cr reports, stakeholder engagement and ngo / …...safe products, and services … are accountable...

TRANSCRIPT

© AccountAbility 2006

CR Reports, Stakeholder CR Reports, Stakeholder Engagement and NGO / Business Engagement and NGO / Business

PartnershipsPartnerships

Ruth WoodallRuth Woodall

National Centre for Business and SustainabilityNational Centre for Business and Sustainability

June 10June 10thth, Budapest, Budapest

© AccountAbility 2006

• Founded by the Co-operative Bank in association with the four Greater Manchester universities

• Independent not-for-profit consultancy

• Assists public and private sector organisations to improve their environmental and social performance

The NCBSThe NCBS is a solutionsThe NCBS is a solutions--orientated orientated

notnot--forfor--profit consultancyprofit consultancyCR and SD Experts

and Licensed Provider of AA 1000 training

© AccountAbility 2006

• Consultancy

• CR and sustainability training

• Research

• Stakeholder engagement and partnership development

We offer services in 4 areas

© AccountAbility 2006

• Mission:

– Spread an understanding, and a belief in sustainability

– Move organisations in the region from understanding to achieving sustainability

– Offer compelling arguments in an engaging and inspirational way

Our sister organisation, Sustainability Northwest

© AccountAbility 2006

Programme

• CR Reports:– Context – CR and reporting– Analysing CR reports: AA1000AS

• Materiality, completeness and responsiveness• CR assurance statements

• Stakeholder Engagement– Context– Doing stakeholder engagement: worked example:

• Identifying and prioritising stakeholders• Planning an engagement

• NGO / Business Partnerships– Context– Types of partnership– Benefits and risks– Things to consider for successful partnerships

© AccountAbility 2006

Corporate Responsibility

© AccountAbility 2006

Defining Corporate Responsibility

Corporate responsibility is shorthand for business’contribution to sustainable development.

© AccountAbility 2006

Defining Corporate Responsibility

Corporate responsibility is shorthand for business’contribution to sustainable development.

“A concept whereby companies integrate social and environmental concerns in their business operations and in their interaction with stakeholders on a voluntary basis”

Promoting a European Framework for Corporate Social Responsibility, EU Green Paper (2001)

“A new business strategy in which companies conduct business responsibly by contributing to the economic health and sustainable development of the communities in which they operate, offer employees healthy, safe, and rewarding work conditions, offer good, safe products, and services … are accountable to stakeholders … and provide a fair return to shareholders whilst fulfilling the above principles. CSR Europe

UN Global Compact expects signatories to “embrace, support and enact, within their sphere of influence, a set of core values in the areas of human rights, labour standards, environmental sustainability and anti-corruption; and engage with partners in other projects that give concrete expression to the Global Compact principles, in addition to advancing the broader development goals of the UN.”

© AccountAbility 2006

“Sustainable development is both a moral responsibility and an economic necessity”

Suez Lyonnaise des Eaux

.

Business and sustainable development

© AccountAbility 2006

Defining Corporate Responsibility

© AccountAbility 2006

What does effective corporate responsibility mean to you?

What organisation most impresses you?

Examples of organisations you are engaging with on CR

Defining Corporate Responsibility

© AccountAbility 2006© AccountAbility 2004

Growing public distrust towards large corporations

Social and environmental screening of investments

Increasing need for environmental and social risk management, growing insurance premiums

Standardisation for quality management & comparability

Campaigns by non-governmental organisations

Growing market for ethical goods & servicesLearning for products & process innovation

Legislative developments

Staff retention and attraction

Consumer boycotts

Corporate Responsibility Trends

© AccountAbility 2006

Reputation managementand licence to operate

Risk management

Investor relations & access to capital

Learning & innovation

Competitiveness & market positioning

Operational efficiencyEmployee motivation

AccountAbility launched theCWD website in Nov’03(www.conversations-with-disbelievers.net)

Driving Performance…

A growing evidence base

The Business Case

Corporate Responsibility - The business case

© AccountAbility 2006

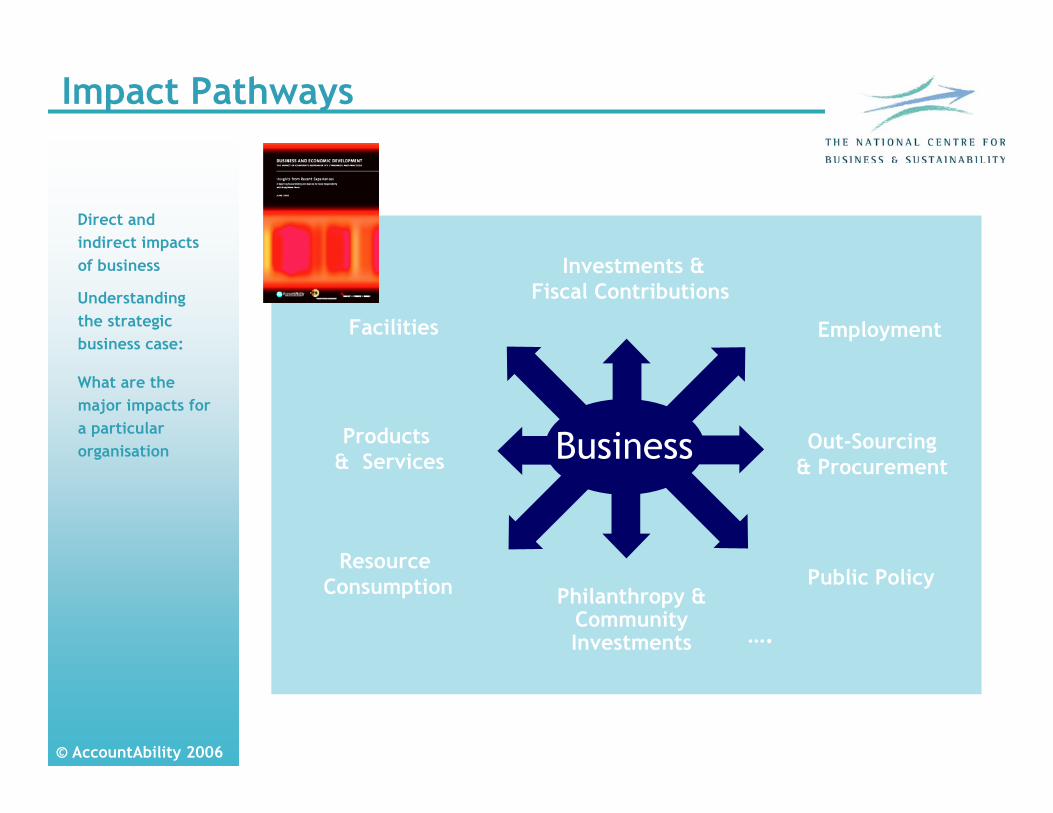

Direct and indirect impacts of business

Understanding the strategic business case:

What are the major impacts for a particular organisation

Philanthropy & Community Investments

Investments & Fiscal Contributions

Employment

ResourceConsumption

Products & Services

Facilities

Out-Sourcing& Procurement

Public Policy

Business

Impact Pathways

….

© AccountAbility 2006

"I believe that responsible business practices can be a significant competitive advantage for us"

7 2 1163

241

139

050

100150200250300

NoResponse

StronglyDisagree

Disagree NeitherAgree NorDisagree

Agree StronglyAgree

Responsible Business Practice Counts

Do you believe in the business case?

You can dowell by doing good.

