cycle-based procedures: order to cash self -study

TRANSCRIPT

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

Cycle-Based Procedures: Order to Cash Self-Study August 2020

For Internal Distribution Only

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

Contents

Cycle-Based Procedures: Order to Cash Self-Study ..................................................................................... 1

Overview ..................................................................................................................................................... 3

Risk Assessment .......................................................................................................................................... 3

Key Considerations .................................................................................................................................. 3

Concepts in Action — ABC Company, Inc. ............................................................................................... 4

Design and Implementation of Relevant Controls, Including General IT Controls ...................................... 5

Key Considerations .................................................................................................................................. 5

Concepts in Action — ABC Company, Inc. ............................................................................................... 5

Analytics ...................................................................................................................................................... 6

Key Considerations .................................................................................................................................. 6

Concepts in Action — ABC Company, Inc. ............................................................................................... 6

Perform Journal Entry Analysis.................................................................................................................... 7

Key Considerations .................................................................................................................................. 7

Concepts in Action — ABC Company, Inc. ............................................................................................... 8

Identification of Risk of Material Misstatements (RoMMs) (Including Related RoMMs) and Substantive Procedures ............................................................................................................................................. 9

Key Considerations .................................................................................................................................. 9

Concepts in Action — ABC Company, Inc. ............................................................................................... 9

Identification of Deliberative Risks (Including Fraud Risks) — RoMMs Not Addressed by Cycle-Based Procedures ........................................................................................................................................... 12

Key Considerations ................................................................................................................................ 12

Concepts in Action — ABC Company, Inc. ............................................................................................. 12

Resources .................................................................................................................................................. 13

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

Overview

Using a simple set of case facts and video demonstrations of firm-issued templates, this self-study resource illustrates how engagement teams may apply the core concepts of accumulating and evaluating audit evidence in connection with planning cycle-based procedures. Specifically, it explores if cycle-based procedures will provide sufficient appropriate audit evidence to address more than one risk of material misstatement (RoMM) within the order-to-cash cycle for example entity ABC Company, Inc. (“ABC Co.”).

The Audit Evidence Guide provides core concepts for accumulating and evaluating audit evidence, including performing cycle-based procedures.

Our evaluation of the audit evidence from the following procedures is particularly important when determining whether cycle-based procedures are appropriate to thoughtfully design substantive procedures that could address one or more significant accounts and related RoMMs:

• Risk assessment procedures;

• The design and implementation of relevant controls;

• Analytical procedures;

• Journal entry analysis; and

• Identification of deliberative risks (including fraud risks).

The self-study resource will highlight key considerations for each of the categories above and provide practical application examples, including how to leverage the available resources.

It is important to remember that auditing is an iterative process; accordingly, the procedures may not necessarily be performed sequentially, and the considerations outlined within this self-study may be performed in combination. Engagement teams may reference Chapter 5 of the Audit Evidence Guide when designing their cycle-based procedures.

Risk Assessment

Key Considerations

Performing risk assessment procedures to obtain an adequate understanding of the entity’s processes and significant transaction cycles is typically the first step to determine whether cycle-based procedures may be an appropriate audit response to an identified RoMM. By understanding the entity’s process for recording transactions, we can determine whether there are certain transaction cycles, or transaction types within a cycle, that would allow for the use of procedures to address multiple significant accounts and related RoMMs. Often, prescriptive processes, and therefore prescriptive RoMMs and related assertions, identified through these risk assessment procedures would be those best suited for cycle-based procedures. However, there may be situations that could invalidate using a cycle-based procedure approach and/or circumstances that are indicative of deliberative RoMMs.

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

Concepts in Action — ABC Company, Inc.

ABC Co. is a manufacturer and wholesale distributor of nonalcoholic beverages. For all its products, the entity purchases the raw materials, mixes the ingredients, cans or bottles the beverages, packages them, and sells them to its customers. The entity also manufactures and distributes custom beverages (health drinks) based on customer specifications.

