critical review of jakarta water concession contract review.pdf · critical review of jakarta water...

TRANSCRIPT

CRITICALREVIEW

OF JAKARTAWATER

CONCESSIONCONTRACT

AMRTA Institutefor Water Leteracy

Cont

ent

Chapter 1CRITICAL REVIEW OF JAKARTA WATER 1CONCESSION CONTRACT

Chapter 2ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCECOOPERATION AGREEMENT PAM JAYA, PALYJA AND TPJ

Introduction 5

Performance of PAM Jaya, Palyja and TPJ 7

Study on Business Aspect of the CA 8

Termination Trap 12

Termination, Is it Possible? 15

Problem of Status of PAM JAYA’s Employees 16Assigned to assist Private Partners

Conclusion and Recomendation 18

What should we do with the complicated CA? 19

Revision on the CA 19

Continue the CA 22

CRITICAL REVIEW OF JAKARTA WATER CONCESSION CONTRACT

1

CRITICAL REVIEW OF JAKARTAWATER CONCESSION CONTRACT

Wijanto Hadipuro and Nila Ardhianie1

1 Wijanto Hadipuro: Founder of Amrta Institute for Water Literacy and Lecture at Soegijapranata Catholic UniversitySemarangNila Ardhianie: Director Amrta Institute for Water Literacy

2 See The Water Barons, page 71.3 See article Erik Swyngedouw, Privatizing H2O, particularly on corruption prejudice for the case of TPJ. Whereas

statement on cronyism may be seen on Chapter 5 book The Water Barons. The first involvement of two multi-national companies in water sector of Ondeo/Suez and Thames Water involving Anthony Salim and Sigit Harjojudanto.Both are crony and son of RI President at the era of Soeharto.

11111

P articipation of private party in cleanwater management in Jakarta seemshave to pass through a long and com-

plicated way. The first participation of pri-vate party was commenced in June 19912

when the World Bank provided a loan toPAM Jaya, a public enterprise of clean watermanagement in Jakarta, amounting to USD92 million in order to improve infrastructuresector. The loan which is also supported bya loan from Japanese Economic CooperationFund is used to build instalation of watermanagement in Pulogadung. The two organi-zations represent the main sponsors in in-volving private party into clean water man-agement in Jakarta.

Role of Thames Water Overseas Ltdwas seemed in 1993. Thames joins with SigitHarjojudanto who is a son of the Presidentin charge at the moment, Soeharto. Suez start-ing its role in clean water supply in Indone-sia since 1980s feels to be stolen and thenjoins with Anthony Salim as a partner.

Jakarta is separated into two areas byCiliwung River. Western area is managed bya company which now is called as PT PAMLyonnaise Jaya (Palyja) and eastern area ismanaged by PT Thames PAM Jaya (TPJ).Form of cooperation between PAM Jaya andits two private partners is a modified conces-sion or it is also named as Operate, Developand Transfer form. The cooperation is ef-fective since February 1, 1998 and will beterminated its twenty-fifth birthday. As theconsequence of Indonesian economical andpolitical crisis in 1998, the agreement isamended and the new one is stated to be ef-fective on October 22, 2001 without anychange stated on the agreement’s term pe-riod.

Involvement of the private partners intoclean water management in Jakarta is full ofcollusion, corruption and nepotism prac-tices3. Sense of economic interest by utiliz-ing political power is very strong in involv-ing the two private partners of PAM Jaya

CRITICAL REVIEW OF JAKARTA WATER CONCESSION CONTRACT

2

prior to the agreement is implemented andin the share selling to private partners whenthe cooperation is going on.

In his presentation and explanation4,Achmad Lanti described about the role ofPresident Soehato in involving process of pri-vate partners into clean water management inJakarta. The involving of private partners aswell, is started by an advice of RI presidentdated on June 12, 1995 for Minister of PublicWork Affairs who was charged by Moochtar5.The advice shall have positive or neutral re-sults but in fact it was ended by the involvingof Sigit Harjojudanto, a son of Soeharto,through PT Kekarpola Thames Airindo(KATI) joining with Thames Water OverseasLtd. in which Thames gives 20% the companyshares to Sigit; and Anthony Salim, a son ofSudono Salim, Soeharto’s crony through PTGaruda Dipta Semesta (GDS) joining withSuez Lyonnaise des Eaux.

In performing of the two foreign pri-vate partners involment, the share ownershipwas assigned several times. When the Coop-eration Agreement (CA) was signed6 on July 6Juli, 1997 KATI shares amounting to 20% isowned by Kekarpola Airindo and the other80% is owned by Thames Water Overseas Ltd.Whereas 60% of GDS shares is owned by PT

Elang Sakti Prabawa and 40% is owned bySuez Lyonnaise des Eaux.

On July 17, 1998 GDS was renamedinto PT PAM Lyonnaise Jaya (Palyja) with100% shares owned by Suez Lyonnaise desEaux. KATI then was renamed into PTThames PAM Jaya (TPJ) with share compo-sition of 5% owned by PT Kekarpola Airindoand 95% owned by PT Thames Water Over-seas Ltd. which then was renamed into RWEThames Water.

On October 22, 2001 when the CA wassigned, Article 7 states that the Second Partyfor Palyja is Ondeo Services (previouslyknown as Suez Lyonnaise des Eaux) and PTBangun Tjipta Sarana. The Second Party forTPJ is Thames Water Overseas Ltd. and PTTera Meta Phora.

The involving of private partners intoclean water management in Jakarta shows thatclean water management has becomed anaarena to exploit economic profit through theinfluence of political power. It is veryintersting to observe the manner of privateparties entering into Jakarta and how theshares of local partners could be assignedfrom a company to the other ones, and how

4 See presentation of Achmad Lanti representing Regulator Body of DKI JakartaDrinking Water Service in a Limited Discussion titled ‘To Apart ComplicatedProblem on Water Priva tization in Jakarta’ held by People Coalitionfor Right on Water and WGPSR on January 16, 2007 andExplanation of Composite Team of TPJ Share As-signment in Composite Work Meeting of DPRDCommission of DKI Jakarta Province inDPRD Building on January 15, 2007.

5 See the book titled The Water Baronspage. 73.

6 See Letter of Governor Number 1108/072to Chief of DPRD of DKI Jakarta dated onApril 13, 2000, Regarding: Result of re-ne-gotiation on cooperation between PAAM Jayaand the private partner.

CRITICAL REVIEW OF JAKARTA WATER CONCESSION CONTRACT

3

at the end the foreign private partners couldsell the shares in large amount to other com-pany.

