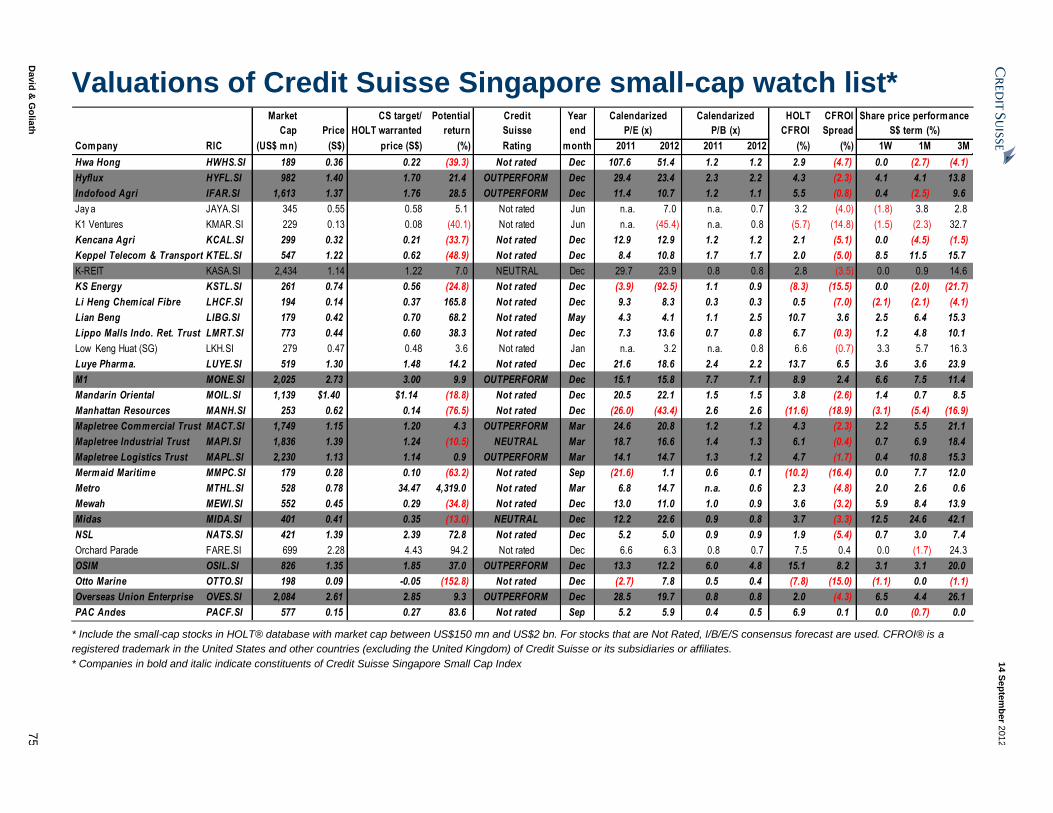

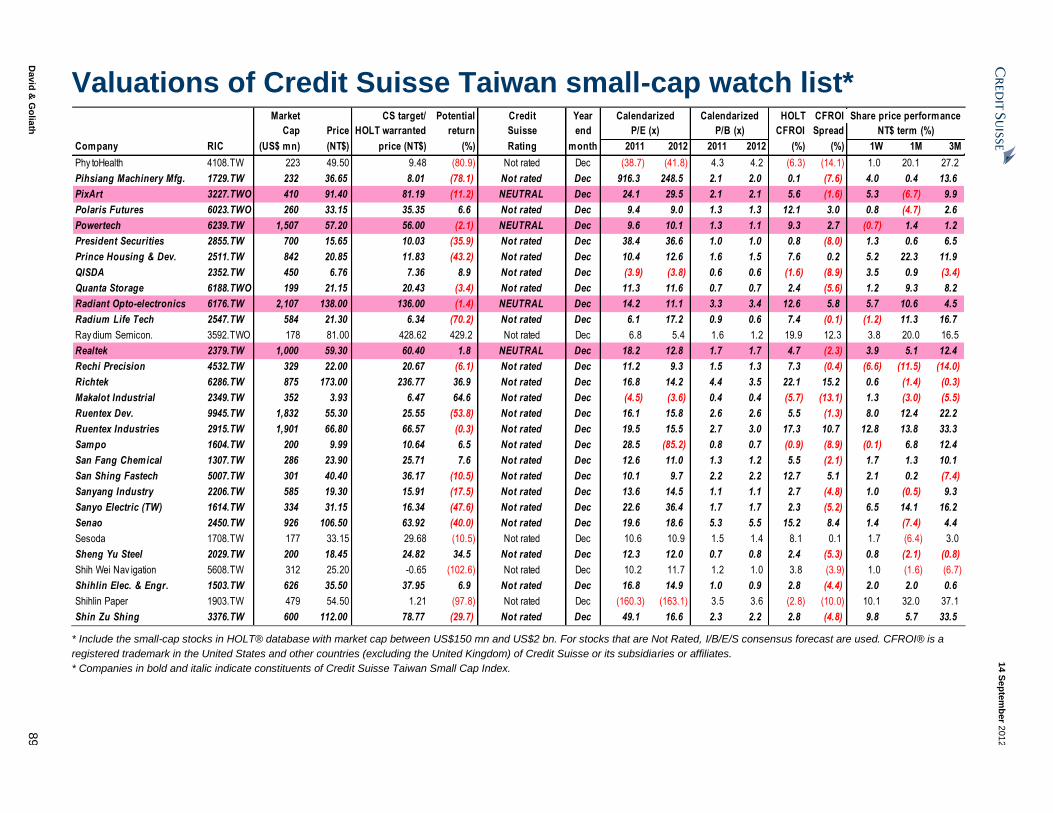

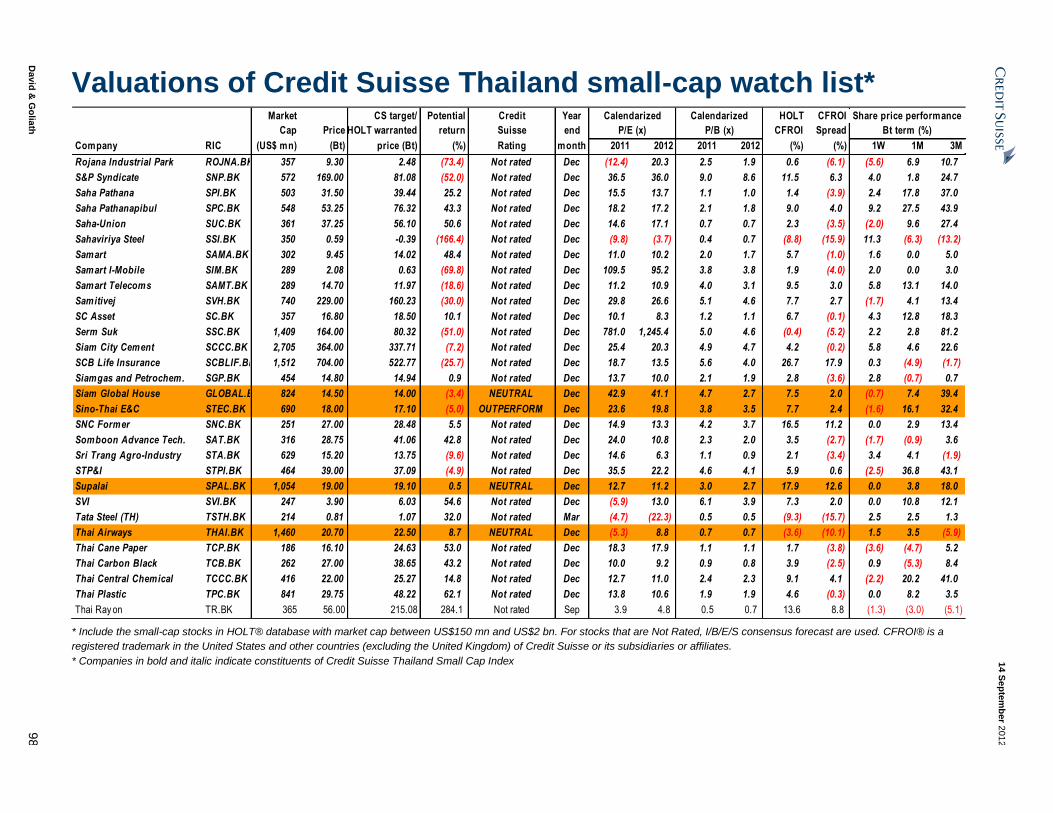

david & goliath - credit suisse

TRANSCRIPT

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

14 September 2012

Asia Pacific

Equity Research

Small Cap Companies

David & Goliath WEEKLY ANALYSIS

Raising hope on low expectations

Share price performance of China small caps, which run their businesses in one

of the world’s fastest growing economies, has been heartrending in the past

three years – they have underperformed in the region for three consecutive

years with a negative return of 31% since 2010. The 2012 consensus earnings

growth has been revised from a growth of 22% to a decline of 13% so far.

Although the lagging sell-side analysts should not have done their earnings

downgrades for 2012, D&G believes the forward-looking market has. In view of

a few more metrics that D&G keeps score of, D&G has turned bullish on China

small caps, as explained in his new report “Hope and Recovery” (link to report).

On the back of fuelling expectations of a Fed easing environment, some laggard

markets, like Korea and HK are catching up, while the outperformance of

ASEAN markets peaked in late July. In view of the high proportion of 66% of

small caps trading below book and easier earnings comparison in 4Q12 and

1H13 with lower bases, D&G expects China small caps to catch up next.

Amid an uncertain economic outlook, fundamental analysis continues to lag the

stock price movement in the current market scenario, making D&G’s buy lists in the

report look feebly convincing to some investors, and thus subject to scepticism.

D&G understands that favourable risk-reward attributes after a significant stock

price decline usually work exceptionally well during a market rebound. D&G also

understands that when the fundamentals of small caps are confirmed to improve,

their share prices may have already been moving for two months.

As a small-cap analyst, D&G is lonely, as always. D&G also fears of being

popular as it usually denotes a market peaking.

Charts of the week

Returns of MSCI large and small-caps (%) China small caps look attractive 2012 YTD -2M

Market Small MSCI Small MSCI

Thailand 31.8 19.2 11.1 2.8 Sing 28.7 22.0 8.3 4.4 Taiwan 17.3 8.1 6.3 8.6 India 14.6 11.9 -2.6 3.9 AxJ 9.8 9.0 3.9 5.7 Malaysia 8.4 6.5 0.1 2.4 HK 7.7 14.1 5.5 7.1 Korea 2.1 10.6 9.7 9.6 China -1.8 1.7 -1.7 2.6 Indonesia -4.2 -0.6 -7.1 3.9

S'pore

HK

IndoAxJ

Korea

M'siaChina

Taiwan

Thailand

India

-40

-20

0

20

40

60

-2.0 0.0 2.0 4.0 6.0

P/E

dis

coun

t (%

)

PEG (x)

Source: Datastream, Credit Suisse estimates

Davids of the week:

Hong Kong: Chow Sang Sang – we initiate coverage of the jeweler with margin

improvement from the rising gold prices; 8.5x 13E P/E, 17% potential upside (p. 10)

Taiwan: Spreadtrum – we raise our forecasts and target price on smartphones and modest GM recovery; 10.1x 13E P/E, 28% potential upside (p. 81)

Research Analysts

Kenny Lau, CFA

852 2101 7914

Eva Wang

852 2101 7365

Anantha Narayan

91 22 67773730

Teddy Oetomo

6221 2553 7911

Minseok Sinn

822 3707 8898

Loke Foong Wai

603 2723 2082

Su Tye Chua

65 6212 3014

Chai Techakumpuch

662 614 6211

14 September 2012

David & Goliath 2

The tales of Davids

Hong Kong

Luk Fook – Major beneficiary of QE3 10

Chow Sang Sang – Most stable earnings growth, but cheapest valuation 10

Pacific Textiles – 1HFY3/13 Preview: Cash cow 11

Texwinca – 1H FY3/13E preview: Waiting for the worst to be over 11

Pacific Basin Shipping – New report: RoRo exit a step in the right direction 12

China

Green Dragon Gas – New report: Darkest before dawn 20

Lonking – Comment on August sales 20

India

Multi Commodity Exchange of India – MCX-SX's equity product kicks off 30

Emami – Key concerns to abate 30

Hexaware Technologies – Management discussions indicate that the company remains well placed 31

Gujarat State Petronet – The new tariff order limits downside. Volume growth key to upside 31

Indonesia

ACE Hardware – ACES expects no impact from the recent regulation changes 45

Mitra Adiperkasa – MAPI’s F&B business may have limited impact from recent regulation 45

Lippo Cikarang – Mixing industrial with residential 46

Surya Semesta Internusa – Additional land bank is the key 46

Bekasi Fajar Industrial Estate – BEST is getting even better 47

Kawasan Industri Jababeka – Offering additional facilities 47

Korea

Shinsegae – Weak trends so far due to time difference in Choosuk holiday 53

Malaysia

SP Setia – Lower earnings forecasts from dilution of proposed placement 65

Singapore

CDL Hospitality Trusts – Industry 7M12 REVPAR up strongly, by 9.4% YoY 72

Taiwan

E Ink – ePaper shipment recovery to drive the year-end rally 79

Hiwin – Inventory remains an issue 79

Novatek – New report: Resolution migration, mid-sized devices, and share gains driving future growth 80

Lextar – Uncertain synergy from the Wellypower acquisition 80

Spreadtrum Communication – New report: Smartphone ramp gains momentum 81

14 September 2012

David & Goliath 3

Taiwan Surface Mounting Tech – Softer outlook ahead with slower-than-expected margin expansion 81

