credit appraisal of term loans and working capital...

TRANSCRIPT

A Project Report

On

Credit appraisal

Of

Term Loans and Working Capital Limits

Submitted by

M Laxmana Swamy (DM-72)

BIMTECH (2011-2013)

At

Andhra Bank, Head Office, Hyderabad

In partial fulfilment for the award

Of

POST GRADUATE DIPLOMA IN MANAGEMENT (2011-13)

Under the guidance of

Industry Mentor:

R.V.Raju

Senior Manager,

Mid Corporate Department

Andhra Bank-Head Office

Hyderabad.

Faculty Mentor:

Prof. Kamal Kalra

BIMTECH

ContentsContents............................................................................................................... 1

List of tables........................................................................................................... i

Summer Project Certificate.................................................................................. iii

Andhra Bank Certificate....................................................................................... iv

Acknowledgement.................................................................................................v

Executive Summary............................................................................................vii

Letter of Transmittal............................................................................................ ix

Letter of Authorization..........................................................................................x

About the company...............................................................................................1

Literature review...................................................................................................3

Statement of the problem.....................................................................................5

Methodology and Process Description..................................................................6

Data and Process Analysis....................................................................................9

Credit Facilities..................................................................................................9

About the borrower firm and their proposal.......................................................9

Step 1: Calculating credit exposures to individual/group borrower:................11

Step 2: Calculating Term loan eligibility: ........................................................12

Step 3: Primary and collateral security:...........................................................13

Step 4: Credit Risk rating and pricing..............................................................15

Credit risk rating model:...............................................................................16

CRISIL Rating and Industry analysis:............................................................22

Step 5: Calculating applicable interest rate and tenure:..................................26

Step 6: Working capital assessment................................................................26

Step 7: Credit investigation, due diligence & verification of defaulters list:.....29

Step 8 Financial analysis and compliance:.......................................................31

Step 9 Term and conditions:............................................................................35

Results................................................................................................................39

Credit risk rating results..................................................................................39

DSCR results:...................................................................................................39

Sensitivity analysis results:..............................................................................40

Working capital Results:..................................................................................41

Compliance to policy........................................................................................41

1

Conclusions.........................................................................................................42

Limitations..........................................................................................................44

Recommendations..............................................................................................45

References..........................................................................................................46

Appendix I...........................................................................................................47

Appendix II..........................................................................................................49

Appendix-III.........................................................................................................50

Glossary of abbreviations....................................................................................52

2

3

List of tablesTable 1 Term loan I.............................................................................................10

Table 2 Term loan II............................................................................................10

Table 3 Working capital limits.............................................................................11

Table 4 Exposure ceilings...................................................................................11

Table 5 Exposures to Individual and group.........................................................12

Table 6 Margin money calculation......................................................................12

Table 7 Collateral available.................................................................................15

Table 8 Collateral required..................................................................................15

Table 9 Net worth of individuals.........................................................................15

Table 10 CRRM rating and their meaning...........................................................17

Table 11 Factors considered under Industry risk................................................17

Table 12 Factors considered under Business risk...............................................18

Table 13 Factors considered under financial risk................................................18

Table 14 Factors considered under Management risk.........................................19

Table 15 Factors considered under facility risk...................................................20

Table 16 Factors considered under project risk..................................................20

Table 17 weight associated with each risk parameter........................................20

Table 18 Parameters considered under CRAS model and their weights..............21

Table 19 Parameters under CRS model..............................................................21

Table 20 Credit rating and their meaning in CRS model.....................................22

Table 21 Factors considered by CRISIL for industry score...................................23

Table 22 Operating margins for commercial real estate.....................................25

Table 23 Applicable spread.................................................................................26

Table 24 Turn over method calculations.............................................................27

Table 25 II method calculations..........................................................................28

Table 26 Cash deficit method of the borrower....................................................29

Table 27 Defaulters list.......................................................................................30

Table 28 conduct of the borrower.......................................................................31

Table 29 key financial indicators.........................................................................31

Table 30 Remarks on key financial indicators.....................................................32

Table 31 sales receipts.......................................................................................33

Table 32 Auditors comments..............................................................................35

i

Table 33 Rating given to the borrower................................................................39

Table 34 Other ratings........................................................................................39

Table 35 DSCR estimations.................................................................................40

Table 36 Sensitivity Results................................................................................40

Table 37 Working capital build up.......................................................................41

Table 38 Compliance to loan policy guidelines...................................................42

ii

Summer Project Certificate

This is to certify that Mr. M Laxmana Swamy, Roll

No. 72, a student of PGDM (Finance) has worked

on a summer project titled ‘Credit appraisal of

Term loans and Working Capital limits’ at Andhra

Bank after Trimester-III in partial fulfilment of the

requirement for the Post Graduate Diploma in

Management programme. This is his original

work to the best of my knowledge.

Date: ____________ Signature

_______

(_____________________) Prof

Kamal Kalra

BIMTECH SEAL

Faculty mentor

iii

Andhra Bank Certificate

Date: June, 09, 2012

TO WHOMSOEVER IT MAY CONCERN

Sub: Training Certificate

We hereby certify that Mr M Laxmana Swamy a Full Time

Student of Post Graduate Diploma In Management Course,

2011-2013, of Birla Institute of Management Technology

(BIMTECH) has undergone his Summer Internship as mandated

for the completion of his above course from BIMTECH, for a

period of 8 weeks starting from April, 16,2012

The title and scope of his project was “Credit Appraisal of Term

Loans and Working Capital Limits”. The project was carried out

under the guidance of Mr. R V Raju, Senior Manager.

We found him to be a dedicated and diligent student. We take

this opportunity to wish him success in his future endeavours.

iv

Sincerely,

Mr. R V Raju

Senior Manager

Andhra Bank- Head Ofiice,

Hyderabad.

Acknowledgement

I would like to gratefully acknowledge the contribution of all the people who took active part

and provided valuable support to me during the course of this project. To begin with, I would

like to offer my sincere thanks to R.V Raju, Senior Manager, for all his support at Andhra

Bank. Without his guidance and valuable suggestions during the research, the project would

not have been accomplished.

My heartfelt gratitude also goes to S T Sridhar, Chief Manager at Andhra bank for his

valuable assistance.

I also sincerely thank Prof Kamal Kalra, my faculty mentor at BIMTECH, who provided

valuable suggestions, shared his rich corporate experience, and helped me script the exact

requisites.

v

vi

Executive Summary

Term loans and working capital limits are the major source of funding for the corporates. For

availing either term loans or working capital limits from a bank, the borrower has to satisfy

certain conditions and follow the process prescribed by the bank. Andhra Bank has got its

own loan policy method for evaluating the Credit proposals.

Mid Corporate Department at Head Office deals with Credit proposals ranging from Rs. 25-

60 crores. Branches/Zonal Offices of Andhra Bank after initial scrutiny of the proposals,

they forward the proposals with their recommendations for sanction to the Head Office. The

objective of my project work at Andhra Bank is to appraise one loan proposal received by

the Mid-corporate department at Head Office. The scope of this project is to study the credit

approval process followed by Andhra Bank.

The credit approval process at Andhra Bank starts with checking the exposure limits as per

the bank guidelines. The next step is credit rating of the borrower and decide the applicable

interest rate. Andhra bank follows its own internally developed method called Credit Risk

rating method (CRRM) for the purpose of credit rating of the borrower. Andhra bank also

avails CRISIL rating for the purpose of industry analysis and industry score.

The financials of the borrower are checked and various ratios are calculated for the purpose

of checking the financial compliance of the borrower as per bank guidelines. Working

capital assessment also needs to be done. For the purpose of assessing the working capital,

methods such as turnover method, II method and cash budget method have been prescribed.

Out these methods, cash budget method has been used for the borrower as he belongs to

Commercial Real estate.

For purpose of availing term loans, the eligibility is calculated based on margins as stipulated

by the bank’s policy guidelines. Margin means a fixed amount of money that must be

brought in by the borrower. As security for availing term loan the borrower has to provide

collateral security along with primary security. Collateral security is taken for the purpose of

recovering the funds given by the bank in case the borrower defaults.

vii

Results such as risk rating, interest applicable, EMI payable and working capital limits

approved would be mentioned. The conclusion of the project report includes comments on

methodology followed. Recommendations would also be provided.

