customer loyalty and its antecedents in...

TRANSCRIPT

303

CHAPTER 7

CUSTOMER LOYALTY AND ITS

ANTECEDENTS IN COOPERATIVES

Under the current liberalisation, privatisation, and globalisation era in

India the central government has encouraged the private sector to enter

housing finance market. More and more private sector housing finance

companies and banks have emerged in the scene with their state-of-the art

technology and highly personalised services and products. The competition

has become fierce. This increased competition has posed the biggest

challenge to PHCs which are the important source of housing finance to the

weaker sections and low income groups in rural areas. In the context of these

developments in the housing finance market the PHCs are forced to reinvent

their competitive advantages vis-à-vis private housing finance companies and

commercial banks. They recognise the inherent characteristic of a co-

operative (co-operative identity) as a platform to build member loyalty. There

are striking similarities between the bases of loyalty and co-operative identity.

Like co-operative identity customer satisfaction is linked with loyalty.

Customer satisfaction serves as antidote for customer defection. Hence there

is a strong need for PHCs to focus on gaining and sustaining member loyalty.

The objective of this chapter is to propose and to examine empirically

a model that considers cooperative identity, service quality, customer

satisfaction and switching costs as antecedents of customer loyalty in PHCs.

The rest of this chapter is organized as follows. The first section shows the

conceptual model and research hypotheses that test the relationship between

service quality and customer satisfaction, service quality and customer

loyalty, customer satisfaction and customer loyalty, co-operative identity and

customer loyalty and switching costs and customer loyalty. Section two

304

describes measurement and measures of the constructs. While the Section

three analyses the empirical data on customer loyalty and its antecedents in

PHCs the Section four tests the hypotheses.

7.1 Conceptual model and hypothesis development

Figure 7.1 presents the customer loyalty model in co-operative

organizations which identifies the key constructs included in the study. The

hypothesized model shows loyalty as anteceded by co-operative identity,

service quality, satisfaction and switching costs. The proposed model analyses

the effects of co-operative identity, service quality, customer satisfaction and

switching costs on customer loyalty in the primary housing co-operatives.

The present study focuses on the proposal that framework of loyalty

and its antecedents shown in Fig. 7.1 are the drivers of customer loyalty in

housing finance co-operatives. The rationale for the proposed conceptual

model is drawn, in part, from the theories and findings in earlier studies (e.g.

Cronin et al. 2000; Anderson and Mittal, 2000; Oliver, 1997; Cronin and

Taylor, 1992; Parasuraman et al. 1994). The rationale for the relationship

between the constructs and proposed hypotheses are outlined below.

Figure 7.1: Conceptual Model

Co-operative Identity

Switching

Costs

Customer Satisfaction

Customer Loyalty

305

7.1.1The relationship between Service Quality and Customer Satisfaction

“Perhaps the most intriguing issue facing service marketers today is the

interplay between quality, satisfaction, and value. Specifically, which are

antecedents, which are mediating and which are consequent? To date, no

definitive answer exists” (Rust and Oliver, 1994). Taylor and Baker (1994)

have observed “our understanding of the specific nature of the relationship

between service quality and customer satisfaction, as well as how these two

constructs combine to impact consumer purchase intentions, continues to

perplex marketing scholars”. Rust and Oliver’s call for research into

interrelationships did not go unanswered. Later, several studies have

examined the “antecedent, mediating and consequent” relationships among

these three variables (e.g. Fornell et al., 1996; Zeithaml, Berry and

Parasuraman, 1996; Hallowell, 1996; Spreng, Mackenzie and Olshavsky,

1996). The result is that at least partial consensus has emerged.

Perceived service quality is believed to precede satisfaction, which in

turn precedes customer loyalty. Service quality is considered to be an

important factor in enhancing customer satisfaction and loyalty in a financial

service organisation. When the PHC provides high quality services to its

customers, the customers become satisfied which leads to customer being

loyal to PHC. Thus service quality and customer satisfaction are antecedents

of customer loyalty in PHCs. The investigation into the relationship between

service quality and its consequences including customer satisfaction may

provide a strong ground for further research on service quality (Zeithaml,

Berry and Parasuraman, 1996). This leads to suggest the following

hypotheses.

H1a: Service quality is positively related to customer satisfaction.

H1b: Service quality is positively related to customer loyalty.

306

7.1.2The relationship between customer satisfaction and customer loyalty

The link between customer satisfaction and customer loyalty has

gained much attention in the service marketing literature. Many researchers,

based on empirical evidence, propose that higher satisfaction levels lead to

higher purchase intentions (Anderson and Sullivan, 1993; Zeithaml, Berry

and Parasuraman, 1996). Satisfied customers are often willing to pay more

and stay with a firm that meets their needs rather than take the risk associated

with lower-priced service (Hoffman and Bateson, 1997). Bolton (1998)

affirms that satisfied customers stay longer with the service provider.

Cronin, Brady and Hult (2000) found considerable evidence linking

satisfaction to customer’s behavioural intentions. The two items they used to

measure behavioural intentions included (1) repurchase intentions and (2)

intentions to stay with the same service provider. Thus, in effect, these

intentions lead to customer loyalty. Customer satisfaction functions as an

antecedent of customer loyalty. It prevents customer churn and consolidates

retention, thereby constituting an important cause of customer loyalty

(Fornell, 1992; Reichheld, 1996). As a result, organizations strive to enhance

customer loyalty by increasing the level of customer satisfaction. Other

researchers, however, observed that satisfied customers may not be sufficient

to create loyal customers (Cronin and Taylor, 1992; Fornell, 1992). Their

observations are consistent with the notion that customer satisfaction is not a

surrogate for customer retention or customer loyalty (Reicheld, 1993).

Primary housing co-operative customers may be considered loyal to

their co-operative if they hold favourable attitude towards it. Positive attitudes

could manifest itself in a number of ways, e.g. as recommendations of the

company to others (Zeithaml et al., 1996; Parasuraman et al., 1994; Butcher et

al., 2001), a low sensitivity to price increases (Zeithaml et al., 1996;

Parasuraman et al., 1994), preferences for a particular provider (Zeithaml et

307

al., 1996; Butcher et al., 2001), and a high resistance to the change of the

service provider (Parasuraman et al.,1994; Zeithaml et al.,1996; Butcher et al.,

2001). Nevertheless customer satisfaction is an important factor which leads

to customer loyalty, its relationship with loyalty is inconsistent. Thus, the

present study advances the following hypothesis.

H2: Customer satisfaction is positively related to customer loyalty.

7.1.3 The relationship between co-operative identity and customer loyalty

Co-operative identity is considered as an inherent characteristic of any

co-operative organization. When a group of people decide to set up a co-

operative organization it should adhere to co-operative principles and respect

co-operative values of the International Co-operative Alliance (1995). All the

principles and values contribute to enhance commitment level of members

(Morales, 1996). The double role of member-customer in a co-operative leads

to an increase in commitment by the people involved in building the

organisation. A positive relationship exists between participation and the level

of satisfaction and commitment on the part of the members (Locke and

Schwiger, 1979; Schwiger and Leana, 1986). Although the degree of loyalty

of the member-customer is not the same for every co-operative, it is generally

agreed that organizations that have a higher degree of commitment on the

part of members or customers due to co-operative principles and values,

generate a higher level of loyalty. This reasoning leads to suggest the

following hypothesis.

H3: Co-operative identity is positively related to customer loyalty.

7.1.4 The relationship between switching costs and customer loyalty

Switching cost are those costs which are associated with changing

from one service provider to another (Guiltinan, 1989; Zeithaml, 1981).

308

Switching costs include investments of time, money, or effort, perceived by

customers as factors that make it difficult to purchase from a different firm

(Guiltinan, 1989). Switching costs may enhance customer loyalty by making

it difficult for the customer to switch to another provider. This may lead to a

positive relationship between switching costs and customer loyalty.

According to Gronhang and Gilly (1991) dissatisfied customer may remain

loyal because of high switching costs. The perception of switching costs is

considered a significant factor affecting customer loyalty (Andreasen, 1985;

Storbacka et al., 1994; Sharma and Patterson, 2000). Dissatisfied customers

stay with their co-operatives because time, money and effort involved in

choosing a new housing finance agency are perceived high. Hence the

following hypothesis is proposed.

H4: Switching costs are positively related to customer loyalty.

7.2 Measurement

Scale development was based on a review of relevant literature.

Service quality was operationalised using the SERVPERF model because of

its superiority over SERVQUAL. SERVPERF scale performs better when

measuring service quality directly than estimating it as the result of the gap

between expectations and perceptions (Cronin and Taylor, 1992; Teas, 1993;

Brady, Cronin and Brand, 2002; Carman, 1990). As to the nature of

measurement, the method used in the present study was similar to that of

Cronin et al. (2000). Minor alterations in the form of re-classification and re-

phrasing were made to this measurement to meet the specific requirements of

the present research. Various dimensions of service quality were measured by

nine point Likert-type agreement scales with anchors of “strongly disagree”

(1) and “strongly agree” (9).

309

Even though the satisfaction with a service provider is perceived as

being both an evaluative and emotion based response to a service encounter

(Olive, 1997), the study used evaluative set of measurements of customer

satisfaction and measured the satisfaction construct by three items (Cronin

and Taylor, 1992; Cronin, Brady and Hult, 2000). The scoring format for the

first two questions of customer satisfaction construct was a 9 point Likert-

type agreement scales with anchors “strongly disagree” (1) and “strongly

agree” (9), where as the third question was of a nine point Likert-type format

with anchors of “not at all dissatisfied” (1) and “very much satisfied” (9).

Co-operative identity of a co-operative organisation emanates from co-

operative principles and values. Therefore cooperative identity was measured

using two items construct on a nine point Likert-type scale. Switching costs

include investments of time, money, or effort perceived by customers as

factors that make it difficult to change from one service provider to another

(Guiltinan, 1989). Thus a three items switching costs construct was developed

to assess the switching costs based on the customers’ perception of cost, time

and effort associated with changing primary housing co-operatives.

