data monitor market analysis nice

TRANSCRIPT

www.datamonitor.com Datamonitor USA

245 Fifth Avenue

4th Floor

New York, NY 10016

USA

t: +1 212 686 7400

f: +1 212 686 2626

Datamonitor Europe

119 Farringdon Road

London EC1R 3DA

United Kingdom

t: +44 20 7551 9000

f: +44 20 7675 7500

Datamonitor Middle East

and North Africa

Datamonitor

PO Box 24893

Dubai, UAE

t: +49 69 9754 4517

f: +49 69 9754 4900

e: datamonitormena@

datamonitor.com

Datamonitor Asia Pacific

Level 46, 2 Park Street

Sydney, NSW 2000

Australia

t: +61 2 8705 6900

f: +61 2 8705 6901

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 1

INDUSTRY PROFILE

Dairy in

India

Reference Code: 0102-0711

Publication Date: October 2010

EXECUTIVE SUMMARY

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 2

EXECUTIVE SUMMARY

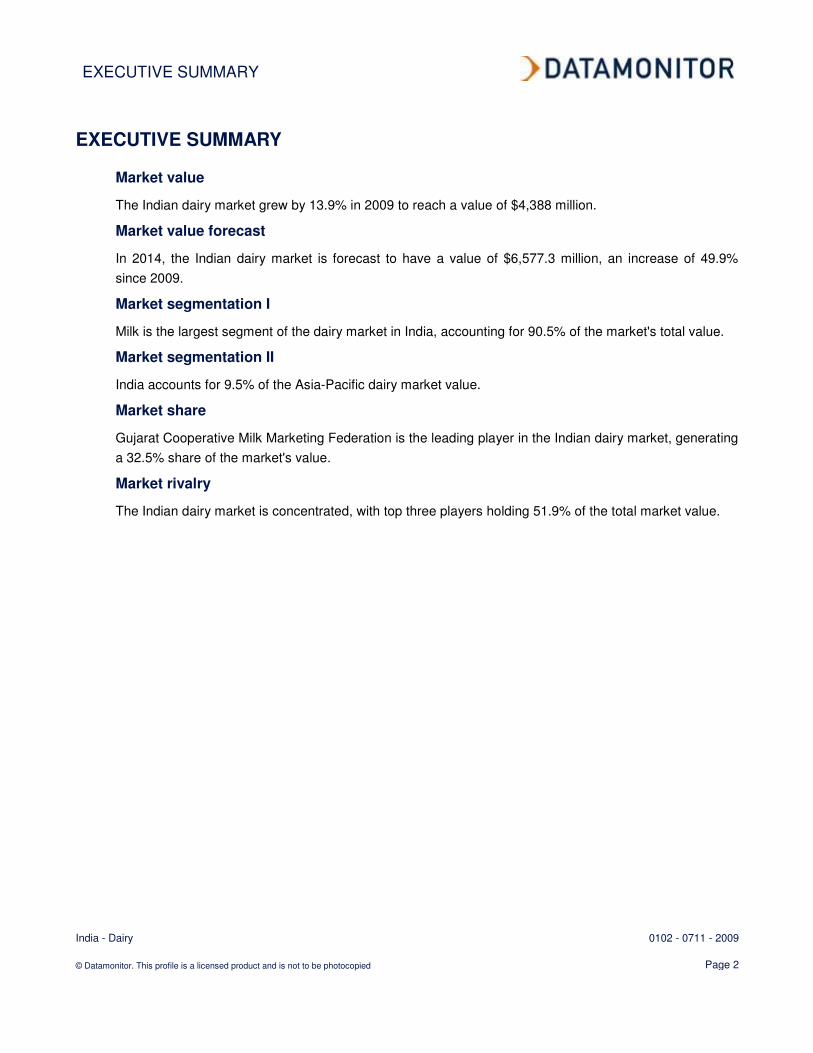

Market value

The Indian dairy market grew by 13.9% in 2009 to reach a value of $4,388 million.

Market value forecast

In 2014, the Indian dairy market is forecast to have a value of $6,577.3 million, an increase of 49.9%

since 2009.

Market segmentation I

Milk is the largest segment of the dairy market in India, accounting for 90.5% of the market's total value.

Market segmentation II

India accounts for 9.5% of the Asia-Pacific dairy market value.

Market share

Gujarat Cooperative Milk Marketing Federation is the leading player in the Indian dairy market, generating

a 32.5% share of the market's value.

Market rivalry

The Indian dairy market is concentrated, with top three players holding 51.9% of the total market value.

