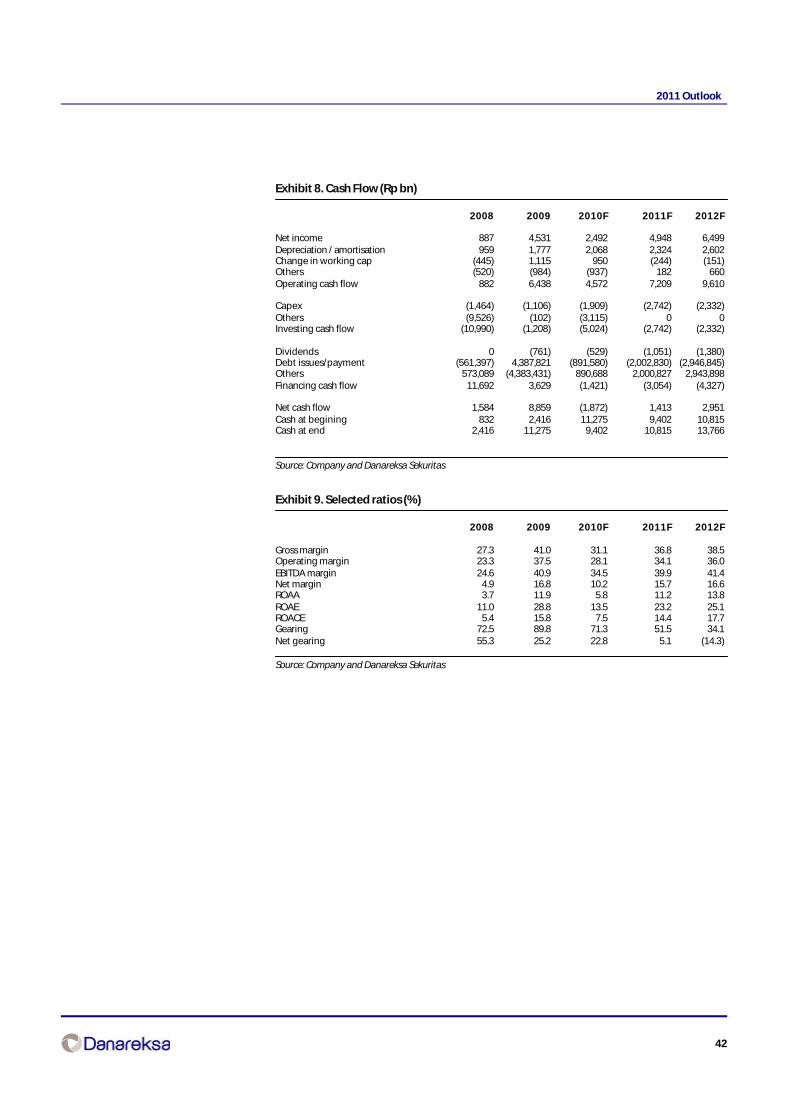

danareksa market outlook 2011

TRANSCRIPT

E Q U I T Y R E S E A R C H

www.danareksa.com See important disclosure on the back of this report

Market Outlook2011 roadmap

OVERWEIGHT

JCI Index 3,581YE11F target 4,100Mkt Cap Rp tn 3,123in US$bn 346

09 10E 11F

GDP growth, % 4.5 6.1 6.43mth Deposit, % 7.5 6.6 6.2Inflation MoM, % 2.8 6.3 6.0Inflation YoY, % 2.8 6.5 6.2Rp/US$ YE 9,400 9,071 9,304Rp/US$ average 10,356 9,099 9,214

Indonesia Economic Indicators

Equity Research TeamHead of Equity ResearchBonny B. Setiawan CFA(62-21) 2352 [email protected]

AnalystsChandra S. Pasaribu(62-21) 351 [email protected]

Lydia Suwandi(62-21) 350 9888 ext. [email protected]

Merlissa P.Trisno(62-21) 350 9888 ext. [email protected]

Peter P. Sutedja(62-21) 350 9888 ext. [email protected]

Indra P. Yudison(62-21) 350 9888 ext. [email protected]

Metty F. Wardhani(62-21) 350 9888 ext. [email protected]

Research AssistantsEdwin Sabam S/Vina Hosea(62-21) 350 9888 ext. 3505/[email protected]@danareksa.com

EditorMartin R. Jenkins(62-21 350 9888 ext. [email protected]

The market has shown strong performance in 2010, with the JCI up 41.3% YTD, at a 14.9x 12-mth forward PER, thanks to strong earnings growth amidst brisk economic expansion.Indeed, our economic cycle is still at an early phase of a 7-year cycle, meaning strong earningsgrowth to come. We now set our FY11E index target at 4,100, based on a bottom-up approach,implying 16.3x 2011 PER. Our conviction is supported by continuation of benign inflationand therefore record low interest rates, sustainable earnings growth of 24.8% and anupsurge in FDI-led investment growth. Our estimate of 2011 GDP growth remains at 6.4%,buoyed by robust investment aside from the higher consumption growth. Bank lending hasbeen supportive as well, with loans growth likely to reach 18.6% next year. Upside is froma potential upgrade in the sovereign rating and realization of infrastructure projects, whiledownside risks are potential global economic slowdown and a sudden upsurge in inflation.

22 December 2010

Cut off data December 17,2010

2

2011 Outlook

Recommendation Page

Market outlook OVERWEIGHT 3Automotive parts OVERWEIGHT 13Banking sector OVERWEIGHT 15Coal sector OVERWEIGHT 19Consumer sector NEUTRAL 23Plantation sector OVERWEIGHT 27Property sector OVERWEIGHT 31

Recommendation Target Price PageRp/share

ACE Hardware Indonesia HOLD 2,550 35Adaro Energy BUY 2,950 39AKR Corporindo SELL 1,340 43Alam Sutera Realty BUY 400 47Astra Agro Lestari HOLD 24,500 51Astra International HOLD 58,500 57Bakrie Telecom HOLD 240 61Bank Central Asia HOLD 7,000 65Bank Danamon BUY 8,050 69Bank Mandiri BUY 8,300 73Bank Negara Indonesia BUY 5,700 77Bank Rakyat Indonesia BUY 14,400 81Bayan Resources SELL 9,700 85Bukit Asam BUY 26,650 89Bumi Resources BUY 3,625 93Bumi Serpong Damai BUY 890 97BW Plantation BUY 1,350 101Ciputra Development BUY 450 107Gajah Tunggal BUY 3,125 111Gudang Garam BUY 55,000 115Holcim Indonesia BUY 3,170 119Indika Energy BUY 4,825 123Indo Tambangraya Megah HOLD 55,300 127Indocement Tunggal Prakarsa BUY 19,820 131Indofood CBP HOLD 5,500 135Indofood Sukses Makmur BUY 6,000 139Indosat SELL 6,400 143Jasa Marga BUY 4,300 147Kalbe Farma HOLD 3,500 151Lippo Karawaci BUY 1,272 155London Sumatera BUY 14,850 159Mayora Indah HOLD 13,000 165Mitra Adiperkasa HOLD 2,600 169Multistrada Arah Sarana BUY 530 173Perusahaan Gas Negara BUY 5,400 177Ramayana Lestari Sentosa BUY 1,120 181Sampoerna Agro BUY 3,700 185Selamat Sempurna BUY 1,500 191Semen Gresik BUY 10,875 195Sorini Asia Corporindo SELL 2,350 199Summarecon Agung HOLD 1,400 203Telkom Indonesia BUY 9,550 207Tempo Scan Pacific BUY 2,050 211Unilever Indonesia SELL 15,000 215United Tractors BUY 27,250 219XL Axiata BUY 7,500 223

Table of contents

3

2011 Outlook

Market Outlook2011 roadmap

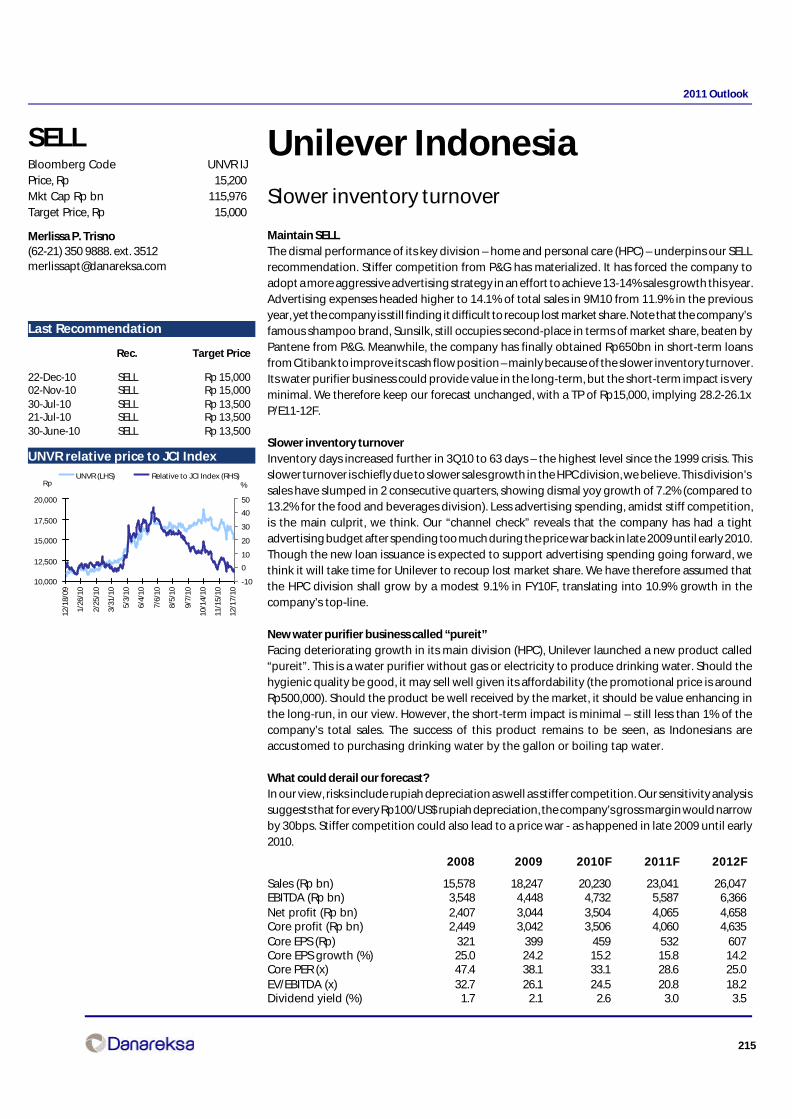

New index target set at 4,100The market has shown strong performance in 2010, with the JCI up 41.3% YTD, at a 14.9x 12-mthforward PER, thanks to strong earnings growth amidst brisk economic expansion. Indeed, oureconomic cycle is still at an early phase of a 7-year cycle, meaning strong earnings growth to come.We now set our FY11E index target at 4,100, based on a bottom-up approach, implying 16.3x 2011PER. Our conviction is supported by continuation of benign inflation and therefore record lowinterest rates, sustainable earnings growth of 24.8% and an upsurge in FDI-led investment growth.Our estimate of 2011 GDP growth remains at 6.4%, buoyed by robust investment aside from thehigher consumption growth. Bank lending has been supportive as well, with loans growth likelyto reach 18.6% next year. Upside is from a potential upgrade in the sovereign rating and realizationof infrastructure projects, while downside risks are potential global economic slowdown and asudden upsurge in inflation.

The macro outlook looks rosyWhile inflation carries a big risk to our economy, the recent years of economic expansion havetended to insulate consumers from rising costs. We estimate inflation to rise to 6.2% by YE11, nota big jump from the current year’s 6.0%, although we may see some upward pressure mid-year.The BI rate is likely to be kept at 6.5% - that’s assuming BI’s inflation-targeting policy still stands.Continuity in food supplies – specifically rice, is one of the big risks, we believe, given a lack ofinfrastructure. Yet market operations and the likelihood the government doesn’t obstruct importsmay ease demand-pull inflation. Concerns over the growing base money (M0), and thereforepotentially higher inflation, appear to be unfounded, as well. This is especially true given the briskrate of GDP growth. Besides, one needs to consider the unused government account in BIamounting to Rp169trn as of October.

So, what may derail our inflation forecast? Well, food supply issues aside, efforts to reduce theconsumption of subsidized fuel is a challenge. Only recently, the nation’s parliament approveda long-awaited measure curbing fuel subsidies. By the end of March next year, subsidized fuel shallonly be available for public transport vehicles and motorcycles. As a result, inflation is likely toincrease by 0.3%, not much, we think; although that’s assuming that only private cars are prohibitedfrom using subsidized fuel.

Investment driven growthThe key theme for economic expansion remains investment growth and government spending.So far, FDI has increased by 27.5% YoY to about US$11.9bn and by 43.6% for domestic investment.Despite the economic expansion, production utilization is relatively unchanged, which in a waysuggests that demand has kept pace with the investment growth. What remains a bottleneck toour economy is realization of infrastructure projects, although around US$47bn are expected tobe tendered over the next 5 years. Next year, investment growth should reach a strong 12.9% -after a good start this year. Much will hinge on the ability of banks to lend aggressively. Thus far,lending has been robust, and as the economy continues to expand, loans growth is expected tostay above 15% p.a.

OVERWEIGHT

JCI Index 3581YE11 target 4,100Mkt Cap Rp tn 3,123in US$mn 346

09 10E 11FGDP growth, % 4.5 6.1 6.43mth Deposit, % 7.5 6.6 6.2Inflation MoM, % 2.8 6.3 6.0Inflation YoY, % 2.8 6.5 6.2Rp/US$ YE 9,400 9,071 9,304Rp/US$ average 10,356 9,099 9,214

Economic Indicators

4

2011 Outlook

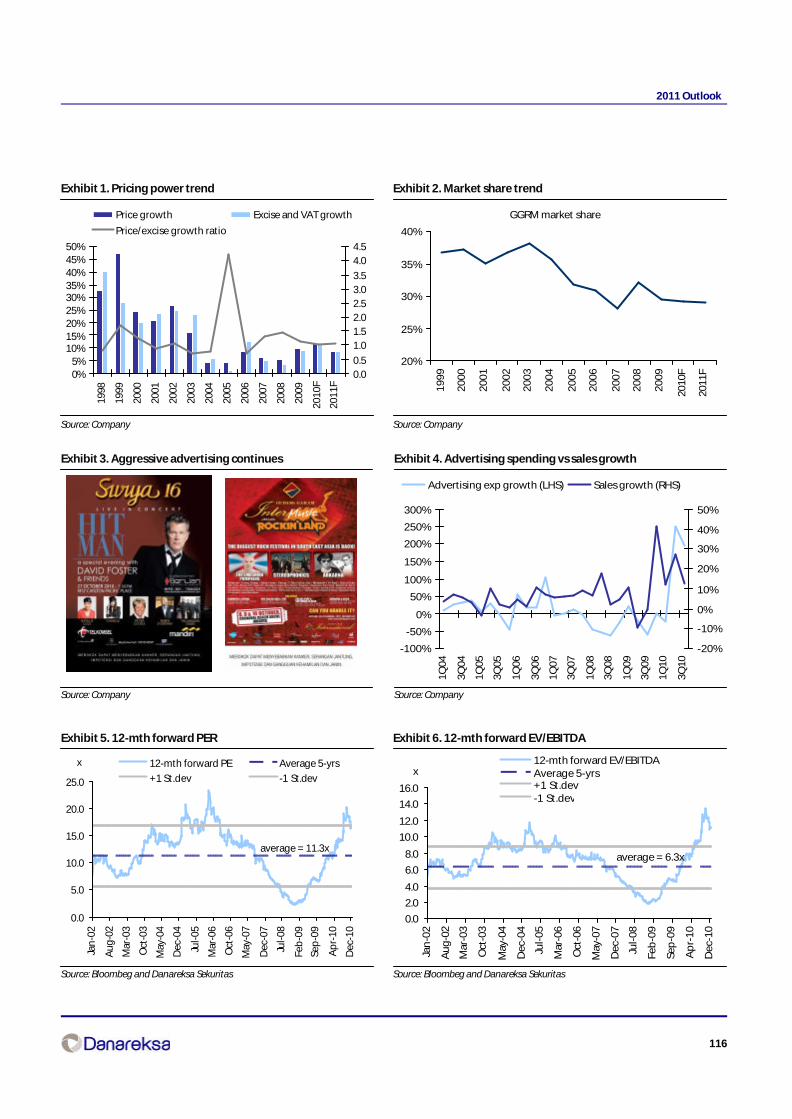

Cyclical stocks likely to outperformEarnings growth shall stay firm next year, reaching 25.1% on a yearly basis. Cyclical stocksexposed to commodities shall drive earnings expansion, although we also remain upbeaton the prospects for property stocks – which stand to book strong revenues thanks torobust marketing sales this year, aside from sustained bank lending. In regard tocommodity stocks, supply constraints on the back of harsh weather may drive commodityprices further up, helped by strong demand from China and India. The plantation sectorshall see earnings expand by 46.9% next year, while the mining sector’s earnings are forecastto grow by 34.6%. On that note, our top picks include ADRO, UNTR, LSIP and BWPT. Yet thestrength of the economy remains domestic consumption. And buoyed by the early phaseof economic expansion, INDF and GGRM are two major beneficiaries. Other stocks exposedto domestic consumption that we like are BBRI, INTP, JSMR and ASRI. Among the smallerstocks, we like MASA.

