cracking the organizational code for growth aerospace ... · pdf filecracking the...

TRANSCRIPT

© OLIVER WYMAN

Cracking the organizational code for growth

Aerospace & Defense growth analysis

March 2013

1 1 © OLIVER WYMAN

Contents

1) Key organizational challenges in the industry 2

2) Growth performance of key players 4

3) How industry players are exploiting organizational levers 13

4) Why participate in Oliver Wyman’s study? 17

Page

2

Key organizational challenges in the industry

Section 1

3 3 © OLIVER WYMAN

Organizing for growth in the Aerospace and defense industries

• While strategic issues impacting this sector have been analysed at length, designing and implementing the right organization

remains a key lever to both enable and achieve sustainable growth

• Major A&D companies need to overcome the organizational challenges associated with:

- Creating the right organizational set-up to prepare the future while delivering short-term results

- Achieving the right power and resource distribution between:

Regions, business units and the corporate center (to achieve synergies and remain agile)

Programmes and functions (for clear lines of command and matrix ways of working)

- Developing an efficient footprint to balance global and local needs

- Re-inventing their products and conception processes to create and sustain demand

- Design for customization to serve multiple customers using the right enabling platforms / catalogues

- Migrating from ATA to functions and from make to systems integration

- Implementing customer-oriented processes and developing a growth-nurturing culture

- Doing more without more

- Implementing organization and processes aimed at reducing cost and time to market

- Gearing for growth and innovation in a very constrained environment

- Increasing efficiency while maintaining a healthy cost base

- Implementing new ways of working with customers and suppliers

- Working with suppliers and customers in an ever more integrated manner

- Keeping and developing critical skills and making efficient use of contractors

- Building and executing complex deals involving offset agreements and offshoring of activities

• Oliver Wyman is currently launching a study to further understand, qualify and quantify the required organizational levers and

how they impact the long-term sustainable growth prospects within the aerospace and defense industry

• The following pages provide a preliminary view of recent growth results within the sector, based on publicly available

information, in order to showcase the importance of identifying the organizational levers that propelled star performers’ growth

trajectories

4

Growth performance of the key players

Section 2

5 5 © OLIVER WYMAN

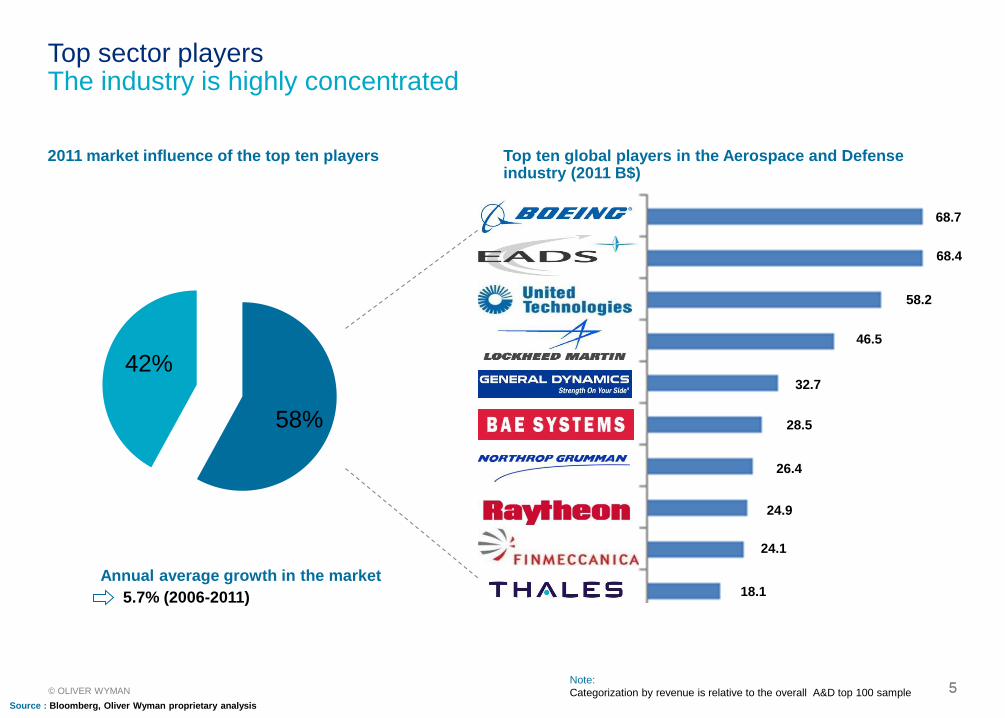

2011 market influence of the top ten players Top ten global players in the Aerospace and Defense industry (2011 B$)

