crapshoot investing -...

TRANSCRIPT

Crapshoot Investing:

How Tech-Savvy Traders and CluelessRegulators Turned the Stock Market

into a Casino

Jim McTague

Vice President, Publisher Tim Moore

Associate Publisher and Director of Marketing Amy Neidlinger

Executive Editor Jim Boyd

Editorial Assistant Pamela Boland

Development Editor Russ Hall

Operations Manager Gina Kanouse

Senior Marketing Manager Julie Phifer

Publicity Manager Laura Czaja

Assistant Marketing Manager Megan Colvin

© 2011 by Jim McTague

Publishing as FT Press

Upper Saddle River, New Jersey 07458

This book is sold with the understanding that neither the author nor the publisher isengaged in rendering legal, accounting, or other professional services or advice bypublishing this book. Each individual situation is unique. Thus, if legal or financialadvice or other expert assistance is required in a specific situation, the services of acompetent professional should be sought to ensure that the situation has been evalu-ated carefully and appropriately. The author and the publisher disclaim any liability,loss, or risk resulting directly or indirectly, from the use or application of any of thecontents of this book.

FT Press offers excellent discounts on this book when ordered in quantity for bulk purchasesor special sales. For more information, please contact U.S. Corporate and Government Sales,1-800-382-3419, [email protected]. For sales outside the U.S., please contactInternational Sales at [email protected].

Company and product names mentioned herein are the trademarks or registered trademarksof their respective owners.

All rights reserved. No part of this book may be reproduced, in any form or by any means,without permission in writing from the publisher.

Printed in the United States of America

First Printing March 2011 with modifications May 2011

Pearson Education LTD.Pearson Education Australia PTY, Limited.Pearson Education Singapore, Pte. Ltd.Pearson Education Asia, Ltd.Pearson Education Canada, Ltd.Pearson Educatión de Mexico, S.A. de C.V.Pearson Education—JapanPearson Education Malaysia, Pte. Ltd.

Library of Congress Cataloging-in-Publication Data:

McTague, Jim, 1949-Crapshoot investing : how tech-savvy traders and clueless regulators turned the stock market

into a casino / Jim McTague.p. cm.

ISBN 978-0-13-259968-9 (hardback : alk. paper)1. Investment analysis—United States. 2. Stock exchanges—Law and legislation—UnitedStates. 3. Electronic trading of securities. 4. Stocks—Law and legislation—United States. 5. Capital market—United States. I. Title. HG4529.M397 2011332.64'273—dc22

2010051301

ISBN-10: 0-13-259968-6

ISBN-13: 978-0-13-259968-9

Cover Designer Chuti Prasertsith

Managing Editor Kristy Hart

Project Editor Anne Goebel

Copy Editor Gill Editorial Services

Proofreader Water Crest Publishing

Senior Indexer Cheryl Lenser

Senior Compositor Gloria Schurick

Manufacturing Buyer Dan Uhrig

To my wife, Rachel, for her understanding, help, and encouragement.

This page intentionally left blank

Contents

Acknowledgments . . . . . . . . . . . . . . . . . . . . vii

About the Author . . . . . . . . . . . . . . . . . . . . viii

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . 1

Chapter 1: Strange Encounters . . . . . . . . . . . . . . . . . . 11

Chapter 2: Not Your Grandma’s Market . . . . . . . . . . . 27

Chapter 3: Screaming Headlines . . . . . . . . . . . . . . . . . 39

Chapter 4: Accidental Senator . . . . . . . . . . . . . . . . . . . 47

Chapter 5: Flash Crash . . . . . . . . . . . . . . . . . . . . . . . . . 61

Chapter 6: Shock and Awe . . . . . . . . . . . . . . . . . . . . . . 81

Chapter 7: Poster Child . . . . . . . . . . . . . . . . . . . . . . . . 85

Chapter 8: Accident Investigation . . . . . . . . . . . . . . . . 91

Chapter 9: The Trouble with Mary—and Gary . . . . . . 97

Chapter 10: The Road to Ruin . . . . . . . . . . . . . . . . . . . 105

Chapter 11: Busted! . . . . . . . . . . . . . . . . . . . . . . . . . . . 113

Chapter 12: Precursor . . . . . . . . . . . . . . . . . . . . . . . . . . 125

Chapter 13: Birth of High-Frequency Trading . . . . . . 135

Chapter 14: Evil Geniuses? . . . . . . . . . . . . . . . . . . . . . 149

Chapter 15: Dirty Rotten Scoundrels . . . . . . . . . . . . . 165

Chapter 16: Dark Pools . . . . . . . . . . . . . . . . . . . . . . . . 171

Chapter 17: Volatility Villains . . . . . . . . . . . . . . . . . . . . 175

vi CRAPSHOOT INVESTING

Chapter 18: The Investigation . . . . . . . . . . . . . . . . . . . 183

Chapter 19: The Vigilantes . . . . . . . . . . . . . . . . . . . . . . 193

Chapter 20: The Tide Turns . . . . . . . . . . . . . . . . . . . . . 199

Chapter 21: Letter Bomb . . . . . . . . . . . . . . . . . . . . . . . 207

Chapter 22: Scapegoat . . . . . . . . . . . . . . . . . . . . . . . . . 213

Chapter 23: The Real Culprits . . . . . . . . . . . . . . . . . . . 221

Chapter 24: Investing in a Shark-Infested Market . . . 229

Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 237

Acknowledgments

I want to thank my most memorable college professor and lifelongfriend, Francis Burch, S.J., a brilliant scholar and author who encour-aged me to become a columnist and an author.

This book was produced under a tight deadline to bring veryimportant information to the attention of the investing public. Iwould not have been able to tackle the project without the encour-agement of my colleagues at Barron’s: Editor and President EdwinFinn; Managing Editor Richard Rescigno; and Assistant ManagingEditor Phil Roosevelt. I also owe thanks to my officemate Tom Don-lan, our editorialist and the author of several books, for his sugges-tions, especially those regarding Harvey Houtkin.

Chris Anderson, one of the smartest men on Wall Street, pro-vided me with insights about the changing nature of the equities mar-ket. Ken Safian, another Wall Street legend, offered invaluableinsights about high-frequency trading. Jamie Selway of InvestmentTechnology Group LLC shared insights on market structure.

Will Ackworth of the Futures Industry Association was exceed-ingly generous in sharing his knowledge about the history of the com-modities markets. Wayne Lee of NASDAQ, Ray Pellecchia of theNYSE Euronext, John Heine of the Securities and Exchange Com-mission, and Dan Chicoine of TD Ameritrade were especially helpfulin connecting with market experts.

I also want to thank the many lawyers, regulators, and traderswho spoke to me about market structure and high-frequency tradingon deep background.

Finally, I offer special thanks to my daughter Alex, a patent litiga-tor, and Bob Schewd of WilmerHale, a brilliant literary contractattorney, for assisting me in my negotiations with the publisher.

About the Author

Jim McTague has been Washington Editor of Barron’s Magazinesince 1994—a post that gives him privileged access to key players inWashington and on Wall Street. A credentialed White House andCapitol Hill correspondent, he’s covered every administration sincethe first President Bush. McTague has appeared on NBC, CNN,CNBC, MSNBC, FOX, and is a frequent guest on FOX BusinessNews. His extensive analysis of the underground economy in 2005exploded the myth that illegal aliens were a small percentage of theU.S. population, triggering today’s border security debate. McTagueholds an MA in English from Pennsylvania State University and a BSin English from St. Joseph’s University in Philadelphia.

Introduction

The stock market has changed radically since 2005, yet few personsrealized the greatness of the seismic shift until May 6, 2010, when themajor averages collapsed over the course of 10 minutes. The publicsuddenly realized that a venue designed to efficiently move capitalfrom investors to the most promising enterprises had become as riskyas a Las Vegas casino. This book is the story of well-intentioned butdisastrously wrong-headed decisions by Congress and securities regu-lators that resulted in the destruction of a great American institutionand possible long-lasting damage to the entire U.S. economy. Fixingthis mess is without a doubt the most important challenge for U.S.policy makers in the years ahead, yet few of them understand this.They are still looking backward at the credit crisis of 2007 to 2008 andfail to see the bigger threat that is right before their eyes.

Just prior to May 6 during the first quarter of 2010, the all-clearsiren sounded for shell-shocked Wall Street investors. All seemedwell with the stock market. The major stock indexes, which had hit12-year lows in March 2009 in the midst of the turbulent GreatRecession, miraculously recovered by 74% the same month a yearlater. Investors once again were able to look at the returns in theirretirement accounts without becoming physically ill. Confidence inthe stock market, which had been badly shaken during the marketmeltdown of the previous two years, began to strengthen. In April2010, retail investors began shifting money from safe havens like gold,commodities, and treasury bonds into equities and equity mutualfunds, which was good news for cash-starved American enterprises.

