crown capital corporation · company expanding operations in philippines to meet ... penequity...

TRANSCRIPT

CROWN CAPITAL PARTNERS INC.TSX: CRWN

Investor presentation

September 2017

Forward looking statements

This presentation contains certain “forward looking statements” and certain “forward looking information” as defined under

applicable Canadian securities laws. Forward-looking statements can generally be identified by the use of forward-looking

terminology such as “may”, “will”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “continue”, “plans” or similar

terminology. Forward-looking statements in this news release include, but are not limited to, statements with respect to

Crown’s future cash flows and earnings, future dividends, transaction pipeline, and the Corporation’s business plans and

strategy. Forward-looking statements are based on forecasts of future results, estimates of amounts not yet determinable

and assumptions that while believed by management to be reasonable, are inherently subject to significant business,

economic and competitive uncertainties and contingencies. Forward-looking statements are subject to various risks and

uncertainties concerning the specific factors identified in the Crown’s periodic filings with Canadian securities regulators. In

addition, Crown’s dividend policy will be reviewed from time to time in the context of the Company’s earnings, financial

requirements for Crown’s operations, and other relevant factors and the declaration of a dividend will always be at the

discretion of the Board of Directors. Shareholders will be entitled to receive dividends only when any such dividends are

declared and there is no entitlement to any dividend prior thereto. Crown undertakes no obligation to update forward-looking

information except as required by applicable law. Such forward-looking information represents management’s best judgment

based on information currently available. No forward-looking statement can be guaranteed and actual future results may

vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements or information.

