could dynamic variance-covariance settings and jump diffusion techniques enhance the accuracy of...

Post on 19-Dec-2015

217 views

TRANSCRIPT

Could Dynamic Variance-Covariance Settings and Jump Diffusion Techniques Enhance the Accuracy

of Risk Measurement Models? A Reality Test

Li, Ming-Yuan Leon

Motivations

• The importance of VaR (Value at Risk)

• The limitations of VaR

• Stress and scenario testing

• Improve the measurement of VaR

Motivations

• Three methods that are in common use to calculate VaR– (1) Parametric VaR– (2) Historical Simulation– (3) Monte Carlo Simulation

• Relative strengths and weakness

• VaR contribution (VaRC)

Motivations

• Limitations of the parametric VaR– Stable variances and correlations– Poor description of extreme tail events

• Solutions– Time-varying variances and covariance – A jump diffusion system– EVT (extreme value theory)

Literature review

• Billio and Pelizzon (2000) & Li, et al. (2004)

• Regime switching models to estimate VaR

• Limitations of them:– Li (2004): univariate system– Billio and Pelizzon (2000) : a simple setting on

variances

Literature review

• Unlike them– Bivariate system– Not only state-varying technique but also tim

e-varying process on the variances– Meaningful volatility-correlation relationship– Stable periods versus crisis periods

Model Specifications

• The linear model with constant variance and covariance

txxtx euR ,,

tyyty euR ,,

),0(~|| 1,

,1 HBN

e

ee t

ty

txtt

Model Specifications

2

2

yyx

yxxH

Model Specifications

tytxtp RRR ,,,

pyx uuVaR 32.2)(

yxyxp 222

Model Specifications

• The MVGARCH model with time-varying variance and covariance

2

,2,

2,

2,

tytxy

txytxtH

Model Specifications

s

nntxntxmtx

r

mmtxxtx e

1

2,,

2,

1,0,

2, )(

s

nntyntymty

r

mmtyyty e

1

2,,

2,

1,0,

2, )(

tytxtxy ,,2,

Model Specifications

tytxtytxyx

tpyxt

uu

uuVaR

,,2,

2,

,

232.2)(

32.2)(

Model Specifications

• The DCC proposed by Engle (2002):

1,1,1,1,2110 / tytxtytxtt eeqq

]1)/[(exp()exp( ttt qq

tytxttxy ,,2,

Model Specifications

• The jump diffusion model with regime-switching variance and covariance

x

s

mtxr

mmtxxx

s

tx

xmt

xt

g

e

g

2,

1,0,

2, )(

y

s

mtyr

mmtyyy

s

ty

ymt

yt

g

e

g

2,

1,0,

2, )(

1 X ARCH (r)

g2 X ARCH (r)

Model Specifications

tytxsstxy yt

xt

,,,

2,

xxt

xt

xxt

xt pssppssp 221111 )2|2(,)1|1(

yyt

yt

yyt

yt pssppssp 221111 )2|2(,)1|1(

Volatility-correlation relationship

Model Specifications

2

1

2

1

2

1

2

1,1)|,,,,,(32.2

)(

xt

xrt

yt

yrts s s s

tptyrt

yt

xrt

xt

yxt

ssssp

uuVaR

tytxsstytxtp yt

xt

,,,

2,

2,, 2

Back-testing of VaR Results

Back-testing of VaR Results

Data

• Daily index returns for the Canada, UK and US equity markets, as compiled by Morgan Stanley Capital International (MSCI)

• The two portfolios addressed by this study are (1) Canada-US and (2) UK-US

• The data cover the period from January 1st, 1990 through May 7th, 2007, and include 4,526 observations

• All the stock prices are stated in dollar terms

Rolling estimation process

• In the VaR back-testing, the final 2,500 daily observations of the sample are omitted from the initial sample

• Ten back testing periods with the 250 daily observations for each period

Rolling estimation process

• At time t, 2,026 (equal to 4,526 minus 2,500) historical data are incorporated into the estimation of the model parameters

• Based on these variance and correlation estimates, the VaR estimates are then constructed

