david r. agrawal, william f. fox

TRANSCRIPT

8708 2020

November 2020

Taxing Goods and Services in a Digital Era David R. Agrawal, William F. Fox

Impressum:

CESifo Working Papers ISSN 2364-1428 (electronic version) Publisher and distributor: Munich Society for the Promotion of Economic Research - CESifo GmbH The international platform of Ludwigs-Maximilians University’s Center for Economic Studies and the ifo Institute Poschingerstr. 5, 81679 Munich, Germany Telephone +49 (0)89 2180-2740, Telefax +49 (0)89 2180-17845, email [email protected] Editor: Clemens Fuest https://www.cesifo.org/en/wp An electronic version of the paper may be downloaded · from the SSRN website: www.SSRN.com · from the RePEc website: www.RePEc.org · from the CESifo website: https://www.cesifo.org/en/wp

CESifo Working Paper No. 8708

Taxing Goods and Services in a Digital Era

Abstract

Taxing consumption in the digital economy poses unique challenges for fiscal authorities. Recent institutional reforms, such as states changing remittance rules for the sales and use tax following the Supreme Court decision in South Dakota v. Wayfair, were enacted in order to increase tax revenue collections and create a more neutral tax system. Although these reforms induced more remote vendors to remit taxes on a destination basis, the revenue gains were modest, consistent with most large online vendors remitting taxes prior to the reforms. Instead, following the recent large shock to online shopping from the Covid-19 pandemic, the shift to destination-based taxation has redistributed revenues between large and small local jurisdictions. Increased online shopping raises revenue growth in small jurisdictions while contracting revenues in large jurisdictions. But, Wayfair is not the end of the story: technological changes that induce new consumption patterns, promise new challenges for fiscal authorities. Critical challenges for the next decades include limiting administrative and compliance costs of enforcing taxes in a digital world, determining filing thresholds, dealing with online marketplaces and facilitators, and taxing the consumption of digital services from two-sided platforms. With respect to digital services, we discuss whether consumption taxes should be imposed on both monetized platforms and non-monetized platforms such as social media, and the mechanisms for doing so. JEL-Codes: H200, H700, K300, L800, R500. Keywords: sales tax, e-commerce, online shopping, enforcement, compliance, South Dakota v. Wayfair, consumption tax, digital services, platforms.

David R. Agrawal Martin School of Public Policy &

Department of Economics University of Kentucky Lexington / KY / USA [email protected]

William F. Fox The University of Tennessee, Knoxville Boyd Center for Business & Economic Research,

Haslam College of Business Knoxville / TN / USA

2

I. INTRODUCTION

Many classic problems in public finance concern the breadth of the tax base, the scope

for tax evasion, administrative and compliance costs, the behavioral responses of firms and

individuals, and the equity of the distribution of revenues across local governments. Online

shopping and the consumption of digital services, which pose many challenges for fiscal systems

around the world, are interesting applications of these classic problems.

Consumption taxes on goods and services such as the value added tax are common

around the world. However, the U.S. systems of consumption taxation generally has a narrower

base, mainly taxing the retail sales of tangible goods and limited services, though the value

added tax (VAT) base falls short of taxing all consumption. Although the retail sales tax in the

United States was the largest source of state revenue for decades and the second largest source

for local governments, it has stagnated in its revenue raising capability, as recent tax increases

were not sufficient to offset the narrowing of the tax base.

In this article, we focus on two critical reasons for the decline of the retail sales tax base:

the shift of consumption away from goods towards services and technological change that has

spurred online shopping and the creation of new digital services. Relative to the income tax base,

the sales tax base is generally smaller: partly because consumption is less than income, but partly

because of the historical application of the retail sales tax to tangible goods. Unlike the income

tax, where legislators started with a relatively broad base and may shrink it over time through

various deductions or exemptions, the sales tax starts with a relatively narrow base that must

attempt to keep up with real-time changes in consumption patterns and new types of products.

This is a daunting challenge.

Technological change can be a double-edged sword. Technological change that lowers

the cost of moving people, factors, and goods, may negatively affect tax systems by heightening

tax competition for mobile factors. At the same time, technological change may create

opportunities for governments by allowing them to enforce taxes better by using computerized

systems and comprehensive digital records.

With respect to the retail sales tax, this is not the first time that states have had to grapple

with these issues. Indeed, this is an apt time to review the future of the sales tax given the

publication of this article marks the 100th anniversary of a U.S. state introducing a tax resembling

the retail sales tax (Hines, 2007). When states first began to adopt general sales taxes in the Great

Depression, services represented approximately 25 percent of consumption. Starting in the

1950s, this share – which was previously stagnant – began growing, reaching approximately 50

percent of consumption by 2000 (Buera and Kaboski, 2012). As of 2017, services represent 69%

of personal consumption expenditures. Technological change has been critical to the growth of

many service sectors such as health care. Despite this rapid growth in services, states generally

failed to respond to these technological changes. As services become more important than the

3

consumption of goods, states attempted to offset the narrowing base by raising rates. Some states

expanded the base to include services, but this happened selectively.

More recently, technological change spurring the advent of remote catalog sales and

eventually, online purchases, raised new and important issues for state and local governments.

For years, states were restricted by a Supreme Court ruling in Quill Corp v. North Dakota

(preceded by National Bellas Hess v. Department of Revenue of Illinois) that only allowed states

to require remote vendors to remit sales taxes if the vendor had physical presence in the state.

With Congress unwilling to intervene and remote sales growing extensively over time, this

substantially eroded the sales tax base in the early days of the internet.1

The issue of online shopping highlights the importance of remittance rules in the design

of optimal tax systems (Slemrod, 2019). Quill effectively designated millions of online shoppers

as the remitting party when the vendor did not have presence in the consumer’s state. Thus,

extremely high administrative costs of tracking these purchases or auditing millions of individual

purchases effectively left many online purchases tax-free. In this way, the internet acted as a tax

haven that facilitated consumer tax evasion and avoidance strategies, much like cross-border

shopping did earlier. However, such a problem is mitigated – although not eliminated – if,

instead, large vendors are the remitting parties.

More recently, technological changes to business models and supply chains provided

some hope of counteracting declining revenues from e-commerce. Large vendors such as

Amazon established physical presence in more and more states to get goods quicker to market,

thus triggering the requirement to remit state and local taxes. And more recently, evolving

institutions, following the Supreme Court’s recent South Dakota v. Wayfair decision, now allow

states to adopt an economic nexus standard instead of a physical presence standard with respect

to tax remittance. In particular, taxation by vendors with economic presence follows the

destination principle, meaning that the vendor remits the taxes due to the state and locality where

the consumer lives. Indeed, there are many theoretical arguments for taxing consumption on a

destination basis. For example, destination-based taxation eliminates competition for mobile

cross-border shoppers (Agrawal and Mardan 2019). Moreover, as discussed in McLure (1998)

and McLure (1999), destination-based taxes are more likely to reflect the provision of benefits of

public services and are less likely to be exported inappropriately to residents of other

jurisdictions.

Policy commentators have been overjoyed at states’ newfound ability to effectively

require remote vendors to remit taxes based on the destination principle. Will the Court ruling

open the floodgates, resulting in large gains of tax revenue from previously untaxed online

purchases? Given the massive shock to online shopping because of Covid-19, does destination-

1 Bruce and Fox (2000) estimated sales tax losses of approximately $20 billion by 2003.

4

based taxation of online sales affect the distribution of sales tax revenue across counties and

localities? What are the costs to states and firms of this new economic nexus standard and will

the added revenue outweigh the administrative and compliance costs? Given the persistence of

institutions and the historical choices of how states define the tax base, does the Court ruling

help states address future digitization of consumption via both monetized services and non-

monetized services like Netflix, Uber, Airbnb, Facebook, Google, and Twitter?2 We attempt to

answer these questions in this article, while also providing guidance to policymakers for how to

proceed for the future of taxing consumption. While the first two questions truly hinge on

Wayfair, many of the answers to the remaining questions apply even in the absence of the

Supreme Court ruling. For this reason, we view the Court ruling as both an impetus to some

economic effects, but also a point in calendar time from which we can evaluate the future of

consumption taxes going forward. Moreover, the answers to the questions on digital services

apply to other countries around the world.

