ct 2007 ar-eng-ppt-final(chinese script) by sylvia3 (7& 11 ... · 6 highlights strong free cash...

TRANSCRIPT

China Telecom Corporation Limited31 March 2008

www.chinatelecom-h.com

2

Certain statements contained in this document may be viewed as “forward-looking statements” within the meaning of Section 27A of the U.S. Securities Act of 1933 (as amended) and Section 21E of the U.S. Securities Exchange Act of 1934 (as amended). Such forward-looking statements are subject to known and unknown risks, uncertainties and other factors, which may cause the actual performance, financial condition or results of operations of China Telecom Corporation Limited (the “Company”) to be materially different from any future performance, financial condition or results of operations implied by such forward-looking statements. In addition, we do not intend to update these forward-looking statements. Further information regarding these risks, uncertainties and other factors is included in the Company’s most recent Annual Report on Form 20-F filed with the U.S. Securities and Exchange Commission (the “SEC”) and in the Company’s other filings with the SEC.

Forward-Looking Statements

3

Executive Director, EVP & CFOExecutive Director, EVP & CFOMadam Wu AndiMadam Wu Andi

Executive Director, President & COOExecutive Director, President & COOMr. Leng RongquanMr. Leng Rongquan

Chairman & CEOChairman & CEOMr. Wang XiaochuMr. Wang Xiaochu

Management Team

4

Agenda

OverviewOverview

Business ReviewBusiness Review

Financial PerformanceFinancial Performance

Overview

6

Highlights

Strong free cash flow greatly supports future development

Strategic transformation successfully consolidates revenue and profit

Rapidly growing non-voice business effectively alleviates operating risk

Optimized CAPEX structure significantly enhances competitive edges

7

2006

Solid Results (Excl. Connection Fees)

25.9%

-1.2%

35.6528.32Broadband Subs (Mil)

220.33223.04Access Lines in Services (Mil)

1.1%0.2780.275EPS* (RMB)

17.2%33,96428,991Free Cash Flow** (RMB Mil)

1.1%

-0.7pp

1.3%

2.8%

22,51722,270Net Profit* (RMB Mil)

49.0%49.7%EBITDA Margin

85,97484,866EBITDA (RMB Mil)

175,362170,645Operating Revenue (RMB Mil)

2007 Growth

Note: Unless otherwise stated, all financial data used hereinafter exclude upfront connection fees* Excluding the impact of revaluation in 2007 of property, plant & equipment every 3 years (see slide 25)** Free Cash Flow = EBITDA (Excl. connection fees) – CAPEX – Income Tax

