ctc 475 review public projects public projects why b/c ratio is used why b/c ratio is used pitfalls...

TRANSCRIPT

CTC 475 Review CTC 475 Review

Public ProjectsPublic Projects Why B/C ratio is usedWhy B/C ratio is used

Pitfalls of the B/C ratioPitfalls of the B/C ratio

CTC 475 CTC 475

DepreciationDepreciation

ObjectivesObjectives

Know the historical (SL, DB, SYD) and Know the historical (SL, DB, SYD) and MACRS-GDS methods to determine MACRS-GDS methods to determine book values and depreciationbook values and depreciation

Tax ConceptsTax Concepts

Taxes affect cash flows Taxes affect cash flows Depreciation affects taxesDepreciation affects taxes Depreciation method is determined Depreciation method is determined

by law:by law: Post ’86-MACRS Post ’86-MACRS (Modified Accelerated Cost Recovery System)(Modified Accelerated Cost Recovery System)

’’81-’86 ACRS 81-’86 ACRS (Accelerated Cost Recovery System)(Accelerated Cost Recovery System)

Pre ’81-other methods (SL, DB, SYD)Pre ’81-other methods (SL, DB, SYD) SL-straight line; DB-declining balance; SL-straight line; DB-declining balance;

SYD-sum of the year’s digitsSYD-sum of the year’s digits

Depreciable PropertyDepreciable Property3 Requirements3 Requirements

1.1. Must be used in business or held for Must be used in business or held for the production of incomethe production of income

2.2. Life can be determined and is longer Life can be determined and is longer than one yearthan one year

3.3. Must be something that wears out, Must be something that wears out, decays, gets used up, becomes decays, gets used up, becomes obsolete, or loses value from natural obsolete, or loses value from natural causescauses

Depreciable PropertyDepreciable Property

Tangible (machines, cars, computers)Tangible (machines, cars, computers) Intangible (copyrights, franchises)Intangible (copyrights, franchises) Real (erected on land, growing on Real (erected on land, growing on

land, attached to land; however, land land, attached to land; however, land itself is not depreciable)itself is not depreciable)

Personal (machines, cars)Personal (machines, cars) Most depreciable property is Most depreciable property is

tangible, personaltangible, personal

Adjusted Cost BasisAdjusted Cost Basis

Cost of property +Cost of property + Cost of additions +Cost of additions + Installation costInstallation cost

Book ValueBook Value

The worth of a depreciable property The worth of a depreciable property as shown on the accounting recordsas shown on the accounting records

Recovery PeriodRecovery Period

Time over which cost basis can be Time over which cost basis can be recovered recovered

For MACRS-GDS law sets asFor MACRS-GDS law sets as 3,5,7,10,15, or 20 (for tangible property-see 3,5,7,10,15, or 20 (for tangible property-see

Table 7-2; page 311)Table 7-2; page 311) 27.5 (for residential real property)27.5 (for residential real property) 31.5/39 years (for nonresidential real property)31.5/39 years (for nonresidential real property)

The recovery period is usually shorter than The recovery period is usually shorter than the actual physical lifethe actual physical life

ExamplesExamples 3-year property3-year property

Tractor units, special tools, race horsesTractor units, special tools, race horses 5-year property5-year property

Autos, buses, computers, office machineryAutos, buses, computers, office machinery 7-year7-year

Office furniture, theme/amusement park assetsOffice furniture, theme/amusement park assets 10-year property10-year property

Vessels, tugs, assets used in petroleum refiningVessels, tugs, assets used in petroleum refining 15-year property15-year property

Sewage treatment plants, sidewalks, roads, drainage Sewage treatment plants, sidewalks, roads, drainage facilities bridges, fencing, landscaping, transmission facilities bridges, fencing, landscaping, transmission lineslines

20-year property20-year property Farm buildingsFarm buildings

Depreciation MethodsDepreciation Methods

SL-straight lineSL-straight line DB-declining balanceDB-declining balance SYD-Sum of the years digitsSYD-Sum of the years digits MACRS, GDS-modified accelerated MACRS, GDS-modified accelerated

cost recovery system, general cost recovery system, general depreciation systemdepreciation system