© AccountAbility 2006

CR affecting Shareholder Value

Value of £100 invested over five years

020406080100120140160180

Mar

-99

Jun

-99

Sep

-99

Dec

-99

Mar

-00

Jun

-00

Sep

-00

Dec

-00

Mar

-01

Jun

-01

Sep

-01

Dec

-01

Mar

-02

Jun

-02

Sep

-02

Dec

-02

Mar

-03

Jun

-03

Sep

-03

Dec

-03

Mar

-04

Pounds

GPTW Cumulative FTSE All Share Cumulative FTSE 100 Cumulative

UK's Best Workplaces

[Source: GP2W 2004 www.greatplacetowork.co.uk]

The Great Place to Work companies which are listed in the FTSE have outperformed the general FTSE index by far as the graph below shows.Strong

connection between good HR practices and financial performance

87% of European employees feel greater loyalty to socially-engaged employers [Source: Fleishman Hillard (1999)]

© AccountAbility 2006

70

50

58

219

28

24

21

Lack of technical innovation Lack of knowledge Unwilligness to take riskCompetition Short-term financial targets OtherNo answer

Most significant constraints

Progressing Responsible Business Practice

“I have a narrow

window of time to absorb a great deal of information. I will look at these issues (social and

environmental factors) when

I getthe time…I don’t know

when that will be.”

“We find that firms are willing to sacrifice economic value in order to meet a short-run earnings…55% of managers would avoid initiating a very positive NPV project if it meant falling short of the current quarter’s consensus earnings”.

John Graham et al, ‘The Economic Implications of Corporate Financial Reporting

Ha ! Prove it.

© AccountAbility 2006

Developing a coherent response

institutionalizedlatent

ISSUE MATURITY

matureemerging

defensive

GEN

ERA

TIO

NA

L LE

AN

RIN

G

managerial

civil

strategic

compliance

“pioneers”

“laggards”

“That is how things

are”

“Its not ourjob to fix

THAT”

New business models

Partnerships and

public policy

Business has to fix

it

We need regulatory

or collaborative solutions

institutionalizedlatent

ISSUE MATURITY

matureemerging institutionalizedlatent

ISSUE MATURITY

matureemerging

defensive

GEN

ERA

TIO

NA

L LE

AN

RIN

G

managerial

civil

strategic

compliance

defensive

GEN

ERA

TIO

NA

L LE

AN

RIN

G

managerial

civil

strategic

compliance

“pioneers”

“laggards”

“That is how things

are”

“Its not ourjob to fix

THAT”

New business models

Partnerships and

public policy

Business has to fix

it

We need regulatory

or collaborative solutions

© AccountAbility 2006

institutionalizedlatent

ISSUE MATURITY

matureemerging

Civil Learning – Labor Standards

defensive

GEN

ERA

TIO

NA

L LE

AN

RIN

G

managerial

civil

strategic

compliance 2001Wal-Mart Mart

Code of Conduct

1998Nike

Code of Conduct

1992Levi Straus

Terms of Engagement

2004Nike, Gap, etc

Post-MFA Alliance

2000/1Nike

UN Global Compact

© AccountAbility 2006

CR Reporting

© AccountAbility 2006

Credibility in a Low-Trust World

Where are we?

© AccountAbility 2006

CR reporting

• Recent increase in CR reporting linked to demand for greater accountability and transparency

• Approaches to reporting are varied –inconsistency

• Metrics and evaluation methods are growing in number – potentially greater comparability and more objective measurement if common approaches

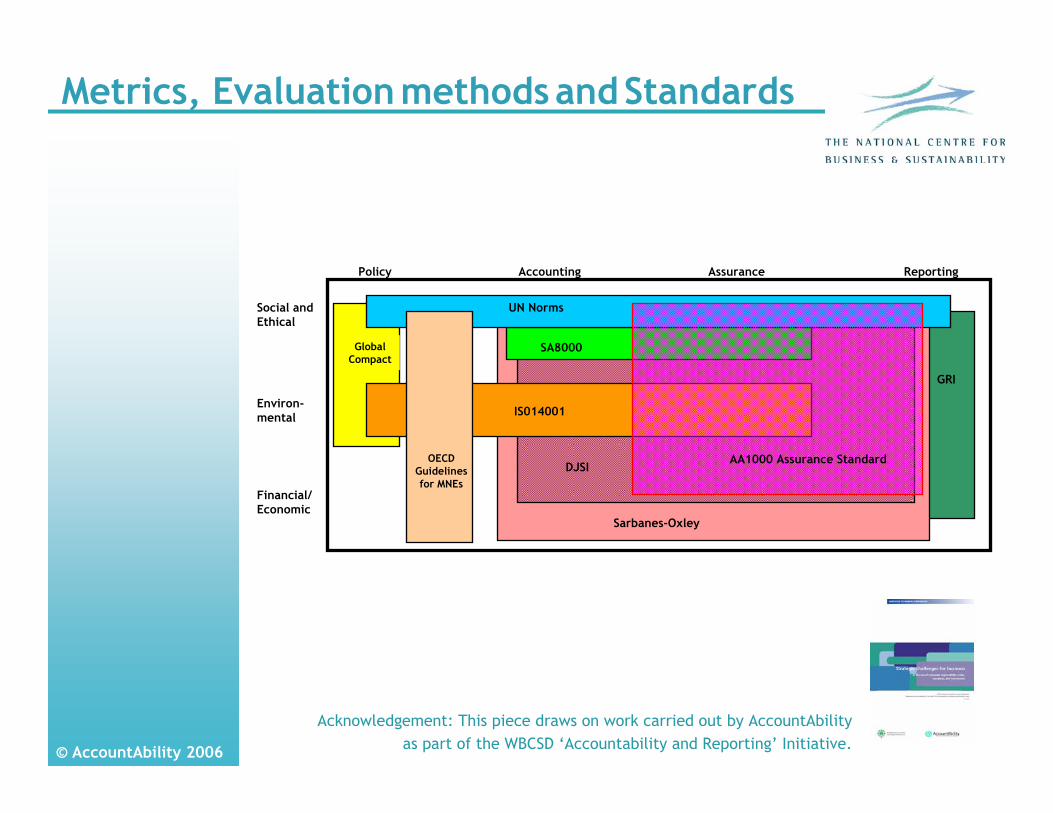

© AccountAbility 2006

Social and Ethical

Environ-mental

Financial/ Economic

Accounting Assurance Reporting

SA8000

Sarbanes-Oxley

DJSI

Policy

Global Compact

IS014001

UN Norms

OECD Guidelines for MNEs

GRI

AA1000 Assurance Standard

Acknowledgement: This piece draws on work carried out by AccountAbility as part of the WBCSD ‘Accountability and Reporting’ Initiative.

Metrics, Evaluation methodsandStandards

© AccountAbility 2006

CR reporting

• 52% of the 250 largest global companies produce CR reports (KPMG)

• 3750 companies report in EU, 45 in Hungary since 1999 (Corporate Register)

• Globally: highest number of reports –Japan; 2nd highest- UK (KPMG)

• Reports are getting longer; new formats.

© AccountAbility 2006

How useful are CR reports?

Which CR reports impress you and why?

The value of CR reports

© AccountAbility 2006

…Lots of Data Everywhere!

Credibility in a low trust world

The rise and rise of non-financial reporting

“Over the last few years, the quantity of information that has to be disclosed in reports has reached the point where even investors fail to read the detail…the time has come to call a halt to disclosure for disclosure’s sake. I think we have reached a point where providing less of the right quality will indeed yield more.”

