decision 21520-d01-2016 fortis 2014 true-up and 2016 … · (dcc)/supervisory control and data...

TRANSCRIPT

Decision 21520-D01-2016

FortisAlberta Inc. 2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing September 15, 2016

Alberta Utilities Commission

Decision 21520-D01-2016

FortisAlberta Inc.

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing

Proceeding 21520

September 15, 2016

Published by the:

Alberta Utilities Commission

Fifth Avenue Place, Fourth Floor, 425 First Street S.W.

Calgary, Alberta

T2P 3L8

Telephone: 403-592-8845

Fax: 403-592-4406

Website: www.auc.ab.ca

Decision 21520-D01-2016 (September 15, 2016) • i

Contents

1 Decision .................................................................................................................................. 1

2 Introduction ........................................................................................................................... 1

3 Compliance with the Commission’s directions in Decision 20497-D01-2016 .................. 2 3.1 Direction 1: Unmetered Oilfield Services ....................................................................... 2 3.2 Direction 2: Automated Meter, Metering Unmetered Oilfield Services, and Metering

and Other ......................................................................................................................... 3 3.3 Direction 3: Compliance, Safety, Aging Facilities and Reliability (CSAR), Worst

Performing Feeders, and Urgent Repairs programs ........................................................ 4

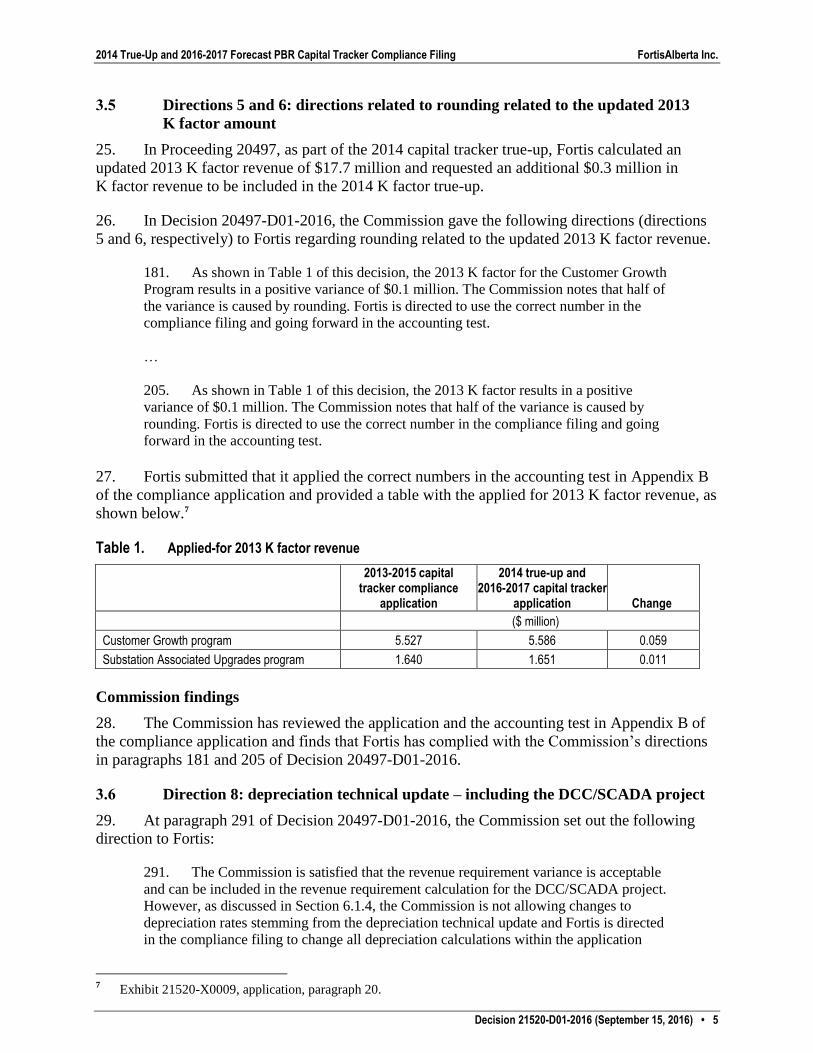

3.4 Direction 4: depreciation technical update – excluding the Distribution Control Centre

(DCC)/Supervisory Control and Data Acquisition (SCADA) project ............................ 4

3.5 Directions 5 and 6: directions related to rounding related to the updated 2013 K factor

amount ............................................................................................................................. 5 3.6 Direction 8: depreciation technical update – including the DCC/SCADA project ......... 5 3.7 Direction 10: Additional allocated revenue requirement amounts ................................. 6 3.8 Directions 9, 11, 12 and 13: accounting test and materiality test directions ................... 6

4 Resulting 2014 actual and 2016, 2017 forecast K factor amounts .................................... 8

5 Remaining Commission direction from Decision 20497-D01-2016 ................................ 10

6 Order .................................................................................................................................... 11

Appendix 1 – Proceeding participants ...................................................................................... 13

Appendix 2 – Commission directions addressed in the compliance filing ............................. 14

Appendix 3 – Summary of Commission directions .................................................................. 17

List of tables

Table 1. Applied-for 2013 K factor revenue ............................................................................ 5

Table 2. Capital trackers K factor revenue ............................................................................. 9

Table 3. Summary of impacts K factor revenue ................................................................... 10

Decision 21520-D01-2016 (September 15, 2016) • 1

Alberta Utilities Commission

Calgary, Alberta

FortisAlberta Inc.

