current trends in master limited partnerships (mlps) · pdf filepartnerships (mlps) march 14,...

TRANSCRIPT

Current Trends in Master Limited Partnerships (MLPs)

March 14, 2013

Todd D. Keator Thompson & Knight LLP

214-969-1797 [email protected]

©2013 Todd D. Keator

1

Agenda

• Introduction • Formation Issues • Legal Structure • Trends in “Qualifying Income” • Market Opportunity

2

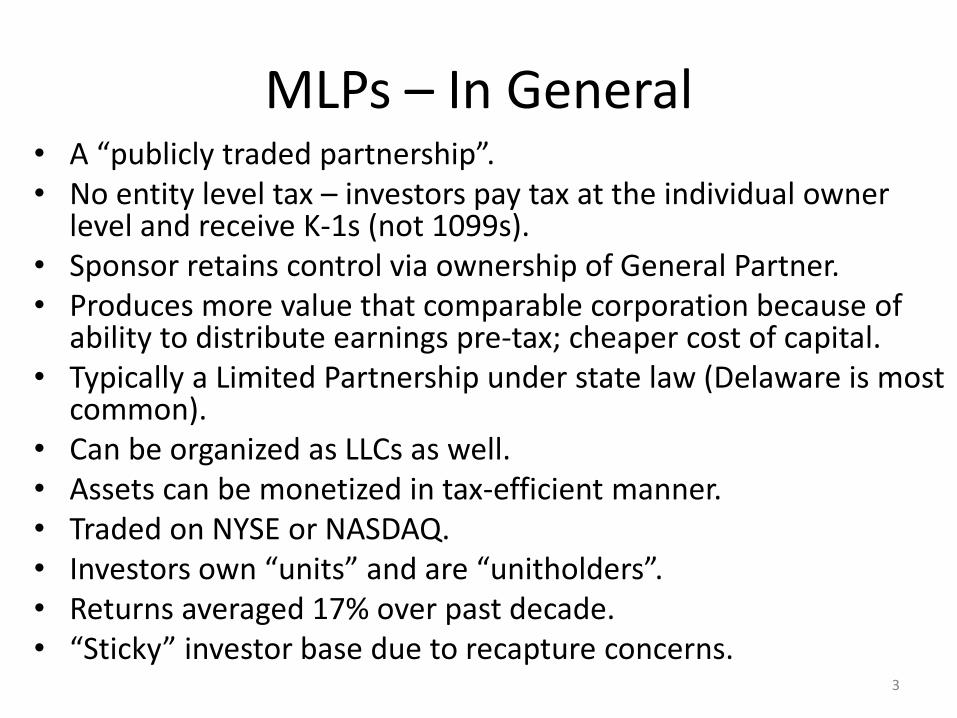

MLPs – In General • A “publicly traded partnership”. • No entity level tax – investors pay tax at the individual owner

level and receive K-1s (not 1099s). • Sponsor retains control via ownership of General Partner. • Produces more value that comparable corporation because of

ability to distribute earnings pre-tax; cheaper cost of capital. • Typically a Limited Partnership under state law (Delaware is most

common). • Can be organized as LLCs as well. • Assets can be monetized in tax-efficient manner. • Traded on NYSE or NASDAQ. • Investors own “units” and are “unitholders”. • Returns averaged 17% over past decade. • “Sticky” investor base due to recapture concerns.

3

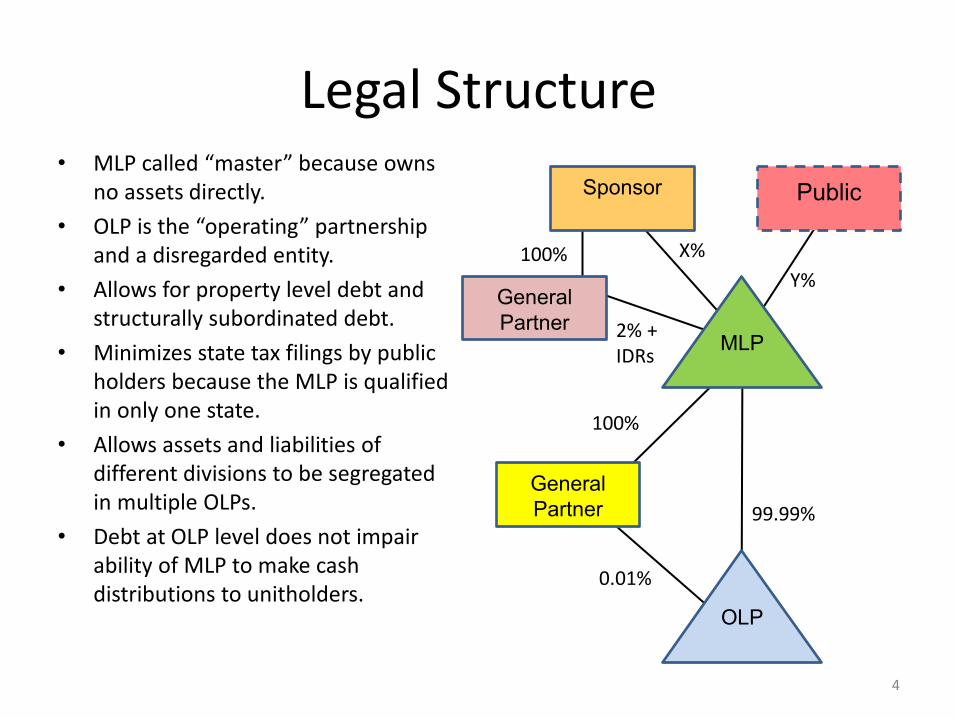

Legal Structure • MLP called “master” because owns

no assets directly. • OLP is the “operating” partnership

and a disregarded entity. • Allows for property level debt and

structurally subordinated debt. • Minimizes state tax filings by public

holders because the MLP is qualified in only one state.

• Allows assets and liabilities of different divisions to be segregated in multiple OLPs.

• Debt at OLP level does not impair ability of MLP to make cash distributions to unitholders.