Using data on Tennessee state and local tax revenue and information about remote sales,

we first document, following Wayfair and adoption of an economic nexus standard, how tax

revenues increased from new vendors previously not remitting state and local taxes. This

increase in revenue was modest. Newly registered vendors represented 2.5% of local tax

revenue. The relatively small increase is likely a result of most large online vendors already

remitting state and local taxes, including many apparently on a voluntary basis.

However, the distribution of revenue across counties, which levy local sales taxes in

Tennessee, was critically affected by the new economic nexus standard. Consistent with the

theoretical evidence in Agrawal and Wildasin (2020), immediately following the economic

nexus reform, we document a slight increase in revenue in small counties and either a flat or a

declining share of revenue in the largest counties. In part, this is because prior to reforms

following Wayfair, remote vendors with nexus in Tennessee had the option to remit taxes using a

common local rate or on a destination-basis, but needless to say, many vendors elected the

former simpler approach for which the formula to distribute the revenues advantaged larger

population jurisdictions. Then, following the massive shock resulting from Covid-19, where

many households switched to online shopping, tax revenue from the sales tax dramatically grew

in small jurisdictions despite the economic downturn, but fell in large jurisdictions. The

institutional rules regarding economic nexus were critical for the distributive effects of this

massive shock to online shopping on the allocation of revenues across counties.

2 The recent GAFA Tax (Google, Amazon, Facebook and Apple Tax) in France attempts to tax

sufficiently large companies’ income at a flat rate. However, these digital taxes are usually

focused on the challenge of taxing corporate income in market countries given international

agreements rather than including digital goods and services in consumption tax structures.

5

The basic intuition is as follows. Theoretically, assuming that the fall in demand was

similar across jurisdictions, a shock that increases online shopping implies that rural consumers

are no longer driving to jurisdictions with shopping malls and retail agglomerations. Prior to the

Covid-19 shock, revenues would have accrued to the town containing the shopping mall. But,

with destination-based taxation of online shopping, the tax revenue accrues to the smaller

hometown. As an example, consider a resident in a small rural community outside of Tulsa,

Oklahoma. Previously, this resident may have driven to shopping malls in Tulsa and its suburbs

because their small hometown may not have any big box retailers; tax revenue accrues to Tulsa

or its suburbs. During Covid-19, this resident may be more inclined to buy online, which

generates tax revenue to the small home community.3 In this way, Wayfair redistributes revenues

of taxing goods from large jurisdictions to small jurisdictions. Even in the absence of Covid-19,

ignoring the issues of adding services to the tax base, we would have likely seen such a pattern,

but it would have been more gradual as consumers continue to gradually switch from shopping

malls in relatively large jurisdictions to online shopping as technological change lowers the

relative cost of buying online.

The ruling will have important implications on the tax system as a whole. In practice, we

show that the Wayfair ruling does not significantly broaden the definition of what is in the tax

base, but rather changes the remittance rules of the sales and use tax system.4 By shifting the

remitting party to the online vendor, economic nexus lowers administrative (enforcement) costs

of raising an equivalent amount of revenue. Rather than needing to audit many small individuals

with little hope of detecting online purchases, the government can now audit firms, which raises

the cost effectiveness of spending an extra dollar on enforcement. Of course, states may still

experience large administrative costs as they seek to audit many small out-of-state firms,

depending on the states’ compliance thresholds and on the extent of coordination with other

states. Even so, the new administrative costs of enforcing the tax code via audits of out-of-state

firms are not clear and effective enforcement may require coordination across multiple state

governments.

The compliance costs to firms are potentially non-trivial. Although many states have

simplified tax systems, some states delegate authority over the tax base and filing responsibilities

3 Given the small community has few large-scale shopping opportunities, why does it have a

sales tax in the first place? Although small communities are void of big-box retailers, they may

have small stores or sales by firms providing non-exportable services.

4 Even prior to Wayfair, online sales of tangible property were subject to taxation. The issue is

that for sales from vendors without nexus, the remitting party was the consumer who was legally

obliged to remit consumer use taxes, but tax evasion on these purchases was rampant. In this

way, Wayfair simply changes who remits the tax and facilitates government enforcement of taxes

on the same taxable base.

6

to municipalities. This was presumably, part of the reason why sufficiently small firms were

exempt from the tax. Moreover, the tax authority must be cognizant that added enforcement may

yield modest success (Johannesen, Langetieg, Reck, Risch, and Slemrod, 2020). In particular, the

shift of the remitting party to the vendor may induce new evasion or avoidance strategies: firms

may attempt to bunch under the economic nexus filing threshold, firms may use multiple

platforms and marketplaces to conceal sales or firms may just hope that enforcement is not yet

established and simply evade taxes. We discuss the effect of the ruling from a compliance costs

and administrative cost perspective.

Finally, we discuss the future of the sales tax in the context of continued technological

changes. As consumption continues to shift toward services, the sales tax becomes less effective

at raising revenue. Path dependence and slow moving institutions have often led states to only

incrementally expand the tax base to services. But this is not only a problem for the sales tax, as

many value added taxes often do not tax some major service sectors. The shift towards the

consumption of services is increasingly to platform-based technologies. The taxation of digital

services raises interesting challenges for policymakers, especially when the consumption

services provided by platforms are non-monetized. In some cases, these services, such as Netflix

or Uber, are not currently taxed in some states relative to more traditional services such as cable

television or taxicabs subject to the retail sales tax. Furthermore, many platforms, especially

social media firms, raise a majority of revenue through the sale of advertising with consumption

of the service being unpriced to the consumer. We discuss the arguments for expanding the sales

tax to include these types of consumption, emphasizing efficiency arguments. Regardless,

finding ways to broaden the base, not only selectively, will be critical for the future of the tax.

Although the retail sales tax has stagnated as a source of revenue in recent years, the

Wayfair decision provides opportunities for states to begin long-overdue reforms. Many

economists and policymakers see consumption taxation as a desirable policy goal. Given the

U.S. lacks a broad-based federal tax on consumption, the existing state and local retail sales taxes

provide a means to tax consumption. But, to be successful, these states must look beyond the

economic nexus reforms recently passed in almost every state. In many ways, Wayfair and the

resulting state reforms may have been too late. But, as we discuss, with appropriate and

comprehensive reforms, the sales tax can be an important tax for the next one hundred years and

not just a legacy of the last century.

To summarize, the Wayfair ruling has only modest implications for the design of sales

tax structures, as it only affects the ability to enforce taxation on a particular set of goods.

Wayfair lowers compliance costs and makes destination-based taxation more feasible, so it has

already had significant impact on sales tax practice. However, we caution against viewing

Wayfair as settling issues with respect to the base erosion of the sales tax. Traditional goals of

tax design, including neutrality, fairness, efficiency, and low compliance and administration

costs, should still be employed to determine the sales tax’s breadth. Some resulting specific

policy counsel for the sales tax includes: a) the tax should be levied against a broad consumption

7

base, b) the tax should generally be levied on final and not intermediate transactions, c) the

channel or the form through which consumption is obtained should be irrelevant to taxability

unless compliance or administrative costs are excessive for some channels, and d) the tax should

be levied on a destination basis.