1

2 CRAPSHOOT INVESTING

Investors were understandably cautious—nervous as cats, actually—owing to what they had been through. And the stock market, despiteits remarkable rebound, remained a frightening place. It was prone tojolting aftershocks in the form of wild, inexplicable, intraday priceswings that saw the Dow Jones Industrial Average (DJIA) rising andfalling by 100 or more points in a matter of hours. Prior to 2008, thissort of dramatic, volatile, intra-day shifting was rare. Often it tookmonths for the DJIA to move 100 points, not half a day. Investors hadgrown accustomed over the years to parking their savings in the stockmarket for the long haul in the expectation of fairly predictablereturns, not wild, hourly reversals of fortune. Since 2008, however, themarket had become radically unstable, with 15 of the 20 largest intra-day price swings in the history of the DJIA having occurred in 2008.1

Heightened volatility seemed to be a new normal. Volatility as meas-ured by the Chicago Board of Options Exchange SPX Volatility Indexor the VIX had been highly elevated in both 2008 and 2009.2

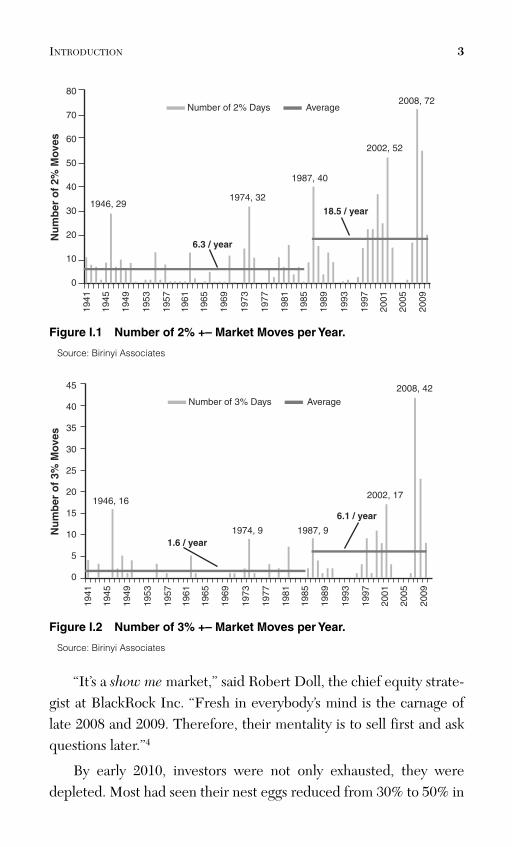

An intraday move of 3% in the Standard & Poor’s (S&P) 500 isconsidered unusually large. According to Birinyi Associates, a stockmarket research group, there were 42 days with 3% moves in 2008compared to 1 day in 2007 and 0 days from 2004 through 2006 (seeFigure I.1). Moves of 2% are significant. There were 149 2% daysduring the 1990s and nearly as many—131 from 2000 through2006—explained in part by the devastating 9-11 attacks. The GreatRecession beginning in 2007 eclipsed that trying period, with 156days of 2% moves (see Figure I.2).

The market’s intraday swings were particularly unnerving duringthe 146 trading days between October 1, 2008 and March 31, 2009.3

Retail investors typically invest first thing in the morning, at the mar-ket opening. On these wild days, their newly purchased shares oftendropped significantly in value by the time the market closed at 4 p.m.EST. Consequently, equity investors began to lose that old-time, buy-and-hold religion and became risk adverse to the extreme. No item ofbad news was ignored; no piece of good news was accepted uncriti-cally. No new money was flowing into the stock market, either.

INTRODUCTION 3

80

70

60

50

40

30

20

10

0

1946, 29

Number of 2% Days Average

6.3 / year

1974, 32

1987, 40

18.5 / year

2002, 52

2008, 72

1941

1945

1949

2001

2005

2009

1953

1957

1961

1965

1969

1973

1977

1981

1985

1989

1993

1997

Nu

mb

er o

f 2%

Mov

es

Figure I.1 Number of 2% +– Market Moves per Year.

Source: Birinyi Associates

45

40

35

30

25

20

15

10

5

0

1946, 16

Number of 3% Days Average

1.6 / year1974, 9

6.1 / year

1987, 9

2002, 17

2008, 42

1941

1945

1949

2001

2005

2009

1953

1957

1961

1965

1969

1973

1977

1981

1985

1989

1993

1997

Nu

mb

er o

f 3%

Mov

es

Figure I.2 Number of 3% +– Market Moves per Year.

Source: Birinyi Associates

“It’s a show me market,” said Robert Doll, the chief equity strate-gist at BlackRock Inc. “Fresh in everybody’s mind is the carnage oflate 2008 and 2009. Therefore, their mentality is to sell first and askquestions later.”4

By early 2010, investors were not only exhausted, they weredepleted. Most had seen their nest eggs reduced from 30% to 50% in

4 CRAPSHOOT INVESTING

2007 and 2008. None but those who had lived through the GreatDepression had ever experienced anything quite so frightening. Cer-tainly, there had been tough times in the past, with recessions of 16-months duration in both the 1970s and 1980s. But equities since 1983generally had been appreciating. Year after year, they were among thebest-performing investments. Stocks had become so predictable thatpeople forgot the risks. They forgot that stock market returns werenot guaranteed and that the market was not a place to sink moneythat they could ill afford to lose.

Few people had foreseen the catastrophic collapse of the mort-gage markets that would bring down well-known investment bankssuch as Bear Stearns and Lehman Brothers and that would trigger acredit draught and, consequently, the loss of more than 8 million jobs,which raised the total number of unemployed to 15 million persons.Just before the downturn, the public mood was optimistic. The econ-omy appeared to be booming. The unemployment rate was at 4.7%,and the rate had been below 5% for 23 consecutive months. Housingprices were rising along with stock prices. With the rate of home own-ership greater than 65%, the appreciation made people feel rich.They took out home equity loans to buy cars and vacation villas. Thefuture looked golden.

On October 9, 2007, the DJIA hit a high of 14,164.53. That sameday, the S&P 500 had made an all-time high of 1565.15. Popular MSNMoneyCentral blogger Jon Markman captured the narcoleptic eupho-ria of the pre-recession era in May 2007 when he guaranteed his read-ers that the DJIA would climb significantly higher. He wrote, “Unlessthe world economic system completely runs off the rails, Dow 21,000by 2012 is a lock. And anyone who says that ain’t so lives in a Never-land, where kids never grow up, companies never innovate, con-sumers stop buying stuff, and home sweet home is a bomb shelter.”That bit of juvenile sarcasm turned out to be closer to the truth thanMarkman or anyone else ever could have imagined. The market didrun off its rails. In 2008, the DJIA fell 37.8%, its worst swoon since the

INTRODUCTION 5

1930s. The S&P 500 tumbled 36.6%, which was its third worst year onrecord. The NASDAQ plunged by 40.5%. And this was only the firstact of the investment horror show. A year after the market peak, onOctober 9, 2008, the DJIA closed at 8579.19. The DJIA kept falling in2009, finally hitting a bottom on March 6, 2009 when it closed at6547.05, a level it had last seen on April 15, 1997. Billions in savingshad been wiped out. The unemployment rate was at 8.6%—the high-est level in 26 years—and would reach 10% before the year was out.5

So it was with a vengeance that the investing public relearnedthat the market can be an unforgiving place. During the Great Reces-sion, not even highly diversified mutual funds provided shelter fromthe economic storm. Diversification didn’t work when stocks andbonds and real estate were dropping in tandem.

The downturn had been especially brutal for the large contingentof baby boomers who had been planning for a comfortable retirementfunded by their pension and 401(K) accounts. The oft-repeated, grimhumor of the day was that their 401(K) plans had become 201(K) plans.

Boomers frantically liquidated what was left of their stock hold-ings and shifted the proceeds into the safest, most predictable invest-ments available, including Treasury securities with negative yieldswhen adjusted for inflation. In the words of mordant pundits, theseinvestors were looking for the return of their capital as opposed to areturn on their capital.

The March 2009 market recovery came as a surprise. There wasno fundamental reason for the bulls to be running. In fact, their buy-ing portended the end of the recession three months later.

The actual nature of a recovery was a matter of intense debateamong bulls, bears, and super bears even before many recognizedthat the recession had ended. The most optimistic economists, andthere were not many of them, predicted a V-shaped economicrebound, meaning that economic activity would pick up as quickly asit had come down in 2007 and 2008 during the credit and housing

6 CRAPSHOOT INVESTING

crisis. In their view, the market rally reflected this outcome and thuswas behaving rationally by bouncing back up like a super ball.

The conventional view was a pessimistic one. This broad campargued that the recovery would be U-shaped, with slow gross domes-tic product (GDP) growth and high unemployment into the earlyyears of the next decade. In their view, the stock markets were pre-maturely optimistic, the result of wishful thinking as opposed to solidearnings. There were some suspicions among this gloomy tribe thatbanks and Wall Street firms had been bidding up the price of stocksby trading them back and forth among themselves.6 Such activitywould generate higher returns for their substantial reserves of cash,which they were reluctant to lend, owing to economic conditions. Italso would have boosted their capital positions.

