cost management as a strategic weapon - accountex usa · cost management as a strategic weapon ......

TRANSCRIPT

Cost Management as a Strategic Weapon

Raef Lawson, PhD, CMA, CPA

Vice President-Research & Policy

Institute of Management Accountants

November 17, 2016 1:30 – 2:20 pm

Cost Management as a Strategic Weapon - Agenda

• Accountants as Drivers of Economic Value

• Information for Effective Decision Making • The importance of decision models

• Activity based costing

• Strategic Cost Management • Customer value / profitability

• Process improvement

• The Accountant as a Decision Leader

Accountants as Drivers of Economic Value

Management accounting is the internal business building role of accounting and finance professionals who work inside organizations. These professionals are involved in designing and evaluating business processes, budgeting and forecasting, implementing and monitoring internal controls, and analyzing, synthesizing, and aggregating information – to help drive economic value.

© 2016 IMA

What is Management Accounting?

Economic Value?

An organization’s ability to generate income over time.

Drive? To supply a motive force that powers advancement

towards an objective.

Driving Economic Value

© 2014 D. T. Hicks & Co.

The demands of external reporting, regulatory compliance and financial administration have kept accountants from performing their role in driving economic value.

Obsession with GAAP-based financial and performance measurements has also kept accountants from contributing to their company’s economic value.

Have Accountants Been Driving Economic Value?

Management has depended on the accountant to “keep them out of trouble” and provide traditional reports, but has not looked to him or her to provide new insights that can drive the organization’s economic value.

Not really.

© 2014 D. T. Hicks & Co.

Information for Effective Decision Making

The Importance Of Decision Models

• Most phenomena are too complex to be completely understood.

• To function effectively we create “models” of those phenomena.

• These models represent our “internal version” of the outside world that makes the world more understandable and easier to deal with.

• Good decisions require good models.

© 2012 D. T. Hicks & Co.

Variety Corporation Cost Objectives

Selling, General & Administrative

Costs

Operating Costs –

Direct Labor

Operating Costs –

Overhead

Direct Material, Services and Components

Direct Material, Services and Components

Operating Costs –

Direct Labor

Operating Costs –

Overhead

Selling, General & Administrative

Costs

ABC Corporation Costs

Direct-Labor Based

Overhead Rate

Percentage of Total

Accumulated Cost

ABC Corporation Cost Objectives

Typical Accounting Model

• Determine the cost of a purchased component or service

• Determine the benefit of creating a manufacturing cell to replace three independent operations

• Estimate (or measure) the cost of managing an exhibit while it’s on a multi-show, multi-state tour

• Compare the cost of acquiring business for each market served by the company

Typical Uses for Costing Information

Does the traditional costing model provide a valid understanding and perception of reality?

The General Ledger View is Structurally Deficient for Decision Analysis

Insurance Claims Processing Department

Salaries Equipment Travel expense Supplies Use and occupancy Total

$621,400

161,200

58,000

43,900

30,000

$914,500

$600,000

150,000

60,000

40,000

30,000

$880,000

$(21,400)

(11,200)

2,000

(3,900)

––

$(34,500)

Plan Actual Favorable/

(unfavorable)

Chart-of-Accounts View

When managers get this kind of report, they are either happy or sad, but they are rarely any smarter!

©t 2016 www.garycokins.com

Cost Accounting Information is NOT Decision Cost Information

• Includes only “inventoriable” costs

• Satisfied with entity-wide inventory and COGS measurement

• Populated with GAAP-defined cost data

• Locked into only one or – where alternative rates are possible – two sets of assumptions.

• Permits the direct labor-based assignment of costs even when inappropriate

• Focuses on “fully-absorbed” costs

• Must include all business costs

• Demands accuracy at process, product and customer levels

• Populated with economic cost data appropriate to the situation – ‘different costs for different purposes’

• Must allow for unlimited sets of assumptions

• Requires assignment of cost on a basis consistent with the company’s operating realities

• Must generate both “fully-absorbed” and “incremental” cost information

Cost Accounting Information Decision Cost Information

© 2011 D. T. Hicks & Co.

