deere & company investor relations - john deere us ... · this presentation includes...

TRANSCRIPT

John Deere Committed to Those Linked to the Land

Deere & Company December 2012 / January 2013

| Deere & Company | December 2012 / January 2013

Safe Harbor Statement & Disclosures

This presentation includes forward-looking comments subject to important risks and uncertainties. It may also contain financial measures that are not in conformance with accounting principles generally accepted in the United States of America (GAAP).

Refer to Deere’s reports filed on Forms 8-K (current), 10-Q (quarterly), and 10-K (annual) for information on factors that could cause actual results to differ materially from information in this presentation and for information reconciling financial measures to GAAP.

Guidance noted in the following slides was effective as of the company’s most recent earnings release and conference call (21 November 2012). Nothing in this presentation should be construed as reaffirming or disaffirming such guidance.

This presentation is not an offer to sell or a solicitation of offers to buy any of Deere’s securities.

2

|

Table of Contents

Slide #

John Deere Strategy 4

2012 in Review 6

Looking Ahead 11

Supplemental Information:

Foundational Success Factors 20

Global Markets and Opportunities 30

John Deere Financial Services 48

Farm Fundamentals 51

Appendix 55

Deere & Company | December 2012 / January 2013 3

John Deere Strategy

| 5 Deere & Company | December 2012 / January 2013

2012 in Review

|

2012 in Review Equipment Operations

Deere & Company | December 2012 / January 2013 7

Exceptional Results

• Record net sales… $33.501 billion

• Record net income… $3.065 billion

• 13.1% operating profit margin

• Cash flow from operations… $2.9 billion

• SVA… $2.602 billion

• OROA… 29.4%

Attributable to Deere & Company

|

Net Sales by Major Market Equipment Operations

Deere & Company | December 2012 / January 2013 8

$13.8 $15.1

$13.0 $14.8

$17.4

$20.8

20

07

20

08

20

09

20

10

20

11

20

12

U.S. & Canada 9% CAGR

$3.9 $4.6

$3.4 $3.4 $4.4 $4.3

20

07

20

08

20

09

20

10

20

11

20

12

Western Europe 2% CAGR

$1.0

$1.9

$0.7 $0.7 $1.4 $1.7

20

07

20

08

20

09

20

10

20

11

20

12

Central Europe & CIS 11% CAGR

$1.6 $2.6

$1.8 $2.6

$3.6 $3.6

20

07

20

08

20

09

20

10

20

11

20

12

Central & South America 18% CAGR

$0.8 $1.1 $1.2 $1.4 $1.9 $2.1

20

07

20

08

20

09

20

10

20

11

20

12

Asia, Africa & Middle East 21% CAGR

$0.4 $0.6 $0.6 $0.6 $0.8 $1.0

20

07

20

08

20

09

20

10

20

11

20

12

Australia & New Zealand 20% CAGR

|

2012 in Review

Deere & Company | December 2012 / January 2013 9

Investments in the Business

• Capex and R&D for equipment operations… ~ $2.750 billion

• Announced three capacity increases in the United States

• Established financial services operations in Russia, India, Chile, and Thailand

Capital Returned to Shareholders

• Operating cash flow returned to shareholders… ~ 75% • Quarterly dividend… increased to $0.46 per share (+12%) • Shares repurchased… 20.2 million shares

| Deere & Company | December 2012 / January 2013

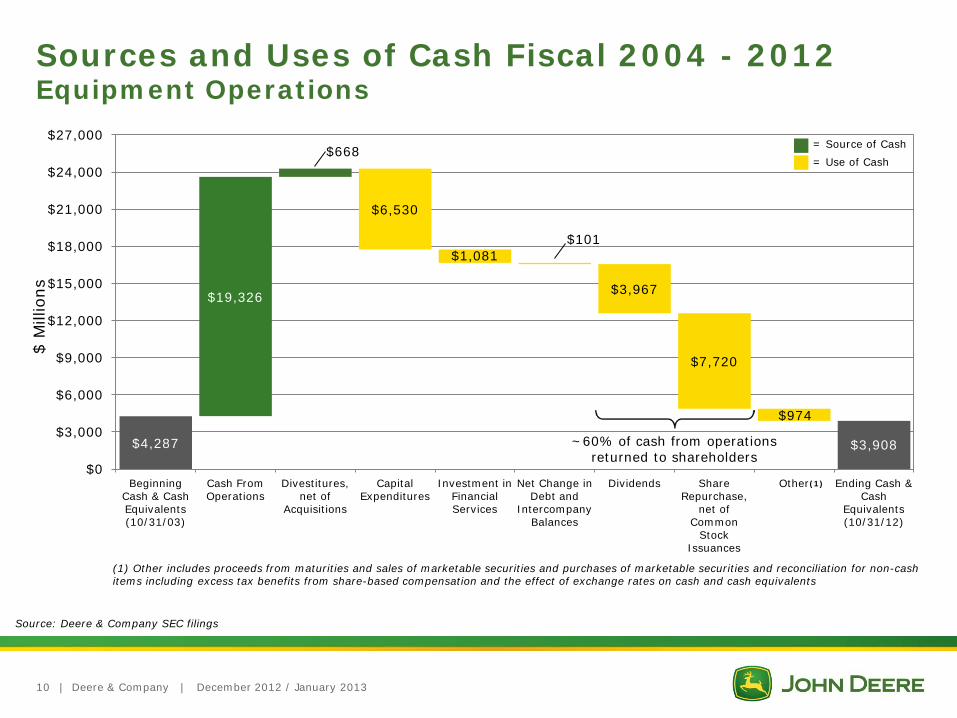

Sources and Uses of Cash Fiscal 2004 - 2012 Equipment Operations

Source: Deere & Company SEC filings

10

(1) Other includes proceeds from maturities and sales of marketable securities and purchases of marketable securities and reconciliation for non-cash items including excess tax benefits from share-based compensation and the effect of exchange rates on cash and cash equivalents

$4,287

$19,326

$668

$6,530

$1,081 $101

$3,967

$7,720

$974

$0

$3,000

$6,000

$9,000

$12,000

$15,000

$18,000

$21,000

$24,000

$27,000

Beginning Cash & Cash Equivalents (10/31/03)

Cash From Operations

Divestitures, net of

Acquisitions

Capital Expenditures

Investment in Financial Services

Net Change in Debt and

Intercompany Balances

Dividends Share Repurchase,

net of Common

Stock Issuances

Other Ending Cash & Cash

Equivalents (10/31/12)

(1)

$ M

illio

ns

$3,908 ~60% of cash from operations returned to shareholders

= Source of Cash

= Use of Cash

Looking Ahead

|

Fiscal Year 2013 Outlook Equipment Operations

Deere & Company | December 2012 / January 2013 12

Strong Company Outlook

• Net sales… up ~ 5% vs. FY 2012

• Net income… ~ $3.2 billion

• Strong operating profit margins

• Cash flow from operations… ~ $3.4 billion

Deere & Company Forecast as of 21 November 2012

Attributable to Deere & Company

|

Absorbing Our Investments to Grow the Business

• Capital expenditures • 2012… ~ $1.3 billion • 2013 forecast… ~ $1.3 billion

• SA&G expense • 2012… ~ $3.0 billion • 2013 forecast… up ~ 7%

• R&D expense • 2012… ~ $1.4 billion • 2013 forecast… up ~ 3%

Global Growth Equipment Operations

Deere & Company | December 2012 / January 2013 13

Deere & Company Forecast as of 21 November 2012

|

Global Growth Major Equipment Factory Investments

Deere & Company | December 2012 / January 2013 14

New Factories Major Expansions or Modernizations

Indaiatuba, Brazil C&F Division

• Backhoe Loaders • 4WD Loaders

Indaiatuba, Brazil (JV) C&F Division

• Excavators

Orenburg, Russia A&T Division

• Seeding Equipment • Tillage Equipment • Spraying Equipment

Dewas, India A&T Division

• Tractors

Harbin, China A&T Division

• Combine Front-End Equipment • Tractors • Planters • Sprayers • Irrigation Products

