credit chapter 10 credit you’re in charge what’s ahead 10.1 what is credit? 10.2 how to qualify...

TRANSCRIPT

CHAPTER 10

CREDITCREDITYou’re In ChargeWHAT’S AHEAD10.1 What Is Credit?10.2 How to Qualify for Credit10.3 Sources of Consumer Credit10.4 Credit Rights and Responsibilities10.5 Maintain a Good Credit Rating

Slide 2

Chapter 10

LESSON 10.1

What Is Credit?GOALSGOALSIdentify reasons to borrow and the trade-offs

you make when you borrowDiscuss how to plan when and how much to

borrow

Slide 3

Chapter 10

Why Borrow?For your goalsFor a home

A home as an investmentEquityTaxes and homeownership

For your educationInvesting in yourself

For your health

Slide 4

Chapter 10

Plan Your Borrowing

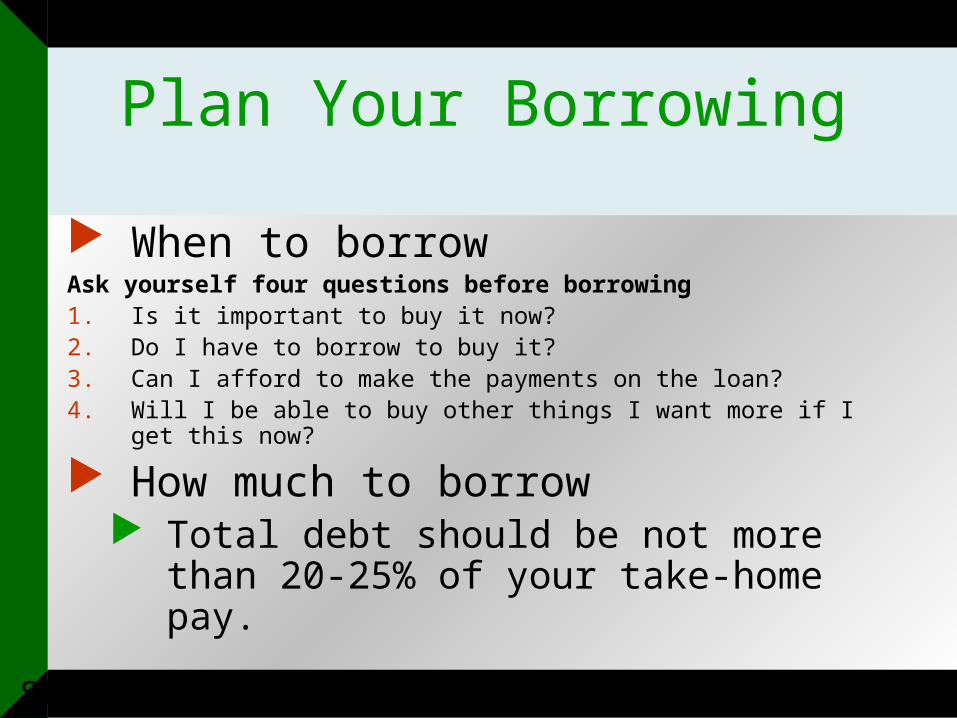

When to borrowAsk yourself four questions before borrowing1. Is it important to buy it now?2. Do I have to borrow to buy it?3. Can I afford to make the payments on the loan?4. Will I be able to buy other things I want more if I get this now?

How much to borrow Total debt should be not more than 20-25% of

your take-home pay.

Slide 5

Chapter 10

LESSON 10.2

How to Qualify for CreditGOALSGOALSExplain how lenders judge your

creditworthinessDescribe the factors that go into your

credit rating

Slide 6

Chapter 10

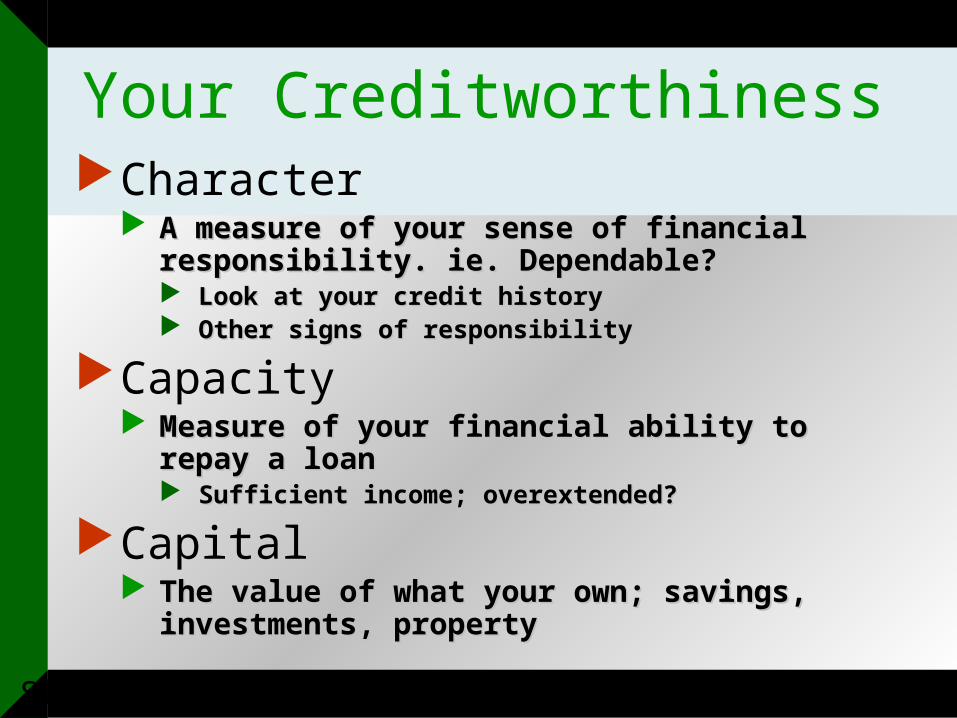

Your CreditworthinessCharacter

A measure of your sense of financial responsibility. ie. A measure of your sense of financial responsibility. ie. Dependable?Dependable? Look at your credit historyLook at your credit history Other signs of responsibilityOther signs of responsibility

Capacity Measure of your financial ability to repay a loanMeasure of your financial ability to repay a loan

Sufficient income; overextended?Sufficient income; overextended?