2014 True-Up and 2016-2017 Forecast PBR Decision 21520-D01-2016

Capital Tracker Compliance Filing Proceeding 21520

1 Decision

1. In this decision the Alberta Utilities Commission determines FortisAlberta Inc.’s

compliance with the Commission’s directions issued in Decision 20497-D01-2016.1 For the

reasons outlined in this decision, the Commission finds that Fortis has complied with all but one

of the Commission’s directions in Decision 20497-D01-2016 that are relevant to the compliance

application, and directs Fortis to comply with the outstanding direction as soon as practicable.

The Commission approves Fortis’ 2013 additional K factor revenue as well as the 2014, 2016

and 2017 K factor revenue amounts as applied-for in the application.

2 Introduction

2. On February 20, 2016, the Commission issued Decision 20497-D01-2016, which dealt

with Fortis’ 2014 capital tracker true-up and 2016-2017 capital tracker forecast application under

performance-based regulation (PBR).

3. On April 15, 2016, Fortis filed with the Commission a compliance application to

Decision 20497-D01-2016. On April 19, 2016, the Commission issued a notice of application

that required interested parties to submit a statement of intent to participate (SIP) by April 29,

2016. In their SIPs, parties were to provide a description of their interest in the proceeding, an

explanation of their position including information in support of the position, and submissions as

to whether further process is required. Only the Consumers’ Coalition of Alberta (CCA) filed a

SIP.

4. In a letter dated May 6, 2016, the Commission determined that the compliance

application would be considered by way of a minimal written process as set out in

Bulletin 2015-09.2 The Commission established the following process schedule:

Process step Deadline

Information requests (IRs) to Fortis May 25, 2016

IR responses from Fortis June 13, 2016

Argument June 30, 2016

Reply argument July 19, 2016

5. On May 25, 2016, the CCA advised that it had no IRs for Fortis. The Commission, by

letter issued on June 16, 2016, requested that parties file submissions on the need for further

process. On June 20, 2016, the CCA filed a letter stating that it did not intend to file argument or

1 Decision 20497-D01-2016: FortisAlberta Inc., 2014 PBR Capital Tracker True-Up and 2016-2017 PBR Capital

Tracker Forecast, Proceeding 20497, February 20, 2016. 2 Bulletin 2015-09, Performance standards for processing rate-related applications, March 26, 2015.

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

2 • Decision 21520-D01-2016 (September 15, 2016)

reply argument. Fortis did not file a submission on the need for further process. The Commission

considers the record for this proceeding to have closed on June 20, 2016.

6. In reaching the determinations set out within this decision, the Commission has

considered all relevant materials comprising the record of this proceeding, as well as related PBR

and capital tracker decisions. Accordingly, reference in this decision to specific parts of the

record are intended to assist the reader in understanding the Commission’s reasoning relating to a

particular matter and should not be taken as an indication that the Commission did not consider

all relevant portions of the record with respect to a particular matter.

7. Section 3 of this decision addresses Fortis’ compliance with the Commission’s directions

in Decision 20497-D01-2016 that are relevant to this compliance application. Section 4 deals

with the resulting 2014 actual and 2016, 2017 forecast K factor amounts. Section 5 addresses the

remaining Commission direction from Decision 20497-D01-2016.

3 Compliance with the Commission’s directions in Decision 20497-D01-2016

8. In Decision 20497-D01-2016, the Commission issued 14 directions. In Fortis’ view,

12 of these directions related to the compliance application, and two applied to future capital

tracker applications. Specifically, Fortis indicated that directions 1 and 7 from Decision 20497-

D01-2016 will be addressed in future applications, though Fortis did provide submissions

regarding Direction 1 in the compliance application.3

9. Fortis included a summary table of concordance,4 reproduced in Appendix 2 to this

decision, which lists all Commission directions from Decision 20497-D01-2016.

10. The Commission’s findings on each of the directions set out in Decision 20497-D01-

2016 are set out below.

3.1 Direction 1: Unmetered Oilfield Services

11. At paragraph 60 of Decision 20497-D01-2016, the Commission set out the following

direction to Fortis:

60. Similarly, the Commission does not accept, as an adequate justification for its

Metering Unmetered Oilfield Services project grouping, Fortis’ explanation that

efficiencies arise in the design and construction of each of these projects when the work

is completed together. Again, this is owing to the fact that grouping is an accounting

exercise. However, the costs of three-wire to four-wire conversions and the costs of

adding meters to the unmetered oilfield services have not historically been tracked

separately. Therefore, for simplicity, the Commission will not require Fortis to

disaggregate this project at this time. The inclusion of the three-wire to four-wire

conversions in the Metering Unmetered Oilfield Services project is approved for the

purposes of the first PBR term. However, separately tracked data may be relevant to

future Commission consideration of this issue. As such, the Commission directs Fortis to

track the costs of three-wire to four-wire conversions and the costs of adding meters to

the unmetered oilfield services separately going forward.

3 Exhibit 21520-X0009, application, paragraphs 9 and 11.

4 Exhibit 21520-X0008, Appendix A.

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

Decision 21520-D01-2016 (September 15, 2016) • 3

12. In the compliance application, Fortis stated that it will track any additional costs related

to these three-wire to four-wire conversions and the Metering Unmetered Oilfield Services

project separately in the next PBR term. Fortis noted that the Metering Unmetered Oilfield

Services project is scheduled to end in 2017.