Tianjin (TEDA), China C&F Division

• 4WD Loaders • Excavators

Tianjin (TEDA), China John Deere Power Systems

• Engines

Des Moines, IA, USA A&T Division

• Spraying Equipment • Cotton Harvesting Equipment • Tillage Equipment • Seeding Equipment

Domodedovo, Russia A&T and C&F Division

• Tractors • Combine Harvesters • Combine Front-End Equipment • Backhoes, Loaders, Graders • Skidders

Pune, India A&T Division

• Engines • Transmissions • Tractors

Rosario, Argentina A&T Divison and

John Deere Power Systems • Engines • Tractors • Combines

Waterloo, IA, USA A&T Division

• Foundry

Waterloo, IA, USA A&T Division

• Ag Tractors

Davenport, IA, USA C&F Division

• Articulated Dump Trucks • 4WD Loaders • Motor Graders • Skidders • Wheeled Feller Bunchers

Moline, IL, USA Cylinder Division

• Hydraulic Cylinders

Valley City, ND, USA A&T Division

• Seeding Equipment • Tillage Equipment

Moline, IL, USA A&T Division

• Planting Equipment

|

Global Growth Investments in New Products

Deere & Company | December 2012 / January 2013 15

Deere & Company Forecast as of 21 November 2012

John Deere’s first small track combine

R40 STC Combine

Lower-priced platform for overseas markets

WL56 Loader First entirely Deere-designed articulated dump truck

E-Series ADT

Can harvest 350+ acres per day; available in 45 countries

S-Series Combine

Local production in Brazil; qualifies for FINAME financing

4730 Sprayer

Industry-first hybrid electric wheel loader

644K Hybrid Loader

High HP utility solution for livestock and arable segments

6210R Tractor

|

Global Growth Financial Services and Intelligent Solutions

Deere & Company | December 2012 / January 2013 16

Supporting our Global Growth

• Financial Services… expanding into growth regions • Russia, China, India, Chile, and Thailand • EU-27… expanding coverage to majority of countries

• Intelligent Solutions… John Deere FarmSightTM

• JDLink Telematics Connection • All large Ag machines

• Remote Customer Support • Remote Display Access • Service Advisor Remote

• Machine Sync • John Deere Field Connect • John Deere Mobile Farm Manager

Deere & Company Forecast as of 21 November 2012

|

Engine Emissions Interim Tier 4

Deere & Company | December 2012 / January 2013 17

Successful Transition

• Integrated vehicle solution

• Meeting customer performance and reliability requirements

• Nearly 60 applications launched*

• More than 40,000 engines in the field with >15 million customer hours*

• Warranty claims on 9.0L engine 33% lower compared to Tier 3

• Fuel economy 1-5% better than competitive equipment on tractors with 9.0L engine**

• * As of 31 October 2012 •** Per Nebraska Tractor Test Laboratory results

|

Engine Emissions Final Tier 4

Deere & Company | December 2012 / January 2013 18

• Challenge to absorb costs of continuing new emissions technologies

• SCR introduces packaging and other new challenges • DEF freezing can be a concern in colder

climates

• Shorter implementation horizon than iT4

• More applications to transition to FT4 than past programs

• Maintain Tier 2 and Tier 3 solutions for global markets

iT4 success gives confidence in our ability to meet FT4 challenges

|

Feet on the Ground, Eyes on the Horizon

Deere & Company | December 2012 / January 2013 19

Feet on the Ground • Cautiously optimistic in the near-term

• Fiscal Cliff and Euro Zone could prove to be major disruptors to our 2013 plan

• Prepared to pull levers if needed

Eyes on the Horizon • Global economy supports our confidence in long-term macroeconomic trends

• By 2050 • World population will reach ~ 9 billion • Agricultural output must double • Migration from rural areas creates boom for infrastructure

• Making the global investments to meet these challenges

Performance the past three years supports confidence in the John Deere Strategy and our 2018 Ambitions

Supplemental Information Foundational Success Factors

| Deere & Company | December 2012 / January 2013

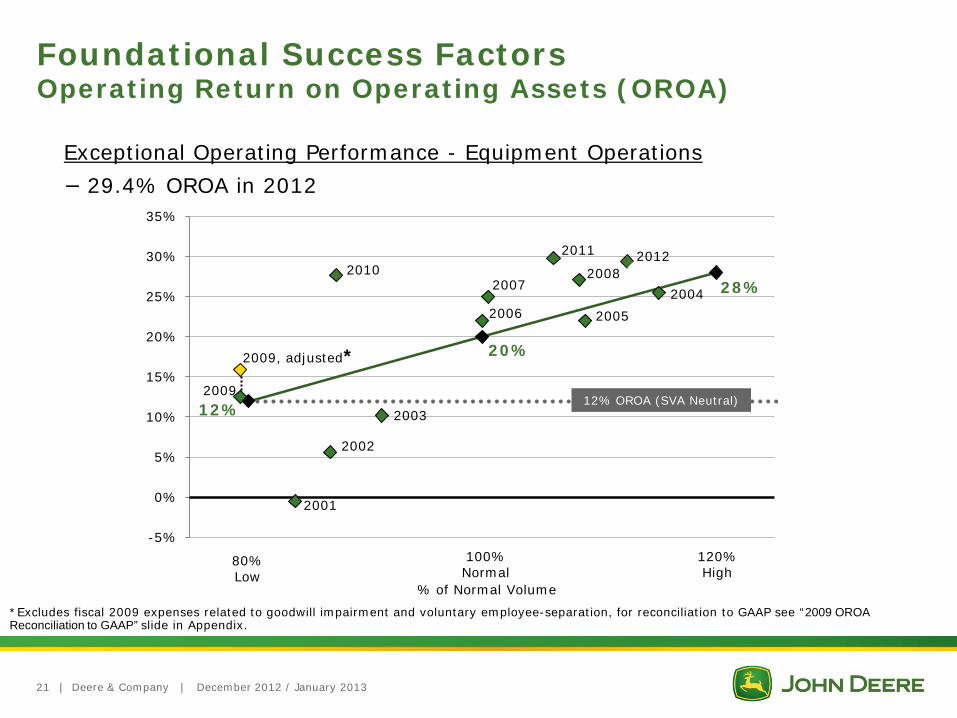

*Excludes fiscal 2009 expenses related to goodwill impairment and voluntary employee-separation, for reconciliation to GAAP see “2009 OROA Reconciliation to GAAP” slide in Appendix.