8

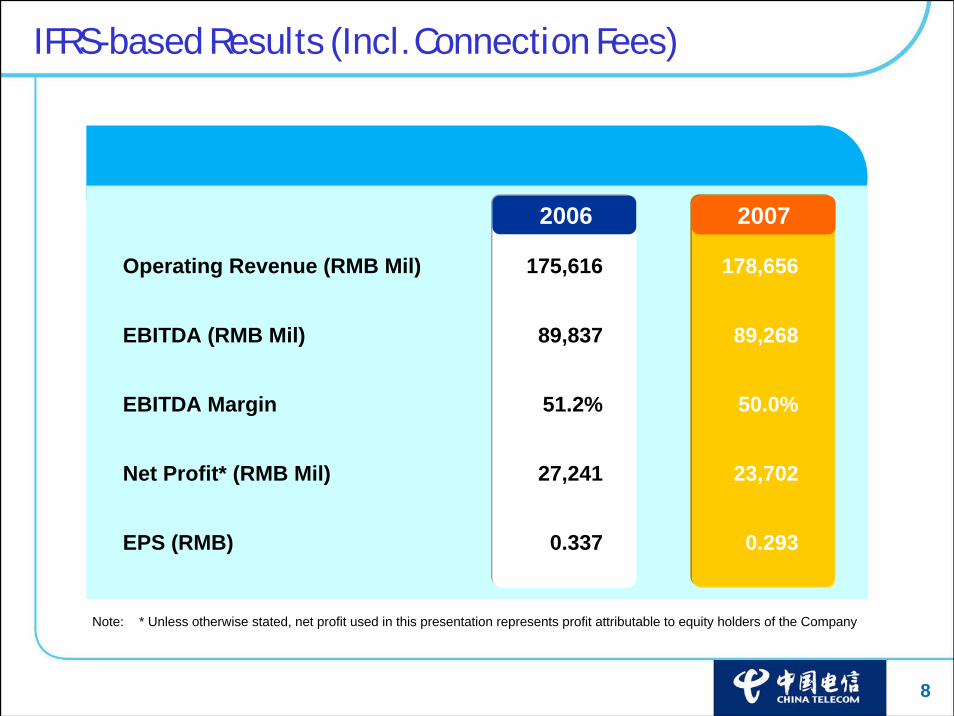

0.2930.337EPS (RMB)

23,70227,241Net Profit* (RMB Mil)

50.0%51.2%EBITDA Margin

89,26889,837EBITDA (RMB Mil)

178,656175,616Operating Revenue (RMB Mil)

IFRS-based Results (Incl. Connection Fees)

20072006

Note: * Unless otherwise stated, net profit used in this presentation represents profit attributable to equity holders of the Company

9

Voice Business*

2006 2007

RMB Mil

2.8% Contribution

Managed Data, Leased Line &

Others

Internet Access

VAS & Integrated

Information Services

Revenue Growth Drivers

+4.5pp-5.6pp +2.9pp +1.0pp

+2.8%1,6725,028-9,599 7,616

Note: * Voice Business Revenue includes Monthly Fees, Local Usage Fees, Upfront Installation Fees, DLD/ILD and Interconnection Revenue

170,645175,362

10

Proactively Managing Voice Challenges

Revenue Growth by Customer Segments in 2007

Steady Aggregate Revenue

Voice Revenue Non-Voice Revenue

RMB Mil

2006 2007

120,911 111,312

49,734 64,050

Major challenges in voice business

Rapidly declining mobile voice tariff (-17.7% yoy) & new means of communications

-Voice revenue 7.9%-Voice ARPU: RMB41.8 10.1%

Major initiatives

Strengthen integrated development of voice and non-voice businesses to improve voice services’ value to customers and mitigate voice revenue decline

Target at key customer segments like government & enterprise and household customers

Strictly control marketing expense on low-end customers to ensure return

11.2%

-13.9%

4.3%

Household IndividualGovernment & Enterprise

170,645 175,362

CT’s overall revenue growth (+2.8%)

-7.9%

+2.8%

+28.8%

Share of Revenue: 33.8% 48.0% 18.2%

11

Robust non-voice revenue growth supported steady aggregate revenue and healthy fundamental

Optimized revenue structure effectively alleviated operating risk

Non-voice revenue as a % of operating revenue:06: 4.7pp 07: 7.4pp

Enhanced core competitiveness & sustainable development

49,734

RMB Mil

29.1%

64,050

36.5%

+24.9%

Non-Voice Revenue as a % of Operating Revenue2005 2006 2007

24.4%

39,828

Strategic Transformation Gaining Momentum

Accomplishments+28.8%

21.1%( 14.2% yoy)

VAS & Integrated Information Services

Managed Data, Leased Line & Others

InternetAccess

30.0%( 35.4% yoy) 48.9%

( 32.1% yoy)

Non-Voice Revenue

Non-Voice Revenue Composition in 2007

12

27.3% yoy35.4% yoy

VAS & Integrated Information Services

32.9% yoyBroadband Access

InvestmentRevenue

CAPEX

CAPEX as a % of Operating Revenue

RMB Mil

28.8%

26.0%

49,116

45,55845,000

2006 2007 2008E

CAPEX

-7.2%-1.2%

Continuous CAPEX reduction leads to progressive decline of depreciation & amortization expenses as a % of operating revenue and enhances operating return

