deere & company investor relations · pdf fileíintegral part of business strategy,...

TRANSCRIPT

John DeereCommitted to Those Linked to the Land

Strategy Overview

Deere & CompanyNovember 2013

| Deere & Company | November 2013

Safe Harbor Statement & Disclosures

This presentation includes forward-looking comments subject to important risks and uncertainties. It may also contain financial measures that are not in conformance with accounting principles generally accepted in the United States of America (GAAP).

Refer to Deere’s reports filed on Forms 8-K (current), 10-Q (quarterly), and 10-K (annual) for information on factors that could cause actual results to differ materially from information in this presentation and for information reconciling financial measures to GAAP.

Guidance noted in the following slides was effective as of the company’s most recent earnings release and conference call (20 November 2013). Nothing in this presentation should be construed as reaffirming or disaffirming such guidance.

This presentation is not an offer to sell or a solicitation of offers to buy any of Deere’s securities.

2

|

Table of Contents

Slide #John Deere Strategy 4

Macroeconomic Tailwinds 18

Appendix 25

Deere & Company | November 20133

John Deere Strategy

|5 Deere & Company | November 2013

*

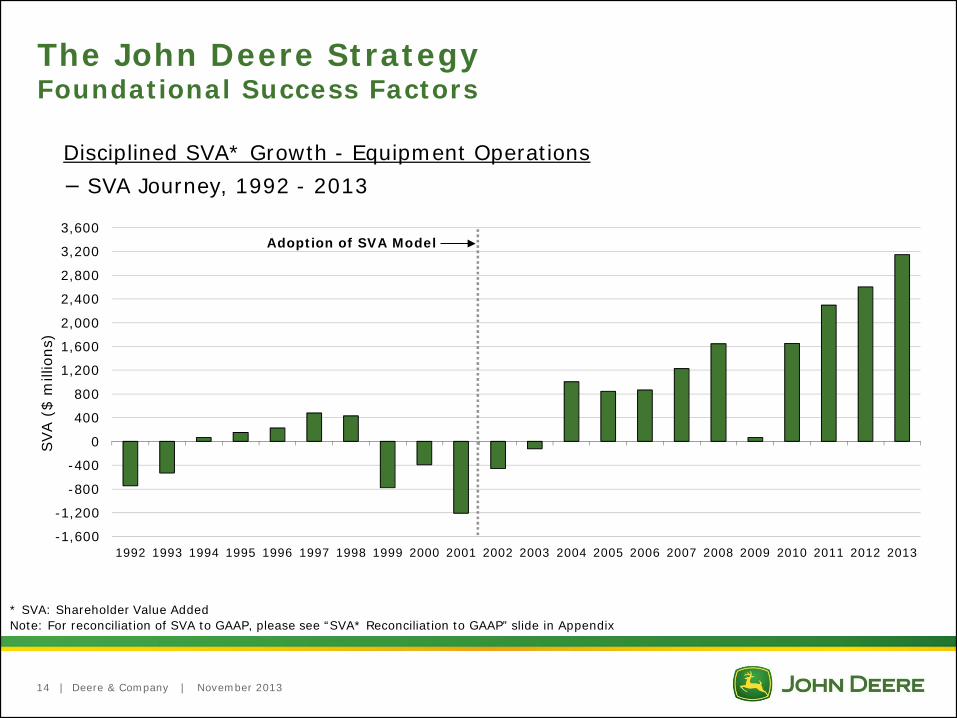

* SVA: Shareholder Value Added

*

| Deere & Company | November 2013

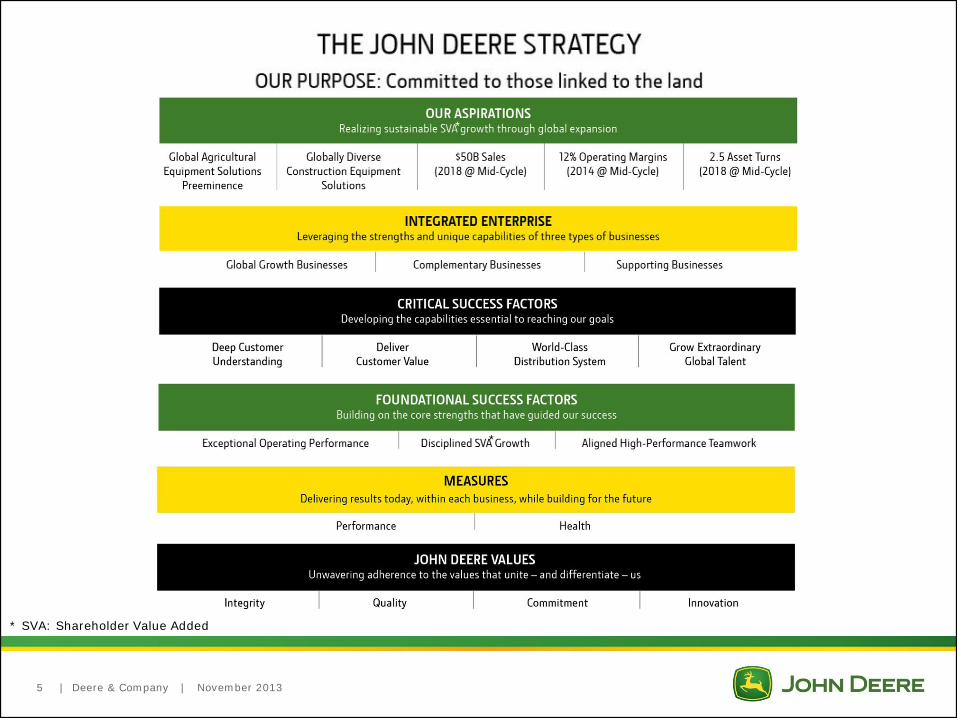

The John Deere StrategyOur Purpose: Committed to those linked to the land

6

Global macro-trends present significant opportunities for John Deere– Global population and income growth– Global infrastructure needs

New customer segments

Technology advances

744K Wheel Loader

460E Articulated Dump Truck

8360R Tractor

S690 Combine

X728 Riding Mower843K Wheeled Feller Buncher

|

Sustainable SVA* growth is delivered by distinctively serving our customers, employees, and investors

Extend and enhance our financial and operating achievements of recent years

Our challenge: to capture anticipated tailwinds by attracting more customers to the John Deere Experience across our six key geographies (US/Canada, EU 28, Brazil, CIS/Russia, China, India) in a manner that meets local needs while leveraging our global scale