• Two-step procedure in MVSWARCH model

Parameter estimates

Parameter estimates

Parameter estimates

Parameter estimates

Parameter estimates

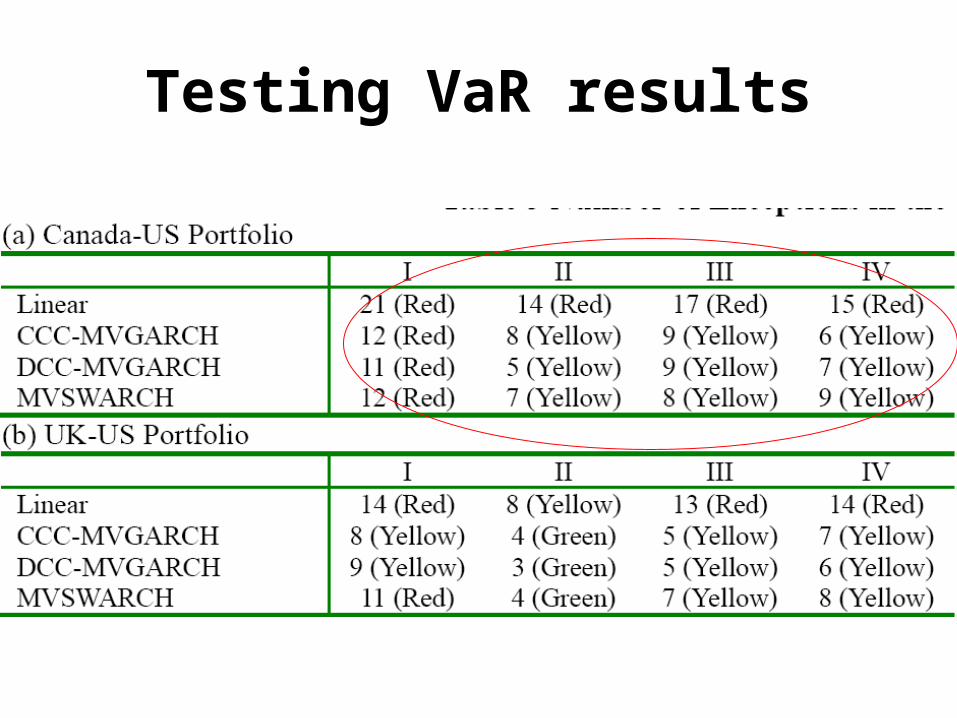

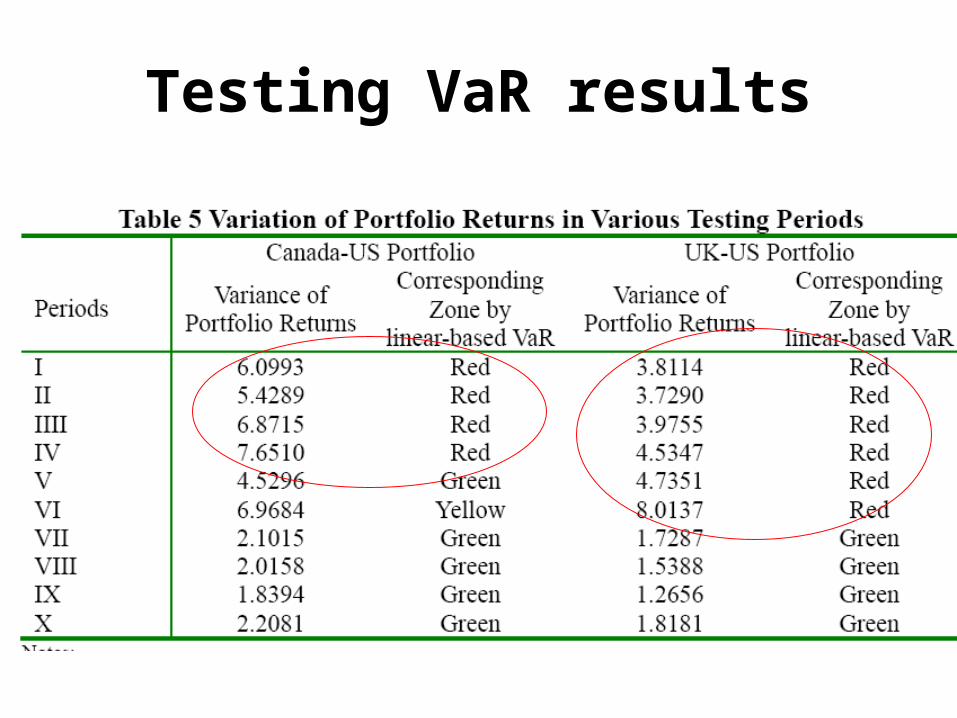

Testing VaR results

Testing VaR results

Testing VaR results

Testing VaR results

Testing VaR results

Conclusions

• During the stable period– The linear-based model and the three advanc

ed VaR models behave similarly

• During the crisis period – The linear-based model yields poorer results – The two MVGARCH and the MVSWARCH mo

dels do enhance the precision of VaR estimates in crisis periods

Three caveats

• In crisis periods, the of exceptions obtained with the three advanced models is still higher than four, the upper bound for the “Green” zone

• The improvement of the accuracy of VaR measurement obtained with the two dynamic correlation settings in comparison with the CCC-MVGARCH is less promising

• A system with more than two dimensions