creating value in common spaces

TRANSCRIPT

Creating Value in Common Spaces

Richard Peiser, Ph.D., Harvard Graduate School of DesignChristopher Kelly, Convene

Please rate this session

Richard Peiser, Ph.D.Michael D. Spear Professor of Real Estate DevelopmentHarvard Harvard Graduate School of Design

Christopher KellyCo-Founder, President and Chief Development OfficerConvene

The Research

Richard Peiser, Ph.D.

TRADITIONALLY, OFFICE DEMAND WAS JOBS

U. S. OFFICE SPACE ELASTICITY

The Evidence

Office space utilization per employee is shrinking. BLS/Costar show 2014 figures at 190 SF per worker, while CoreNet reports shrinkage from 225 SF per worker in 2010 to 150 SF per worker in 2017.

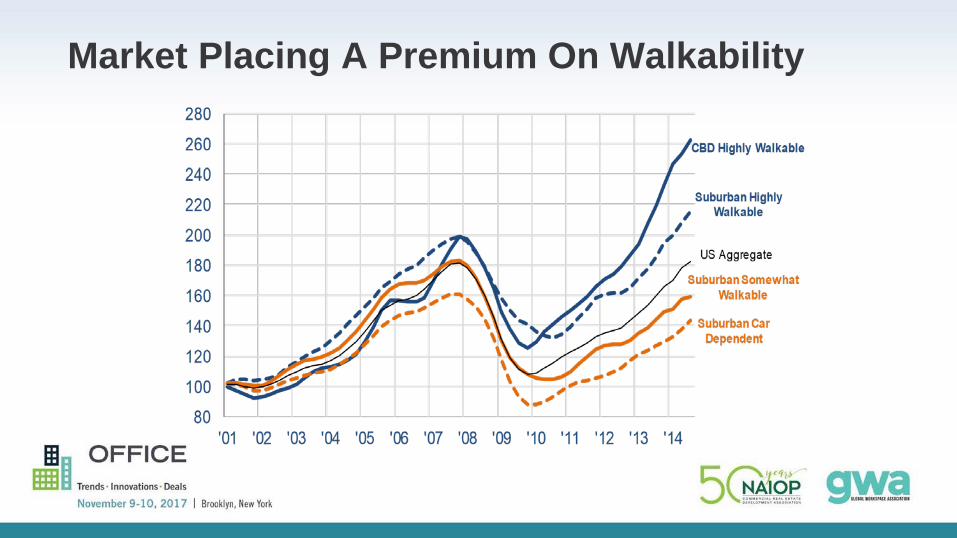

Market Placing A Premium On Walkability

“SUBURBAN OFFICE PARKS ARE A RELIC”

“The suburban office park—generally cut off from public transportation, lacking retail and amenities and employee housing options—is a dying breed.”

“Plentiful free parking is no longer sufficient to attract tenants.”

Challenges

How to make your office space more competitive?

1 How to compete with WeWork?

2

Goodwin Proctor Building Downtown Boston

Low ceilings and

cramped space

Individual Offices

Goodwin Proctor Building Seaport District

Stairway connects multiple floors and open plan

Lots of glass to open up spaces

Locational Choices: Boston Center of Gravity

Boston Center of GravityMarch 5, 1770

Boston Center of Gravity2000s

Boston (continued)4 Towers at Center vs. Seaport Innovation Sub-Market

Trends

•Declining Demand for Office Space −“Work is what you do, not where you do it!”

•Locational shift as to where space is demanded•Relaxed dress codes, plentiful parking and free beer not competitive!

Background to Study

• Office lobbies transforming from “exhibition” spaces to "vibrant" areas

• Office is borrowing from hotel lobbies• Similar is occurring in multi‐family lobbies• Research Committee sought to understand how, why and costs associated with activating common spaces in office buildings

Overview of NAIOP Study

• Methodology• Why Owners are Providing these Extra Amenities• Typical (nee old) and New (communal goals) Amenities• Favored Locations for New Amenities• Favored Activities Carried Out in Common Spaces• Costs Associated with Amenities and Activation• Why Employers Seek More Vibrant Settings• Desire for Active Settings by Industry

Methodology

•Surveys of owners and service providers currently exploring and implementing this concept

• Interviews with survey participants•Literature review

Why Owners are Providing Extra AmenitiesQ. Do you believe that offering these types of amenities has or will increase leasing velocity and/or rates?

