course introduction/ determine the difference between internal and external reporting © dale r....

TRANSCRIPT

Course Introduction/Course Introduction/Determine the Difference Between Determine the Difference Between

Internal and External ReportingInternal and External Reporting

© Dale R. Geiger 2011 1

2© Dale R. Geiger 2011

Terminal Learning ObjectiveTerminal Learning Objective• Task: Determine the difference between internal

and external reporting• Condition: You are training to become an ACE

with access to ICAM course handouts, readings, and spreadsheet tools and awareness of Operational Environment (OE)/Contemporary Operational Environment (COE) variables and actors

• Standard: with at least 80% accuracy:• Define the 4 characteristics of accounting information• Identify key components of GFEBS output• Classify GFEBS reports as internal or external

© Dale R. Geiger 2011 3

Cost Maturation ProcessCost Maturation Process

Single Use

EstimatedFuture Cost

Cost BenefitAnalysis

Cost InformedDecisions

Persistent Use

Expected and Actual Cost

Continuous Improvement

Cost-Managed Organizations

Universal Use

Planned & Actual Cost

Role Based, Org Based, Output Based Control

Cost-Managed Enterprise

Cost War Cost War High Cost War Full Insurgency Intensity Conflict Spectrum Operations

Starting here (Some work is being done now) TARGET© Dale R. Geiger 2011 4

Transforming the Army:Transforming the Army:Four Requirements for SuccessFour Requirements for Success

Need Status Action

Leadership Team with ACE to create “informed” leaders

Exploit existing strong leadership capabilities

ACE Build strong staff, strong organization

Select, develop ACEs (Asst to Comdr – Enterprise)

Design and deliver advanced training

Process Modify “winning the cost war” template as needed

Cost Info Use new tools as they come online

© Dale R. Geiger 2011 5

• Principles of Cost Analysis and Management• Targeted at entry level CP11 Personnel, Sergeants,

Lieutenants, Junior Captains• Course Length: Three Weeks• Pre-requisites: On Line Math Refresher

• Intermediate Cost Analysis and Management• Targeted at mid career CP11 Personnel, Staff Sergeants

and above, Senior Captains, Majors and above• Course Length: Three Weeks• Pre-requisites: On Line Math Refresher

ACE Development: PCAM & ICAMACE Development: PCAM & ICAM

© Dale R. Geiger 2011 6

All CEs will require basic, advanced, and master skills with a concentration in:Readiness – Capacity management and force cost analysisMateriel – Logistics and working capital funds cost analysisHuman Capital – Manpower cost analysisServices & Infrastructure – Services and capital asset costingFAs and CPs that are common to all CEs should train to become a master in any CE

Stackable CredentialsStackable Credentials

* NOTE: Stackable credentials are based on Financial Management (BC36/CP11) career field demands for cost management, which is the Army maximum; other career fields will use a subset of these requirements.

Based on the Financial Management Career Field

© Dale R. Geiger 20117

ICAM ICAM

• Develop advanced cost management skills• Next step for those already fulfilling the role of

ACE or who wish to become and ACE

© Dale R. Geiger 2011 8

Purpose of CoursePurpose of Course

• Develop skills in Cost Management• Includes conference, demonstration and practical

exercises, and case study• Emphasizes critical thinking• Introduces Excel templates to facilitate calculations

• Introduce and apply skills in Leadership Driven Management• Heavy emphasis on case studies requires students to

analyze real-world scenarios.

© Dale R. Geiger 2011 9

Remember Valley ForgeRemember Valley Forge

• Refer to the article by Ms. Matiella• Why does the Army need to become more

cost effective?• What is the difference between Cost Benefit

Analysis and a Cost-Managed Organization?• How do fiscal constraints pose an “asymmetric

threat”?• How should we respond?