Commission findings

13. As discussed above, Fortis explained that Direction 1 in Decision 20497-D01-2016 was

relevant to a future capital tracker application. However, in the Commission’s view, Direction 1

applied on a go-forward basis following the release of Decision 20497-D01-2016 and is relevant

to the compliance application. The Commission intended for Fortis to separately track data

during the period of 2016 and 2017, as this information may be relevant to future Commission

consideration of this issue. Accordingly, the Commission finds Fortis to be non-compliant with

the direction.

14. The Commission directs Fortis to track the costs of three-wire to four-wire conversions

and the costs of adding meters to the unmetered oilfield services separately as soon as practicable

following the release of this decision, and until this program is complete.

3.2 Direction 2: Automated Meter, Metering Unmetered Oilfield Services, and

Metering and Other

15. At paragraph 61 of Decision 20497-D01-2016, the Commission set out the following

direction to Fortis:

61. The Commission considers that the purpose of the Automated Meter project,

Metering Unmetered Oilfield Services project, and the Metering and Other program is the

replacement, repair, and installation of meters. The programs are similar in nature and

have a common requirement for capital investment. The Commission does not consider

the Automated Meter project and Metering Unmetered Oilfield Services project to be

sufficiently unique and substantial so as to merit separate capital tracker groups. The

Commission directs Fortis to group these three programs together for the purposes of the

compliance filing and its future capital tracker applications.

16. In the compliance application, Fortis stated that it has regrouped its capital tracker

projects and programs to aggregate the Automated Meter project, Metering Unmetered Oilfield

Services project, and the Metering and Other program.

17. Fortis indicated that the System Purchases program, which was included in the Metering

and Other program, is related to the purchase of Rural Electrification Association distribution

assets. Accordingly, Fortis excluded the historical rate base associated with the Systems

Purchases program from the aggregated metering group and included it in the accounting test as

a separate project grouping. Fortis submitted that this did not impact the results of the accounting

test.

Commission findings

18. The Commission has reviewed the schedules provided by Fortis in the compliance

application and finds that Fortis has complied with the Commission’s directions in paragraph 61

of Decision 20497-D01-2016. The Commission finds reasonable and approves Fortis’ exclusion

of the historical rate base of the System Purchases program from the aggregated metering group

and its inclusion in the accounting test as a separate project grouping.

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

4 • Decision 21520-D01-2016 (September 15, 2016)

3.3 Direction 3: Compliance, Safety, Aging Facilities and Reliability (CSAR), Worst

Performing Feeders, and Urgent Repairs programs

19. At paragraph 62 of Decision 20497-D01-2016, the Commission set out the following

direction to Fortis:

62. The Commission considers that while each of the CSAR, Worst Performing

Feeders, and Urgent Repairs programs has a different process to identify the work, the

work completed under each program is similar in function. Furthermore, all three

programs share a common requirement for capital investment. The Commission,

therefore, directs Fortis to group these three programs together for the purposes of the

compliance filing and its future capital tracker applications.

20. In the compliance application, Fortis stated that it has grouped the CSAR, Worst

Performing Feeders and Urgent Repairs programs together, as directed by the Commission.

Commission findings

21. The Commission has reviewed the schedules provided by Fortis in the compliance

application and finds that Fortis has complied with the Commission’s directions in paragraph 62

of Decision 20497-D01-2016.

3.4 Direction 4: depreciation technical update – excluding the Distribution Control

Centre (DCC)/Supervisory Control and Data Acquisition (SCADA) project

22. At paragraph 143 of Decision 20497-D01-2016, the Commission set out the following

direction to Fortis:

143. For the above reasons, the Commission finds that the determinations made in

paragraph 688 of Decision 2012-237[5] also apply to K factors. Given that Fortis’

depreciation technical update proposal is contrary to the Commission’s determinations

found in paragraph 688 of Decision 2012-237, Fortis’ application to change existing

depreciation rates for all project groupings through the K factor calculation associated

with the deprecation technical update is denied. In the compliance filing to this decision,

Fortis is directed to remove the updated depreciation amounts from the K factor

calculation and base its revenue requirement calculation associated with all project

groupings on the amounts reflective of the depreciation rates approved in the company’s

last depreciation study using plant balances as of December 2010.

23. In the compliance application, Fortis stated that it removed the technical update

depreciation amounts from the K factor calculation, and that the revenue requirement

calculations associated with all project groupings incorporate the depreciation rates approved in

Fortis’ last depreciation study.6

Commission findings

24. The Commission has reviewed the schedules and explanations provided by Fortis in the

compliance application and finds that Fortis has complied with the Commission’s directions in

paragraph 143 of Decision 20497-D01-2016.

5 Decision 2012-237: Rate Regulation Initiative, Distribution Performance-Based Regulation, Proceeding 566,

Application 1606029-1, September 12, 2012. 6 Exhibit 21520-X0009, application, paragraph 16.

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

Decision 21520-D01-2016 (September 15, 2016) • 5

3.5 Directions 5 and 6: directions related to rounding related to the updated 2013

K factor amount

25. In Proceeding 20497, as part of the 2014 capital tracker true-up, Fortis calculated an

updated 2013 K factor revenue of $17.7 million and requested an additional $0.3 million in

K factor revenue to be included in the 2014 K factor true-up.