Top sector players The industry is highly concentrated

68.7

68.4

58.2

46.5

32.7

28.5

26.4

24.9

24.1

18.1

58%

42%

Note:

Categorization by revenue is relative to the overall A&D top 100 sample

Source : Bloomberg, Oliver Wyman proprietary analysis

Annual average growth in the market

5.7% (2006-2011)

6 6 © OLIVER WYMAN

What was the impact of the 2008 economic crisis on the industry? While 85% managed double-digit growth pre-crisis, only 34% achieved this following the worst effects of the recession

Catching-up

7% of companies

Anemic

8% of companies

Rev

en

ue G

row

th (

CA

GR

2009

-2011)

Note: Origins of each axis set to 10% to differentiate

double-digit growth

Superstars

27% of companies

Stalling

58% of companies

Revenue Growth (CAGR 2005-2007)

Decelerating Growth Accelerating Growth

AAR CORP.

Alliant Techsystems Inc.

Avio

BAE Systems plc

BBA Aviation

BE Aerospace, Inc.

Cobham plc

Cubic Corporation

Curtiss-Wright Corporation

Dassault Aviation

Delta Tucker Holdings / DynCorp International

Elbit Systems Ltd.

Embraer S.A.

Esterline Technologies Corporation

European Aeronautic Defence and Space Company.

Exelis

Finmeccanica SpA

FLIR Systems

General Dynamics Corporation

GKN Aerospace

Israel Aerospace Industries Ltd.

Korea Aerospace Industries, Ltd.

L-3 Communications Holdings, Inc.

Lockheed Martin Corporation

Loral Space & Communications Inc.

Meggitt PLC

Moog Inc.

MTU Aero Engines Holding AG

Nabtesco Corp

Orbital Sciences Corporation Parker Hannifin Aerospace

Raytheon Company

Rheinmetall AG

Rockwell Collins, Inc.

Rolls-Royce Holdings plc

Saab AB

Safran

Singapore Technologies Engineering

Spirit AeroSystems

Teledyne Technologies Incorporated

Textron Inc.

Thales The Boeing Company

TransDigm Group Incorporated

United Technologies Corporation

Xi'an Aircraft Industry (Group) Company Ltd.