The entity recognizes revenue when control is transferred to customer, which generally occurs upon shipment of the finished product as customers consist primarily of big box retailers, grocery store chains, convenience stores, and restaurants and have a history of timely payments. Revenue is recorded at the net sales price, including estimates for variable consideration for which reserves are established. Variable considerations include provisions for customer volume rebates and product returns and are recorded as a reduction of revenue in the same period the related sales are recorded. Such variable consideration is based on historical experience, understanding of the market and customers, and expectations regarding future trends. Sales, cost of sales, and gross margin percentages have been, and are expected to be, relatively consistent from year to year.

Accounts receivable are recorded when the right to consideration becomes unconditional, typically upon shipment of finished product. Payments received from customers are generally based upon payment terms of 0.5 percent 10, net 30 days. The engagement team has evaluated the appropriateness of the entity’s revenue recognition policy and determined it is appropriate.

Based on inquiries and review of process narratives, the ABC Co. engagement team obtained an understanding of the revenue process as summarized below:

• Upon product leaving the warehouse, the inventory is scanned. Information about inventory shipped is then electronically transferred to the entity’s enterprise resource planning (ERP) system.

• The ERP system then automatically records both of the following related to the delivered products:

– Credit to revenue and debit to accounts receivable

– Debit to cost of sales and credit to inventory.

• Similarly, when there are returns associated with the product, once the product is received, the ERP system automatically records the following:

– Debit customer returns (contra revenue) and credit accounts receivable customer returns (contra accounts receivable).

– Debit inventory and credit cost of sales.

• A majority of the revenue transactions are processed through the ERP system. The entity also processes batch entries in addition to manual entries to record customer volume rebates (promotional allowances). Quarterly, the entity performs a separate analysis to reflect any changes to estimates (variable consideration) for reporting purposes.

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

• The entity performs a full physical inventory count annually.

• There are no customer disputes or pricing errors.

Design and Implementation of Relevant Controls, Including General IT Controls

Key Considerations

Our understanding of business processes and relevant controls provides the basis for the identification and assessment of RoMMs and enables us to identify and understand all significant transaction types affecting the significant accounts for which we are considering cycle-based procedures. Note that existence of a deficiency in the design, implementation, or operating effectiveness of one or more controls informs our risk assessment but does not necessarily mean that the use of evidence across accounts and assertions within a cycle is not appropriate.

Concepts in Action — ABC Company, Inc.

As part of obtaining an understanding of the revenue process and relevant controls to support their risk assessment, the ABC Co. engagement team performed the following walkthroughs and design and implementation procedures for relevant controls related to revenue:

• Management review of monthly financial reporting package including budget-to-actual and current-year-to-prior-year variance analysis;

• Reconciliation of subsidiary sales records to general ledger balances;

• Approval of pricing information within the ERP system;

• Review of reports reconciling all inventory shipped to billings issued on a daily basis;

• Reconciliation of the promotional allowance (rebates) accrual to the general ledger and the review of the mathematical accuracy of the underlying calculation; and

• Review of the completeness of the promotional allowance (rebates) accrual by verifying all promotional agreements are appropriately considered in the promotional allowance accrual.

In addition, the ABC Co. engagement team performed the following walkthroughs and design and implementation procedures for relevant controls related to accounts receivable and inventory processes because these represent related accounts to revenue:

• Reconciliation of accounts receivable from the accounts receivable aging to the general ledger.

• Review of the allowance for doubtful accounts calculation.

• Review and approval of the issuance of credit memos.

• Physical inventory is counted periodically, and discrepancies are investigated and corrected

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

within the inventory records. Inventory records based on the physical inventory are reconciled to the general ledger, with any differences being recorded as a book-to-physical inventory adjustment.

• Reconciliation of perpetual inventory records to the general ledger balances.

