cs vz en prezentacni i 09 - Česká spořitelna

TRANSCRIPT

ČESKÁ SPOŘITELNA

Annual Report 2007

Consolidated Financial Highlights under International Financial Reporting Standards (IFRS)

Balance Sheet Highlights

MCZK 2007 2006 2005 2004 2003

Total assets 814,125 728,393 654,064 581,780 555,417

Loans and advances to fi nancial institutions 65,688 73,179 97,846 77,112 82,121

Loans and advances to customers 418,415 329,105 283,420 239,289 214,903

Securities 226,813 230,354 192,210 191,627 180,738

Amounts owed to fi nancial institutions 58,482 46,361 34,898 32,905 29,641

Amounts owed to customers 588,526 537,487 481,556 444,771 428,572

Shareholders’ equity 55,576 48,594 43,322 39,299 34,408

Profi t and Loss Account Highlights

MCZK 2007 2006 2005 2004 2003

Net interest income 24,727 21,206 18,719 17,416 15,874

Net fee and commission income 9,639 8,997 8,384 8,238 7,915

Operating income 36,724 32,471 28,834 27,217 25,268

Operating expenses (18,349) (17,316) (16,395) (15,883) (15,073)

Operating profi t 18,375 15,155 12,439 11,334 10,195

Net profi t net of minority interests 12,148 10,385 9,134 8,137 7,615

Basic Ratios

2007 2006 2005 2004 2003

ROE 23.8% 23.0% 22.3% 21.8% 23.7%

ROA 1.5% 1.5% 1.4% 1.4% 1.4%

Cost/income 50.0% 53.3% 56.9% 58.4% 59.7%

Non-interest income/operating income 32.7% 34.7% 35.1% 36.0% 37.2%

Net interest margin to gross assets 3.2% 3.0% 3.0% 3.0% 2.9%

Customer loans/customer deposits 71.1% 61.2% 58.9% 53.8% 50.1%

Capital adequacy* 9.4% 11.1% 11.1% 13.3% 14.6%

*in 2003–2006 BIS, in 2007 Basel II

Key Operating Indicators

Number 2007 2006 2005 2004 2003

Staff (average headcount) 10,897 10,809 11,406 11,805 12,786

Česká spořitelna’s branches 636 637 646 647 666

Clients 5,294,470 5,276,897 5,326,378 5,353,923 5,519,627

Sporogiro accounts 2,838,173 2,789,076 2,761,062 2,757,929 2,755,113

Active cards 3,340,180 3,095,614 2,941,843 2,758,486 2,576,552

of which: credit cards 622,161 447,089 340,510 204,564 101,155

Active users of SERVIS 24 and BUSINESS 24 1,142,170 1,033,198 934,874 772,185 609,563

ATMs 1,124 1,090 1,076 1,071 1,067

Rating

Rating agency Long-term rating Short-term rating Outlook

Fitch A F1 positive

Moody's A1 Prime-1 stable

Standard & Poor's A A1 stable

1

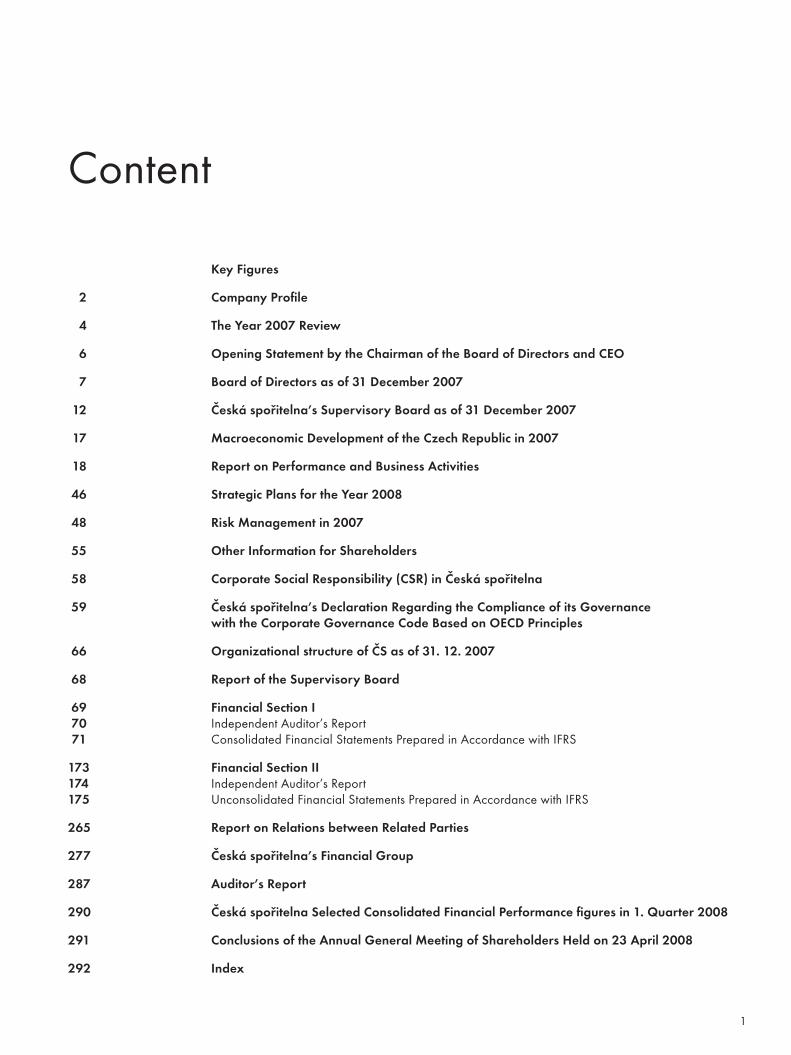

Content

Key Figures

2 Company Profi le

4 The Year 2007 Review

6 Opening Statement by the Chairman of the Board of Directors and CEO

7 Board of Directors as of 31 December 2007

12 Česká spořitelna’s Supervisory Board as of 31 December 2007

17 Macroeconomic Development of the Czech Republic in 2007

18 Report on Performance and Business Activities

46 Strategic Plans for the Year 2008

48 Risk Management in 2007

55 Other Information for Shareholders

58 Corporate Social Responsibility (CSR) in Česká spořitelna

59 Česká spořitelna’s Declaration Regarding the Compliance of its Governance with the Corporate Governance Code Based on OECD Principles

66 Organizational structure of ČS as of 31. 12. 2007

68 Report of the Supervisory Board

69 Financial Section I 70 Independent Auditor’s Report 71 Consolidated Financial Statements Prepared in Accordance with IFRS

173 Financial Section II 174 Independent Auditor’s Report 175 Unconsolidated Financial Statements Prepared in Accordance with IFRS

265 Report on Relations between Related Parties

277 Česká spořitelna’s Financial Group

287 Auditor’s Report

290 Česká spořitelna Selected Consolidated Financial Performance fi gures in 1. Quarter 2008

291 Conclusions of the Annual General Meeting of Shareholders Held on 23 April 2008

292 Index

2

Company Profi le

MarketWith 5.3 million clients, Česká spořitelna is the largest

fi nancial institution and also has the longest history among

banking institutions on the Czech market. The Bank has been

included in the esteemed Central European Erste Bank Group,

which has 16 million clients in eight European countries

(Czech Republic, Slovakia, Austria, Hungary, Croatia, Serbia,

Romania and Ukraine), since 2000.

Česká spořitelna is seen as a modern but credible bank offering

a whole range of services for all client groups on the Czech

market. Retail banking services have traditionally constituted

its core activity, but small, medium-sized and large fi rms are

also among Česká spořitelna’s key clients. More importantly,

Česká spořitelna has been the fi nancial partner of Czech cities

and municipalities, as well as a services provider in the area

of fi nancial markets. In the last few years, the Bank has won

a leading position on the market in modern banking disciplines

such as credit cards, internet banking, mortgage and consumer

lending and other services.

The fi nancial group manages clients’ fi nancial assets exceed-

ing CZK 814 billion. The Bank generated a net profi t of

CZK 12.15 billion in 2007, which makes Česká spořitelna one of

the leading Erste Bank Group companies in terms of profi tability.

HistoryThe roots of Česká spořitelna date back to 1825, when

Spořitelna Česká, the oldest legal predecessor of today’s Česká

spořitelna, began its activities. One of the most important

objectives of the Bank since then has been emphasis on a close

relationship with clients intrusting the Bank with their savings.

The Bank therefore focused on building a broad network of

branches in the past and continues to focus on this objective.

Česká spořitelna decided to follow the tradition of the Czech

and later Czechoslovak savings institutions, when it arose as

a newly-established joint stock company in 1992. In 2000

Česká spořitelna became a member of the Erste Bank Group,

which was a break from the past and the beginning of Česká

spořitelna's modern history. This union with a strong partner

on the highly competitive European market provided Česká

spořitelna with a solid basis for the fulfi lment of their vision

of a strong and competitive bank.

The Bank undertook an ambitious transformation from

July 2000 to December 2001 which affected all areas of the

Bank’s life. Česká spořitelna was gradually transformed into

a modern, client-oriented fi nancial institution with a broad

offering of quality products. One of the most important steps

was the reinforcement of rentability and profi tability of the

whole fi nancial group and also the adoption of the Erste Bank

Group’s corporate design.