Depreciation Methods-ExampleDepreciation Methods-Example

7-year property7-year property Basis is $100KBasis is $100K SV=0SV=0

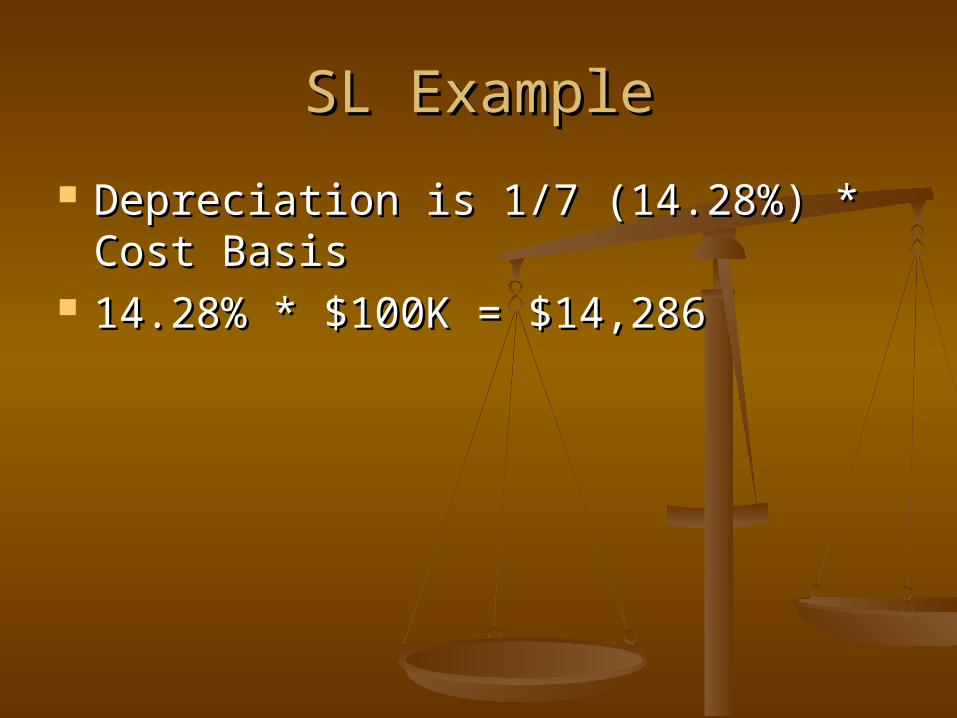

SL ExampleSL Example

Depreciation is 1/7 (14.28%) * Cost Depreciation is 1/7 (14.28%) * Cost BasisBasis