© Dale R. Geiger 2011 10

Program of Instruction Program of Instruction OverviewOverview

Understanding Cost Applying the ProcessLearning the Process

Cost Benefit Analysis CBA Examples Cost Management After Action Review Cost Management Cases

Cost Control Theory Org Based Control Role Based Control Output Based Control Change Management

Week One Week ThreeWeek Two

© Dale R. Geiger 2011 11

What Do Accountants Do?What Do Accountants Do?

© Dale R. Geiger 2011 12

What Do Accountants Do?What Do Accountants Do?

• Provide INFORMATION that is USEFUL to Decision Makers

• Information must be RELIABLE• Free from Bias• Verifiable

• Information must be RELEVANT• Will make a difference in the decision• Timely – frequency and lag time• Relevance is in the eye of the User

© Dale R. Geiger 2011 13

What Do Accountants Do?What Do Accountants Do?

• Provide INFORMATION that is USEFUL to Decision Makers

• Information must be RELIABLE• Free from Bias• Verifiable

• Information must be RELEVANT• Will make a difference in the decision• Timely – frequency and lag time• Relevance is in the eye of the User

© Dale R. Geiger 2011 14

What Do Accountants Do?What Do Accountants Do?

• Provide INFORMATION that is USEFUL to Decision Makers

• Information must be RELIABLE• Free from Bias• Verifiable

• Information must be RELEVANT• Will make a difference in the decision• Timely – frequency and lag time• Relevance is in the eye of the User

© Dale R. Geiger 2011 15

What Do Accountants Do?What Do Accountants Do?

• Provide INFORMATION that is USEFUL to Decision Makers

• Information must be RELIABLE• Free from Bias• Verifiable

• Information must be RELEVANT• Will make a difference in the decision• Timely – frequency and lag time• Relevance is in the eye of the User

© Dale R. Geiger 2011 16

What Do Accountants Do?What Do Accountants Do?

• Provide INFORMATION that is USEFUL to Decision Makers

• Information must be RELIABLE• Free from Bias• Verifiable

• Information must be RELEVANT• Will make a difference in the decision• Timely – frequency and lag time• Relevance is in the eye of the User

© Dale R. Geiger 2011 17

What Do Accountants Do?What Do Accountants Do?

• Provide INFORMATION that is USEFUL to Decision Makers

• Information must be RELIABLE• Free from Bias• Verifiable

• Information must be RELEVANT• Will make a difference in the decision• Timely – frequency and lag time• Relevance is in the eye of the User

© Dale R. Geiger 2011 18

Who are the Users?Who are the Users?

• Users may be INTERNAL or EXTERNAL• Internal users are:

• Managers and Leaders • What types of Decisions might they make?• What information might they need?

• External users are:• Investors, Creditors, Regulators and Legislators• What types of Decisions might they make?• What information might they need?

© Dale R. Geiger 2011 19

Who are the Users?Who are the Users?

• Users may be INTERNAL or EXTERNAL• Internal users are:

• Managers and Leaders • What types of Decisions might they make?• What information might they need?

• External users are:• Investors, Creditors, Regulators and Legislators• What types of Decisions might they make?• What information might they need?

© Dale R. Geiger 2011 20

Who are the Users?Who are the Users?

• Users may be INTERNAL or EXTERNAL• Internal users are:

• Managers and Leaders • What types of Decisions might they make?• What information might they need?

• External users are:• Investors, Creditors, Regulators and Legislators• What types of Decisions might they make?• What information might they need?

© Dale R. Geiger 2011 21

Who are the Users?Who are the Users?

• Users may be INTERNAL or EXTERNAL• Internal users are:

• Managers and Leaders • What types of Decisions might they make?• What information might they need?

• External users are:• Investors, Creditors, Regulators, Legislators and

Citizens • What types of Decisions might they make?• What information might they need?

