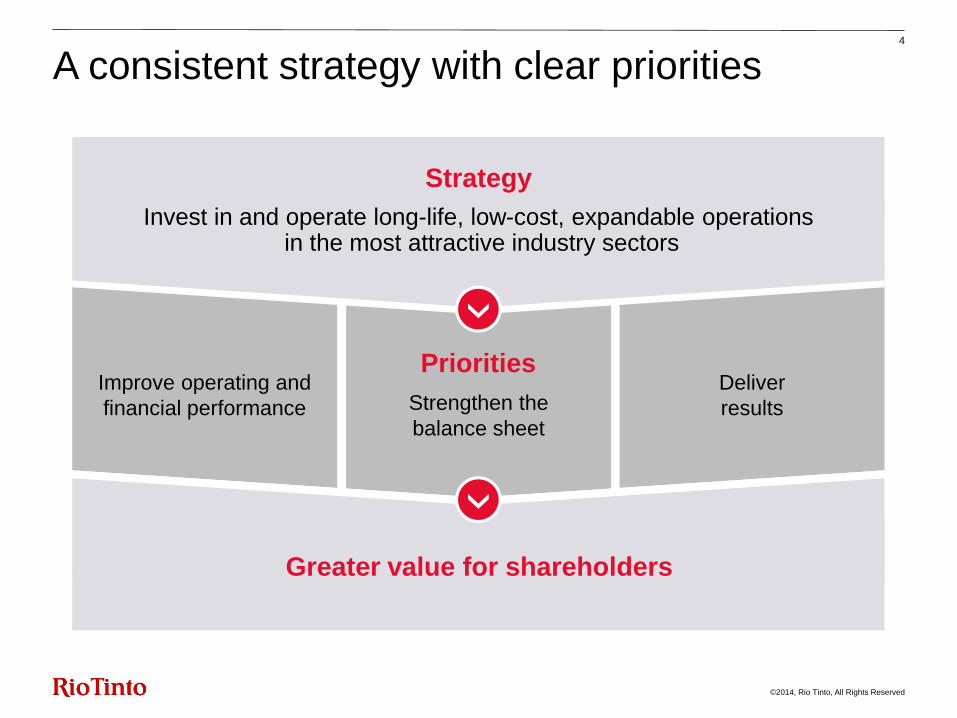

A consistent strategy with clear priorities

Improve operating and

financial performance

Priorities

Strengthen the

balance sheet

Deliver

results

Strategy

Invest in and operate long-life, low-cost, expandable operations in the most attractive industry sectors