Products Our clients may use standard banking services provided at

Česká spořitelna’s branches, but they also conclude contracts

of building savings, pension insurance, life insurance, leasing

or contracts on collective investing in mutual funds. Česká

spořitelna also offers advisory, leasing and factoring services

to corporate clients. The Bank’s close cooperation with its

fourteen subsidiaries facilitates the provision of this compre-

hensive offering.

Česká spořitelna believes that there is no such thing as an

average client. All clients are unique and have specifi c wishes

and needs. The Bank is ready to individually advise a client

on loans, so that the repayment schedule and the drawn

amount perfectly suit the client's needs and possibilities. Česká

spořitelna offers fl exible personal accounts for transactions

which vary according to the clients’ needs. The Bank provides

a detailed investment profi le according to the specifi c pos-

sibilities and needs of each client interested in investing. Our

experts then recommend each client a method of deposit which

suits the client’s individual needs and approach to risks.

Česká spořitelna is primarily a bank for retail clients, but

the support of small and medium-sized enterprises in their

development is part of the Bank's programmes. In the last few

years, Česká spořitelna has succeeded in building one of the

best and most dynamic growing corporate banking services on

the market. Besides programmes for retail and medium-sized

enterprises, Česká spořitelna is a strong player in fi nancing

large enterprises and corporations, and the Bank’s share in this

closely watched segment of the market is still growing.

Services provided for cities and municipalities constitute

a key area for Česká spořitelna. The Bank manages complex

accounts of budget management and secures systems of

3

ContentCompany Profi leThe Year 2007 Review

payment for most of them. Advantageous fi nancial services

enable the municipalities to accelerate a number of investment

transactions principally concerning the reconstruction and

construction of infrastructure or new fl ats.

Česká spořitelna also facilitates the drawing of funding from

the European Union. The Bank offers cities, municipalities and

fi rms a complex programme, and prepares and helps imple-

ment projects that are fi nanced by this funding.

Česká spořitelna is the leading player in introducing new

services and technologies. More and more clients use the Bank’s

modern direct banking services thanks to this approach, both

over the phone and through the internet. Over a million clients

use our direct banking services, i. e. SERVIS 24 for retail clients

and BUSINESS 24 for fi rms. Česká spořitelna holds a leading

position in the area of payment and credit cards. The number

of payment cards with Česká spořitelna’s logo has exceeded

3.3 million, of whichmore than 620 thousand are credit cards.

Česká spořitelna’s specialised centres have facilitated faster and

more convenient access to new services and support of their

cohesion over the last few years of their existence. Mortgage

centres, offering comprehensive services for the fi nancing of

housing or investments in real estate, including offers of suitable

property, are established throughout the territory of the Czech

Republic. Česká spořitelna has also been opening commercial

centres – affi liated service points of branches specialised in

services for corporate clients. The Bank has opened the Expat

Centre in Prague, which is the fi rst specialised point of business

for foreign-language clients in the Czech Republic.

Česká spořitelna is expanding its services provided through the

ATM network. These have become multifunctional appliances

that clients can use for both cash withdrawals and also mobile

phone recharges or placing of payment orders. Česká spořitelna

introduced the very fi rst ATM for the visually impaired in the

Czech Republic at the beginning of 2005, of which now there

are a total 51 available throughout the country.

4

The Year 2007 Review

January• Česká spořitelna provides a guarantee against unauthorised

transactions performed with lost or stolen credit cards that

exceed CZK 4,500 in the 48 hour period before the card is

blocked. The Bank also expanded insurance to cover card

misuse 96 hours before the card is blocked and includes

PIN transactions.

• SERVIS 24 provided a new START service for clients who

do not have any account with Česká spořitelna and want

to be informed about their products provided by Česká

spořitelna’s subsidiaries.

February• Česká spořitelna introduced a Price List providing

a summary of prices for the most frequently used products

and services, primarily relating to every-day transactions.

Thanks to the Price List it is not necessary to add up

individual tariff rates of which the fi nal cost is composed.

In the same period, the Bank fundamentally modifi ed and

simplifi ed its tariff structure.

March• Clients can invest in the fi rst real estate fund in the Czech Re-

public for retail investors – 1st Real Estate Fund administered

by the Bank’s subsidiary, REICO investiční společnost ČS.

April• The number of issued credit cards exceeded half a million.

• Over 430 branches extended their working hours by more

than 800 hours a week. The working hours were extended

based on research of client needs.

• At the General Meeting, Česká spořitelna’s sharehold-

ers approved payment of dividends in the amount of

CZK 4,560 million from the 2006 profi t, which represents

CZK 30 per share.

• Moody’s increased the rating of Česká spořitelna’s long-

term deposits in a foreign currency from A2 to A1.

May• Gernot Mittendorfer became the new CEO and the Chair-

man of the Board of Directors of Česká spořitelna replacing

Jack Stack who was elected a member of the Supervisory

Board of Erste Bank.

• The fi rst offi cial Day for Charity with Česká spořitelna was

organised on 18 May. The Česká spořitelna Financial Group

joined leading global fi rms in providing their employees

with an opportunity to dedicate two working days to

charity, help to people in need, and publicly benefi cial

projects. Days for Charity with Česká spořitelna follows

the long-term projects and activities of the Česká spořitelna

Foundation and are closely related to the First Choice Bank

concept and the Corporate Social Responsibility strategy in

Česká spořitelna.

• Česká spořitelna was elected the Employer of the Region

in 2007 in the Prague region in the fi fth annual Employer

of the Year competition organised by AXA; at the national

level, a professional jury awarded the Bank a silver medal

in the main category – Employer of the Year 2007.

• The TOP Energy Programme is designed for clients

from among small and medium-sized enterprises. The

programme supports the preparation and implementation of

innovative energy projects in energy saving and production

from renewable sources. The services range from providing

initial information and funding to project management.

June• SERVIS 24 Internetbanking provides clients with the

opportunity to model a personal investment portfolio

with the most appropriate allocation of investments and

subsequently purchase, sell or exchange selected investment

products directly via internet banking.

• RAVEN EU Advisory became Česká spořitelna’s subsidiary

providing comprehensive consulting services within the

Group in the Czech and EU subsidy policy.

• Česká spořitelna received a bronze medal in the 2007 Cor-

porate Bank of the Year contest organised by MasterCard.

The decision was made based on the polling of over 150

CFOs of the most important fi rms in the Czech Republic

associated in the Czech Top 100.

• Fitch Ratings increased Česká spořitelna’s long-term rating

from A- to A and its short-term rating from F2 to F1.

5

Company Profi leThe Year 2007 ReviewOpening Statement by the Chairman of the Board of Directors and CEO

July• Česká spořitelna is the fi rst bank in the Czech market to

introduce a unique new product, @FAKTURA 24, which

allows electronic invoices between individual fi rms to be

exchanged. The electronic invoicing service provides the

advantage of sending electronic invoices safely while elimi-

nating the signifi cant time and costs required to administer

hard copy invoices.

• A new concept of comprehensive private banking services

was established under the Erste Private Banking brand.

This concept follows the standards of the Austrian Erste

Bank Group’s private banking and is targeted to clients with

fi nancial assets over CZK 5 million.

• Fitch Ratings improved the rating of Česká spořitelna’s

outlook from ‘stable’ to ‘positive’.

August• Česká spořitelna introduced a revolutionary new account to

the market – the Personal Account. Clients can now form

their own personal account by selecting the exact products

and services they want to use. The Personal Account

comprises up to 30 various levels of products and services

and clients can change and add products and services as

required.

• The total volume of the retail mortgage loan portfolio

exceeded CZK 100 billion.

September• Česká spořitelna introduced the fi rst four life cycle funds

with various investment horizons. Life cycle funds represent

a very liquid alternative to the private fi nance administration

when taking into account retirement. The key advantage of

the funds is active administration based on a fl exible mix

of money market investments, bonds, commodities and

equities during the fund period.

• In early September, Private Accounts were used by the fi rst

100 thousand clients.

October• In the sixth year of the 2007 MasterCard Bank of the Year

competition, Česká spořitelna won the Most Credible Bank

of the Year award for the fourth time in a row. The Private

Account placed fi rst in the Account of the Year category.

A professional jury named Česká spořitelna the second best

bank in the Czech Republic, and Pojišťovna ČS received

a silver medal for the Flexi life insurance. The Bank was

awarded third place in the Mortgage of the Year category

and Buřinka became third in the Construction Savings Bank

category.

• The number of giro accounts with an overdraft facility

exceeded CZK 1 million.

• In the TOP Firemní Filantrop 2007 List prepared by the

Donor Forum, Česká spořitelna placed second in the

Absolute Volume of Provided Funds category and with

CZK 59 million it was the most generous bank in the Czech

Republic.

• Standard and Poor’s improved Česká spořitelna‘s long-term

rating from A- to A and its short-term rating from A2 to A1.

November• Penzijní fond České spořitelny achieved 600 thousand

clients, and with its 16 percent share, it supported its

position as the second largest pension fund in terms of the

number of participants.

