credit profile and rating migration of iron and steel industry in latin america

TRANSCRIPT

CREDIT PROFILE AND RATING MIGRATIONIRON AND STEEL

INDUSTRY IN LATIN AMERICA

ABHINAV GARG

ROLL NO 954

CREDIT PROFILE

WHAT IS A CREDIT PROFILE?

• A credit profile is a document which provides information about a person’s or a business entity’s credit history.

• Credit profiles are used by lenders and other agencies which offer credit to determine creditworthiness.

• They are also utilized by prospective landlords and other people who might have an interest in an entity’s credit history.

• A good credit profile will make it easier for someone to access credit, and a bad credit profile can become a major stumbling block.

WHAT DOES A CREDIT PROFILE CONTAIN?

• The profile includes a complete history of the credit accounts someone has open or has held in the past, along with information about their limits, the balances carried on them, and the person's payment history.

• The maximum ever carried on each account will be listed, as will information about late or incomplete payments. Old accounts are eventually dropped from a credit profile after a set number of years, classically seven.

• A credit profile also often includes information about someone's employment history, along with listings of any inquiries made about someone's credit.

• If, for example, someone takes out a loan to buy a car, the inquiry from the lender will show up on his or her credit profile, and another lender will be able to see that an inquiry was made. The inquiry history may be used to determine whether or not credit was granted to someone, or to alert the person reviewing the credit profile to the fact that a new credit account may be in the process of being opened.

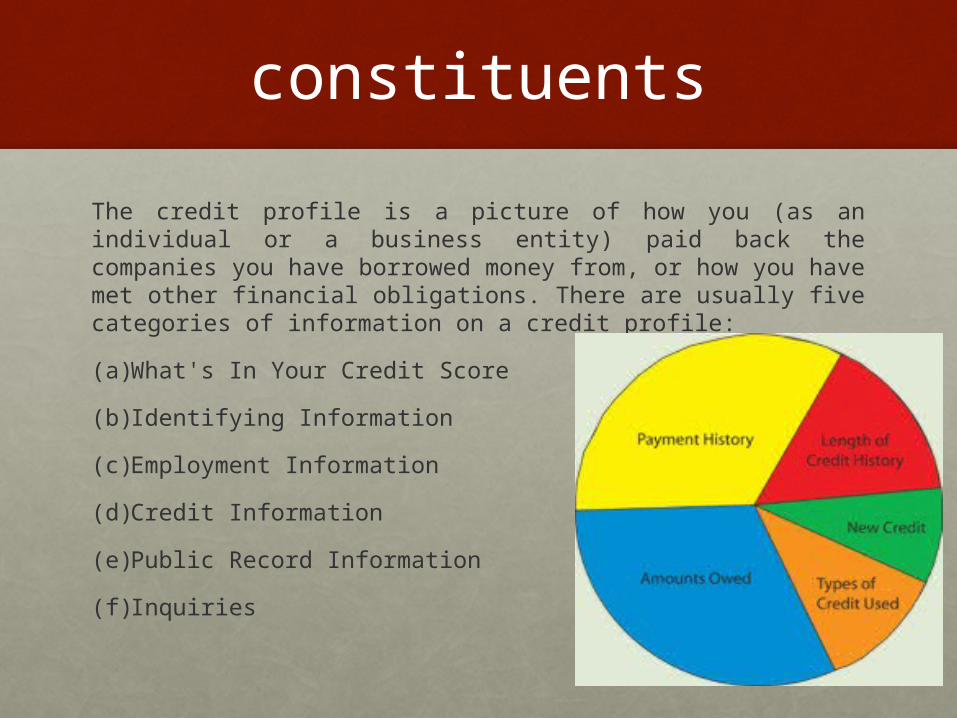

constituents

The credit profile is a picture of how you (as an individual or a business entity) paid back the companies you have borrowed money from, or how you have met other financial obligations. There are usually five categories of information on a credit profile:

(a) What's In Your Credit Score

(b) Identifying Information

(c) Employment Information

(d) Credit Information

(e) Public Record Information

(f) Inquiries

WHO CAN HAVE A CREDIT PROFILE?

• Credit profiles can be found for individuals and businesses.

