creation to value realisation our 2020 vision/media/files/g/green-dragon-gas/...creation to value...

TRANSCRIPT

Green Dragon Gas

Creation to Value Realisation

Our 2020 Vision

Capital Markets Day

April 27, 2016

“20 Years of CBM in China” www.greendragongas.com

LSE: GDG.LN

Creation to Value Realisation: Our 2020 Vision

Disclaimer

This presentation does not constitute an invitation to underwrite, subscribe for, or otherwise acquire or dispose of any shares of Green

Dragon Gas Ltd. (the “Company”) in any jurisdiction. The Company’s shares have not been and will not be registered under the US

Securities Act of 1933 (the “Securities Act”) and may not be offered or sold within the United States absent registration under the

Securities Act or an exemption from registration.

The information contained in this presentation is given in good faith but no representation or warranty is made in relation to the accuracy

or completeness of the information, or any oral information provided in connection therewith, or the data it generates and no

responsibility, obligation or liability is or will be accepted by the Company or its affiliates or advisors or by any of their respective officers,

employees or agents in relation to it.

This presentation contains certain forward looking statements with respect to the financial condition, results, operations and businesses

of the Company. The statements and forecasts involve risk and uncertainty because they relate to events and depend on

circumstances that will occur in the future. There are a number of factors that could cause actual results or developments to differ

materially from those expressed or implied by these forward looking statements and forecasts.

Past performance is no guide to future performance and persons needing advice should consult an independent financial advisor.

This presentation and the information contained in it are confidential and should not be distributed, published or reproduced, in whole or

in part, or disclosed by recipients directly or indirectly to any other person.

-2-Creation to Value Realisation: Our 2020 Vision

Capital Markets Day

• Introduction………………………………Randeep S. Grewal, Chairman & CEO

“Creation to Value Realisation”

• Financials ………………………………Tim Eastmond, Chief Accounting Officer

• Operational Review & Update………..Jorg Kohnert, Chief Operating Officer

• Our Vision to 2020 …………………….Randeep S. Grewal, Chairman & CEO

• Q&A

• SCADA online

Agenda

Creation to Value Realisation: Our 2020 Vision -3-

Introduction

Creation

• Through 20 years of hard work on the shoulders of a relentless and committed workforce we have:

• Built strong acreage position• De-risked 25 Tcf of gas resources

• Develop technology with proven results

“Creation to Value Realisation”

Value Realisation

• 2020 Vision outlines the steps to realising value for our shareholders through:

• Asset appropriate funding structure and shareholder liquidity

• Upstream focused• Monetise value forward through on farmouts - NPV

-4-Creation to Value Realisation: Our 2020 Vision

Creation to Value Realisation: Our 2020 Vision

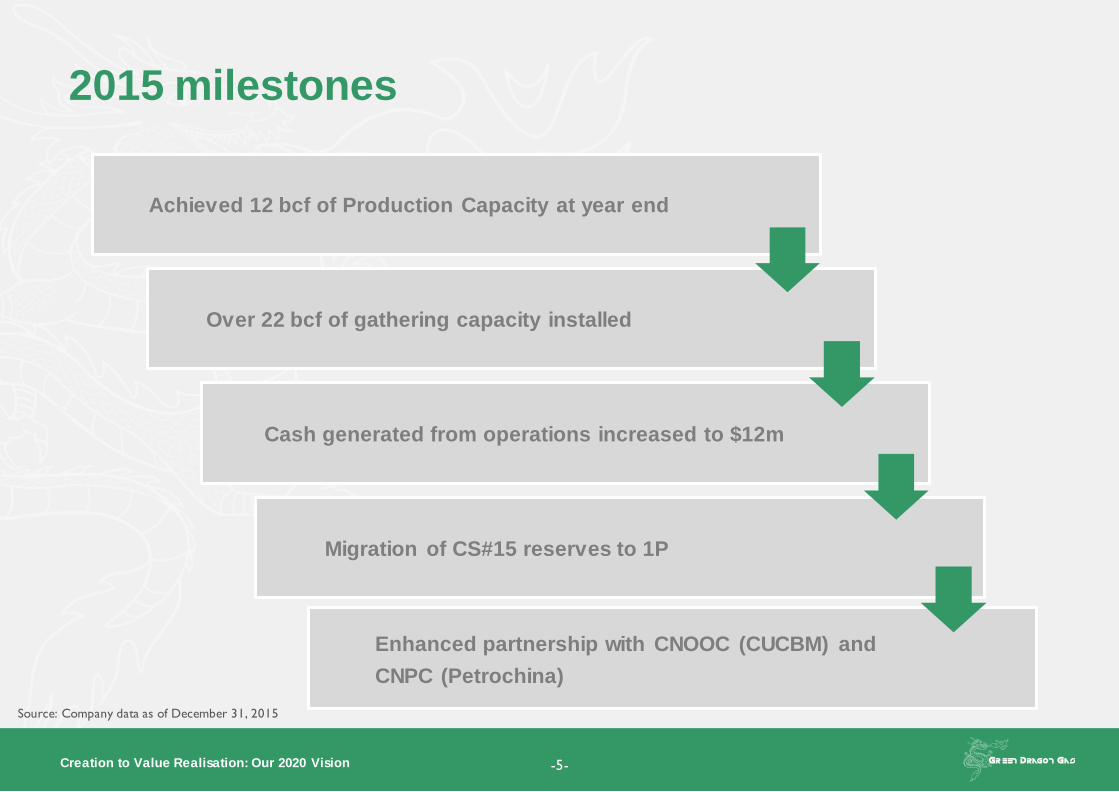

2015 milestones

Source: Company data as of December 31, 2015

Achieved 12 bcf of Production Capacity at year end

Over 22 bcf of gathering capacity installed

Cash generated from operations increased to $12m

Migration of CS#15 reserves to 1P

Enhanced partnership with CNOOC (CUCBM) and

CNPC (Petrochina)

-5-

Creation to Value Realisation: Our 2020 Vision

GDG – a snapshot

Focus on production and cash flow

• Exceeded 2015 annual production capacity target of 12 bcf

• Investment in infrastructure – converting production potential to sales

• Monetising invested capital to enhance shareholder return

• CNOOC significantly advancing infrastructure build on GSS in line with

commitments

• GCZ providing consistent cash flow following cost recovery by CNPC

2016 – A transformational year

• Build on production success through additional well connections and

infrastructure

• Coal Seam 15 to compound reserve growth and production potential

• Target 16 bcf gross annual production rate

• Significant sales and production increases from existing wells

“Connections are everything…”

-6-

Creation to Value Realisation: Our 2020 Vision

Leading China CBM independent

Large reserves base • Largest publicly listed CBM reserves base in China: 1P: 173 bcf; 2P: 549 bcf; 3P: 2,379 bcf*

• Reserves independently verified by 10 consecutive CPRs

• Six Inland Production Sharing Contracts covering 1,869,599 acres (7,566 km² )

• Ongoing migration to 1P reserves: 17% increase at year-end 2015

Integrated operations and strong partners• Strong, highly capitalised Chinese partners: CUCBM (CNOOC), CNPC and PetroChina

• Proven PSC titles: Protected by Netherlands-PRC Bilateral Investment Treaty

• Equity participation in over 2,037 wells

Centrally located among China’s gas consumers

• Multiple routes to monetise gas: GDG-owned refuelling stations, industrial customers, multiple

gas pipelines, sales via electricity

Experienced leadership and strong corporate profile

• Highly experienced operational management team with a track record in Coal Bed Methane

• High quality shareholder base: includes Aberdeen, Chandler Corp, Fidelity, Platinum Asset,