Changes in Cost Structure over Time

Cost

Components

100%

Overhead (indirect expenses)

Direct Labor

Material

1950 2000

Direct

0%

Broadly averaged cost allocation was acceptable.

Cost errors are large and misleading.

Activity-Based Costing (ABC) is a “lens” for taking the complex operations of a business enterprise and developing a cost model that accurately reflects

the relationships between the company’s costs, activities, and products.

The purpose of Activity-Based Costing is insight, not

calculations.

Activity-Based Costing

© 2004 D. T. Hicks & Co.

• Products and services cause activities and those activities cause costs

© 2004 D. T. Hicks & Co.

• Associate costs with the activities that make them necessary and accumulated activity costs with the products or services that make them necessary

Activity-Based Costing

Single and Multiple-Stage ABC

Expanded ABC

Resources

Resources

Activities

Objects

Objects

Activities

Simple ABC

© 2016 www.garycokins.com

The effectiveness of an activity-based costing model or system is more

dependent on its design than on its method of implementation or the data used to populate the model or system.

“It is better to estimate the right

things than to precisely measure the

wrong things.”

“It is better to be approximately correct

than to be precisely wrong.”

ABC – An Important Underlying Principle

© 2014 D. T. Hicks & Co.

Customer Value / Profitability

Customer Profitability using ABC

$ 30 sales

- 28 expenses

= $ 2 profit

$ 2 profit

Unrealized profit revealed by ABM

Net Revenues

Minus ABM costs =

profit

Value of Company = f(Value from Customers)

The only value a company will ever create is the value that comes from its customers – the current ones

and the new ones acquired in the future.

To remain competitive, one must determine how to keep customers longer, grow them into bigger

customers, make them more profitable, serve them more efficiently, and acquire relatively more

profitable customers.

© 2016 www.garycokins.com

What about Costs Below Product Costs ?

INCOME STATEMENT

Sales $ 100

- Product direct costs -20

- Overhead cost -10

----------------------------------------------

= Gross profit margin $ 70

- selling costs -20

- distribution costs -10

- marketing costs -20

- administrative costs -10

----------------------------------------------

= Total Profit $ 10

The accountants

report these by

each product (but

they are wrong

without ABC).

? We have no visibility

of these costs by

customer (except in

total) !

© 2016 www.garycokins.com

Why Do Customer-related Costs Matter? The Perfect Storm

• Customer Retention • It is relatively much more expensive to acquire a

new customer than to retain an existing one. • Sources of Competitive Advantage

• As products and standard service-lines become commodity-like, then the shift is towards service-differentiation.

• CRM’s “One-to-One” Marketing • Technology has become the enabler to (1) identify

customer segments, and (2) tailor marketing offers. • Power Shift

• The Internet is shifting power from sellers to buyers.

Migrating Customers to Higher Profitability

High (Creamy)

Low (Low Fat)

Low High

Cost-to-Serve

Product Mix Margin

Very

Profitable

Very

unprofitable

Types of Customers

© 2016 www.garycokins.com

Customer Sales Volume Versus Profits

Sales Volume (logarithmic scale)

Profitability

$ 0

$ (unprofitable)

$ profitable

Customers tend to cluster. Medium-volume customers can be much more profitable than large-volume customers!

These losers drag down profits

$ small $ large

© 2016 www.garycokins.com

A Shift in the CFO’s Emphasis

• The CFO must now help Sales and Marketing better target customers.

• The spending budget for sales and marketing is critical … but it should be treated as a scarce resource used to generating the highest long-term profits.

• This means answering questions like:

• Which type of customer is attractive to newly acquire, retain, grow, or win back? And which types are not?

• How much should we optimally spend attracting, retaining, growing, or recovering each customer micro-segment?

Optimizing Customer Value

You can destroy shareholder wealth creation by …

… over-spending unneccessarily on loyal customers for what is needed to retain them.

… under-spending on marginally loyal customers and risk their defection to a competitor.

The optimum spending level for differentiated services varies for the various micro-segments of customers.