2

3

There is a major funding gap in Canada’s middle market

Canadian

companies

6,000Canadian

companies

6,000

bank debt

Dilutive

Ownership control

public / private

equity

Poorly structured to service mid-market

Less active due to increased regulation

& capital requirements

Canada’s mid-market: The unsung hero of our economy

4

6,000Canadian companies

The middle market has significantly outpaced the growth of large cap companies

31%

1.9mm

$670B

of Canada’s

GDP

Canadian

jobs

annual

sales

$

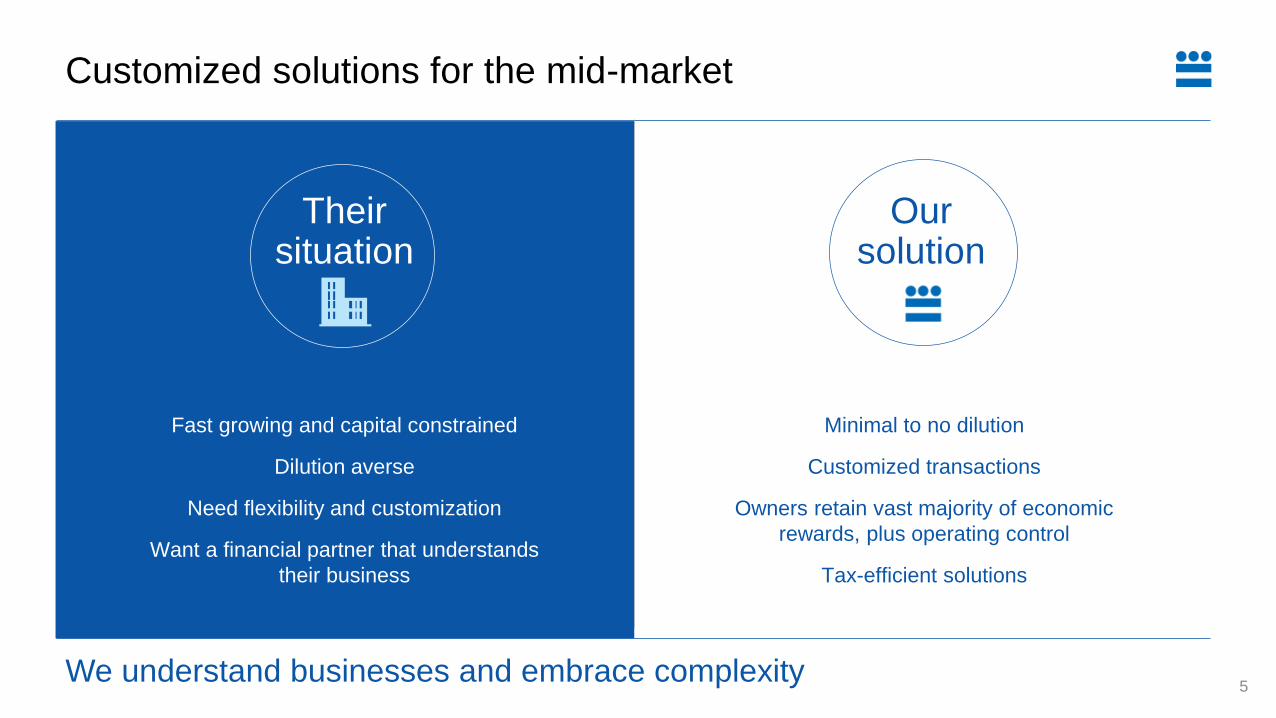

Fast growing and capital constrained

Dilution averse

Need flexibility and customization

Want a financial partner that understands

their business

5

Customized solutions for the mid-market

We understand businesses and embrace complexity

Their situation

Our solution

Minimal to no dilution

Customized transactions

Owners retain vast majority of economic

rewards, plus operating control

Tax-efficient solutions

6

Crown Capital Partners: Financing Canada’s middle market

16 42 $600 year track

recordtransactions million in loans

to date

+

How we choose investments