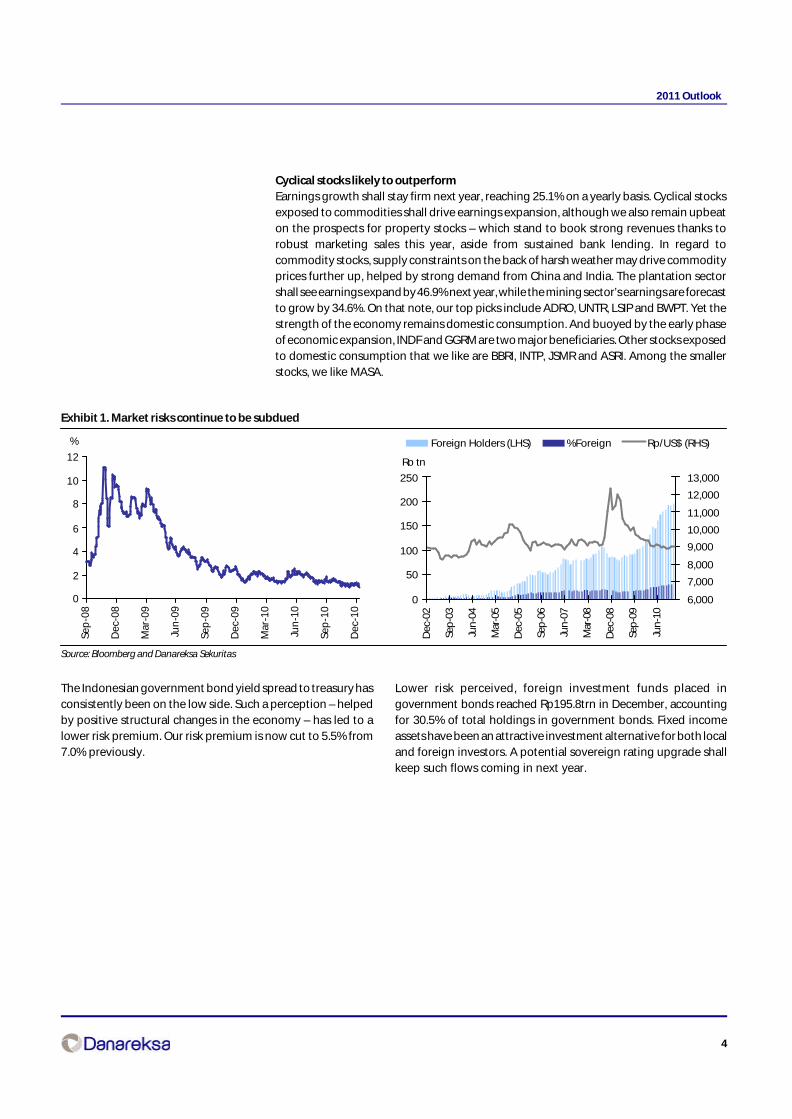

Exhibit 1. Market risks continue to be subdued

Source: Bloomberg and Danareksa Sekuritas

0

2

4

6

8

10

12

Sep

-08

Dec

-08

Mar

-09

Jun

-09

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

%

0

50

100

150

200

250

Dec

-02

Sep

-03

Jun

-04

Mar

-05

Dec

-05

Sep

-06

Jun

-07

Mar

-08

Dec

-08

Sep

-09

Jun

-10

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

Foreign Holders (LHS) %Foreign Rp/US$ (RHS)

Rp tn

The Indonesian government bond yield spread to treasury hasconsistently been on the low side. Such a perception – helpedby positive structural changes in the economy – has led to alower risk premium. Our risk premium is now cut to 5.5% from7.0% previously.

Lower risk perceived, foreign investment funds placed ingovernment bonds reached Rp195.8trn in December, accountingfor 30.5% of total holdings in government bonds. Fixed incomeassets have been an attractive investment alternative for both localand foreign investors. A potential sovereign rating upgrade shallkeep such flows coming in next year.

5

2011 Outlook

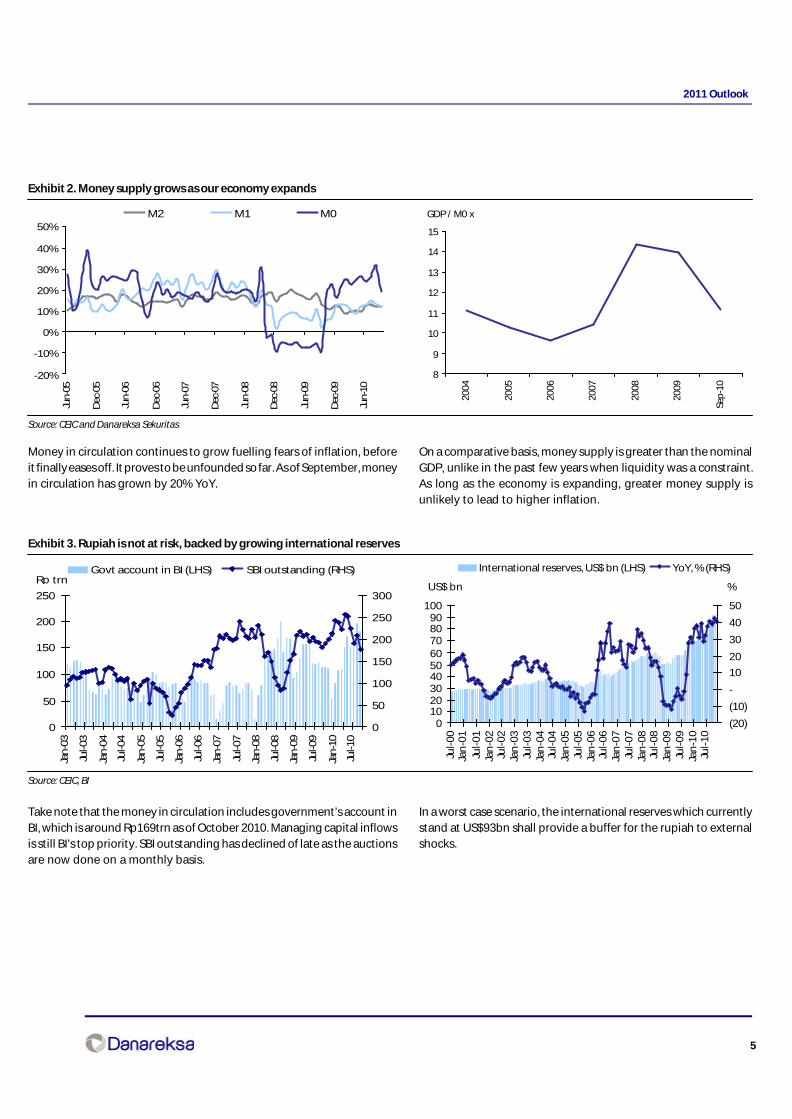

Exhibit 2. Money supply grows as our economy expands

Source: CEIC and Danareksa Sekuritas

Money in circulation continues to grow fuelling fears of inflation, beforeit finally eases off. It proves to be unfounded so far. As of September, moneyin circulation has grown by 20% YoY.

On a comparative basis, money supply is greater than the nominalGDP, unlike in the past few years when liquidity was a constraint.As long as the economy is expanding, greater money supply isunlikely to lead to higher inflation.

Exhibit 3. Rupiah is not at risk, backed by growing international reserves

Source: CEIC, BI

Take note that the money in circulation includes government’s account inBI, which is around Rp169trn as of October 2010. Managing capital inflowsis still BI’s top priority. SBI outstanding has declined of late as the auctionsare now done on a monthly basis.

In a worst case scenario, the international reserves which currentlystand at US$93bn shall provide a buffer for the rupiah to externalshocks.

-20%

-10%

0%

10%

20%

30%

40%

50%

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

M2 M1 M0

8

9

10

11

12

13

14

15

2004

2005

2006

2007

2008

2009

Sep

-10

GDP / M0 x

0

50

100

150

200

250

Jan

-03

Jul-0

3

Jan

-04

Jul-0

4

Jan

-05

Jul-0

5

Jan

-06

Jul-0

6

Jan

-07

Jul-0

7

Jan

-08

Jul-0

8

Jan

-09

Jul-0

9

Jan

-10

Jul-1

0

0

50

100

150

200

250

300

Govt account in BI (LHS) SBI outstanding (RHS)Rp trn

0102030405060708090

100

Jul-

00

Jan

-01

Jul-

01

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

(20)

(10)

-

10

20

30

40

50

International reserves, US$ bn (LHS) YoY, % (RHS)

US$ bn %

6

2011 Outlook

Exhibit 4. Economy growth remains firm

Source: CEIC and Danareksa Research Institute

Our GDP growth forecasts are 6.0% and 6.4%, respectively, forFY10-11. 3Q10’s GDP growth of 5.8% is the sixth straightquarterly increase, with consumption growing at 5.2%, a slightimprovement from 2Q10’s 5.0%. We expect consumption tostay firm next year, posting 5.0% growth by YE11. By 2014, SBYtargets 7.0-7.7% GDP growth..

October’s exports jumped 16.7% MoM to US$14.22bn, largely drivenby oil & gas related items. On a YoY basis, Jan-Oct exports rose by35.5%. The largest export growth for non oil and gas related itemscame from rubber, +95% YoY, and mining, +33% YoY, whileagricultural exports only grew 34% YoY. As of October, the tradebalance was a surplus of US$13.5bn.

Exhibit 5. Investment realization has picked up

Source: Investment Cordinating Board

The strength of the economy relies on investment growth. FDIreached US$11.9bn in 9M10, up 27.5% YoY, far exceeding thepre-crisis level. What remains a bottleneck is realization ofinfrastructure projects, with around US$47bn to be tenderedover the next 5 years.

Meanwhile, domestic investment realization was more than Rp40.4trnin 9M10 or +43.6% YoY. It has reached an historic high.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Mar

-02

Sep

-02

Mar

-03

Sep

-03

Mar

-04

Sep

-04

Mar

-05

Sep

-05

Mar

-06

Sep

-06

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

-5.0

0.0

5.0

10.0

15.0

20.0

GDP (LHS) Private (RHS) Investment (RHS)

% %

-5,000

10,000

15,000

20,00025,000

30,000

35,00040,000

45,000

Mar

-08

Jun

-08

Sep

-08

Dec

-08

Mar

-09

Jun

-09

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

-1,0002,000

3,000

4,0005,000

6,000

7,0008,000

9,000

Imports Export Trade balanceUS$ mn US$ mn

Source: BPS

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

9M10

-100%

-50%

0%

50%

100%

150%

200%

250%

Foreign investment, US$ bn (LHS) YoY growth, % (RHS)

Rp trn

0.05.0

10.015.020.025.0

30.035.040.045.0

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

9M10

-80%-60%-40%-20%0%20%40%60%80%100%120%

Domestic investment, Rp trn (LHS) YoY growth, % (RHS)

Rp trn

7

2011 Outlook

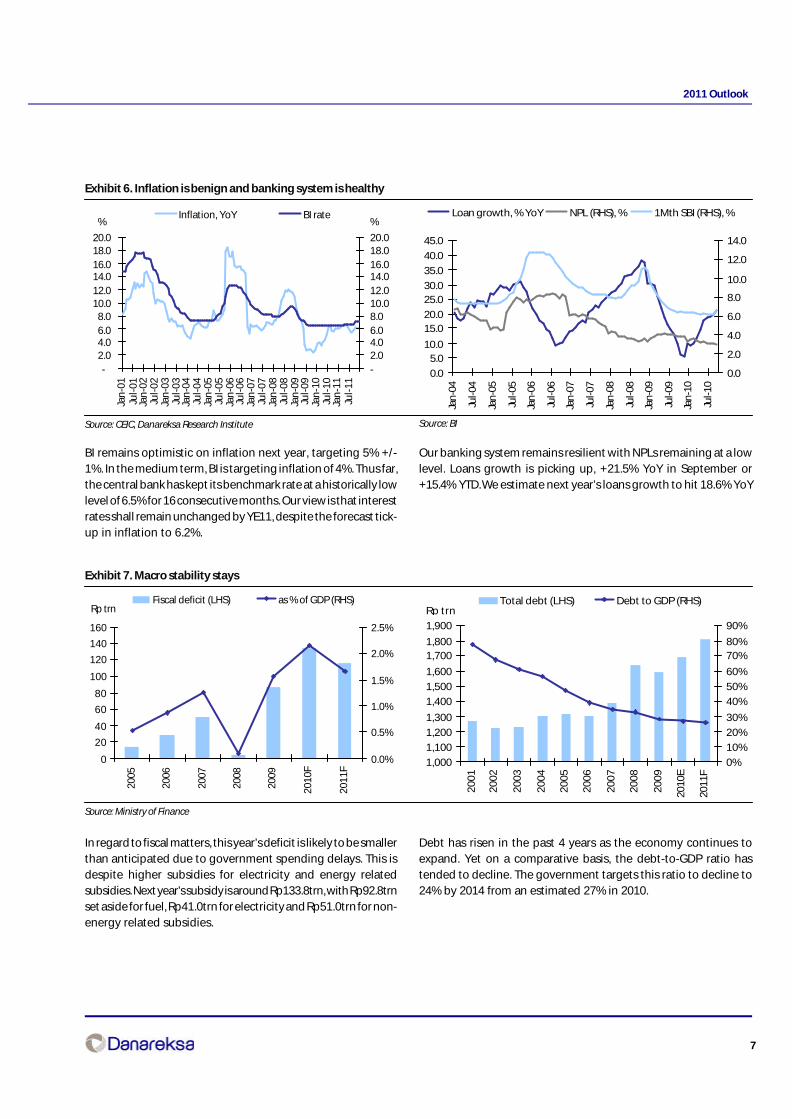

Exhibit 6. Inflation is benign and banking system is healthy

Source: CEIC, Danareksa Research Institute

BI remains optimistic on inflation next year, targeting 5% +/-1%. In the medium term, BI is targeting inflation of 4%. Thus far,the central bank has kept its benchmark rate at a historically lowlevel of 6.5% for 16 consecutive months. Our view is that interestrates shall remain unchanged by YE11, despite the forecast tick-up in inflation to 6.2%.

Our banking system remains resilient with NPLs remaining at a lowlevel. Loans growth is picking up, +21.5% YoY in September or+15.4% YTD. We estimate next year’s loans growth to hit 18.6% YoY

Exhibit 7. Macro stability stays

Source: Ministry of Finance

In regard to fiscal matters, this year’s deficit is likely to be smallerthan anticipated due to government spending delays. This isdespite higher subsidies for electricity and energy relatedsubsidies. Next year’s subsidy is around Rp133.8trn, with Rp92.8trnset aside for fuel, Rp41.0trn for electricity and Rp51.0trn for non-energy related subsidies.

Debt has risen in the past 4 years as the economy continues toexpand. Yet on a comparative basis, the debt-to-GDP ratio hastended to decline. The government targets this ratio to decline to24% by 2014 from an estimated 27% in 2010.

Source: BI

-2.04.06.08.0

10.012.014.016.018.020.0

Jan

-01

Jul-

01Ja

n-0

2Ju

l-02

Jan

-03

Jul-

03Ja

n-0

4Ju

l-04

Jan

-05

Jul-

05Ja

n-0

6Ju

l-06

Jan

-07

Jul-

07Ja

n-0

8Ju

l-08

Jan

-09

Jul-

09Ja

n-1

0Ju

l-10

Jan

-11

Jul-

11

-2.04.06.08.010.012.014.016.018.020.0

Inflation, YoY BI rate% %

0.0

5.010.0

15.020.0

25.030.0

35.0

40.0

45.0

Jan

-04

Jul-0

4

Jan

-05

Jul-0

5

Jan

-06

Jul-0

6

Jan

-07

Jul-0

7

Jan

-08

Jul-0

8

Jan

-09

Jul-0

9

Jan

-10

Jul-1

0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Loan growth, % YoY NPL (RHS), % 1Mth SBI (RHS), %

0

20

40

60

80

100

120

140

160

2005

2006

2007

2008

2009

2010

F

2011

F

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Fiscal deficit (LHS) as % of GDP (RHS)Rp trn