GIC, Management

8Blocks

$4.0bn2P Reserves

2,037Drilled Wells

1.9macres

*YE2015

-7-

Financials

Tim Eastmond

Chief Accounting Officer

Creation to Value Realisation: Our 2020 Vision

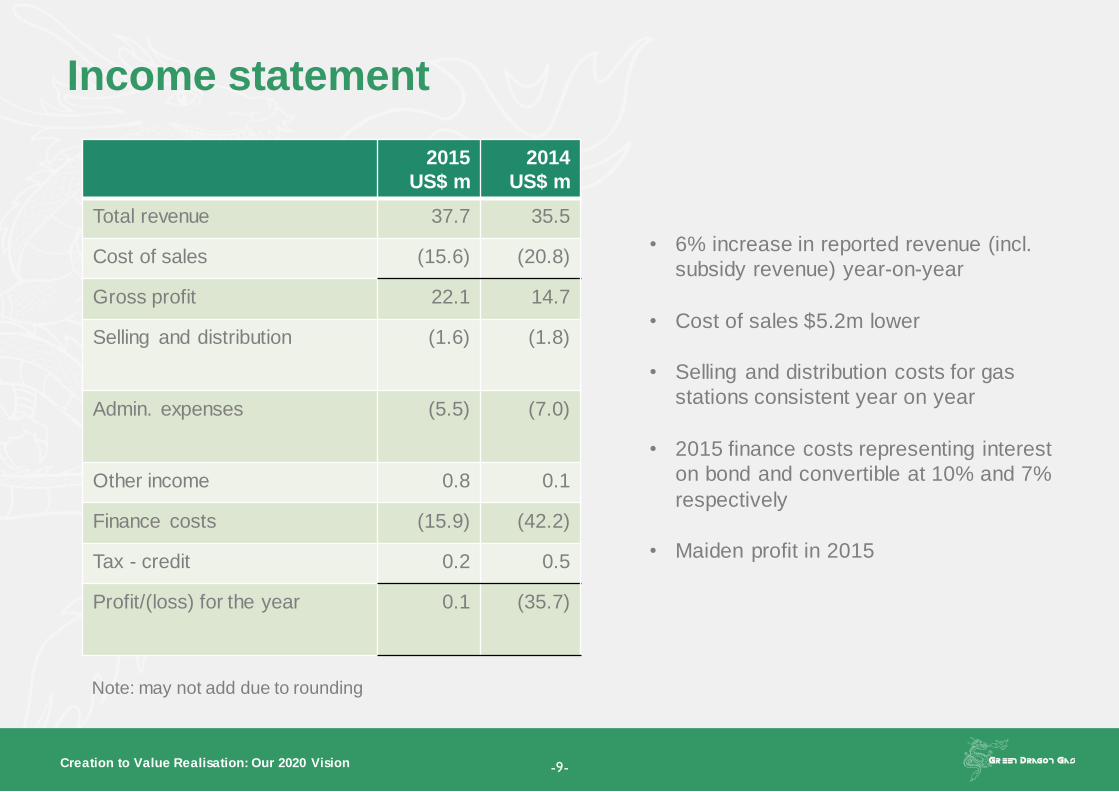

Income statement

2015

US$ m

2014

US$ m

Total revenue 37.7 35.5

Cost of sales (15.6) (20.8)

Gross profit 22.1 14.7

Selling and distribution (1.6) (1.8)

Admin. expenses (5.5) (7.0)

Other income 0.8 0.1

Finance costs (15.9) (42.2)

Tax - credit 0.2 0.5

Profit/(loss) for the year 0.1 (35.7)

• 6% increase in reported revenue (incl.

subsidy revenue) year-on-year

• Cost of sales $5.2m lower

• Selling and distribution costs for gas

stations consistent year on year

• 2015 finance costs representing interest

on bond and convertible at 10% and 7%

respectively

• Maiden profit in 2015

Note: may not add due to rounding

-9-

Creation to Value Realisation: Our 2020 Vision

Balance sheet

2015

US$ m

2014

US$ m

PP&E 272.0 157.6

Exploration assets 1,043.9 1,157.9

Other 5.2 5.6

Current assets 51.5 103.2

Total assets 1,372.6 1,424.4

Current liabilities 15.4 22.2

Convertible notes 48.3 47.2

Bonds 86.8 85.1

CUCBM provision 370.2 367.0

Deferred tax liability 154.3 163.5

Total liabilities 675.2 685.0

Net assets 697.4 739.3

• PP&E increase on GSS transition to

production and recording CUCBM

investment

• Cash on hand of $26.9m

• Total assets decreased due to

exchange on translation

• CUCBM provision increased due to

2015 expenditure to be recovered

• Net assets reduced entirely due to

exchange on translation from

functional currency

Note: may not add due to rounding

-10-

Creation to Value Realisation: Our 2020 Vision

Cash flow

2015

US$ m

2014

US$ m

Operations

Cash from ops 20.1 5.4

Cash after working cap

and tax

12.4 0.6

Investing

Expln. activities (42.3) (39.8)

Other (5.2) (53.8)

Total investing (47.5) (93.6)

Financing (12.3) 139.0

Net inc/decrease (47.3) 46.1

Exchange (5.8) (0.7)

Closing cash (26.9) (80.0)

• Cash from operations increases

to $12.4m

• Operating cash includes initial

receipts from GCZ following cost

recovery by CNPC

• Increases investment in

exploration and production assets

• 2014 investing includes one-off

Conoco settlement of $40.0m

• Financing cash flow in 2015

represents interest paid on bonds

entered on 2014

• Financing inflow in 2014 due to

new bonds

Note: may not add due to rounding

-11-

Creation to Value Realisation: Our 2020 Vision -12-

Inflection Point

-10,000

-5,000

0

5,000

10,000

15,000

1H 12 2H 12 1H 13 2H 13 1H 14 2H 14 1H 15 2H 15

Profit from Operations (US$'000)

