currency trader (200708)

DESCRIPTION

TRANSCRIPT

August 2007

Volume 4, No. 8

Strategies, analysis, and news for FX Traders

DOLLAR AT THE CROSSROADS:Battered buck testing key levels p. 38

TREND RUNS IN CURRENCIES:Facts and figures p. 16

EXOTIC CURRENCIES:Trading outside the “majors” p. 8

THE YEN’S new uptrend? p. 12

LONG-TERM INTEREST RATES:Implications for currencies p. 34

INTERNATIONALTRADE AND CURRENCIES,part 2 p. 26

Contributors . . . . . . . . . . . . . . . . . . . . .6

Global MarketsBeyond the majors: The exotic waters of emerging-market currencies . . . . . .8Some forex brokers are offering access tomore currency pairs, but you need to knowthe risks associated with these markets beforeyou consider trading them.By Currency Trader Staff

On the MoneyThe rising yen — here we go again . . . . . . . . . . . . . . . .12The yen has been on the rise vs. the dollar. Find out if it’s a reversal or just a correction.By Barbara Rockefeller

Trading StrategiesShort-term trends in the EUR/USD pair . . . . . . . . . . . . .16This study shows how often different runs of consecutive higher or lower highs, lows, and closes occur in the euro/dollar pair. By Currency Trader Staff

Advanced StrategiesMinor currencies and federal reserve trade weights . . . . . .26A continuation of last month’s analysis of the relationship between trade and currencies undermines one of the basic premises of the floating exchange-rate system. By Howard L. Simons

Trading BasicsLong-term interest rates and the U.S. dollar . . . . . . . . . . . . . . .34What the recent rise in T-bond and T-noteyield implies for the FX market. By David Mantell

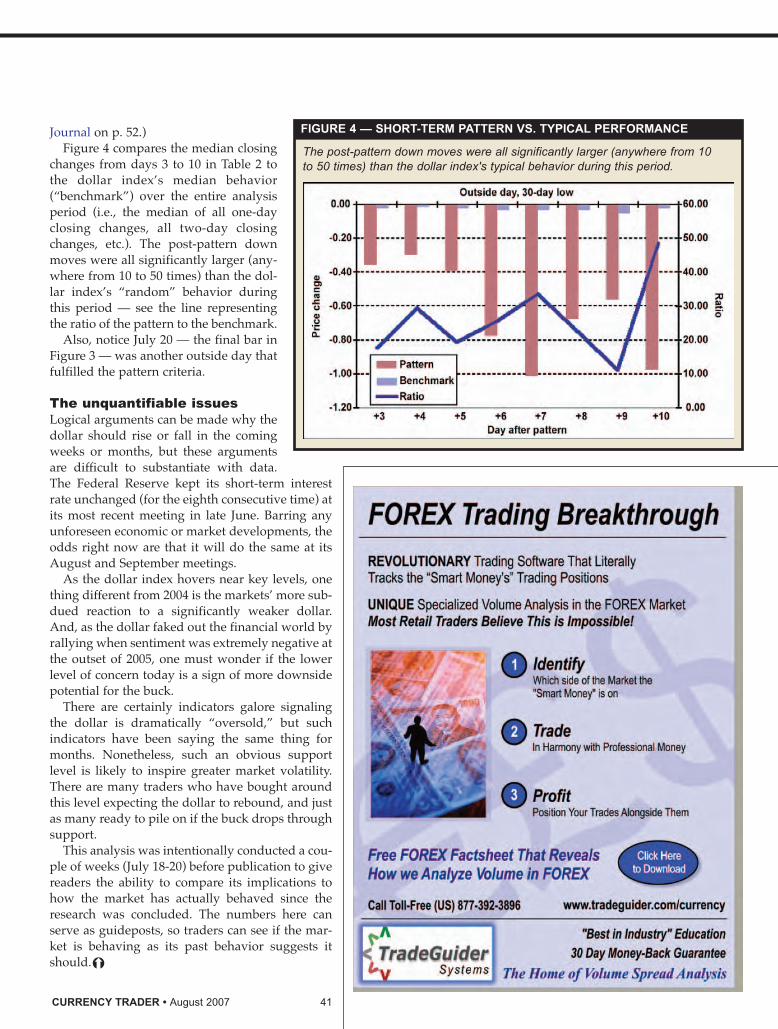

Spot CheckU.S. dollar index . . . . . . . . . . . . . . . .38The greenback has recently established all-time lows against many currencies. Find out what analysis of the dollar index says about the probabilities of the buck’s next move.By Currency Trader Staff

CONTENTS

2 August 2007 • CURRENCY TRADER

continued on p. 4

4 August 2007 • CURRENCY TRADER

CONTENTS

Have a question about something you’ve seen in Currency Trader?

Submit your editorial queries or comments to

Looking for an advertiser?Consult the list below and click on the company name for a direct link to the ad in this month’s

issue of Currency Trader.

Advertising index

Industry NewsNew NFA proposal could cause significant shakeup among forex brokerages . . . . . . . . . . . . . . . .42The National Futures Association wants new capital requirements that could force several forex brokerages out of business.

USFE to list forex futures . . . . . . . . .42The United States Futures Exchange will roll out currency futures that mimic the pricing of spot forex positions.

Currency Futures . . . . . . . . . . . . . . .44Currency fund manager performance.

Global News Briefs . . . . . . . . . . . . .45

International Market Summary . . . . . . . . . . . . . . . . . . . . . . .46

Currency, interest rate, and equity performance from around the globe.

Global Economic Calendar . . . . . . . . .48Key dates for currency traders.

New Products and Services . . . . . . . . .49

The Face of Trading . . . . . . . . . . . . . . .49Rolling with the punches.

Key Concepts . . . . . . . . . . . . . . . . . . . .50

Events . . . . . . . . . . . . . . . . . . . . . . . . . .51Conferences, seminars, and other events.

Forex Trade Journal . . . . . . . . . . . .52Too late to sell the dollar? A position in the dollar index futures tells the tale.

CMS Forex

Currency Trader Bookstore

Deutsche Bank

eSignal

Forex.com

Forex Expo

Forexrtadingseminar.com

FXCM

FXStreet.com

InterbankFX

Market Technicians Assoc.

MetaStock

NewsTrader Pro

TradeGuider

About the authorEdward Ponsi is the President of FXEducator LLC and is the former Chief Trading Instructor for Forex Capital Markets (FXCM). An experienced trader and mentor, Ed gives personal, one-on-one trading instruction to students around the world, and has advised hedge funds, Interbank traders, and individuals of all levels of skill and experience.

Why is it the fastest growing segment for individual investors and many former equity and futures traders?

MetaStock, the leading creator of technical analysis software, is excited about the FOREX market — and for good reason. It’s one of the best ways for YOU to get started in investing. To help you along, we want to give you a FREE copy of “Successful FOREX Trading.” Written by the former Chief Trading Instructor for FOREX Capital Markets. This book explains technical analysis as it relates to currency trading. This valuable information is FREE, no strings attached. To get your copy, visit our web site, or give us a call at (800) 432-4917 and mention the promotion code CT67

Click Here for your FREE Book

This is neither a solicitation to buy or sell any type of financial instruments, nor intended as investment recommendations. All investment trading involves multiple substantial risks of mon-etary loss. Don’t trade with money you can’t afford to lose. Trading is not suitable for everyone. Past performance, whether indicated by actual or hypothetical results or testimonials are no guarantee of future performance or success. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE SHOWN. IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL PERFORMANCE RESULTS OR TESTIMONIALS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY ANY PARTICULAR TRADING PROGRAM. Furthermore, all internal and external computer and software systems are not fail-safe. Have contingency plans in place for such occasions. Equis International assumes no responsibility for errors, inaccuracies, or omissions in these materials, nor shall it be liable for any special, indirect, incidental, or consequential damages, including without limitation losses, lost revenue, or lost profits, that may result from the reliance upon the information materials presented.

FOREXBy far the largest cash value traded market in the world. The trade happening in the forex markets across the globe currently exceeds US$1.9 trillion/day (on average).

FREE Book

�Howard Simons is president of

Rosewood Trading Inc. and a strategist for

Bianco Research. He writes and speaks fre-

quently on a wide range of economic and

financial market issues.

� Barbara Rockefeller (http://www.rts-forex.com) is an

international economist with a focus on foreign exchange. She

has worked as a forecaster, trader, and consultant at Citibank

and other financial institutions, and currently publishes two

daily reports on foreign exchange. Rockefeller is the author of

Technical Analysis for Dummies (For Dummies, 2004), 24/7

Trading Around the Clock, Around the World (John Wiley &

Sons, 2000), The Global Trader (John Wiley & Sons, 2001), and

How to Invest Internationally, published in Japan in 1999. A

book tentatively titled How to Trade FX is in the works.

� David Mantell is a currency trader at Chicago Global

Investors, where he trades currency futures in the euro, yen,

British pound, Swiss franc, and Canadian dollar. He began his

career in the financial markets 15 years ago as a financial

advisor. Mantell is a former equity research analyst, having

covered the media & telecommunications (wireline and wire-

less) industries. As part of his MBA, Mantell attended the

ESSEC Business School in Paris. He can be contacted at

� Thom Hartle (http://www.thomhartle.com) is director

of marketing for CQG and a contributing edi-

tor to Active Trader magazine. In a career span-

ning more than 20 years, Hartle has been a

commodity account executive for Merrill

Lynch, vice president of financial futures for

Drexel Burnham Lambert, trader for the

Federal Home Loan Bank of Seattle, and edi-

tor for nine years of Technical Analysis of Stocks & Commodities

magazine. Hartle also writes a daily market blog called hartle

& flow (http://www.hartleandflow.com).

6 August 2007 • CURRENCY TRADER

Editor-in-chief: Mark [email protected]

Managing editor: Molly [email protected]

Senior editor: Jeff Ponczak [email protected]

Contributing writers:Barbara Rockefeller,

Howard Simons, Marc Chandler

Editorial assistant andWebmaster: Kesha Green

Art director: Laura [email protected]

President: Phil [email protected]

Publisher,Ad sales East Coast and Midwest:

Ad sales West Coast and Southwest only:

Allison [email protected]

Classified ad sales: Mark [email protected]

Volume 4, Issue 8. Currency Trader is published monthly by TechInfo, Inc., 150 S. Wacker Drive, Suite 880, Chicago, IL 60606. Copyright © 2007TechInfo, Inc. All rights reserved. Information in this publication may not bestored or reproduced in any form without written permission from the publisher.

The information in Currency Trader magazine is intended for educational pur-poses only. It is not meant to recommend, promote or in any way imply theeffectiveness of any trading system, strategy or approach. Traders are advisedto do their own research and testing to determine the validity of a trading idea.Trading and investing carry a high level of risk. Past performance does notguarantee future results.