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,7001,800

1,900

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

2010

E

2011

F

0%

10%

20%

30%

40%

50%

60%

70%80%

90%

Total debt (LHS) Debt to GDP (RHS)Rp trn

8

2011 Outlook

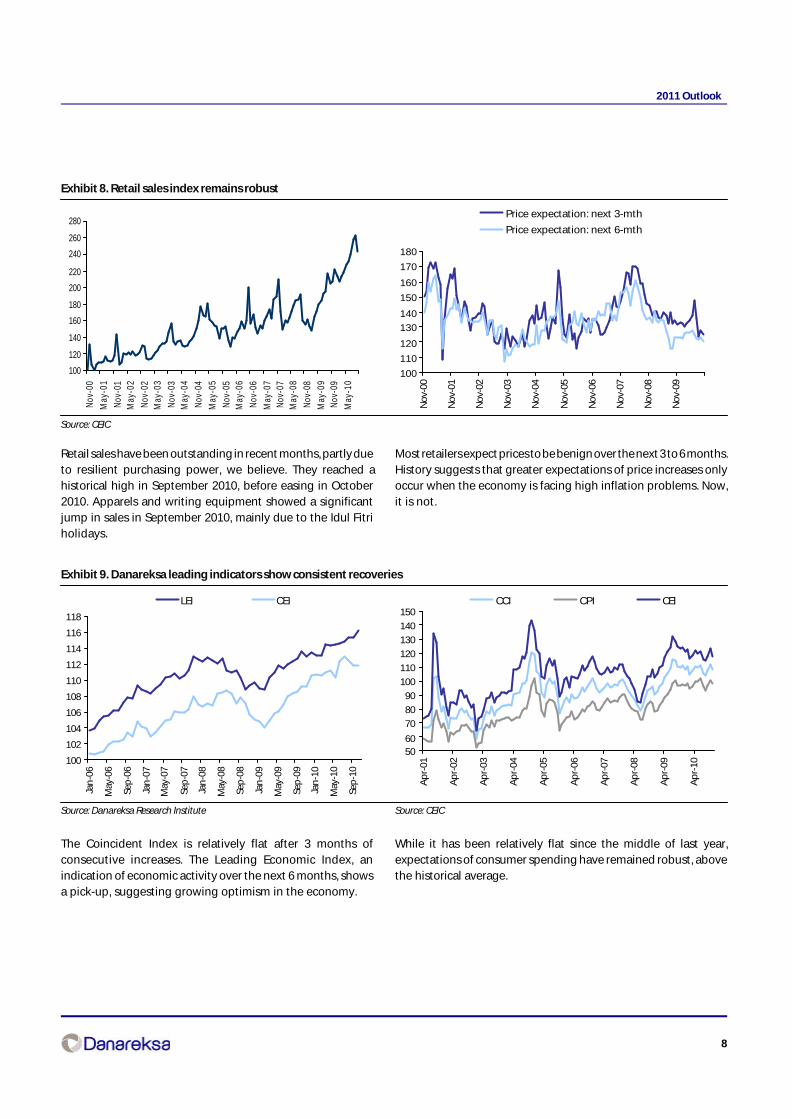

Exhibit 8. Retail sales index remains robust

Source: CEIC

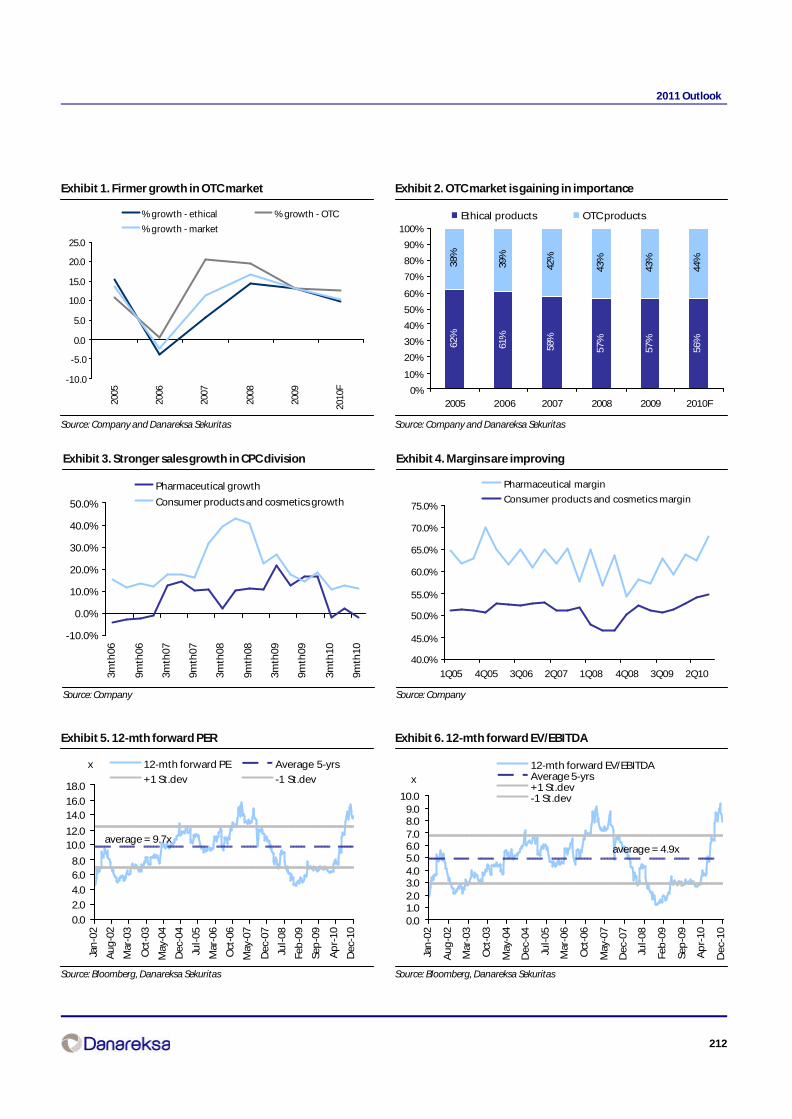

Retail sales have been outstanding in recent months, partly dueto resilient purchasing power, we believe. They reached ahistorical high in September 2010, before easing in October2010. Apparels and writing equipment showed a significantjump in sales in September 2010, mainly due to the Idul Fitriholidays.

Most retailers expect prices to be benign over the next 3 to 6 months.History suggests that greater expectations of price increases onlyoccur when the economy is facing high inflation problems. Now,it is not.

100

110

120

130

140

150

160

170

180

No

v-00

No

v-01

No

v-02

No

v-03

No

v-04

No

v-05

No

v-06

No

v-07

No

v-08

No

v-09

Price expectation: next 3-mth

Price expectation: next 6-mth

100

120

140

160

180

200

220

240

260

280

Nov-

00M

ay-0

1No

v-01

May

-02

Nov-

02M

ay-0

3No

v-03

May

-04

Nov-

04M

ay-0

5No

v-05

May

-06

Nov-

06M

ay-0

7No

v-07

May

-08

Nov-

08M

ay-0

9No

v-09

May

-10

Exhibit 9. Danareksa leading indicators show consistent recoveries

Source: Danareksa Research Institute

The Coincident Index is relatively flat after 3 months ofconsecutive increases. The Leading Economic Index, anindication of economic activity over the next 6 months, showsa pick-up, suggesting growing optimism in the economy.

While it has been relatively flat since the middle of last year,expectations of consumer spending have remained robust, abovethe historical average.

100

102

104

106

108

110

112

114

116

118

Jan

-06

May

-06

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

LEI CEI

Source: CEIC

5060

70

80

90

100

110

120

130

140

150

Ap

r-01

Ap

r-02

Ap

r-03

Ap

r-04

Ap

r-05

Ap

r-06

Ap

r-07

Ap

r-08

Ap

r-09

Ap

r-10

CCI CPI CEI

9

2011 Outlook

Exhibit 10. Risks: higher inflation and fuel prices

Source: BPS

November’s inflation was 0.60%, mainly contributed by higher processedfood prices. It contributed 63% of total inflation, which rose by 0.38%in October. On a YoY basis, inflation is 5.98%. Core inflation is 4.31%YoY or 3.89% YTD.

The restrictions on the use of subsidized fuel, starting next year, areunlikely to have a significant impact on inflation – around 0.3%,according to our estimates. Note that for every 10% increase in fuelprices, the impact on inflation is 0.7%

Exhibit 11. Corporate profitability

Source: Bloomberg and Danareksa Sekuritas

2007 core earnings growth was driven by resources. Since 2008,consumers and banks have taken the lead. The 19.2% YoY coreearnings growth forecast for 2010 bodes well for a good year.Resources and cyclical stocks shall see faster growth than other stocksnext year. We estimate 25.1% YoY earnings growth next year.

The ROE will continue to be robust at 25%, while the capex to salesratio is estimated to reach 12%. The fact that companies areinvesting more suggests corporate optimism toward future growth.Revenues are estimated to pick up next year amidst economicrecovery.

Source: Danareksa Research Institute

100105110115120125130135140145150

Jan

-09

Mar

-09

May

-09

Jul-0

9

Sep

-09

No

v-09

Jan

-10

Mar

-10

May

-10

Jul-1

0

Sep

-10

No

v-10

CPI FoodF&B, Tobacco Housing, Electricity, FuelClothing HealthEducation Transportation

0

50

100

150

200

250

2005 2006 2007 2008 2009 2010F 2011F

0%

1%

1%2%

2%

3%3%

4%4%

5%

5%

Fuel subsidy (LHS) as % of GDP (RHS)Rp trn

-50%

0%

50%

100%

150%

200%

2007 2008 2009 2010F 2011F

0%

10%

20%

30%

40%

50%

60%

70%

Banks Cyclical Consumer

Resources Total

Source: Danareksa Sekuritas

0%

5%

10%

15%

20%

25%

30%

2007 2008 2009 2010F 2011F

ROAE Capex to sales Revenue growth

10

2011 Outlook

Exhibit 12. Trading values

Source: IDX and Danareksa Sekuritas

The JCI has risen by 1,000 points from its low in February 2010.Daily trading remains high, averaging around Rp4.5trn per day,or about US$502mn. Trading activities are dominated by localsrather than foreign players.

Foreign players were net sellers of Rp2.5trn or around US$280mnin November 2010. Yet from Jan-Nov 10, foreign players were netbuyers of around US$2.1bn, with the largest net inflow in September2010.

Exhibit 13. JCI valuation – index target is 4,100

Source: Danareksa Sekuritas and IDX (Closing price as of Dec 16, 2010)

The market PE has re-rated over the past 1 year and is arguablylikely to continue re-rating - albeit more slowly - given greaterearnings visibility and potential upside from earnings revisions.

868.

4 1,98

9.8

(2,6

56.3

)1,

460.

0 3,79

3.6

(444

.6)

(895

.4)

467.

22,

694.

44,

140.

16,

461.

182

4.4

(1,1

60.2

)(5

61.5

)1,

815.

32,

602.

01,

973.

874

6.5

3,08

9.8

1,34

4.7

92

4.9

(3,1

18.1

)1,

793.

9 3,83

9.4

832.

7(2

,007

.9)

4,92

2.0

1,52

4.1

4,81

1.1

2,03

0.3

5,91

6.6

322.

2(2

,514

.9)

4,49

6.6

(1,6

52.0

)

-7,000

-5,000

-3,000

-1,000

1,000

3,000

5,000

7,000

Jan

-08

Ap

r-08

Jul-0

8

Oct

-08

Jan

-09

Ap

r-09

Jul-0

9

Oct

-09

Jan

-10

Ap

r-10

Jul-1

0

Oct

-10

Rp bn

0.02.04.06.08.0

10.012.014.016.0

Jan

-10

Feb

-10

Mar

-10

Ap

r-10

May

-10

Jun

-10

Jul-

10

Au

g-1

0Se

p-1

0O

ct-1

0N

ov-

101

-Dec

-10

2-D

ec-1

03

-Dec

-10

6-D

ec-1

08

-Dec

-10

9-D

ec-1

010

-Dec

-10

13-D

ec-1

014

-Dec

-10

15-D

ec-1

016

-Dec

-10

2,5002,7002,9003,1003,3003,5003,7003,900

Average Daily transaction (LHS) Foreign transaction (LHS)

Domestic Transaction (LHS) JCI Index (RHS)Rp trn

-

5

10

15

20

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

P/E Forward +2st.dev +1st.dev

Mean -1st.dev -2st.dev

x

14.9

7.0

18.9

The mining and agriculture sectors have underperformed so far.The banking and consumer sectors outperformed. Our view ofstrong global demand suggests that resources and agriculturestocks will continue to do well over the next 6 months.

Change in %16-Dec-10 1 Week 1 Month 3 Months 1 Year Ytd

Trade 457 (0.3) 9.9 25.1 70.6 65.7Consumer 1,045 (8.3) (9.8) (4.3) 59.6 55.6Finance 464 (7.6) (3.4) 6.7 56.6 54.0Misc. Industry 899 (7.6) (7.8) (6.8) 50.1 49.4JCI Index 3,572 (5.7) (2.9) 5.5 42.3 40.9Basic Industry 385 (4.5) (3.1) (2.3) 43.2 40.5Property 202 (1.8) 0.5 9.8 40.3 37.9Mining 3,005 (4.4) (0.2) 20.4 39.6 36.4Agriculture 2,153 (3.1) (8.2) 15.1 20.6 22.8Infrastructure 796 (4.3) (3.5) (0.8) 6.9 9.3

11

2011 Outlook

Exhibit 14. Stock pick bottom up

TP, Rp Potential Market cap EPS growth, % PER,x EV/EBITDA,x PBV,x Div Yield, %upside, % Rp bn 2010F 2011F 2010F 2011F 2010F 2011F 2010F 2011F 2010F 2011F

ADRO 2,950 15.7 81,564 -45 99 32.7 16.5 10.2 6.6 4.2 3.5 0.6 1.3ASRI 400 31.1 5,448 157 63 22.2 13.6 15.2 8.7 2.5 2.2 0.9 1.5BBRI 14,400 34.0 131,332 21 32 15.9 12.1 7.3 6.4 4.3 3.5 2.2 2.9BWPT 1,350 18.4 4,602 3 67 22.0 13.2 13.8 7.5 4.2 3.3 0.5 0.8GGRM 55,000 33.3 79,369 23 21 19.1 15.8 12.4 10.2 3.8 3.3 0.0 0.0INDF 6,000 29.0 40,829 24 13 15.9 14 8.2 7.5 1.7 1.5 2.0 2.5INTP 19,820 23.8 58,716 17 17 18.5 15.7 11.4 9.5 4.6 3.9 1.9 2.2JSMR 4,300 25.5 23,290 21 31 19.6 15.0 12.9 12.6 2.7 2.3 0.0 0.0LSIP 14,850 23.8 16,375 20 45 19.6 13.5 11.9 8.5 3.8 3.1 1.7 2.0MASA 450 34.3 2,051 2 34 11.4 8.5 7.8 6.7 1.2 1.1 0.3 0.0UNTR 27,250 13.8 79,679 -6 24 22.3 18.0 10.3 7.9 5.0 4.2 1.9 1.9

Source: Bloomberg (closing price as of Dec 15, 2010) and Danareksa Sekuritas

Our top picks, taking into consideration the momentum of higher commodity prices, include ADRO, UNTR, LSIP and BWPT. Meanwhile, we alsolike INDF and GGRM given their exposure to domestic consumption. Other stocks we like are BBRI, INTP, JSMR and ASRI. Among the smaller stocks,we like MASA.

12

2011 Outlook

Sector Outlook(In Alphabetical order)

13

2011 Outlook

Automotive partsRide on growth

BUY MASA and SMSMThe automotive parts sector has good prospects. Currently the sector’s valuation is still attractivewith 11F-12F Core PER of 8.3x-7.3x. Sales growth prospects are bright. Our top picks in the sectorare MASA and SMSM. Our BUY recommendation on MASA is underpinned by its strong revenuesgrowth prospects (37% CAGR over the next 2 years, in our estimate), supported by its rapidexpansion and higher orders. For SMSM, our BUY recommendation is underpinned by ourconfidence in the sustainability of the company’s revenues growth going forward, its attractive09-11F ROE of 25%-30% and its generous dividend payout policy.

Revenues should grow by 17% in 2011We expect the automotive parts sector core profits to grow by 17% in 2011. Domestically, demandgrowth should be driven by the increase in the number of new cars and motorcycles (around 7%p.a. and 14% p.a. respectively in the past two years in our estimate). Whilst in the exports market,Indonesia’s cost efficient manufacturing should allow the Indonesian companies to adoptcompetitive pricing to win more market share. For tire producers specifically, the additional USimport duties on Chinese tires (35%-30%-25% in the first-second-third years from September 2009)should mean that Indonesian tires are more competitive than before.

Capacity will increase to support demand growthTo be able to capture the growing demand, GJTL and MASA are now expanding their radial tiresand motorcycle tires production capacity. In percentage terms, MASA’s expansion is moreaggressive. MASA targets production capacity of radial tires and motorcycle tires to increase to28,500 tires/day and 16,000 tires/day respectively in early 2011 or around 63% and 100% higherthan the capacity in 9M10. GJTL meanwhile targets production capacity to increase to 45,000 radialtires/day and 105,000 motorcycle tires/day in 2012 or around 22% and 52% higher than the capacityin 9M10. As for the filter and radiator manufacturer, SMSM, it still has excess production capacityto accommodate further growth in 2011.

Key risks: rubber price and exchange ratesRubber price fluctuations are a primary risk for the tire producers (MASA and GJTL), as rubber(natural and synthetic) accounts for around 44% of the tires production cost. However, when therubber prices spike, most of the other tire producers also see their gross margins come underpressure, encouraging them to raise selling prices. Hence, a rapid increase in natural rubber pricesshould only result in temporary margins compression. As for the automotive filter and radiatormanufacturer, SMSM, exchange rate fluctuations are the primary risk, as around 75% of its revenuesare in foreign currency, while only 44% of its production costs are in foreign currency.

Indra P. Yudison(62-21) 350 9888 ext. [email protected]

OVERWEIGHT

Rec Price TPRp Rp

MASA BUY 325 450GJTL BUY 2,200 3,125SMSM BUY 1,060 1,500

Price Mkt cap Core PER,x PBV,X Core Profit ROAE,%Rp Rpbn growth, %

11F 12F 11F 12F 11F 12F 11F

MASA 325 1,990 8.1 5.8 1.1 0.9 42.6 39.8 13.6GJTL 2,200 7,667 8.3 7.7 1.8 1.4 15.4 8.0 23.8SMSM 1,060 1,526 9.1 8.0 2.4 2.0 10.6 13.1 29.0

Cut off data December 16,2010

14

2011 Outlook

Exhibit 1. Forward 12 months earnings yield

Source: Companies, Danaraksa estimates and Bloomberg

Exhibit 2. Forward 12 months EV/EBITDA

Source: Companies, Danaraksa estimates and Bloomberg

Exhibit 3. Forward 12 months PBV

Source: Companies, Danaraksa estimates and Bloomberg

Exhibit 4. Core ROAE

Source: Companies, Danareksa estimates

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

6/9/

2005

12/9

/200

5

6/9/

2006

12/9

/200

6

6/9/

2007

12/9

/200

7

6/9/

2008

12/9

/200

8

6/9/

2009

12/9

/200

9

6/9/

2010

12/9

/201

0

Forward 12 Months Earnings Yield Average

-1.02.03.04.05.06.07.08.09.0

10.0

6/9/

2005

12

/9/2

00

5

6/9/

2006

12

/9/2

00

6

6/9/

2007

12

/9/2

00

7

6/9/

2008

12

/9/2

00

8

6/9/

2009

12

/9/2

00

9

6/9/

2010

12

/9/2

01

0

Forward 12 EV/EBITDA Average

-

0.5

1.0

1.5

2.0

2.5

6/9/

2005

12/9

/200

5

6/9/

2006

12/9

/200

6

6/9/

2007

12/9

/200

7

6/9/

2008

12/9

/200

8

6/9/

2009

12/9

/200

9

6/9/

2010

12/9

/201

0

Forward 12 months PBV Average

0%

5%

10%

15%

20%

25%

30%

35%

2008 2009 2010F 2011F 2012F

Total MASA GJTL SMSM

15

2011 Outlook

Banking sectorMoving to a higher valuation matrixRaising TPs; top picks BBNI and BBRIWe raise our TPs for all banks under our coverage, using a lower equity risk premium of 5.5%, a likelysustainable figure over the medium term, we believe. Indeed, the yield on Indonesian 10-year bondshas dropped to an historic low of 7.4%, while the spread on US 10-year Treasury bonds has declinedto an historic low of 1.2%. With banks having strong fundamentals, our valuations for banks are liftedto a higher multiple of 4.0x 12-month forward PBV. Earnings have grown by 26.5% so far this year andare likely to be sustained at 26.2% next year, helped by 18.6% loans growth and in some cases, bad debtrecovery. ROE stays at a solid 24.8%, and the NIM is firm at 5.8%. NPLs are well under control, while thepreservation of capital is the current priority of banks. All in all, the strong performances of banks shallbe maintained next year. Our top picks in the sector are BBNI and BBRI, given the cheap share price andturnaround story of the former and the strong profitability and solid business model of the latter.