Tilting investments towards transformationbusiness to drive revenue

Vs. 07E saving of RMB1,442 mil

Reducing CAPEX to enhance return; Optimizing structure to

promote developmentInclude an extraRMB960 mil due

to snowstorm

13

Performance ofBeijing Telecom in 2007

Revenue: RMB2,455 mil

Net Profit: RMB470 mil

Acquisition of Beijing Telecom

RMB5,557 million

RMB5,557 million

China Telecommunications

Group

China Telecom Corporation LimitedLeveraging the business

opportunities in the capital city (political, economic and

cultural center)

Enhancing services to our key government & enterprise

customers with headquarters in Beijing

Note: The above financial data are unaudited and IFRS-based

Earnings Accretive Acquisition

14

Dividend Per Share

HKD

0.085 0.085

2006 2007

Dividend

The Board of Directors recommended a final dividend

of HKD0.085 for 2007

Proper balance between shareholders’ cash return demand and company’s future investment needs, especially the funding requirement for coming full services offerings

15

Driving Transformation to Enhance Value

Seize Leading Advantages in Information Services

Customer-focused

Market Segmentation

Capturing Opportunities

Seize Leading Advantages in Information Services

Customer-focused

Market Segmentation

Capturing Opportunities

Integrated and bundled services of

fixed and mobile businesses

Integrated development of fixed

and mobile broadband

Integrated and bundled services of

fixed and mobile businesses

Integrated development of fixed

and mobile broadband

Integrated Information Services

Provider

Integrated Information Services

Provider

FMCFMC

Quadruple Play

Quadruple Play

Enhancing Shareholders’ ValueEnhancing Shareholders’ Value

Enriching Customers’ LifeEnriching Customers’ Life

Talents Pool

Brand Management

Capital Accumulation

Network Enhancement

Information Services

Talents Pool

Brand Management

Capital Accumulation

Network Enhancement

Information Services

Fixed + Mobile+ +

Media + Data

Fixed + Mobile+ +

Media + Data

Customer-focused Innovative Informatization

Strategies

Customer-focused Innovative Informatization

StrategiesFull Services

OfferingFull Services

Offering

Proactive Preparation for Full Services Operations

BusinessR E V I E W

17

Share of Operating Revenue

2006(RMB Mil) Growth2007

(RMB Mil)

Revenue Breakdown

17.9%32.1%31,34023,724Internet Access

40.1%-9.8%70,42478,074Sub-total

100%

7.7%

11.0%

7.9%

15.4%

24.1%

14.4%

1.6%

2.8%175,362170,645Total

14.2%13,47911,807Managed Data, Leased Line & Others

35.4%19,23114,203VAS & Integrated Information Services

-1.5%13,87914,095Interconnections

-6.0%27,00928,742Long Distance

-8.3%42,34346,188Local Usage Fees

-12.5%25,34628,973Monthly Fees

-6.1%2,7352,913Upfront Installation Fees

Local Voice

18

Local Voice Business

Mil 220.3223.0

2006.12 2007.12

Household

Government & Enterprise

Individual62.7

15.522.5

122.3

24.8

121.8

58.0

15.7Public Telephone

PAS PAS

Local Voice Business

Usage Revenue

422,562406,268

-3.9%PulsesMil

RMB Mil -9.8%

78,07470,424

2006 2007

Public Telephone

Consolidating Traditional Businesses via effective bundling with Transformation Businesses

Government & Enterprise customers: Promoting “BizNavigator” to stabilize usage

-Revenue 11.2% yoy

Household customers: Leveraging “One Home” to consolidate household market

-Revenue 4.3% yoy

Individual customers: Severechallenge due to intensified mobile substitution especially on PAS

-Revenue 13.9% yoy

To strengthen bundled packages to consolidate high-end PAS subs while strictly controlling marketing expense on low-end customers to ensure return