For all subscriber services:www.currencytradermag.com

A publication of Active Trader®

CONTRIBUTORSCONTRIBUTORS

While the vast majority of forex tradingoccurs in the so-called “majors” — thecurrencies of G-10 countries — someretail forex brokerages are beginning to

expand their offerings to include emerging-market or“exotic” currencies.

Such currencies include the Mexican peso, South Africanrand, Singapore dollar, Thailand baht, Brazilian real, andHong Kong dollar.

There are many reasons forex trading revolves around ahandful of currency pairs, most of which include either theU.S. dollar or the euro, but the most important are liquidityand stability. It’s often said the forex market is the most liq-uid in the world, and that liquidity is based on the stabilityof a few countries and regions that, through history and for-tune, have come to dominate global trade and finance. It isno coincidence that oil and gold are priced globally in dol-lars.

For example, Brazil is a developing country at the fore-front of a Latin American boom — several countries arebucking for “first-world” status. But despite the fact it’s hadone of the hottest currencies in recent years, Brazil has gonethrough a few “new” currencies in the past two decades asits economy has busted and boomed.

Nonetheless, some emerging market currencies are edg-ing into the mainstream of the forex world.

Why trade exotics?Some analysts contend exotic currencies tend to trend bet-ter than the majors because their economies are often nar-rowly focused, or even dependent on one specific industryor investment theme.

GFT Forex and Oanda.com currently include exotic cur-rency trading on their retail trading platforms.

“Exotic currency pairs provide traders with the ability totake advantage of trends that can be established by largemoney taking positions in these less-liquid currencies,”says Paul Jamgotch, dealing desk manager at GFT. “Exoticsare also attractive to traders who keep their eyes on the fun-damental factors that can affect these smaller financial mar-kets. Also, it gives retail traders a way to speculate in theeconomies of countries that don’t offer easy access to othertrading vehicles, such as bonds or stocks.”

Diversification is another argument in favor of expand-ing into the exotic arena.

“Having exposure to just the major pairs really narrowsthe scope of a trader’s portfolio,” says Richard Lee, curren-cy strategist at FXCM. “Portfolio returns in emerging mar-kets are also outpacing major-currency investments.”

While FXCM currently does not provide access to emerg-ing market currencies on their retail platform, they do pro-vide research in the Hong Kong and Singapore dollars, aswell as the Chinese yuan.

“Additional instruments are good because they offer

GLOBAL MARKETS

Beyond the majors: The exotic waters

of emerging market currencies

8 August 2007 • CURRENCY TRADER

BY CURRENCY TRADER STAFF

Experience required: There are opportunities in emerging-market currencies, but traders should

nonetheless be careful about venturing outside the highly liquid major currency pairs.

Some strategists caution that only the

most seasoned retail players should

enter the exotic currency arena

because of its higher volatility, lower

liquidity, and wider spreads.

CURRENCY TRADER • August 2007 9

diversification,” says Richard Olsen, co-founder ofOanda.com. “Anyone trading any market wants to diversi-fy.”

Oanda gradually began adding exotic cross rates to itsretail platform starting in 2006 and Olsen says it has beenmet with “an astonishing amount of interest.” Oanda has a fairly wide offering of exotic currency crosses, includingcrosses with the euro dollar vs. emerg-ing market currencies. (For a list of Oanda’s current exotic pairs offer-ings see: https://fxtrade.oanda.com/spreads/all_spreads.shtml.)

Higher risk levelsWith opportunity, of course, comesrisk. Brian Dolan, chief currencystrategist at Forex.com, a division ofGain Capital, says his firm currentlydoes not offer emerging market cur-rencies to retail clientele because of liq-uidity and the lack of running prices.

“There is tremendous potential insome of the [exotic currencies], but it isa whole new level of risk versus the G-10 currencies,” he says.

Wider spreads, more volatilityForex traders should not jump into theworld of the exotics without a greatdeal of research and understanding ofthe risks associated with these curren-cies. Some strategists caution that onlythe most seasoned retail playersshould enter this arena because of thehigher volatility, lower liquidity, andwider spreads these currencies tend todisplay.

“The spreads on exotics can be fair-ly wide because these markets are lessliquid,” says GFT’s Jamgotch. “Retailtraders need to keep in mind there islimited liquidity in many exotic pairs,which means spreads tend to widenwhen these local financial markets arenot open.

“The typical GFT spread for theUSD/ZAR (U.S. dollar/South Africanrand pair) is 150 pips, and during somemarket conditions, such as when theSouth African market is closed, it is notuncommon for the spread to widen tomore than 500 pips.”

FXCM’s Lee says volatility and liq-uidity are bigger concerns than people

think when trading emerging markets because retailtraders are not used to violent fluctuations.

”Unless retail investors trade crosses such as thepound/yen, they are more [accustomed to] 30-pip dailyfluctuations,” he says. “The rand moves almost 10 timesthat in single session. However, you always have to take

continued on p. 10

into account the pip cost, which essentially puts things backinto perspective.”

A pip in the ZAR currently is worth about $1.45 vs., say,roughly $10 for a pip in the euro/dollar pair.

“Another factor retail traders should be aware of is thevolatility in exotic currencies around fundamental newsreleases can be much higher than in major currencies,” saysGFT’s Jamgotch. “This means market gaps and slippage aremore common.”

Keep things smallAs market conditions can shift rapidly in the exotic curren-cy environment, strategists advise retail customers to mon-itor and limit position sizes carefully.

“Exotic currencies can become very volatile and illiquidwithout warning,” Jamgotch says.

For example, he pointed to when the Thai baht fell morethan four percent against the U.S. dollar in December 2006when the Bank of Thailand imposed penalties on invest-ments held for less than a year. Spreads on the U.S. dol-lar/Thai baht cross spiked from 5 pips to 100 or more,depending on the institution. Jamgotch says many marketmakers chose not to offer Thai baht crosses during this tur-bulent time.

Exotic currency traders also have to face the reality that itmay be difficult to exit positions because of lack of liquidi-ty outside of local trading hours.

“At the end of the day, it is almost like a futures marketposition, when the futures close at 2 o’clock and you can’tget out until the next day,” warns Forex.com’s Dolan. Forexample, he notes that outside of North American tradinghours, liquidity is “pretty poor” in the Mexican peso.

“Whatever you do, put on smalltrades,” suggests Oanda co-founderOlsen.

Longer-term playsGiven the wider spreads and reducedliquidity of some exotic currencies,some strategists feel the longer-termtime frame is a better choice than daytrading in this arena. Dolan cautionsthose interested in expanding into theexotics.

“For the retail guy, the risks probablyoutweigh the rewards,” he says. “If theydo get into it, it has to be more of astrategic and longer-term play.”

Olsen agrees on the time frame out-look.

“While a euro/dollar trader mighttrade a two- to three-hour position, ayuan play could last two to five weeks,”he says. “Trades put on in emergingmarket currencies are different in

nature, and tend to be on more of a long-term time frame.”

Do your homeworkGaining access to the appropriate fundamental informationneeded to make trading decisions may be harder whenlooking at the exotic currency landscape.

“There are fewer news announcements and bankresearch available for some of these exotic currencies,” saysGFT’s Jamgotch. “This means that it can be more difficultfor retail traders to conduct proper research needed tomake informed decisions based on fundamental data.”

“Exotic” to watch: South African randFXCM’s Lee says the South African rand (ZAR) is a curren-cy to watch near-term (Figure 1).

“Given the recent attention on carry trades and interestrates, I still think that the ZAR has some potential,” he says.”Technically, however, I might be waiting a bit for a betterprice, as we’re approaching a major support level (in lateJuly).”

The South African Reserve Bank hiked interest rates inearly June from 9.0 percent to the current 9.5 percent.Bullish interest-rate differentials alone favor the rand vs.the U.S. dollar’s 5.25 percent fed funds rate.

Looking at the differential, Lee says it’s still a good per-centage to play.

Rand: Key fundamentalsGold and platinum prices are two factors that drive theSouth African rand; some traders essentially use the rand asa proxy for the world gold market.

Clyde Wardle, senior emerging market FX strategist at

GLOBAL MARKETS continued

10 August 2007 • CURRENCY TRADER

In late July the U.S. dollar/South African rand pair was just beginning to penetratethe bottom of its long-term range and was trading at its lowest level in a year.

FIGURE 1 — DOLLAR/RAND

Source: ADVFN (http://www.advfn.com)

CURRENCY TRADER • August 2007 11

HSBC, notes the rand strengthened roughly five percentfrom June to July.

“It was at 7.20-7.30 in early June and now it has movedbelow 7.00,” he says.

As of late July, the USD/ZAR was trading at 6.88. Wardlepointed to the rally in the gold market from late June as onefactor supporting the rand in recent weeks.

HSBC forecasts overall grossdomestic product (GDP) growth at 5.4percent for South Africa in 2007, vs.2006’s 5.0-percent reading. Inflationremains high, which has been a drivertoward tighter monetary policy. TheMay CPI ex-food and energy figureposted a 6.4-percent reading year-over-year in South Africa.

“The economy is improving andhas been improving for the past cou-ple of years,” Lee says. “GDP andmanufacturing are healthy and con-sumer spending has picked up.”

Wardle adds in the past the SouthAfrican Reserve Bank had discomfortwith currency strength below 7.00amid worries that it would hurtdomestic manufacturing.

“Given rising inflation, the centralbank should be comfortable with thestrengthening currency,” he says.

Rand: Key price levelsOverall, HSBC forecasts continuedstrengthening in the rand toward 6.75by the end of third quarter. Weaknessis seen into early 2008, with a first-quarter forecast of 7.25.

“I’m looking for a technical break ofthe support the currency pair is cur-rently trading at, around the 6.8606(the May 8 low),” Lee says. “If thislevel is broken, I would be looking toinitiate a long around that area withtargets set at 6.4050, just below the6.427, 76.4-percent Fibonacci retrace-ment of the 5.9446-7.983 bull wave.”

Global risk appetite helps,tooThe global environment remainsfavorable toward emerging markets,which is positive for the rand. Also,given its relatively high interest rate,the rand has been a player in the glob-al carry trade, as well.

“The global risk appetite has

improved,” Wardle says. “Liquidity is still very looseacross the globe, which encourages managers to search foryield.”