Capital The value of what your own; savings, investments, The value of what your own; savings, investments,

propertyproperty

Slide 7

Chapter 10

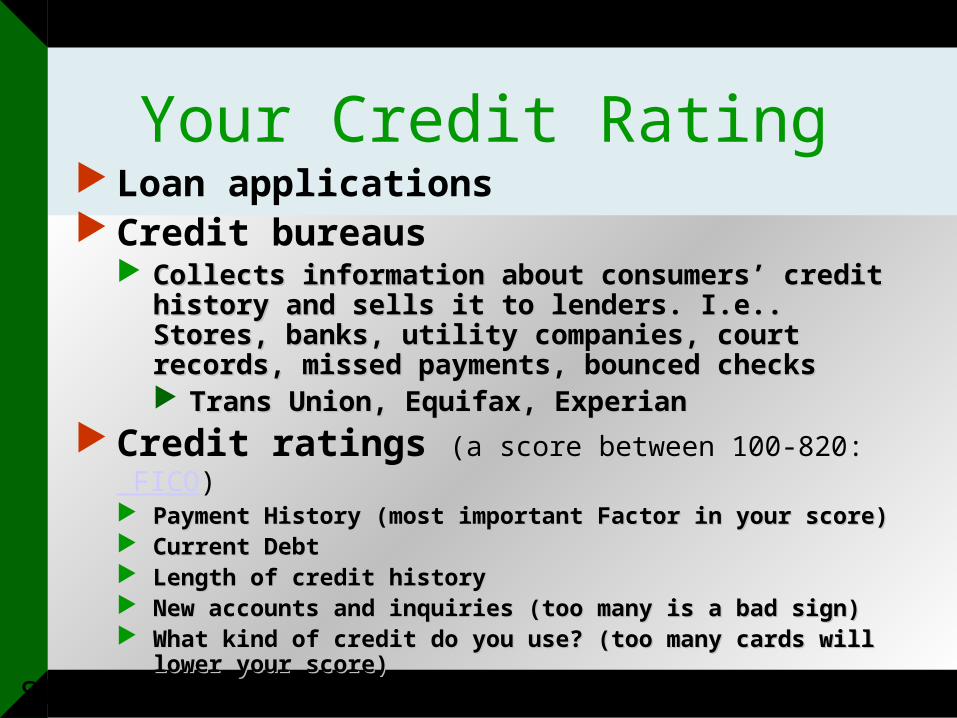

Your Credit Rating Loan applications Credit bureaus

Collects information about consumers’ credit history and Collects information about consumers’ credit history and sells it to lenders. I.e.. Stores, banks, utility companies, sells it to lenders. I.e.. Stores, banks, utility companies, court records, missed payments, bounced checkscourt records, missed payments, bounced checks Trans Union, Equifax, ExperianTrans Union, Equifax, Experian

Credit ratings (a score between 100-820: FICO) Payment History (most important Factor in your score)Payment History (most important Factor in your score) Current DebtCurrent Debt Length of credit historyLength of credit history New accounts and inquiries (too many is a bad sign)New accounts and inquiries (too many is a bad sign) What kind of credit do you use? (too many cards will lower your score)What kind of credit do you use? (too many cards will lower your score)

Slide 8

Chapter 10LESSON 10.3

Sources of Consumer CreditGOALSGOALSIdentify different options for getting creditDescribe the benefits and costs of credit

cards

Slide 9

Chapter 10Types of Consumer Borrowing

Secured loan (backed by something of value)

CollateralCollateral: property pledged to back a loan: property pledged to back a loan Installment loanInstallment loan: repaid in a certain number of : repaid in a certain number of

payments with a certain interest rate. payments with a certain interest rate. (also called (also called closed-end closed-end creditcredit. One time, one amt. loan). One time, one amt. loan)

Unsecured loan (not backed by collateral)

Grants credit based on your creditworthiness aloneGrants credit based on your creditworthiness alone Usually pay a higher interest rate than secured loan Usually pay a higher interest rate than secured loan

because greater riskbecause greater risk

Slide 10

Chapter 10

Sources of LoansBanking institutions

Shop around for best interest rate, fees, other costs.Other sources

Finance companies (higher rates than banks)Life insurance companiesCredit card cash advances (17-24% interest rate)PawnbrokersRent-to-own companies (not a good deal: p.343)

Slide 11

Chapter 10

Credit Cards Regular charge accounts

Must pay balance in full each monthMust pay balance in full each month American Express, Diner’s ClubAmerican Express, Diner’s Club

Revolving charge accounts Can carry a balance each month; pay interestCan carry a balance each month; pay interest

Sources of credit cards VISA, American Express, MasterCard, DiscoverVISA, American Express, MasterCard, Discover Others: charities, gas companies, universitiesOthers: charities, gas companies, universities

Credit card incentives Free gas, airline miles, car discounts, cash back, purchasesFree gas, airline miles, car discounts, cash back, purchases

