cost benefit analysis in a government context - fmi*igf benefit analysis in a government... · cost...

TRANSCRIPT

Cost Benefit Analysis in a Government ContextFMI PD Week: November 25th,2014

Elias Hage, CPA, CA, CISA, Advisory Services, Ernst & Young (EY)Henri Besnier, M.Sc. CPA, CMA, Advisory Services, Ernst & Young (EY)

Page 2

Agenda

► What is a cost benefit analysis

► When and how to use a cost benefit analysis in Government

► Cost benefit analysis examples

► Challenges and success factors

► Questions

Page 3

What is a cost benefit analysis

Page 4

What is a cost benefit analysis (CBA)?

The purpose of a CBA is to perform an analysis where expected costs and benefits resulting from an opportunity are analyzed for selected scenarios (including status quo).

► The CBA helps to understand and compare the initial and on-going expenditures to the expected financial and non-financial benefits.

► Generally, the first step of a CBA involves an investigation and assessment of the opportunity.

► In examining the preferred option, it is also important to consider alternatives, including the base case (or ‘do nothing’ alternative) for comparative purposes.

Page 5

Components of a CBA

A CBA should contain for a given time period:

► Expected costs► Expected benefits

Page 6

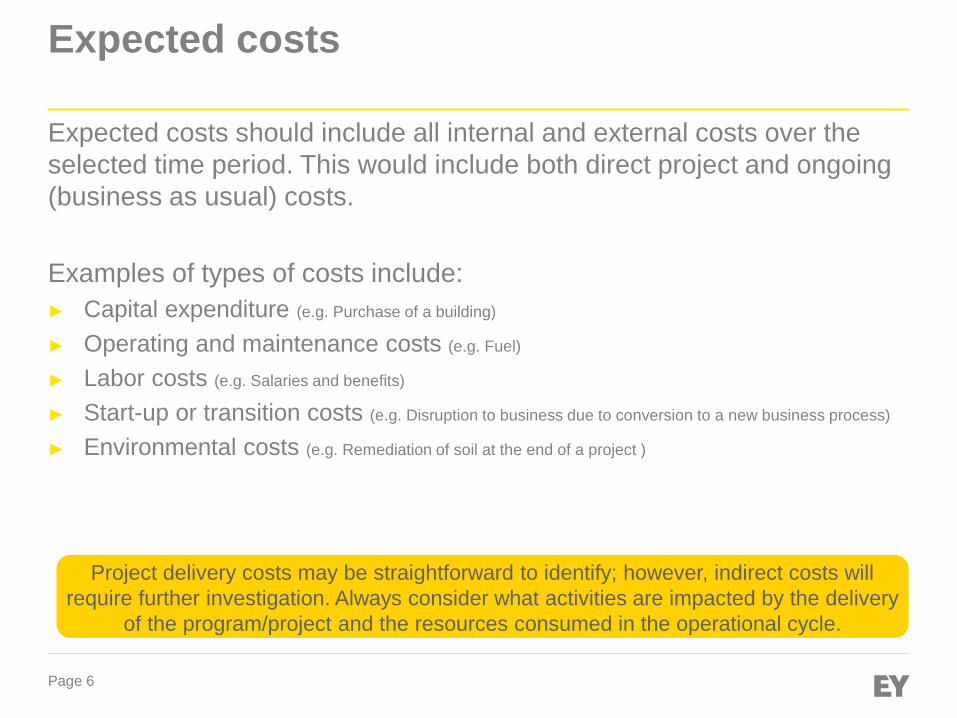

Expected costs

Expected costs should include all internal and external costs over the selected time period. This would include both direct project and ongoing (business as usual) costs.

Examples of types of costs include:► Capital expenditure (e.g. Purchase of a building)

► Operating and maintenance costs (e.g. Fuel)

► Labor costs (e.g. Salaries and benefits)

► Start-up or transition costs (e.g. Disruption to business due to conversion to a new business process)

► Environmental costs (e.g. Remediation of soil at the end of a project )

Project delivery costs may be straightforward to identify; however, indirect costs will require further investigation. Always consider what activities are impacted by the delivery

of the program/project and the resources consumed in the operational cycle.