In addition, with the assistance of an IT specialist, the ABC Co, engagement team gained an understanding of the overall IT environment and tested the design and implementation of relevant general IT controls. This included testing the design and implementation of relevant general IT controls for the ERP system, as well as the related IT infrastructure that supports the ERP system and the automated control that results in the recording of cost of sales concurrently with the recording of revenue.

Analytics

Key Considerations

Analytics, including preliminary analytical procedures and the analytics described in the Guided Risk Assessments (GRAs), can produce important audit evidence to support our risk assessment conclusions and help us conclude whether cycle-based procedures will be appropriate. Additional analytics can provide further risk assessment evidence that the engagement team may consider in determining the appropriateness of cycle-based procedures. These analytics may focus on the relationships between significant accounts within a transaction cycle.

The nature and extent of the analytics deemed necessary to perform as part of our risk assessment procedures are matters of professional judgment and will depend on a variety of factors.

Concepts in Action — ABC Company, Inc.

The ABC Co. engagement team completed the risk factor questionnaires available within the GRA for revenue and accounts receivable and performed the suggested analytics as part of the process. Further, based on professional judgement, the ABC Co. engagement team performed additional analytics to determine the appropriateness of cycle-based procedures. One of various analytics performed by the ABC Co. engagement team is illustrated below. The purpose of this analysis — from a cycle-based testing perspective — was to help the ABC Co. engagement team enhance its understanding of the expected relationship between the related accounts and provide additional evidence as part of risk assessment to plan and perform cycle-based procedures.