The main risk, Wardle warns, is the external environ-ment. If global stock markets were to come under pressure,money managers could trim exposure to emerging-marketpositions, which would likely result in a weaker rand.�

12 August 2007 • CURRENCY TRADER

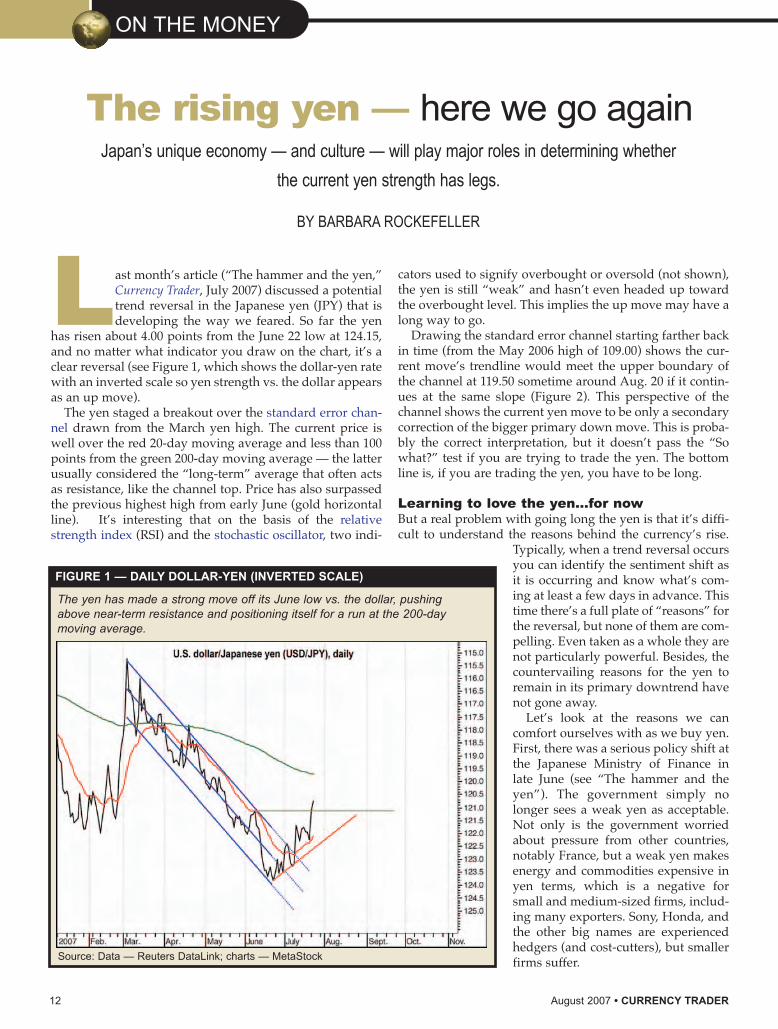

Last month’s article (“The hammer and the yen,”Currency Trader, July 2007) discussed a potentialtrend reversal in the Japanese yen (JPY) that isdeveloping the way we feared. So far the yen

has risen about 4.00 points from the June 22 low at 124.15,and no matter what indicator you draw on the chart, it’s aclear reversal (see Figure 1, which shows the dollar-yen ratewith an inverted scale so yen strength vs. the dollar appearsas an up move).

The yen staged a breakout over the standard error chan-nel drawn from the March yen high. The current price iswell over the red 20-day moving average and less than 100points from the green 200-day moving average — the latterusually considered the “long-term” average that often actsas resistance, like the channel top. Price has also surpassedthe previous highest high from early June (gold horizontalline). It’s interesting that on the basis of the relativestrength index (RSI) and the stochastic oscillator, two indi-

cators used to signify overbought or oversold (not shown),the yen is still “weak” and hasn’t even headed up towardthe overbought level. This implies the up move may have along way to go.

Drawing the standard error channel starting farther backin time (from the May 2006 high of 109.00) shows the cur-rent move’s trendline would meet the upper boundary ofthe channel at 119.50 sometime around Aug. 20 if it contin-ues at the same slope (Figure 2). This perspective of thechannel shows the current yen move to be only a secondarycorrection of the bigger primary down move. This is proba-bly the correct interpretation, but it doesn’t pass the “Sowhat?” test if you are trying to trade the yen. The bottomline is, if you are trading the yen, you have to be long.

Learning to love the yen…for nowBut a real problem with going long the yen is that it’s diffi-cult to understand the reasons behind the currency’s rise.

Typically, when a trend reversal occursyou can identify the sentiment shift asit is occurring and know what’s com-ing at least a few days in advance. Thistime there’s a full plate of “reasons” forthe reversal, but none of them are com-pelling. Even taken as a whole they arenot particularly powerful. Besides, thecountervailing reasons for the yen toremain in its primary downtrend havenot gone away.

Let’s look at the reasons we cancomfort ourselves with as we buy yen.First, there was a serious policy shift atthe Japanese Ministry of Finance inlate June (see “The hammer and theyen”). The government simply nolonger sees a weak yen as acceptable.Not only is the government worriedabout pressure from other countries,notably France, but a weak yen makesenergy and commodities expensive inyen terms, which is a negative forsmall and medium-sized firms, includ-ing many exporters. Sony, Honda, andthe other big names are experiencedhedgers (and cost-cutters), but smallerfirms suffer.

ON THE MONEY

The rising yen — here we go againJapan’s unique economy — and culture — will play major roles in determining whether

the current yen strength has legs.

BY BARBARA ROCKEFELLER

The yen has made a strong move off its June low vs. the dollar, pushingabove near-term resistance and positioning itself for a run at the 200-daymoving average.

FIGURE 1 — DAILY DOLLAR-YEN (INVERTED SCALE)

Source: Data — Reuters DataLink; charts — MetaStock

CURRENCY TRADER • August 2007 13

It’s wise to respect a stated policyshift such as this because governmentscan be powerful influences, althoughwe hardly ever see the influence atwork. It’s done behind the scenesusing what is euphemistically called“moral suasion.” In a phone call, overdrinks, or at the golf course, an officialmakes a gentle suggestion to a bankeror broker, (“…and Bob’s your uncle”),and the disliked behavior stopsinstantly. Governments regulate banksand brokers, plus they tax everybody.You disobey a government official’ssuggestion at your peril. And in Japan,respect for authority runs high.

There are numerous ways the gov-ernment could nudge institutionsaway from a weaker yen. Japaneseretail investors are avidly pursuingaccounts denominated in other curren-cies, for example, but that would tendnot to be the focus. Instead, attentionwould likely turn to cutting lines ofcredit to speculators, chiefly hedgefunds, especially if they invested inU.S. sub-prime paper. This would killtwo birds with one stone — halting anoutflow from yen and reducing expo-sure to high-risk paper.

The sub-prime housing problem inthe U.S. has already hit a number ofhedge funds, the main players in thecarry trade. An Australian hedge fundhired Blackstone to advise it on sub-prime investments, and immediatelyeveryone suspects these investmentswere made with borrowed yen. Wedon’t know that for a fact, but the meresuspicion suffices to goad sometraders into imagining that if there isone firm doing this, there might bedozens.

As far as we know, no hedge fundusing borrowed yen to invest in U.S.sub-prime has actually gone under,and we do not know if the sub-primeproblem is going to contaminate othercollateralized debt funds to the pointof failure. But from the hysteria in theblogosphere, you’d think widespreadinstitutional failure is imminent.Nearly all hedge funds are non-Japanese, but if Japanese banks areproviding the funding, they are at risk,too.

Japan has no intention of letting its

banks fall victim to dud loans to suchinstitutions — or forex trades, either.Presumably, lending to hedge fundshas been curtailed, along with creditlines for simple position-taking trad-ing. As for lending to domesticJapanese funds, Japan’s nine biggestbanking groups have more than ¥1 tril-lion ($8.3 billion) in various instru-ments backed by U.S. sub-prime mort-gages, according to the JiJi newswire.

In late July, Financial ServicesAgency (FSA) chief Yuji Yamamototold the press the government is close-ly monitoring Japanese financial insti-tution risk-management practices. TheFSA finds the banks “well-prepared.”Considering the entire banking sectorwas in the tank only 10 years ago andsurvived only with massive govern-ment bailouts, we wonder whetherthis can be true, but never mind. Weshould probably assume thatYamamoto told the banks to stopinvesting in the sector and perhapseven to dump some of the paper. Suchtrades are, in effect, repatriation, andautomatically entail buying yen.

This presupposes the Japanese insti-tutions do not just switch to better-quality foreign paper. After all, theyield differential is still vastly in the

The reversal on the daily time frame currently is nothing more than a correctionin the yen’s long-term downtrend.

FIGURE 2 — WEEKLY DOLLAR-YEN (INVERTED SCALE)

Source: Data — Reuters DataLink; charts — MetaStock

continued on p. 14

ON THE MONEY continued

14 August 2007 • CURRENCY TRADER

favor of the Australian dollar, New Zealand dollar, Britishpound, euro, and U.S. dollar. If the Japanese government wereasking its financial institutions to forego that additional yield,it would be a shocking interference with private business.(That doesn’t mean they wouldn’t do it.)

Another “reason” behind the yen’s rise is the widely expect-ed Bank of Japan (BOJ) rate hike in September or October,although possibly as early as August. This argument reallydoesn’t hold water. A rate hike would still leave a very largegulf between Japanese and foreign paper, although we canadmit that if the famously reticent BOJ were to raise rates in theabsence of inflationary pressure in the name of “normaliza-tion” and a nod to superior growth, then we need to pay atten-tion; more hikes will be on the way. This is a tremendously con-tentious issue: Under what circumstances should a centralbank, facing zero inflation, raise rates?

One answer is that Japan has failed to become a global finan-cial center on par with New York or London, but has not aban-doned the objective. Japan has the world’s second-largest econ-omy but Tokyo is not the world’s second largest financial cen-ter. In fact, Tokyo has lost rank over the past 15 years. TheTokyo Stock Exchange is the world’s second-largest after theNew York Stock Exchange, but its capitalization is only 10 per-cent of world capitalization, even as emerging markets rockethigher. It had one-third of world capitalization in 1990.

Foreigners don’t want to list their companies in Tokyo, withonly 25 listing last year, from 125 the year before. New York,even with the deterrent of Sarbanes-Oxley rules, attractedmore than 440 in 2006. Worse, in recent years the Tokyo StockExchange has had some huge technology failures that shutdown trading for entire days. Despite being the land of elec-tronics, the exchange is considered technologically deficient.Singapore and Hong Kong, with tiny economies, are biggerand more dynamic — and associated by language, history, andculture with China, which is rapidly displacing Germany asthe third largest economy.

The first study group on enhancing Japan’s position as aninternational financial center was held in 2003, but it seems tobe new FSA chief Yamamoto who is reviving the initiative. Headheres to the belief that you can’t be a major world financialcenter with a falling currency that fails to reflect good econom-ic fundamentals, which in Japan’s case is the highest growthrate in the world in 2006. However, wishing to be a worldfinancial center is not the same thing as knowing how to getthere.

Is it even remotely reasonable to assume that engineering astronger yen can be viewed as a prerequisite to this goal, andlet’s worry about the rest of the components of becoming aworld center later on? Yes. It is exactly the kind of straight-linethinking we have seen from Japan in the past — and oddly, itoften succeeds.