A third, super-bearish contingent of economists predicted thatthe economy would sputter and then conk out sometime in 2010 asfederal stimulus dollars diminished, a phenomenon they described asa double-dip recession. Some of them said the second leg of the slow-down might drag the country into a depression.

The endless debate among economists and market gurus, carriedalmost daily on the business pages, heightened the skittishness ofinvestors. Yet many of them crept back into the market in April becauseof a greater fear they might miss a ride on a profitable post-recessionbull market that would enable them to put their 2007 to 2008 lossesbehind them. They were desperate to recoup their savings. And theyremembered tales by their great grandfathers about the Great Depres-sion and the fortunes that were made by investors who had jumped intothe market after it had crashed. Given their nervous condition, how-ever, it would not take much of a fright to send them scrambling back tothe sidelines.

Fast-forward to May 6, 2010, a day with nerve-jangling headlines.The citizens of nearly bankrupt Greece were rioting, casting doubtson the future of the Euro. There was an election in Great Britain thatwould have a material effect on its economic prospects. Millions of

INTRODUCTION 7

gallons of crude oil were spewing from a broken BP wellhead nearly amile under the waters of the Gulf of Mexico, threatening unspeakabledamage to one of the world’s most magnificent marine habitats anddisaster for the tourist and fishing industries of at least four states.The DJIA, which had been at 11,151.83 just three days earlier, hadclosed on April 5 at 10,868.12. Investors who had been creeping backinto the market were worried and began to take some profits, whichseemed the wise thing to do. Some commentators were predictingthat events in Europe might tip the world’s economy back into a deeprecession.

Then at 2:30 p.m. EDT occurred one of the most bizarre and mys-terious meltdowns in stock market history, an event destined to becomeknown as the Flash Crash.7 The DJIA plunged more than 700 points inten minutes, its largest one-day fall ever. Then in the next ten minutes,it began to recover. The speed at which the event transpired was bothstunning and alarming. There had been other one-day market plunges,most notably Black Monday in October 1987. But the regulators sup-posedly had fixed the markets after that staggering event so that noth-ing like it could ever happen again. This infamous day on May 6 showedinvestors that the equities market had become explosively volatile andthat they could be wiped out in a matter of seconds. And it raised suspi-cions that the event had been deliberate, engineered by a new breed ofmarket player, the so-called high-frequency traders. These tech-savvytraders pitted a new generation of computing machines against humaninvestors, and the machines always seemed to win.

Some of the same physicists and mathematicians who haddesigned the exotic, synthetic mortgage securities that had wreckedhavoc on the world’s credit markets in 2007 and 2008 were now day-trading millions of shares of stocks, holding on to them for 2 minutesor less to make a fraction of a penny here and a fraction there, whichat the end of the day added up to real money. Data showed that anestimated 73% of all U.S. equity trades involved high-frequencytraders, who could execute an order in milliseconds.8

8 CRAPSHOOT INVESTING

They thrived on volatility, which is anathema to long-terminvestors; and the suspicion was that the high-frequency traders weresomehow at the bottom of the increasingly extreme, intraday marketmoves, using their superior technology and algorithms to manipulatestock prices. Even more disconcerting, the exchanges were sellingthese traders unfair advantages. In a real-life version of The Sting, thesehigh-frequency traders knew of the prices of stocks and the direction ofthe market before the data was posted on the ticker—the consolidatedtape that supplies the data to the public. It’s small wonder then thatretail investors took their money and ran for the doors immediately fol-lowing the Flash Crash. Some headed back to bonds. Retail day traders,who bought and sold shares dozens of times each session, shifted theirfocus to the commodities markets, reasoning that if the stock markethad become as risky as a pork bellies pit, they might as well go over tothe CME, formerly known as the Commodities Mercantile Exchange(CME), where margins and taxes were more attractive, and play withits stock index futures. So many retail day traders made the switch thatAmeritrade began introducing new commodities services aimed specif-ically at them. It was the firm’s most robust area of growth.

“We see things commonly now that we didn’t see 6 months ago,”said Chris Nagy, managing director of routing order strategy forAmeritrade during a September 2010 interview. He went on, “Retailtraders who sometimes acted as equity market specialists were saying,‘This market isn’t fair.’”

And most retail investors stayed on the sidelines through the fallbecause the volatility seemed more pronounced in the aftermath ofthe Flash Crash. Economist Ed Yardeni perfectly captured retailinvestors’ mood when he wrote in his August 5, 2010 newsletter, “Thestock market has been exhibiting bipolar symptoms in recent monthswith intense mood swings from mania to depression and back. ...Sincethe S&P 500 peaked on April 23 through yesterday, it has been down38 days and up 33 days. During the down days it lost a whopping 527points. During the up days it gained 437 points. Over the same period,

INTRODUCTION 9

the DJIA lost 4,231 points during the 37 down days and gained a totalof 3,708 points during the 34 up days. All that commotion, with so lit-tle motion one way or the other, has generated lots of swings betweenbearish and bullish emotion, leaving most investors exhausted.”

In fact, the markets would never be the same. Well-intentionedregulators and lawmakers had meddled with market structure over theyears and inadvertently changed what had been considered a nationaltreasure into a casino dominated by unpredictable, high-speed com-puters. The Flash Crash was a symptom of the mess they had made.

This book tells the real story of the Flash Crash and its causes—onethat you will not find in the official government accounts. It describeshow Congress and the Securities and Exchange Commission, or SEC,beginning in the early 1970s played God with the market, setting out tocreate a paradise for long-term investors and inadvertently changed itinto a financial purgatory. Blind in their belief that automation wouldmake the markets fairer and more efficient, they inadvertently wreckedone of the world’s great capital-allocation and job-creation engines andturned it into a wild playground for algorithmic traders. Initial publicofferings of new, dynamic companies have all but disappeared. Capital,the lifeblood of the economy, is flowing into less productive assets, suchas government bonds, precious metals, and third-world countries. Andinvestors remain sidelined because the market is now the equivalent ofa crapshoot.

Endnotes1. Historical Index Data, The Wall Street Journal online (July 2, 2010).

2. Report of the staffs of the CFTC and SEC to the Joint Advisory Committee onEmerging Regulatory Issues, “Preliminary Findings Regarding the MarketEvents of May 6, 2010,” Washington, DC (2010): 12–13.

3. Clemens Kownatzki, “Here’s Why You Are Getting Sick from the Markets,”Clemens Kownatzki’s Instablog (2010), http://seekingalpha.com/author/clemens-kownatzki/instablog.

4. Tom Lauricella, “Dow Slides 10% in a Volatile Quarter,” The Wall Street Journal,July 1, 2010.

10 CRAPSHOOT INVESTING

5. According to the Bureau of Labor Statistics, the unemployment rate was 8.8% inOctober 1983.

6. Rodrigue Tremblay, “The Great Fed-Financed Dollar Decline and Stock MarketRally of 2009,” http://www.globalresearch.ca/index.php?context=va&aid=15350.

7. All times are reported as Eastern Daylight Time.

8. Robert Iati, Adam Sussman, and Larry Tabb, “US Equity High-Frequency Trading: Strategies, Sizing, and Market Structure,” VO7:023, September 2009(www.tabbgroup.com): 14.

Strange Encounters

Beginning in 2007, two long-time equities traders named Sal Arnukand Joseph Saluzzi noticed some weirdly disturbing price movementsin the stock markets as they observed client trades on their multiplescreens in a small trading room in quiet Chatham, New Jersey. Whenthey went to hit a bid on certain exchanges, the price suddenly disap-peared and either a lower or higher bid instantly appeared in itsplace. It was as though some invisible, malign force was attempting totrick the traders into chasing the stock up or down the price ladder.Never before had they seen anything like it. The ghostly presence wasso incredibly fast that there was absolutely no chance of the tradersever winning the game. The deck was stacked against them. If theytook the bait, they would always end up paying more or getting lessthan the market’s consolidated tape of prices had initially advertized.

The price jumps were aggravating. Arnuk’s and Saluzzi’s job wasto obtain the best execution price on large orders of shares for theirinstitutional clients, which included large mutual fund managers suchas INVESCO. Somebody was threatening their livelihood. Theirfirm, Themis Trading LLC, was named for a Greek goddess who per-sonified fairness and trust.1 Someone subtly was trying to subtractthese two attributes from the market, and this got their blood boiling.It also got them wondering how the bastard was doing it.

The blocks of stock handled by Arnuk and Saluzzi were not smallpotatoes. They frequently ranged in size from 300,000 shares to 2 mil-lion shares. The transactions had to be conducted gingerly to avoid

1

11

12 CRAPSHOOT INVESTING

“information leakage” that could cause imbalances in the market, rais-ing the cost of transacting the business. The stock market always hadprovided a habitat for predators who exploited weaknesses and ineffi-ciencies in its structure, and if you did not avoid these cold-heartedtraders, you had about as much chance as an anchovy in a shark tank.The game of hide and seek was relentless. The predators always wereprobing for new weaknesses. If, for instance, the predators discoveredthrough the grapevine that a seller had a huge inventory of stock tounload, they would short the stock, sending its price lower and costingthe institution precious nickels, dimes, and pennies. If they discoveredthat a mutual fund or a pension fund was attempting to accumulate alarge position in a stock, they would front-run the order, buying up theshares ahead of the bigger buyer and then selling the shares to him fora cent or two more than he would have paid if his intentions hadremained secret.

