course title: financial statement analysis course code: mgt-537 course instructor: dr. hafiz...

TRANSCRIPT

Course Title: Financial Statement Analysis

Course Code: MGT-537

Course Instructor: Dr. Hafiz Muhammad Ishaq

Total Lectures: 32

Previous Lecture Summary

• Accounting Cycle, • Auditor’s Opinion and Auditor’s Report • Closing of Temporary Accounts• T-Accounts• Balance Sheet formats • Types of Assets • Inventory Methods

Today's Lecture Topic

• Basic Elements of the Balance Sheet

• Assets, Current and Fixed Assets• Different methods of depreciation• Current liabilities.

Current Assets

• Prepaid– Expenditures made in advance of the use

of the service or goods.– Examples

• Insurance• Advertising

Long-Term Assets: Tangible

• Land– Carried at acquisition cost– Not subject to depreciation– Natural resources are depleted

• Buildings– Cost plus permanent improvements– Depreciated over the useful life

Long-Term Assets: Tangible (cont’d)

• Machinery– Acquisition cost plus costs of delivery,

installation, and permanent improvements– Depreciated over the useful life

• Construction in Progress– Assets under construction– Transferred to permanent asset account

upon completion

Long-Term Assets: Tangible (cont’d)

• Accumulated Depreciation– Carries the to-date depreciation of plant assets– Factors used in depreciation calculation

• Asset cost• Length of the life of the asset• Estimated salvage (residual) value of asset when retired

– Depreciation methods– Straight Line – Double Declining Balance– Sum-of-the-Years’-Digits – Units of Production

• Balance sheet presentation

Cost of the asset – Accumulated depreciation= Net book value

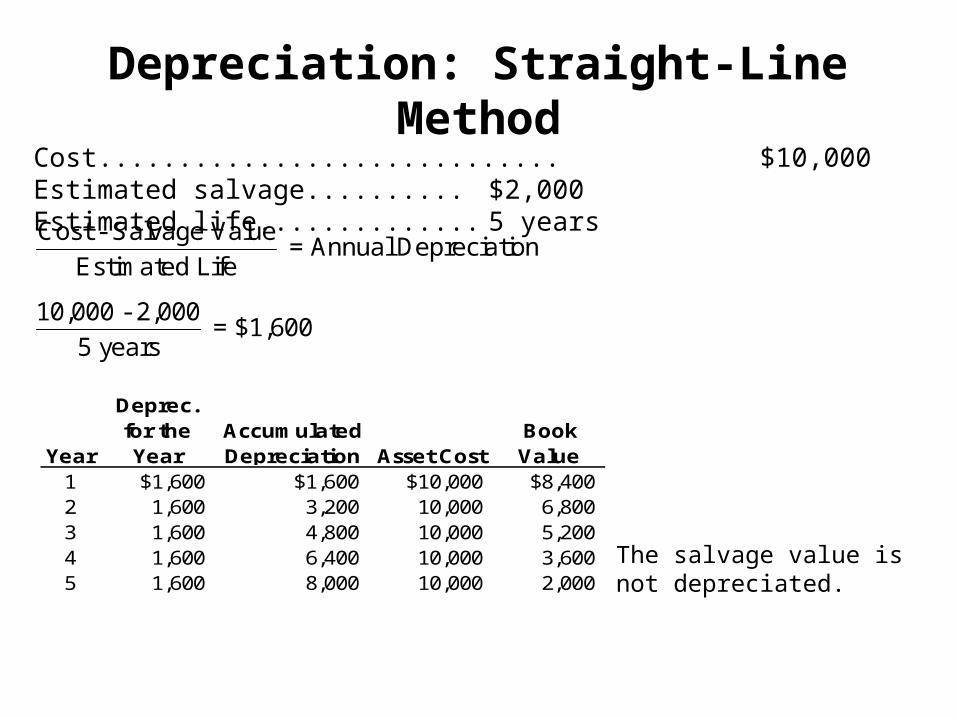

Depreciation: Straight-Line Method

Cost - Salvage Value = Annual Depreciation

Estimated Life

10,000 - 2,000 = $1,600

5 years

Cost............................. $10,000 Estimated salvage.......... $2,000Estimated life.............. 5 years

Year

Deprec. for the Year

Accumulated Depreciation Asset Cost

Book Value

1 $1,600 $1,600 $10,000 $8,4002 1,600 3,200 10,000 6,800 3 1,600 4,800 10,000 5,200 4 1,600 6,400 10,000 3,600 5 1,600 8,000 10,000 2,000

The salvage value is not depreciated.