Thailand

Major Cineplex – Ticket sales likely to fall YoY again in 3Q 95

14 September 2012

David & Goliath 4

Small-cap index performance Figure 1: Non-Japan Asia Figure 2: China

80

90

100

110

09/11 12/11 03/12 06/12 09/12

MSCI AxJ Small Caps MSCI Asia Ex-Japan

70

80

90

100

110

09/11 12/11 03/12 06/12 09/12

MSCI China Small Caps MSCI AxJ Small Caps MSCI China

Figure 3: Hong Kong Figure 4: India

65

75

85

95

105

09/11 12/11 03/12 06/12 09/12

MSCI HK Small Caps MSCI AxJ Small Caps MSCI HK

75

85

95

105

115

09/11 12/11 03/12 06/12 09/12

MSCI India Small Caps MSCI AxJ Small Caps MSCI India

Figure 5: Indonesia Figure 6: South Korea

70

80

90

100

110

120

09/11 12/11 03/12 06/12 09/12

MSCI Indonesia Small Caps MSCI AxJ Small Caps MSCI Indonesia

80

90

100

110

120

09/11 12/11 03/12 06/12 09/12

MSCI Korea Small Caps MSCI AxJ Small Caps MSCI Korea

Figure 7: Malaysia Figure 8: Singapore

80

90

100

110

120

09/11 12/11 03/12 06/12 09/12

MSCI Malaysia Small Caps MSCI AxJ Small Caps MSCI Malaysia

80

90

100

110

09/11 12/11 03/12 06/12 09/12

MSCI Singapore Small Caps MSCI AxJ Small Caps MSCI Singapore

Figure 9: Taiwan Figure 10: Thailand

75

85

95

105

115

09/11 12/11 03/12 06/12 09/12

MSCI Taiwan Small Caps MSCI AxJ Small Caps MSCI Taiwan

75

85

95

105

115

125

09/11 12/11 03/12 06/12 09/12

MSCI Thailand Small Caps MSCI AxJ Small Caps MSCI Thailand

Source: MSCI, Credit Suisse estimates Source: MSCI, Credit Suisse estimates

14 September 2012

David & Goliath 5

Small-cap index valuation and sector performance Figure 11: Valuation

Index Net profit Book value Trailing Index performance Country/ weighting (US$ mn) (US$ mn) P/E (x) P/B (x) Yield (local currency term)

region (%) 2011 2012 2011 2012 2011 2012 2011 2012 (%) 1W 1M 3M 6M 1Y 2Y

China 13.7 20,867 18,035 180,798 203,076 7.5 8.7 0.9 0.8 2.9 4.5 1.2 (2.9) (17.0) (8.1) (34.7) Hong Kong 7.8 8,686 8,811 103,921 111,590 10.3 10.1 0.9 0.8 3.4 2.8 2.6 3.3 (11.3) (5.9) (20.1) India 16.9 12,585 15,135 127,921 146,011 15.3 12.7 1.5 1.3 1.6 2.4 1.1 3.8 (4.9) (0.2) (27.3) Indonesia 7.4 5,315 6,223 42,322 47,493 16.0 13.7 2.0 1.8 1.8 1.5 0.2 2.1 (1.5) 8.9 37.1 Korea 15.3 8,554 13,736 157,276 168,445 20.4 12.7 1.1 1.0 1.3 2.2 5.1 10.0 (4.7) 0.9 (5.2) Malaysia 7.9 6,182 6,429 57,834 61,662 14.6 14.0 1.6 1.5 3.2 (0.3) (3.2) 2.6 1.2 14.0 16.8 Singapore 8.2 7,830 7,243 81,117 88,611 12.0 13.0 1.2 1.1 3.2 2.8 4.1 10.7 2.3 9.9 (8.6) Taiwan 15.8 7,528 8,422 136,793 143,247 24.0 21.5 1.3 1.3 3.8 2.7 2.1 4.5 (8.4) 1.6 (17.3) Thailand 7.0 3,310 4,314 40,684 43,568 24.1 18.5 2.0 1.8 2.7 1.7 6.5 13.5 14.5 27.8 28.7 NJA 100.0 80,857 88,347 928,666 1,013,702 14.1 12.9 1.2 1.1 2.6 2.9 2.6 6.0 (7.7) (1.6) (16.2)

Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance Non-Japan Asia weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term)

Sector (%) 2011 2012 2011 2012 2011 2012 2011 2012 1W 1M 3M 6M 1Y 2Y

Consumer Discretionary 19.4 15,224 16,847 136,775 150,811 14.6 13.2 1.6 1.5 2.9 3.4 6.5 (6.6) (0.9) (2.7) Consumer Staples 10.4 7,732 8,358 66,771 72,383 15.4 14.3 1.8 1.6 1.6 2.2 10.0 3.0 9.9 4.4 Energy 3.2 1,907 3,100 29,981 35,694 19.4 11.9 1.2 1.0 3.0 (0.4) (0.7) (21.4) (16.6) (28.8) Financials 18.8 25,556 24,592 247,110 272,557 8.4 8.7 0.9 0.8 3.4 2.3 5.7 (4.5) 2.6 (16.2) Health Care 5.0 2,653 3,001 25,739 28,457 21.5 19.0 2.2 2.0 2.2 3.8 17.4 11.5 13.9 (7.6) Industrials 15.5 8,123 11,437 155,086 167,769 21.8 15.5 1.1 1.1 3.0 1.5 3.2 (13.2) (6.8) (27.0) Information Technology 12.0 5,152 6,517 104,504 111,757 26.6 21.1 1.3 1.2 4.0 4.7 4.5 (11.1) 0.2 (23.9) Materials 11.2 12,507 11,533 125,237 133,753 10.2 11.1 1.0 1.0 2.9 1.7 3.9 (15.1) (13.3) (19.7) Telecommunication Services 1.7 (261) 83 8,998 9,460 (72.2) 226.1 2.1 2.0 2.3 7.4 14.8 3.4 2.5 (9.8) Utilities 2.8 2,264 2,879 28,463 31,061 14.2 11.2 1.1 1.0 2.4 1.8 4.7 (10.5) (6.9) (32.4)

Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance China weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term)

Sector (%) 2011 2012 2011 2012 2011 2012 2011 2012 1W 1M 3M 6M 1Y 2Y

Consumer Discretionary 21.8 3,708 3,883 26,498 29,990 9.2 8.8 1.3 1.1 4.0 1.9 (5.2) (25.6) (17.9) (41.0) Consumer Staples 8.8 1,340 1,360 12,221 13,785 10.3 10.2 1.1 1.0 2.5 (1.4) (6.6) (18.0) (15.3) (42.2) Energy 4.4 605 618 5,262 6,026 11.3 11.1 1.3 1.1 4.8 3.1 (1.5) (29.8) (7.0) (48.0) Financials 18.8 6,717 5,039 55,041 62,348 4.4 5.8 0.5 0.5 6.2 1.9 1.4 6.8 15.7 (14.4) Health Care 6.3 545 674 4,889 5,473 18.0 14.6 2.0 1.8 1.7 1.3 11.2 4.7 17.2 (35.8) Industrials 14.6 3,146 2,533 29,467 33,917 7.2 9.0 0.8 0.7 6.1 0.6 (7.7) (20.6) (9.0) (33.3) Information Technology 5.7 536 563 10,188 10,872 16.6 15.8 0.9 0.8 4.7 2.5 (2.8) (25.8) (22.9) (47.2) Materials 14.0 3,704 2,465 28,834 31,505 5.9 8.8 0.8 0.7 4.2 (0.0) (8.3) (29.8) (21.3) (37.2) Telecommunication Services 0.3 59 62 410 436 7.8 7.5 1.1 1.1 2.1 (2.6) 7.1 (15.2) (14.8) (46.0) Utilities 5.3 506 838 7,988 8,725 16.4 9.9 1.0 1.0 4.7 3.5 8.4 (5.1) 14.8 (21.4)

Source: DataStream, Credit Suisse estimates

14 September 2012

David & Goliath 6

Index Net profit Book value Index performance Hong Kong weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term)

Sector (%) 2011 2012 2011 2012 2011 2012 2011 2012 1W 1M 3M 6M 1Y 2Y

Consumer Discretionary 40.4 3,428 3,315 27,690 30,970 10.5 10.9 1.3 1.2 2.7 3.7 5.1 (9.9) (3.4) 7.9 Consumer Staples 4.4 274 315 2,272 2,508 14.5 12.6 1.7 1.6 0.9 (1.7) 1.0 (0.0) 8.4 (10.3) Energy 2.9 (353) (73) 3,198 3,329 (7.3) (34.9) 0.8 0.8 1.7 (13.1) (20.6) (43.2) (49.1) (63.9) Financials 18.8 2,381 2,353 34,473 36,830 7.1 7.1 0.5 0.5 3.6 4.9 6.1 (7.7) 1.8 (26.5) Health Care 2.1 39 72 1,503 1,626 48.7 26.7 1.3 1.2 1.5 10.6 34.7 1.7 7.4 (51.2) Industrials 12.0 1,172 915 15,250 15,407 9.1 11.7 0.7 0.7 4.6 4.7 2.5 (10.8) (11.9) (25.2) Information Technology 6.6 941 924 10,737 11,462 6.3 6.4 0.5 0.5 6.7 3.7 3.1 (22.4) (22.7) (51.6) Materials 6.7 437 577 5,084 5,554 13.7 10.4 1.2 1.1 0.7 (4.7) (4.7) (23.8) (14.6) (48.0) Telecommunication Services 4.0 275 311 2,474 2,632 13.0 11.5 1.4 1.4 (2.1) (0.9) (2.2) (1.3) 13.5 33.6 Utilities 2.1 91 103 1,240 1,273 20.8 18.5 1.5 1.5 (0.5) 4.9 8.7 20.5 42.8 69.9

Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance

India weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term)

Sector (%) 2011 2012 2011 2012 2011 2012 2011 2012 1W 1M 3M 6M 1Y 2Y

Consumer Discretionary 12.7 1,099 1,339 12,054 13,984 22.3 18.3 2.0 1.8 2.1 1.0 5.8 (0.5) (2.2) (16.9) Consumer Staples 9.6 519 577 4,797 4,649 35.7 32.1 3.9 4.0 (0.0) 5.7 15.1 19.1 16.4 5.2 Energy 4.1 41 471 6,663 7,223 192.3 16.9 1.2 1.1 1.9 (1.9) (0.9) (11.5) (6.0) (49.5) Financials 18.9 4,980 5,502 43,092 50,383 7.3 6.6 0.8 0.7 2.9 (1.9) (5.4) (18.8) (9.1) (41.5) Health Care 9.5 753 902 7,183 7,866 24.2 20.2 2.5 2.3 3.1 5.0 18.8 24.9 28.2 20.2 Industrials 17.8 1,869 2,372 21,897 25,091 18.4 14.5 1.6 1.4 2.6 (2.1) (3.3) (16.9) (14.9) (47.1) Information Technology 6.6 1,070 1,264 5,197 6,320 11.9 10.1 2.4 2.0 7.0 9.0 14.4 15.0 31.4 (0.6) Materials 13.2 2,053 2,385 14,910 17,051 12.4 10.7 1.7 1.5 2.3 4.2 8.8 0.2 8.9 (8.3) Telecommunication Services 1.2 (691) (582) 1,859 1,882 (3.2) (3.8) 1.2 1.2 (0.3) (3.5) 3.1 (10.3) (12.1) (48.3) Utilities 6.3 891 904 10,269 11,564 13.5 13.3 1.2 1.0 0.3 (3.5) (7.2) (25.6) (26.0) (51.8)

Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance Indonesia weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term)

Sector (%) 2011 2012 2011 2012 2011 2012 2011 2012 1W 1M 3M 6M 1Y 2Y

Consumer Discretionary 21.9 740 982 5,641 6,168 25.1 19.0 3.3 3.0 2.1 1.2 6.8 18.9 52.9 162.8 Consumer Staples 15.7 754 838 3,976 4,532 17.7 15.9 3.4 2.9 2.3 0.7 8.3 5.3 10.7 36.8 Energy 9.5 666 851 5,742 6,675 12.1 9.5 1.4 1.2 3.6 (6.5) (6.1) (39.9) (43.0) (34.1) Financials 25.0 1,686 2,035 12,914 14,746 12.6 10.4 1.6 1.4 1.0 (0.4) (2.8) (5.0) (0.3) 20.3 Health Care 3.0 139 155 751 791 18.1 16.4 3.4 3.2 5.7 7.8 12.2 32.0 21.4 96.2 Industrials 9.0 473 558 3,908 4,378 16.3 13.8 2.0 1.8 (2.2) 4.6 7.0 9.0 37.7 92.6 Information Technology 1.0 41 59 281 323 19.7 13.7 2.9 2.5 0.9 (3.5) 16.9 29.6 27.3 209.3 Materials 9.6 823 682 8,164 8,841 9.9 12.0 1.0 0.9 2.4 (1.1) 1.5 (18.8) (17.2) (26.4) Telecommunication Services 5.4 (6) 62 946 1,040 (765.9) 73.5 4.8 4.4 (0.2) (0.2) (1.7) (12.0) (40.5) 15.5

Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance Korea weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term)

Sector (%) 2011 2012 2011 2012 2011 2012 2011 2012 1W 1M 3M 6M 1Y 2Y

Consumer Discretionary 23.9 2,467 3,384 26,905 29,335 16.9 12.3 1.5 1.4 1.7 7.8 8.4 1.8 2.5 23.3 Consumer Staples 12.3 1,432 1,878 18,404 19,409 15.1 11.5 1.2 1.1 1.9 7.9 19.5 23.7 24.3 40.6 Energy 0.5 111 137 877 908 8.4 6.8 1.1 1.0 2.5 2.5 28.5 19.4 14.3 71.5 Financials 10.0 1,823 1,993 22,902 24,484 9.6 8.8 0.8 0.7 2.6 0.9 4.6 (15.6) 3.0 (24.2) Health Care 5.1 370 271 4,988 5,389 24.1 32.8 1.8 1.7 0.7 5.6 21.5 18.3 6.8 (16.3) Industrials 17.0 (1,076) 1,310 31,582 33,094 (27.6) 22.7 0.9 0.9 2.8 2.9 10.4 (12.5) (5.5) (27.5) Information Technology 13.8 848 1,477 11,290 13,125 28.5 16.3 2.1 1.8 2.7 5.8 6.1 (6.3) 12.6 2.8 Materials 15.7 2,374 2,963 35,492 37,645 11.6 9.3 0.8 0.7 2.3 2.5 8.4 (14.7) (20.6) (9.7) Telecommunication Services 0.5 (13) 19 971 990 (75.6) 49.0 1.0 1.0 7.9 21.2 26.1 6.6 2.9 (32.0) Utilities 1.0 219 303 3,866 4,066 8.3 6.0 0.5 0.4 0.6 7.8 19.6 13.0 9.1 12.2

Source: DataStream, Credit Suisse estimates

14 September 2012

David & Goliath 7

Index Net profit Book value Index performance Malaysia weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term)

Sector (%) 2011 2012 2011 2012 2011 2012 2011 2012 1W 1M 3M 6M 1Y 2Y

Consumer Discretionary 16.8 1,257 1,178 8,060 8,826 12.1 12.9 1.9 1.7 0.8 (1.4) 6.1 1.6 12.2 13.8 Consumer Staples 24.7 1,732 1,615 11,066 11,830 12.8 13.8 2.0 1.9 (1.2) (3.8) 3.6 4.1 25.9 51.4 Energy 2.6 51 146 2,045 2,145 46.8 16.2 1.2 1.1 (0.8) (3.0) (4.2) (5.2) 2.3 28.0 Financials 24.6 1,937 1,557 17,883 18,708 11.5 14.2 1.2 1.2 0.3 (2.0) 5.7 6.8 18.4 22.5 Health Care 5.1 263 298 1,586 1,783 17.4 15.3 2.9 2.6 (0.7) (3.8) 5.1 8.6 28.3 (0.3) Industrials 16.7 279 783 9,182 9,893 53.9 19.2 1.6 1.5 (0.5) (3.0) (1.5) (7.7) 0.8 (5.9) Information Technology 1.3 74 176 988 1,102 16.0 6.7 1.2 1.1 (0.4) (22.7) (26.6) (15.4) 15.2 (34.5) Materials 7.3 544 543 6,344 6,579 12.2 12.2 1.0 1.0 (0.9) (4.8) 1.2 0.4 6.8 9.7 Telecommunication Services 0.7 43 43 645 773 14.1 14.2 0.9 0.8 (2.1) (2.1) (1.5) (10.2) 12.1 (0.6) Utilities 0.2 3 89 35 23 66.0 2.0 5.0 7.5 0.8 1.5 0.8 (5.0) 9.1 (52.7)

Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance Singapore weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term)

