dealing with shrinking resources presented by: nicholas a. pittner, esq. bricker & eckler llp...

TRANSCRIPT

Dealing with Shrinking Resources

Presented by:

Nicholas A. Pittner, Esq.Bricker & Eckler LLP

January 5, 2012

BASA and Bricker & Eckler Present:

Overview

• Three factors dominate education-related provisions of the budget bill:

– Overall reduction in operating funds for schools.

– Increased measurement and comparison of schools.

– Continued shift in priority away from the “common school” concept embodied in the Ohio Constitution.

School Funding

• Loss of federal stimulus money.

• Evidence-Based Model repealed.

School Funding

• State foundation support based on a distribution formula – not a funding formula.

– New charge-off calculation based on statewide median per-pupil amount.

– Individual school districts adjusted up or down based on median.

– Other adjustments keep distributions within overall appropriations.

School Funding

• “Bridge Formula.”

– Contemplates the possibility of a new funding formula this biennium.

– Adjusted to ensure that each district will not receive less in state support (but excluding SFSF funding) than was received for FY 2011.

• $17 per pupil to the “Excellent” or “Excellent with Distinction” districts.

School Funding

• TPP reimbursement loss – the largest state revenue reduction feature.

– Fixed-rate operating levy losses eliminated if reimbursement is 2% or less of district total revenue for FY 12 and 4% for FY 13.

– Tangible personal and public utility personal property reimbursements are calculated separately.

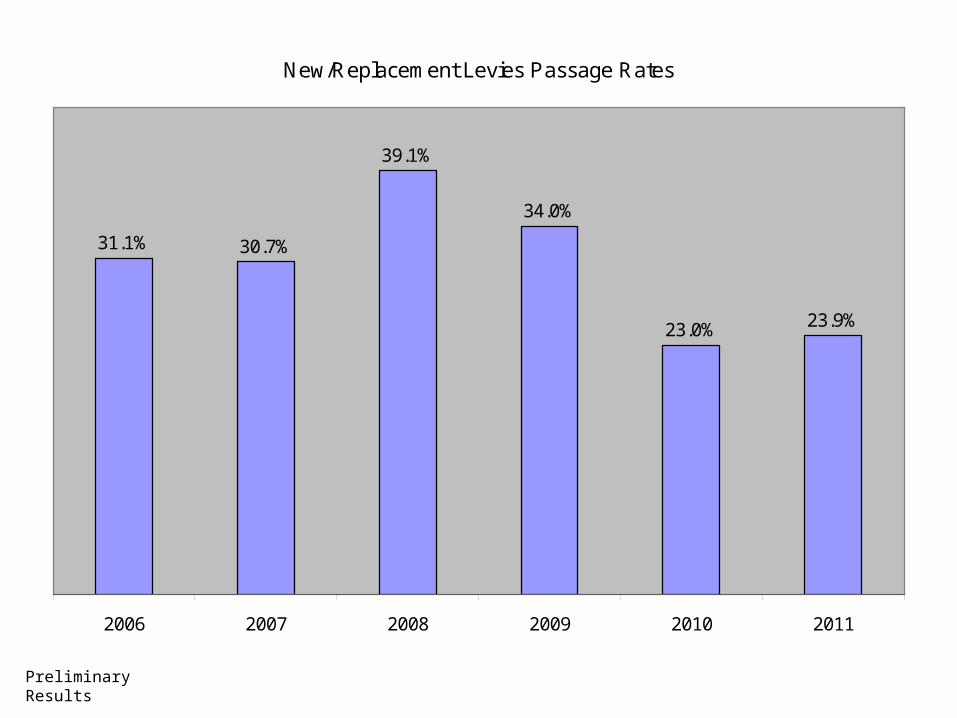

School Levies

• Nov. 2011 Election Results– Approx. 24% of new/replacement levies

passed.– 89% of renewal levies passed.