Foundational Success Factors Operating Return on Operating Assets (OROA)

21

Exceptional Operating Performance - Equipment Operations

− 29.4% OROA in 2012

12%

20%

28%

2001

2002

2003

2004

2005 2006

2007 2008

2009

2009, adjusted*

2010 2011 2012

-5%

0%

5%

10%

15%

20%

25%

30%

35%

% of Normal Volume

80% Low

100% Normal

120% High

12% OROA (SVA Neutral)

| Deere & Company | December 2012 / January 2013

Foundational Success Factors Cash Flow From Operations

22

Exceptional Operating Performance - Equipment Operations

− Higher Net Cash Flow, More Consistently

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

$ M

illio

ns

Sale of Trade Receivables to Credit

Adoption of SVA Model

Over $7.5 billion in Pension/OPEB contributions, 2001-2012

| Deere & Company | December 2012 / January 2013

Note: For reconciliation of SVA to GAAP, please see “Equipment Ops SVA Reconciliation to GAAP” slide in Appendix

23

Foundational Success Factors Shareholder Value Added (SVA)

Disciplined SVA Growth - Equipment Operations

− SVA Journey, 1991 - 2012

-1,600

-1,200

-800

-400

0

400

800

1,200

1,600

2,000

2,400

2,800

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

SVA (

$ m

illio

ns)

| Deere & Company | December 2012 / January 2013

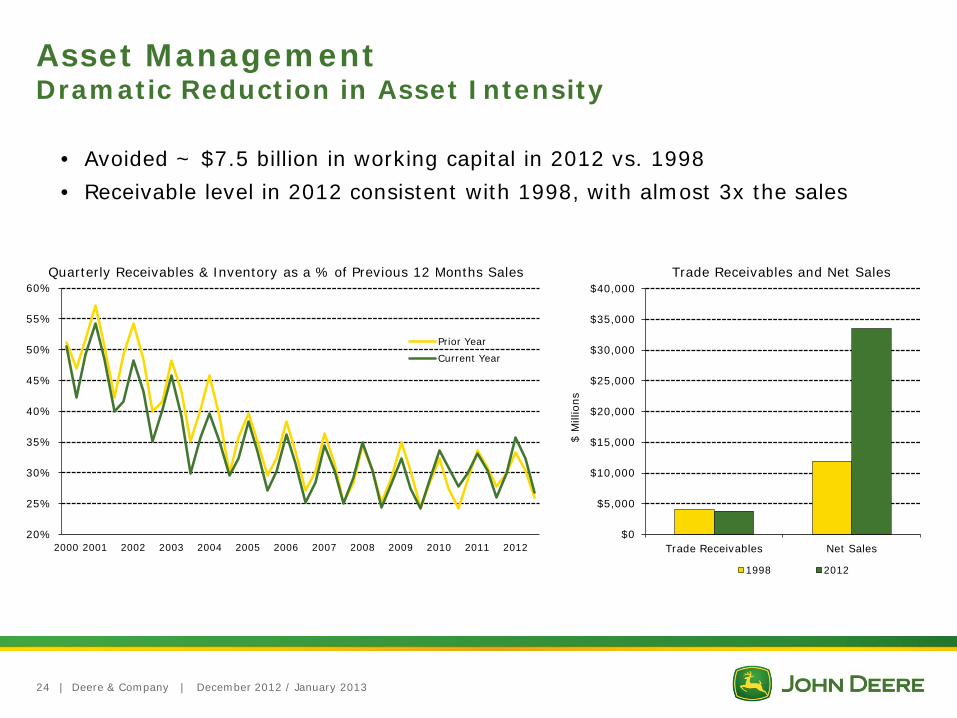

Asset Management Dramatic Reduction in Asset Intensity

20%

25%

30%

35%

40%

45%

50%

55%

60%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Prior Year

Current Year

Trade Receivables and Net Sales

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

Trade Receivables Net Sales

$ M

illio

ns

1998 2012

• Avoided ~ $7.5 billion in working capital in 2012 vs. 1998

• Receivable level in 2012 consistent with 1998, with almost 3x the sales

Quarterly Receivables & Inventory as a % of Previous 12 Months Sales

24

| Deere & Company | December 2012 / January 2013

Investment in New Products and Technologies

R&D as Percent of Net Sales

Source: Deere & Company and competitor SEC filings

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Deere R&D $ Deere % Competitor A % Competitor B % Competitor C %