Sector (%) 2011 2012 2011 2012 2011 2012 2011 2012 1W 1M 3M 6M 1Y 2Y

Consumer Discretionary 8.2 491 482 8,576 8,934 15.7 16.0 0.9 0.9 5.1 5.5 16.1 (0.6) 0.3 (18.2) Consumer Staples 16.5 1,160 1,232 9,628 10,665 13.3 12.6 1.6 1.5 1.4 0.7 12.4 (1.2) 11.7 (7.3) Energy 6.0 535 667 4,125 7,273 10.5 8.4 1.4 0.8 2.3 15.1 22.0 10.5 35.3 (10.1) Financials 31.5 2,825 2,498 31,838 33,334 10.5 11.8 0.9 0.9 3.3 5.1 13.3 12.4 17.0 2.7 Health Care 5.2 296 337 3,328 3,793 16.5 14.5 1.5 1.3 (0.6) (0.6) 6.2 (4.8) 3.7 19.0 Industrials 22.2 1,765 1,233 16,870 17,768 11.8 16.9 1.2 1.2 2.1 2.6 4.6 (6.7) 3.9 (19.7) Information Technology 5.1 302 381 4,056 4,003 16.0 12.6 1.2 1.2 4.8 5.2 4.0 (5.9) 10.2 (9.0) Materials 1.4 222 171 1,625 1,682 6.1 8.0 0.8 0.8 3.7 6.3 9.3 (13.7) (9.1) (55.7) Telecommunication Services 2.2 134 128 264 284 15.1 15.8 7.7 7.1 6.6 7.5 11.4 9.2 6.2 21.3 Utilities 1.7 100 113 808 874 15.9 13.9 2.0 1.8 2.9 0.5 9.2 (4.3) (7.8) (29.0)

Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance Taiwan weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term)

Sector (%) 2011 2012 2011 2012 2011 2012 2011 2012 1W 1M 3M 6M 1Y 2Y

Consumer Discretionary 15.7 1,460 1,568 16,132 16,748 19.5 18.1 1.8 1.7 3.3 0.0 9.9 (3.8) 6.7 6.4 Consumer Staples 2.2 173 168 1,992 2,118 23.0 23.7 2.0 1.9 3.5 0.9 15.9 0.2 6.1 27.2 Financials 13.1 2,229 2,299 20,444 22,053 10.6 10.3 1.2 1.1 3.2 6.4 10.8 (1.5) 5.8 (0.1) Health Care 1.2 122 135 942 1,051 18.5 16.6 2.4 2.1 1.4 0.2 2.9 1.9 24.4 7.7 Industrials 13.7 530 1,328 19,736 20,708 46.9 18.7 1.3 1.2 2.0 (0.6) 4.1 (8.8) 3.5 (11.1) Information Technology 41.9 1,181 1,413 59,693 62,403 64.1 53.6 1.3 1.2 2.7 3.2 1.4 (12.0) 0.9 (31.2) Materials 11.9 1,797 1,473 17,571 17,885 11.9 14.6 1.2 1.2 2.8 0.7 1.9 (8.4) (10.6) 2.8 Utilities 0.2 35 37 284 281 11.4 10.7 1.4 1.4 0.5 1.8 0.5 (14.3) 5.5 24.7

Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance Thailand weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term)

Sector (%) 2011 2012 2011 2012 2011 2012 2011 2012 1W 1M 3M 6M 1Y 2Y

Consumer Discretionary 19.3 574 716 5,220 5,856 26.9 21.5 3.0 2.6 1.0 5.5 11.5 17.2 37.2 71.9 Consumer Staples 8.0 348 374 2,415 2,888 18.3 17.0 2.6 2.2 1.6 5.3 16.2 29.7 57.7 94.3 Energy 3.4 252 282 2,070 2,116 10.8 9.6 1.3 1.3 2.2 0.5 1.3 (14.6) 7.6 45.5 Financials 22.3 977 1,316 8,525 9,672 18.2 13.5 2.1 1.8 1.5 4.2 9.9 12.1 12.6 1.2 Health Care 5.0 126 157 570 686 31.5 25.4 7.0 5.8 (1.4) 5.9 31.2 55.3 97.5 150.4 Industrials 13.6 (36) 404 7,193 7,513 (300.2) 26.9 1.5 1.4 1.7 8.2 10.9 5.8 19.8 2.1 Information Technology 3.9 160 260 2,075 2,147 19.2 11.9 1.5 1.4 2.7 6.7 9.6 1.1 10.8 (7.1) Materials 11.5 553 274 7,213 7,011 16.6 33.5 1.3 1.3 2.3 5.2 11.2 2.9 14.7 13.4 Telecommunication Services 5.5 (64) 40 1,430 1,423 (69.6) 111.7 3.1 3.1 4.7 25.9 42.7 38.7 50.1 50.9 Utilities 7.5 419 492 3,973 4,255 14.4 12.2 1.5 1.4 3.0 6.6 16.6 39.6 50.9 49.8

Source: DataStream, Credit Suisse estimates

14 September 2012

David & Goliath 8

D&G15 portfolio – the small-cap picks in the region

Mkt Cap Price Year P/E (x) Potential CS

Company Ticker (US$ mn) Cncy Price End FY1 FY2 TP Gain (%) Rating China/Hong Kong

ASM Pacific* 0522.HK 4,718 HKD 92.00 Dec 22.7 20.0 73.50 (20.1) U

Haitian* 1882.HK 1,624 HKD 7.89 Dec 11.0 10.9 6.50 (17.6) U

KWG Property 1813.HK 1,679 HKD 4.50 Dec 5.1 5.3 4.70 4.4 N

Lee & Man Paper* 2314.HK 1,935 HKD 3.20 Mar 10.4 9.0 2.75 (14.1) U

Skyworth 0751.HK 1,151 HKD 3.30 Mar 5.4 4.8 5.70 72.7 O

Techtronic* 0669.HK 2,981 HKD 12.68 Dec 14.7 13.2 9.65 (23.9) N

Varitronix 0710.HK 111 HKD 2.66 Dec 4.6 4.7 3.65 37.2 O

VTech 0303.HK 3,037 HKD 94.05 Mar 14.2 13.2 84.00 (10.7) N

Source: Company data, Credit Suisse estimates * ASM Pacific, Haitian, Lee & Man Paper, and Techtronic are SHORT ideas.

14 September 2012

David & Goliath 9

Hong Kong – Street talk * C C Land (1224.HK, HK$1.65, NR) announces Aug contracted sales. C C Land announced that it recorded contracted sales for the month Aug of Rmb645 mn, representing an increase of 185% YoY. (10-Sep)

40

60

80

100

120

09/11 12/11 03/12 06/12 09/12

C C Land MSCI Hong Kong

Yue Yuen (0551.HK, HK$24.60, N, TP HK$25.70) announces revenue for August. Yue Yuen announced that the net consolidated operating revenue for the month Aug 2012 was US$567 mn. And the net consolidated accumulative operating revenue for the eight months ended Aug 2012 amounted to US$4.81 bn. (11-Sep)

65

80

95

110

125

140

09/11 12/11 03/12 06/12 09/12

Yue Yuen Industrial Holding MSCI Hong Kong

Sunevision (8008.HK, HK$1.64, NR) announces final results. Sunvision recorded a profit attributable to owners of HK$450 mn for 1H12. The firm declared the payment of a final dividend of HK$0.082 per share in respect of the year. (12-Sep)

70

100

130

160

190

09/11 12/11 03/12 06/12 09/12

Sunevision Holdings MSCI Hong Kong

China Overseas Grand Oceans (0081.HK, HK$7.95, NR) sales value for August decreased by 8% to HK$1.06 bn. China Overseas Grand Oceans reported a property sales value of HK$1.06 bn for Aug, down 8% MoM. In the same month its property sales area jumped 33% MoM to 103,700 sqm. From Jan to Aug of this year the company reaped 695,700 sqm in property sales area and HK$10.22 bn in sales value, accounting for 79% of its yearly target of HK$13 bn. (13-Sep)

40

60

80

100

120

140

09/11 12/11 03/12 06/12 09/12

China Overseas Grand Oceans MSCI Hong Kong

*Source: China Press Digest, CIS, DataStream

14 September 2012

David & Goliath 10

Hong Kong – Company updates Luk Fook (0590.HK, HK$22.45, N [V], TP HK$23.30) Chow Sang Sang (0116.HK, HK$17.06, O, TP HK$20.00)

Major beneficiary of QE3

■ The low gold price hedging ratio of only 20% has led to a high

correlation between Luk Fook’s performance and the gold prices,

given 80% of the holding gain of inventory passes on directly to

the gross margin.

■ Therefore, we believe the less bearish gold price outlook should

justify the re-rating of Luk Fook from its current valuation of an 8-

9x CY13E P/E.

■ The worse-than-expected rental pressure has offset the benefits

from the recent positive gold price momentum. We have lowered

our FY3/13-FY3/14 earnings forecasts by 0.4-2.9%. Note,

potential gross margin improvement is not priced in yet, in our

view.

■ Luk Fook traded as high as a 16x CY13E P/E on the gold price

rally in July 2011. We set our target price of HK$23.3 based on a

10x CY13E P/E (previously 8x FY3/13E P/E), with the more

aggressive multiple assigned on the back of a less bearish gold

price outlook. However, with only 9% potential upside to our

target price, we maintain our NEUTRAL rating on the stock.

Most stable earnings growth, but cheapest valuation

■ We initiate coverage on Chow Sang Sang (CSS) with an

OUTPERFORM rating and a target price of HK$20.0 based on

10x CY2013 P/E, which implies 0.56x PEG. We like its stable

earnings outlook and 100% self-operated model which allows a

flexible expansion strategy as well as prudent inventory

management.

■ Despite the overall weakness in gold price as well as jewellery

demand, CSS still registered a solid SSSG of around 16% YoY in

June quarter 2012 in Hong Kong and outperformed the overall

Hong Kong market growth of 6.8% YoY. Stripping out the holding

gain/loss, net profits saw 10.6% YoY growth in 1H12.

■ With the negative YoY change in gold price narrowing, we expect

Chow Sang Sang’s earnings momentum to bottom out in 3Q2012

and recover from 4Q onward.

■ CSS is trading around lowest valuation range, which in our view

is not justified. We believe CSS stable earnings outlook deserves

to trade at least the same valuation of Luk Fook (~10x CY2013

P/E). Risks on CSS include unfavourable gold price movement

and strong reliance on mainland Chinese visitors to HK/Macau.

Bbg/RIC 21.35

23.30 (16.50)

589.11 9

3.4

8.5

Free float (%) 54.7 Performance 1M 3M 12M

Absolute (%) 12.1 42.9 (44.1)

Relativ e (%) 13.4 35.9 (43.6)

Year 03/11A 03/12A 03/13E 03/14E 03/15E

8,091 11,907 13,498 16,150 19,280

1,083 1,665 1,527 1,889 2,255

866 1,334 1,181 1,438 1,686

1.71 2.43 2.00 2.44 2.86

n.a. n.a. (3) 0 1

n.a. n.a. 2.15 2.56 3.01

58.3 42.0 -17.3 21.8 17.3

12.5 8.8 10.6 8.7 7.5

3.2 4.3 4.2 5.1 6.0

10.7 6.6 6.8 5.2 4.2

3.2 2.1 1.9 1.7 1.5

34.1 29.6 19.4 20.4 21.0

-27.9 -27.2 -32.8 -35.2 -36.2

38.2 - 14.7

12,577.5/ 1,621.6

ROE (%)

Note1:Luk Fook Holdings (International) Limited is an investment holding company. It is engaged in the sourcing, designing, wholesaling and retailing of a

range of gold jewellery, gold ornaments, gem-set jewellery, jadeite, gemstones, and other accessory items..

Mkt cap (HK$/US$ mn)Daily trad v al - 6m av g (US$ mn)

Major shareholders Luk Fook (Control) Limited

Net debt(cash)/equity (%)

Rev enue (HK$ mn)

52-w k range (HK$)

590 HK / 0590.HK

N (N) [V]

Daily trad v ol - 6m av g (mn)

Rating (prev. rating)

Shares outstanding (mn)

Price (07 Sep 12 , HK$)

TP (prev. TP HK$)

Est. pot. % chg. to TP

EBITDA (HK$ mn)

Net profit (HK$ mn)

EPS (HK$)

- Change from prev . EPS (%)

- Consensus EPS (HK$)

EPS grow th (%)

P/E (x )

Div idend y ield (%)

EV/EBITDA (x )

P/B (x )

Bbg/RIC 15.98

20.00 (NA)

676.92 25

0.8

1.8

Free float (%) 43.8 Performance 1M 3M 12M

Absolute (%) (1.4) 0.1 (38.9)

Relativ e (%) 0.0 (6.9) (38.3)

Year 12/10A 12/11A 12/12E 12/13E 12/14E

11,705 17,158 19,651 23,917 29,089

1,077 1,557 1,485 1,937 2,521

757 1,094 1,052 1,354 1,793

1.16 1.62 1.55 2.00 2.65

n.a. n.a. 0 0 0

n.a. n.a. 1.46 1.81 2.18

21.9 39.0 -3.8 28.7 32.5

13.7 9.9 10.3 8.0 6.0

2.7 3.8 3.9 5.0 6.6

10.8 7.9 8.4 6.2 5.1

1.8 1.7 1.5 1.3 1.1

15.8 18.2 15.5 17.3 19.8

14.8 23.0 21.6 14.7 19.3

26.2 - 15.0

10,817.2/ 1,394.6

ROE (%)

Note1:Chow Sang Sang mainly engaged in the manufacture and retail of gold, gem-set jewellery products and watches (> 70% of revenue in 2011),

wholesale of precious metals, securities and commodity broking, and gold bullion trading and property investment..

Mkt cap (HK$/US$ mn)Daily trad v al - 6m av g (US$ mn)

Major shareholders Ev erw in Co. Ltd. (17.73%)

Net debt(cash)/equity (%)

Rev enue (HK$ mn)

52-w k range (HK$)

116 HK / 0116.HK

O (NA)

Daily trad v ol - 6m av g (mn)

Rating (prev. rating)

Shares outstanding (mn)

Price (07 Sep 12 , HK$)

TP (prev. TP HK$)

Est. pot. % chg. to TP

EBITDA (HK$ mn)

Net profit (HK$ mn)

EPS (HK$)

- Change from prev . EPS (%)

- Consensus EPS (HK$)

EPS grow th (%)

P/E (x )

Div idend y ield (%)

EV/EBITDA (x )

P/B (x )

Price performance vs. MSCI Hong Kong Price performance vs. MSCI Hong Kong

30

50

70

90

110

09/11 11/11 01/12 03/12 05/12 07/12 09/12

Luk Fook MSCI Hong Kong

50

65

80

95

110

09/11 11/11 01/12 03/12 05/12 07/12 09/12

Chow Sang Sang MSCI Hong Kong

Gabriel Chan, CFA / Research Analyst / 852 2101 6523 /

Extracted from The Asian Daily 10 Sep 2012

Gabriel Chan, CFA / Research Analyst / 852 2101 6523 /

Extracted from The Asian Daily 10 Sep 2012

14 September 2012

David & Goliath 11

Hong Kong – Company updates Pacific Textiles (1382.HK, HK$5.01, O, TP HK$5.60) Texwinca (0321.HK, HK$5.33, N, TP HK$5.50)

1HFY3/13 Preview: Cash cow

■ Our recent channel checks indicated that the overall environment

remains tough for export textile manufacturers in general.

However, we believe Pacific Textiles is still in a better shape

among its competitors despite near term pressure.

■ Reasons behind operational outperformance include: (1)

exposure to synthetic yarns and fabrics which has less China-

international price difference; (2) usage of cheaper imported

cotton yarns from countries like Pakistan and India; (3) well

controlled inventory position and (4) rich cash on hand.

■ We found the company’s cash on hand is close to historical

highs, therefore there is a good chance for another special

dividend.