II. BRIEF HISTORY

In this section, we discuss the history of retail sales taxation in the United States,

including recent Court decisions that have influenced the design of the tax system.

A. Background to Sales Taxation

As already previewed in the introduction, state sales taxes were the largest source of state

tax revenues for decades, but the tax has eroded as a share of both GDP and total state tax

revenues over the past 15 years (Figure 1). The sales tax’s revenue share stabilized between

1995-2005 and was first surpassed by the personal income tax in 1997. Frequent sales tax rate

increases since the 1970s maintained the sales tax share for many years but ultimately the rate

increases were not sufficient to offset narrowing of the base. Personal income taxes have mostly

lowered the share of revenue from unit based selective sales taxes on tobacco products, alcohol

and motor fuels, which have not seen nearly enough quantity growth to sustain their revenue

share in light of infrequent rate hikes. In total, the income tax share of state revenues has nearly

doubled over the past 50 years while the sales tax share has remained approximately constant.

Inability to enforce the sales tax effectively on remote sales has been an important reason

that the sales tax has declined in importance recently. As buyers shifted many in-store purchases

to online vendors, tax collection was often complicated and not enforced.5 Other factors include

the propensity of sales taxes to be levied more broadly on goods than services, as the latter have

grown much more rapidly as a share of the economy (health care, for example, has grown from 5

percent of GDP in 1960 to 12 percent in 1990 and 18 percent in 2018). Table 1 shows the growth

in services as a share of total expenditures. State decisions to exempt items, such as food at

home, and to implement tax holidays, have further eroded the base. In addition, states’ slow

response to taxing new technologies, new goods, and consumption via new distribution channels

has the same effect as exempting certain items from tax. Other taxes’ bases, such as the personal

income tax, are often broad enough and structured in a way that accommodates emerging

technologies, but the sales tax’s historical structure limits its ability to stay current. This is

discussed in more detail below.

5 See Fox (2016) for further discussion of sales tax growth over time.

8

B. Online Shopping

As is well known, e-commerce has grown substantially over the last decade, rising to 10

percent of total retail trade. In particular, sales from e-commerce retailers amounted to

approximately $520 billion in 2019, relative to total retail sales of $5,270 billion. Given retail

sales are the bulk of the base for the sales taxes in the United States, the growth in online

shopping created many concerns for state and local governments as the internet facilitated tax

avoidance. These concerns were heightened by numerous studies showing that online shopping

patterns are sensitive to the tax treatment of brick-and-mortar purchases relative to online

purchases (Ballard and Lee, 2007; Baugh, Ben-David and Park, 2018; Einav, Knoepfle, Levin

and Sundaresan, 2014; Ellison and Ellison, 2009; Goolsbee, 2000; Goolsbee, Lovenheim, and

Slemrod, 2010).

C. The Influence of the Court: Quill and Wayfair

A critical element of the U.S. sales tax system is the remittance rules that govern whether

firms or buyers remit taxes to the government. From an enforcement perspective, requiring

vendors to remit the tax is more effective than requiring many consumers to remit the tax. A

series of judicial decisions shaped these remittance rules and initially limited states abilities to

enforce tax compliance in the online era.

Quill Corp. v. North Dakota6 required that firms have physical presence in a state before

they could be compelled to remit the state’s sales tax.7 This ruling effectively meant that each

consumer must remit taxes on online sales when the online vendor did not have physical

presence in the state. Under this regime, states were reliant on consumers remitting use taxes

rather than vendor compliance to collect tax on many remote transactions. Individual compliance

with the use tax is widely believed to be very poor, at least in part because little if any auditing of

individual use tax returns takes place. Business use tax compliance is also weak, though some

auditing occurs in this case. For example, with respect to businesses, Smith (2018) finds 14.9

percent non-compliance with the Washington State use tax compared with 0.9 percent for the

sales tax. Still, Smith (2018) found much better business use tax compliance than in earlier

studies conducted over the previous several decades by Washington.

6 Quill Corp. v. North Dakota, 504 U.S. 298 (1992). Technically, the physical presence

requirement was established National Bellas Hess, Inc. v. Department of Revenue, and Quill

simply reiterated the holding. Several justices concurred solely based on the doctrine of stare

decisis.

7 See Stark (2021) for detailed discussion of previous and current Supreme Court rulings on

states’ ability to enforce compliance responsibilities on remote firms.

9

Over time, many states were aggressive in defining physical presence (see Agrawal and

Fox, 2017), but the earlier Quill decision hampered and delayed enforcement and resulted in

significant base erosion. The potential for revenue losses in the Quill era was mitigated by

evolving business practices and supply chains, whereby large online vendors established physical

presence in many states in order to get goods to consumers quickly. Thus, in the average state by

2012, more than half of the sales from the 300 largest online vendors had the tax remitted

(Bruce, Fox and Luna, 2015).

South Dakota v. Wayfair8 offers the opportunity to reverse some of the base erosion

resulting from rampant tax evasion of the use tax on online purchases by enhancing states’

ability to collect sales taxes on remote transactions. The Wayfair decision reversed the physical

presence requirement by allowing states to determine nexus based an economic rather than

physical presence. While the Court did not provide a definitive statement on what triggers

economic nexus, it is widely recognized that an online vendor must have a significant number of

transactions or a significant amount of sales into a state. Effectively, Wayfair altered states’

ability to compel compliance, which significantly improves the ability to enforce tax on a

destination basis.

D. State Reactions to Wayfair

States responded very rapidly to Wayfair, with some passing legislation prior to the

Supreme Court decision (see Table 2).9 Given the opportunity offered by Wayfair, all states

except Florida and Missouri enacted legislation requiring remote firms to remit the sales tax.10

The effective dates ranged from in 2018 to Texas in October 2020. States generally exempt firms

with a sufficiently small number of transactions or value of sales into the state. 11 State collection

thresholds range from $100,000 to $500,000, with Kansas saying that no threshold may apply.

Many states also have a threshold for the number of transactions, which can operate with either

both thresholds required or either being sufficient to trigger remittance responsibility for the

vendor. The quantity and dollar valued thresholds allows two different views of what it means to

exploit a state’s economy, but they are simply measurable standards and not theoretically derived

8 South Dakota v. Wayfair, Inc., 585 U.S. ___ (2018).

9 Alabama and Tennessee were among other states that faced court challenged during the same

period as the South Dakota v. Wayfair case.

10 See also Afonso (2019) and Mikesell and Ross (2019) for a discussion of state reforms and the

role of the use tax after Wayfair.

11 Most states, such as Wisconsin, have a requirement of either the dollar or the transactions

threshold, but New York requires both thresholds to be met.

10

measures of presence. States continue to develop their economic nexus legislation. For example,

several states, including Tennessee, have already lowered their dollar threshold and several have

eliminated their transaction threshold.

Recently, states have also begun to enact reforms related to the remittance rules with

respect to online marketplace facilitators. 12 A marketplace facilitator is defined as a marketplace

that contracts with third party sellers to promote their sale of physical property, digital goods,

and services through the marketplace. Digital Commerce 360 reports $552 billion in marketplace

sales in 2019. Following Pennsylvania, Rhode Island, and Washington in 2018, at least 42 states

have legislation requiring marketplace facilitators to collect taxes on behalf of individual firms.

Marketplace facilitator laws “require third-party marketplace platforms that advertise or sell

goods on behalf of others (marketplace sellers) to collect and remit tax on behalf of marketplace

sellers” (Kranz, 2020). These laws shift marketplace facilitators from having the option to collect

tax for third parties operating on their site to being required to collect for them.13 Marketplace

facilitator laws lessen state problems of identifying individual sellers and potentially reduce the

number of tax returns. As with economic nexus laws, state statutes vary widely and are often

very general, leaving the implementation details to revenue departments. Many states are still

developing the details of how the laws will operate and many challenges likely remain

unforeseen. Firms have a number of concerns, such as how the tax on product returns is treated,

the liability that facilitators have for determining tax on many detailed goods and services that

are sold by others, and whether local governments will enact their own facilitator legislation. It

also remains uncertain as to which taxes, in addition to the sales tax, that facilitators must collect.