Sponsor

MLP

Public

General Partner

OLP

General Partner

100%

2% + IDRs

X% Y%

100%

0.01%

99.99%

4

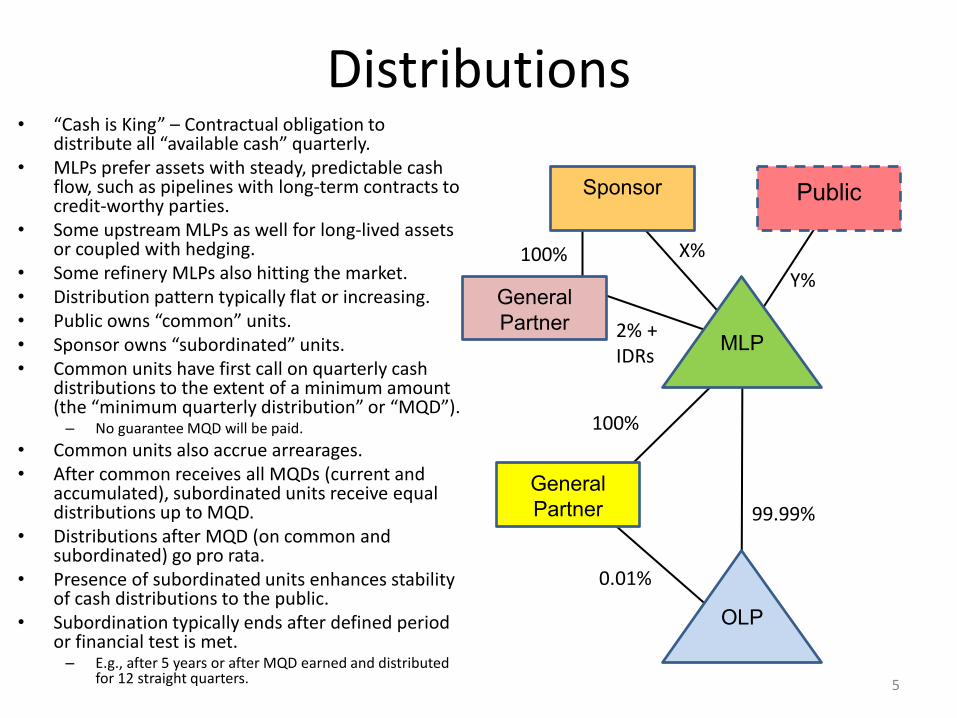

Distributions • “Cash is King” – Contractual obligation to

distribute all “available cash” quarterly. • MLPs prefer assets with steady, predictable cash

flow, such as pipelines with long-term contracts to credit-worthy parties.

• Some upstream MLPs as well for long-lived assets or coupled with hedging.

• Some refinery MLPs also hitting the market. • Distribution pattern typically flat or increasing. • Public owns “common” units. • Sponsor owns “subordinated” units. • Common units have first call on quarterly cash

distributions to the extent of a minimum amount (the “minimum quarterly distribution” or “MQD”).

– No guarantee MQD will be paid. • Common units also accrue arrearages. • After common receives all MQDs (current and

accumulated), subordinated units receive equal distributions up to MQD.

• Distributions after MQD (on common and subordinated) go pro rata.

• Presence of subordinated units enhances stability of cash distributions to the public.

• Subordination typically ends after defined period or financial test is met.

– E.g., after 5 years or after MQD earned and distributed for 12 straight quarters.

Sponsor

MLP

Public

General Partner

OLP

General Partner

100%

2% + IDRs

X% Y%

100%

0.01%

99.99%

5

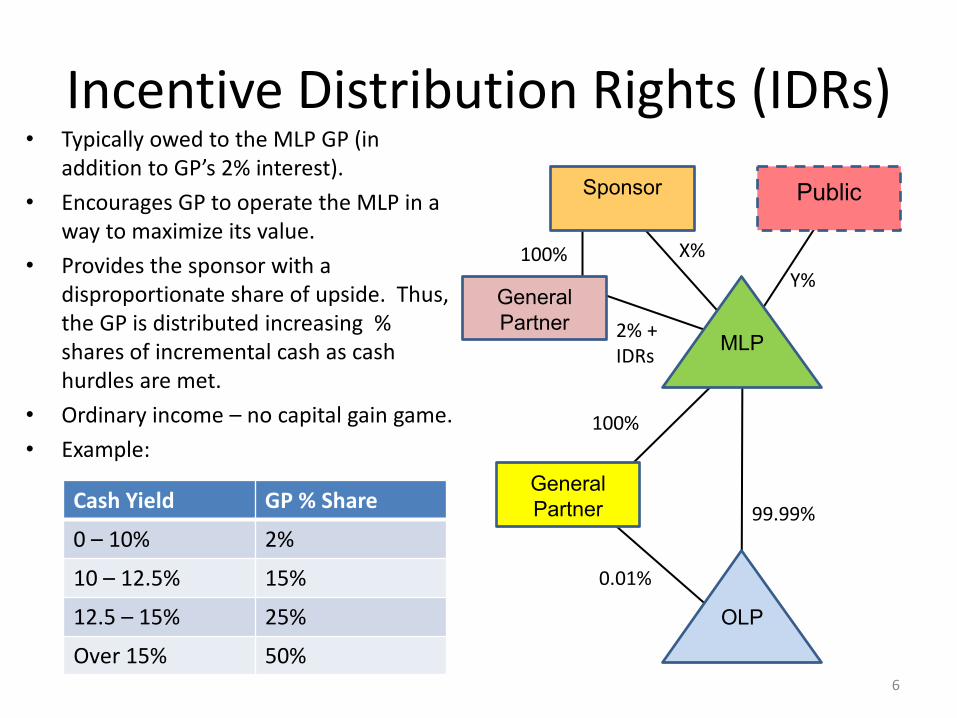

Incentive Distribution Rights (IDRs) • Typically owed to the MLP GP (in

addition to GP’s 2% interest). • Encourages GP to operate the MLP in a

way to maximize its value. • Provides the sponsor with a

disproportionate share of upside. Thus, the GP is distributed increasing % shares of incremental cash as cash hurdles are met.

• Ordinary income – no capital gain game. • Example:

Sponsor

MLP

Public

General Partner

OLP

General Partner

100%

2% + IDRs

X% Y%

100%

0.01%

99.99% Cash Yield GP % Share

0 – 10% 2%

10 – 12.5% 15%

12.5 – 15% 25%

Over 15% 50% 6

Formation Issues • Most MLP assets formerly owned by corporations. • Corporate sponsor typically contributes assets to MLP in

exchange for subordinated units. • Asset contribution raises legal issues:

– Contractual prohibitions on asset transfers. – Consent requirements. – Rights of first refusal. – Licenses and permits (FERC “certificate of public convenience” is a

key issue). – Debt that is not pre-payable. – Transfer taxes.

• Transfer via merger may solve some legal issues. • Conversions also possible (treated as taxable liquidation). • MLP then undergoes IPO and issues common units to the

public for cash.

7

Tax Consequences of Formation • Typically structured as primary IPOs where sponsor contributes

appreciated assets and public contributes cash for new units; cash then distributed to sponsor.

• Assets typically contributed “tax-free” by sponsor to MLP under IRC Sec. 721.

• “Disguised sale” issues arise depending upon use of IPO cash or MLP debt. • Key exceptions to disguised sale:

– Reimbursement of pre-formation Capex. – Debt-financed distributions. – See Treas. Reg. Secs. 1.707-4 and -5.

• Gain deferred by sponsor typically is allocated only to the sponsor over the useful life of the contributed assets using “remedial allocations.”

• Maintains uniformity of units via IRC Sec. 754 elections and remedial allocations. Thus, each purchaser receives uniform tax benefits based on the price paid for the units.