7 Deere & Company | November 2013

The John Deere StrategyRealizing Sustainable Growth Through Global Expansion

* SVA: Shareholder Value Added

|

Agricultural Equipment Solutions Strategy– Defend and grow market share in

developed markets– Grow market share in developing

markets

Construction Equipment Solutions Strategy– Continue to grow strong #2

position in North America– Globalize the business

8 Deere & Company | November 2013

The John Deere StrategyAgricultural and Construction Equipment Aspirations

6488 Combine - China

755K Crawler Loader - USA

9530T Tractor - USA

435 Backhoe Loader - India

|

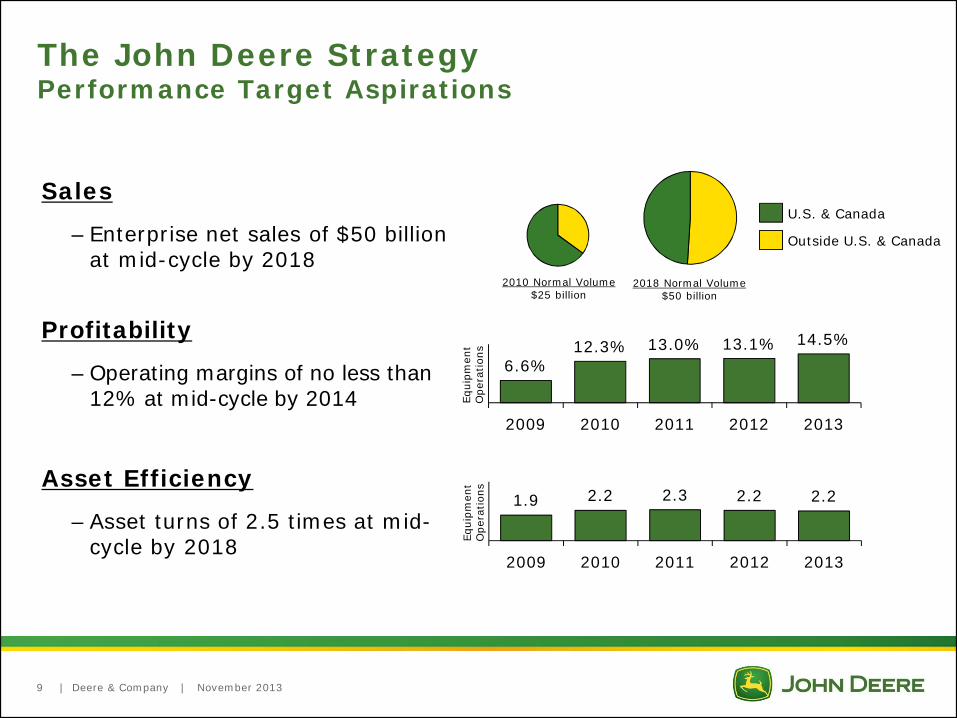

Sales

– Enterprise net sales of $50 billion at mid-cycle by 2018

Profitability

– Operating margins of no less than 12% at mid-cycle by 2014

Asset Efficiency

– Asset turns of 2.5 times at mid-cycle by 2018

2010 Normal Volume$25 billion

2018 Normal Volume$50 billion

U.S. & Canada

Outside U.S. & Canada

6.6%12.3% 13.0% 13.1% 14.5%

2009 2010 2011 2012 2013

1.9 2.2 2.3 2.2 2.2

2009 2010 2011 2012 2013

9 Deere & Company | November 2013

The John Deere StrategyPerformance Target Aspirations

Equi

pmen

tO

pera

tions

Equi

pmen

tO

pera

tions

|

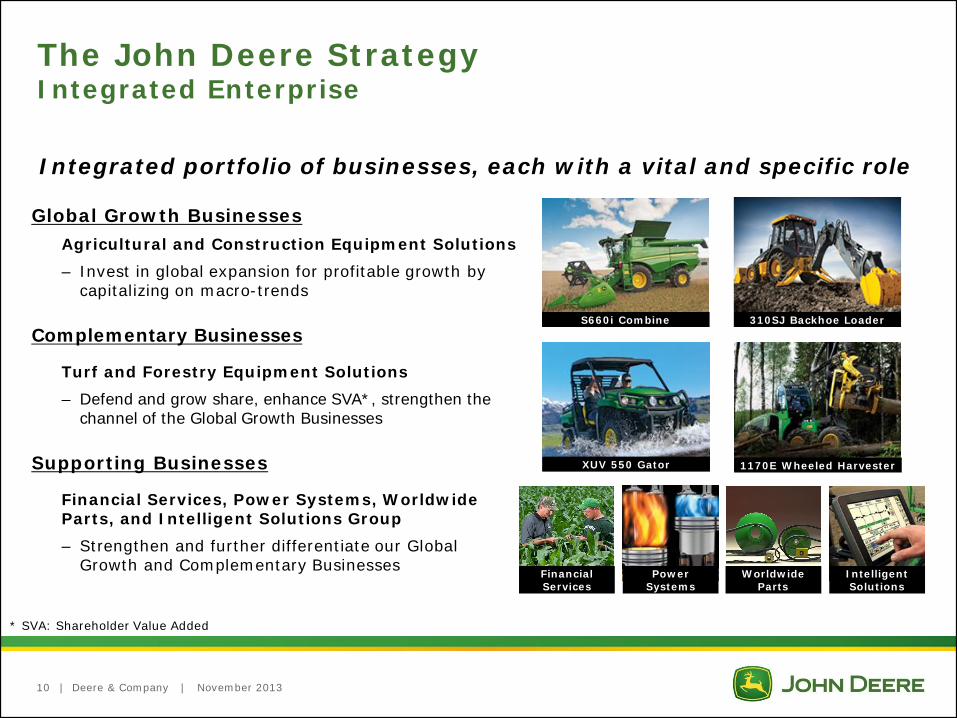

The John Deere StrategyIntegrated Enterprise

Integrated portfolio of businesses, each with a vital and specific role

10 Deere & Company | November 2013

Global Growth BusinessesAgricultural and Construction Equipment Solutions– Invest in global expansion for profitable growth by