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

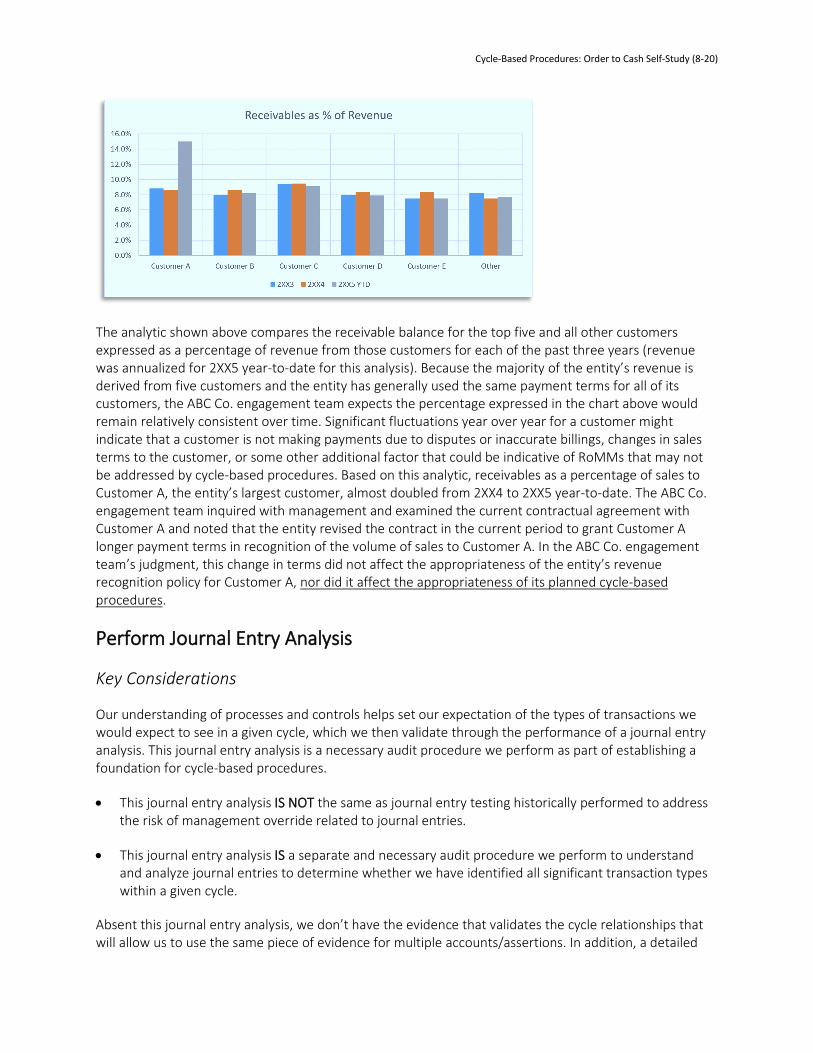

The analytic shown above compares the receivable balance for the top five and all other customers expressed as a percentage of revenue from those customers for each of the past three years (revenue was annualized for 2XX5 year-to-date for this analysis). Because the majority of the entity’s revenue is derived from five customers and the entity has generally used the same payment terms for all of its customers, the ABC Co. engagement team expects the percentage expressed in the chart above would remain relatively consistent over time. Significant fluctuations year over year for a customer might indicate that a customer is not making payments due to disputes or inaccurate billings, changes in sales terms to the customer, or some other additional factor that could be indicative of RoMMs that may not be addressed by cycle-based procedures. Based on this analytic, receivables as a percentage of sales to Customer A, the entity’s largest customer, almost doubled from 2XX4 to 2XX5 year-to-date. The ABC Co. engagement team inquired with management and examined the current contractual agreement with Customer A and noted that the entity revised the contract in the current period to grant Customer A longer payment terms in recognition of the volume of sales to Customer A. In the ABC Co. engagement team’s judgment, this change in terms did not affect the appropriateness of the entity’s revenue recognition policy for Customer A, nor did it affect the appropriateness of its planned cycle-based procedures.

Perform Journal Entry Analysis

Key Considerations

Our understanding of processes and controls helps set our expectation of the types of transactions we would expect to see in a given cycle, which we then validate through the performance of a journal entry analysis. This journal entry analysis is a necessary audit procedure we perform as part of establishing a foundation for cycle-based procedures.

• This journal entry analysis IS NOT the same as journal entry testing historically performed to address the risk of management override related to journal entries.

• This journal entry analysis IS a separate and necessary audit procedure we perform to understand and analyze journal entries to determine whether we have identified all significant transaction types within a given cycle.

Absent this journal entry analysis, we don’t have the evidence that validates the cycle relationships that will allow us to use the same piece of evidence for multiple accounts/assertions. In addition, a detailed

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

analysis of journal entries is a powerful procedure that not only produces audit evidence that validates our original expectations of relationships but provides insights into potential risks related to transaction types that we did not originally expect.

Our Deloitte Way of establishing a cycle-based foundation suggests that we perform the preliminary journal entry analysis early in the audit process during our risk assessment procedures to establish a foundation to support the design of our substantive response to our identified RoMMs.

For public registrants, we recommend engagement teams consider performing the journal entry analysis quarterly as a step toward continuous auditing and an opportunity to identify unexpected relationships and transaction types early in the audit process and design further substantive procedures as deemed necessary.

At year-end, we again obtain the journal entries forming the complete population of transaction types that make up an account balance and reconcile it to the general ledger. This separate journal entry analysis at year-end helps us determine, using a complete set of journal entry data, if we have accumulated audit evidence that supports the relationships between the related accounts. It also may provide us with incremental insight into anything unusual that may have occurred during the period between the initial evaluation of the journal entries and year-end.

Concepts in Action — ABC Company, Inc.

Based on the risk assessment procedures outlined above, the ABC Co. engagement team identified transaction types impacting revenue. To perform the journal entry analysis and determine the appropriate tool, the ABC Co. engagement team first reviewed the Workflow for Journal Entry Analysis When Applying Cycle-Based Testing Approach template. Based on the considerations documented within the Workflow for Journal Entry Analysis When Applying Cycle-Based Testing Approach template and depending upon the size and complexity of the data, the ABC Co. engagement team determined the Cycle-Based Journal Entry Automation (Self-Service) Template was most appropriate for the journal entry analysis . The team then performed a preliminary analysis of ABC Co.’s entire journal entry population as of an interim date to determine if they had appropriately identified all transaction types for revenue balances.