Page 7

Expected benefits

Expected benefits should be measurable and can be classified as:► Financial► Non-financial – quantitative (e.g. output, efficiency)► Non-financial – qualitative (e.g. customer satisfaction, compliance)

Examples of types of benefits include:► Revenues (e.g. Incremental sales)

► Cost saving (e.g. Reduction of wastes,)

► Productivity improvement (e.g. Process more requests)

► Access to better information (e.g. Citizens can see their electric consumption over internet)

Page 8

Varying complexity of CBA

CBAs can significantly vary in level of complexity. There are several factors which can impact the time and effort required to produce a functional CBA, such as:► Identifying all relevant expected costs or benefits► Availability of data and information to measure expected costs or benefits► Constructing fair alternatives

Com

plex

ity: B

enef

its

Complexity: Costs

High

HighLow

LowLegend

Project / program

C

D

B

F

G

HE

A

Non-complex

Complex

Cost/benefit complexity matrix

It is important to clearly state any assumptions made in determining costs or quantifying and delivering benefits.

Consider the complexity of project E versus project H:► An example of Project E may be the implementation of an

automated envelope stuffer – a low complexity measure of costs and benefits► Expected costs: Cost of purchasing, implementing and maintaining the

hardware► Expected benefits: Avoided cost of staff required to manually stuff the

envelopes

► An example of Project G, on the other hand, may be the replacement of a governmental program – high complexity measure of both costs and benefits► Expected costs: Direct costs may be simple to measure (the cost of

transition); however, indirect costs such as the impact on other programs can be difficult to measure.

► Expected benefits: Security and safety of citizens, but how would this benefit be measured? What factors would be used? What assumptions would be made?

Page 9

When and how to use a cost benefit analysis in Government

Page 10

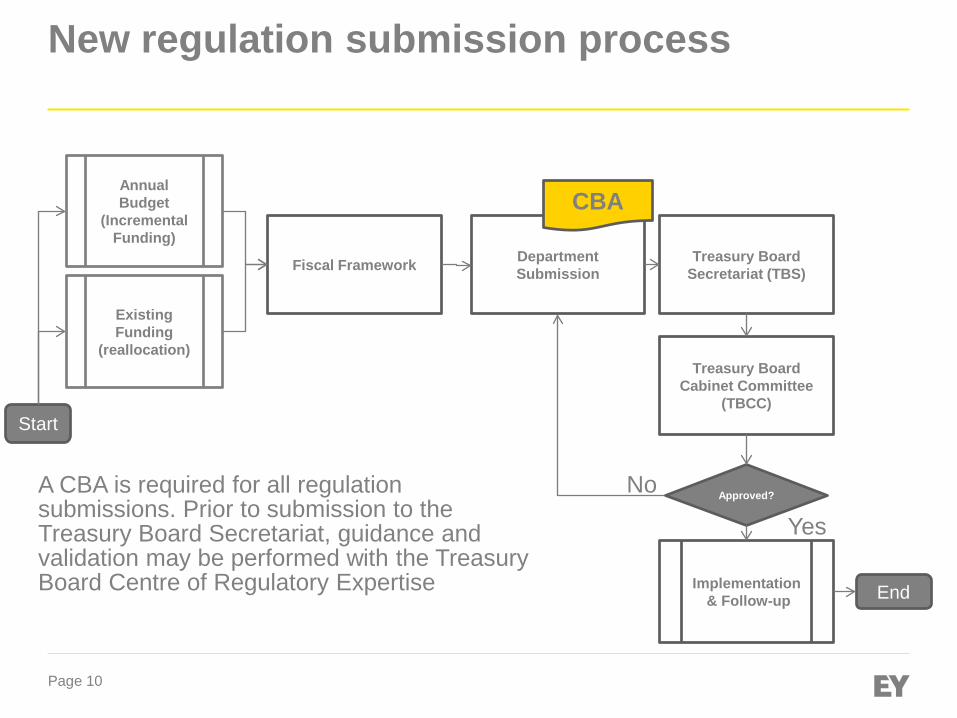

DepartmentSubmissionFiscal Framework Treasury Board

Secretariat (TBS)

Treasury Board Cabinet Committee

(TBCC)Start

Annual Budget

(Incremental Funding)

Implementation& Follow-up

Approved?