CONTENTS

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 3

TABLE OF CONTENTS

EXECUTIVE SUMMARY 2

MARKET OVERVIEW 6

Market definition 6

Research highlights 7

Market analysis 8

MARKET VALUE 9

MARKET SEGMENTATION I 10

MARKET SEGMENTATION II 11

MARKET SHARE 12

COMPETITIVE LANDSCAPE 13

LEADING COMPANIES 15

Gujarat Cooperative Milk Marketing Federation Ltd. 15

KCMMF (Kerala Cooperative Milk Marketing Federation) 17

Mother Dairy Fruit & Vegetable Pvt. Ltd. 18

MARKET DISTRIBUTION 19

MARKET FORECASTS 20

Market value forecast 20

MACROECONOMIC INDICATORS 21

APPENDIX 23

Methodology 23

Industry associations 24

Related Datamonitor research 24

Disclaimer 26

ABOUT DATAMONITOR 27

Premium Reports 27

Summary Reports 27

Datamonitor consulting 27

CONTENTS

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 4

LIST OF TABLES

Table 1: India dairy market value: $ million, 2005–09 9

Table 2: India dairy market segmentation I:% share, by value, 2009 10

Table 3: India dairy market segmentation II: % share, by value, 2009 11

Table 4: India dairy market share: % share, by value, 2009 12

Table 5: Gujarat Cooperative Milk Marketing Federation Ltd.: key facts 15

Table 6: KCMMF (Kerala Cooperative Milk Marketing Federation): key facts 17

Table 7: Mother Dairy Fruit & Vegetable Pvt. Ltd.: key facts 18

Table 8: India dairy market distribution: % share, by value, 2009 19

Table 9: India dairy market value forecast: $ million, 2009–14 20

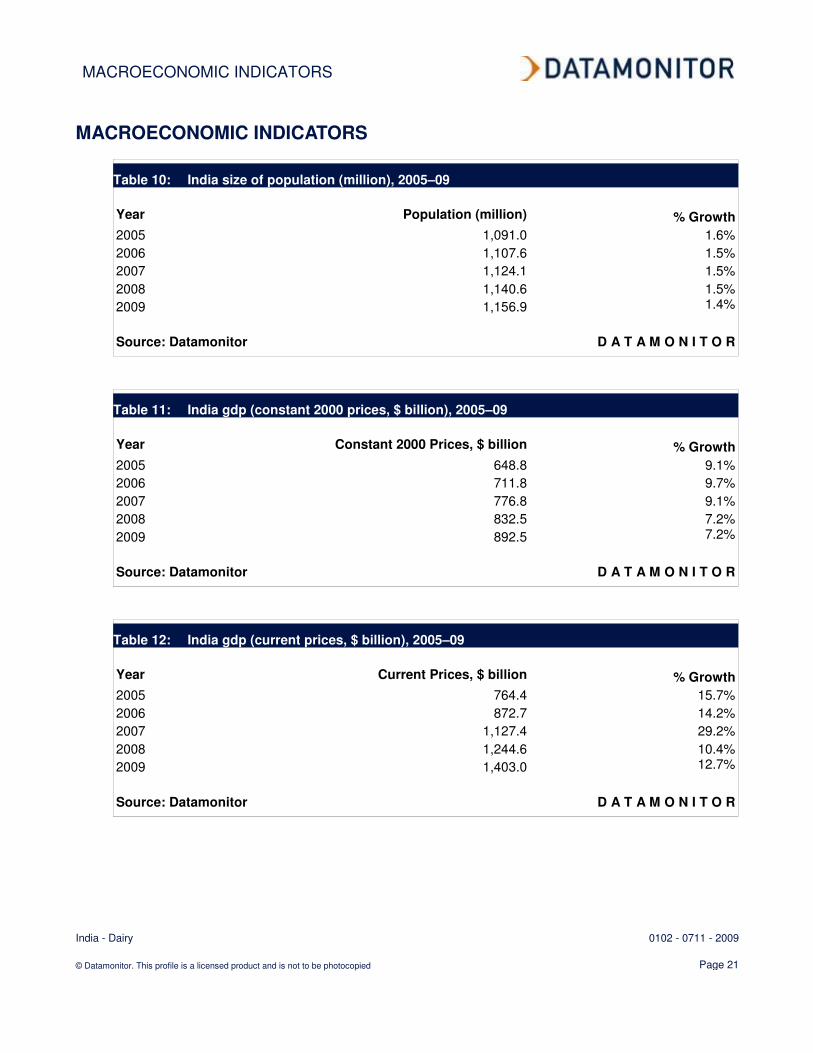

Table 10: India size of population (million), 2005–09 21

Table 11: India gdp (constant 2000 prices, $ billion), 2005–09 21

Table 12: India gdp (current prices, $ billion), 2005–09 21

Table 13: India inflation, 2005–09 22

Table 14: India consumer price index (absolute), 2005–09 22

Table 15: India exchange rate, 2005–09 22

CONTENTS

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 5

LIST OF FIGURES

Figure 1: India dairy market value: $ million, 2005–09 9

Figure 2: India dairy market segmentation I:% share, by value, 2009 10

Figure 3: India dairy market segmentation II: % share, by value, 2009 11

Figure 4: India dairy market share: % share, by value, 2009 12

Figure 5: India dairy market distribution: % share, by value, 2009 19

Figure 6: India dairy market value forecast: $ million, 2009–14 20

MARKET OVERVIEW

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 6

MARKET OVERVIEW

Market definition

The dairy market consists of retail sales of cheese, chilled desserts, cream, fromage frais, milk,

spreadable fats and yogurt. Any currency conversions used in the creation of this report have been

calculated using 2009 annual average exchange rates.

For the purpose of this report Asia-Pacific comprises Australia, China, Japan, India, Singapore, South

Korea and Taiwan.

MARKET OVERVIEW

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 7

Research highlights

The Indian dairy market generated total revenues of $4.4 billion in 2009, representing a compound annual

growth rate (CAGR) of 11.9% for the period spanning 2005-2009.

Milk sales proved the most lucrative for the Indian dairy market in 2009, generating total revenues of $4

billion, equivalent to 90.5% of the market's overall value.

The performance of the market is forecast to decelerate, with an anticipated CAGR of 8.4% for the five-

year period 2009-2014, which is expected to lead the market to a value of $6.6 billion by the end of 2014.

MARKET OVERVIEW

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 8

Market analysis

The Indian dairy market grew strongly in 2005-2009 period, reaching double digit rates, as a result of

strong sales growth in the cheese category. Gradual deceleration is expected in the forecast period;

however, the growth within the market will remain strong.

The Indian dairy market generated total revenues of $4.4 billion in 2009, representing a compound annual

growth rate (CAGR) of 11.9% for the period spanning 2005-2009. In comparison, the Chinese and

Japanese markets grew with CAGRs of 2.5% and 2.6% respectively, over the same period, to reach

respective values of $16.5 billion and $21.4 billion in 2009.

Milk sales proved the most lucrative for the Indian dairy market in 2009, generating total revenues of $4

billion, equivalent to 90.5% of the market's overall value. In comparison, sales of spreadable fats

generated revenues of $161.5 million in 2009, equating to 3.7% of the market's aggregate revenues.

The performance of the market is forecast to decelerate, with an anticipated CAGR of 8.4% for the five-

year period 2009-2014, which is expected to lead the market to a value of $6.6 billion by the end of 2014.

Comparatively, the Chinese and Japanese markets will grow with CAGRs of 8.9% and 2.9% respectively,

over the same period, to reach respective values of $25.2 billion and $24.8 billion in 2014.

MARKET VALUE

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 9

MARKET VALUE

The Indian dairy market grew by 13.9% in 2009 to reach a value of $4,388 million.

The compound annual growth rate of the market in the period 2005–09 was 11.9%.