25

|

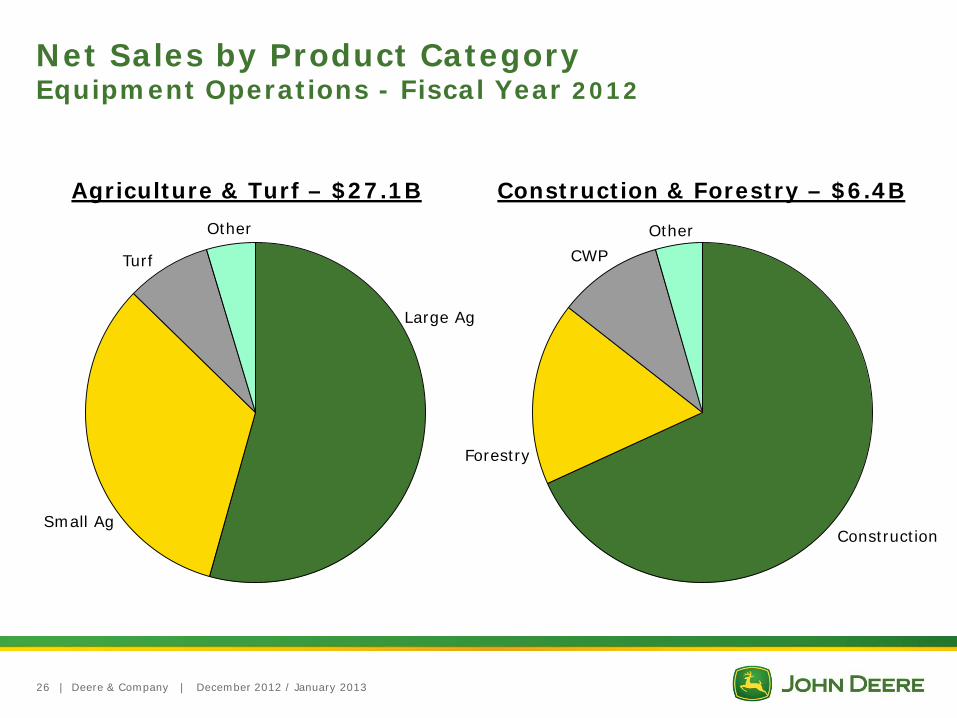

Net Sales by Product Category Equipment Operations - Fiscal Year 2012

Deere & Company | December 2012 / January 2013

Agriculture & Turf – $27.1B Construction & Forestry – $6.4B

Construction

Forestry

CWP

Other

Large Ag

Small Ag

Turf

Other

26

| Deere & Company | December 2012 / January 2013

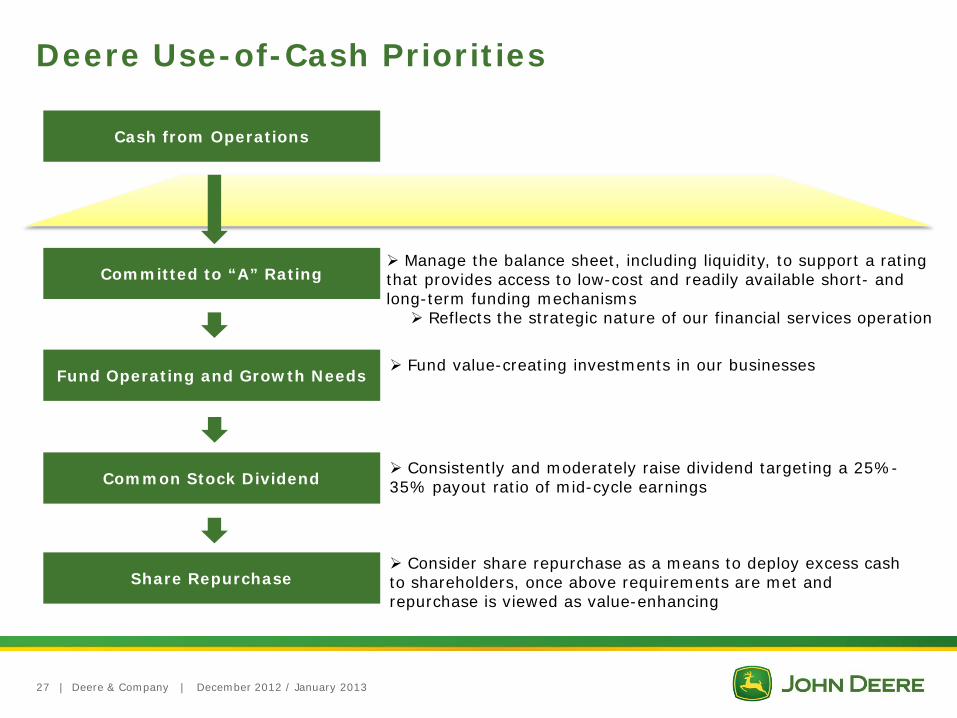

Deere Use-of-Cash Priorities

Manage the balance sheet, including liquidity, to support a rating that provides access to low-cost and readily available short- and long-term funding mechanisms Reflects the strategic nature of our financial services operation

Committed to “A” Rating

Cash from Operations

Fund Operating and Growth Needs

Common Stock Dividend

Share Repurchase

Fund value-creating investments in our businesses

Consistently and moderately raise dividend targeting a 25%-35% payout ratio of mid-cycle earnings

Consider share repurchase as a means to deploy excess cash to shareholders, once above requirements are met and repurchase is viewed as value-enhancing

27

| Deere & Company | December 2012 / January 2013

Share Repurchase As Part of Publicly Announced Plans

28

Cumulative cost of repurchases 2004-2012: ~ $9.2 billion Amount remaining on May 2008 authorization of $5 billion: ~ $2.5 billion 31 October 2012 period ended shares (basic): ~ 387.8 million (diluted): ~ 392.5 million Shares repurchased 2004-2012: ~ 160.7 million Average repurchase price 2004-2012: $57.10

* All shares adjusted for two-for-one stock split effective 26 November 2007 ** Rounded totals for each period – sum may not tie to cumulative cost of repurchases 2004-2012

Actual Shares

Repurchased* (in millions)

Total Amount** (in billions)

2004 5.9 $0.2

2005 27.7 $0.9

2006 34.0 $1.3

2007 25.7 $1.5

2008 21.2 $1.7

2009 0.0 $0.0

2010 5.2 $0.4

2011 20.8 $1.7

2012 20.2 $1.6

|

$0.11

$0.14 $0.16

$0.20 $0.22

$0.25

$0.28 $0.30

$0.35

$0.41

$0.46

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

$0.45

$0.50

'03 Q

1

Q2

Q3

Q4

'04 Q

1

Q2

Q3

Q4

'05 Q

1

Q2

Q3

Q4

'06 Q

1

Q2

Q3

Q4

'07 Q

1

Q2

Q3

Q4

'08 Q

1

Q2

Q3

Q4

'09 Q

1

Q2

Q3

Q4

'10 Q

1

Q2

Q3

Q4

'11 Q

1

Q2

Q3

Q4

'12 Q

1

Q2

Q3

Q4

Deere & Company | December 2012 / January 2013

Deere Quarterly Dividends Declared* Q1 2003 – Q4 2012

* Adjusted for 2 for 1 stock split on 26 November 2007 ** See slide 5 for revised John Deere Strategy

29

Dividend raised 64% since launch of the revised John Deere Strategy in 2010**

Supplemental Information Global Markets and Opportunities

| Deere & Company | December 2012 / January 2013

Net Sales by Major Markets Fiscal Years 2012, 2011, 2010, 2009

(in millions of dollars) 2012 2011 %

Change 2010 2009

United States 18,128 15,028 +21% 13,027 11,568

Canada 2,679 2,329 +15% 1,767 1,454

Western Europe 4,271 4,382 -3% 3,360 3,427

Central Europe & CIS 1,720 1,407 +22% 746 749

Central & South America 3,589 3,613 -1% 2,623 1,787

Asia, Africa & Middle East 2,124 1,930 +10% 1,430 1,166

Australia & New Zealand 990 777 +27% 620 605

Total 33,501 29,466 +14% 23,573 20,756

31

|

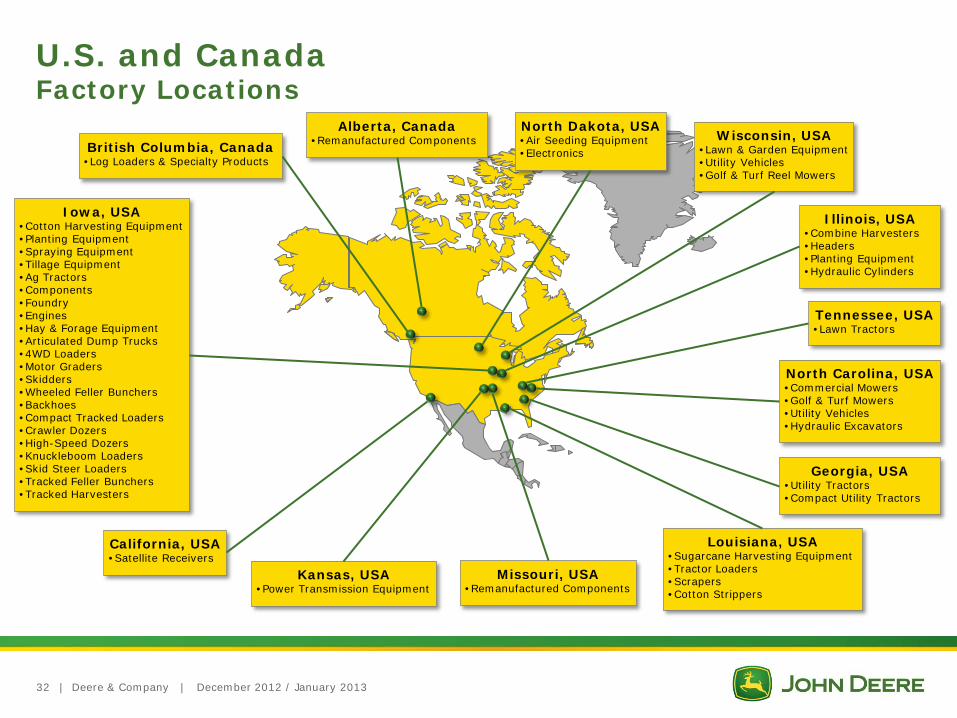

U.S. and Canada Factory Locations

Deere & Company | December 2012 / January 2013 32

Iowa, USA • Cotton Harvesting Equipment • Planting Equipment • Spraying Equipment • Tillage Equipment • Ag Tractors • Components • Foundry • Engines • Hay & Forage Equipment • Articulated Dump Trucks • 4WD Loaders • Motor Graders • Skidders • Wheeled Feller Bunchers • Backhoes • Compact Tracked Loaders • Crawler Dozers • High-Speed Dozers • Knuckleboom Loaders • Skid Steer Loaders • Tracked Feller Bunchers • Tracked Harvesters

Illinois, USA • Combine Harvesters • Headers • Planting Equipment • Hydraulic Cylinders