Economic interest gained by private part-ners expressed on several articles and mecha-nisms in the CA. One of them is mechanismof payment. Mechanism of payment for pri-vate partner is in form of water charge. As anote that water charge has no relationship withthe tariff charged to the costumers. Articles28. 1 the CA was amended and restated onOctober 22, 2001 (hereinafter referred to asCA) point e states that the first water chargewhich is effective on April 1, 2001 is Rp. 2,400,-and it would be revised for every six monthsaccording with the formula written on theAttachement 5 of the CA. The payment madethrough the water charge and its escalation for-mula provides profit security for private part-ners during the cooperation period. How itcould be happened to be further discussed atthe following section.

The increasing of water charge un-bal-anced with tariff improvement results short-fall for PAM Jaya. The consequence is a for-mula of automatic tariff adjustment madewithin every six months which was agreed onJuly 2004 for the period ended in 2007. Sincethe cooperation is performed tariff increas-ing has been happened on July 24, 1998, March29, April 4, 2003, December 31, 2003, Janu-ary 2005, July 1, 2005 and December 30, 20057.

Revenue obtained from water tariff isdivided pursuant to provision set on Article28. Revenue for PAM Jaya is monthly costof PAM Jaya, payment of loan to FinancialAffairs Department, expense for RegulatorBody and payment for Region Original In-come to DKI Jakarta Provincial Government

which values are on Attachment 6 of the CA.Nevertheless the revenue of PAM Jaya doesnot mean a profit for PAM Jaya because ifall revenue obtained from the tariff is notsufficient for payment of water charge toprivate partner, PAM Jaya have to be respon-sible on the loss in a form of shortfall.

Regulator Body was established on Sep-tember 19, 2001. Its position is uncommon,due to its function and authority is regulatedon the CA particularly on Article 51.1. Theexistence of Regulator Body is mandated onthe article of the CA, even more Article 51.1states that :

The Parties agree that regulator body(Supervisory Body) to be established byGovernor of DKI Jakarta shall havefunction and authority as regulated onthe Letter of Decree of Governor of DKIJakarta Province written on Attachment20….

Usually Regulator Body is independ-ent and should have been established priorto the CA is signed. In many states like Eng-land and Wales which Regulator Body couldbe the model for other states, their Regula-tor Body is even functioned nationally.Hopefully the Regulator Body should com-pare the performance and tariff charged tothe costumers and costumers would not beencumbered with inefficient matters by theprivate partners. For such case in Jakarta, ifRegulator Body is really independent and es-tablished prior to the CA made, then we willget a better CA which does not too side withand protect business interests of the privatepartners.

7 See Presentation of Nila Ardhianie in several mass medias in Jakarta in November 2006.

4

CRITICAL REVIEW OF JAKARTA WATER CONCESSION CONTRACT

5

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

Introduction

Legal principles directly relating with theCooperation Agreement (CA) between PAMJaya with Palyja and TPJ is an Instruction ofMinister of Home Affairs Number 21 of1996 concerning Directory for Cooperationbetween Perusahaan Daerah Air Minum(PDAM) and Pivate Party. The Instructionof Minister of Home Affairs states that eachand every activity of PDAM with PrivateParty is basically purposed to improve itsservices covering:

1. Increasing Quantity.2. Increasing Quality.3. Increasing continuity.4. Increasing Efficiency.5. Increasing Society Prosperity. 9

The Cooperation Agreement (asamended and restated on Ooctober 22, 2001)on Supply and Improvement of Clean Wa-ter in Jakarta states that aims and objectivesof the cooperation agreement set out onpoint 2.2 are as follows:

1. to support economic and socialdeveloment in the Area of DKI JakartaProvince by means of developing onwater infrastructure in the Area of Co-operation pursuant to the provisionsherein;

2. reach the range of piping water supplywidespreadly in the Area of Cooperation;

3. reach substantial expansion in distribu-tion networking of Clean Water andDrinking Water;

4. to involve participation of private partyin producing and distributing Clean

22222ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

COOPERATION AGREEMENTPAM JAYA, PALYJA AND TPJ8

8 Forgive me please if data for the analysis is very limited reminding that Clause 47 of the CA states that the competentauthorities keep the secret all of therir commercial and technical information. It is strange that there is such a clausein a CA relating with public interest even relating with the need of many people.

9 On November 9, 2005, President issues a Presidential Regulation (PP) Number 67 of 2005 on Cooperation of theState and Private Business Enterprise in Providing Infrastructure. The PP is further progressive compared to theexisting regulation including the Instruction of Minister of Home Affairs as well as the regulation for it. Clause 6point f of the PP states that the cooperation shall mutually result profit and Clause 12 paragraph 2 and Clause 18states that the system must go through a general auction. Mutual cooperation is not mentioned in the Instruction ofMinister of Home Affairs. In the Instruction the cooperation process may be carried out by direct appointment andnot having to be with a general auction.

6

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

Water and Drinking Water in Area ofDKI Jakarta Province in order to accel-erate rapid removal of water supplybacklog10 (according with English trans-lation in the CA) and to continue theimprovement of Service Quality to Con-sumers;

5. to provide a system obliging thecostumers to follow a change from un-derground water supply into piping wa-ter supply system for the places wherepiping water has been available;

6. to improve supply and management ofClean Water and Drinking Water, if itsfinance and technique is proper, includ-ing by means of reforming The ExistingProduction Facility and The Existing Dis-tribution Facility, and if it is proper, tobuild New Production Facility and NewDistribution Facility to supply Clean Wa-ter and Drinking Water in the Area of Co-operation;

7. to improve efficiency in water supply sys-tem;

8. to secure quantity, quality and continuityof Supply of Clean Water and DrinkingWater and Facility of Production and Dis-tribution in the Area of Cooperation;

9. to comply with Technical Target and Serv-ice Standard;

10. to improve Service to Costumers in theArea of Cooperation;

11. to decrease quantity of Water Loss levelin the Area of Cooperation in accordanceto Technical Target;

12. to improve operational performance, toincrease the ability in managing the com-pany and personal performance bytrainings, technology transformation andgeneral improvement on skill of theEmployees working on the Project andto develop operational and terchnologysystem;

13. to increase Ratio of Service Range in theArea of Cooperation by accelerating theavailibility of new connections to supplyClean Water and Drinking Water toCostumers; and

14. to make a project which is able to financeitself and carry out economically for theParties.

According with the CA, private partneras the Second Party shall have skill and fundand other resources relating with the plan,construction, management (including to readmeter, to prepare bill and to dun) and opera-tion of facilities for production and distri-bution of Clean Water and Drink Water.