8

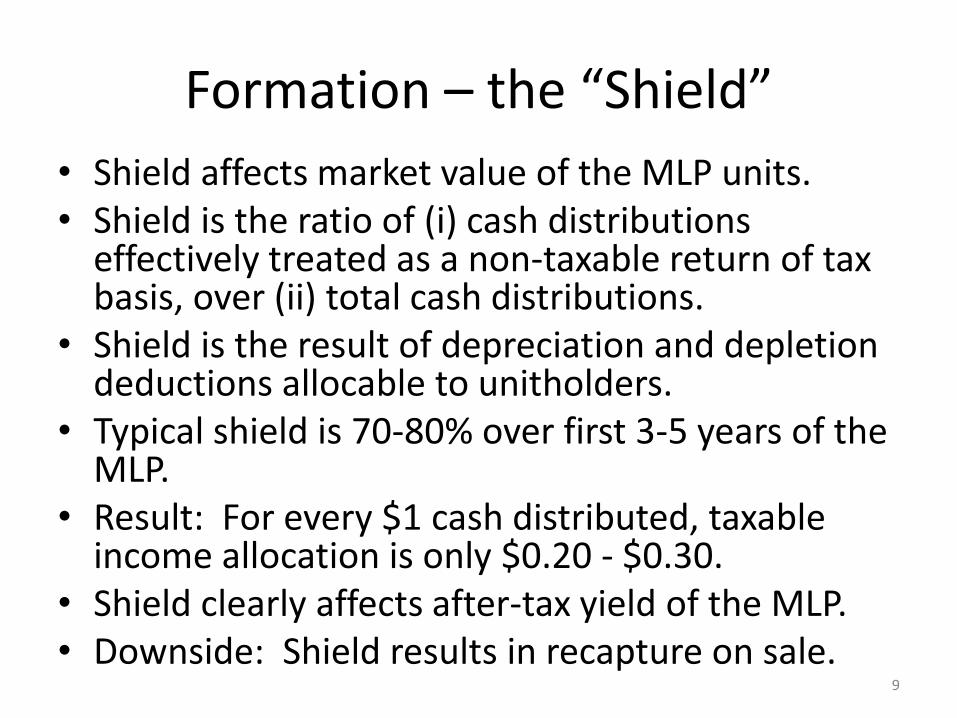

Formation – the “Shield” • Shield affects market value of the MLP units. • Shield is the ratio of (i) cash distributions

effectively treated as a non-taxable return of tax basis, over (ii) total cash distributions.

• Shield is the result of depreciation and depletion deductions allocable to unitholders.

• Typical shield is 70-80% over first 3-5 years of the MLP.

• Result: For every $1 cash distributed, taxable income allocation is only $0.20 - $0.30.

• Shield clearly affects after-tax yield of the MLP. • Downside: Shield results in recapture on sale.

9

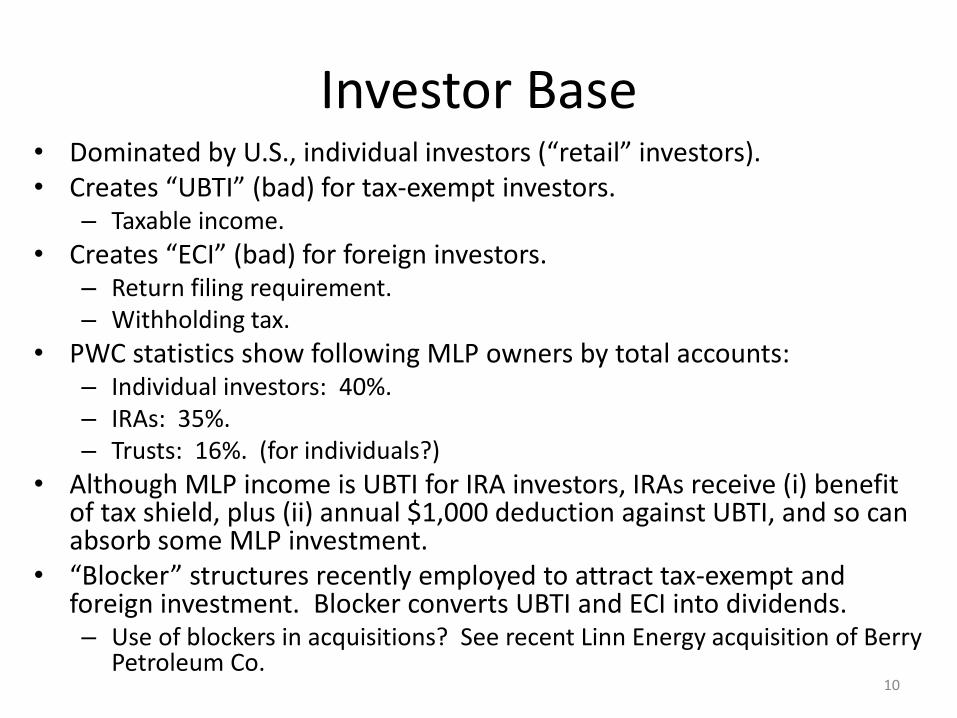

Investor Base • Dominated by U.S., individual investors (“retail” investors). • Creates “UBTI” (bad) for tax-exempt investors.

– Taxable income. • Creates “ECI” (bad) for foreign investors.

– Return filing requirement. – Withholding tax.

• PWC statistics show following MLP owners by total accounts: – Individual investors: 40%. – IRAs: 35%. – Trusts: 16%. (for individuals?)

• Although MLP income is UBTI for IRA investors, IRAs receive (i) benefit of tax shield, plus (ii) annual $1,000 deduction against UBTI, and so can absorb some MLP investment.

• “Blocker” structures recently employed to attract tax-exempt and foreign investment. Blocker converts UBTI and ECI into dividends. – Use of blockers in acquisitions? See recent Linn Energy acquisition of Berry