You need to have accurate costing models/information on which to base these decisions.

Process Improvement

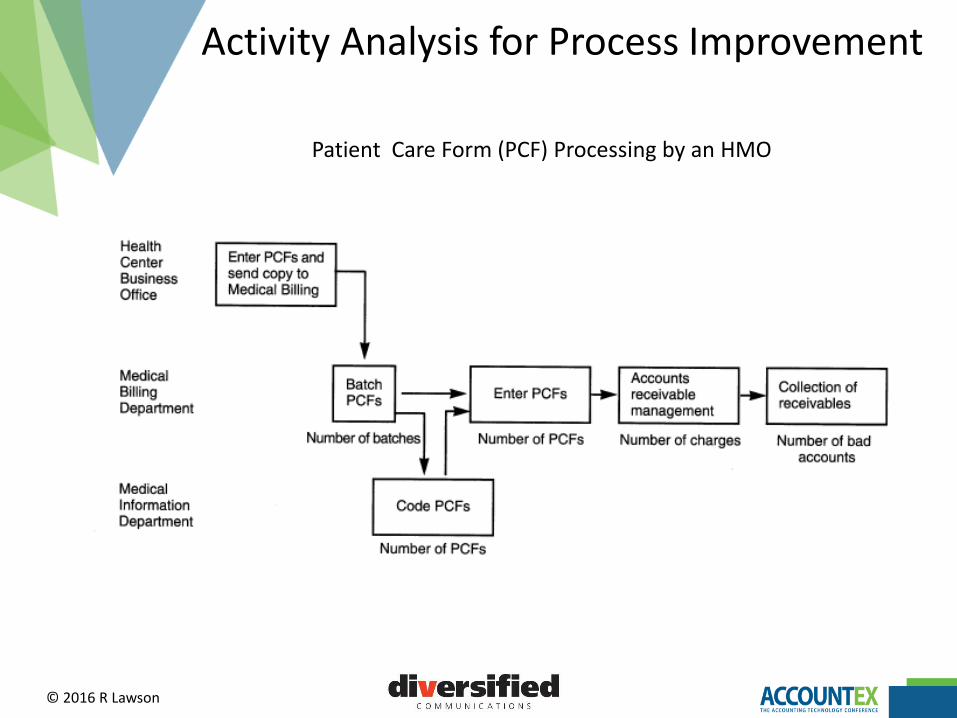

Activity Analysis for Process Improvement

© 2016 R Lawson

Patient Care Form (PCF) Processing by an HMO

Activity Analysis for Process Improvement

Eliminate the activity to

reduce cost

Can activity be

eliminated?

Does activity contain

low-value added tasks?

Is activity required by a customer?

Can the

driver frequency be

reduced?

All cost reduction

opportunities identified

Eliminate low-value added

work to reduce cost

Reduce the activity frequency to reduce cost

Target an activity for improvement

Yes Yes

No No No

No Yes

Yes

Activity analysis judges work based on need, efficiency, and value.

© 2016 www.garycokins.com

There are different costs for different purposes! A management accountant has to think; not just memorize mechanics. Management accounting consists of concepts to be applied, not forms to be filled in…

© 2007 D. T. Hicks & Co.

There is No One “Correct” Cost

The Accountant as a Decision Leader

“Management and leadership are not the same thing. Management copes with complexity, relying on budgets, plans, targets, and organizational charts. Managers tend to follow rules and are risk adverse. In contrast, leaders cope with change – change that is accelerating. Leadership requires vision, direction-setting, inspiring employees, and intelligent risk management.”