26. In Decision 20497-D01-2016, the Commission gave the following directions (directions

5 and 6, respectively) to Fortis regarding rounding related to the updated 2013 K factor revenue.

181. As shown in Table 1 of this decision, the 2013 K factor for the Customer Growth

Program results in a positive variance of $0.1 million. The Commission notes that half of

the variance is caused by rounding. Fortis is directed to use the correct number in the

compliance filing and going forward in the accounting test.

…

205. As shown in Table 1 of this decision, the 2013 K factor results in a positive

variance of $0.1 million. The Commission notes that half of the variance is caused by

rounding. Fortis is directed to use the correct number in the compliance filing and going

forward in the accounting test.

27. Fortis submitted that it applied the correct numbers in the accounting test in Appendix B

of the compliance application and provided a table with the applied for 2013 K factor revenue, as

shown below.7

Table 1. Applied-for 2013 K factor revenue

2013-2015 capital tracker compliance

application

2014 true-up and 2016-2017 capital tracker

application Change

($ million)

Customer Growth program 5.527 5.586 0.059

Substation Associated Upgrades program 1.640 1.651 0.011

Commission findings

28. The Commission has reviewed the application and the accounting test in Appendix B of

the compliance application and finds that Fortis has complied with the Commission’s directions

in paragraphs 181 and 205 of Decision 20497-D01-2016.

3.6 Direction 8: depreciation technical update – including the DCC/SCADA project

29. At paragraph 291 of Decision 20497-D01-2016, the Commission set out the following

direction to Fortis:

291. The Commission is satisfied that the revenue requirement variance is acceptable

and can be included in the revenue requirement calculation for the DCC/SCADA project.

However, as discussed in Section 6.1.4, the Commission is not allowing changes to

depreciation rates stemming from the depreciation technical update and Fortis is directed

in the compliance filing to change all depreciation calculations within the application

7 Exhibit 21520-X0009, application, paragraph 20.

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

6 • Decision 21520-D01-2016 (September 15, 2016)

using the originally approved depreciation rates including those calculations for the

DCC/SCADA project, if applicable.

30. In the compliance application, Fortis stated that it incorporated the weighted average

indicative service life to reflect the approved revenue requirement variance for the DCC/SCADA

project. In doing so, Fortis submitted that it removed the technical update depreciation amounts

from the K factor calculation and incorporated the originally approved depreciation rates for the

DCC/SCADA project.8 Fortis indicated that this change is reflected in Appendix B of the

compliance application for 2016 and 2017.

Commission findings

31. The Commission has reviewed the schedules and explanations provided by Fortis in the

compliance application and finds that Fortis has complied with the Commission’s directions in

paragraph 291 of Decision 20497-D01-2016. The Commission is satisfied that Fortis removed

the depreciation technical update amounts from the K factor calculation and correctly

incorporated the originally approved depreciation rates for the DCC/SCADA project.

3.7 Direction 10: Additional allocated revenue requirement amounts

32. At paragraph 391 of Decision 20497-D01-2016, the Commission set out the following

direction to Fortis:

391. Accordingly, the Commission does not approve the true-up year allocation

methodology used by Fortis for 2014. In its compliance filing, Fortis is directed to use the

same allocation methodology for the allocation of additional amounts of revenue

requirement in the true-up for 2014 that is used in forecast years.

33. In the compliance application, Fortis indicated that it used the same methodology for the

allocation of additional amounts of revenue requirement in the 2014 true-up as that used in

forecast years, as shown in Appendix B of the compliance application.9

Commission findings

34. The Commission has reviewed the schedules provided by Fortis in Appendix B of the

compliance application and finds that Fortis has complied with the Commission’s directions in

paragraph 391 of Decision 20497-D01-2016. The Commission is satisfied that Fortis has used

the same methodology for the allocation of additional amounts of revenue requirement in the

2014 true-up as that used in forecast years.

3.8 Directions 9, 11, 12 and 13: accounting test and materiality test directions

35. At paragraph 357 of Decision 20497-D01-2016 (Direction 9), the Commission directed

Fortis to revise its accounting test for 2016 to use the approved 2016 I-X index value of 0.90 per

cent, and the Q factor based on the forecast billing determinants approved in Decision 20818-

D01-2015,10 for the purposes of its 2016 and 2017 capital tracker forecast accounting test.

8 Exhibit 21520-X0009, application, paragraph 17.

9 Exhibit 21520-X0009, application, paragraph 18 and Exhibit 21520-X0007, Appendix B, 2016-2017 Capital

Tracker Accounting Test. 10

Decision 20818-D01-2015: FortisAlberta Inc., 2016 Annual Performance-Based Regulation Rate Adjustment

Filing, Proceeding 20818, December 17, 2015.

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

Decision 21520-D01-2016 (September 15, 2016) • 7

36. In the compliance application,11 Fortis indicated that it updated its accounting test for the

I-X index and Q factors approved in Decision 20818-D01-2015 and provided the I, X and

Q factors used for the period 2013-2016.12

37. At paragraph 397 of Decision 20497-D01-2016 (Direction 11), the Commission directed

Fortis to revise its accounting test for 2014, 2016 and 2017, based on the approved final forecast

or the actual capital additions, the 2016 model assumptions, and other directions set out in the

other sections of Decision 20497-D01-2016. The Commission also directed Fortis to provide two

summary tables in its compliance application. The Commission directed that the first table

should include, for each capital tracker project or program, a comparison of the 2014 actual

capital additions applied for in Proceeding 20497 and the 2014 actual capital additions, revised

in accordance with the directions set out in Decision 20497-D01-2016. The second table would

provide a similar comparison for the forecast 2016 and 2017 capital trackers.