89% Yes

8% No

1% Did not answer

Why Owners are Providing Extra Amenities:(Comments by owners)

We need to offer these amenities in order to

remain competitive. Our tenants are willing to pay

a bit more because of them.”

[Unique amenities] differentiate our building, make it memorable after

the tour.

“I believe the amenities have a smaller impact on rates and a bigger impact on velocity.

It is more about leasing up faster. The impact on increasing rent is very small.

The key is not [to] get higher rent, but to lease up quickly. Amenities are very helpful in reducing the leasing time, at least by 25%.

It has moved from being a ‘differentiator’ to a

‘requirement’ in many markets.

Typical Amenities(Ranked by owners from most to least popular)

Cimpress, Waltham, MAPhoto: Warren Patterson Photography

87% Shower rooms and lockers

84% Fitness Facility

79% Bike Storage

77% Cafeteria/Food Vendor

New Amenities(Ranked by owners from most to least popular)

Cafeteria/Food Vendor

84% Access to outdoor spaces

76% Shared meeting/conference rooms

64% Food Trucks

56% Coffee/tea in commons spaces

55% Co-working space

49% Access to games (ping pong, corn hole, etc.

New Amenities: (Comments by owners)

We are seeing a move toward more tenant interaction and community‐building. Lounge areas, game areas, happy hours, fitness centers, conference centers, etc. are all commonplace now.

We've found that the feedback has been very positive and that creative design can limit upkeep and security requirements for these areas.

Our newest office building has a large roof deck complete with a meeting space and large area for outdoor yoga. The lobby has a generous lounge area and three small spaces that will be programmed with rotating activities or exhibits focused on health and wellness.

Adding restaurant with wine bar, self‐playing piano, rotating and permanent art installations

For all of these questions I don't think that access to games and a bar serving alcohol are the key amenities. Having different seating groups, fast Wi‐Fi, coffee bar, connections to retail, views to active sidewalks, etc. are more important.

Favored Locations for AmenitiesRanked by owners from most to least popular*

• Outdoor Areas

• Lobby

• Roof

• Hallways/Circulation areas

• Basement

• OthersJay Suites, New York, NYPhoto: Liquidspace.com

Favored Activities for Activating SpacesRanked by owners from most to least popular*

Google, Cambridge, MAPhoto: Halkin Mason Photography, LLC

43% Happy hour/social events

39% Fitness classes

37% Art Installations in lobby areas

33% Ride share/lifts to public transportation

24% Guest speakers

10% Film screenings

Favored Activities: (Comments by owners)

Shuttle service to public transportation [must be offered] to get leased, though not a lot of people take advantage [of it.] [We are] exploring doing it with Uber.

In our industrial space we sponsor a forklift rodeo. The best operators of forklifts in our 2.5 million sq. ft. foot park compete for prizes.

We provide events 4 times per year. We have a Christmas holiday event, a summer ice cream social, a spring hot dog event and a fall barbeque.

[We offer] crafts [and feature] security speakers.

[This is about] … making amenity space available by reservation for tenants to hold parties, meetings etc. Also building holiday parties, charity drives, etc.”

They are open to the public not just tenants.

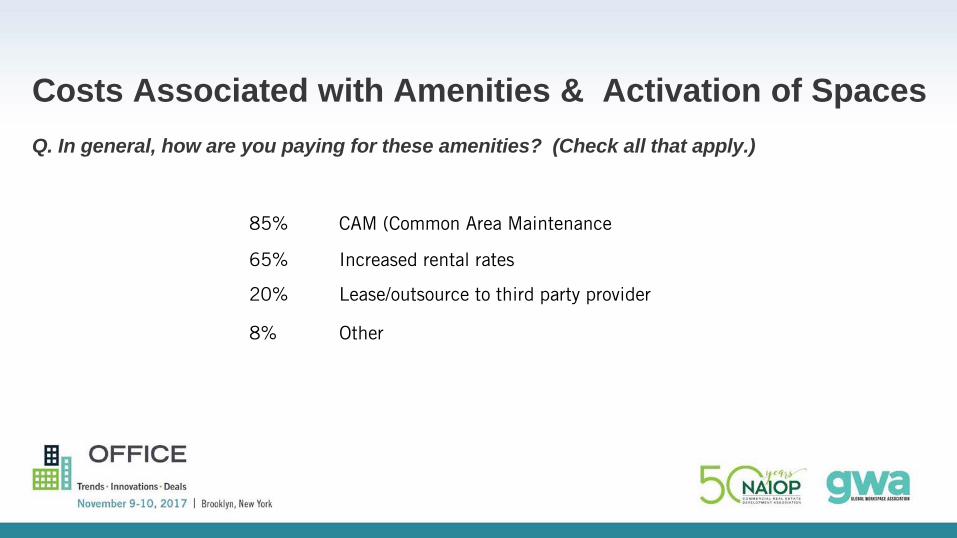

Costs Associated with Amenities & Activation of SpacesQ. In general, how are you paying for these amenities? (Check all that apply.)