2006 2007

Access Lines in Services

19

Market Share by Usage

Long Distance Business

Domestic Long Distance

International Long Distance

Consolidating Long Distance Business

Usage Revenue

95,567 98,251

+2.8%Minutes Mil

32.8%39.2%

RMB Mil -5.4%

25,517 24,127

13.8%15.0%

Usage Revenue

1,601 1,588

-0.8%Minutes Mil

42.5%45.8%

RMB Mil -10.6%

3,225 2,882

1.6%1.9%

Long Distance Revenue as a % of Operating Revenue

Intensified competition in long distance market led to continuous decline in average unit price; avoiding direct price competition and stimulating long distance usage by customized bundling packages

- DLD usage 2.8% yoy- ILD usage relatively stable

Leveraging flexible strategies to promote integrated development of voice and integrated information services

2006 2006

2006 2006

2007 2007

2007 2007

20

Broadband Business

2006.12 2007.12

28.3235.65

7.307.33

Net Adds

Mil +25.9%

Subs

77 80

+32.9%

2006 2007

23,147

30,768

Access Revenue

Broadband ARPU (RMB)

RMB Mil

Office Automation

SecurityControl

OnlineMusic

SearchEngine

ERPSystems

OnlineVideo

VirtualNetwork

e-administrationSystems VOIP e-Payment

…… e-Trading ……

Government &Government &EnterpriseEnterprise

Household &Household &IndividualIndividual

Profitable Scale Development with Differentiated Operations

Broadband subs 7.33 mil with ARPU slightly increased to RMB 80 in 2007

To realize wireless access roaming for broadband subs by enriching means and convenience of access

To fully implement broadband account number operation & promote co-operation and customization of terminal devices, Internet applications and content

To strengthen interactive promotion of Internet access & application businesses

InternetBankingSystems

Broadband

21

20072006

14,20319,231

RMB Mil

VAS & Integrated Information Services

Revenue

+35.4%

Strategies

Revenue Growth & Mix in 2007

11.0%

VAS & Integrated Information Services Revenue as a % of Operating Revenue

19.5% 56.0% 108.1% 90.1% 155.5%

415.8%

69.8%

12.6% 8.4% 2.2% 3.8% 3.2%

Revenue Growth

Revenue Mix

Note: * Fixed-line VAS mainly includes Caller-ID, Telephone Information Services, SMS & Color Ring Tone**Internet VAS mainly includes VNet, IDC, IP/VPDN

8.3%

Fixed-line VAS*

Internet VAS**

IT Services & Applications

Enterprise Informatization

Applications

Best Tone Video Applications

Fixed-line VAS: Focus on services like fixed-line color ring-tone, fixed-line payment, phone-radio…to increase VAS penetration and promote scale development

Internet VAS: Integrate VNet with content resources and enrich Internet applications like searching, digital music, One Home customer terminals... to enhance customer brand value and stimulate consumption

Integrated Information Services: Consolidate telephone number resource services and explore demand from government & enterprise customers to promote the scale development of Best Tone and IT Services & Applications

22

InformatizationInformatization DevelopmentDevelopment

Enhance value through integrated &

differentiated services

Enhance value through integrated &

differentiated services

IPIPCommunicationsCommunications

Information Information TechnologyTechnology

InformationInformationServicesServices

CustomerCustomer--focusedfocused

Focus on converged

areas of “3Is”

Focus on converged

areas of “3Is”