Preliminary Results

New/Replacement Levies Passage Rates

31.1% 30.7%

39.1%

34.0%

23.0% 23.9%

2006 2007 2008 2009 2010 2011

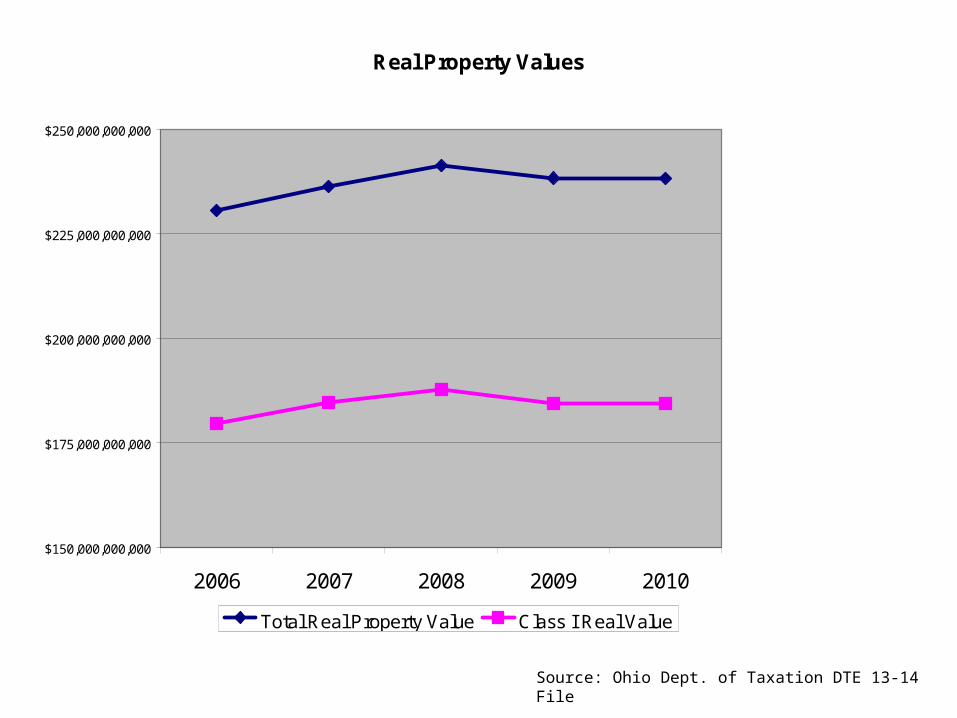

Local Revenue

• Pressure on local revenue sources.