First article of the chapter shall makeendeavor to see attainment of the above ob-jective even though with limited data. Thesecond article of the chapter consists ofstudy of business aspect of the CA particu-larly from the side of Private Partner and thecase of PAM Jaya employees assigned to as-sist the private partners.

10 Backlog according with AS Hornby Dictionary is an accumulation of work or business (e.g. arrears of unfulfilledorders) not yet attended to.

7

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

Performance of PAMJaya, Palyja and TPJ

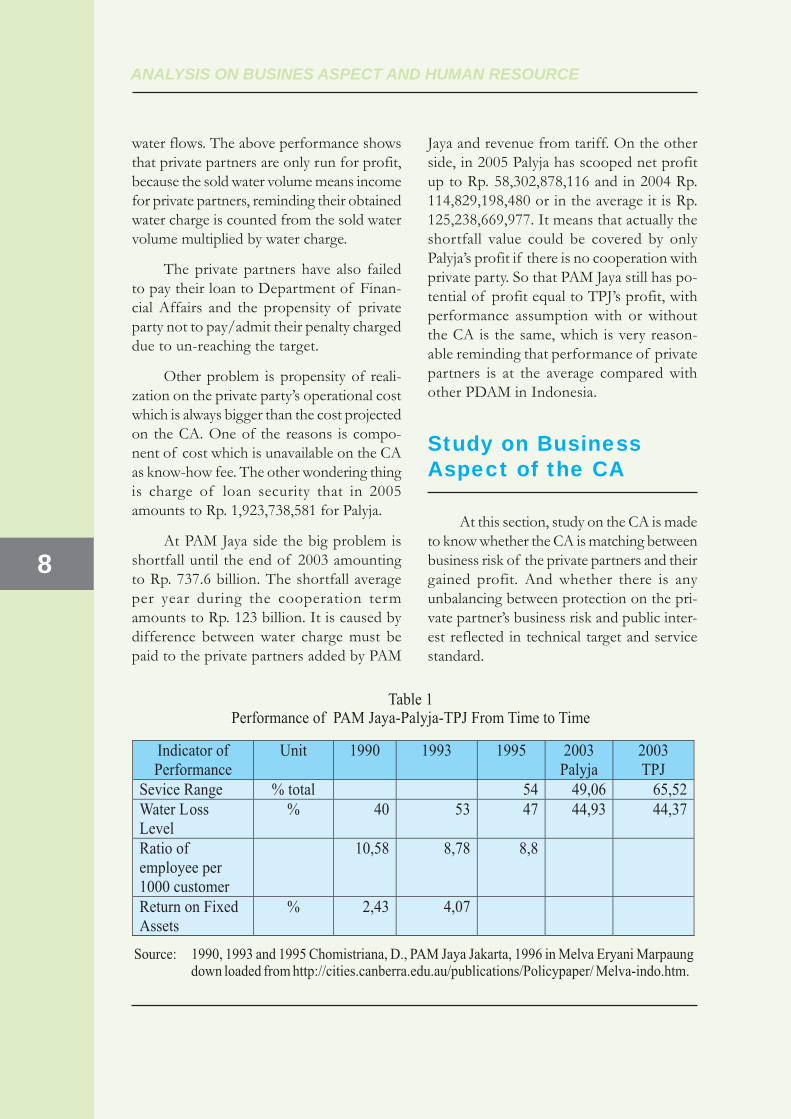

Table 1 shows that PAM Jaya prior tocooperate with private partner was a PDAMthat capable to get profit. In 1990 Its Returnon Fixed Assets was 2,43%.

Based on Letter of Decree of Ministerof Home Affairs Number 47 of 1999 con-cerning Guideline for PDAM PerformanceAssessment, then PDAM Jaya both prior toand after getting partnership with privateparty, indicates average and bad points. Badpoint with lowest score of 1 and good pointwith highest score is 4 or 5. Service rangehase score about 3 and 4 (score 3 for servicerange of 40% - 60%, whereas score 4 is forservice range of 60% - 80%). Score of losslevel is only 1 (for water loss level > 40%).Whereas score ratio of employee per 1000costumers is about 1 and 3 (score 1 for ratio> 10 and score 2 for ratio 7 – 9).

Based on Report of 2003 Annual Per-formance Evaluation made by PAM Jaya thereare several interesting matters to be researched.Firstly that production of water must be ful-filled, therefore nothing could be the reasonfor private partner not to reach the target ofother parameter. Secondly, it is wonder thatthe service range target is down compared withdata on Table 1 of the chapter. In 1995 theservice range has reached 54%11, whereas tar-get of Palyja in 2003 is only 51% and TPJ is64,4%. The same thing is happened for waterloss level. Palyja’s Target is 45,52% and TPJ is41,03%.

Based on the report it is proven that per-formance of Palyja un-reaching the target is

service range (realization is 49.06% of the tar-get 51%) and at performance TPJ is water losslevel (realization is 44.37% of the target41.03%). There are some samples un-meet-ing with quality standard particularly on chem-istry/physically and bacteriological control atfacility of production and as bacteriology pa-rameter at facility of distribution for both part-ners. In case of costumer’s complaint, com-plaint on breaking of main pipe is 4.968(Palyja) and TPJ which cannot be evaluated.Complaint on no water current is 15.741 forPalyja and 11.891 for TPJ. Complaint on wa-ter quality is 1.960 for Palyja and 508 for TPJ.Principle problem faced by the private part-ners is water pressure at connection point.Both partners cannot reach the target.

Tabel 2 shows ratio on target and reali-zation prior to the CA and until the CA isterminated. Target attached on the table isthe target after the CA amended. It is seenthat the amended CA results that the targetof service range is down drastically. In 2000target of service range is 63%, while afterthe CA is amended in 2001 target of servicerange is only 50%. As well as water loss level,in 2000 target of water lose level is 42%whereas in 2001 it is adjusterd into 47%. Tar-get of sold water is also adjusted from 281milliion cubic in 2000 becomes 236 millioncubic in 2001.

From the table we see that realizationof sold water since 2001 is always over thetarget, but water loss level is always underthe target. Whilst service range is a little more/ less than the target. Water service does notmean that service to customers better, be-cause service is only measured by numberof lines not by quality of service as waterpressure and reliability and how long the

11 Actually inhabitan of Jakarta in 1995 is only 8,8 million people whereas in 2005 it is about 9,9 million.

8

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

water flows. The above performance showsthat private partners are only run for profit,because the sold water volume means incomefor private partners, reminding their obtainedwater charge is counted from the sold watervolume multiplied by water charge.

The private partners have also failedto pay their loan to Department of Finan-cial Affairs and the propensity of privateparty not to pay/admit their penalty chargeddue to un-reaching the target.