A three items customer loyalty construct was developed to gauge the

range of customers’ behavioural consequences to service quality, cooperative

identity, customer satisfaction and switching costs. Customer loyalty was

assessed by multi-dimensional scale measuring the behavioural and attitudinal

dimensions of the construct on nine point Likert scale (e.g. Zeithaml et al.,

1996; Nguyen and Blanc, 1998; Oliver, 1999). Agreement scale of the

constructs cooperative identity, switching costs and customer loyalty were

anchored by “strongly disagree” (1) and “strongly agree” (9). Constructs and

indicators are presented in Table 7.1.

310

Table 7.1

Measurement Scales of Constructs

Q. No. Cooperative identity measures

1 My society adheres to the cooperative principles.

2 My society respects cooperative values.

Service quality measures

3 Employees of the society provide service reliably, consistently and dependably.

4 Employees of the society are willing and able to provide service in a timely manner.

5 Employees of the society are competent (i.e. knowledgeable and skillful).

6 Employees of the society are approachable and easy to contact.

7 Employees of the society are courteous, polite and respectful.

8 Employees of the society listen to me and speak in a language that I can understand.

9 Employees of the society are trustworthy, believable, and honest.

10 Employees of the society make the effort to understand my needs.

11 The forms in the society are legible and are in local language.

12 The Physical facilities and employees of the society are neat and clean.

Customer satisfaction measures

13 My choice to take loan from the society is a wise one.

14 I think I did the right thing when I took the loan from the society.

15 My overall feelings towards the services provided by the society can be described as ----.

Switching cost measures

16 It would cost me a lot of money to switch from the society to another housing finance provider.

17 It would take a lot of effort to switch from the society to another housing finance provider.

311

Q. No. Cooperative identity measures

18 It would take a lot of time to switch from the society to another housing finance provider.

Customer loyalty measures

19 I have the intention to continue being a customer of the society in the future.

20 I would positively recommend the society to my friends and relatives.

21 I would stay with the society, although I would have to incur a somewhat higher cost.

7. 2.1 Basic Statistics on Customer Responses

Out of 21 question on customer loyalty and its antecedents in PHCs

there are two indicators in the questionnaire for measuring co-operative

identity (Q1 and Q 2), ten on service quality (Q3 – Q 12), three on customer

satisfaction (Q 13, Q14 and Q 15), three on switching cost (Q 16, Q 17, and Q

18) and three on customer loyalty (Q19, Q 20 and Q 21).

Table 7. 2

Distribution of Questions by Level of Score

Level of Score

No. of Qns. Question No. CI SQ CS SC CL

Low (<6) 1 21

Moderate (6,7) 14 1, 2, 3, 4, 5, 7, 8, 9, 10, 13,

14, 15, 19, 20 2 7 3 2

High (>7) 6 6, 11, 12, 16, 17, 18 3 3 Source: Survey data.

It is seen from the Table 7.2 only Q21 (CL) has evoked low score.

While most of the questions on SQ, two questions on (CL) and all the

312

questions on CI and CS have secured moderate score, all the questions on SC

and three questions on SQ have bagged high score on the Likert Scale. Figure

7.2 shows the mean scores of all the questions. Looking at the numbers

presented in the figure, it can be observed that while Q11 has the highest

mean score (8.1), the Q21 has the lowest mean score (5.3).

Figure 7.2

Mean Scores for SQ, CS, CI, SC, and CL

Source: Survey data.

Table 7.3 reveals the descriptive statistics of the factors of customer

loyalty. It is observed from the table a majority questions have generated

moderate scores. While Q3, Q6, Q11, Q12, and Q17 have minimum standard

deviations indicating consistent response, Q20, Q15 and Q10 have high

standard deviations showing fluctuations in the responses of customers.

313

Table 7.3

Descriptive Statistics on Variables for Factors of Customer Loyalty in PHCs

Question No. Mean SD Median Mode

Q1 6.8 1.1 7.0 7.0

Q2 6.9 1.2 7.0 7.0

Q3 6.3 0.9 6.0 6.0

Q4 6.5 1.1 7.0 7.0

Q5 6.2 1.0 6.0 6.0

Q6 7.7 0.9 8.0 8.0

Q7 6.3 1.1 6.0 6.0

Q8 6.9 1.1 7.0 7.0

Q9 6.5 1.2 7.0 7.0

Q10 6.6 1.5 7.0 7.0

Q11 8.1 0.8 8.0 8.0

Q12 7.9 0.9 8.0 8.0

Q13 6.8 1.0 7.0 7.0

Q14 6.9 1.2 7.0 7.0

Q15 6.1 1.3 6.0 7.0

Q16 7.0 1.0 7.0 7.0

Q17 7.8 0.9 8.0 8.0

Q18 7.0 1.1 7.0 7.0

Q19 6.2 1.2 6.0 6.0

Q20 6.2 1.3 6.0 6.0

Q21 5.3 1.2 5.0 5.0 Source: Survey data.

314

7.3 Analysis of Factors of Customer Loyalty in PHCs

7.3.1 Cronbach’s Alpha Test of Reliability

In order to test the internal reliability of the loyalty model used in the

study Cronbach’s Alpha Test of Reliability has been conducted. While

performing the test different factors pertaining to loyalty are grouped and

performed the test on each factor. Table 7.4 shows the alpha scores of the

different factors of loyalty.

Table 7.4

Cronbach’s Alpha Scores

Factor Cronbach’s Alpha

Service Quality (SQ) Co-operative Identity (CI) Customer Satisfaction (CS) Switching Cost (SC) Customer Loyalty (CL)

0.7598 0.6302 0.8005 0.5044 0.8662

Source: Survey data.

The Cronbach’s Alpha scores of all the factors range from 0.50 to 0.87.

Alpha scores for service quality, customer satisfaction and customer loyalty

exceed 0.7 which indicates high internal reliability of the scale items.

Although the reliability score for switching costs is less than the reliable score

of 0.6, considering its importance in the study, it is retained for the purpose of

factor analysis.

In order to analyse the responses collected from the sample customers,

Factor Analysis has been performed on the variables of the model with the

Principal Component Analysis as extraction method and varimax as rotation

method with Kaiser Normalization. Performing factor analysis by the usual

method and adjusting some components with their significance and observing

315

Cronbach’s Alpha scores of the duplicate components in each case, the

following factors are fixed.

The first factor is labeled as service quality (SQ). SQ is composed of

components Q3, Q4, Q5, Q6, Q8, Q9, Q10 and Q12 with Cronbach’s Alpha

score of 0.7233. But in the empirical SQ factor there are 10 components (Q3 –

Q12) with Cronbach’s Alpha score of 0.7590. As Q7 and Q11 have some

adverse effect on the empirical SQ factor they are considered as probable

candidates for exclusion. However, considering the significance of the

component Q7 in the service quality, it is retained and Q11 is eliminated.

After the exclusion of Q11, Cronbach’s Alpha score has increased to

0.7598. The modified SQ factor in the theoretical model has Q3, Q4, Q5, Q6,

Q7, Q8, Q9, Q10 and Q12 as its components with a mean of 61.13 (SD =

5.16).The results of Bartlett’s test of sphericity has indicated that data are

appropriate for factor analysis (p=0.00<0.05). Moreover, Kaiser-Meyer-Olkin

(KMO) measure of sampling adequacy is 0.805 which exceeds the minimum

level of 0.4 for good factor analysis.

Co-operative Identity (CI) is diagnosed by factor analysis as second

factor in the model. It has two components viz., Q1 and Q2. Its Cronbach’s

Alpha score is 0.6302. The mean of the factor is 13.64 (SD=1.97). There is

significant correlation between the components of co-operative identity.

These components also satisfy KMO measure of sampling adequacy

(0.50>0.4) and Bartlett’s test of sphericity (p=0.00<0.05). This model is

highly suitable for co-operative identity as 100 % of variance is explained by

the model (CI=1.464*Q1+0.536*Q2).

The third factor is Customer Satisfaction which is fully explained by

the components Q13, Q14 and Q15. The Cronbach’s Alpha score of this

factor is 0.8005 showing high internal consistency. It has a mean of 19.79

316

with standard deviation of 3.016. There is a reasonable correlation between

these components. This factor satisfies both KMO (0.692>0.4) and Bartlett’s

test of sphericity (p=0.00<0.05).

The linear component factor CS=2.153*Q13+0.516*Q14+0.331*Q15.

Switching Cost is the fourth factor developed by the factor analysis. It

is composed of Q16, Q17 and Q18. The Cronbach’s Alpha score (0.5044)

shows moderate consistency among the variable. Its mean and standard

deviations are 21.90 and 2.15 respectively. The Bartlett’s test of sphericity

(p=0.00<0.05) has indicated the statistical probability that the correlation

matrix has significant correlations among at least some of the variables and

KMO measure of sampling adequacy (0.571) has shown required sampling

adequacy.

The Customer Loyalty is the last factor of the model identified by the

factor analysis and which is composed of Q19, Q20 and Q21. This factor has

a very high Cronbach’s Alpha score of 0.8662 indicating high internal

consistency. The mean of the factor is 17.73 with standard deviation of 3.304.

KMO and Bartlett’s test are satisfied by the data for sampling adequacy and

variability as K=0.723 and p=0.00<0.05. The components explained are –

2.369 * Q19 + 0.382 * Q20 + 0.249 * Q21.

7.3.2 Analysis of Variables of Service Quality

7.3.2.1 Reliable, consistent and dependable service by employees (Q3)

It is evident from Table 7.3 that Q3 has median and mode of 6. A

median of 6 means that service quality on this variable as perceived by 50%

of customers is moderate. Similarly a mode of 6 indicates that majority of

customers have anchored their opinion at 6. The mean score of this variable is

6.3 (SD=0.9), implying that customers get the level of service quality which

317

they consider what the service ‘should be’. Looking at the Figure 7.3, it can

be observed that only 8.33% of the customers have stated 8 or 9 on the Likert

scale, meaning that only 8.33 % of the customers have perceived high quality

on this aspect of service quality in PHCs. These results reveal that quality on

this variable as perceived by customers is moderate.