Petroleum Co. 10

Partnership Qualification

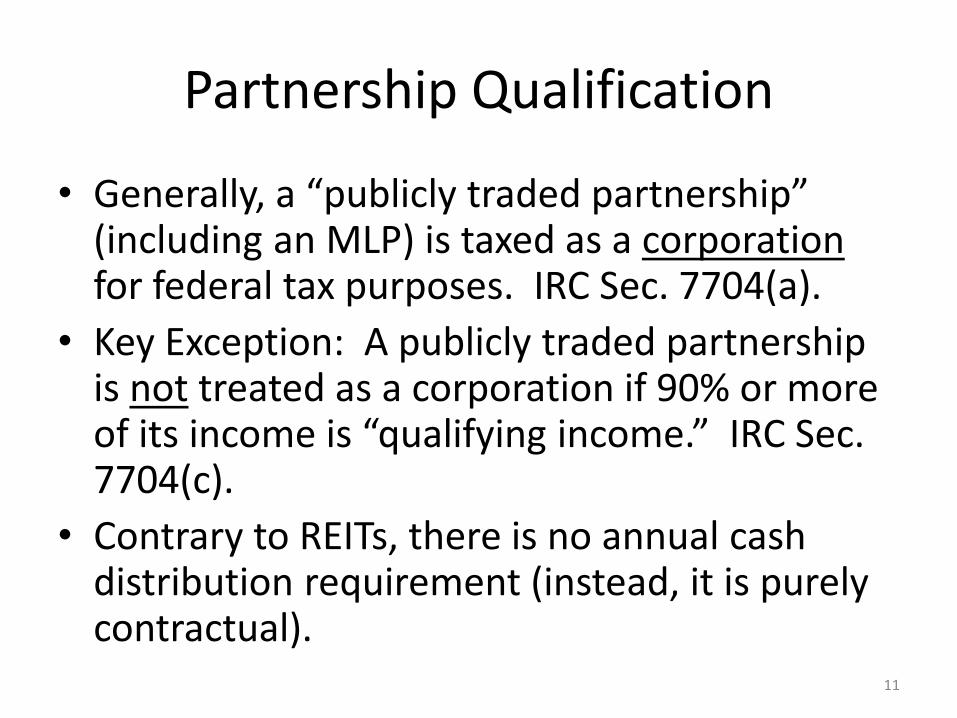

• Generally, a “publicly traded partnership” (including an MLP) is taxed as a corporation for federal tax purposes. IRC Sec. 7704(a).

• Key Exception: A publicly traded partnership is not treated as a corporation if 90% or more of its income is “qualifying income.” IRC Sec. 7704(c).

• Contrary to REITs, there is no annual cash distribution requirement (instead, it is purely contractual).

11

Qualifying Income

• Interest. • Dividends. • Real property rents (cross references the REIT

definition of “rents from real property”). – Real property can be in either an MLP or a REIT. – Historically REITs are preferred over MLPs for real

property and have traded at a higher multiple. • Gain from the sale of real property (even by

“dealers”). • Natural resource exception!

12

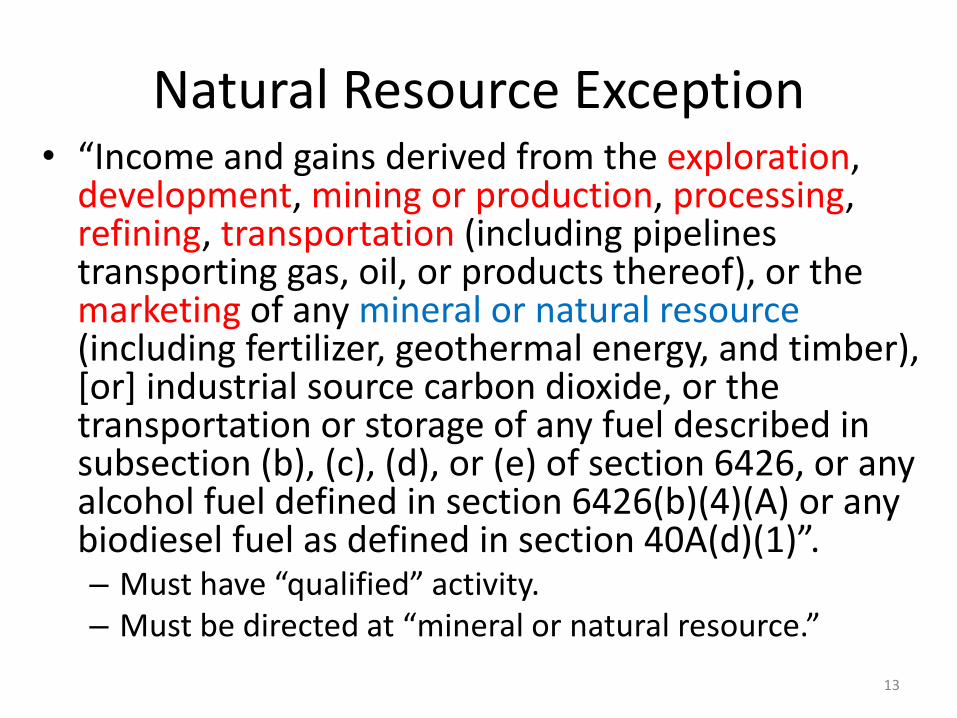

Natural Resource Exception • “Income and gains derived from the exploration,

development, mining or production, processing, refining, transportation (including pipelines transporting gas, oil, or products thereof), or the marketing of any mineral or natural resource (including fertilizer, geothermal energy, and timber), [or] industrial source carbon dioxide, or the transportation or storage of any fuel described in subsection (b), (c), (d), or (e) of section 6426, or any alcohol fuel defined in section 6426(b)(4)(A) or any biodiesel fuel as defined in section 40A(d)(1)”. – Must have “qualified” activity. – Must be directed at “mineral or natural resource.”

13

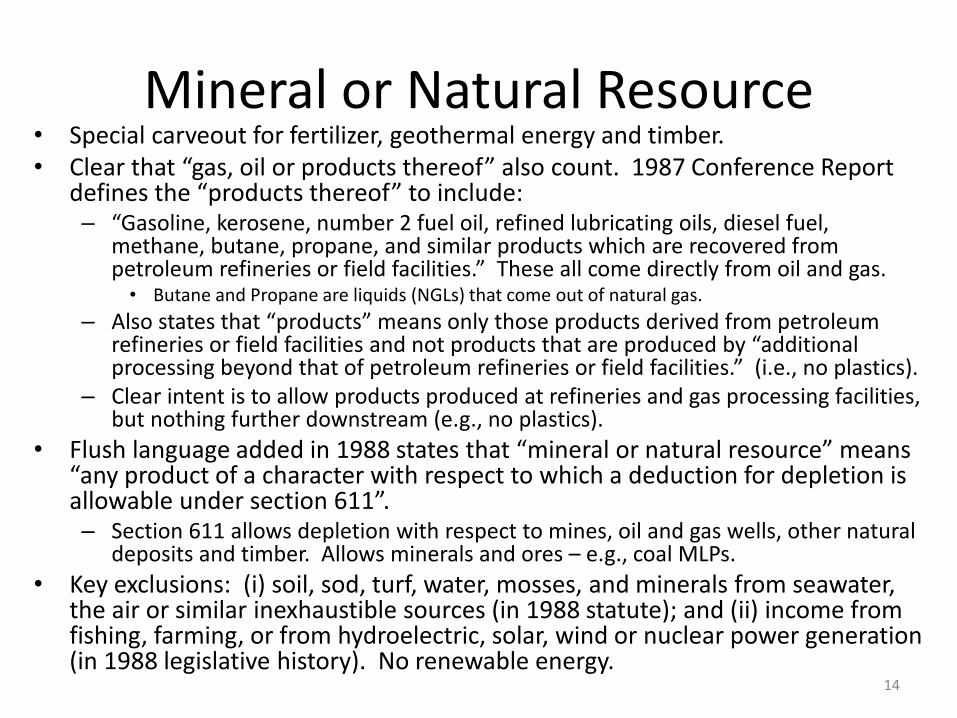

Mineral or Natural Resource • Special carveout for fertilizer, geothermal energy and timber. • Clear that “gas, oil or products thereof” also count. 1987 Conference Report

defines the “products thereof” to include: – “Gasoline, kerosene, number 2 fuel oil, refined lubricating oils, diesel fuel,

methane, butane, propane, and similar products which are recovered from petroleum refineries or field facilities.” These all come directly from oil and gas. • Butane and Propane are liquids (NGLs) that come out of natural gas.