• In order to support real estate funding, the Bank established

nine specialised Development Centres which promote

the development of project fi nancing loans in Prague and

individual regions of the Czech Republic and support the

development of private mortgages from fi nanced housing

projects.

• The total volume of the client loan portfolio exceeded

CZK 400 billion.

December• ČS Real Estate Fund expanded its portfolio by four build-

ings located in Prague, Ostrava and České Budějovice.

• In December, collections from ATMs exceed their historic

maxima: on 14 December, over CZK 1.6 billion was

withdrawn from ATMs.

• The number of Private Accounts reached 400 thousand and

continues to grow.

6

Opening Statement by the Chairman of the Board of Directors and CEO

Gernot Mittendorfer, Chairman of the Board of Directors and CEO

Dear Shareholders, Ladies and Gentlemen, Clients, and Colleagues,

When I replaced Jack Stack as Česká sporitelna’s CEO last May,

I became the chief executive of a well-functioning and highly

respected fi nancial institution which had been making systematic

efforts to maintain its leading position on the Czech market, and

offer its clients top quality products and services. We will naturally

continue with this strategy and approach, thus keeping up with the

demands of today’s globally competitive environment.

Hopefully, you will not think of me as boastful when I say that

2007 was a very successful year. This success was primarily

due to the various initiatives implemented in previous years,

specifi cally the First Choice Bank programme, which reached

numerous milestones in 2007. All the measures carried out under

the Programme were specifi cally aimed at strengthening Česká

spořitelna’s leading position in retail banking and fi nancial

markets, as well as increasing its signifi cance as a bank for small

and medium-sized businesses.

To be more specifi c, last year we offered the revolutionary

‘Personal Account’, which allows our clients to customize

their accounts according to their exact needs. We extended the

opening hours of more than four hundred of our branches, and

began offering life cycle funds, as well as a new real estate fund.

We also increased the Bank’s liability for unauthorised transac-

tions made via lost cards and simplifi ed our pricing rates. These

are just some of the many examples of how we are continuously

striving to meet and exceed client expectations. The client comes

fi rst at Česká spořitelna, and we work to prove to our clients that

they benefi t by doing business with us.

Our client satisfaction survey clearly shows a long-term increas-

ing trend in the level of customer satisfaction, which just con-

fi rms that we are on the right track in providing great products,

services and value to our clients Our clients have once again

voiced their confi dence in us by giving us their highest award for

the fourth time in a row: Česká spořitelna won the 2007 “Most

Trustworthy Bank” award at the prestigious MasterCard Bank

of the Year annual awards ceremony. In addition, the ‘Personal

Account’ ranked fi rst in the “Account of the Year” category,

demonstrating that our competitors and reputable fi nancial

professionals also recognize and appreciate the quality of Česká

spořitelna’s products and services.

Another very signifi cant aspect confi rming that our strategy is

on the right track is the Bank’s fi nancial results. In 2007, we

reported a record net consolidated profi t of CZK 12.15 billion,

which is 17 percent more than in 2006, and the highest profi t

achieved in the history of our bank.

Details about Česká spořitelna’s operating results and many

other key events of 2007 are provided in the Annual Report,

which you are currently holding. All of the positive news

contained within, would not have been possible without the tire-

less efforts of the employees of the Česká spořitelna Financial

Group, who did a tremendous amount of work in 2007, and

have every right to be proud of the excellent results that we have

achieved. I am confi dent that I will be in a position to report just

as much, if not more, positive information to you next year.

April 2008

Gernot Mittendorfer

7

Opening Statement by the Chairman of the Board of Directors and CEOBoard of Directors as of 31 December 2007Česká spořitelna’s Supervisory Board as of 31 December, 2007

Board of Directors as of 31 December 2007

PAVEL KYSILKAMember of the Board of Directors and Deputy CEO

DUŠAN BARAN Vice Chairman of the Board of Directors and First Deputy CEO

JOHN JAMES STACK Chairman of the Board of Directors and CEO

Mr. Stack resigned from his positions in Česká spořitelna, a. s. as of 30 May 2007.

GERNOT MITTENDORFER Chairman of the Board of Directors and CEO

8

PETR HLAVÁČEK Member of the Board of Directors and Deputy CEO

JIŘÍ ŠKORVAGAMember of the Board of Directors and Deputy CEO

HEINZ KNOTZERMember of the Board of Directors and Deputy CEO

DANIEL HELER Member of the Board of Directors and Deputy CEO

9

Opening Statement by the Chairman of the Board of Directors and CEOBoard of Directors as of 31 December 2007Česká spořitelna’s Supervisory Board as of 31 December, 2007

GERNOT MITTENDORFER born on 2 July 1964Chairman of the Board of Directors and CEOReference Address: Olbrachtova 62, Prague 4, CZ

Mr. Mittendorfer studied law at the University of Linz and is

a graduate of Webster University in Vienna (Master of Busi-

ness Administration, specialization in fi nance). He joined Erste

Österreichische Spar-Casse Bank AG in 1990. In 1997, he was

appointed to the Board of Directors of Sparkasse Mühlviertel

West Bank AG. In 1999 he was appointed as a member of the

Board of Directors of Erste Bank Sparkassen (CR), where

he was responsible for retail banking. From July 2000 he

has been the member of the Board of Directors of Česká

spořitelna, responsible for corporate banking. He resigned

from all his functions in Financial Group of Česká spořitelna

as of 31 July 2004 after accepting the offer to become the CEO

of Salzburger Sparkasse, a member of the Erste Bank Group

family. He resigned from this function and as of 31 May 2007

he became the Chairman of the Board of Directors and CEO of

Česká spořitelna.

JOHN JAMES STACKBorn on 4 August 1946Chairman of the Board of Directors and CEOReference Address: Olbrachtova 62, Prague 4, CZ

Mr. Stack is an American citizen. He studied at Iona College

majoring in mathematics and economics (BA, 1968) and the

Harvard Graduate School of Business Administration specialis-

ing in fi nance and management (MBA, 1970).

From 1970 until 1976, Mr. Stack worked in municipal

government in New York. From 1977 until 1999 he served at

Chemical Bank, which merged into Chase Manhattan Bank,

in a variety of increasingly important positions. Before joining

Česká spořitelna he was an Executive Vice President at Chase

Manhattan Bank.

On 1 March 2000, Mr. Stack became Deputy Chairman of the

Board of Directors of Česká spořitelna. On 4 July 2000, he was

elected Chairman of the Board of Directors and CEO of Česká

spořitelna and re-elected into the function in 2004. Since 2005

Mr. Stack is a member of the Czech Banking Association.

Mr. Stack resigned from his positions in Česká spořitelna, a. s.

as of 30 May 2007.

DUŠAN BARANBorn on 6 April 1965Vice Chairman of the Board of Directors and First Deputy CEO Reference Address: Olbrachtova 62, Prague 4, CZ

Mr. Baran is a graduate of the Mathematics and Physics

Faculty of Charles University in Prague; an International

Executive MBA program at Katz Graduate School of Business,

the University of Pittsburgh together with the CMC Graduate

School of Business in Čelákovice and a banking course at

the Graduate School of Banking, University of Colorado,

Colorado, USA. During 1991–1993 he worked for Agrobanka,

a. s. in the treasury function. He joined Česká spořitelna in

November 1993, where he held various managerial positions

in Treasury and Risk Management division. He was appointed

a member of the Board of Directors and Deputy CEO of Česká

spořitelna in May 1998 and was promoted to Chairman of the

Board of Directors and CEO in March 1999. On 4 July 2000

he was elected Vice Chairman of the Board of Directors of

Česká spořitelna and appointed the First Deputy CEO. He is

also the Chief Financial Offi cer of Česká spořitelna. Mr. Baran

is a Vice Chairman of the Steering Committee of the Czech

Institute of Directors and a Treasurer of the Board of Directors

of the European Savings Banks Group (ESBG) in Brussels.

DANIEL HELERBorn on 12 December 1960Member of the Board of Directors and Deputy CEO Reference Address: Na Perštýně 1, Prague 1, CZ

Mr. Heler is a graduate of the Prague University of Econom-

ics, Faculty of International Trade. He held internships with

J. P. Morgan, Goldman Sachs, S. Montagu, UBS, N. M.

Rothschild, Shearson and Bayerische Hypobank. He has also

attended a number of courses focused on global banking,

profi tability in banking, retail banking strategy, treasury and

risk management. He has worked in the banking sector since

1983. First he held various positions in the Department of

Foreign Exchange and Money Markets and then, in 1990,

he became the Director of the Financial Markets Division

10

of Československá obchodní banka Praha. In 1992 he was

appointed as Treasurer and member of the Board of Directors

of Crédit Lyonnais Bank Praha. In 1998, he was appointed as

a member of the Board of Directors of Erste Bank Sparkassen

(CR) and assumed the responsibility for the Financial Markets.

In 1999, he became the Vice Chairman of the Board of Direc-

tors of Erste Bank Sparkassen (CR) and since 1 July 2000

he has been the member of the Board of Directors of Česká

spořitelna responsible for asset management and retail invest-

ment products, corporate fi nance and investment banking,

treasury sales and trading, capital markets, balance sheet

management, fi nancial institutions and corresponding banking.