The borrower in the case study is a privately held construction company. The borrower has

asked for term loan of 15 crores and Working capital limits of 7 crores for the purpose of

construction of a Mall in Chennai.

viii

Letter of TransmittalDate: June, 09, 2012

Mr. R V Raju,

Senior Manager,

Mid corporate department, Head Office.

Hyderabad.

Dear Sir,

Re: Summer Project Report

Attached herewith is a copy of my summer-project report “Credit Appraisal of Term loans

and Working Capital limits” which I am submitting in order to mark the completion of an

8 week summer project at you organization. This report was prepared by me using the best of

practices and summarizes the work performed on the project and is being submitted in partial

fulfilment of the requirements for award of diploma.

I would like to mention that the overall experience with the organization was very good, and

helped me to know how work is carried out in real practice with the help of your esteemed

organization. I feel honoured that I got an opportunity to work with Andhra bank, a company

of great repute.

I hope I did justice to the project and added some value to the organization.

Suggestions/comments would be appreciated.

Yours truly,

M Laxmana Swamy

ix

Letter of Authorization

I, M Laxmana Swamy, a student of Birla Institute of Management Technology (BIMTECH),

hereby declare that I have worked on a project titled “Credit Appraisal of Term loans and

Working Capital limits” during my summer internship at “Andhra Bank”, in partial

fulfilment of the requirement for the Post Graduate Diploma in Management program.

I guarantee/underwrite my research work to be authentic and original to the best of my

knowledge in all respects of the process carried out during the project tenure.

My learning experience at Andhra Bank, under the guidance of Industry Mentor R V Raju,

Senior Manager, and Faculty guide Prof. kamal Kalra has been truly enriching.

Date: June, 09, 2012

M Laxmana Swamy

x

About the company

Andhra Bank is one of the leading banks in the country among the mid size public sector

banks. Andhra Bank has been founded by Late Mr Dr Bhogaraju pattabhi Sitaramayya in

1923 in Machilipatnam, with a paid up capital of 1 lakh rupees and authorised capital of 10

lakhs rupees. In April 1980 the bank was converted to wholly owned government bank.

Government of India holds up to 51.55 % and Life Insurance Corporation owns nearly 10 %

of the shares. The bank has its head quarters situated in Saifabad, Hyderabad.

Since 2002 Shri B A Prabhakar is chairman and Managing director of the bank. Andhra

bank has a global presence with over 1729 branches globally including developed nations

such as USA and UAE. The bank also started a joint venture with Bank of Baroda and L&G

a foreign partner to form the India first Life insurance Company limited. Andhra Bank has

got around 14,000 employees working with it.

The Head office of Andhra Bank located at Hyderabad is divided into various departments

namely SME sector, Mid and Large Corporate department, Retail department, Legal

department, and Integrated Risk department.

Vision of the bank:

Envisions being a Trustworthy, Efficient and Strong Bank committed to increase market

share by generating innovative Customer-Centric services and products igniting the

Passion and Creative talents in Human resource leveraging Technology to expand the

clientele & deliver Quality and Value Leading to Customer Delight.

Mission of the bank:

Amplify the front line capabilities to Serve Customers develop Processes leveraging

Technology dynamically locate & empower People fast-cycle knowledge into

innovative Products create Possibilities to reach the business goals & position the Bank as

a rising star in the Financial Horizon.

Key financials:

1. Total deposits by March 2012 stood at Rs 105851 crore as compared to Rs 92156

crore by the end of March 2011.

1

2. Advances showed a year on year growth of 17% till March 2012 reaching a level of

Rs. 84684 crores as compared to Rs. 72154 crore by the end of March 2011.

3. CASA deposits increased to Rs. 27947 crore in March 2012 compared to Rs 26779

by the end of March 2011.

4. CASA share in total deposits stood at 26.4% in March 2012.

5. Total income during Q4 FY11-12 rose by 21.3% to Rs 3220 crore.

6. Total income during the FY 11-12 rose by 32% and stood at value of Rs. 12,199

crore.

7. Net interest income during the Q4 FY 11-12 improved to Rs. 914 crore recording a

growth of 6.2 % compared to Q4 FY10-11.

8. NII for the FY11-12 improved by 16.7 % and rose to Rs. 3759 crore.

9. Operating profit for the 12 month of FY11-12 grew 16.7% and stood at Rs. 2815

crore compared to Rs 2413 crore in FY10-11.

10. Net profit for the 12 month ended March 2012 stood at Rs 1345 crore with a growth

of 6.1% from previous month.

11. Gross NPA ratio stood at 2.12% as at March 2012 compared to NPA of 0.91% by the

end of March 2011.

12. Net interest margin stood at 3.34 % for the quarter ended March 2012 and 3.67 % for

12 months ended March 2012.

13. CRAR of the bank stood at 13.18% under BASEL-II (Tier I capital: 9.02% and Tier-

II capital: 4.16%)

14. Priority Sector Advances improved to Rs.27027 Crore as on 31.03.2012 from

Rs.23,082 Crore as on 31.03.2011, recording a growth of 17.1%.

15. Advances to Agriculture have gone up to Rs.12, 459 Crore as on 31.03.12 from

Rs.10, 369 Crore as on 31.03.11, recording a growth of 20.1%.

16. MSME Advances registered a growth of 18.3% and stood at Rs.13132 Crore as at the

end of March 2012 as against Rs.11,105 Crore in March 2011.

17. Retail Credit Portfolio of the Bank increased to Rs.11, 301 Crore as on 31.03.2012

compared to Rs.10, 479 Crore as on 31.03.2011, registering a Y-o-Y growth of 7.8%.

2

Literature review

Risk management has become one of the most important aspects for any corporate entity.

Financial institutions must be more prudent as far risk management is concerned. In Master

circular –prudential norms on capital adequacy-Basel I Frame work RBI has defined credit

risk in the following way: “Credit risk is most simply defined as the potential that a bank’s

borrower or counterparty may fail to meet its obligations in accordance with agreed terms.

It is the possibility of losses associated with diminution in the credit quality of borrowers or

counterparties”. The importance of credit risk management has emphasised in the same

document. Maximising the banks risk adjusted rate of credit would be the goal of credit risk

management. Maintaining the exposures within acceptable level would also come under

credit risk management. Banks apart from managing credit risk at portfolio level, Credit risk

should also be managed at individual transaction level. A proper credit management system

would also be a part of credit risk management.

‘Report of the Committee on Comprehensive Regulation for Credit Rating Agencies (2009)’

highlighted the importance of ‘Credit rating agency’s’. Credit rating agencies and the ratings

given by them help allocate capital efficiently across all sectors of the economy by pricing

risk appropriately. Though not compulsory, banks get their loan portfolio rated by external

agencies due to the fact that increased risk weight must be assigned to unrated loans.

According to the Basel II guidelines (Credit requirement directive-CRD) banks are required

to implement either standardised or internal rating based approach. Since RBI has not come

out with final guidelines regarding Internal Based Approach, all banks in India are required

to follow Standardised approach where the risk weights are given by RBI. RBI had however

issued guidelines asking banks to put in place systems to measure credit risk, market risk and

operational risk to ensure capital adequacy. Pending the issue of final guidelines, RBI has

asked to parallel run both systems (standardised approach and internal rating based

approach) and furnish CRAR (Capital to Risk weighted assets). Hence Andhra Bank is doing

a parallel run of both systems.

Basel II norms state that for internal based approach parameters such as probability at default

(PD), exposures at default, maturity are required. The basic requirement for calculating

3

probability at default (PD) is a robust rating model. Hence, Andhra Bank with the help of

NIBM, Pune has developed CRRM model.

Prior to Tandon committee report recommendations (1974) banks followed securitized

method for working capital lending. Tandon committee report for the first time came up with

the concept of “maximum permissible bank finance”. Tandon committee report clearly

mentioned that banks should only finance a part of working capital need. The rest of funds

must be brought in by the borrower using long term sources.

Tandon committee report recommended three methods of lending which are discussed in the

report. Tandon committee also emphasised that the corporates should maintain less in current

assets. The committee also suggested holding norms for different classes of current assets.

Of three methods suggested by the Tandon committee, only the first and second methods of

lending are broadly used. However the third method of lending is not widely used due to the

complexities involved in the method.

Chore committee report which later came up in 1979 worked within the framework of

Tandon committee. Chore committee emphasised the importance of bill discounting in

working capital of the company. The committee also came up with many recommendations

regarding such as quarterly submission of current assets details by the company; maintain

current ratio of 1.33:1, peak and non peak limits and etc.