Slide 12

Chapter 10

Slide 13

Chapter 10

Age Debt Age Debt

18-29 $8,636 50-59 $20,157

30-39 $16,298 60-69 $15,964

40-49 $18,659 70+ $6,500

Slide 14

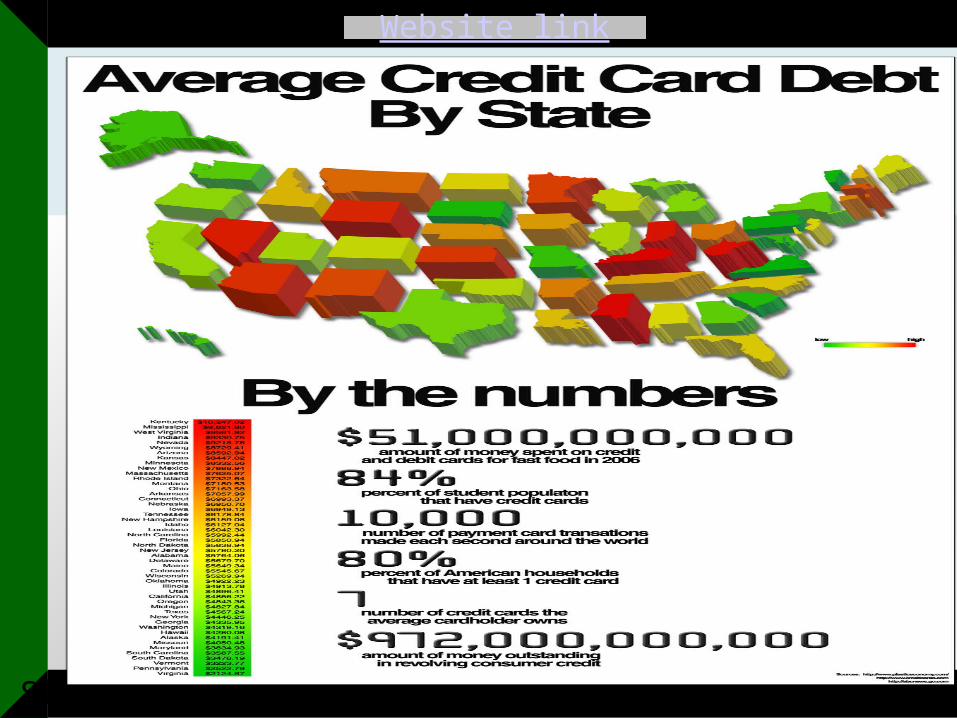

Chapter 10 Website link

Slide 15

Chapter 10

Slide 16

Chapter 10

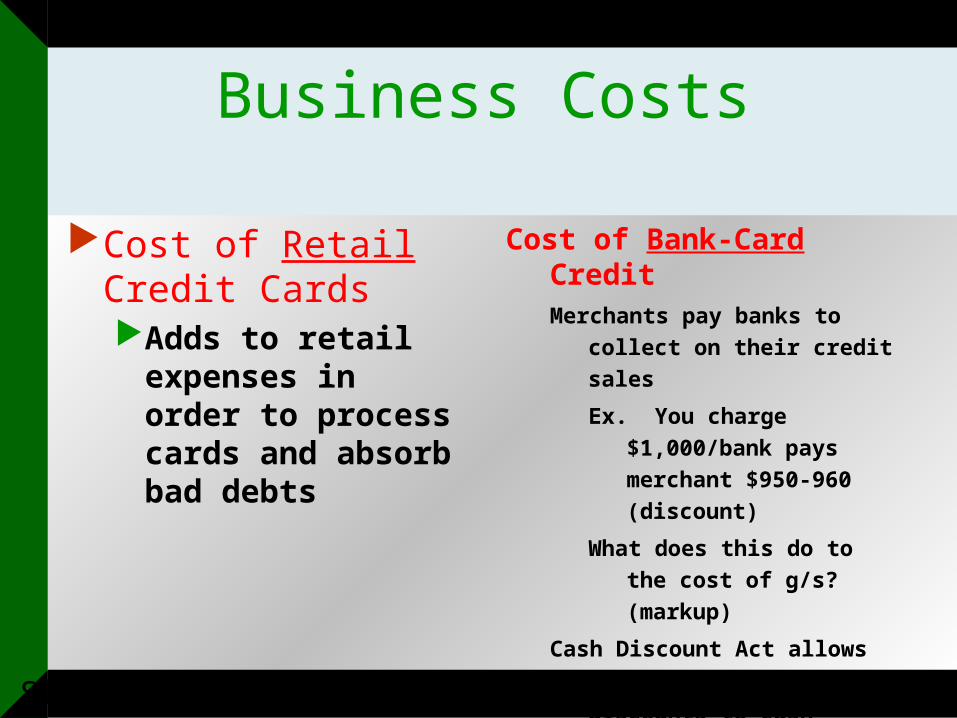

Business Costs

Cost of Retail Credit CardsAdds to retail expenses

in order to process cards and absorb bad debts

Cost of Bank-Card CreditMerchants pay banks to collect on

their credit sales

Ex. You charge $1,000/bank

pays merchant $950-960

(discount)

What does this do to the cost of

g/s? (markup)

Cash Discount Act allows merchants

to give discounts to cash

customers

Slide 17

Chapter 10

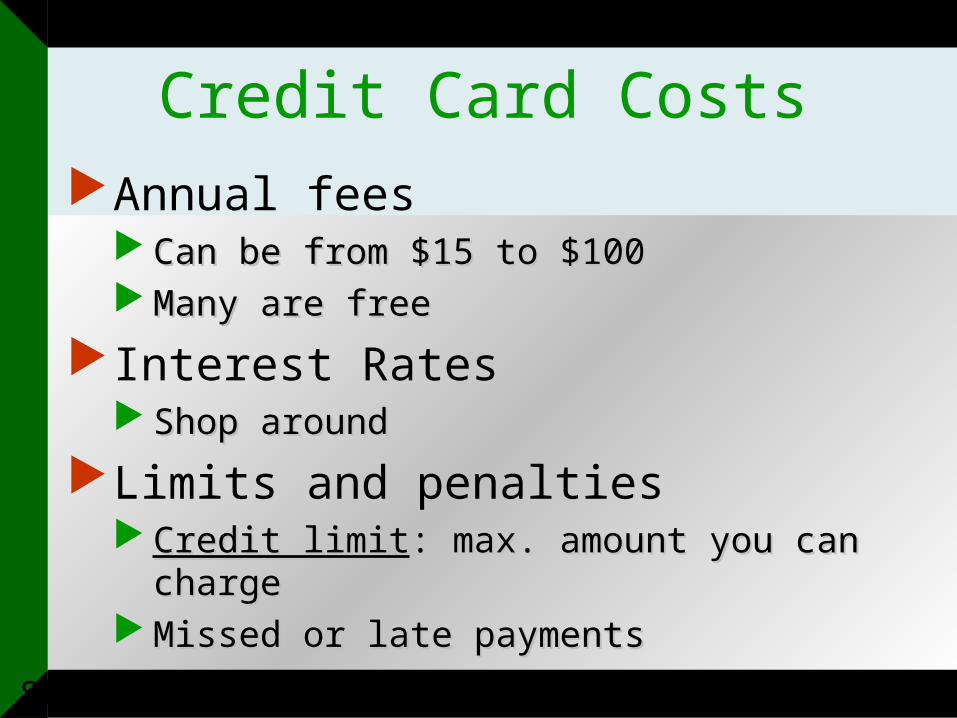

Credit Card CostsAnnual fees

Can be from $15 to $100Can be from $15 to $100 Many are freeMany are free

Interest Rates Shop aroundShop around

Limits and penalties Credit limitCredit limit: max. amount you can charge: max. amount you can charge Missed or late paymentsMissed or late payments

