cost accounting part 2

TRANSCRIPT

CA-CMA Inter

Cost Accounting

Part 2

Dr CMA T K Sridhar

Edition: September, 2021

Price: ₹250 [for volumes I and II]

For users who are benefited, pay to…

Account holder name: Singar Educational and Charitable Trust

Account number: 1262 1150 0000 9481

IFSC code: KVBL0001262

Bank name: Karur Vysya Bank

CALL OR VISIT FOR COPIES

Published by

SINGAR BOOKS AND PUBLICATIONS

Head Office: 32-B, Vivekananda Nagar, Ramalinga Nagar, Woriur, Trichy 620 003, TN

Branch Office: 76/1, New Street, Valluvar Kottam High Road,

Nungambakkam, Chennai – 600 034

Ph: Trichy: 93451 22645 | Chennai: 93453 96855

www.singaracademy.in | [email protected]

CONTENT

Page

Cost Accounting

1 Cost Book Keeping 1

2 Methods of Costing

2.1 Job Costing 12

2.2 Batch Costing 19

2.3 Contract Costing 21

2.4 Process Costing 34

2.5 Joint Products & By Products 57

2.6 Service Costing / Operating Costing 64

3 Cost Accounting Technique

3.1 Marginal Costing 74

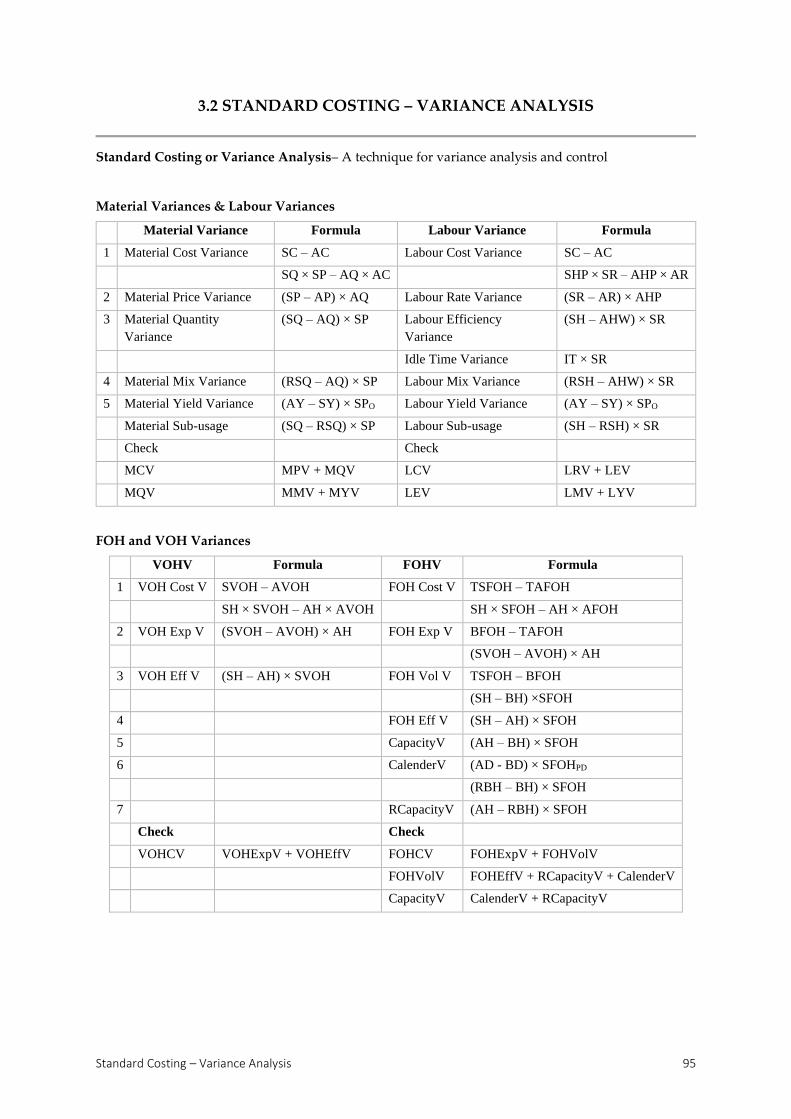

3.2 Standard Costing – Variance Analysis 95

3.3 Budget and Budgetary Control 109

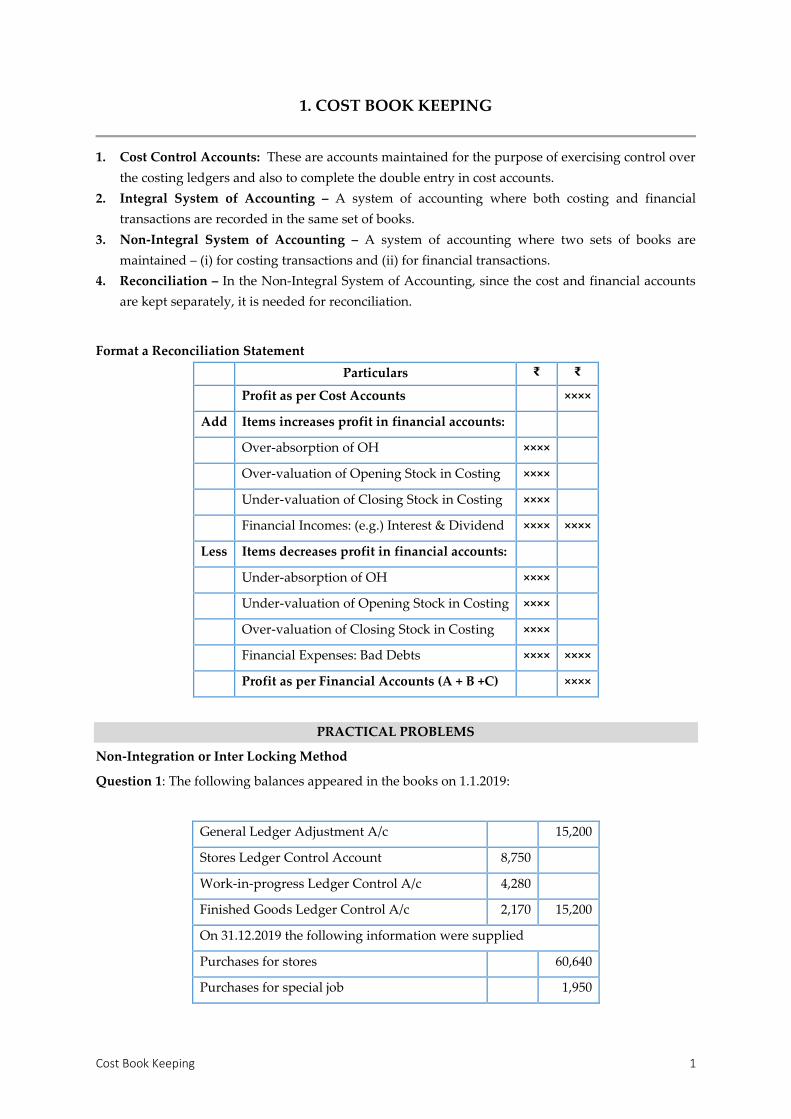

Cost Book Keeping 1

1. COST BOOK KEEPING

1. Cost Control Accounts: These are accounts maintained for the purpose of exercising control over

the costing ledgers and also to complete the double entry in cost accounts.

2. Integral System of Accounting – A system of accounting where both costing and financial

transactions are recorded in the same set of books.

3. Non-Integral System of Accounting – A system of accounting where two sets of books are

maintained – (i) for costing transactions and (ii) for financial transactions.

4. Reconciliation – In the Non-Integral System of Accounting, since the cost and financial accounts

are kept separately, it is needed for reconciliation.