Marathe committee which came up later had come up with various factors effecting working

capital management. The committee report emphasised that borrowers must reduce the

dependence on bank funds for working capital requirement. Borrowers must try to reduce the

working capital requirements from 1.33:1 to 1:1.

4

Statement of the problem

Andhra Banks offer various credit facilities to corporate for their requirements. Term loan is

one such facility offered to the corporates. A term loan can be either short term or medium or

long term. For the purpose of sanctioning term loan, there is prescribed procedure to be

followed in order to ensure the credibility of the project and the borrower.

The process of credit approval includes risk rating the borrower. Risk rating is done using

CRRM under internal risk approach as per RBI guidelines. Applicable interest rate is

decided based on the rating obtained. The borrower however can ask for finer rates of

interest if he satisfies certain stipulated conditions. Security requirements needs to be

calculated based on the bank guidelines. Required primary and collateral security needs to be

calculated.

The working capital limits that can be availed by the borrower will also be calculated. For

this purpose suitable method must be selected first. Apart from all the above steps it also

very important to check the credit worthiness of borrower. RBI stipulates every bank to go

through various defaulters such as RBI caution list, RBI defaulter list, RBI wilful defaulters

list, SAL wilful defaulters list.

The scope of the project work at Andhra bank would be to appraise one credit proposal and

study all the above mentioned steps.

5

Methodology and Process Description

Andhra Bank provides Credit services both fund based and non fund based. The Credit

facilities includes term loan, demand loan, Overdraft, cash Credits, WCDL, advances

against bills, letter of Credit, guarantees, etc. To receive sanctioned advices from Head

Office, a proper appraisal system is required. Andhra Bank has got its own loan policy

method for evaluating the Credit proposals. The Credit appraisal to be done has following

stages mentioned below:

I. The process starts with checking the overall fund and non fund based limits that

can be given. Limits applicable to the unit, group and the industry segment on

whole are checked as per Banks loan policy guide lines/RBI guidelines.

II. Verifying the technical and market feasibility of the project/proposal and

undertaking SWOT analysis of the borrower.

III. Risk Rating the borrower (e.g. A+++, A++, A+, A, B, C, D) based on the CRRM

(Credit Rating Risk Model) model followed by the Bank. For various parameters

such as management risk factors, financial risk factors, industry risk factor are

rated. Then based on the Credit rating the applicable interest rates and repayment

period is decided.

IV. The past, present and projected financials of the borrower are verified:

a. Balance sheet.

b. Profit and loss account.

c. Fund flow statements.

d. Cash flow statements

V. Calculations of the ratios such as

a. Debt service coverage ratio(DSCR)

b. Capital gearing ratio

6

c. Current ratio

d. Debt equity ratio

e. TOL/TNW ratio

VI. Calculating required primary and collateral security required.

VII. Performing sensitivity analysis on Debt service coverage ratio(DSCR) by

a. Increasing and decreasing cost of raw material

b. Increasing and decreasing the projected sales

c. Increasing and decreasing the applicable interest rates

VIII. Calculating of the drawing power of the borrower.

IX. Assessment of working capital limits or requirement based on turnover method or

II method or cash budget method whichever is applicable.

Sources of data:

Data regarding the borrower would be collected from the borrower itself. The

borrower has to submit various financial statements to the bank when he wants to

avail certain credit facilities from the bank. Various RBI documents are also referred

for understanding various policies.

7

8

Data and Process Analysis

Credit Facilities

Andhra bank provides various credit facilities to individuals and corporate entities. These

facilities can be fund and non fund based. Some of fund based facilities are mentioned below

Term loans: Term loans include short, medium and long term loans. Long term loans are

loans with maturity greater than 8 years while loans with maturity 1 to 8 years are called

medium term loans. Term loans are taken generally for capital requirement. The interest

applicable for a term loan depends upon the risk involved in the project and varies from case

to case.

For the purpose of short term requirements either bridge loans or short term loans are given.

These loans have a maturity less than 1 year. Generally the short term loans carry higher

interest rate compared to long term loan. Bridge loans are generally obtained as an

intermediary source of fund before getting funds from a new and large source of funds. The

money from new source of fund is used to repay the bridge loan.

Working capital limits: For the purpose of meeting the working capital requirements various

facilities are offered by the banks. These facilities include various Open cash Credit limit

(OCC) and Overdraft facilities. Over draft facilities can be clean overdraft and secured

overdraft.

Non fund based facilities: Non fund based facilities include various facilities like letter of

credit (LC), letter of comfort (LOC) and bank guarantees (BG).

About the borrower firm and their proposal

M/S ABC builders, engineers and contractors is a registered partnership firm dealing with

Andhra Bank since 2003. The firm in engaged in the development of residential and

commercial flats in Chennai and Bangalore. Mr XXX is the main promoter and managing

director of the firm. He is a qualified civil engineer and from 1995 he is in civil construction

line and having vast experience. This company has been doing construction work almost

since a decade.

9

Proposal: ABC builders and engineers and constructors have approached Andhra Bank for

the purpose of availing term loan as well as working capital limit renewal. The proposal

under consideration comes under Commercial real estate (CRE).The details are given below:

1. Recommendation for renewal cum enhancement of Secured Over Draft(SOD) from

Rs 4.50 crores to Rs 7 crores

2. Sanction of term loan I (project funding) for Rs 8.00 crores and term loan II for 7.00

crores.

Table 1 Term loan I

1 Facility Term loan I(project funding) Limit Rs 8 crore

purpose

To construct commercial spaces In two basement and

ground and first floor Margin 50%

repayment period

Repayable in Three years, Interest to be serviced as and

when debited. The loan is to be repaid as and when the

shops are registered in favour of the buyer. interest/Commission BR+4%+0.25 % i.e. 15% p.a. presently

Table 2 Term loan II

2 Facility Term loan II Limit 7 crore

purpose

to construct and lease out commercial space for halls in

second to fifth floor Margin 50%

Repayment period

Repayable in 60 EMI of Rs 16.66 lakhs each with a period

of 24 months Interest/ Commission BR+4 %+0.25% i.e. 15% p.a. presently

10

Table 3 Working capital limits

3 Facility SOD(Against Real estate) Limit Rs. 7 crore purpose Working capital Margin 50% Repayment period One year Interest/ Commission BR+7.25 % i.e.18 % presently

Table 1, table 2, table 3 show the credit facilities requested by the borrower. It can be seen

that total term loan has been divided into 2 different loans. It is the different purpose and

different amortization schedules of the loan that made the company to differentiate the loan

into 2 types. Term loan I has been for the purpose of construction of 2 basements, ground

and first floor. The term loan II has been for the purpose of construction of second to fifth

floor where the proposed cinema theatres are planned to be constructed. For the purpose of

credit appraisal there is a step by step procedure to be followed as explained below.

Step 1: Calculating credit exposures to individual/group borrower:

RBI guidelines very clearly indicate the banks to maintain certain fixed amount of exposure

per borrower and to the group. Apart from exposure limits to individuals and groups, there

are exposure limits set for industry/segment.

The exposure ceiling limits would be 15% of the capital funds (of Andhra Bank) in case of a

single case borrower and 40% of the capital funds in the case of a borrower group. The

capital funds for the purpose will comprise of Tier I and Tier II capital. However there are

various norms that allow deviations depending upon the sector. For example infrastructure