1. Tentative Abstract Results for Residential Property• 2011 Reappraisal Counties Average Tentative

Change: -4.2%• 2011 Update Counties Average Tentative

Change: -6.33%

Real Property Values

$150,000,000,000

$175,000,000,000

$200,000,000,000

$225,000,000,000

$250,000,000,000

2006 2007 2008 2009 2010

Total Real Property Value Class I Real Value

Source: Ohio Dept. of Taxation DTE 13-14 File

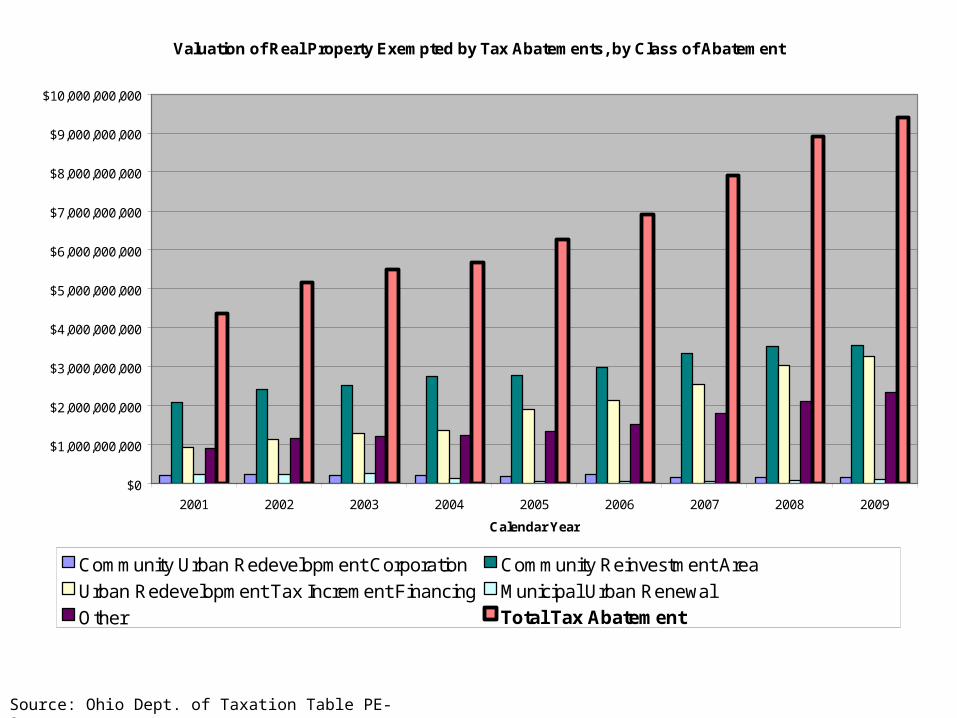

Source: Ohio Dept. of Taxation Table PE-3

Valuation of Real Property Exempted by Tax Abatements, by Class of Abatement

$0

$1,000,000,000

$2,000,000,000

$3,000,000,000

$4,000,000,000

$5,000,000,000

$6,000,000,000

$7,000,000,000

$8,000,000,000

$9,000,000,000

$10,000,000,000

2001 2002 2003 2004 2005 2006 2007 2008 2009

Calendar Year

Community Urban Redevelopment Corporation Community Reinvestment Area

Urban Redevelopment Tax Increment Financing Municipal Urban Renewal

Other Total Tax Abatement

Ohio Income Tax Collections

0

2,000,000,000

4,000,000,000

6,000,000,000

8,000,000,000

10,000,000,000

12,000,000,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Fiscal Year

Source: Ohio Dept. of Taxation Table TS-7 (Oct. 5, 2011)

Average Federal Adjusted Gross Incomefrom Ohio Income Tax Returns By School District

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

2003 2004 2005 2006 2007 2008 2009

Source: Ohio Dept. of Taxation Table Y-2

Business Bankruptcy FilingsU.S. Bankruptcy Court (Ohio Northern & Southern Districts)

Cases Commenced, During the 12-Month Period Ending September

0

500

1,000

1,500

2,000

2,500

2006 2007 2008 2009 2010 2011

Source: www.uscourts.gov (bankruptcy statistics)

Source: www.uscourts.gov (bankruptcy statistics)

Non-Business Bankruptcy FilingsU.S. Bankruptcy Court (Ohio Northern & Southern Districts)

Cases Commenced, During the 12-Month Period Ending September

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2006 2007 2008 2009 2010 2011

Total Statewide Delinquent Property TaxesIncludes all property taxes reported as unpaid in a calendar year, including taxes that became

delinquent in preceding years which were still unpaid.

$0

$500,000,000

$1,000,000,000

$1,500,000,000

$2,000,000,000

$2,500,000,000

2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Ohio Dept. of Taxation Table TD-1

Oct. 2011 Five Year ForecastLine 12.01

% of Districts Projecting Deficit

1.8% 3.1%

14.9%

34.5%

58.8%

75.3%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

2011 Actual 2012 2013 2014 2015 2016

School Funding

• Local Revenue Issues:

– Declining property values trigger (a) increases in effective tax rates for rate-based levies, (b) increased levy rates for emergency levies and (c) loss of revenue from inside millage.

School Funding

– New rate-based levies will apply to taxable property values without adjustment until inflation-based increases in property values are made.

– Declining levels of personal income will affect many districts as well.

School Funding

• Other School Finance Changes:

– Alternate fund certification available if non-salary and multi-year savings can be demonstrated.

– Transfer of unneeded funds from bond and bond retirement accounts to permanent improvement funds made easier by shifting approval authority to the county budget commission.

School Funding

– Income tax and property tax levy – now available as a single ballot issue.

– Expanded borrowing authority for special needs districts.

Ten (and a few more) Things For Consideration

Revenue Enhancement

– Consider the creation of a county school financing district.

I. County School Financing District

• An ESC may create a county school financing district to include:– the territory of local school districts within the

ESC that do not opt out, and

– other school districts that opt into the county school financing district.

County School Financing District

• County school financing districts are authorized to propose the passage of property tax levies for a broad range of school purposes. In addition, county school financing districts can form the basis for the formation of cooperative education school districts. R.C. 3311.50, 3311.51 and 3311.52.