Leverage extensive

communications infrastructure

Leverage extensive

communications infrastructure

Scale Development of Transformation Businesses

Golden Golden OpportunityOpportunity

Excavate new informatization demand

from customers

Customer-focused operation & resource

allocation

Excavate new informatization demand

from customers

Customer-focused operation & resource

allocation

FinancialPerformance

24

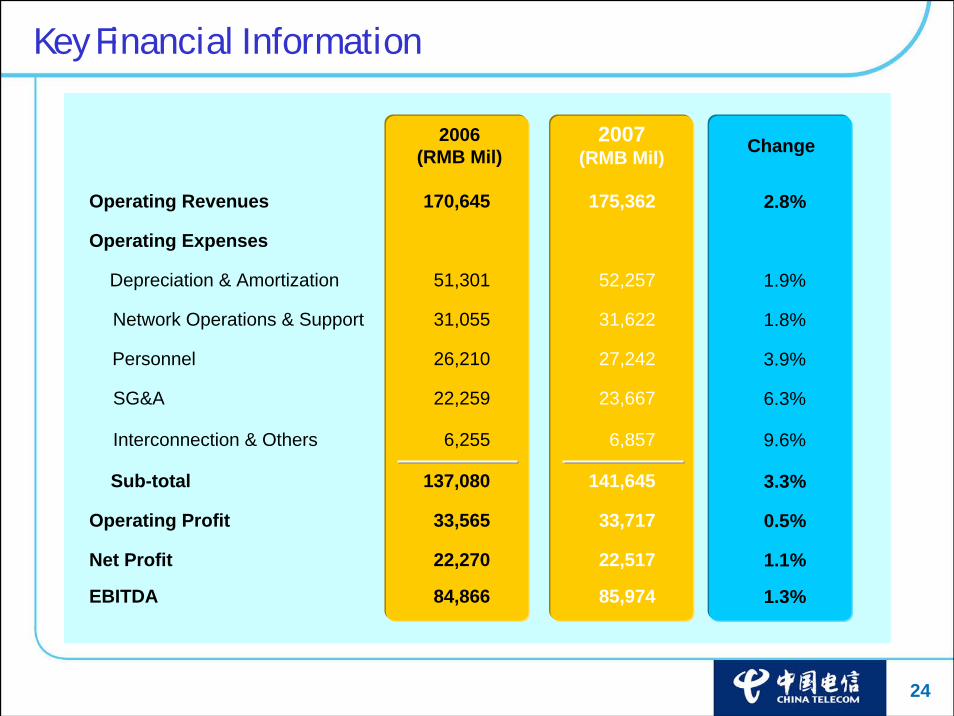

2006(RMB Mil)

2007(RMB Mil) Change

3.3%141,645137,080Sub-total

1.3%

1.1%

0.5%

9.6%

6.3%

3.9%

1.8%

1.9%

2.8%

85,974

22,517

33,717

6,857

23,667

27,242

31,622

52,257

175,362

84,866EBITDA

22,270Net Profit

33,565Operating Profit

6,255Interconnection & Others

22,259SG&A

26,210Personnel

31,055Network Operations & Support

51,301Depreciation & Amortization

Operating Expenses

170,645Operating Revenues

Key Financial Information

25

2007 Revaluation

Property, Plant & Equipment Revaluation

RMB Mil

Revaluation Surplus

Revaluation Deficit

4,809

(2,755)

Per IFRS:Revaluation Surplus EquityRevaluation Deficit Income Statement

Revalued PPE every 3 years per IFRS. Overall net revaluation surplus showed good asset quality

RMB22,517 milAdjusted net profit:

2,109 milEx-revaluation deficit & related tax impact:

(3,294) milEx-upfront connection fees:

RMB23,702 milIFRS-based net profit:

26

Operating Expenses

Depreciation & Amortization

Network Operations & Support

SG&A

Personnel

80.8%

Interconnection & Others

29.8%

18.1%

15.5%

13.5%

3.9%2006 2007

Cost Structure

Operating Expenses as a % of Operating Revenue

80.3%

30.1%

18.2%

15.4%

13.0%

3.6%

27

Optimized Cost Structure to Support Business Development

Cost Initiatives 2007 Results

Depreciation &AmortizationReduced depreciation as a % of operating revenue continuously via strict CAPEX control & enhanced resource utilization

Network Operations & SupportTilted and smoothed resource allocation towards transformation businesses to support development

PersonnelEnhanced employees’ incentive & strengthened recruitment of IP, IT and IS talents

SG&APromoted brand operation & transformation businesses, enhanced customer retention but strictly controlled PAS handset subsidy