capitalizing on macro-trends

Complementary Businesses

Turf and Forestry Equipment Solutions– Defend and grow share, enhance SVA*, strengthen the

channel of the Global Growth Businesses

Supporting Businesses

Financial Services, Power Systems, Worldwide Parts, and Intelligent Solutions Group– Strengthen and further differentiate our Global

Growth and Complementary Businesses

S660i Combine 310SJ Backhoe Loader

XUV 550 Gator 1170E Wheeled Harvester

Financial Services

Power Systems

Worldwide Parts

Intelligent Solutions

* SVA: Shareholder Value Added

|

The John Deere StrategyCritical Success Factors

11 Deere & Company | November 2013

Developing the capabilities essential to reaching our goalsDeep Customer Understanding (DCU) - Understanding our customers’ most important

local needs, and translating these into winning products and services better than any competitor

Deliver Customer Value (DCV) - Profitably translating our customers’ needs into products and services at prices our customers are willing to pay

World-Class Distribution System - Enabling our customers around the world to participate in the unique John Deere Experience by developing world-class channels of dealers that are professional, profitable and sustainable businesses, oriented to the customer, aligned with John Deere and achieving market preeminence

Grow Extraordinary Global Talent - Enabling pre-eminent customer value and business results through extraordinary leaders and engaged employees delivering aligned high-performance teamwork globally