Mr. Heler is additionally a member of the bodies of the follow-

ing companies: Nadace České spořitelny, Brokerjet ČS, Erste

Corporate Finance, a. s., RAVEN EU Advisory a. s., REICO

investment copany of ČS, the Stock Exchange Chamber and

the Deposit Insurance Fund.

HEINZ KNOTZERBorn on 8 April 1960Member of the Board of Directors and Deputy CEOReference Address: Olbrachtova 62, Prague 4, CZ

Mr. Heinz Knotzer is a graduate of the University of Vienna

where he obtained the title of JUDr. (Doctor of Jurisprudence).

He started his career in banking in after practicing as legal

assistant at courts in Austria. He worked in the legal division of

Österreichische Investitionkredit AG (Investkredit) and joined

later Girozentrale und Bank der Österreichischen Sparkassen

AG (which, after a merger in 1997, became a part of Erste

Bank), where he worked in the Investment Banking Division.

Beginning 1996 he was seconded to Creditanstalt, a. s., Prague,

after successfully completing special professional training at

Creditanstalt AG, Vienna, and assumed at fi rst the position

Manager of the Division for Corporate Customers. Later, he

became the Assistant General Director / the Corporate Custom-

ers Division. In the merged Bank Austria Creditanstalt Czech

Republic, a. s., (1988) he became director of the Corporate

Customers II Division / International Business Division / Loans

Division. In June 1999 he joined Erste Bank Sparkassen (CR),

a. s. and was appointed as a Member of the Board of Directors

and Executive Director. After privatization and acquisition of

Česká spořitelna by Erste Bank and the transfer of Erste Bank

CR into Česká spořitelna in 2000 he was named Director of the

Commercial Centers Section of Česká spořitelna. Since July

2003 he is a member of the bank’s Senior Management Team.

From August 2004 till June 2007 he was appointed Member of

the Board of Directors and a Deputy CEO of Česká spořitelna,

responsible for corporate and commercial banking, mortgages

and real estate fi nance and the municipalities section. Since July

2007 he leads the newly formed Risk Division of the bank.

He is the Chairman of the Supervisory Board of

s Autoleasing, a. s., Leasing Česke spořitelny, a. s., Factoring

Česke spořitelny, a. s., and a Member of the Supervisory

Board of Erste Corporate Finance, a. s.

PETR HLAVÁČEK Born on 19 November 1955Member of the Board of Directors and Deputy CEOReference Address: Olbrachtova 62, Prague 4, CZ

Mr. Petr Hlaváček graduated from the Prague University of

Economics and the University of Toronto. He has been active

in the banking sector since 1984. After nine years of work for

the Canadian Imperial Bank of Commerce, he joined the Czech

National Bank as an advisor to a member of the Banking Board

in 1993. In 1994 he joined Česká spořitelna where he held the

post of Director of the Capital Investment Division. In June 1999

he was appointed as the member of the Board of Directors of

Česká spořitelna responsible for the preparation of privatisation

and investment banking. In 2000 he joined the Senior Manage-

ment Team and became Director of the Transformation Program

‘Naše spořitelna.’ In his capacity as a Board member, he is

responsible for project management and IT area.

Mr. Hlaváček is additionally a member of the bodies of the

following companies: Consulting České spořitelny, a. s. and

Informatika České spořitelny, a. s.

11

Opening Statement by the Chairman of the Board of Directors and CEOBoard of Directors as of 31 December 2007Česká spořitelna’s Supervisory Board as of 31 December, 2007

JIŘÍ ŠKORVAGABorn on 26 April 1963Member of the Board of Directors and Deputy CEOReference Address: Olbrachtova 62, Prague 4, CZ

Mr. Jiří Škorvaga is a graduate from the Institute of Chemi-

cal Technology in Prague and from the post-gradual studies

at Czechoslovak Academy of Sciences. He joined Česká

spořitelna Financial Group in 1994, as a project manager. In

1998 he took over the position of Card Center Head and in

1999 he was appointed as a Head Manager of retail banking.

Since 2000 he was responsible for business management of

retail business and was a member of Senior Management

Team. In November 2006 Mr. Škorvaga became a member of

the Board of Directors and a Deputy CEO of Česká spořitelna.

He is responsible for retail banking.

Mr. Škorvaga is a member of the Supervisory Board of

Stavební spořitelna České spořitelny, a. s. and Investiční

společnost České spořitelny, a. s and brokerjet České

spořitelny, a. s. and he is a member of the Managing Board of

Prague Spring, o. p. s.

PAVEL KYSILKABorn 5 September 1958Member of the Board of Directors and Deputy CEOReference Address: Olbrachtova 62, Prague 4, CZ

Mr. Kysilka is a graduate of Faculty of Economics of the

University of Economics in Prague; in 1986 he passed internal

postgraduate research there. In 1986–1990 he worked at the

Institute of Economics of the Czechoslovak Academy of

Sciences.

In 1990–1991 Mr. Kysilka worked in the Ministry for Eco-

nomic Policy as the Chief economic advisor to the Minister for

economic policy. In the 1990s he held various positions up to

the post of Executive Governor in the Czech National Bank,

where he also managed the splitting of the Czechoslovak cur-

rency in 1993. At the same time in 1994–1997 he acted as an

expert of International Monetary Fund and he participated in

implementation of national currencies in several East European

countries. In the 90’s he was President of Česká ekonomická

společnost. Before joining Česká spořitelna Mr. Kysilka

worked in Erste Bank Sparkassen (CR) in Prague as Executive

Director responsible for IT, Organization, Human Resources,

and Services. He started to work for Česká spořitelna in 2000

as Chief Economist and Member of the Senior Management

Team. On 5 October 2004, the Supervisory Board of Česká

spořitelna appointed him a Member of the Board of Directors.

Mr. Kysilka is responsible for payment systems, fi nancial

market analyses, security, EU Offi ce and corporate cash

management and pooling. Among others he is member of the

Scientifi c Board and the Managing Board of University of

Economics in Prague.

12

Česká spořitelna’s Supervisory Board as of 31 December, 2007ANDREAS TREICHLBorn on 16 June 1952Chairman of the Supervisory BoardReference Address: Am Graben 21, Vienna, Austria

Mr. Andreas Treichl studied economic sciences at Vienna

University in 1971–1975. After completing a training program

in New York, he began his career at Chase Manhattan Bank in

1977. In 1983 he began to work at Die Erste for the fi rst time.

In 1986 he accepted a General Manager position with Chase

Manhattan Bank Vienna. In 1994 Mr Treichl was appointed

to the Management Board of Die Erste. In July 1997, he was

appointed as CEO.

He became a member of the Supervisory Board of Česká

spořitelna at the Extraordinary General Meeting in June 2000;

subsequently he was elected its Chairman. The General Meet-

ing in April 2006 re-elected Mr. Treichl in his function.

Mr. Treichl is additionally a member of the bodies of the fol-

lowing companies: Erste Bank der österreichischen Sparkas-

sen AG, Banca Comerciala Romana SA, Donau Versicherung

AG, Sparkassen Versicherung AG, MAK – Österreischisches

Museum für Angewandte Kunst, Die Erste oesterreischische

Spar-Casse Privatstiftung, Österrichischen Sparkassenver-

band, Felima Privatstiftung, Ferdima Privatstiftung, Dritte

Wiener Vereins-Sparkasse AG, s Haftungs – und Kundenab-

sicherungs GmbH.

CHRISTIAN CORETH, Born on 31 March 1946Member of the Supervisory BoardReference Address: Am Graben 21, Vienna, Austria

Mr Coreth graduated from the University of Vienna in 1972

with a Law Degree. In the period from 1972 to 1982, he

worked for Creditanstalt-Bankverein, Vienna. From the

Deputy Head of the International Loan Department, where

he started in 1982, he moved to New York to European

American Bank (EAB) as Senior Vice President. In 1985, Mr

Coreth returned to Creditanstalt. Since 1998, Mr Coreth has

worked as Head of the International Division of Erste Bank

der oesterreichischen Sparkassen AG in Vienna. In July 2004

he was appointed to the Managing Board of Erste Bank der

österreichischen Sparkassen AG with responsibility for Group

Risk Management.

He was elected a member of Česká spořitelna’s Supervisory

Board on 22 May 2002.

Mr. Coreth resigned upon his function as of 7 February 2007.

MAXIMILIAN HARDEGGBorn on 26 February 1966Member of the Supervisory BoardReference Address: Am Graben 21, Vienna, Austria

Mr. Hardegg graduated from Agricultural Sciences in

Weihenstephan, Germany. In the period 1991–1993, he

worked at AWT Trade and Finance Corp, which is part of

the Creditanstalt Group. He also worked as an advisor to the

Czech Ministry of Agriculture in respect of the privatisation of

agriculture.

Since 1993, he has been engaged in agriculture management.

He has participated in the Phare, Sapard and Leader+ titles

projects, which are designed to support the cooperation

among agricultural systems within the EU. He is also

a member of lobbyist groups in Austria and the EU, which

are focused on supporting sustainable development in land

use and agriculture. He was elected a member of Česká

spořitelna’s Supervisory Board on 22 May 2002 and re-

elected in April 2005.