To avoid predation, mutual funds employed numerous strategiesto camouflage both their identities and their order size. If a bigmutual fund wanted to sell several hundred thousand shares of astock to rebalance its portfolio, they might use a trusted broker as anintermediary to locate another, equally large institution to buy theposition at a negotiated price. It was hush-hush. Blabbermouths wereexcluded from such arrangements.

If a large counterparty could not be found, they might take a por-tion of the order to a so-called dark pool, an off-exchange venuewhere block traders anonymously submit buy and sell orders, hopingto get at least a portion of the order executed. Some dark pools wereexclusive. Participants were expected to be fair and honest, and anyviolation of the rules could result in immediate suspension or evenpermanent expulsion. Because the bid and offers in a dark pool werenot posted in the public or “lit” markets, they did not affect the priceson the consolidated quote. The public or lit market had no idea that aseller was looking for buyers and vice versa until stock was actuallysold. Then the execution price was listed on the consolidated tape—the data feed one sees crawling across the bottom of CNBC.

CHAPTER 1 • STRANGE ENCOUNTERS 13

To sell the remaining shares, the fund often resorted to auto-mated trading software to break up the block into smaller orders,which then were sent to the various lit exchanges. The size and fre-quency of the orders was determined by algorithms looking at priceand volume and the time parameters of the transaction. Finally, thefunds and institutions enlisted the aid of human traders such asArnuk and Saluzzi to use their wiles to avoid the predators.

Each of the methods had an Achilles’ heel. For instance, therewere limits on order sizes at the dark pools. And the algorithms thatwere employed to slice and dice big orders could be reverse-engi-neered in a matter of milliseconds by a predator’s faster, more sophis-ticated algorithm, allowing it to automatically front-run the order. Inthe course of a year, a millisecond advantage for a high-frequencytrader over the institutional traders can be worth $100 million.2

The funny business detected by Arnuk and Saluzzi was on a muchhigher level than the usual pitfalls that traders faced. The flickeringprices were so radical that it was like a squadron of F-16 fighter jetssuddenly appearing among the Sopwith Camels of World War I. Iron-ically, the phenomenon had appeared just about the time the U.S.Securities and Exchange Commission (SEC) had implemented itsRegulation NMS (National Market System)—a sweeping reformaimed at increasing competition among the exchanges to bothdecrease customer costs and make the stock market friendlier tolong-term investors. The rule, demanded by Congress in 1975, finallyhad been produced by the SEC 30 years later in 2005 and activated 2years after that. Clearly, there was a link. Intrigued, the two tradersdecided to dig into the matter.

Arnuk and Saluzzi had not been spoiling for a fight or longing forthe limelight. They had no idea what they were getting into and nopremonition that their discovery would rattle the investment world.Since 2002, both had been living the good life in the upscale subur-ban community of Chatham, a rustic borough tucked off a highwaynear the uber-chic Short Hills Mall. Take the exit off of Route 24 by

14 CRAPSHOOT INVESTING

Neiman Marcus and, behold, you were on Main Street in Leave It toBeaver land, with handsome, 1940s-era wood houses, tree-linedstreets, and neatly trimmed lawns. Chatham was just 25 miles fromWall Street, but it might as well have been 10,000 miles away. Noneof Lower Manhattan’s furious rush was evidenced here. There wereno throngs of sharp-elbowed, driven people barreling down side-walks, no blaring taxis clogging the streets. During the week, itseemed as quiet as Sunday.

Both men were veterans of Wall Street. After a decade working forbig firms, they had traded a 2-hour round-trip commute between Man-hattan and Brooklyn for a 10-minute, round-trip commute that savedthem enough time to coach their kids’ Little League games.3 This was autopia. They could balance their priorities of breadwinning and parent-ing with no maddening traffic jams and crowded subways in between.

They leased an office in a quaint, wooden retail village in the heartof town, opposite a dance studio, a tea restaurant, a tennis shop, and abeauty salon. It was not the locale usually associated with a tradingfloor. Their space was open and airy and had big windows on three wallsto let the sun shine in. If they hadn’t taken the space, it probably wouldhave been occupied by a real estate office or a small accounting firm.

Inside, it had the air of a man cave, with golf clubs leaning againstthe wall. Arnuk and Saluzzi and three other traders dressed their Sat-urday’s best: dungarees or shorts, and tee shirts. And there were lotsof computers. Their “trading floor” was a long desk topped with fouror five multiscreened computer screens where they watched theworld, the markets, and their clients buy and sell orders and talkedabout the frustrating New York Mets between trades.

Both men love baseball, although neither played beyond theyouth-league level. As adults, they both coached their sons’ teams withpassion. Arnuk, who had attended the prestigious Poly Prep highschool in Brooklyn, a private high school whose alumni include formerSEC Chairman Arthur Levitt, had bonded with his father and siblingsas he grew up watching baseball on a black-and-white television. He

CHAPTER 1 • STRANGE ENCOUNTERS 15

also bonded with his own kids through baseball. Arnuk was a sturdy,soft-spoken man who wore black-rimmed glasses and looked like aprofessor. His calm exterior belied his highly competitive side. Saluzzi,who had attended Bishop Ford High School in Brooklyn, carried him-self like a ball player. He was trim and walked with a relaxed, sure-footed gait.

The Brooklyn natives went a long way back and appeared to be asclose as brothers. They had met in the late 1980s at Morgan Stanley,their first employer after college. Arnuk, who grew up in Brooklyn’sBay Ridge section, had a BA in finance from SUNY Binghamton Uni-versity; and Saluzzi, who hailed from the Sheepshead Bay neighbor-hood, had a BA in finance from NYU. After a few years at theprestigious firm, they both concluded independently that to advancein the world of finance, they’d have to obtain graduate degrees. Sothey both left Morgan Stanley to enroll in MBA programs. Arnukstarted attending the Stern School of Business at NYU part time; andSaluzzi resigned a few months later to attend the Kenan-Flagler Busi-ness School of the University of North Carolina.

Arnuk graduated in 1991, and Saluzzi in 1993. Arnuk beganworking for Instinet, a global brokerage firm that specialized in com-puterized trading. He recruited Saluzzi for a job there. They wereneighbors at this point. Both men had married and secured homes inBay Ridge.

In 2002, Saluzzi and Arnuk got tired of the rat race and decidedto move to New Jersey and start their own company. Arnuk was thefirst to go, and he convinced Saluzzi to join him in a trading venture.

They were not making the kind of big money that drives a con-gressman to denounce Wall Street from the floor of the House or theSenate, but they were not doing badly either. The business wasn’texclusively about money anyway. They were self-sufficient. Theywere their own bosses. But in 2007, someone was threatening theirbusiness by playing unfairly. It was like a ball player shooting up onsteroids so he could muscle the ball farther than anyone else.

16 CRAPSHOOT INVESTING

Someone in the market was using the equivalent of steroids to tradein and out of the market faster than everybody else.

As the men began to track down the hombre, they learned just howradically Regulation NMS had changed the market, and it surprisedthem. The change had engendered an explosion in the number ofhigh-frequency traders plying the markets with super-charged com-puters and advanced pattern-recognition and statistical softwaredesigned to beat the market. These guys always had been around, butnow there seemed to be a lot more of them, and their robotic tradingmachines were much faster than anything ever deployed in the mar-kets. They programmed these overclocked computers to make moneybuying and selling stocks without direct human oversight. For everydozen firms, there were hundreds of these robotic trading wun-derkinds, and their numbers were growing every day because venturecapitalists and hedge funds were bankrolling start-ups left and right.Clearly, a lot of people thought high-frequency trading (HFT) was apath to quick and easy profits.

The general investment public had no idea that this market ver-sion of the Invasion of the Body Snatchers was under way. Some ofthe biggest players in the high-frequency trading sector were nothousehold names: They were proprietary trading firms such as Getcoand Tradebot and hedge funds such as Millennium, DE Shaw,WorldQuant, and Renaissance Technologies. Others were householdnames, but investors hadn’t paid much attention to their forays intomechanized trading because it was a relatively small portion of theirearnings and they did not break out the numbers in their annualreports. Goldman Sachs, which had become notorious in the public’seyes, owing to its role in the collapse of the mortgage market, had asizable high-frequency trading desk. Registered brokers like Bank ofAmerica and Lime Brokerage and Credit Suisse offered suites ofexotic trading algorithms and other services to customers who wantedto engage in the practice. But they all were secretive about the suc-cess of these operations. Why tempt copycats?