| Deere & Company | November 2013

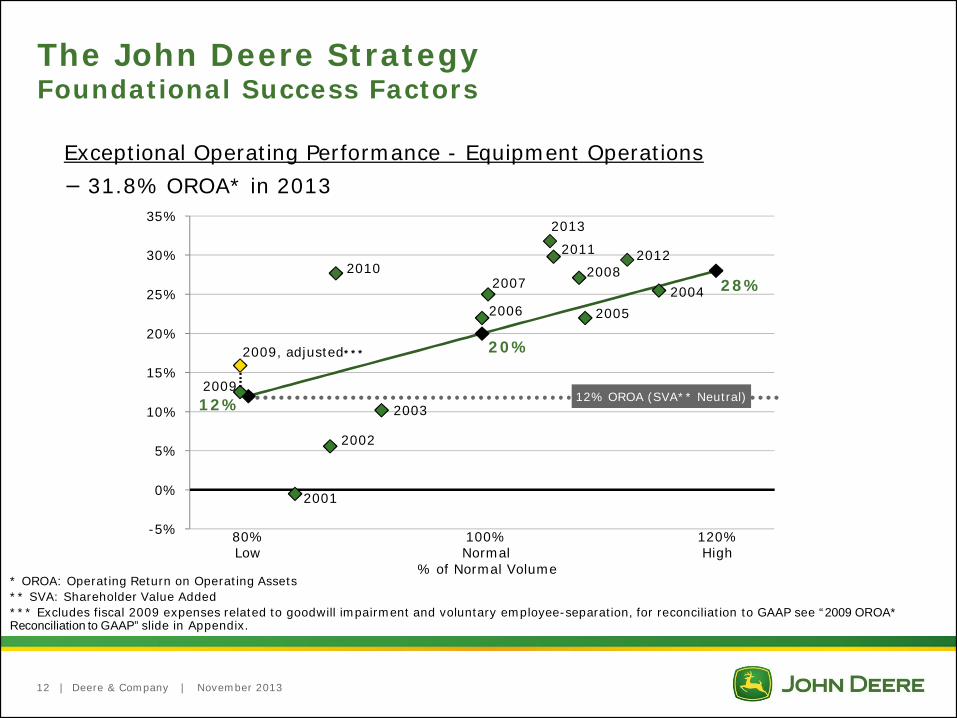

* OROA: Operating Return on Operating Assets** SVA: Shareholder Value Added*** Excludes fiscal 2009 expenses related to goodwill impairment and voluntary employee-separation, for reconciliation to GAAP see “2009 OROA* Reconciliation to GAAP” slide in Appendix.

The John Deere StrategyFoundational Success Factors

Exceptional Operating Performance - Equipment Operations31.8% OROA* in 2013

12%

20%

28%

2001

2002

2003

200420052006

20072008

2009

2009, adjusted***

20102011 2012

2013

-5%

0%

5%

10%

15%

20%

25%

30%

35%

% of Normal Volume

80%Low

100%Normal

120%High

12% OROA (SVA** Neutral)

12

| Deere & Company | November 2013

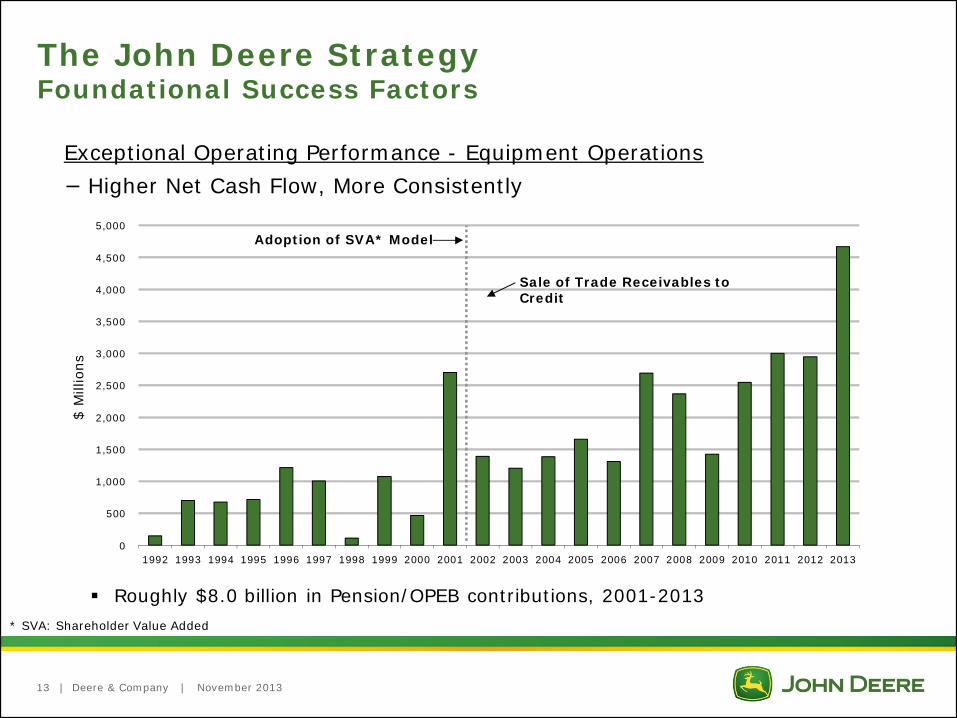

Exceptional Operating Performance - Equipment OperationsHigher Net Cash Flow, More Consistently

The John Deere StrategyFoundational Success Factors

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ M

illio

ns

Sale of Trade Receivables to Credit

Adoption of SVA* Model

Roughly $8.0 billion in Pension/OPEB contributions, 2001-2013

13

* SVA: Shareholder Value Added

|

-1,600

-1,200

-800

-400

0

400

800

1,200

1,600

2,000

2,400

2,800

3,200

3,600

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Deere & Company | November 2013

SVA

($ m

illio

ns)

* SVA: Shareholder Value AddedNote: For reconciliation of SVA to GAAP, please see “SVA* Reconciliation to GAAP” slide in Appendix

Disciplined SVA* Growth - Equipment OperationsSVA Journey, 1992 - 2013

14

The John Deere StrategyFoundational Success Factors

Adoption of SVA Model

| Deere & Company | November 2013

Aligned High-Performance TeamworkIntegral part of business strategy, reinforced with compensationGlobal Performance Management reinforces alignment Base pay changes linked to achieving goals

STI: Short-Term Incentive – Bonus focuses on OROA*/ROE**Covers most worldwide salaried employeesApplies one enterprise-wide bonus metric

MTI: Mid-Term Incentive – Bonus driven by sustained SVA*** creationAbout 10,400 management employees eligible