North Dakota, USA • Air Seeding Equipment • Electronics

North Carolina, USA • Commercial Mowers • Golf & Turf Mowers • Utility Vehicles • Hydraulic Excavators

Alberta, Canada • Remanufactured Components British Columbia, Canada

• Log Loaders & Specialty Products

California, USA • Satellite Receivers

Kansas, USA • Power Transmission Equipment

Missouri, USA • Remanufactured Components

Louisiana, USA • Sugarcane Harvesting Equipment • Tractor Loaders • Scrapers • Cotton Strippers

Georgia, USA • Utility Tractors • Compact Utility Tractors

Tennessee, USA • Lawn Tractors

Wisconsin, USA • Lawn & Garden Equipment • Utility Vehicles • Golf & Turf Reel Mowers

| Deere & Company | December 2012 / January 2013

U.S. and Canada Recent Announcements

• November 2012 – $58 million investment at Moline, IL planter factory to enhance efficiency and quality

• June 2012 – $47 million investment at Moline, IL cylinder operations to expand manufacturing capacity

• March 2012 – Final Tier 4/Stage IV solution to combine proven EGR Interim Tier 4 platform with customized selective catalytic reduction (SCR) system

• March 2012 – $70 million investment at Waterloo, IA factory to expand production of large farm tractors by 10%

• January 2012 – Strategic agreement with MacDon to manufacture self-propelled windrowers

• December 2011 – $85 million in capital improvements at Des Moines, IA factory to expand production of self-propelled sprayers

33

2008- 2010

2010- 2012

2012- 2013

25%

15%

10%

Waterloo Works Capacity Expansion

2008 to 2013

Deere & Company Forecast as of 21 November 2012

| Deere & Company | December 2012 / January 2013

EU 27 Factory Locations

Joensuu, Finland • Wheel Forwarders • Wheel Harvesters • Forestry Attachments

Bruchsal, Germany • Tractor, Harvesting & Forestry Cabs

Mannheim, Germany • Tractors

Zweibrücken, Germany • Combine & Forage Harvesters

Arc-les-Gray, France • Forage Equipment • Balers • Ag Loaders

Saran, France • Engines

Madrid, Spain • Components

Horst, The Netherlands • Spraying Equipment

Stadtlohn, Germany • Forage Harvesters • Headers

Gummersbach, Germany • Walk-Behind Mowers

34

|

• October 2012 – Grand opening of new Polish branch headquarters and training center

• Represents a $26 million investment in the region

• November 2011 – Awards received at Agritechnica 2011

• 7280R – “Tractor of the Year 2012”

• 6R tractor – “Machine of the Year”

• Five silver medals

• June 2011 – Largest new product introduction for Region 2*

• Over 100 new products

• 80% of large tractor and combine models new or updated

• Focus on Dealer of Tomorrow strategy

• May 2011 – John Deere and Kuhn Group sign strategic cooperation

• Provides large square balers into Region 2* in 2012

Deere & Company | December 2012 / January 2013

EU 27 Recent Announcements

* Region 2: EU 27, CIS (including Russia), Mediterranean countries in Africa, and the Near and Middle East

35

|

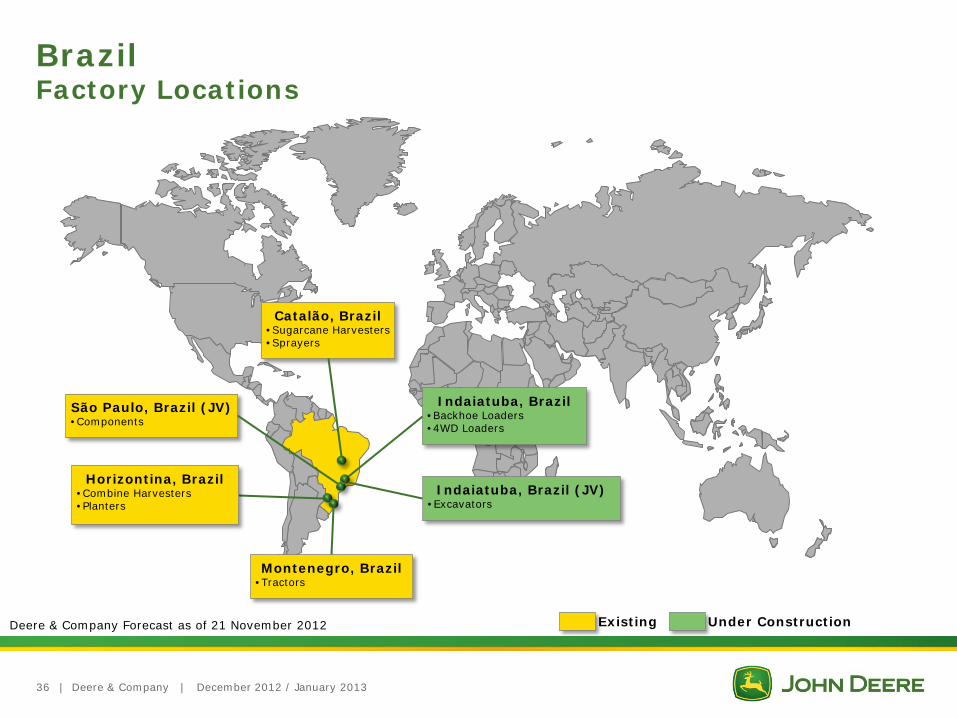

Brazil Factory Locations

Deere & Company | December 2012 / January 2013

São Paulo, Brazil (JV) • Components

Catalão, Brazil • Sugarcane Harvesters • Sprayers

Montenegro, Brazil • Tractors

Horizontina, Brazil • Combine Harvesters • Planters

Indaiatuba, Brazil • Backhoe Loaders • 4WD Loaders

Indaiatuba, Brazil (JV) • Excavators

Deere & Company Forecast as of 21 November 2012

36

Existing Under Construction

| Deere & Company | December 2012 / January 2013

Brazil Recent Announcements

• October 2011 – Two new factories in São Paulo to manufacture construction equipment

• Solely-owned Deere factory

• Backhoes and four-wheel-drive loaders

• Partner with Hitachi in second factory

• Excavators

• Expect production to begin in 2014

Deere & Company Forecast as of 21 November 2012

1 Carta da Anfavea, November 2011 and November 2012

• Agriculture portfolio and dealer expansion

• 50 new or updated products in 2010/2011

• Dealer locations roughly doubled since 2007

• Achieved about 6 points of tractor market share in 2-year period - FY 2011 and FY 20121

37

|

CIS Factory Locations

Orenburg, Russia • Seeding Equipment • Tillage Equipment • Spraying Equipment

Deere & Company | December 2012 / January 2013 38

Orenburg, Russia • Seeding Equipment • Tillage Equipment • Spraying Equipment

Domodedovo, Russia • Tractors • Combine Harvesters • Combine Front-End Equipment • Backhoes, Loaders, Graders • Skidders

Existing Under Construction Deere & Company Forecast as of 21 November 2012

| Deere & Company | December 2012 / January 2013

CIS Recent Announcements

• November 2011 – Orenburg, Russia • Move existing operations to a new, larger facility

• Increase available manufacturing space by ~ 600 percent

• Expand product offering from four to fifteen models

• Expect production to begin in 2013

• March 2011 – Domodedovo, Russia • Double manufacturing space at the factory

• Expand capacity for existing products

• Enable addition of new products such as front-end equipment

39

|

India Factory Locations

Deere & Company | December 2012 / January 2013

Gummidipoondi, India (JV) • Side-Shift Backhoes • 4WD Loaders (planned production 2014)