Watch the “Workflow for JE Analysis” on-screen demonstration located within THIS video.

This demonstration illustrates how the ABC Co. engagement team used the Workflow for Journal Entry Analysis when Applying Cycle-Based Testing Approach template to streamline the journal entry data request process and determined the most appropriate tool/template to perform the preliminary journal entry analysis.

Watch the “Preliminary JE Analysis” on-screen demonstration located within THIS video.

The ABC Co. engagement team determined it was most appropriate to use the Cycle-Based Journal Entry Automation (Self-Service) Template to perform the preliminary journal entry analysis. This demonstration illustrates how the ABC Co. engagement team used the Cycle-Based Journal Entry Automation (Self-Service) Template to perform the preliminary journal entry analysis.

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

Identification of Risk of Material Misstatements (RoMMs) (Including Related RoMMs) and Substantive Procedures

Key Considerations

As a result of our risk assessment procedures as described above, including understanding of process and controls and preliminary journal entry analysis, we identify and assess RoMMs within our GRAs. Once we have identified and assessed RoMMs, we again leverage our understanding from the preliminary journal entry analysis of the significant transaction types and related accounts to determine if cycle-based procedures will address RoMMs for one significant account within the transaction cycle while ALSO providing audit evidence for RoMMs for related account(s). Our documentation is to clearly describe how (specifically) carefully and thoughtfully designed planned substantive procedures will address the intended RoMMs for the significant and related account(s), if applicable.

Concepts in Action — ABC Company, Inc.

Once the ABC Co. engagement team had accumulated audit evidence about the significant account relationships within the revenue transaction cycle by performing preliminary journal entry analysis and based on completion of all the tailoring and risk assessment questions within the GRAs, the ABC Co. engagement team identified applicable RoMMs and relevant controls for revenue and considered if (and how) substantive procedures performed for one or more related RoMMs for accounts receivable and inventory provide audit evidence to address one or more RoMMs for revenue.

Revenue and Accounts Receivable: Considering revenue and accounts receivable, let us see how the ABC Co. engagement team concluded that the related significant accounts/assertions are appropriate:

Risks of Material Misstatement Related Significant Accounts Assertions

Revenue recorded does not represent actual transactions that occurred.

• Revenue.

• Accounts receivable.

• Occurrence.

• Existence.

Revenue is recorded at incorrect transaction amount.

• Revenue.

• Accounts receivable.

• Accuracy.

• Valuation and allocation.

As part of designing substantive procedures, the ABC Co. engagement team considered how the planned substantive procedures would address the intended revenue and accounts receivable RoMMs:

• Because the entity’s revenue arrangements involve a single performance obligation, the entity appropriately recognizes revenue when the product is shipped. Because customers would not be expected to pay for products they do not receive, the collection of billed revenues constitutes evidence of the occurrence of that revenue. Similarly, the entity has a simple pricing structure, and there is no history of significant pricing disputes with customers nor issuances of customer

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

credits as a result of incorrect pricing. As a result, collection of billed revenues also provides evidence with respect to the accuracy of revenue recognized.

• Based on the above, the ABC Co. engagement team concluded that if material amounts of revenue were erroneously recognized either because customers were billed for shipments that did not occur or because customers were billed an overstated amount, customers would not pay the related invoices. As a result, the amounts related to overstated revenues would remain in accounts receivable at year-end and be subject to the ABC Co. engagement team’s year-end accounts receivable procedures or such amounts would be written-off during the year. The ABC Co. engagement team concluded that its planned substantive procedures to test the existence, valuation, and allocation of accounts receivable would provide sufficient appropriate audit evidence with respect to RoMMs related to the occurrence and accuracy of revenue, respectively: “Revenue is recorded at incorrect transaction amount” and “Revenue does not represent actual transactions that occurred.”