[Chief Executive, UK Institute of Chartered Secretaries and Administrators]

But does it hit the Mark…?

© AccountAbility 2006

The Situation

Reports are not believed by stakeholders

Reports are not used to make decisions by stakeholders

Unclear whether reporting impacts on performance

The Idea

Credibly communicates to stakeholders

Enables report users (stakeholders) to make decisions

Improves performance

Intended Benefits of Reporting

Getting Reporting to Work

© AccountAbility 2006

Intended Benefits of Reporting

…so what’s the answer?

The Role of Assurance

Organisations and their stakeholders increasingly recognise that robust

assurance is a means of not only raising the credibility of reporting but inherently also

the effectiveness and quality of related sustainability management processes and

thus ultimately a means of improving performance and aligning ones operation

to societies expectations.

© AccountAbility 2006

“Assurance is an evaluation method that uses a specified set of principles and standards to assess the quality of an organisation’s subject matter and the underlying systems, processes and competencies that underpin its performance.”

AA1000 Assurance Standard

What do we mean by Assurance?

Defining Assurance

© AccountAbility 2006

…Not Doing Auditing

Assurance is the outcome one is seeking to achieve…

…to assure stakeholders so as to influence their behaviour, thereby impacting on the organisation’s success…

… it must not be confused with auditing and verification, which are no more or less than particular ways to achieve that result.

‘Assurance’is the Desired

Result, Not the Tool

Its About Delivering Assurance

© AccountAbility 2006

Principles

Completeness

“knowing your impact & what people think

of you”

Materiality

“knowing what is important to you and your stakeholders”

Responsiveness

“demonstrating adequate response

communicated in an adequate manner”

“accounting for stakeholders’aspirations and needs”

The Accountability Commitment‘Inclusivity’

The AA1000 Principles…

“accounting for stakeholders’aspirations and needs”

© AccountAbility 2006

“should address the credibility of the Report and the underlying systems, processes and competencies that deliver the relevant information and underpin the organisation’s performance.”

An AA1000 Assurance Statement…

© AccountAbility 2006

Adopting Companies Astrazeneca

BA

British Airports Authority

BAT

UU

BP

BT

Camelot

Citizens Bank of Canada

City West Water

The Co-operative Bank

CIS

Danisco

Danone

Diageo

Fuji Films

First Group

EDF Energy

Innogy

Landcare Research

Marks & Spencers

mm02

Newmont Mining

Northumbrian Water

Novo Nordisk

Novozymes

Premier Oil

SABMiller

Scottish Power

Southern Water

Stora Enso

Smiths Group

Tradecraft

Unilever

United Utilities

VanCity

Westpac Banking

Etc.

AA1000AS in use ...

© AccountAbility 2006

Sustainability Assurance

• Materiality• Completeness• Responsiveness

© AccountAbility 2006

“The Materiality Principle requires that the reporting organisation discloses information about its performance required by its stakeholders for them to be able to make informed judgements, decisions and actions.”

AA1000AS advocates an ‘open scope’ for the process –i.e. all potentially material issues should be considered to avoid significant omissions.

It is about decision-making

Materiality defined

- 3 -

© AccountAbility 2006

The 5-part Materiality

Generating a complete picture without implying a scope

5 buckets that can assist in identifying material issues and which information on the company’s non-financial performance should be disclosed in the report, in ways that it meets stakeholders needs.

© AccountAbility 2006

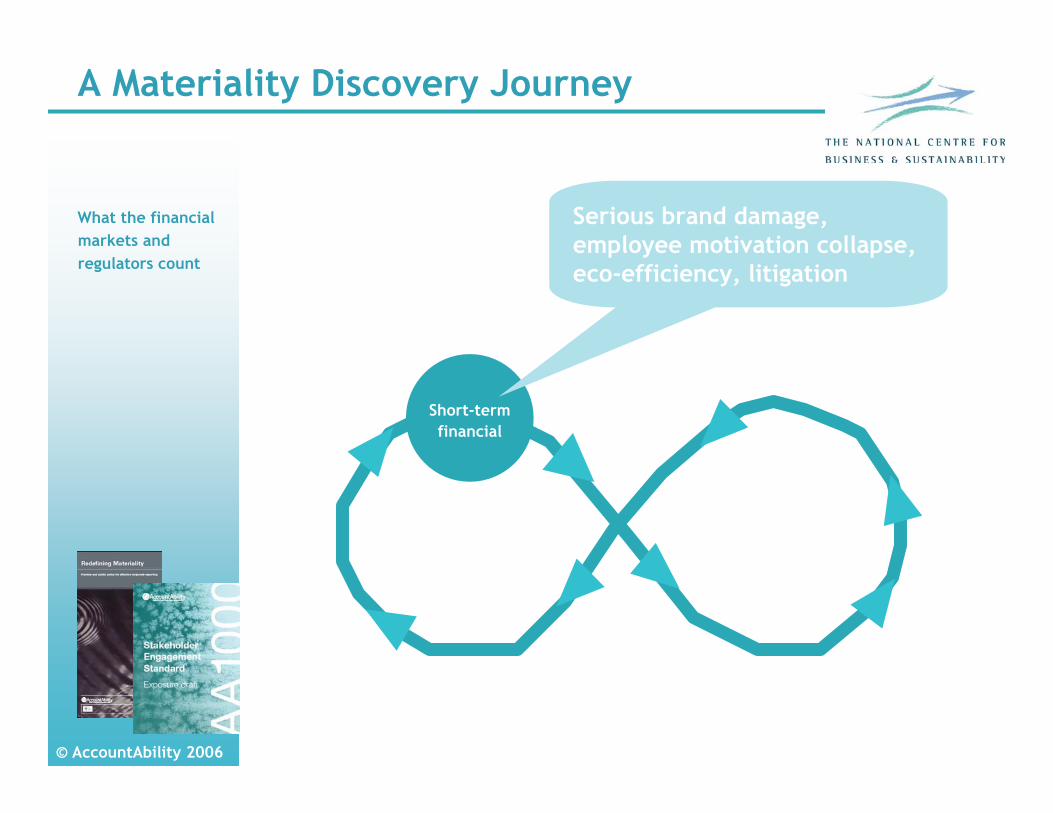

A Materiality Discovery Journey

What the financial markets and regulators count

Short-term financial

Serious brand damage, employee motivation collapse, eco-efficiency, litigation

© AccountAbility 2006

A Materiality Discovery Journey

What the organisation thinks is important

AND

Policy-based performance

Peer-based norms

Adidas, Reebok or others consider Nike-relevant aspects to be material

What my peers think is important

Core business strategy, public-stated policies on labour compliance etc.

© AccountAbility 2006

A Materiality Discovery Journey

What stakeholders think is important enough to act on

Stakeholder concerns and

behaviour

Investors chose whether to invest, employees whether to leave/work, consumers whether to buy.

© AccountAbility 2006

A Materiality Discovery Journey

What the wider society thinks is important enough to regulate or standardise

Societal norms

GRI, regulation

© AccountAbility 2006

“The AA1000 Completeness Principle requires that the reporting organisation understands its performance, impacts and stakeholder views relating to material issues.”

It is about management & measurement

Completeness defined

Sustainability Performance … meaning all Sustainability Performance associated with activities, products, services, sites and subsidiaries, for which it has management and legal responsibility and beyond

where it has influence in the outcome...