Creation to Value Realisation: Our 2020 Vision

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2012 2013 2014 2015

Revenue, including subsidy Cash from operations

2012-2015 - Strong underlying revenue

and cash performance

• Consistent revenue growth and

improving cash performance

year-on-year

• Cash from operations at $12.4m

• Further production and

infrastructure enhancements to

drive cash flow in 2016

-13-

Note: Normalised to take into account one-off events

Creation to Value Realisation: Our 2020 Vision

Reserves

case

2016

Capex

2017

Capex

2018

Capex

Total

capex

NPV 10

US $ m

1P 74.6 39.9 Nil 114.5 1,227.2

2P 178.0 171.9 2.8 358.8 4,022.0

Unlocking value – discretionary capex investment

-14-

• Significant value in reserves base

• Target RBL funding on approval of ODP for development capital

• Continuing to pursue farmout opportunities in exploration areas

Source: NSAI 2015 independent reserves report

Creation to Value Realisation: Our 2020 Vision

Track record of delivering value through investment

0 100 200 300 400 500 600

2015

2014

2013

2012

bcf2P 1P

86%

6%3%5%

2P reserves distribution

GSS

GCZ

GSN

GFC

• GDG has consistently provided reserves

growth year on year through investment

• Further investment in 2016 and 2017 unlock

significant additional NPV 10 value

• Capex for NPV 10 case is modest at $114.5m

• Moderate additional investment transforms

the business – moving to self-sustaining from

operations

• Potential in multiple blocks

• 86% of 2P reserves from 5% of land bank –

significant 2P growth potential

Annual Audited Reserve values (bcf)

2P Reserves Distribution (%)

-15-

Creation to Value Realisation: Our 2020 Vision -16-

Long term value creation

What Next? - 1P Development Plan

Creation to Value Realisation: Our 2020 Vision

ODP Process

-17-

Weeks 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 …… 26

ODP Application Letter (5 Copies) 7d

Economical Model compile (Waiting for SA) 35d (for finalizing SA)14d (complete

the model)

Finalize Main ODP Draft Waiting for Economic Model 7d

Specialists Review Main ODP Draft 7d

Revise ODP Draft Base on Specialists Suggestions 7d

Submit ODP to CNOOC Investment Committee 28d

Environmental impact assessment 49d

Energy Conservation Review 14d

Financial statement and capital credit certificate 21d

Resolution of Board of Directors for Additional Share 21d

Submit Main ODP Report to NDRC for Approval 94d

Operational Review & Update

Jorg Kohnert

President and Chief Operating Officer

Creation to Value Realisation: Our 2020 Vision

Corporate Social Responsibility

Commitment to the environment

• Zero use of harmful chemicals

• Own gas to generate power for operations

• Clean water as a by-product of production for irrigation or consumption

• Use of biodegradable drilling mud

• No recorded environmental incidents

-19-

Commitment to the community

• Drilling of water wells for local villages

• Maintenance of local infrastructure

Commitment to our people

• Zero lost time incidents in 2015

• In depth HSE policy and continuous training

• Ongoing commitment to safety

Creation to Value Realisation: Our 2020 Vision

Upstream asset portfolio: 6 PSCs over 8 Blocks

Xinjiang

Tibet

Qinghai

Inner Mongolia

Heilongjiang

Jilin

Liaoning

Beijing

Hebei

ShandongNingxia

Gansu

Shanxi

Shaanxi

Jiangsu

HubeiShanghai

Zhejiang

Fujian

Jiangxi

Guizhou

Sichuan

YunnanGuangxi Guangdong

Hong Kong

Anhui

Hunan

Chongqing

Tianjin

Qinyuan PSC

(GQY PSC)

3,665km2

Baotian-

Qingshan

PSC (GGZ

PSC) 947km2

Fengcheng PSC

(GFC PSC)

1,541km2

Shizhuang South

PSC (GSS PSC)

388km2

Shizhuang

North PSC

(GSN PSC)

375km2

Chengzhuang

Block (GCZ

Block) 67km2

Existing main gas pipelines

CNG mother stations

Group CBM blocks

Capital of province

Henan

Panxie East PSC

(GPX PSC)

584km2

P Production

D Development / Pilot stage

EA Exploration & Appraisal

P

P

D

EA

EA

EA

EA

Both included under Shizhuang South PSC

GSS

GDG interest: 60%

Partner: CNOOC

Operator: GDG

1P/2P/3P: 153/473/1,379 bcf

GCZ

GDG interest: 47%

Partner: PetroChina

Operator: PetroChina

1P/2P/3P: 15/31/52 bcf

GSN

GDG interest: 50%

Partner: CNOOC

Operator: CNOOC

1P/2P/3P: 5/18/721 bcf

GQY (A)

