debt collection and scra instructor: assistant instructor:

TRANSCRIPT

Debt Collection and SCRA

Instructor:

Assistant Instructor:

3

Federal Trade Commission

The Federal Trade Commission (FTC) enforces the Fair Debt Collection Practices Act ("Act"). It

prohibits unfair, deceptive, and abusive debt collection practices by collection agencies and

other third-party debt collectors. It also gives you certain rights when you are being treated

improperly by a debt collector.

4

The Act generally does not cover either the collection of commercial debts or the collection activities of the party to whom you allegedly owe your debt (the creditor).

Fair Debt Collection Practices Act

5

Fair Debt Collection Practices Act

The Act applies only to third-party debt collectors collecting consumer debts.

6

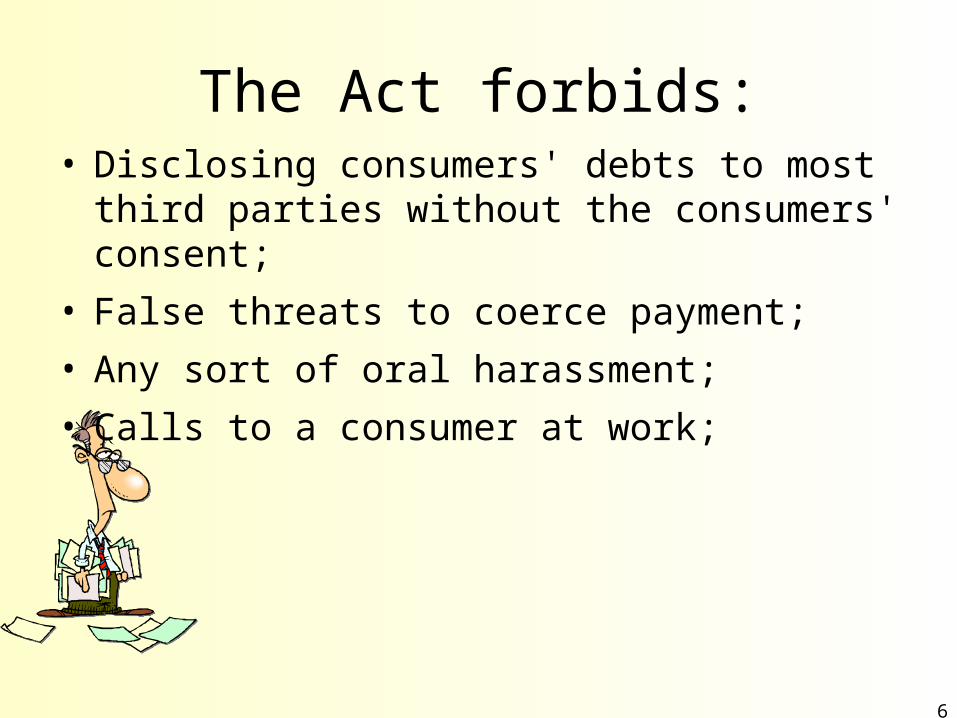

The Act forbids:• Disclosing consumers' debts to most third

parties without the consumers' consent;

• False threats to coerce payment;

• Any sort of oral harassment;

• Calls to a consumer at work;

7

The Act forbids:

• Calls made very early in the morning or late at night;

• Charges may not be added to the debt

• no suits against a consumer by a debt collector may be filed outside the district:

• (1) of the consumer's residence or (2) where the contract creating the debt was signed.

8

If you believe that you do not owe the debt, you may file a dispute with the debt collector (in writing).

9

If you believe that the debt collector who is contacting you violated the law in this or any other way, you may:

1. File a complaint online with the FTC, or with your state or local consumer protection office and/or the party to whom you originally owed the debt (the debt collector's client).

2. File a private suit against the debt collector for violating the Act.

10

Remember that the Act does not erase a valid debt, even if a debt collector has violated the law in attempting to collect it from you.

11

Debt Collectors

Remember also that some collection techniques, while unpleasant or distasteful, are not law violations. A debt collector may: 1. Contact third parties solely to determine where you are, so long as

the collector does not disclose the existence of your debt.

2. Contact you at work if the debt collector has no reason to believe that your employer prohibits the contact (and you have not filed a cease-communication request).

12

3. Use a rude or angry tone on the telephone, if the overall communication with you cannot truly be characterized as abusive or harassing.