E. Technological Change and the Future

Broadening the sales tax base to include emerging technologies and goods is the sales

tax’s challenge for the future. The accelerating speed with which new channels for delivering

services develop, new products are created, and the pace at which users adopt them pressure

states to modernize or restructure their tax systems. States must respond by accelerating their

modernization pace given rapidly changing business and consumer behavior. Unless the structure

evolves with the economy, the sales tax will continue eroding and burdening traditional

consumption relative to new alternatives.

12 Much of this paragraph draws from Kranz (2020).

13 Firms such as Amazon and Walmart were already required to collect and remit taxes on

transactions on their own account.

11

Autonomous vehicles are one example of new technologies and changing channels for

meeting consumer tastes. Fox (2020)14 discusses how development of autonomous vehicles

could reduce state transportation tax revenues by around 60 percent in a number of states, given

the interaction between electric autonomous vehicles and existing state tax structures. Loss of

fuel tax revenue explains much of the decline as vehicles are increasingly electric, but reduced

sales tax on selected taxable vehicle services and vehicle sales may be even larger as the number

of vehicles falls. Fox (2020) argues that dedicated companies (such as Uber or Lyft) are likely

the providers of mobility in the future and transportation services should be taxed rather than

various transportation inputs, such as the vehicles.15 The sales tax is one instrument that could be

used for this purpose, though the service is unlikely to be automatically accommodated within

most states existing statutes. Other examples of new technologies include, for example, digital

services such as streaming services, social networking platforms, and cloud storage spaces.16 An

interesting distinction that perhaps influences the political feasibility of tax base reforms is

whether the new technology replaces other physical goods that were previously taxed versus new

technologies that are completely new consumption goods. In the former case, including the new

technologies in the tax base compensates for lost revenue due to product substitution, while the

latter case expands the set of products that is taxable.

Historically, most state sales taxes were created as taxes on tangible personal property,

which limit the breadth of the tax base and require services and some new goods to be separately

articulated in state tax law as they develop. Gross receipts based sales taxes levied in some states,

such as in Hawaii, do not suffer from this weakness to the same extent. Similarly, a value added

tax often does not require legislative action as new goods and services are created unless

particular types of sales fall under previously exempted or zero-rated categories. Income tax

bases are generally structured much more broadly and include new forms of income.17 The

challenge with the sales tax is that legislative action is likely needed in most states to effectuate

the base expansions. History is not encouraging. The 1986 Florida base expansion experience18

14 Also, see Fisher (2020) and Clark (2020) for discussion of autonomous vehicles.

15 Other options for replacing lost vehicle taxes include a gross receipts tax on transportation

services and vehicle miles travelled fees.

16 In the presence of lines that delineate high-tax and low-tax products, technological change can

facilitate tax-driven product innovation as new products are developed to avoid the higher tax

rate (Gillitzer, Kleven, and Slemrod 2017). But, often time, new products are not developed for

tax avoidance reasons.

17 Carried interest is an exception which is characterized as capital income when it is better

described as labor income.

18 See, Hellerstein (1988) for discussion of the experience.

12

and paucity of sales tax base expansions despite widespread discussion,19 suggest that states will

remain slow in responding. The result will be a tax system that relatively penalizes traditional

commerce (particularly goods consumption) and benefits emerging goods and technologies.

Obviously, this raise numerous efficiency issues, especially if the physical goods are close

substitutes with the new digital services.

Later in the paper, we discuss several potential remedies that tackle issues related to the

consumption taxation of multi-sided platforms. But more generally, legislative remedies must

either substantially expand the definition of the sales tax base in ways that include emerging

technologies or states must enact piecemeal expansions. Historical efforts to significantly

broaden the base have generally failed, offering limited hope that states will seek broad

solutions.

III. EVIDENCE ON THE REVENUE EFFECTS OF WAYFAIR

In this section, we study the tax revenue effects of the Wayfair decision. We focus on one

state, Tennessee, for several reasons. First, Tennessee publicly releases monthly revenue data at

both the state and local level. Second, we have obtained information on tax revenues remitted by

remote vendors – data not readily available in most other states. To study the revenue effects, we

collect monthly data on tax revenues at the state and local level.

A. A Case Study of the Institutional Reforms in Tennessee

Prior to the passage of economic nexus rules in Tennessee, remote vendors that were

remitting taxes had a choice over how to remit local taxes. Historically, remote vendors could

elect to remit county taxes based on the consumer’s destination or remote vendors with no

physical presence in Tennessee were able to apply a uniform 2.25% local option sales tax rate.

Under the latter approach, the vendor did not need to keep track of local sales tax rates or situs

sales in local jurisdictions and instead could remit the state rate plus the uniform local rate. Then,

any local taxes from out-of-state dealers not using destination sourcing were distributed to

counties based upon the ratio of local tax collections in the county over total local tax collections

in all counties. Unlike most other states, Tennessee applies an origin sourcing rule for intrastate

e-commerce sales, even if the purchase is delivered to a home address.

The timeline of events in Tennessee was as follows. In October 2016, Sales and Used

Tax Rule 1320-05-01-.129 Subparagraph 2 – informally, Rule 129(2) – was proposed by the

Tennessee Department of Revenue. This rule, similar to South Dakota’s law said that remote

vendors with more than $500,000 of sales to consumers in the state have nexus for sales and use

19 See Fox and Murray (1988) for an early discussion of the case for sales taxing services.

13

tax purposes. The Rule states that by March 2017, these vendors should register with the state

and begin remitting taxes starting on July 1, 2017. As with South Dakota’s law, this was met

with legal challenges. More problematic, the Tennessee state government enacted Public Charter

452 in May 2017, which prohibited the Department of Revenue from collecting taxes under the

rule even if permitted under a court ruling until Rule 129(2) was approved by the legislature. The

Wayfair ruling was handed down in June 2018. Then, the state passed Public Chapter 429 in

May 2019. This authorized the Department of Revenue to begin enforcing Rule 129(2) to collect

sales tax from remote vendors without physical presence but who have more than $500,000 of

sales into the state of Tennessee. Firms that met Tennessee’s threshold by July 31, 2019 were

expected to begin collecting sales taxes no later than October 1, 2019.

Although Public Chapter 429 allowed for collection from remote vendors without

physical presence, these vendors still had the ability to use the uniform local tax rate option.

Public Chapter 491, which was effective October 1, 2019, required these remote vendors to

apply and remit the specific local sales tax rate in the city or county to which the good was

delivered. After October 2019, any local taxes from out-of-state dealers not using destination

sourcing will be based upon the local tax collections in the county from dealers with no location

in the state that can be identified by situs over the total local tax collections in all counties from

dealers with no location in the state that can be identified by situs. However, this formula should

apply to very little revenue because the vendors are required to remit at destination and the

formula would only be applied if the vendor did not provide sufficient information with respect

to destination-sourcing. Note that the effective date of Public Chapter 491 is the same as the date

as when firms were expected to first begin collecting taxes under Public Chapter 429. Thus,

although we will reference Public Chapter 491 as the October date for simplicity, all our

empirical results should be interpreted as the joint effect of both laws.

B. The Amount of Tax Revenue from Remote Vendors Following Economic Nexus Reforms

Against this backdrop, we study the effect of these events on tax revenue. As

background, for fiscal year 2017-2018, the Tennessee state sales tax raised $8.9 billion and local

taxes in the state collected $2.6 billion. Thus, in the fiscal year prior to the June 2018 Court

decision, the state collected on average $741 million per month and local governments collected

$217 million per month.