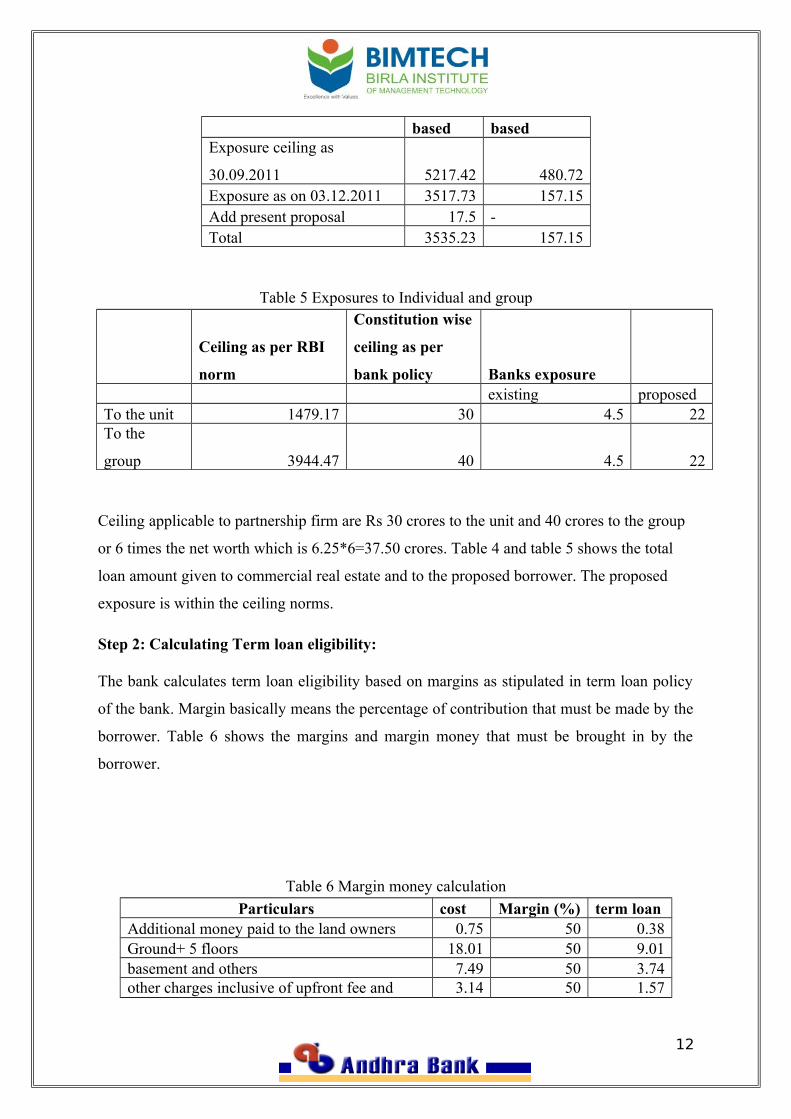

companies may be allowed a deviation of 5 % and 10% to individual and group borrower

respectively. The industry wise credit exposure limit to commercial real estate has been fixed

at 7% of total fund based advances of previous quarter.

Table 4 Exposure ceilingsParticulars Fund Non fund

11

based basedExposure ceiling as

30.09.2011 5217.42 480.72Exposure as on 03.12.2011 3517.73 157.15Add present proposal 17.5 -Total 3535.23 157.15

Table 5 Exposures to Individual and group

Ceiling as per RBI

norm

Constitution wise

ceiling as per

bank policy Banks exposure existing proposedTo the unit 1479.17 30 4.5 22To the

group 3944.47 40 4.5 22

Ceiling applicable to partnership firm are Rs 30 crores to the unit and 40 crores to the group

or 6 times the net worth which is 6.25*6=37.50 crores. Table 4 and table 5 shows the total

loan amount given to commercial real estate and to the proposed borrower. The proposed

exposure is within the ceiling norms.

Step 2: Calculating Term loan eligibility:

The bank calculates term loan eligibility based on margins as stipulated in term loan policy

of the bank. Margin basically means the percentage of contribution that must be made by the

borrower. Table 6 shows the margins and margin money that must be brought in by the

borrower.

Table 6 Margin money calculation

Particulars cost Margin (%) term loanAdditional money paid to the land owners 0.75 50 0.38Ground+ 5 floors 18.01 50 9.01basement and others 7.49 50 3.74other charges inclusive of upfront fee and 3.14 50 1.57

12

other charges/fees like CMDA plans approval

charges, TNEB charges deposits and TL

interest during construction periodcontingencies 0.6 50 0.30Total 29.99 15

As can be seen from above table, the total cost of the project is 30 crores. Out of the total

cost 15 crores is bought in by the borrower, the rest in proposed to be brought in as term

loan.

Step 3: Primary and collateral security:

Repayment capacity of the borrower and economic viability of the project will be the prime

consideration while evaluating the proposal. Security and guarantee offered by the borrower

shall be considered as secondary source of payment.

In order to obtain either a fund based or non fund based facility from the bank, security must

be given. In case the borrower defaults in paying back the borrowed funds, then banks will

have the right to liquidate the security and recover the funds given by them to the borrower.

Security offered by the borrower to the banks is divided into primary and collateral security.

The assets acquired out of the bank finance shall be taken as primary security for the

exposure. Anything offered/pledged apart from primary security is taken as collateral

security. Collateral security can be anything such as land, building, etc. Collateral security

can even be from members who are not stake holders in the deal/company. While extending

finance for acquisition of fixed assets or working capital finance against current assets,

prescribed margins shall be ensured in tune with norms prescribed by the bank.

Security can also be given in the form guarantees. In cases where collateral securities are

given by third parties guarantees or co-obligations are taken from the borrower. In case when

real estate is given as collateral security, sometimes the promoters may be required to give

guarantee to the extent of land value. In case of public companies guarantees are taken from

the directors. Taking personal guarantee makes borrower more accountable and responsible.

In proposed project, the details of primary and secondary security offered are given below:

Primary security:

13

• For term loan I and II: 50% of undivided share of land situated in Mahabalipuram

Road and 50 % share in the super structure to be built there upon.

• For Secured Over Draft (SOD) security: Real estate valuing 19.23 crores (Which is

also extended to term loans)

Collateral Security-Proposed:

Vacant land of about 7392 sft located at poonamalle high road, Nerkundram, Chennai-

600107 with Market value is 5.54 crores.

Further to the discussion where in Zonal office had highlighted the positive factors about the

proposal, requested the promoter to offer additional security and the borrower has agreed to

give the following additional securities:

1. Land to an extent of 2697 sq. ft with the building at Venkatesm Street , T Nagar,

Chennai belonging to father-in-law and mother-in-law of Mr AAA worth Rs 4 crores.

2. Vacant land to an extent of 8100 sft at site no 11, sarjapur belonging to Mr AAA

worth 4 crore.

Thus the total value of collateral security offered is valued at 13.54 crores (5.54 +4+ 4).Table

7 and table 8 shows the amount collateral available and total amount of collateral required.

As can be seen the collateral available is greater than collateral required.

14

Table 7 Collateral available

SI. No Particulars

Amount

(crores)1 Value of existing security 19.232 Total value of new security proposed to be given ( Rs 5.5 + Rs 4+ Rs 4) 13.543 Total security offered 32.77

Table 8 Collateral required

SI.No Particulars Amount(crores)1 Collateral security required at 200 % of SOD limit of 4.5 crore 92 200 % for short term loan of 8 crores 163 100 % for term loan of 7 crores 74 Total term loan requested 325 Security coverage 102%

Guarantors- Joint and several liabilities of partners: Since the firm is partnership firm, all

partners have their liability status is unlimited. The net worth of the all the partners has been

given below in table 9.

Table 9 Net worth of individuals

Name Net worth( in crores)AAA 16BBB 2.17CCC 5.85DDD 1.5

Step 4: Credit Risk rating and pricing

Bank has its own policy for risk rating of the borrower. Andhra follows different models

depending on the credit limit. For all advances with credit limit between 5 crores and 50

lakhs CRAS (Credit Risk Assessment System) model is followed. CRS (Credit rating

system) model is followed and when the limits are between 5 lakhs to 50 lakhs. For all credit

limits above 5 crores, CRRM (Credit rating risk management) model is used for credit

rating. For credit limits less than 5 lakhs various other systems are used for risk rating.

15

Initially CRAS model was used even for credit limits greater than 5 crores. But based on RBI

guidelines to implement the BESEL-II guidelines, CRRM model has been implemented. For

the purpose of rating a borrower, past financials are made use of. In case the borrower is

implementing a new project, then projected financial are made use for the purpose of risk

rating a borrower.

In case the borrower is new to the bank, it is mandatory that he must secure an overall

minimum score of 40% with a minimum of 40% score in each of the parameter. For

considering finer rates of interests the borrower should be rated ‘B ‘and above under

CRS/CRAS and should be rated above ‘B++ ‘under CRRM.

Credit risk rating model:

Andhra Bank with help of NIBM, Pune has developed an Internal rating system called as

CRRM based on the RBI guidelines. For development of the model risk parameters such as

Probability of default (PD), Loss given default (LGD), exposure at default and exposure at

maturity are used. This new model is software driven and BASEL compliant model capable

of providing rating migration statistics, PD calculations apart from several useful reports for

management information.