7Great companies, great pricing drives our model

Successful Companies

Premium Pricing

Asset Rich

Market allows

2 3of

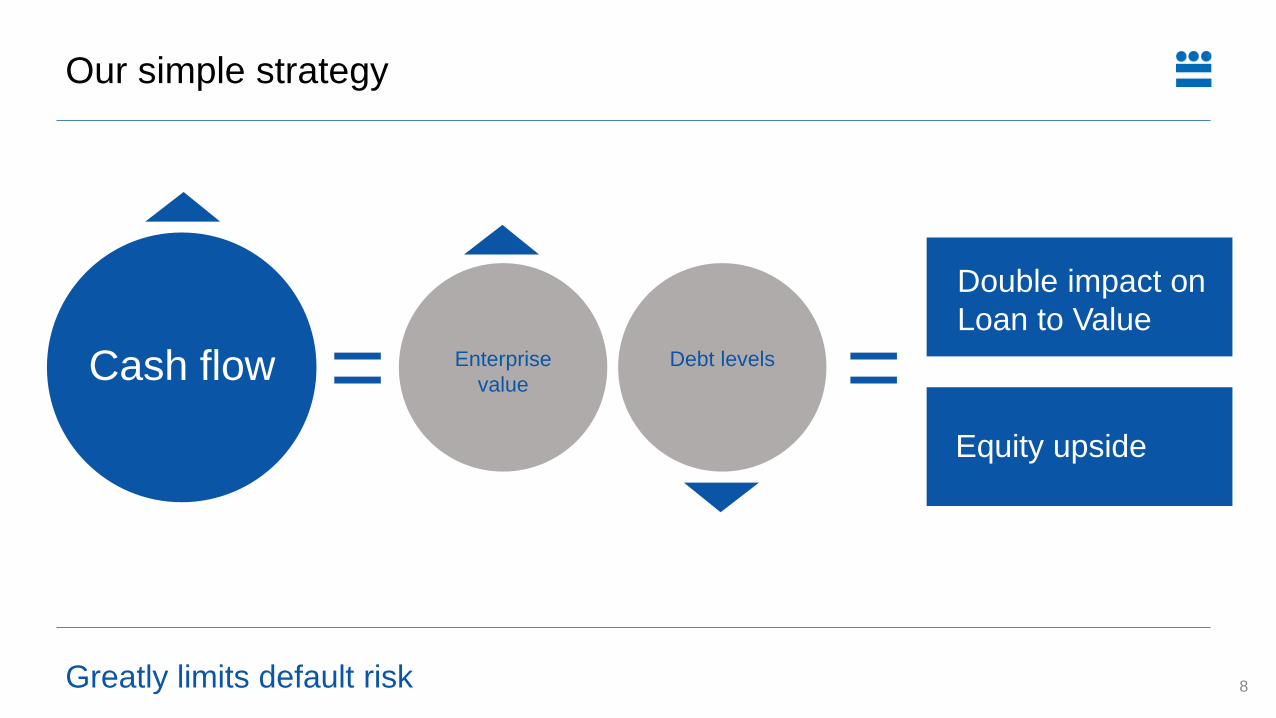

Our simple strategy

8

=

Greatly limits default risk

Debt levelsEnterprise

valueCash flow =

Double impact on

Loan to Value

Equity upside

Alternative capital for mid-market companies

9

Type Special situations Long term

Form Senior / subordinated debentures

Fixed rate long-term loans / participating

loans / perpetual debt structures / recurring

revenue structures

Duration <5 years >5 years

Prepayment

costLow Medium to high

Bonus

featureYes No

Target cash

yield 10-14% 12-16%

Target gross

yield 12-18% 12-16%

Transitory capital with

high returns

High-value portfolio comprised of

stable, sustainable cash flows

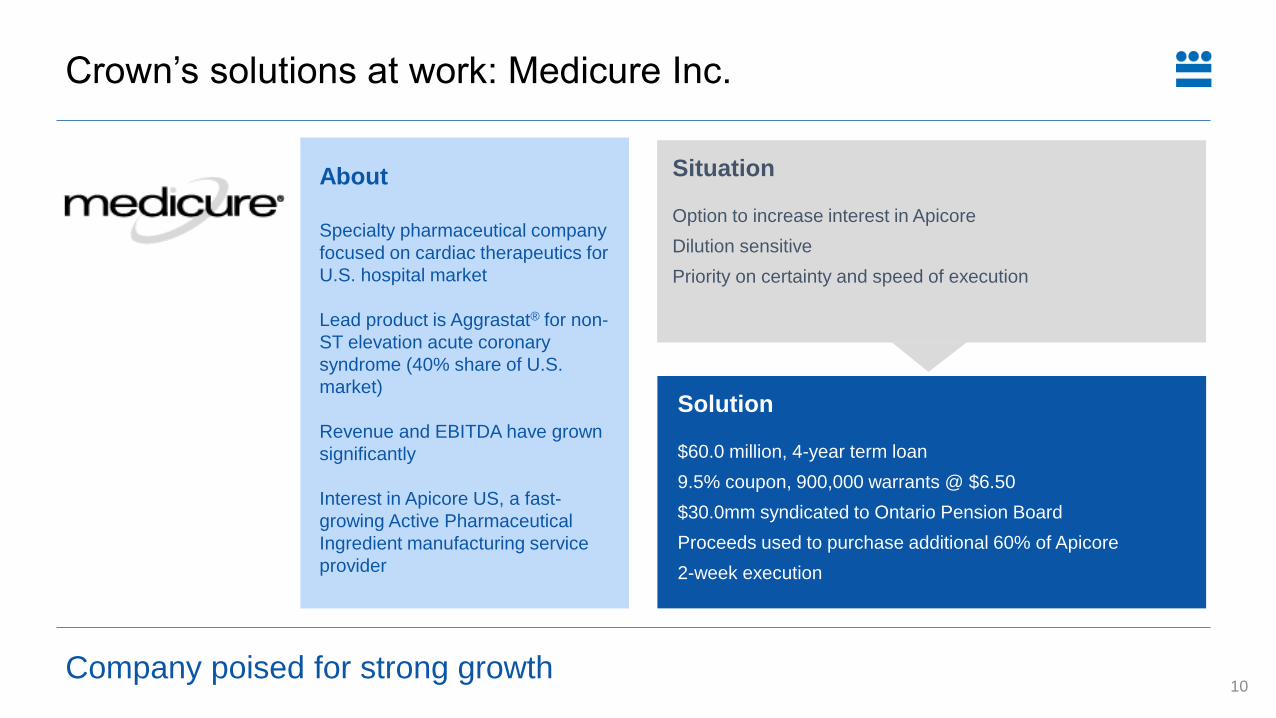

Crown’s solutions at work: Medicure Inc.

10Company poised for strong growth

About

Specialty pharmaceutical company

focused on cardiac therapeutics for

U.S. hospital market

Lead product is Aggrastat® for non-

ST elevation acute coronary

syndrome (40% share of U.S.

market)