© Dale R. Geiger 2011 22

External User NeedsExternal User Needs

• Examining an organization’s performance over time demands CONSISTENCY• Assures users that the information is prepared in

the same manner over multiple time periods• Deciding whether to fund competing

organizations or programs demands COMPARABILITY• Assures that the information from all organizations

is prepared according to the same set of principles

© Dale R. Geiger 2011 23

External User NeedsExternal User Needs

• Examining an organization’s performance over time demands CONSISTENCY• Assures users that the information is prepared in

the same manner over multiple time periods• Deciding whether to fund competing

organizations or programs demands COMPARABILITY• Assures that the information from all organizations

is prepared according to the same set of principles

© Dale R. Geiger 2011 24

External User NeedsExternal User Needs

• Examining an organization’s performance over time demands CONSISTENCY• Assures users that the information is prepared in

the same manner over multiple time periods• Deciding whether to fund competing

organizations or programs demands COMPARABILITY• Assures that the information from all organizations

is prepared according to the same set of principles

© Dale R. Geiger 2011 25

External User NeedsExternal User Needs

• Examining an organization’s performance over time demands CONSISTENCY• Assures users that the information is prepared in

the same manner over multiple time periods• Deciding whether to fund competing

organizations or programs demands COMPARABILITY• Assures that the information from all organizations

is prepared according to the same set of principles

© Dale R. Geiger 2011 26

External User NeedsExternal User Needs

• Examining an organization’s performance over time demands CONSISTENCY• Assures users that the information is prepared in

the same manner over multiple time periods• Deciding whether to fund competing

organizations or programs demands COMPARABILITY• Assures that the information from all organizations

is prepared according to the same set of principles

© Dale R. Geiger 2011 27

Consistent Combat Ship

16" guns

cruise missiles

landing gatesperiscope

ballistic missiles

flight deck

submersible hull

helicopter pad

torpedotubes

© Dale R. Geiger 2011 28

Learning CheckLearning Check

• Which characteristic requires timely information?

• Which characteristic requires verifiable information?

• Why would users demand consistency?