– Also states that “products” means only those products derived from petroleum refineries or field facilities and not products that are produced by “additional processing beyond that of petroleum refineries or field facilities.” (i.e., no plastics).

– Clear intent is to allow products produced at refineries and gas processing facilities, but nothing further downstream (e.g., no plastics).

• Flush language added in 1988 states that “mineral or natural resource” means “any product of a character with respect to which a deduction for depletion is allowable under section 611”. – Section 611 allows depletion with respect to mines, oil and gas wells, other natural

deposits and timber. Allows minerals and ores – e.g., coal MLPs. • Key exclusions: (i) soil, sod, turf, water, mosses, and minerals from seawater,

the air or similar inexhaustible sources (in 1988 statute); and (ii) income from fishing, farming, or from hydroelectric, solar, wind or nuclear power generation (in 1988 legislative history). No renewable energy.

14

Qualified Activities • The “activities” in IRC Sec. 7704(d)(1)(E) are not

defined. They include: – Exploration. – Development. – Mining or Production. – Processing. – Refining. – Transportation. – Marketing.

• But see legislative history forbidding “marketing minerals and natural resources to end users at the retail level” (e.g., gas station operations are specifically excluded).

• Note that legislative history also mentions “storage.”

15

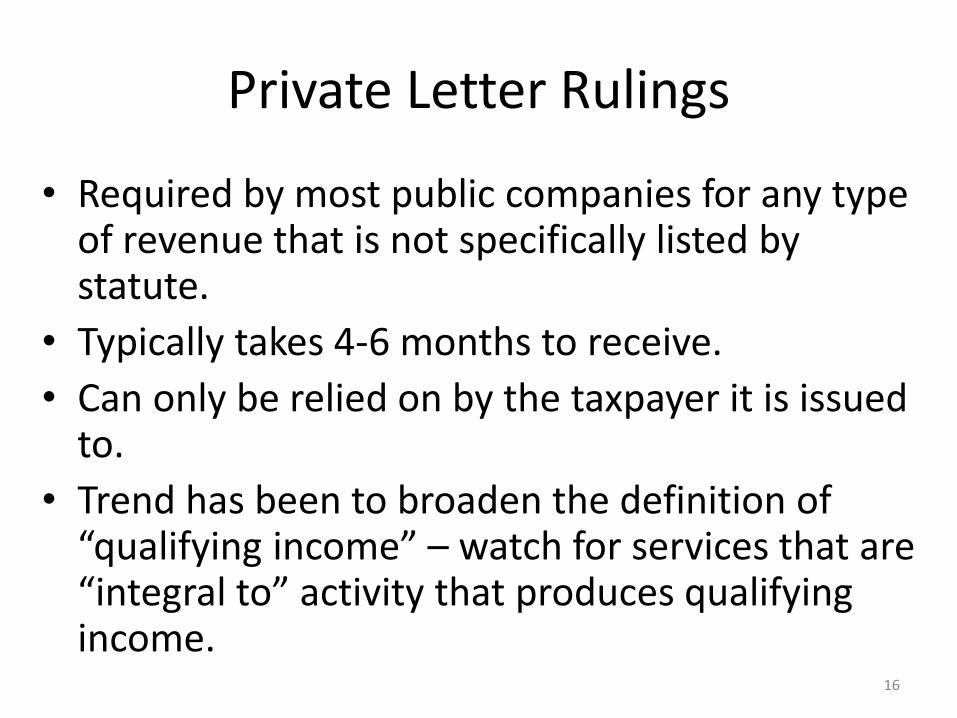

Private Letter Rulings

• Required by most public companies for any type of revenue that is not specifically listed by statute.

• Typically takes 4-6 months to receive. • Can only be relied on by the taxpayer it is issued

to. • Trend has been to broaden the definition of

“qualifying income” – watch for services that are “integral to” activity that produces qualifying income.

16

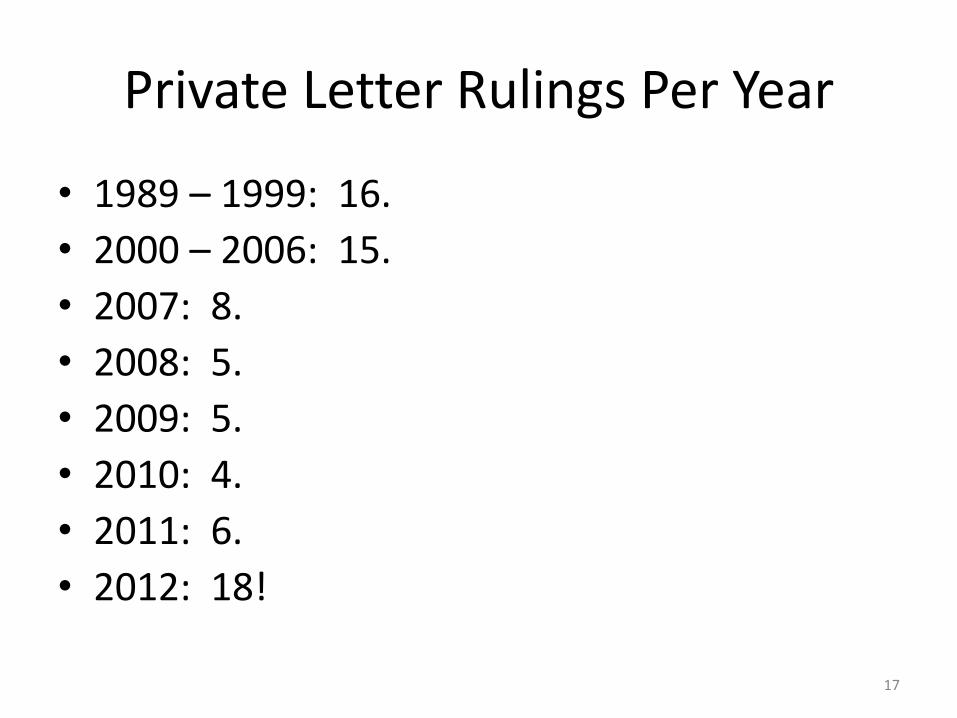

Private Letter Rulings Per Year

• 1989 – 1999: 16. • 2000 – 2006: 15. • 2007: 8. • 2008: 5. • 2009: 5. • 2010: 4. • 2011: 6. • 2012: 18!