• Important to this conclusion is that (1) when revenues are recorded, accounts receivable are also recorded and (2) reductions to accounts receivable recorded during the year result from one of the following: the receivable is collected in cash or removed via a credit memo. Based on the ABC Co. engagement team’s risk assessment procedures performed during the year, the ABC Co. engagement team determined it has sufficient evidence that receivables are reduced as previously described. Such determination was not merely based on understanding of the process; however, the ABC Co. engagement team performed a detailed journal entry analysis on accounts receivable and demonstrated understanding of the entire transaction cycle from initiation of sale through cash collection. Also, note this conclusion does not contemplate intentionally erroneous reductions to accounts receivable where the offsetting debit is recorded to an account other than cash, revenue (as is the case for credit memos), or to the allowance for doubtful accounts.

Note: If the engagement team had identified a RoMM related to intentional erroneous reductions of accounts receivable, that RoMM would be a fraud risk and therefore a significant risk for which the engagement team would perform specifically responsive procedures.

• Finally, the ABC Co. engagement team considered the possibility that revenues are inaccurately recorded as a result of accuracy errors that understate revenue. The ABC Co. engagement team noted that customers may be less likely to notify the entity with respect to the under billing of revenue. The ABC Co. engagement team determined that based on the risk assessment procedures performed (e.g., preliminary analytical procedures and inquiry of management) there was no indication that unintentional accuracy errors resulting in understatement of revenue were any more likely than unintentional accuracy errors resulting in overstatement of revenue. Further, in light of the simple pricing structure of the entity and the absence of customer disputes and pricing errors noted through risk assessment procedures, the ABC Co. engagement team concluded that its procedures to test the existence, valuation, and allocation of accounts receivable would also be sufficient to address potential understatement of revenue resulting from inaccurate recording of revenue.

• Based on considerations summarized above, the ABC Co. engagement team appropriately concluded that its planned audit procedures to address the RoMM relating to existence, valuation, and allocation of accounts receivables would provide sufficient appropriate audit evidence with respect to the RoMM relating to occurrence and accuracy of revenue.