• People who are just starting businesses should take steps to create a separate business profile. This ensures that personal credit black marks will not count against the business, and it can generate access to business loans and other types of accounts which are only open to businesses, not to individuals.

• Both business and personal profiles should be regularly reviewed for errors, and if errors are identified, a request for correction should be filed.

HOW TO BUILD A CREDIT PROFILE?

• The best way to build up a credit profile is to keep current on all credit accounts, making payments on time and in the amounts required, or in excess of the minimum.

• It is also a good idea to avoid carrying a balance in excess of 50% of someone's available credit on a revolving credit account, and to avoid opening two many revolving credit accounts, as this can make someone look like a credit risk.

• Consumers should be aware that agencies which claim to “fix” someone's credit are often highly questionable, as usually activities which alter a credit profile can only be undertaken by the person whom the profile concerns.

CONSTITUENTS OF A CREDIT PROFILE

• There are generally five constituents of a credit profile of a person or a business entity. These 5 categories are listed below:

1. Payment History

2. Amounts Owed

3. Length of Credit History

4. New Credit

5. Types of Credit Used

WEIGHTAGE OF CONSTITUENTS IN A CREDIT PROFILE

Rating Migration

• Credit Rating Transition is the migration of a debt instrument from one rating to another rating over a period of time.

• This migration is either an upgrade or a downgrade from an existing rating.

• This movement indicates the change in the credit quality of the instrument assessed by the rating agency.

• Agencies such as S&P’s, Moody’s and Fitch assess the credit quality of all the debt instrument in their portfolio and assign a rating to the credit quality. This rating changes as and when new information is available about the obligor's financial health.

IRON AND STEEL INDUSTRY IN LATIN AMERICA

overview

• The iron and steel sector was one of the hardest hit by the global crisis, with a 24% fall in iron and steel consumption.

• In recent years, production of steel in Latin America grew an average 4.4% per year.

• Given the size and importance of iron and steel companies, governments have always paid attention to this sector.

• Latin America’s appallingly inadequate infrastructure spending also manifests in its per capita annual consumption of steel, a major raw material for the infrastructure sector.

overview

• In Latin America, Brazil concentrates 51% of production of steel, while Mexico produces 27%, followed by Argentina (8%) and Venezuela (6%).

• Brazil is the main steel exporter in Latin America, ranking 13th place worldwide. It is also the main world exporter of iron.

• FDI in iron and steel is also concentrated in Brazil and Mexico. In Brazil it amounts to 28% of total FDI in manufacturing and in Mexico 17%. FDI flows to this sector is explained by growing demand, opportunities to buy companies being privatized, lower production costs and the search for natural resources.

companies

• The major players in the iron and steel industry in the region of Latin America are –

• Vale, the global mining behemoth;• Gerdau SA, the world’s 14th largest and Latin

America’s largest steelmaker;• Subsidiaries of ArcellorMittal in Latin America.

Vale SA

• Vale, with total iron ore reserves of about 14 billion metric tons, is the largest iron ore producer in the world. A $150 billion diversified mining company, it has the capacity to produce about 400 million tons of iron ore a year and accounts for more than 80% of Brazil’s total iron ore exports.

• Headquartered in Rio de Janeiro, Brazil, Vale is one of the largest mining enterprises in the world, with substantive positions in iron ore, nickel, copper, and coal, as well as supplemental positions in energy production and positions in steel production.

• Although the firm is a mining giant - with nickel, coal, aluminum, copper and coal production as well as logistics units - iron ore mining is its largest business and generates more than 60% of its revenues.

• For the twelve months through December 31, 2013, Vale had net operating revenues of $46.8 billion.

Corporate credit rating

• In April 2014, Moody's Credit Rating Agency changed the rating outlook for Vale S.A. (Vale) to positive from stable.

• The change in outlook to positive from stable acknowledges Vale's more focused and disciplined approach to project development, capital allocation, resizing of its asset portfolio to strategically important business segments, divestiture of such non strategic assets, and focus on cost reduction.

• This is exemplified by the company's reduction in research and development costs in 2013 by approximately 45% to around $663 million, reduction in capital expenditures by about $2 billion to around $14.2 billion, and overall reduction in production and general costs, although some benefit in these last areas was derived from favorable currency movements, which might not be sustainable.