Table 1: India dairy market value: $ million, 2005–09

Year $ million Rs. million € million % Growth

2005 2,798.5 136,705.1 2,012.5

2006 2,982.6 145,701.5 2,145.0 6.6%

2007 3,174.5 155,075.6 2,283.0 6.4%

2008 3,851.6 188,148.7 2,769.9 21.3%

2009 4,388.0 214,355.7 3,155.7 13.9%

CAGR: 2005–09 11.9%

Source: Datamonitor D A T A M O N I T O R

Figure 1: India dairy market value: $ million, 2005–09

Source: Datamonitor D A T A M O N I T O R

MARKET SEGMENTATION I

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 10

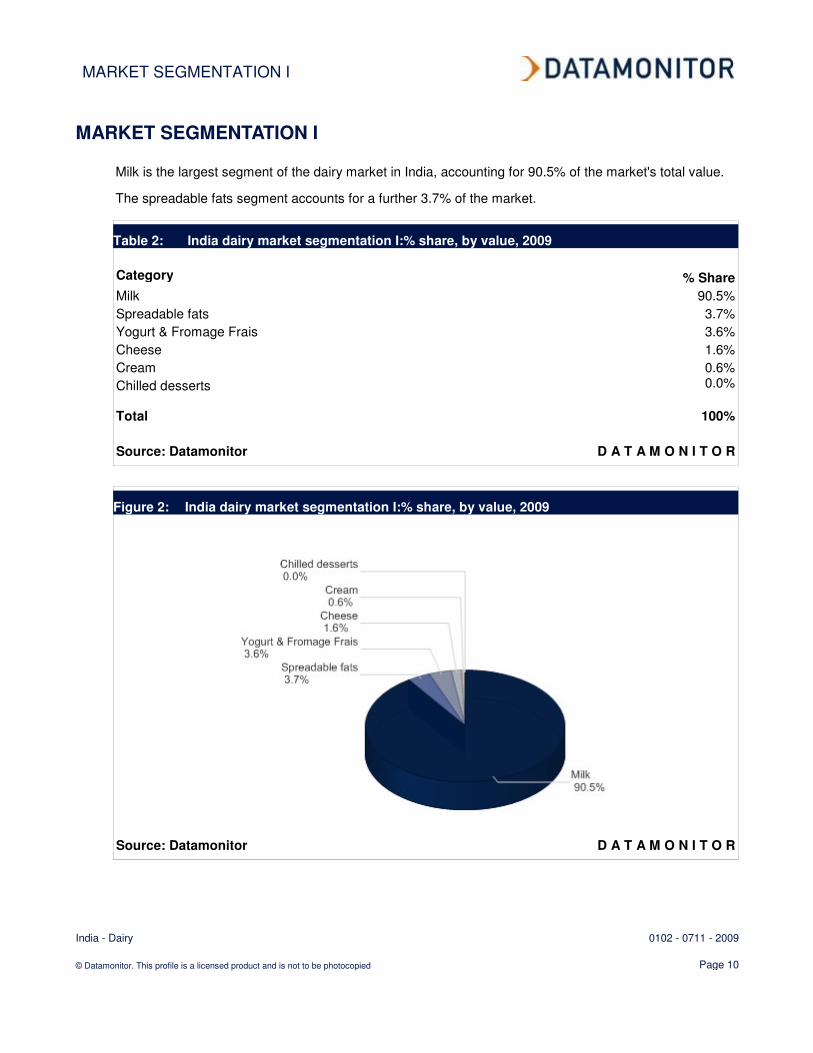

MARKET SEGMENTATION I

Milk is the largest segment of the dairy market in India, accounting for 90.5% of the market's total value.

The spreadable fats segment accounts for a further 3.7% of the market.

Table 2: India dairy market segmentation I:% share, by value, 2009

Category % Share

Milk 90.5%

Spreadable fats 3.7%

Yogurt & Fromage Frais 3.6%

Cheese 1.6%

Cream 0.6%

Chilled desserts 0.0%

Total 100%

Source: Datamonitor D A T A M O N I T O R

Figure 2: India dairy market segmentation I:% share, by value, 2009

Source: Datamonitor D A T A M O N I T O R

MARKET SEGMENTATION II

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 11

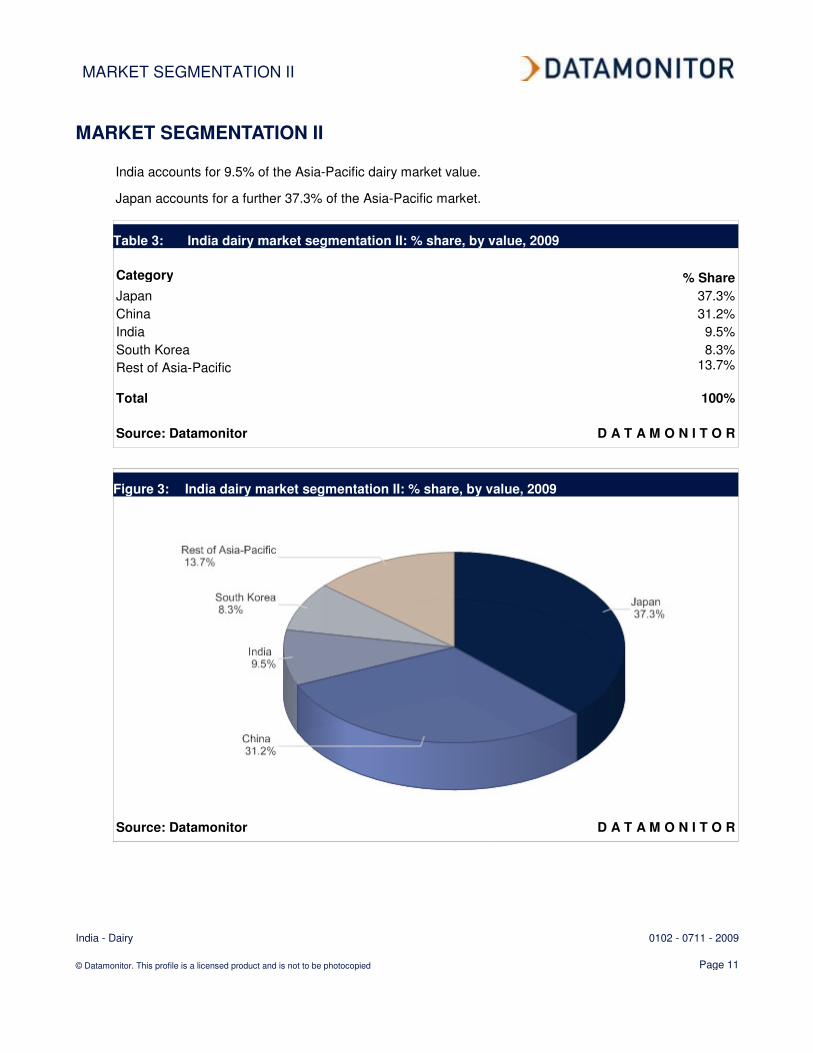

MARKET SEGMENTATION II

India accounts for 9.5% of the Asia-Pacific dairy market value.

Japan accounts for a further 37.3% of the Asia-Pacific market.