Revenue and EBITDA have grown

significantly

Interest in Apicore US, a fast-

growing Active Pharmaceutical

Ingredient manufacturing service

provider

Situation

Option to increase interest in Apicore

Dilution sensitive

Priority on certainty and speed of execution

Solution

$60.0 million, 4-year term loan

9.5% coupon, 900,000 warrants @ $6.50

$30.0mm syndicated to Ontario Pension Board

Proceeds used to purchase additional 60% of Apicore

2-week execution

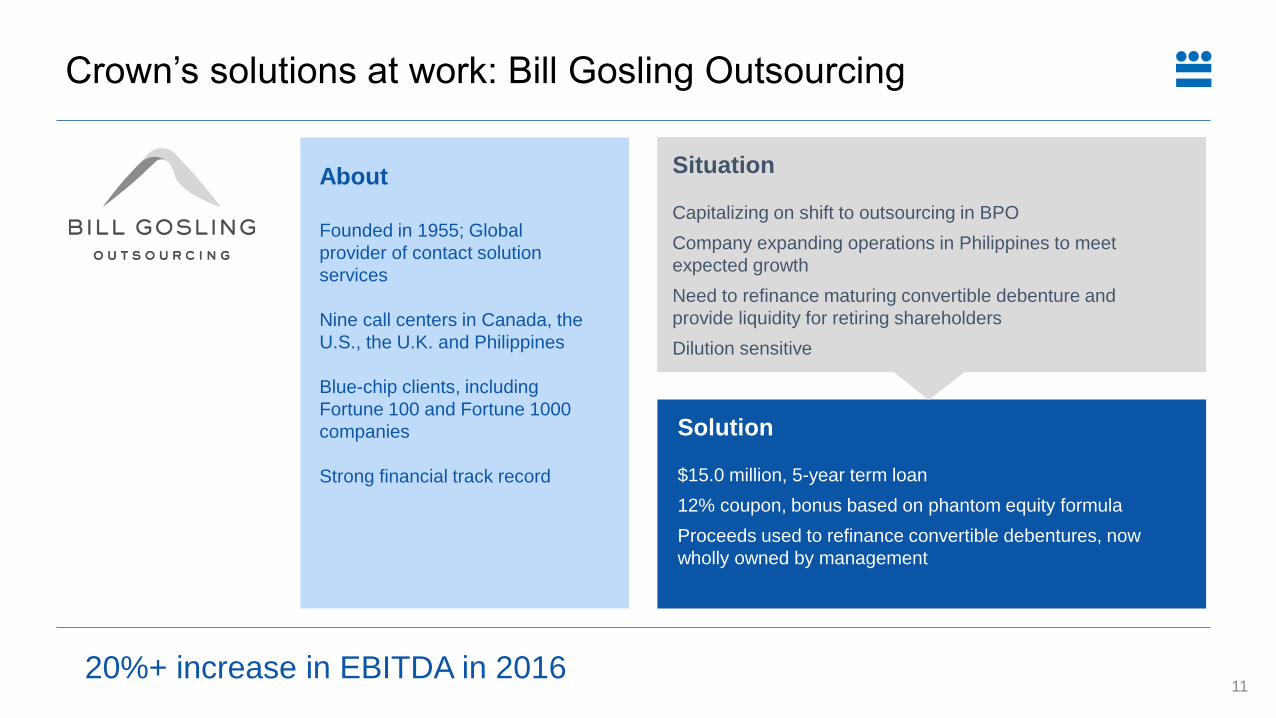

Crown’s solutions at work: Bill Gosling Outsourcing

1120%+ increase in EBITDA in 2016

Situation

Capitalizing on shift to outsourcing in BPO

Company expanding operations in Philippines to meet

expected growth

Need to refinance maturing convertible debenture and

provide liquidity for retiring shareholders

Dilution sensitive

Solution

$15.0 million, 5-year term loan

12% coupon, bonus based on phantom equity formula

Proceeds used to refinance convertible debentures, now

wholly owned by management

About

Founded in 1955; Global

provider of contact solution

services

Nine call centers in Canada, the

U.S., the U.K. and Philippines

Blue-chip clients, including

Fortune 100 and Fortune 1000

companies

Strong financial track record

Crown’s solutions at work: Source Energy Services

12

Situation

Currently supplies approximately 50% of the proppant

market in Western Canada

Well positioned to capitalize on intensification of usage

of frac sand as well as increased drilling activity

Solution

$15.0 million investment in $130 million 5-year senior

secured first lien notes

10.5% coupon, right to equity participation

Proceeds used to refinance existing syndicate of senior

lenders

About

Leading supplier of frac sand to

key oil and gas producers in

Western Canada

Vertically integrated operations,

including one frac sand mine and

eight transload terminals

Company’s logistical network

offers access to customers

operating in key areas located in