Other problem is propensity of reali-zation on the private party’s operational costwhich is always bigger than the cost projectedon the CA. One of the reasons is compo-nent of cost which is unavailable on the CAas know-how fee. The other wondering thingis charge of loan security that in 2005amounts to Rp. 1,923,738,581 for Palyja.

At PAM Jaya side the big problem isshortfall until the end of 2003 amountingto Rp. 737.6 billion. The shortfall averageper year during the cooperation termamounts to Rp. 123 billion. It is caused bydifference between water charge must bepaid to the private partners added by PAM

Jaya and revenue from tariff. On the otherside, in 2005 Palyja has scooped net profitup to Rp. 58,302,878,116 and in 2004 Rp.114,829,198,480 or in the average it is Rp.125,238,669,977. It means that actually theshortfall value could be covered by onlyPalyja’s profit if there is no cooperation withprivate party. So that PAM Jaya still has po-tential of profit equal to TPJ’s profit, withperformance assumption with or withoutthe CA is the same, which is very reason-able reminding that performance of privatepartners is at the average compared withother PDAM in Indonesia.

Study on BusinessAspect of the CA

At this section, study on the CA is madeto know whether the CA is matching betweenbusiness risk of the private partners and theirgained profit. And whether there is anyunbalancing between protection on the pri-vate partner’s business risk and public inter-est reflected in technical target and servicestandard.

9

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

CA’s objectives are detailed in the tech-nical target and service standard on Attach-ment 8.2 and 8.3 herein. Article or clause onthe CA regulating the two matters namelyClause 20 for Technical Target and Clause21 for Service Standard.

Unfortunately service standard andtechnical target reflecting public interest islimited by various terms which no guaranteethe attainment. As the example :

1. Clause 20 point a states that technical tar-get may be amended from time to time inline with Financial Projection. It meansthat if financial realization is deviatedagainst the projection then the technicaltarget may be amended.

2. As well as service standard regulated onClause 20 point a.

3. Clause 24.1 point iv12 states that if annualinvestment plan, program of annual Op-eration and Maintenance, annual FinancialProjection and annual budget approved bythe First Party and/or Regulation Bodymaterially different with Financial Projec-tion set out on Attachment 6, The Partiesshall agree with the amendment to theTechnical Target and/or Service Standarddirectly resulted by the action.

In relating with the above point 4, theprivate partners have tried to play with op-erational cost by carrying out transaction withunique supplier and the supplier has specialrelationship with them. One of the evidencesis the arising of knowhow cost for Suez En-vironment having special relationship withPalyja and cost of loan security by the samecorporation.

It is very hard to get guarantee that pub-lic interest existing on the technical target andservice standard will be reached, becausethere are many clauses enabling to amend thetechnical target and service standard, such as:

1. In case of arising a problem relating withbasic water from PJT II and processed fall-ing water from PDAM Tirta Kerta RaharjaTangerang both in quality and/or quan-tity then technical target and service stand-ard must be discussed in order to adjustthem. The adjusment shall be effectivesince the date when the first lack happenedon quality and quantity (see Clause 11 page64 of the Palyja CA). Such agreementshould be made by private party to sup-plier not to PAM Jaya.

2. In case of PAM Jaya fails in endeavoringto cover the people’s deep well in whichthe service has been covered by the pri-vate party, then technical standard andservice standard may be lowered (seeClause 12 point c).

3. As well as in case of new retributioncharged by governmental institution tocustomers, which may influence customerservice demand so that it may result de-crease significantly at portion of the pri-vate party then technical target and serv-ice standard must be adjusted since theretribution is effective (see Clause 26.6).

Financial Projection on Clause 27 takesan important role in relating with interest ofthe private parties. In fact, revenue of theprivate partners is based on water charge (noton tariff, for the private partners tariff noincreased is not a problem because shortfallis burden of PAM Jaya), but it is wander thatoperational cost which is controlable for the

12 See Clause 1 point on Finacial Projection (Page 13 for the CA of).

10

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

13 Do not wander if there is a complaint stating that salary of the new employee sourced from PAM Jaya does notincrease within 6 years of the cooperation. PAM Jaya is in a very dilematic position because if their salary is in-creased then water charge will be increased too then it will result an increase on the shortfall. posisi yang dilematiskarena jika gaji mereka dinaikkan maka water charge akan naik yang akan berakibat pada kenaikan shortfall.

private partners is proven to be able in influ-encing technical target and service standard.

Based on Shedule 5 water charge willbe adjusted automatically based on the fol-lowing formula:

Cn = [Co x {(Fn x Gn) + (Hn x On)}] + Ksn + Kin

Notes:C : water chargen and o : period of water chargeF : quality of capital cost alocationH : quqlity of operation cost alocationF+H = 1 and for period 2002-2007 F= 25% andH= 75%G : coefficient of adjustment on the pri

vate partner’s capital cost which the80% is in fluenced by constructionindex and the 20% by ConsumerPrice.

O : coefficient of adjustment on theprivate partner’s operational cost.

Ksn : compensation for variation on rupiahexchange value against foreigncurrency.

Kin : compensation fot variation oninterest level.

The interesting thing is K component inwater charge formula. K Component guaran-tees that business of the private partners issecured from fluctuation of exchange valueand interest level.

Whereas O formula is as follow:

On = an (Ln)/Lo + bn (Xn)/Xo + cn (En)/Eo + dn(Mn)/Mo + en (Bn)/Bo+ fn (Nn)/No + gn(Tn)/To

Notes:L : index of manpower (more specific thing is

annual average cost (basic salary, allowance, pension, insurance, income tax) forthe last 12 months of an employee, whichis transfered)

X : index of chemistry materialE : index of electricity powerM : index of materialB : index of basic waterN : index of purchasing clean water via meter

inter areasT : index of purchasing clean water

At the formula we see that all uncon-trollable costs for the private partners areincluded into water charge escalation, includ-ing transferred salary of PAM Jaya’s employ-ees whereas policy is on PAM Jaya side13, in-flation, fluctuation of exchange value andinterest rate. If in an ordinary business, casethe endeavor to omit risk of company’s ex-change value, the company has to pay a cer-tain aggregate of money in order to carryout hedging, in this case even the private part-ners may gain more profit than fluctuationof exchange value.

11

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

As well as a change on tariff of tax. Iftax assumption is changed then the partiesare obliged to adjust the water charge withdue observance of each and every loss suf-fered and profit gained by the privatepartners (see Clause 38.5 of the CA).