38. In the compliance application, Fortis submitted that it revised its accounting test for 2014,

2016 and 2017 based on the requirements in Direction 11. Fortis provided the summary tables in

the compliance application in Appendix E.13 Further, at paragraphs 419 and 421 of Decision

20497-D01-2016 (directions 12 and 13, respectively), the Commission directed Fortis to use the

approved 2016 I-X index value of 0.90 per cent to calculate the first and second tier materiality

thresholds for 2016 and 2017, and to reassess whether its projects or programs proposed for

capital tracker treatment in 2014 on an actual basis and in 2016-2017 on a forecast basis, satisfy

the two-tiered materiality test requirement of Criterion 3. For this reassessment, Fortis was to use

the approved 2014 threshold amount, as well as revised 2016-2017 threshold amounts.

39. In the compliance application, Fortis provided the revised schedules with the results of

the accounting test under Criterion 1 and materiality tests under Criterion 3, reflecting the

Commission’s directions in Decision 20497-D01-2016. Fortis submitted that it used the I-X

index of 0.90 per cent approved in Decision 20818-D01-2015 to recalculate its first and second

tier materiality thresholds for 2016 and 2017. Fortis reported that the first tier materiality

thresholds for 2016 and 2017 were $0.349 million and $0.352 million, respectively, and the

second tier materiality thresholds for 2016 and 2017 were $3.491 million and $3.523 million,

respectively. Fortis confirmed that its applied-for capital tracker projects and programs continue

to meet the materiality thresholds, based on the approved 2014 materiality threshold amounts, as

well as the revised 2016 and 2017 materiality threshold amounts.

Commission findings

40. The Commission has reviewed Fortis’ updated accounting test calculations and the 2016

and 2017 materiality thresholds, and finds that Fortis has accurately updated its accounting test

schedules to reflect the 2016 I-X index value of 0.90 per cent and the Q factors are based on the

forecast billing determinants, both of which were approved by the Commission in Decision

20818-D01-2015.14

41. Upon reviewing Fortis’ updated accounting test calculations, the Commission is satisfied

that Fortis has revised its accounting test for 2014, 2016 and 2017, based on the approved final

11

Exhibit 21520-X0009, application, paragraph 22. 12

Exhibit 21520-X0006, Appendix C, 2013-2016 I, X and Q factors. 13

Exhibit 21520-X0002, Appendix E, 2014, 2016-2017 Net Capital Addition Summaries. 14

Decision 20818-D01-2015, paragraph 76.

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

8 • Decision 21520-D01-2016 (September 15, 2016)

forecast or the actual capital additions, the 2016 model assumptions, and other directions set out

in the other sections of Decision 20497-D01-2016.

42. Further, the Commission has reviewed Fortis’ reassessment of its capital tracker project

and program K factor amounts against the updated materiality threshold amounts under

Criterion 3, and is satisfied that Fortis’ capital tracker project and program K factor amounts

meet the updated threshold amounts. Finally, the Commission has reviewed, and is satisfied

with, the summary tables provided by Fortis, comparing the forecast capital additions applied for

in Decision 20497-D01-2016, with the revised forecast capital additions applied for in this

compliance application. Therefore, the Commission is satisfied that Fortis has complied with the

directions set out at paragraphs 357, 397, 419 and 421 of Decision 20497-D01-2016.

4 Resulting 2014 actual and 2016, 2017 forecast K factor amounts

43. In Decision 20497-D01-2016, the Commission determined that all of Fortis’ projects or

programs proposed for capital tracker treatment in 2014 on an actual basis and in 2016-2017 on a

forecast basis satisfied the requirements of Criterion 2.15

44. Additionally, in Decision 20497-D01-2016, based on the project assessment under

Criterion 1, the Commission approved the need for each project or program that Fortis proposed

for capital tracker treatment, either on an actual basis for 2014 or on a forecast basis for 2016 or

2017. The Commission also confirmed the prudence of actual capital additions for the true-up of

each of the capital tracker projects or programs in 2014 and the reasonableness of Fortis’ forecast

capital expenditures for the proposed 2016-2017 capital tracker projects, subject to the

adjustments and Commission directions to be addressed in this compliance filing. At the same

time, because these adjustments would affect actual 2014 costs and/or forecast 2016 or 2017

costs for all projects or programs, the Commission indicated it could not make a determination in

that decision as to whether any of Fortis’ projects or programs proposed for capital tracker

treatment in 2014 on an actual basis, and in 2016 and 2017 on a forecast basis, satisfy the project

assessment requirement of Criterion 1.16

45. Further, the Commission found the general form of Fortis’ accounting test model to be

reasonable and consistent with the methodology approved in Decision 2013-435.17 However,

because Fortis’ accounting test for each of 2014, 2016 and 2017 had to be revised, the

Commission could not make a determination in that decision as to whether any of Fortis’

projects or programs proposed for capital tracker treatment in 2014 on an actual basis, and in

2016 and 2017 on a forecast basis, satisfied the accounting test requirement of Criterion 1 and

accordingly, whether any of Fortis’ projects or programs satisfied Criterion 1 in its entirety.18

Similarly, the Commission indicated that it could not determine in that decision whether any of

Fortis’ projects or programs proposed for capital tracker treatment in 2014 on an actual basis and

in 2016-2017 on a forecast basis satisfied the materiality test requirement of Criterion 3.19

15

Decision 20497-D01-2016, paragraph 407. 16

Decision 20497-D01-2016, paragraphs 393-394. 17

Decision 2013-435: Distribution Performance-Based Regulation, 2013 Capital Tracker Applications,

Proceeding 2131, Application 1608827-1, December 6, 2013. 18

Decision 20497-D01-2016, paragraphs 395-396. 19

Decision 20497-D01-2016, paragraph 420.