It is often difficult to evaluate the revenue impacts of nexus rules because states do not

publicly release data on revenue collected from remote vendors specifically. However, the state

of Tennessee provided us access to two unique data series. The first represents the revenue

remitted by remote vendors without a physical presence in the state of Tennessee. Because the

data only cover vendors without a physical presence, this should not be construed as the total

revenue resulting from online shopping, as it does not include online sales from instate vendors

like Walmart. Nonetheless, this is the best data to evaluate the effect of Wayfair and economic

nexus on the amount of additional tax revenue. The second dataset is the revenue raised from

14

vendors that are newly registered as remote sellers since June 2018, i.e., since the decision in

Wayfair. The information on remote vendor status self-reported and possibly subject to

underreporting.

To study these effects, we present a series of figures. The vertical lines in the graph, and

in subsequent figures, show the month prior to Wayfair and implementation of Public Chapter

491. The latter event also corresponds to the month prior to when vendors with economic nexus

were required to begin remitting taxes under Public Chapter 429.

The solid line in Figure 2 shows the total revenue remitted to localities from remote

vendors, adjusted for month fixed effects.20 Given the higher tax rate, the remittances to the state

are likely three times as large. Prior to Wayfair, sales tax revenue from out-of-state vendors

represented approximately 14 percent of local tax revenue, suggesting that online purchases from

remote vendors is critical to financing local public services. However, the court decision and

subsequent passage of economic nexus and the abolition of the uniform local rate option, seem to

have had minimal effects, with the $40 million from remote vendors after Wayfair representing a

similar share of total local revenue.

The dashed line in Figure 2 reinforces this result. This series is constructed based upon

answers to questions in the filing data from taxpayers who have registered as remote sellers since

June 2018, i.e., since the decision in Wayfair. As can be seen, newly registered vendors

contributed only $5 million in local sales tax revenue per month by 2020. This is approximately

2.5 percent of local monthly sales tax revenue. 21 This small effect likely results from several

factors. First, Tennessee’s threshold for economic nexus is relatively high compared to other

states. Second, as shown in Bruce, Fox, and Luna (2015), many of the largest online vendors

were already remitting taxes at the state and local level even as early as 2012. Third, several

large vendors (such as Wayfair) appear to have begun voluntary compliance after the Supreme

Court decision.

The evidence on the effects of economic nexus in other states is limited. Using multiple

states, Fox, Hargaden, and Luna (2020) estimate that state sales tax revenues rose about 3.5

percent from imposing economic nexus requirements and a comparable amount from

marketplace facilitator legislation. Mikesell and Ross (2019) find that remote vendor

20 Given our main analysis will focus on the distribution of revenues, we focus on the revenue

impact to local governments.

21 The results are likely a lower bound because the Tennessee revenues analyzed here are based

on firms self-identifying as remote firms. Further, some remote firms may have been remitting

revenues on a destination basis, even before it was required. Marketplace sales are also not

included because Tennessee only recently passed legislation for the marketplaces.

15

registrations tripled in Indiana after the passage of economic nexus, but the impacts on state tax

revenues were modest.

The dashed series in Figure 3 shows the amount of local revenue from newly registered

(after Wayfair) remote vendors without a physical presence as a share of total local revenue from

all remote vendors without a physical presence. As can be seen, these new vendors represent a

bit more than 10% of revenue from remote vendors. Given remote vendors without physical

presence raise approximately 14 percent of total local revenue, consistent with the prior figure,

newly registered vendors contribute only a small increase to total revenue.

However, the solid line in Figure 3 shows a potential redistribution of local revenue.

Recall that prior to Public Chapter 491 any local taxes from out-of-state dealers not using

destination sourcing were distributed to counties based upon the ratio of local tax collections in

the county over total local tax collections in all counties. Given the formula is based upon local

tax revenue for physical goods (where the goods sell), the formula does not well-approximate

destination sourcing and advantages large jurisdictions with many retail agglomerations.

Theoretically, large jurisdictions are potentially advantaged for two reasons. First, the bulk of

physical sales occur in places with retail agglomerations. Second, in standard tax competition

models (Kanbur and Keen 1993) large jurisdictions set higher tax rates than smaller jurisdictions,

potentially raising more revenue all else equal.22

As can be seen by the solid line in Figure 3, immediately following the passage of Public

Chapter 491, the number of vendors applying destination-sourcing to local sales increases

dramatically. By the middle of 2020, almost one hundred percent of remote vendors without a

physical presence have switched to destination sourcing.

B. The Distribution of Revenues Across Counties After Economic Nexus Reforms

While the prior section focused on the amount of new revenue, Figure 3 also suggests

that the distribution of revenues may have changed. Public Chapter 491 affects not just the

amount of revenue, but also the distribution of revenue. In Tennessee, this may have occurred

because of movement away from a formula that favored large jurisdictions and because online

sales from new vendors or resulting from shocks that encourage online shopping relative to

brick-and-mortar shopping, are now sourced at destination.

22 In Tennessee, this second reason is likely to play a minimal role because jurisdictions often

max out at the highest possible county sales tax rate (Luna, Bruce, and Hawkins 2007). Further,

small rural jurisdictions may primarily sell nontraded goods, such as in small restaurants, and can

set tax rates with minimal concern for cross border competition. But such an effect might arise in

other states or at a finer municipal level where there is potentially more variation in tax rates.

16

With respect to the latter channel, Covid-19 provides one such shock to online shopping.

Because of the rapid spread of Covid-19 starting in March 2020, many state governments began

to shut down and placed substantial limitations on what businesses could remain open.

Therefore, many individuals switched a substantial fraction of their retail purchases from brick-

and-mortar purchases to online purchases.

Agrawal and Wildasin (2020) provide a theoretical model that allows us to think about

the effects of such a shock. This dramatic shift to online purchases, combined with economic

nexus regulations that require online vendors to remit taxes on a destination-basis, erodes the tax

base of large agglomerated jurisdiction while increasing the tax base of smaller jurisdictions.

Intuitively, prior to the Covid-19 shock, individuals living in more remote and rural jurisdictions

needed to travel to suburban or urban jurisdictions for many of their purchases. Driving to these

retail shopping centers meant that they contributed tax revenue to these large jurisdictions. As a

result of the Covid-19 shock, these individuals no longer purchased goods at shopping malls

located outside of their hometowns and instead made the purchases online, which given the sales

are taxed at destination, contributed tax revenue to their home community. Thus, Covid-19

should provide a shock that erodes agglomeration benefits of large towns and redistributes

revenue from large to small jurisdictions.23 Critically, this redistribution would have been

dampened without the Wayfair ruling and appropriate state reforms.

In this section, we present compelling visual evidence on the distributional effects on tax

revenues across local governments as a result of the Wayfair ruling, the passage of economic

nexus, and due to the massive shock to online shopping from Covid-19. To do this, we split the

sample of 95 counties in Tennessee into three groups: the largest counties, the smallest counties,

and all other counties. While subjective, for purposes of this paper,24 we define the largest

counties as the four counties housing the principal cities (Memphis, Nashville, Knoxville, and

Chattanooga) in Tennessee’s main metropolitan areas. All four of these counties have more than

350,000 people living in them. The smallest counties are defined as counties in the bottom 50%

of counties based on population size. This threshold corresponds to counties with less than

32,000 people. Population acts as an exogenous proxy for economic activity.