Zodiac Aerospace

Bombardier Aerospace

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

-10% 0% 10% 20% 30% 40% 50%

Source : Bloomberg, Oliver Wyman proprietary analysis

7 7 © OLIVER WYMAN

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

Rev

en

ue C

AG

R

Company Rank

2005-2007

2009-2011

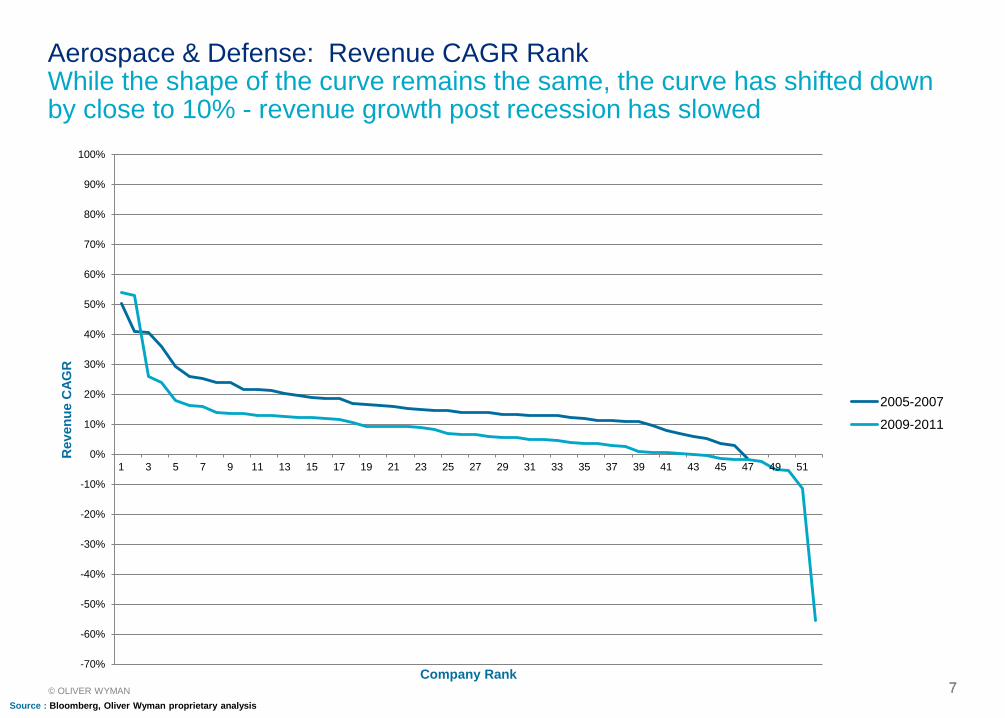

Aerospace & Defense: Revenue CAGR Rank While the shape of the curve remains the same, the curve has shifted down by close to 10% - revenue growth post recession has slowed

Source : Bloomberg, Oliver Wyman proprietary analysis

8 8 © OLIVER WYMAN

AAR CORP.

Alliant Techsystems Inc.

Avio

BAE Systems plc

BBA Aviation

BE Aerospace, Inc.

Chemring Group PLC Cobham plc

Cubic Corporation

Curtiss-Wright Corporation

Dassault Aviation

Elbit Systems Ltd.

Embraer S.A. Esterline Technologies Corporation

European Aeronautic Defence and Space Company EADS N.V.

Exelis

FLIR Systems

General Dynamics Corporation

GKN Aerospace

Israel Aerospace Industries Ltd.

Korea Aerospace Industries, Ltd.

L-3 Communications Holdings, Inc.

Lockheed Martin Corporation

Meggitt PLC

Moog Inc.

MTU Aero Engines Holding AG

NABTESCO CORPORATION

Northrop Grumman Corporation

Orbital Sciences Corporation

Parker Hannifin Aerospace

Raytheon Company

Rheinmetall AG

Rockwell Collins, Inc.

Rolls-Royce Holdings plc

Saab AB

Safran Singapore Technologies Engineering

Spirit AeroSystems

Teledyne Technologies Incorporated

Textron Inc.

Thales

The Boeing Company

TransDigm Group Incorporated

United Technologies Corporation

Xi'an Aircraft Industry (Group) Company Ltd.

Zodiac Aerospace

Bombardier Aerospace

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

-20% -15% -10% -5% 0% 5% 10% 15% 20% 25% 30%

EB

ITD

A C

AG

R (

2009

-2011)

Should growth or efficiency be pursued? With an average revenue growth of 7% and EBITDA growth of 9%, strategies were to protect EBITDA, sometimes at the detriment of revenue

Efficiency play

10% of companies Highly profitable growth

33% of companies

Less or unprofitable growth

14% of companies

Falling behind

43% of companies

Revenue Growth (CAGR 2009-2011) Source : Bloomberg, Oliver Wyman proprietary analysis

9 9 © OLIVER WYMAN

Aerospace & Defense: Market Capitalization Companies experiencing highly profitable growth clearly outperformed the market cap growth of their competitors

Source : Bloomberg, Oliver Wyman proprietary analysis

-1.8%

1.3%

30.1%

-5.0%

-20.0%

0.0%

20.0%

40.0%

Falling behind Less or unprofitable growth Highly profitable growth Efficiency play

Mark

et

Cap

CA

GR

(2

0009

-2011)

10 10 © OLIVER WYMAN

AAR CORP.

Aerospace Communications Holdings Co., Ltd.

Alliant Techsystems Inc.

Avio

BAE Systems plc

BBA Aviation

BE Aerospace, Inc.

Chemring Group PLC

Cobham plc

Cubic Corporation

Curtiss-Wright Corporation

Dassault Aviation

Delta Tucker Holdings / DynCorp International

Elbit Systems Ltd.

Embraer S.A.

Esterline Technologies Corporation

European Aeronautic Defence and Space Company EADS N.V.

Exelis

Finmeccanica SpA

FLIR Systems

General Dynamics Corporation

GKN Aerospace

Israel Aerospace Industries Ltd.