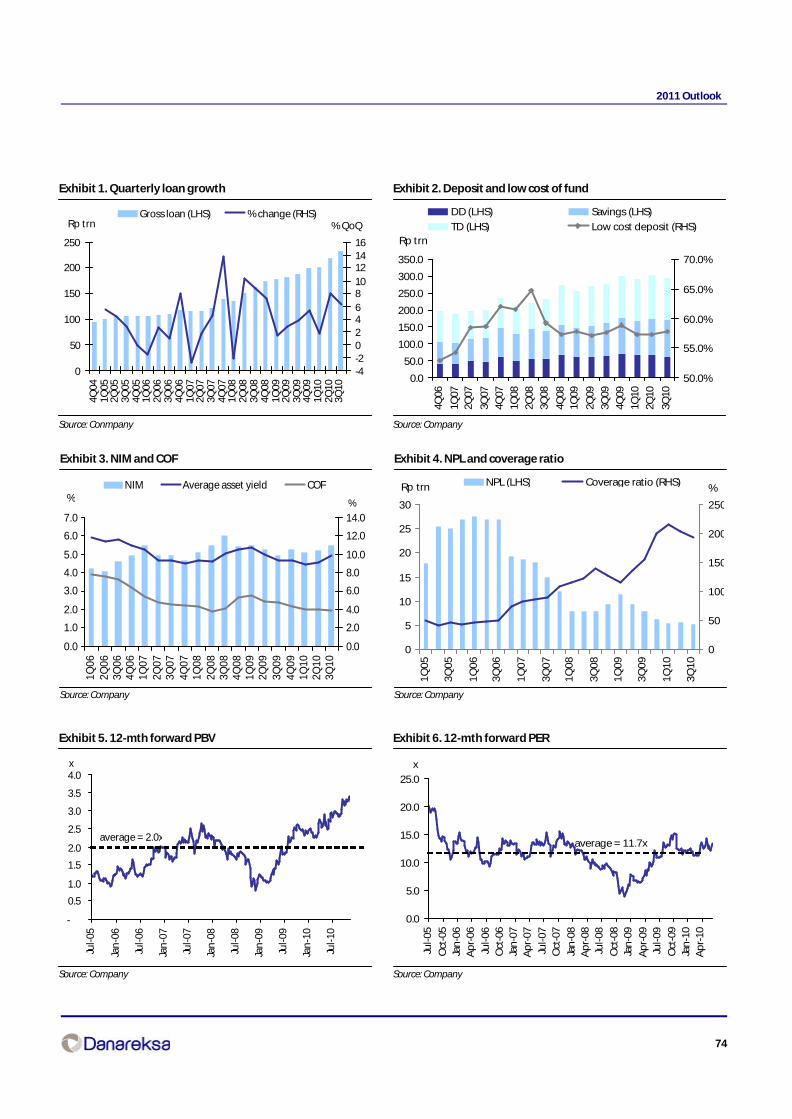

Will profitability be sustained?Inevitably, the NIM shall narrow in the longer run. Tight competition in the extending of loans shallkeep the asset yield at a relatively stable 6-7%, while the requirement of greater funding will lead toa higher COF. However, any decline in the NIM is unlikely to be significant in the next 2 years. We estimatethe NIM to stay at 5.6% next year, helped by a greater volume of loans channeled. Much of the newloans extended are now shifted towards high yielding segments to offset an additional COF of around15-20bps. Note that commercial banks have seen their loans growth driven by the extension of SMEloans. Indeed, the higher COF is expected largely due to regulatory impacts – an additional 3% SRR andprobably an increase in high cost TD, as banks seek greater funding. Deposits growth is likely to slowto 12.4%, as there is a vast availability of alternative investments. Still, a combination of strong loansgrowth, a solid NIM and well-managed NPLs shall likely lead to a healthy ROE of 25% next year.

Preserving capital and liquidityWhilst liquidity remains aplenty, marginal CAR levels have led banks to search for greater capital, eitherthrough rights issues or making lower dividend payouts. In some cases, banks are channeling a largerproportion of their loans to less-weighted micro segments to keep their CARs above 12%. Thus far,about Rp15.8tnn has been raised, with BBNI accounting for the bulk of it. Liquidity, however, is aplentywith around 6.7% and 5.0% of banks’ assets placed in SBIs and marketable securities, excluding recapgovernment bonds. Alternative funding – i.e. through bonds issuances - is another possibility, ifnecessary. Of the five banks under our coverage, three banks, BBCA, BBRI and BDMN, have stated theirinterest in issuing Rp6-7trn of sub-debt/bonds in total, just sufficient to ensure that their capital meetsBI’s requirement, especially since they are growing their loans in excess of 20% p.a.

Risks to watchSo, what could derail our projections? Well, the main risk is higher NPLs - which could be the result ofan economic slowdown or improper lending. Inflation and therefore a high benchmark rate may leadto slower loans growth, greater NPLs and therefore higher provisioning charges, although profits couldstill be made, in particular by banks that have high variable rate assets on their books. BI’s plans forgreater lending may also lead to higher asset quality risk, if the funds are not properly lent. So far, NPLshave been kept down at 3.0%, with coverage exceeding 100%. At least for now, this shall act as a cushionagainst any shocks from possible economic slowdown.

Price Mkt cap PBV, x PER, x ROE, %US$ mn FY10E FY11E FY10E FY11E FY10E FY11E

BBCA IJ 6,700 18,100 5.2 4.6 21.7 19.6 25.6 25.0BMRI 6,400 14,724 3.3 2.6 16.7 14.4 21.3 21.2BBRI IJ 10,250 13,859 3.8 3.1 14.3 10.9 29.3 31.6BDMN IJ 5,800 5,350 2.8 2.6 17.6 13.5 16.8 20.0BBNI IJ 3,775 6,318 2.7 2.1 15.0 13.6 19.2 18.8

Bonny B Setiawan CFA(62-21) 2352 [email protected]

OVERWEIGHT

Last Recommendation

Jakfin relative to JCI Index

250

350

450

550

12/1

8/09

2/1/

10

3/10

/10

4/19

/10

5/26

/10

7/2/

10

8/9/

10

9/22

/10

10/2

8/10

12/6

/10

-5

0

5

10

15

Jakfin (LHS) Relative to JCI Index (RHS)%Rp

16

2011 Outlook

Exhibit 1. Industry loan growth is robust

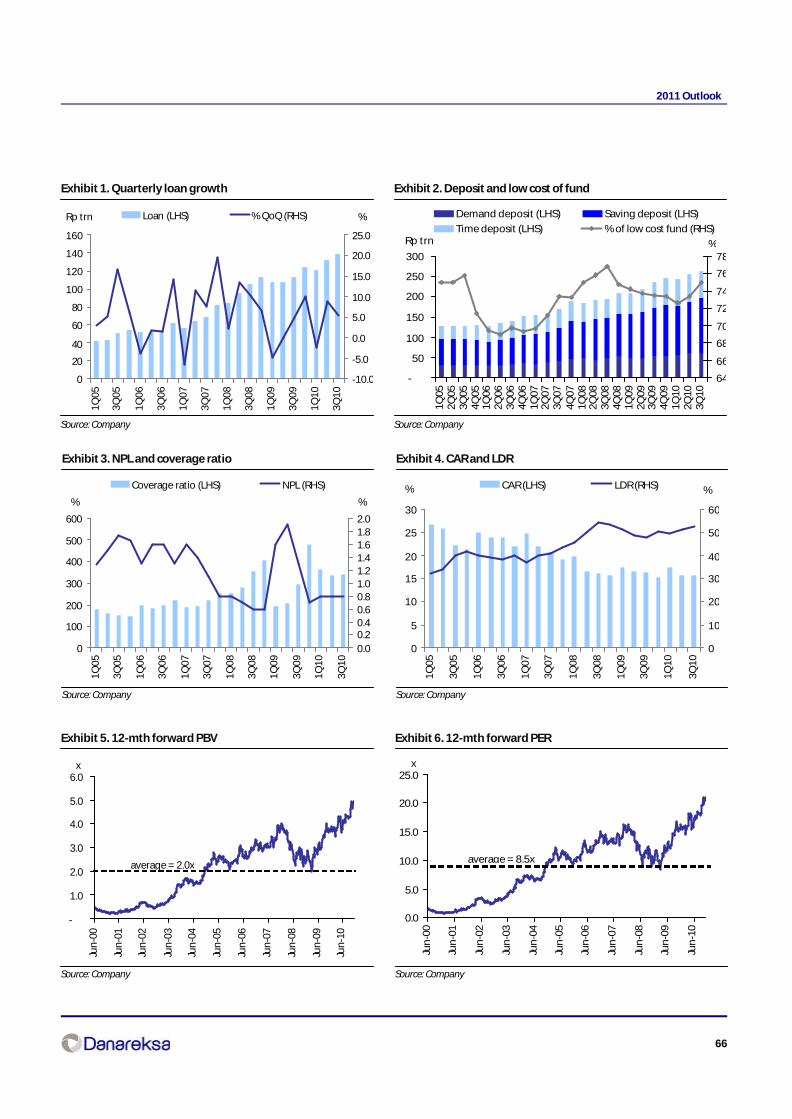

Source: BI

Exhibit 2. NPL has been in the declining trend

Source: BI

Exhibit 3. Earnings growth has stayed at 27%

Source: BI

Exhibit 4. Preserving capital is banks’ current priority

Source: BI

Exhibit 5. Lending in SMEs has trended up

Source: BI

Exhibit 6. Commercial banks are focusing towards SME

Source: BI

05

10152025

30354045

Jan

-04

No

v-04

Sep

-05

Jul-

06

May

-07

Mar

-08

Jan

-09

No

v-09

Sep

-10

%

6

7

8

9

10

11

12

13

14%

Loan growth, YoY (LHS) SBI 1-mth (RHS)

%

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Jan

-03

Aug

-03

Mar

-04

Oct

-04

May

-05

Dec

-05

Jul-

06

Feb

-07

Sep

-07

Ap

r-08

Nov

-08

Jun

-09

Jan

-10

Aug

-10

% NIM NPL

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Feb

-07

Aug

-07

Feb

-08

Aug

-08

Feb

-09

Aug

-09

Feb

-10

Aug

-10

YoY

10

20

30

40

50

60

70

80

90

Jan

-03

Au

g-0

3

Mar

-04

Oct

-04

May

-05

Dec

-05

Jul-

06

Feb

-07

Sep

-07

Ap

r-08

No

v-08

Jun

-09

Jan

-10

Au

g-1

0

%

101214

1618

20222426

28

%LDR (LHS) CAR (RHS)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Jan

-05

May

-05

Sep

-05

Jan

-06

May

-06

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

Jan

-05

May

-05

Sep

-05

Jan

-06

May

-06

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

SOE Regional development bank Commercial

YoY

17

2011 Outlook

Exhibit 7. Domestic peer comparisons

Bloomberg Price Mcap PBV, x PER, x ROE, % ROA, % Dvd yield, %Code (LC) (USD mn) 2010E 2011E 2010E 2011E 2010E 2011E 2010E 2011E 2010E

BBCA IJ 6,700 18,283 5.2 4.6 21.7 19.6 25.6 25.0 2.5 2.4 2.3BMRI IJ 6,400 14,808 3.3 2.6 16.7 14.4 21.3 21.2 1.9 2.1 2.1BBRI IJ 10,250 13,989 3.8 3.1 14.3 10.9 29.3 31.6 2.6 2.9 3.5BDMN IJ 5,800 5,367 2.8 2.6 17.6 13.5 16.8 20.0 2.6 2.8 2.8BBNI IJ 3,775 6,382 2.7 2.1 15.0 13.6 19.2 18.8 1.6 1.9 3.3BNII IJ 800 4,430 5.4 5.4 57.7 46.0 16.2 15.0 0.9 NA 0.7PNBN IJ 1,090 2,451 2.1 1.8 15.6 12.8 14.0 14.9 1.9 2.3 2.3BNGA IJ 2,150 5,696 3.9 3.3 23.6 20.5 17.9 17.5 1.8 1.8 0.3BTPN IJ 13,700 1,431 4.2 3.2 18.5 13.8 31.2 30.3 3.0 2.9 0.0BBTN IJ 1,620 1,139 2.3 2.1 17.7 12.8 13.8 17.2 1.2 1.5 1.4Weighted average 3.9 3.3 20.4 17.1 22.6 23.1 2.1 2.2 2.3

Source: Bloomberg and Danareksa Sekuritas

Exhibit 8. Regional peer comparisons

Bloomberg Price Mcap PBV, x PER, x ROE, % ROA, % Dvd yield, %Code (LC) (USD mn) 2010E 2011E 2010E 2011E 2010E 2011E 2010E 2011E 2010E

CM CN 77.8 29,655 2.4 2.2 12.5 10.9 20.7 20.6 0.7 0.8 4.43988 HK 0.5 39,686 1.6 1.4 9.5 8.6 17.5 17.5 1.1 1.1 4.4998 HK 0.6 7,878 1.4 1.2 8.5 7.7 17.3 17.2 1.0 1.0 3.0939 HK 0.9 201,371 2.2 1.9 10.7 9.2 22.0 22.0 1.3 1.4 4.0601166 CH 3.6 18,187 1.6 1.3 8.4 7.1 22.5 20.8 1.1 1.1 2.2601398 CH 0.6 158,923 1.8 1.6 9.2 7.8 21.0 21.6 1.3 1.3 4.9600036 CH 2.0 23,732 2.1 1.8 11.0 9.0 21.8 21.2 1.1 1.2 1.9AXSB IN 28.9 10,364 3.3 2.9 20.5 17.0 18.4 18.6 1.5 1.6 0.9BOI IN 9.7 5,076 1.8 1.6 10.0 8.7 16.2 18.5 0.8 1.0 1.6004940 KS 10.1 6,536 0.9 0.8 7.4 6.6 12.5 13.3 1.1 1.1 5.4024110 KS 16.5 8,392 1.1 1.0 8.5 7.4 14.0 14.2 0.9 0.9 2.3005280 KS 12.5 2,341 1.1 1.0 7.3 6.8 16.0 15.1 1.2 1.1 2.6005270 KS 13.1 1,725 1.0 0.9 8.1 6.5 12.7 14.4 0.8 1.0 2.6HLBK MK 3.0 4,736 2.3 1.9 15.5 13.1 15.7 15.8 1.1 1.3 2.2MAY MK 2.7 19,203 2.2 2.0 16.4 14.0 14.2 15.0 1.1 1.2 3.0CIMB MK 2.7 9,708 2.6 2.3 17.2 14.4 16.2 16.9 1.4 1.5 2.0BBL TB 4.9 9,364 1.3 1.2 11.4 10.5 12.0 12.0 1.4 1.4 3.1SCB TB 3.4 8,531 2.2 2.0 14.4 12.5 16.3 16.9 1.8 1.9 2.8KK TB 1.2 650 1.0 1.0 7.1 6.9 15.2 13.7 2.1 2.0 6.6KTB TB 0.6 6,299 1.5 1.4 12.8 10.4 12.8 13.9 0.9 1.1 3.0OCBC SP 7.5 23,482 1.7 1.6 14.1 13.1 12.3 12.4 1.2 1.1 3.3UOB SP 13.7 20,829 1.4 1.4 11.1 10.9 13.2 12.8 1.2 1.2 4.0DBS SP 10.9 24,974 1.3 1.2 17.1 12.0 7.5 10.4 0.8 1.0 3.9Weighted average 1.9 1.7 11.1 9.5 19.1 19.4 1.2 1.3 3.9