Under the New Capital Adequacy framework [ Based on BASEL II document], the concept

of Credit Risk, Market Risk and Operational Risk is introduced with guidelines on

classification of assets, methodologies for measuring these risks and the approaches

available to banks are furnished.

As mentioned earlier CRRM model is used for rating when credit limits are greater than 5

crores. CRRM model is used for both fund based and non fund bases. CRRM model is a very

comprehensive model. CRRM model is a software based model. All sanctioning authorities

and Zonal offices have this software loaded into their systems.

In CRRM model various types of risks are indentified. Under each risk, several parameters

are selected and under each parameter, several risk factors are taken up for evaluation and

rating on a 1 to 6 scale, with 6 being the highest score and 1 the least. Weights are attached

to Parameters/ Factor. Final ratings are assigned based on the weighted average scores. Table

10 shows various grades that can be obtained and their meaning under CRRM.

The internal and external risks are evaluated under the following heads:

16

a) Financial Risk Evaluation

b) Industry Risk Evaluation [External Risk]

c) Business Risk Evaluation

d) Management Evaluation

e) Security/Conduct of account

f) Project Risk Evaluation (in respect of Term Loan accounts)

Table 10 CRRM rating and their meaning

Score Rating Description

6.0-5.4 A++

An exceptionally high position of strength. Very high

degree of sustainability

5.39-4.9 A+

A high degree of strength on factors among peer groups.

High degree of sustainability4.89-4.2 A A moderate degree of strength with positive outlook4.19-3.6 B++ A moderate degree of strength with stable outlook

3.59-3.0 B+

A moderate degree of strength with stable and marginally

negative outlook

2.99-2.4 B

Weakness on a parameter in comparison with peers.

Unstable outlook

2.39-1.0 C

A fundamental weakness with regard to the factor.

Unlikely to improve under normal conditions.0 D Defaulter

Industry Risk Evaluation: The Industry risk section evaluates the outlook for the industry

over the medium term. Three Distinct risk parameters have been identified and a number of

risk factors within each risk parameter have been identified. Under industry risk the

following factors are considered under which further properties are considered. Table 11

gives the factors that are considered under industry risk evaluation. There a total of 3 factors

with each factor having many sub factors considered.

Table 11 Factors considered under Industry risk

SI.NO Name of factor Number of parameters1 Industry

Characteristics

4 parameters

2 Competitive forces 8 parameters3 Industry Financials 3 parameters

17

The department handling the Credit Risk Rating at the Head Office will rate the Industry

Parameters either using Internal Industry Intelligence or using External Industry Database

and communicate the data on the Industry parameters to the credit rating officers at the 9

Branches or Zones. The Industry Ratings will be reviewed periodically to keep them in tune

with the changes in the environment.

The Branches and Zones do not have the facility to change the Industry ratings once it is pre-

determined by the Head Office. The rating officers at Zones or Branches have to select the

appropriate Industry for the Company/Borrower under consideration and the corresponding

Industry data will be automatically retrieved from the Industry database and Industry rating

will be generated automatically.

Andhra Bank has subscribed to CRISINFAC’s Industry Risk Scores, who provides the inputs

to the Industry scores. According to CRSINFAC, the industry score is 2.3 on a scale of 6,

which indicates unfavourable. However as per the background of the promoter and

feasibility of the project, ZO has recommended for the credit limits.

Business risk: Business risk is measured through parameters that determine the company’s

business position within the industry and its sustainability. Table 12 gives factors considered.

Table 12 Factors considered under Business riskSI. No Factor Number of parameters1 Market position 52 operating efficiency 33 Growth 4

Financial risk: By measuring the financial risk the overall risk involved in the financial

system of the company is measured. The following factors are taken into account while

measuring the financial risk. The factors considered under financial risk are given in table

13.

Table 13 Factors considered under financial riskSI. No Factor Number of parameters1 Quality of financial statements 32 past financial performance 53 financial flexibility 24 Cash flow adequacy projections 5

18

Management risk: This risk parameter tries to access the management quality and the risk

that can arise due to management. Factors considered under management risk are given in

table 14.

Table 14 Factors considered under Management riskSI. No. Factors1 Number of years of experience in industry2 quality of management personnel3 Percentage of actual sales achieved to projection made last year4 Percentage of net profit achieved to projections made last year5 Percentage of actual net working capital to projections made last year6 Payment record to bankers/Institutions7 group support 8 management succession9 Corporate governance10 credibility

Facility risk/ Security risk: This risk parameter tries to access the possible risk that can arise

due to securities such as guarantees and collateral security that are given the borrower.

Factors considered under facility risk are given in table 15.

19

Table 15 Factors considered under facility riskSI. No. Factor1 Collateral security2 Personal or corporate guarantee3 Past payment record4 compliance with terms of sanction5 Operations in account

Project risk: This risk parameter tries to estimate the risk involved in the project for which

the borrower is borrowing funds. Factors considered under project risk are given in table 16.

Table 16 Factors considered under project riskSI. No. Factor1 Average debt service coverage ratio for the project2 Repayment period for the project including moratorium3 Asset coverage ratio for the project

Table 17 gives the weights given to each parameter under CRRM model. Based in these

weight final score is computed.

Table 17 weight associated with each risk parameter

Category weightFinancial risk 5Business risk 2Industrial risk 1Management risk 1.5facility risk 0.5Project risk 1

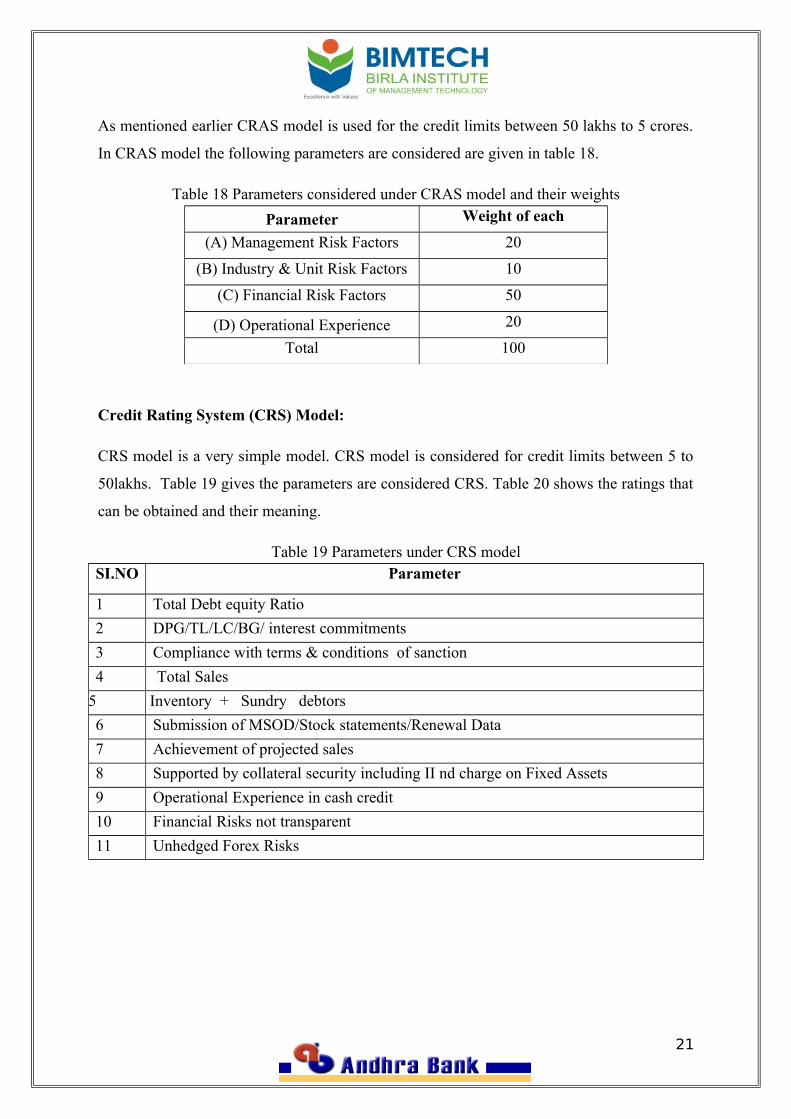

Credit Risk Assessment System (CRAS) Model:

20

As mentioned earlier CRAS model is used for the credit limits between 50 lakhs to 5 crores.

In CRAS model the following parameters are considered are given in table 18.