Table 3: India dairy market segmentation II: % share, by value, 2009

Category % Share

Japan 37.3%

China 31.2%

India 9.5%

South Korea 8.3%

Rest of Asia-Pacific 13.7%

Total 100%

Source: Datamonitor D A T A M O N I T O R

Figure 3: India dairy market segmentation II: % share, by value, 2009

Source: Datamonitor D A T A M O N I T O R

MARKET SHARE

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 12

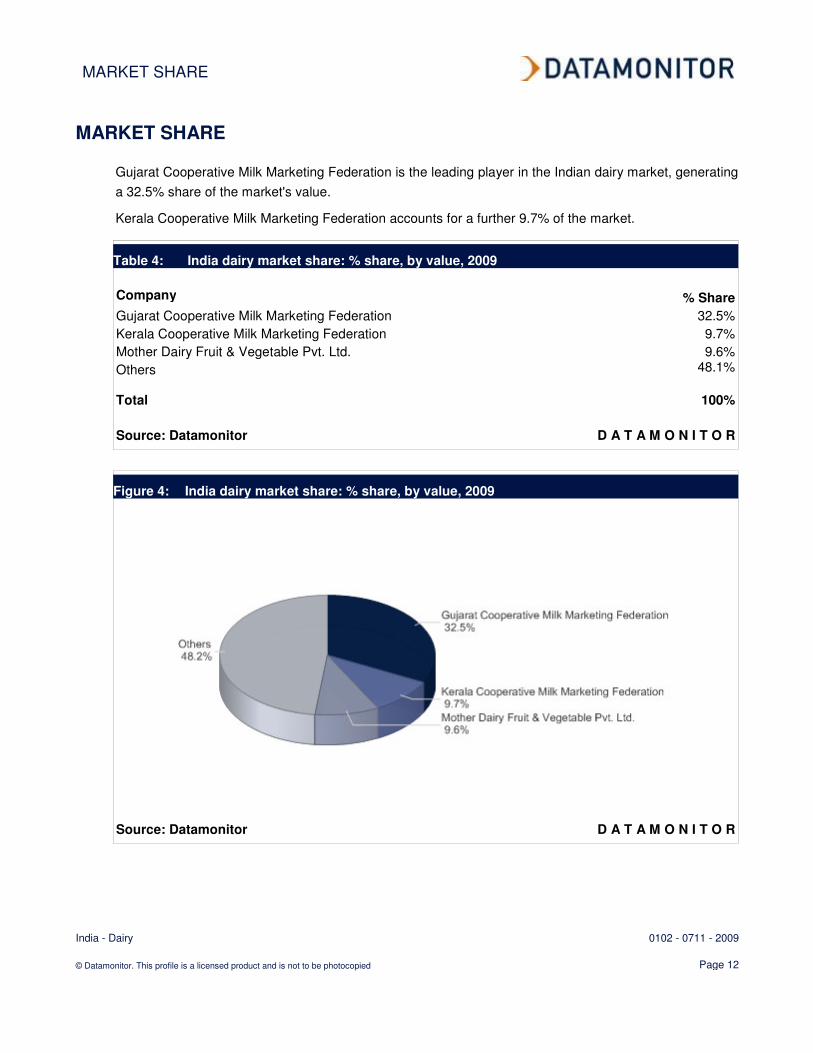

MARKET SHARE

Gujarat Cooperative Milk Marketing Federation is the leading player in the Indian dairy market, generating

a 32.5% share of the market's value.

Kerala Cooperative Milk Marketing Federation accounts for a further 9.7% of the market.

Table 4: India dairy market share: % share, by value, 2009

Company % Share

Gujarat Cooperative Milk Marketing Federation 32.5%

Kerala Cooperative Milk Marketing Federation 9.7%

Mother Dairy Fruit & Vegetable Pvt. Ltd. 9.6%

Others 48.1%

Total 100%

Source: Datamonitor D A T A M O N I T O R

Figure 4: India dairy market share: % share, by value, 2009

Source: Datamonitor D A T A M O N I T O R

COMPETITIVE LANDSCAPE

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 13

COMPETITIVE LANDSCAPE

The dairy market will be analyzed taking manufacturers/packagers of dairy products as players. The key

buyers will be taken as food retailers, and dairy farmers as the key suppliers.

The Indian dairy market is concentrated, with top three players holding 51.9% of the total market value.

Suppliers commonly integrate forward, as dairy co-operatives offer farmers the opportunity to access

larger markets and use capital items, such as packaging and processing plants. The dairy market is fairly

easy to enter as a small enterprise, however in order to supply to the mass market consumer companies

must be large and have some level of integration, if successful market entry is to be secured. A wide

range of food and drink products can be used in similar ways to dairy products and therefore it becomes

easy for consumers to replace dairy products with such alternatives, if dairy prices rise too high. Rivalry,

however, is strong as there are numerous players present that are generally similar to one another

despite most operating diverse dairy portfolios.

In India, the main distribution channels for the dairy market are independent retailers, which account for

10.9% of the total market value. Food and beverage retail is fragmented in India: the non-organized

segment accounts for a significant share of its revenues, and independents and small supermarket chains

are significant in the organized segment. Stringent regulations make it difficult for large foreign retailers,

such as Wal-Mart, to gain access to the retail market. In these circumstances, where market players have

many small potential buyers, buyer power is weakened. It is difficult to differentiate staple foods, such as

milk and butter; however, cheese and yogurt products are more differentiated, with a number of niche

cheese markets in operation. The dairy market is highly price sensitive, as buyers will tend to choose the

cheaper option, especially in the milk market, subsequently enhancing buyer power. Manufacturers can

target end-users with their branding strategies, or develop more individual, premium products, such as

organic yoghurt, to counter balance the power of buyer to make purchasing decisions on price alone.

Overall, buyer power is assessed as strong.

Key suppliers to this market are dairy farmers. Dairy products are by definition made of milk, and there

are therefore no real alternatives to raw materials. Dairy cooperatives, which typically integrate dairy

farming, milk collection, processing, and packaging, are present in developed-economy markets (e.g.

Campina in Europe); however, they have a much more prominent role in India. Almost 100,000 dairy

cooperatives are organized into 170 "producer unions", which are combined at state level into 15

cooperative milk marketing federations. Some of the latter have strong brands and enjoy consumer

recognition, i.e. Amul. As the Indian market is dominated by such cooperatives, the suppliers of interest

are further upstream, and include manufacturers of cattle feed, milking machines, packaging, and

providers of service, such as veterinary care and artificial insemination. The products involved are fairly

commoditized, and there are a reasonable number of suppliers; also, the ability of cooperatives to

purchase on behalf of their members (who may be very small-scale farmers) means that supplier power is

correspondingly decreased. Overall, supplier power is moderate.