Pune, India • Engines • Transmissions • Tractors (36-75 hp) • Electronics

Sirhind, India • Combine Harvesters

Dewas, India • Tractors (36-50 hp)

Deere & Company Forecast as of 21 November 2012

40

Existing Under Construction

|

• January 2011 – New tractor factory in Dewas and expand current tractor facility in Pune

• ~ $100 million investment

• Expect production in Dewas to begin in 2013

• October 2010 – Ashok Leyland John Deere Construction Equipment Company inauguration

• Production of backhoes commenced in 2011

• Four-wheel-drive loader production expected in 2014

• September 2010 – New combine factory in Sirhind

• Production commenced February 2012

• John Deere has been the largest exporter of tractors from India for past 8 years

Deere & Company | December 2012 / January 2013

India Recent Announcements

Deere & Company Forecast as of 21 November 2012

41

|

China Factory Locations

Deere & Company | December 2012 / January 2013

Xuzhou, China (JV) • Excavators

Ningbo, China • Tractors (28-70 hp) • Small Combine Harvesters

Tianjin, China (JV) • Tractors (75-135 hp)

Tianjin (TEDA), China • Transmissions

Jiamusi, China • Large Combine Harvesters • Corn Pickers • Cotton Pickers

Harbin, China • Combine Front-End Equipment • Tractors (150+ hp) • Planters • Sprayers • Irrigation Products

Tianjin (TEDA), China • 4WD Loaders • Excavators

Tianjin (TEDA), China • Engines

Deere & Company Forecast as of 21 November 2012

42

Existing Under Construction

| Deere & Company | December 2012 / January 2013

China Recent Announcements

Deere & Company Forecast as of 21 November 2012

Construction Equipment (New)

Engines (New)

Product Test (PV&V)

Office (New)

Tianjin Economic-Technological Development Area (TEDA) Site

Drivetrain

• May 2011 – New engine facility in Tianjin

• ~ $60 million investment

• Initial occupancy July 2012

• Expect production to begin in 2013

• May 2011 – New factory in Harbin

• ~ $80 million initial outlay

• Mid- and large-sized tractors

• Harvesting front-end equipment

• Planters and sprayers

• Irrigation products

• Opened November 2012

• Expect production to begin in 2013

• December 2010 – New construction equipment factory in Tianjin

• ~ $50 million investment

• Initial occupancy July 2012

• Expect production to begin in 2013

43

|

Other Regions Factory Locations

Deere & Company | December 2012 / January 2013 44

Kibbutz Beit Hashita, Israel • Cotton Picker Components

Rosario, Argentina • Engines • Tractors • Combines

Monterrey, Mexico • Rotary Cutters • Implements • Components

Ramos, Mexico • Ag Loaders • Compact Utility Tractor Loaders • Utility Tractor Cabs

Saltillo, Mexico • Ag Tractors • Transaxles

Torreon, Mexico • Axles • Engines • Electronics

Richards Bay, South Africa • Articulated Dump Trucks • Loaders

Tokoroa, New Zealand • Forestry Harvester Heads

|

Worldwide Parts Services Supporting the Global Growth of Our Equipment Operations

Deere & Company | December 2012 / January 2013 45

Highlights: ● Nagpur, India

Announced India Parts Distribution Center… target to open in 4Q 2013

● Johannesburg, South Africa New Regional Distribution Center opened 4Q 2012

● Rosario, Argentina New, larger Regional Distribution Center opened 4Q 2012

● Stockholm, Sweden New Regional Distribution Center serving C&F and A&T opened May 2012

● Bruchsal, Germany E-PDC deconsolidation & packaging facility opened Nov 2011

Anchor Parts Distribution Centers

Regional Parts Distribution Centers or Depots Distribution Centers under construction

| Deere & Company | December 2012 / January 2013

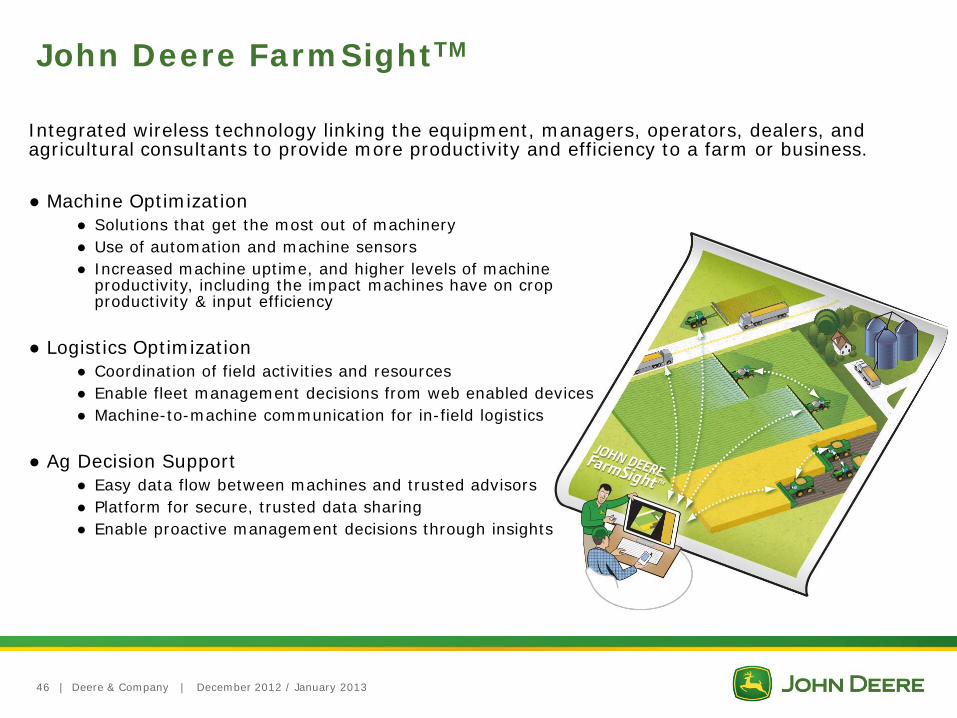

Integrated wireless technology linking the equipment, managers, operators, dealers, and agricultural consultants to provide more productivity and efficiency to a farm or business.

John Deere FarmSightTM

46

● Machine Optimization ● Solutions that get the most out of machinery ● Use of automation and machine sensors ● Increased machine uptime, and higher levels of machine

productivity, including the impact machines have on crop productivity & input efficiency

● Logistics Optimization ● Coordination of field activities and resources ● Enable fleet management decisions from web enabled devices ● Machine-to-machine communication for in-field logistics

