debt-to-income ratios on va loans

TRANSCRIPT

RATIOS ON VA LOANSDEBT-TO-INCOME

The United States of America appreciates all those serving and who have served in the armed forces.

They are honored in parades and patriotic ceremonies. And “Thank you for your service” is a common sentiment expressed towards veterans.

But it’s always meaningful to receive more tangible recognition. To this end, the U.S. Department of Veterans Affairs guarantees home loans for qualified veterans.

In so doing, the government makes financing a home easier and more affordable for those who have served.

A significant attraction of VA loans is the debt-to-income ratio threshold. It is higher than would be acceptable in a conventional mortgage.

THE CREDIT PROCESS

Mortgage loan underwriters look at several variables before approving a loan application. For one thing, they want to know how much equity the applicant will have in the house.

They measure the loan amount against the appraised worth of the property. This calculation is called the loan-to-value ratio.

Another area of interest is credit rating. Does the prospective borrower have a history of paying bills on time?

By the same token, lenders want to be reasonably sure that loan applicants will continue to make timely payments.

Therefore, a determination is made as to whether the loan is affordable. This assessment is made by means of a debt-to-income ratio (DTI).

LOAN DEBT SERVICE

Credit analysts at banks and finance companies take a hard look at monthly payments reflected on a credit report (e.g. credit cards, student loans, cell phones, cable TV).

These payments are combined with the calculated monthly payment for the home loan. This total often includes escrows for taxes and insurance.

The monthly burden is weighed against monthly revenue from employment, investments and earned interest for example. These figures create a debt-to-income ratio.

If the figure falls outside a given range, whereby the debt is too high or the income is too low, the bank may reject the application because the loan payments are not affordable.

Even if past credit history is sterling, this ratio can kill an otherwise strong application.

WHAT MAKES A VA LOAN DIFFERENT?

Since the Dept. of Veterans Affairs guarantees these loans, that is, promises to pay them off in the event of default, banks and other lenders are more flexible with approval standards.

Borrowers can get by with less (or even zero) equity, for example, than would be demanded in a conventional loan.

Credit scores need not be as high. Most significantly the standard DTI ratio is 36% for a conventional loan whereas it is 41% for a VA loan.

Hence, a VA borrower can have up to 41% of gross income consumed by monthly obligations. This is an easier benchmark to meet.

Furthermore, if residual or tax-free incomes make up an appreciable amount of the gross, lenders have some flexibility to raise the DTI by a few points.

Many veterans still choose conventional loans to finance their houses. However, when budgets are tight and expenses are high, they do have the VA loan option.

It provides a little more financial breathing room to pursue the American dream which vets have certainly earned.

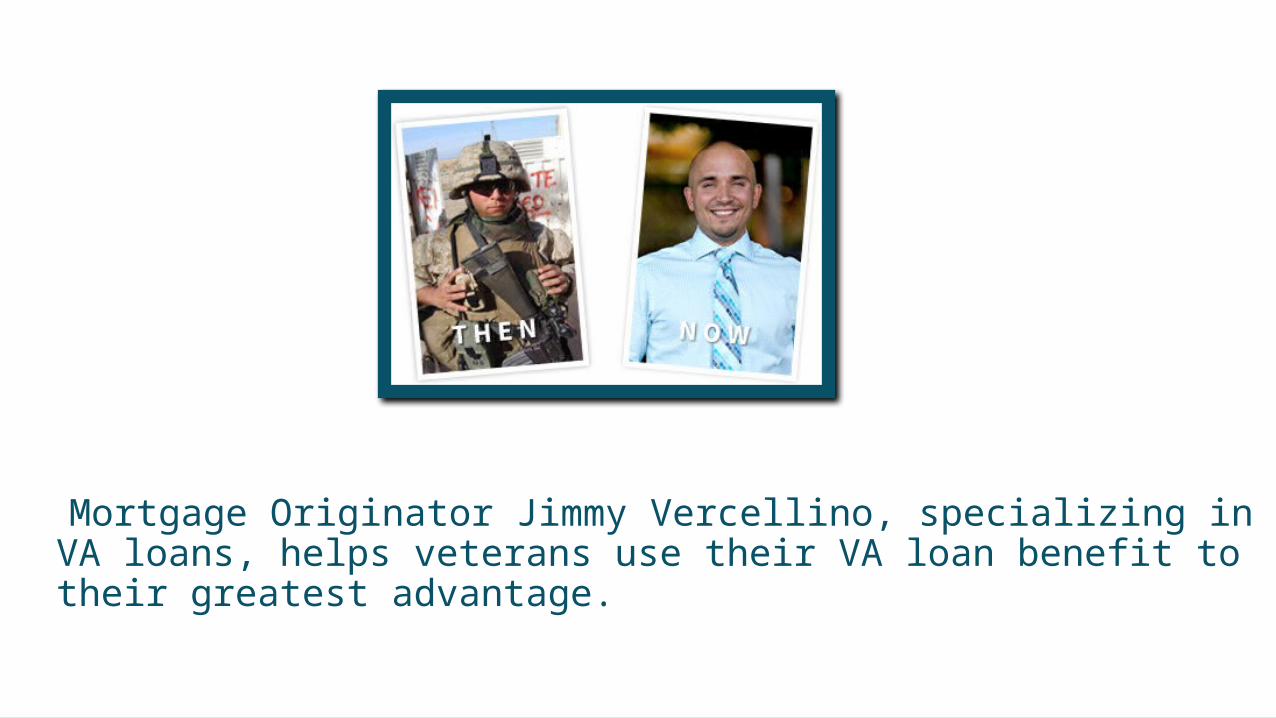

Mortgage Originator Jimmy Vercellino, specializing in VA loans, helps veterans use their VA loan benefit to their greatest advantage.

For more details call 480-351-5904. Visit the site at www.valoansforvets.com

VA LOANS FOR VETS7600 E. Doubletree Ranch Road #200Scottsdale, AZ 85258Phone: (480) 351-5904Email: [email protected]