© AccountAbility 2006

Stakeholder Issues Evolve Dynamically

Well defined

Boundaries emerging

Boundaries being debated by society

Undefined boundaries with limited societal debate

Boundaries of Corporate Responsibility

Signals

Strong stakeholder expectationsState or inter-governmental regulation

Coherent stakeholder expectationsCorporate self regulation Co or multi-lateral regulation

Growing stakeholder expectationsCivil society regulation

No regulationLimited stakeholder expectations

Boundaries, Expectations & Regulation of Issue

Political actionsJudicial action

Multi-sector partnerships (e.g. GRI, Global Compact)Business Associations (e.g. Responsible Care)

NGO lobbyingMedia attentionPolitical awareness

Opinion leader interestActivist interest

Stakeholder Modes of Engagement

Strong evidence emerging Consensus building

Established

Evidence accepted

Institutionalised

Detailed research, but no conclusions

Emerging

Early awarenessExploratory research, perceptions but no evidence

Latent

EvidenceLevel of maturity

Maturity of issue …

© AccountAbility 2006

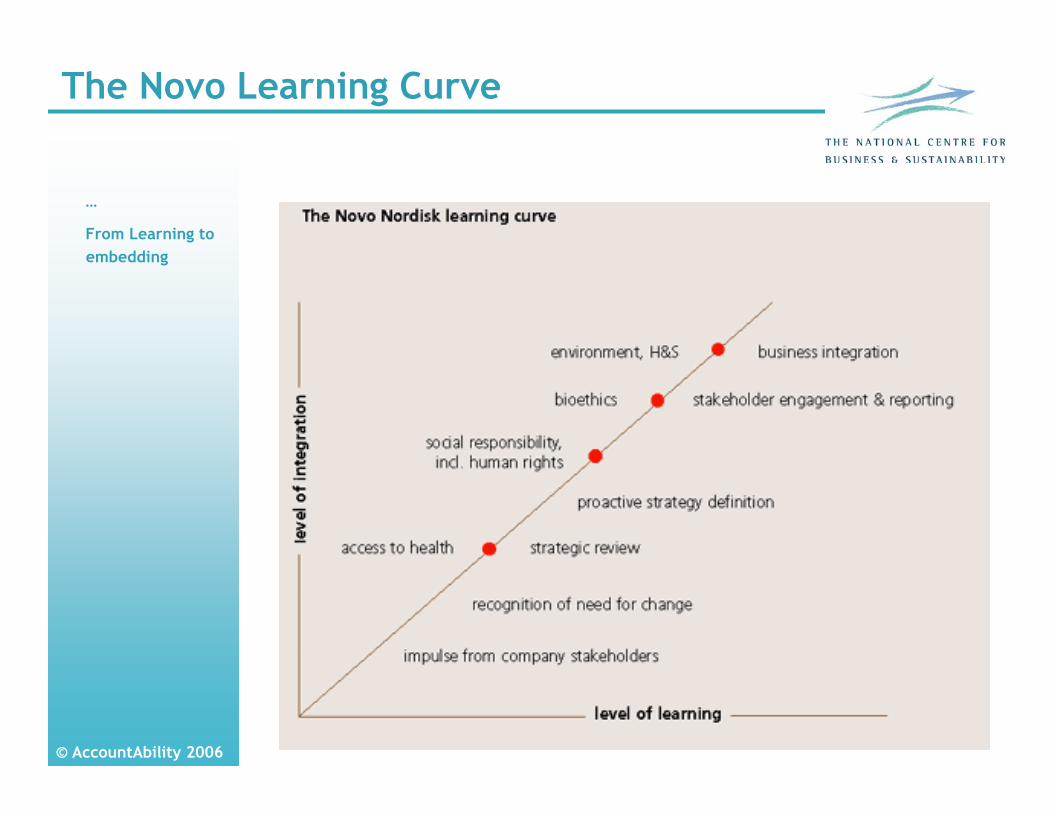

…

From Learning to embedding

The Novo Learning Curve

© AccountAbility 2006

“The AA1000 Responsiveness Principle requires that the assurance provider evaluates whether the reporting organisation has responded to material stakeholder issues concerns and adequately communicated these responses in its Report.”

It is about demonstrating response to people’s concerns

Responsiveness defined

The Responsiveness Principle requires that the Reporting Organisation demonstrate in its Report what it has decided to do in response to specified Stakeholder concerns and interests…

… considering the past and future

© AccountAbility 2006

… but keeping it

realistic

However…

This principle does not require the organisation to agree or comply with all stakeholder concerns and interests, but that it demonstrates that it has a process in place to identify stakeholders views and expectations, to prioritise its response and has responded coherently and consistently to them in an accessible manner.

It is about making it real…

“The acid test of credible and value adding reporting is whether the organisation reflects an adequate response to material issues surfaced by the accountability process.”

© AccountAbility 2006

Statement on use of AA1000 Assurance Standard

Basic description of work undertaken

Description of Assurance level pursued (i.e. limitations concerning the work undertaken or the accountability boundary set by the organisation or scope for the assignment)

Description of the agreed criteria to be used during the process

Key Components of an AA1000AS Statement

© AccountAbility 2006

Opinion/ Conclusion as to the quality of the Report and underlying organisational processes, systems and competencies concerning:

Materiality: The Report provides a fair and balanced representation of material aspects of the organisation’s performance.

Completeness: The organisation has an effective process in place for identifying and understanding activities, performance, impacts and stakeholder views.

Responsiveness: The organisation has an effective process in place to respond to stakeholder views, including any significant weaknesses in the underlying. process.

Assurance Statement - Components

© AccountAbility 2006

Commentary on:

Progress since last report

Suggested improvements

Practitioner's Competency, Independence and Impartiality

Assurance Statement - Components

© AccountAbility 2006

Review the two assurance statements and discuss:

Which one makes you feel most assured?

Why?

What is the added value of the assurance statement?

Exercise: Assurance Statements

© AccountAbility 2006

Stakeholder Engagement

© AccountAbility 2006

What is good stakeholder engagement?