COMPETITIVE LANDSCAPE

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 14

In the Indian dairy market, small-scale entry, perhaps as an artisanal producer of premium dairy products,

does not require very large amounts of capital. However, for new entrants aiming to challenge the major

players in the mass-consumer market, entry barriers are higher. Scale economies in production are

important, especially in countries, where a consolidated food retail sector means that players are forced to

compete intensely on price. Most dairy products are perishable, which means that reliable supply and

distribution chains are vital to avoid the costs of wastage - this can be a particular barrier to entry in less

developed economies. Leading dairy product manufacturers may have strong brands, more apparent

yogurt and butter products, aimed at retaining end-user loyalty, which means that new players will have a

more difficult task to distinguish their own brands. Overall, there is a strong likelihood of new players in

the dairy market.

From the consumer's point of view, dairy products may be used directly as food or beverages, but also

ingredients for other home-made foods. There is a wide range of food and drink that can be used in

similar ways to dairy products, so if dairy prices raise too high, it is possible for consumers to replace

them with alternatives. This reduces the pricing freedom of retailers and market players. Some of the

alternatives may have advantages for retailers, such as cheaper storage or higher margins. Dairy

products are important parts of most peoples' diet, with the benefits of calcium highly publicized, therefore

are unlikely to be completely replaced. Overall, the threat of substitutes is assessed as moderate.

The Indian dairy market is tending towards concentration, with top three players holding 51.9% of the total

market value. The market is dominated by milk federations, such as Gujarat Co-operative Milk Marketing

Federation and Kerala Cooperative Milk Marketing Federation. This indicates the presence of large sized

competitors, which boosts rivalry. Switching costs for buyers are not particularly high, although some

retailers may allocate contracts to single suppliers of dairy products. The larger multinational players tend

to operate in a number of fast moving consumer goods markets, therefore may not be as reliant on sales

of dairy products, which decreases rivalry. As dairy products are usually perishable, storage costs are

high. Industrial production of dairy products requires substantial, specialized assets, and the need to sell

these off when leaving the market translates into high exit costs. The strong growth in the Indian dairy

products market in recent years eases rivalry to a certain extent. Overall, rivalry is assessed as moderate.

LEADING COMPANIES

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 15

LEADING COMPANIES

Gujarat Cooperative Milk Marketing Federation Ltd.

Table 5: Gujarat Cooperative Milk Marketing Federation Ltd.: key facts

Head office: Amul Dairy Road, Anand 388 001, Gujarat, IND

Telephone: 91 2692 258 506

Fax: 91 2692 240 208

Website: www.amul.com

Source: company website D A T A M O N I T O R

Gujarat Cooperative Milk Marketing Federation (GCMMF) is a dairy product co-operative engaged in the

marketing and distribution of dairy products, including milk powder, cheese, butter, ghee, ice cream and

baby milk. The company primarily operates in India, where it is headquartered in Anand, Gujarat.

GCMMF sells its products largely under the Amul brand name. It offers a range of fresh, UHT and low fat

milk products, as well as cheeses, flavored milk and yogurts under this name. The company also markets

a malt chocolate drink under the brand Nutramul.

The company's product lines include spreads, cheese, ethnic sweets, UHT milk, milk for infants, milk

powders, sweetened condensed milk, fresh milk, curd, ice creams, chocolate and confectionery, brown

beverages, milk drinks and health beverages.

The company offers spreads under the brands Amul Butter, Amul Lite and Delicious Table Margarine.

Its milk drinks portfolio consists of brands such as Amul Kool Millk Shaake, Amul Kool, Amul Kool Cafe,

Kool Koko, Nutramul energy drink, Amul Lassee, Amul Masti (spiced buttermilk), and Amul Kool Thandai.

GCMMF’s powder milk products comprises infant milk foods marketed under the Amul Spray Infant Milk

Food brand; full cream milk powder under the Amul Instant Full Cream Milk Powder brand; skimmed milk

powder and tea & coffee whitener under the brand Sagar; and dairy whitener under the brand Amulya.

Fresh milk with different pasteurizations are marketed under brands such as Amul Gold, Amul Fresh,

Amul Taaza (double toned milk), Amul Lite Slim and Trim Milk, Amul Fresh Cream, Amul Shakti (toned

milk), and Amul calci+ and Amul Buttermilk.

GCMMF markets pasteurized processed cheese under the brands Amul Pasteurised Processed Cheese,

Amul Cheese Spreads, Amul Emmental Cheese, Amul Pizza Mozzarella Cheese and Gouda Cheese.

LEADING COMPANIES

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 16

The company also offers desserts such as ice creams (Amul Ice Creams), traditional sweets (Amul

Shrikhand), chocolates (Amul Chocolates), and concentrated milk based products (Amul Basundi).

The company provides cooking products such as butter, pizza (Amul Utterly Delicious Pizza), sweetened

condensed milk (Amul Mithai Mate), and packed curd (Amul Masti Dahi). The company also offers health

drinks under the brands such as Nutramul and Amul Shakti.

The company markets its products through dairy and ice-cream distributors, as well as online website.

GCMMF also exports its products to the US, the Gulf countries and Singapore. In July 2009, GCMMF

announced plans to set up 6,000 Amul retail parlors across India during the period 2009-2010. The

company currently has a network of 4,000 outlets of which 2,000 were added during 2008-2009.

Key Metrics

As this company is privately held, financial information is not available.

LEADING COMPANIES

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 17

KCMMF (Kerala Cooperative Milk Marketing Federation)

Table 6: KCMMF (Kerala Cooperative Milk Marketing Federation): key facts

Head office: Milma Bhavan, Pattom Palace, Thiruvananthapuram, Kerala, IND

Telephone: 91 471 2555981

Fax: 91 471 2555992

Website: www.milma.com

Source: company website D A T A M O N I T O R

Kerala Co-operative Milk Marketing Federation (KCMMF) is engaged in the manufacturing and marketing

of milk and milk derivatives. Its product portfolio includes milk (fat free milk, toned milk, standardized milk

and pasteurized flavored skimmed milk); ice cream (available in a range of flavors: vanilla, chocolate,

mango, strawberry and fruit & nut); curd (butter milk, curd and sweetened curd); cattle feed; beverages

(flavored health drinks and mango drink); and sweets (cream roll).