Mr. Hardegg is a member of the Supervisory Board of DIE

ERSTE österreichische Spar-Casse Privatstiftung, Sparkassen

Pruefungsverband.

MONIKA HOUŠTECKÁBorn on 6 December 1963Member of the Supervisory BoardReference Address: Budějovická 1912, Prague 4, CZ

Mrs. Houštecká graduated from the Economic University,

Faculty of Domestic Trade. After completion of her studies,

she worked in the area of trade and in 1994 she started to work

in Česká spořitelna. Since 1997 Mrs. Houštecká is working

in the HQ in the area of Financing of Foreign Trade. As of

13

Board of Directors as of 31 December 2007Česká spořitelna’s Supervisory Board as of 31 December, 2007Macroeconomic Development of the Czech Republic in 2007

August 2000 Mrs. Houštecká was appointed into the function

of Director of Trade Finance Department.

With effect from 28 November 2003 Mrs Houštecká has been

elected by the ČS employees into the function of a Supervisory

Board Member.

The term of offi ce of Mrs. Houštecká expired as of 28 Febru-

ary 2007.

HERBERT JURANEKBorn on 13 November 1966Member of the Supervisory BoardReference Address: Am Graben 21, Vienna, Austria

Mr. Juranek graduated from the Commercial College in Austria

– Bruck/Leitha. He began his career in Girozentrale der

österreichischen Sparkassen in the area of securities. During

years 1996–1998 in Reuters Ges. m.b.H., he lead all sales and

risk management activities of Reuters Austria. Since 1999 he

performed various functions in Erste Bank der österreichischen

Sparkassen AG – mainly leading operations activities with

securities. As the CEO of “ecetra Central European e-Finance”

and “ecetra Internet Services AG” he took overall responsibil-

ity for the online broker and internet bank of Erste Bank

Group. In the meantime, Mr. Juranek as the General Manager

Group IT is in charge of all IT, project management and bank-

organization related activities within Erste Bank Group with

a direct reporting hierarchy in Austrian and a matrix structure

on a Group level.

Mr. Juranek was elected by the General Meeting into the func-

tion of a Supervisory Board Member as of 29 April 2005.

Additionally he is a member of the bodies of the following

companies: Slovenská sporiteľna, a. s. s IT Solutions AT

Spardat G.m.b.H., IT Austria Ges.m.b.H., ecetra Central

European e-Finance, ecetra Internet Services AG , Dezentrale

IT – Infrastruktur Services GmbH; Banca Comerciala Romana

SA; s IT Solutions SK, spol. s r.o., IT Services SK, spol. s r.o.,

Erste Bank der örsterreichischen Sparkassen AG.

MONIKA LAUŠMANOVÁBorn on 30 October 1962Member of the Supervisory BoardReference Address: Na Perštýně 1, Prague 1, CZ

Mrs. Laušmanová graduated from the Faculty of Mathematics

and Physics. Her carrier started on the Faculty of Matheamtics

where she worked as an assistant in the area of fi nance and

insurance mathematics.

In 1997 she worked as a risk manager and analyst in Expandia

Finance. In 1998 she joined Erste Bank (CR) in the position

of Head of Risk Management. Since the merger of Česká

spořitelna and Erste Bank Mrs. Laušmanová is responsible

for the Central Risk Management in ČS. Mrs. Laušmanová

is a member of Czech Banking Association, she is Head of

Commission for the Bank regulation.

As of 12 August 2005 she was elected by the ČS employees as

a Member of the Supervisory Board of Česká spořitelna, a. s.

REINHARD ORTNERBorn on 6 January 1949Vice Chairman of the Supervisory BoardReference Address: Am Graben 21, Vienna, Austria

Mr Reinhard Ortner completed studies of social and economic

sciences at Vienna University in 1971. In 1971, he joined Erste

oesterreichische Spar-Casse, where he has held various posi-

tions in the accounting and controlling functions since 1973.

He has been a member of the Board of Directors of Erste Bank

der österreichischen Sparkassen AG since 1984.

He was elected as a member of the Supervisory Board of

Česká spořitelna at the Extraordinary General Meeting that

was held on 27 June 2000; the General Meeting in 2006

re-elected Mr. Ortner into the function of a Member of the

Supervisory Board.

Mr. Ortner resigned upon his function as of 26 April 2007.

14

MAREK POSPĚCHBorn on 1 October 1967Member of the Supervisory BoardReference Address: Nám. Dr. Beneše 6, Ostrava, CZ

Following graduation from a secondary professional school of

construction in Valašské Meziříčí, Mr. Pospěch worked with

Tesla Rožnov in the control and quality assurance department

for six years. In 1992, he joined Česká spořitelna’s branch

offi ce in Ostrava where he worked in the operations security

department. From 1995, he worked in the general administra-

tion department and is currently a head offi ce manager of the

property management department. With effect from 1994, he

has sat on the Organisation-wide Committee of the CS Labour

Union. Since 2006 he is a member of Czech Institute of Direc-

tors within certifi cation of Corporate Governance Program.

With effect from 1 April 2002, he has been elected by the

employees of Česká spořitelna as a member of the Supervisory

Board, and re-elected in July 2005.

BERNHARD SPALTBorn on 25 June 1968 Member of the Supervisory BoardReference Address: Am Graben 21, Vienna, Austria

Mr. Spalt graduated from the Law Faculty of Vienna University

where he specialised in European law.

During his studies in 1991, he joined DIE ERSTE österreichische

Spar-Casse Bank AG, where he started to work in the Legal

Department. From September 1994 to June 1997, he performed

various positions in the Work Out Department. Following the sale

of Erste Bank Sparkassen (CR), a. s. to Česká spořitelna, a. s., Mr.

Spalt took over the responsibility of the Work Out Department

in Česká spořitelna, a. s. In June 2002, he returned to Erste Bank,

Vienna where he was responsible for Strategic Risk Management

until Oct. 2006. In Nov. 2006 he was appointed to the Managing

Board of Erste Bank der österreichischen Sparkassen AG with

responsibility for Group Risk Management.

Mr. Spalt was elected into the function of a Supervisory Board

member as of 15 May 2003 and re-elected in 2006 by the

General Meeting.

Mr. Spalt is a member of the bodies of the following com-

panies: Erste Bank Hungary Nyrt., Erste Reinsurance S. A.,

Open, Joint Stock Company Erste Bank, Erste Bank der

oesterreichischen Sparkassen AG, Erste Bank Ukraine, Banca

Commerciala Romana SA, ecetra Central European e-Finance

AG, ecetra Internet Services AG, Slovenská sporiteľna, a. s.,

s Haftungs- und Kundenabsicherungs GmbH.

JITKA ŠROTÝŘOVÁBorn on 18 November 1948Member of the Supervisory BoardReference Address: Olbrachtova 62, Prague 4, CZ

Mrs. Šrotýrová graduated from the secondary school of

general education in Prague. In 1967, she joined Tesla Prague

as a specialist. From 1970 to 1984 she worked as a supply

manager for Tesla Eltos and the Project and Engineering

Organisation. She has worked with Česká spořitelna since

1985, largely as a senior professional offi cial of the recrea-

tion department where she is in charge of the operation of

recreation facilities. Since 1986, she has been a member of the

Organisation-wide Committee of the CS Labour Union. She is

also chairwoman of the Sports Committee at Česká spořitelna.

With effect from 1 April 2002, she has been elected by the

employees of Česká spořitelna as a member of the Supervisory

Board and re-elected in 2005.

MANFRED WIMMERBorn on 31 January 1956Member of the Supervisory BoardReference Address: Am Graben 21, Vienna, Austria

Mr. Wimmer graduated from the Law Faculty of the University

of Innsbruck where he was awarded the Doctor of Law degree.

From 1978 to 1982, he worked as an academic assistant in

private law. From 1982 to 1998, he worked in the International

Division of Creditanstalt. In 1998, he joined the International

Division of Erste Bank der österreichischen Sparkassen AG.

Since February 2002 Mr. Wimmer was Head of the Strategic

Group Development Division of Erste Bank. Since August

2005 Mr. Wimmer was Executive Director Group Architecture

and Group Program Mng.

15

Board of Directors as of 31 December 2007Česká spořitelna’s Supervisory Board as of 31 December, 2007Macroeconomic Development of the Czech Republic in 2007

He has been a member of the Supervisory Board of Česká

spořitelna since 27 June 2000; the General Meeting in 2006

re-elected Mr. Wimmer into the function of a Member of the

Supervisory Board.

Mr. Wimmer resigned upon his function as of 26 April 2007.

HEINZ KESSLERBorn on 19 August 1938Member of the Supervisory BoardReference Address: Am Graben 21, Vienna, Austria

Immediately after fi nishing his studies, in 1964 Dr. Kessler

became employed by Nettingsdorfer Papierfabrik AG,

became a member of the Board from 1974 and Chairman of

the Board from 1982.

Mr. Kessler was elected by the General Meeting into the func-

tion of Supervisory Board Member on April 2007.