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

Decision 21520-D01-2016 (September 15, 2016) • 9

46. As a result of complying with the Commission’s directions from Decision 20497-D01-

2016, Fortis recalculated the actual K factor for 2014, as well as the forecast K factors for 2016

and 2017. A comparison of the 2014 actual, 2016 and 2017 forecast K factor revenue, by capital

tracker, as applied for in Proceeding 20497 and as updated for compliance with the

Commission’s directions, including revised project and program groupings, is shown in Table 2

below.

Table 2. Capital trackers K factor revenue

2014 2016 2017

Applied

for

Per compliance

filing Applied

for

Per compliance

filing Applied

for

Per compliance

filing

($ million)

Customer Growth program* 13.6 13.3 28.0 26.5 32.5 31.5

AESO Contributions program 10.4 10.0 14.9 15.9 20.9 22.1

Substation Associated Upgrades program 3.9 3.7 6.1 6.1 7.9 7.9

Distribution Line Moves program* 1.3 1.4 3.5 3.2 4.0 3.7

Urgent Repairs 1.1 2.6 3.1

Worst Performing Feeders program 0.4 1.1 1.4

Compliance, Safety, Aging Facilities, and Reliability program

0.7 1.8 2.3

Urgent Repairs, WPF, CSAR 2.1 5.3 6.8

Distribution Capacity Increases program

0.9 0.8 1.4 1.4

Metering Unmetered Oilfield Services project 0.4 1.6 2.5

Pole Management program 1.7 1.6 7.1 6.9 9.1 9.0

Cable Management program 0.4 0.3 1.4 1.4 2.0 2.0

Distribution Control Centre/SCADA project 4.0 4.3 2.4 4.9 2.7 5.0

Total 38.0 36.6 71.5 70.9 89.9 89.5

* Net of contributions.

47. Fortis prepared a summary of the impacts of the directions on the capital tracker revenue

for 2014, 2016 and 2017, which is reproduced in Table 3 below.

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

10 • Decision 21520-D01-2016 (September 15, 2016)

Table 3. Summary of impacts K factor revenue

2014 actual

2016 forecast

2017 forecast

($ million)

Capital trackers per 2014 true-up and 2016-2017 capital tracker application 38.0 71.5 89.9

Directions:

2. Combine Automated Meter, Metering Unmetered Oilfield Services, Metering and Other programs

(0.4) (1.6) (2.5)

3. Combine CSAR, Worst Performing Feeders, Urgent Repairs programs - - -

4. Reverse depreciation technical update, excluding DCC/SCADA - (0.6) (0.7)

8. Reverse depreciation technical update for DCC/SCADA - 0.7 0.6

9. Update I-X index and Q factors - 1.0 2.1

10. Use forecast allocation method for actual additional allocated amounts (1.0)

Capital trackers per 2014 true-up and 2016-2017 capital tracker compliance filing

36.6 70.9 89.5

48. Fortis submitted that the Commission in Decision 20497-D01-2016 approved additional

amounts for 2013 related to capitalized overhead, the Worst Performing Feeders program and

line rebuilds associated with the Pole Management program, and the related additional K factor

revenue for 2013 of $0.3 million. Fortis indicated that the collection of this amount will be

included in Fortis’ 2017 annual PBR rates application.20

Commission findings

49. In previous sections of this decision, the Commission determined that Fortis complied

with all but one of the directions set out in Decision 20497-D01-2016. Based on the

Commission’s review of Fortis’ proposed capital tracker projects or programs in Decision

20497-D01-2016, and its acceptance of the compliance application calculations, the Commission

finds the revised actual capital additions in 2014 to be prudent and forecast capital additions in

2016 and 2017 to be reasonable for each capital tracker project or program proposed by Fortis.

The Commission also finds the resulting K factor calculations for 2014, 2016 and 2017, as

provided in the compliance application, to be reasonable. Accordingly, the Commission finds

that all of Fortis’ projects or programs proposed for capital tracker treatment for each of 2014,

2016 and 2017, as shown in Table 2 above, satisfy the requirements of the first and third criteria

for capital tracker treatment. Capital tracker treatment for these projects or programs is approved.

50. In light of the above consideration, the Commission approves on an actual basis, the 2013

additional K factor revenue of $0.3 million, as applied for in Proceeding 20497, and the 2014

K factor of $36.6 million, as calculated in the compliance application. The 2016 and 2017

K factors of $70.9 million and $89.5 million, respectively, calculated in this compliance

application, are approved on a forecast basis.

5 Remaining Commission direction from Decision 20497-D01-2016

51. Direction 14 related to filing the compliance application on or before April 14, 2016. By

letter dated February 24, 2016, Fortis requested an extension to the deadline for filing the

20

Exhibit 21520-X0009, application, paragraph 4.