Slide 18

Chapter 10

Slide 19

Chapter 10

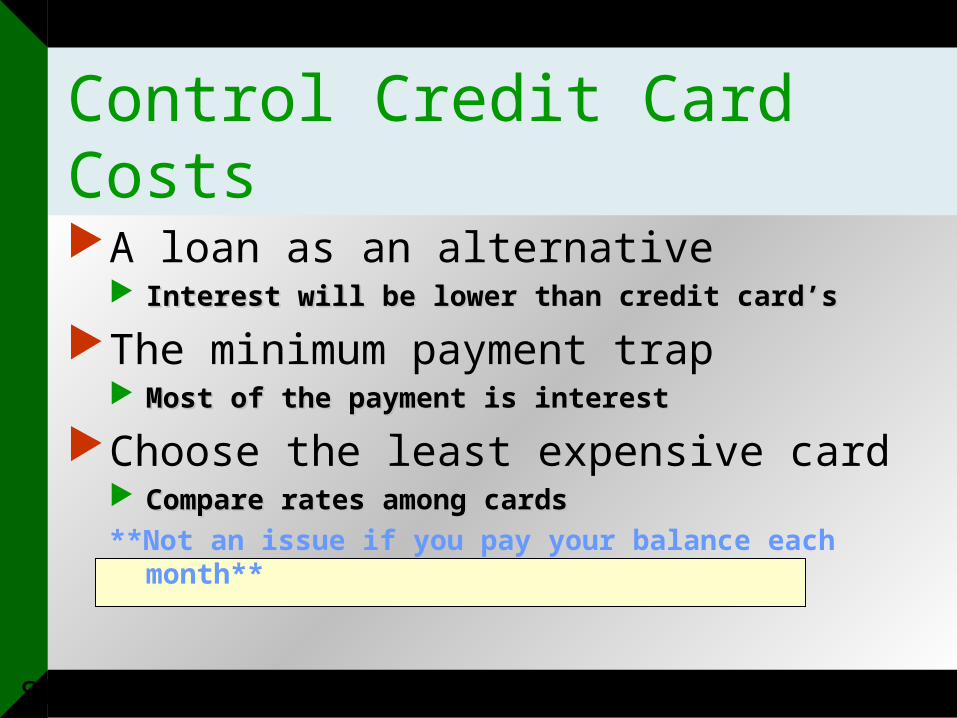

Control Credit Card CostsA loan as an alternative

Interest will be lower than credit card’sInterest will be lower than credit card’s

The minimum payment trap Most of the payment is interestMost of the payment is interest

Choose the least expensive card Compare rates among cardsCompare rates among cards