85% CAM (Common Area Maintenance

65% Increased rental rates

20% Lease/outsource to third party provider

8% Other

How Owners are Paying for Activated Amenities : (Comments by owners)

If you have competitive advantage beyond your

competitors, amenities are a meaningful differentiator. For example, you can boost the

rent from $20 to $35.

$2 per sf per year

3%‐5% premium for good amenities.

Tenants might be willing to pay an extra 50 cents to the dollar extra per sf at most to see some of these benefits. A big, innovative company in need of attracting young people would pay that. Going above an extra $1/sq. ft. seems infeasible.”

We charge about 10 cents/sf/month higher than our competitors.

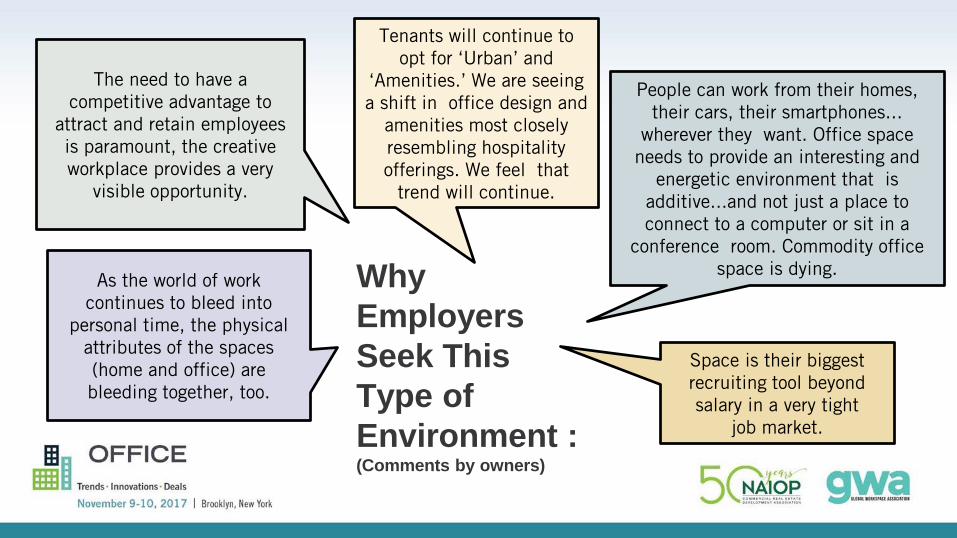

Why Employers Seek This Type of Environment : (Comments by owners)

The need to have a competitive advantage to

attract and retain employees is paramount, the creative workplace provides a very

visible opportunity.

Tenants will continue to opt for ‘Urban’ and

‘Amenities.’ We are seeing a shift in office design and

amenities most closely resembling hospitality offerings. We feel that

trend will continue.

As the world of work continues to bleed into

personal time, the physical attributes of the spaces (home and office) are bleeding together, too.

People can work from their homes, their cars, their smartphones...

wherever they want. Office space needs to provide an interesting and

energetic environment that is additive...and not just a place to connect to a computer or sit in a

conference room. Commodity office space is dying.

Space is their biggest recruiting tool beyond salary in a very tight

job market.

What types of companies are seeking these vibrant environments? (Comments by owners)

91

77

61

40

33

19

0 10 20 30 40 50 60 70 80 90 100

Very prevalent among technology companies

Very prevalent among information companies

Very prevalent among arts, entertainment, and recreationcompanies

Very prevalent among retail companies

Very prevalent among professional and business servicescompanies

Very prevalent among finance and insurance companies

Percentages

Examples of spaces

Innovation Park, Charlotte,NCPhoto: BECO Management

Schreiber Foods HQ, Green Bay, WIPhoto credit: DarrisLeeHarris

Burlington Stores’ HQ, Burlington,NJPhoto: KSS Architects

One 11 Office Building, Chicago,ILPhoto: Mark Ballogg, BalloggPhotography

WeWork, South Lake Union, Seattle,WAPhoto:WeWork

Google, Madison, WIPhoto: Alan Gartzke

Cimpress, Waltham,MAPhoto: Warren PattersonPhotography

What have we learned?