While population is not a measure of retail agglomeration, it is correlated with

agglomeration. As shown in Figure 4, in normal times, the four largest counties raise

approximately 42 percent of all state and local sales tax revenue – more than proportional than

23 Covid-19 also triggers an economic shock, potentially reducing demand for retail purchases.

Thus, in our analysis below, we assume that any negative demand shock is similar in large and

small jurisdictions. Given we seek to analyze this issue descriptively, such an assumption is

plausible.

24 Results are similar if we use other definitions of large and small counties.

17

their share of the state’s population. The bottom 50 percent of counties contain 12 percent of the

state’s population and are approximately 9 percent of the state’s personal income but raise only 6

percent of total tax revenue. Given large counties raise proportionally more revenue than their

populations and small counties raise proportionally less revenues than their populations, this

highlights the spatial asymmetry of retail shopping opportunities. Critically, from Figure 4 we

can already see that the share of revenue raised in small counties has increased substantially

during the recent Covid-19 pandemic.

Note that any response immediately after the Wayfair decision should be due entirely to

voluntary compliance, as Tennessee did not change the compliance responsibility until October

2019, corresponding to the effective date of Public Chapter 491. For simplicity, we omit a line

for Covid-19, which led to many states closing non-essential businesses in March/April 2020.25

To study the effects of Wayfair, Public Chapter 491, and Covid-19 on the distribution of

tax revenues, Figure 5 plots tax revenue in the largest and smallest counties. Then, in Figure 6,

we plot the year-over-year growth rate (e.g., March 2019 relative to March 2018). Graphs

involving tax revenue levels are smoothed by removing month fixed effects and plotting a

moving average with equal weight to the given month, month prior and month later. Year over

year growth rate graphs (March 2019 / March 2020) do not remove month fixed effects and

simply plot a moving average.

Keeping in mind that Figure 5 removes seasonality using month fixed effects, in level

terms, the Wayfair ruling has no noticeable effect on tax revenues of small and large

jurisdictions, consistent with the number of newly registered out-of-state vendors being minimal.

However, in the few months after passage of Public Chapter 491, the level of revenues accruing

to small counties increases by several million dollars. Following the start of the Covid-19 shock,

which induced a dramatic shift to online purchases, revenues in small jurisdictions continue to

rise despite the negative economic shock from the virus. At the same time, revenues fall in large

jurisdictions following the shutdown of economic activity.

These effects are more noticeable in the year-over-year growth rates in Figure 6, which

because the year-over-year changes reduce seasonality, we do not adjust for month fixed effects.

Following the passage of Public Chapter 491, the growth rate increases in small counties more so

than in large counties. This is consistent with a shift from vendors using a single uniform rate

toward destination-based taxation. The online shopping shock induced by Covid-19 amplifies the

growth, with revenue in small jurisdictions rising 15 percent, while in large jurisdictions it turns

25 The Governor of Tennessee issued various executive orders, including restrictions on mass

gatherings on March 13, a request for business to shift to “alternative business models” on March

22, “safer at home” guidelines on March 30, and Executive Order No. 23 requiring Tennesseans

to stay at home except for essential activities on April 2, 2020.

18

to negative 15 percent. Certainly, the economic shock to Covid-19 is likely larger in urbanized

areas, and we do not claim these are the causal effects of a pure shift to online shopping. But

critical for us is that the growth rates in cities and more rural communities are opposite in sign,

which can only be explained by a shift to online shopping.26

With respect to the external validity of these results, the effect identified may be even

greater in other states. Several states, including Tennessee, apply an origin sourcing rule for

intrastate e-commerce sales, even if the purchase is delivered to a home address. In these nine

states,27 the online vendor applies tax to the product based on the point of origin (the “ship from

address”) for all transactions within the same state. In this way, if Amazon provides fulfilment

services for a local Tennessee firm, the tax revenue will go to the locality where the inventory

was stored. However, online transactions fulfilled by out-of-state remote vendors with nexus are

to be sourced at destination.

In states that do not have an origin sourcing rule, online sales are sourced at destination

regardless of whether they are intrastate or interstate. In these cases, the effects we identify

would apply to both intrastate sales and interstate sales. Given within state e-commerce

transactions are a nontrivial share of e-commerce (Hortaçsu, Martínez-Jerez, and Douglas, 2009),

we thus view the results in Tennessee as providing a lower bound on the shift of revenue from

large to small jurisdictions in purely destination sourcing states.

C. Local Sales Tax Issues of the Future

The prior analysis suggests an interesting redistribution of revenues following a massive

shock to online shopping. But the sign of the effects would also apply to smaller – and more

gradual – shocks that might arise from the cost of online shopping falling relative to the cost of

brick-and-mortar shopping. Costs may decline gradually as shipping costs fall, as aggregator

websites make it easier for consumers to find goods, as consumers become much more

accustomed to online shopping for more and more goods, or as retail-shopping locations become

further away due to store closures.

26 This assumes that Covid-19 does not induce individuals in smaller counties to switch from

larger urban places to local physical shopping (corner stores, etc.) According to the Department

of Commerce and Chetty, Friedman, Hendren, Stepner, and the Opportunity Insights Team

(2020), online purchases increased by 37% from the first to the second quarter of 2020,

suggesting the effect to online shopping represents a first-order effect especially as many goods

are likely not available at smaller local stores.

27 Two other states apply a hybrid sourcing rule where origin sourcing applies on some intrastate

e-commerce sales.

19

Overtime, such shocks will shift consumer purchases away from retail agglomerations

toward online purchases, which given economic nexus, can be taxed at the place of residence.

This will erode the taxable agglomeration rents of large jurisdictions with retail agglomerations

and fill the revenue coffers of smaller – more remote – jurisdictions. Thus, the sign of the effects

we identify in response to the Covid-19 shock may be similar to more gradual shocks from

technological change in the coming decades. In turn, in the future twenty years from now,

Wayfair may create winners and losers as online shopping costs continue to fall. Although

Wayfair, provides agglomerated jurisdictions with a way to tax their resident online purchases,

their tax bases may decline as they no longer may be able to engage in tax exporting to cross-

border shoppers who previously drove to shopping malls in large jurisdictions simply because

they had no retail centers nearby. In this way, even with economic nexus, the tax base remains

footloose, which in turn might encourage these jurisdictions to lower their tax rates, as they can

no longer take advantage of their agglomerations. But smaller jurisdictions benefit from online

shopping and destination sourcing, which lowers consumer mobility, perhaps encouraging them

to raise their tax rates.

Interestingly, as discussed in Agrawal and Wildasin (2020), as online shopping transfers

tax revenue from large to small jurisdictions, total local tax revenue may fall. If small

jurisdictions traditionally levy lower tax rates than large jurisdictions (Kanbur and Keen, 1993),

an online sale from a resident of a rural community is likely to be taxed at a lower rate than an

equivalent bricks-and-mortar purchase from an urban or suburban jurisdiction. In the nationally

representative dataset from Agrawal (2019), the average town plus sub-municipal district tax rate

in states allowing for local taxes is 1.16 percent for the top quartile of towns on the basis of

population and 0.70 for towns in the bottom three quartiles based on population.

The basis of the sales tax is often de facto defined as the place where receipt of goods or

services is taken. Consumers going into another state to cross border shop presumably create

issues similar to an e-commerce sale when a firm delivers goods to the consumers’ homes, even

though this issue has received little attention. In-state local taxes could also be altered in those

states that grant legal taxing authority of local sales taxes on a destination basis.

With respect to local tax competition, even if online sales are taxed under the destination-

principle, tax competition will still exist.28 As long as some goods (or services), need to be

purchased from a physical store, tax-induced incentives for cross-border shopping will persist.

Moreover, even though online vendors are required to remit taxes at destination, physical stores

and service providers still remit based on the origin principle. Moreover, jurisdictions may also

28 For studies of local tax competition, see Agrawal (2015), Agrawal (2019), Burge and Piper

(2012) and Burge and Rogers (2011).