The private partners also assume thatif an emergency needing action plan (as anexample given by the writer namely dryseason in which people need water supply)is happened accordingly all expenses andcosts incurred by the private partners shallbe admitted as a loan of PAM Jaya to theprivate partners (see the CA on Clause36.2). 14

The most wandering thing is that pri-vate partners are secured to get profit at 22%through terms of Internal Rate of Returnon Clause 27.1 and Schedule 6 of Consoli-dated Financial Projection.

Endeavor to secure profit of privatepartners is also seen at cases arising due totermination which will be discussed at thefollowing part. More over profit projectionof the private partners must also be paid byPAM Jaya if termination is made prior to thenatural termination time of the CA.

Essence of the description is a fact show-ing an unbalancing between public interest andit is reflected on technical target and servicestandard which can be changed anytime andthe fact of shortfall average namely Rp. 123Billion per year; with a very strong profit se-curity of the private partners seen from thelarge number of clauses endeavoring to se-cure their profit even from uncontrollable andcontrollable risks as operational cost. High

profit high risk is not effective in this case.But high profit no risk is effective in the CA.

Based on the CA it is stated that theprivate partners are appointed due to havefund. Is that true? In case of Palyja (TPJ hasno data), investment on fixed asset amount-ing to Rp. 644,761,756,833 is financed byloan. All are loan at Calyon Merchant BankLtd. and European Investment Bank. At themoment obligation with net value is Rp.646,235,274,767. It means that all investmentis financed by loan. So that it is nonsense thatprivate partners have funding capability. Thefund paid by private partners is only paid capi-tal amounting to Rp. 200.630.000.000 whichvalue is actually not so big compared withDKI Jakarta budget amounting to Rp. 17.94trillion. The paid capital has been covered byaccumulated profit of Palyja that until De-cember 31, 2005 has reached an amount ofRp. 211,003,903,490.

14 It has been happened (See the Report on Investigation Result on Deficit/Shortfall, Capex, Opex and Loan of PTPAM Lyonaisse Jaya (Palyja) for Period of February 1, 1998 up to March 31, 2001) made by Supervisory Body onFinance and Development Representative of DKI Jakarta Province I Page 5 on water charge upon non-waterbilledof tanker car.

12

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

Termination Trap

In view of the facts showing that theCA seriously protects the private partnersfrom all risks and the realization that actuallyperformance of the private partners is ordi-nary and that shortfall can actually be cov-ered by only profit gained by Palyja (not byTPJ). Accordingly it is really necessary to ex-amine the possibility of making terminationfar prior to the cooperation agreement whichshould be terminated in 2022.

Based on the termination consequences,termination is divided into 5 categories:

1. Termination I: It is happened pursuantto clause 41.2 (force majeure) or 49.3 (be-coming non economic due to amendmentto rules and legislations).

Consequence of the Termination: The I Partyis obliged to pay Basic Price of Termina-tion deducted by money amount of in-surance policy + excess amount if any.

2. Termination II: It is happened pursuantto clause 42.1(c) (natural Termination dueto the II Party fails to give Implementa-tion Security of asset maintenance) orclause 42.2 (Termination made by the IParty).

Consequence of the Termination: the I Party isoblilgated to pay Basic Price of Termina-tion deducted by fine and deducted by costof the I Party’s termination ...........

Termination made by the I Party if :

· A miss statement made by the II Party re-sulting that the CA is ilegal.

· Default of the II Party in a calendar yearreaching 70% of the Technical Target.

· Default of the II Party in making payment

to the I Party........· Default of the II Party in taking over re-

sponsibility on the contract in Clause19.3.· Share assigning (including all issance of ad-

ditional shares, loan security or procure-ment) other than the things that is pursu-ant to Clause 7.

3. Termination III: It is happened pursu-ant to clause 42.5 (Termination made bythe II Party)

Consequence of the Termination: The I Partyis obliged to pay Basic Price of Termina-tion added by Current Net Value (EBT)amounting to 50% of the remaining yearsbased on the average of 2-year historicalprofit and projection of the next 2-years.

Termination is made by the II Party if:

· Default of the II Party in receiving pay-ment.

· Action to private the I Party which makesthe II Party lossing out.

· The I Party is liquided.· A miss statment of the I Party resuting

that the CA is ilegal.· Unreached resolution of deviation on

devided income.

4. Termination IV: It is happened pursuantto clause 43 (option to purchase of the IParty after 10 years the CA has been run-ning or in 2007).

Consequence of the Termination: Basic Priceof the Termination added by Current NetValue of profit projection from 100% ofthe CA’s remainding years.

5. Termination V: It is happened pursuantto clause 42.1 (a) (when the period is ter-minated).

13

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

Some terminologies in termination:

1. Net Book Value: asset value (Rp) in ac-counting of the II Party.

2. Current Net Value: value (Rp) at the mo-ment when the calculation is made fromprojection of annual profit of the II Partyin the next time. Before tax with discountfactor 15%.

3. Basic Price of Termination : Net BookValue added by cost arising due to termi-nation.

Data of Net Book Value may be ex-cerpted from Ballance Sheets of the PrivateParty. Per December 31, 2005, for Palyja theNet Book Value of Fixed Asset amounts to

Rp. 644,761,756,833 of the total asset amount-ing to Rp. 1,232,835,146,823. and certantlyadded by PAM Jaya’s receivable due to short-fall amounting to Rp. 264,462,005,436.

Projection of profit may be obtainedfrom Schedule 6 on Consolidated FinancialProjection (Total Second Parties ProjectedRevenue Shares) deducted by OperationalCost in agreed Operational Expenditure.

As Palyja’s profit report before tax in2005 amounts to Rp. 84,459,714,445 and Rp.166,017,625,509 in year 2004. In the averageit amounts to Rp. 125,238,669,977. (+/- Rp.125 Billion)

The following table shows alteration oftermination and its consequence.

14

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

From the side of pocket cost, Termi-nation V is the cheapest cost, because thereis no termination cost. But we have to re-member that potential of shortfall will bemore and larger because water charge will al-ways raises whilst tariff increases uncertainly(particularly after period of Automatic Tar-iff Adjustment is ended, we have to remem-ber that there is many political interests andsocial resistance). Shortfall in the future isassumed to be covered by profit of one ofthe private party (if the CA is terminated thenprofit of the private party becomes profit ofPAM Jaya), because average of shortfall in ayear is almost the same as the average ofPalyja’s profit amounting to Rp. 125 billion.If profit of TPJ is the same with profit ofPalyja, accordingly opportunity cost for Ter-mination V is Rp. 125 billion multiplied with16 years of the CA remaining years or equalto Rp. 2 trillion. We have to remember thatsince semester II in 2003 the tariff average islarger than water charge, so that if the con-dition is continued the potential of profit willbe larger and as the consequence is that op-portunity cost letting the CA naturally endedin 2022 will be larger.