- Gary Cokins

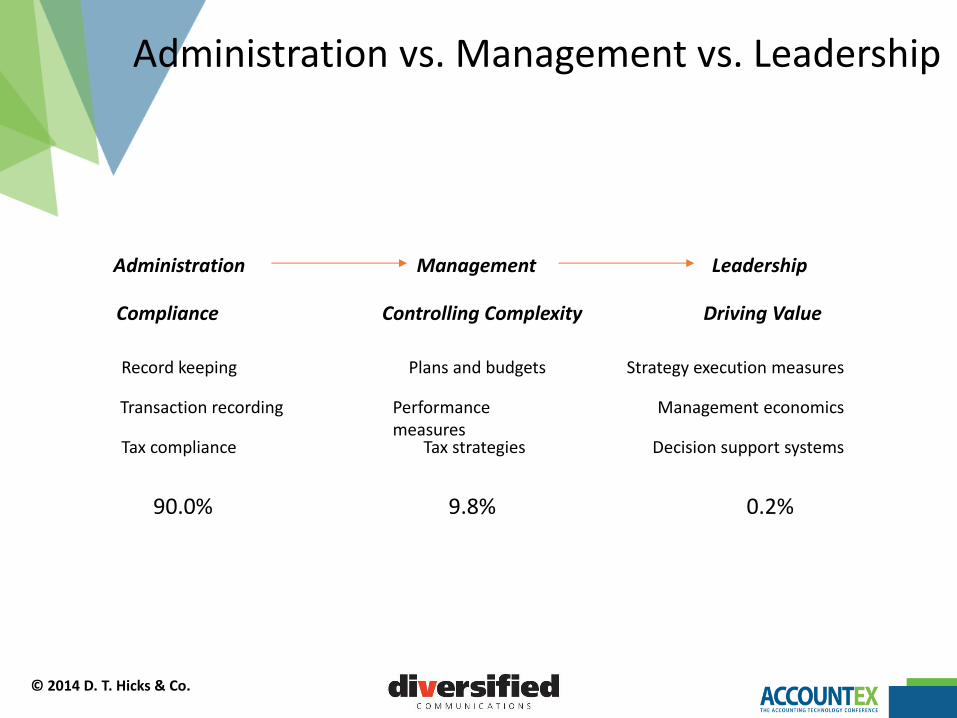

Administration vs. Management vs. Leadership

Administration vs. Management vs. Leadership

Administration Management Leadership

Record keeping

Transaction recording

Tax compliance

Plans and budgets Strategy execution measures

Driving Value Controlling Complexity Compliance

Performance measures

Tax strategies

Management economics

Decision support systems

90.0% 9.8% 0.2%

© 2014 D. T. Hicks & Co.

Making Quality Management Decisions

• Businesspeople tend to blame poor performance on outside conditions that are beyond their personal control; a bad economy, unfair competition, unfavorable economic policies, etc.

• It’s not my fault!

• In reality, poor performance is most often the result of ineffective decisions; inappropriate management responses to outside conditions.

© 2014 D. T. Hicks & Co.

What Makes Decisions Ineffective?

• Cognitive biases – mental errors caused by our simplified information processing strategies.

• Dysfunctional goals, objectives, or incentives – inappropriate measurements for gauging the success of a decision

• Single-point decisions – treating decision making as an event – a discrete choice that takes place at a single point in time.

• Poor costing models

Accountants are in a unique position to serve as decision leaders and add substantial value to their organizations.

Adapted from © 2014 D. T. Hicks & Co.

Decision Maker vs. Decision Leader

• A decision maker has ultimate responsibility for making the decision.

• A decision leader takes the lead in ensuring the quality of the decision-making process.

© 2014 D. T. Hicks & Co.

The Accountant as a Decision Leader

• Information generated by accountants is part of almost every business decision

• Accountants are the closest thing most companies have to an “economist”

• Accountants are already active in systems development and act in an “oversight” capacity

• Accountants have “wall-to-wall” responsibilities within the organization

• Accountants are present when most major decisions are being discussed by or presented to decision makers

© 2014 D. T. Hicks & Co.

How Does an Accountant Become a Good Decision Leader?

• Be on the alert for cognitive biases that corrupt the decision making process and take steps to eliminate them.

• Insure that the economic measures used to support decisions are comprehensive, accurate, relevant, and based on a valid economic model of the business.

• Work to develop effective decision-making systems that provide a structure within which key management decisions are made.

© 2014 D. T. Hicks & Co.

Thank you! - Questions?