LTI: Long-Term Incentive – Primarily stock options Top 1,000 employees eligibleMinimum stock holding requirements for senior management (~ top 125)

15

The John Deere StrategyFoundational Success Factors

•* OROA: Operating Return on Operating Assets•** ROE: Return on Equity•*** SVA: Shareholder Value Added

| Deere & Company | November 2013

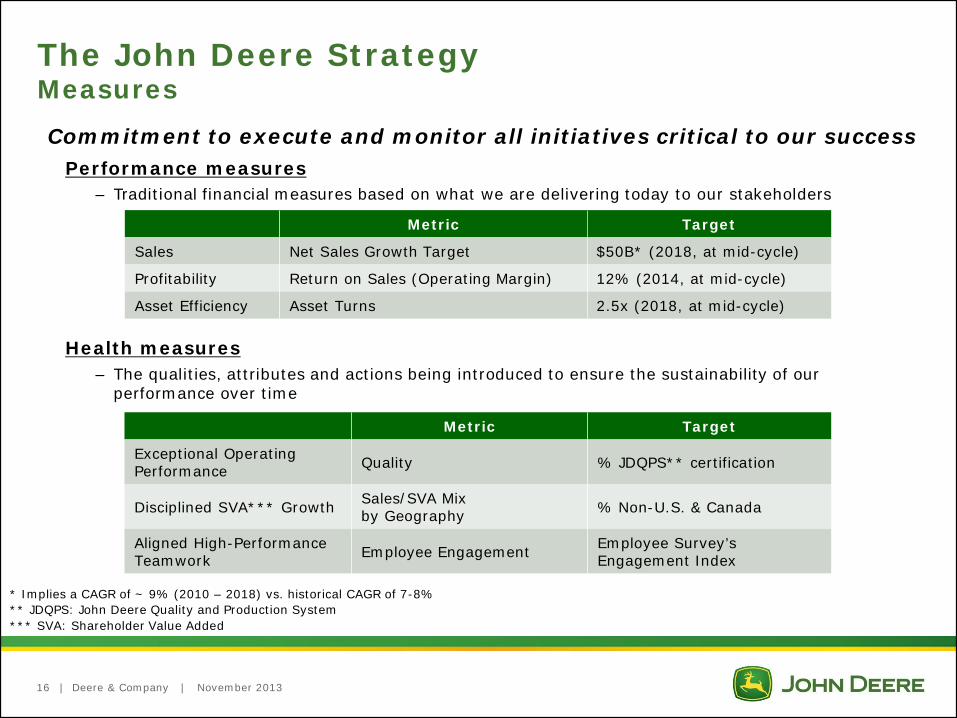

The John Deere StrategyMeasures

16

Commitment to execute and monitor all initiatives critical to our successPerformance measures

– Traditional financial measures based on what we are delivering today to our stakeholders

Health measures – The qualities, attributes and actions being introduced to ensure the sustainability of our

performance over time

Metric Target

Sales Net Sales Growth Target $50B* (2018, at mid-cycle)

Profitability Return on Sales (Operating Margin) 12% (2014, at mid-cycle)

Asset Efficiency Asset Turns 2.5x (2018, at mid-cycle)

Metric Target

Exceptional Operating Performance Quality % JDQPS** certification

Disciplined SVA*** Growth Sales/SVA Mix by Geography % Non-U.S. & Canada

Aligned High-Performance Teamwork Employee Engagement Employee Survey’s

Engagement Index

* Implies a CAGR of ~ 9% (2010 – 2018) vs. historical CAGR of 7-8%** JDQPS: John Deere Quality and Production System*** SVA: Shareholder Value Added