4. Threaten consequences of non-payment that are truthful.

5. Accept or solicit a post-dated check, if the collector does not deposit it before the date on the check.

6. Refuse to accept a partial payment for a debt (even if you had such an arrangement with the creditor). If there is more than one debt, the collector must credit the account that you designate.

Debt Collectors

13

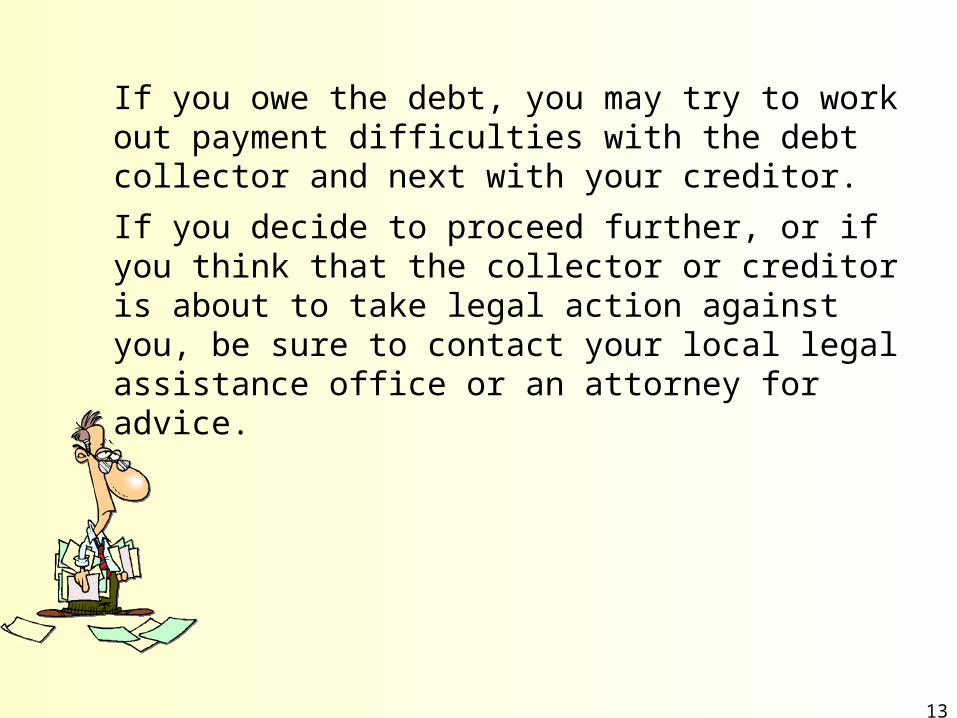

If you owe the debt, you may try to work out payment difficulties with the debt collector and next with your creditor.

If you decide to proceed further, or if you think that the collector or creditor is about to take legal action against you, be sure to contact your local legal assistance office or an attorney for advice.

14

Servicemembers Civil Relief Act (SCRA)

A federal law that gives all military members some important rights as they

enter active duty.