GDG interest: 10%

Partner: CNOOC

Operator: CNOOC

1P/2P/3P: N/A

GQY (B)

GDG interest: 60%

Partner: CNOOC

Operator: GDG

2C: 17 bcf

GFC

GDG interest: 49%

Partner: CNOOC

Operator: GDG

1P/2P/3P: N/A /26/228 bcf

GPX

GDG interest: 60%

Partner: CNOOC

Operator: GDG

Best Prospective: 16 bcf

GGZ

GDG interest: 60%

Partner: PetroChina

Operator: GDG

Best Prospective: 416 bcf* Total wells is inclusive of non operated wellsReserves by Netherland, Sewell & Associates, Inc as of December 31, 2015

EA

D

-20-

Creation to Value Realisation: Our 2020 Vision -21-

2015 Operational Statistics

Exploration and Production

• GDG operated 322 wells at year-end

• 13 LiFaBriC wells drilled and 27 connected to sales infrastructure in 2015

• Total of 46 LiFaBric wells selling in GSS at year end

• 2015 gross production of 10.3bcf and an exit capacity of 12.12 bcf per year

Sales Gas Volumes

• Total gross sales for 2015 of 3.7 bcf

• 1.8 bcf of PNG sales in GCZ

• 1.1 bcf of PNG sales in GSS

• 0.7 bcf of CNG sales

• 0.17 bcf of Gas to Power sales

Source: Company data as of December 31, 2015

Creation to Value Realisation: Our 2020 Vision

• 25 bcf, 40 bcf and 694 bcf of 1P, 2P and 3P

reserves booked respectively

• 1P and 2P NPV grew by US$197m and

US$850m respectively

• 132 bcf, 276 bcf and -244 bcf of 1P, 2P and

3P reserves booked

• 1P, 2P and 3P NPV grew by US$977m,

US$2.5bn and US$877m respectively

• 900 bcf of 1P production

• NPV value of US$8bn

• Migration of exploration block into 1P

• 1P capex of US$1bn

Reserve Progression

2006-2010

2011-2015

2016-2020

-22-

2010 reserves (GSS Example)

CS#3 CS#15

CS#3 CS#15

2015 reserves (GSS Example)

2020 reserves (GSS Example)

CS#3 CS#15

Creation to Value Realisation: Our 2020 Vision

Infrastructure – GDG Operated GSS Block

-23-

Creation to Value Realisation: Our 2020 Vision

Recent Achievements – Pipeline Compression

-24-

Creation to Value Realisation: Our 2020 Vision

Recent Achievements – Example Circuit 3

• Prior to optimisation, the circuit contained 4

compressors with compression capacity of

300kW

• 6 compressors were brought online in January

2016 to bring compression capacity to 570kW

• Wells on circuit were bypassed to optimise flow

• Sale volumes increased from 1.04MMcf to

1.68MMcf representing a 60% volume increase

circuit 3 production (mcf/d)