Depreciation: Declining-Balance Method

1 2 = double the straight-line rate

Estimated Life

1 2 Book Value at Beginning of Year = Annual Depreciation

5

YearAsset Cost

Beginning Accum.

Dep.Beginning

Book ValueDeprec. for

the Year

Ending Book Value

1 $10,000 $0 $10,000 $4,000 $6,0002 10,000 4,000 6,000 2,400 3,600 3 10,000 6,400 3,600 1,440 2,160 4 10,000 7,840 2,160 160 2,000 5 10,000 8,000 2,000 - 2,000

Scrap value is not used in the depreciation formula but depreciation ends when the book value is equal to the salvage value.

Cost............................. $10,000 Estimated salvage.......... $2,000Estimated life.............. 5 years

Double the straight-line rate is the maximum rate

Depreciation: Sum-of-the-Years’-Digits Method

Cost............................. $10,000 Estimated salvage.......... $2,000Estimated life.............. 5 years

Number of Remaining Years Cost - Salvage = Annual Depreciation

Sum of Digits of Estimated Life

5 10,000 - 2,000 = $2,666.67

1+2+3+4+5

Year

Cost Minus

Salvage FractionDeprec. for

the Year

Ending Accum.

Dep.

Ending Book Value

1 $8,000 5/15 $2,666.67 2,666.67$ 7,333.33$ 2 8,000 4/15 2,133.33 4,800.00 5,200.00 3 8,000 3/15 1,600.00 6,400.00 3,600.00 4 8,000 2/15 1,066.67 7,466.67 2,533.33 5 8,000 1/15 533.33 8,000.00 2,000.00

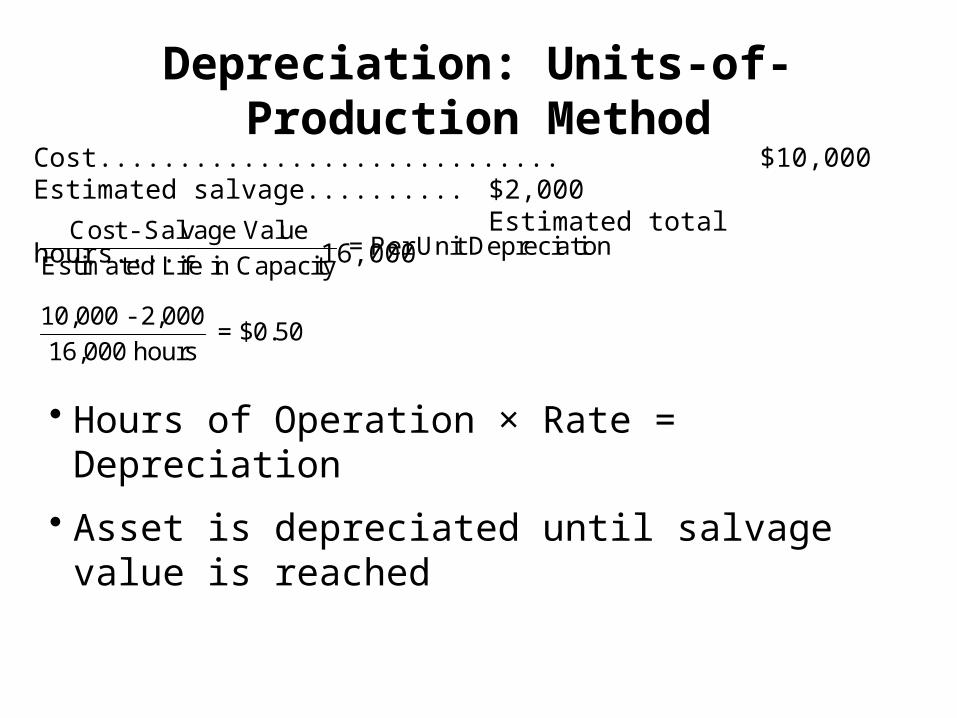

Depreciation: Units-of-Production Method

Cost - Salvage Value = Per Unit Depreciation

Estimated Life in Capacity

10,000 - 2,000 = $0.50

16,000 hours

Cost............................. $10,000 Estimated salvage.......... $2,000Estimated total hours..... 16,000

• Hours of Operation × Rate = Depreciation

• Asset is depreciated until salvage value is reached

Chapter End ProblemAn item of equipment acquired on January 1 at a cost of $100,000 has an estimated life of ten years Required: Assuming that the equipment will have a salvage value of $10,000 determine the depreciation for each of the first three years by the • Straight line method• Declining balance method• Sum of the year digit method