20

compete for online shoppers: agglomerated jurisdictions may adjust their tax rates in order to

discourage online shopping. In the very long term, we could imagine a world where the cost of

online shopping is extremely low relative to brick-and-mortar sales and all purchases are online.

Only then will economic nexus eliminate inefficient tax competition for cross-border shoppers.

But, such a world may create other types of competition as individuals might then migrate to

avoid a purely destination-based sales tax, much like they may to avoid local income taxes (e.g.,

Schmidheiny 2006; Martinez 2019).

Finally, in most states, vendors file their local tax returns with the state government, and

they need not file returns in each locality. The future of local sales taxes may also be influenced

by the presence of six home rule states.29 Home rule states are those where local governments

(either county, town, districts or tribal governments) may collect and administer taxes

independently of the state government. However, the amount of independence varies across

states. Following Wayfair, the states also differ in how they are applying economic nexus rules

for localities. We discuss compliance costs in the next section, but generally abstract from the

added compliance costs imposed by home rule localities, which may be substantial.

IV. ADMINISTRATIVE AND COMPLIANCE ISSUES

A. Administrative Issues for Sourcing

States and businesses must settle on the meaning of “destination” and “origin,”

particularly in states where instate sales are taxed at origin and out of state sales at destination for

local tax purposes. The courts may also impose constraints on these decisions as shipments to a

particular location from out of state may result in both different compliance costs and different

tax rates than for shipments intrastate to the same location. As demonstrated above for

Tennessee, these decisions can have large distributional effects as revenues move from large to

small counties. The range of issues30 is likely to evolve with supply chains, development of

channels for obtaining goods and services, digitization of products and so forth. For example, at

what rate is tax imposed and which county receives the revenues for a sale by an out of state

vendor that is fulfilled through an instate location of a third-party facilitator? What if fulfillment

takes place from an out of state location for an in-state vendor? Such decisions potentially

require detailed information on which inventories are used for fulfillment and where the

inventories are held. Third party vendors could be required to separate the same product

29 These states include Alabama, Alaska, Colorado, Idaho, and Louisiana. In addition, Arizona

administers local jurisdictions’ sales taxes, but home rule applies for local tribal governments.

30 Interestingly, discussion has often focused traditionally on the difficulty of identifying

destination for indirect taxes. The concerns we raise suggest that determining origin can also be

very complicated as means of fulfillment transition over time.

21

according to specific ownership as they trace products to their origin or destination. Conclusions

on where origin and destination are located may offer tax planning opportunities for vendors.

B. Compliance Costs, the Filing Notch, and Audits

The Quill ruling created a characteristic notch based on geography and physical presence.

Firms without physical presence in a state could not be compelled to collect sales tax, though as

noted above, buyers were still expected to remit use tax. The notch existed because of

differential enforcement capacity for the sales tax relative to the use tax and not by an explicit

statute. Wayfair narrowed the notch by allowing states to require remote firms to collect and

remit sales tax, but all states (potentially except Kansas) include a small seller exception in their

economic nexus statutes. Thus, compliance is required for larger but not smaller remote firms.

Both large and small in-state firms are required to collect tax.31

Each state created a complex set of notches in its Wayfair economic nexus statute

regarding collection and remittance of tax by remote firms. The effective notches potentially

depend on the size of the state, the minimum threshold for a collection responsibility, the

channels added together to measure whether the threshold is met, and the frequency with which

the thresholds are calculated. As discussed above, states established compliance thresholds

ranging from $100,000 to $500,000 in yearly sales into the state (see Table 2), with some states

also having a requirement based on the number of transactions during the year. Other differences

exist across states. For example, some states base the threshold on the previous year’s sales and

others have a rolling threshold based on the most recent 12 months. Generally, these thresholds

are forward looking and either apply to the next calendar year or the next 12 months. Some states

may seek to assert that firms have taxable presence going forward once the threshold is met, but

the specific administrative rules are still being developed and generally have not been tested

through the legal system. These thresholds likely mean that much smaller firms are more likely

to be required to collect tax in large market states (high population/income) than in small market

states. For example, a firm selling evenly in proportion to population across the country would

need only $4.2 million in national sales to have a collection responsibility that met California’s

$500,000 threshold, but the same firm would need $37.1 million in sales to meet South Dakota’s

much lower $100,000 threshold.

Many firms sell through multiple channels including their own website and one or more

marketplaces. States differ in how and which sales are aggregated to determine whether the

threshold is met. As noted above, most states with economic nexus legislation also require

collection by marketplaces. The marketplaces may calculate and collect the tax but they

31 Some exceptions may exist for very low activity levels and differences often exist in required

frequency of filing tax returns.

22

generally do not remit the tax on behalf of vendors, which must file their own tax returns or hire

someone to do it for them. Some states sum all of these channels in determining whether the

threshold is met and others do not. Table 2 identifies states that include marketplace sales in

determining if the threshold is met.

The notches discussed above could increase compliance and administration costs and

cause bunching below the threshold. Firms cannot alter their current year compliance

responsibility by bunching in states that determine presence based on prior year sales, though

they potentially can influence nexus in the following year. Compliance burdens exist for those

firms that have a collection responsibility, but also for firms that need to track their sales to

determine whether they have sufficient economic presence to create nexus. Voluntary

compliance may be greater in states that determine nexus based on the most recent 12 months of

sales. Firms may be unsure whether they have a compliance responsibility may then voluntarily

comply to reduce their risks of failing to comply or to avoid certain compliance costs.

Different thresholds and approaches to measuring total sales across states add to the

compliance burdens as firms must understand the requirements for collecting for each state in

addition to measuring destination-based remote sales. The problem is exacerbated when firms

operate through multiple channels and need to aggregate data from different information systems

to determine whether thresholds are met and the associated tax liabilities. Further, states do not

always require destination situsing for instate sales even though they require it for out-of-state

sales, adding additional burdens as firms may situs some sales on a destination basis and other on

an origin basis.

The notches may be effectively larger than their legislated structure because states can

find it difficult to identify potential taxpayers and determine whether they are appropriately

complying with the law. The result could lead to significant evasion if states are unable to

convincingly audit firms. States will likely use multiple means to identify these firms, including

audits and data that is collected from related firms. Several vendors are also seeking to sell

software to states, that among other things, identifies firms that are believed to meet the

thresholds. Absent such third part reporting, some coordination across states may be necessary.

Although the notches could also cause bunching as firms seek to remain just under the

threshold, several factors reduce this possibility. Decentralization of thresholds to the state level

likely reduces bunching relative to a larger national threshold. Moreover, complexity of state

thresholds and collection by marketplaces makes bunching more difficult and perhaps not

worthwhile. But, in the extreme example, firms may seek to limit compliance by dividing into

multiple separate legal entities providing different products into states and targeting advertising

by geography. The costs and benefits of seeking legal ways to remain under thresholds may

cause firms to risk non-compliance as the means of avoiding a compliance responsibility.

23

V. TAXING DIGITAL SERVICES

A. Introduction to Taxation of Digital Services

In this section, we discuss several policy issues of the future in the context of

technological change creating new types of consumption patterns. Although the health care

sector is one of the fastest growing sectors in the economy, we exclude discussion of taxation of

health services given that such proposals are not politically feasible, and moreover, because

many broad-based consumption taxes around the world exempt the health care sector. Instead,

we focus on major issues most closely relating to online purchases and the digital economy. We

also emphasize base expansions that are of current interest to policymakers.