These products are marketed under brands such as Milma milk, Milma ice-cream, Milma Sambharam

(butter milk), Milma Butter (butter), Milma Refresh (mango drink) and Milma Peda (sweets).

The company manufactures these products through 11 dairies, 13 milk chilling centers, two cattle feed

plants and one milk powder plant, and markets them through a chain of 5,200 retail outlets across Kerala.

Key Metrics

KCMMF generated revenues of $33.1 million in the financial year (FY) 2008-09, an increase of 14.6%

over FY2007-08. The company's net income totaled $3 million in FY2008-09.

LEADING COMPANIES

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 18

Mother Dairy Fruit & Vegetable Pvt. Ltd.

Table 7: Mother Dairy Fruit & Vegetable Pvt. Ltd.: key facts

Head office: NDDB House, Opposite Kamal Cinema Complex, Safdarjung Enclave, New Delhi-110029, IND

Telephone: 91 11 41 52 91 00

Fax: 91 11 41 52 71 70

Website: www.motherdairy.com

Source: company website D A T A M O N I T O R

Mother Dairy Fruits & Vegetables (Mother Dairy) is an India based dairy and vegetable company. Mother

Dairy is a wholly owned subsidiary of National Dairy Development Board of India. Mother Dairy is

headquartered in New Delhi, India.

Mother Dairy markets and sells dairy products, vegetables and oils under the brand names Mother Dairy,

Safal and Dhara, respectively. Its range of dairy products includes liquid milk, UHT milk, yogurt, ice

creams, yogurt based drinks, flavored milk, cheese, and butter. Milk varieties offered include full cream,

standardized, toned, double toned, skimmed, cow and bulk vended token milk. It markets around 2.8

million liters of milk daily and operates around 845 exclusive outlets and also through 14,000 retail outlets.

Fresh and frozen fruits and vegetables are marketed under the brand name Safal through a chain of more

than 400 fruit and vegetable shops; and 20,000 retail outlets. Edible oils are marketed under the brand

Dhara, which includes range of oils, such as refined vegetable oil, refined soybean oil, refined sunflower

oil, refined rice bran oil, kachi ghani mustard oil and filtered groundnut oil. Mother Dairy also offers extra

virgin olive oil under the brand name Daroliva.

Mother Dairy also exports fruit pulp, pastes, purees and concentrates around the world and with its

marketing office in Rotterdam, Netherlands.

Key Metrics

Financial information of the company is not available.

DISTRIBUTION

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 19

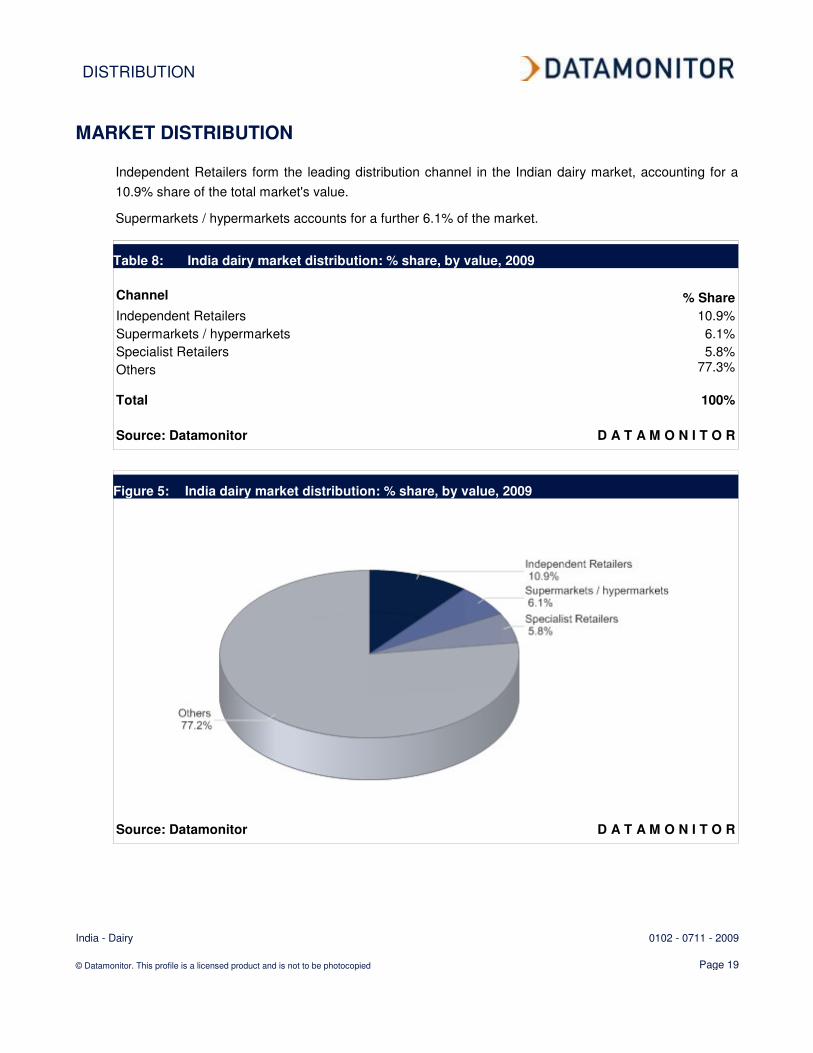

MARKET DISTRIBUTION

Independent Retailers form the leading distribution channel in the Indian dairy market, accounting for a

10.9% share of the total market's value.

Supermarkets / hypermarkets accounts for a further 6.1% of the market.