14.28% * $100K = $14,28614.28% * $100K = $14,286

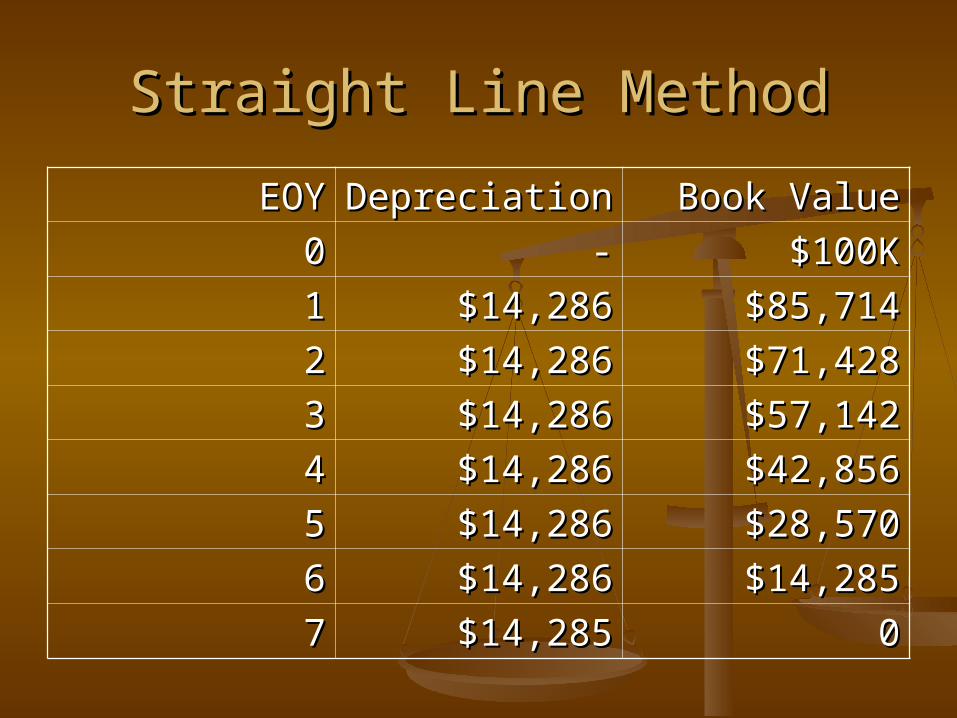

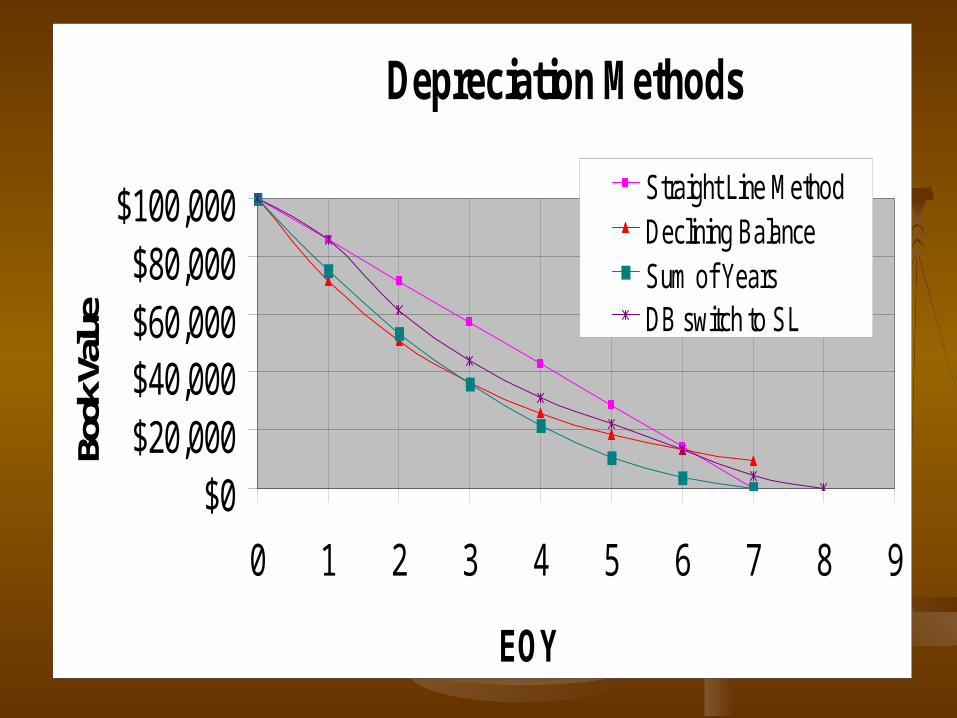

Straight Line MethodStraight Line Method

EOYEOY DepreciationDepreciation Book ValueBook Value

00 -- $100K$100K

11 $14,286$14,286 $85,714$85,714

22 $14,286$14,286 $71,428$71,428

33 $14,286$14,286 $57,142$57,142

44 $14,286$14,286 $42,856$42,856

55 $14,286$14,286 $28,570$28,570

66 $14,286$14,286 $14,285$14,285

77 $14,285$14,285 00

What’s Wrong with this Method?What’s Wrong with this Method?