Source: Bloomberg and Danareksa Sekuritas

18

2011 Outlook

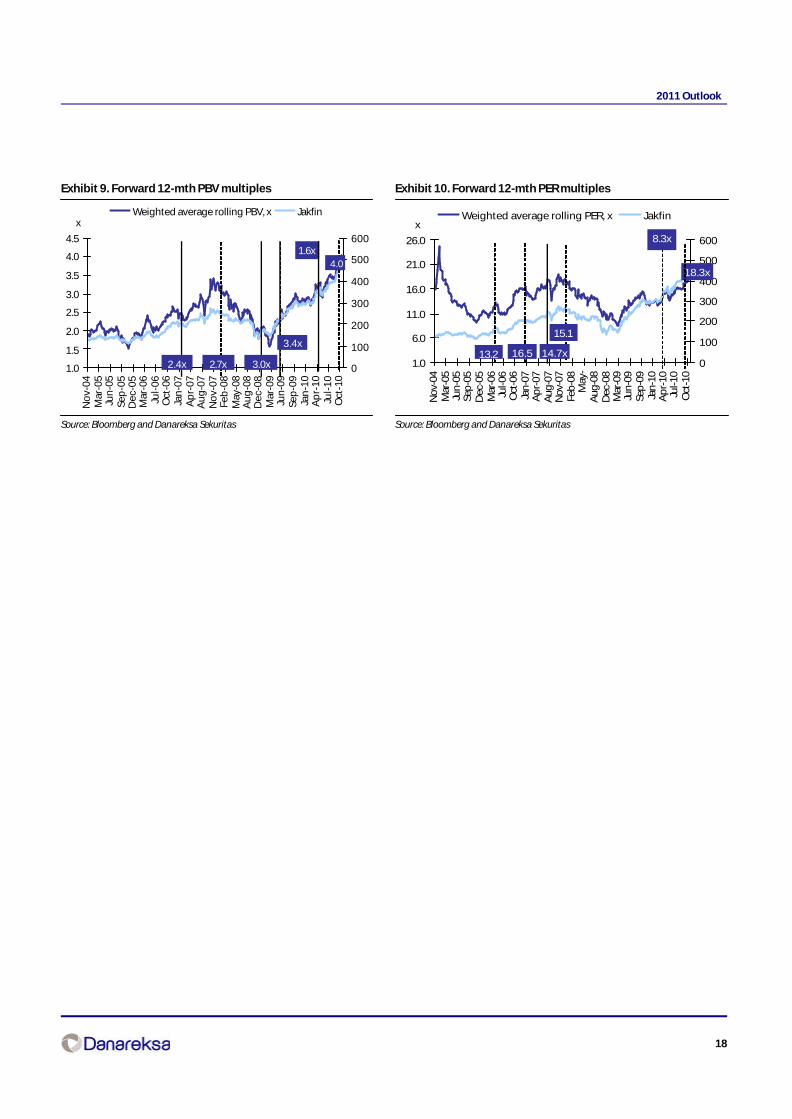

Exhibit 9. Forward 12-mth PBV multiples

Source: Bloomberg and Danareksa Sekuritas

Exhibit 10. Forward 12-mth PER multiples

Source: Bloomberg and Danareksa Sekuritas

1.0

6.0

11.0

16.0

21.0

26.0

No

v-04

Mar

-05

Jun

-05

Sep

-05

Dec

-05

Mar

-06

Jul-0

6O

ct-0

6Ja

n-0

7A

pr-

07A

ug-0

7N

ov-

07Fe

b-0

8M

ay-

Aug

-08

Dec

-08

Mar

-09

Jun

-09

Sep

-09

Jan

-10

Ap

r-10

Jul-1

0O

ct-1

0

0

100

200

300

400

500

600

Weighted average rolling PER, x Jakfinx

13.2 16.5 14.7x

15.1

8.3x

18.3x

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

No

v-04

Mar

-05

Jun

-05

Sep

-05

Dec

-05

Mar

-06

Jul-

06

Oct

-06

Jan

-07

Ap

r-07

Au

g-0

7N

ov-

07Fe

b-0

8M

ay-0

8A

ug

-08

Dec

-08

Mar

-09

Jun

-09

Sep

-09

Jan

-10

Ap

r-10

Jul-

10

Oct

-10

0

100

200

300

400

500

600

Weighted average rolling PBV, x Jakfinx

2.4x 2.7x 3.0x

3.4x

1.6x4.0

19

2011 Outlook

Coal sectorThe black magic is back

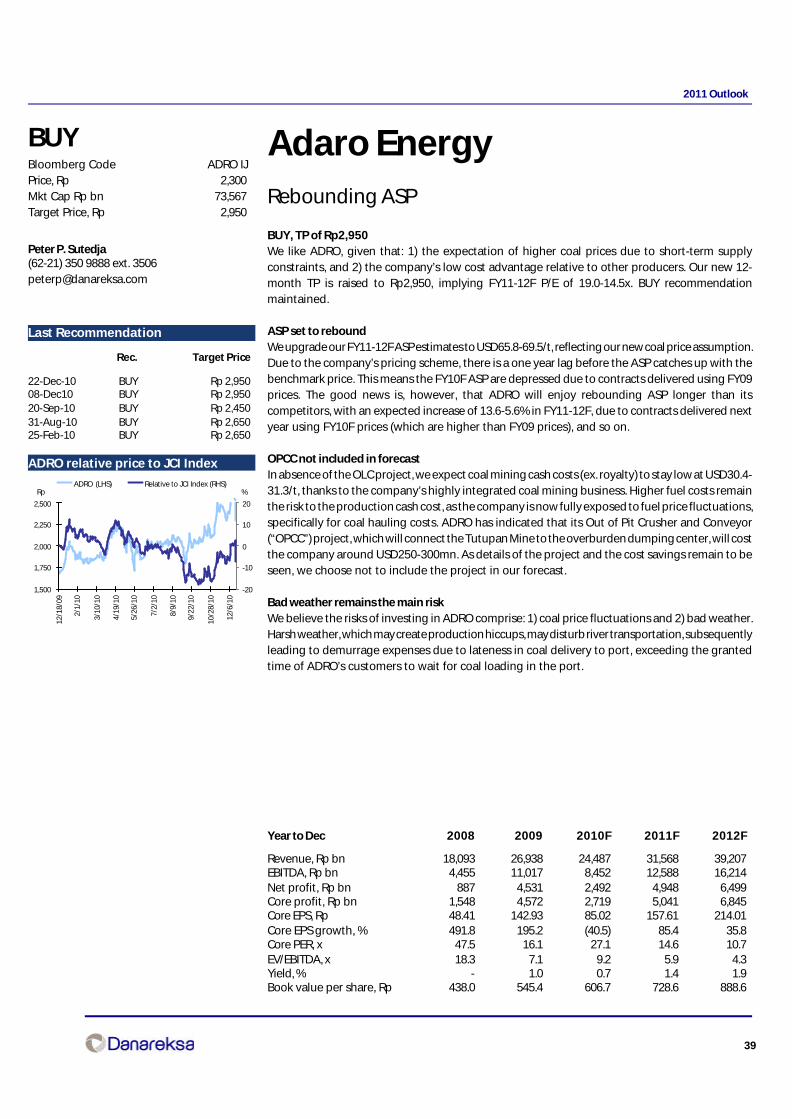

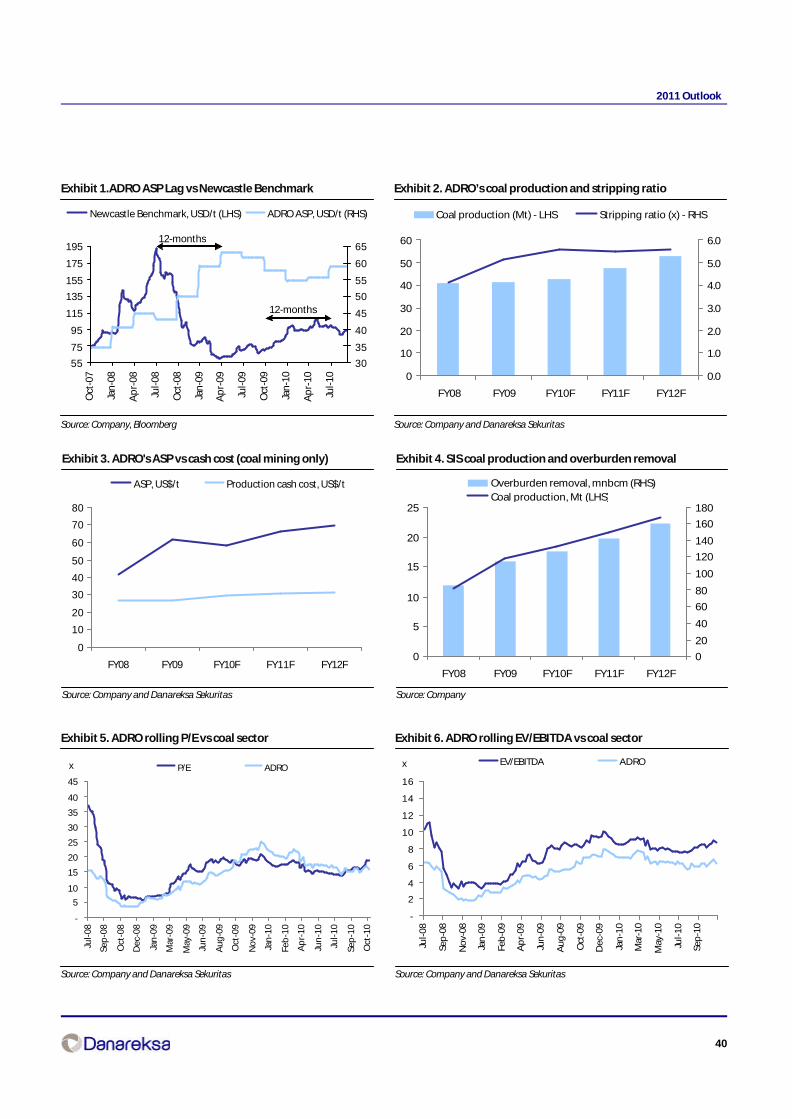

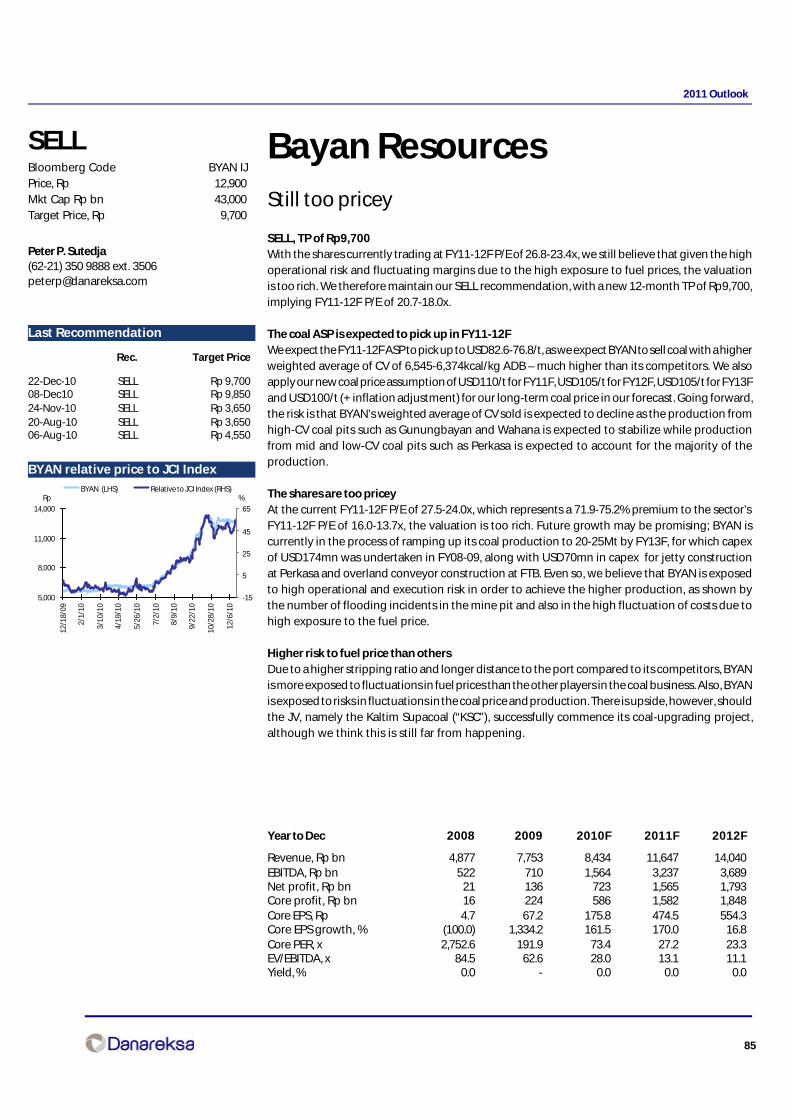

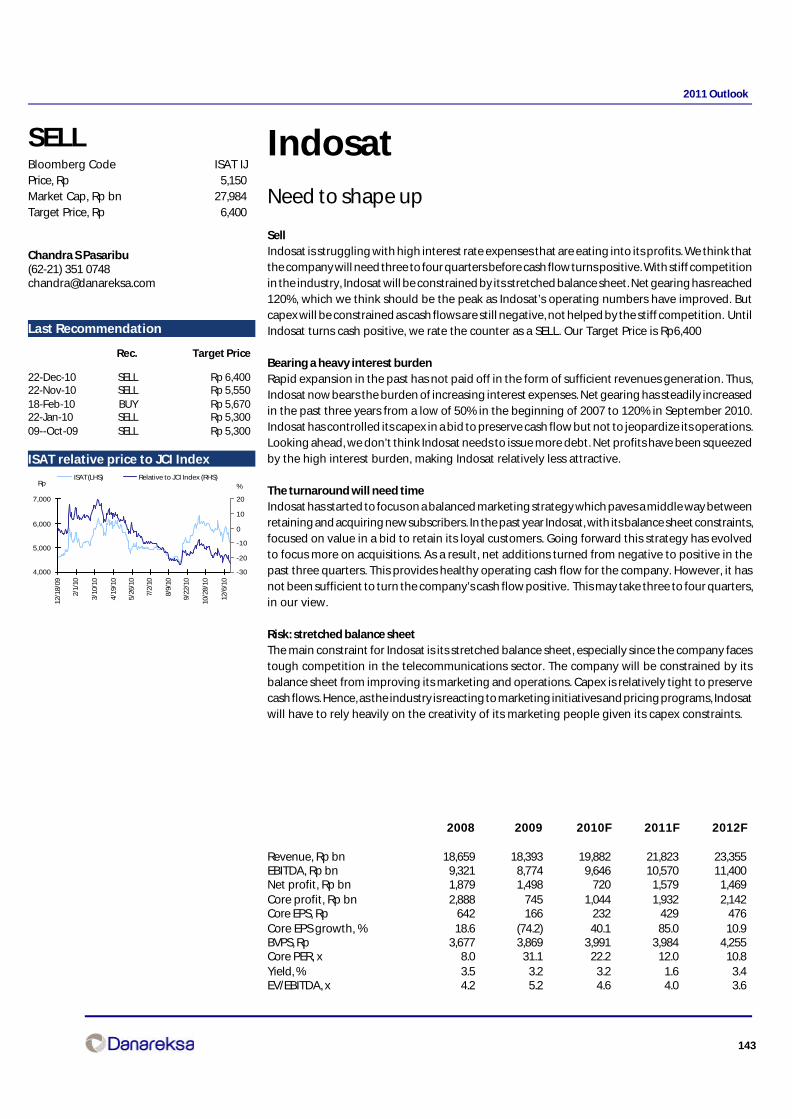

Supply shortfall continuesWe have seen coal companies missing their production guidance in 9M10. This means some ofthe coal deliveries that originally have been contracted for this year will not be met, and this short-term supply shortfall will create upward pressures on the coal price. On the demand side, we seehuge demand building up long-term, as India is stepping up to becoming one of the largest coalimporters alongside China in order to fuel their 100GW power projects by 2017. In light of this,we upgrade our coal price forecast to USD110/t for FY11F, USD105/t for FY12F, USD105/t for FY13Fand USD100/t for our long-term coal price. Our top pick in the sector is ADRO. We like the companyfor its low-cost advantage, which we believe will provide strong profitability amidst volatility incoal prices.

The weather is not going to improve anytime soonAnticipating more bad weather, we have lowered our overall coal production target by 5.6-7.6%for this year and next year. The shortfall will result in rising coal prices in the future. Bad weatherin Indonesia, which is attributed to the La Niña weather phenomenon, is expected to persist untilthe first quarter of next year. The World Meteorological Organization in November said in its pressrelease that “La Niña conditions may possibly further strengthen during the next four to sixmonths”. This means that coal supply shortfall can be expected, and we’re about to see morecompanies missing their production targets, as the bad weather will create difficulties in coalextracting, overburden removing, coal hauling and barging through rivers.

Longer-term demand from global power plant projectsWe expect demand for coal to remain strong, with India and China to be the main drivers ofdemand, which is expected to total 76quad btu or equivalent to around 2,850Mt of coal with CVof 6,700 kcal/kg NAR specification by 2015. India, in an effort to overcome its domestic powershortfall, plans to build 9x4000MW coal-fired Ultra Mega Power Projects (“UMPP”), whereby eachUMPP will require 15Mtpa of coal. So far, four of the UMPPs have been tendered and commissioningis expected to start in the next five years. China’s forecast 8.4% growth CAGR over the next 5 yearswill trigger more imports for coal, as the domestic production cost is still higher than the cost ofimports. From the domestic side in Indonesia, PLN, the state-owned electricity company, istargeting coal usage of 58% from the total power generating capacity by 2019. This will translateinto coal demand of 107Mt in 2018 or CAGR growth of 9.4% over the next 8 years. All in all, we expectthe growing demand coupled with the supply constraints to drive the coal price higher in the nearterm.

RisksProlonged rain may provide risks of investing in the coal sector, as this will affect coal miners’production this year, although we believe it will be compensated by higher coal prices should therebe any supply shortfall. Also worth watching is that if prices go up too high, then China may reopenits coal mines since it will be economical for them to use domestic coal. Also any change in India’senvironmental policy (which currently prevents them from mining coal in forest areas) will poserisks to our coal price assumptions.

OVERWEIGHT

Peter P. Sutedja(62-21) 350 9888 ext. [email protected]

Jakmine Relative to JCI Index

Rec Price TPRp Rp

ADRO IJ BUY 2,300 2,950BYAN IJ SELL 12,900 9,700BUMI IJ BUY 2,900 3,600INDY IJ BUY 4,275 4,825ITMG IJ HOLD 51,000 55,300PTBA IJ BUY 20,850 26,650

Rec TP P/E, x EV/EBITDA, x Dividend Yield, %Rp/share FY10F FY11F FY10F FY11F FY10F FY11F

ADRO IJ BUY 2,950 29.5 14.9 9.2 5.9 0.7 1.4BYAN IJ SELL 9,700 59.5 27.5 28.0 13.1 0.0 0.0BUMI IJ BUY 3,600 19.5 14.0 8.8 6.0 0.8 1.3INDY IJ BUY 4,825 21.0 13.3 82.7 38.0 1.6 2.4ITMG IJ HOLD 55,300 23.4 12.2 12.2 7.3 3.8 3.8PTBA IJ BUY 26,650 25.3 15.9 18.5 10.9 2.4 1.8

1,500

2,000

2,500

3,000

3,500

12/1

8/09

2/1/

10

3/10

/10

4/19

/10

5/26

/10

7/2/

10

8/9/

10

9/22

/10

10/2

8/10

12/6

/10

-20

-10

0

10

JAKMINE (LHS) Relative to JCI Index (RHS)%

20

2011 Outlook

Exibit 1. World coal production outlook ...