ITT Corporation

Korea Aerospace Industries, Ltd.

L-3 Communications Holdings, Inc.

Lockheed Martin Corporation

Loral Space & Communications Inc.

Meggitt PLC

Moog Inc.

MTU Aero Engines Holding AG

Nabtesco Corp Northrop Grumman Corporation

Orbital Sciences Corporation

Parker Hannifin Aerospace Raytheon Company

Rheinmetall AG

Rockwell Collins, Inc.

Rolls-Royce Holdings plc

Saab AB Safran Singapore Technologies Engineering

Spirit AeroSystems

Teledyne Technologies Incorporated

Textron Inc.

Thales

The Boeing Company

TransDigm Group Incorporated

Triumph Group, Inc. United Technologies Corporation

Xi'an Aircraft Industry (Group) Company Ltd.

Zodiac Aerospace

Bombardier Aerospace

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

500 5000 50000

EB

ITD

A M

arg

in (

2009

-2011)

Average Revenue (2009-2011)

Does company size impact growth? Smaller companies tend to display higher variability in EBITDA

Source : Bloomberg, Oliver Wyman proprietary analysis

11 11 © OLIVER WYMAN

AAR CORP.

Alliant Techsystems Inc.

Avio

BAE Systems plc

BBA Aviation

BE Aerospace, Inc.

Chemring Group PLC

Cobham plc

Cubic Corporation

Curtiss-Wright Corporation

Dassault Aviation

Delta Tucker Holdings / DynCorp International

Elbit Systems Ltd.

Embraer S.A.

Esterline Technologies Corporation

European Aeronautic Defence and Space Company EADS N.V.

Exelis Finmeccanica SpA

FLIR Systems

General Dynamics Corporation

GKN Aerospace

Israel Aerospace Industries Ltd.

Korea Aerospace Industries, Ltd.

L-3 Communications Holdings, Inc.

Lockheed Martin Corporation

Loral Space & Communications Inc.

Meggitt PLC

Moog Inc.

MTU Aero Engines Holding AG

Nabtesco Corp

Northrop Grumman Corporation

Orbital Sciences Corporation Parker Hannifin Aerospace

Raytheon Company

Rheinmetall AG

Rockwell Collins, Inc.

Rolls-Royce Holdings plc Saab AB

Safran

Singapore Technologies Engineering

Spirit AeroSystems Teledyne Technologies Incorporated

Textron Inc.

Thales The Boeing Company

TransDigm Group Incorporated

United Technologies Corporation

Xi'an Aircraft Industry (Group) Company Ltd.

Zodiac Aerospace

Bombardier Aerospace

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

500 5000 50000Sale

s R

ev

en

ue C

AG

R (

2009

-2011)

Average Revenue (2009-2011)

Aerospace & Defense: Revenue CAGR vs. Average Revenue Smaller companies show agility and ability to grow at a higher rate, yet the main players still display consistent growth rates, even though lower. Mid-size players appear to be in a danger zone.

Source : Bloomberg, Oliver Wyman proprietary analysis

12 12 © OLIVER WYMAN

EBITDA vs. Sales Revenue There is a consistent grouping in the area of 12 to 15% EBITDA margin, however, growth above 12% (twice the industry growth) tends to generate oversized returns

AAR CORP.

Alliant Techsystems Inc.

Avio

BAE Systems plc

BBA Aviation

BE Aerospace, Inc.

Chemring Group PLC

Cobham plc

Cubic Corporation

Curtiss-Wright Corporation

Dassault Aviation

Delta Tucker Holdings / DynCorp International

Elbit Systems Ltd.

Embraer S.A.

Esterline Technologies Corporation

European Aeronautic Defence and Space Company EADS N.V.

Exelis

Finmeccanica SpA

FLIR Systems

General Dynamics Corporation

GKN Aerospace

Israel Aerospace Industries Ltd.

Korea Aerospace Industries, Ltd.

L-3 Communications Holdings, Inc.

Lockheed Martin Corporation

Loral Space & Communications Inc.

Meggitt PLC

Moog Inc.

MTU Aero Engines Holding AG

Nabtesco Corp Northrop Grumman Corporation

Orbital Sciences Corporation

Parker Hannifin Aerospace Raytheon Company

Rheinmetall AG

Rockwell Collins, Inc.