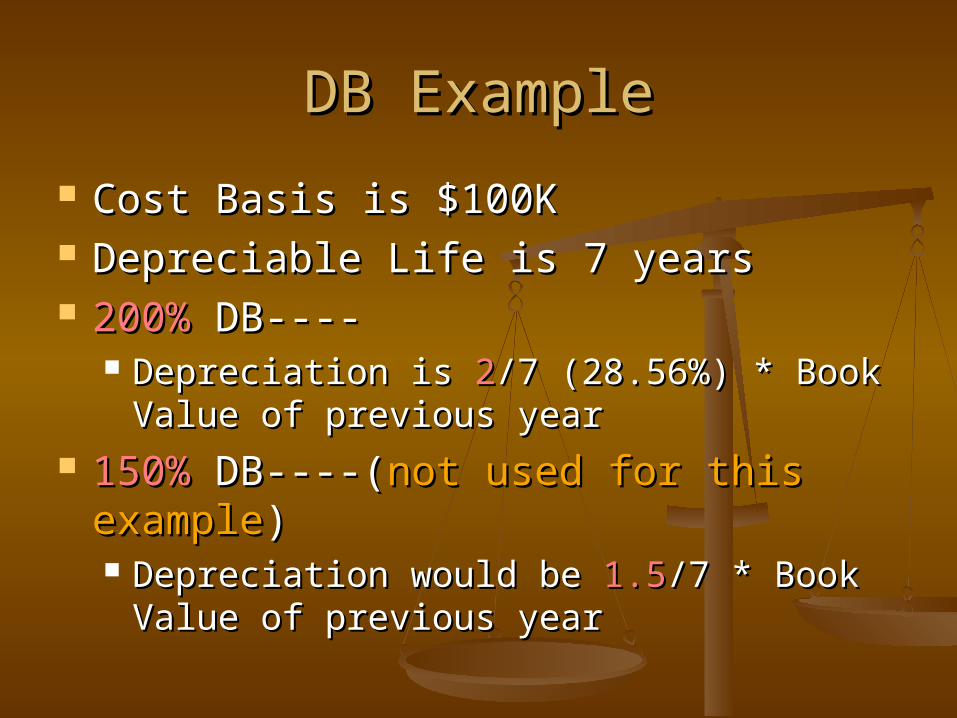

DB ExampleDB Example

Cost Basis is $100KCost Basis is $100K Depreciable Life is 7 yearsDepreciable Life is 7 years 200%200% DB---- DB----

Depreciation is Depreciation is 22/7 (28.56%) * Book /7 (28.56%) * Book Value of previous yearValue of previous year

150%150% DB----( DB----(not used for this not used for this exampleexample)) Depreciation would be Depreciation would be 1.51.5/7 * Book Value /7 * Book Value

of previous yearof previous year

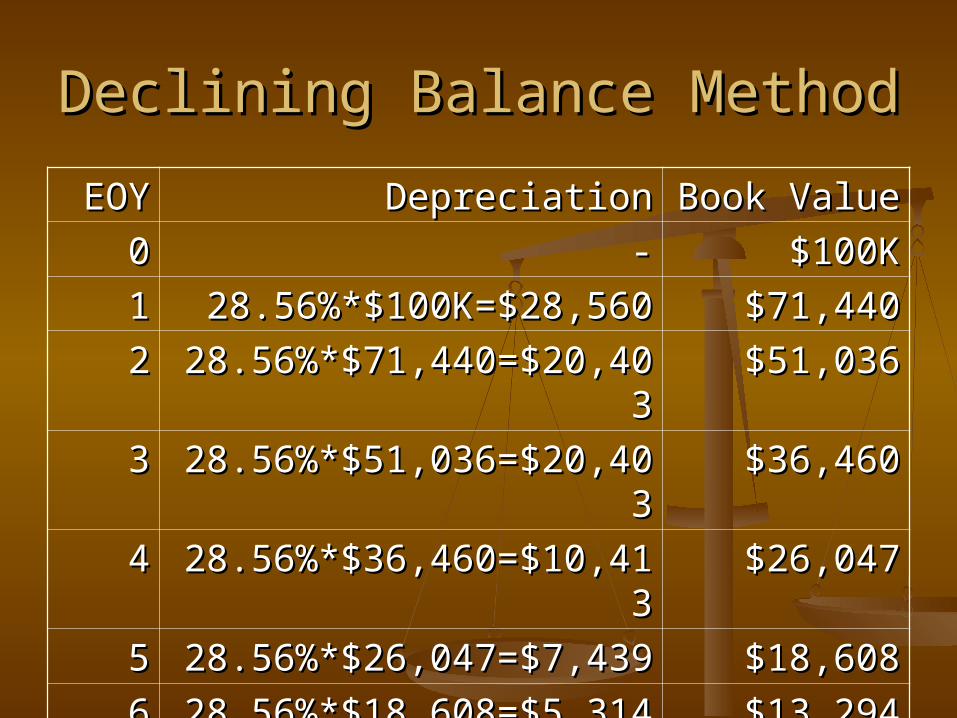

Declining Balance MethodDeclining Balance Method

EOYEOY DepreciationDepreciation Book ValueBook Value

00 -- $100K$100K

11 28.56%*$100K=$28,56028.56%*$100K=$28,560 $71,440$71,440

22 28.56%*$71,440=$20,4028.56%*$71,440=$20,4033

$51,036$51,036

33 28.56%*$51,036=$20,4028.56%*$51,036=$20,4033

$36,460$36,460

44 28.56%*$36,460=$10,4128.56%*$36,460=$10,4133

$26,047$26,047

55 28.56%*$26,047=$7,43928.56%*$26,047=$7,439 $18,608$18,608

66 28.56%*$18,608=$5,31428.56%*$18,608=$5,314 $13,294$13,294

77 28.56%*$13,294=$3,79728.56%*$13,294=$3,797 $9,497$9,497

What’s Wrong with this Method?What’s Wrong with this Method?