Mr. Kessler is member of the bodies in following companies:

Erste Bank der österreichischen Sparkassen AG, Die Erste

oesterreichische Spar-Casse Privatstifung AG, Allegemeine

Sparkasse Oberösterreich Bankaktiengesellschaft, AVS Beteil-

ligungsgesellschaft m.b.H, Tiroler Sparkasse Bankaktienge,

Dritte Wiener Vereins-Sparcasse AG.

JOHANNES KINSKYBorn on 7 August 1964Vice Chairman of the Supervisory BoardReference Address: Am Graben 21, Vienna, Austria

Mr. Kinsky studied on the Institut d´Etudes politiques de

Paris, where he graduated in 1988 in fi nance, law, history and

political science. His career started at Deutsche bank, where

he performed various positions as credit analyst, Head of Debt

Capital Market and fi nally as a country manager for the Czech

Republic, Slovakia and Croatia. Since 1999 Mr. Kinsky was

Managing Director and Head of CEE at JP Morgan. In July

2007 Mr. Kinsky became a member of the Erste Bank Group

Executive Board.

Mr. Kinsky was elected by the General Meeting into the

function of a Supervisory Board Member in April 2007 and

Vice Chairman of the Supervisory Board in May 2007.

Mr. Kinsky is member of the bodies in following companies:

Österreichische Kontrollbank Aktiengesellschaft, IMMORENT

Aktiengesellschaft, Erste Bank AD Novi Sad, Erste

Steiermärkische bank d.d. Rijeka, Erste Bank der oesterreich-

ischen Sparkassen AG, Erste Corporate Finance GmbH, Dritte

Wiener Vereins-Sparkasse AG, Erste Securities Polska S. A.

PÉTER KISBENEDEKBorn on 12 September 1964Member of the Supervisory BoardReference Address: Am Graben 21, Vienna, Austria

Mr. Kisbenedek graduated from University of Economics

in Budapest in 1988 with specialization in Foreign Trade

and Marketing Line. In 1988 he began to work for Sancella

Hungary as a Product Manager and further as Sales Director.

From 1991 until 1995 he performed various managing posi-

tions in Philip Morris. In 1995 Mr. Kisbenedek was appointed

into the function of Deputy CEO of Sales and Marketing in

ÁB – AEGON General Insurance. Within the Company he

was appointed as a Head of Retail Division and Deputy CEO

of Non-life Insurance. Since 2000 he has been working in the

Erste Bank Group, till 31. 12. 2006 he was CEO of Erste Bank

Hungary with responsibilities especially for Strategic Manage-

ment, Human resources, Legal, Marketing. Since 1st July

2007 is Mr. Kisbenedek a Chief Financial Offi cer, CPO (Chief

Performance Offi cer) and Member of the Board of Directors of

the Erste Bank Group.

Mr. Kisbenédek was elected by the General Meeting into the

function of Supervisory Board Member in April 2007.

Mr. Kisbenédek is member of the bodies in following compa-

nies: Open Joint-Stock Company Erste Bank, Banca Comer-

ciala Romana SA, Erste Steiermärkische Bank d.d. Rijeka,

PayLife Bank gmbH, Slovenská sporiteľna, a. s. Sparkassen

Versicherung AG, Erste Bank AD Novi Sad, Erste Bank der

oesterreichsichen Sparkassen AG, Dritte Wiener Vereins-Spar-

kasse AG, JSC Erste Bank Ukraine.

16

ANDREAS KLINGEN Born on 18 August 1964Member of the Supervisory BoardReference Address: Am Graben 21, Vienna, Austria

Mr. Klingen is a graduate of Technische Universität in Berlin

with specialization in physics and philosophy and a graduate

of Rotterdam School of Management. His professional

career started as a researcher in Festkörper – Laser-Institut in

Germany. During years 1993–1998 he worked as an analyst

and associate in Lazard Freres, afterwards until 2005 as senior

Associate and senior Vice President of JP Morgan in London.

He joined Erste Bank der österreichischen Sparkassen AG in

2005 as a General manager for Strategic Group Development.

Mr. Klingen was elected by the General Meeting into the

function of Supervisory Board Member in April 2007.

Mr. Klingen is member of the bodies in following compa-

nies: Open Joint Stock Company Erste Bank, Erste Bank

Hungary Nyrt.

JOLANA DYKOVÁBorn on 23 July 1966Member of the Supervisory BoardReference Address: Malé nám. 219, Rokycany, CZ

Mrs. Dyková is a graduate from the secondary technical

college for machinery in Kladno and completed a term at the

Czech Technical University in Prague. She started her profes-

sional career in 1985 at Czech Radio where she worked as an

assistant to the editor-in-chief. Then she held the position of

a deputy manager in the company Západočeské kamenolomy

(West Czech Stone Quarries) for two years. In 1991 she joined

Česká spořitelna as a bank offi cer, later she became the head

of the branch in Zbiroh. Since 2002 she has been a manager

at the advisory branch in Rokycany and since October 2007

a manager of microregion Rokycany.

Mrs. Dyková was elected to the Supervisory Board by ČS

employees as of November 2007.

Members of Managing and Supervisory Boards declares not

to be aware of possible confl ict of business, private and other

interests or duties.

17

Česká spořitelna’s Supervisory Board as of 31 December, 2007Macroeconomic Development of the Czech Republic in 2007Report on Performance and Business Activities

Macroeconomic Development of the Czech Republic in 2007Economy Above 6%, Slowdown in 2008 Due to ReformsThe Czech economy grew by an estimated 6.6 percent in 2007,

which was about the same rate as in 2006 (6.4 percent). The key

driver was the increase in domestic consumption, which, based

on the Bank’s estimates, grew by approximately 6 percent in

real terms due to both the growth in real wages and employment

(the average unemployment rate in 2007 was 6.6 percent) and

low interest rates. Other components of the gross domestic

product (GDP) developed as in 2006 – export growth was in

double digits (15 percent) due to massive demand from the

European Union; however, faster consumption pulled imports

up as well (13.1 percent), which made the contribution of net

exports to GDP positive, though not signifi cant. With a surplus

of CZK 86 billion, the fi nal trade balance was the fundamental

factor behind the strengthened Czech crown. Compared to

the Eurozone (where the GDP growth rate was 2.6 percent),

the Czech Republic keeps growing at a pace that is allowing

the Czech Republic to gradually catch up with the economic

standards of the Eurozone (in terms of PPP per capita, the Czech

economy has reached 68 percent of the Eurozone’s GDP).

In 2008, the Bank expects the economy to slow down to 4.3 per-

cent, mainly because of the government reforms that contributed

to the growth of infl ation to 7.5 percent in January 2008, which

will limit the growth of real wages and consumption this year.

The available net household income will be further decreased

by cuts in the government’s social spending. In the short-term,

tax changes and cuts in social spending are bad news for most

individuals and fi rms. Nevertheless, this effect is expected

to disappear in 2009 and be replaced by a moderate growth

stimulus (shift in taxation to indirect taxes, lower corporate taxes

etc.). The Bank forecasts growth above 5 percent in 2009.

Infl ation – The Top Story The average rate of infl ation accelerated to 2.9 percent in 2007.

Early 2007 faced a threat of demand-driven infl ation caused by

the rapid growth of consumption, which forced the Czech Na-

tional Bank (ČNB) to take further action to tighten the monetary

policy (rates were fi nally raised by 1 percentage point in 2007).

In the second half of 2007, the strengthening of the Czech crown

helped reduce infl ation; however, cost shocks (food and energy

prices) towards the end of 2007 coupled with the administrative

measures in January 2008 sent infl ation soaring to a 10-year

high in January 2008 (7.5 percent). The Bank expects infl ation

to stay high in 2008 (6.1 percent on average) and fall only at

the beginning of 2009. The infl ation structure will continue to

threaten infl ation expectations.

The Czech Crown’s Rollercoaster RideThe Czech crown gained 2 percent against the euro in 2007.

In comparison to 2006, the trade balance surplus doubled and

was the fundamental force behind the strengthened crown (the

infl ow of foreign direct investments roughly covered the outfl ow

of dividends). The development of the Czech crown’s exchange

rate was heavily infl uenced by the situation in the USA where

the subprime mortgage crisis erupted in mid-2007, which had

implications for other fi nancial market segments (loans, money

market etc.). While in the fi rst half of 2007 the Czech crown

weakened consistently, most likely due to the build-up of carry

trade positions (taking loans in low interest currencies and saving

in currencies bearing higher interest rates), aversion to these posi-

tions increased with the outbreak of the crisis, which led to their

termination and strengthened leaps in the Czech crown. In autumn

2007, the problems on the other side of the Atlantic escalated and

the Czech crown, riding on its reputation as a quasi safe-haven

currency and having solid macro and rising interest rates, became

an attractive substitute for the US dollar and in several leaps

strengthened to as high as CZK 25/EUR 1. The crown diverted

from its long-term trend and its fundamentally justifi able level by

approximately 5 percent. In line with a more favourable outlook

for the US economy and a higher outfl ow of dividends, the Bank

expects the Czech crown to weaken to 26.8 crowns to the euro

towards the middle of 2008 and then strengthen towards the end

of 2008. The average exchange rate is estimated to be 26.4 against

the euro and 18.6 against the US dollar.