CHAPTER 1 • STRANGE ENCOUNTERS 17

Joining the gold rush were commodities traders and teams ofcomputer scientists and mathematicians with formulas designed tooutsmart any human trader. The human brain was not smart enoughor quick enough to compete with the over-clocked, nitrogen-cooledcomputing engines designed by whiz kids and trading hundreds ofmillions of stock shares every day. The trader-scientists began writingalgorithms so that their computers could outsmart competing tradingcomputers, triggering the equivalent of an arms race. Teams of math-ematicians and computer scientists worked round-the-clock toimprove their machines.

Arnuk and Saluzzi discovered that these new competitors hadanother significant technological advantage: Most of them possessedservers that were “collocated” at or near the exchanges. This meantthat for a steep, monthly rental, a high-frequency trading firm wasallowed to link its servers directly to the servers of the stockexchanges and get price and trading data milliseconds faster than any-one who could not or would not spring for such a hookup, like retailinvestors. In the view of the HFT crowd, this “low-latency” network-ing was completely within the bounds of acceptable behavior. AlistairBrown, founder of Lime Brokerage, which caters to high-frequencytraders, said in a magazine interview in 2007, “Any fair market isgoing to select the best price from the buyer or seller who gets theirorder in their first. Speed definitely becomes an issue. If everyone hasaccess to the same information, when the market moves, you want tobe the first. The people who are too slow are going to be left behind.”4

Depending on which strategies they employed, the HFT firmsprogrammed their computers to hold the stocks anywhere from 2minutes to 2 days. Their object was to make a little money on eachtrade, not swing for the fence. It was a fairly predictable businessbecause the shorter the period of time under study, the easier it is toforecast the future based on historic pricing, volume, and other data.Systems become increasingly unstable over time, which is why long-range weather forecasts are unreliable and which is why hedge funds

18 CRAPSHOOT INVESTING

making multiyear credit bets lost their shirts in 2007. The lesson of2007 had made a deep impression on so-called quants, which wasshort for “quantitative investors.” They embraced HFT with religiousfervor. Less risk equaled more money. The founder of Tradebot, anHFT located in Kansas City, Missouri, told students in 2008 that hisfirm typically held stocks for 11 seconds and had not suffered a losingday in four years.5

There was no public source of information of HFT industry prof-its, just anecdotes and rumors, so no one knew for certain how muchmoney they were pulling down in a given year. The best conservativeestimate was $20 billion just for firms that tried to earn small spreadsand fees from the exchanges by playing the role of market maker.They represented less than 10% of the HFT universe.

A market maker takes the opposite side of an incoming order toearn a small profit on the spread on fees. Often this is less than 2cents per share. But if the HFT firm trades millions of shares eachday, it can rack up a handsome annual return. Some earn returns ofclose to 300%.

By December 2008, Saluzzi and Arnuk had a strong suspicion asto what was going on in the markets. Like all good investigators, theyhad cultivated inside sources from a number of HFT firms. Whatthey found was disturbing: Based on their reading of the facts, high-frequency shops were using their superior computing power in new,devious, and possibly unethical ways to covertly attack institutionalcustomers and consequently raise their trading costs. Some of thestrategies looked like bare-faced attempts to manipulate the market.Arnuk and Saluzzi detected signs of momentum ignition, in which analgorithm initiates a series of trades in an attempt to trick othermachines into believing that a particular stock is headed higher orlower; and spoofing, a practice in which the machines feign interest inbuying or selling a stock to manipulate its price. The victims of thesequestionable techniques included mutual funds and pensions, so inthe final analysis, it was the small investor who was getting nicked by

CHAPTER 1 • STRANGE ENCOUNTERS 19

this new iteration of Wall Street avarice. No one had noticed—leastof all the SEC and examiners at the Financial Industry RegulatoryAuthority (FINRA), an industry-financed outfit charged with policingbrokers and the stock exchanges. The SEC staff members had so lit-tle day-to-day personal contact with Wall Street professionals thatthey knew almost nothing about what was really happening therebeyond the direction of the stock averages. They relied on FINRA,which had a reputation of being less than diligent.

Arnuk and Saluzzi were not politically connected. Theirs was asmall-fry firm. But they felt compelled to sound an alarm and bringtheir suspicions to the attention of the broader investing public.Something was askew in the marketplace. So the men elected to dis-seminate their findings in a white paper to their 30 institutionalclients and then post the paper on their blog. Those clients typicallyran just 2% to 5% of their order flow through Themis Trading. Arnukand Saluzzi figured the clients were losing lots of money to high-fre-quency traders on the remainder of the order flow transacted else-where because they were unaware of what was going on.

They titled their paper “Toxic Equity Trading Order Flow onWall Street: The Real Force Behind the Explosion in Volume andVolatility.” The white paper read more like an op-ed piece than theacademic treatise suggested by its title. Arnuk and Saluzzi offered noempirical evidence, just their hunches. Hard evidence was tough tocome by; no one, not even HFT consultant Tabb Group, could saywith absolute certainty how many HFT firms existed. The HFT cor-ner of the market was unregulated. It was also guarded. Tradersworked behind closed doors with upmost secrecy to protect their“secret sauces,” the algorithms that they used to outsmart othertraders. The duo did have 40 years of combined trading experience,however. They understood the mechanics of the market, and they hadseen hundreds of schemes designed to take advantage of unwaryinvestors. And they had their snitches. They were convinced that suchscheming was occurring now on a grand scale.

20 CRAPSHOOT INVESTING

The white paper asserted that the explosion in market volatilitythat most people ascribed to the global financial crisis that had begunin August 2007 was largely the product of high-frequency traders whohad invaded the market en masse to exploit changes wrought bySEC’s new rules.

“The number of quote changes has exploded,” they wrote. “Thereason is high-frequency traders searching for hidden liquidity. Someestimates are that these traders enter anywhere from several hundredto one million orders for every 100 trades they actually execute.”HFT machines would enter an order and cancel it almost immedi-ately, just to see if there was buying interest at a particular price level.Arnuk and Saluzzi referred to this practice as pinging, conjuring theimage of a destroyer conducting a sonar sweep for a hidden subma-rine. High-frequency trading computers would issue an order ultra-fast away from the listed price of a stock, and if nothing happened,they would cancel it immediately and send out another. Themachines were looking for hidden information to use to their advan-tage, such as whether there were big institutional customers afoot try-ing to fill large orders.

The strategy was cunning. Say there was an institutional traderwho had instructed a computer to purchase shares of a stock forbetween $20.00 and $20.03, but no higher. Theoretically, no one elsein the marketplace would know this. The high-frequency trader’salgorithm, however, might recognize that a pattern of purchases forthe particular stock’s shares at $20 was typical of algorithms employedby institutions accumulating a large position. So the HFT algorithmwould ping the institution’s algorithm, offering perhaps to sell 100shares of the stock to the institution at $20.05. If nothing were to hap-pen, the HFT algorithm immediately would cancel the trade andoffer 100 shares at $20.04. If nothing again happened, it would canceland offer $20.03. If the institution’s algorithm were to buy the stock,the HFT algorithm would know that it had found a buyer willing topay up to $20.03 for a stock listed at $20. The HFT algorithm then

CHAPTER 1 • STRANGE ENCOUNTERS 21

would quickly plunge back into the market, offering to buy the samestock at a penny above the institution’s original $20.00 bid. Then itwould turn around and continuously sell those shares to the institu-tion’s algorithm at $20.03. That extra penny, Arnuk and Saluzziasserted, amounted to a “stealth tax” on retail and institutionalinvestors.

Most investors—retail lambs and the large, bovine institutionaltraders—didn’t realize that they were being bled because it was adeath by a thousand cuts as opposed to a pneumatically propelled boltto the forehead. They had no way of knowing that an uninvited mid-dleman had come between them and the stock market.

This sort of shenanigan had begun in 2007 because RegulationNMS took away the duopoly status of NASDAQ and the New YorkStock Exchange (NYSE) by allowing any exchange to trade listedsecurities. Previously, the majority of trades on NYSE-listed stockswere done on the NYSE and NASDAQ-listed stocks in the NASDAQmarket. New computerized exchanges proliferated, anxious to get aslice of NASDAQ’s and the NYSE’s lucrative business. To survive inthe face of the new competition, NASDAQ and the NYSE were com-pelled to go public. Suddenly, they were accountable to stockholderswho vocally demanded a decent return on their investment; so theonce-dominant exchanges had to fight tooth and claw against the newcompetitors for the trade volume they had lost. They soon discovereddeep-pocketed customers in the form of the high-frequency traders,who were arbitraging price inefficiencies among the dozen or soequity exchanges and between the equities markets and the com-modities markets. The NYSE and the NASDAQ solicited the HFTbusiness, as did all the other exchanges. They offered these primecustomers special trading advantages as an inducement.