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

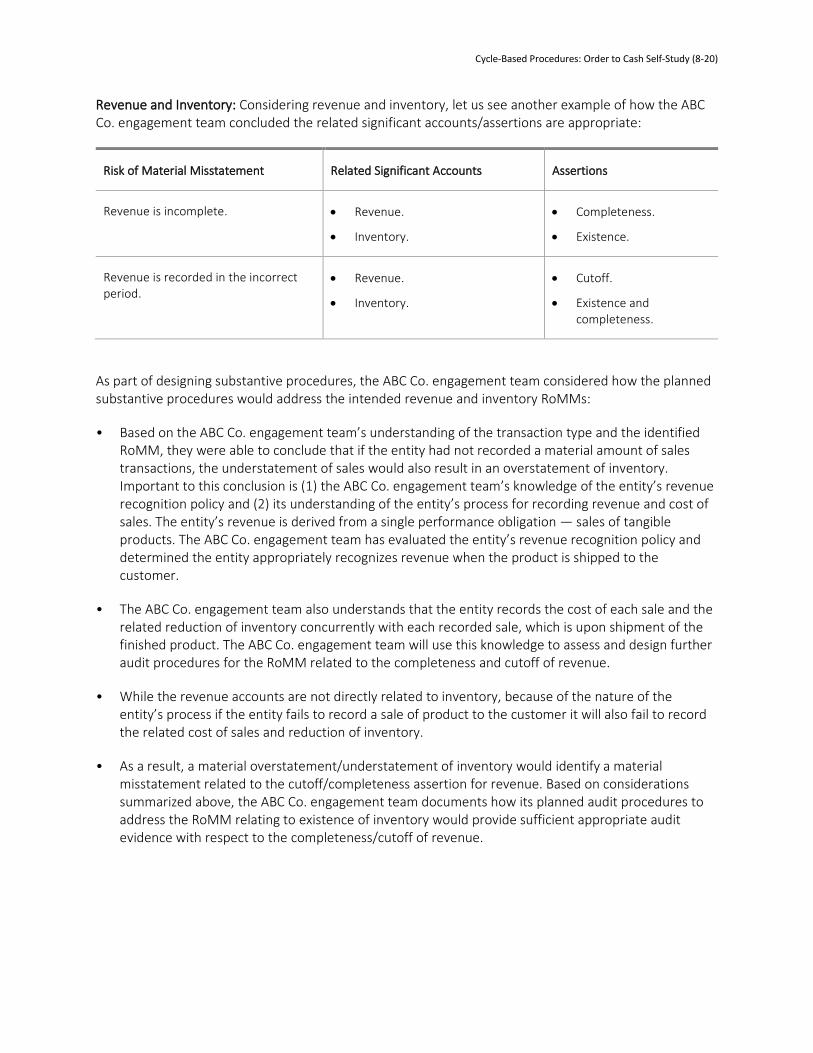

Revenue and Inventory: Considering revenue and inventory, let us see another example of how the ABC Co. engagement team concluded the related significant accounts/assertions are appropriate:

Risk of Material Misstatement Related Significant Accounts Assertions

Revenue is incomplete. • Revenue.

• Inventory.

• Completeness.

• Existence.

Revenue is recorded in the incorrect period.

• Revenue.

• Inventory.

• Cutoff.

• Existence and completeness.

As part of designing substantive procedures, the ABC Co. engagement team considered how the planned substantive procedures would address the intended revenue and inventory RoMMs:

• Based on the ABC Co. engagement team’s understanding of the transaction type and the identified RoMM, they were able to conclude that if the entity had not recorded a material amount of sales transactions, the understatement of sales would also result in an overstatement of inventory. Important to this conclusion is (1) the ABC Co. engagement team’s knowledge of the entity’s revenue recognition policy and (2) its understanding of the entity’s process for recording revenue and cost of sales. The entity’s revenue is derived from a single performance obligation — sales of tangible products. The ABC Co. engagement team has evaluated the entity’s revenue recognition policy and determined the entity appropriately recognizes revenue when the product is shipped to the customer.

• The ABC Co. engagement team also understands that the entity records the cost of each sale and the related reduction of inventory concurrently with each recorded sale, which is upon shipment of the finished product. The ABC Co. engagement team will use this knowledge to assess and design further audit procedures for the RoMM related to the completeness and cutoff of revenue.

• While the revenue accounts are not directly related to inventory, because of the nature of the entity’s process if the entity fails to record a sale of product to the customer it will also fail to record the related cost of sales and reduction of inventory.

• As a result, a material overstatement/understatement of inventory would identify a material misstatement related to the cutoff/completeness assertion for revenue. Based on considerations summarized above, the ABC Co. engagement team documents how its planned audit procedures to address the RoMM relating to existence of inventory would provide sufficient appropriate audit evidence with respect to the completeness/cutoff of revenue.

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

Watch the “Cycle-Based Testing Analysis” demonstration located within THIS video.

• This demonstration shows how the ABC Co. engagement team used the Cycle-Based Testing Analysis Template to document how its substantive procedures address each of the related significant accounts and assertions.

• In addition, this demonstration shows how the ABC Co. engagement team used cycle-based specific substantive templates (including the Accounts Receivable Confirmation Supporting Cycle-Based Testing of Revenue Template and the Accounts Receivable — Cycle-Based Combined Substantive Testing Template) for documenting evidence when they applied cycle-based procedures.

Watch the “GRA — Selecting Cycle-Based Procedures” demonstration located within THIS video.

This demonstration shows how the ABC Co. engagement team selected substantive procedures within the applicable GRA after finalizing the Cycle-Based Testing Analysis Template.