Yes

No

End

Existing Funding

(reallocation)

New regulation submission process

CBA

A CBA is required for all regulation submissions. Prior to submission to the Treasury Board Secretariat, guidance and validation may be performed with the Treasury Board Centre of Regulatory Expertise

Page 11

Business cases for programs / projects

CBAs are used as part of business cases at the Federal, Provincial and Municipal level, and may not always require review or approval by the Treasury Board Secretariat.

The purpose of a CBA as part of the Government of Canada business case process includes:► Linking investments with program results and strategic outcomes► Effectively communicating the costs and benefits of implementing a

project or program, including relevant assumptions used for measurement

Page 12

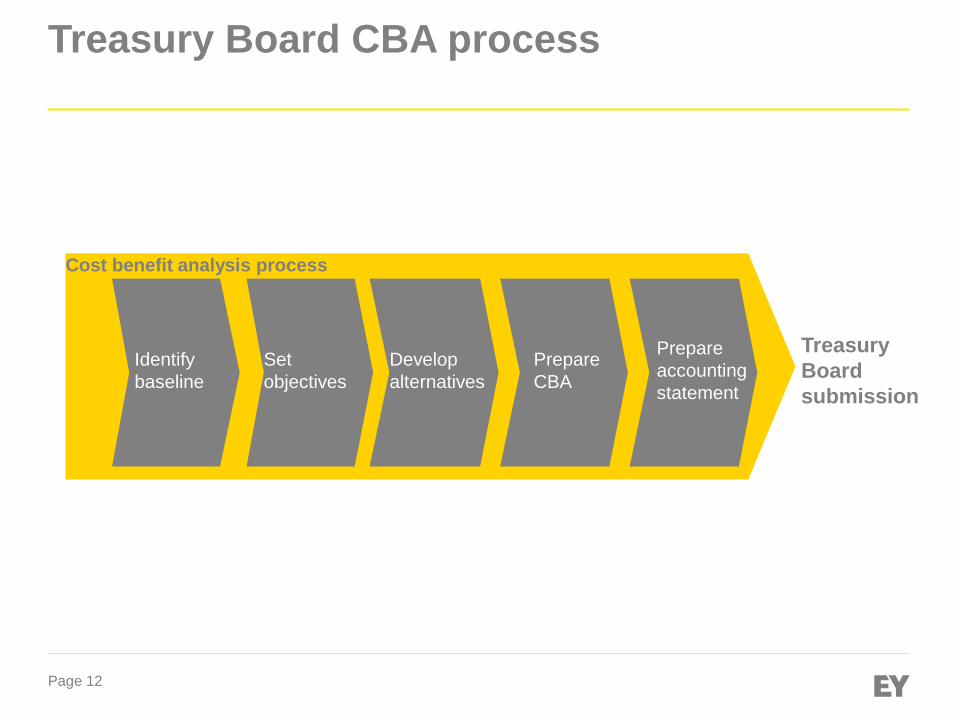

Treasury Board CBA process

Identify baseline

Set objectives

Develop alternatives

Cost benefit analysis process

Prepare CBA

Prepare accounting statement

Treasury Board submission

Page 13

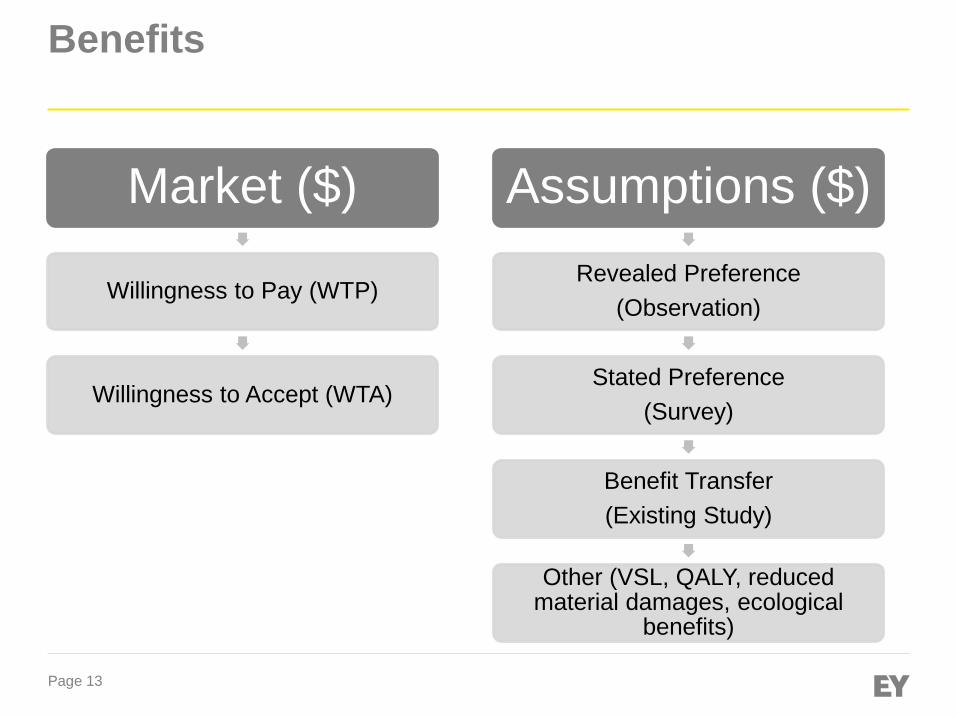

Benefits

Market ($)

Willingness to Pay (WTP)

Willingness to Accept (WTA)

Assumptions ($)Revealed Preference

(Observation)

Stated Preference(Survey)

Benefit Transfer(Existing Study)

Other (VSL, QALY, reduced material damages, ecological

benefits)

Page 14

Costs

Private sector(Opportunity costs)

Compliance costs(capital, operating, maintenance,

admin, cost of substitutes)

Transitional Costs

Government

Administrative (Capital, Operating Costs)