Figure 7.3

Percentage of Customers with High Scores

Source: Survey data.

7.3.2.2 Willingness and ability of employees in providing service in a

timely manner (Q4)

Referring to the variable Q4, the Table 7.3 shows its median and mode

value as 7 which means that most of the customers perceive quality on this

variable more than the desired level. A mean score of 6.5 (SD=1.1) also

suggest that the PHCs have just exceeded the expectations of the majority of

the customers on this aspect of service quality. Furthermore, nearly 83% of

the customers have received desired level of quality or above on this variable.

However the Figure 7.4 shows that 16.43% of the customers have answered 5

or below indicating that they do not receive desired level of quality as far as

318

the willingness and ability of employees in providing service in a timely

manner is concerned. This finding leads to the conclusion that there is still

some deficiency in the delivery of quality service to the customers in PHCs.

Table 7.5

Percentage of Customers by Service Quality (SQ) Score Group

Score Group SQ Variables

Low (<6) Moderate (6,7) High (>7)

Q3 14.52 77.14 8.33

Q4 16.43 67.86 15.71

Q5 25.71 62.62 11.67

Q6 2.14 33.57 64.29

Q7 23.57 62.14 14.29

Q8 9.29 58.57 32.14

Q9 22.62 55.00 22.38

Q10 24.76 44.76 30.48

Q12 0.71 30.00 69.29

SQ^ 14.00 50.98 35.02 Source: Survey data.

7.3.2.3 Competence of the employees (Q5)

According to the data presented in the Table 7.3 this variable has a

median of 6 which implies that 50% of the customers have received the

desired level of quality on this aspect of service quality in PHCs. Looking at

the numbers presented in Figure 7.3, it can be observed that the quality

perceived by customers is not high on this item, which can also be concluded

from the fact that the mode of the variable is 6. Moreover, the Figure 7.4

shows that 25.71% of the customers have answered 5 or below on this

319

question. This indicates that the expectations of more than one fourth of the

customers about this variable are not met on a desired level.

Figure 7.4

Percentage of Customers with Low Scores

Source: Survey data.

From this finding it becomes clear that PHCs should try to improve the

employee competence aspect of service quality. Not improving this aspect of

service quality in PHCs might lead to the deterioration of quality of

relationship with customers and hence increases the risk of losing customers.

7.3.2.4 Approachable and easy to contact employees (Q6)

This variable of service quality has a median value of 8 indicating that

50% customers strongly agree that employees of PHCs are approachable and

easy to contact. The mode of the variable is 8. It signals that most of

customers have perceived high quality on this variable. The mean score of

this variable is 7.7 (SD=0.9) which also confirms the relatively high quality

on this variable. These results lead to the conclusion that in general

employees of PHCs are easy to contact and approachable. Furthermore, from

320

the Table 7.5 it is seen that only 2.14% of the customers have perceived low

quality (see Figure 7.4), 64.29% of customers have perceived very high

quality (see Figure 7.3), and 33.57% of customers have perceived moderate

quality (see Figure 7.5).

7.3.2.5 Courteous, polite and respectful employees (Q7)

In a highly interactive service environment such that of housing

finance customers often evaluate service quality on the basis of attitude of

staff towards them. The reason for this can be attributed to the fact that in an

environment where housing finance products are considered as equal, the only

differentiating factor is the service provided by the employees who are not

equal. Therefore it is pertinent to analyse the scores assigned by the customers

to this variable of service quality.

As per Table 7.3 both median and mode values for the variable are 6.

A median of 6 suggests that 50% of customers perceive service quality on this

variable as moderate. The value 6 for mode means that the highest number of

the customers has assigned the score 6 for this variable. The mean score of 6.3

(SD=1.1) also suggests that the level of quality on this variable as perceived

by customers is moderate. In other words, the quality on this variable is equal

to what the customers consider the quality ‘should be’. The Table 7.5 reveals

that the percentage of customers who have chosen 6 or 7 on the Likert scale

as 62.14, which supports the above findings. Moreover, the figure 7.4 displays

that 23.57% of the customers have perceived low quality on this variable. In

comparison only 14.29% of the customers have perceived high quality. The

finding that 23.57% have perceived low quality on this variable of service

quality is of high importance to PHCs as this variable needs improvement so

that the total perceived service quality would increase.

321

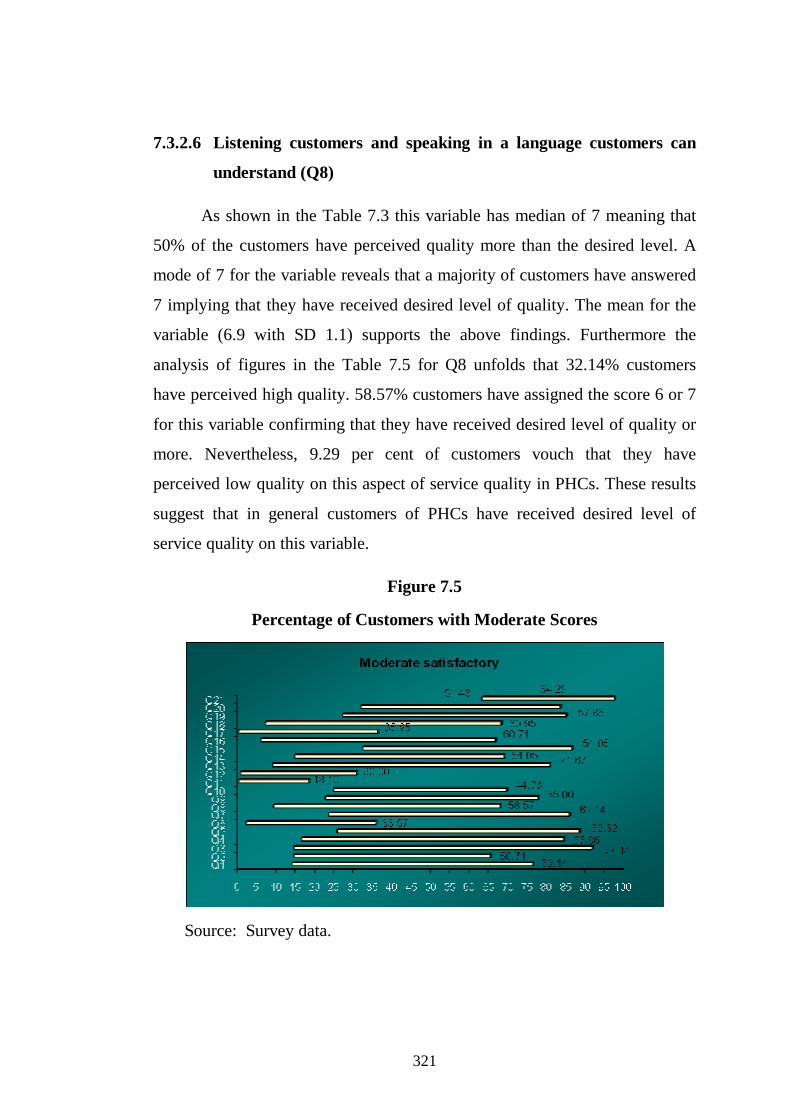

7.3.2.6 Listening customers and speaking in a language customers can

understand (Q8)

As shown in the Table 7.3 this variable has median of 7 meaning that

50% of the customers have perceived quality more than the desired level. A

mode of 7 for the variable reveals that a majority of customers have answered

7 implying that they have received desired level of quality. The mean for the

variable (6.9 with SD 1.1) supports the above findings. Furthermore the

analysis of figures in the Table 7.5 for Q8 unfolds that 32.14% customers

have perceived high quality. 58.57% customers have assigned the score 6 or 7

for this variable confirming that they have received desired level of quality or

more. Nevertheless, 9.29 per cent of customers vouch that they have

perceived low quality on this aspect of service quality in PHCs. These results

suggest that in general customers of PHCs have received desired level of

service quality on this variable.

Figure 7.5

Percentage of Customers with Moderate Scores

Source: Survey data.

322

7.3.2.7 Trustworthy, believable and honest employees (Q9)

This variable reflects one of the core components of service quality in

financial service organizations. The three attributes of this variable –

‘trustworthy’ ‘believable’ and ‘honest’ are important traits that customers

seek in the employees of PHCs. The reason is simple. Customers are reluctant

to transact with organisations that have employees who lack the above

qualities. This variable of service quality in PHCs has median and mode of 7.

A median of 7 implies that 50% of customers agree that the employees of the

PHCs are trustworthy, believable and honest. A mode of 7 indicates that a

highest number of customers have assigned the score 7 for this variable. This

would mean that a majority of customers have received more than the desired

level quality on this variable. The mean score of the variable is 6.5 (SD=1.2)

which confirms that the quality as perceived by the most of the customers has

exceeded the desired level. The data in Table 7.3 and the Figure 7.5 support

the above results. While 55% of customers have answered 6 or 7 on this

variable 22.38% have perceived high quality (8 or 9). However, 22.62% of

customers have perceived low quality on the variable. From these results it

becomes clear that PHCs need to improve this core component of service

quality because employees who are not trustworthy, believable and honest

may lead to risk of losing customers.

7.3.2.8 Understanding Customer Needs (Q10)

Employees making effort to understand customer needs may enhance

the performance quality of service delivered to the customers. If the

employees are not making efforts to understand the customer needs, the

customers may perceive quality as poor. Poor quality puts PHCs at a

competitively disadvantageous position. Moreover, if the customers perceive

quality as poor they would engage in unfavourable behavioural responses

(show tendency to switch).