-25-

Creation to Value Realisation: Our 2020 Vision

Real Time Operations Centre

Real time data for making real time decisions

• Monitoring of the entire production, gathering and downstream sales process

• Efficient and effective allocation of resources

• Advance warning of problems and ability to act instantaneously

-26-

Creation to Value Realisation: Our 2020 Vision

Real Time Operations Control Centre

• OCC can monitor and generate reports throughout

the entire operation

• Generate reports for data analysis and long term

planning

Sales

Production

-27-

Creation to Value Realisation: Our 2020 Vision

Ongoing SCADA Deployment

Well installation progress and forecast

Installation Status

SCADA meters and monitors installed at both the well head and rig site

allow for real time data feed of production volumes, water level, casing

pressure and visual inspection via CCTV to be received at the

centralised operation centre

-28-

Creation to Value Realisation: Our 2020 Vision

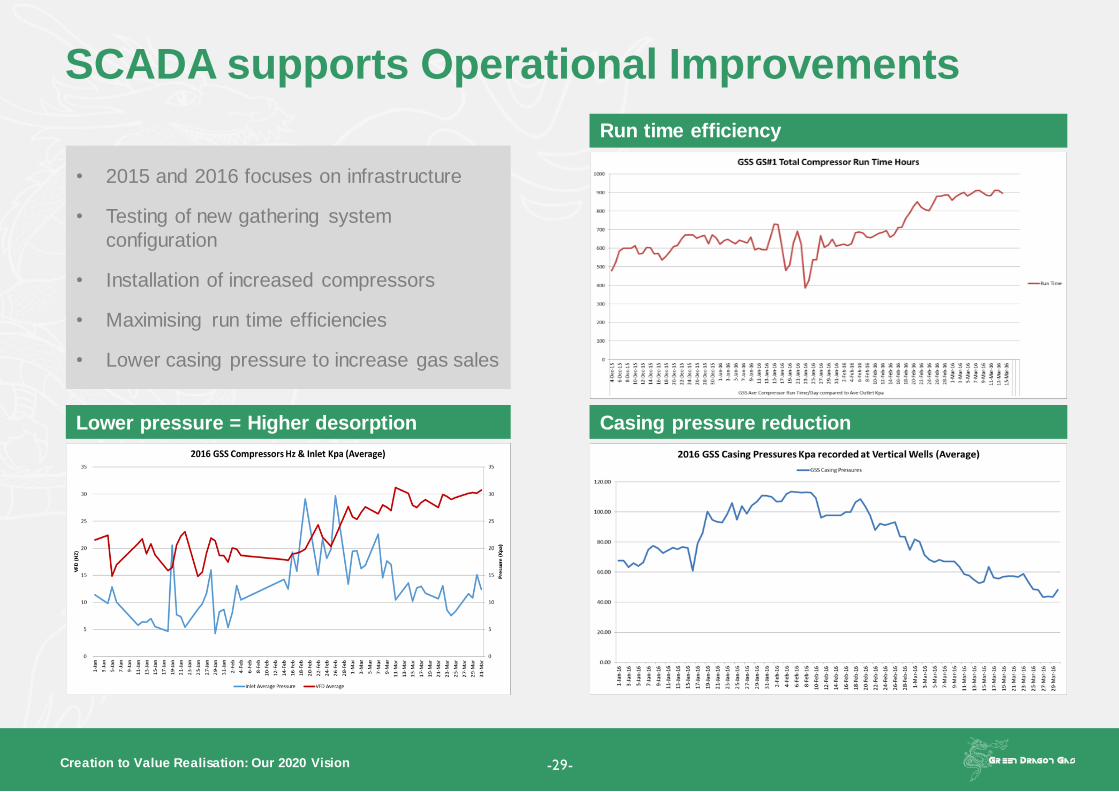

SCADA supports Operational Improvements

-29-

Lower pressure = Higher desorption Casing pressure reduction

• 2015 and 2016 focuses on infrastructure

• Testing of new gathering system

configuration

• Installation of increased compressors

• Maximising run time efficiencies

• Lower casing pressure to increase gas sales

Run time efficiency

Creation to Value Realisation: Our 2020 Vision

What next? – Screw Compressor

-30-

• Lower gas discharge temperature due to more efficient

cooling system

• Vacuum at well head

• Capable of operating with negative suction pressures and

discharges > 1.5 MPa

• Basic difference in wellhead vs centralised gathering

• Well-head located compressor eliminates pressure

drop in the suction line to the compressor

• Locating compressor at / near the wellhead provides

the lowest possible well head pressure

• Pipeline size efficiency Moisture – Well head compression

allows efficient removal of moisture from the gas stream

Creation to Value Realisation: Our 2020 Vision

What next? – Screw Compressor Initial Results

Completed the first test run of Greka's own Screw

Compressor on April 22, 2016.

Screw Compressor internal design

-31-

Well

GSS-188

W/H

pressure

Inlet

Pressure Flow rate

Before 145KPa 9KPa 152mcf/d

After 9KPa -35Kpa 225mcf/d

Creation to Value Realisation: Our 2020 Vision

What next? – Expanding and optimising Infrastructure

• Annual processing capacity of 22.81 bcf

• Shizhuang and Shizhuang #1 Stns complete on time

• CNOOC constructed pipe network >90% complete

• Ongoing tie-in wells to infrastructure

-32-

CNOOC Trunk Line (Existing)

CNOOC Branch lines (Existing)

CNOOC Branch lines (Construction)