Monitoring

Enforcing

Page 15

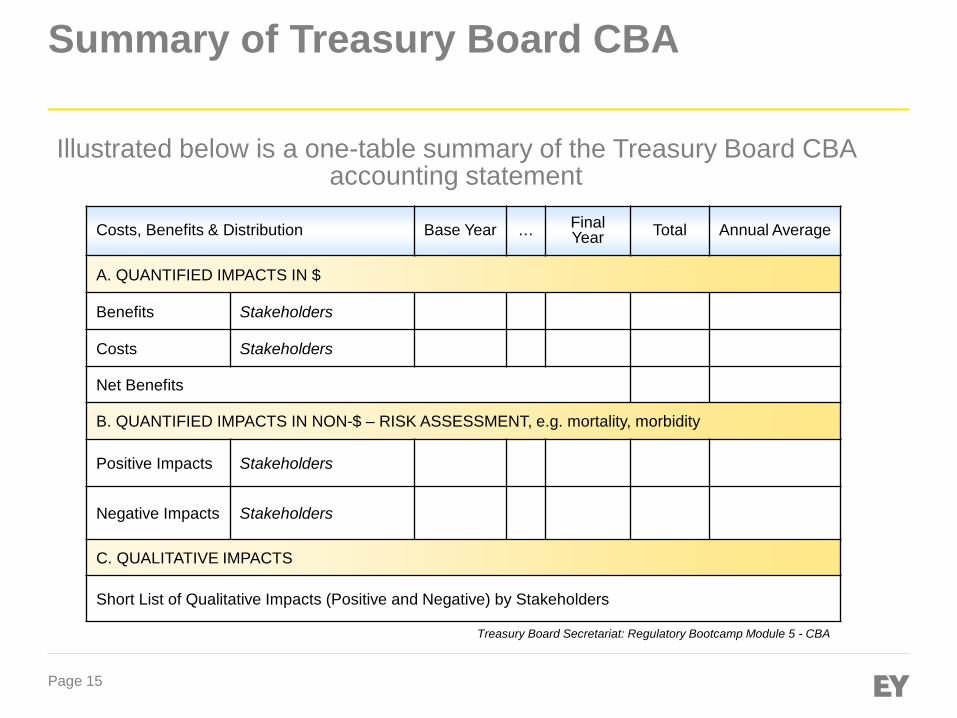

Summary of Treasury Board CBA

Costs, Benefits & Distribution Base Year … Final Year Total Annual Average

A. QUANTIFIED IMPACTS IN $

Benefits Stakeholders

Costs Stakeholders

Net Benefits

B. QUANTIFIED IMPACTS IN NON-$ – RISK ASSESSMENT, e.g. mortality, morbidity

Positive Impacts Stakeholders

Negative Impacts Stakeholders

C. QUALITATIVE IMPACTS

Short List of Qualitative Impacts (Positive and Negative) by Stakeholders

Treasury Board Secretariat: Regulatory Bootcamp Module 5 - CBA

Illustrated below is a one-table summary of the Treasury Board CBA accounting statement

Page 16

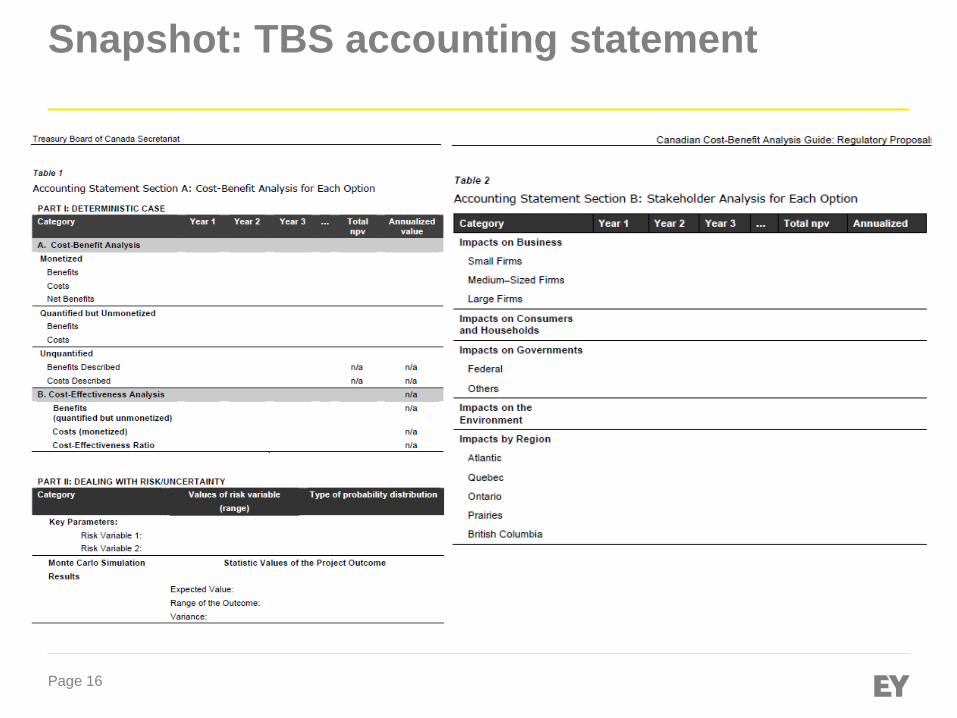

Snapshot: TBS accounting statement

Page 17

CBA examples

Page 18

Example: Regulations amending the Food and Drug Regulations

These Regulations will provide a net benefit to Canadians, with a net present value (NPV) of about $33.4 million over 10 years. The quantified benefits relate primarily to cost savings to industry due to removal of poor-quality drug products at the active ingredient (AI) stage instead of recalls at the dosage-form stage. The qualitative benefits relate primarily to better protection for Canadians from poor-quality drug products.