© Dale R. Geiger 2011 29

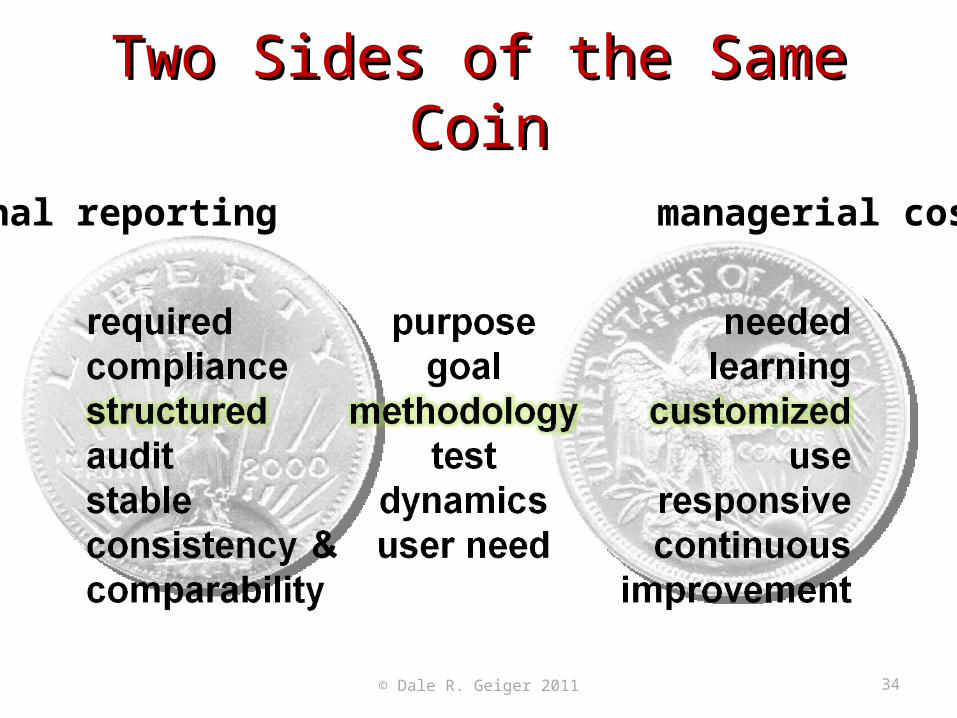

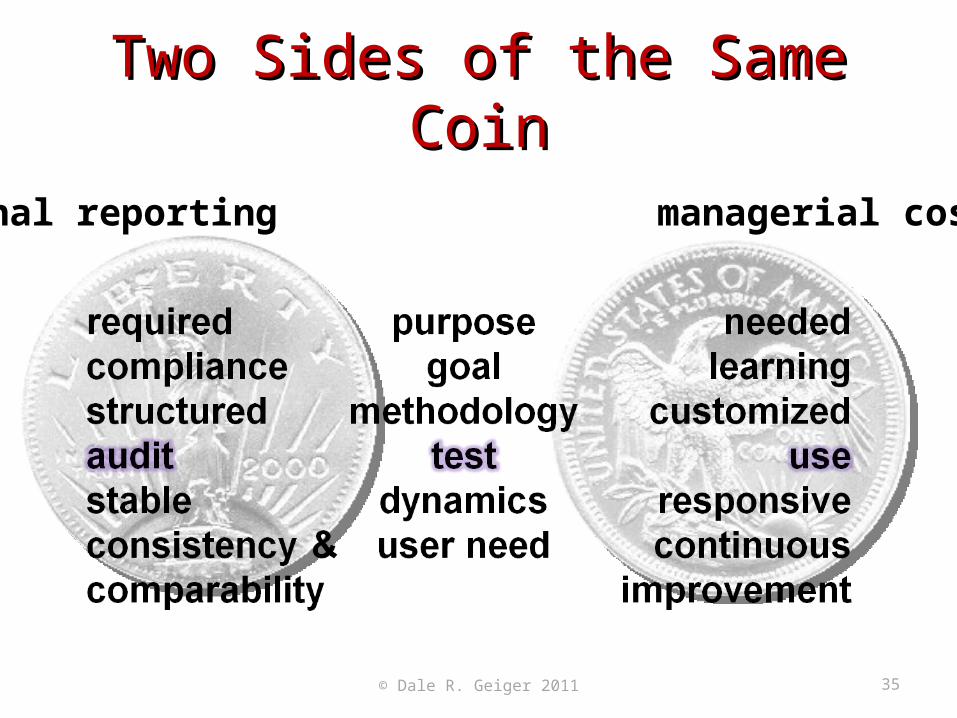

Two Sides of the Same CoinTwo Sides of the Same Coin

requiredcompliancestructuredauditstableconsistency &comparability

purposegoal

methodologytest

dynamicsuser need

neededlearning

customizeduse

responsivecontinuous

improvement

external reporting managerial costing

© Dale R. Geiger 2011 30

Two Sides of the Same CoinTwo Sides of the Same Coin

external reporting managerial costing

© Dale R. Geiger 2011 31

Two Sides of the Same CoinTwo Sides of the Same Coin

external reporting managerial costing

© Dale R. Geiger 2011 32

Two Sides of the Same CoinTwo Sides of the Same Coin

external reporting managerial costing

© Dale R. Geiger 2011 33

Two Sides of the Same CoinTwo Sides of the Same Coin

external reporting managerial costing

© Dale R. Geiger 2011 34

Two Sides of the Same CoinTwo Sides of the Same Coin

external reporting managerial costing

© Dale R. Geiger 2011 35

Two Sides of the Same CoinTwo Sides of the Same Coin

external reporting managerial costing

© Dale R. Geiger 2011 36

ExampleExample

External Report: Tax Return • Why?• How?• Test of success?• Dynamics?

Internal Report: Checkbook• Why?• How?• Test of success?• Dynamics?