Chapter End Problem

An item of equipment acquired on January 1 at a cost of $60,000 has an estimated use of 25,000 hours. During the first three years the equipment was used 5,000 ,6000 and 4,000 hours respectively. The estimated salvage value of the equipment is $10,000Required: Determine the depreciation for each of three years, using the unit of production method

Long-Term Assets: Leases

• Capital lease– In-substance ownership– Recorded as an asset net of amortization

Long-Term Assets: Investments

• Debt or equity securities– Held to maintain business relationship or to

exercise control• Debt classification

– Held-to-maturity carried at amortized cost– Available-for-sale carried at fair value

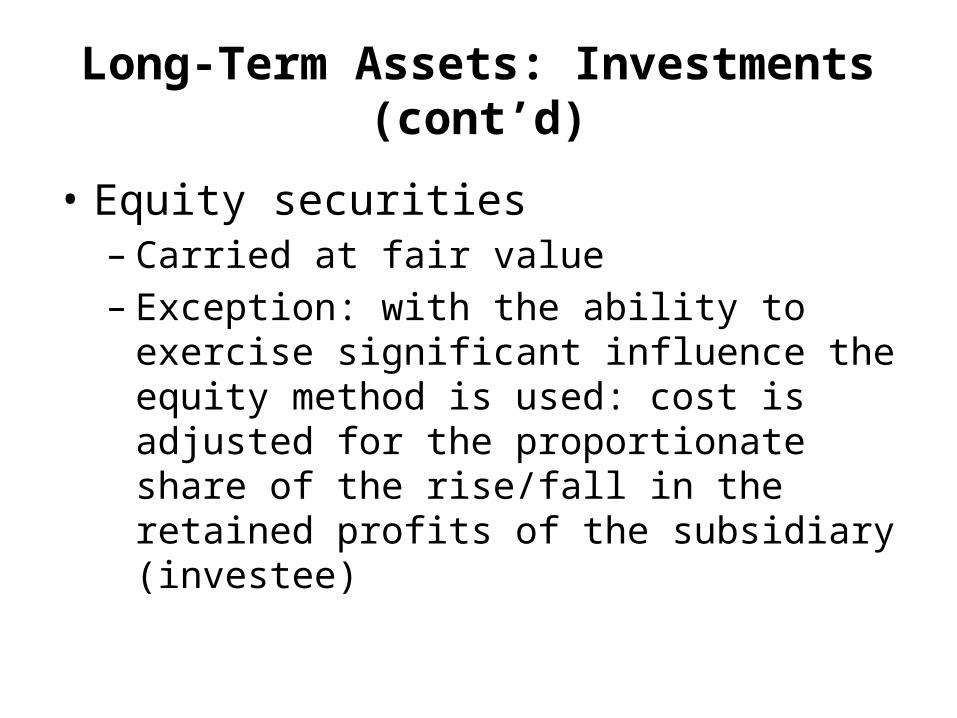

Long-Term Assets: Investments (cont’d)

• Equity securities– Carried at fair value– Exception: with the ability to exercise significant

influence the equity method is used: cost is adjusted for the proportionate share of the rise/fall in the retained profits of the subsidiary (investee)

Long-Term Assets: Intangibles• Goodwill

– Purchase of a business where price paid exceeds the fair value of net assets

– GAAP: not amortized; test annually for impairment• Patents

– 20 years– Amortized over shorter of legal or useful life

• Trademarks– Indefinite legal life– Not amortized; test annually for impairment

Long-Term Assets: Intangibles (cont’d)

• Franchises– Life based on contract– Amortize over shorter of legal or useful life

• Copyrights– Life of the creator plus 70 years– Amortize over shorter of legal or useful life

Liabilities• Probable future sacrifices of economic

benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the futures as a result of past transactions or events

– Current Liabilities

– Long-Term Liabilities

Current Liabilities

• Obligations whose liquidation is reasonably expected to

• Require the use of– Existing current assets– Creation of other current liabilities

• Within one year or the operating cycle, whichever is longer

Current Liabilities (cont’d)

• Payables– Short-term obligations created by the

acquisition of goods or services• Unearned Income

– Payments collected in advance of the performance of services or delivery of goods

• Other current liabilities– As circumstances warrant

Lecture Summary• Basic Elements of the Balance Sheet• Assets, Current and Fixed Assets• Tangible Assets • Intangible Assets• Different methods for calculation of

depreciation• Current liabilities.