►Option 1: Status Quo►No financial impact►Continued health risks to Canadians

►Option 2: More active and ongoing promotion of the voluntary implementation of GMP for AI►Non-regulatory option►Unlikely to have a material benefit / impact on the existing health risks

►Option 3: Regulatory amendment►Benefits to consumers, government and industry►Costs to government and industry

Costs

Cost-benefit statement

Source: Food and Drug Regulations Regulations SOR - 2013-74 (26-04-2014)

Page 19

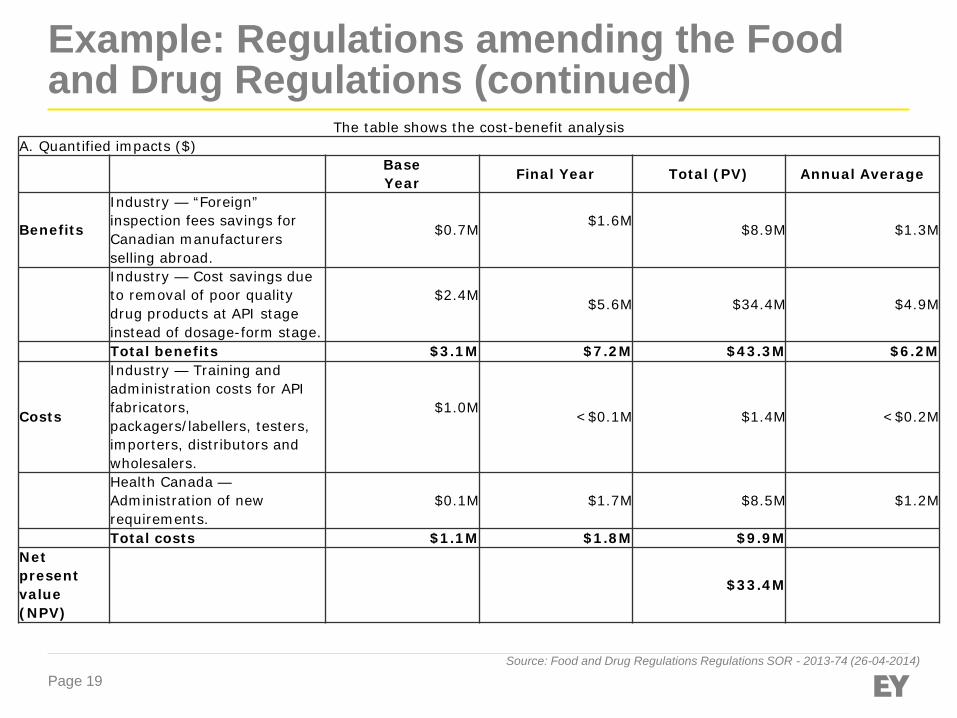

Example: Regulations amending the Food and Drug Regulations (continued)

Source: Food and Drug Regulations Regulations SOR - 2013-74 (26-04-2014)

The table shows the cost-benefit analysisA. Quantified impacts ($)

Base Year Final Year Total (PV) Annual Average

Benefits

Industry — “Foreign” inspection fees savings for Canadian manufacturers selling abroad.

$0.7M $1.6M $8.9M $1.3M

Industry — Cost savings due to removal of poor quality drug products at API stage instead of dosage-form stage.

$2.4M $5.6M $34.4M $4.9M

Total benefits $3.1M $7.2M $43.3M $6.2M

Costs

Industry — Training and administration costs for API fabricators, packagers/labellers, testers, importers, distributors and wholesalers.

$1.0M <$0.1M $1.4M <$0.2M

Health Canada —Administration of new requirements.