17

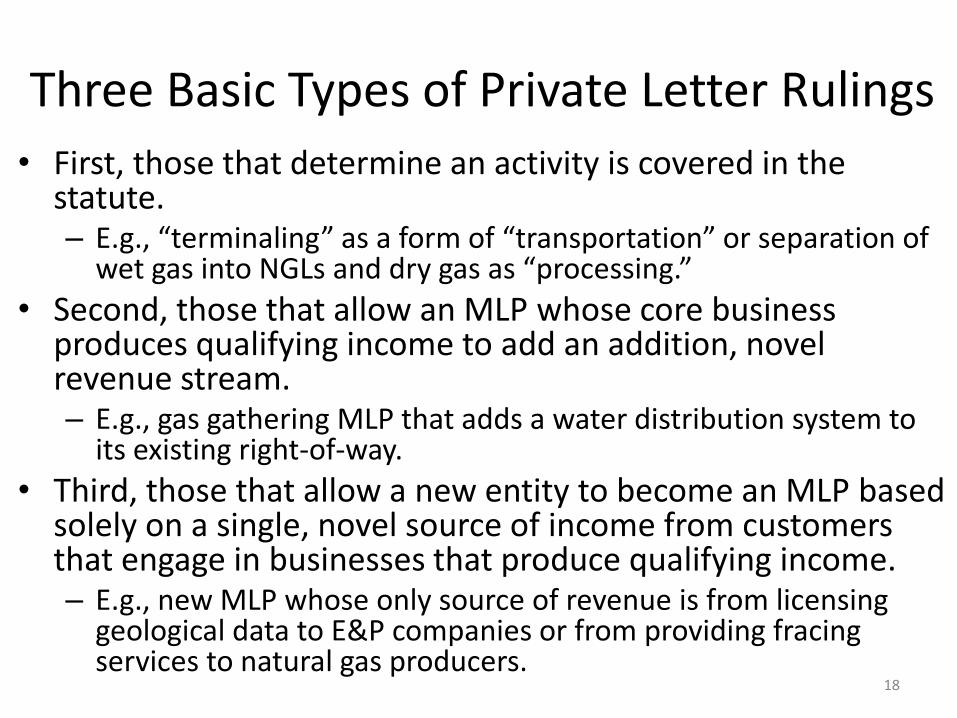

Three Basic Types of Private Letter Rulings • First, those that determine an activity is covered in the

statute. – E.g., “terminaling” as a form of “transportation” or separation of

wet gas into NGLs and dry gas as “processing.” • Second, those that allow an MLP whose core business

produces qualifying income to add an addition, novel revenue stream. – E.g., gas gathering MLP that adds a water distribution system to

its existing right-of-way. • Third, those that allow a new entity to become an MLP based

solely on a single, novel source of income from customers that engage in businesses that produce qualifying income. – E.g., new MLP whose only source of revenue is from licensing

geological data to E&P companies or from providing fracing services to natural gas producers.

18

Trends in Private Letter Rulings

• Early PLRs allowed income streams that fit easily with the scope of the statute. Examples: – 199338028: Income from sales of plywood and

fiberboard produced from timber. Treated as income from “processing” of timber.

– 199339014: Sale of nitric acid and carbon dioxide produced as a bi-product of fertilizer production.

– 199452013: Income from storage of natural gas. – 199639011: Income from “processing” wet natural

gas into NGLs and dry gas.

19

Early “Integral to” Rulings

• 199340031: Taxpayer conducted “terminaling” operations for petroleum products and represented that terminaling activities were an “integral part of the transportation of oil and gas and products thereof.” IRS ruled that the terminaling activities were “integral to the transportation of petroleum and related products.” Therefore, the fees were qualifying income.

• 199619011: If owners of oil and gas purchase derivative products to hedge price changes, income from such products is “integral to” a qualifying activity and gives rise to qualifying income.

20

Current “Integral to” Rulings • 200845035: X’s core business was transportation, gathering and storage

of natural gas. Also entered into “interconnect agreements” whereby new customers agreed to reimburse X for cost of constructing pipeline extensions to customer’s fields. X represented that (i) the interconnect agreements were “an integral party of the tranportation of oil, gas, and/or products thereof” and (ii) that the “sole purpose of the interconnect agreement is to facilitate the transportation and/or gathering agreement.”

• IRS ruled that “the interconnect agreements are integral to the transportation and/or gathering of gas, oil, or products thereof. Therefore, the amounts X receives from pipeline transportation customers as reimbursement for construction of pipeline extensions . . . for the transportation of gas, oil, or products thereof constitute qualifying income within the meaning of § 7704(d)(1)(E).”

• However, the ruling did not extend to any amount of the reimbursement payments that exceeded the pipeline extension construction costs.

• Note that X’s core business was transportation and gathering, which clearly produce qualifying income.

21

Current “Integral to” Rulings • 200909006. X was in the business of “acquiring and licensing

land and marine seismic data to oil and gas producers.” X maintained a library of seismic data for license to oil and gas producers.

• X represented that (i) aside from oil and gas exploration, there is no other commercial use for X’s seismic data, and (ii) “the seismic data services provided by X are integral to the exploration of oil and gas resources, because the exploration . . . of oil and gas resources would be significantly curtailed in the absence of such services.”

• X sought the ruling in conjunction with an IPO of a new MLP. • IRS ruled that X’s incomd from acquiring and licensing seismic

data to oil and gas producers for use in their exploration activity produced qualifying income.

• Note that this is the first ruling involving a separate income stream that is not related to a core MLP business.

22

Current “Integral to” Rulings • 201025037. X conducted a marine terminaling business. The

terminal included marine docks for LNG tankers to offload imported LNG. X’s terminals then converted the LNG back to gas in a process called regasification. Through a disregarded entity, X also provided marine services to customers using the marine terminals. Services included: escorting LNG vessels; assisting in berthing and unberthing the vessels; “standing-by” the vessels at all times while docked; performing fire-fighting, life saving and emergency response services; conducting salvage or marine wreckage services; and providing picket boat services. X used specially-designed tug boats to provide these services. X represented that the marine services were “an integral and necessary part of the terminal’s operations of transporting and processing the LNG delivered to the terminal.”

• IRS ruled that the income from marine services was qualifying income.

• Note that X’s core income from terminaling was qualifying income. 23

Current “Integral to” Rulings • 201226018: X was in the “extractive logistics” business. X derived income

from delivery and sale of refined petroleum products (diesel fuel and lubricating oil), antifreeze, methanol, and other chemicals to E&P customers at the drilling sites. Services also included online reporting of fuel deliveries; on-site refueling of customer’s oil and gas drilling equipment; removal, recycling and disposal of used oil, lubricants, and non-hazardous waste from drilling; maintenance of drilling rig equipment; equipment inspections; provision of storage tanks; and supply and/or transportation of fracturing fluid to well sites, supply of “frac tanks,” removal of production fluid and flowback generated in the fracturing process, and the disposal or treatment of the production fluid or flowback. X represented that the extractive logistics services were “integral to the exploration, production and development of oil, gas and coal resources” because such activity “would be significantly curtailed in the absence of such services.”