Greater value for shareholders

©2014, Rio Tinto, All Rights Reserved

Mine of the Future™ is delivering results today 5

Pilbara – AutoHaulR

Processing Excellence Centre

AP60 aluminium smelter produces first hot metal

Pilbara operations centre

Pilbara – autonomous haulage system

©2014, Rio Tinto, All Rights Reserved

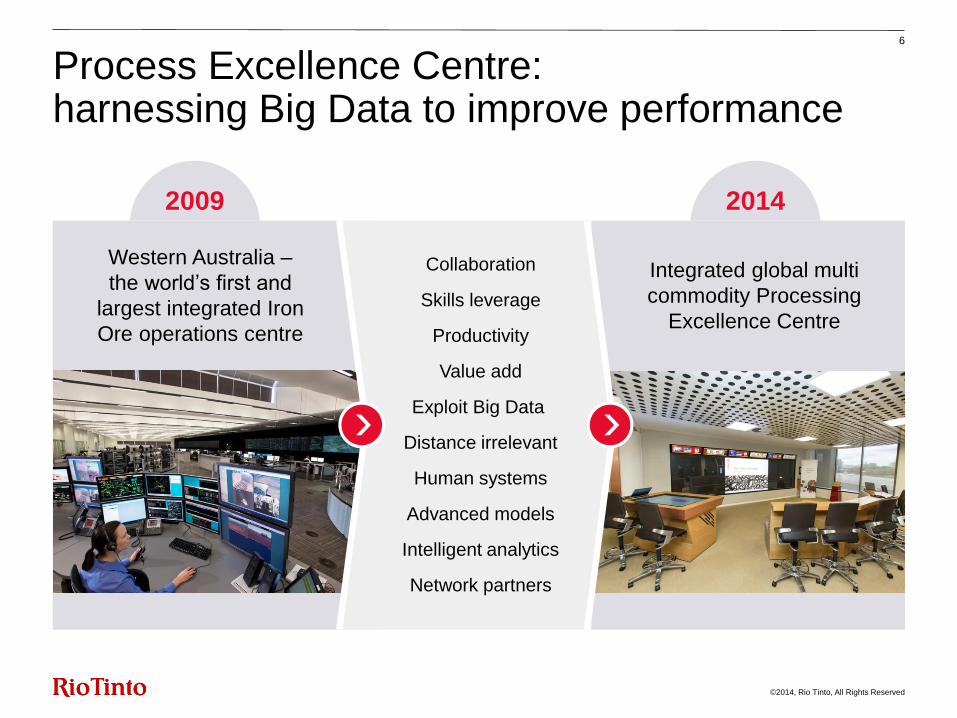

Process Excellence Centre: harnessing Big Data to improve performance

6

Integrated global multi

commodity Processing

Excellence Centre

2014

Western Australia –

the world’s first and

largest integrated Iron

Ore operations centre

2009

Collaboration

Skills leverage

Productivity

Value add

Exploit Big Data

Distance irrelevant

Human systems

Advanced models

Intelligent analytics

Network partners

©2014, Rio Tinto, All Rights Reserved

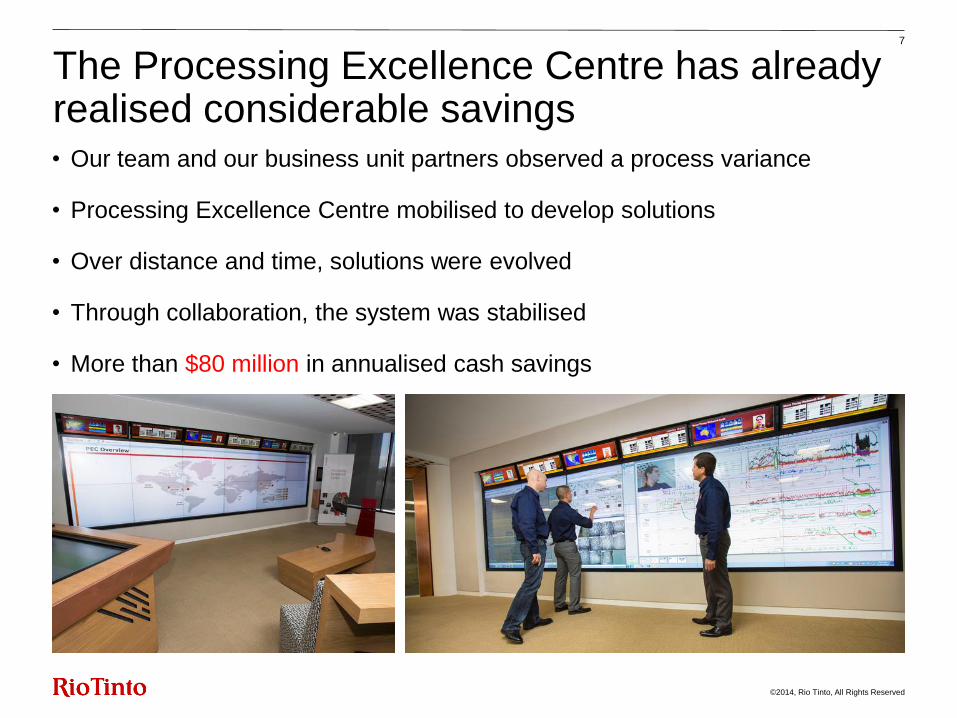

The Processing Excellence Centre has already realised considerable savings

7

• Our team and our business unit partners observed a process variance

• Processing Excellence Centre mobilised to develop solutions

• Over distance and time, solutions were evolved

• Through collaboration, the system was stabilised

• More than $80 million in annualised cash savings

©2014, Rio Tinto, All Rights Reserved

• Autonomous Haulage System

− Current truck fleet of 53, moving to 65 by end of 2014

− >180Mt of material autonomously moved since 2008

− Improved safety, truck cycle times, maintenance and control

− Expect 10-15% increase in effective utilisation in mature operation

• Pilbara AutoHaulR

− First heavy haul network in the world to be fully automated

− Continued trialing in 2014 and scheduled to be operational in 2015

− Safety, cycle time and capacity improvements

− Eliminating 3.6 million kilometres driven by vehicles each year associated with driver changeovers

8

Autonomous deployment continues to drive real business value

AutoHaulR

Autonomous trucks

©2014, Rio Tinto, All Rights Reserved

9

Pilbara growth: 290 Mt/a project at full capacity

Cape Lambert

• Construction completed 4 months ahead of schedule and $400m under budget

• Commissioning Cape Lambert B:

− First ore on ship four months ahead of schedule

− Delivered value in advance of full system re-rate

• 290Mt/a system run rate achieved two months ahead of schedule

• Low spend, high return productivity initiatives continue across fully integrated

mine, rail and port system

©2014, Rio Tinto, All Rights Reserved

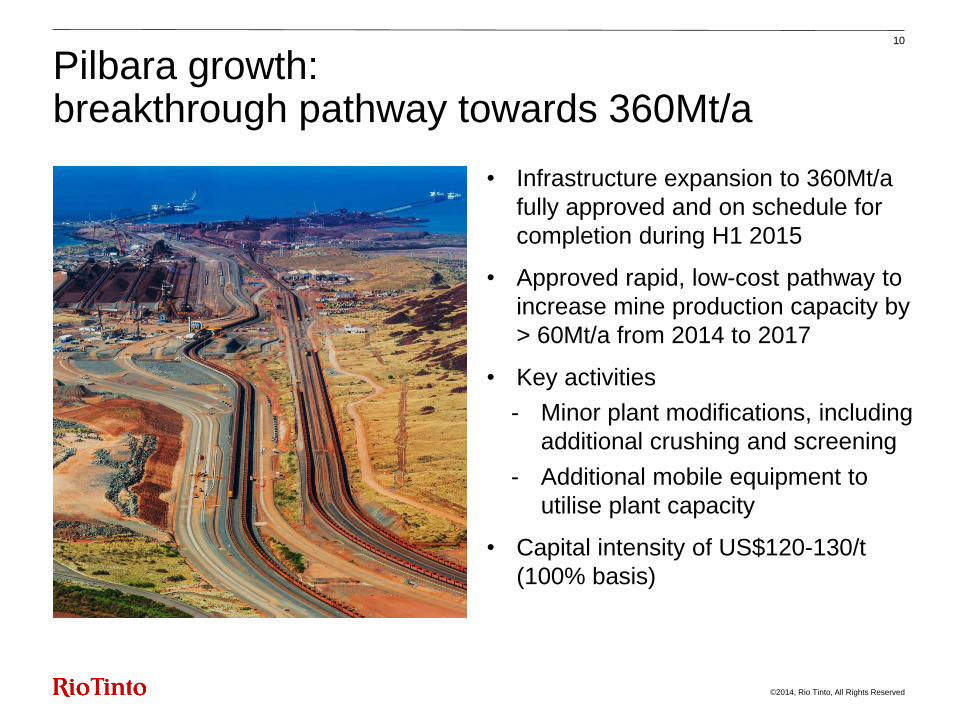

• Infrastructure expansion to 360Mt/a

fully approved and on schedule for

completion during H1 2015

• Approved rapid, low-cost pathway to

increase mine production capacity by

> 60Mt/a from 2014 to 2017

• Key activities

- Minor plant modifications, including

additional crushing and screening

- Additional mobile equipment to

utilise plant capacity

• Capital intensity of US$120-130/t

(100% basis)

10

Pilbara growth: breakthrough pathway towards 360Mt/a

©2014, Rio Tinto, All Rights Reserved

• 2013 full year cash unit cost in the

Pilbara was US$20.80/t, 11% lower

than 2012

• 2013 EBITDA margin 71%

• Geographic proximity to key

customers

• Unfettered access to ports and rail

• Pilbara Blend is the benchmark

product

Full year cash unit cost US$ per tonne

11

We are extending our lead as the Pilbara’s lowest cost producer

0

5

10

15

20

25

2006 2007 2008 2009 2010 2011 2012 2013

AUD cost USD cost

©2014, Rio Tinto, All Rights Reserved

High quality growth options across the portfolio 12

Copper: La Granja

Bauxite: South of the Embley

Copper: Oyu Tolgoi phase 2

Iron ore: Simandou

Iron ore: Pilbara optimisation

©2014, Rio Tinto, All Rights Reserved

13

Sequencing the best projects in line with our capital allocation priorities

Debt reduction

Compelling

growth

Further

cash

returns to

shareholders

1 Essential sustaining capex

2 Iterative cycle of:

3 Progressive dividends

©2014, Rio Tinto, All Rights Reserved

Copper equivalent production calculated at long-term consensus price forecasts

14

Delivering high quality growth with less capital expenditure

Rio Tinto copper equivalent production 2012 = 100

Expected capital expenditure profile* US$ billion

17.6

12.9

<11

~8

0

5

10

15

20

2012A 2013A 2014F 2015F

Sustaining Pilbarasustaining mines

Pilbara growth Other growth

* Forecast capex is subject to variation in future exchange rates

>20%

26%

>15%

0

20

40

60

80

100

120

140

2012A 2013A 2014F 2015F

Actual Forecast

CAGR

> 8%

©2014, Rio Tinto, All Rights Reserved

15

Delivering greater value for shareholders

Consistent execution of a clear strategy

Strong operational performance

Disciplined capital allocation

Transformation underpinned by innovation