Identification of Deliberative Risks (Including Fraud Risks) — RoMMs Not Addressed by Cycle-Based Procedures

Key Considerations

If we have identified a deliberative RoMM (including fraud/significant risk), we design substantive procedures that are typically tailored to address the RoMM. In these circumstances, the audit evidence accumulated from cycle-based procedures would generally not result in sufficient appropriate evidence to fully address the RoMM identified. This is due to the tailored nature of the deliberative RoMM, which then needs a corresponding tailored substantive response.

Further, classification RoMMs (both prescriptive or deliberative) are typically not fully addressed by cycle-based procedures or supported solely by cycle-based evidence.

Concepts in Action — ABC Company, Inc.

At year-end, the ABC Co. engagement team again obtained the journal entries forming the complete population of transaction types that make up an account balance and reconciled it to the general ledger. Based on the analysis, the ABC Co. engagement team, using a complete set of journal entry data, accumulated audit evidence that supports the relationships between the related accounts and also gained incremental insight into anything unusual that may have occurred during the period between the initial evaluation of the journal entries and year-end.

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

Watch the “Year-End JE Analysis” demonstration located within THIS video.

• This demonstration illustrates how the ABC Co. engagement team used the Cycle-Based Journal Entry Automation (Self-Service) Template to perform the year-end journal entry analysis and

• In addition, this demonstration illustrates how this analysis led to the identification of a transaction type that then led the ABC Co. engagement team to identify a deliberative risk.

Watch the “JE Analysis Documentation” demonstration located within THIS video.

This demonstration illustrates how the ABC Co. engagement team used the Cycle-Based Journal Entry Automation (Self-Service) Template — Example to document the year-end journal entry analysis performed, including cross-referencing to testing workpapers and completing the tie out and other tabs in their entirety.

Resources

• Audit Evidence Guide

• Cycle-Based Testing Analysis Template.

• Cycle-Based Journal Entry Automation (Self-Service) Template.

• Cycle-Based Journal Entry Automation (Self-Service) Template Tutorial.

• Spotlight.

• Video learning module for Cycle-Based Functionality in Spotlight.

• Cycle-Based Journal Entry Automation (Self-Service) Template — Example.

• Cycle-Based Journal Entry Analysis (Manual) Template.

• FAQs Related to Journal Entry Analysis for Cycle-Based Testing Approach.

• Journal Entry Client Data Request Overview.

• Workflow for Journal Entry Analysis When Applying Cycle-Based Testing Approach.

Substantive Templates by Topic

Accounts Payable

• Accounts Payable — Cycle-Based — Combined Substantive Testing Template.

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

Accounts Receivable

• Accounts Receivable Confirmation Supporting Cycle-Based Testing of Revenue — Template.

• Accounts Receivable — Cycle-Based Combined Substantive Testing Template.

Inventory

• Inventory — Cycle-Based — Goods-in-Transit Template.

• Inventory — Cycle-Based — Actual Cost Testing — Cost Element — Test of Details Testing Template.

• Inventory — Cycle-Based — Actual Cost — Per Unit — Test of Details Template.

• Inventory — Cycle-Based — Physical Inventory Count Planning and Summary Template.

• Inventory — Cycle-Based — Physical Inventory Count Rollforward — Test of Details Testing Template.

• Inventory — Cycle-Based — Physical Inventory Count Testing Template.

• Inventory — Cycle-Based — Standard Cost — Cost Element — Test of Details Testing Template.

• Inventory — Cycle-Based — Standard Cost Testing — Per Unit — Test of Details Testing Template.

• Inventory — Cycle-Based — Third-Party Confirmation Testing.

Cycle-Based Procedures: Order to Cash Self-Study (8-20)

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. In the United States, Deloitte refers to one or more of the US member firms of DTTL, their related entities that operate using the “Deloitte” name in the United States and their respective affiliates. Certain services may not be available to attest clients under the rules and regulations of public accounting. Please see www.deloitte.com/about to learn more about our global network of member firms. Copyright © 2020 Deloitte Development LLC. All rights reserved.