Table 18 Parameters considered under CRAS model and their weights

Parameter Weight of each

parameter(A) Management Risk Factors 20

(B) Industry & Unit Risk Factors 10

(C) Financial Risk Factors 50

(D) Operational Experience 20

Total 100

Credit Rating System (CRS) Model:

CRS model is a very simple model. CRS model is considered for credit limits between 5 to

50lakhs. Table 19 gives the parameters are considered CRS. Table 20 shows the ratings that

can be obtained and their meaning.

Table 19 Parameters under CRS modelSI.NO Parameter

1 Total Debt equity Ratio

2 DPG/TL/LC/BG/ interest commitments

3 Compliance with terms & conditions of sanction

4 Total Sales

5 Inventory + Sundry debtors

6 Submission of MSOD/Stock statements/Renewal Data

7 Achievement of projected sales

8 Supported by collateral security including II nd charge on Fixed Assets

9 Operational Experience in cash credit

10 Financial Risks not transparent

11 Unhedged Forex Risks

21

Table 20 Credit rating and their meaning in CRS modelMarks

secured

Credit

Rating

Grade

Acceptable Credit Rating:Above

95%

A+++ Prime

>90 to

95%

A++ Excellent

>80 to

90%

A+ Very good

>70 to

80%

A Good

>60 to

70%

B Satisfactory

>40 to

60%

C Average

Unacceptable Credit Ratings:40% &

Below

D Poor

CRISIL Rating and Industry analysis:

Andhra bank has also subscribed to CRISIL for the purpose of risk rating the borrower. Even

though Andhra Bank has its own method for rating the borrower, CRISIL ratings are used

for cross checking the rating obtained using its own rating system.

Industry: commercial Real estate (Commercial real estate has been defined as the

construction of office and retail spaces (including malls and multiplexes).

The main players in this industry are real estate developers. Small regional players continue

to dominate the commercial real estate market, while large players have been trying to

expand beyond cities in which they have traditionally operated. The industry is predominant

unorganised, but less as compared to residential housing industry. However, the unorganised

nature of the industry has resulted in high finance costs, which have further raised its risk

profile. Table 21 gives the factors considered by CRISIL and the weights given to them.

22

Table 21 Factors considered by CRISIL for industry score

Factor Weight Score

Industry characteristics 85

Demand supply gap 35

-Fluctuation in demand supply gap - Growth potential -CyclicalityGovernment policy 20

-Importance to economy -Sensitivity of government policies

Input related risk 30

Extent of competition 15

-Threat of imports/Substitutes/Unorganised sector - Barriers to entry -Technology risk -International competitiveness

-Bargaining power of buyer industries -Bargaining power of supplier industries

Total Score 2.4

For purpose of evaluating Industry risk score, the factors mentioned in the above table are

considered. The industry risk score obtained for commercial real estate is 2.4.

Demand and supply scenario:

Demand for commercial space has shown signs of revival with improvement in economy and

absorption levels have improved slightly. Many large occupiers in IT/Ites sector are

evaluating tier i/ii cities for setting up new offices but are adopting a cautious approach

before selecting a location or property. An improvement in demand has led to many of the

projects that were postponed witnessing fresh interest. However, the supply in office space

and retail space exists and hence lease rentals for both commercial office space and retail

space are expected to remain more or less stable across the tem major cities that CRISIL

tracks in 2011.

Key drivers:

1. The demand for office space is mainly driven by IT/ITES sector, BPO and call

centres.

23

2. Increasing disposable incomes, faster growth in urban population and rising

demand for branded products are the man drivers for growth of malls and

multiplexes in India.

Output/capacity:

The commercial real estate industry is relatively more organised as compared to the

residential segment. This is primarily because, unlike residential segments where in the

project is partly sponsored by the customer advance, commercial projects have to be funded

largely by the way of promoter contribution and debt.

More over the asset starts generating revenue only after it is leased. Both funding difficulty

and the underlying risk with regard to leasing the property have been discouraging

developers to enter this segment. As a result, only established players with strong brand

images have ventured into commercial properties.

The industries organised nature improves its overall rating. Track record and reputation acts

as important differentials among players. Thus while developers with a brand image are able

to sell their office, small players face intense competition. Falling demand and excess supply

has increased competition. There by putting considerable pressure on the margins and

rentals.

Outlook:

1. Rentals for commercial spaces are likely to remain more or less stable in 2011.

2. Demand for commercial sector would remain muted over next one year. Increase in

prices of major inputs like steel and cement are expected to increase construction

cost. The proposed levy of 18.5 % minimum alternate tax on developers of special

economic zones will impact the profitability of developers.

3. The oversupply position is expected to increase competition; hence the medium term

outlook for the sector continues to be unfavourable.

Price realization:

The average value of operating profit that is generally available for commercial real estate is given in table 22.

24

Table 22 Operating margins for commercial real estate

Year 2004-5 2005-6 2006-7 2007-8 2008-9 2009-10Operating profit margin (%) 36.81 34.75 59.79 58.44 54.5 51Return on capital employed (%) 12.8 19.17 13.86 16.91 9.48 10.4

1. Land is the major component of costs accounting for nearly 30-50 % of the total

project costs, with construction accounting for the rest. In the residential real

estate segment, the developer benefit from customer advances as a source of

finance.

2. On the other hand, developers in the commercial real estate segment first have to

construct and then lease or sell the property. Hence they have to bear the risk

themselves. Increased volatility in commodity prices and problems in land

acquisition have increased input related risks for developer.

3. The prices of major inputs namely cement and steel are expected to increase apart

from the increase in the excise duty.

Government policy:

1. With the importance of the sector in aiding gross fixed capital formation and

employment generation, the government had recently relaxed norms for FDI in real

estate.

2. Funding by banks for commercial real estate used to be assigned a risk weight of 150

per cent which has a major deterrent in the financing of commercial projects.

However the reserve bank of India has relaxed the risk weight from 150 per cent to

100 percent for loans given to real estate companies by the bank. This change in risk

weight is expected to boost fund availability for commercial developers in long term.

3. While the urban land ceiling and regulation act(ULCRA) and rent control act(RCA)

have created scarcity of land in urban markets, other regulations such as coastal

regulatory zone (CRZ), mill land regulation and property taxes and stamp duties have

further affected growth in real estate.

Fiscal policy:

25

1. In union budget 2009-10, the tax holiday for software companies in software

technology parks was extended by one year. Foreign direct investment norms have

been relaxed for this sector.

2. But in the union budget 2011-12 a levy of 18.5 % minimum alternate tax on

developers of special economic zones has been proposed which will negatively

impact the sector. Also the tax holiday for software companies are major drivers of

demand for office space in urban areas.

Risk factors:

1. Impact on profitability on account of cost and time overturns due to the volatility in

land prices, disputes in title, eviction of tenants.

2. High finance cost

3. Adverse economic conditions

Step 5: Calculating applicable interest rate and tenure:

The applicable rate of interest in decided based on credit rating secured by the borrower.

Table 22 shows the applicable spread that can be applied under various rating obtained.

Table 23 Applicable spread

Credit rating under CRRM Applicable spread for commercial real estateA++ 6.5%-7%A+ 7.25%-7.5%A 7.5%

B++ 7.5%B+ 7.5%B 7.5%C 7.5%

Step 6: Working capital assessment

Working capitals limits are asked in order carry out day to day operations of the bank. There

are 3 methods used by the bank for the purpose of assessment of working capital

requirements.

The working capital gap can also be funded using bank facility like overdraft or open cash

credit. Each type of financing has its own pros and cons. It is up to the management team of

26

the company to decide which type of funds they would want to avail. For the purpose of

availing working capital facilities assessment needs to be done. This assessment of Working

capital assessment would be done as prescribed by RBI depending upon the applicability.

Turn over method or I method: The bank is following Turnover method for assessment of

credit limits for all sectors (manufacturing & trading) with fund based working capital limits

up to Rs. 6 crore from the banking system. Under this method three months of turnover is

financed as working capital irrespective of level of inventories, maintained by the

constituent.

Banks finance can be availed up to 75% of the working capital gap. The rest 25 % should be brought out from long term sources of funds. Under this method working capital eligibility has to be arrived based on 25% of turnover projected less 5% of turnover or actual NWC available whichever is more. If actual NWC is less than required NWC, the borrower has to bring in the shortfall and sanctioning Authority has to ensure the same. Actual NWC means NWC available as per latest audited balance sheet. The assessment of working capital limits should be done both as per Turnover Method and Inventory Method and higher of the two is to be sanctioned depending upon the need. Table 24 shows the methodology followed under Turn over method.