GDG Trunk line

Greka IPF station

CNOOC Gathering Stations

Gathering Stations expected in 2017

Existing Gathering Stations

Station bcf Status

Greka IPF 6.5 Online

Guixian station 3.6 Online

Shizhuang station 1.4 Online

Shizhuang south #1 11.2 Online

Online & operating - subtotal 22.7

Shizhuang south #2 10.4 Ongoing

Shizhuang south #3 10.1 Ongoing

Shizhuang south #4 10.2 Ongoing

Total 53.4

Creation to Value Realisation: Our 2020 Vision -33-

Coal Seam 3 and 15 floor contour map in Zaoyuan area

What Next? – GSS – Reserve Migration for CS#15

Source: Company data

• Well defined coal seams #3 and #15

• 1st LFB drilled in CS15 encountered a 4m thick

coal

• Vertical intersection avoided penetration to

adjacent LST

• Well following standard dewatering progress

• Exhibiting casing pressure – a sign of gas

desorption

• GSS Block,CS15 has a GIP of 1.2 Tcf

• Total drilled and logged 80 wells in coal seam

CS15

• Distance between #3 & #15CS is 89-120m, Ave

106 m

Coal NO.Vitrinite

ReflectanceDepth Thickness Gas Content PERM Saturaton

(%) (m) cm³/g(daf) (md) (%)

3# 2.96 574.08 6.23 12.21 0.76 50.00

15# 3.01 698.67 4.53 17.51 0.22 61.00

Exploration

Jorg Kohnert

President and Chief Operating Officer

Creation to Value Realisation: Our 2020 Vision

Achievements• 7 producing wells

• 3 workovers completed

• GGZ Static Model 40% completed

Current Activities• 3rd Party data acquisition

• Seismic data interpretation and re-processing

• Stratigraphic correlations

Deliverables• 3D Static Model

• Preparing data and reports for CRR

• ODP

GGZ Block 2015

Contour Map

-35-

Creation to Value Realisation: Our 2020 Vision

• Exploration drilling: 27 wells (incl. 6 Slim holes, 6 directional wells)

• LiFaBriC drilling: 3 wells (incl. 2 re-drill)

• Fractured 3 wells / 9 layers

• 6 wells produced (peak of 900 m3/d)

• 1 G&G Study

• Drilled 8 vertical exploration wells

• Fractured 6 wells across 10 layers

BQ2, BQ1-D1, BQ1-D2, BQ18, BQ20, BQ17

• Producing 6 wells to test commerciality

• Preparation of CRR

BQ2, BQ1-D1, BQ1-D2, BQ18, BQ20, ACE-ZY04-3

• CRR submitted and reserves certified

• ODP submitted and approved

• Commercial production and sales

GGZ History

2006-2014

2015

2020

-36-

Wells drilled in 2015

Creation to Value Realisation: Our 2020 Vision

12 12 12 12 11 11 11

12 12 12 12 11 11 11

12 12 12 12 12 12 12 12 11 11 11

12 12 12 12 12 12 12 12 11 11 11

12 12 12 12 12 12 12 12 11 11 11

12 12 12 12 12 12 12 12 12 11 11

12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 11 11

12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 11 11

12 12 12 12 12 12 12 12 12 12 12 12 12 12 11 11 11

11 12 12 12 12 12 12 12 12 12 12 13 12 12 12 11 11 12

11 12 12 12 12 12 12 12 12 12 13 12 12 12 12 12

12 12 12 12 12 12 12 12 12 12 13 12 12 11 12 12

12 12 12 12 12 12 12 12 12 12 13 13 13 13 12 12 12 12 12 12

12 12 12 12 12 12 12 12 12 13 13 13 12 12 12 12 12 12 12 12 12 12 12 12 12 12 11

12 12 12 12 12 12 12 12 12 13 13 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 11

11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 12 12 13 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 11

11 11 11 11 12 12 12 12 12 12 12 12 12 12 13 13 13 13 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12

12 12 12 12 12 12 12 12 12 12 12 12 12 13 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12

11 12 12 12 12 12 12 12 12 12 12 12 13 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12

11 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12

11 12 12 12 12 12 12 12 12 12 12 12 12 12 13 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 11

12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 11 11

12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 13 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 11 11

12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12

12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 11 12

12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12

12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 11 11

12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12

12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12

12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12

12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12

11 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12

11 11 11 12 12 12 12 12 12 12 13 12 12 12 12 12 12 12 12 12 12 12 12 12 12 12

11 12 12 12 12 12 12 12 13 13 12 12 12 12 12 12 12 12 11 11 12 12 12 12

11 12 12 12 12 12 12 12 13 12 12 12 12 12 11 11 11 11 11 11 12 12 12

11 12 12 12 12 12 12 12 12 12 12 12 11 11 11 11 11 11 11

12 12 12 12 12 12 12 12 12 11 11 11 11 11 12

12 12 12 12 13 13 13

-37-

GGZ Block – Location and Reserves

Low Estimate Prospective Resources

Best Estimate Prospective Resources

High Estimate Prospective Resources

Area: 869.9 km2NSAI (SPE-PRMS)