● Ag Decision Support ● Easy data flow between machines and trusted advisors ● Platform for secure, trusted data sharing ● Enable proactive management decisions through insights

| Deere & Company | December 2012 / January 2013

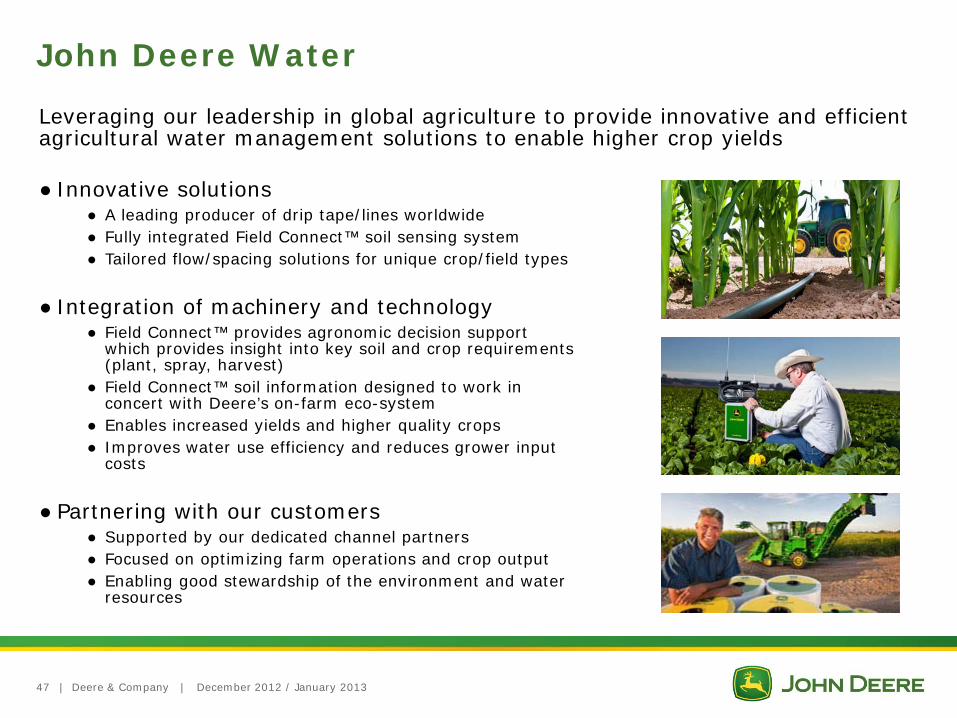

John Deere Water

Leveraging our leadership in global agriculture to provide innovative and efficient agricultural water management solutions to enable higher crop yields

● Innovative solutions ● A leading producer of drip tape/lines worldwide ● Fully integrated Field Connect™ soil sensing system ● Tailored flow/spacing solutions for unique crop/field types

● Integration of machinery and technology ● Field Connect™ provides agronomic decision support

which provides insight into key soil and crop requirements (plant, spray, harvest)

● Field Connect™ soil information designed to work in concert with Deere’s on-farm eco-system

● Enables increased yields and higher quality crops ● Improves water use efficiency and reduces grower input

costs

● Partnering with our customers ● Supported by our dedicated channel partners ● Focused on optimizing farm operations and crop output ● Enabling good stewardship of the environment and water

resources

47

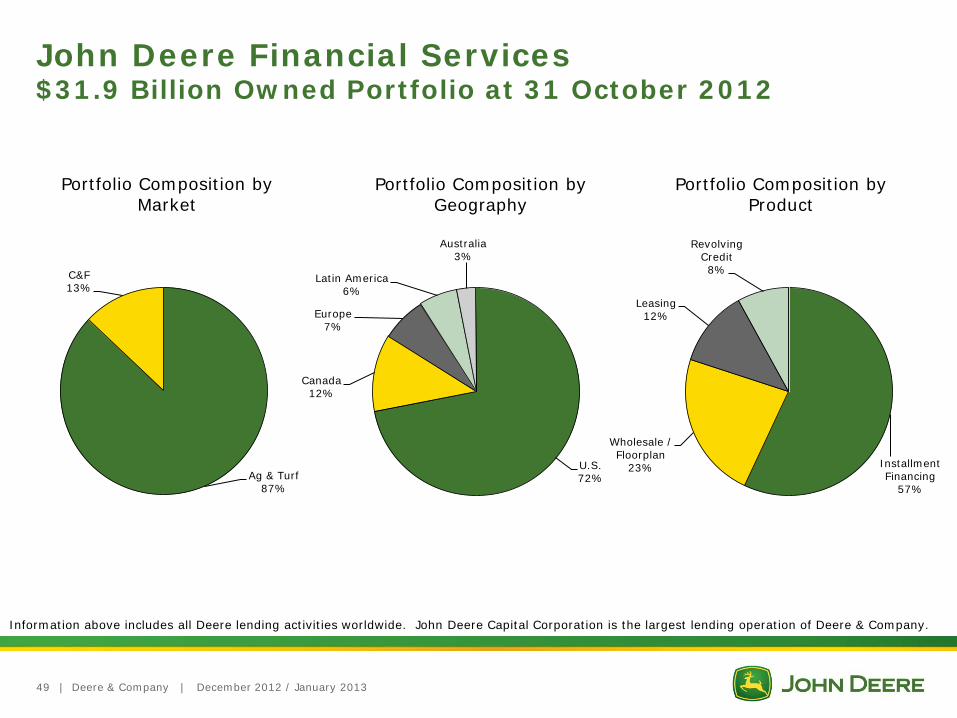

Supplemental Information John Deere Financial Services

| Deere & Company | December 2012 / January 2013

Portfolio Composition by Market

John Deere Financial Services $31.9 Billion Owned Portfolio at 31 October 2012

Portfolio Composition by Geography

Portfolio Composition by Product

Information above includes all Deere lending activities worldwide. John Deere Capital Corporation is the largest lending operation of Deere & Company.

Ag & Turf 87%

C&F 13%

U.S. 72%

Canada 12%

Europe 7%

Latin America 6%

Australia 3%

49

Installment Financing

57%

Wholesale / Floorplan

23%

Leasing 12%

Revolving Credit 8%

| Deere & Company | December 2012 / January 2013

John Deere Capital Corporation Profitability and Growth

50

383

275 291 311

282

149

319 364

2005 2006 2007 2008 2009 2010 2011 2012

Net Income ($ Millions)

0.16% 0.22% 0.29% 0.33%

0.70%

0.48%

0.12% 0.05%

2005 2006 2007 2008 2009 2010 2011 2012

Write-offs/Average Owned Portfolio

17.7 18.6 19.0 19.1 19.3 21.1

23.3

26.6

2005 2006 2007 2008 2009 2010 2011 2012

Administered Portfolio Growth ($ Billions)

Supplemental Information Farm Fundamentals

|

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012F 2013F

$ B

illio

ns

Government Payments Total Cash Receipts

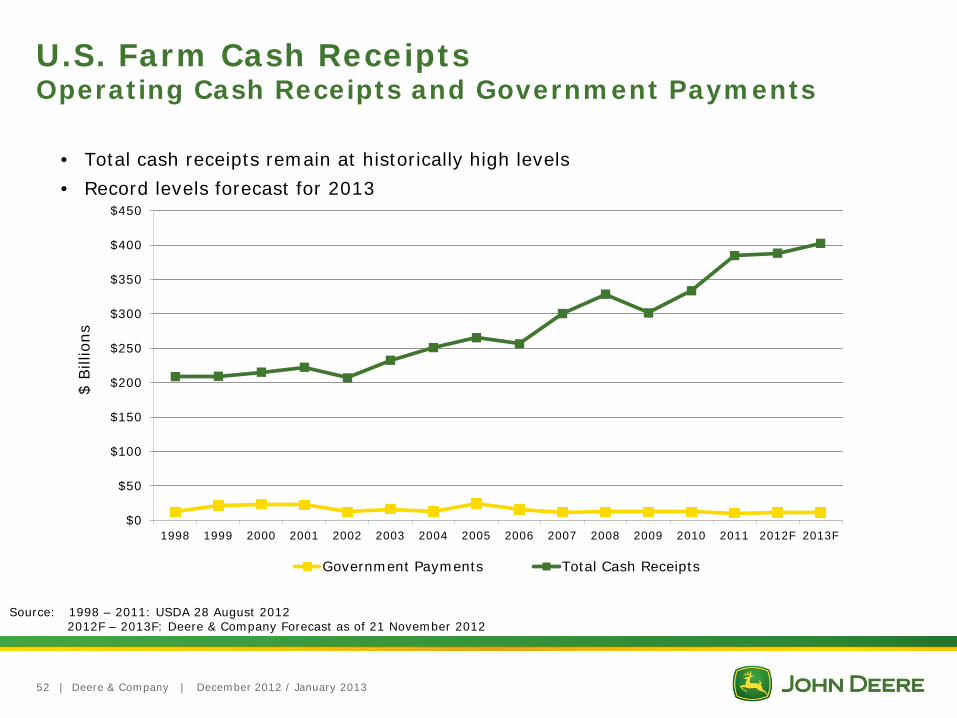

Deere & Company | December 2012 / January 2013

U.S. Farm Cash Receipts Operating Cash Receipts and Government Payments

• Total cash receipts remain at historically high levels

• Record levels forecast for 2013

Source: 1998 – 2011: USDA 28 August 2012 2012F – 2013F: Deere & Company Forecast as of 21 November 2012