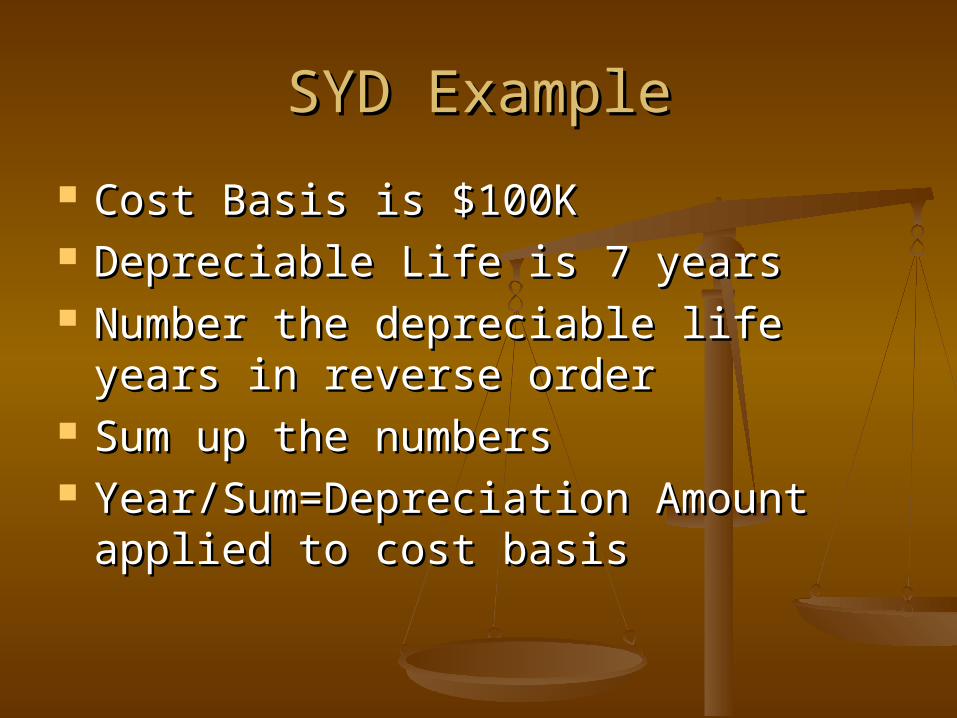

SYD ExampleSYD Example

Cost Basis is $100KCost Basis is $100K Depreciable Life is 7 yearsDepreciable Life is 7 years Number the depreciable life years in Number the depreciable life years in

reverse orderreverse order Sum up the numbersSum up the numbers Year/Sum=Depreciation Amount Year/Sum=Depreciation Amount