Working on becoming a world financial center could remainan objective of whatever government is in office, and PrimeMinister Shinzo Abe and his coalition government risk losingpower in the July 29 elections. Even if Yamamoto does notremain the FSA chief, the next guy would be bound by the

Other Barbara Rockefeller articles:

“The hammer and the yen”Currency Trader, July 2007.Recent statements by Japan’s Ministry of Finance hint atbig things on the horizon for the yen.

“Too big to fail”Currency Trader, June 2007.If the dollar is poised to rebound, it might be getting helpwhere it least expects it.

“Do stocks hold the key to currency levels?” Currency Trader, May 2007.The correlation between stock market and currency pricesisn’t what many people think.

“The coming commodity boom” Currency Trader, April 2007.Commodities are already having an impact on globaleconomies.

“The yen: Canary in the currency coal mine” Currency Trader, March 2007.Keep an eye on capital flows and the yen — they couldbe telling you more about the dollar than first meets the eye.

“Indicator failure and scientific analysis” Currency Trader, February 2007.This discussion of market biases and fallacies provides amore rigorous way to think about trading.

“Reserve diversification, Part II” Currency Trader, January 2007.What is the U.S. doing to ensure the Chinese governmentwill not alter the $700 billion it has in U.S. dollar reserves?

“Charts are not enough” Currency Trader, December 2006. Breaking down price action in light of the news.

“When will the yen go to the moon?” Currency Trader, October 2006. The fundamentals are all pointing toward an up move inthe Japanese yen. So what’s it waiting for?

“Why is everybody losing money in forex?” Currency Trader, September 2006. Despite unprecedented liquidity, professional currencymanagers have had a rough go of it in 2005 and 2006.Has something changed in the forex world?

“Gauging trader commitment” Currency Trader, August 2006. Is this a good breakout or a false move? TheCommitment of Traders report can help currency tradersfill in some of the holes left by the absence of traditionalvolume data in forex.

You can purchase and download past articles athttp://www.activetradermag.com/purchase_articles.htm.

overarching government objective.Japan has a splendid history of long-term planning. The next FSA head willpick up the internationalization effortwhere Yamamoto left off.

Having a stronger currency based inpart on higher interest rates is not theonly obstacle Yamamoto faces in try-ing to make Tokyo a global financialcenter. He also has to overcome a pen-chant for regulatory red tape that sti-fles innovation and encourages peopleto find ways around regulatory agen-cies (including the FSA itself) insteadof simply asking for exceptions andhelp.

Most observers say the biggestproblems are cultural. To be an inter-national center, you have to attract for-eigners to live and work in Tokyo. Butthe language is difficult to learn andhas complex nuances — the word for“risk” didn’t exist in Japanese, andcomes from English. Women are sec-ond-rate citizens and not representedat executive levels, a waste of half themanpower of the country. Japan hasits fair share of smart people, but argu-ing and disagreeing with others issocially unacceptable. It makes brain-storming particularly difficult. Andrespect for older people, while laud-able, restrains brash youngsters frommaking a splash. But splashiness anddisorder are what you need to sponsorchange.

The story is the storyOf all the reasons for the yen to be onthe upswing, the sub-prime hedgefund story seems to be the one that hascaptured traders’ imagination. Thatwe have no hard evidence of yen-funded hedge-fund failures and noevidence of a lending pullback,whether government-mandated ornot, is no deterrent to traders. It’s ajuicy story. It makes sense. All it willtake is one outright yen-fundedhedge-fund failure to send the yen tothe moon.

The yen can also go to the moon ifcarry trades actually do get unwound.We have been pooh-poohing thatstory, which has been used to explainany and every minor bounce upward

in the yen for the past six months,because hedge fund managers have a“strong hand.” It's not easy to stam-pede them out of lucrative positions.But each manager has a breakevenpoint and nerves get frayed evenwhen the yen is hundreds of pointsaway. After all, currencies can movehundreds of points in a short whileand currencies are famous for over-shooting, too.

More importantly, folks riding thecoattails of the yen carry trade, includ-ing those with plain vanilla futuresand forwards, are easy to panic. Asrisk aversion rises with every newstory about losses in subprime andother collateralized debt that was mis-priced, incompetently rated by the rat-ings agencies, or can’t be marked tomarket with any confidence, the carrytrade gets lumped in with other paperdeemed “high-risk.” This is not accu-rate — with the carry trade, all youneed to know is your breakeven point.You can count on the forex market toprovide sufficient liquidity for anorderly exit at just about any hour ofthe day or night. With truly high-riskpaper, the unknowns are plentiful,including markets so thin (illiquid)that no trading gets done at all. But therelative ease of exit doesn't matter tothose prone to panic — the yen carrytrade is considered speculative, andplenty of traders will simply dumppositions.

Add to that a possible rate hike anda government determined to rise inthe ranking of global financial centerson the back of a high currency and youhave a recipe for further gains.

Is this a castle built out of spunsugar? You bet. The whole thing cancome crashing down if the sub-primeproblem fades away with no big insti-tutional failures, Abe loses the elec-tion, the BOJ refuses to raise ratesbecause there is no inflationary reasonto raise rates, and the timetable forrestoring Tokyo to world status is seento be a project for a decade, not thenext three months. But in the mean-time, you have to go with the flow.�

For information on the author see p. 6.

CURRENCY TRADER • August 2007 15

TRADING STRATEGIES

16 August 2007 • CURRENCY TRADER

Acommon problem in the markets is tradingwith hindsight. For example, you make atrade, book a profit, and then watch themove continue — realizing you left money

on the table by not being more patient. Other times you waitfor that nice run that never materializes.

Trading with hindsight can introduce psychologicalissues when managing a trade. You might think you canjudge by the current conditions whether a big move is athand or not. But if you second-guess yourself for gettingout too early or too late, you’ll have problems taking thenext trade.

TRADING STRATEGIES

Analyzing both the duration and size of different price moves can clue you

in to more accurate trade setups.

BY CURRENCY TRADER STAFF

Short-term trendsin the EUR/USD pair

FIGURE 1 — DAILY EUR/USD

Source: CQGNet (http://www.cqg.com)

Two sharp runs — one up, one down — are marked on the chart. How often does this currency pair make consecutive dailyhigher highs or lows?

The best way to avoid this is to per-form a thorough analysis of marketbehavior and get some hard numberson which to base your trades. You willknow what typical market behavior isand can develop strategies aroundthat knowledge. In addition, perform-ing this type of market analysis on aregular basis will alert you to changesin market volatility.

For example, in Figure 1, the pricerun next to arrow “A” is a run of 13consecutive higher highs but only sixconsecutive higher closes. Arrow “B”marks a run of four consecutive lowerlows, but only three consecutive lowercloses. The question is, just how oftendo such runs occur?

This analysis dissects trend runsusing daily bars of the euro/U.S. dol-lar (EUR/USD) pair from July 1, 2003through June 29, 2007 and identifiesthe number of consecutive higher orlower highs, higher or lower lows,and higher or lower closes in different

continued on p. 18

FIGURE 2 — WEEKLY EUR/USD

Source: CQGNet (http://www.cqg.com)

The review period spanned July 2003 through June 2007.

CURRENCY TRADER • August 2007 17

18 August 2007 • CURRENCY TRADER

price moves, as well as other patterns. Figure 2 shows the review period using weekly bars, but

the analysis was performed on daily data.

Up moves vs. down movesTo get a handle on typical moves vs. what could be consid-ered outliers, Tables 1 and 2 show the EUR/USD’s basic

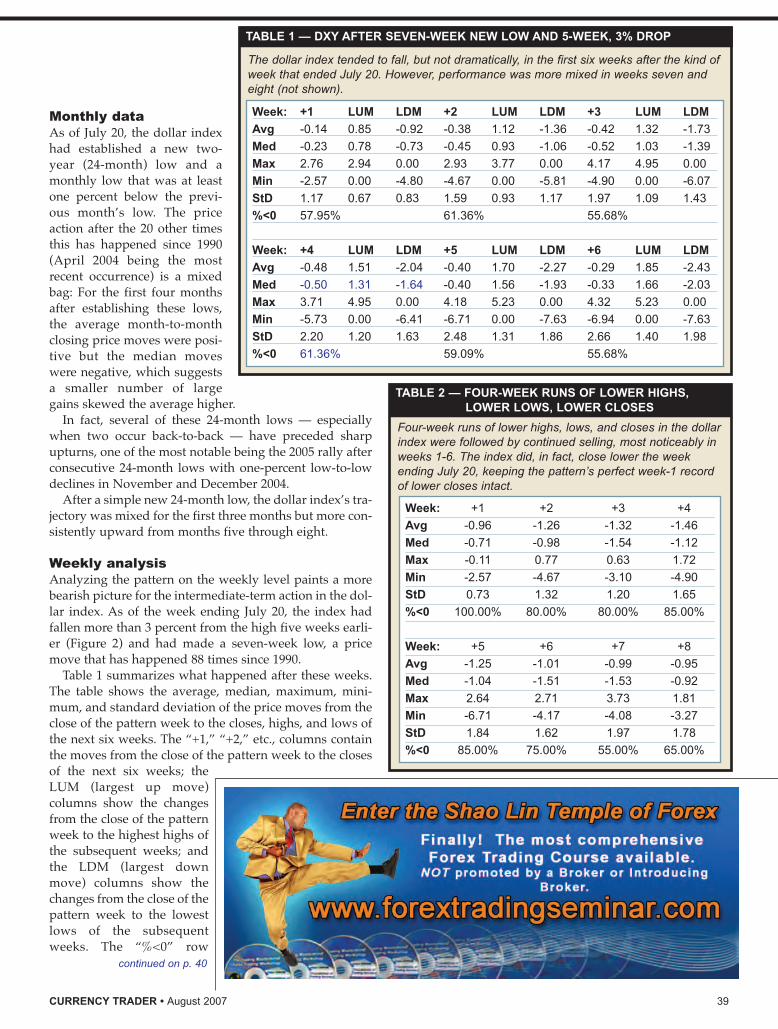

daily price range behavior. The top half of Table 1 compares one day’s session

to the next day’s session, detailing the number oftimes there were consecutive higher highs (HH),higher lows (HL), higher closes (HC), higher highsand higher closes (HH +HC), and higher highs, high-er lows, and higher closes (HH+HL+HC)

The bottom half of Table 1 shows the number oftimes there were consecutive lower lows (LL), lowerhighs (LH), lower closes (LC), lower lows and lowercloses (LL +LC), and lower lows, lower highs, andlower closes (LL+LH+LC).

First, the percentage change (on a closing basis) forthe entire review period was a gain of just over 17 percent.The table shows the influence of this long-term trend, but itis relatively minor — the numbers in the top half of thetable are slightly larger than the bottom. A closer look at thenumbers points to some interesting price action.