■ We cut FY13/14E EPS by 32/12% on lower ASP and sales

volume assumptions. We believe the industry recovery is more

likely to be the theme for FY3/14E. We roll over our valuation

basis to CY13. Our new target price of HK$5.60 (from HK$5.20)

is based on 9x CY13E EPS. We believe the stock’s high dividend

yield and strong balance sheet are attractive. Maintain

OUTPERFORM rating.

1H FY3/13E preview: Waiting for the worst to be over

■ Our recent channel checks indicated that the overall environment

remains tough for export textile manufacturers. Texwinca seems

to be among the worst given its recent profit warning.

■ This time the situation is even worse than the financial crisis in

2008. We expect Texwinca to record 15% ASP decline, 5%

volume drop and only 7% gross margin in 1H FY3/13E for its

textile business.

■ Figure 2 shows that Texwinca’s gross margin contraction was

among the worst in 2H FY3/12, which raises a question about its

product competitiveness. Its inventory increase added another

concern. Having said that, the positive is the company was still

keen to hold on to cash and was in a net cash position as of last

reported.

■ Texwinca’s stock price has dropped 24% since it issued a profit

warning in mid-August (already priced in, in our view). We slash

FY13/14E EPS by 56/46% on lower ASP, volume and margin

assumptions. Accordingly, we cut our target price to HK$5.50

(from HK$9.30), based on an unchanged 9.0x P/E and CY13E

EPS. Maintain NEUTRAL.

Bbg/RIC 4.99

5.60 (5.20)

1,433.21 12

0.6

0.4

Free float (%) 30.5 Performance 1M 3M 12M

Absolute (%) (10.1) (10.3) 13.2

Relativ e (%) (10.1) (17.0) 7.7

Year 03/11A 03/12A 03/13E 03/14E 03/15E

7,181 6,420 6,234 7,421 8,370

1,394 1,215 1,113 1,373 1,570

876 893 728 936 1,094

0.61 0.62 0.51 0.65 0.76

n.a. n.a. (32) 0 0

n.a. n.a. 0.61 0.63 0.62

9.1 1.9 -18.5 28.7 16.8

8.2 8.0 9.8 7.6 6.5

6.6 14.0 5.6 7.2 8.4

4.6 4.4 4.9 3.5 2.8

1.9 1.8 1.8 1.6 1.4

24.8 23.0 18.2 21.6 22.2

-19.9 -46.6 -40.5 -49.6 -51.4

- Consensus EPS (HK$)

EPS grow th (%)

P/E (x )

Div idend y ield (%)

EV/EBITDA (x )

P/B (x )

EBITDA (HK$ mn)

Net profit (HK$ mn)

EPS (HK$)

- Change from prev . EPS (%)

Price (12 Sep 12 , HK$)

TP (prev. TP HK$)

Est. pot. % chg. to TP

52-w k range (HK$)

1382 HK / 1382.HK

O (O)

Daily trad v ol - 6m av g (mn)

Rating (prev. rating)

Shares outstanding (mn)

5.65 - 3.93

7,151.7/ 922.2

ROE (%)

Note1:Pacific Textile focuses on the manufacturing of customised knitted fabrics with the cooperation with well-known international retailer brands. It has

production sites in China, Sri Lanka and Bangladesh. Most of its fabrics are for export garments..

Mkt cap (HK$/US$ mn)Daily trad v al - 6m av g (US$ mn)

Major shareholders Mr. lp Ping Im (28.3%)

Net debt(cash)/equity (%)

Rev enue (HK$ mn)

Bbg/RIC 5.38

5.50 (9.30)

1,363.37 2

1.1

1.1

Free float (%) 45.7 Performance 1M 3M 12M

Absolute (%) (24.8) (38.0) (41.1)

Relativ e (%) (23.2) (43.1) (40.9)

Year 03/11A 03/12A 03/13E 03/14E 03/15E

11,862 13,766 13,252 14,323 15,678

1,672 1,266 988 1,374 1,767

1,133 930 630 910 1,208

0.83 0.68 0.46 0.66 0.88

n.a. n.a. (56) (46) 0

n.a. n.a. 0.81 0.95 0.94

10.8 -18.8 -32.3 44.2 32.7

6.4 7.9 11.7 8.1 6.1

9.9 9.3 5.1 7.4 9.8

4.0 5.1 6.1 3.8 2.9

1.4 1.3 1.3 1.2 1.1

23.1 17.3 11.1 15.2 18.6

-11.7 -15.2 -20.9 -31.3 -31.1

- Consensus EPS (HK$)

EPS grow th (%)

P/E (x )

Div idend y ield (%)

EV/EBITDA (x )

P/B (x )

EBITDA (HK$ mn)

Net profit (HK$ mn)

EPS (HK$)

- Change from prev . EPS (%)

Price (10 Sep 12, HK$)

TP (prev. TP HK$)

Est. pot. % chg. to TP

52-w k range (HK$)

321 HK / 0321.HK

N (N)

Daily trad v ol - 6m av g (mn)

Rating (prev. rating)

Shares outstanding (mn)

10.08 - 5.27

7,334.9/ 945.9

ROE (%)

Note 1: Texwinca Holdings Limited produces knitted fabric and yarn, which accounts for 80-90% of its operating profits. The company is also engaged in the

retail and distribution business with over 4,000 outlets in Asia and ~80% of retail sales from China.

Mkt cap (HK$/US$ mn)Daily trad v al - 6m av g (US$ mn)

Major shareholders Mr. Poon Bun Chak (48.3%)

Net debt(cash)/equity (%)

Rev enue (HK$ mn)

Price performance vs. MSCI Hong Kong Price performance vs. MSCI Hong Kong

70

85

100

115

130

09/11 11/11 01/12 03/12 05/12 07/12 09/12

Pacific Textiles MSCI Hong Kong

50

65

80

95

110

09/11 11/11 01/12 03/12 05/12 07/12 09/12

Texwinca MSCI Hong Kong

Eva Wang / Research Analyst / 852 2101 7365 /

Extracted from The Asian Daily 13 Sep 2012

Eva Wang / Research Analyst / 852 2101 7365 /

Extracted from The Asian Daily 13 Sep 2012

14 September 2012

David & Goliath 12

Hong Kong – Company updates Pacific Basin Shipping (2343.HK, HK$3.84, U [V], TP

HK$3.40)

New report: RoRo exit a step in the right direction

■ Pacific Basin (PB) has sold its RoRo division for €153 mn—

essentially for book value and drawing a line under its unhappy

association with this attempt at diversification.

■ All six vessels are being sold to Grimaldi over a three-year

period, during which time those pending transfer will be employed

on bare-boat charters, which should eliminate the losses we had

baked into our estimates.

■ While this does not add value to the business, it does remove a

drag on earnings and eases concerns about further impairments:

we have lifted our estimates for FY12 and FY13 from US$27 mn

and US$158 mn, respectively, to US$32 mn and US$175 mn.

■ Excess supply and short-term demand pressures in its core

business remains unrelenting, however, and mean that—other

than perhaps a slight bounce on this news—PB’s stock price

performance is unlikely to startle this side of Christmas. We retain

our UNDERPERFORM rating, along with a barely changed

HK$3.40 price target, based on a 0.6x P/B.

Bbg/RIC 3.40

3.40 (3.30)

1,936.58 —

4.8

2.3

Free float (%) 90 Performance 1M 3M 12M

Absolute (%) (6.3) (0.6) (5.0)

Relativ e (%) (4.7) (5.1) (4.7)

Year 12/10A 12/11A 12/12E 12/13E 12/14E

1,269 1,343 1,363 1,530 1,598

203.4 168.8 132.4 274.5 324.0

119.5 57.8 31.8 174.8 229.2

0.06 0.03 0.02 0.09 0.12

n.a. n.a. 17 10 0

n.a. n.a. 0.00 0.03 0.04

2.0 -51.8 -45.0 450.7 31.1

7.1 14.7 26.7 4.8 3.7

5.7 1.5 0.0 8.4 12.2

5.0 6.1 8.2 4.1 3.1

0.5 0.6 0.6 0.6 0.6

8.0 3.8 2.3 12.9 15.6

11.0 12.2 18.2 18.8 9.3

4.45 - 2.82

6,584.4/ 849.0

ROE (%)

Note 1: ORD/ADR=20.00. Note 2: Pacific Basin Shipping Limited is an investment holding company. It is engaged in the provision of dry bulk (primarily

vessel owning and vessel chartering) and RoRo shipping services, and services to the energy and infrastructure sector.

Mkt cap (HK$/US$ mn)Daily trad v al - 6m av g (US$ mn)

Major shareholders Aberdeen - 10%, Mondrian -

Net debt(cash)/equity (%)

Rev enue (US$ mn)

52-w k range (HK$)

2343 HK / 2343.HK

U (U) [V]

Daily trad v ol - 6m av g (mn)

Rating (prev. rating)

Shares outstanding (mn)

Price (07 Sep 12 , HK$)

TP (prev. TP HK$)

Est. pot. % chg. to TP

EBITDRAF (US$ mn)

Net profit (US$ mn)

EPS (US$)

- Change from prev . EPS (%)

- Consensus EPS (US$)

EPS grow th (%)

P/E (x )

Div idend y ield (%)

EV/EBITDRAF (x )

P/B (x )

Price performance vs. MSCI Hong Kong

70

80

90

100

110

120

09/11 11/11 01/12 03/12 05/12 07/12 09/12

Pacific Basin Shipping MSCI Hong Kong

Timothy Ross / Research Analyst / 65 6212 3337 /

Extracted from The Asian Daily 10 Sep 2012

14 S

epte

mber 2

012

David

& G

olia

th

13

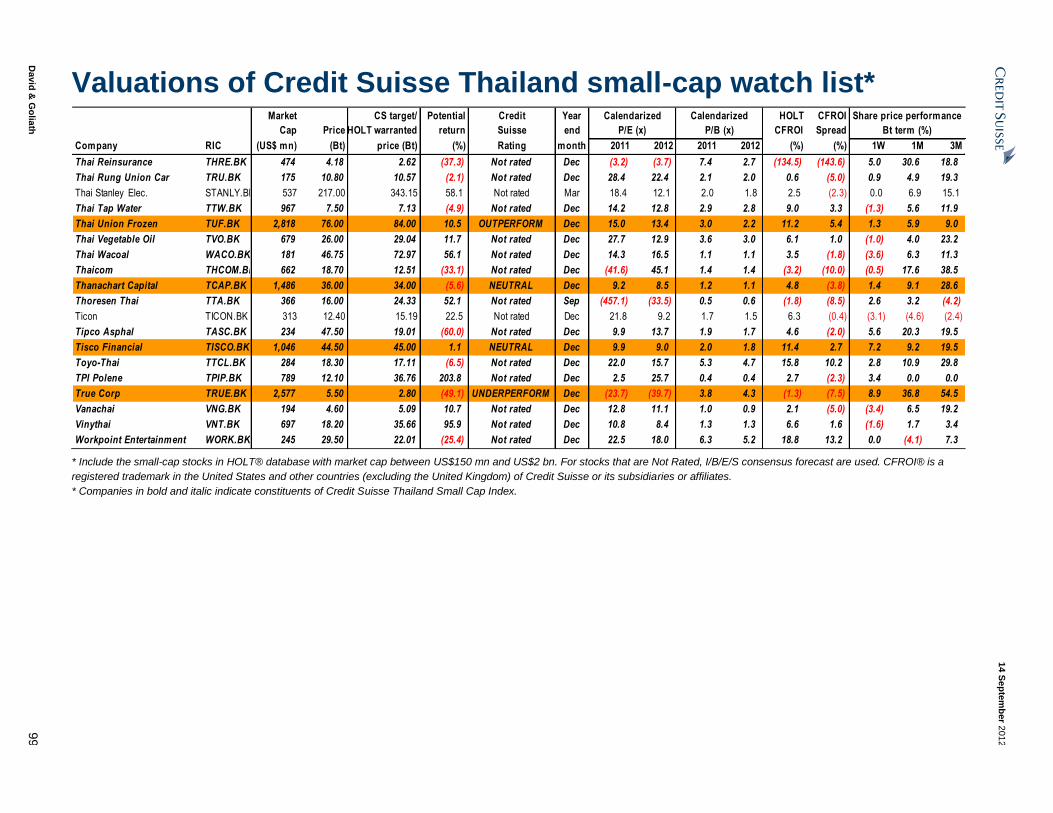

Valuations of Credit Suisse HK small-cap watch list*

Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI Spread

Company RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2011 2012 2011 2012 (%) (%) 1W 1M 3M

Aeon Credit 0900.HK 343 6.35 5.35 (15.7) Not rated Feb n.a. 9.1 n.a. 1.2 8.0 (1.5) 0.8 (0.8) (2.3)

AEON Stores 0984.HK 704 21.00 7.28 (65.3) Not rated Dec 13.5 18.0 3.5 3.2 6.5 (1.6) (4.5) (7.9) (6.7)

Alco Holdings 0328.HK 123 1.64 1.99 21.4 Not rated Mar n.a. 11.3 n.a. 0.5 2.3 (6.6) 1.2 (3.5) (27.1)

Allied Group 0373.HK 442 17.92 40.37 125.3 Not rated Dec 3.2 6.9 0.3 0.2 2.9 (6.4) (0.4) 1.2 2.4

Allied Properties 0056.HK 851 0.97 2.13 119.6 Not rated Dec 3.7 3.2 0.4 0.3 4.2 (5.0) 2.1 (1.0) 1.0

AMVIG 2300.HK 298 2.50 3.02 20.9 Not rated Dec 4.2 5.4 0.5 0.5 16.3 8.2 5.0 (27.1) (16.9)

Apollo Solar Energy 0566.HK 364 0.21 1.51 617.1 Not rated Dec 3.6 1.9 0.3 0.3 30.5 22.4 3.4 (7.5) (4.5)

Asia Financial 0662.HK 386 2.94 3.46 17.7 Not rated Dec (21.8) (21.7) 0.6 0.5 (4.9) (14.3) 1.4 7.7 5.8

Asia Sat. Telecom. 1135.HK 1,223 24.25 22.22 (8.4) Not rated Dec 11.5 10.3 1.4 1.3 9.6 1.6 (1.8) 9.2 12.8

ASM Pacific 0522.HK 4,718 92.00 73.50 (20.1) UNDERPERFORM Dec 12.4 22.7 5.8 5.0 21.5 15.0 2.2 5.1 (1.8)

Associated Int'l Hotels 0105.HK 789 17.00 20.92 23.1 Not rated Mar 22.1 12.0 n.a. 0.6 2.5 (5.6) (1.2) 1.2 6.3

Bonjour 0653.HK 394 1.02 0.48 (53.1) Not rated Dec 12.8 15.0 10.6 10.0 13.7 5.5 1.0 10.9 (12.1)

Brightoil Petroleum 0933.HK 1,639 1.45 1.31 (9.9) Not rated Jun 8.4 7.7 1.8 1.4 7.8 1.0 2.1 (1.4) 0.0

C C Land 1224.HK 551 1.65 1.67 1.1 Not rated Dec 14.0 8.3 0.3 0.3 0.9 (6.9) 2.5 (1.2) (10.8)

C.P. Pokphand 0043.HK 2,147 0.98 0.62 (36.6) Not rated Dec 13.4 12.6 2.7 2.3 13.1 5.9 0.0 (1.0) 6.5

Café De Coral 0341.HK 1,685 22.85 8.54 (62.6) Not rated Mar 26.7 25.0 4.1 3.8 5.7 (1.8) 2.5 4.6 15.2

Chaoy ue 0147.HK 1,216 0.50 0.01 (97.1) Not rated Mar n.a. (415.6) n.a. (79.9) (48.5) (56.5) (27.5) 63.9 185.7