applied to cost basisapplied to cost basis

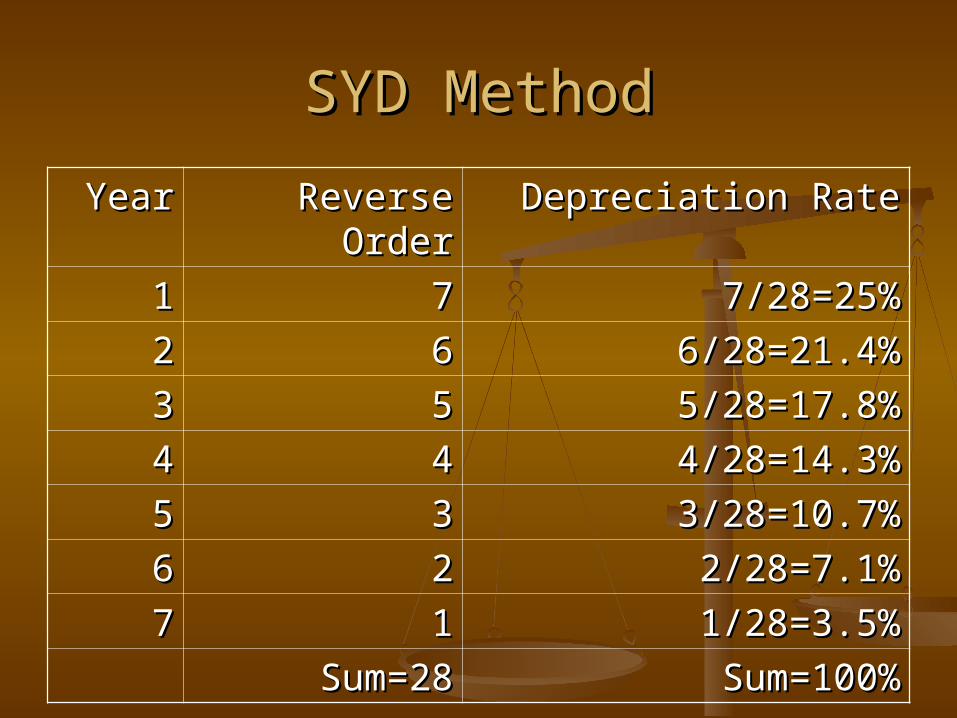

SYD MethodSYD Method

YearYear Reverse Reverse OrderOrder

Depreciation RateDepreciation Rate

11 77 7/28=25%7/28=25%

22 66 6/28=21.4%6/28=21.4%

33 55 5/28=17.8%5/28=17.8%

44 44 4/28=14.3%4/28=14.3%

55 33 3/28=10.7%3/28=10.7%

66 22 2/28=7.1%2/28=7.1%

77 11 1/28=3.5%1/28=3.5%

Sum=28Sum=28 Sum=100%Sum=100%

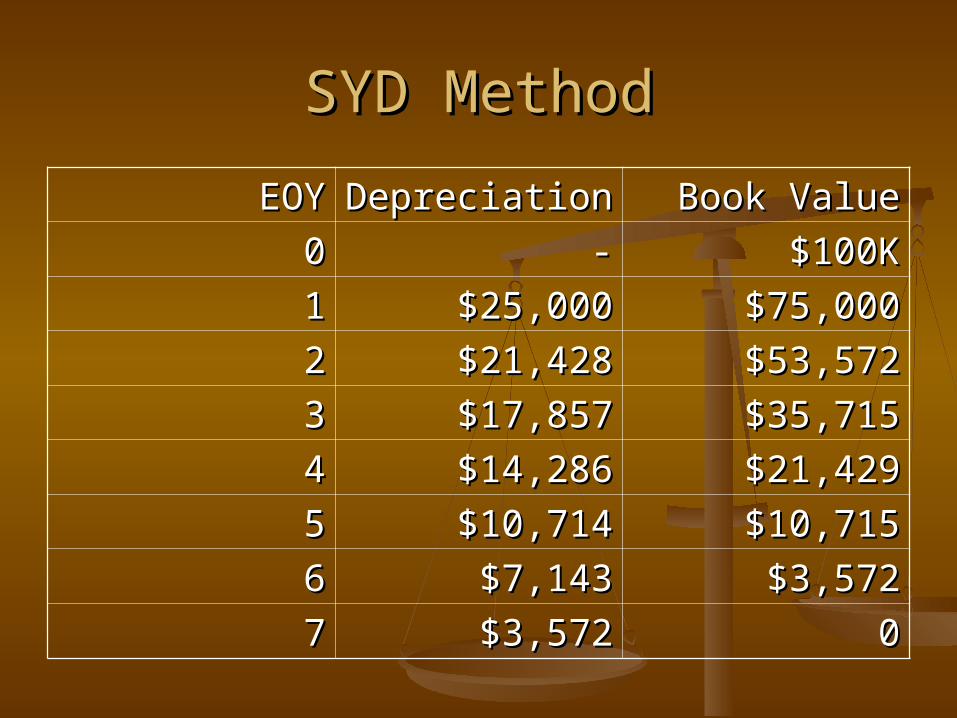

SYD MethodSYD Method

EOYEOY DepreciationDepreciation Book ValueBook Value

00 -- $100K$100K

11 $25,000$25,000 $75,000$75,000

22 $21,428$21,428 $53,572$53,572

33 $17,857$17,857 $35,715$35,715

44 $14,286$14,286 $21,429$21,429

55 $10,714$10,714 $10,715$10,715

66 $7,143$7,143 $3,572$3,572

77 $3,572$3,572 00

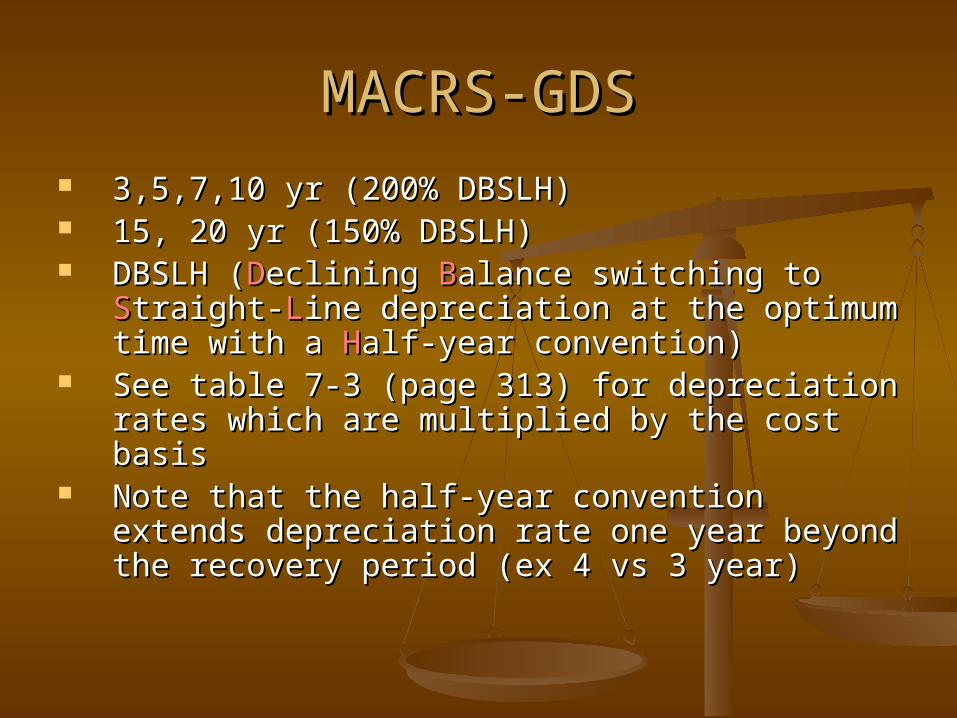

MACRS-GDSMACRS-GDS

3,5,7,10 yr (200% DBSLH)3,5,7,10 yr (200% DBSLH) 15, 20 yr (150% DBSLH)15, 20 yr (150% DBSLH) DBSLH (DBSLH (DDeclining eclining BBalance switching to alance switching to

SStraight-traight-LLine depreciation at the optimum ine depreciation at the optimum time with a time with a HHalf-year convention)alf-year convention)