Western Canada and North

Dakota

Completed $175 million Initial Public Offering in April

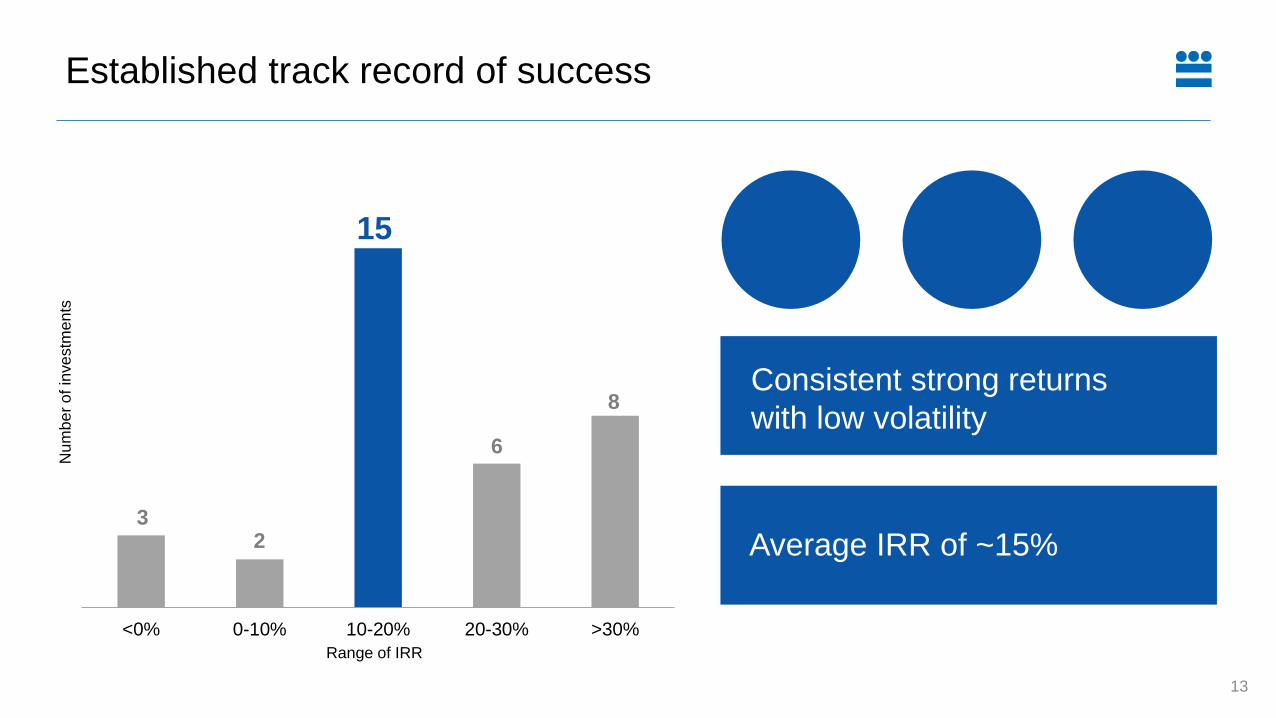

0

2

4

6

8

10

12

14

16

<0% 0-10% 10-20% 20-30% >30%

Established track record of success

13

Range of IRR

32

6

8

15

Num

be

r o

f in

ve

stm

en

ts

Consistent strong returns

with low volatility

Average IRR of ~15%

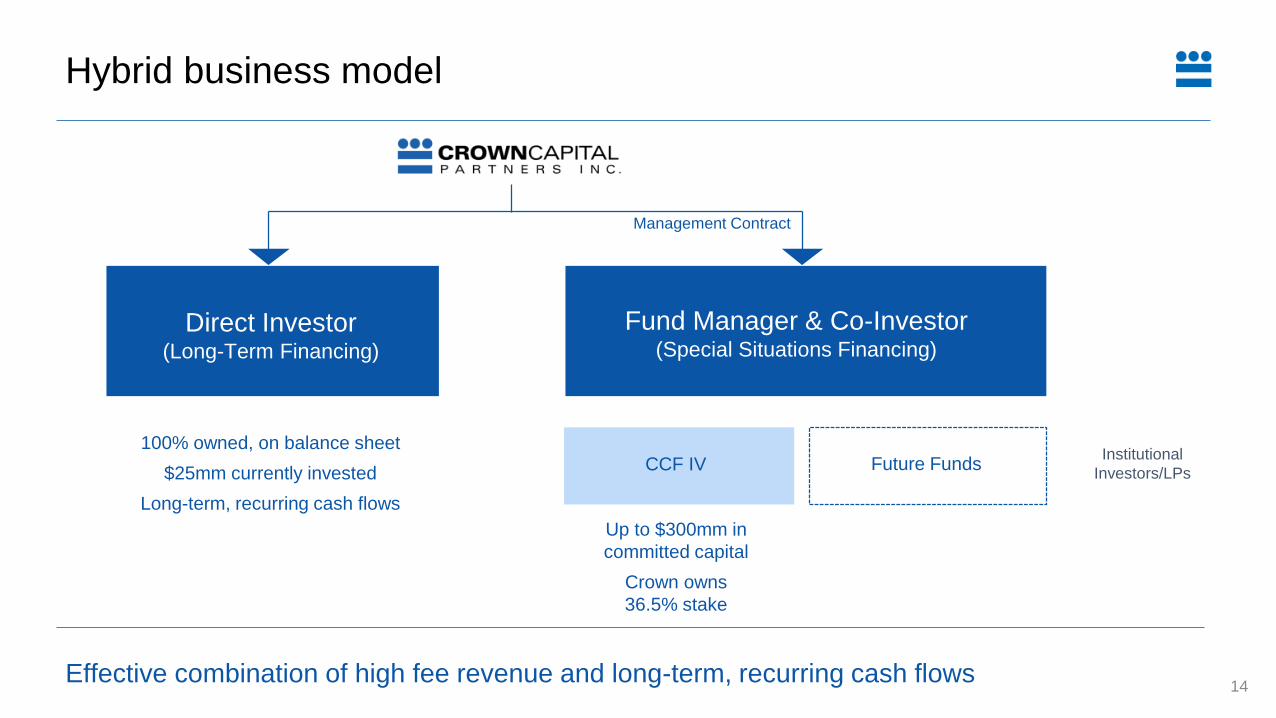

Hybrid business model

Direct Investor(Long-Term Financing)

Fund Manager & Co-Investor(Special Situations Financing)

100% owned, on balance sheet

$25mm currently invested

Long-term, recurring cash flows

Up to $300mm in

committed capital

Crown owns

36.5% stake

CCF IV Future FundsInstitutional

Investors/LPs

Management Contract

Effective combination of high fee revenue and long-term, recurring cash flows 14

Current portfolio

15

$15.0 million

Refinancing

May 2016

$25.0 million

Growth Financing

December 2015

$30.0 million

Refinancing

May 2017

$15.0 million

Refinancing

November 2016

$15.0 million

Growth Financing

February 2017

$30.0 million

Acquisition Financing

November 2016

$15.0 million

Refinancing

December 2016

$25.0 million

Refinancing

May 2017

[long term]

$25.0 million

Refinancing

June 2017

Broad sector experience and diversification

16

12%

52%15%

21%

CompanyLoan Amount

($MM)Industry Province Fund / Direct

Bill Gosling $15.0 Business Services Ontario CCF IV

Touchstone $15.0 Energy Alberta CCF IV

Marquee $30.0 Energy Alberta CCF IV

Source $12.5 Energy Services Alberta CCF IV

Ferus $25.0 Energy Services Alberta CCF IV

Medicure $30.0 Healthcare Manitoba CCF IV

Petrowest $15.0 Infrastructure Alberta CCF IV

Petrowest $10.0 Infrastructure Alberta CCF IV

PenEquity $25.0 Real Estate Ontario Direct

Solo Liquor $15.0 Retail Alberta CCF IV

$192.5

Outstanding loans by industry

23%

20%

16%

13%

13%

8%

8%

Energy - 23% Energy Services - 20% Healthcare - 16%Infrastructure - 13% Real Estate - 13% Retail - 8%Business services - 8%