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

Decision 21520-D01-2016 (September 15, 2016) • 11

compliance application from April 1, 2016 to April 15, 2016. The Commission granted the

requested extension. Accordingly, the Commission finds that Fortis complied with this direction.

52. Fortis confirmed that it will address the requirements in paragraph 240 of Decision

20497-D01-2016 (Direction 7), the only remaining direction, in a future filing as contemplated

by the Commission.21 Fortis is directed to address the remaining Commission direction from

Decision 206497-D01-2016 in a subsequent capital tracker application.

6 Order

53. It is hereby ordered that:

(1) The 2013 additional actual K factor revenue of $0.3 million is approved.

(2) The 2014 actual K factor of $36.6 million is approved.

(3) The 2016 and 2017 K factors of $70.9 million and $89.9 million, respectively, are

approved on a forecast basis.

Dated on September 15, 2016.

Alberta Utilities Commission

(original signed by)

Anne Michaud

Commission Member

21

Exhibit 21520-X0009, application, paragraph 9 and Exhibit 21520-X0008, Appendix A, Commission

Directions to FortisAlberta.

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

Decision 21520-D01-2016 (September 15, 2016) • 13

Appendix 1 – Proceeding participants

Name of organization (abbreviation) Company name of counsel or representative

FortisAlberta Inc.

Consumers’ Coalition of Alberta (CCA)

Alberta Utilities Commission Commission panel A. Michaud, Commission Member

Commission staff

J. Graham (Commission counsel) G. Nadeau P. Genderka C. Runge E. Deryabina

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

14 • Decision 21520-D01-2016 (September 15, 2016)

Appendix 2 – Commission directions addressed in the compliance filing

Note: The list below includes all Commission directions from Decision 20497-D01-2016

relevant to this compliance filing and for future capital tracker applications.

Fortis addressed in the compliance filing Commission directions 2-6, 8-14, relevant to this

compliance filing,22 and will address the remaining Commission directions 1 and 7 from

Decision 20497-D01-2016, in future filings.23

Decision 20497-D01-

2016 reference Direction

Application reference

Exhibit 21520-X0009

1 Paragraph 60

Similarly, the Commission does not accept, as an adequate justification for its Metering Unmetered Oilfield Services project grouping, Fortis’ explanation that efficiencies arise in the design and construction of each of these projects when the work is completed together. Again, this is owing to the fact that grouping is an accounting exercise. However, the costs of three-wire to four-wire conversions and the costs of adding meters to the unmetered oilfield services have not historically been tracked separately. Therefore, for simplicity, the Commission will not require Fortis to disaggregate this project at this time. The inclusion of the three-wire to four-wire conversions in the Metering Unmetered Oilfield Services project is approved for the purposes of the first PBR term. However, separately tracked data may be relevant to future Commission consideration of this issue. As such, the Commission directs Fortis to track the costs of three-wire to four-wire conversions and the costs of adding meters to the unmetered oilfield services separately going forward.

Paragraph 11

2 Paragraph 61

The Commission considers that the purpose of the Automated Meter project, Metering Unmetered Oilfield Services project, and the Metering and Other program is the replacement, repair, and installation of meters. The programs are similar in nature and have a common requirement for capital investment. The Commission does not consider the Automated Meter project and Metering Unmetered Oilfield Services project to be sufficiently unique and substantial so as to merit separate capital tracker groups. The Commission directs Fortis to group these three programs together for the purposes of the compliance filing and its future capital tracker applications.

Paragraph 12

3 Paragraph 62

The Commission considers that while each of the CSAR, Worst Performing Feeders, and Urgent Repairs programs has a different process to identify the work, the work completed under each program is similar in function. Furthermore, all three programs share a common requirement for capital investment. The Commission, therefore, directs Fortis to group these three programs together for the purposes of the compliance filing and its future capital tracker applications.

Paragraph 14

22

Exhibit 21520-X0008, Appendix A. 23

Exhibit 21520-X0009, application, page 3.

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

Decision 21520-D01-2016 (September 15, 2016) • 15

Decision 20497-D01-

2016 reference Direction

Application reference

Exhibit 21520-X0009

4 Paragraph 143

For the above reasons, the Commission finds that the determinations made in paragraph 688 of Decision 2012-237 also apply to K factors. Given that Fortis’ depreciation technical update proposal is contrary to the Commission’s determinations found in paragraph 688 of Decision 2012-237, Fortis’ application to change existing depreciation rates for all project groupings through the K factor calculation associated with the deprecation technical update is denied. In the compliance filing to this decision, Fortis is directed to remove the updated depreciation amounts from the K factor calculation and base its revenue requirement calculation associated with all project groupings on the amounts reflective of the depreciation rates approved in the company’s last depreciation study using plant balances as of December 2010.

Paragraph 16

5 Paragraph 181

As shown in Table 1 of this decision, the 2013 K factor for the Customer Growth Program results in a positive variance of $0.1 million. The Commission notes that half of the variance is caused by rounding. Fortis is directed to use the correct number in the compliance filing and going forward in the accounting test.

Paragraph 20

6 Paragraph 205

As shown in Table 1 of this decision, the 2013 K factor results in a positive variance of $0.1 million. The Commission notes that half of the variance is caused by rounding. Fortis is directed to use the correct number in the compliance filing and going forward in the accounting test.