Table 8: India dairy market distribution: % share, by value, 2009

Channel % Share

Independent Retailers 10.9%

Supermarkets / hypermarkets 6.1%

Specialist Retailers 5.8%

Others 77.3%

Total 100%

Source: Datamonitor D A T A M O N I T O R

Figure 5: India dairy market distribution: % share, by value, 2009

Source: Datamonitor D A T A M O N I T O R

MARKET FORECASTS

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 20

MARKET FORECASTS

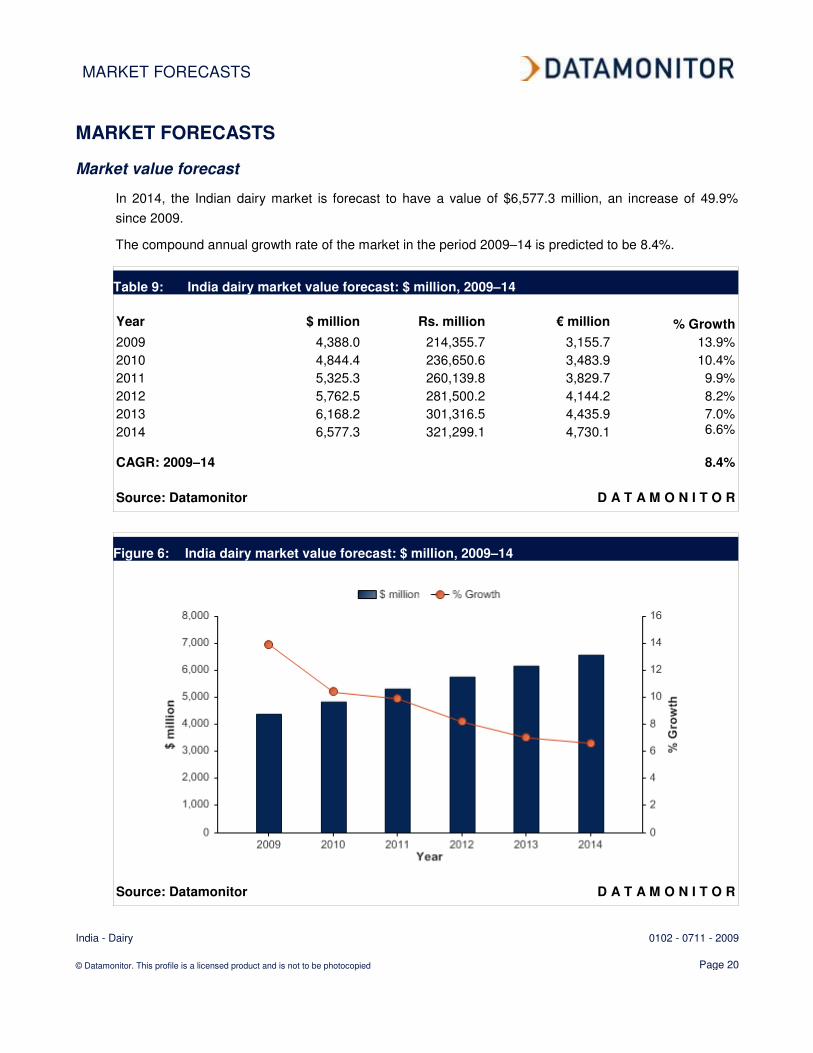

Market value forecast

In 2014, the Indian dairy market is forecast to have a value of $6,577.3 million, an increase of 49.9%

since 2009.

The compound annual growth rate of the market in the period 2009–14 is predicted to be 8.4%.

Table 9: India dairy market value forecast: $ million, 2009–14

Year $ million Rs. million € million % Growth

2009 4,388.0 214,355.7 3,155.7 13.9%

2010 4,844.4 236,650.6 3,483.9 10.4%

2011 5,325.3 260,139.8 3,829.7 9.9%

2012 5,762.5 281,500.2 4,144.2 8.2%

2013 6,168.2 301,316.5 4,435.9 7.0%

2014 6,577.3 321,299.1 4,730.1 6.6%

CAGR: 2009–14 8.4%

Source: Datamonitor D A T A M O N I T O R

Figure 6: India dairy market value forecast: $ million, 2009–14

Source: Datamonitor D A T A M O N I T O R

MACROECONOMIC INDICATORS

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 21

MACROECONOMIC INDICATORS

Table 10: India size of population (million), 2005–09

Year Population (million) % Growth

2005 1,091.0 1.6%

2006 1,107.6 1.5%

2007 1,124.1 1.5%

2008 1,140.6 1.5%

2009 1,156.9 1.4%

Source: Datamonitor D A T A M O N I T O R

Table 11: India gdp (constant 2000 prices, $ billion), 2005–09

Year Constant 2000 Prices, $ billion % Growth

2005 648.8 9.1%

2006 711.8 9.7%

2007 776.8 9.1%

2008 832.5 7.2%

2009 892.5 7.2%

Source: Datamonitor D A T A M O N I T O R

Table 12: India gdp (current prices, $ billion), 2005–09

Year Current Prices, $ billion % Growth

2005 764.4 15.7%

2006 872.7 14.2%

2007 1,127.4 29.2%

2008 1,244.6 10.4%

2009 1,403.0 12.7%

Source: Datamonitor D A T A M O N I T O R

MACROECONOMIC INDICATORS

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 22

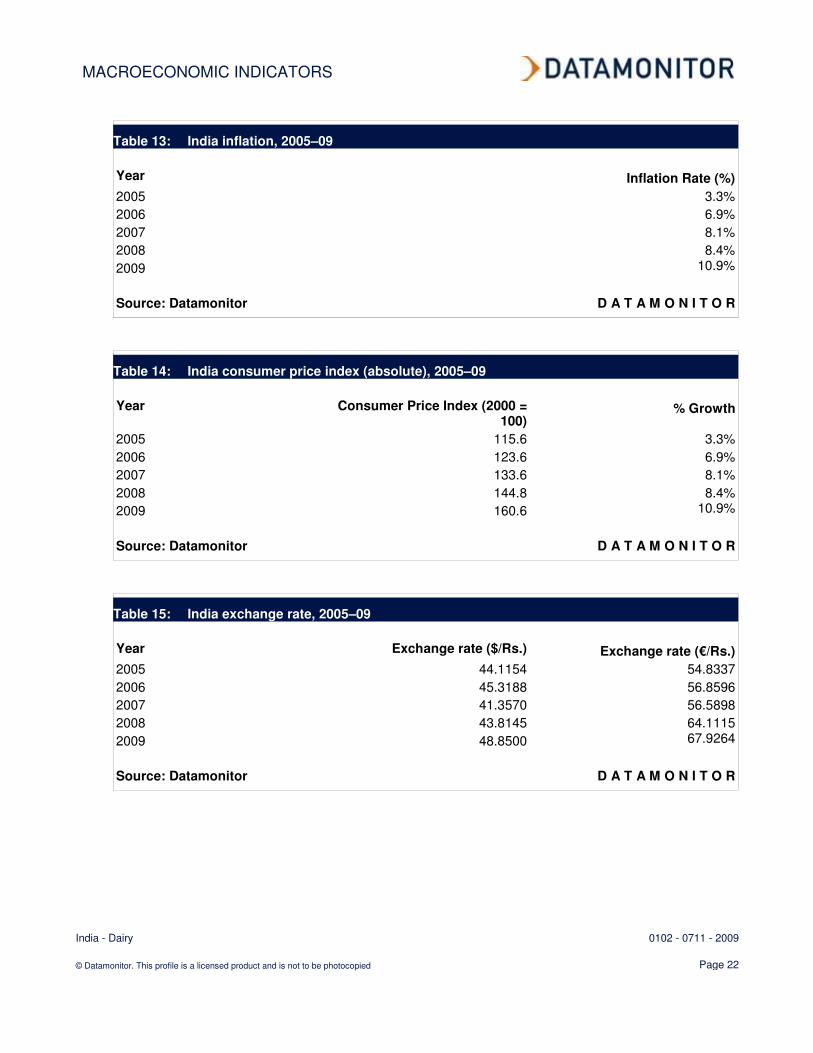

Table 13: India inflation, 2005–09

Year Inflation Rate (%)