323

It is observed from the Table 7.3 that both median and mode values for

the variable are 7. Median value of 7 implies that 50% of customers have

agreed that the employees of PHCs are making effort to understand their

needs and that their expectations on this aspect of service quality have been

exceeded. The value of mode supports this finding, indicating that the highest

number of customers have assigned the score 7. The fact that quality on this

variable has exceeded the expectations of customers is also supported by the

value of mean score which is 6.6 (SD=1.5).

But the Table 7.5 shows that 24.76% of the customers have answered 5

or below on the Likert scale. This would mean that nearly one fourth of the

customers are dissatisfied with this attribute of service quality in CHFSs.

Although high percentage of customers receive either desired level or above,

still 24.76% is a relatively high percentage for customers not being satisfied

with the efforts made by the employees to understand customer needs. This is

very dangerous in the competitive housing finance environment in Kerala

because customers can easily switch to another housing finance agency.

7.3.2.9 Legible Forms in Local Language (Q11)

This attribute of service quality is a key factor which is recognized for

its importance on the performance quality of PHCs. It is a factor of tangible

nature and is better linked to customer memory and ultimately influences

customer behavioural responses. This variable of service quality in PHCs has

median and mode of 8 indicating that a majority of customers have perceived

high service quality. The mean value of 8.1 with standard deviation of 0.8 for

this factor confirms the above findings. Furthermore, the Table 7.3 shows

that only 0.24% of customers have stated 5 or below on Likert-Scale for this

variable. This indicates that only 0.24% of the customers are dissatisfied with

this feature of service quality in PHCs which implies that in general most of

the customers (81.67%) are highly satisfied with the forms of PHCs which are

324

legible and in local language. These results can be considered rewarding for

PHCs as this feature differentiates PHCs from other housing finance agencies.

7.3.2.10 Physical facilities and employees (Q12)

This attribute of service quality is key factor which is recognised for its

importance on the performance quality of PHCs. It is a factor of tangible

nature and is better linked to customer memory and thus influences customer

behaviour. This variable of service quality in PHCs has median and mode of 8

indicating that a majority of customers have perceived high quality. The mean

value of 7.9 with standard deviation of 0.9 for this variable confirms the

above findings. Moreover, the Table 7.5 shows that only 0.71% of the

customers has assigned 5 or below on the Likert scale. This indicates that only

0.71% of the customers are dissatisfied with this feature of service quality in

PHCs which implies that in general physical facilities and employees are neat

and clean.

7.3.2.11 Evaluation of Service Quality on the basis Different Quality

Variables

An analysis of the percentage of customers who have chosen 5 or

below, 6 or 7 and 8 or 9 on the Likert scale unfolds how many customers in

percentage of the total number of customers have perceived poor service

quality, minimum, moderate and high level of service quality. The Figure 7.4

shows that 'most' customers have received low service quality on the

following variables of service quality in PHCs: ‘competence of employees’

(Q5) – 25.71%; ‘making the efforts to understand customer needs’ (Q10) -

24.76%; ‘courteous, polite and respectful employees’ (Q7) – 23.57%; and

‘trustworthy, believable and honest employees’ (Q9) – 22.62%. As these

features of service quality in PHCs have evoked poor scores they demand

immediate improvement so that total service quality would increase.

325

Figure 7.6

Mean Scores of SQ and its Variables

Source: Survey data.

On the other hand, the variables (dimensions) of service quality on

which most customers have perceived moderate level of quality are the

following: ‘Employees providing service reliably, consistently and

dependably’ (Q3) – 77.14%; ‘willingness and ability of employees to provide

service in a timely manner’ (Q4) – 67.86%; ‘competence of employees’ (Q5)

– 62.62%; and ‘courteous, polite and respectful employees’ (Q7) – 62.14%.

Since these features of service quality are of high importance to PHCs, they

need attention of the management to improve the total service quality. In

comparison most customers have perceived highest level of quality on ‘neat

and clean physical facilities and employees’ (Q12) – 69.29% and

‘approachable and easy to contact employees’ (Q 6) – 64.29%. These results

may be considered rewarding for PHCs as they may take competition on these

features of service quality.

326

Figure 7.7

Percentage of Customers with High, Moderate and Low SQ Scores

Source: Survey data.

Looking at the descriptive statistics on service quality presented in

Table 7.3 it is inferred from the values of median and mode that most of the

customers of PHCs have perceived service quality more than the desired

level. A mean score of 6.9 (SD=1.3) for service quality confirms that the

service quality as perceived by the majority of customers have just exceeded

their expectations. These findings are supported by the percentage of

customers who have received low service quality (14%), moderate service

quality (50.98%) and high service quality (35.02%) (see Figure 7.7)

7.3.3 Customer Satisfaction

A high service quality leads to greater customer satisfaction or delight

which in turn leads to customer loyalty. Customer satisfaction (CS) depends

on how customer needs and expectations are being fulfilled. The customer

satisfaction in PHCs is measured using three variables viz., Q13, Q14 and

Q15.

327

Figure 7.8

Mean Scores of CS and its Variables

Source: Survey data.

The median of Q13 and Q14 is 7 which means that 50% of customers

are satisfied with the services and products provided by PHCs. Their values

for mode are 7 implying that highest number of customers has answered 7 on

the Likert scale. Mean values for Q13 and Q14 are 6.8 (SD=1.0) and 6.9

(SD=1.2) respectively (see Figure 7.8). Furthermore, it is seen from the Table

7.6 that 71.67% of the customers for Q13 and 54.05% for Q14 have received

moderate level of satisfaction, supporting the above results.

Table 7.6

Percentage of Customers by CS Score Group

Q13 Q14 Q15 CS^

<6 9.05 14.76 32.38 18.73

6,7 71.67 54.05 54.05 59.92

>7 19.29 31.19 13.57 21.35 Source: Survey data.

328

Q15 is the variable for measuring the overall feelings of the customers

towards the services provided by PHCs. Median and mode values of Q15 are

6 and 7 respectively. A median of 6 would mean that the overall feelings of

one half of the customers towards the services provided by PHCs are ‘just

satisfied’. A mode of 7 implies that the highest number of customers assigned

the score 7 for this variable, indicating moderate level of satisfaction. These

results are supported by the mean value which is only 6.1 (SD=1.3).

Moreover, Table 7.6 reveals that 54.05% of the customers have experienced

moderate level of satisfaction.

Figure 7.9

Percentage of Customers with High, Moderate and Low CS Scores

Source: Survey data.

Conclusively, median and mode values of all the variables of customer

satisfaction construct taken together are 7, indicating that the customers of

PHCs have been experiencing only moderate level of satisfaction. The mean

score for customer satisfaction is 6.6 (SD=1.2) which supports the above

results. These results are, further confirmed by the percentage of customers

who have shown low level of satisfaction (18.73%), moderate level of

satisfaction (59.92%) and high level of satisfaction (21.35%) (see Figure 7.9).

329

7.3.4 Co-operative Identity

Co-operative identity (CI) is a unique characteristic of a co-operative

organisation. Co-operative identity has its roots in co-operative principles and

values (CPV). The co-operative principles and values were developed by

International Co-operative Alliance (1995) in order to form the structural

setting for promoting membership and loyalty. The co-operative identity thus

has a profound impact on the member/customer loyalty. It is in this context an

attempt is made here to analyse the strength of co-operative identity in the

PHCs.

Table 7.7

Percentage of Customers by CI Score Group

Q1 Q2 CI

<6 14.05 14.52 14.29

6,7 62.14 50.71 56.43

>7 23.81 34.76 29.29 Source: Survey data.

Co-operative identity is measured using two variables viz., Q1 and Q2.

Q1 has a median and mode value of 7 meaning that a majority of customers

moderately agree with the statement that PHCs adhere to the co-operative

principles. Mean value of the variable is 6.8 (SD=1.1) supporting the above

result. These results are consistent with the percentage of customers who have

moderately agreed i.e. 62.14%.

330

Figure 7.10

Percentage of Customers with High, Moderate and Low CI Scores

Source: Survey data.

Referring to the variable Q2, it can be inferred from its median value

of 7 and mode of 8 that in general customers have agreed with the statement

that PHCs respect co-operative values. The mean value of 6.9 also lends

support to the above finding. Moreover the percentages of customers who

have strongly agreed (34.76%) and moderately agreed (50.71%) confirm the

findings. Nevertheless Table 7.7 reveals that 14.52% of the customers have

answered 5 or below on the Likert scale, indicating that they do not agree

with the statement.

331

Figure 7.11

Mean Scores of CI and its Variables

Source: Survey data.

Conclusively, looking at co-operative identity (taking the two variables

of co-operative identity together) it is observed that it has a median and mode

of 7 vouching that the strength of co-operative identity in PHCs is moderate.

A mean score of 6.8 with standard deviation 1.0 confirms that the strength of

co-operative identity is not very strong in PHCs. The percentages of

customers who have disagreed (14.29%), moderately agreed (56.43%) and

strongly agreed (29.29%) lend support to the above findings. These results

assume significance in that 14.29% of customers believe that the basic

premise of a co-operative organization is being defeated and they find no

difference between co-operative and other organizations and therefore when

they have inferior perceptions about service quality they would switch to

another housing finance agency.

7.3.5 Switching Costs

Switching cost (SC) refers to the cost involved in terminating the

relationship with the current housing finance provider and acquiring new

CI^ Q2 Q1

332

relationship with another housing finance provider. Analysing switching costs

is important for PHCs because these costs stand as a barrier to customer

switching and hence lead to customer loyalty. Costs of switching from PHCs

to another housing finance agency are measured using three variables viz.,

Q16, Q17 and Q18.

Table 7.8

Percentage of Customers by SC Score Group

Q16 Q17 Q18 SC^

<6 5.95 0.24 7.14 4.44

6,7 60.71 35.95 60.95 52.54

>7 33.33 63.81 31.90 43.02 Source: Survey data.

Both Q16 and Q18 have median value of 7 meaning that 50% of

customers moderately agree that it would take a lot of time and cost them a lot

of money to switch from the PHCs to another housing finance company.