The next cheapest cost of terminationis Termination I and Termination II. PAMJaya only pays the Basic Price of Termina-tion and it is still deducted by cost or policyincome. Termination I is possible to be hap-pened if there is a force majeure resultingvarious impacts as described on Clause 41.1namely war, public riot, natural disaster,worker strike, radiation, nationalization, lackof material, lack of electricity power, press-ing and supersonic sound, and condition ofweather. In Termination I the most possi-ble event is force majeure of worker strikeor nationalization, such as through the Lawsof the Regional-Owned Enterprise that isarranged and states that PDAM must benationalized because it is related to the need

of large people. Termination II is possibleto be happened if the II Party for TPJ can-not reach 70% of the technical target andif the share assignment is not appropriateto the procedure as it is which legal conse-quence is run after. The above cost is stilldeducted by opportunity cost shortfallwhich is happened at the Termination untilending of the CA. Cost for Termination Iand II in gross is the cost of out of pocketdeducted by opportunity cost. Cost of outof pocket is value of Basic Price of Termi-nation which value is equal to net value ofthe asset added by loan of PAM Jaya oramounting to Rp. 644,761,756,833 added by

15

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

Rp. 264,462,005,436. total of out of pocketcost is about Rp. 910 billion. Such amountmust be deducted by opportunity cost whichvalue is equal to value of opportunity costof Termination 5 amounting to Rp. 2 tril-lion. So if we take Termination I or II thenthere will be profit amounting to Rp. 1.09trillion.

If the profit average before tax (EBT)of Palyja in 2004 and 2005 may be assumedas standard of profit projection of the twoparties in the future, then in every year theprivate partners will get profit amounting toRp. 250 billion.

Cost of out of pocket of TerminationIII consists of Basic Price of Terminationadded by Current Net Value for 8 years (re-maining period of the CA) deducted by op-portunity cost. Basic Price of Terminationamounting to Rp. 910 billion added by profitper year of the private partners amountingto Rp. 250 billion multiplied by 8 years anddeducted by opportunity cost which value isequal with opportunity cost of Termination5 amounting to Rp. 2 trillion. Cost of Ter-mination III amounts to Rp. 910 billion.

Cost of Termination IV (option ofPAM Jaya to buy back the share) is the mostexpensive due to beside the cost of Termi-nation V it shall be added by investment valuein 2006 net and the aggregate of Current NetValue is not for the 50% period of the CAbut for the 100% of CA remaining period orequal to 15 years. The opportunity cost is for15 years. Termination IV is the most expen-sive. Once trapped in involving private partythen share assignment prior to the CA’s ter-mination will be the most expensive cost..

Termination,Is it Possible?

Share assignment of TPJ in 2006-2007actually constitutes an important moment ifthe Government of DKI Jakarta throughPAM Jaya intends to terminate the CA. un-fortunately the Governor and formed Com-posite Team exactly seek various reasons toset straight the share assignment both by le-gal opinion of Amir Syamsudin & PartnersLegal Consultant that tries to re-construeArticle 7.2.c (the article contains multielucidations. What a pity the legal opinionstates that the shareholders has no relation-ship with the private partners’ professional-ism) and by setting straight the share assign-ment which is strengthened by the first party(PAM Jaya) trough a notary deed on 12 pre-requisite having no legal power. Includinginto the setting straight is the moment whenPAM Jaya and the Composite Team ask serv-ice of a Singaporean legal consultant to in-vestigate the new private partner. It is obli-gation of the new private partner to proveits reliability but not the first party trying se-riously to do it. If PAM Jaya is hesitatewhether on the new share holder’s hand TPJmanagement won’t be handled by profes-sional management having skill in businessof water management and whether the newshareholder has sufficient fund to, then ac-tually PAM Jaya may not issue approval andTermination II has been happened for thecase of TPJ.

Termination I is due to force majeureif the case of employment and its conse-quence is opened to all employees of PAMJaya who are assigned to assist and then theyrefuse this condition, it is potentially hap-pened. The followings are complete detailson employment problem of PAM Jaya, whoare assigned to assist the private partners.

16

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

Problem of Status of PAMJAYA’s EmployeesAssigned to assist PrivatePartners

One of problems faced by both theprivate partners and employees of PAM Jayais the status of PAM Jaya’s employee as-signed to assist the private parties. A Letterof Governor Number 1108/072 on resultof cooperation negotiation between PDAMJaya and the private partners to Chief ofDPRD of DKI Jakarta Province dated onApril 13, 2000 point 5 describing the prob-lem and the resolution which is (exactly)taken by the Governor.

Based on the CA dated July 6, 1997, alloperational employees of PDAM Jaya are au-tomatically assigned to assist the private part-ners with status as employee of PDAM Jaya.We don’t know whether based on whoseevaluation and when the evaluation is made,point 5 of the Letter of Governor states that‘In the field implementation there is oftenhappened an un-equivalence in treating be-tween employees of PDAM Jaya, assignedto assist the private partners and direct localemployees of the private parties, due to a du-alism treating upon the management systemof employee and management’.

The new Cooperation Agreement haschanged the system of employee managementinto single management. The private partnersagree to receive all employees with status ofpermanent without prejudice the employee’srights on employment, income, career oppor-tunity and the employees are asked to chooseone of the three options:

1. Become direct privat patners’ employee.2. To be Fully assisted by the private part-

ners but still hold NPP.

3. Voluntarilly resigns from the position withseparation pay.

The option is reconfirmed through In-struction of Governor of DKI Jakarta Prov-ince No. 94 of 2000 dated May 5, 2000 onImplementation of Single Management foremployees of PAM Jaya who are assistedthrough Employee Assignation with thereeoptions.

The amended and restated CA dated onOctober 22, 2001 at Article 36 on HumanResources detailly determines the status ofemployee. Article 36 on 32.2 and 32.3 dis-tinctively states that direct employee bothwith and without Identity Number is statedto be resigned as the employee of the FirstParty (PAM Jaya) and at the same time he/she is obliged to be re-employed by the Sec-ond Party. The difference between them isthat direct employee is entitled to receive ap-preciation money from PAM Jaya as well asthe private partner. Whereas the direct em-ployee with identity number receives appre-ciation money from PAM Jaya without ap-preciation money from private partner. Pur-suant to 32.6 PAM Jaya shall issue a letter ofdecision for the employee choosing one ofthe three options and shall give minutes ofthe employee surrendering and receiving andthe private party shall sign the work agree-ment with the direct employee and directemployee with identity number.