52

| Deere & Company | December 2012 / January 2013

U.S. Farm Balance Sheet Strong

53

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

30%

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000 1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012F

2013F

$ B

illio

ns

Farm Debt Farm Equity Debt to Equity Ratio (%) Debt to Asset Ratio (%)

Source: 1970 – 2011: USDA 27 November 2012 2012F – 2013F: Deere & Company Forecast as of 21 November 2012

|

World Farm Fundamentals Global Stocks-To-Use Ratios

Deere & Company | December 2012 / January 2013 54

0%

10%

20%

30%

40%

50%

60%

70%

80% 1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011E

2012P

Source: USDA - 11 December 2012

Cotton

Wheat

Corn

Soybeans

Supplemental Information Appendix

| Deere & Company | December 2012 / January 2013

Equipment Ops SVA Reconciliation to GAAP

Equipment Operations 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001Net Sales 5,848 5,723 6,479 7,663 8,830 9,640 11,082 11,926 9,701 11,169 11,077 Average Identifiable Assets

With Inventories at LIFO 5,585 5,765 5,449 5,551 6,187 6,502 6,682 7,672 7,724 8,069 8,743 With Inventories at Standard Cost 6,702 6,846 6,442 6,494 7,131 7,488 7,703 8,711 8,739 9,039 9,678

Operating Profit 16 77 242 847 1,006 1,125 1,402 1,476 272 693 (46) Percent of Net Sales 0.3% 1.3% 3.7% 11.1% 11.4% 11.7% 12.6% 12.4% 2.8% 6.2% -0.4%

Operating Return on AssetsWith Inventories at LIFO 0.3% 1.3% 4.4% 15.3% 16.3% 17.3% 21.0% 19.3% 3.5% 8.6% -0.5%With Inventories at Standard Cost 0.2% 1.1% 3.8% 13.0% 14.1% 15.0% 18.2% 16.9% 3.1% 7.7% -0.5%

SVA Cost of Assets (804) (821) (773) (780) (856) (898) (924) (1,045) (1,049) (1,085) (1,162) SVA (788) (744) (531) 67 150 227 477 431 (776) (392) (1,208)

Equipment Operations 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Net Sales 11,703 13,349 17,673 19,401 19,884 21,489 25,803 20,756 23,573 29,466 33,501 Average Identifiable Assets

With Inventories at LIFO 6,229 5,965 6,482 7,248 7,546 8,092 9,652 9,647 9,196 11,516 13,594 With Inventories at Standard Cost 7,147 6,925 7,477 8,312 8,634 9,205 10,812 10,950 10,494 12,875 14,965

Operating Profit 401 708 1,905 1,842 1,905 2,318 2,927 1,365 2,909 3,839 4,397 Percent of Net Sales 3.4% 5.3% 10.8% 9.5% 9.6% 10.8% 11.3% 6.6% 12.3% 13.0% 13.1%

Operating Return on AssetsWith Inventories at LIFO 6.4% 11.9% 29.4% 25.4% 25.2% 28.6% 30.3% 14.1% 31.6% 33.3% 32.3%With Inventories at Standard Cost 5.6% 10.2% 25.5% 22.2% 22.1% 25.2% 27.1% 12.5% 27.7% 29.8% 29.4%

SVA Cost of Assets (858) (831) (897) (998) (1,036) (1,094) (1,284) (1,301) (1,259) (1,545) (1,795) SVA (457) (123) 1,008 844 869 1,224 1,643 64 1,650 2,294 2,602

(millions of dollars unless stated otherwise)

56

| Deere & Company | December 2012 / January 2013

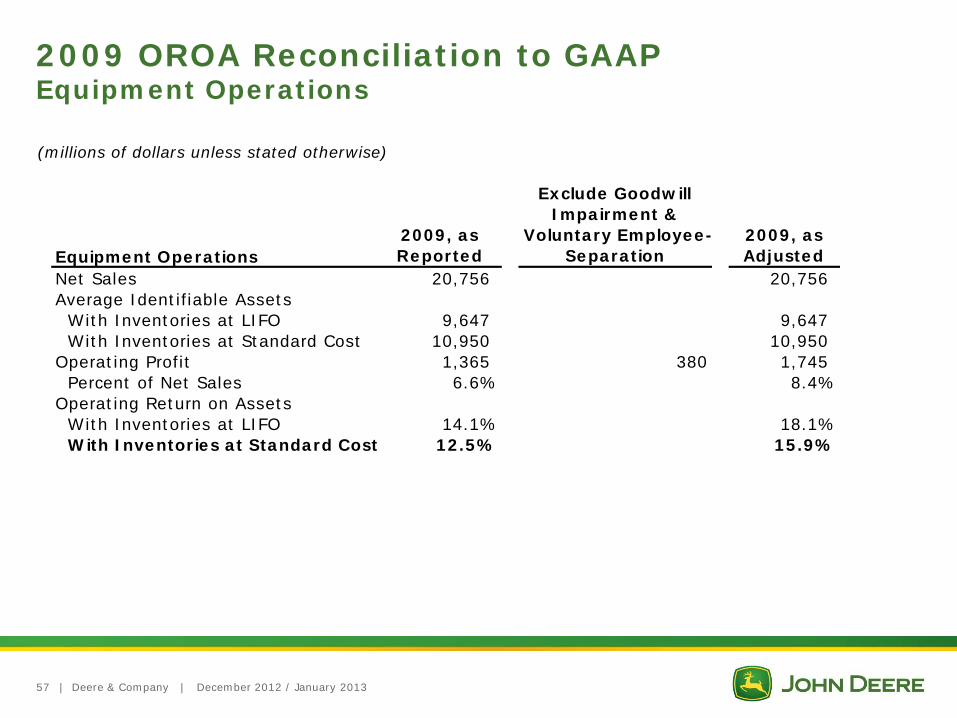

2009 OROA Reconciliation to GAAP Equipment Operations

Equipment Operations2009, as Reported

Exclude Goodwill Impairment &

Voluntary Employee-Separation

2009, as Adjusted

Net Sales 20,756 20,756 Average Identifiable Assets

With Inventories at LIFO 9,647 9,647 With Inventories at Standard Cost 10,950 10,950

Operating Profit 1,365 380 1,745 Percent of Net Sales 6.6% 8.4%

Operating Return on AssetsWith Inventories at LIFO 14.1% 18.1%With Inventories at Standard Cost 12.5% 15.9%

(millions of dollars unless stated otherwise)

57