**Not an issue if you pay your balance each month**

Slide 20

Chapter 10

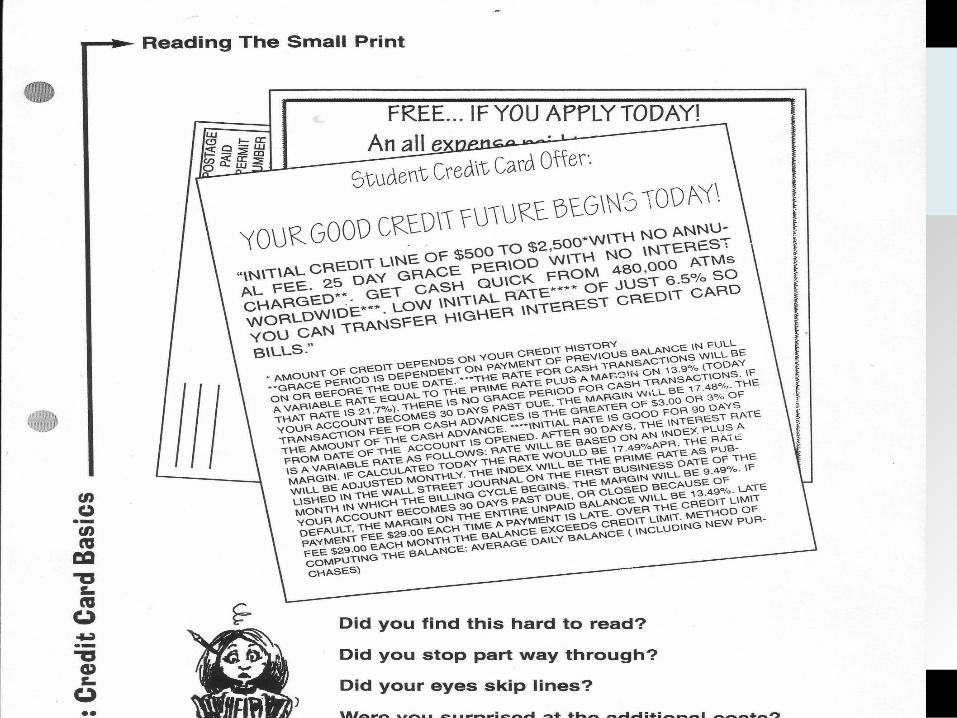

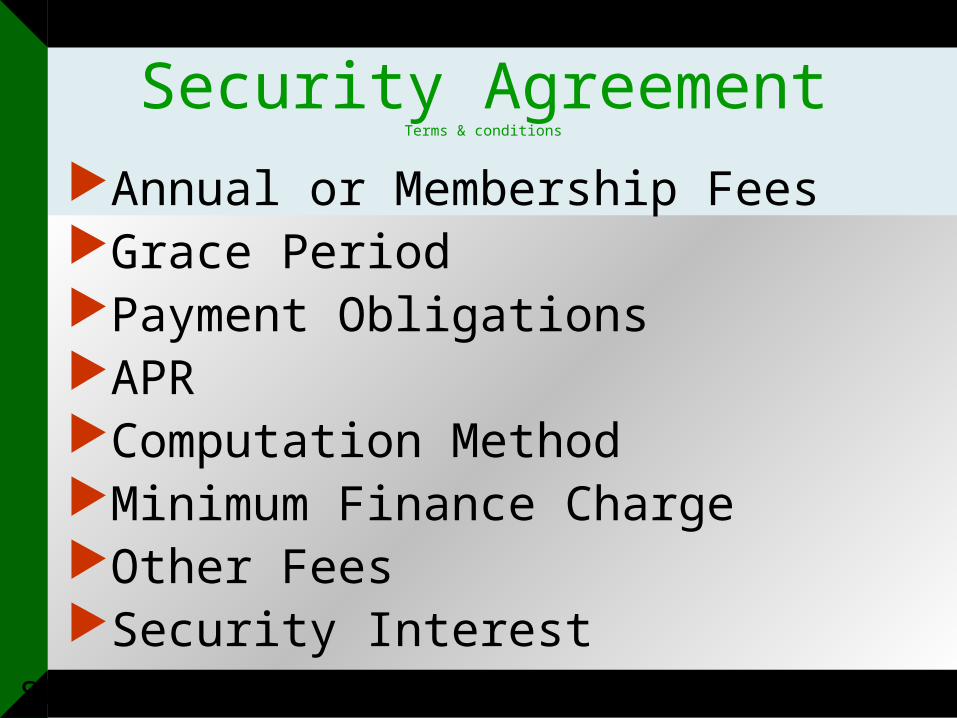

Security AgreementTerms & conditions

Annual or Membership FeesGrace PeriodPayment ObligationsAPRComputation MethodMinimum Finance ChargeOther FeesSecurity Interest

Slide 21

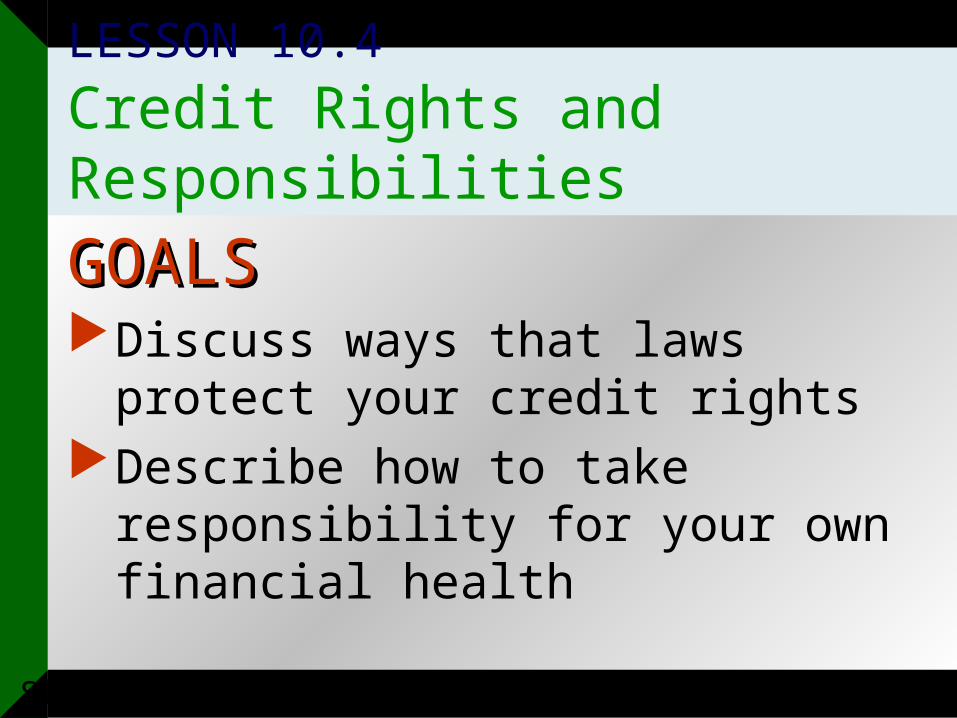

Chapter 10LESSON 10.4

Credit Rights and Responsibilities

GOALSGOALSDiscuss ways that laws protect your credit

rightsDescribe how to take responsibility for your

own financial health

Slide 22

Chapter 10

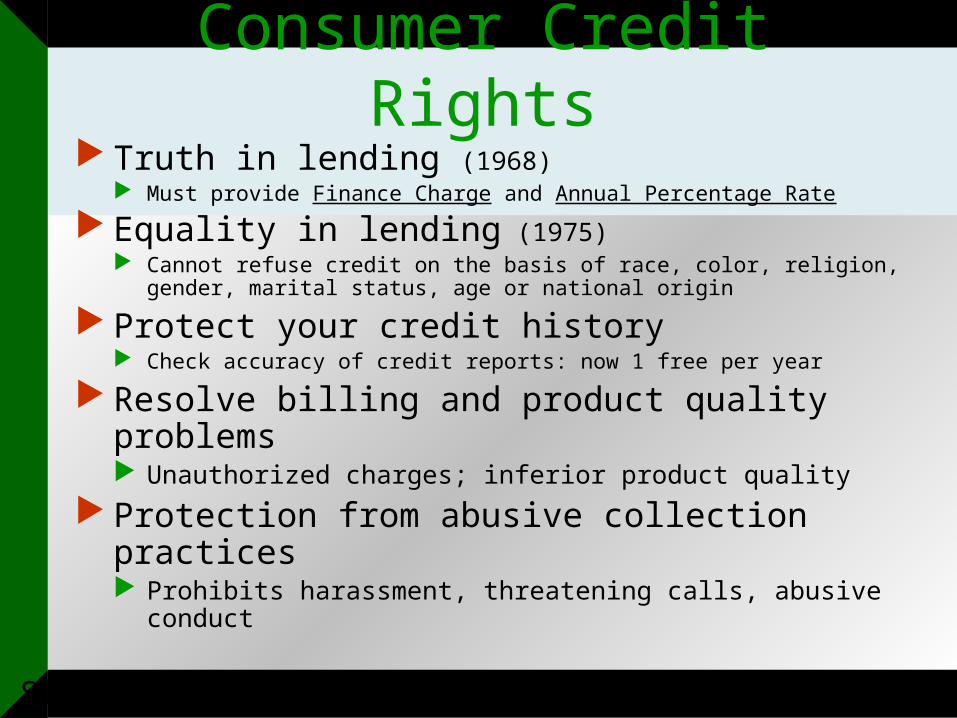

Consumer Credit Rights Truth in lending (1968)