“Before 2007 and Regulation NMS, you really didn’t have thishigh-frequency stuff,” said Saluzzi. “The NYSE was still a slow mar-ket, and 80% of the trades were on the floor of the exchange. Butonce those trades migrated to newer, electronic exchanges, tradingbecame fast. Overall market volume went from 3 billion shares to

22 CRAPSHOOT INVESTING

10 billion shares because regulation NMS opened a whole new play-ground for high-frequency traders, and they went crazy.”

Some of the exchanges offered the HFT firms rebates of sub-pennies-per-share for serving as market makers and buying stocksfrom other customers. Buy and sell tens of millions of shares a day,and that fraction of a cent adds up to substantial profit. Arnuk andSaluzzi said in their white paper that the rebate scheme inadvertentlyled to what they termed hot-potato trading that inflated market vol-ume statistics and made the market seem much more liquid than itwas.

“If two guys trade 1,000 shares back and forth a million times,that’s a billion shares. Did a billion shares actually trade, or did thethousand shares change hands a million times between two guys play-ing hot potato? We argue that the real volume is 1,000 shares.”

The volume, real or not, generated data for the consolidated tape,which in turn was a marketable product. The more data that anexchange generated for the tape at year end, the bigger its share ofthe revenues from sales of that data to information vendors and bro-kerages. So they were not about to crack down on this practice.

Saluzzi and Arnuk charged that the high-frequency traderswere playing other games as well, all because they were able tomove faster than everyone else. In part, it was because the NYSEand the NASDAQ had invited them to collocate their servers closeto the exchange’s servers. This arrangement reduced the timerequired to get an order executed. The cost ranged from $1,500 to$50,000 per month for each server cabinet. There also was aninstallation charge that ran anywhere from $5,000 to $50,000. TheNYSE was so grateful for the new business that it took steps inOctober 2007 to make it easier for program traders to move themarkets higher and lower. The NYSE publicly removed curbs thatshut down the program trading if the market moved more than twopercent in any direction, the white paper stated. NYSE assertedthat the approach to limiting market volatility envisioned by the use

CHAPTER 1 • STRANGE ENCOUNTERS 23

of the “trading collars” was not as meaningful today as it had beenin the late 1980s when the rules were adopted. The rules had beenput in place in 1987 following Black Monday, the largest one-daycrash since the Great Depression. The white paper said, “On amore commercial level, the NYSE had been at a competitive disad-vantage because other market centers that didn’t have curbs weregetting the program trading business.”

One nefarious-sounding strategy, cited by the white paper, wasdesigned to quickly move the price of a share higher by 10 to 15 centsby employing a handful of 100- to- 500- share trades executed inrapid succession. Then the high-frequency trader would suddenlyshort the stock, knowing full well he had artificially pumped up theprice and that it shortly would begin to fall.

In a fictional example by the authors, an institutional buyer is try-ing to accumulate stock between $20 and $20.10 per share. Using thesame techniques as the rebate trader, a high-frequency trader spotsthe $20 bid as an institutional order. When the institution next bids$20.01, the high-frequency trader buys stock at $20.02, driving up theprice. The institution follows and buys more shares at $20.02. Thehigh-frequency trader in this matter runs the stock up to $20.10 pershare, with the institution chasing the stock. At this point, the high-frequency traders also stock short at $20.10 knowing it is highly likelythat the price of the stock will fall back to the low $20 range.

Finally, the two traders accused their high-frequency competitionof a sin known in the parlance of the industry as momentum ignition.The high-frequency traders engage this strategy to juice a marketalready moving up or down, creating either a major decline or a bigupward spike in prices. A trader could rapidly submit and cancelmany orders, and execute some actual trades to “spoof” the algo-rithms of other traders into action and cause them to buy or sell moreaggressively. Or the trader might try to trigger some standing stop lossorders that would cause a price decline. By establishing a positionearly on, the trader could profit by liquidating the position if he is

24 CRAPSHOOT INVESTING

successful in igniting a price movement. This strategy might be mosteffective in less actively traded stocks, which receive little help andpublic attention and are vulnerable to price movements sparked by arelatively small amount of volume.6

After sending the paper to clients, Arnuk and Saluzzi posted acopy of the white paper on their blog site, where they expected itscontents to be discovered by the larger investing world and thenwidely disseminated and discussed. That, after all, was the way thingsregularly happened on the World Wide Web, wasn’t it?

“We were not trying to make a name for ourselves,” Arnuk saidlater. “All that we wanted to do was fix what was wrong. We weresharing it with our customers so they could improve what they weredoing when they traded away from us.”

The charges by Arnuk and Saluzzi were sensational and poten-tially explosive. The markets were being manipulated. No one else hadnoticed what they had noticed. Regulators had been asleep. They had-n’t blown any time-out whistles or thrown any penalty flags for spoof-ing or momentum ignition or pinging. This was outrageous, becausethe SEC and FINRA were supposed to be cleaning up their act aftermissing abuses like Bernie Madoff’s outrageous Ponzi scheme.

But after the two traders disseminated the white paper, nothinghappened—nothing at all. Investors in December 2008 had otherthings on their minds. They were consumed by bailouts, failures,bankruptcies, and the incoming Democratic administration of BarackObama. The white paper was little more than background noise.

“Outside of our clients, no one made a stink or even mentionedour findings,” recalled Arnuk.7

The two men may have been disappointed, but they were notquitters. For them, this was personal. The HFT firms were a threat totheir way of life. They continued to plug away, albeit in relativeobscurity. In a prescient, follow-up white paper published in earlyJuly, Arnuk and Saluzzi warned of the possibility of a lightning-fast

CHAPTER 1 • STRANGE ENCOUNTERS 25

market collapse induced by high-frequency traders with unfilteredconnections to the stock exchanges through so-called “sponsoredaccess agreements” with a registered broker. The brokers essentiallyvouched for the integrity of their customers without doing real duediligence. The firms might be thinly capitalized or controlled by crim-inals, for all the regulators knew.

“Many of these arrangements do not have any pre-trade risk con-trols since these clients demand the fastest speed. Due to the fullyelectronic nature of the equity markets today, one keypunch errorcould wreak havoc. Nothing would be able to stop a market destroy-ing order once the button was pressed,” they wrote.

Once again, few people paid attention. It sounded shrill and far-fetched, like the Y2K scare that had predicted a meltdown of comput-ers worldwide on January 1, 2000 because twentieth-centurycomputer programs would not recognize dates after 1999. This apa-thy about their white paper would begin to evaporate days later as aresult of a quasi-comic confluence of events involving the FBI, short-tempered Wall Street bankers, a Bulgarian-born blogger, and apreening U.S. senator.

Endnotes1. Kate Welling, “Playing Fair?,” welling@weeden, June 11, 2010.

2. Richard Martin, “Wall Street’s Quest to Process Data at the Speed of Light,”InformationWeek, April 21, 2007.

3. Kate Welling, “Playing Fair?,” welling@weeden, June 11, 2010.

4. Richard Martin, “Data Latency Having an Ever Increasing Role in EffectiveTrading,” InformationWeek, May 25, 2007.

5. Stephen Gandel, “Is KC Firm the New King of Wall Street?,” Curious Capitalblogs, Time Magazine, May 18, 2010.

6. Securities and Exchange Commission, “Concept Release on Equity Market Struc-ture: Proposed Rule,” The Federal Register (January 21, 2010) 3609.

7. Author interview in June 2010.

This page intentionally left blank

This page intentionally left blank

INDEXAAccenture, aftermath of Flash

Crash, 85-87, 90Agnew, Spiro, 101AIG, 98Aldridge, Irene, 44Aleynikov, Sergey, 39, 42All-Tech, 137Alternative Trading Systems

(ATSs), 93American Banknote

Company, 117American Stock Exchange, 33, 76analysts, lack of, 189-191Angel, James J., 194arbitrage, 161-162arbitrage opportunities, 70Archipelago, 33Arnuk, Sal, 11-25, 44-45, 61, 217Atkins, Paul, 145-146ATSs (Alternative Trading

Systems), 93regulation of, 139-144

Australia (film), 78

237

automated liquidity provision, 161

Automatic Trading Systems(ATSs), 93, 139-144

Aykroyd, Dan, 29

BBachus, Spencer, 187Baker, Jim, 130BATS (Better Alternative Trading

System) Exchange, 78Bee, Samantha, 44Berkeley, Alfred, 173Biden, Joe, 47-49, 52-53“Big Picture” blog (Ritholtz), 234Birk, Roger, 116Black Monday (October 19, 1987),

125-133, 179Blair, Bruce, 160Blankfein, Lloyd, 99Blodgett, Henry, 189-190Bloomberg, Michael, 100Boesky, Ivan, 126Boggs, Caleb, 48

238 INDEX

Bookstaber, Richard, 157Born, Brooksley, 99Boston Stock Exchange, 33BP oil spill (Deepwater

Horizon), 67Brady Commission, 128Brady, Nicholas, 83, 128broken trades after Flash Crash,

83, 225brokerage houses, internal trades,

31-32Brown, Alistair, 17Brown, Gordon, 66Budge, Hamer, 107Buffett, Warren, 234Bulgaria Confidential