• IRS ruled that “X’s gross income from the extractive logistics business (excluding any portion of such income derived from the delivery or sale of products to customers who are not engaged in drilling, exploration and production, or mining activities) . . . is qualifying income. “

• Note that X otherwise did not have a core “qualifying income” stream. 24

Current “Integral to” Rulings • 201227001: X is principally derives income from the

exploration, development, mining or production, transportation, and marketing of a mineral or natural resource. X also expects to derive income from the transportation of refined petroleum products and other products to customers engaged in E&P operations at the drilling sites. X represented that (i) the vehicles used to provide these services are specially designed and custom built to deliver products to above-ground tanks in remote locations and (ii) the services provided “are integral to the exploration, production and development of oil, gas and coal resources” because such activities “would be significantly curtailed in the absence of such services.”

• IRS ruled that X’s gross income from the transportation of refined petroleum products and other products to customers engaged in E&P activity at the site of such activity is qualifying income.

25

Current “Integral to” Rulings • 201234005: X engaged in the transportation and processing of natural

gas (via gathering lines, pipelines and processing facilities). X’s customers are natural gas producers that use hydraulic fracturing (“fracing”) to extract natural gas. Fracing requires large volumes of water. To meet the water needs of its customers, X (through a subsidiary) constructed and operated a water delivery pipeline for the purpose of supplying water to X’s customers and other natural gas producers for use in the production of natural gas through fracing. Under the water agreements, customers will pay X for the pipeline supply and transportation of fresh water. X represented that the supply and transportation of water to natural gas producers for use in fracing was “integral to the exploration and production of natural gas from shale formations and the preservation and growth of X’s existing activity of natural gas transportation.”

• IRS ruled that X's gross income derived from the supply and transportation of water to oil and gas producers for use in the exploration, development, and production of oil or natural gas is qualifying income

26

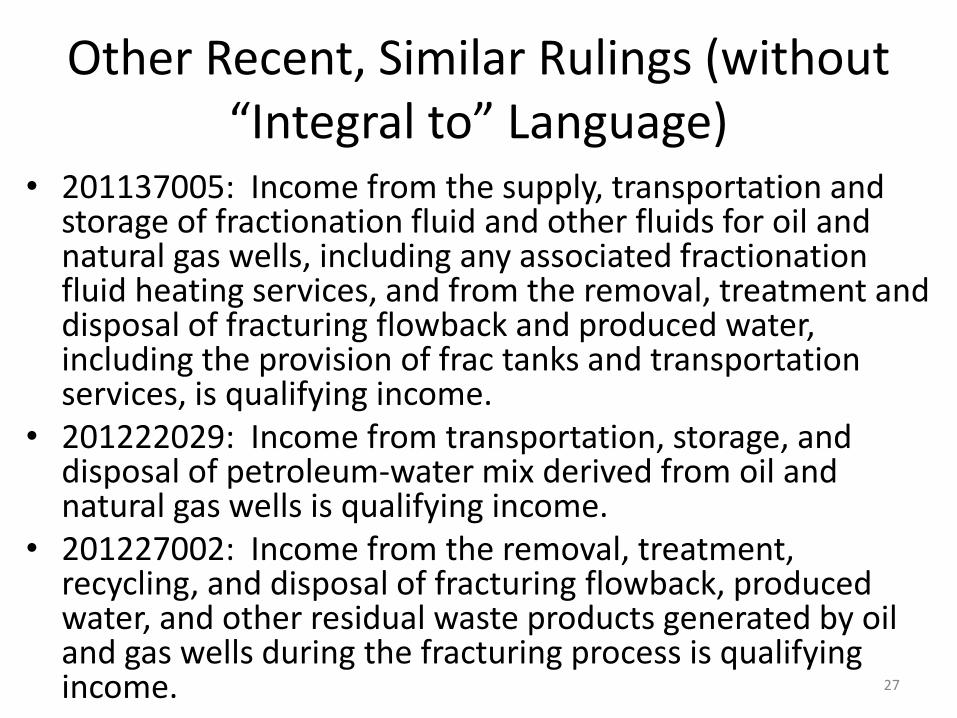

Other Recent, Similar Rulings (without “Integral to” Language)

• 201137005: Income from the supply, transportation and storage of fractionation fluid and other fluids for oil and natural gas wells, including any associated fractionation fluid heating services, and from the removal, treatment and disposal of fracturing flowback and produced water, including the provision of frac tanks and transportation services, is qualifying income.

• 201222029: Income from transportation, storage, and disposal of petroleum-water mix derived from oil and natural gas wells is qualifying income.

• 201227002: Income from the removal, treatment, recycling, and disposal of fracturing flowback, produced water, and other residual waste products generated by oil and gas wells during the fracturing process is qualifying income. 27

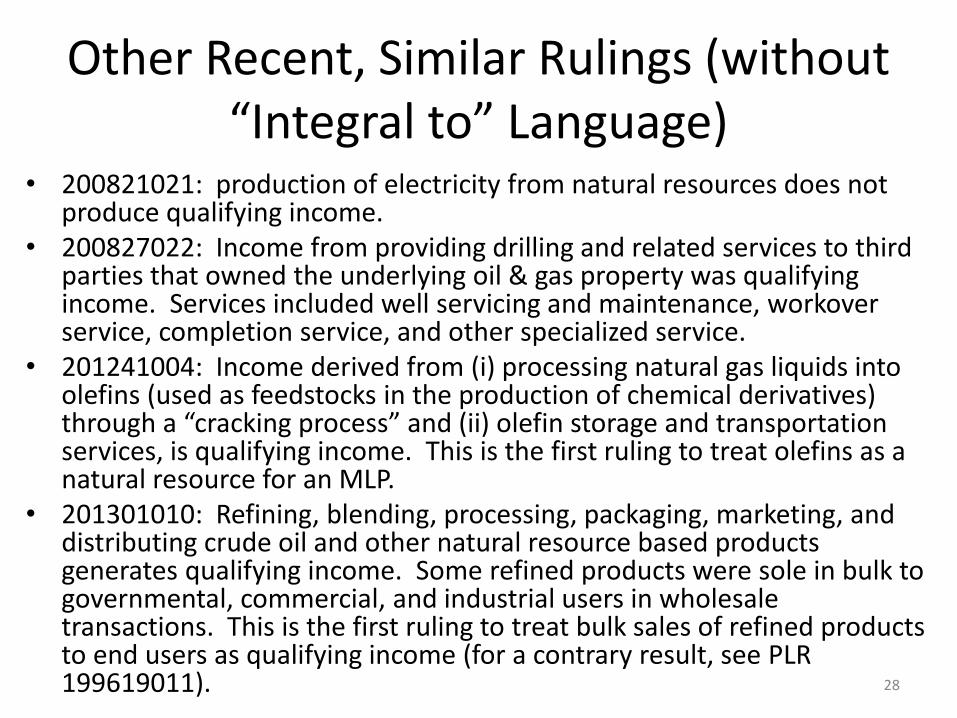

Other Recent, Similar Rulings (without “Integral to” Language)

• 200821021: production of electricity from natural resources does not produce qualifying income.