The market made either a higher high, higher low, orhigher close more than 50 percent of the time — unsurpris-

ing given the long-term trend.However, combining higher highsand higher closes dropped the per-centage to 35 percent of the time, andback-to-back higher highs, higherlows, and higher closes occurred justunder 29 percent of the time. This sug-gests that despite the buying pressurefrom one session to the next, traderstended to take profits going into theclose over 70 percent of the time.

None of the statistics in the bottomhalf of the table break the 50-percentlevel. However, the percentage oflower closes was higher than the per-centage of lower lows or lower highs.This implies there were inside dayswhen the market essentially paused;when the market could not generatean up move, traders moved out oflong positions, producing lower clos-es.

The percentage of consecutivelower lows and lower closes is justunder 32 percent and the percentageof consecutive lower lows, lowerhighs, and lower closes is slightly lessthan 25 percent. The bullish trend is

TRADING STRATEGIES continued

The EUR/USD trend was up for more than four years, which isreflected by the slight edge in the numbers for higher prices (tophalf of the table) vs. lower prices (bottom half of the table).

TABLE 1 — HIGHER HIGHS VS. LOWER LOWS

HH HL HC HH+HC HH+HL+HC

543 531 524 367 300

52.11% 50.96% 50.29% 35.22% 28.79%

LL LH LC LL+LC LL+LH+LC

503 492 512 332 256

48.27% 47.22% 49.14% 31.86% 24.57%

CURRENCY TRADER • August 2007 19

also reflected in these two statistics, because they suggestthere were times the market traded lower than the previoussession, but buyers came in and bid the market up to a high-er closing price.

Table 2 displays a more detailed breakdown of the fre-quency and length of runs in the EUR/USD pair. The “No.of days” row is the number of sessions that met the criteria.For example, “7” means a run of seven (or more) consecu-tive days; “6” means a run of six ormore sessions, etc.

Although, the table does not explic-itly show the exact number of occur-rences in each category, simple arith-metic reveals the answers. For exam-ple, there were 117 runs of three ormore consecutive higher closes (HC);these 117 runs are also part of the 254runs of two or more consecutive high-er closes (254 occurrences). As a result,there were 137 (254 - 117) runs of onlytwo consecutive days of higher closes.

The top half of Table 2 shows themarket made seven consecutive high-er closes only three times, or just 0.29percent of the time. The same statisticsare detailed for consecutively higherhighs and higher closes (HH+HC),and higher highs, higher lows, andhigher closes (HH+HL+HC). The bot-tom half of the table shows the infor-mation for lower closes (LC), lowerlows and lower closes (LL+LC), andlower highs, lower lows, and lowercloses (LH+LL+LC).

In light of the fact the long-term

trend was up during the review period, Table 2 has someinteresting details. First, there were more times the marketclosed down seven consecutive times than up. Of course,the difference (two) is not statistically significant, but thenumber of runs of consecutive lower closes is larger thanthe number of consecutive higher closes from lengths offour to seven days. (However, the percentage price changes

Despite the EUR/USD’s upward bias, the market posted seven consecutive higher closes (HC) only three times, while it madeseven consecutive lower closes on five different occasions.

TABLE 2 — EUR/USD RUNS

HC HH+HC HH+HL+HC

No. of days 7 6 5 4 3 2 7 6 5 4 3 2 7 6 5 4 3 2

Count 3 13 28 56 117 254 0 2 8 25 69 150 0 0 4 15 46 109

% 0.29% 1.25% 2.69% 5.37% 11.23% 24.38% 0.00% 0.19% 0.77% 2.40% 6.62% 14.40% 0.00% 0.00% 0.38% 1.44% 4.41% 10.46%

LC LL+LC LH+LL+LC

No. of days 7 6 5 4 3 2 7 6 5 4 3 2 7 6 5 4 3 2

Count 5 15 31 58 111 242 0 3 10 22 53 131 0 2 7 16 35 87

% 0.48% 1.44% 2.98% 5.57% 10.65% 23.22% 0.00% 0.29% 0.96% 2.11% 5.09% 12.57% 0.00% 0.19% 0.67% 1.54% 3.36% 8.35%

continued on p. 20

20 August 2007 • CURRENCY TRADER

TRADING STRATEGIES continued

during these runs is not included here.)There’s a similar pattern in the number of higher highs

and higher closes (HH+HC) relative to lower lows andlower closes (LL+LC). Neither category had any runs last-ing seven consecutive days, but the percentage of six- andfive-day runs of lower lows and lower closes edged out thepercentage of higher highs and higher closes.

The final comparison is higher highs, higher lows, andhigher closes (HH+HL+HC) vs. lower highs, lower lows,and lower closes (LC). There were two runs of six consecu-tive LH+LL+LC days on the bear side, and the five-day andfour-day runs outnumbered the HH+HL+HC counterparts.

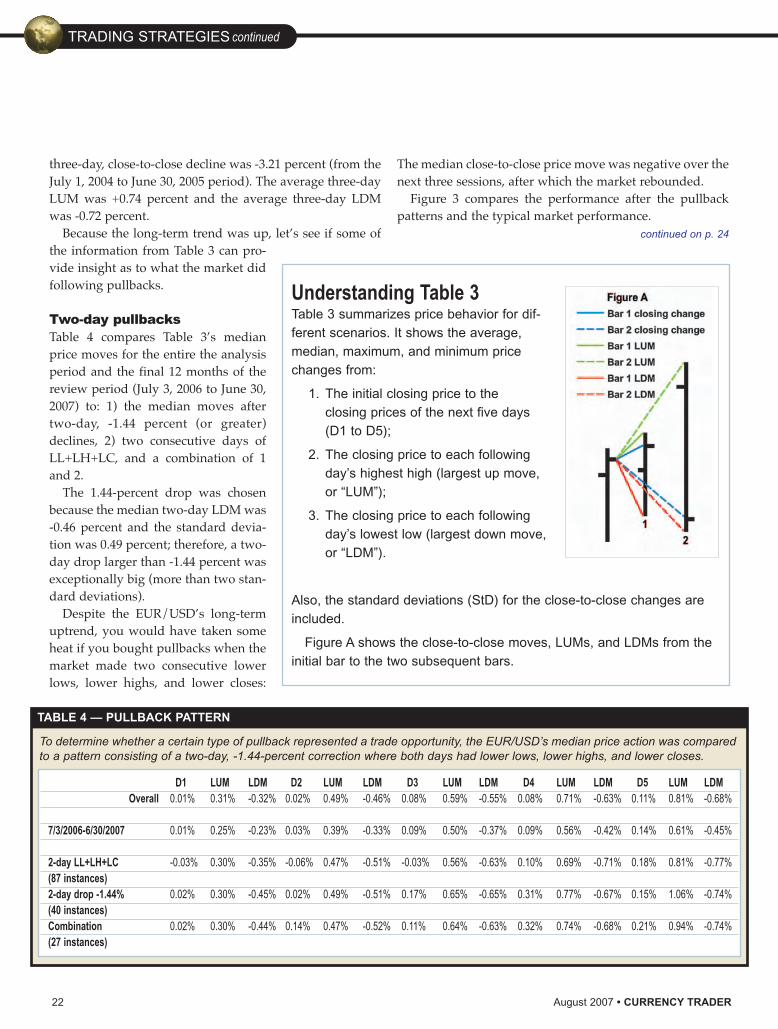

Size of price movesTable 3 details the percentage size of price moves from oneto five days in length for the entire review period, as well asin 12-month increments. Included are the average, median,maximum, minimum, and standard deviation for eachclose-to-close move, largest up move (LUM), and largestdown move (LDM) for each period (see “UnderstandingTable 3” for details about the statistics).

For example, for the entire analysis period, the averagethree-day close-to-close change was a gain of 0.05 percent,the maximum gain was +2.99 percent (which occurred inthe July 1, 2003 to June 30, 2004 period) and the largest

The percentage price moves from one to five days is shown for the total review period as well as for 12-month sub-periods.

TABLE 3 — MARKET PERFORMANCE

Total D1 LUM LDM D2 LUM LDM D3 LUM LDM D4 LUM LDM D5 LUM LDMAvg 0.02% 0.41% -0.42% 0.03% 0.60% -0.59% 0.05% 0.74% -0.72% 0.07% 0.86% -0.82% 0.08% 0.97% -0.90%Med 0.01% 0.31% -0.32% 0.02% 0.49% -0.46% 0.08% 0.59% -0.55% 0.08% 0.71% -0.63% 0.11% 0.81% -0.68%STD 0.56% 0.35% 0.35% 0.77% 0.47% 0.49% 0.93% 0.57% 0.59% 1.08% 0.65% 0.68% 1.19% 0.73% 0.75%7/1/2003-6/30/2004Avg 0.02% 0.51% -0.53% 0.05% 0.74% -0.75% 0.08% 0.92% -0.92% 0.10% 1.07% -1.05% 0.14% 1.21% -1.17%Med 0.04% 0.41% -0.45% 0.10% 0.64% -0.58% 0.17% 0.81% -0.70% 0.27% 0.95% -0.80% 0.35% 1.12% -0.87%Max 1.91% 1.99% 0.00% 2.39% 2.62% 0.00% 2.99% 3.25% 0.00% 3.49% 3.62% 0.00% 3.94% 3.99% 0.00%Min -1.93% 0.00% -2.11% -2.80% 0.00% -3.19% -2.97% 0.00% -3.47% -3.32% 0.00% -3.47% -3.69% 0.00% -3.85%STD 0.71% 0.41% 0.44% 0.96% 0.55% 0.61% 1.12% 0.65% 0.73% 1.31% 0.76% 0.83% 1.43% 0.84% 0.92

7/1/2004-6/30/2005Avg -0.01% 0.39% -0.44% -0.01% 0.57% -0.63% -0.02% 0.70% -0.77% -0.03% 0.82% -0.89% -0.04% 0.91% -1.00%Med -0.02% 0.30% -0.35% -0.02% 0.46% -0.50% 0.02% 0.57% -0.62% 0.00% 0.68% -0.71% 0.02% 0.81% -0.77%Max 1.84% 1.95% 0.00% 1.90% 2.01% 0.00% 2.12% 2.20% 0.00% 2.35% 2.53% 0.00% 2.50% 2.68% 0.00%Min -1.44% 0.00% -1.66% -2.36% 0.00% -2.53% -3.21% 0.00% -3.37% -3.05% 0.00% -3.37% -3.68% 0.00% -3.90%STD 0.56% 0.34% 0.36% 0.79% 0.45% 0.51% 0.98% 0.53% 0.63% 1.14% 0.61% 0.72% 1.28% 0.67% 0.81%