Article 32.12 regulates on Employee Re-Moving when the CA is terminated. Point astates that if PAM Jaya won’t employ a partof the private party’s employees then the pri-vate partner is entitled to continue employ-ing or discharging and giving separation fee.

Status of PAM Jaya’s employees whoare assigned to assist the private partners, inspite of there is an instruction of Governorand a regulation in the CA, until the report is

17

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

made (January 29, 2007) is still uncertain.PAM Jaya’s employee who are assigned toassist the private partners still assume thatthey are employees of PAM Jaya, whereasbased on an instruction of Governor and theCA it is clear that they are not employees ofPAM Jaya anymore. The floating status is as-sumed to be done in order to avoid the nextfluctuation if the status assignment is dis-tinctively and transparently stated to them.

Change of the PAM Jaya employees’status clearly has larger and further implica-tion for the employees. As employee of PAMJaya, they obey a Letter of Decree of Minis-ter of Home Affairs Number 34 of 2000on Guideline of Employment for RegionalEnterprise of Drinking Water/PerusahaanDaerah Air Minum (PDAM), and as em-ployee of private partner they have to obeyto regulation of Department of Manpower.

Some of the implication is that pursu-ant to Letter of Decree of Minister of HomeAffairs on Article 6 it is practically impossi-ble that an employee of PDAM is discharged.An employee is approved to resign or be dis-charged if :

1. Passes away.2. Proposes to resign upon his will.3. His/Her duty period is ended due to have

reached maximal age for the job namely56 years old.

4. He/She doe not comply with provision setout on Article 3 points c, d, g, h and i.

5. He/She has made PDAM losing out.

Article 3, point:c. He/She has never been sentenced in jail

based on Judgment of a Court having apermanent legal power.

d. He/She has never involved into any move-ment inconsistent with Pancasila and UUD

1945 and the State as well as the Govern-ment.

g. Having good conduct which is proven bya Certificate issued by local Police Depart-ment.

h. Having healthy body which is proven by aCertificate issued by a Physician.

i. At the same time may not be the employeeof other Company or as a Civil Servant ofthe State.

An employee of PAM Jaya clearly doesnot apply a working discharge only due tothe CA is terminated. Whilst as an employeeof private partner such work discharge con-stitutes a common condition. And the CAregulates the possibility of laying off afterthe CA is terminated.

Besides laying off, based on aforesaidLetter of Decree of Minister of Home Af-fairs, employee of PDAM shall also get vari-ous allowances as production service givenif at the closing of fiscal year, PDAM gainsprofit. (Article 9) and award both due to

18

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

working period and working achivement orpension period (Article 10). The provision isuncertain if the employee’s status is assignedinto an employee of the private partner.Moreover after the report is made there isno Collective Labor Agreement for the em-ployee working in for the privat partner.

The status of PDAM’s employees ingeneral is not Civil Servant. Pursuant to Ar-ticle 1 of Letter of Decree of Minister ofHome Affairs at point d states that “Em-ployee is PDAM’s Employee who are ap-pointed by and discharged by Board of Di-rectors”. If there is an employee he/she hasto be and assisted employee. But even thoughthey are not Civil Servant, status of PDAMemployees based on Letter of Decree ofMinister of Home Affairs, is not the same asemployees’ status of PDAM’s private part-ner. Directory Data of Perpamsi of 2006 stat-ing that 0 total of Civil Servant in DPD DKIJakarta is possible to be happened, even ithas to be checked whether there is Civil Serv-ant who is assigned to be employee of theprivate partner.

The above description shows that in-volving private party in manging PDAM asmodel in Jakarta, modified consession orOperate, Develop and Transfer has arisencomplicated problem on the employees whopreviously are the employee of PDAM bothfor the private partner and for the employeeof PDAM.

In the case happened in Jakarta Theprivate partner has a sophisticate thoughtabout the status of employee. Salary of thePAM Jaya’s employees who are assigned toassist or whose status is assigned into em-ployee of the private partner has been in-serted into component of water charge cal-culation with escalation formula. But the pri-vate partner does not estimate that status ofPAM Jaya employment makes them uneasy

to organize their employees because employ-ees of PAM Jaya as if obey to the two bossesand off course they prefer feel as employeeof PAM Jaya and obey to the boss, if theboss is exists and still in function and if it isnot in function they won’t fully obey to theprivate partners.

Development of employee status con-stitutes a deceit to the employees and publicand it may lose out the public due to theirunoptimal performance.

Conclusion andRecomendation

CA between PAM Jaya and private part-ners need to be considered to be terminatedas soon as possible in view of the privatepartners’ performance that is not differentwith and even turns down if it is comparedwith the condition prior to the CA, it is thefact that the private partners have clearly nofund, no security on the public interest to befullfilled and surplus on the private parties’profit.

19

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

The above description shows that thereare many problems in the CA that have beenamended and restated on October 22, 2001.There are 3 alterations to be taken:

1. PAM Jaya shall take termination on the CAwith its various alternatives.

2. To amend the CA in order to make it ba-lance between interests of public and theprivate partners.

3. To let the CA naturally terminated.

This part particularly will try to explainnecessary revision if the CA will be still con-tinued and its consequences if the CA is notrevised and naturally terminated in 2022.

Revision on the CA

The smoother step is by continuing theCA but the CA have to be revised. Chanceto revise the CA for TPJ is rather openedthrough a notary deed made for the shareassigning. It is a pity that the Composite Teamdoes not in duty or intentionally does not onduty to prepare in details the necessary revi-sion on the CA. The moment to utilize a goodbargaining position at the moment the TPJshare assignment but it is not well utilized.

One of the revision principles of theCA is an endeavor to balance the public andprivate interests. The endeavor to balancethem is by pressing the achievement on tech-nical target and service standard or by de-creasing protection on economic interest to

gain financial profit (IRR) with small risk forthe private partners or combination betweenthem.

Revision to the CA mentioned below isa part of the necessary revisions to be car-ried out. Deeper study on various aspects andknowledge should be made completely inorder to get a balance CA. One of the im-portant thing on the CA Jakarta, distinguish-ing it with other CA as Atlanta CA in whichthe First Party distinctively and explicitly givea job so that the First Party shall be domi-nant. It does not happen in Jakarta CA.

In related to the technical target, the im-portant thing is total of connections. Addi-tion of total new connections has to be ad-dressed to those who really need or in orderto prevent environmental degradation causedby excessive absorption of soil water. If pri-ority is for anyone who needs then the mar-ginal and poor groups shall be priority, if thedestroyer is prioritized then service to indus-try should be prioritized. Both have very dif-ferent implication. The need for quality in-dustry is not the same high with the need ofdomestic drinking water. For poor and mar-ginal group beside claim of quality is higherand the tariff is cheaper.