Depreciation &AmortizationReduced depreciation as a % of operating revenue continuously via strict CAPEX control & enhanced resource utilization

Network Operations & SupportTilted and smoothed resource allocation towards transformation businesses to support development

PersonnelEnhanced employees’ incentive & strengthened recruitment of IP, IT and IS talents

SG&APromoted brand operation & transformation businesses, enhanced customer retention but strictly controlled PAS handset subsidy

Depreciation &AmortizationRMB52,257 mil (-0.3 pp as a % of operating revenue)

Network Operations & SupportRMB31,622 mil (-0.1 pp as a % of operating revenue)

PersonnelRMB27,242 mil (maintained relatively stable as a % of operating revenue)

SG&ARMB23,667 mil (+0.5 pp as a % of operating revenue)

Depreciation &AmortizationRMB52,257 mil (-0.3 pp as a % of operating revenue)

Network Operations & SupportRMB31,622 mil (-0.1 pp as a % of operating revenue)

PersonnelRMB27,242 mil (maintained relatively stable as a % of operating revenue)

SG&ARMB23,667 mil (+0.5 pp as a % of operating revenue)

Strengthened cost control

Optimized cost structure

Maintained relatively stableEBITDA margin

Strengthened cost control

Optimized cost structure

Maintained relatively stableEBITDA margin

28

CAPEX Structure

Enhanced CAPEX Structure

RMB Mil

2006 2007 Note: *Others include communication infrastructure and

other capital expenditure

49,116 45,558

10.5%

23.3%

29.5%

7.7%

18.9%

43.7%

24.0%

20.1%6.0%

2.4%

Enhanced CAPEX structure to support strategic transformation

Internet & Data 37.4% yoy

IT Support -

Fixed Line Switches 31.9% yoy

Local Transmission & Access 22.2% yoy

PAS 63.4% yoy

Others 24.8% yoy

Tilting investment to improve network capability for supporting transformation businesses while strictly controlling CAPEX on traditional business

6.7%

7.2%

Internet & Data

IT Support

Fixed Line SwitchesLocal Transmission& AccessPAS

Others*

29

Solid Financial Strength

RMB Mil

35.5%

2006 2007

28,99130.8%33,964

Total Debt / Total Capitalization Free Cash Flow

+17.2%-4.7pp

2006 2007

1.21

2006 2007

0.98

Net Debt / EBITDA

-0.23x

Solid financial fundamental and strong cash flow proactively equSolid financial fundamental and strong cash flow proactively equip the ip the Company to capture future growth opportunitiesCompany to capture future growth opportunities