7/1/2005-6/30/2006Avg 0.03% 0.42% -0.42% 0.06% 0.62% -0.58% 0.08% 0.78% -0.70% 0.11% 0.92% -0.78% 0.14% 1.04% -0.86%Med 0.00% 0.33% -0.33% 0.02% 0.49% -0.49% 0.04% 0.60% -0.60% 0.05% 0.74% -0.66% 0.06% 0.84% -0.71%Max 1.70% 1.91% 0.00% 2.52% 2.73% 0.00% 2.56% 3.03% 0.00% 2.79% 3.03% 0.00% 2.76% 3.03% 0.00%Min -1.23% 0.00% -1.38% -2.15% 0.00% -2.24% -2.23% 0.00% -2.46% -2.42% 0.00% -3.01% -2.56% 0.00% -3.01%STD 0.54% 0.36% 0.31% 0.77% 0.51% 0.40% 0.92% 0.62% 0.49% 1.05% 0.69% 0.55% 1.15% 0.76% 0.61%

7/1/2006-6/30/2007Avg 0.02% 0.31% -0.28% 0.04% 0.44% -0.40% 0.07% 0.54% -0.47% 0.09% 0.63% -0.53% 0.11% 0.71% -0.58%Med 0.01% 0.25% -0.23% 0.03% 0.39% -0.33% 0.09% 0.50% -0.37% 0.09% 0.56% -0.42% 0.14% 0.61% -0.45%Max 1.15% 1.27% 0.00% 1.48% 1.73% 0.00% 1.97% 2.06% 0.00% 2.26% 2.51% -0.01% 2.76% 2.84% -0.01%Min -1.05% 0.00% -1.12% -1.42% 0.00% -1.48% -2.04% 0.00% -2.19% -2.01% 0.00% -2.25% -2.13% 0.01% -2.36%STD 0.36% 0.23% 0.21% 0.52% 0.32% 0.30% 0.62% 0.38% 0.37% 0.71% 0.44% 0.43% 0.79% 0.49% 0.47%

continued on p. 22

bringing Deutsche Bank, the world’s No.1 FX bank, to the retail market

Now the retail market can benefit from Deutsche Bank’s award-winning

expertise in foreign exchange. dbFX, the state-of-the-art foreign exchange

trading platform, allows individuals and small institutions to trade FX with

the world’s leading FX liquidity provider on a platform tailored to their needs.

Why trade with Deutsche Bank?

� Deutsche Bank is the world’s largest

foreign exchange liquidity provider and

has been voted No.1 Foreign Exchange

House in the world for three years in

a row by Euromoney magazine.

� When you trade through dbFX, you

receive direct access to the world's

foreign exchange market. dbFX is as

close to the inter-bank market as a

individual trader can be.

� 24-hour online access through the dbFX

Trading Station, competitive pricing and

market access with the highest level

of client support, including professional

services in 9 languages 24 hours a day.

� Direct access to research from Deutsche

Bank’s award winning analysts.

Why trade FX on dbFX?

� Streaming real-time executable rates

� Funds are deposited directly with

Deutsche Bank AG, London

� Account funding starting at $5,000

or the equivalent in GBP, EUR or JPY

� Margin as low as 1% for qualified

clients, one simple margin level

� Minimum trade size of 100,000 units

� Optional Position Management Tool,

allowing you to have simultaneous

long and short positions in the same

currency pair

� Online news and research

� Real time charts and charting tools

How to get started?

Getting started with dbFX is simple: please visit dbfx.com/CT forcomplete information on the service. Start with an online demo account.

dbFX sales staff are available to give you a personalized demo of the full functionality

and power of dbFX. Open an account online with the self service application for

individuals and corporations.

Contact Us.

dbFX Instant Messenger at dbfx.com

Toll-Free US Sales1-866-519-3239

Why trade with Deutsche Bank?

This advertisement has been approved and/or communicated by Deutsche Bank AG London. The services described in this advertisement are provided by Deutsche Bank AG or by its subsidiariesand/or affiliates in accordance with appropriate local legislation and regulation. Deutsche Bank AG is authorised under German Banking Law (competent authority: BaFin – Federal FinancialSupervising Authority) and with respect to UK commodity derivatives business by the Financial Services Authority; regulated by the Financial Services Authority for the conduct of UK business.© Deutsche Bank 2007

www.dbfx.com/CT

TRADING STRATEGIES continued

three-day, close-to-close decline was -3.21 percent (from theJuly 1, 2004 to June 30, 2005 period). The average three-dayLUM was +0.74 percent and the average three-day LDMwas -0.72 percent.

Because the long-term trend was up, let’s see if some ofthe information from Table 3 can pro-vide insight as to what the market didfollowing pullbacks.

Two-day pullbacksTable 4 compares Table 3’s medianprice moves for the entire the analysisperiod and the final 12 months of thereview period (July 3, 2006 to June 30,2007) to: 1) the median moves aftertwo-day, -1.44 percent (or greater)declines, 2) two consecutive days ofLL+LH+LC, and a combination of 1and 2.

The 1.44-percent drop was chosenbecause the median two-day LDM was-0.46 percent and the standard devia-tion was 0.49 percent; therefore, a two-day drop larger than -1.44 percent wasexceptionally big (more than two stan-dard deviations).

Despite the EUR/USD’s long-termuptrend, you would have taken someheat if you bought pullbacks when themarket made two consecutive lowerlows, lower highs, and lower closes:

The median close-to-close price move was negative over thenext three sessions, after which the market rebounded.

Figure 3 compares the performance after the pullbackpatterns and the typical market performance.

continued on p. 24

22 August 2007 • CURRENCY TRADER

Understanding Table 3Table 3 summarizes price behavior for dif-ferent scenarios. It shows the average,median, maximum, and minimum pricechanges from:

1. The initial closing price to the closing prices of the next five days (D1 to D5);

2. The closing price to each following day’s highest high (largest up move, or “LUM”);

3. The closing price to each following day’s lowest low (largest down move,or “LDM”).

Also, the standard deviations (StD) for the close-to-close changes areincluded.

Figure A shows the close-to-close moves, LUMs, and LDMs from theinitial bar to the two subsequent bars.

To determine whether a certain type of pullback represented a trade opportunity, the EUR/USD’s median price action was comparedto a pattern consisting of a two-day, -1.44-percent correction where both days had lower lows, lower highs, and lower closes.

TABLE 4 — PULLBACK PATTERN

D1 LUM LDM D2 LUM LDM D3 LUM LDM D4 LUM LDM D5 LUM LDMOverall 0.01% 0.31% -0.32% 0.02% 0.49% -0.46% 0.08% 0.59% -0.55% 0.08% 0.71% -0.63% 0.11% 0.81% -0.68%

7/3/2006-6/30/2007 0.01% 0.25% -0.23% 0.03% 0.39% -0.33% 0.09% 0.50% -0.37% 0.09% 0.56% -0.42% 0.14% 0.61% -0.45%

2-day LL+LH+LC -0.03% 0.30% -0.35% -0.06% 0.47% -0.51% -0.03% 0.56% -0.63% 0.10% 0.69% -0.71% 0.18% 0.81% -0.77%(87 instances)2-day drop -1.44% 0.02% 0.30% -0.45% 0.02% 0.49% -0.51% 0.17% 0.65% -0.65% 0.31% 0.77% -0.67% 0.15% 1.06% -0.74%(40 instances)Combination 0.02% 0.30% -0.44% 0.14% 0.47% -0.52% 0.11% 0.64% -0.63% 0.32% 0.74% -0.68% 0.21% 0.94% -0.74%(27 instances)

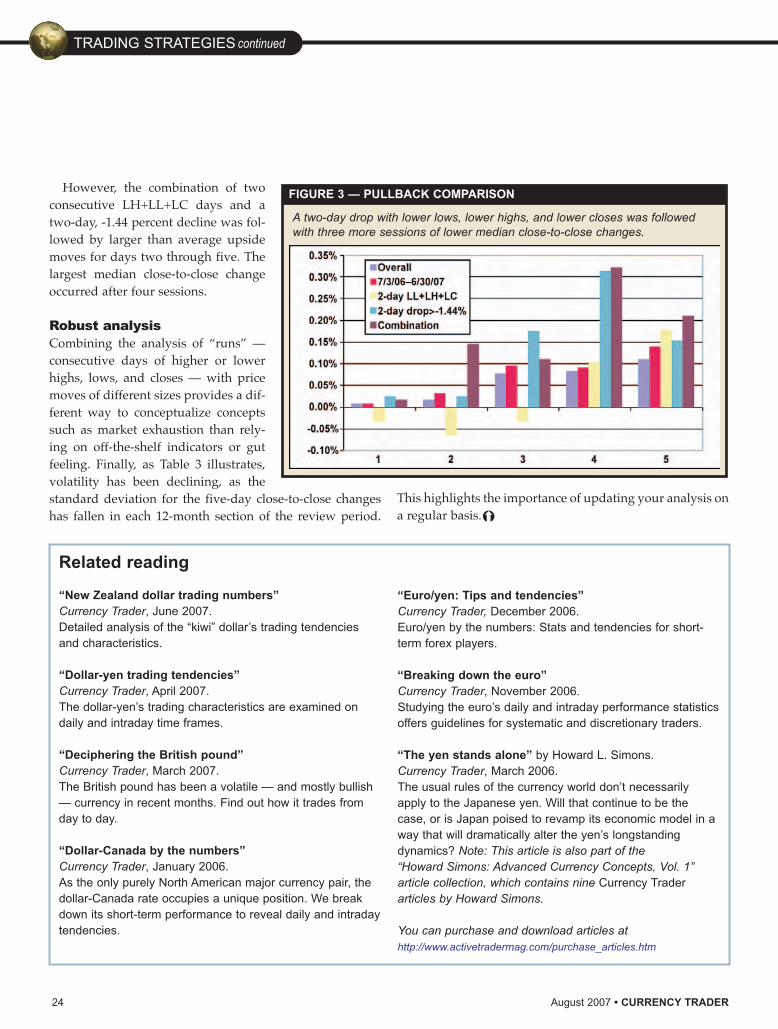

However, the combination of twoconsecutive LH+LL+LC days and atwo-day, -1.44 percent decline was fol-lowed by larger than average upsidemoves for days two through five. Thelargest median close-to-close changeoccurred after four sessions.

Robust analysisCombining the analysis of “runs” —consecutive days of higher or lowerhighs, lows, and closes — with pricemoves of different sizes provides a dif-ferent way to conceptualize conceptssuch as market exhaustion than rely-ing on off-the-shelf indicators or gutfeeling. Finally, as Table 3 illustrates,volatility has been declining, as thestandard deviation for the five-day close-to-close changeshas fallen in each 12-month section of the review period.