© Dale R. Geiger 2011 37

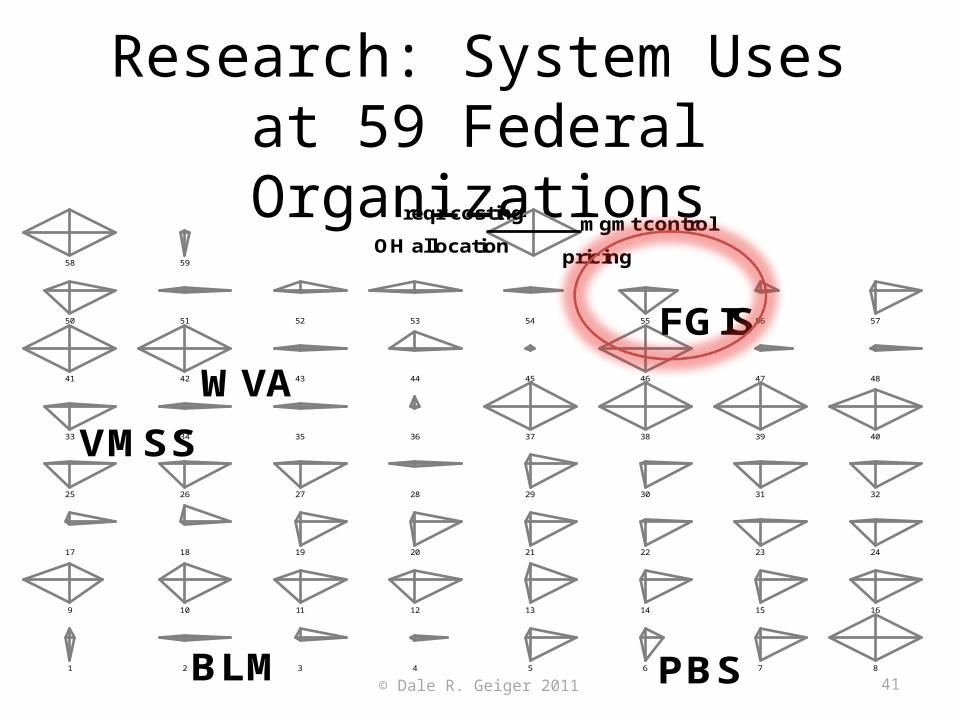

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

© Dale R. Geiger 2011 38

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

© Dale R. Geiger 2011 39

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

© Dale R. Geiger 2011 40

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

© Dale R. Geiger 2011 41

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

© Dale R. Geiger 2011 42

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

© Dale R. Geiger 2011 43

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

© Dale R. Geiger 2011 44

Learning CheckLearning Check

• What are the basic uses for Cost Accounting systems?

• Should all cost systems be the same?• Why or why not?

© Dale R. Geiger 2011 45

What about GFEBS?What about GFEBS?

• General Fund Enterprise Business System• Used Army-wide• Permits real-time posting of financial

transactions• Reports costs according to Budget-relevant

and non-Budget-relevant Cost Objects• Are GFEBS reports internal or external?

© Dale R. Geiger 201146

Unit Cost ReportUnit Cost Report

© Dale R. Geiger 2011 47

Unit Cost ReportUnit Cost Report

This report shows the actual and planned quantities and actual and

planned (average) unit cost for various SKFs (Statistical Key Figures)

such as Headcount.

© Dale R. Geiger 2011 48

Discussion QuestionsDiscussion Questions

• Who would use this report? • How might they use it?• If you were the Senior Leader of this organization,

would you be surprised that your cost per headcount was $78,919.20?

• What would you want to know about that number?

• Would this be an internal or external report for you?

© Dale R. Geiger 2011 49

Learning CheckLearning Check

• What characteristics would identify a report as internal to an organization?

• What characteristics would identify a report as external to an organization?

© Dale R. Geiger 2011 50

ConclusionConclusion

• Needs for internal cost information are as varied as the organizations themselves

• External cost reports:• Facilitate comparison of organizations by external

users• Are unlikely to meet internal management

information needs

© Dale R. Geiger 2011 51