$0.1M $1.7M $8.5M $1.2M

Total costs $1.1M $1.8M $9.9MNet present value (NPV)

$33.4M

Page 20

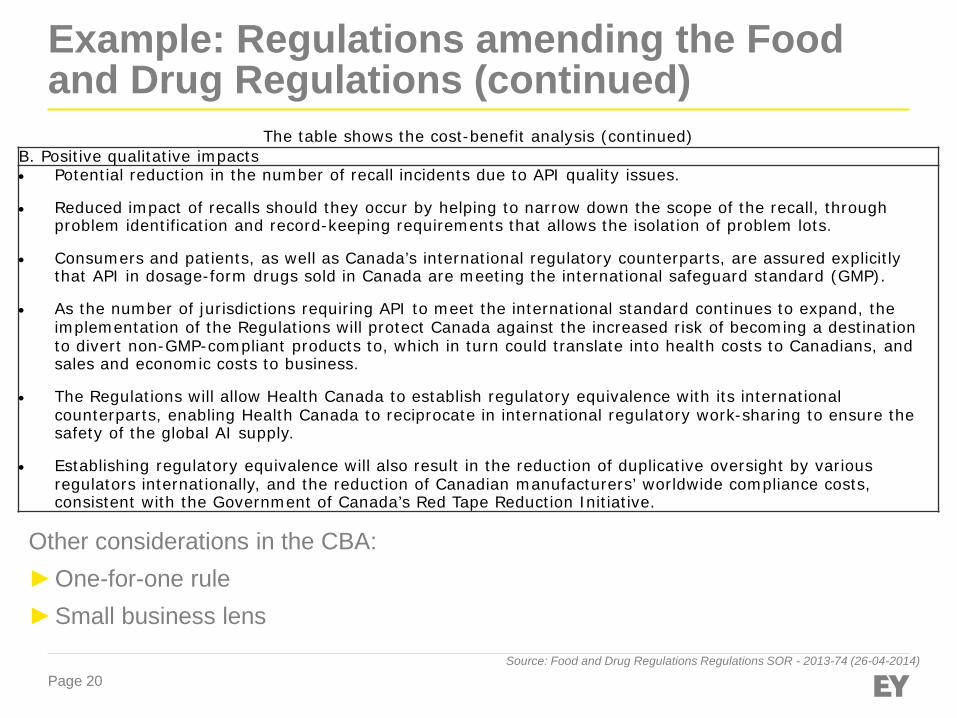

Example: Regulations amending the Food and Drug Regulations (continued)

Source: Food and Drug Regulations Regulations SOR - 2013-74 (26-04-2014)

The table shows the cost-benefit analysis (continued)B. Positive qualitative impacts• Potential reduction in the number of recall incidents due to API quality issues.

• Reduced impact of recalls should they occur by helping to narrow down the scope of the recall, through problem identification and record-keeping requirements that allows the isolation of problem lots.

• Consumers and patients, as well as Canada’s international regulatory counterparts, are assured explicitly that API in dosage-form drugs sold in Canada are meeting the international safeguard standard (GMP).

• As the number of jurisdictions requiring API to meet the international standard continues to expand, the implementation of the Regulations will protect Canada against the increased risk of becoming a destination to divert non-GMP-compliant products to, which in turn could translate into health costs to Canadians, and sales and economic costs to business.

• The Regulations will allow Health Canada to establish regulatory equivalence with its international counterparts, enabling Health Canada to reciprocate in international regulatory work-sharing to ensure the safety of the global AI supply.

• Establishing regulatory equivalence will also result in the reduction of duplicative oversight by various regulators internationally, and the reduction of Canadian manufacturers’ worldwide compliance costs, consistent with the Government of Canada’s Red Tape Reduction Initiative.