This highlights the importance of updating your analysis ona regular basis.�

Related reading

“New Zealand dollar trading numbers”Currency Trader, June 2007.Detailed analysis of the “kiwi” dollar’s trading tendenciesand characteristics.

“Dollar-yen trading tendencies”Currency Trader, April 2007. The dollar-yen’s trading characteristics are examined ondaily and intraday time frames.

“Deciphering the British pound” Currency Trader, March 2007. The British pound has been a volatile — and mostly bullish— currency in recent months. Find out how it trades fromday to day.

“Dollar-Canada by the numbers”Currency Trader, January 2006. As the only purely North American major currency pair, thedollar-Canada rate occupies a unique position. We breakdown its short-term performance to reveal daily and intradaytendencies.

“Euro/yen: Tips and tendencies”Currency Trader, December 2006. Euro/yen by the numbers: Stats and tendencies for short-term forex players.

“Breaking down the euro” Currency Trader, November 2006. Studying the euro’s daily and intraday performance statisticsoffers guidelines for systematic and discretionary traders.

“The yen stands alone” by Howard L. Simons.Currency Trader, March 2006. The usual rules of the currency world don’t necessarilyapply to the Japanese yen. Will that continue to be thecase, or is Japan poised to revamp its economic model in away that will dramatically alter the yen’s longstandingdynamics? Note: This article is also part of the “Howard Simons: Advanced Currency Concepts, Vol. 1” article collection, which contains nine Currency Traderarticles by Howard Simons.

You can purchase and download articles at http://www.activetradermag.com/purchase_articles.htm

FIGURE 3 — PULLBACK COMPARISON

A two-day drop with lower lows, lower highs, and lower closes was followedwith three more sessions of lower median close-to-close changes.

24 August 2007 • CURRENCY TRADER

TRADING STRATEGIES continued

26 August 2007 • CURRENCY TRADER

ADVANCED STRATEGIES

Minor currencies and federal reserve trade weights

The verdict is in: Currency rates don’t affect trade.

BY HOWARD L. SIMONS

Last month’s article “Currencies and federal reservetrade weights” (Currency Trader, July 2007), whichexamined major currencies’ impact on Federal

Reserve trade weights, concluded: “A review of U.S. tradepatterns with major currency trading partners reveals littleevidence that a weaker currency leads to greater exportcompetitiveness and a lower ability to import.” In short, the

entire premise behind the floating exchange-rate regime ofthe past 35 years is wrong.

As all currency traders learn quickly, major currencieshave different trading patterns and represent differentunderlying economies than minor currencies, which arebuffeted more by speculative capital flows even as theirmarkets are shallower than the majors’. Will analysis of the

minors support the findings of thestudy of the majors, or are FederalReserve trade weights for theminor currencies more sensitive tochanges in the currencies them-selves?

Recap of data and methodologyFirst, the analysis process usedhere is identical to that used lastmonth:

To maintain its trade-weighted dol-lar index (http://www.federalre-serve.gov/releases/H10/Weights/), theFederal Reserve must keep track of thechanging use of various currencies theU.S. receives in return for its exportsand pays for its imports. In thesecharts, export weights are depicted inblue and import weights in green.

These weights are calculated on anannual basis and, of necessity, afterthe fact. Because the Federal Reserve isunable to license its dollar index forcommercial purposes, many tradersare unfamiliar with this data.

Also, these currency weights reflecttheir use in bilateral trade with theU.S. and do not reflect total bilateraltrade. This is critical for countriesfrom whom the U.S. imports largequantities of goods priced in dollars,such as crude oil and various metals.

Annual data are of little trading use

FIGURE 1 — THE CHINESE YUAN AND ITS WEIGHT IN U.S. TRADE

FIGURE 2 — THE TAIWAN DOLLAR AND ITS WEIGHT IN U.S. TRADE

CURRENCY TRADER • August 2007 27

in a continuous market such as cur-rencies. We can create smoothed seriesof import and export weights via a sta-tistical technique called “cubic splineinterpolation.” This technique is usedtwice in the charts below — once tocreate quarterly series from the annu-al numbers and a second time to createmonthly numbers from the quarterlyresults.

The resulting interpolations are fareasier to absorb than the annual num-bers, but as they involve two separatedata transformations, we did notattempt any further statistical analy-sis against monthly currency values(presented in red in the charts). Inaddition, please be advised all curren-cies are displayed in the “USD per”convention familiar to traders of theeuro, the British pound, and currencyfutures. The currency scale is invertedfor currencies commonly expressed as“per USD,” so a rising red line alwaysconveys strength vs. the dollar and afalling red line always conveys weak-ness.

A second passage from lastmonth is mentioned here for clari-ty:

Even though the principal advocateof floating exchange rates, the lateMilton Friedman, was the antithesisof a protectionist, his arguments havebeen seized by this faction to the extentthat the notion a weaker currency

continued on p. 28

FIGURE 3 — THE HONG KONG DOLLAR AND ITS WEIGHT IN U.S. TRADE

FIGURE 4 — THE SINGAPORE DOLLAR AND ITS WEIGHT IN U.S. TRADE

FIGURE 5 — THE KOREAN WON AND ITS WEIGHT IN U.S. TRADE

The entire premise

behind the floating

exchange-rate

regime of the past

35 years is wrong.

28 August 2007 • CURRENCY TRADER

should stimulate exports and reduceimports will be referred to as the “pro-tectionist argument.”

East Asian currenciesWith all the political rhetoric call-ing for a stronger Chinese yuan, itis easy to lose sight of the fact thatexport weights to China rosesteadily between 2000 and 2006.Moreover, as China’s wealth levelgrows, so should both the volumeand the value-added content of itsimports from the U.S. This so-called “marginal propensity toimport” is characteristic of allgrowing economies.

The surge in import weightsfrom China is, of course, the dom-inant feature in Figure 1. Nonation on earth has China’s costadvantages in labor, a state-con-trolled banking system with over$1 trillion in foreign exchangereserves, low levels of environ-mental and safety costs, and pro-ductivity advantages from newplants and equipment. Giventhese advantages, we do need toask whether any level of the yuan(CNY) would have offset theseformidable advantages; the bet-ting here is the yuan could bemuch stronger with no adverseeffects on Chinese exports.

Taiwan’s importance as anexporter to the U.S. has beendeclining steadily since the mid-1980s. In all likelihood, exportsfrom Taiwan have been displacedby exports from China. Theisland’s share in U.S. exportweights has tracked changes inthe TWD to a degree (Figure 2).This indicates some measure ofcurrency price elasticity inTaiwan’s import decisions.

Hong Kong provides an inter-esting rebuttal to the protectionistargument. Although its currencyhas been locked in a tight range since the mid-1980s, itsimport weights have fallen steadily since then (Figure 3). Ifthe protectionist argument was correct, we would have toconclude the Hong Kong dollar (HKD) was overvalued atthis lower range. Moreover, we also would have to con-

clude the uptrend in export weights between 1986 and 1996meant the HKD was overvalued.

Neither is likely. As in the Taiwan example, the simplestexplanation is the best. Hong Kong’s exports to the U.S.have been displaced by exports from China.

ADVANCED STRATEGIES continued

FIGURE 6 — THE THAI BAHT AND ITS WEIGHT IN U.S. TRADE

FIGURE 7 — THE MALAYSIAN RINGGIT AND ITS WEIGHT IN U.S. TRADE

FIGURE 8 — THE INDONESIAN RUPIAH AND ITS WEIGHT IN U.S. TRADE

CURRENCY TRADER • August 2007 29

We can draw the same conclusion by examiningSingapore, which we will group with the East Asian ratherthan the South Asian countries by virtue of its largelyChinese population. The 1997-2001 decline in the SGD didnothing to arrest its falling importweights, and the 2002-2006 rallydidn’t do anything to accelerate thedowntrend already in place (Figure4). These simply reflect China’sascendancy. Export weights toSingapore rose modestly in themid-1990s “Asian Tiger” epoch,but have flattened since.

The final East Asian currency isthe Korean won (KRW, Figure 5).This currency was hugely affectedby the 1997-1998 Asian crisis.Although import weights fromKorea — which had been in declinesince 1988 — reversed after theKRW’s plunge and declined afterthe KRW’s post-2004 rally, the realimpact was the large drop in exportweights to Korea during the Asiancrisis. This reflected both changesin the currency and the large dropin Korean national income duringthis period.

South Asian currenciesSpeaking of the Asian crisis, let’slook at the currency that started itall, the Thai baht (THB). Prior to1998, both the import and theexport weights for the baht weretrending higher (Figure 6). Thecheaper baht did nothing toincrease its import weights, and theloss of purchasing power inThailand did surprisingly little toreduce export weights to Thailand.Overall, Thailand’s contribution toU.S. trade is and has been fairlyminor.

The picture for Malaysia is simi-lar to that of Thailand (Figure 7).Both import weights fromMalaysia and export weights to itgrew rapidly between 1986 and1996 — and were unaffected by theringgit’s (MYR) sharp drop.Neither the MYR nor the course ofthe Malaysian economy affected itstrade weights with the U.S.

Indonesia also suffered in the

Asian crisis (Figure 8). The 1997 collapse of the rupiah (IDR)preceded a decline — not the theorized increase — inimport weights. The same cannot be said for exportweights, however: Indonesia’s sudden impoverishment led

continued on p. 30

FIGURE 9 — THE PHILIPPINE PESO AND ITS WEIGHT IN U.S. TRADE

FIGURE 10 — THE MEXICAN PESO AND ITS WEIGHT IN U.S. TRADE

FIGURE 11 — THE BRAZILIAN REAL AND ITS WEIGHT IN U.S. TRADE

ADVANCED STRATEGIES continued

30 August 2007 • CURRENCY TRADER

to a swift decline in export weights, one that has yet torecover.

The last South Asian currency to be examined is thePhilippine peso (PHP), which is yet another refutation ofthe protectionists (Figure 9). Its import weights fell sharply

after the PHP fell in 1997, butexport weights to the suddenlypoorer country actually trendedhigher between 1998 and 2003before falling sharply in 2004.

Latin American currenciesMexico is a special case on severallevels. Its peso (MXN) has col-lapsed on three separate occasionswithout triggering the macroeco-nomic collapses normally associ-ated with such events. As a mem-ber of NAFTA, its trade with theU.S. on both the import andexport sides has grown regardlessof the currency. Its major source offoreign exchange, crude oilexports, is priced in USD, and ithas another major source of dol-lars, the remittances of Mexicannationals living and working inthe U.S. And like Colombia,Mexico has large, undocumentedsources of U.S. dollars.

U.S. export weights to Mexicosurged after NAFTA and have lev-eled off near a large 15 percentlevel (Figure 10). Import weightsfrom Mexico have fallen as manyof the light manufactured exportsfrom Mexican maquiladora plantshave been displaced by cheapergoods from China. All of these fac-tors combine to make the MXNrate largely irrelevant as the U.S.’sfourth-largest trading partner.