The priority determination is very im-portant because it directly results to the short-fall and to prevent addition of undirectedconnection. We have to remember that theprivate partners will have tendency to addconnections where water pressure can fulfillpressure service standard on the customerconnection.

WHAT SHOULD WE DOWITH THE COMPLICATED CA?

20

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

Other balance is that relating with pen-alty. As the example: penalty on a default tofulfill target of leakage. Formula in Attach-ment 15 for water loss level is Rp. 50 million(target of leakage deducted by realization)100. it means that for different of target is1% or 1/100 and penalty is Rp. 50 millionmultiplied by 1 and multiplied by 100 oramounting to Rp. 5 billion. If the target iswell arranged and implemented actually thepenalty is sufficient. The problem is thatwhether the target is arranged and imple-mented well or otherwise. Penalty for a newconnection is Rp. 10.000 per connection. Forthe example: addition for every end year (Seepoint 8.2.2 Indicative Technical Target, At-tachment 8):

The first to the second is 30.000 con-nections (281,607 deducted by 251,607). Ifit does not fulfill the target at all then totalof penalty is Rp. 300 million. The total is notmaterial. But the total of penalty shows thatPAM Jaya does not prioritize to add its totalconnetion. The second to the third is equalto the above conections.

· The third to the fourth is only 15.000 con-nections, and

· The fourth to the fifth is 35.000 connec-tions.

Total of the penalty does not supportthe private partners to prioritize the additionon the connection because additional targetis small and the pinalty is not significant.

Technical implementation of Penaltyshould be paid attention is anything relatingwith service standard. In case of water pres-sure, if three times consecutively the pres-sure on the customer’s point does not com-ply with the standard then the private partyshall be charged by penalty amounting to Rp.7 million per point of customer. Unfor-

tunatelly there is no explanation of who willmeasure and how about the frequence.Certaintly person who precisely knowswhether the pressure is stable or not is thecustomer not officer of PAM.

From the above sample we concludethat there are three main problems relatingwith fine and penalty: it is necessary to en-force the fine implementation for the fineappropriate to the priority of targerachivement as for water loss level, the fine istoo small for technical target or certaint serv-ice standard as total of connection and tech-nical implementation of monitoring. It isnecessary to be revised in the next CA (ifthere is a next CA).

Total of the fine properly multipled bytotal of the private partner’s profit. If on theaverage profit is Rp. 125 billion then the fineshall be suit particularly for the priority things.It means that if IRR is 22% then total fineshall be largerer accordingly if the privatepartners do not do anything to reach the tar-get it shall be certained that the private partywill suffer from loss, does not still gain profitas it does.

IRR shall be examined for its nature.Value of 22% is clearly excess for businesswith minimal risk as the CA. Level of IRR isa little above the interest rate of free risk asdeposit or the state promisory notes is aproper level for the private partners. As a tar-iff comparation determined on Regulationof Minister of Home Affairs No. 2 of 1998on Guideline for Stipulation of DrinkingWater Tariff at PDAM and Instruction ofMinister of Home Affairs No. 8 of 1998 onGuideline for Implementation of Stipulationon Drinking Water Tariff at PDAM, the high-est tariff is level of full cost of Return onTotal Assets determined at 10%. It is withnote that majority of consumers is not at levelof full cost. It is important to study whether

21

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

IRR of the private partners could be madein appropriate to the Regulation of Ministerof Home Affairs mentioned above.

In order to avoid financial speculationas in case of share assignment. It is usefulthat imprtant financial ratios as Debt to Eq-uity Ratio shall be attached on the CA andthe Attachment shall not be treated as it isdone by Palyja which with capital of Rp. 200billion it gains profit for 8 year operation,amounting to more than the capital and allinvestment of its fixed assets is still financedby loan.

Operational Expenditure and CapitalExpenditure have important role. Thereforethey are should be arranged accurately todetail what point should be inserted and whenit should be carried out and what standardwill be applied. Signal of salary for expatri-ate employee, know how fee, and cost of loansecurity should not be happened if opera-tional expenditure is well arranged and theimplementation is enforced. As well as thesecurity amounting to USD 15 million writ-ten on the notary deed of TPJ share assign-ment shall not be necessary if the implemen-tation of capital expenditure is well arrangedand enforced. Fines for operational expendi-ture and capital expenditure are properly anddirectly related to deduction of escalationpercentage of water charge or other incen-tive-based compensation.

Operational expenditure and capital ex-penditure will only be well monitored if onlythere is a transparency. What a pity that thetransparency determined on Clause 35 onAdministration has never been implemented.

The other matter to be changed is esca-lation formula on water charge and offcourses its initial water. It is not fair if allrisks are inserted into escalation formula onwater charge, as change on currency and in-

terest rate. Moreover at this time Palyja loanis in rupiah obligation, not in USD or othercurrency.

Other necessary change is clause on ter-mination. It is proper that mistake of theprivate partners shall be applied when termi-nation is implemented. It may be percentationof discount on Basic Price of Terminationin order that private partner will not termi-nate the CA in whatever way. Important noteis also investment feasibility. PAM Jaya shallreally carry out audit whether investmentvalue is really the same as it is reported bythe private partner. Share sale of the privatepartner should give a pre-emptive change toPAM Jaya to buy, not with protection ofClause 43 indicating that the private partnerunwishes PAM Jaya to buy back its shares.

Role of Regulator Body must be revisedin the next time. And off course not in theCA. ideal role of the Regulator Body is as itwhich is implemented in England with itsOfwat, how to make profit of the privatepartners is proper and not burdened by inef-ficiency for management.

22

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE

The heavy homework is anything relat-ing with employee status, how the CA cansecure the employees assigned to assist arestill motivated and can be managed by pri-vate partners. Qualification for professionalmanagement of private partner if it is com-plied perhaps will decrease such problem.

There are still many other necessarychanges in order not to use legal opinion oflaw office for each article on the CA as Clause7.2.c.

The following table covers the articleson the CA and the possibility to revise thatpart of them have been described above.

Continue the CA

In such condition desribed above, it isa deceit or public cheating if the CA is stillcontinued. It is our collective role to makeimportant the pressure in order to revise theprivate partners involvement into clean wa-ter sector in Jakarta.

If the CA is continued there will bemany victims as employees of PAM Jaya as-signed to assist, costumers and poor peoplewhich have not been serviced. The CA willonly be profit for the private partners.

23

ANALYSIS ON BUSINES ASPECT AND HUMAN RESOURCE