Rolls-Royce Holdings plc

Saab AB

SAFRAN Singapore Technologies Engineering

Spirit AeroSystems

Teledyne Technologies Incorporated

Textron Inc.

Thales

The Boeing Company

TransDigm Group Incorporated

United Technologies Corporation

Xi'an Aircraft Industry (Group) Company Ltd.

Zodiac Aerospace

Bombardier Aerospace

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

-15% -10% -5% 0% 5% 10% 15% 20% 25% 30%

EB

ITD

A M

arg

in (

2009

-2011)

Sales Revenue CAGR (2009-2011)

Source : Bloomberg, Oliver Wyman proprietary analysis

13

How industry players are exploiting organizational

levers

Section 3

14 14 © OLIVER WYMAN

BAE Systems COMPANY AT A GLANCE

• Sales 2011: $28.5 Billion

• 93,500 employees

• Presence in more than 100 countries

• Second largest global defense supplier

KEY ORGANIZATIONAL ATTRIBUTES (con’t)

ORGANIZATION

The business is reported through five principal reporting segments

• Electronic Systems

• Cyber & Intelligence

• 3 Platforms & Services: US – UK – and International

Executive Committee and other direct reports to the Chief Executive

TALENT

Center for Performance Excellence dedicated to the development and transfer

of best practices

Jobs campaign through radio and social media to detect and support the talent

pipeline in the US

CEO is homegrown – was the former COO

INNOVATION

2011: 1,807 M$ spent on R&D (7% of Revenue)

BAE Systems investment in innovation (I3) is a multi-million dollar program to

develop technologies

Partnership with academia as well as small and medium size businesses

CULTURE AND VALUES

Trusted – Innovative – Bold (challenge and initiative)

Customer Focus, Financial Performance, Program Execution and Responsible

Behavior

Diversity ( 25% of BAE Board are women)

TRANSFORMATION

In October 2011, the Group announced changes to its external reporting

segments to improve performance visibility

KEY ORGANIZATIONAL ATTRIBUTES

PURPOSE / VISION

To be the premier global defense, aerospace and security company

To deliver sustainable growth in shareholder value through

commitment to Total Performance

STRATEGY

Support customers in safeguarding their vital interests

Drive shareholder value by improving financial performance and

competitive positions across the business

Sustain a leadership position in the electronic warfare market

Increase productivity and efficiency

Improve profit and cash generation

Increase international business

ACQUISITONS

Acquisition to sustain the group’s position - especially for its Cyber and

Intelligence division:

• 2011: L-1 Identity Solutions, Inc.’s Intelligence Services Group

• 2011: Norkom Group plc

• 2011: ETI A/S

• 2011: Stratsec.net Pty Limited

Source : Public information , annual report

15 15 © OLIVER WYMAN

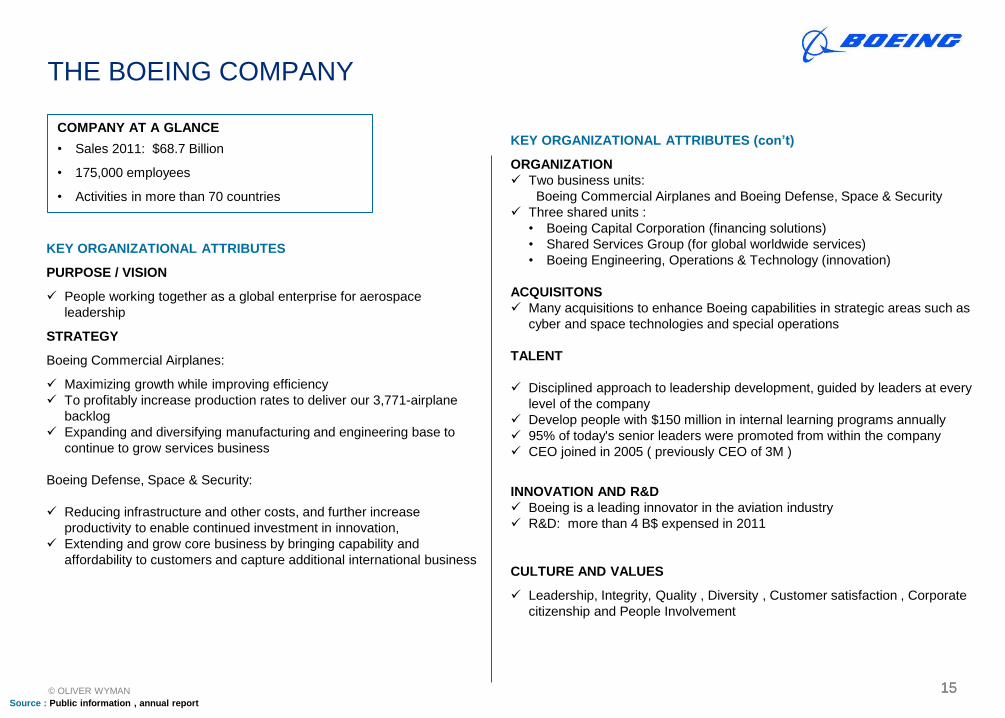

THE BOEING COMPANY

COMPANY AT A GLANCE

• Sales 2011: $68.7 Billion

• 175,000 employees

• Activities in more than 70 countries

KEY ORGANIZATIONAL ATTRIBUTES (con’t)

ORGANIZATION

Two business units:

Boeing Commercial Airplanes and Boeing Defense, Space & Security

Three shared units :

• Boeing Capital Corporation (financing solutions)

• Shared Services Group (for global worldwide services)

• Boeing Engineering, Operations & Technology (innovation)

ACQUISITONS

Many acquisitions to enhance Boeing capabilities in strategic areas such as

cyber and space technologies and special operations

TALENT

Disciplined approach to leadership development, guided by leaders at every

level of the company

Develop people with $150 million in internal learning programs annually

95% of today's senior leaders were promoted from within the company

CEO joined in 2005 ( previously CEO of 3M )

INNOVATION AND R&D

Boeing is a leading innovator in the aviation industry

R&D: more than 4 B$ expensed in 2011

CULTURE AND VALUES

Leadership, Integrity, Quality , Diversity , Customer satisfaction , Corporate

citizenship and People Involvement

KEY ORGANIZATIONAL ATTRIBUTES

PURPOSE / VISION

People working together as a global enterprise for aerospace

leadership

STRATEGY

Boeing Commercial Airplanes:

Maximizing growth while improving efficiency

To profitably increase production rates to deliver our 3,771-airplane

backlog

Expanding and diversifying manufacturing and engineering base to

continue to grow services business

Boeing Defense, Space & Security:

Reducing infrastructure and other costs, and further increase

productivity to enable continued investment in innovation,

Extending and grow core business by bringing capability and

affordability to customers and capture additional international business

Source : Public information , annual report

16 16 © OLIVER WYMAN

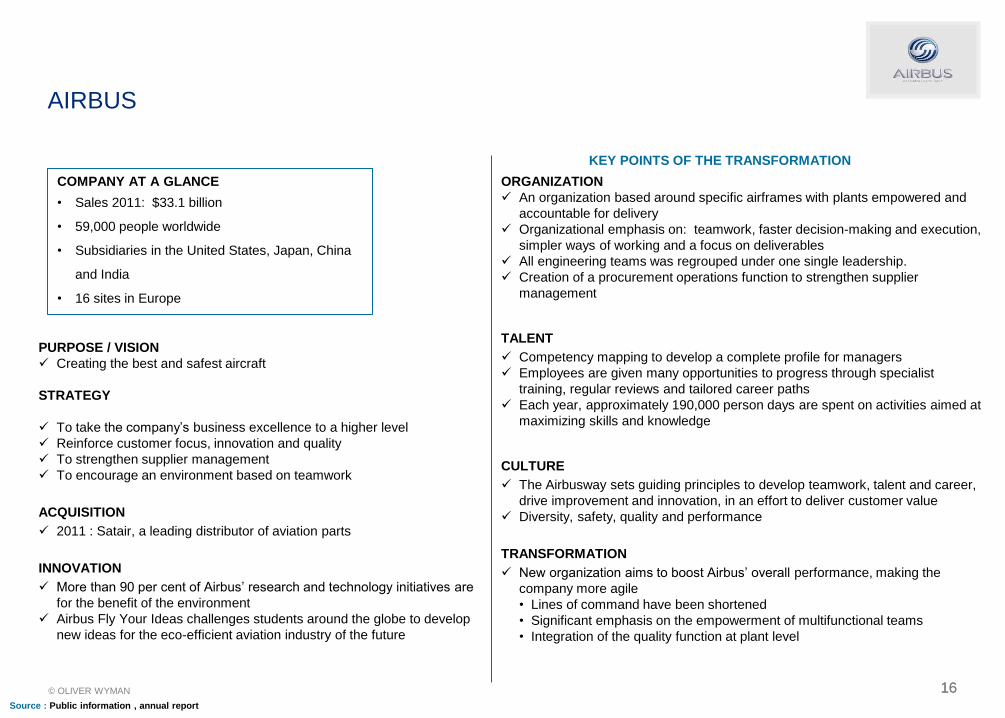

AIRBUS

KEY POINTS OF THE TRANSFORMATION

ORGANIZATION

An organization based around specific airframes with plants empowered and

accountable for delivery

Organizational emphasis on: teamwork, faster decision-making and execution,

simpler ways of working and a focus on deliverables

All engineering teams was regrouped under one single leadership.

Creation of a procurement operations function to strengthen supplier

management

TALENT

Competency mapping to develop a complete profile for managers

Employees are given many opportunities to progress through specialist

training, regular reviews and tailored career paths

Each year, approximately 190,000 person days are spent on activities aimed at

maximizing skills and knowledge

CULTURE

The Airbusway sets guiding principles to develop teamwork, talent and career,

drive improvement and innovation, in an effort to deliver customer value

Diversity, safety, quality and performance

TRANSFORMATION

New organization aims to boost Airbus’ overall performance, making the

company more agile

• Lines of command have been shortened

• Significant emphasis on the empowerment of multifunctional teams

• Integration of the quality function at plant level

PURPOSE / VISION

Creating the best and safest aircraft

STRATEGY

To take the company’s business excellence to a higher level

Reinforce customer focus, innovation and quality

To strengthen supplier management

To encourage an environment based on teamwork

ACQUISITION

2011 : Satair, a leading distributor of aviation parts

INNOVATION

More than 90 per cent of Airbus’ research and technology initiatives are

for the benefit of the environment

Airbus Fly Your Ideas challenges students around the globe to develop

new ideas for the eco-efficient aviation industry of the future

COMPANY AT A GLANCE

• Sales 2011: $33.1 billion

• 59,000 people worldwide

• Subsidiaries in the United States, Japan, China

and India

• 16 sites in Europe

Source : Public information , annual report

17

Why participate in Oliver Wyman’s study?

Section 4

18 18 © OLIVER WYMAN

Why participate in Oliver Wyman’s study? To understand the organizational drivers behind the variations in growth results - looking beyond the typical strategic contributors

• The most comprehensive study in

the sector on the subject

• High caliber of global corporations

participating within your industry

• Privileged access to insights on the

key trends to face industry

challenges

• Customized report highlighting how

your company’s measures against

best practices

• Flexible approach to optimize your

involvement (a short interview or

online questionnaire)

• Complimentary participation

Reasons for participating

For more info, or to register for

participation, please contact us at

1. Key Industry Trends

• A comprehensive view of key trends and their impact on the

industry

• Perspectives on how these trends have had an impact on growth

within the industry

• Conclusions as to what has contributed to the success of the

“Superstars” and those companies achieving highly profitable

growth

2. Customized analysis: how Company X measures up

against the industry

• A detailed comparison of Company X against each of the

identified organizational levers and best practices

• Comparison to peers with respect to the application of the levers

and best practices and the resulting growth success

3. Key highlights and best practices

• A summary perspective of Company X relative to the industry and

our best practices analysis

4. Backup

• Flat report with answers from Company X

Cracking the Organizational Code for Growth: Feedback Report - Company X

CONFIDENTIALITY

Our clients’ industries are extremely competitive. The confidentiality of companies' plans and data is obviously critical. will

protect the confidentiality of all such client information.

Similarly, management consulting is a competitive business. We view our approaches and insights as proprietary and therefore

look to our clients to protect 's interests in our presentations, methodologies and analytical techniques. Under no circumstances

should this material be shared with any third party without the written consent of .

Copyright ©