Similarly their values for mode are 7 indicating that highest number of

customers has answered 7. Moreover, their values for mean are 7 confirming

that in general switching costs are moderate. Percentages of customers who

have moderately agreed with Q16 (60.71%) and Q18 (60.95%) support the

above findings (see Table 7.8)

333

Figure 7.12

Percentage of Customers with High, Moderate and Low SC Scores

Source: Survey data.

It is seen from the Table 7.3 that while Q17 has a median and mode of

8, it has a mean of 7.8 with standard deviation 0.9. These numbers imply that

a majority of the customers have strongly agreed that it would take a lot of

effort to switch from PHCs to another housing finance company. This finding

is further supported by the percentage of customers who have very strongly

agreed with Q17 (63.81%).

Figure 7.13

Mean Scores of SC and its Variables

Source: Survey data.

Q16 Q17 Q18 SC^

334

However, an anlysis of descriptive statistics on switching cost in Table

7.3 reveals that both median and mode values for the overall switching costs

(taking all the three variables of SC together) are 7 and mean score is 7.3

(SD=1.1). It can be inferred from the above results that the switching cost in

CHFSs is high and it would serve as blockade to customer switching. The

percentage of customers who have disagreed with high overall switching cost

(4.44%) lends support to the above finding.

7.3.6 Customer Loyalty

Customer loyalty is the positive attitude that a customer shows towards

the product or service of a service provider and resorts only to the use of the

product or service from the same provider. A member/customer loyalty of a

PHCs is described as a loyal customer when the customer spreads good word-

of-mouth about the co-operative to other potential customers who then

become customers of the co-operative. A loyal customer of PHCs will not

switch to other housing finance providers even when the customer is

dissatisfied or when the product or service does not meet the expectations of

the customers. Member/customer loyalty in a PHCs is measured by using

three variables viz, Q19, Q20 and Q21. These variables of loyalty capture the

behavioural and attitudinal loyalty reposed by the customers in the PHCs.

Table 7.9

Percentage of Customers by CL Score Group

Q19 Q20 Q21 CL^

<6 27.14 31.90 63.10 40.71

6,7 57.86 51.43 34.29 47.86

>7 15.00 16.67 2.62 11.43 Source: Survey data.

335

It is observed from the Table 7.3 that Q19 and Q20 of the variables of

loyalty have median and mode values of 6. These values indicate that a

majority of customers have shown moderate degree of loyalty towards PHCs.

Mean value of both the variable is 6.2 which confirms the above finding.

These results are further supported by the percentage of customers who have

shown moderate level of loyalty – 57.86% (Q19) and 51.43% (Q20).

However, it is important to note that 15% of the customers for Q19 and

16.67% of the customers for Q20 have shown higher degree of loyalty (see

Table 7. 9)

Figure 7.14

Percentage of Customers with High, Moderate and Low CL Scores

Source: Survey data.

On the other hand, referring to Q21, most customers PHCs have shown

low level of loyalty. The median and mode value of 5 for Q21 shows that

majority of customers are indifferent to this aspect of loyalty i.e. customers

would stay with the co-operative, although they would have to incur a

somewhat higher cost. Mean of the variable is 5.3 (SD=1.2), supporting the

above finding. The percentage of customers who have answered 5 or below is

63.10 which also lends support to the finding (see Table 7.9). It appears from

336

the Table 7.9 that only 2.62% of customers are willing to incur higher cost to

stay with the co-operative.

Figure 7.15

Mean Scores of CL and its Variables

Source: Survey data.

Conclusively, median and mode value of customer loyalty (taking all

the variables together) are 6, revealing that the customers of PHCs in general

show moderate level of loyalty. The mean score for loyalty is 5.9 with

standard deviation 1.3 confirms the above results. Furthermore, these results

are supported by the percentage of customers who have shown low level of

loyalty (40.71%), moderate level of loyalty (47.86%) and high level of loyalty

(11.43%) (see Figure 7.14)

Q19 Q20 Q21 CL^

337

7.3.7 Service quality, Customer satisfaction, Co-operative identity,

Switching cost and Customer Loyalty – Region, Gender, Age, and

Education wise Analysis

Table 7. 10

Factors of Customer Loyalty: Descriptive Statistics (Region wise analysis)

Region N Mean Std. Deviation Trivandrum 100 14.3600 1.54737 Ernamulam 180 13.1278 2.07951 Kozhikode 140 13.7929 1`92483

Co-op. Identity

Total 420 13.6429 1.97141 Trivandrum 100 68.7800 4.66260 Ernamulam 180 68.4333 6.42716 Kozhikode 140 70.7286 6.24078

Service Quality

Total 420 69.2762 6.06448 Trivandrum 100 19.7200 2.25666 Ernamulam 180 19.5000 3.00744 Kozhikode 140 20.2071 3.44431

Customer Satisfaction

Total 420 19.7881 3.01632 Trivandrum 100 21.6100 2.14568 Ernamulam 180 21.8167 2.10312 Kozhikode 140 22.2000 2.08868

Switching Costs

Total 420 21.8952 2.15475 Trivandrum 100 17.5100 2.07191 Ernamulam 180 17.5055 3.73792 Kozhikode 140 18.1714 3.39899

Customer Loyalty

Total 420 17.7266 3.30367 Trivandrum 100 141.9600 9.34298 Ernamulam 180 140.3833 13.33979 Kozhikode 140 145.1000 14.55295

Total Score

Total 420 142.3310 13.12970 Source: Survey data.

338

Mean scores of the factors of customer loyalty in PHCs are further analysed on the basis of regions. As provided in the Table 7.10 mean scores of all the factors of customer loyalty are different in the three sample regions. Mean scores for service quality, customer satisfaction, switching cost and customer loyalty are highest in Kozhikkode region followed by Thiruvananthapuram. However, the mean score for switching cost in Ernakulam region is higher than Thiruvananthapuram. These results indicate that there are differences in the perception of customers in the different regions. Therefore F-test has been conducted to test whether there is any significant difference in the perceptions of customers in the three regions of Kerala.

Table 7.11 Results of Analysis Variance

(ANOVA)

Sum of squares D.F. Mean-

Square F-

value P-

value Between Groups 102.335 2 51.167 Within Groups 1526.094 417 3.660 Co-op.

Identity Total 1628.429 419

13.981 .000

Between Groups 449.836 2 224.918 Within Groups 14960.126 417 35.876 Service

Quality Total 419 419

6.269 .002

Between Groups 39.988 2 19.994 Within Groups 3772.153 417 9.046 Customer

Satisfaction Total 3812.140 419

2.210 .111

Between Groups 22.250 2 11.125 Within Groups 1923.140 417 4.612 Switching

Costs Total 1945.390 419

2.412 0.091

Between Groups 41.187 2 20.593 Within Groups 4531.570 417 10.868 Customer

Loyalty Total 4573.057 419

1.895 .152

Between Groups 1770.008 2 885.004 Within Groups 1526.094 417 3.660 Total Score Total 1628.429 419

5.238 .006

Source: Survey data.

339

Results indicate that significant differences exists for service quality

(p<0.05) and co-operative identity (p<0.05). But there exist no significant

differences (p>0.05) in the case of customer satisfaction, switching cost and

customer loyalty (7.11). Moreover a Post HOC Test has been conducted to

study the significance of differences in the perception of customers on service

quality, customer satisfaction, co-operative identity, switching cost and

customer loyalty in the three sample regions using Fisher’s Least Significant

Difference (LSD) method.

Table 7.12

Factors of Customer Loyalty in Regions (Results of Post-Hoc Tests)

Dependent Variables (I) Region (J) Region

Mean Difference

(W)

Std. Error Sig.

Trivandrum Ernakiulam Kozhikde

1.23222* .56714*

.23860

.25047 .000 .024

Eranakulam Trivandrum Kozhikode

-1.23222* -.66508*

.23860

.21557 .000 .002 Co-op. Identity

Kozhikode Trivandrum Ernakuam

-.56713* .66508*

.25047

.21557 .024 .002

Trivandrum Ernakiulam Kozhikde

.32667 -1.96857*

.74704

.78423 .662 .012

Eranakulam Trivandrum Kozhikode

-.32667 -2.29524*

.74704

.67495 .662 .001 Service Quality

Kozhikode Trivandrum Ernakulam

1.968576* 2.29524*

.78423

.67495 .012 .001

Trivandrum Ernakiulam Kozhikde

.22000 -.48714

.37512

.36379 .558 .217

Eranakulam Trivandrum Kozhikode

-.22000 -.70714*

.37512

.33892 .558 .038

Customer Satisfaction

Kozhikode Trivandrum Ernakulam

.48714 .70714*

.39379

.33892 .217 .038

340

Dependent Variables (I) Region (J) Region

Mean Difference

(W)

Std. Error Sig.

Trivandrum Ernakiulam Kozhikde

-.20667 -.59000*

.26784

.28118 .441 .036

Eranakulam Trivandrum Kozhikode

.20667 -.38333

.26784

.24200 .441 .114

Switching Costs

Kozhikode Trivandrum Ernakulam

.59000* .38333

.28118

.24200 .036 .154

Trivandrum Ernakiulam Kozhikde

.00444 -.66143

.41116

.43163 .991 .126

Eranakulam Trivandrum Kozhikode

-.00444 -.66587

.41116

.37149 .991 .074

Customer Loyalty

Kozhikode Trivandrum Ernakulam

.66143 .665897

.43163

.37149 .128 .074

Trivandrum Ernakiulam Kozhikde

1.57667 -3.14000

1.62125 1.70195

.31 .066

Eranakulam Trivandrum Kozhikode

-1.57667 -4.71667*

1.62125 1.46461

.331

.001 Total Score

Kozhikode Trivandrum Ernakulam

3.14000 4.71667*

1.70195 1.45481

.066

.001 *The mean difference is significant at 0.05 level Source: Survey data.