See table 7-3 (page 313) for depreciation See table 7-3 (page 313) for depreciation rates which are multiplied by the cost basisrates which are multiplied by the cost basis

Note that the half-year convention extends Note that the half-year convention extends depreciation rate one year beyond the depreciation rate one year beyond the recovery period (ex 4 vs 3 year)recovery period (ex 4 vs 3 year)

MACRS-GDS MethodMACRS-GDS Method

EOYEOY DepreciationDepreciation Book ValueBook Value

00 -- $100K$100K

11 14.29%*$100K=$14,29014.29%*$100K=$14,290 $85,710$85,710

22 24.49%*$100k=$24,49024.49%*$100k=$24,490 $61,220$61,220

33 17.49%*$100K=$17,49017.49%*$100K=$17,490 $43,730$43,730

44 12.49%*$100K=$12,49012.49%*$100K=$12,490 $31,230$31,230

55 8.93%*$100K=$8,9308.93%*$100K=$8,930 $22,310$22,310

66 8.92%*$100K=$8,9208.92%*$100K=$8,920 $13,390$13,390

77 8.93%*$100K=$8,9308.93%*$100K=$8,930 $4,460$4,460

88 4.46%*$100K=$4,4604.46%*$100K=$4,460 $0$0

Depreciation Methods

$0$20,000$40,000$60,000$80,000

$100,000

0 1 2 3 4 5 6 7 8 9

EOY

Book

Valu

e

Straight Line MethodDeclining BalanceSum of YearsDB switch to SL

Next lectureNext lecture

TaxesTaxes

ATCF’s taking into ATCF’s taking into account depreciationaccount depreciation