The C-Suite is engaged and recognizes that workplace design can significantly impact:

• Growth • New Product Development & Launch • Ability to Implement Change• Costs & Uses of Capital • Acquisition of New Talent • Workforce Motivation & Retention • Mentoring & Communications• Reduction of Disruptive Turnover• Security of All Forms• Mergers & Acquisitions

The Case Study

Christopher KellyCo-Founder, President and Chief Development OfficerConvene

- B I L L C L I N T O N

“Ignore the Headlines,Follow the Trend Lines.”

When technology changes,

When technology changes, our economy changes...

When technology changes, our economy changes...

our work changes…

When technology changes, our economy changes...

our work changes…our lives change.

Our workplaces and work lives must evolve to catch up

From truck-sized, 5MB computers that put man on the moon to iPhones

Technology Changes

Economy Changes

From raw materials & manufacturing to raw

talent & knowledge-based economies

Work Changes

From going home to going to work some

more

Lives Change

From Unreasonable to Imperative

Nobody told you, but your CRE customer has changed

too.

Talent Priorities are ChangingFrom Total Compensation to Overall Quality of Life

Tenant Priorities are ChangingFrom Cost Mitigation to Amenitization & Agility

The Landlord’s Role Changes From Selling Square Feet to Selling Experience

Experience Becomes the Landlord’s Greatest Opportunity

From Commodity to a Brand

What Talent Wants,

Is What Tenants Need,

Is What Landlords Must Build.

W HY CONVENE

Convene is a “workplace-as-a-service” platform that partners with landlords to create the next generation office building –

one that works and feels more like a full-service, lifestyle hotel.

Convene’s Integrated Platform

R E T A I L O F F E R I N G S

H O S P I T A L I T YS E R V I C E SE L E V A T E

A one-stop solution for landlords looking to differentiate their assets through flexible space, services, & technology.

C O N V E N E E N AB L E D+ + =

Convene + Durst: One World Trade Center Case Study

FOR F IVE CAFE

ONE WORLD COMMONS GAME ROOM

OWC COMMUNITY PROGRAMMING: YOGA

OWC COMMUNITY PROGRAMMING: TANGO

MEETING & EVENT SPACE

The Results

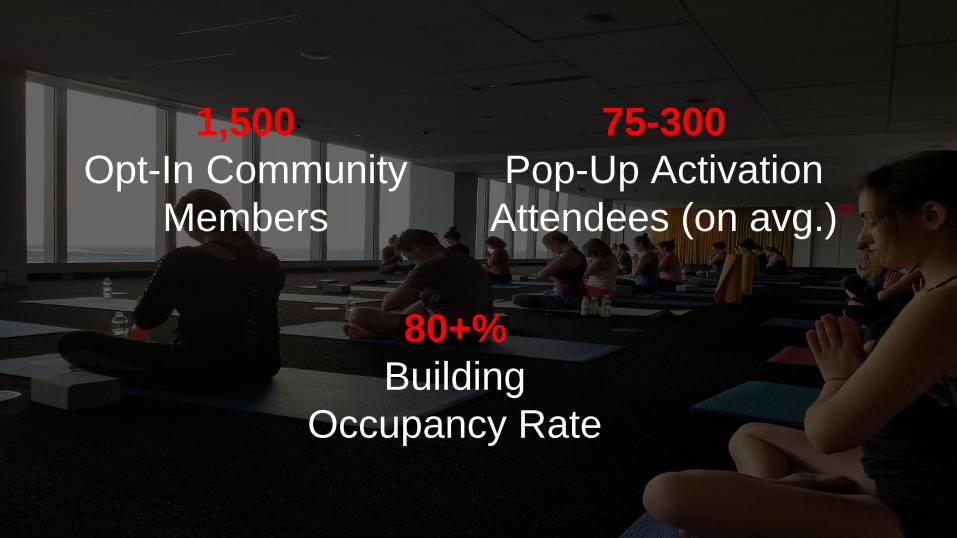

1,500 Opt-In Community

Members

1,500 Opt-In Community

Members

75-300 Pop-Up Activation

Attendees (on avg.)

80+% Building

Occupancy Rate

75-300 Pop-Up Activation

Attendees (on avg.)

1,500 Opt-In Community

Members

Q A