The results of Post HOC Test are presented in Table7.12. Table 7.12

shows that in the case of co-operative identity mean differences between

Thiruvananthapuram – Ernakulam, Thiruvananthapuram – Kozhikkode, and

Ernakulam – Kozhikkode regions are significant. In the case of service

quality, differences between Thiruvannathapuram – Kozhikkode regions are

significant. In the case of customer satisfaction difference is significant

between Ernakulam and Kozhikkode and in the case of switching cost

between Thiruvananthapuram – Kozhikkode regions. However no significant

differences are found among regions on customer loyalty.

341

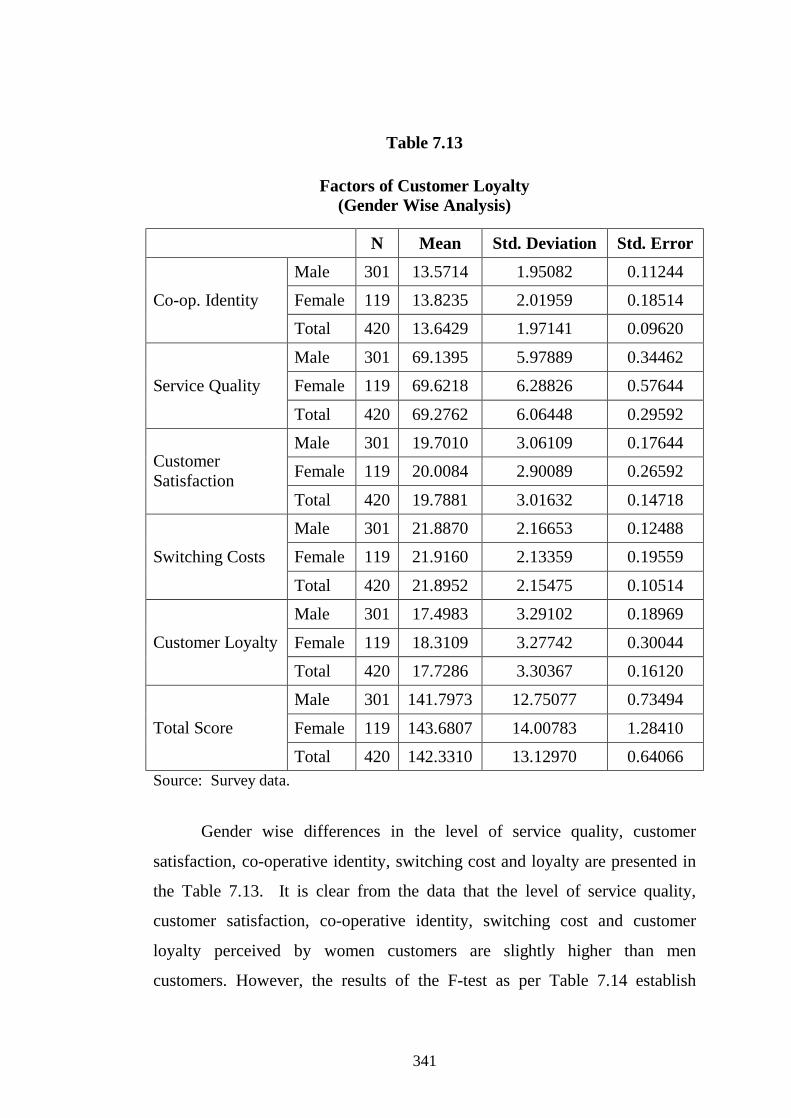

Table 7.13

Factors of Customer Loyalty (Gender Wise Analysis)

N Mean Std. Deviation Std. Error Male 301 13.5714 1.95082 0.11244

Female 119 13.8235 2.01959 0.18514 Co-op. Identity

Total 420 13.6429 1.97141 0.09620

Male 301 69.1395 5.97889 0.34462

Female 119 69.6218 6.28826 0.57644 Service Quality

Total 420 69.2762 6.06448 0.29592

Male 301 19.7010 3.06109 0.17644

Female 119 20.0084 2.90089 0.26592 Customer Satisfaction

Total 420 19.7881 3.01632 0.14718

Male 301 21.8870 2.16653 0.12488

Female 119 21.9160 2.13359 0.19559 Switching Costs

Total 420 21.8952 2.15475 0.10514

Male 301 17.4983 3.29102 0.18969

Female 119 18.3109 3.27742 0.30044 Customer Loyalty

Total 420 17.7286 3.30367 0.16120

Male 301 141.7973 12.75077 0.73494

Female 119 143.6807 14.00783 1.28410 Total Score

Total 420 142.3310 13.12970 0.64066 Source: Survey data.

Gender wise differences in the level of service quality, customer

satisfaction, co-operative identity, switching cost and loyalty are presented in

the Table 7.13. It is clear from the data that the level of service quality,

customer satisfaction, co-operative identity, switching cost and customer

loyalty perceived by women customers are slightly higher than men

customers. However, the results of the F-test as per Table 7.14 establish

342

significant difference only in the case of loyalty as the obtained ‘P’ value is

less than 0.05. This would mean that the strength loyalty shown by women is

stronger than men.

Table 7.14

Result of Analysis of Variance

Sum of Squares Df Mean

Square F-

value P-

value

Between groups 5.420 1 5.420 1.396 0.238

Within groups 1623.008 418 3.883 Co-op. Identity

Total 1628.429 419

Between groups 19.839 1 19.839 0.539 0.463

Within groups 15390.123 418 36.818 Service Quality

Total 15409.962 419

Between groups 8.059 1 8.059 0.886 0.347

Within groups 3804.081 418 9.101 Customer Satisfaction

Total 3812.140 419

Between groups 0.071 1 0.071 0.015 0.902

Within groups 1945.319 418 4.654 Switching Costs

Total 1945.390 419

Between groups 56.312 1 56.312 5.211 0.023

Within groups 4516.745 418 10.806 Customer Loyalty

Total 4573.057 419

Between groups 302.494 1 302.494 1.758 0.186

Within groups 71928.503 418 172.078 Total Score

Total 82230.998 419 Source: Survey data.

343

Table 7.15 Factors of Customer Loyalty (Age wise Analysis)

N Mean Std. Deviation

1 9 13.7778 1.48137 2 85 14.0118 1.75590 3 170 13.6588 2.01505 4 124 13.4274 2.00476 5 32 13.3750 2.21068

Co-op. Identity

Total 420 13.6429 1.97141 1 9 68.6667 5.14782 2 85 69.5412 5.41944 3 170 69.5647 5.98212 4 124 69.0484 6.30377 5 32 68.0938 7.45031

Service Quality

Total 420 69.2762 6.06448 1 9 19.6667 2.82843 2 85 20.1529 2.52372 3 170 19.8824 3.08043 4 124 19.5565 3.14501 5 32 19.2500 3.42665

Customer Satisfaction

Total 420 19.7881 3.01632 1 9 20.7778 2.58736 2 85 22.1412 2.04795 3 170 21.8941 2.17856 4 124 21.9032 2.14673 5 32 21.5313 2.19948

Switching Costs

Total 420 21.8952 2.15475 1 9 18.0000 2.12132 2 85 18.2471 2.95565 3 170 17.6882 3.24582 4 124 17.4919 3.67478 5 32 17.4063 3.25140

Customer loyalty

Total 420 17.7286 3.30367 1 9 140.8889 10.77549 2 85 144.0941 11.75506 3 170 142.6882 13.22014 4 124 141.4274 13.60904 5 32 139.6563 14.74867

Total score

Total 420 142.3310 13.12970 Source: Survey data.

344

Age wise differences in scores for service quality, customer

satisfaction, co-operative identity, switching cost and loyalty exhibited in the

Table 7.15 reveal that mean co-operative identity, customer satisfaction,

switching cost and customer loyalty scores of customers in ‘30-40’ years age

group are slightly greater than customers in all other age groups. But in the

case of service quality mean score for ’40-50’ years age group is little better

than other age groups. In short, it is clear from the table that there are

variations in the mean scores of the factors of customer loyalty for the

customers in different age groups.

Table 7.16

Result of Analysis of Variance

Sum of Squares Df Mean

Square F-

value P-

value Between groups 19.826 4 4.957 1.279 0.278 Within groups 1608.602 415 3.876 Co-op.

Identity Total 1628.429 419 Between groups 74.639 4 18.660 0.505 0.732 Within groups 15335.323 415 36.953 Service

Quality Total 15409.962 419 Between groups 28.877 4 7.219 0.792 0.531 Within groups 3783.264 415 9.116 Customer

Satisfaction Total 3812.140 419 Between groups 20.627 4 5.157 1.112 0.350 Within groups 1924.763 415 4.638 Switching

Costs Total 1945.390 419 Between groups 34.058 4 8.515 0.778 0.540 Within groups 4538.999 415 10.937 Customer

Loyalty Total 4573.057 419 Between groups 634.820 4 158.705 0.920 0.452 Within groups 71596.178 415 172.521 Total Score Total 72230.998 419

Source: Survey data.

345

The results of analysis of variance (Table 7.16) indicate that there no

significant differences in the perceptions of customers in the different age

groups on service quality, customer satisfaction, co-operative identity,

switching cost and loyalty as the ‘P’ values of the factors are greater than

0.05. It can be inferred from the results that perceptions of customers in

different age groups on the factors of customer loyalty in PHCs are identical.