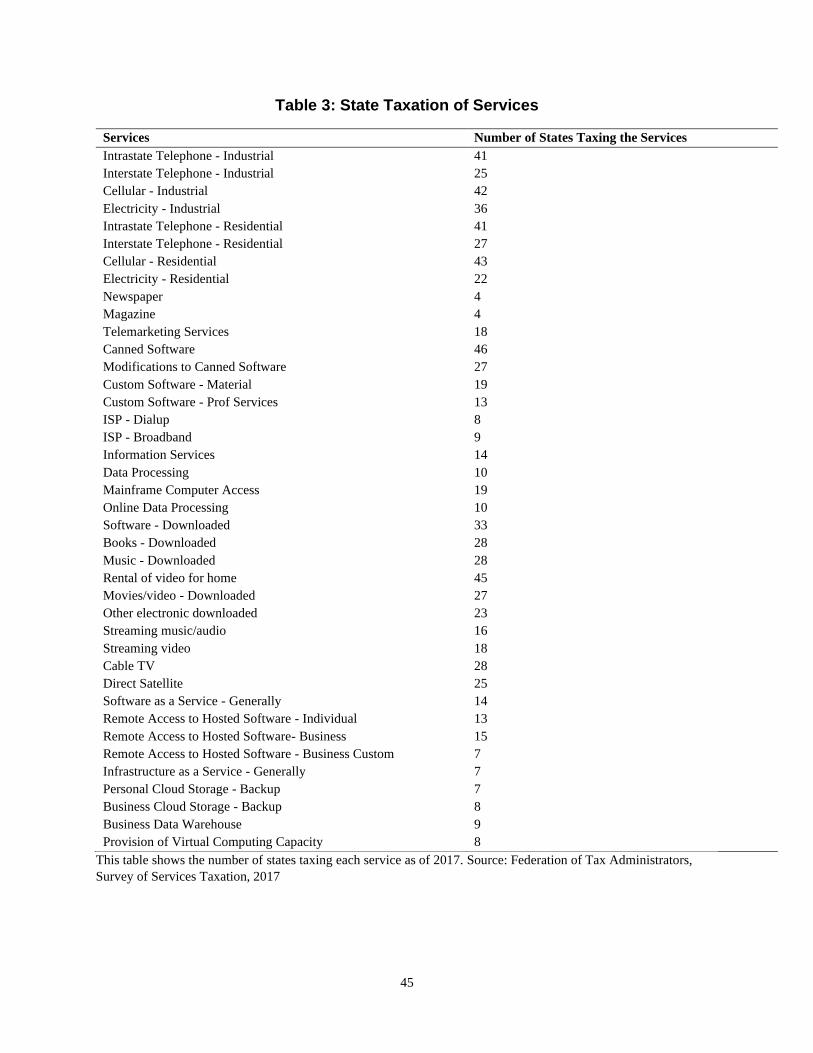

This section focuses on digital goods and services (as illustrated in Table 3) and not on

digital transaction platforms used to obtain goods and services. Airbnb, Uber, Amazon and

others are transaction platforms are marketplaces for obtaining goods and services and are not

the goods or services directly consumed, though as discussed below, they clearly add value by

allowing efficient access to these goods and services. Obviously, if a broad base is desired, final

goods and services obtained through these mechanisms should be subject to sales tax. The

marketplace or channel will generally be the most cost-effective means to collect and remit tax.

In particular, platforms like Airbnb and Uber can collect and remit tax more efficiently than the

myriad providers of transient housing and mobility.32 Moreover, these types of platforms are not

subject to the same types of externalities that are challenging for taxing two-sided platforms.

B. Digital Services

The policy prescriptions at the end of the introduction offer direction for expanding sales

tax structures as technological changes and digitization create new goods, services and

consumption channels. Wayfair reflects the Court’s understanding and allowance of taxation that

is neutral with respect to distribution channels, with small seller exceptions to limit the

compliance costs arising from sales into multiple markets. However, Wayfair only addresses

nexus issues associated with remote sales of taxable goods and services and does not speak to the

problem of sales tax laws that are too narrowly construed and out of date with respect to current

consumption behavior. Frequent updates of the sales tax base are imperative if states are to tax

evolving forms of consumption. Alternatively, states could entirely restructure their sales tax

laws to broadly tax consumption, which would generally incorporate new forms of consumption

32 See for example, Bibler, Teltser and Temblay (2020).

24

in the base, rather than the current approach often requiring piecemeal addition of services.

However, given recent history, such a broad reform is unlikely.

1. Current State Practice for Taxing Digitized Transactions

Taxing digitized transactions is not a new issue for states and remains a key next step for

many states to take given the rapid movement toward digitized goods and services. State statutes

vary widely in their coverage of digital goods and services and the sales tax in most states would

benefit from base expansions. Table 3 identifies the propensity of states to tax selected digital

and media services.33 Neutrality and equity, usually argue for taxing goods and services when

provided to consumers in digitized (as well as tangible) form to move the sales tax closer to a

consumption base. Further, the sales tax’s revenue elasticity will be greater if the tax base

includes evolving and rapidly growing components of consumption. The imperative of taxing

digitized services grows if very similar services are taxed in physical form.

States generally created their sales taxes as levies on tangible personal property (DVDs,

landline telephones, etc.) and services and digitized transactions have been added through a

variety of means, though often to a limited extent and with substantial variation across states.

Several states, including Hawaii, New Mexico34 and South Dakota tax many digitized services

and most consumer services (with a few exceptions). On the other hand, Garrett and Nulle

(2020) observe that Georgia, Nevada and Oklahoma are at the other extreme with little or no

taxation of digital transactions. Specific statutes were enacted in some states to expand the base

to select services,35 but in some cases without consideration of digitization. Some other states

have interpreted certain digitized transactions as the transfer of tangible personal property and

imposed tax through existing statutes. For example, 28 states define tangible personal property to

include prewritten computer software (see Garrett and Nulle, 2020), though they differ on

definitions of prewritten software. The problems of modernizing tax systems are complicated in

33 State taxation of services is taken from the Federal of Tax Administrators’ Services Tax

Survey for 2017. In some cases, the tax is imposed at a rate that differs from the general sales

tax. In other cases, states levy a tax other than the sales tax, such as in Delaware, which taxes

many of the services through gross receipts taxes and does not have a general sales tax, and in

Washington, which levies tax through its Business and Occupations Tax (potentially in addition

to the sales tax).

34 Hawaii and New Mexico’s sales taxes are gross receipts taxes on business revenues (with

certain exemptions), which often avoid the need to articulate specific services.

35 For example, North Carolina added digital newspapers, magazines, photographs and greeting

cards to the sales tax base in 2019 and updated the definitions of a number of digital products.

See N.C. Gen. Stat. § 105-164.3(#) and others.

25

states, such as Missouri, which have passed constitutional amendments to prohibit taxation of

new services. Constitutional bans, which surely have been enacted on political rather than

economic grounds, may include newly digitized goods requiring these states to use increasingly

inefficient tax structures.

At least 12 states define certain digital products, such as prewritten software, so that the

method of delivery is irrelevant but this is not the norm across the range of digital transactions.36

Nine states only tax prewritten software if delivered through tangible medium (see Garett and

Nulle, 2020). In addition, Rosen and Haffield (2016) observe that every state taxes tangible

recordings (such as DVDs and music CDs), but digital analogues are often not taxed. Only 27

states tax downloaded videos and 18 tax streaming of video. Twenty-eight states tax e-books;

states seldom tax magazines and newspapers, whether in physical or digital form.

2. Challenges for Taxing Digitized Transactions

Garrett and Nulle (2020) observe that state sales tax decisions on digital transactions

appear to be determined by whether the transactions are a digital product or a digital service,

whether software is different from digitally delivered content, whether the purchases are

downloaded or merely accessed, or whether they are live or recorded content. These distinctions

may fit taxation into existing statutes, but fail to address taxation of digital products in term of