Table 24 Turn over method calculations

II method of working

capital assessment:

Under this method

the borrower should

provide for at least

25% of the current

assets from long term sources of funds (equity and long term loan). This also means that total

of current assets including banks borrowings should not exceed 75% of the current assets.

Under this system current assets and current liabilities are calculated. The gap between

current assets and current liabilities is called as working capital gap. Then the procedure

explained in the table below is followed by the bank in calculating the working capital

requirement or Maximum bank permissible funds (MPBF). Table 25 gives the methodology

followed under second method.

27

Turn Over MethodA. TurnoverB. 25% of (A)C. Margin Required at 5% of (A)D. Margin (NWC)E. (B - C)F. (B-D)G. MPBF ( E or F whichever is lower)H. Excess borrowing

Table 25 II method calculationsA) Current Assets( without bank funds)B) Current liabilities(Without bank

funds)C) Working Capital Gap ( A-B)D) Minimum stipulated. NWC (25% of

CA excl. Export receivables)E) Actual/Projected NWCF) Item C Minus Item DG) Item C Minus Item EH) Eligible Credit (Item F or G

whichever is lower)

Cash budget method: This method is used in calculating cash deficit that exists throughout

the year. This method is also used in seasonal sectors such as agro-based like sugar, food,

tea, tobacco, fertilizers and etc. This method is also applicable to seasonal industries such as

air conditioning, cotton textiles. This method is also applicable for construction industries.

For the before mentioned industries other method of working capital assessment or II method

are not applicable as the fluctuation levels of current assets and current liabilities in high.

Under Cash budget method maximum gap between total receipts and total payment is

covered by the banks finance. Disbursement are allowed based on monthly cash budgets

The borrower is a builder and contractor and the working capital assessment is worked out

based on the cash budget method.

28

Table 26 Cash deficit method of the borrower

Month Surplus/DeficitApr-11 -700.93

May-

11 -700.63Jun-11 -700.31Jul-11 -700.14

Aug-11 -700.24Sep-11 -700.57Oct-11 -700.16

Nov-11 -700.12Dec-11 -700.15Jan-12 -700.27Feb-12 -700.49Mar-12 -700.86

The maximum deficit is 7.01 crores in noticed during the months as can be seen from table

26. The borrower is eligible for SOD limit of Rs 7 crore.

The firm requested for sanction of SOD limit of 7 crores at finer rates of 7 crore as they are

executing projects of 23.3 crores apart from the proposed OMR project cost of Rs 29.99

crore

The firm working capital limits are renewed by Head Office, where in the enhancement of

SOD limit from 4.5 crores to7 crores was not considered in view of the NIL sales booked in

the year 2010-11. Branch/Zonal office recommends for enhancement of SOD limit from 4.5

crores to 7 crores keeping in view the various projects on hand.

Step 7: Credit investigation, due diligence & verification of defaulters list:

Whenever credit limits are requests are to be considered, it is necessary to conduct a credit

investigation before taking up such proposals for evaluation. This process of preliminary

study needs to be undertaken invariably before detailed evaluation.

a) Areas of credit investigation:

29

Integrity of the borrower has no substitute. Before entering into any agreement with the

borrower it is very imperative that the bank understands the borrower and his propose

properly. Banks generally carry out interviews with the borrower and enquire about his past

record, details of associates, sister concerns and etc. Apart from quantitative aspect like past

financials, qualitative aspects such as market reputation are also checked. ‘Know your

customer’ principle is equally important in the case of borrower. If the bank comes to know

about the unethical practices and illegal activities with which a firm or borrower is linked

then the bank tries to distance itself from the borrower. Pre sanction and post sanction of unit

are also a part of credit investigation.

b) Defaulters list:

It is mandatory for the bank to cross the names of borrowers with that of the names in the

previous wilful defaulters list. Table 27 gives the list of defaulters list to be checked.

Table 27 Defaulters list

Name of the list Yes/NoRBI defaulters list dated March 2011(Rs 1 crore and above) noCaution list dated June 2011 noWilful defaulters list dated June 2011,(Rs 25 crore and

above) noECGC SAL list dated 12.12.2011 noCIBIL suit filed Rs 1 core and above 30.06.11 noCIBIL suit filed (wilful) Rs 25 lakhs and above 30.06.2011 no

Areas of strengths and weakness of the borrower

Strengths: The managing director Mr AAA is in this line of activity for more than a decade.

He is also a qualified civil engineer. The overall conduct obtained by borrower in table 28.

Weakness:

1. All partners are from single family

2. Normal business competition which can be, however be overcome by maintaining

quality in the works better customer care and the reputation it has built up for itself

all over the years.

30

3. Heavy competition, government policies, natural calamities will influence the

industry and the damages if any costs heavily

Table 28 conduct of the borrower

ABILITY CONDUCT REPUTATION CONDITIONcapable prudent shrewd sound

experienced steady honest progressiveincapable conservative tricky stagnant

inexperienced overtrade dishonest decliningspeculative

Step 8 Financial analysis and compliance:

Key financial Indicators: Table 29 shows various key financials obtained.

Table 29 key financial indicators

Audited Audited Projection Audited provisionalFinancial indicators 31-03-2009 31-03-2010 31-03-2011 31-03-2011 31-09-2011Net sales 1.33 7.34 0 0 3.03Other income 0 0.04 0.11 0.14 0.08Profit before tax 0.14 0.25 0.97 0.39 0.92Profit after tax 0.12 0.24 0.97 0.39 0.92Depreciation 0.04 0.05 0.06 0.06 0.03Cash generation 0.16 0.29 1.03 0.45 0.95paid up capital 1.65 2.43 6.15 6.25 7.07Tangible net worth 1.65 2.43 6.15 6.25 7.07Adjusted TNW 4.07 Gross Fixed assets 0.32 0.51 0.45 0.48 0.42Net fixed assets 0.28 0.46 0.39 0.42 0.39Term liabilities 2.93 1.27 2 1.99 2.51Banks 0.25 0.21 1.9 1.9 1.18Friends and relatives 2.68 1.06 0.09 0.09 1.33Investments 0 0 0 2.18 0Current assets 8.1 10.03 22.18 20.99 26.87Current liabilities 5.98 8.97 16.61 15.35 19.91Net working capital 2.12 1.06 5.57 5.64 6.96Current ratio 1.35 1.12 1.34 1.37 1.35TOL/TNW 5.4 4.21 3.02 2.77 3.17Adjusted TOL/TNW 4.26 Debt equity ratio 1.78 0.52 0.32 0.32 0.35Interest coverage ratio 1.43 1.6 3.31 2.05 3.06

31

Net profit / net sales 9.02 3.27 3.29(Table 29 contd.)

As can be seen from the above table, the key financials are presented. Table 30 gives remarks on key financials.

Table 30 Remarks on key financial indicatorsRemarks on retained profits The firm retained 100% of the profit earned

during the year 2009-10 in the business. The

firm has introduced additional capital of Rs

3.50 crore during 2010-11Remarks on tangible net worth TNW of the firm increased from Rs 2.43

crores as on 31.3.10 to Rs 6.25 crores as on

31.3.2011 due to retention of profits and

infusion of capital of Rs 3.50 croresRemarks on Net working capital The NWC has increased from Rs 1.06 crores

as at 31.3.2010 to Rs 5.57 crores by

31.3.2011. The increase in the NWC is due to

retention of profits of Rs 3.50 crores and

increase in tem liability.Remarks on Current ratio The current ratio of the firm as at 31.3.2011

is 1.37 and satisfactory which is above the

minimum required level of 1.33Remarks on Total outside liabilities to TNW TOL/TNW as at 31.3.2010 is 4.21 and as at

31.3.2011 is 2.77. The decrease in the ratio

is on account of increase in TNW due to

infusion of additional capital into the firmRemarks on debt/equity ratio Debt equity ratio marginally improved from

0.52 as on 31.3.10 to 0.32 as on 31.3.2011 on

account of increase in TNWRemarks on interest coverage ratio Interest coverage stood at 2.05 as per ABS

31.3.2011 and is satisfactoryRemarks on Investment/advances to associate

concerns

The firm owns a property at Gandhi bazaar,

Bengaluru and is shown as investment,

amounting to Rs 2.18 croresRemarks on diversion of funds There is no diversion of funds from short

term sources to long term uses in the FY

32

2011Remarks on borrowings from friends and

relatives

Unsecured loans reduced from Rs1.06 crores

as on 31.3.10 to Rs 0.09 as on 31.3.11Remarks on overdue statutory liabilities NilRemarks on contingent liabilities not

provided for

Nil

Remark on EPS and share value Not applicableDoes the account show sign of incipient

sickness

No

(Table 30 contd.)