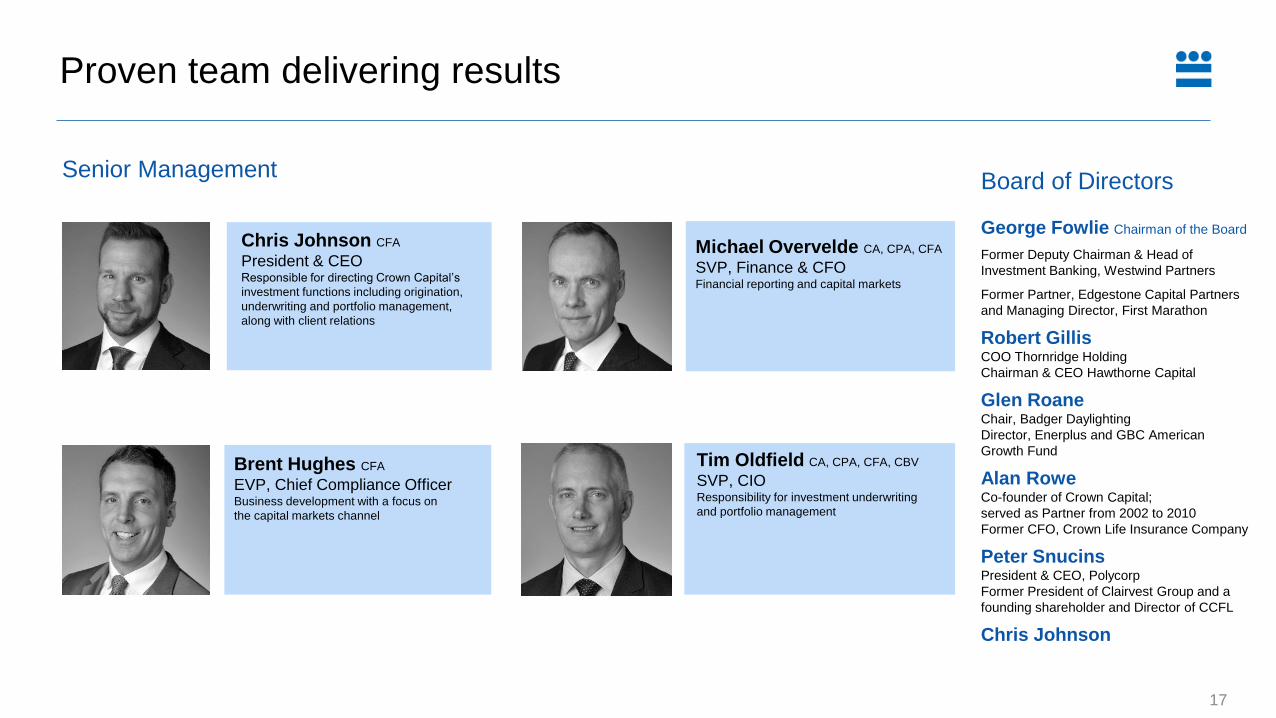

Proven team delivering results

17

Chris Johnson CFA

President & CEOResponsible for directing Crown Capital’s

investment functions including origination,

underwriting and portfolio management,

along with client relations

Brent Hughes CFA

EVP, Chief Compliance OfficerBusiness development with a focus on

the capital markets channel

Tim Oldfield CA, CPA, CFA, CBV

SVP, CIOResponsibility for investment underwriting

and portfolio management

George Fowlie Chairman of the Board

Former Deputy Chairman & Head of

Investment Banking, Westwind Partners

Former Partner, Edgestone Capital Partners

and Managing Director, First Marathon

Robert GillisCOO Thornridge Holding

Chairman & CEO Hawthorne Capital

Glen RoaneChair, Badger Daylighting

Director, Enerplus and GBC American

Growth Fund

Alan RoweCo-founder of Crown Capital;

served as Partner from 2002 to 2010

Former CFO, Crown Life Insurance Company

Peter SnucinsPresident & CEO, Polycorp

Former President of Clairvest Group and a

founding shareholder and Director of CCFL

Chris Johnson

Board of DirectorsSenior Management

Michael Overvelde CA, CPA, CFA

SVP, Finance & CFOFinancial reporting and capital markets

Specialists in the core fundamentals

18

Robust

origination

Disciplined

underwriting

Proven portfolio

management

Extensive experience and

broad contact base across

Canada and the U.S.