Examples of stakeholder engagement methods that have been effective for you

Stakeholder engagement

© AccountAbility 2006

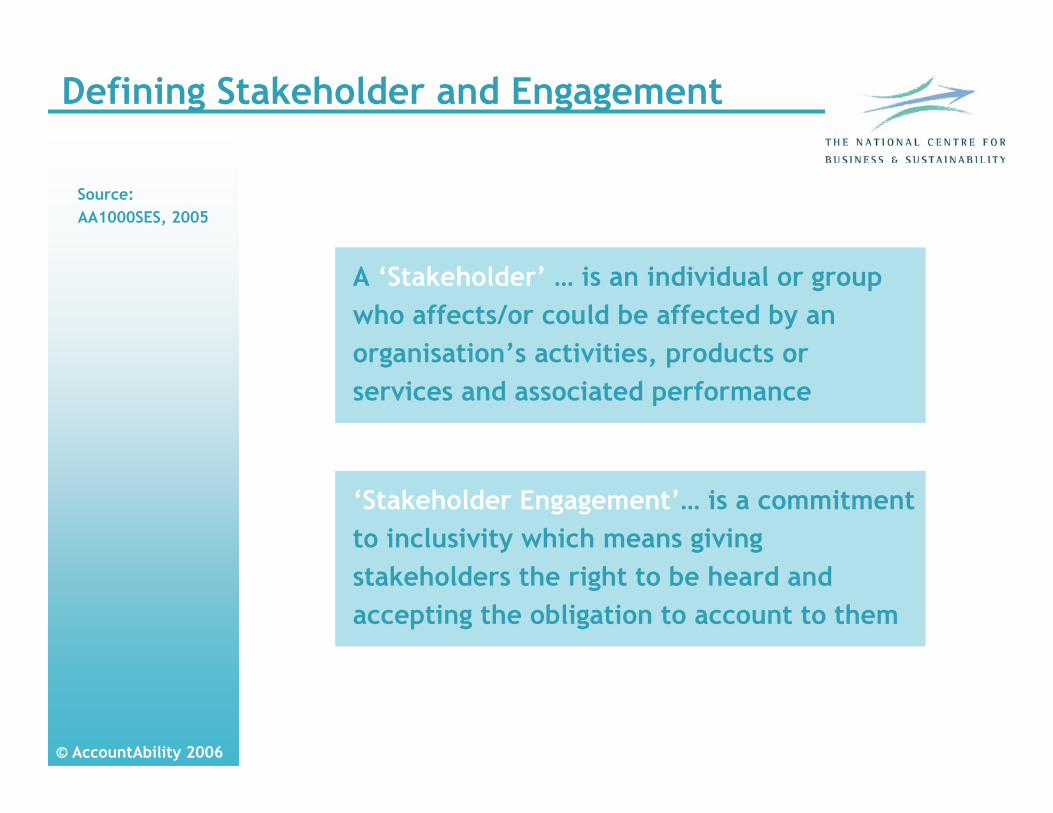

Source: AA1000SES, 2005

Defining Stakeholder and Engagement

A ‘Stakeholder’ … is an individual or group who affects/or could be affected by an organisation’s activities, products or services and associated performance

‘Stakeholder Engagement’… is a commitment to inclusivity which means giving stakeholders the right to be heard and accepting the obligation to account to them

© AccountAbility 2006

What do we mean by effective (or successful) SE?

Learning, Innovation & Performance

Increases understanding of stakeholders and the business environment, inc. market developments

Enables better management of risk & reputation

Builds trust-based relationships

Informs stakeholders decisions and actions that impact on the company and on society

Allows for the pooling of resources (knowledge, people, money & technology) for joint problem solving

Contributes to more equitable and sustainable development by giving those who have a right to be heard the opportunity to be heard

for companies, NGOs, governments and partnerships...

© AccountAbility 2006

Start here…

And then stakeholder strategies shift

Poor engagement on an issue:

no communication,poor understanding,

confusion, wasted energy,

missed opportunities,unmet needs,

stand-off,conflict,violence

Setting the Scene

© AccountAbility 2006

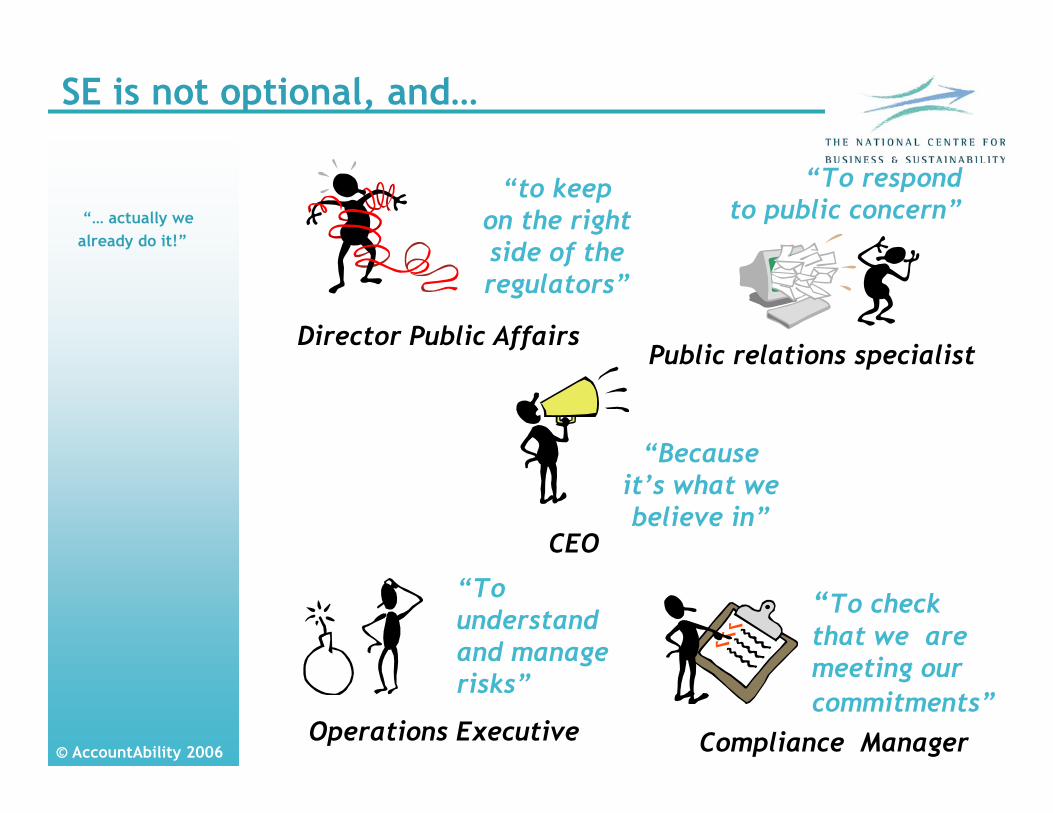

SE is not an option!

If they didnIf they didn’’t theyt they’’d be d be out of business.out of business.

“ Stakeholder engagement isinteraction and dialogue between an organisation and its stakeholders.”

Why do businesses engage?

It’s a No-brainer

© AccountAbility 2006

“To respondto public concern”

“to keep on the right side of the regulators”

“To check that we are meeting our commitments”

“To understand and manage risks”

Director Public Affairs

Compliance Manager

Public relations specialist

Operations Executive

CEO

“Because it’s what we believe in”

“… actually we already do it!”

SE is not optional, and…

© AccountAbility 2006

“The traditional model of communications and decision-making, based on the pyramid of authority is no longer relevant.

It's been replaced by the sphere of cross influence, which means that companies and brands must build a one-to-one personal dialogue with many different stakeholders.”

Richard Edelman

SE is not optional, and…

“… actually we already do it!”