Chen Hsong 0057.HK 169 2.08 2.68 28.9 Not rated Mar 6.4 9.7 0.5 0.4 3.6 (5.2) 1.5 (5.0) (12.2)

Chev alier 0025.HK 333 9.30 9.01 (3.1) Not rated Mar n.a. 6.0 n.a. 0.5 3.6 (4.9) (7.0) (1.6) 14.1

China Haidian 0256.HK 440 0.80 0.62 (21.9) Not rated Dec 12.9 14.3 1.1 0.9 6.8 (1.7) 5.3 1.3 2.6

China Motor Bus 0026.HK 365 62.00 99.22 60.0 Not rated Jun n.a. 4.8 n.a. 0.5 3.5 (5.3) (1.6) 1.7 6.0

China Oriental 0581.HK 676 1.79 2.63 46.9 Not rated Dec 3.5 11.8 0.5 0.4 8.2 0.8 3.5 (3.2) (10.5)

Chong Hing Bank 1111.HK 719 12.82 10.41 (18.8) Not rated Dec 9.9 13.9 0.8 0.8 5.1 (4.2) 1.1 0.9 3.9

Chow Sang Sang 0116.HK 1,489 17.06 20.00 17.2 OUTPERFORM Dec 10.6 11.0 1.8 1.6 9.5 2.4 9.8 6.9 6.1

City Telecom (HK) 1137.HK 208 1.99 2.89 45.4 Not rated Aug 5.3 6.5 0.8 1.2 9.6 1.2 (2.0) 14.4 (54.5)

CK Life Sciences 0775.HK 768 0.62 0.12 (80.7) Not rated Dec 47.3 34.0 1.1 1.1 6.5 (1.6) (1.6) 17.0 51.2

Comba Telecom Sys. 2342.HK 464 2.36 1.88 (20.5) NEUTRAL Dec 5.4 37.3 0.9 0.9 10.5 3.0 22.9 38.8 (30.0)

Convenience Retail 0831.HK 419 4.40 1.41 (68.0) Not rated Dec 19.4 18.3 3.4 3.2 6.1 (2.4) 2.1 (0.9) (2.0)

Cross-Harbour 0032.HK 304 6.33 6.48 2.3 Not rated Dec 9.7 9.4 0.8 0.7 (4.4) (13.1) 2.1 3.1 2.1

Dah Chong Hong 1828.HK 1,693 7.19 5.66 (21.3) Not rated Dec 9.9 9.7 1.7 1.5 7.5 0.4 2.6 2.9 (4.6)

Share price performance

HK$ term (%)P/B (x)P/E (x)

CalendarizedCalendarized

* Include the Hong Kong Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$150 mn and US$2 bn.

For stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit

Suisse or its subsidiaries or affiliates.

* Companies in bold and italic indicate constituents of Credit Suisse Hong Kong Small Cap Index

14 S

epte

mber 2

012

David

& G

olia

th

14

Valuations of Credit Suisse HK small-cap watch list*

Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI Spread

Company RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2011 2012 2011 2012 (%) (%) 1W 1M 3M

Dah Sing Banking 2356.HK 1,146 7.10 8.50 19.7 NEUTRAL Dec 8.1 7.7 0.6 0.6 4.2 (4.9) 2.2 (3.1) 4.9

Dah Sing Financial 0440.HK 994 26.00 29.00 11.5 NEUTRAL Dec 7.5 7.1 0.5 0.5 3.7 (5.5) 2.4 2.2 13.5

Dickson Concepts 0113.HK 198 4.13 2.72 (34.0) Not rated Mar n.a. 7.4 n.a. 0.6 4.1 (4.6) (0.2) (3.7) (1.4)

Embry 1388.HK 208 3.90 2.23 (42.7) Not rated Dec 10.0 11.1 1.3 1.1 7.2 (1.5) 1.3 14.7 6.8

Emperor Entertainment 0296.HK 257 1.54 3.41 121.2 Not rated Mar n.a. 5.1 n.a. 0.9 18.7 9.7 10.0 11.6 30.5

Emperor Watch & Jewellery 0887.HK 650 0.75 0.64 (15.0) Not rated Dec 7.7 9.1 1.3 1.0 11.2 3.5 5.6 (1.3) (6.3)

Epro 8086.HK 493 0.72 0.16 (77.7) Not rated Jun n.a. 39.0 n.a. 10.5 17.9 9.9 1.4 1.4 (10.0)

ERA Mining 8043.HK 638 0.87 0.25 (70.9) Not rated Dec (348.0) 34.8 3.8 3.6 4.9 (3.5) 0.0 0.0 0.0

EVA Precision 0838.HK 145 0.65 0.28 (56.2) Not rated Dec 5.1 13.3 0.6 0.4 5.7 (2.5) 6.6 1.6 (19.8)

Fairw ood 0052.HK 276 17.12 3.96 (76.9) Not rated Mar 18.2 15.0 n.a. 4.0 6.2 (2.8) 5.0 12.6 35.7

Fortune REIT 0778.HK 1,288 5.89 2.79 (52.6) Not rated Dec 2.9 22.5 0.7 0.7 2.7 (5.1) 0.7 8.7 34.2

Giordano 0709.HK 1,192 6.00 4.01 (33.1) Not rated Dec 12.4 11.8 3.3 3.1 8.4 0.8 (0.2) 9.9 14.5

Glorious Sun 0393.HK 310 2.27 -0.05 (102.3) Not rated Dec 7.6 13.2 1.0 1.0 3.6 (4.6) 1.8 (6.6) (4.6)

Goldlion 0533.HK 433 3.42 3.73 9.0 Not rated Dec 8.0 8.5 1.1 1.1 8.3 (0.2) (0.3) 5.6 11.4

Great Eagle 0041.HK 1,799 22.10 31.20 41.2 OUTPERFORM Dec 8.3 8.3 0.4 0.4 4.0 (3.3) 5.0 8.3 13.3

G-Resources 1051.HK 939 0.39 0.56 45.2 NEUTRAL Jun (37.1) 9.9 1.1 1.0 (13.2) (21.1) 1.3 (14.4) (14.4)

Harbour Centre Dev. 0051.HK 1,038 11.36 10.77 (5.2) Not rated Dec 7.3 22.3 0.7 0.6 2.1 (5.7) 3.3 15.4 22.2

Henderson Investment 0097.HK 216 0.55 0.50 (9.6) Not rated Dec 15.7 12.1 1.0 1.0 8.6 (0.3) 0.0 (5.2) (3.5)

Hi Sun Tech. (China) 0818.HK 279 0.81 0.71 (11.9) Not rated Dec (8.4) (20.6) 0.8 0.8 (9.0) (17.1) 47.3 (1.2) (13.8)

HKC 0190.HK 419 0.30 0.55 84.9 Not rated Dec 12.8 (179.5) 0.3 0.3 0.0 (8.2) 0.0 0.0 (9.2)

HKR 0480.HK 543 3.12 7.87 152.1 Not rated Mar 6.8 5.9 0.3 0.3 0.9 (7.0) 9.5 7.6 14.3

Honbridge 8137.HK 473 0.59 -0.02 (104.1) Not rated Dec (11.7) 214.2 6.6 6.6 3.2 (4.1) (1.7) (3.3) (23.4)

Hong Kong Ferry 0050.HK 309 6.73 10.73 59.4 Not rated Dec 4.2 7.9 0.5 0.5 4.0 (4.9) (0.1) 1.4 5.5

HK & S Hotels 0045.HK 1,792 9.25 14.67 58.6 Not rated Dec 6.1 32.5 0.4 0.4 1.6 (5.4) 1.5 (3.0) (7.9)

HongKong Chinese 0655.HK 298 1.16 3.97 241.9 Not rated Dec 2.6 2.2 0.3 0.2 7.1 (2.3) (1.7) 1.8 (3.3)

Hopewell Highway Infra. 0737.HK 1,505 3.94 2.87 (27.1) Not rated Jun 11.5 11.6 1.3 1.3 7.0 (0.1) 1.8 4.2 7.4

Huabao 0336.HK 1,705 4.20 4.55 8.3 NEUTRAL Mar 8.1 7.5 2.3 1.9 34.2 27.3 (2.8) 8.5 34.6

Hutchison Harbour Ring 0715.HK 763 0.66 0.40 (38.8) Not rated Dec 65.3 65.1 1.0 1.0 1.4 (6.4) 6.5 1.5 4.8

Hutchison Telecom HK 0215.HK 2,144 3.45 4.20 21.7 NEUTRAL Dec 16.3 13.4 1.6 1.5 6.8 (0.4) (2.3) (7.0) 1.5

I.T. 0999.HK 524 3.31 2.33 (29.7) Not rated Feb 8.7 8.0 1.8 1.5 7.9 0.2 (5.7) (7.0) 9.2

HK$ term (%)P/E (x) P/B (x)

Calendarized Calendarized Share price performance

* Include the Hong Kong Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$150 mn and US$2 bn.

For stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit

Suisse or its subsidiaries or affiliates.

* Companies in bold and italic indicate constituents of Credit Suisse Hong Kong Small Cap Index

14 S

epte

mber 2

012

David

& G

olia

th

15

Valuations of Credit Suisse HK small-cap watch list*

Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI Spread

Company RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2011 2012 2011 2012 (%) (%) 1W 1M 3M

Int'l Entertainment 1009.HK 160 1.05 0.73 (30.9) Not rated Mar n.a. 16.9 n.a. 0.7 0.9 (7.9) 0.0 5.0 (18.0)

IRC 1029.HK 257 0.57 1.49 161.5 Not rated Dec 245.0 (14.7) 0.3 0.3 (0.1) (8.2) 1.8 (18.6) (33.7)

Johnson Electric 0179.HK 2,317 4.98 4.80 (3.6) NEUTRAL Mar 12.6 11.8 1.6 1.5 10.6 3.5 7.1 13.7 6.2

Ju Teng 3336.HK 509 3.49 3.31 (5.2) Not rated Dec 15.4 7.2 0.8 0.8 1.2 (7.2) 2.3 19.1 90.7

K. Wah Int'l 0173.HK 1,159 3.44 6.97 102.8 Not rated Dec 7.1 3.0 0.7 0.6 6.1 (1.6) 5.8 20.3 14.3

Kingboard Chemical 0148.HK 1,869 16.96 17.80 5.0 NEUTRAL Dec 5.6 7.2 0.5 0.5 4.7 (2.0) 2.3 (1.3) 2.5

Kingboard Laminates 1888.HK 1,207 3.12 3.70 18.7 Not rated Dec 7.1 7.3 0.9 0.8 5.8 (1.4) 7.6 2.0 12.2

Kingston Financial 1031.HK 906 0.58 0.42 (27.6) Not rated Mar 3.3 8.6 n.a. 0.5 15.5 8.2 13.7 (26.6) (19.4)

Kosmopolito Hotels 2266.HK 487 1.89 0.31 (83.4) Not rated Mar 7.7 10.7 1.1 1.0 5.6 (2.8) 1.1 21.2 40.0

Kowloon Dev. 0034.HK 1,232 8.30 9.23 11.3 Not rated Dec 6.2 9.7 0.5 0.4 1.4 (5.9) 8.2 7.4 12.3

Le Saunda 0738.HK 161 1.95 2.10 7.5 Not rated Feb n.a. 6.4 n.a. 1.0 8.6 (0.2) 0.5 (4.4) (15.2)

Lee & Man Paper 2314.HK 1,935 3.20 2.75 (14.1) UNDERPERFORM Mar 10.1 10.6 1.1 1.1 5.0 (1.9) 2.9 (5.3) 1.9

Lee's Pharma. 0950.HK 340 5.08 3.00 (40.9) Not rated Dec 28.4 20.3 7.7 4.6 27.5 18.2 4.5 16.0 50.3

Lippo 0226.HK 207 3.24 11.07 241.6 Not rated Dec 2.7 4.1 0.2 0.2 2.7 (6.9) 3.2 6.9 14.1

Luk Fook 0590.HK 1,706 22.45 23.30 3.8 NEUTRAL Mar 10.0 10.6 2.4 2.1 17.0 9.9 12.3 15.1 47.7

Lung Kee 0255.HK 210 2.58 2.92 13.1 Not rated Dec 5.9 10.1 0.7 0.7 3.7 (5.0) 2.4 (3.7) (5.8)

Man Wah 1999.HK 389 3.35 2.54 (24.1) Not rated Mar 8.4 8.6 1.0 0.8 5.2 (2.5) 10.9 20.1 (9.0)

Media Chinese 0685.HK 803 3.69 2.44 (33.8) Not rated Mar n.a. 13.2 n.a. 2.0 12.8 4.5 (1.6) 2.5 40.3

Melco 0200.HK 1,018 6.40 4.30 (32.8) OUTPERFORM Dec 23.4 11.0 1.0 1.1 (4.0) (11.7) 7.9 11.5 2.1

Midland 1200.HK 408 4.41 5.34 21.1 OUTPERFORM Dec 23.9 12.0 2.1 1.9 3.9 (4.3) 2.6 2.8 12.8

Min Xin 0222.HK 252 4.26 6.31 48.2 Not rated Dec 6.5 6.0 0.7 0.6 8.8 (0.8) 0.9 6.5 5.4

Mingfa 0846.HK 1,729 2.20 0.94 (57.3) Not rated Dec 6.8 12.4 1.5 1.3 3.7 (3.5) 4.8 10.0 4.8

Miramar 0071.HK 692 9.30 23.78 155.7 Not rated Dec 4.0 3.6 0.5 0.5 12.2 4.2 4.5 9.2 14.7

Mongolia Energy 0276.HK 261 0.30 1.15 283.4 Not rated Mar (0.5) (1.4) n.a. 0.2 (402.1) (409.6) (1.6) (15.5) (31.8)

Nagacorp 3918.HK 1,179 4.39 4.44 1.2 Not rated Dec 12.8 11.3 3.3 3.0 24.2 15.8 12.6 10.0 38.1

Natural Beauty 0157.HK 253 0.98 0.61 (37.8) Not rated Dec 16.9 16.7 2.5 2.6 15.9 7.3 (6.7) (15.5) (22.8)

New World Dept. St. China 0825.HK 915 4.21 2.75 (34.7) Not rated Jun 9.9 9.8 1.4 1.2 5.4 (2.1) 0.5 0.5 (3.0)

Nex t Media 0282.HK 212 0.68 0.42 (38.6) Not rated Mar n.a. (2.0) n.a. 0.5 (20.3) (28.9) 3.0 41.7 23.6

Oriental Press 0018.HK 244 0.79 0.70 (11.9) Not rated Mar n.a. 23.4 n.a. 0.6 1.5 (7.3) 0.0 0.0 (13.2)

Oriental Watch 0398.HK 175 2.38 2.32 (2.4) Not rated Mar 7.4 6.8 0.7 0.6 6.4 (2.1) 4.8 (1.7) 6.2

Calendarized Calendarized Share price performance

P/E (x) P/B (x) HK$ term (%)

* Include the Hong Kong Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$150 mn and US$2 bn.

For stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit

Suisse or its subsidiaries or affiliates.