(newspaper), 42Bush, George H.W., 102Bush, George W., 50busted trades after Flash

Crash, 88buttonwood trees, 168

CCameron, David, 66Canaday, Ed, 41capital crisis of 1969-70, 105-111Casey, William, 120CBOT (Chicago Board of Trade),

28-30Cembalest, Michael, 207-208CFTC (Commodities Futures

Trading Commission), 27Flash Crash report, 213-227immediate reaction to Flash

Crash, 82

investigation of Flash Crash,183, 187

consolidated tape delays,202-204

quick fix rules after Flash Crash,85-87, 90

CFTC-SEC Joint AdvisoryCommitteeAccenture testifying before,

85-90investigation of Flash Crash,

91-95Chicago Board of Trade (CBOT),

28-30Chicago Mercantile Exchange

(CME), 28-30Chilton, Bart, 214Christie, William, 139circuit breaker rule, 188circuit breakers, 63-64, 89Citigroup, 166Clinton, Bill, 53, 97, 100-102, 143Clinton, Hillary, 100Close Encounters of the Third

Kind (film), 49CME (Chicago Mercantile

Exchange), 28-30collocated servers, 17, 22, 34collocation, origins of, 165-169commission structure, fixed

commissions, 118-120commodities exchanges

correlation with equitiesexchanges, 94

history in United States, 27-30unification with equities

exchanges, 36, 70

INDEX 239

Commodities Futures TradingCommission. See CFTC

competition among stockexchanges, creating, 116-118

computers, increasing role instock market, 115

Congressimmediate reaction to Flash

Crash, 81-84pressure on SEC by, 47-59

Conley, Joan C., 194Connaughton, Jeffrey, 49-53,

193, 210consolidated tape, 8, 12, 31

delay of, 72, 199-205, 225-226lack of during capital crisis of

1969-70, 110Consolidated Tape

Association, 165consolidation

of commodities exchanges, 30of equities exchanges, 33

Cook, G. Bradford, 111correlation, 68Cox, Christopher, 50-51, 58Craig, Pamela J., 85-87, 90Cramer, Jim, 207crashes. See Flash Crashcredit default swaps, 98Cronin, Kevin, 186Cummings, David, 216customers, influx of during captial

crisis of 1969-70, 106-108

DDaily Show (television

program), 44Damgard, John, 101

dark pools, 12, 32, 74, 94, 141,171-174

DARPA (Defense AdvancedResearch Projects Agency), 158

day trading. See high-frequencytrading

dealers, 133decimal pricing, 144Deepwater Horizon oil spill, 67Defense Advanced Research

Projects Agency (DARPA), 158Deja.com, 151delay of consolidated tape, 72,

199-205, 225-226Depository Trust and Clearing

Corporation, 117derivatives, predictions

concerning, 98Designated Order Turnaround

(DOT), 132Dhar, Vasant, 167Diebold, 195Direct Edge, flash orders, 42-43dividend capture, 230-231Dividend Capture: From Theory

to Practical Application(Hartzell and Sorathia), 231

Division of Risk, Strategy andFinancial Innovation (SEC),formation of, 97

DJIA (Dow Jones IndustrialAverage)on Black Monday (October 19,

1987), 125-133Flash Crash, details of, 61-79Great Recession, details of, 4volatility, 2

Dodd, Chris, 55, 186-187

240 INDEX

Dodd, David, 177Dodd-Frank Act, 103, 187, 204Doll, Robert, 3Donaldson, William H., 145Donovan, Jeffrey, 199DOT (Designated Order

Turnaround), 132Dow Jones Industrial Average.

See DJIADreyfuss, Richard, 49Duhigg, Charles, 43Dunkelberg, William, 234Durden, Tyler. See Ivandjiiski,

Dan, 41-42

EE-Mini futures contracts in Flash

Crash, 68-69, 215-219ECNs (electronic communications

networks), 94, 142Edelman, Asher, 136Engelberg, Jeff, 191Equinix, 167equities exchanges

correlation with commoditiesexchanges, 94

Flash Crash, details of, 61-79Regulation NMS changes to, 21,

31-37unification with commodities

exchanges, 36, 70erosion of investor confidence,

207-210ETFs (exchange-traded

funds), 185in Flash Crash, 76-77mutual funds versus, 232

ethics issues in Flash Crashinvestigation, 193-198

Eurex, 30Euronext N.V., 33European commodities

exchanges, modernization of, 29event trading, 161exchange-traded funds

(ETFs), 185in Flash Crash, 76-77mutual funds versus, 232

exchangescollocation, origins of, 165-169commodities exchanges, history

in United States, 27-30equities exchanges, Regulation

NMS changes to, 21, 31-37Flash Crash, details of, 61-79individual stock circuit

breakers, 89integration, lack of, 128intraday moves after Great

Recession, 2-3unification of commodities and

equities exchanges, 36, 70executing brokers, 32exhaust, 33

FFacciponte, Joseph, 40failed trades in capital crisis of

1969-70, 106-108Federal Reserve, regulation of

markets through, 129FINRA (Financial Industry

Regulatory Authority), 19, 41Mary Schapiro’s leadership of, 97Trillium Brokerage Services

LLC, case against, 210-212

INDEX 241

fixed commissions, 118-120Flash Crash

Accenture, affect on, 85-87, 90details of, 6-8, 61-79immediate Congressional

reaction to, 81-84investigation of, 91-95, 183-185,

189-191consolidated tape delays,

199-205SEC ethics issues, 193-198

precursors to, 1, 4-6SEC and CFTC report on,

213-227trades busted afterwards, 88

flash orders, 36, 42-43banning, 47-59

FOIA (Freedom of InformationAct), 113-114

Ford, Gerald, 120Fox, Kevin N., 40Frank, Barney, 55, 186Fraud Enforcement and

Recovery Act of 2009, 49Freedom of Information Act

(FOIA), 113-114Freeman, John P., 197front-running by hedge

funds, 140Futures Industry Association of

America, 101

GGalbraith, John Kenneth, 58Gastineau, Gary, 232Geithner, Timothy, 81Gensler, Gary, 86, 97-101, 216Getco, 157, 196

Gillespie, Ed, 53Giuliani, Rudolph, 126Glassman, Cynthia, 146Goldman Sachs, 39-41, 92, 99Goldstein, Michael, 68, 186Gorelick, Richard, 151-152, 155Graham, Benjamin, 177Grassley, Charles, 197Great Britain, elections prior to

Flash Crash, 66Great Depression, volatility

after, 179Great Recession

details of, 4recovery from, 1, 4-6

Greece, debt of, 65-66Greenspan, Alan, 98Gulf of Mexico, BP oil spill

(Deepwater Horizon), 67

HHartzell, David, 230-231Hathaway, Frank, 178Hawaiian Holdings, Inc., 41hedge funds, 159-160

front-running by, 140Hensarling, Jeb, 187high-frequency trading (HFT)

accusation of marketmanipulation, 39-45

blamed by Congress for FlashCrash, 83-84

collocation, origins of, 165-169Congressional pressure on SEC

to reform, 54-59eroded market confidence from,

207-210explanation of, 149-164

242 INDEX

Flash Crashconsolidated tape delays,

199-205details of, 61-79investigation of, 91-92,

183-185, 189-191in report, 221-227role in, 7-8SEC ethics issues, 193-198

origins of, 135-147public relations efforts of, 150Quants versus, 157-160retail trades and, 32statistics on, 156strategies employed by, 11-25,

34-37, 161-162Trillium Brokerage Services

LLC, case against, 210-212volatility

reasons for, 175-182rhythm of, 176-177

history of commodities exchangesin United States, 27-30

Hoffman, Stuart, 234hot-potato trading, 22Houtkin, Harvey Ira,

133-139, 161Hu, Henry, 44, 58, 98Hunsader, Eric Scott, 199-205,

225-226Hunt, Ben, 163hybrid market, 78

IICE (Intercontinental

Exchange), 30Ichan, Carl, 136

individual stock circuit breakers, 89

initial public offerings (IPOs),142-144

integration of exchanges, lack of, 128

Intercontinental Exchange (ICE), 30

internal trades, 31-32internalization

during Flash Crash, 73in Flash Crash report, 222-225

intraday moves after GreatRecession, 2-3

investigation of Flash Crash, 91-95, 183-185, 189-191consolidated tape delays,

199-205SEC ethics issues, 193-198

investor behavior, overcorrelationof, 177

investor confidenceafter Flash Crash, 62erosion of, 207-210

investor recommendations, 229-234

IPOs (initial public offerings),142-144

Ira Haupt & Co., 108Island (ECN), 144-145Ivandjiiski, Krassimir, 42Ivandjiiski, Dan, 41-42

J–KJohnson, Lyndon, 114Johnson, Simon, 186Junger, Sebastian, 67justifiable trades, 88