The CNB Normalises Rates, 25 Basis Points Are Expected This Year The Czech National Bank responded to the expected rise in

infl ation and fi scal expansion (increase in social spending) by

raising the rates four times in 2007 from 2.5 to 3.5 percent.

Higher headline infl ation and the public’s perception thereof,

e.g. higher food prices, will constitute a threat to infl ation ex-

pectations and to achieving the target infl ation rate (2 percent

by 2010). The expected weakening of the Czech crown will

eliminate one of the strongest obstacles to increasing interest

rates. With one more hike expected by the Bank in 2008, the

rates are thus estimated to be 4 percent at the end of 2008.

18

Report on Performance and Business ActivitiesCONSOLIDATED RESULTS OF OPERATIONS(INTERNATIONAL FINANCIAL REPORTING STANDARDS)

The Česká spořitelna Financial Group reported another very successful year, all of the important indicators of good performance have improved. The record results refl ect the

continuous expansion of lending transactions, growing deposits

and assets under management, increased volumes and numbers

of transactions, professional conduct of staff, growing interest

and non-interest income, effi cient cost management, new

innovative products, increased quality of provided services and

client satisfaction. Clients voted Česká spořitelna the Most Credible Bank of the Year for the fourth time in a row.

PROFIT AND LOSS ACCOUNT

For the year ended 31 December 2007, Česká spořitelna reported, under International Financial Reporting Standards

(IFRS), a consolidated net profi t, net of minority interest,

of CZK 12,148 million. Compared to 2006 when the net

profi t amounted to CZK 10,385 million the net profi t grew by

1,763 million, i. e. 17 percent. The key indicator of return on equity (ROE) improved to 23.8 percent due to the increase in net profi t. In 2006, ROE was 23 percent. Return

on assets (ROA) remained on the same level, 1.5 percent, due

to the massive growth in the asset volume. Profi t before taxes

and minority interest (gross profi t) increased by 11 percent to

CZK 15,589 million year on year.

The Bank achieved another signifi cant success in reaching high

effectiveness – the key cost/income ratio was successfully decreased to 50 percent thanks to the considerable growth in operating income, which is a year-on-year improvement of

33 basis points. Operating profi t, determined as the difference

between operating income and expenses, reported marked growth of CZK 3,220 million to CZK 18,375 million, which is

a 21 percent increase.

Total operating income, comprising net interest income,

net fee and commission income, net profi t on fi nancial

operations and net insurance income, rose by 13 percent to CZK 36,724 million. Non-interest income accounts for

33 percent of the total operating income, which is a moderate

decrease. Operating expenses, comprising staff costs, other

administrative expenses and depreciation/amortisation charges

on property and equipme nt and intangible assets, increased by 6 percent to CZK 18,349 million.

The signifi cant operating income was predominantly driven

by net interest income. Despite a revival in interest rates in

the latter half of 2007, the interest rates in the Czech Republic

were below the level of interest rates in the Eurozone (the

two-week repo rate announced by the Czech National Bank in

2007 increased gradually in June, July and August by 25 basis

points from 2.5 percent to 3.5 percent at the end of November).

Operating profi t Net profi t

Net profi t and operating profi t (CZK mil)

16,000

8,000

0

4,000

12,000

20,000

11,334

8,1379 ,134

12,439

10,195

7,615

10,385

15,155

2003 2004 2005 2006 2007

12,148

18,375

2003 2004 2005 2006 2007

Cost/Income (%)

80

40

0

20

60 58.459.7

56.953.3 50.0

19

Macroeconomic Development of the Czech Republic in 2007Report on Performance and Business ActivitiesStrategic Plans for the Year 2008

Net interest income for the year ended 31 December 2007 amounted to CZK 24,727 million, which represents

a signifi cant year-on-year increase of 17 percent.

The successful result was primarily attributable to a mas-sive increase in lending to individuals and corporate clients

of 27 percent (CZK 89.3 billion) giving rise to a notable

26-percent increase in interest income on client receivables that

represent 65 percent of interest income. The fastest growing

component of interest income was income from rental of real

estate owned by real estate funds that increased by 47 percent.

The interest rate growth supported growth in income from

inter-bank loans and debt securities in spite of the absolute

year-on-year decrease in the volume of their portfolio. In total, interest income grew by 21 percent to CZK 34,601 million.

The growth of interest expenses refl ected the increased

volume of passive products as well as growing interest rates.

Principally, interest expenses on client deposits, amounts owed

to banks and issued bonds, including the fair value of hedging

derivatives relating to certain issues of mortgage bonds and

subordinated debt increased. The total interest expenses represent CZK 9,874 million, which is a 32 percent

year-on-year increase.

The net interest margin in relation to interest-earning assets

improved by 14 basis points to 3.72 percent.

Net fee and commission income increased by 7 percent year on

year, reaching CZK 9,639 million. The achieved year-on-year growth in net fee and commission income was primarily driven by the expansion of loan transactions, and an increase

in the volume and number of fi nancial transactions effected by

the Group’s clients.

The favourable performance primarily resulted from the fee from lending activities which increased by 23 percent due to the

continuing expansion of lending transactions, e.g. the total number

of mortgage loans grew by 25 percent. Securities transaction fees

and commissions increased by 14 percent in connection with

trading with mutual funds administered primarily by Investiční

společnost ČS, the increase of brokerage services provided by the

parent bank and Brokerjet ČS, and the increase in the volume of

assets under management. Income from transaction fees, which are the largest income component, rose by 4 percent due to the

increase in the volume and number of payment transactions (e. g.

the volume of card transactions grew by 20 percent, the number of

withdrawals through ATMs rose by 5 percent, and the number of

giro account transactions grew by 5 percent).

The proportion of net income from fees and commissions to

total operating income has been gradually decreasing, from

31 percent in 2004 to 26 percent in 2007.

The net profi t on fi nancial operations for the year ended

31 December 2007 totalled CZK 1,709 million, a moderate

decrease of 2 percent year on year. The net profi t on fi nancial operations was specifi cally driven by income on foreign currency transactions that reported a 35-percent year-on-year

increase attributable to the growing importance of structured

products with a currency component and the continuous growth

in trading for corporate clients. The growing interest rates had

a markedly adverse effect on securities held for trading, predomi-

nantly bonds, but increased interest derivative income. Income

from the revaluation of equity derivatives in the trading book

decreased year-on-year due to turbulent market developments.

Net insurance income represented CZK 649 million of profi t,

an increase of 23 percent compared to the previous period.

18,719

8,3848,997

21,206

2003 2004 2005 2006 2007

Net interest income Net fee and commission income

Other non-interest operating income

Net interest income and other operating income (CZK mil)

17,416

8,2387,915

15,87416,000

8,000

0

4,000

12,000

20,000

9,639

24,727

1,7312,268

1,5631,479

2,358

24,000

20

Structure of operating expenses (CZK mil)

3,272 (18%)Depreciation and amortisation of tangible and intangible assets

6,654 (36%)Administrative expenses

8,423 (46%)Staff costs

Structure of operating income (CZK mil)

649 (2%)Net insurance income

1,709 (5%)Net profi t on fi nancial operations

9,639 (26%)Net fee and commission income

24,727 (67%)Net interest income

The increased volume of net insurance income was attribut-able primarily to the growth of received insurance premiums due to the successful performance of Pojišťovna ČS in 2007.

The general administrative expenses (operating expenses)

grew by 6 percent year-on-year in 2007 but compared to the half-year results, the growth pace of operating expenses was reduced due to the measures aimed at reducing expenses

incurred in the latter half of 2007. The total amount of general

administrative costs was CZK 18,349 million.

Staff costs of CZK 8,423 million represented nearly a half

of the total general administrative expenses. In comparison with 2006, staff costs rose by 9 percent owing to the growth in wages arising from, among other things, the extension of

working hours and the increase in the staff bonus fund relating

to excellent performance, including compensation linked to the

Erste Bank Group’s results.

Other administrative expenses, the second largest compo-nent of operating expenses, grew by 7 percent to CZK 6,654

million. The year-on-year growth is attributable namely to the

increase in data processing expenses of 19 percent relating to the

outsourcing of IT services. Offi ce space costs and advertising

and marketing expenses also grew as a result of the continuous

business expansion of the Bank, new subsidiaries and real estate

funds. Trading transaction costs grew in line with the ongoing

implementation of the Group’s central procurement focused

on using synergies within the entire Erste Bank Group. Costs

associated with advisory and legal services decreased.

The largest item within administrative expenses is data

processing expenses representing 30 percent. Other signifi cant

expenses relate to offi ce space (21 percent), trading transac-

tions (18 percent) and advertising and marketing (14 percent).

The volume of depreciation/amortisation of tangible and intangible assets, primarily hardware, was reduced by

2 percent to CZK 3,272 million due to the outsourcing of

IT services. The depreciation/amortisation structure slightly

changed as amortisation of intangible assets grew by 6 percent

to CZK 1,736 million due to the investment in information

systems (software). Depreciation of tangible assets fell by

10 percent to CZK 1,536 million.

The net charge for provisions for credit risks reported

a negative balance of CZK (2,211) million which represents

nearly a one-third increase compared to the previous period.