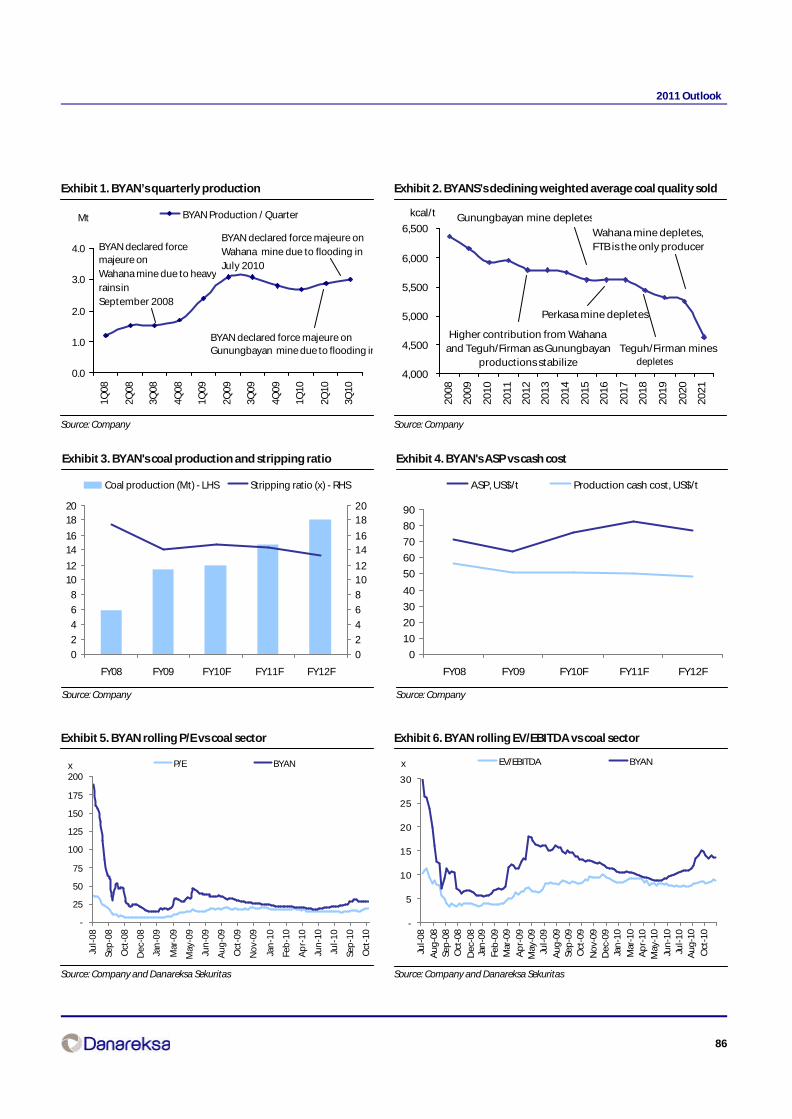

Source: International Energy Outlook 2010

Exibit 2. ... and China and India still expected to lead the world coal consumption

Source: International Energy Outlook 2010

Exibit 3. Domestic coal demand also sees increase ...

Source: PLN

0

20

40

60

80

100

120

2007 2010F 2015F 2020F 2025F 2030F 2035F

Australia ChinaIndia Other Non-OECD AsiaOECD ex Australia Non-OECD ex Asia

quad btu

0

25

50

75

100

125

2005 2006 2007 2015F 2020F 2025F 2030F 2035F

OECD Non-OECD ex China & India China Indiaquad btu

0

40

80

120

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

0%

10%

20%

30%

40%

50%

60%

70%

Domestic coal demand (LHS) Growth (RHS)Mt

21

2011 Outlook

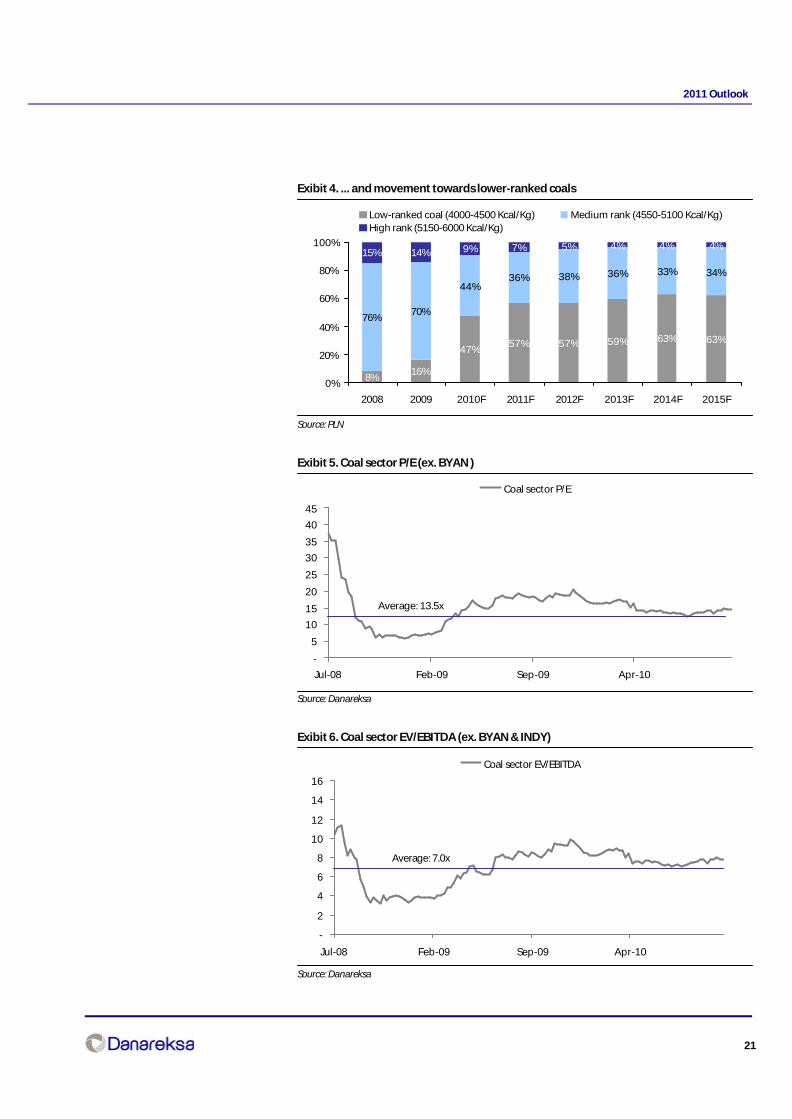

Exibit 4. ... and movement towards lower-ranked coals

Source: PLN

Exibit 5. Coal sector P/E (ex. BYAN )

Source: Danareksa

Exibit 6. Coal sector EV/EBITDA (ex. BYAN & INDY)

Source: Danareksa

8%16%

47%57% 57% 59% 63% 63%

76%70%

44%36% 38% 36% 33% 34%

15% 14% 9% 7% 5% 4% 4% 4%

0%

20%

40%

60%

80%

100%

2008 2009 2010F 2011F 2012F 2013F 2014F 2015F

Low-ranked coal (4000-4500 Kcal/Kg) Medium rank (4550-5100 Kcal/Kg)High rank (5150-6000 Kcal/Kg)

-

5

10

15

20

25

30

35

40

45

Jul-08 Feb-09 Sep-09 Apr-10

Coal sector P/E

Average: 13.5x

-

2

4

6

8

10

12

14

16

Jul-08 Feb-09 Sep-09 Apr-10

Coal sector EV/EBITDA

Average: 7.0x

22

2011 Outlook

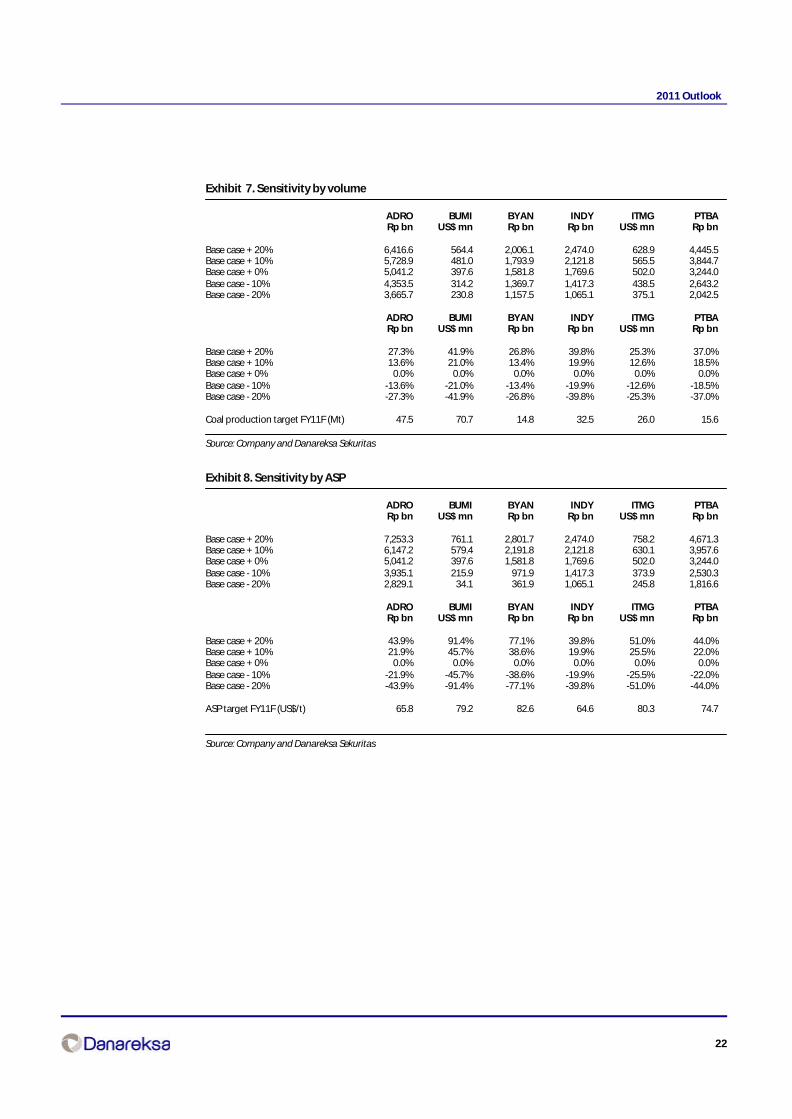

Exhibit 7. Sensitivity by volume

ADRO BUMI BYAN INDY ITMG PTBARp bn US$ mn Rp bn Rp bn US$ mn Rp bn

Base case + 20% 6,416.6 564.4 2,006.1 2,474.0 628.9 4,445.5Base case + 10% 5,728.9 481.0 1,793.9 2,121.8 565.5 3,844.7Base case + 0% 5,041.2 397.6 1,581.8 1,769.6 502.0 3,244.0Base case - 10% 4,353.5 314.2 1,369.7 1,417.3 438.5 2,643.2Base case - 20% 3,665.7 230.8 1,157.5 1,065.1 375.1 2,042.5

ADRO BUMI BYAN INDY ITMG PTBARp bn US$ mn Rp bn Rp bn US$ mn Rp bn

Base case + 20% 27.3% 41.9% 26.8% 39.8% 25.3% 37.0%Base case + 10% 13.6% 21.0% 13.4% 19.9% 12.6% 18.5%Base case + 0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Base case - 10% -13.6% -21.0% -13.4% -19.9% -12.6% -18.5%Base case - 20% -27.3% -41.9% -26.8% -39.8% -25.3% -37.0%

Coal production target FY11F (Mt) 47.5 70.7 14.8 32.5 26.0 15.6

Source: Company and Danareksa Sekuritas

Exhibit 8. Sensitivity by ASP

ADRO BUMI BYAN INDY ITMG PTBARp bn US$ mn Rp bn Rp bn US$ mn Rp bn

Base case + 20% 7,253.3 761.1 2,801.7 2,474.0 758.2 4,671.3Base case + 10% 6,147.2 579.4 2,191.8 2,121.8 630.1 3,957.6Base case + 0% 5,041.2 397.6 1,581.8 1,769.6 502.0 3,244.0Base case - 10% 3,935.1 215.9 971.9 1,417.3 373.9 2,530.3Base case - 20% 2,829.1 34.1 361.9 1,065.1 245.8 1,816.6

ADRO BUMI BYAN INDY ITMG PTBARp bn US$ mn Rp bn Rp bn US$ mn Rp bn

Base case + 20% 43.9% 91.4% 77.1% 39.8% 51.0% 44.0%Base case + 10% 21.9% 45.7% 38.6% 19.9% 25.5% 22.0%Base case + 0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Base case - 10% -21.9% -45.7% -38.6% -19.9% -25.5% -22.0%Base case - 20% -43.9% -91.4% -77.1% -39.8% -51.0% -44.0%

ASP target FY11F (US$/t) 65.8 79.2 82.6 64.6 80.3 74.7

Source: Company and Danareksa Sekuritas

23

2011 Outlook

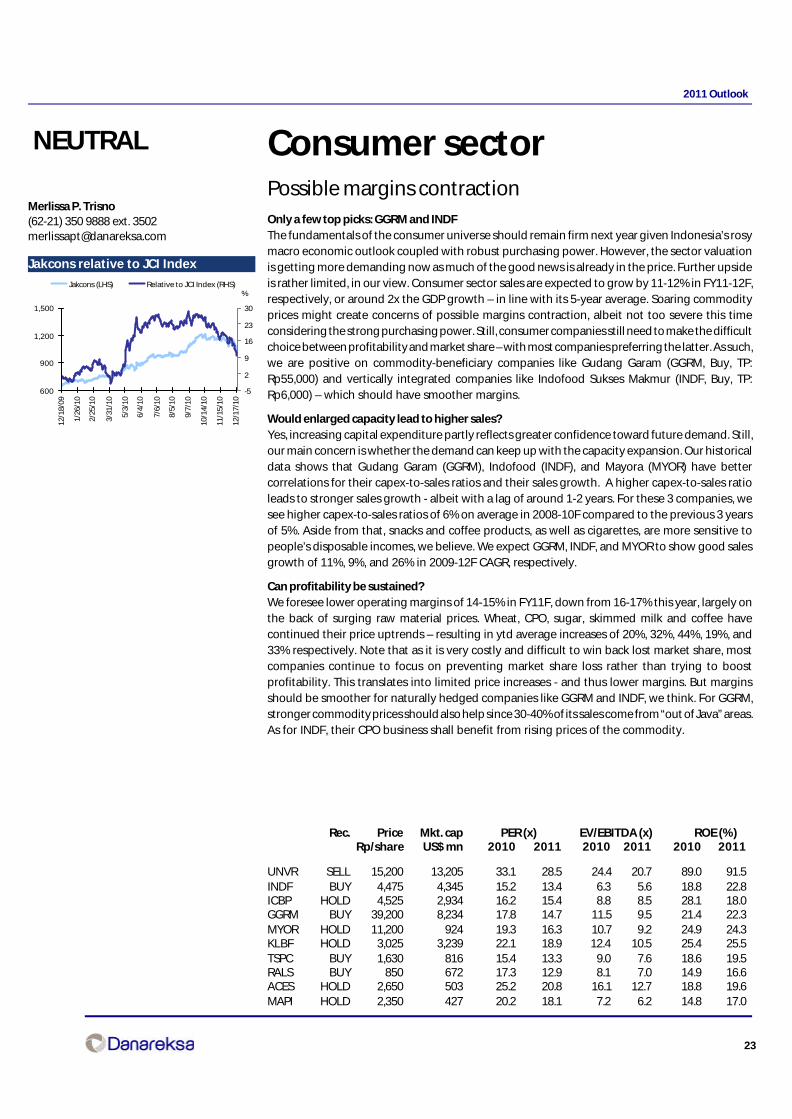

Consumer sectorPossible margins contractionOnly a few top picks: GGRM and INDFThe fundamentals of the consumer universe should remain firm next year given Indonesia’s rosymacro economic outlook coupled with robust purchasing power. However, the sector valuationis getting more demanding now as much of the good news is already in the price. Further upsideis rather limited, in our view. Consumer sector sales are expected to grow by 11-12% in FY11-12F,respectively, or around 2x the GDP growth – in line with its 5-year average. Soaring commodityprices might create concerns of possible margins contraction, albeit not too severe this timeconsidering the strong purchasing power. Still, consumer companies still need to make the difficultchoice between profitability and market share – with most companies preferring the latter. As such,we are positive on commodity-beneficiary companies like Gudang Garam (GGRM, Buy, TP:Rp55,000) and vertically integrated companies like Indofood Sukses Makmur (INDF, Buy, TP:Rp6,000) – which should have smoother margins.

Would enlarged capacity lead to higher sales?Yes, increasing capital expenditure partly reflects greater confidence toward future demand. Still,our main concern is whether the demand can keep up with the capacity expansion. Our historicaldata shows that Gudang Garam (GGRM), Indofood (INDF), and Mayora (MYOR) have bettercorrelations for their capex-to-sales ratios and their sales growth. A higher capex-to-sales ratioleads to stronger sales growth - albeit with a lag of around 1-2 years. For these 3 companies, wesee higher capex-to-sales ratios of 6% on average in 2008-10F compared to the previous 3 yearsof 5%. Aside from that, snacks and coffee products, as well as cigarettes, are more sensitive topeople’s disposable incomes, we believe. We expect GGRM, INDF, and MYOR to show good salesgrowth of 11%, 9%, and 26% in 2009-12F CAGR, respectively.

Can profitability be sustained?We foresee lower operating margins of 14-15% in FY11F, down from 16-17% this year, largely onthe back of surging raw material prices. Wheat, CPO, sugar, skimmed milk and coffee havecontinued their price uptrends – resulting in ytd average increases of 20%, 32%, 44%, 19%, and33% respectively. Note that as it is very costly and difficult to win back lost market share, mostcompanies continue to focus on preventing market share loss rather than trying to boostprofitability. This translates into limited price increases - and thus lower margins. But marginsshould be smoother for naturally hedged companies like GGRM and INDF, we think. For GGRM,stronger commodity prices should also help since 30-40% of its sales come from “out of Java” areas.As for INDF, their CPO business shall benefit from rising prices of the commodity.