| Deere & Company | November 2013

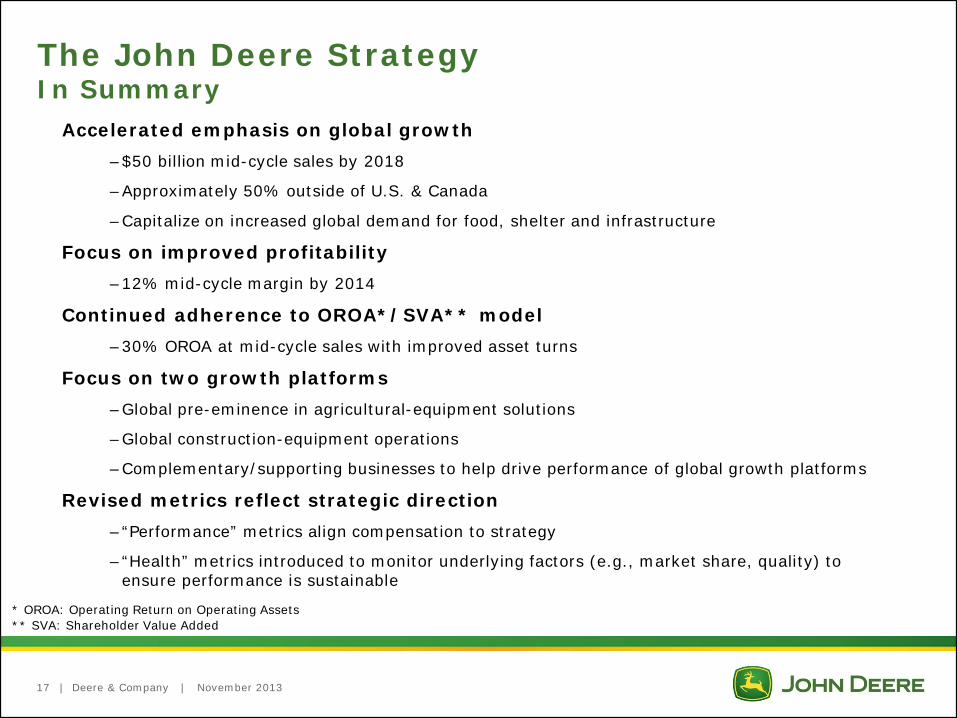

Accelerated emphasis on global growth –$50 billion mid-cycle sales by 2018

–Approximately 50% outside of U.S. & Canada

–Capitalize on increased global demand for food, shelter and infrastructure

Focus on improved profitability–12% mid-cycle margin by 2014

Continued adherence to OROA*/SVA** model–30% OROA at mid-cycle sales with improved asset turns

Focus on two growth platforms–Global pre-eminence in agricultural-equipment solutions

–Global construction-equipment operations

–Complementary/supporting businesses to help drive performance of global growth platforms

Revised metrics reflect strategic direction–“Performance” metrics align compensation to strategy

–“Health” metrics introduced to monitor underlying factors (e.g., market share, quality) to ensure performance is sustainable

17

The John Deere StrategyIn Summary

•* OROA: Operating Return on Operating Assets•** SVA: Shareholder Value Added

Macroeconomic Tailwinds

Support John Deere’sGlobal Growth Businesses

|19 Deere & Company | November 2013

Long-Term Macroeconomic TailwindsSupport Global Growth Opportunities

Population growing in size and affluence• By 2050, world population will exceed 9 billion, up from ~7 billion today,

with most growth in Asia and Africa• Large middle class emerging in Latin America, China, India, and other

developing economies

Opportunity #1: Feeding the world• Agricultural output must double by 2050• To achieve this, the rate of productivity growth must accelerate over recent

trend rates• Natural resources under strain, especially water and land

Opportunity #2: Massive urbanization• Migration from rural areas creates need for infrastructure development• More than 50% of the global population today lives in urban areas, will

surpass 70% by 2050

| Deere & Company | November 2013

Absolute increase in real value added 2012-20, $ BillionsSector

204

Real Estate & Dwellings

238

Wholesale Trade

266

Other Business Activities

276

Public Admin, Sanitary & Personal Srvs

303

Construction

305

Transportation & Storage

308

Financial Institutions

346

Medical, Dental, Veterinary, Other Health

416

Communications465

203

524

Agriculture, Hunting, Forestry, Fishing

610

Processed Food

636

Energy Mining and Quarrying

698

Restaurants and Hotels

789

Electricity, Gas, and Water

796

Computer and Related Activities

915

Motor Vehicle and Motorcycle Sales, Repair, Maint.

985

Insurance

1,042

Retail Trade except Motor Vehicle, and MotorcycleEducational Services

Radio, TV, and Communications Equipment

CAGR 2012-20 Percent

2.74.03.21.93.94.13.72.64.42.82.56.42.83.73.02.83.23.52.93.0

20.5

Retail Trade except Motor Vehicle, and Motorcycle

22.1Medical, Dental, Veterinary, Other Health

26.9Real Estate & Dwellings 29.7

Computer and Related Activities

33.7

Insurance

36.3

Communications

38.8

Restaurants and Hotels41.4Financial Institutions41.8

Educational Services

43.3

12.9

44.9

Radio, TV, and Communications Equipment

46.9

Transportation & Storage

52.1

Energy Mining and Quarrying56.8Electricity, Gas, and Water59.4

Construction

60.2

Public Admin, Sanitary & Personal Srvs

60.8

Wholesale Trade

67.3Processed Food79.5

Other Business Activities

Agriculture, Hunting, Forestry, Fishing

Motor Vehicle and Motorcycle Sales, Repair, Maint.

Share of growth from BRIIC1

PercentSector

While several sectors are expected to grow in the G-20 countries from 2012-2020 . . .

. . Agriculture and Construction will derive significant growth from the BRIIC countries

Strong Global Tailwinds in Ag & Construction Significant Growth from Developing Economies

Note: G20 countries account for 77% and 89% of agriculture and construction segments respectively.Total global growth for agriculture is $405B and construction is $890B

20

1Brazil, Russia, India, Indonesia, ChinaSource: Global Insight World Industry Service

Real value-added 2005 USD

|

Developing Economies Growing Faster

While developed economies have always accounted for a larger share of GDP . . .