Net reserves/resources bcf

PRMS Low Estimate Prospective 20.4

PRMS Best Estimate Prospective 415.9

PRMS High Estimate Prospective 941.2

OGIP 4,552

Source: Netherland, Sewell & Associates, Inc as of Dec 31 2015

Creation to Value Realisation: Our 2020 Vision -38-

GGZ Block – 7 Coal Seams with high Gas Content

Coal seam 3#: 14 m3/t (494 ft3/t)

Coal seam 5#: 14.5 m3/t (512 ft3/t)

Coal seam 12#: 14 m3/t (494 ft3/t)

Coal seam 17#: 16 m3/t (565 ft3/t)

Coal seam 19#: 17 m3/t (600 ft3/t)

Coal seam 26#: 16 m3/t (565 ft3/t)

Coal seam 29#: 15 m3/t (529 ft3/t)

Coal

Seam

Depth mtvd

(Min - Max)

Thickness mtvd

Min-Max (Ave)

Gas Cont m3/t

(Min-Max/Ave)

CS#3 0 - 800 0.3-2.2 (Ave:1.2) 6.22-21.27 11.35

CS#5 50 - 850 0-2.8 (Ave: 0.6) 4.80-22.33/11.45

CS#12 100 – 900 0-2.2 (Ave: 1.4) 6.56-20.96/12.69

CS#17 140 – 1000 0-13.6 (Ave: 5.2) 8.26-23.98/14.14

CS#19 170 – 1100 0.7-12.0(Ave:6.7) 5.17-26.37/14.10

CS#26 250 – 1150 0-3.3 (Ave:1.3) 7.21-22.38/13.60

CS#29 270 - 1200 0-9.0 (Ave:2.9) 5.83-20.85/13.69

Creation to Value Realisation: Our 2020 Vision

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

GGZ Data Prep. & Static Modeling Data QC Static Modeling

Production eval. & Volumetrics

CRR evaluation & preparation

ODP Preparation

GQY Data Prep. & Static Modeling Data QC Static Modeling

Production eval. & Volumetrics

CRR evaluation & preparation

ODP Preparation

GFC Data Prep. & Static Modeling Data QC Static Modeling

Production eval. & Volumetrics

CRR evaluation & preparation

ODP Preparation

GPX Data Prep. & Static Modeling Data QC Static Modeling

Production eval. & Volumetrics

CRR evaluation & preparation

ODP Preparation

2016 Plan in Exploration Blocks

-39-

Our Vision to 2020

Randeep S. Grewal

Chairman and Chief Executive

Creation to Value Realisation: Our 2020 Vision

“Bringing value forward for shareholders”

Our vision to 2020

Where we are now

• Significant acreage and asset positions in China

• De-risked asset base, substantial reserve value growth

• Most lucrative gas margins globally

• Technical and commercial proof of concept established

• Stable Government and policy support

Our mission – accelerating value

• Secure asset appropriate financing

• Bring forward block development and subsequent cash

generation for shareholder value

• Deliver enhanced NPV where possible

-41-

Creation to Value Realisation: Our 2020 Vision

Funding and liquidity

-42-

• Clear focus on asset appropriate financing including reserve based lending,

divestiture, farmouts, equity/convertibles

• Roadmap to RBL

- Consistent and growing production and sales

- Significant NPV 10 base

- Development based financing for development investment

- ODP approval to unlock access to RBL

• Other shareholder value considerations

- Fixing low free float/liquidity in the shares

Creation to Value Realisation: Our 2020 Vision

Delivering value to shareholders as assets mature

A plan to return value

• Ring-fenced cash flows from individual assets

• Triggers including:

- Maturity of production and free cash flow

- Protecting cash for debt service

- Secure capex for growth and enhanced NPV

• Progressive shareholder return

• Visibility of shareholder return on an asset-by-asset

basis

• Escalating returns with asset maturity

-43-

Creation to Value Realisation: Our 2020 Vision

A strategic review for downstream

• Corporate vision as an upstream production company

• Rationalising downstream operations

- Monetise downstream assets – reinvestment in

upstream and simplify our business model and logistics

“A pure play upstream group focused

on delivering value at the well head”

-44-

Creation to Value Realisation: Our 2020 Vision

Farm out opportunities

• Significant exploration and development position

• Proof of concept in place, R&D dollars already spent

• Strengthening our balance sheet and financial position- Accelerating development

- Realising value for shareholders on farm out

- Enhancing project economics and present value

• Bringing value forward- From sequential development to concurrent development

- Pulling production forward on multiple assets

- Enhanced shareholder NPV

- Acceleration of returns/satisfying capital requirements

- Re-rating our intrinsic value

-45-