* Companies in bold and italic indicate constituents of Credit Suisse Hong Kong Small Cap Index

14 S

epte

mber 2

012

David

& G

olia

th

16

Valuations of Credit Suisse HK small-cap watch list*

Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI Spread

Company RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2011 2012 2011 2012 (%) (%) 1W 1M 3M

Pacific Andes 1174.HK 225 0.37 0.25 (32.7) Not rated Sep 4.1 6.9 0.2 0.3 6.5 (1.6) 1.4 (11.9) (21.3)

Pacific Basin 2343.HK 959 3.84 3.40 (11.5) UNDERPERFORM Dec 16.6 30.1 0.6 0.7 2.8 (4.6) 19.3 6.7 12.6

Pacific Textiles 1382.HK 926 5.01 5.60 11.8 OUTPERFORM Mar 8.1 9.3 1.8 1.8 12.8 4.8 1.8 (9.7) (10.1)

Paliburg 0617.HK 359 2.48 41.41 1,569.8 Not rated Dec 1.9 1.2 0.3 0.2 8.1 (0.5) 0.8 5.5 6.4

Phoenix Satellite 2008.HK 1,481 2.30 2.12 (7.8) Not rated Dec (171.6) 12.8 3.2 2.9 11.4 4.1 2.2 1.3 10.6

Pico Far East 0752.HK 276 1.76 1.76 (0.0) Not rated Oct 8.4 7.5 1.6 1.9 12.5 3.5 0.0 0.6 (4.3)

Polytec Asset 0208.HK 401 0.70 1.66 137.2 Not rated Dec 15.2 20.6 0.3 0.3 (1.7) (11.1) 1.4 (4.1) (7.9)

Pou Sheng 3813.HK 264 0.48 1.01 110.4 Not rated Sep 5.8 8.3 0.3 0.4 7.7 (0.4) (5.9) (15.8) (23.8)

Public Financial 0626.HK 496 3.50 2.47 (29.5) Not rated Dec 10.3 11.5 0.6 0.6 5.3 (4.0) 9.4 9.4 14.0

Regal Hotels 0078.HK 404 3.25 7.40 127.6 Not rated Dec 29.5 3.2 0.3 0.3 0.1 (8.2) 3.8 6.2 10.9

Regal REIT 1881.HK 819 1.95 1.91 (2.1) Not rated Dec 2.1 15.4 0.5 0.5 4.8 (2.9) (4.4) 1.0 14.0

RexLot 0555.HK 549 0.50 0.99 98.5 Not rated Dec 5.4 4.8 0.9 0.7 23.8 15.7 0.0 7.5 (16.7)

Road King Infra. 1098.HK 507 5.30 7.88 48.7 Not rated Dec 4.8 5.5 0.4 0.3 3.3 (6.1) 2.7 2.1 10.4

Royale Furniture 1198.HK 85 0.86 0.86 (0.3) Not rated Dec 2.8 3.0 0.5 0.4 10.0 1.1 10.3 (16.5) (46.9)

Sa Sa 0178.HK 1,794 4.93 5.00 1.4 OUTPERFORM Mar 21.5 17.3 8.9 7.4 15.2 7.9 0.4 5.8 19.1

SCMP 0583.HK 302 1.50 1.49 (0.8) Not rated Dec 6.3 12.3 0.9 0.8 4.6 (4.1) 1.4 4.9 4.9

Shui On Con. & Mats. 0983.HK 455 7.17 5.10 (28.9) Not rated Dec 3.9 27.8 0.4 0.3 1.9 (6.1) 1.1 (4.4) (7.1)

Shun Tak 0242.HK 1,105 2.87 4.13 43.9 OUTPERFORM Dec 8.0 16.4 0.4 0.5 1.7 (5.8) 2.5 3.2 1.8

Singamas Container 0716.HK 562 1.80 1.53 (14.9) Not rated Dec 4.0 7.3 1.0 0.8 13.1 5.2 7.1 4.7 (10.0)

Sino Hotels 1221.HK 298 2.48 3.58 44.5 Not rated Jun n.a. 11.9 n.a. 0.7 1.3 (7.5) 1.6 (0.8) 2.5

Sinofert 0297.HK 1,332 1.47 2.16 47.1 Not rated Dec 12.4 10.5 0.6 0.7 7.3 0.4 3.5 (8.7) 19.5

Sitoy 1023.HK 452 3.50 3.53 0.8 Not rated Jun n.a. 10.2 n.a. 3.2 40.8 34.2 0.3 7.7 0.6

Southgobi Resources 1878.HK 413 17.62 19.27 9.4 Not rated Dec 6.7 (16.8) 0.6 0.5 (0.8) (8.1) 3.3 (43.3) (55.8)

Stelux 0084.HK 201 1.49 0.98 (34.5) Not rated Mar 8.0 5.5 1.5 1.3 5.6 (3.4) (0.7) (6.3) (1.8)

Sun Hung Kai & Co. 0086.HK 995 3.62 4.92 36.0 Not rated Dec 7.4 6.7 0.6 0.6 6.4 (2.7) 0.3 (1.4) (8.4)

Sunev ision 8008.HK 491 1.64 1.58 (3.5) Not rated Jun 23.0 12.6 n.a. 1.3 8.5 (0.4) 1.2 9.3 42.6

Sunlight REIT 0435.HK 654 3.16 2.73 (13.7) Not rated Jun 5.5 4.8 0.6 0.6 5.6 (2.6) 0.6 8.2 26.4

Tan Chong 0693.HK 527 2.03 2.57 26.5 Not rated Dec 6.8 7.1 0.5 0.5 4.2 (4.1) 2.0 1.0 2.0

Tao Heung 0573.HK 553 4.20 2.31 (45.1) Not rated Dec 16.7 15.1 3.1 2.8 7.8 (0.7) 0.2 6.6 8.0

Techtronic 0669.HK 2,981 12.68 9.65 (23.9) NEUTRAL Dec 17.4 14.7 2.1 1.9 8.4 1.2 3.3 21.9 35.3

Calendarized Calendarized Share price performance

P/E (x) P/B (x) HK$ term (%)

* Include the Hong Kong Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$150 mn and US$2 bn.

For stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit

Suisse or its subsidiaries or affiliates.

* Companies in bold and italic indicate constituents of Credit Suisse Hong Kong Small Cap Index

14 S

epte

mber 2

012

David

& G

olia

th

17

Valuations of Credit Suisse HK small-cap watch list*

Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI Spread

Company RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2011 2012 2011 2012 (%) (%) 1W 1M 3M

Texwinca 0321.HK 937 5.33 5.50 3.2 NEUTRAL Mar 7.4 10.4 1.3 1.3 3.8 (3.4) (0.2) (24.8) (38.7)

Tian Teck Land 0266.HK 425 6.95 6.34 (8.8) Not rated Mar n.a. 24.4 n.a. 0.6 2.7 (5.9) (0.7) 2.2 8.6

Titan Petrochemicals 1192.HK 248 0.25 -0.23 (193.1) Not rated Dec (2.4) (2.8) 4.1 4.1 (5.3) (13.4) 0.0 0.0 13.9

TOM 2383.HK 412 0.82 -0.35 (142.6) Not rated Dec (6.4) (10.7) 2.8 3.2 (3.3) (11.5) (3.5) 6.5 22.4

Tomson Group 0258.HK 315 1.70 3.05 79.2 Not rated Dec 157.4 18.1 0.2 0.2 3.2 (5.0) 0.0 1.2 10.4

Tongda 0698.HK 172 0.28 0.55 97.0 Not rated Dec 5.2 4.2 0.7 0.6 10.5 1.4 1.8 (3.4) (3.4)

Towngas China 1083.HK 1,904 6.00 3.18 (47.1) Not rated Dec 20.8 18.5 1.5 1.5 7.2 (0.2) (0.5) 4.9 8.7

TPV 0903.HK 478 1.58 1.60 1.5 Not rated Dec 4.0 5.1 0.3 0.3 5.4 (2.2) 9.0 3.9 (6.0)

Transport Int'l 0062.HK 785 15.08 15.45 2.5 Not rated Dec 25.1 18.2 0.9 0.9 (0.5) (8.2) 0.7 0.0 7.4

Trinity 0891.HK 1,174 5.30 3.02 (42.9) Not rated Dec 17.5 16.1 2.8 2.8 14.3 6.8 4.5 (3.5) (9.1)

Truly 0732.HK 375 1.05 0.98 (6.7) UNDERPERFORM Dec 8.3 6.4 0.7 0.6 5.6 (1.5) 0.0 (3.7) (7.9)

United Energy 0467.HK 1,933 1.15 0.68 (40.8) Not rated Dec 27.6 23.5 2.6 2.4 2.3 (4.9) 0.0 (3.4) (5.0)

United Labs 3933.HK 799 3.81 1.53 (59.8) Not rated Dec 51.9 24.6 1.0 0.9 0.7 (6.6) 3.3 3.3 17.2

Value Partners 0806.HK 776 3.43 1.35 (60.8) Not rated Dec 36.1 29.8 2.6 2.1 2.5 (6.7) 3.3 (0.3) (6.0)

Varitronix 0710.HK 111 2.66 3.65 37.2 OUTPERFORM Dec 5.1 4.6 0.6 0.6 5.6 (3.6) 0.0 0.4 (16.4)

Victory City 0539.HK 156 0.78 1.24 59.1 Not rated Mar n.a. 4.1 n.a. 0.3 3.3 (5.4) 2.6 2.6 (1.3)

Vitasoy 0345.HK 919 6.97 3.78 (45.7) Not rated Mar 25.3 22.1 4.8 4.5 9.4 1.4 4.8 3.9 11.5

VST 0856.HK 235 1.47 1.94 32.1 Not rated Dec 4.0 3.7 0.7 0.6 10.3 1.7 1.4 14.0 2.8

VTech 0303.HK 3,037 94.05 84.00 (10.7) NEUTRAL Mar 15.5 14.5 5.5 5.3 14.2 7.1 (1.7) 2.3 5.6

Wing On 0289.HK 697 18.30 29.41 60.7 Not rated Dec 3.0 8.9 0.5 0.5 3.4 (4.8) 0.5 7.6 13.2

Wing Tai Properties 0369.HK 813 4.73 7.46 57.8 Not rated Dec 2.8 10.7 0.5 0.5 0.9 (8.5) 2.8 7.0 22.9

Winsor Properties 1036.HK 591 17.64 35.22 99.7 Not rated Dec 7.7 4.6 0.4 0.4 5.1 (3.1) 7.4 37.8 116.1

YGM Trading 0375.HK 374 17.48 11.28 (35.4) Not rated Mar 5.2 7.9 n.a. 1.3 8.3 (0.1) 3.1 2.8 (6.5)

Yip's Chemical 0408.HK 369 5.10 2.79 (45.3) Not rated Dec 14.0 11.4 1.1 1.0 4.2 (3.9) 4.1 0.8 2.0

Yue Yuen 0551.HK 5,231 24.60 25.70 4.5 NEUTRAL Sep 12.6 10.5 1.4 1.3 7.7 1.2 0.6 6.5 (0.2)

Calendarized Calendarized Share price performance

P/E (x) P/B (x) HK$ term (%)

* Include the Hong Kong Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$150 mn and US$2 bn.

For stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit

Suisse or its subsidiaries or affiliates.

* Companies in bold and italic indicate constituents of Credit Suisse Hong Kong Small Cap Index

14 S

epte

mber 2

012

David

& G

olia

th

18

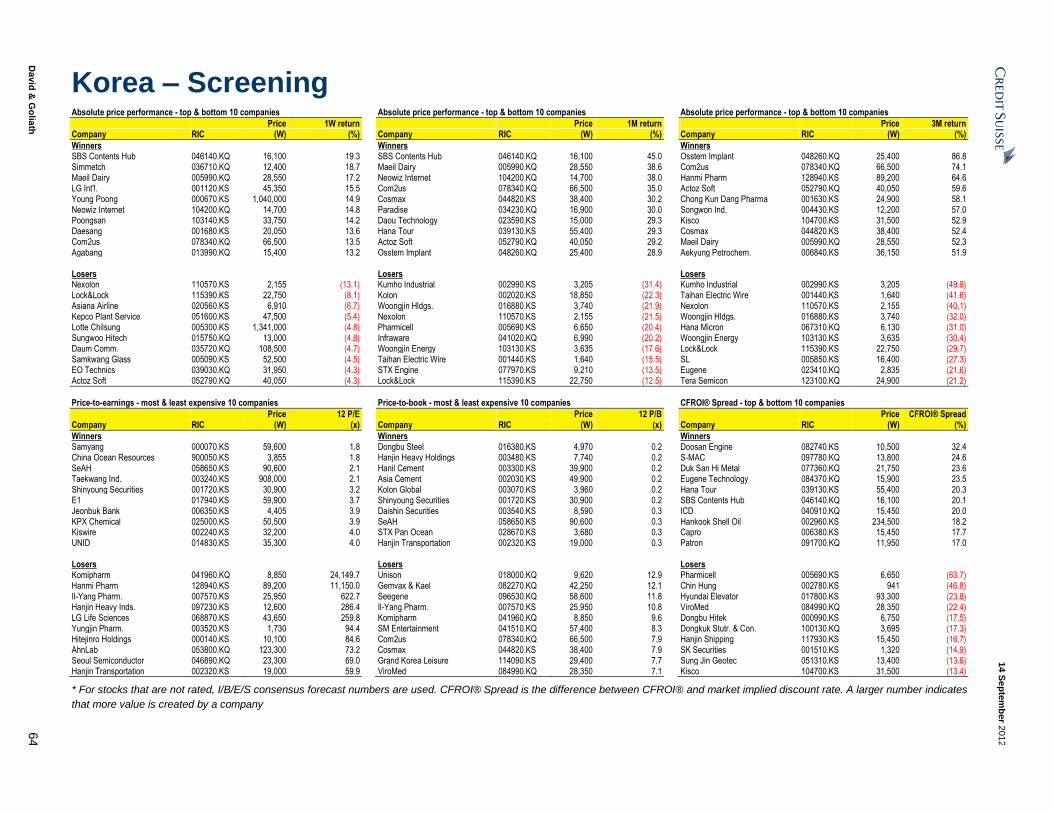

Hong Kong – Screening Absolute price performance - top & bottom 10 companies Absolute price performance - top & bottom 10 companies Absolute price performance - top & bottom 10 companies

Price 1W return Price 1M return Price 3M return Company RIC (HK$) (%) Company RIC (HK$) (%) Company RIC (HK$) (%)