Sourced through referral,

brokers or contact initiated

directly

Offices in Toronto and

Calgary

~12-week process

Due diligence results serve as

input to proprietary credit

score

Portfolio risk minimized

through close working

relationships and rigorous

reporting requirements

In the event of

underperformance, Crown’s

primary objective is to assist the

financing client in restoring

performance

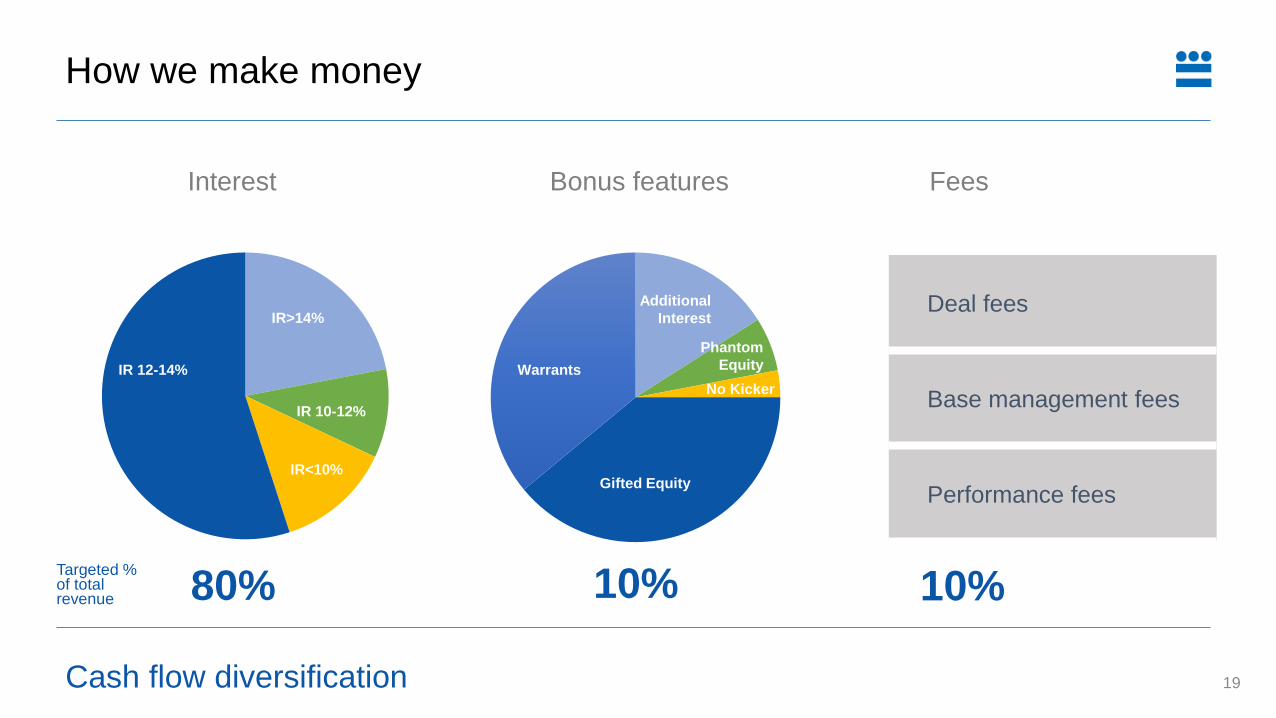

How we make money

19

Interest Bonus features Fees

IR>14%

IR 10-12%

IR<10%

IR 12-14%

Cash flow diversification

Warrants

Additional

Interest

Phantom

Equity

Gifted Equity

No Kicker

Deal fees

Base management fees

Performance fees

80% 10% 10%Targeted % of total revenue

20

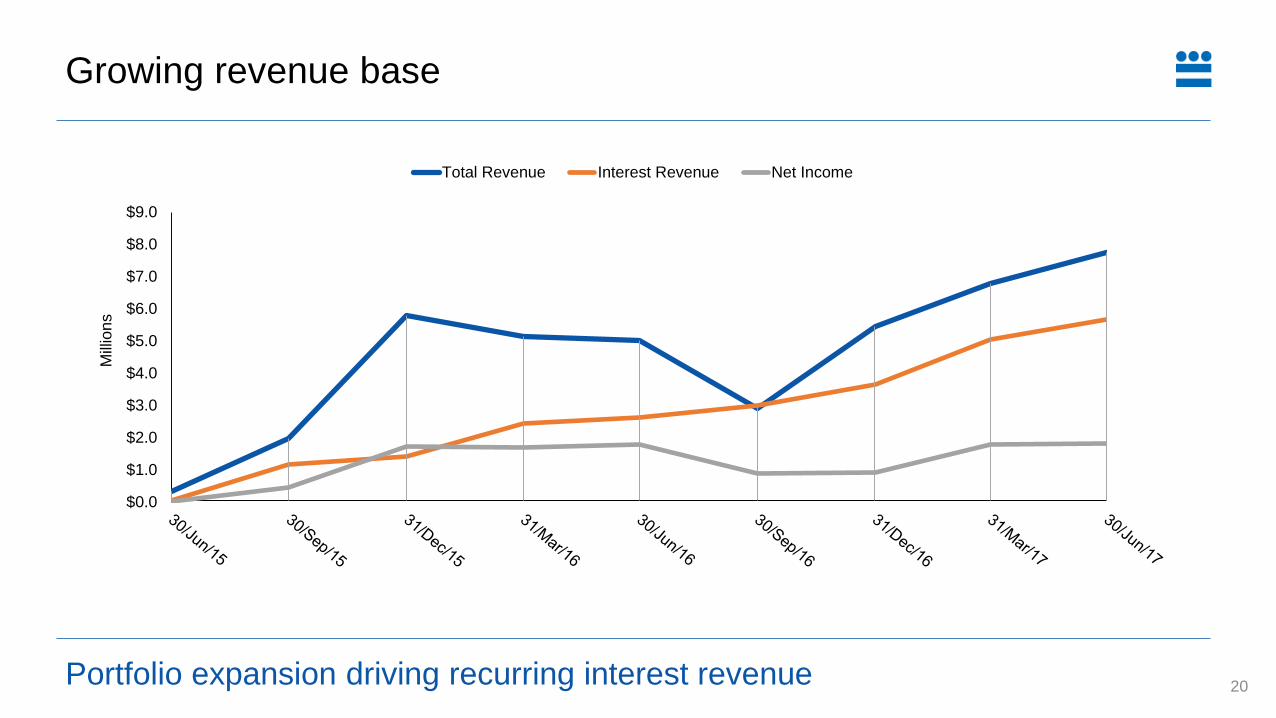

Growing revenue base

Portfolio expansion driving recurring interest revenue

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$9.0

Mill

ion

s

Total Revenue Interest Revenue Net Income

Q2 2017 highlights

Increased funding capacity; $50mm raised

in CCF IV, bringing capital committed to

$225mm

3 new transactions – over $65mm of

capital deployed

2 successful repayments with strong IRRs

Increased dividend to $0.13/share

21

$7.7mmTotal revenue

$3.1mmAdjusted EBIT

$1.8mmNet income