Must provide Finance Charge and Annual Percentage Rate

Equality in lending (1975) Cannot refuse credit on the basis of race, color, religion, gender, marital

status, age or national origin

Protect your credit history Check accuracy of credit reports: now 1 free per year

Resolve billing and product quality problems Unauthorized charges; inferior product quality

Protection from abusive collection practices Prohibits harassment, threatening calls, abusive conduct

Slide 23

Chapter 10 Consumer Credit Responsibilities

Accept responsibility Know your debt capacity Credit and family Self-control with credit

Pay more than the minimum Avoid too many credit cards Pay cash Keep accurate records

Pay your balancePay your balanceEach month Each month

AndAndYou won’tYou won’tHave anyHave anyProblems!Problems!

Slide 24

Chapter 10LESSON 10.5

Maintain a Good Credit RatingGOALSGOALSExplain how to establish a positive credit

historyDiscuss how to avoid credit problems and

how to get help if you need it

Slide 25

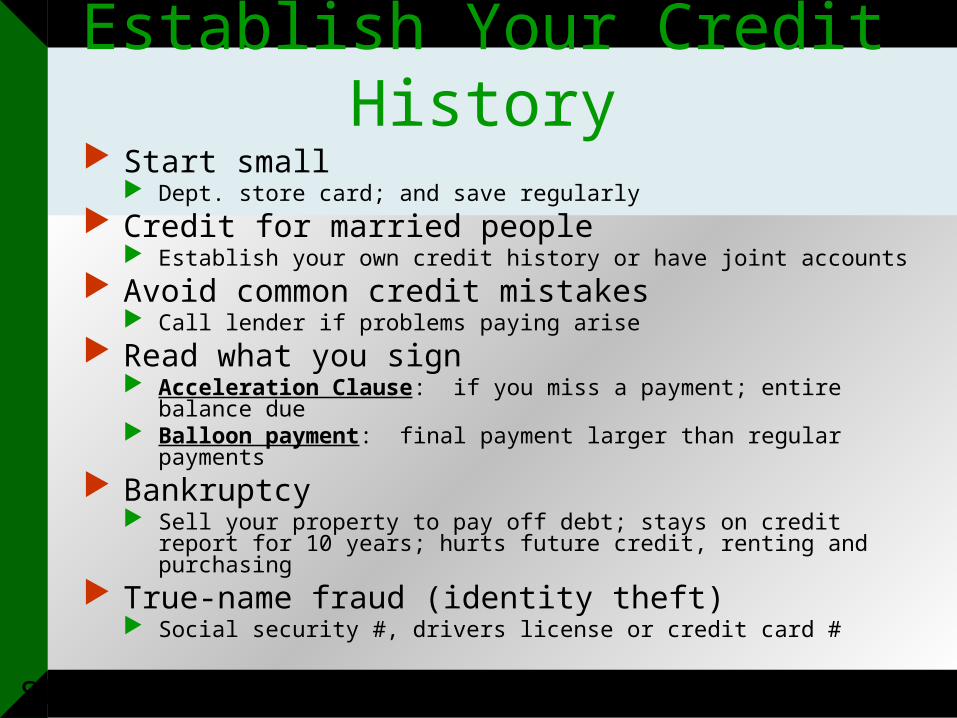

Chapter 10Establish Your Credit History

Start small Dept. store card; and save regularly

Credit for married people Establish your own credit history or have joint accounts

Avoid common credit mistakes Call lender if problems paying arise

Read what you sign Acceleration Clause: if you miss a payment; entire balance due Balloon payment: final payment larger than regular payments

Bankruptcy Sell your property to pay off debt; stays on credit report for 10 years; hurts

future credit, renting and purchasing True-name fraud (identity theft)

Social security #, drivers license or credit card #

Slide 26

Chapter 10

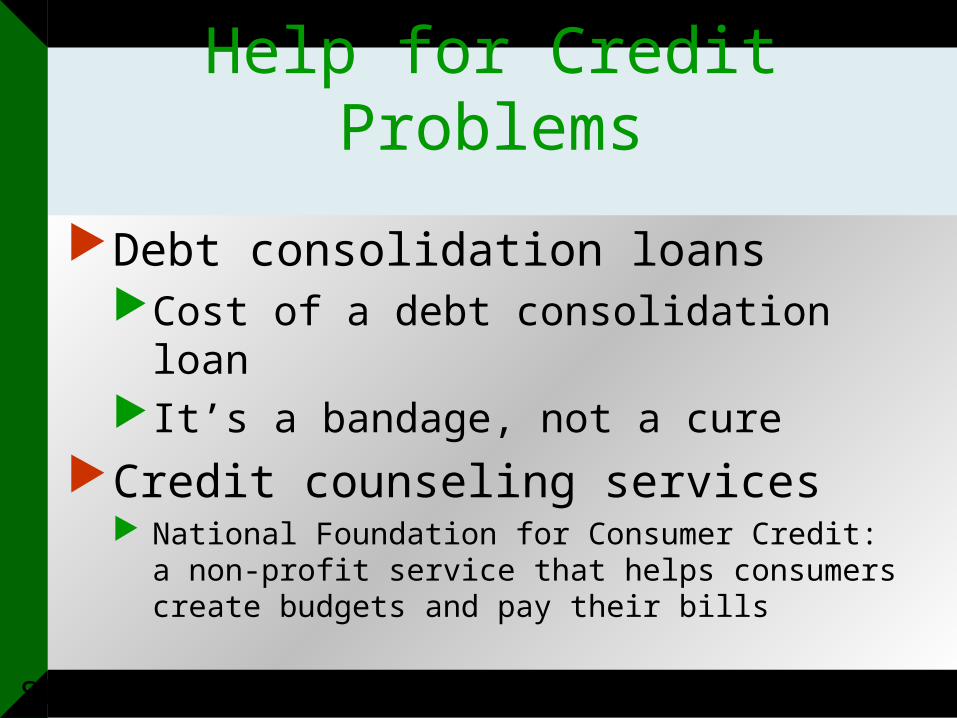

Help for Credit Problems

Debt consolidation loansCost of a debt consolidation loanIt’s a bandage, not a cure