© AccountAbility 2006

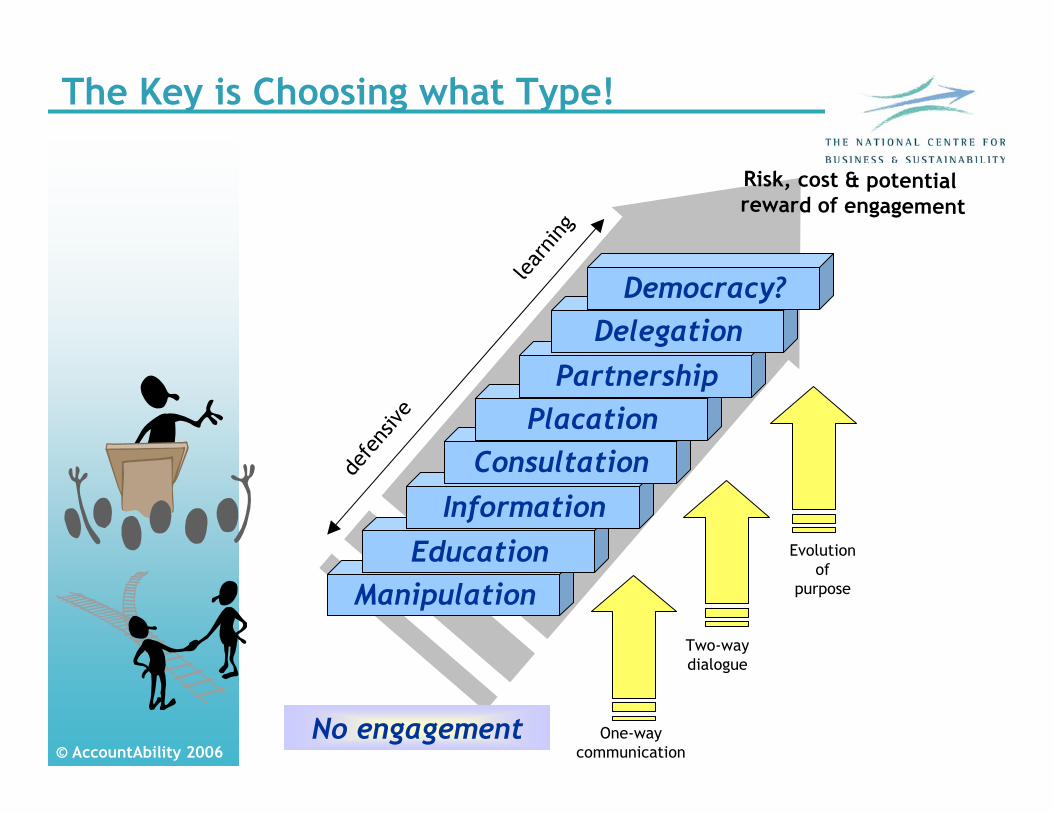

ManipulationEducation

Risk, cost & potentialreward of engagement

InformationConsultation

PlacationPartnership

DelegationDemocracy?

One-waycommunication

Two-waydialogue

Evolution of

purpose

defe

nsive

lea

rnin

g

No engagement

The Key is Choosing what Type!

© AccountAbility 2006

Global Compliance Program Evolution for Gap Inc.

“There are no easy answers to complex problems. Monitoring helps, but

sustainable change across our industry will only occur through collaboration

with partners worldwide”Dan Henkle, Gap Inc. 2004

“We’ve taken important steps toward safer conditions and better treatment for

workers in garment factories, but the social responsibility issues across

industry remain immensely complex”Paul Pressler, Gap Inc., 2005

An Example in Practice…

© AccountAbility 2006

Gap Inc’s changing approach to engaging with NGOs as public interest intensifies over time

Time

Inte

nsit

y

1992Sourcing

Guidelines

1995Mandarin Int. Labor Conflict

1996Code of Vendor Conflict

1999SaipanLawsuit

2000Child Labor

allegations

2001Contract Worker Rights

2002Reporting, Partnership & Training

2003SAI & Global

Compact

20041st SR Report

2005Global Vendor Summit

Publ

ic In

tere

st

An Example in Practice…

© AccountAbility 2006

Carrying out Stakeholder engagement:thinking strategically…

Where you start will depend on your own context, and on whether you are already engaging or are a newcomer

© AccountAbility 2006

UNEP Stakeholder Engagement Manual

Uses for organisations:• Engagement with your organisation’s

stakeholders on issues• Assessing stakeholder engagement

exercises carried out by other organisations / companies

• Understanding the context of stakeholder engagement that you take part in

© AccountAbility 2006

UNEP Stakeholder Engagement Manual

1. Think strategically2. Analyse and plan3. Strengthen capacities for engagement4. Design the process and engage with

stakeholders5. Act, review and report

© AccountAbility 2006

Think strategically

• Who are the stakeholders?• What are the strategic engagement risks,

opportunities and objectives?• How important are the issues to the

different stakeholder groups?

© AccountAbility 2006

Stakeholders that affect your organisation

Stakeholders affected by your organisation

Stakeholders that you interact with most

Stakeholders core to your mission and values

“People without whose support your business would fail in the short

term”

“People who could benefit from your business if you ran it with them in mind”

“People you would ignore except that they have

friends in powerful places”

“People who will play a part in your company’s

future success”

Prioritising Stakeholders…

Drawing on the 6-part Stakeholder Mapping test

© AccountAbility 2006

Influence and Dependency Matrix…

© AccountAbility 2006

Exercise: identifying stakeholders

© AccountAbility 2006

Analyse and plan

Do you understand the issues and stakeholders sufficiently to design a robust engagement process?

– How are the issues currently managed in your organisation?

– Draw on learning from others on how to address the issues

– Profile your stakeholders – how do they prefer to engage? What are their expectations and influence?

– What is you organisation able and not able to do on these issues?

– Develop an engagement plan.

© AccountAbility 2006

Exercise: analyse and plan

© AccountAbility 2006

Strengthen capacities for engagement

Does your organisation have the capacity to understand the issues, engage effectively and respond coherently?

– What skills and capacities are needed for engagement?

– Consider stakeholder capacities and other practical issues

© AccountAbility 2006

Design the process and engage

• Does the engagement process meet the needs of your organisation and stakeholders?– Best way to engage– Design and prepare for the process– Engage

© AccountAbility 2006

One to one interviews

Group interviews

Focus groups

Workshops and seminars

Public meetings

Questionnaires

Web discussions

Experiential Learning

Techniques

© AccountAbility 2006

Act, review and report

Are you able to respond to and learn from stakeholders’ concerns and opinions?

– Report back to stakeholders– Review the process for future

© AccountAbility 2006

Allow stakeholders to assist in the identification of other stakeholders.

Involve stakeholders in defining the terms of engagement.

Ensure that stakeholders trust the social and ethical accountant collecting and processing the findings of the engagement.

Ensure all parties have sufficient preparation time and briefing to have well-informed opinions and decisions.

Allow stakeholders to voice their views without restriction and without fear, but with awareness that if their opinions are acted upon, this will have consequences upon them and other stakeholders.

Useful points to remember

© AccountAbility 2006

Something to think about

© AccountAbility 2006

How does Tesco Engage & Identify Issues?

Regeneration of deprived areas,Long-term unemployment,Impacts on local shops

Health promotion,Disability

Stable relationshipsProduct info & safety,Compliance

Development opportunities,Worker safety

Ethics in the supply chain,Cost of healthy food

Examples of key issues:

Community partnerships, provision of local training schemes, annual independent survey

CR committee

Anonymous survey, supplier meetings and conferences

Anonymous staff surveys, in-shop focus groups, internal CR communications group

General and issue specific focus groups, surveys

Example engagement mechanism:

Local communities & the wider public

NGOs

Suppliers

Staff

Customers

Stakeholders:

Engagement of stakeholders to identify issues in the food retail industry

© AccountAbility 2006

NGO/Business Partnerships

© AccountAbility 2006

Partnerships

• “People and organisations form some combination of public, business and civil constituencies who engage in voluntary, mutually beneficial innovative relationships to address common societal aims through combining resources and competencies”– Copenhagen Centre

© AccountAbility 2006

Examples

• Employer-supported volunteering (volunteers learn from and build the strength of community organisations)

• National governments, unions, NGOs, industry come together to address labour issues in supply chains

© AccountAbility 2006

Discussion: partnerships

Is your organisation involved in any partnerships with business?

Why did it get involved in these?

What are your experiences?

© AccountAbility 2006

Why the growth in partnerships?