Paragraph 20

7 Paragraph 240

With respect to the UCA’s concerns regarding the proposed formula, the Commission finds that the individual components within the formula, and the calculation of the different components in utilizing this formula to be reasonable. Accordingly, the updated forecasting methodology for the Pole Management program, including the line-rebuilds formula, is approved as filed. Based on the forecasting changes identified by Fortis, the Commission accepts the total annual forecast costs. In the true-up application, the Commission expects that Fortis will provide individual projects details for line-rebuild projects, similar to what was provided for the 2014 line-rebuild projects. As actual unit costs will not be provided since Fortis does not track actual unit costs, the Commission continues to direct Fortis to provide information detailing project descriptions, project scope documents for projects over $300,000 and other relevant information necessary to support the timing, level, scope and costs of the individual line-rebuild projects.

Not addressed in the application.

8 Paragraph 291

The Commission is satisfied that the revenue requirement variance is acceptable and can be included in the revenue requirement calculation for the DCC/SCADA project. However, as discussed in Section 6.1.4, the Commission is not allowing changes to depreciation rates stemming from the depreciation technical update and Fortis is directed in the compliance filing to change all depreciation calculations within the application using the originally approved depreciation rates including those calculations for the DCC/SCADA project, if applicable.

Paragraph 17

9 Paragraph 357

Regarding the 2016 forecast, the Commission observes that, since the filing of the application, the 2016 I-X index of 0.90 per cent and billing determinants forecast were approved in Decision 20818-D01-2015. To minimize future true-ups, the Commission directs Fortis, in its compliance filing to this decision, to use the approved 2016 I-X index value and the Q factor based on the forecast billing determinants approved in Decision 20818-D01-2015 for purposes of its 2016 and 2017 capital tracker forecast accounting test.

Paragraph 22

10 Paragraph 391

Accordingly, the Commission does not approve the true-up year allocation methodology used by Fortis for 2014. In its compliance filing, Fortis is directed to use the same allocation methodology for the allocation of additional amounts of revenue requirement in the true-up for 2014 that is used in forecast years.

Paragraph 18

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

16 • Decision 21520-D01-2016 (September 15, 2016)

Decision 20497-D01-

2016 reference Direction

Application reference

Exhibit 21520-X0009

11 Paragraph 397

The Commission directs Fortis, in its compliance filing to this decision, to revise its accounting test for 2014, as well as for 2016-2017, based on approved final forecast or actual capital additions, the 2016 model assumptions and other directions as set out in the previous sections of this decision. Fortis is further directed to provide two summary tables in the compliance filing to this decision. The first table should include for each capital tracker project or program, a comparison of the 2014 actual capital additions applied for in this proceeding and the 2014 actual capital additions, revised in accordance with the directions set out in this decision. The second table should provide a similar comparison for the forecast 2016 and 2017 capital trackers.

Paragraphs 24-25

12 Paragraph 419

However, since the filing of the application, the 2016 I-X index of 0.90 per cent has been approved in Decision 20818-D01-2015. Consistent with the findings in Section 7.1, to minimize future true-ups, the Commission directs Fortis, in its compliance filing to this decision, to use the approved 2016 I-X index value of 0.90 per cent to calculate the first and second tier materiality thresholds for 2016 and 2017.

Paragraphs 27-28

13 Paragraph 421

Given these findings, the Commission directs Fortis, in its compliance filing to this decision, to reassess whether its projects or programs proposed for capital tracker treatment in 2014 on an actual basis and in 2016-2017 on a forecast basis, satisfy the two-tiered materiality test requirement of Criterion 3. For this reassessment, Fortis will use the approved 2014 threshold amount, as well as revised 2016 threshold amounts, as directed above.

Paragraphs 27-28

14 Paragraph 439

(1) FortisAlberta Inc. is directed to file a compliance filing application in accordance with the directions contained within this decision on April 1, 2016.

Paragraph 2

2014 True-Up and 2016-2017 Forecast PBR Capital Tracker Compliance Filing FortisAlberta Inc.

Decision 21520-D01-2016 (September 15, 2016) • 17

Appendix 3 – Summary of Commission directions

This section is provided for the convenience of readers. In the event of any difference between

the directions in this section and those in the main body of the decision, the wording in the main

body of the decision shall prevail.

1. In this decision the Alberta Utilities Commission determines FortisAlberta Inc.’s

compliance with the Commission’s directions issued in Decision 20497-D01-2016. For

the reasons outlined in this decision, the Commission finds that Fortis has complied with

all but one of the Commission’s directions in Decision 20497-D01-2016 that are relevant

to the compliance application, and directs Fortis to comply with the outstanding direction

as soon as practicable. The Commission approves Fortis’ 2013 additional K factor

revenue as well as the 2014, 2016 and 2017 K factor revenue amounts as applied-for in

the application. .................................................................................................. Paragraph 1

2. The Commission directs Fortis to track the costs of three-wire to four-wire conversions

and the costs of adding meters to the unmetered oilfield services separately as soon as

practicable following the release of this decision, and until this program is complete.

.......................................................................................................................... Paragraph 14

3. Fortis confirmed that it will address the requirements in paragraph 240 of Decision

20497-D01-2016 (Direction 7), the only remaining direction, in a future filing as

contemplated by the Commission. Fortis is directed to address the remaining Commission

direction from Decision 206497-D01-2016 in a subsequent capital tracker application.

.......................................................................................................................... Paragraph 52