Credit counseling services National Foundation for Consumer Credit: a non-profit service

that helps consumers create budgets and pay their bills

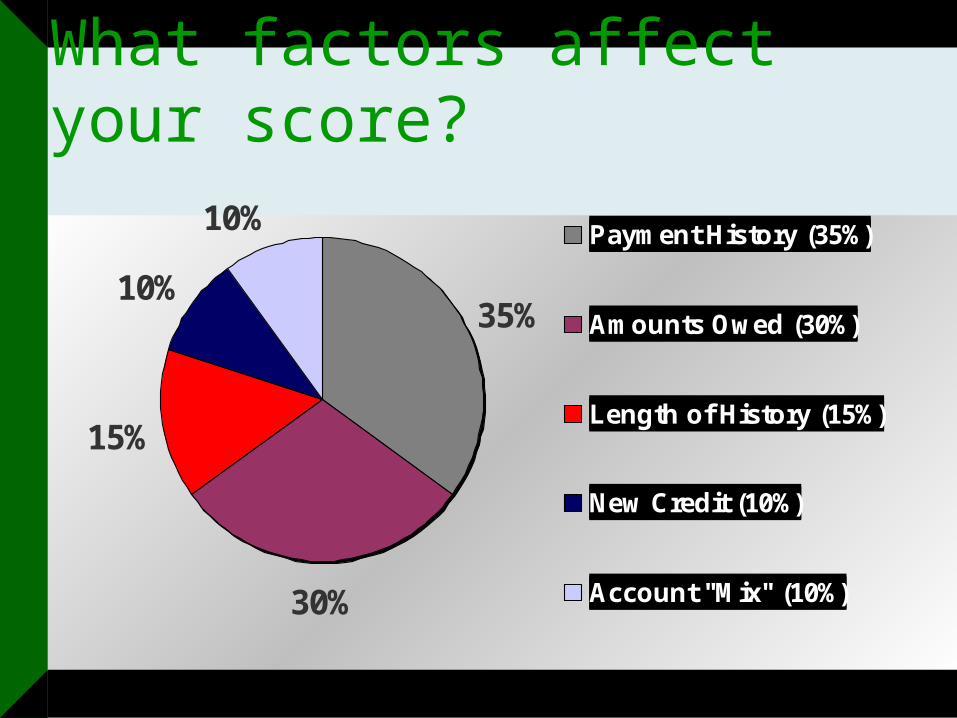

Chapter 10What factors affect your score?

35%

30%

15%

10%

10%Payment History (35%)

Amounts Owed (30%)

Length of History (15%)

New Credit (10%)

Account "Mix" (10%)