10.023.9

37.0

1.3

14.0

29.5

1990

5.6

11.3

1970

51.04.0

2008

Real GDP1

$ Trillions

6.5

CAGR,1970-2008Percent

3.5

37.0 44.769.5

14.0

2.9

204320202008

70.3

138.4

68.9

25.651.0

Real GDP1

$ Trillions

4.7

CAGR,2008-2043Percent

... their growth will slow significantly, relative to that of developing economies

1 Real GDP (expenditure method) base year 2005Developed countries include OECD. Developing countries include all developing markets (Regions as defined by Global Insight)

1.8x2.6x

1.8

Developing Developed

Deere & Company | November 2013

Source: Global Insight World Market Monitor

21

| Deere & Company | November 2013

Dynamics of Food Demand

Source: World Development Indicators 2010, The World Bank, April 2013

>$10.00per day

25% of world’s population(Most hunger problems solved at

$2.50 threshold)

Services

Processed Products

Livestock Products

Commodities

Per CapitaIncome

18% of world’s population(2/3rds experience hunger &

malnutrition)

$2.50-$10.00 per day

$1.25-$2.50 per day

<$1.25 per day

22

| Deere & Company | November 2013

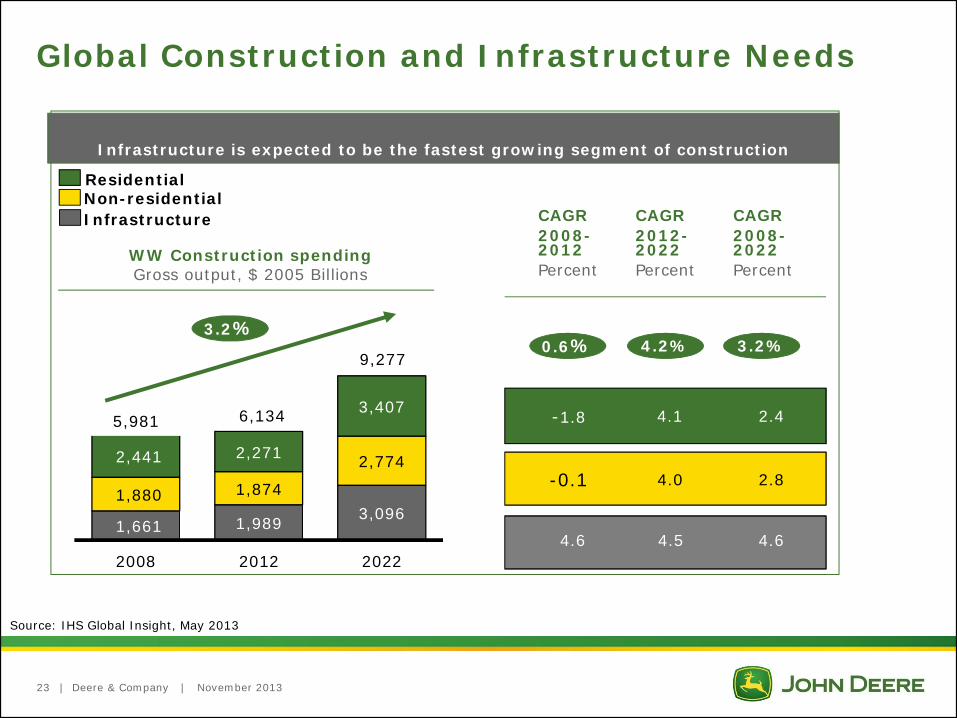

Global Construction and Infrastructure Needs

1,661 1,989 3,0961,880 1,874

2,7742,441 2,271

3,407

2008 2012 2022

3.2%

Infrastructure is expected to be the fastest growing segment of construction

ResidentialNon-residentialInfrastructure

WW Construction spendingGross output, $ 2005 Billions

Source: IHS Global Insight, May 2013

23

-1.8 4.1

-0.1 4.0

4.6 4.5

CAGR2008-2012Percent

CAGR2012-2022Percent

CAGR2008-2022Percent

2.8

5,981

4.6

2.46,134

9,2770.6% 4.2% 3.2%

|

Infrastructure

Non-residential

Residential

Construction spending 2022 absolute, Top 10 (Billions of 2005 $s)

China + U.S. & Canada 39% of 2022 absolute, compared to 33% todayChina + U.S. & Canada + Brazil, Russia, India 50% of 2022 absolute, compared to 42% today

Construction spending 2012-2022 change, Top 10 (Billions of 2005 $s)

Infrastructure

Non-residential

Residential

Global Construction Spending in 2022Concentrated in a Small Number of Markets

Deere & Company | November 2013

Source: IHS Global Insight, Deere Analysis, March 2013

24

China

U.S.

Japan

India

UK

Germany

France

Australia

Italy

Canada

1,014

702

676

444

322

315

211

209

199

China

U.S.