15

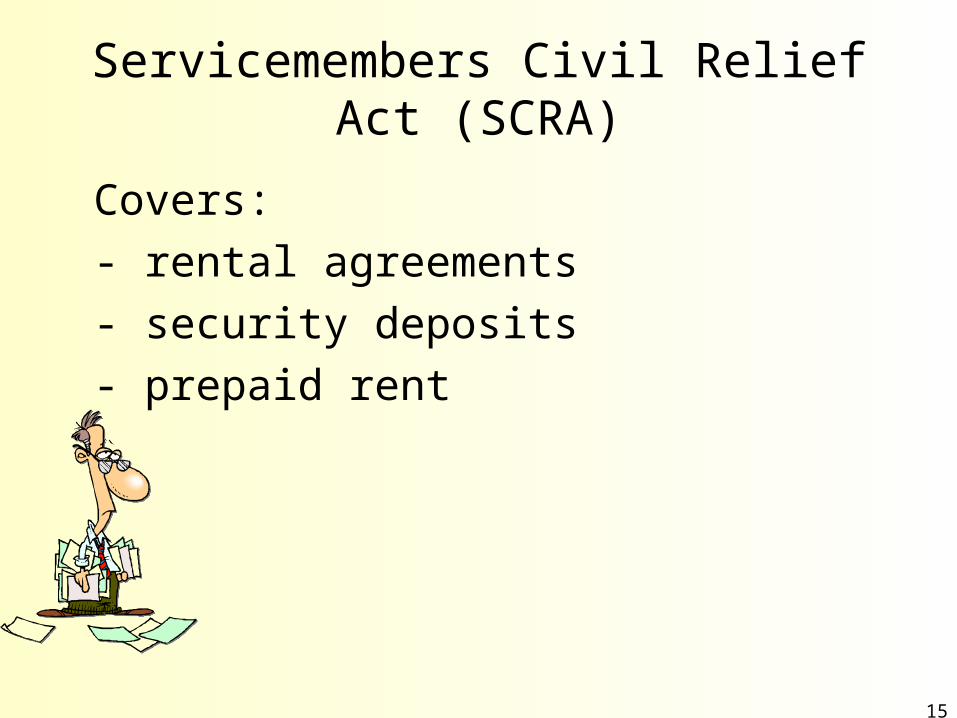

Servicemembers Civil Relief Act (SCRA)

Covers:

- rental agreements

- security deposits

- prepaid rent

16

- eviction

- installment contracts

- credit card interest rates

- mortgage interest rates

- mortgage foreclosure

Servicemembers Civil Relief Act (SCRA)

17

- civil judicial proceedings

- income tax payments

It also provides many important protections to military members while on

active duty.

Servicemembers Civil Relief Act (SCRA)

18

The SCRA protects active duty military members and reservists or members of the National Guard called to active duty

(starting on the date active duty orders are received) and, in limited situations,

dependents of military members (e.g., certain eviction actions).

19

To receive protection under some parts of the SCRA, the member must be prepared to show that military service has had a "material effect" on the legal or financial matter involved.

20

Protection under SCRA must be requested during the member's military duty or within 30 to 180 days after military service ends, depending on the protection being requested.

21

The Six Percent Rule

Three months ago Mr. Smith and his wife bought a car for $13,000, paying $1,000 down and financing $12,000 at 9% interest. Last week, Mr. Smith was called to active duty as Staff Sergeant (SSG) Smith. Before entering active duty Mr. Smith earned $42,000 per year. As a staff sergeant he now earns almost $27,000 (a staff sergeant with over 12 years of military service from Defense Finance & Accounting Service pay scale. Because of the SCRA, SSG Smith may ask the car financing company to lower the interest rate to 6% while he is on active duty -- military service has materially affected his ability to pay since he is earning less money on active duty than before.

22

SSG Smith should inform the finance company of his situation in writing with a copy of the orders to active duty attached, and request immediate confirmation that they have lowered his interest rate to 6% under the SCRA. The finance company must adjust the interest down to 6% unless it goes to court. In court, the finance company, not SSG Smith, would have to prove that SSG Smith's ability to pay the loan has not been materially affected by his military service.

The Six Percent Rule

23

The 3% difference is forgiven or excused, and SSG Smith need not pay that amount. SSG Smith does need to continue making the monthly payments of principal and interest (at 6%) to avoid his account being considered delinquent. Continuing payments should also avoid any adverse credit reports from the finance company. (See Section 207, SCRA)

The Six Percent Rule

24

SCRA permits active duty servicemembers, who are unable to appear in a court or administrative proceeding due to their military duties, to postpone the proceeding for a mandatory minimum of ninety days upon the servicemember's request.

25

SCRA allows termination of leases by active duty servicemembers who subsequently receive orders for a permanent change of station (PCS) or a deployment for a period of 90 days or more. The SCRA also includes automobiles leased for personal or business use by servicemembers and their dependents.

26

The SCRA does not excuse soldiers from paying rent, it does afford some relief if military service makes payment difficult. Military members and their dependents (in their own right) have some protection from eviction under the Servicemembers Civil Relief Act (SCRA), Section 301.

27

If a default judgment is entered against a servicemember during his or her active duty service, or within 60 days thereafter, the SCRA allows the service member to reopen that default judgment and set it aside.

28

The SCRA also permits the servicemember to request deferment of certain commercial life insurance premiums and other payments for the period of military service and two years thereafter.

29

The SCRA provides that a nonresident servicemember's military income and personal property are not subject to state taxation if the servicemember is present in the state only due to military orders.

30

The SCRA further provides for the reinstatement of any health insurance upon termination or release from service. The insurance must have been in effect before such service commenced and terminated during the period of military service.

31

QUESTIONS?QUESTIONS?