Winners Winners Winners Hi Sun Tech. (China) 0818.HK 0.81 47.3 Chaoyue 0147.HK 0.50 63.9 Chaoyue 0147.HK 0.50 185.7 Comba Telecom Sys. 2342.HK 2.36 22.9 Next Media 0282.HK 0.68 41.7 Winsor Properties 1036.HK 17.64 116.1 Pacific Basin 2343.HK 3.84 19.3 Comba Telecom Sys. 2342.HK 2.36 38.8 Ju Teng 3336.HK 3.49 90.7 Kingston Financial 1031.HK 0.58 13.7 Winsor Properties 1036.HK 17.64 37.8 CK Life Sciences 0775.HK 0.62 51.2 Nagacorp 3918.HK 4.39 12.6 Techtronic 0669.HK 12.68 21.9 Lee's Pharma. 0950.HK 5.08 50.3 Luk Fook 0590.HK 22.45 12.3 Kosmopolito Hotels 2266.HK 1.89 21.2 Luk Fook 0590.HK 22.45 47.7 Man Wah 1999.HK 3.35 10.9 K. Wah Int'l 0173.HK 3.44 20.3 Sunevision 8008.HK 1.64 42.6 Royale Furniture 1198.HK 0.86 10.3 Man Wah 1999.HK 3.35 20.1 Media Chinese 0685.HK 3.69 40.3 Emperor Entertainment 0296.HK 1.54 10.0 Ju Teng 3336.HK 3.49 19.1 Kosmopolito Hotels 2266.HK 1.89 40.0 Chow Sang Sang 0116.HK 17.06 9.8 CK Life Sciences 0775.HK 0.62 17.0 Nagacorp 3918.HK 4.39 38.1 Losers Losers Losers Chaoyue 0147.HK 0.50 (27.5) Southgobi Resources 1878.HK 17.62 (43.3) Southgobi Resources 1878.HK 17.62 (55.8) Chevalier 0025.HK 9.30 (7.0) AMVIG 2300.HK 2.50 (27.1) City Telecom (HK) 1137.HK 1.99 (54.5) Natural Beauty 0157.HK 0.98 (6.7) Kingston Financial 1031.HK 0.58 (26.6) Royale Furniture 1198.HK 0.86 (46.9) Pou Sheng 3813.HK 0.48 (5.9) Texwinca 0321.HK 5.33 (24.8) Texwinca 0321.HK 5.33 (38.7) I.T. 0999.HK 3.31 (5.7) IRC 1029.HK 0.57 (18.6) IRC 1029.HK 0.57 (33.7) AEON Stores 0984.HK 21.00 (4.5) Royale Furniture 1198.HK 0.86 (16.5) Mongolia Energy 0276.HK 0.30 (31.8) Regal REIT 1881.HK 1.95 (4.4) Pou Sheng 3813.HK 0.48 (15.8) Comba Telecom Sys. 2342.HK 2.36 (30.0) TOM 2383.HK 0.82 (3.5) Natural Beauty 0157.HK 0.98 (15.5) Alco Holdings 0328.HK 1.64 (27.1) Huabao 0336.HK 4.20 (2.8) Mongolia Energy 0276.HK 0.30 (15.5) Pou Sheng 3813.HK 0.48 (23.8) Hutchison Telecom HK 0215.HK 3.45 (2.3) G-Resources 1051.HK 0.39 (14.4) Honbridge 8137.HK 0.59 (23.4)

Price-to-earnings - most & least expensive 10 companies Price-to-book - most & least expensive 10 companies CFROI® Spread - top & bottom 10 companies

Price 12 P/E Price 12 P/B Price CFROI® Spread Company RIC (HK$) (x) Company RIC (HK$) (x) Company RIC (HK$) (%)

Winners Winners Winners Paliburg 0617.HK 2.48 1.2 Lippo 0226.HK 3.24 0.2 Sitoy 1023.HK 3.50 34.2 Apollo Solar Energy 0566.HK 0.21 1.9 Paliburg 0617.HK 2.48 0.2 Huabao 0336.HK 4.20 27.3 HongKong Chinese 0655.HK 1.16 2.2 Tomson Group 0258.HK 1.70 0.2 Apollo Solar Energy 0566.HK 0.21 22.4 K. Wah Int'l 0173.HK 3.44 3.0 HongKong Chinese 0655.HK 1.16 0.2 Lee's Pharma. 0950.HK 5.08 18.2 Royale Furniture 1198.HK 0.86 3.0 Mongolia Energy 0276.HK 0.30 0.2 Nagacorp 3918.HK 4.39 15.8 Regal Hotels 0078.HK 3.25 3.2 Allied Group 0373.HK 17.92 0.2 RexLot 0555.HK 0.50 15.7 Allied Properties 0056.HK 0.97 3.2 Apollo Solar Energy 0566.HK 0.21 0.3 ASM Pacific 0522.HK 92.00 15.0 Miramar 0071.HK 9.30 3.6 TPV 0903.HK 1.58 0.3 Epro 8086.HK 0.72 9.9 VST 0856.HK 1.47 3.7 Victory City 0539.HK 0.78 0.3 Luk Fook 0590.HK 22.45 9.9 Lippo 0226.HK 3.24 4.1 HKC 0190.HK 0.30 0.3 Emperor Entertainment 0296.HK 1.54 9.7 Losers Losers Losers Honbridge 8137.HK 0.59 214.2 Epro 8086.HK 0.72 10.5 Mongolia Energy 0276.HK 0.30 (409.6) Hutchison Harbour Ring 0715.HK 0.66 65.1 Bonjour 0653.HK 1.02 10.0 Chaoyue 0147.HK 0.50 (56.5) Epro 8086.HK 0.72 39.0 Sa Sa 0178.HK 4.93 7.4 Next Media 0282.HK 0.68 (28.9) Comba Telecom Sys. 2342.HK 2.36 37.3 Honbridge 8137.HK 0.59 6.6 G-Resources 1051.HK 0.39 (21.1) ERA Mining 8043.HK 0.87 34.8 VTech 0303.HK 94.05 5.3 Hi Sun Tech. (China) 0818.HK 0.81 (17.1) CK Life Sciences 0775.HK 0.62 34.0 ASM Pacific 0522.HK 92.00 5.0 Asia Financial 0662.HK 2.94 (14.3) HK & S Hotels 0045.HK 9.25 32.5 Lee's Pharma. 0950.HK 5.08 4.6 Titan Petrochemicals 1192.HK 0.25 (13.4) Pacific Basin 2343.HK 3.84 30.1 Vitasoy 0345.HK 6.97 4.5 Cross-Harbour 0032.HK 6.33 (13.1) Value Partners 0806.HK 3.43 29.8 Titan Petrochemicals 1192.HK 0.25 4.1 Melco 0200.HK 6.40 (11.7) Shui On Con. & Mats. 0983.HK 7.17 27.8 Fairwood 0052.HK 17.12 4.0 TOM 2383.HK 0.82 (11.5)

* For stocks that are not rated, I/B/E/S consensus forecast numbers are used. CFROI® Spread is the difference between CFROI® and market implied discount rate. A larger number indicates

that more value is created by a company

14 September 2012

David & Goliath 19

China – Street talk * Central China Real Estate (0832.HK, HK$1.89, NR) contracted sales drop by 35% YoY. Central China Real Estate, a Henan Province-based and Hong Kong-listed property developer, announced that its contracted sales in Aug sat at Rmb978 mn, up 22% MoM but down 35% YoY. In the month its property contracted sales area decreased 14% MoM and 36% YoY to 165,345 sqm. In the first eight months of this year the company's contracted sales totalled Rmb6.9 bn, up 8% YoY and accounting for 77% of its sales target of Rmb9 bn. Meanwhile, its contracted sales area hit 1.07 mn sqm, up 3% YoY. (10-Sep)

70

80

90

100

110

120

09/11 12/11 03/12 06/12 09/12

Central China Real Estate MSCI China

China Molybdenum (3993.HK, HK$3.43, NR) receives formal written approval from CSRC. China Molybdenum announced that it received the formal written approval from the CSRC for the A share issue on 7 Sep. The A share issue will comprise the allotment and issue of not more than 542,000,000 A shares to qualified public investors. (10-Sep)

50

65

80

95

110

09/11 12/11 03/12 06/12 09/12

China Molybdenum MSCI China

SMIC (0981.HK, HK$.30, N [V], TP HK$.41) revenue increases SMIC has reported that revenues for 2Q12 climbed 27% QoQ and 20% YoY to a record US$422 mn. SMIC credited the positive sales performance to rising sales generated from its 65nm/55nm process technologies, and specialty processes for the manufacture of power management ICs, EEPROM and others. (12-Sep)

40

60

80

100

120

09/11 12/11 03/12 06/12 09/12

SMIC MSCI China

China Tianyi (0756.HK, HK$1.18, NR) net profit climbs 63%. China Tianyi registered a profit attributable to owners of Rmb250 mn for the year ended Jun 2012, jumping approximately 63%. The firm did not declare the payment of a final dividend to shareholders in respect of the year. (13-Sep)

50

65

80

95

110

09/11 12/11 03/12 06/12 09/12

China Tianyi Holdings MSCI China

*Source: China Press Digest, CIS, DataStream

14 September 2012

David & Goliath 20

China – Company updates Green Dragon Gas (GDG.L, $4.10, O [V], TP $11.70) Lonking (3339.HK, HK$1.34, N [V], TP HK$1.80)

New report: Darkest before dawn

■ 1H12 results—still loss making: With no major production gain,

the first-half loss was unsurprising, but all eyes likely turn to the

balance sheet—to see that near cash (cash + ‘other financial

assets’) reduced by US$56 mn in the half to US$80 mn.

■ Production update I—more wells drilled: GDG recorded 8,789

metres of in-seam drilling in 1H12; we assume that eight lateral

wells were drilled in the half.

■ Production update II—exit production waiting to ramp: We

update our drill-up/production forecasts—now exiting 2012 at

2.1Bcf, and reaching 18Bcf in 3Q14, assuming additional funding

is introduced on a timely basis.

■ Reiterate OUTPERFORM, new TP at $11.7/share: A recent site

visit confirmed a significant increase in on-site activity; however,

GDG has slipped from our earlier growth forecast. We update our

drill-up/production model, but retain our valuation methodology

i.e. de-risking our GSS DCF forecast via a percentage of total

wells drilled. Our new TP is arrived at US$11.7/sh (from

US$15.1/sh) and we retain our OUTPERFORM rating.

Comment on August sales

■ Lonking released its August sales on 11 September. Wheel

loader sales at 1,810 units, fell 25.4% YoY, moderating from 37%

YoY decline in July and largely within expectations. Sequentially,

unit sales grew by 4% MoM. We estimate Lonking’s market share

will remain below 15%, declining from above 18% in 2011.

■ The company’s excavator sales were stronger than expected.

Excavator sales in August were at 242 units, recording a 14.7%

YoY increase. Sequentially, sales rose 18.6% MoM (versus 17%

MoM decline in August last year), driven by higher exports (44

units versus 12 units in July). Domestic unit sales grew modestly

by 3% MoM. Lonking’s market share in excavator market is

showing solid improvement: from low of 2.5% in 1Q12 to 3.8% in

August.

■ Trading at 0.7x P/B with overhang from convertible bond

redemption removed coupled with prudent risk management, we

believe Lonking’s shares are cheap.

■ But the stock could face further earnings cuts and re-rating

requires improvement in industry fundamentals, which is not yet

within sight. We maintain our NEUTRAL rating on the stock.

Bbg/RIC 4.15

11.70 (15.10)

136.54 182

0.0

0.1

Free float (%) 35 Performance 1M 3M 12M

Absolute (%) (19.4) (30.6) (50.8)

Relativ e (%) (15.7) (29.7) (48.3)

Year 12/10A 12/11A 12/12E 12/13E 12/14E

49.7 75.2 80.7 154.4 228.9

1.3 -13.0 -4.9 2.9 44.9

-13.2 -27.6 -15.1 -16.9 11.6

(0.11) (0.20) (0.11) (0.12) 0.08

n.a. n.a. n.m n.m (87)

n.a. n.a. 0.03 0.15 1.14

n.m. n.m. n.m. n.m. n.m.

n.m. n.m. n.m. n.m. 48.9

0.0 0.0 0.0 0.0 0.0

401.7 -42.8 -122.2 254.7 18.9

0.8 0.9 0.9 0.9 0.9

-2.2 -4.2 -2.4 -2.7 1.9

-8.2 -1.3 4.1 29.3 44.1

10.13 - 3.70

566.5

ROE (%)

Note1: Green Dragon Gas (GDG) is the largest independent CBM producer in China. GDG holds 6 PSCs in China on its upstream side, owns its

transportation fleet and pipelines in midstream distribution, and sells its gas through CNG stations on its downstream side.

Mkt cap (US$ mn)Daily trad v al - 6m av g (US$ mn)

Major shareholders Randeep Grew al 64%

Net debt(cash)/equity (%)

Rev enue (US$ mn)

52-w k range (US$)

GDG LN / GDG.L

O (O) [V]

Daily trad v ol - 6m av g (mn)

Rating (prev. rating)

Shares outstanding (mn)

Price (10 Sep 12 , US$)

TP (prev. TP US$)

Est. pot. % chg. to TP

EBITDA (US$ mn)

Net profit (US$ mn)

EPS (US$)

- Change from prev . EPS (%)

- Consensus EPS (US$)

EPS grow th (%)

P/E (x )

Div idend y ield (%)

EV/EBITDA (x )

P/B (x )

Bbg/RIC 1.30

1.80 (1.80)

4,280.10 38

20.6

4.6

Free float (%) 39.3 Performance 1M 3M 12M

Absolute (%) (17.2) (35.6) (57.1)

Relativ e (%) (13.4) (34.7) (54.6)

Year 12/10A 12/11A 12/12E 12/13E 12/14E

12,020 12,721 9,472 10,551 10,551

2,560 2,358 1,410 1,628 2,166

1,766 1,730 544 738 1,191

0.41 0.40 0.13 0.17 0.28

n.a. n.a. 0 0 0

n.a. n.a. 0.19 0.23 0.27

120.7 -2.0 -68.5 35.6 61.4

2.6 2.6 8.4 6.2 3.8

2.9 7.8 13.3 4.2 5.7

2.9 3.5 5.1 4.2 2.7

0.9 0.7 0.7 0.7 0.6

39.1 29.7 8.5 11.1 16.2

55.5 57.4 42.6 32.3 15.8

3.50 - 1.01

5,564.1/ 717.6

ROE (%)

Note1:ORD/ADR=50.00.Note2:Lonking Holdings Limited is engaged in the manufacture and distribution of wheel loaders, road rollers, excavators, fork lifts,

and other infrastructure machinery and the provision of finance lease for the infrastructure machinery..