Japan

India

UK

Germany

France

Australia

Italy

Canada

1,232

286

122

377

122

32

41

65

30

19

2,374

Appendix

| Deere & Company | November 2013

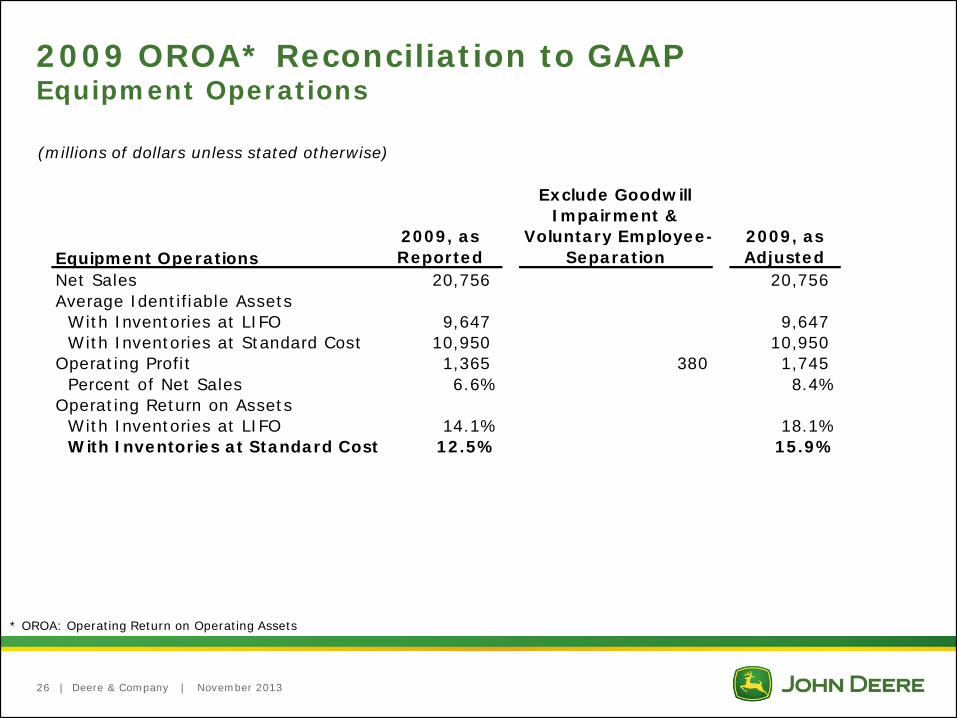

2009 OROA* Reconciliation to GAAPEquipment Operations

Equipment Operations2009, as Reported

Exclude Goodwill Impairment &

Voluntary Employee-Separation

2009, as Adjusted

Net Sales 20,756 20,756 Average Identifiable Assets

With Inventories at LIFO 9,647 9,647 With Inventories at Standard Cost 10,950 10,950

Operating Profit 1,365 380 1,745 Percent of Net Sales 6.6% 8.4%

Operating Return on AssetsWith Inventories at LIFO 14.1% 18.1%With Inventories at Standard Cost 12.5% 15.9%

(millions of dollars unless stated otherwise)

26

* OROA: Operating Return on Operating Assets

| Deere & Company | November 2013

SVA* Reconciliation to GAAPEquipment Operations

Equipment Operations 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002Net Sales 5,723 6,479 7,663 8,830 9,640 11,082 11,926 9,701 11,169 11,077 11,703 Average Identifiable Assets

With Inventories at LIFO 5,765 5,449 5,551 6,187 6,502 6,682 7,672 7,724 8,069 8,743 6,229 With Inventories at Standard Cost 6,846 6,442 6,494 7,131 7,488 7,703 8,711 8,739 9,039 9,678 7,147

Operating Profit 77 242 847 1,006 1,125 1,402 1,476 272 693 (46) 401 Percent of Net Sales 1.3% 3.7% 11.1% 11.4% 11.7% 12.6% 12.4% 2.8% 6.2% -0.4% 3.4%

Operating Return on AssetsWith Inventories at LIFO 1.3% 4.4% 15.3% 16.3% 17.3% 21.0% 19.3% 3.5% 8.6% -0.5% 6.4%With Inventories at Standard Cost 1.1% 3.8% 13.0% 14.1% 15.0% 18.2% 16.9% 3.1% 7.7% -0.5% 5.6%

SVA Cost of Assets (821) (773) (780) (856) (898) (924) (1,045) (1,049) (1,085) (1,162) (858) SVA (744) (531) 67 150 227 477 431 (776) (392) (1,208) (457)

Equipment Operations 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013Net Sales 13,349 17,673 19,401 19,884 21,489 25,803 20,756 23,573 29,466 33,501 34,998 Average Identifiable Assets

With Inventories at LIFO 5,965 6,482 7,248 7,546 8,092 9,652 9,647 9,196 11,516 13,594 14,569 With Inventories at Standard Cost 6,925 7,477 8,312 8,634 9,205 10,812 10,950 10,494 12,875 14,965 15,924

Operating Profit 708 1,905 1,842 1,905 2,318 2,927 1,365 2,909 3,839 4,397 5,058 Percent of Net Sales 5.3% 10.8% 9.5% 9.6% 10.8% 11.3% 6.6% 12.3% 13.0% 13.1% 14.5%

Operating Return on AssetsWith Inventories at LIFO 11.9% 29.4% 25.4% 25.2% 28.6% 30.3% 14.1% 31.6% 33.3% 32.3% 34.7%With Inventories at Standard Cost 10.2% 25.5% 22.2% 22.1% 25.2% 27.1% 12.5% 27.7% 29.8% 29.4% 31.8%

SVA Cost of Assets (831) (897) (998) (1,036) (1,094) (1,284) (1,301) (1,259) (1,545) (1,795) (1,911) SVA (123) 1,008 844 869 1,224 1,643 64 1,650 2,294 2,602 3,147

(millions of dollars unless stated otherwise)

27

* SVA: Shareholder Value Added

|