2005 3.3%

2006 6.9%

2007 8.1%

2008 8.4%

2009 10.9%

Source: Datamonitor D A T A M O N I T O R

Table 14: India consumer price index (absolute), 2005–09

Year Consumer Price Index (2000 =

100) % Growth

2005 115.6 3.3%

2006 123.6 6.9%

2007 133.6 8.1%

2008 144.8 8.4%

2009 160.6 10.9%

Source: Datamonitor D A T A M O N I T O R

Table 15: India exchange rate, 2005–09

Year Exchange rate ($/Rs.) Exchange rate (€/Rs.)

2005 44.1154 54.8337

2006 45.3188 56.8596

2007 41.3570 56.5898

2008 43.8145 64.1115

2009 48.8500 67.9264

Source: Datamonitor D A T A M O N I T O R

APPENDIX

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 23

APPENDIX

Methodology

Datamonitor Industry Profiles draw on extensive primary and secondary research, all aggregated,

analyzed, cross-checked and presented in a consistent and accessible style.

Review of in-house databases – Created using 250,000+ industry interviews and consumer surveys

and supported by analysis from industry experts using highly complex modeling & forecasting tools,

Datamonitor’s in-house databases provide the foundation for all related industry profiles

Preparatory research – We also maintain extensive in-house databases of news, analyst

commentary, company profiles and macroeconomic & demographic information, which enable our

researchers to build an accurate market overview

Definitions – Market definitions are standardized to allow comparison from country to country. The

parameters of each definition are carefully reviewed at the start of the research process to ensure they

match the requirements of both the market and our clients

Extensive secondary research activities ensure we are always fully up-to-date with the latest

industry events and trends

Datamonitor aggregates and analyzes a number of secondary information sources, including:

- National/Governmental statistics

- International data (official international sources)

- National and International trade associations

- Broker and analyst reports

- Company Annual Reports

- Business information libraries and databases

Modeling & forecasting tools – Datamonitor has developed powerful tools that allow quantitative

and qualitative data to be combined with related macroeconomic and demographic drivers to create

market models and forecasts, which can then be refined according to specific competitive, regulatory

and demand-related factors

Continuous quality control ensures that our processes and profiles remain focused, accurate and

up-to-date

APPENDIX

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 24

Industry associations

Indian Dairy Association

IDA House, Sector-IV, R.K. Puram, New Delhi-110 022

Tel.: 91 11 2617 0781

Fax: 91 11 2617 4719

www.indairyasso.org

Related Datamonitor research

Industry profiles

Dairy in Europe

Dairy in Colombia

Dairy in Italy

Dairy in Denmark

Dairy in Ireland

Dairy in Mexico

Global Dairy

Dairy in the United Kingdom

Dairy in the Netherlands

Dairy in Venezuela

Dairy in the Czech Republic

Dairy in Sweden

Dairy in South Korea

Dairy in Japan

Dairy in Taiwan

Dairy in Norway

Dairy in Hungary

Dairy in Portugal

Dairy in Russia

Dairy in Peru

APPENDIX

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 25

Dairy in France

Dairy in Poland

Dairy in Spain

Dairy in the United States

Dairy in Germany

Dairy in Singapore

Dairy in Chile

Dairy in Brazil

Dairy in Australia

Dairy in China

Dairy in Belgium

Dairy in Asia-Pacific

Dairy in Canada

Dairy in South Africa

Dairy in Saudi Arabia

Dairy in Egypt

Dairy in Israel

Dairy in United Arab Emirates

Dairy in Switzerland

APPENDIX

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 26

Disclaimer

All Rights Reserved.

No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form

by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior

permission of the publisher, Datamonitor plc.

The facts of this report are believed to be correct at the time of publication but cannot be guaranteed.

Please note that the findings, conclusions and recommendations that Datamonitor delivers will be

based on information gathered in good faith from both primary and secondary sources, whose

accuracy we are not always in a position to guarantee. As such Datamonitor can accept no liability

whatever for actions taken based on any information that may subsequently prove to be incorrect.

ABOUT DATAMONITOR

India - Dairy 0102 - 0711 - 2009

© Datamonitor. This profile is a licensed product and is not to be photocopied Page 27

ABOUT DATAMONITOR

The Datamonitor Group is a world-leading provider of premium global business information, delivering

independent data, analysis and opinion across the Automotive, Consumer Markets, Energy & Utilities,

Financial Services, Logistics & Express, Pharmaceutical & Healthcare, Retail, Technology and

Telecoms industries.

Combining our industry knowledge and experience, we assist over 6,000 of the world’s leading

companies in making better strategic and operational decisions.

Delivered online via our user-friendly web platforms, our market intelligence products and services

ensure that you will achieve your desired commercial goals by giving you the insight you need to best

respond to your competitive environment.

Premium Reports

Datamonitor's premium reports are based on primary research with industry panels and consumers.

We gather information on market segmentation, market growth and pricing, competitors and products.

Our experts then interpret this data to produce detailed forecasts and actionable recommendations,

helping you create new business opportunities and ideas.

Summary Reports

Our series of company, industry and country profiles complements our premium products, providing

top-level information on 30,000 companies, 3,000 industries and 100 countries. While they do not

contain the highly detailed breakdowns found in premium reports, profiles give you the most important

qualitative and quantitative summary information you need - including predictions and forecasts.

Datamonitor consulting

We hope that the data and analysis in this profile will help you make informed and imaginative business

decisions. If you have further requirements, Datamonitor’s consulting team may be able to help you. For

more information about Datamonitor’s consulting capabilities, please contact us directly at

Copyright of Dairy Industry Profile: India is the property of Datamonitor Plc and its content may not be copied

or emailed to multiple sites or posted to a listserv without the copyright holder's express written permission.

However, users may print, download, or email articles for individual use.