Table 7.17

Factors of Customer Loyalty (Education Wise Analysis)

N Mean Std. Deviation

Below SSLC 168 13.5417 1.98151 SSLC 184 13.7446 1.94879 Degree 25 13.6400 2.28910 Others 43 13.6047 1.87895

Co-op. Identity

Total 420 13.6429 1.97141 Below SSLC 168 69.0952 6.13446 SSLC 184 69.2989 7.74016 Degree 25 70.0800 4.90982 Others 43 69.4186 6.06448

Service Quality

Total 420 69.2762 3.06599 Below SSLC 168 19.7202 3.06599 SSLC 184 19.7663 3.06483 Degree 25 20.9600 3.07517 Others 43 19.4651 2.47222

Customer Satisfaction

Total 420 19.7881 3.01632 Below SSLC 168 21.9583 2.10603 SSLC 184 21.8533 2.23122 Degree 25 21.5600 2.14243 Others 43 22.0233 2.06430

Switching Costs

Total 420 21.8952 2.15475

346

N Mean Std. Deviation

Below SSLC 168 17.5536 3.45676 SSLC 184 17.8152 3.31392 Degree 25 18.5600 3.41663 Others 43 17.5581 2.50050

Customer Loyalty

Total 420 17.7286 3.30367 Below SSLC 168 141.8690 13.13475 SSLC 184 142.4783 13.18840 Degree 25 144.8000 16.74656 Others 43 142.0698 10.53881

Total Score

Total 420 142.3310 13.12970 Source: Survey data.

Table 7.17 reveals the differences of perceptions of customers on the

service quality, customer satisfaction, co-operative identity, switching cost

and customer loyalty due to differences in the level of education of customers.

The mean scores of the factors indicate differences in the perceptions of

customers having different levels of education.

Table 7.18

Results of Analysis of Variance

Sum of Squares Df Mean

Square F-

value P-

value

Between groups 3.687 3 1.229 0.315 0.815

Within groups 1624.742 416 3.906 Co-op. Identity

Total 1628.429 419

Between groups 22.621 3 7.540 0.204 0.894

Within groups 15387.341 416 36.989 Service Quality

Total 15409.962 419

Between groups 39.981 3 13.227 1.459 0.225

Within groups 3772.460 416 9.068 Customer Satisfaction

Total 3812.140 419

347

Sum of Squares Df Mean

Square F-

value P-

value

Between groups 4.507 3 1.502 0.322 0.809

Within groups 1940.883 416 4.666 Switching Costs

Total 1945.390 419

Between groups 25.057 3 8.352 0.764 0.515

Within groups 4548.000 416 10.933 Customer Loyalty

Total 4573.057 419

Between groups 195.175 3 65.058 0.376 0.771

Within groups 72035.823 416 173.163 Total Score

Total 72230.998 419 Source: Survey data.

Table 7.18 reports the results of the analysis of variance of the

perceptions of customers having different levels of education on service

quality, customer satisfaction, co-operative identity, switching cost and

loyalty. The results of the analysis of variance suggest that there are no

significant differences in the perceptions of customers having different level

of education as the ‘P’ values of all the factors are greater than 0.05

7.3.8 The Relationship between Service Quality, Customer Satisfaction

and Customer Loyalty

Service quality is considered to be an important factor in increasing

customer satisfaction in housing finance companies. Several empirical

findings have agreed that service quality judgments cause satisfaction; that is,

service quality is the antecedent of satisfaction. These findings leads to

suggest that when the PHCs provide quality services to its members/

customers they become satisfied and leads to customers being loyal to the

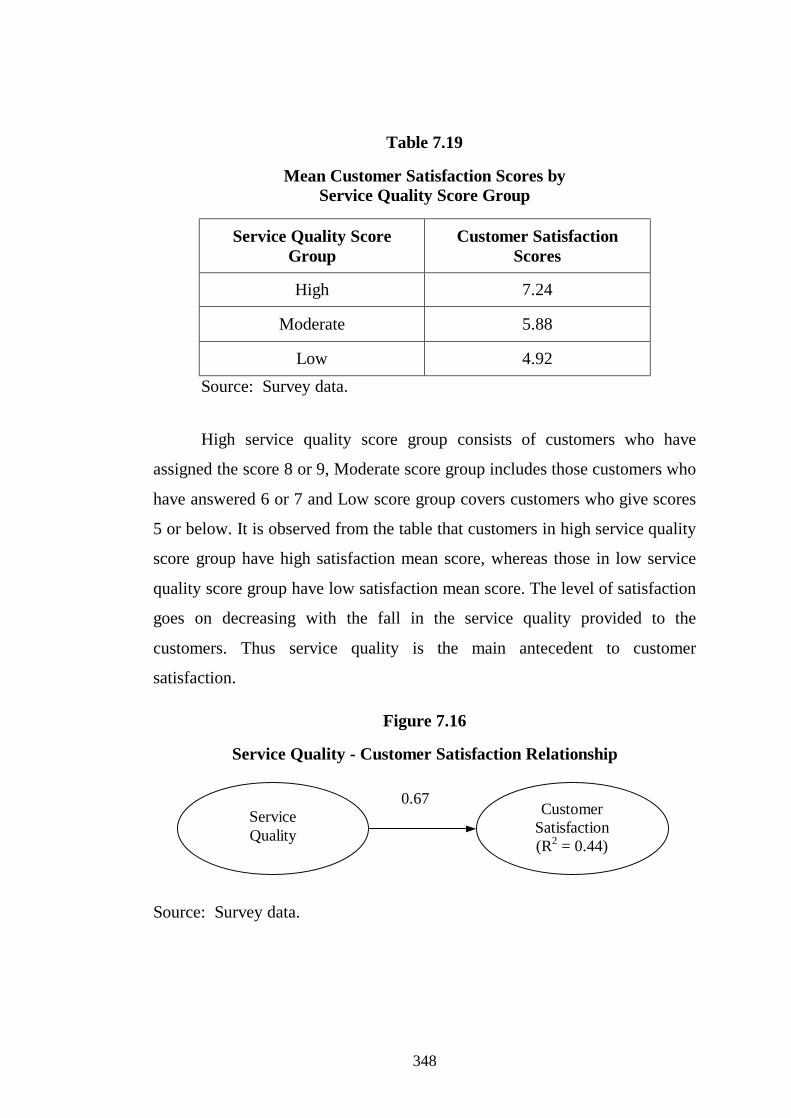

PHCs. Table 7.19 reveals mean customer satisfaction scores for different

service quality score groups.

348

Table 7.19

Mean Customer Satisfaction Scores by Service Quality Score Group

Service Quality Score Group

Customer Satisfaction Scores

High 7.24

Moderate 5.88

Low 4.92 Source: Survey data.

High service quality score group consists of customers who have

assigned the score 8 or 9, Moderate score group includes those customers who

have answered 6 or 7 and Low score group covers customers who give scores

5 or below. It is observed from the table that customers in high service quality

score group have high satisfaction mean score, whereas those in low service

quality score group have low satisfaction mean score. The level of satisfaction

goes on decreasing with the fall in the service quality provided to the

customers. Thus service quality is the main antecedent to customer

satisfaction.

Figure 7.16

Service Quality - Customer Satisfaction Relationship

Source: Survey data.

Customer Satisfaction (R2 = 0.44)

Service Quality

0.67

349

Moreover, Figure 7.16 shows that service quality relates both

significantly and positively to customer satisfaction. More specifically, the

significant relationship between service quality and customer satisfaction is

moderately strong as r=0.67 with p<.01. Service quality explains about 44%

of the variation in customer satisfaction (R2 = 0.44). These results support

that service quality is positively related to customer satisfaction.

7.3.9 The Relationship between Service Quality and Customer Loyalty

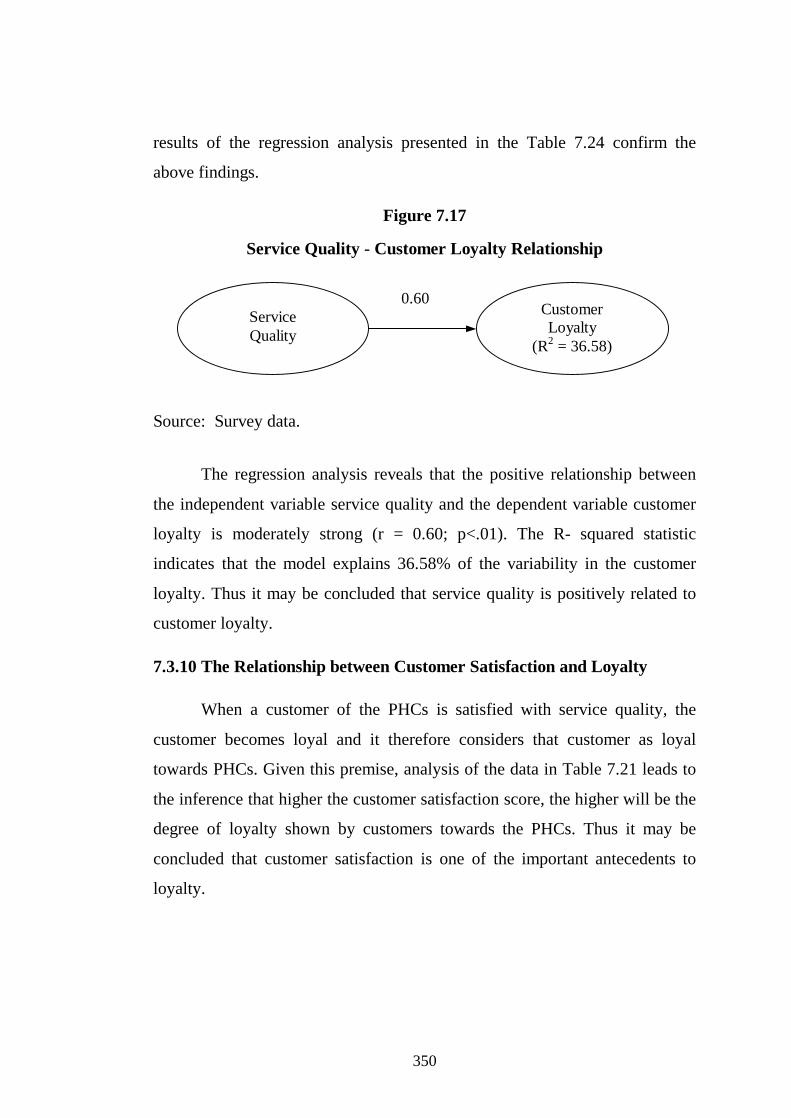

Service quality is an integral component in customer loyalty creation. Higher quality of service leads to increased loyalty, greater tolerance of price increases, and superior image. The level of service quality that the PHCs provide to their customers tends to influence the loyalty of customers towards PHCs. Therefore it is logical to think that there would be a causal link between quality of services provided by PHCs and the level of loyalty shown by the customers. The analysis of the data presented in Table 7.20 sheds light on the causal link between service quality and loyalty in PHCs.