County School Financing District

• Advantages: – Separate taxing entity, apart from the

members of the CSFD.– Public support for special education

programs.– Wide area = large tax duplicate = lower tax

rates.

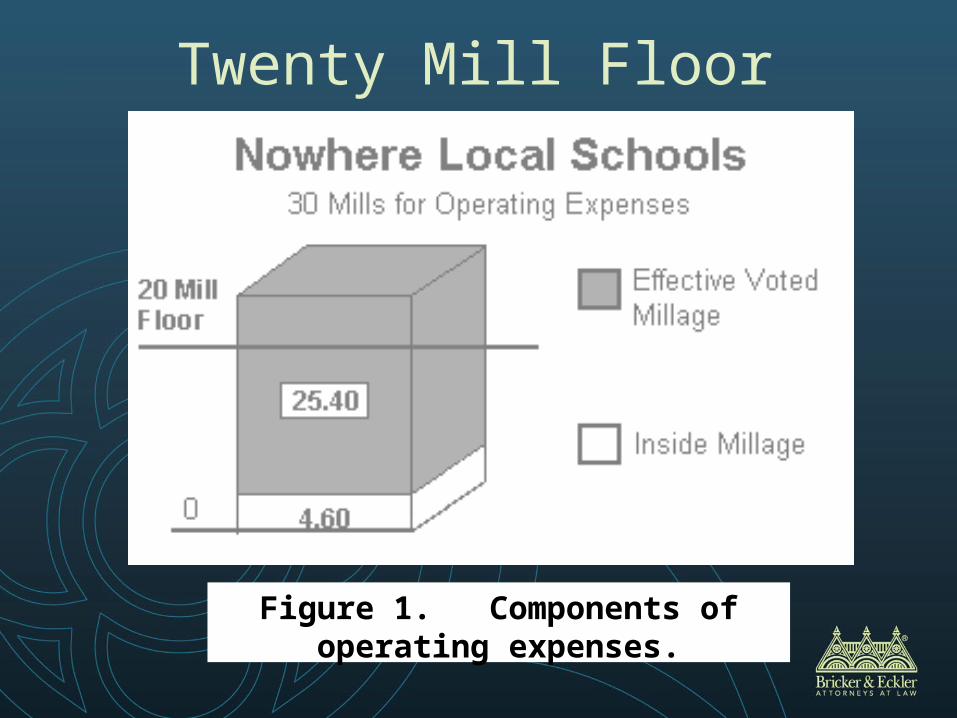

II. For 20 Mill Districts

• Consider the transfer of inside millage from a general fund levy to a permanent improvement or bond retirement levy.

• How it works:

Figure 1. Components of operating expenses.

Twenty Mill Floor

Figure 2. Tax reduction factors reduce the effective voted millage below the twenty mill floor.

Twenty Mill Floor

Figure 3. Effective millage is increased to meet twenty mill floor.

Twenty Mill Floor

Figure 4. Reallocating one unvoted mill to a permanent improvement fund causes the effective voted millage to be

increased by one mill.

Twenty Mill Floor

III. Consider the Creation of a School Support Foundation

Educational Foundations Q & A

• What is an Educational Foundation?– A school support organization that may take

one of several different forms.

• What can it do for my district?– Primary goal is fund raising for board

programs.– Note that board employees cannot be paid

from an independent source for performing board work. (Ohio Ethics Commission 2008-01)

Educational Foundations

• Other benefits include: – identifying a pool of competent volunteers

(future board members),– improved school-community relations, and – improved school performance.

Educational Foundations

• What are the various kinds of school foundation structures?– Board-controlled donation account.– Independent trust fund.– Board-established education foundation funds

(R.C. 3315.40).– Board-created investment trusts.

Educational Foundations

• Not-For-Profit Corporation: – This consists of a corporation organized under the

laws of Ohio for school support purposes. Governance is generally, but not exclusively, independent of the board of education.