• Vale's Baa2 global local currency rating reflects the company's diversified product base, strong coverage ratios, and competitive cost position.

• However, the rating considers the challenges that will continue to impact the company's operating cost profile, particularly for labor as well as increasing royalties.

• The rating also incorporates the volatility in iron ore and metal prices (copper and nickel) as well as metallurgical coal and fertilizers, and Vale's earnings and cash flow sensitivity to movement in these prices of its key minerals, particularly iron ore given the dominance of this segment in the overall performance of the company.

• Vale's rating could be favorably impacted should the company maintain or reduce absolute debt levels over the next 15 months, successfully complete its major capital expansion projects without significant cost overruns, maintain operating cash flow minus dividends to debt of at least 30%, and free cash flow to debt in the 10% range, at a minimum.

• Further considerations would include greater clarity with the company's acquisition strategy and financial policies. A further consideration would be the Brazilian Governments foreign currency bond rating.

Gerdau S.A.

• Gerdau SA is a Brazil-based holding company engaged in the manufacture and sale of steel products. The Company produces long steel and flat steel items, principally through the process of fabrication in electrical furnaces from scrap metal and purchased pig iron, as well as by manufacturing steel from iron ore in the blast furnace and by direct reduction.

• Gerdau is the world’s 14th largest steelmaker and the largest producer of long steel in the Americas. It has 337 industrial and commercial units and more than 45,000 employees across 14 countries.

• Gerdau's core business is to transform steel scrap and iron ore into steel products.

• Gerdau is a leading producer of long steel in the Americas and one of the largest suppliers of special steel in the world.

• It is the largest recycler in Latin America and around the world it transforms, each year, millions of metric tons of scrap into steel, reinforcing its commitment to sustainable development in the regions where it operates.

• With more than 140,000 shareholders, the Company is listed on the stock exchanges of São Paulo, New York and Madrid.

Credit rating

• Despite a weak scenario for the global steel industry, Gerdau S.A. has maintained adequate cash flow generation.

• Reuters provided 'BBB-' global scale and 'brAAA' national scale ratings on Gerdau.

• The ratings on Gerdau reflect the assessment of the company's "satisfactory" business risk profile and "intermediate" financial risk profile. The supporting factors are Gerdau's adequate geographic diversification throughout the Americas, the company's still-favorable cost position in Brazil, its efficient operations overall, and its "strong" liquidity.

• Offsetting these rating strengths are Gerdau's exposure to the cyclical, commodity-oriented, long-steel industry; the fierce competition from imports; and the potentially challenging market conditions in the next 12 months to 18 months.

• Gerdau holds a strong market position in Brazil and benefits from geographic and product diversification in the steel industry in the Americas.

• The company has expanded in specialty steel markets globally. This segment accounted for about 25% of Gerdau's consolidated EBITDA in the last 12 months.

• The recent decline in raw material prices (especially iron ore and metallurgical coal for the company's Ouro Branco mill and scrap for its mini-mills in Brazil and in the U.S.), as well as cheaper energy costs (gas in the U.S. and lower taxes on energy purchases in Brazil) should help offset the competitive pressures and result in some margin improvement through 2013.

• Still, there's believe that import competition in Brazil will likely remain a continuous threat to Gerdau, either active or latent, keeping margins down through the period even under a relatively weaker currency. In North America, demand is improving with positive growth in the nonresidential segments, but it remains volatile because of uncertain market conditions.

• The stable outlook reflects Reuter’s opinion that Gerdau will sustain its debt reduction trend during the next two to three years--even if margins remain depressed during the next 12 months to 18 months.

Conclusion

• Looking at the credit rating for two of the largest iron and steel producing companies in Latin America, we can observe the rising trend in the market.

• The countries in Latin America are developing at a very fast rate, which requires huge expenditure on infrastructural projects. Infrastructure can not be made without the use of iron and steel. Thus, matching the demand and supply in itself linked to the credit rating of these iron and steel companies in Latin America.

• Apart from use of their products in their domicile countries, these companies also export iron and steel, due to rich reserves.

• These are just a few points which influence the credit rating agency's calculations. Giving BBB- and BBB+ rating to these companies reflect strong credit rating for any company at this global level.

Thank you