Chapter 10

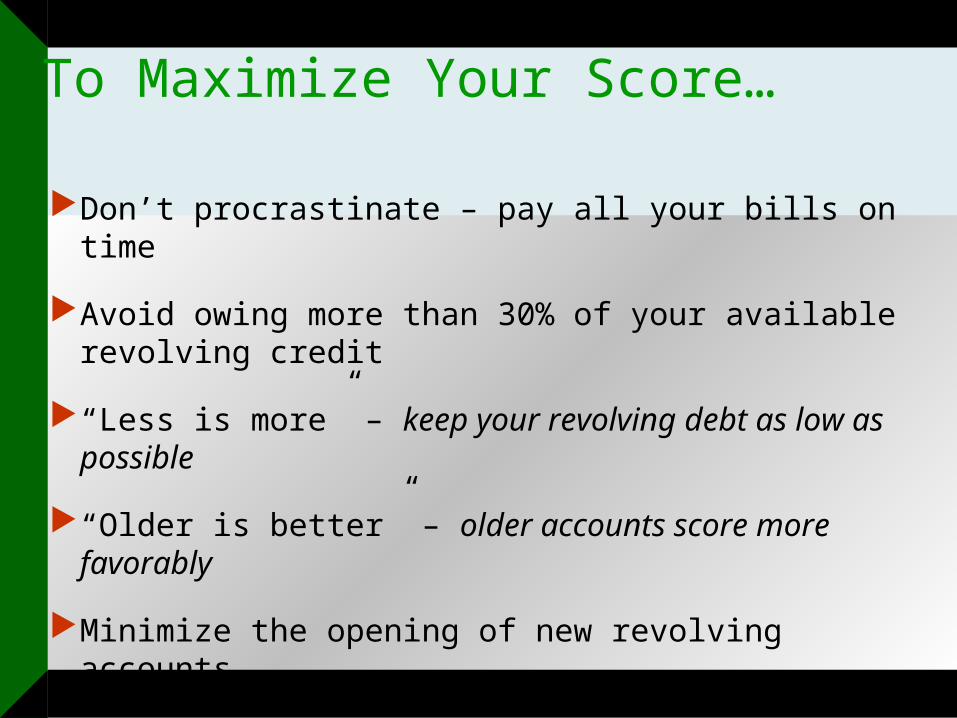

To Maximize Your Score…

Don’t procrastinate – pay all your bills on time

Avoid owing more than 30% of your available revolving credit

“Less is more” – keep your revolving debt as low as possible

“Older is better” – older accounts score more favorably

Minimize the opening of new revolving accounts

Slide 29

Chapter 10

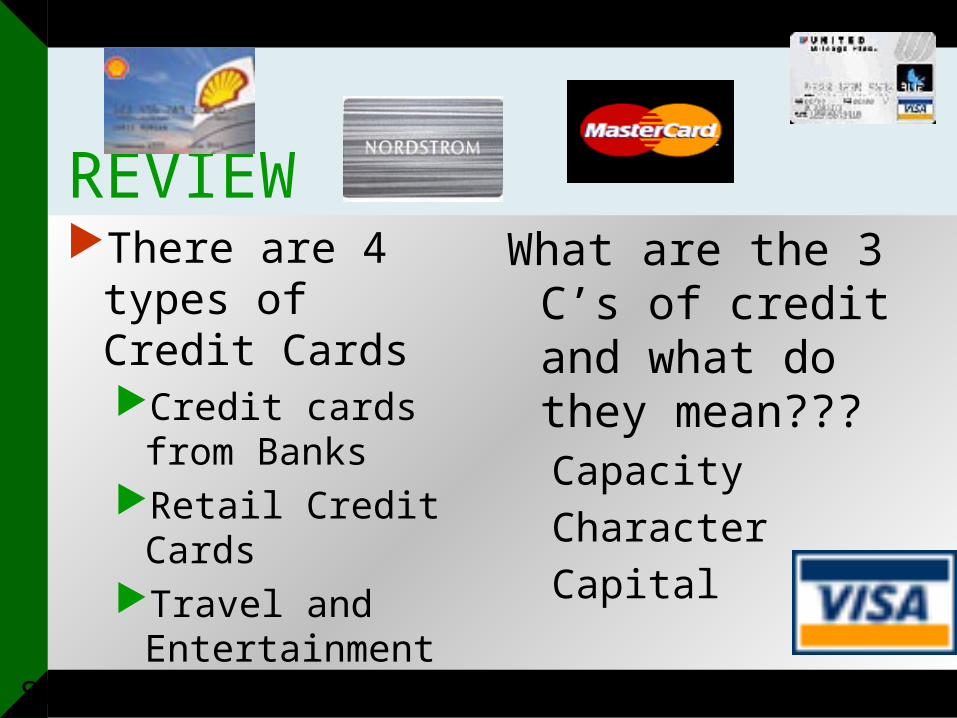

REVIEWThere are 4 types of

Credit CardsCredit cards from

Banks Retail Credit CardsTravel and

Entertainment Credit Cards

Gasoline Credit Cards

What are the 3 C’s of credit and what do they mean???CapacityCharacterCapital

Slide 30

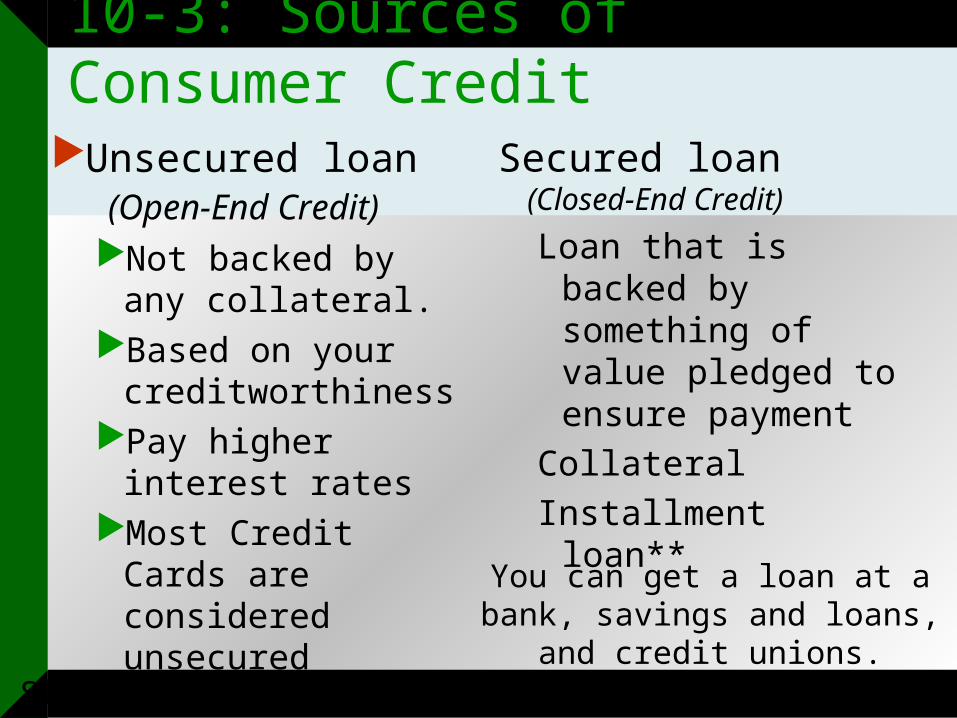

Chapter 1010-3: Sources of Consumer Credit

Unsecured loan (Open-End Credit)Not backed by any

collateral.Based on your

creditworthinessPay higher interest

ratesMost Credit Cards are

considered unsecured

Secured loan (Closed-End Credit)

Loan that is backed by something of value pledged to ensure payment

CollateralInstallment loan**

You can get a loan at a bank, savings and loans, and credit

unions.

Slide 31

Chapter 10Advantages of Credit CardsTemporary expansion of incomeReduced need for cashProvide convenience and securityEstablishes credit

a credit rating is a record, kept by a credit rating agency that tells prospective creditors how good a person is at paying off debts

Advance notice of salesReduced sale prices

Slide 32

Chapter 10

Disadvantages of Credit CardsInterest/Finance ChargesCan lead to overspending (customers spend 20

to 30% more using credit cards than they would with cash)

Can give you bad credit rating (not making payments on time, incurring excessive debt)

College students (with limited or no credit history and income) are charged higher interest rates.

Slide 33

Chapter 10

Credit Card Don’ts

Don’t get a card with a high limitDon’t get more than 1 cardDon’t use them for cash advancesDon’t charge more than you can pay off in

a monthDon’t let banks increase your credit limit

Source: USA Funds Life Skills -Module 1

Slide 34

Chapter 10

Credit Card Do’sLimit the number of cards you haveUse a debit card vs. a credit cardUse a card that has no annual fee and lower

interest ratesKnow all of your card’s hidden feesAlways pay more than the minimum amount

each monthPay on time, all the time.