The Brazilian real (BRL) has ashort history. It came into being in1994 following the untimelydemise of a long list of predeces-sors, but even so it has managed tocollapse three times in 12 years. Indefiance of the protectionists’ the-ories, the impact on importweights has been minimal (Figure11). Export weights to Brazil havedeclined since 1997, a period inwhich economic growth in Brazil

has been strong. This may be a rare case when the currencyprice elasticity of demand exceeds income elasticity ofdemand.

Argentina, like Brazil, has gone through multiple curren-cies. These have included the peso ley, the austral, and a

FIGURE 12 — THE ARGENTINE PESO AND ITS WEIGHT IN U.S. TRADE

FIGURE 13 — THE VENEZUELAN BOLIVAR AND ITS WEIGHT IN U.S. TRADE

FIGURE 14 — THE CHILEAN PESO AND ITS WEIGHT IN U.S. TRADE

CURRENCY TRADER • August 2007 31

direct peg to the USD. There is also the little matter of fre-quent defaults, nationalizations, and other non-currencyimpediments to the free flow of goods and services.

Import weights from Argentina scarcely have budgedsince 1992 (Figure 12). Exportweights to Argentina began to fallin 1999 as the country sufferedduring its dollar-peg epoch, andthen collapsed going into the 2002debt default. They have rebound-ed somewhat with the peso (ARS);this is an income effect, not a cur-rency effect.

Import weights from Venezuelahave been quite low, asVenezuela’s chief export to theU.S., crude oil, is priced in USD(Figure 13). Export weights havefallen as the bolivar has weakenedduring the Chavez era; it’s diffi-cult to discern whether this is cur-rency-related, income-related, orpolitical.

Chile enjoys so much a reputa-tion as South America’s successstory that first-time observershave trouble absorbing the extentof the peso’s (CLP) decline since1988. Export weights to Chile rosebetween 1988 and 1996 even asthe CLP fell, and then fell into2003 as the CLP fell (Figure 14).Factors other than currency move-ments likely were involved.

In addition, the weights ofimports from Chile haveincreased even as the CLP roseafter 2003. Chile’s efficiencies inagricultural exports — its leadingexport, copper, is priced in USD— probably account for this.

Export weights to Colombiahave tracked movements in thepeso (COP) in a manner consis-tent with standard theory (Figure15). Import weights fromColombia have increased since2002 even in the face of a firmerCOP. The U.S.-Colombia tradepicture is so distorted by undocu-mented flows that further com-ments will be withheld.

Other currenciesThe final group of currencies for

India, Russia, Saudi Arabia, and Israel represent specialcases and thus are discussed on a non-geographic basis.

The growing importance of the U.S.-India bilateral eco-nomic relationship is not reflected well in the trade data; it

continued on p. 32

FIGURE 15 — THE COLOMBIAN PESO AND ITS WEIGHT IN U.S. TRADE

FIGURE 16 — THE INDIAN RUPEE AND ITS WEIGHT IN U.S. TRADE

FIGURE 17 — THE RUSSIAN RUBLE AND ITS WEIGHT IN U.S. TRADE

32 August 2007 • CURRENCY TRADER

is increasingly a “post-industrial” relationship. Includedare skilled labor imported from India and informationservices outsourced to India.

Import weights have been increasing steadily since thelate 1980s, which in all likelihood reflects the moderniza-

tion of the Indian economy farmore than the decline in the rupee(INR, Figure 16). Export weights toIndia have jumped since 2001 evenas the rupee has remained near itslows.

Export weights to Russia fellduring the country’s 1998 defaultand have rebounded since theruble’s (RUB) modest recovery(Figure 17). Bilateral trade betweenthe U.S. and Russia is very smalland is confined to specialty goodsand minerals.

The increasing import weightsfrom Israel during the shekel’s(ILS) 1982-2002 decline are asexpected in classic theory (Figure18). The generally increasingexport weights to Israel duringthis same period are antithetical toclassic theory. Too much U.S.-Israel trade is dollar-denominatedor is confined to sectors such astechnology and military hardwarefor currency movements to be areal factor.

Finally, we come to a specialcase — Saudi Arabia. The riyal(SAR) is de facto fixed — note therange — and import weights skirtnear zero (Figure 19). Their princi-

pal export is priced in USD. Export weights to SaudiArabia have declined somewhat over the years, but giventhe importance of military hardware and other sensitiveexports to Saudi Arabia, this data stream probably doesnot reveal much.

Can’t fight the dataWe have reviewed 26 currencies with as many as 34 yearsof trade data accounting for 100 percent of the FederalReserve’s trade-weighting scheme.

We found some isolated instances wherein exportweights to countries whose currencies had appreciatedrose and some isolated instances wherein import weightsfrom countries whose currencies had depreciated rose.These were noted duly.

The preponderance of evidence, however, is incomeelasticities, trade agreements, economic integration, andthe terms in which goods and services are priced, amongother factors, are all more important than currencies inaffecting trade flows.�

For information on the author see p. 6.

ADVANCED STRATEGIES continued

FIGURE 18 — THE ISRAELI SHEKEL AND ITS WEIGHT IN U.S. TRADE

FIGURE 19 — THE SAUDI RIYAL AND ITS WEIGHT IN U.S. TRADE

Related reading

“Currencies and Federal Reserve trade weights”Currency Trader, July 2007.The theory that a weaker dollar makes U.S. goods and services more competitive abroad sounds nice, but the factsargue otherwise.

“Howard Simons: Advanced Currency Concepts, Vol. 1”A discounted collection that includes many of the articles listed here.

You can purchase and download past articles at http://www.activetradermag.com/purchase_articles.htm.

The Premier Convention for Forex Traders

• Learn Specific Trading Strategies You Can Use Immediately:Learn realistic and repeatable methods for making successful trading decisionsduring a weekend dedicated to improving your chances for success.

• Exchange Ideas With Fellow Traders Who’ve Been Where YouAre Now: Some of the best traders in the country are coming to the Expo andthis is your chance to sit down and learn what works for them and how theybecame confident traders.

• Find the Best Services and Tools to Help You Succeed: The Expoallows you to evaluate all of the best tools available to you in the exhibit hall.Meet company representatives to ask specific questions and get the answers youneed to make intelligent decisions about which services you want to use.

September 15–16, 2007Mandalay Bay Resort & CasinoLas Vegas, Nevada

Gold SponsorsPlatinum Sponsor Media Partner

Attend The ONLY Expo Exclusively For Currency Traders—FREE!

Register Online! www.ForexTradingExpo.com(Priority Code 008931)

Three Reasons Why Attending The ForexTrading Expo Will Improve Your Trading:

RobBooker

JohnCarter

Todd Gordon

RagheeHorner

WayneMcDonell

John Person

EdwardPonsi

Russell LaScala

Speakers Include:

...and many more!

Register To Attend FREE!

Technology Sponsor

A Production of InterShow • 1258 N. Palm Avenue, Sarasota, FL 34236 • 800/970-4355 • www.InterShow.com

34 August 2007 • CURRENCY TRADER

Following the direction of short-term interestrates is a vital part of determining the likelydirection of a particular currency or currencypair. But what can long-term interest rates tell

us about the future price behavior of currencies? Rising long-term interest rates have been very much in

the news lately. On June 13, the yield on the 10-year T-noteclimbed to a five-year high of 5.327 percent. The 4.50-per-cent note finished June at a yield of 5.03 percent — 54 basispoints higher than its March 7 low of 4.49 percent. (For areview of T-notes and their terminology, see “Treasurybackgrounder.”)

Normally, the yield curve — which depicts the differencebetween short-term and long-term Treasury yields — rises,reflecting the higher yields usually associated with longerTreasury maturities (Figure 1). When short-term yields arehigher than long-term yields, as has recently been the case,the curve is referred to as “inverted” — a condition that has

historically been interpreted as a warning sign that a reces-sion is looming. With the recent increase in long-term rates,however, the yield curve has returned to its normal shape.

What’s behind the jump in long-term interest rates?

Supported by a strong May retail sales report (the bestshowing in more than a year), traders have become lessconvinced the Federal Reserve will cut short-term interestrates. At least one interpretation, then, of the rise in long-

term rates is that it portends improvement in the prospectsfor economic growth (see “Doom, gloom, and long-terminterest rates,” Active Trader, September 2007).

Another interpretation is that improved economic

TRADING BASICS

Long-term interest ratesand the U.S. dollar

Comparing the yield curve on July 2 and March 5 shows thecurve has regained its “normal” shape — upward sloping, with long-term interest rates higher than short-term rates.

FIGURE 1 — CHANGING YIELD CURVE

One interpretation is the rise in long-term rates portends improvement

in the prospects for economic growth; another is that improved

economic growth could be accompanied by higher inflation.

Rising long-term Treasury yield should imply a higher dollar — at some point — but history shows

many other factors can get in the way of that easy assumption.

BY DAVID MANTELL

CURRENCY TRADER • August 2007 35

growth could be accompanied by higher infla-tion. However, recent price data suggests infla-tion remains mild and appears to be undercontrol. The personal consumption expendi-tures index (excluding food and energy), a keyinflation measure, increased 1.9 percent in Mayvs. the same period last year. This is the small-est year-over-year increase since March 2004.

The currency connectionWhat are the ramifications for the U.S. dollar?If higher long-term rates are indicative of animproving U.S. economy, that would be bullishfor the greenback. If there is an inflation com-ponent to stronger economic growth, and ifhigher long-term rates are indicative of that,the Fed will be more likely to raise short-termrates. That, too, would be positive for the U.S.dollar, causing investors searching for highshort-term yields to put their cash in the U.S.

Overall, higher long-term rates are fairlypromising for the U.S. dollar. Thus far, howev-er, this has not been reflected in the dollar’saction against most major currencies, includ-ing the euro (Figure 2).

What does the past tell us? The U.S. economy experienced a similar sce-nario in April of 2006. On Jan. 23, 2006, the 10-year T-note yielded 4.36 percent — one basispoint lower than its yield on the first day of2006. By April 26 (roughly the same time peri-od as our current scenario), its yield hadclimbed 76 basis points to 5.12 percent, and itremained at or above 5 percent through July28. Strong new home sales and robust ordersfor durable goods helped propel long-terminterest rates higher.

How did the dollar perform vs. the Euroduring this time period? On Jan. 23, theeuro/dollar (EUR/USD) rallied strongly to

continued on p. 36

Despite the recent long-term rate increase, the dollar has remainedweak vs. most major currencies — reflected in the new highs reachedby the euro/dollar pair.

FIGURE 2 — DOLLAR WEAK VS. EURO

Source: TradeStation

Treasury backgrounder