Of the total net charge for provisions for the year ended

31 December 2007, the parent bank represents 96 percent.

The principle reason for the year-on-year increase in the net charge was loan expansion, resulting in the increase in provisioning, principally for receivables – consumer loans.

The comparison with the previous period is partially distorted

by the one-off release of provisions in 2006 due to a change

in methodology.

The net balance of other operating income and expenses of

CZK (575) million at the end of 2007 markedly decreased

compared to 2006. The key reasons for the decrease include

the signifi cantly lower balance of the sale and revaluation of real estate owned by real estate funds and the lower income

21

Macroeconomic Development of the Czech Republic in 2007Report on Performance and Business ActivitiesStrategic Plans for the Year 2008

2003 2004 2005 2006 2007

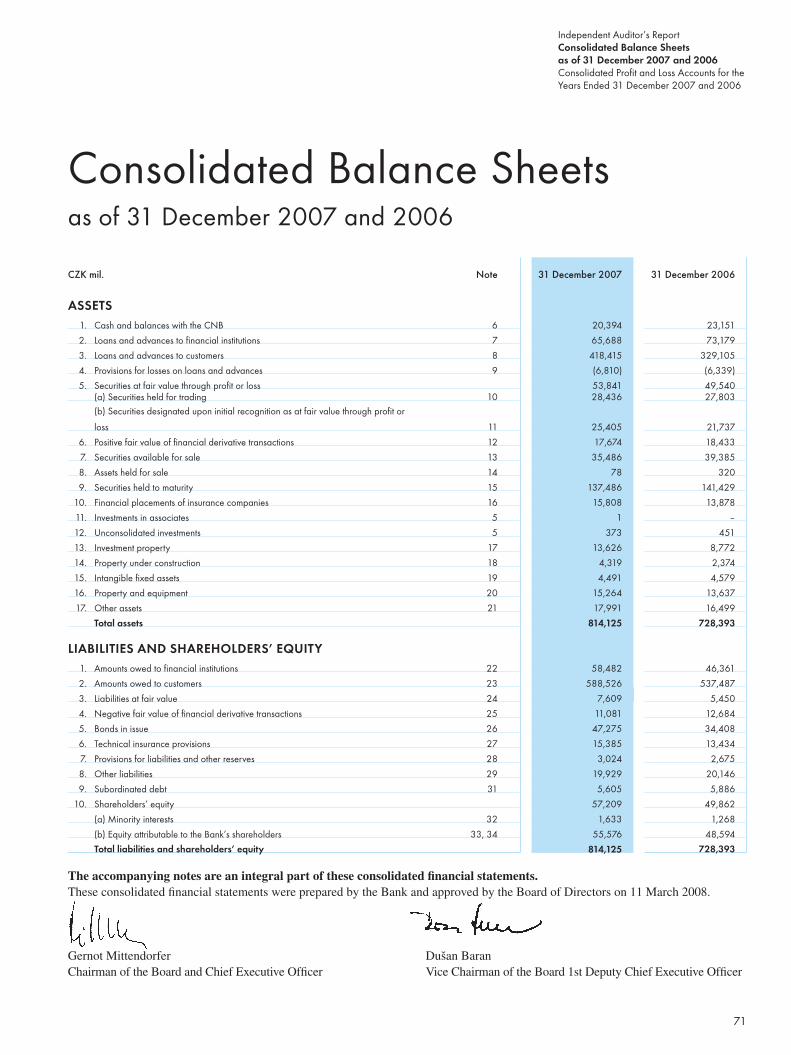

Total assets (CZK billion)

800

400

0

200

600 581.8555.4

654.1

728.4

814.1

from the sale and revaluation of securities available for sale and at-fair-value-through-profi t-or-loss securities due

to the adverse development in fi nancial markets in the latter

half of 2007. The contribution to the Deposit Insurance Fund

increased by 11 percent due to the growth of the insured client

deposits volume. The elimination of profi t allocated to clients

of Penzijní fond ČS also increased.

The tax liability of the Česká spořitelna Financial Group for the year ended 31 December 2007 decreased by 8 percent to CZK 3,213 million, which represents an effective tax

rate of 20.6 percent. This amount comprises the current year

tax charge of CZK 3,908 million and the aggregate impact

of movements in deferred taxation resulting primarily from

the change in the income tax rate in the aggregate amount of

CZK 695 million.

BALANCE SHEET

Liabilities Client (primary) deposits have traditionally formed the key resource of Česká spořitelna’s funding in respect of active

trading, which makes Česká spořitelna substantially independ-

ent of inter-bank funding.

Client deposits amounted to CZK 588.5 billion representing

a year-on-year increase of 9 percent, i. e. CZK 51 billion. Client

deposits accounted for 72 percent of all liabilities. All client segments contributed to the year-on-year increase in deposits. Deposits made by private individuals, which account for

76 percent of all client deposits, increased by 8 percent to CZK 446.1 billion. The largest increase in deposits was noted

in respect of giro accounts, retirement benefi t deposits and term

deposits. By contrast, deposits in savings books suffered a slight

decline. Deposits made by corporate clients rose by 17 percent to CZK 91.3 billion, particularly on current accounts and foreign

currency accounts. Deposits made by the public sector reached CZK 51 billion, which represents an increase of 13 percent. Deposits denominated in foreign currencies represent a stable

4 percent portion of the total client deposit volume.

As of 31 December 2007, the consolidated assets of Česká

spořitelna amounted to CZK 814.1 billion. Compared to 2006, the consolidated assets markedly increased by 12 percent, which, in absolute terms, represents an increase of

CZK 85.7 billion, primarily due to amounts owed to customers

and fi nancial institutions and issued bonds on the liabilities

side of the balance sheet and the increase in customer loans on

the assets side.

The total volume of client funds under the Group’s management (i. e. deposits made by clients and mutual funds

of Investiční společnost ČS and REICO ČS) increased year

on year by 10 percent, totalling CZK 671.5 billion, of which

29 percent is managed by subsidiaries.

2003 2004 2005 2006 2007

Clients deposits (CZK billion)

600

300

0

150

450 444.8428.6

481.6537.5

588.5

22

52.9 (7%)Bonds in issue and subordinated debt

Structure of liabilities (CZK billion)

55.6 (7%)Shareholders’ equity

58.7 (7%)Other liabilities

58.5 (7%)Amounts owed to fi nancial institutions

588.5 (72%)Amounts owed to customers

The balance of amounts owed to fi nancial institutions, comprising loans, term placements and current account balances,

increased year on year by 26 percent (CZK 12.1 billion) and

was CZK 58.5 billion as of 31 December 2007, of which loans

under repo transactions accounted for CZK 12 billion. Only nearly

a half of the year-on-year increase (CZK 5.7 billion) resulted from

Česká spořitelna’s inter-bank market transactions, otherwise it

was due to the increase in funds for business activities of certain

subsidiaries, primarily in leasing (growth of CZK 3.2 billion) and

real estate funds (growth of CZK 3.3 billion).

The total volume of issued bonds increased year on year by

37 percent to CZK 47.3 billion, excluding the issued structured

bonds at fair value. In 2007, Česká spořitelna used tax allow-ances and issued a number of mortgage bonds, especially towards the year’s end. The total volume of mortgage bonds,

representing a stable and long-term source of funding for

increasing mortgage transactions within the balance sheet of the

consolidated group, accounts for CZK 38.6 billion. The volume

of issued bonds and depository bills was CZK 3.7 billion and

CZK 5 billion, respectively.

In the context of dynamic lending growth, Česká spořitelna

issued subordinated bonds to strengthen its capital base in

2005 and 2006. As of 31 December 2007, the subordinated

debt totalled CZK 5.6 billion.

and exchange rate differences), retained earnings and profi t for the

period, grew by 14 percent to CZK 55.6 billion year-on--year, which was primarily attributable to the generated profi t. By

contrast, the balance of equity decreased as a result of the payment

of dividends for 2006 amounting to CZK 4.6 billion.

The individual capital adequacy of Česká spořitelna calculated

in compliance with the Basel II directive was 9.6 percent as of 31 December 2007. The total capital used to calculate the

capital adequacy (Tier 1 and Tier 2 net of deductible items)

was CZK 36.7 billion and the total capital requirements

amounted to CZK 30.7 billion.

Assets Česká spořitelna’s active transactions that generate the pre-

dominant portion of operating income are loans and advances

to customers. In 2007, massive lending growth continued; the total volume of loans and advances to customers grew by

an impressive 27 percent, which accounts for CZK 89.3 billion

in absolute terms, reaching CZK 418.4 billion. Česká spořitelna was successful in boosting the proportion of client loans relative to client deposits by nearly 10 percent

and achieving 71.1 percent. In all active transactions, net loans

and advances to customers account for 51 percent while at the

end of 2003 their proportion represented only 32 percent.

The signifi cant growth in lending transactions was attributable

primarily to mortgage loans and also to construction savings

2003 2004 2005 2006 2007

Proportion of client loans relative to client deposits

80

40

0

20

6053.8

50.1

58.961.2

71.1

100

The balance of shareholders' equity, comprising share capital,

share premium, the statutory reserve fund, the revaluation reserve