• Traditional NGO/business relationships changing:– Value of multiple-perspectives recognised– Limitations of traditional cause-related

marketing; increasing NGO budgets, etc

• Many social issues becoming too complex for 1 organisation to address alone and ‘going it alone’ can be risky

• Changing role of governments

© AccountAbility 2006

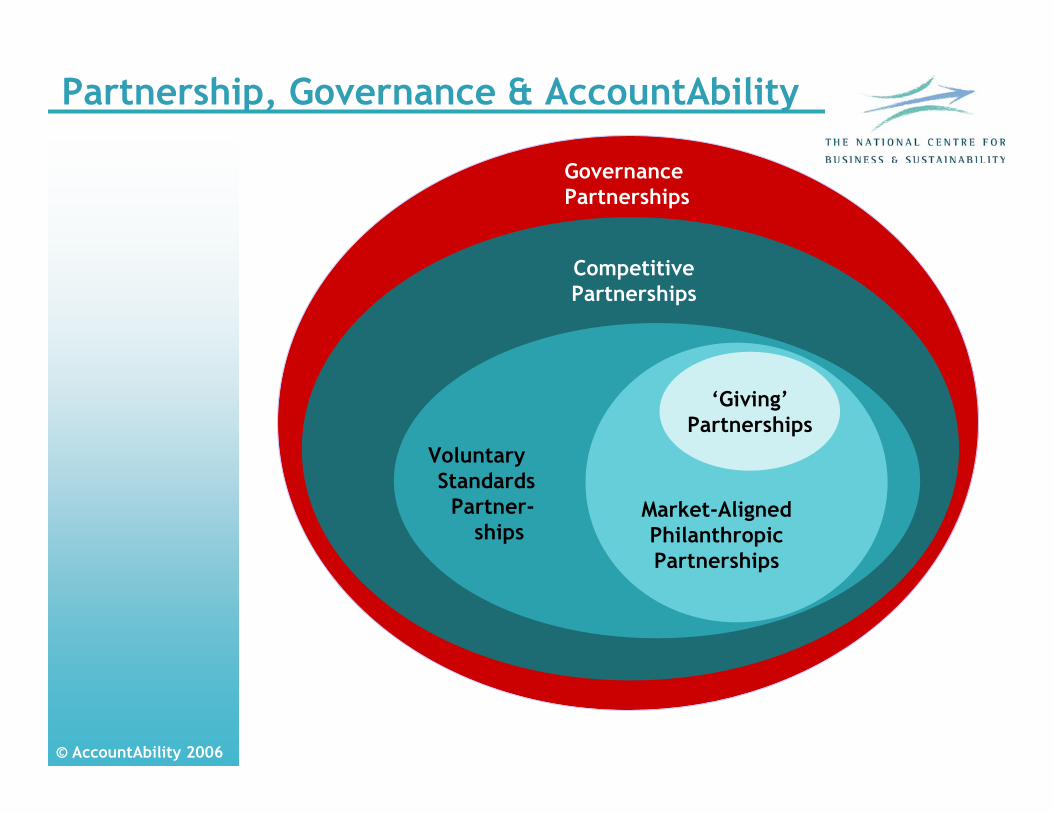

Partnership, Governance & AccountAbility

Governance Partnerships

CompetitivePartnerships

Voluntary Standards

Partner-ships

Market-AlignedPhilanthropicPartnerships

‘Giving’Partnerships

© AccountAbility 2006

Organisationallearning for IBM with SeniorNet

New opportunities:The market for disability

friendly products is rising: 23% of the global population will be

affected by 2020.

Process innovation:SeniorNetworked with its clientele to beta test new technology

Product innovation:IBM develops accessibility technology which allows users to change the way the web is displayed to make it easier to read, understand and interact with.

OrganisationalLearning

Stakeholder engagement:IBM’s Community Relations Unit brokered a partnership between IBM’s research labs and the non-

profit organisation SeniorNet

Insights: What accessibility features do

SeniorNet’s clientele with vision, motor

and memory impairments need?

New approaches to stakeholder engagement:IBM commissioned SeniorNet to staff a help desk providing support to users and feedback to IBM.

Example in Practice:

© AccountAbility 2006

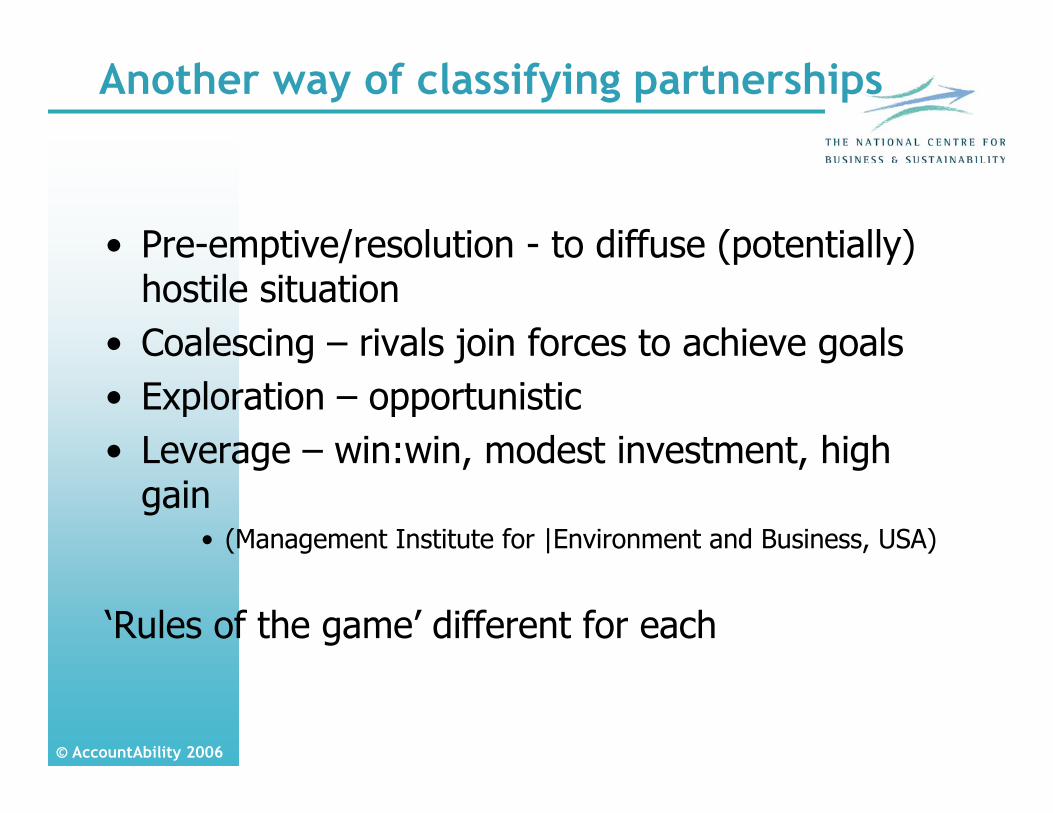

Another way of classifying partnerships

• Pre-emptive/resolution - to diffuse (potentially) hostile situation

• Coalescing – rivals join forces to achieve goals• Exploration – opportunistic• Leverage – win:win, modest investment, high

gain• (Management Institute for |Environment and Business, USA)

‘Rules of the game’ different for each

© AccountAbility 2006

Potential risks of partnerships

Potential benefits of partnerships

For Partnership participants (NGOs, government, business…)

