crude oil prices global market forces jorge montepeque global director market reports moscow january...

TRANSCRIPT

Crude Oil Prices Global Market Forces

Jorge MontepequeGlobal Director Market Reports

MoscowJanuary 24, 2012

Agenda

1. Global benchmarks – factors influencing price Ongoing issues with the main crude benchmarks – Brent, WTI and Dubai

2. Russian domestic prices – internal and external factors affecting price

International oil prices

• Oil price is a function of marginal supply and demand

• Marginal supply and demand change due to conditions led by geopolitical factors

• Oil prices, however, react to changes in aggregate supply and demand and it is difficult for a single market participant or government to affect global supply and demand

• Disruptions in supply and demand in one region are balanced by market forces creating arbitrage opportunities, which help handle shortages or surpluses through price changes

International oil prices in 2011: a storm of global events

• Prices buffeted by earthquakes, political events, wars, monetary policy

• Oil hits the level over $125.00

• Range bound between $100 and $120 since May 2011

• Nuclear event in Japan affects price of LNG but shale gas development hits US prices

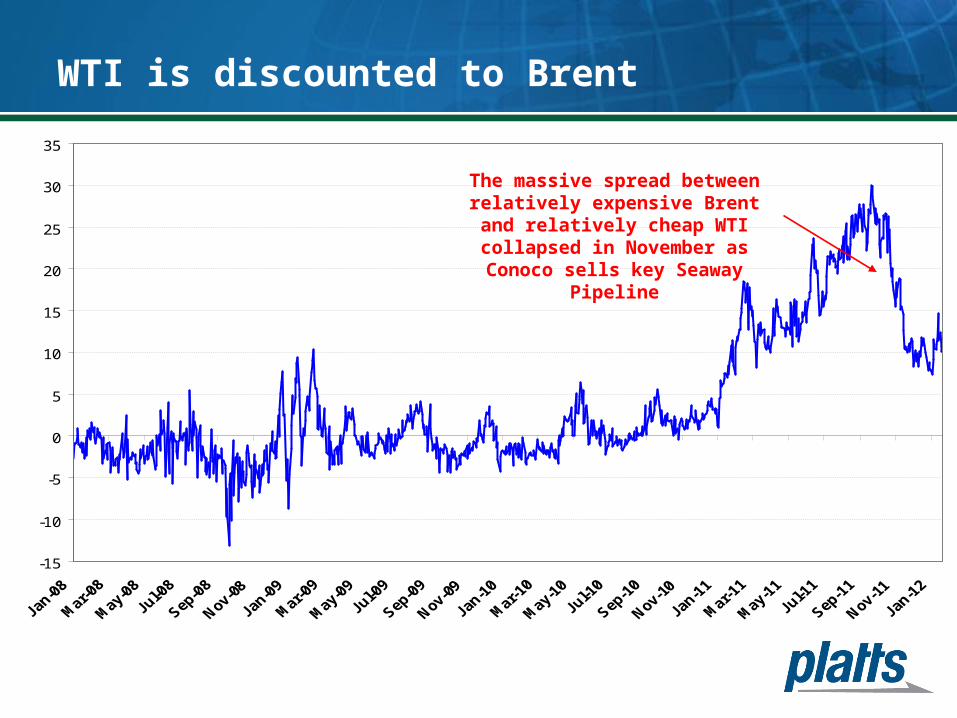

• WTI disconnects from general world prices, but recovers a bit in late 2011 on the decision to reverse the Seaway pipeline

• Trade flows point East, China set to become largest waterborne crude oil importer in a few years

Platts Dated Brent

0

20

40

60

80

100

120

140

160

Oil price collapse on credit crunch

in H2 2008

Political unrest in Middle East and

North Africa led to supply disruptions

Economic instability in Eurozone, slowing down of Chinese economic growth and recovery in the Middle

East and Africa

Brent/Dubai more volatile in 2011

Price Shocks

Relative strength in heavy fuels and relative weakness in light fuels led to robust

sour crude prices

WTI is discounted to Brent

-15

-10

-5

0

5

10

15

20

25

30

35

The massive spread between relatively expensive Brent and

relatively cheap WTI collapsed in November as Conoco sells key

Seaway Pipeline

International market forces affect Russian prices

• Both crude oil and refined products prices across the Russian domestic market are directly related to the international markets

• Any spike in European prices (Northwest Europe and Mediterranean) will result in a bullish Russian market or the inverse

• Authorities and oil market participants calculate domestic prices in a constant comparison with the export alternative

• Moreover, market in different regions balance each other with arbitrage opportunities

• But local market forces may disconnect Russian domestic prices from the international arena