– Three types:• School Board Controlled• Autonomous Board• Embedded Board

IV. Available Reserve Funds?

• H.B. 153 now permits school districts to transfer unneeded reserves in a bond or bond retirement fund to a specified district permanent improvement fund with the approval of the county budget commission. R.C. 5705.14

V. Ohio Medicaid Schools Program

• Funding available for Medicaid-eligible services to qualified special education pupils.

• Ohio Medicaid Schools Program.

VI. Expenditure Reduction Options

• Uniform Salary Reductions.– Lots of hurdles:

• What is a “uniform plan”? • Can city school districts implement uniform

reductions?• Collective bargaining obstacles.

VII. Healthcare – Is Mandatory Pooling in Your Future?

• Healthcare Changes: R.C. 9.901 – School Employees Healthcare Board

eliminated – functions transferred to the department of administrative services (DAS).

– Department of Administrative Services to commission an independent consultant to study existing health plans and report recommendations for a program for pooling purchasing power in the acquisition of employee health care plans. Sixteen separate criteria to be considered.

– Scope: The DAS jurisdiction includes healthcare plans for political subdivisions, public school districts and state institutions of higher education.

Healthcare

VIII. Energy-Related Issues

• Electric utility cost reduction. – Consider the Power4Schools program or

MEC electric utility purchase program for cost reductions.

– Consider Peak Demand Reduction Programs.

IX. Transportation Savings Potential

• Local school districts may again terminate the contracts of transportation employees for reasons of economy. R.C. 3319.0810

• Studies have demonstrated significant potential savings by streamlining intra-district pupil transportation.

X. Shared Services

• Kimball & Becky tell all.

Shared Services / Collaboration

Presented by:

Nicholas A. Pittner, Esq.Bricker & Eckler LLP

January 5, 2012

BASA and Bricker & Eckler Present:

Changes in the Budget Bill (H.B. 153)

• Educational Shared Services Model – Section 267.50.90– The Governor’s Director of 21st Century

Education directed to develop a plan for the integration and consolidation of the publicly supported regional shared services organizations.

– Legislative recommendations due to the Governor and General Assembly not later than Jan. 1, 2012.

Shared Services

• Educational Support organizations to be considered for integration:– Educational service centers– Educational technology centers– Information technology centers– Area media centers– Ohio’s statewide system of support– The education regional service system– Regional advisory boards– Regional staff from the Department of Education

providing direct support to school districts

Shared Services

• Services to be considered for inclusion into the shared services model:

– General instruction– Special education– Gifted education– Academic leadership– Technology– Fiscal management– Transportation

– Food services– Human resources– Employee benefits – Pooled purchasing– Professional

development– Non-instructional

support

Educational Service Centers

• Mandatory ESC Joinder (R.C. 3313.843).– Each city, exempted village, or local school

district with an “average daily student enrollment” of sixteen thousand pupils or less now required to enter into an agreement with the governing board of an ESC for services to the district.

– School districts with an average daily enrollment of more than sixteen thousand pupils may, but are not required to enter into such agreements.

Educational Service Centers

• The services that may be contracted for expanded to include:– “[a]ny other services the district board and

service center governing board agree can be better provided by the service center and are not provided under an agreement entered into under section 3313.845 of the Revised Code.”

Educational Service Centers

– Agreements to be filed with department of education by July 1 of the school year for which the agreement is in effect.

– HB 153 deadlines for terminating agreements modified by HB 157 (effective Dec. 21, 2011).

Educational Service Centers

– ESC agreements may now be terminated by participating boards of education by giving notice to the ESC by March 1, 2012, or by January 1 of any odd-numbered year thereafter. The termination becomes effective on the following June 30.

– If a district board fails to notify an ESC of its intent to terminate an agreement by March 1, 2012 (or by January 1 of any odd-numbered year thereafter), the existing agreement will be renewed.

Educational Service Centers

– If a school district that is required to contract with an ESC terminates an agreement for services, the district must enter into a new agreement with a different ESC that is effective July 1 of that same year.

– A local district that intends to switch to a different ESC in 2012-13 must notify its current ESC by March 1, 2012.

– HB 157 provides that when a local district receives services from a different ESC, the $6.50 per pupil payment will flow to the new ESC (corrects an oversight in HB 153).