Discussion: partnerships

© AccountAbility 2006

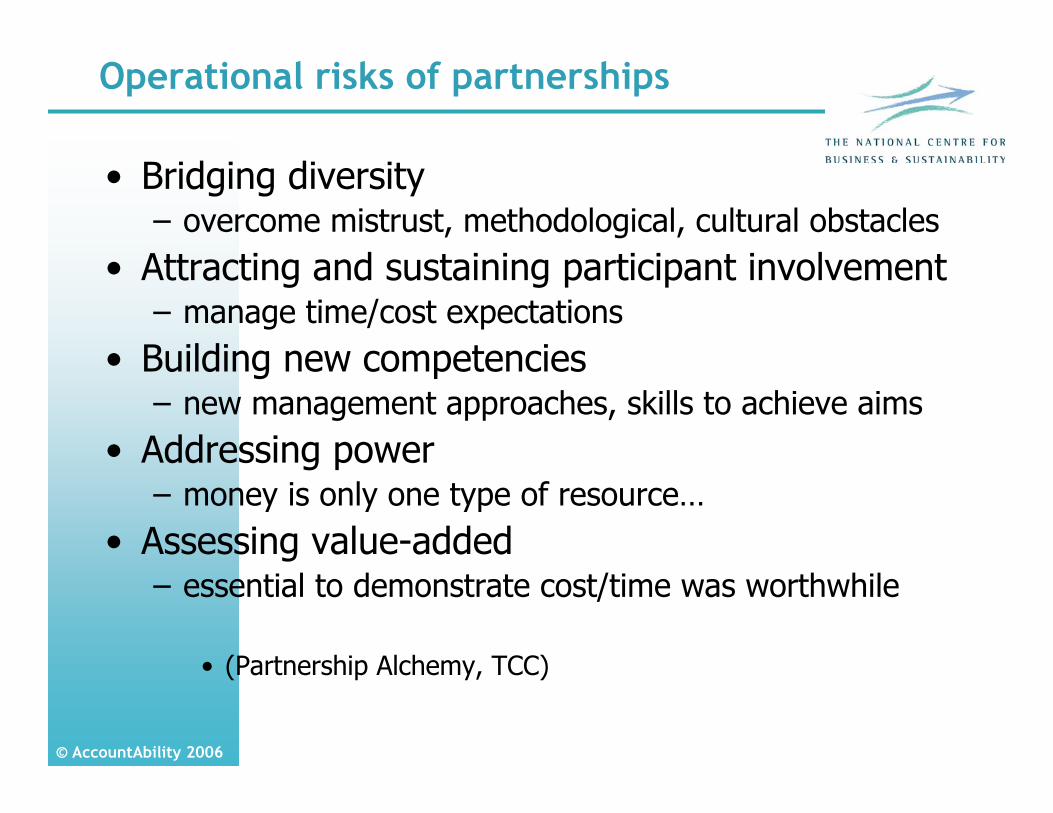

Operational risks of partnerships

• Bridging diversity– overcome mistrust, methodological, cultural obstacles

• Attracting and sustaining participant involvement– manage time/cost expectations

• Building new competencies– new management approaches, skills to achieve aims

• Addressing power– money is only one type of resource…

• Assessing value-added – essential to demonstrate cost/time was worthwhile

• (Partnership Alchemy, TCC)

© AccountAbility 2006

Potential participant benefits of partnerships

• Development of human capital• Improved operational efficiency• Organisational innovation• Increased access to resources• Better access to information• Enhanced reputation and credibility• Creation of a stable society

© AccountAbility 2006

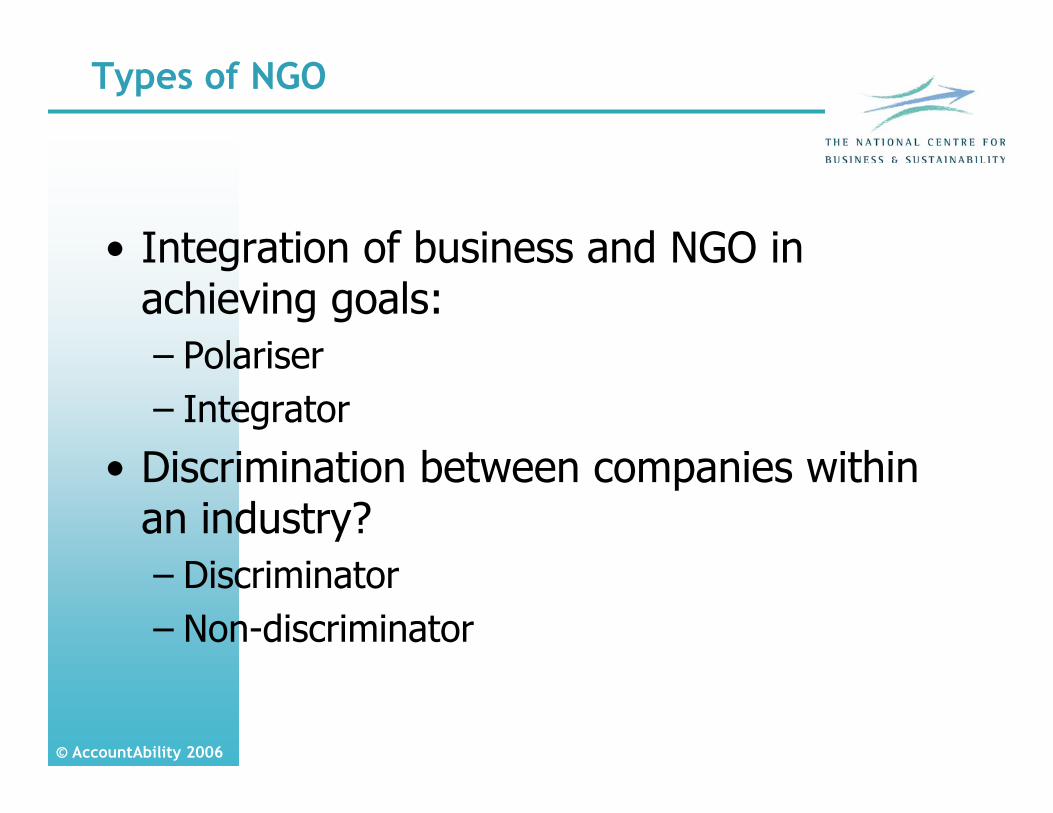

Types of NGO

• Integration of business and NGO in achieving goals:– Polariser– Integrator

• Discrimination between companies within an industry?– Discriminator– Non-discriminator

© AccountAbility 2006

Types of NGO

Polarizer

Integrator

Discriminator

Killer whale

Dolphin

Non-discriminator

Shark

Sealion

Polarizer

Integrator

Discriminator

Killer whale

Dolphin

Non-discriminator

Shark

Sealion

Polarizer

Integrator

Discriminator

Killer whale

Dolphin

Non-discriminator

Shark

Sealion

© AccountAbility 2006

What category does your organisation fall into?

What implication does this have for involvement in NGO/business partnerships?

Discussion: partnerships

© AccountAbility 2006

Things to consider for successful partnerships

• Context– Acknowledgement of drivers and triggers

• Purpose– Mutual agreement on purpose and agenda

• Participants– Effective leadership– Understand resources, skills, capacity needed

• Organisation– Appropriate organisational and legal structure– Transparency and accountability– Communication

• Outcomes– Measurement, evaluation and adaptability

© AccountAbility 2006

PGA Framework

Partnership, Governance & AccountAbility

[Source: AccountAbility, supported by USAID]