$0.19Income per share

Total equity per share increased to $10.86 at end of Q2 2017

Q2 2017 Financial Highlights

Delivering returns for Crown shareholders

80%

Regular dividend increases

Growth Yield

$100MM

Grow portfolio/book value

Grow capital base

Grow distributable cash

Portfolio growth and diversification drive valuation re-rating

annual

deploymentstarget payout

ratio

22

23

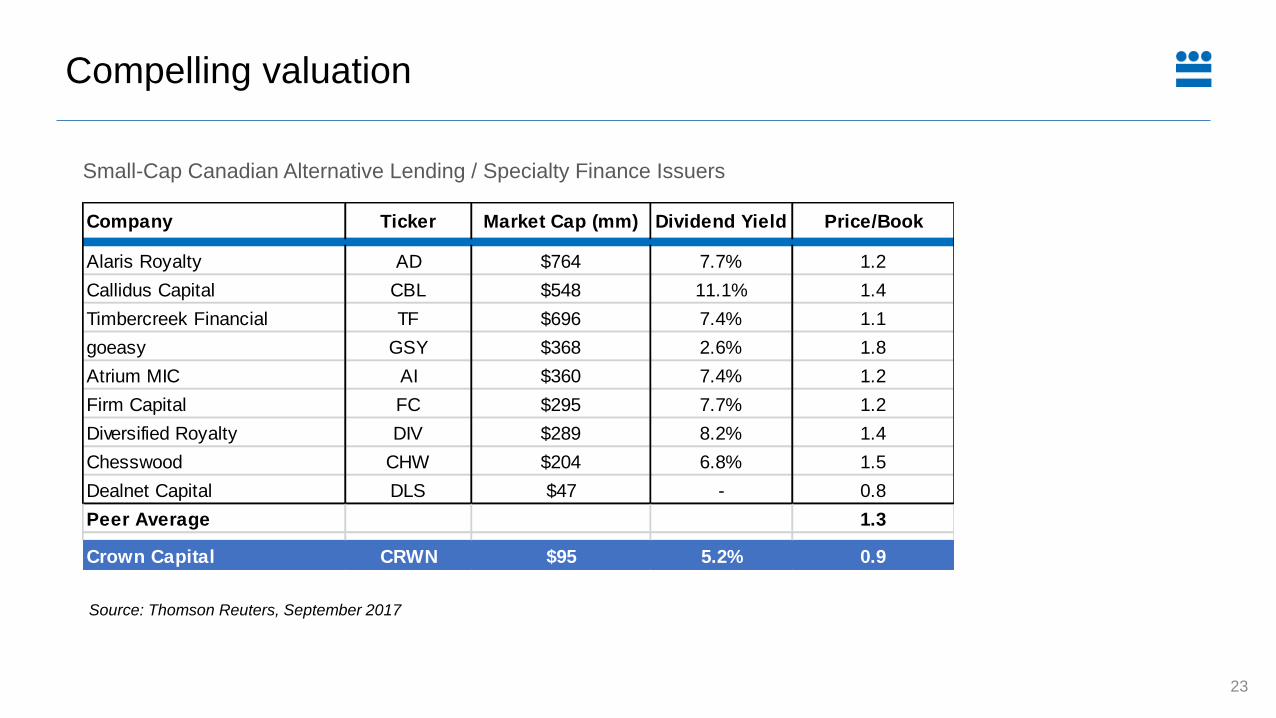

Compelling valuation

Source: Thomson Reuters, September 2017

Small-Cap Canadian Alternative Lending / Specialty Finance Issuers

Company Ticker Market Cap (mm) Dividend Yield Price/Book

Alaris Royalty AD $764 7.7% 1.2

Callidus Capital CBL $548 11.1% 1.4

Timbercreek Financial TF $696 7.4% 1.1

goeasy GSY $368 2.6% 1.8

Atrium MIC AI $360 7.4% 1.2

Firm Capital FC $295 7.7% 1.2

Diversified Royalty DIV $289 8.2% 1.4

Chesswood CHW $204 6.8% 1.5

Dealnet Capital DLS $47 - 0.8

Peer Average 1.3

Crown Capital CRWN $95 5.2% 0.9

Market facts

24

Ticker CRWN

Market cap ~$95 million

52-week

high / low$11.90 – $8.55

Shares

outstanding

(FD)

9.5 million

(9.9 million)

Quarterly

dividend$0.13 per share

Yield ~5.2%

Analyst

coverage

Chris Murray

Stephen MacLeod

Scott Chan

Jeff Fenwick

Stephen Boland

Trevor Johnson

Brenna Phelan