• 200827022: Income from providing drilling and related services to third parties that owned the underlying oil & gas property was qualifying income. Services included well servicing and maintenance, workover service, completion service, and other specialized service.

• 201241004: Income derived from (i) processing natural gas liquids into olefins (used as feedstocks in the production of chemical derivatives) through a “cracking process” and (ii) olefin storage and transportation services, is qualifying income. This is the first ruling to treat olefins as a natural resource for an MLP.

• 201301010: Refining, blending, processing, packaging, marketing, and distributing crude oil and other natural resource based products generates qualifying income. Some refined products were sole in bulk to governmental, commercial, and industrial users in wholesale transactions. This is the first ruling to treat bulk sales of refined products to end users as qualifying income (for a contrary result, see PLR 199619011).

28

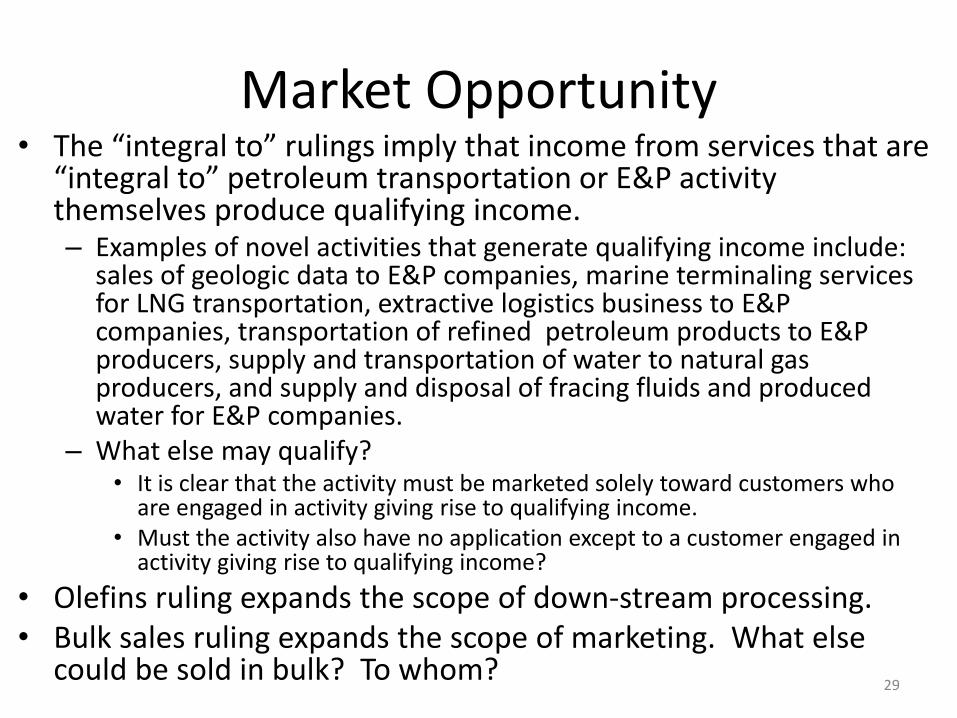

Market Opportunity • The “integral to” rulings imply that income from services that are

“integral to” petroleum transportation or E&P activity themselves produce qualifying income. – Examples of novel activities that generate qualifying income include:

sales of geologic data to E&P companies, marine terminaling services for LNG transportation, extractive logistics business to E&P companies, transportation of refined petroleum products to E&P producers, supply and transportation of water to natural gas producers, and supply and disposal of fracing fluids and produced water for E&P companies.

– What else may qualify? • It is clear that the activity must be marketed solely toward customers who

are engaged in activity giving rise to qualifying income. • Must the activity also have no application except to a customer engaged in

activity giving rise to qualifying income? • Olefins ruling expands the scope of down-stream processing. • Bulk sales ruling expands the scope of marketing. What else

could be sold in bulk? To whom?

29

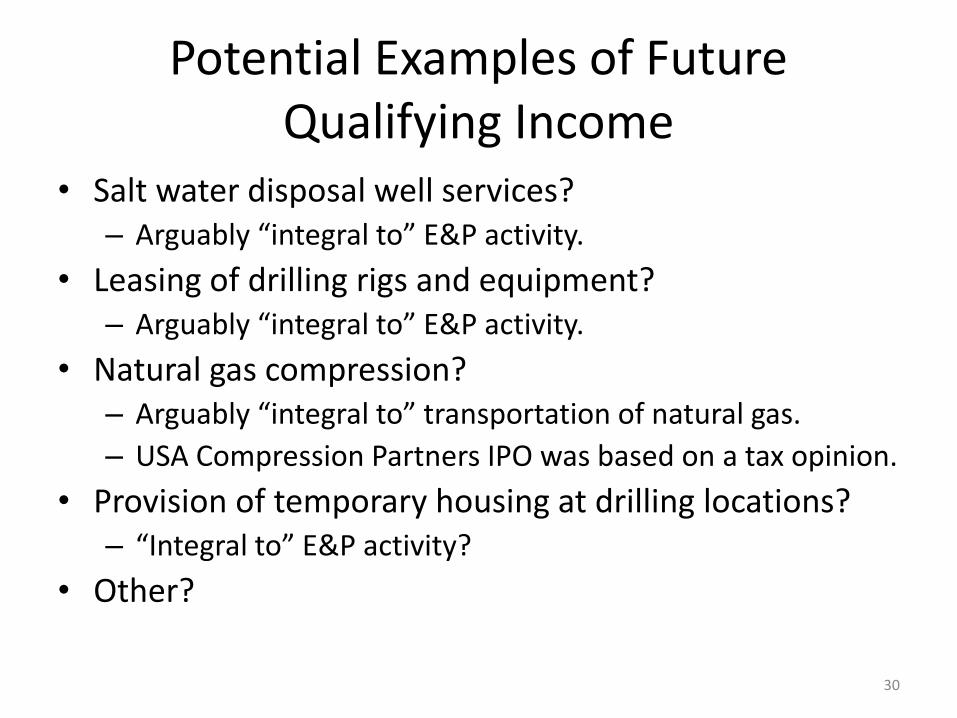

Potential Examples of Future Qualifying Income

• Salt water disposal well services? – Arguably “integral to” E&P activity.

• Leasing of drilling rigs and equipment? – Arguably “integral to” E&P activity.

• Natural gas compression? – Arguably “integral to” transportation of natural gas. – USA Compression Partners IPO was based on a tax opinion.

• Provision of temporary housing at drilling locations? – “Integral to” E&P activity?

• Other? 30