INDEX 243

Kanjilal, Debases, 189Kanjorski, Paul, 81-83Kaufman, Ted, 37, 47-61, 103,

183-187, 193-198, 208-210Kay, Bradley, 231-232Kim, Edward, 142King, Elizabeth, 196Kirilenko, Andrei, 171, 201Kotok, David, 234Kotz, David, 197

Llatency, 167layering, 210-212Leibowitz, Larry, 42Lemov, Michael, 114Levitt, Arthur, 14, 35, 50, 110,

118, 140-144Lewis, Michael, 191life-cycle funds, 230LIFFE (London International

Financial Futures and OptionsExchange), 30

limit orders, market ordersversus, 224

Lincoln, Abraham, 48liquidity during Flash Crash,

72-73Liquidity Replenishment Point

(LPR), 78Liquidnet, 173-174Lo, Andrew W., 160London International Financial

Futures and Options Exchange(LIFFE), 30

Long Term Capital Management,98, 159

Loomis, Philip A., 121

LPR (Liquidity ReplenishmentPoint), 78

Luddites, 150Lukken, Walt, 28

MMadoff, Bernie, 56Malyshev, Misha, 39market manipulation, HFT (high-

frequency traders) accused of,39-45

market orders, limit ordersversus, 224

market volatility. See volatilityMarkman, Jon, 4Massey, Raymond, 49Mathisson, Dan, 36, 141Maulden, John, 234Mayer, Martin, 127McCaughan, Jim, 178, 229-230McGinty, Tom, 197Mecane, Joseph M., 159Melton, Mark, 151Merrill Lynch, 99, 189-190Merrin, Seth, 173-174Merton, Robert C., 159Mikva, Ab, 53Minner, Ruth Ann, 48momentum ignition, 18, 23Moss, John E., 113-122Murphy, Eddie, 29mutual funds, ETFs (exchange-

traded funds) versus, 232

NNagy, Chris, 8, 225naked puts, 127-128

244 INDEX

naked short selling, banning, 47-59

naked sponsored access, 226Nanex, 200Narang, Manoj, 152-156NASD (National Assocation of

Securities Dealers), 102regulation after Black Monday

(October 19, 1987), 136-137NASDAQ

on Black Monday (October 19,1987), 133

initial public offerings (IPOs),142-144

investigation of price fixing, 139modernization of, 33Regulation NMS changes to, 21regulation of ATSs (Automatic

Trading Systems), 139-144SOES (Small Order Execution

System), 136-138National Association of Securities

Dealers. See NASDNational Market System, 116, 145New York Board of Trade, 28-30New York Mercantile Exchange,

28-30New York Stock Exchange. See

NYSENiederauer, Duncan, 172Nixon, Richard, 101Nordson Corp., 185NYSE (New York Stock

Exchange)Black Monday (October 19, 1987),

131-132capital crisis of 1969-70,

105-111

curbs on trading, 22flash orders, avoiding, 42-43modernization of, 33-34reaction to Flash Crash, 78Regulation NMS changes to, 21regulation of ATSs (Automatic

Trading Systems), 139-144volume declines in, 146-147

NYSE Euronext, 168NYSE Market Regulation, merger

with NASD, 102

OO’Brien, William, 42, 84O’Malia, Scott, 63, 83, 202Obama, Barack, 50, 53, 81,

100, 209OCT (Order Confirmation

Transaction), 138Oesterle, Dale, 146oil spill in Gulf of Mexico

(Deepwater Horizon), 67OMX exchange, 33Order Confirmation Transaction

(OCT), 138“Outside the Box” blog

(Maulden), 234overclocking, 158overcorrelation of investor

behavior, 177Overdahl, James, 197

PPacific Stock Exchange, 33A Perfect Storm (Junger), 67Peterson, Kristina, 176Phelan, John, 126Philadelphia Stock Exchange, 33

INDEX 245

Phillips, Susan, 101pinging, 20-21Pipeline Trading LLC, 173portfolio insurance, 130-131Prechter, Robert, 125, 130predatory trading, strategies for

avoiding, 12-13price fixing, NASDAQ

investigation of, 139pricing structures, decimal

pricing, 144principles-based systems, 28public relations efforts of high-

frequency traders, 150puts, naked puts, 127-128

Q–RQuants, high-frequency trading

versus, 157-160Quinn, Jack, 53quote stuffing, 200, 203

Rakoff, Jed, 103Reagan, Ronald, 83, 102, 128-129recession. See Great Recession, 1,

4-6recommendations for investors,

229-234recovery from Great Recession, 1,

4-6regulation

of ATSs (Automatic TradingSystems), 139-144

Congressional pressure on SEC,50-59

Securities Act Amendments of1975, 113-122

self-regulation, 120through Federal Reserve, 129

Regulation ATS, 141Regulation FD, 34Regulation NMS, 13, 145-146, 168

market changes resulting from,16-17, 21, 31-37

regulators. See CFTC; SECresearching stocks,

recommendations for, 233-234retail market, wholesale market

versus, 171-174retail trades, monopoly by

brokerage houses, 31-32retirement savings,

recommendations for, 230Reuters, 195revenue generated from volume,

165-166RGM (HFT company), 151“Rise of the Machines:

Algorithmic Trading in theForeign Exchange Market”(Vega), 98

Ritholtz, Barry, 234Robinette, Robbie, 151Rowen, Harvey A., 106, 116Rubin, Robert, 98-100Rueckert, Cleveland, 180Rumsfeld, Donald, 114

SS&P 500, volatility, 2S&P 500 E-Mini futures contracts

in Flash Crash, 68-69Safian, Ken, 158Salmon, Felix, 211-212Saluzzi, Joseph, 11-25, 44-45, 61Sanders, Bernie, 100-101Sarbanes, Paul, 100

246 INDEX

Sarbanes-Oxley Act, 100Schapiro, Mary, 43, 52-61, 86,

97-103, 183, 188, 198, 209-210,214, 226

Scholes, Myron, 159Schultz, Paul, 139Schumer, Chuck, 43-44, 56,

172, 187Schwab, Charles, 120Schwed, Fred, 105Schwert, G. William, 179-180SEC (Securities and Exchange

Commission)Arnuk and Saluzzi’s finding

discussed with, 44-45Congressional pressure on,

47-59Division of Risk, Strategy and

Financial Innovation,formation of, 97

on erosion of investorconfidence, 208-210

Flash Crash report, 213-227immediate reaction to Flash

Crash, 82investigation of Flash Crash,

183-185, 189-191consolidated tape delays,

199-205ethics issues, 193-198

quick fix rules after Flash Crash,85-87, 90

tracking mechanism, need for, 64

Securities Act Amendments of1975, 113-122

Securities Investor ProtectionCorporation (SIPC), 62, 109, 115

self-regulation, 120Senate. See Congressservers, collocating, 17, 22, 34Shell, Adam, 214short selling, banning naked short

selling, 47-59Silver, Jeff, 163SIPC (Securities Investor

Protection Corporation), 62,109, 115

Sloan, Alfred P., 14small investors in capital crisis of

1969-70, 105-111sniping, 161SOES (Small Order Execution

System), 136-138Sorathia, Mohammed, 231Special Trust Fund, origins of,

108-109speed, role in high-frequency

trading, 166Spiders, 76Spielberg, Steven, 49Spitzer, Eliot Laurence, 189-191spoofing, 18Steel, Bob, 100stock exchanges, creating

competition, 116-118. See alsoequities exchanges

stock-picking, volatility and, 177stop loss orders, 75-76stub quotes, 75-76Summers, Larry, 81

Ttarget date funds, 230Thain, John, 99ticker. See consolidated tape

INDEX 247

time delay of consolidated tape,72, 199-205, 225-226

“Toxic Equity Trading OrderFlow on Wall Street: The RealForce Behind the Explosion inVolume and Volatility” (Arnukand Saluzzi), 19

Toyota, approval ratings, 92trade-through rule, 144-146Tradeworx, 153-155Trading Places (film), 29Trillium Brokerage Services LLC,

210, 212

U–Vuncertainty, volatility and, 177unification of commodities and

equities exchanges, 36, 70“upstairs” market, 119-121Uptick Rule, 50-51, 54

Vanguard Funds, 185Vega, Clara, 98volatility

during Flash Crash, 72-73after Great Recession, 2-3in high-frequency trading

(HFT), 8-9reasons for, 175-182rhythm of, 176-177

volume of tradingdeclines in NYSE, 146-147due to automated trading, 64on equities exchanges, 31during Flash Crash, 81inflating, 22revenue generated from,

165-166

W–ZWachovia National Bank, 100Waddell & Reed Financial, Inc.,

69, 213-219Warner, Mark, 187Washington Post, 196Weild, David, 142-143Weisberg, Theodore, 222Wells Fargo, 100Whalen, Christopher, 40Where Are the Customer’s

Yachts? (Schwed), 105White House, immediate reaction

to Flash Crash, 81-84wholesale market, retail market

versus, 171-174Williams, Harrison “Pete,” 119Wunch, Steve, 143

Yardeni, Ed, 8, 234Yaroshevsky, Yan, 180-181