Merlissa P. Trisno(62-21) 350 9888 ext. [email protected]

NEUTRAL

Jakcons relative to JCI Index

600

900

1,200

1,500

12/1

8/09

1/26

/10

2/25

/10

3/31

/10

5/3/

10

6/4/

10

7/6/

10

8/5/

10

9/7/

10

10/1

4/10

11/1

5/10

12/1

7/10

-5

2

9

16

23

30

Jakcons (LHS) Relative to JCI Index (RHS)%

Rec. Price Mkt. cap PER (x) EV/EBITDA (x) ROE (%)Rp/share US$ mn 2010 2011 2010 2011 2010 2011

UNVR SELL 15,200 13,205 33.1 28.5 24.4 20.7 89.0 91.5INDF BUY 4,475 4,345 15.2 13.4 6.3 5.6 18.8 22.8ICBP HOLD 4,525 2,934 16.2 15.4 8.8 8.5 28.1 18.0GGRM BUY 39,200 8,234 17.8 14.7 11.5 9.5 21.4 22.3MYOR HOLD 11,200 924 19.3 16.3 10.7 9.2 24.9 24.3KLBF HOLD 3,025 3,239 22.1 18.9 12.4 10.5 25.4 25.5TSPC BUY 1,630 816 15.4 13.3 9.0 7.6 18.6 19.5RALS BUY 850 672 17.3 12.9 8.1 7.0 14.9 16.6ACES HOLD 2,650 503 25.2 20.8 16.1 12.7 18.8 19.6MAPI HOLD 2,350 427 20.2 18.1 7.2 6.2 14.8 17.0

24

2011 Outlook

What could derail our forecast?The key risk is inflation, especially since the government plans to end subsidies on fuel forprivate motorists. Although the details are still sketchy, the plan may be implemented in2Q11. The other risks include rupiah depreciation, stiffer competition, and global economicslowdown.

Exhibit 1. Consumer sales vs GDP growth

Source: CEIC and Danareksa Sekuritas

Exhibit 2. GGRM’s capex-to-sales ratio

Source: Company

Exhibit 3. INDF’s capex to sales ratio

Source: Company

Exhibit 4. Commodity prices index

Source: Bloomberg

0.00.51.01.52.02.53.03.54.04.5

2002 2003 2004 2005 2006 2007 2008 2009 2010F2011F

Consumer sales-to-GDP growth ratio

Consumer sales-to-private cons growth ratio

5-years avg ratio:

2.3x

x

0.01.02.03.04.05.06.07.08.09.0

10.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

0%

5%

10%

15%

20%

25%

Capex/sales ratio (LHS) Revenue growth (RHS)

%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

-10%

0%

10%

20%

30%

40%

50%

Capex/sales ratio (LHS) Revenue growth (RHS)%

0

50

100

150

200

250

300

350

400

1Q98

1Q99

1Q00

1Q01

1Q02

1Q03

1Q04

1Q05

1Q06

1Q07

1Q08

1Q09

1Q10

25

2011 Outlook

Exhibit 5. Forward PE

Source: Bloomberg, Danareksa Sekuritas

Exhibit 6. Premium (discount) to market

Source: Bloomberg, Danareksa Sekuritas

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Jan

-96

Sep

-96

May

-97

Jan

-98

Sep

-98

May

-99

Jan

-00

Sep

-00

May

-01

Jan

-02

Sep

-02

May

-03

Jan

-04

Sep

-04

May

-05

Jan

-06

Sep

-06

May

-07

Jan

-08

Sep

-08

May

-09

Jan

-10

Sep

-10

12-mth forward PE Average 5-yrs

+2 St.dev -2 St.devx

average=11.7x

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Jan

-96

Sep

-96

May

-97

Jan

-98

Sep

-98

May

-99

Jan

-00

Sep

-00

May

-01

Jan

-02

Sep

-02

May

-03

Jan

-04

Sep

-04

May

-05

Jan

-06

Sep

-06

May

-07

Jan

-08

Sep

-08

May

-09

Jan

-10

Sep

-10

-60

-40

-20

0

20

40

60

80

Prem (disc) to consumerConsumer - PERJCI - PERx %

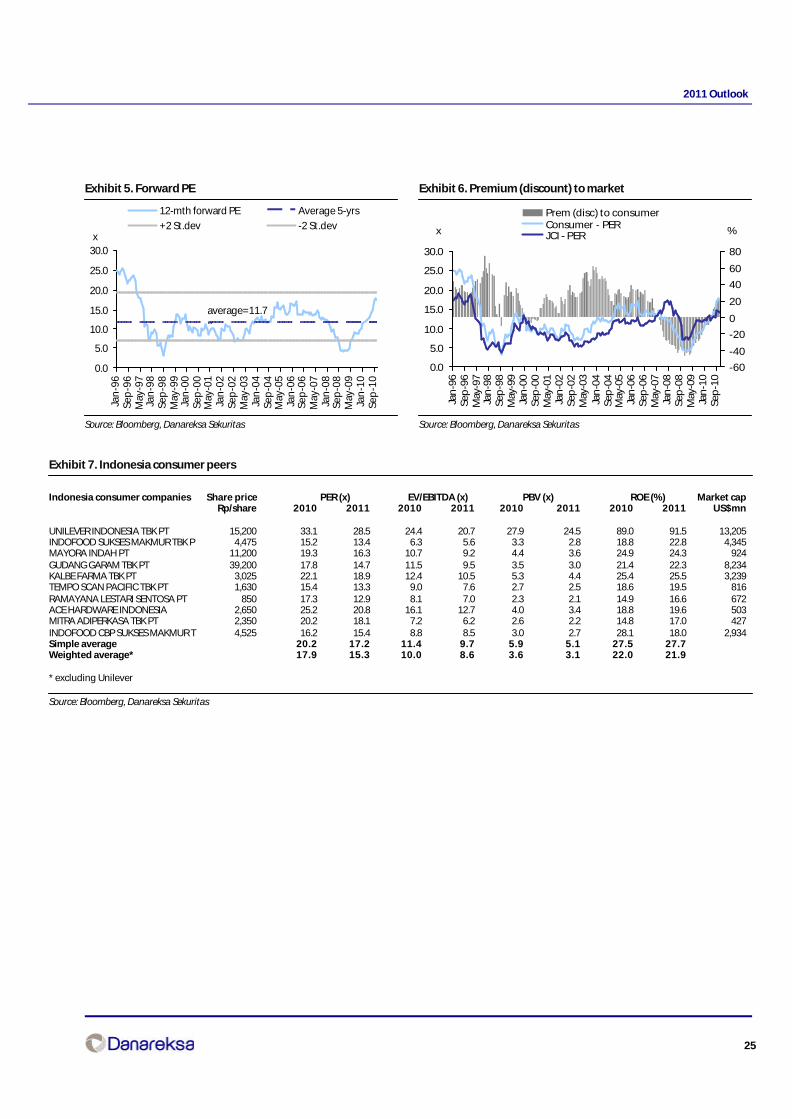

Exhibit 7. Indonesia consumer peers

Indonesia consumer companies Share price PER (x) EV/EBITDA (x) PBV (x) ROE (%) Market capRp/share 2010 2011 2010 2011 2010 2011 2010 2011 US$mn

UNILEVER INDONESIA TBK PT 15,200 33.1 28.5 24.4 20.7 27.9 24.5 89.0 91.5 13,205INDOFOOD SUKSES MAKMUR TBK P 4,475 15.2 13.4 6.3 5.6 3.3 2.8 18.8 22.8 4,345MAYORA INDAH PT 11,200 19.3 16.3 10.7 9.2 4.4 3.6 24.9 24.3 924GUDANG GARAM TBK PT 39,200 17.8 14.7 11.5 9.5 3.5 3.0 21.4 22.3 8,234KALBE FARMA TBK PT 3,025 22.1 18.9 12.4 10.5 5.3 4.4 25.4 25.5 3,239TEMPO SCAN PACIFIC TBK PT 1,630 15.4 13.3 9.0 7.6 2.7 2.5 18.6 19.5 816RAMAYANA LESTARI SENTOSA PT 850 17.3 12.9 8.1 7.0 2.3 2.1 14.9 16.6 672ACE HARDWARE INDONESIA 2,650 25.2 20.8 16.1 12.7 4.0 3.4 18.8 19.6 503MITRA ADIPERKASA TBK PT 2,350 20.2 18.1 7.2 6.2 2.6 2.2 14.8 17.0 427INDOFOOD CBP SUKSES MAKMUR T 4,525 16.2 15.4 8.8 8.5 3.0 2.7 28.1 18.0 2,934Simple average 20.2 17.2 11.4 9.7 5.9 5.1 27.5 27.7Weighted average* 17.9 15.3 10.0 8.6 3.6 3.1 22.0 21.9

* excluding Unilever

Source: Bloomberg, Danareksa Sekuritas

26

2011 Outlook

Exhibit 8. Regional consumer peers

Consumer regional peers Share price PER (x) EV/EBITDA (x) PBV (x) ROE (%) Market caplocal currency 2010 2011 2010 2011 2010 2011 2010 2011 (US$ mn)

NISSIN FOODS HOLDINGS CO LTD 2,936 14.5 15.2 5.8 6.0 1.2 1.1 8.3 7.9 3,882TINGYI (CAYMAN ISLN) HLDG CO 20 32.4 27.0 15.3 12.7 8.5 7.3 27.8 28.3 14,476UNI-PRESIDENT CHINA HOLDINGS 4 21.4 17.3 9.5 7.5 2.0 1.8 9.2 10.7 1,958UNIVERSAL ROBINA CORP 36 11.1 10.3 6.5 6.2 1.8 1.7 18.5 16.6 1,721NONG SHIM CO LTD 201,500 10.5 9.9 4.9 4.7 0.9 0.9 9.5 9.4 1,010WANT WANT CHINA HOLDINGS LTD 7 29.8 23.4 22.4 17.5 10.4 9.1 36.4 41.2 11,431VITASOY INTL HOLDINGS LTD 6 22.4 19.7 11.7 10.4 4.4 4.1 20.4 21.6 831CHINA FOODS LTD 5 28.6 21.0 14.1 11.2 2.3 2.1 8.4 10.5 1,795NESTLE (MALAYSIA) BERHAD 43 23.2 22.1 16.0 15.0 16.0 14.9 66.4 64.1 3,216PETRA FOODS LTD 2 19.8 17.1 13.8 12.1 2.7 2.4 15.5 15.2 685MORINAGA MILK INDUSTRY CO 346 12.3 9.9 5.2 4.9 0.8 0.8 7.0 7.9 1,038YAKULT HONSHA CO LTD 2,368 28.7 24.6 9.6 8.9 1.7 1.6 6.4 6.9 4,872AUSNUTRIA DAIRY CORP LTD 3 15.1 12.3 8.8 6.2 1.8 1.6 15.5 14.5 363BRIGHT DAIRY & FOOD CO LTD-A 11 56.4 45.4 20.1 15.6 4.6 4.2 7.5 8.0 1,666VIET NAM DAIRY PRODUCTS JSC 86,000 8.4 8.5 7.1 5.7 3.5 2.8 45.7 39.2 1,549GUANGXI ROYAL DAIRY CO LTD-A 51 80.7 55.7 n.a. n.a. 6.9 n.a. n.a. n.a. 205CHINA MENGNIU DAIRY CO 21 23.7 18.6 12.2 9.5 3.3 2.9 15.0 17.5 4,691LG HOUSEHOLD & HEALTH CARE 393,000 29.7 24.4 22.4 19.0 8.7 6.7 31.7 30.4 4,995COLGATE-PALMOLIVE CO 80 16.8 15.9 10.1 9.7 14.8 13.6 82.4 81.3 39,753DABUR INDIA LTD 101 29.3 24.1 22.5 18.6 12.9 10.1 50.4 46.4 3,854HINDUSTAN UNILEVER LTD 295 29.3 25.8 22.4 19.7 21.5 18.6 79.0 76.3 14,160HENGAN INTL GROUP CO LTD 66 31.2 25.0 22.5 17.9 8.0 7.1 27.2 29.6 10,411COLGATE PALMOLIVE (INDIA) 872 26.1 23.8 20.6 17.9 29.6 23.9 119.1 108.7 2,607GODREJ CONSUMER PRODUCTS LTD 363 24.7 19.9 19.9 16.2 6.8 5.8 35.3 32.1 2,462SHANGHAI JAHWA UNITED CO -A 37 52.4 38.0 n.a. 28.3 n.a. n.a. 19.6 22.2 2,360PIGEON CORP 2,814 19.7 16.8 9.5 n.a. 2.1 2.0 11.0 11.9 673KOSE CORP 2,079 20.2 18.4 5.2 4.9 1.2 1.1 6.1 6.5 1,442Simple average 26.6 21.9 13.5 12.3 6.9 5.9 30.0 29.4Weighted average 25.0 21.4 14.9 13.2 11.0 9.7 49.6 49.3

Source: Bloomberg and Danareksa Sekuritas

27

2011 Outlook

Plantation sectorMid-term bullishness

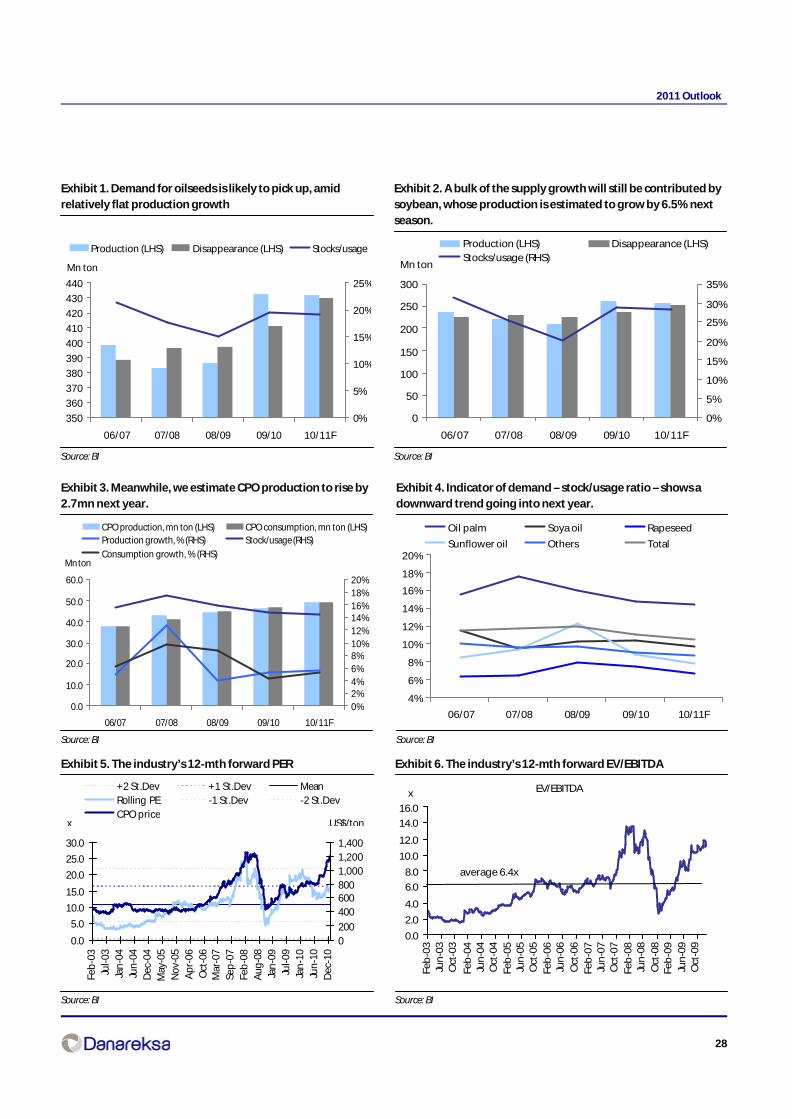

Higher 2011 CPO pricesWe are raising our benchmark CPO price estimate to US$925/ton next year, expecting it to easeto US$870/ton in 2012, buoyed by constrained vegetable oil supply and demand imbalancesamidst a surge in consumption for mandated bio-diesel in Brazil. La Nina still persists in areas ofSouth America, with a plantings slowdown seen in Argentina and Brazil – major producers ofsoybean. Supply constraints are therefore likely to continue, probably until the early part of nextyear, we think. However, the expected subsiding of El Nino, the end of the biological cycle, andthe increase in fertilizer application will likely boost palm oil production, but most likely only inthe second half next year, curbing any further increases in prices. We estimate palm oil productionto increase by 2.7mn tons next year, or higher than this year’s 0.7mn tons increase. Of all plantationstocks under our coverage, our top picks are LSIP and BWPT. Major risks are bad weather and globaleconomic slowdown, led by China and India.

Demand supply imbalancesThe world’s vegetable oil supply is likely to remain constrained, in our view - at least up to the earlypart of next year. Demand shall continue to increase, mainly from higher income and changes indiets in China – despite its intention to curb inflation and India, as well as from mandated bio-diesel in Brazil. We estimate demand for vegetable oil to grow by 4.5% next year, with supply risingonly a mere 3.7%. Much of the supplies are coming from soya oil and palm oil, both growing byaround 8.4% and 6.0% respectively, yet still insufficient to offset the decline in any other vegetableoils. Stock to usage - an indicator of strong demand - will decline in the third consecutive year to11.0%. For now, the risks are in the oilseed production, with the La Nina effect still seen in majorsoybean producers. In effect, such dryness has led to delays in plantings and, in some cases, theyields. As of mid-November, around 7.7mn ha of soybean were planted, down by 9% from a yearago. And in Brazil, only 4.4mn ha was planted, down from 5.1mn ha planted last year. That’s notto mention the potential switch of grain plantings, whose production setback has been severein recent months.

Bio-diesel – small yet great impactWe are not a great fan of bio-diesel, for which consumption of vegetable oils is thought to beimmaterial. However, the rapidly expanding bio-diesel production in Brazil, the 3rd largest worldproducer of soya oil, is likely to reduce the export supply of oils and fats. In fact, it will also increaseimports primarily of palm oil and palm kernel oil to meet demand for food. This year, Brazil’sdomestic consumption of vegetable oil rises by 14.0% YoY, with 28.3% of such demand going intobio-diesel, with the remaining going into food. In any case, exports of soya oil are expected todecline by 15.2% YoY to about 1.2mn tons, creating a decline in the stock to usage of soya oil to10.1% from this year’s 11.6%.