Table 7.20

Mean Customer Loyalty Scores by Service Quality Score Group

Service Quality Score Group Customer Loyalty Scores High 6.44

Moderate 5.86

Low 3.81 Source: Survey data.

It is evident from the above table that customers in high service quality

score group have shown high level of loyalty and those in low service quality

score group have shown low level of loyalty. These results indicate that there

exists positive relationship between service quality and customer loyalty. The

350

results of the regression analysis presented in the Table 7.24 confirm the

above findings.

Figure 7.17

Service Quality - Customer Loyalty Relationship

Source: Survey data.

The regression analysis reveals that the positive relationship between

the independent variable service quality and the dependent variable customer

loyalty is moderately strong (r = 0.60; p<.01). The R- squared statistic

indicates that the model explains 36.58% of the variability in the customer

loyalty. Thus it may be concluded that service quality is positively related to

customer loyalty.

7.3.10 The Relationship between Customer Satisfaction and Loyalty

When a customer of the PHCs is satisfied with service quality, the

customer becomes loyal and it therefore considers that customer as loyal

towards PHCs. Given this premise, analysis of the data in Table 7.21 leads to

the inference that higher the customer satisfaction score, the higher will be the

degree of loyalty shown by customers towards the PHCs. Thus it may be

concluded that customer satisfaction is one of the important antecedents to

loyalty.

Customer Loyalty

(R2 = 36.58)

Service Quality

0.60

351

Table 7.21

Mean Loyalty Scores by Customer Satisfaction Score Group

Customer Satisfaction Score Group Mean Loyalty Scores

High 6.59

Moderate 5.94

Low 4.90 Source: Survey data.

Figure 7.18

Customer Satisfaction - Customer Loyalty Relationship

Source: Survey data.

The results of simple regression analysis indicate that customer

satisfaction has a direct and significant positive effect on customer loyalty.

Specifically, the significant relationship between customer satisfaction and

customer loyalty is moderately strong (r = 0.61; p value < 0.01). As per the

regression analysis customer satisfaction explains about 37% of variation in

customer loyalty (R2 = 0.37). Since the p-value in table is less than 0.01,

there is a statistically significant relationship between customer satisfaction

and customer loyalty.

Customer Loyalty

(R2 = 0.37)

Customer Satisfaction

0.61

352

7.3.11 The Relationship between Co-operative Identity and Customer

Loyalty

Co-operative principles and values, on which the structure of the co-

operative organization is built, clothe co-operative forms of business with a

unique characteristic known as co-operative identity. It is the competitive

advantage that co-operative organizations have over other organizations. Co-

operative identity means that a co-operative exists not to create profits for any

group other than the members and it is member owned and controlled. The

co-operative identity leads to loyalty. Loyalty helps co-operatives to be more

successful. It is in this background the relationship between co-operative

identity and member/customer loyalty is explored.

Table 7.22

Mean Loyalty Scores by Co-operative Identity Score Group

Co-operative Identity Score Group Mean Loyalty Scores

High 6.47

Moderate 5.88

Low 4.90 Source: Survey data.

Table 7.22 reveals that mean loyalty score of customers in the high co-

operative identity score group is more than that of moderate group and mean

loyalty score of moderate group is more than the low co-operative identity

score group. It can be inferred from the mean loyalty scores in the table that

co-operative identity has a profound influence on member/customer loyalty

and therefore it is an important antecedent to loyalty in PHCs.

353

Figure 7.19

Co-operative Identity - Customer Loyalty Relationship

Source: Survey data.

The regression analysis presented Table 7.24 shows that the regression

co-efficient between co-operative identity and customer loyalty as 0.55

(p<0.01). These results establish that there exists a significant positive

relationship between co-operative identity and customer loyalty. The co-

operative identity explains about 30% of the variability in customer loyalty

(R2 = 0.30).

7.3.12 The Relationship between Switching Cost and Customer Loyalty

Switching costs mean costs involved in changing from one service

provider to another. The driving force for the study of switching costs in

PHCs is the assumption that these costs hamper customer switching. Thus the

perception of switching is considered as an important factor influencing

customer loyalty in PHCs. An examination of data presented in Table 7.23

shows that mean loyalty scores of customers who have perceived high

switching costs is higher than those customers who have perceived low

switching costs.

Customer Loyalty

(R2 = 0.30)

Co-operative Identity

0.55

354

Table 7.23

Mean Loyalty Scores by Switching Cost Score Group

Switching Cost Score Group Mean Loyalty Scores

High 6.17

Moderate 5.78

Low 5.00 Source: Survey data.

Figure 7.20

Switching Cost - Customer Loyalty Relationship

Source: Survey data.

While exploring the relationship between switching costs and loyalty

in PHCs, it is found that there exists a statistically significant relationship

between switching costs and customer loyalty. The correlation coefficient

between switching cost and customer loyalty equals 0.27, indicating a

relatively weak relationship between the variables. The R-squared statistic

indicates that the switching cost explains only about 7% of the variation in

customer loyalty (R2 = 0.07).

7.4 Testing of Hypotheses

The hypothesized relationships have been tested using the simple and

multiple regression analysis of SPSS for Windows. The average scores of the

variables which form each construct are used in the data analysis. The R2 is

used to assess the model’s overall predictive fit. The customer loyalty model

Customer Loyalty

(R2 = 0.07)

Switching Cost

0.27

355

in PHCs is presented in Figure 7.20 While in hypothesis H1a the study

examines the relationship between service quality and customer satisfaction,

in hypotheses H1b, H2, H3, and H4 it investigates the influence of service

quality, customer satisfaction, co-operative identity and switching cost on

customer loyalty.

Table.7.24

Customer Loyalty Model: Evaluation and Validity Simple Regression Analysis

Independent Variables

Customer Loyalty - Correlation coefficients

F - Value

P - Value R2

Service Quality 0.605 241.14 0.000 0.3658

Customer Satisfaction 0.611 249.34 0.000 0.3736

Co-operative Identity 0.552 181.54 0.000 0.3028

Switching Cost 0.269 32.60 0.000 0.0723

As shown in Figure 7.16 service quality has a significant positive

influence on customer satisfaction (r=0.67, P<0.01). Hence the hypothesis H1

is supported. Hypotheses H1b, H2, H3 and H4 examine the influence of

service quality, customer satisfaction, co-operative identity and switching cost

on customer loyalty. Service quality (r = 0.60; P<0.01), customer satisfaction

(r = 0.61; P<0.01), co-operative identity (r=0.552; p<0.01), and switching cost

(r = 0.27; P<0.01) have a significant positive effect on customer loyalty.

Therefore the hypotheses H1b, H2, H3 and H4 are supported. Since R-

squared statistic for all the independent variables in simple regression analysis

is small, multiple regression analysis has been considered for examining the

influence of service quality, customer satisfaction, co-operative identity, and

switching cost on customer loyalty.

356

Table.7.25

Customer Loyalty Model: Evaluation and Validity Multiple Regression Analysis

Independent Variables Customer Loyalty -

Correlation coefficients P - Value R2

Service Quality 0.605 0.0000

Customer Satisfaction 0.611 0.0000

Co-operative Identity 0.552 0.0000

Switching Cost 0.269 0.4899

0.4705

As depicted in Table 7.25 service quality (r = 0.53; P<0.01), Customer

Satisfaction (r=0.31; P<0.01) and co-operative identity (r=0.23; P<0.01) have

a moderately strong positive influence on customer loyalty. Although the

regression coefficient of switching cost (r=0.04; P>0.01) is less than service

quality, customer satisfaction and co-operative identity, the removal of the

switching cost from the model does not improve the R-squared statistic.

Rather it decreases R-squared statistic by 10%. Therefore the switching cost

is retained in the model of customer loyalty in PHCs. Moreover, the study

finds that the multiple regression model of customer loyalty in the Figure 7.20

explains a significant percentage of variance in the customer loyalty (R2

=47.05%; P<0.01) than the conceptual model proposed in the Figure 7.1 (see

page 301). According to regression coefficients shown in Figure 7.19, service

quality has exhibited the strongest direct effect on customer loyalty.

357

Figure 7.21

Customer Loyalty Model in PHCs

Source: Survey data.

References:

1. Cronin, J.J.., Brady, M.K., and Hult. G.T.M., (2000), Assessing the

Effects of Quality, Value, and Customer Satisfaction on Consumer

Behavioural Intentions in Service Environments, Journal of Retailing,

76 (2), pp.193-218.

Customer Satisfaction

Switching Costs

Co-operative Identity

Customer Loyalty

(R2=47.05%)

0.31

0.23

0.04

0.53 0.67

Service Quality

358

2. Anderson, Eugene U. and Mittal. Vikas (2000) Strengthening the

Satisfaction Profit Chain, Journal of Services Research, 3 (2), 107-120.

3. Oliver, R.L. (1997) Satisfaction: Behavioural perspective on the

consumer, McGraw-Hill, New York.

4. Cronin, J.J. and Taylor, S.A., (1992), “Measuring Service Quality: A

Reexamination and Extension”, Journal of Marketing, Vol.56, July,

pp.55-68.

5. Parasuraman, A., Zeithaml, V.A., and Berry, L.L., (1994), “Alternative

Scales for Measuring Service Quality: A Comparative Assessment

Based on Psychometric and Diagnostic Criteria, Journal of Retailing,

Vol. 70, pp. 210-230.

6. Rust R.T and Oliver R. L. (1994) Service Quality: New Directions in

Theory and Practice, Sage Publications, Inc., Thousand Oakes, CA, 72-

94.