30

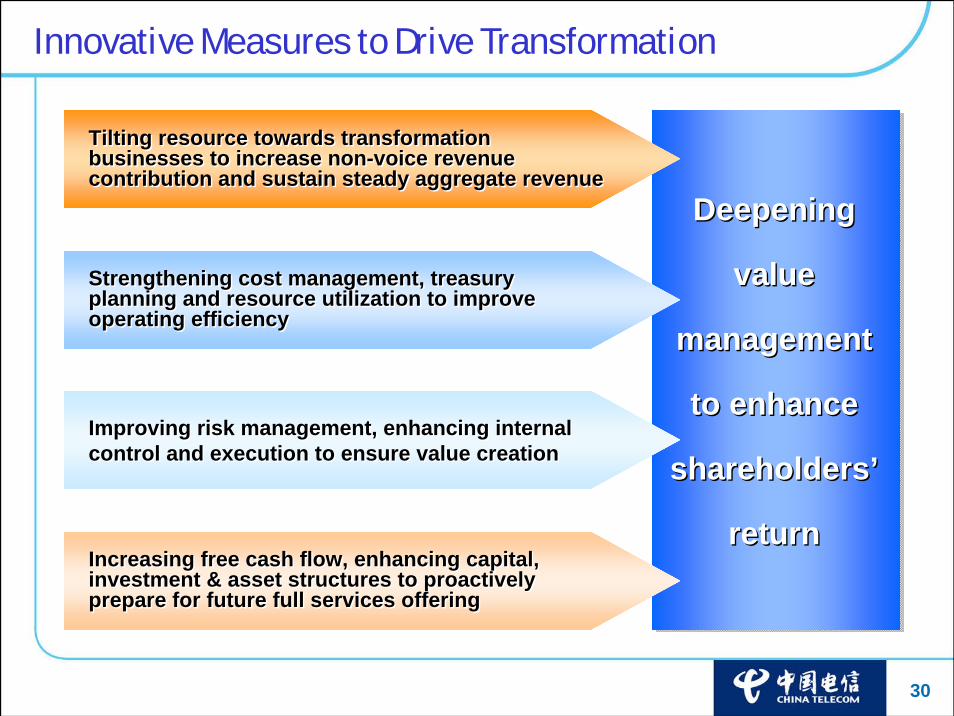

Tilting resource towards transformation businesses to increase non-voice revenue contribution and sustain steady aggregate revenue

Tilting resource towards transformation businesses to increase non-voice revenue contribution and sustain steady aggregate revenue

Deepening

value

management

to enhance

shareholders’

return

Deepening

value

management

to enhance

shareholders’

return

Improving risk management, enhancing internal control and execution to ensure value creationImproving risk management, enhancing internal control and execution to ensure value creation

Innovative Measures to Drive Transformation

Increasing free cash flow, enhancing capital, investment & asset structures to proactively prepare for future full services offering

Increasing free cash flow, enhancing capital, investment & asset structures to proactively prepare for future full services offering

Strengthening cost management, treasury planning and resource utilization to improve operating efficiency

Strengthening cost management, treasury planning and resource utilization to improve operating efficiency

31

ThankY O U

www.chinatelecom-h.com

32

2006(Restated)*

2007

(2,755)-Revaluation Deficit

23,70227,241Equity Holders of the Company

30,25134,083Profit Before Taxation

(141,645)(137,080)Operating Expenses

97

23,799(6,452)

295

(4,300)

3,294

178,656

83Minority Interests

27,324Profit for the Year(6,759)Income Tax

36Investment Loss, Share of Profit from Associates

(4,489)Net Finance Costs

4,971Upfront Connection Fees

175,616Operating Revenues

Extracted from audited consolidated income statementfor the year ended 31 Dec 2007 (incl. upfront connection fees)Appendix 1

Note: *Restated to include the financial impact of acquisition of China Telecom (HK), China Telecom (Americas) and China Telecom System Integration

RMB Mil

33

Extracted from audited consolidated balance sheet as at 31 Dec 2007(incl. upfront connection fees)

2006 (Restated)*

1,4511,448Minority Interests

185,632211,222Total Liabilities

408,004418,871Total Assets

220,921

222,372

47,095

138,537

365,324

42,680

206,201Equity Attributable to Equity Holders of the Company

207,649Total Equity

53,593Non-current Liabilities

157,629Current Liabilities

374,665Non-current Assets

44,206Current Assets

2007

Appendix 2

RMB Mil

Note: *Restated to include the financial impact of acquisition of China Telecom (HK), China Telecom (Americas) and China Telecom System Integration

34

Detailed operating revenues breakdownfor the year ended 31 Dec 2007 (incl. upfront connection fees)

2006 (Restated)*

2007

Appendix 3

Note: *Restated to include the financial impact of acquisition of China Telecom (HK), China Telecom (Americas) and China Telecom System Integration

3,0133,080Managed Data

13,87914,095Interconnections

19,23114,203VAS & Integrated Information Services

5,3214,548Leased Line5,1454,179Others

178,656175,616Total

42,34346,188Local Usage fees24,12725,517DLD

70,42478,074Local Voice Business

31,340

2,882

25,3462,735

3,294

23,724Internet Access

3,225ILD

28,973Monthly Fees2,913Upfront Installation Fees

4,971Upfront Connection Fees

RMB Mil