Achievability of estimated/Projected production sales

Table 31 sales receipts

Year

Actual/estimate

s Receipts2008-2009 Actual 1.332009-2010 Actual 7.342010-2011 Actual 030.09.201

1 Provisional 3.032011-2012 Estimates 21.322012-2013 Projection 21.75

Table 31 provides the details of sales achieved and projected. The firm has estimated sales of

Rs 21.32 crores for the year ending 31.3.2012 and projected Rs 21.75 crores for the year

ending 31/3/2013.

33

The recessionary trend is slowly reversing and the projections can be achieved as they are

having sufficient projects on hand and new OMR projects.

During the year 2010-11, the sales booked are Nil. The profit after tax is 0.39 crores. The

firm has three ongoing projects at Old Mahabalipuram road, Chennai. The firm has

recognised 10% profit on the total cost incurred on the above projects after deducting

administrative and other expenses.

Auditor’s comments: Auditors comments are submitted by the auditors after going through

the financials of the company. Table 32 gives the details of the auditor’s comments

submitted by the borrower. Auditors comment on the company’s balance sheet:

34

Table 32 Auditors comments1 On revaluation of fixed

assets

Nil

2 On change of method of

depreciation

Nil

3 On loans and advances given

to the concerns within the

group

Nil

4 On position of unserviceable

stores/obsolete stock

Nil

5 On position of overdue /

irrevocable debtors

Nil

6 On disputed liabilities not

provided for

Nil

7 On valuation of inventory Nil

8 Others Nil

Step 9 Term and conditions:

Special terms and conditions:

1. Disbursement of term loan shall be based on the work completion certificate by our

approved engineer and CA certificate for the amount spent on the project. The release

of term loan shall be in the ratio 1:1:2 i.e. capital: booking money: term loan.

2. Branch has to maintain ESCROW account to credit the proposed sale proceeds of the

shops for term loan I and a separate ESCOW account for lease rentals for repayment

of term loan II.

3. As and when the sale of the commercial establishment takes place and advance

amount is received, the company shall remit the same into ESCROW account and

any amount received in excess of rupees 7.49 crore shall be utilised for repayment of

the loan. Our bank will have a charge on the ESCROW account and withdrawal from

35

escrow account will first be for the payment of interest on the term loans and towards

repayment of the term loans availed.

4. The binding letter of intent is duly modified by extending the due date of handing

over the possession to the cinipolis by the applicant builder as there might be delay in

handing over the project.

5. Branch may be permitted to issue NOC after repayment of Rs 5000 per sft and to

release the proportionate mortgaged land/undivided share along with shops to be

registered in favour of the customers duly ensuring availability of sufficient security

coverage to the loan amount outstanding at the time of each realization

Pre disbursement conditions:

Before seeking the disbursement of term loan or SOD, the firm has to comply the

following:

1. The owners Mr zzz and his wife shall execute a sale deed alienating their 50% share

of undivided land in favour of M/S builders, and the firm should offer the said

property as security.

2. The firm to submit a notarised letter of undertaking to the bank to the effect that the

firm/builder should not alienate or encumber any part or parts of the 50% share of the

property sold to them without written consent from the bank.

3. The owners of land to give a notarised letter to the bank to the effect that the GPAs

dated 17.10.2007 and 09.07.2008 are valid and subsisting and they will not be

cancelled till the completion of project.

4. The lessee to the firm M/S kkk India PVT limited who had executed binding letter of

agreement on 7.10.2010 shall inform the bank by the way of letter of

acknowledgement that the Binding letter of agreement (BLA) dated 7.10.2010 has

been approved by their Board and the same is subsisting and agreed to execute

agreement to lease as per terms of BLA.

Issues raised by the HO:

36

1. The personal guarantee of all persons giving their property as security against loans

to the firm to be obtained.

2. The party to agree for applicable rate of interest, no logic of concession for

commercial property as risk is high.

3. Promoters to bring more equity and the loan to be reduced proportionately. No

deviation in margin money is desirable.

4. Nothing is mentioned about clear and marketable title, how the firm will mortgage 50

% share of the land when they have not paid for it upfront. Land owners should join

as co-borrowers.

Reply by the Zonal office Chennai:

1. The personal guarantee of all the persons giving their property as security against the

loan to the firm will be given and the land owners will give guarantee limited to the

value of property being mortgaged by tem. As and when sale of office space is

affected the guarantee of the owners is to be reduced proportionately.

2. The firm is agreeable to rate of interest levied by the bank.

3. The form agreed to bring in margin of Rs 149895 lakhs and also bring additional

margin as decided by us.

4. The total extent of land where the office space and multiples is proposed is 45306 sft

out of this, 16954 sft being the undivided share of land pertaining to multiplex will be

transferred to the applicant firm by the way of sale deed and the same deposited by

the firm. An extent of 7248 sft being the proportionate undivided share of land

pertaining to the office space will be mortgaged by the present owner of the land to

the extent of sales made; the bank is requested to issue NOC for building and

corresponding undivided share of land.

5. ZO recommends for sanction of term loan for Rs 7.32 Cr (reduced from 8 crores) and

TL II for 7 crores.

37

38

ResultsCredit risk rating results

The borrower is rated as B as per CRRM. The applicable rate of interest for the term loan is

BR+7.50+TP. Borrower is requesting rate of interest for term loan at BR+4+0.25

i.e.10.75+4+0.25=15%. TP here stands for Term premium. The value of TP is 0.25 is a fixed

value and is applicable only when the tenure of credit facility is greater than 3 years. Table

33 and and table 34 show the ratings obtained by the borrower.

The borrower is rated B under CRRM as per ABS. The credit rating rationale is furnished

below:

Table 33 Rating given to the borrower

Parameter Score RatingA)Financial risk evaluation 3.04 B+B)Business risk evaluation 1.46 CC)Industry risk evaluation assessment 3.1 B+D)Management evaluation 3.35 B+E)Security/conduct of accounts 5.25 A+Overall rating including facility 2.89 BProjected risk evaluation 2.33 COverall rating including facility &

project 2.84 B

Apart from the above ratings as per CRRM, the ratings mentioned below are also obtained.

Table 34 Other ratings

Internal company rating: 2.72 BCompany rating(w/o size criteria) 2.76 BCompany rating(with size criteria) 2.76 B

DSCR results:

39

DSCR ratio has been calculated for the using the past and projected data. DSCR results

obtained have been shown in table 35.

Table 35 DSCR estimations

YEAR DSCR ratioMar-11 provisional 1.77Mar-12 estimates 2.03Mar-13 estimates 1.6Mar-14 estimates 1.51Mar-15 estimates 1.41Mar-16 estimates 1.42Mar-17 estimates 1.73Mar-18 estimates 2.13Mar-19 estimates 2.56

Average DSCR=1.8. This means that the company will be able to service its debt effectively.

Sensitivity analysis results:

Sensitivity analysis results are given below. In sensitivity analysis the variations in DSCR

are found out by varying the input parameters such as cost of production, sales and interest

rate. The table below gives the sensitivity details. Results obtained in sensitivity analysis

have been shown in table 36.

Table 36 Sensitivity Results

Sensitivity analysis DSCRParameter Average Min MaxNormal 1.77 1.41 2.565 % increase in cost of production 1.36 1 215% decrease in receipts/sales

realization 1.76 1.37 2.45Increase on TL & WC increase by 2.5% 1.67 1.33 2.42

1. According to the policy, DSCR ratio should be given 1.5 to 2.

2. It is observed that the activity in insensitive to the extent for the given situation for

the above level of variations and the firm will be stable to service the interest

40

/instalment of the term loan and working capital. Normal weighted average DSCR is

1.71 which is comfortable and complied with policy guidelines.

Working capital Results:

Build up net working capital: For financing working capital long term sources such as equity

and term loans are made use of. Table 37 gives the working build up, which has been done

by adding funds from long term sources and deducting funds to long term used.