Other considerations in the CBA:►One-for-one rule►Small business lens

Page 21

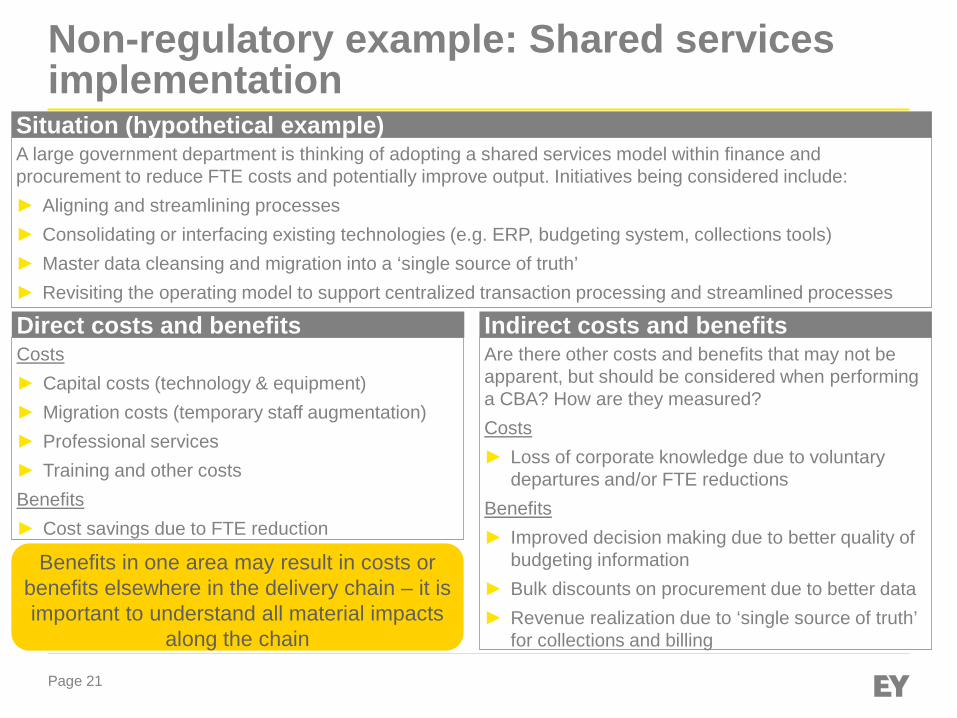

Non-regulatory example: Shared services implementation

A large government department is thinking of adopting a shared services model within finance and procurement to reduce FTE costs and potentially improve output. Initiatives being considered include:► Aligning and streamlining processes► Consolidating or interfacing existing technologies (e.g. ERP, budgeting system, collections tools)► Master data cleansing and migration into a ‘single source of truth’► Revisiting the operating model to support centralized transaction processing and streamlined processes

Situation (hypothetical example)

Costs► Capital costs (technology & equipment)► Migration costs (temporary staff augmentation)► Professional services► Training and other costsBenefits► Cost savings due to FTE reduction

Direct costs and benefitsAre there other costs and benefits that may not be apparent, but should be considered when performing a CBA? How are they measured?Costs► Loss of corporate knowledge due to voluntary

departures and/or FTE reductionsBenefits► Improved decision making due to better quality of

budgeting information► Bulk discounts on procurement due to better data► Revenue realization due to ‘single source of truth’

for collections and billing

Indirect costs and benefits

Benefits in one area may result in costs or benefits elsewhere in the delivery chain – it is important to understand all material impacts

along the chain

Page 22

Challenges and success factors

Page 23

Current CBA challenges in Government

► Choosing the right instrument and design

► Balancing time constraints and accuracy/quality

► Expertise and capacity building within departments

► Lack of standard costs

Page 24

Ten golden rules

1. Start early and continue collecting information throughout the development of the CBA

2. Map out the data collection process before creating models3. The CBA does not have to be “perfect” – 80% science, 20% art4. Identify and define the assumptions being used5. Disclose risks and the cost of managing them6. Compare against a baseline scenario7. Evaluate more than one alternative 8. Objectives should be precise and measurable9. Understand the audience of the CBA10. The CBA should not be impacted by political priorities; it should

provide the most accurate evidence for decision making

Page 25

Resources

► Canadian Cost-Benefit Analysis Guide: Regulatory Proposals► http://www.tbs-sct.gc.ca/rtrap-parfa/analys/analystb-eng.asp

► Business Case Guide► http://www.tbs-sct.gc.ca/emf-cag/business-rentabilisation/bcg-

gar/bcg-gartb-eng.asp

► Center of Regulatory Expertise (TBS)► Regulatory Bootcamp Module 5 – CBA

Page 26

Questions