Bonny B. Setiawan, CFA(62-21) 2352 [email protected]

OVERWEIGHT

Jakagri Relative to JCI Index

Rec. TP Mkt. cap PER, x EV/EBITDA, x Current Div yieldRp/share Rp bn 2010E 2011E 2010E 2011E EV/Ha %

US$/ha

AALI HOLD 24,500 36,376 26.1 18.0 15.9 11.1 21,735 2.8LSIP BUY 14,850 15,147 19.4 13.4 11.7 8.4 17,133 2.1SGRO BUY 3,700 5,765 18.8 12.5 10.6 7.7 11,605 2.4BWPT BUY 1,350 4,683 22.3 13.2 13.9 7.6 13,140 0.8

1,000

1,300

1,600

1,900

2,200

2,500

12/1

8/09

2/1

/10

3/10

/10

4/19

/10

5/26

/10

7/2

/10

8/9

/10

9/22

/10

10/2

8/10

12/6

/10

-25

-20

-15

-10

-5

0

5

10

JAKAGRI (LHS) Relative to JCI Index (RHS)%

28

2011 Outlook

Exhibit 1. Demand for oilseeds is likely to pick up, amidrelatively flat production growth

Source: BI

Exhibit 2. A bulk of the supply growth will still be contributed bysoybean, whose production is estimated to grow by 6.5% nextseason.

Source: BI

350

360

370

380

390

400

410

420

430

440

06/07 07/08 08/09 09/10 10/11F

Mn ton

0%

5%

10%

15%

20%

25%

Production (LHS) Disappearance (LHS) Stocks/usage

0

50

100

150

200

250

300

06/07 07/08 08/09 09/10 10/11F

Mn ton

0%

5%

10%

15%

20%

25%

30%

35%

Production (LHS) Disappearance (LHS)Stocks/usage (RHS)

Exhibit 3. Meanwhile, we estimate CPO production to rise by2.7mn next year.

Source: BI

0.0

10.0

20.0

30.0

40.0

50.0

60.0

06/07 07/08 08/09 09/10 10/11F

Mn ton

0%2%4%6%8%10%12%14%16%18%20%

CPO production, mn ton (LHS) CPO consumption, mn ton (LHS)Production growth, % (RHS) Stock/usage (RHS)

Consumption growth, % (RHS)

Exhibit 4. Indicator of demand – stock/usage ratio – shows adownward trend going into next year.

Source: BI

4%

6%

8%

10%

12%

14%

16%

18%

20%

06/07 07/08 08/09 09/10 10/11F

Oil palm Soya oil Rapeseed

Sunflower oil Others Total

Exhibit 5. The industry’s 12-mth forward PER

Source: BI

Exhibit 6. The industry’s 12-mth forward EV/EBITDA

Source: BI

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Feb

-03

Jul-0

3Ja

n-0

4Ju

n-0

4D

ec-0

4M

ay-0

5N

ov-0

5A

pr-

06O

ct-0

6M

ar-0

7Se

p-0

7Fe

b-0

8A

ug-0

8Ja

n-0

9Ju

l-09

Jan

-10

Jun

-10

Dec

-10

0200

4006008001,0001,2001,400

+2 St.Dev +1 St.Dev MeanRolling PE -1 St.Dev -2 St.DevCPO price

x US$/ton

EV/EBITDA

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Feb

-03

Jun

-03

Oct

-03

Feb

-04

Jun

-04

Oct

-04

Feb

-05

Jun

-05

Oct

-05

Feb

-06

Jun

-06

Oct

-06

Feb

-07

Jun

-07

Oct

-07

Feb

-08

Jun

-08

Oct

-08

Feb

-09

Jun

-09

Oct

-09

x

average 6.4x

29

2011 Outlook

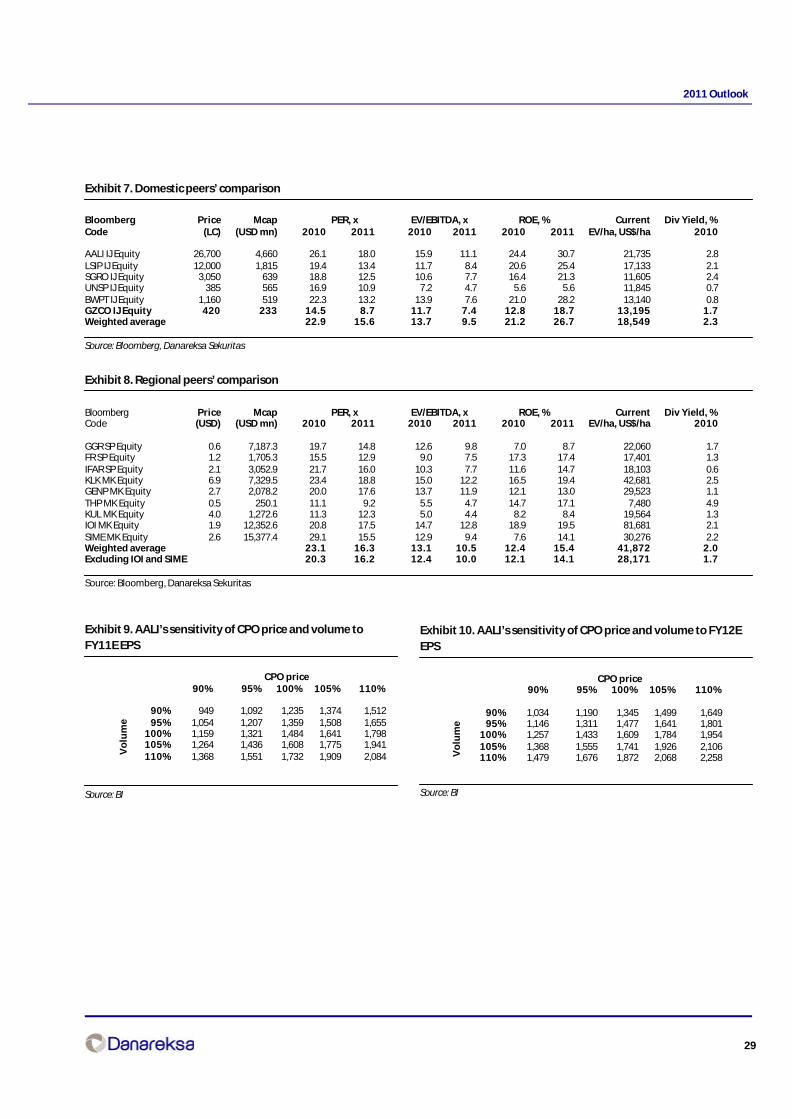

Exhibit 7. Domestic peers’ comparison

Bloomberg Price Mcap PER, x EV/EBITDA, x ROE, % Current Div Yield, %Code (LC) (USD mn) 2010 2011 2010 2011 2010 2011 EV/ha, US$/ha 2010

AALI IJ Equity 26,700 4,660 26.1 18.0 15.9 11.1 24.4 30.7 21,735 2.8LSIP IJ Equity 12,000 1,815 19.4 13.4 11.7 8.4 20.6 25.4 17,133 2.1SGRO IJ Equity 3,050 639 18.8 12.5 10.6 7.7 16.4 21.3 11,605 2.4UNSP IJ Equity 385 565 16.9 10.9 7.2 4.7 5.6 5.6 11,845 0.7BWPT IJ Equity 1,160 519 22.3 13.2 13.9 7.6 21.0 28.2 13,140 0.8GZCO IJ Equity 420 233 14.5 8.7 11.7 7.4 12.8 18.7 13,195 1.7Weighted average 22.9 15.6 13.7 9.5 21.2 26.7 18,549 2.3

Source: Bloomberg, Danareksa Sekuritas

Exhibit 8. Regional peers’ comparison

Bloomberg Price Mcap PER, x EV/EBITDA, x ROE, % Current Div Yield, %Code (USD) (USD mn) 2010 2011 2010 2011 2010 2011 EV/ha, US$/ha 2010

GGR SP Equity 0.6 7,187.3 19.7 14.8 12.6 9.8 7.0 8.7 22,060 1.7FR SP Equity 1.2 1,705.3 15.5 12.9 9.0 7.5 17.3 17.4 17,401 1.3IFAR SP Equity 2.1 3,052.9 21.7 16.0 10.3 7.7 11.6 14.7 18,103 0.6KLK MK Equity 6.9 7,329.5 23.4 18.8 15.0 12.2 16.5 19.4 42,681 2.5GENP MK Equity 2.7 2,078.2 20.0 17.6 13.7 11.9 12.1 13.0 29,523 1.1THP MK Equity 0.5 250.1 11.1 9.2 5.5 4.7 14.7 17.1 7,480 4.9KUL MK Equity 4.0 1,272.6 11.3 12.3 5.0 4.4 8.2 8.4 19,564 1.3IOI MK Equity 1.9 12,352.6 20.8 17.5 14.7 12.8 18.9 19.5 81,681 2.1SIME MK Equity 2.6 15,377.4 29.1 15.5 12.9 9.4 7.6 14.1 30,276 2.2Weighted average 23.1 16.3 13.1 10.5 12.4 15.4 41,872 2.0Excluding IOI and SIME 20.3 16.2 12.4 10.0 12.1 14.1 28,171 1.7

Source: Bloomberg, Danareksa Sekuritas

Exhibit 9. AALI’s sensitivity of CPO price and volume toFY11E EPS

CPO price90% 95% 100% 105% 110%

90% 949 1,092 1,235 1,374 1,51295% 1,054 1,207 1,359 1,508 1,655

100% 1,159 1,321 1,484 1,641 1,798105% 1,264 1,436 1,608 1,775 1,941110% 1,368 1,551 1,732 1,909 2,084

Source: BI

Exhibit 10. AALI’s sensitivity of CPO price and volume to FY12EEPS

CPO price90% 95% 100% 105% 110%

90% 1,034 1,190 1,345 1,499 1,64995% 1,146 1,311 1,477 1,641 1,801

100% 1,257 1,433 1,609 1,784 1,954105% 1,368 1,555 1,741 1,926 2,106110% 1,479 1,676 1,872 2,068 2,258

Source: BI

Vo

lum

e

Vo

lum

e

30

2011 Outlook

Exhibit 11. LSIP’s sensitivity of CPO price and volume toFY11E EPS

CPO price90% 95% 100% 105% 110%

90% 616 680 744 805 86595% 685 754 822 886 950

100% 754 827 899 967 1,034105% 824 900 976 1,048 1,119110% 893 973 1,053 1,129 1,204

Source: BI

Exhibit 12. LSIP’s sensitivity of CPO price and volume to FY12EEPS

CPO price90% 95% 100% 105% 110%

90% 631 700 769 837 90195% 705 778 851 924 992

100% 779 857 934 1,010 1,083105% 853 935 1,016 1,097 1,173110% 927 1,013 1,098 1,183 1,264

Source: BI

Vo

lum

e

Vo

lum

e

Exhibit 13. SGRO’s sensitivity of CPO price and volume toFY11E EPS

CPO price90% 95% 100% 105% 110%

90% 128 149 170 191 21195% 161 184 207 230 252

100% 194 219 244 269 293105% 228 255 282 308 334110% 261 290 319 347 375

Source: BI

Exhibit 14. SGRO’s sensitivity of CPO price and volume to FY12EEPS

CPO price90% 95% 100% 105% 110%

90% 159 184 209 233 25795% 197 224 252 279 305

100% 235 265 294 324 352105% 274 306 337 369 399110% 312 346 380 414 447

Source: BI

Vo

lum

e

Vo

lum

e

Exhibit 15. BWPT’s sensitivity of CPO price and volume toFY11E EPS

CPO price90% 95% 100% 105% 110%

90% 59 66 73 80 8795% 66 73 80 88 95

100% 72 80 88 95 103105% 79 87 95 103 111110% 85 94 102 111 119

Source: BI

Exhibit 16. BWPT’s sensitivity of CPO price and volume to FY12EEPS

CPO price90% 95% 100% 105% 110%

90% 80 89 97 106 11595% 88 97 106 115 124

100% 96 105 115 124 134105% 104 114 124 134 144110% 112 122 132 143 153

Source: BI

Vo

lum

e

Vo

lum

e

31

2011 Outlook

Property sectorMore to come

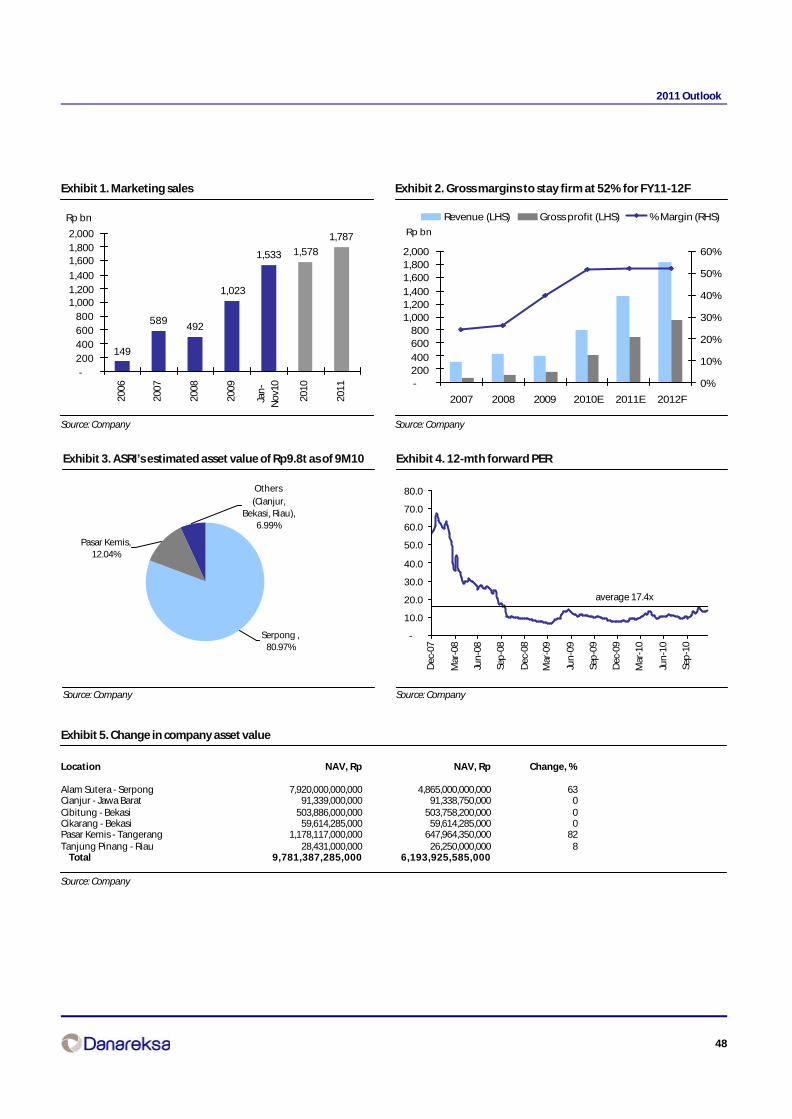

Maintain overweight, top pick ASRIWe believe the bright economic outlook and the growing domestic market will continue to drivedemand for new property projects. Marketing sales of listed property companies within ouruniverse reached Rp 8.4Trn in 3Q10, up 75% YoY from Rp 5Trn in 3Q09. All in all, total 9M10 marketingsales are about 87% of our full year estimate – or broadly inline. Since the majority of the pre-salesstill come from landed residential rather than apartments, we prefer companies with sufficientlandbank located in prime locations, good execution but still attractive valuations – ASRI beingour top pick. The company still has over 1,000Ha of landbank on hand. 48% of it will be ASRI’s futureprojects in Pasar Kemis, a development that will continue the company’s success story inTangerang, where demand for property is expected to be strong from people looking for moreaffordable housing on the fringes of Jakarta. The company’s 9M10 pre-sales surged 108% YoY.The stock currently trades at 13.8-8.7x PER11-12F – lower than the industry average of 20.2-16.8xPER11-12F.

Higher residential demandAnnual demand for housing keeps increasing each year and according to the Indonesian HousingMinistry, housing demand for FY10 might reach 8mn units and is expected to grow by 700,000 unitsper annum. Yet this is no surprise given Indonesia’s huge population of more than 237mn people.More favorable economic conditions and lower mortgage rates also encourage consumers topurchase property, with the Residential Property Purchase Plan Index constructed by DanareksaResearch Institute showing an 80% increase since its bottom in September 2008. Prices also matter,since higher city land prices and land scarcity have created demand for more affordable residentialareas in the suburbs of the Jakarta greater area (Tangerang, Depok, Bogor and Bekasi). As such,we believe profitability for property developers in those areas should be better as Coldwell BankerIndonesia (CBI) predicted land prices to increase by 10% on average compared to prices in the year2010.

Risks to watchBeing an interest rate sensitive sector, the main risk to our projections is rising inflation andtherefore hikes in benchmark interest rates. So far, mortgage loans for the past 10 months havereached Rp 1.2Trn, or up 10% YoY from Rp 1.1Trn in the same period last year. Other risks are potentialeconomic slowdown that curbs consumer purchasing power and significant increases in rawmaterial costs (60% of the total residential building cost is cement). Both of these have an impacton the company’s revenues growth and margins.

Lydia Suwandi(62-21) 350 9888 ext. [email protected]

OVERWEIGHT

Jakprop relative to JCI Index

100

120

140

160

180

4/20

/09

5/18

/09

6/15

/09

7/13

/09

8/10

/09

9/7/

09

10/5

/09

11/2

/09

11/3

0/09

12/2

8/09

1/25

/10

2/22

/10

3/22

/10

4/19

/10

-20

-10

0

10

20

Jakprop Index (LHS) Relative to JCI Index (RHS) %

Price Mkt Cap RNAV/ % disc. PBV,x PER,xRp bn share NAV 10F 11F 10F 11F