Educational Service Centers

• Expanded ESC Contracting Authority.– ESCs are now granted extremely broad

authority to enter into contracts with “any political subdivision” for the delivery of services under terms agreed upon by the ESC and contracting subdivision. Copies of such service contracts must be filed with ODE.

Intergovernmental Contracting

• New R.C. 9.482 (H.B. 153) grants broad contracting authority between and among Ohio’s political subdivisions, including school districts and councils of government made up of school districts.

– Political subdivisions may now “[e]nter into an agreement with another political subdivision whereby a contracting political subdivision agrees to exercise any power, perform any function, or render any service for another contracting recipient political subdivision that the contracting recipient political subdivision is otherwise legally authorized to exercise, perform, or render.”

– Limitations: excludes the levy of any tax, the “exercise of investment powers,” or the performance of any “investment function” by one political subdivision for another.

What Ohio School Districts are Currently Authorized to Do

A. Shared Educational Programs

• Regional Student Education District.– School districts can create a regional student

education district for providing services to autistic and special needs pupils. This authority includes the creation of a separate board of education with separate tax levy authority, but is limited to districts with a majority of their territory lying within counties having a population of one million two hundred thousand (e.g. Cuyahoga). R. C. 3313.83.

A. Shared Educational Programs

• Exchange of Teaching Services.– School districts can exchange teaching

services with other school districts in Ohio, school districts outside the state of Ohio, and school districts outside the United States, and may maintain those teachers on district payroll during the period of sharing. R. C. 3313.84.

A. Shared Educational Programs

• Sharing of Supervisory, Special Instruction and Special Education Teachers.– School districts can, by agreement, share the

services of supervisory, special instruction and special education teachers, as well as other licensed personnel necessary to conduct special education classes and the delivery of related services. The agreement must designate one district to serve as the funding agent for fiscal purposes. R. C. 3313.841.

A. Shared Educational Programs

• Joint Educational Programs.– Boards of education or governing authorities

of two or more school districts or community schools may enter into agreements for the creation of joint or cooperative educational programs which may include any class, course or program that could be included in a school’s graded course of study or staff development programs for teaching or nonteaching employees. Tuition may be charged for some pupils participating in joint educational programs. R.C. 3313.842.

A. Shared Educational Programs

• Cooperative Education School Districts.– This option may become available in two

different ways. Those school districts that are part of a county school finance district may, by mutual agreement, create a cooperative education school district. The district includes the territory of the former county school financing district and has, generally, all of the powers of a city school district. R.C. 3311.52.

A. Shared Educational Programs

– School districts that are not part of a county school financing district may create a cooperative education school district for the purpose of operating a joint high school.

– The operation of a joint high school includes a prohibition on any of the participating school districts also operating a separate high school and requires the formation of a board of education and designation of a superintendent and treasurer for the governance of the joint high school.

A. Shared Educational Programs

– The statutes also provide for joinder of other school districts and dissolution of a cooperative education district. R.C. 3311.521, 3311.522 and 3311.523.

B. Joint Service Provisions

• School districts may agree to share the services of a treasurer. R.C. 3313.222.

C. Joint Building Projects

– Two or more school districts may, with the approval of the superintendent of public instruction, agree to construct or acquire any building or facility. The scope of power conferred is broad, and appears to contemplate the acquisition of buildings or facilities to facilitate joint programming agreements. R.C. 3313.92.

D. Shared Finances

• County School Financing Districts.– An ESC may create a county school financing district to

include:• the territory of local school districts within the ESC that do

not opt out, and • other school districts that opt into the county school financing

district.

– County school financing districts are authorized to propose the passage of property tax levies for a broad range of school purposes. In addition, county school financing districts can form the basis for the formation of cooperative education school districts. R.C. 3311.50, 3311.51 and 3311.52.

D. Shared Finances

• Joint City School Income Taxes.– Municipalities or combinations of municipalities

with boundaries substantially identical to school district boundaries may propose the levy of a municipal income tax on the incomes of municipal residents with proceeds to be shared with the school districts in agreed percentages, but not less than twenty-five percent of the revenue generated by the tax going to the school district. R.C. 718.09, 718.10.

Questions?

Nicholas Pittner, Esq.614.227.8815

www.bricker.comColumbus • Cleveland • Cincinnati-Dayton