Mkt cap (HK$/US$ mn)Daily trad v al - 6m av g (US$ mn)

Major shareholders China Longgong (30.66%)

Net debt(cash)/equity (%)

Rev enue (Rmb mn)

52-w k range (HK$)

3339 HK / 3339.HK

N (N) [V]

Daily trad v ol - 6m av g (mn)

Rating (prev. rating)

Shares outstanding (mn)

Price (11 Sep 12 , HK$)

TP (prev. TP HK$)

Est. pot. % chg. to TP

EBITDA (Rmb mn)

Net profit (Rmb mn)

EPS (Rmb)

- Change from prev . EPS (%)

- Consensus EPS (Rmb)

EPS grow th (%)

P/E (x )

Div idend y ield (%)

EV/EBITDA (x )

P/B (x )

Price performance vs. MSCI China Price performance vs. MSCI China

40

60

80

100

120

09/11 11/11 01/12 03/12 05/12 07/12 09/12

Green Dragon Gas MSCI China

30

50

70

90

110

09/11 11/11 01/12 03/12 05/12 07/12 09/12

Lonking MSCI China

David Hewitt / Research Analyst / +65 6212 3064 /

Extracted from The Asian Daily 12 Sep 2012

Yang Y. Song / Research Analyst / 852 2101 6550 /

Extracted from The Asian Daily 12 Sep 2012

14 S

ep

tem

ber 2

01

2

David

& G

olia

th

21

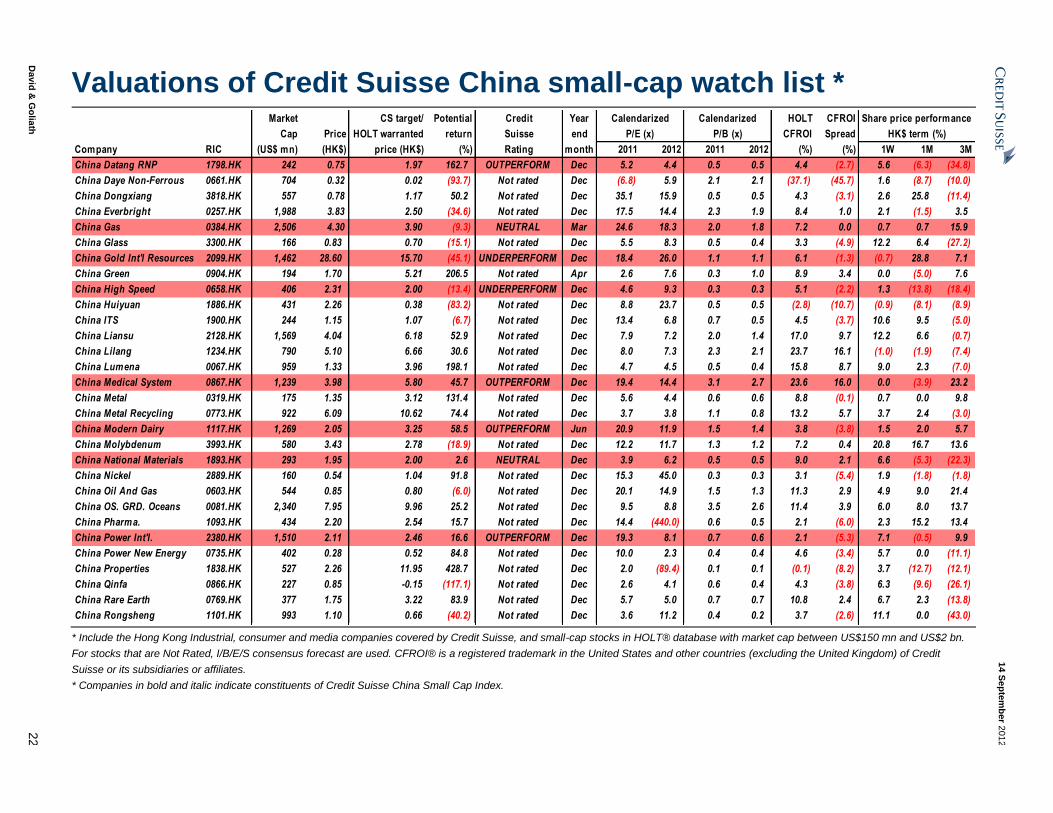

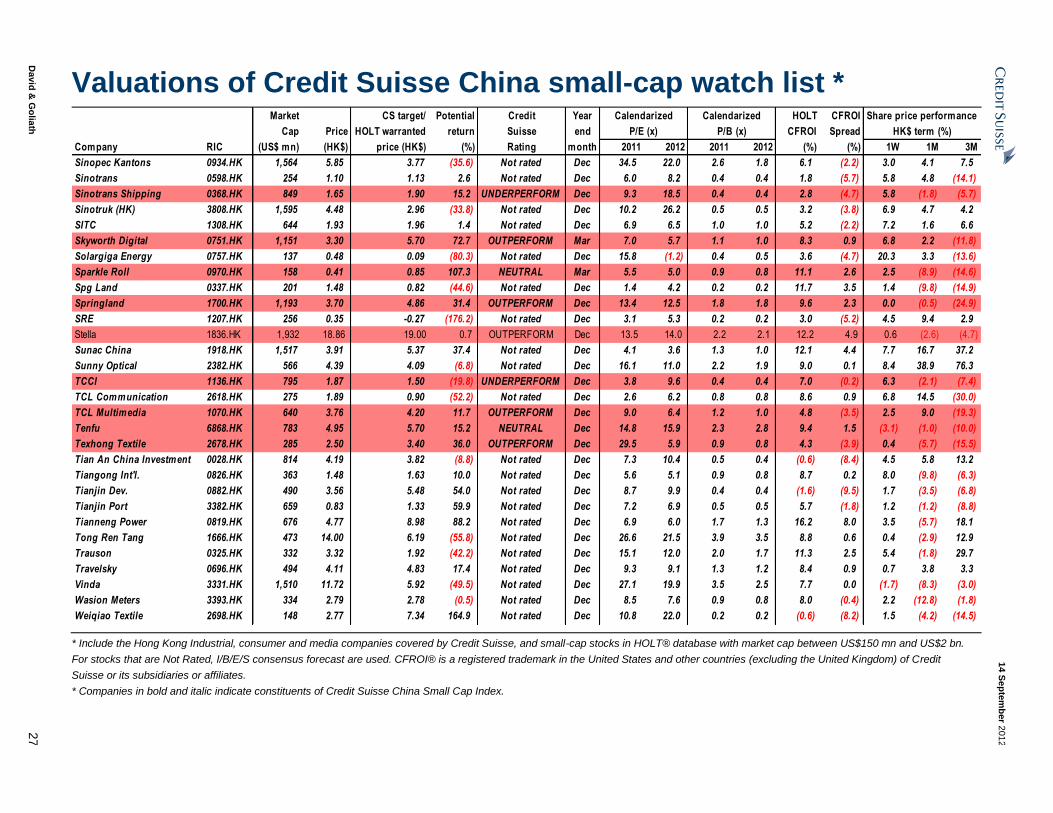

Valuations of Credit Suisse China small-cap watch list*

Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI Spread

Company RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2011 2012 2011 2012 (%) (%) 1W 1M 3M

361 Degrees 1361.HK 531 1.99 3.20 60.8 Not rated Jun n.a. 3.3 n.a. 0.7 24.6 16.8 5.9 2.1 1.0

Ajisen 0538.HK 735 5.31 6.16 15.9 NEUTRAL Dec 17.4 43.1 1.9 1.9 4.8 (2.5) 12.0 (0.4) (6.8)

Anhui Expressway 0995.HK 210 3.31 4.88 47.5 Not rated Dec 5.3 5.7 0.7 0.6 7.0 (1.6) 0.9 (6.5) (3.5)

Anta Sports 2020.HK 1,772 5.51 5.20 (5.6) NEUTRAL Dec 6.5 7.9 1.8 1.6 22.9 16.0 16.0 21.1 (7.6)

Anton Oilfield 3337.HK 530 1.94 1.13 (41.9) Not rated Dec 43.0 19.3 2.0 1.8 6.2 (2.4) 5.4 31.1 67.2

Asia Cement (China) 0743.HK 620 3.09 3.24 4.8 Not rated Dec 2.9 10.3 0.5 0.4 9.1 1.5 5.5 1.6 (9.4)

Asian Citrus 0073.HK 579 3.68 7.37 100.2 Not rated Jun 3.4 3.9 0.6 0.5 14.4 6.5 6.4 (3.2) (11.5)

AviChina Ind.& Tech. 2357.HK 924 3.04 1.90 (37.4) Not rated Dec 30.3 23.7 1.8 1.7 4.9 (2.2) 9.4 18.8 7.8

Baoxin Auto 1293.HK 1,200 3.68 4.51 22.6 Not rated Dec 11.1 7.2 2.5 1.4 11.3 4.2 (1.9) 1.1 (30.7)

Baoye 2355.HK 171 4.25 11.32 166.4 Not rated Dec 3.2 2.9 0.5 0.5 10.6 2.2 3.9 8.7 6.5

Bawang 1338.HK 225 0.60 0.28 (52.7) Not rated Dec (2.6) (8.3) 1.4 1.4 (63.7) (71.9) 3.4 7.1 (4.8)

Beijing Capital Land 2868.HK 290 2.20 1.23 (44.0) Not rated Dec 3.8 3.3 0.6 0.6 5.3 (2.6) 12.8 (10.2) (1.3)

Beijing Enterprises Water 0371.HK 521 1.72 0.40 (76.9) Not rated Dec 19.2 14.3 1.7 1.3 5.9 (1.3) 11.0 11.7 14.7

Beijing Jingkelong 0814.HK 88 3.74 1.39 (63.0) Not rated Dec 6.0 6.3 0.8 0.7 5.6 (2.6) (0.8) (25.3) (31.0)

Beijing Jingneng 0579.HK 355 1.68 1.28 (23.6) Not rated Dec 8.6 8.9 0.9 1.0 5.5 (1.1) 3.1 (6.1) 0.0

Besunyen 0926.HK 126 0.62 0.82 32.2 Not rated Dec (25.4) (29.9) 0.5 0.4 (1.8) (10.3) 0.0 (6.1) (21.5)

Billion Industiral 2299.HK 1,263 4.26 6.29 47.7 Not rated Dec 8.1 8.1 1.6 1.4 14.6 8.0 4.4 3.1 2.7

Biostime Intl 1112.HK 1,627 20.95 15.80 (24.6) Not rated Dec 19.5 15.2 5.2 4.4 22.1 14.3 5.9 15.4 12.6

Boshiwa 1698.HK 450 1.68 2.50 48.8 NEUTRAL Dec 9.1 6.5 0.9 0.8 7.5 2.6 0.0 0.0 0.0

Bosideng 3998.HK 2,375 2.30 1.98 (13.9) Not rated Mar 10.6 10.4 2.1 1.9 13.0 6.0 5.5 1.8 28.5

BYD Electronic 0285.HK 462 1.59 4.40 176.4 Not rated Dec 4.8 5.0 0.4 0.3 4.4 (3.4) 8.2 (1.9) (17.6)

Catic Shenzhen 0161.HK 96 2.69 2.16 (19.6) Not rated Dec 7.0 6.5 0.6 0.6 5.5 (3.0) 9.8 (6.3) (5.6)

Central China Real Estate 0832.HK 592 1.89 6.50 243.7 Not rated Dec 4.6 4.4 0.8 0.8 14.9 6.9 6.2 (5.5) 1.6

Chaowei Power 0951.HK 572 4.41 12.29 178.6 Not rated Dec 8.0 6.5 2.1 1.5 20.1 11.8 4.3 (4.1) 13.7

Chigo 0449.HK 186 0.17 0.19 9.0 Not rated Dec (8.4) 3.7 0.5 0.4 0.8 (7.2) 1.8 (13.6) (18.2)

Chiho-Tiande 0976.HK 524 3.89 1.70 (56.2) Not rated Dec 25.9 21.0 2.0 1.3 4.8 (3.1) 0.0 (1.5) (6.3)

China Aerospace 0031.HK 215 0.54 0.59 9.3 Not rated Dec 4.1 12.4 0.4 0.4 2.9 (5.8) 1.9 (5.3) (11.5)

China All Access 0633.HK 185 1.18 2.48 109.9 Not rated Dec 5.6 4.4 0.9 0.8 13.4 4.6 0.0 (22.9) (18.1)

China Aoyuan 3883.HK 327 0.97 0.77 (20.7) Not rated Dec 4.6 6.0 0.3 0.3 3.5 (4.7) 5.4 (3.0) (4.9)

China Automation 0569.HK 222 1.68 1.83 9.0 Not rated Dec 7.1 6.5 0.8 0.7 11.1 3.0 14.3 17.5 (15.2)

Share price performance

HK$ term (%)P/B (x)P/E (x)

CalendarizedCalendarized

* Include the China Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$150 mn and US$2 bn. For

stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit Suisse or

its subsidiaries or affiliates.

* Companies in bold and italic indicate constituents of Credit Suisse China Small Cap Index.

14 S

ep

tem

ber 2

01

2

David

& G

olia

th

22

Valuations of Credit Suisse China small-cap watch list *

Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI Spread

Company RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2011 2012 2011 2012 (%) (%) 1W 1M 3M

China Datang RNP 1798.HK 242 0.75 1.97 162.7 OUTPERFORM Dec 5.2 4.4 0.5 0.5 4.4 (2.7) 5.6 (6.3) (34.8)

China Daye Non-Ferrous 0661.HK 704 0.32 0.02 (93.7) Not rated Dec (6.8) 5.9 2.1 2.1 (37.1) (45.7) 1.6 (8.7) (10.0)

China Dongxiang 3818.HK 557 0.78 1.17 50.2 Not rated Dec 35.1 15.9 0.5 0.5 4.3 (3.1) 2.6 25.8 (11.4)

China Everbright 0257.HK 1,988 3.83 2.50 (34.6) Not rated Dec 17.5 14.4 2.3 1.9 8.4 1.0 2.1 (1.5) 3.5

China Gas 0384.HK 2,506 4.30 3.90 (9.3) NEUTRAL Mar 24.6 18.3 2.0 1.8 7.2 0.0 0.7 0.7 15.9

China Glass 3300.HK 166 0.83 0.70 (15.1) Not rated Dec 5.5 8.3 0.5 0.4 3.3 (4.9) 12.2 6.4 (27.2)

China Gold Int'l Resources 2099.HK 1,462 28.60 15.70 (45.1) UNDERPERFORM Dec 18.4 26.0 1.1 1.1 6.1 (1.3) (0.7) 28.8 7.1

China Green 0904.HK 194 1.70 5.21 206.5 Not rated Apr 2.6 7.6 0.3 1.0 8.9 3.4 0.0 (5.0) 7.6

China High Speed 0658.HK 406 2.31 2.00 (13.4) UNDERPERFORM Dec 4.6 9.3 0.3 0.3 5.1 (2.2) 1.3 (13.8) (18.4)

China Huiyuan 1886.HK 431 2.26 0.38 (83.2) Not rated Dec 8.8 23.7 0.5 0.5 (2.8) (10.7) (0.9) (8.1) (8.9)

China ITS 1900.HK 244 1.15 1.07 (6.7) Not rated Dec 13.4 6.8 0.7 0.5 4.5 (3.7) 10.6 9.5 (5.0)

China Liansu 2128.HK 1,569 4.04 6.18 52.9 Not rated Dec 7.9 7.2 2.0 1.4 17.0 9.7 12.2 6.6 (0.7)

China Lilang 1234.HK 790 5.10 6.66 30.6 Not rated Dec 8.0 7.3 2.3 2.1 23.7 16.1 (1.0) (1.9) (7.4)

China Lumena 0067.HK 959 1.33 3.96 198.1 Not rated Dec 4.7 4.5 0.5 0.4 15.8 8.7 9.0 2.3 (7.0)

China Medical System 0867.HK 1,239 3.98 5.80 45.7 OUTPERFORM Dec 19.4 14.4 3.1 2.7 23.6 16.0 0.0 (3.9) 23.2

China Metal 0319.HK 175 1.35 3.12 131.4 Not rated Dec 5.6 4.4 0.6 0.6 8.8 (0.1) 0.7 0.0 9.8

China Metal Recycling 0773.HK 922 6.09 10.62 74.4 Not rated Dec 3.7 3.8 1.1 0.8 13.2 5.7 3.7 2.4 (3.0)

China Modern Dairy 1117.HK 1,269 2.05 3.25 58.5 OUTPERFORM Jun 20.9 11.9 1.5 1.4 3.8 (3.8) 1.5 2.0 5.7

China Molybdenum 3993.HK 580 3.43 2.78 (18.9) Not rated Dec 12.2 11.7 1.3 1.2 7.2 0.4 20.8 16.7 13.6

China National Materials 1893.HK 293 1.95 2.00 2.6 NEUTRAL Dec 3.9 6.2 0.5 0.5 9.0 2.1 6.6 (5.3) (22.3)

China Nickel 2889.HK 160 0.54 1.04 91.8 Not rated Dec 15.3 45.0 0.3 0.3 3.1 (5.4) 1.9 (1.8) (1.8)

China Oil And Gas 0603.HK 544 0.85 0.80 (6.0) Not rated Dec 20.1 14.9 1.5 1.3 11.3 2.9 4.9 9.0 21.4

China OS. GRD. Oceans 0081.HK 2,340 7.95 9.96 25.2 Not rated Dec 9.5 8.8 3.5 2.6 11.4 3.9 6.0 8.0 13.7

China Pharma. 1093.HK 434 2.20 2.54 15.7 Not rated Dec 14.4 (440.0) 0.6 0.5 2.1 (6.0) 2.3 15.2 13.4