International arbitrage trades balance price globally

High prices in Rotterdam attract more barrels from

Russia

Cheap gasoil prices in Rotterdam result in product moving towards US, Latin

America, WAF

Gasoil FCA Moscow vs Gasoil FOB ARA vs netback

400

500

600

700

800

900

1000

1100

Gasoil netback Moscow refineryvia St Petersburg, $/mt

Gasoil 0.1 FOB ARA barge, $/mt

Gasoil FCA Moscow assessment,$/mt

Urals FIP Surgut – price formation based on a netback

Crude oil trading in Russia

Active trading occurs at the end of the month after 20th

Prices depend on:

- Export duty which is announced once a month around 15, 16th

- Maintenance at refineries

- Expected demand for oil products

- International benchmarks

During these active trading days, Platts assesses crude oil based on the relevant deal information

Crude oil assessment

However, during most of the month, crude oil FIP Surgut is assessed as a netback to dated Brent, in the following way:

Urals FOB Novorossiisk and Primorsk -

Export duty -

pipeline tariffs (Novo-Surgut and Primorsk-Surgut) *

VAT (18%) * USD/Ruble rate +/- Premium or discount = Urals FIP Surgut

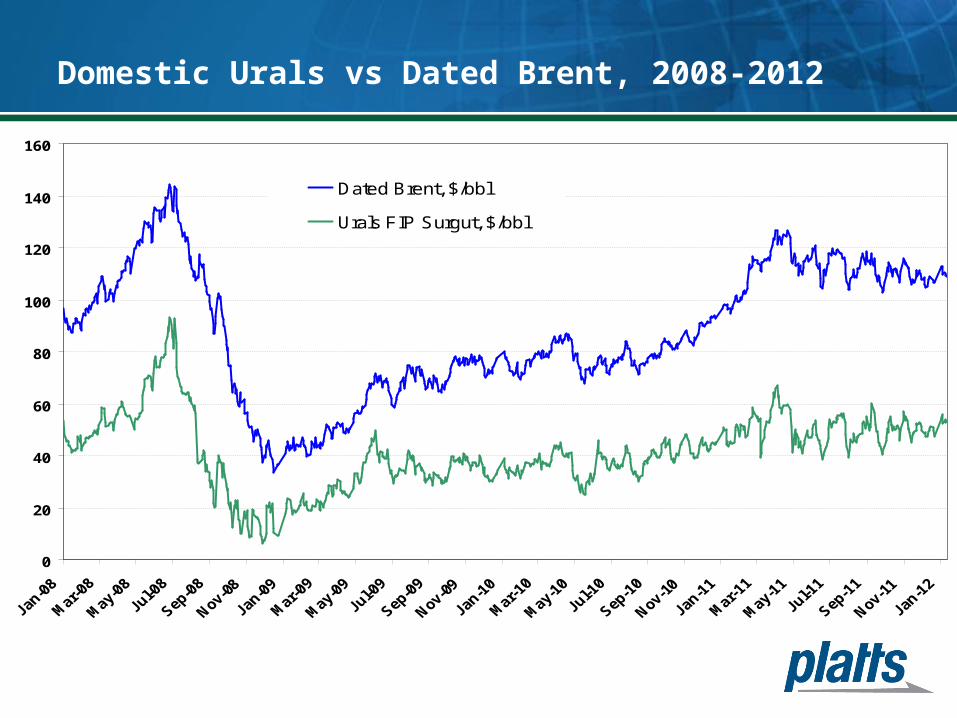

Domestic Urals vs Dated Brent, 2008-2012

0

20

40

60

80

100

120

140

160

Dated Brent, $/bbl

Urals FIP Surgut, $/bbl

Russian events also affect international markets

• The relationship between European and Russian domestic markets works in both ways

• Internal Russian events affecting oil and oil products export supplies have an effect on the European market

• Sept 16, 2011 – Russia bans domestic sales of 0.1 gasoil and moves to 0.05 spec

• Meanwhile, Transnefteprodukt continued pipeline exports of 0.1 gasoil to Europe

• As a result, diesel 10 ppm produced in Russia stays in the country for blending into 0.05 gasoil. This resulted in ULSD 10 ppm export via Primorsk dropping from 500,000 to 100,000 mt in October 2011

• On the other hand, 0.1 gasoil exports gained 15-20% in October 2011

• Refinery maintenance in Europe and Russia as well as building stocks by Rosrezerv ahead of the winter added to the 10 ppm ULSD shortages in Europe

European prices affected by move in Russia towards gasoil 0.05

0

10

20

30

40

50

60

ULSD 10 ppm FOB ARA/Gasoil 0.1 FOB ARA (barge)

Questions?