Format a Reconciliation Statement

Particulars ₹ ₹

Profit as per Cost Accounts ××××

Add Items increases profit in financial accounts:

Over-absorption of OH ××××

Over-valuation of Opening Stock in Costing ××××

Under-valuation of Closing Stock in Costing ××××

Financial Incomes: (e.g.) Interest & Dividend ×××× ××××

Less Items decreases profit in financial accounts:

Under-absorption of OH ××××

Under-valuation of Opening Stock in Costing ××××

Over-valuation of Closing Stock in Costing ××××

Financial Expenses: Bad Debts ×××× ××××

Profit as per Financial Accounts (A + B +C) ××××

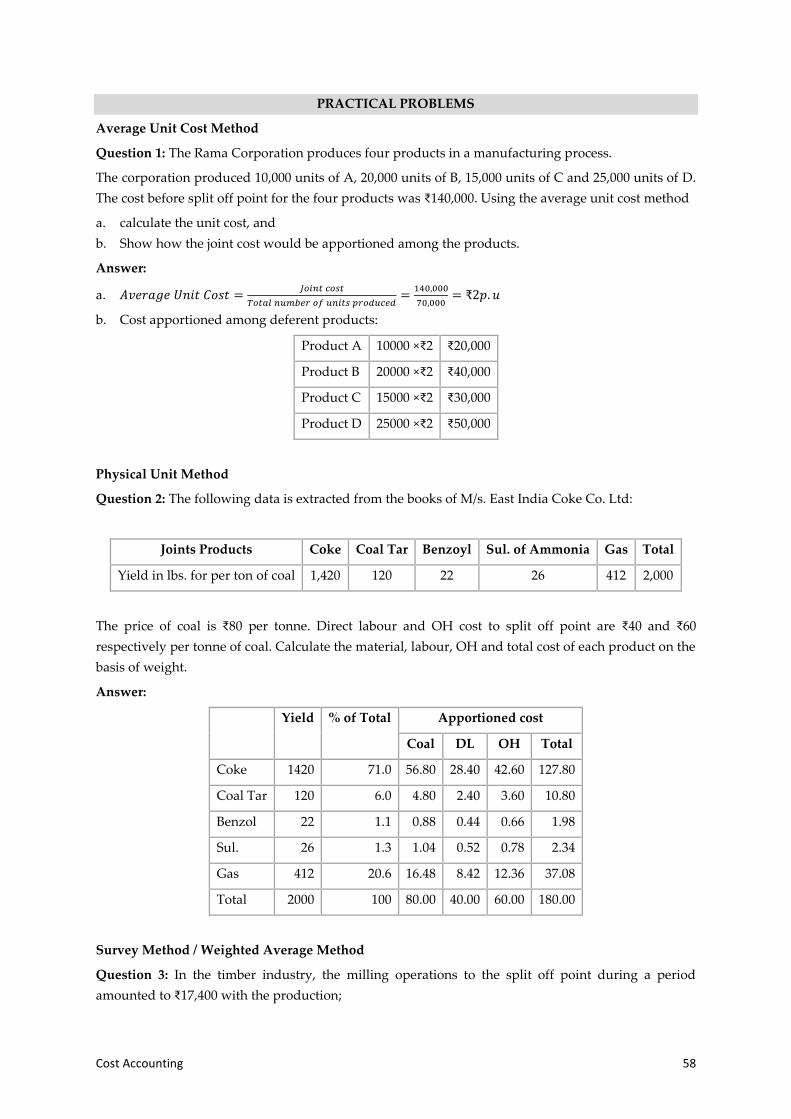

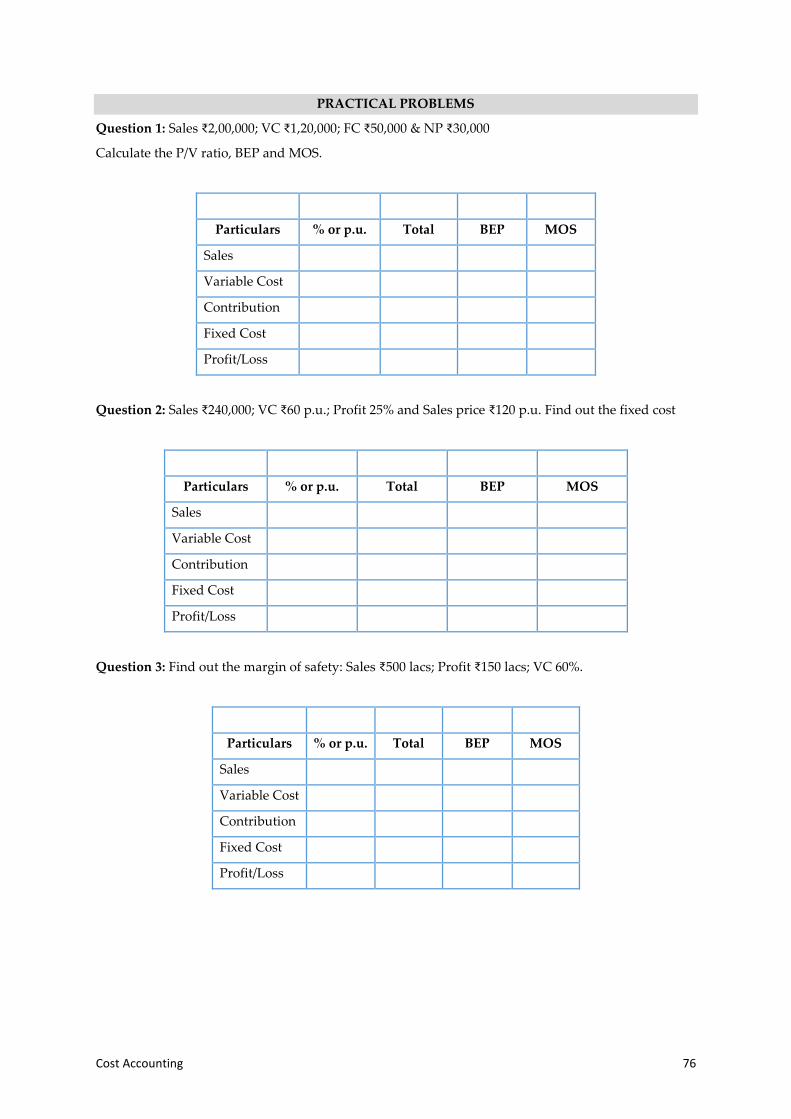

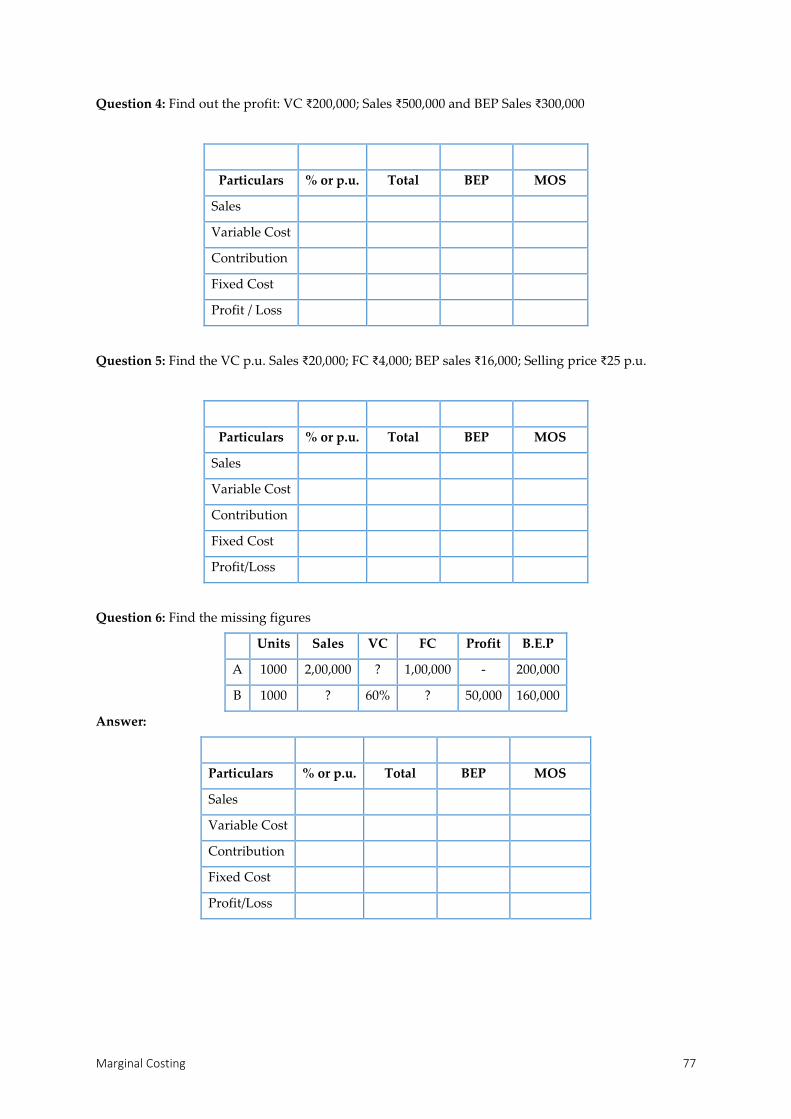

PRACTICAL PROBLEMS

Non-Integration or Inter Locking Method

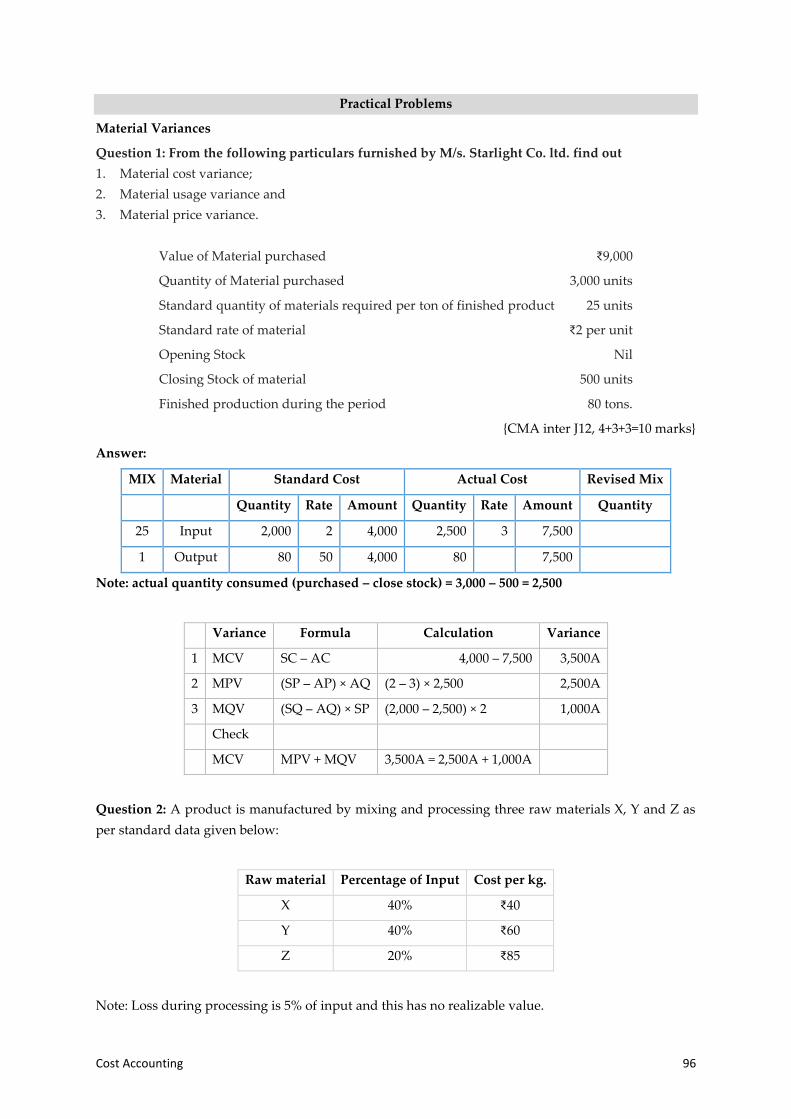

Question 1: The following balances appeared in the books on 1.1.2019:

General Ledger Adjustment A/c 15,200

Stores Ledger Control Account 8,750

Work-in-progress Ledger Control A/c 4,280

Finished Goods Ledger Control A/c 2,170 15,200

On 31.12.2019 the following information were supplied

Purchases for stores 60,640

Purchases for special job 1,950

Cost Accounting 2

Direct wages 38,627

Indirect factory wages 9,543

Administration salaries 6,731

Selling and distribution salaries 4,252 59,153

Production expenses 10,432

Administrative expenses 9,546

Selling and distribution expenses 6,430

Stores issued to production 56,501

Stores issued to maintenance account 2,586

Returns to supplier 312

Production overhead absorbed by production 23,410

Administrative OH absorbed by finished goods 15,150

Selling overhead recovered on sales 9,515

Production finished during the year 1,18,517

Finished goods sold at cost 1,33,382

Sales 1,55,000

You are required to record the entries in cost ledger for the year 2001 and prepare a TB.

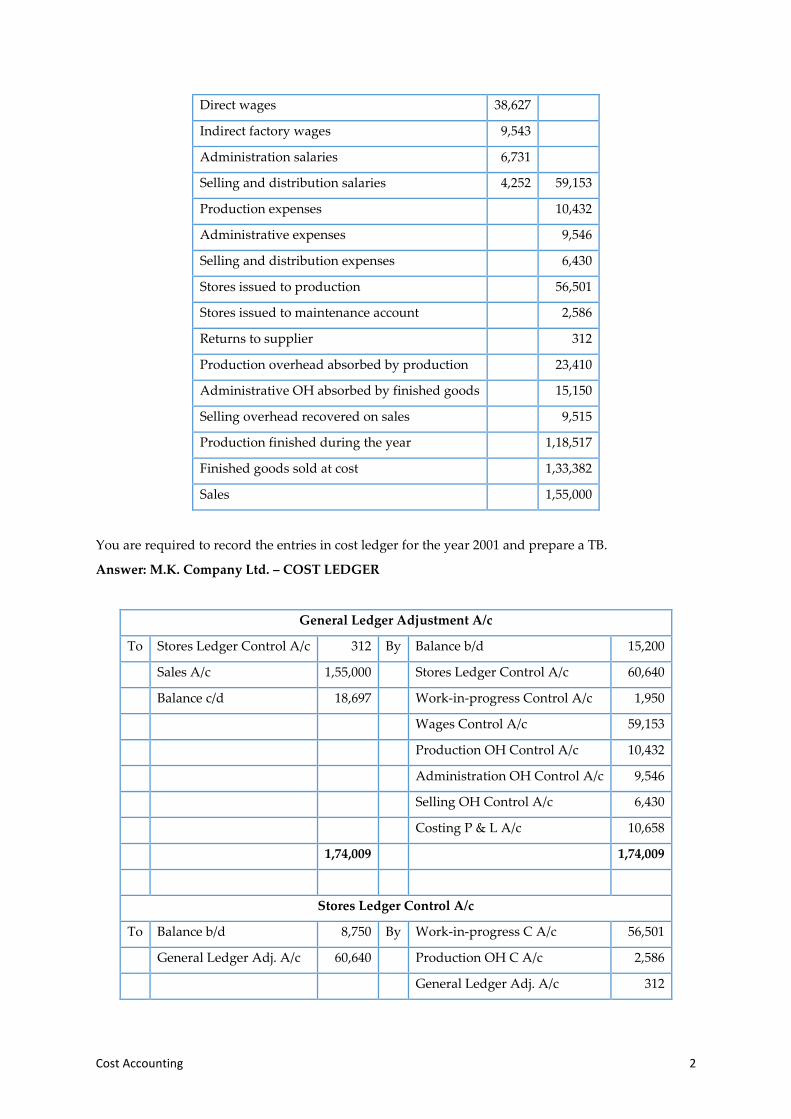

Answer: M.K. Company Ltd. – COST LEDGER

General Ledger Adjustment A/c

To Stores Ledger Control A/c 312 By Balance b/d 15,200

Sales A/c 1,55,000 Stores Ledger Control A/c 60,640

Balance c/d 18,697 Work-in-progress Control A/c 1,950

Wages Control A/c 59,153

Production OH Control A/c 10,432

Administration OH Control A/c 9,546

Selling OH Control A/c 6,430

Costing P & L A/c 10,658

1,74,009 1,74,009

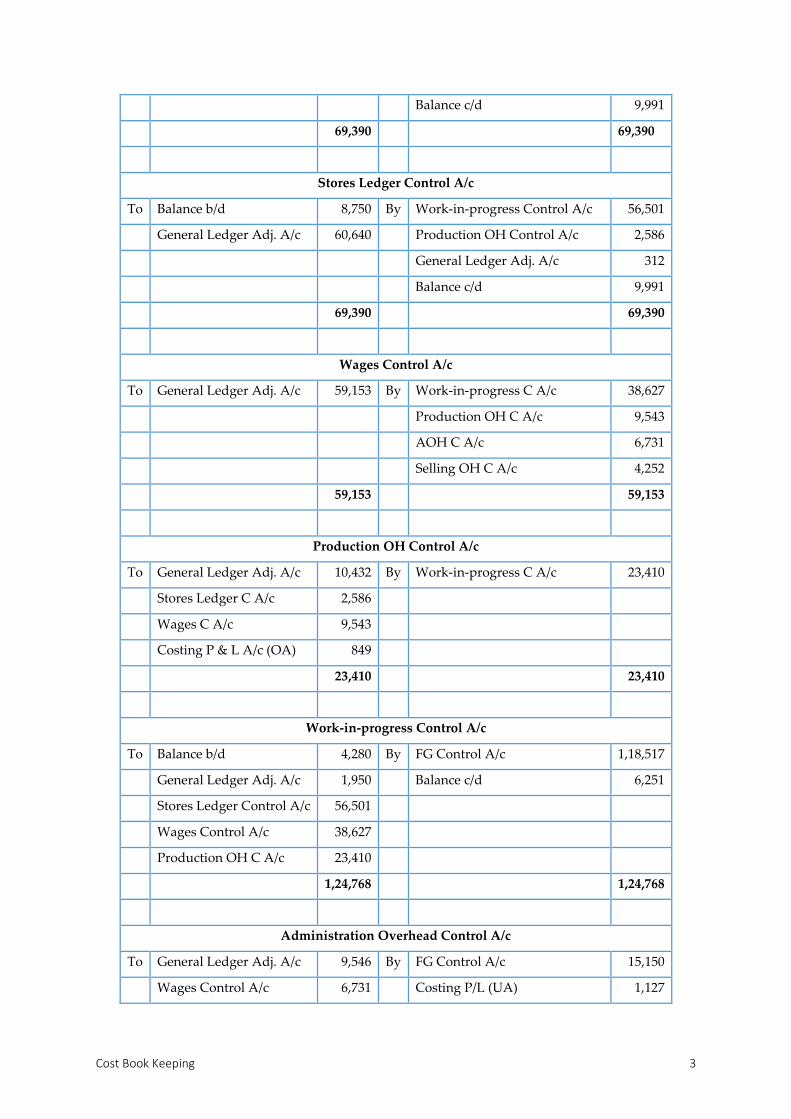

Stores Ledger Control A/c

To Balance b/d 8,750 By Work-in-progress C A/c 56,501

General Ledger Adj. A/c 60,640 Production OH C A/c 2,586

General Ledger Adj. A/c 312

Cost Book Keeping 3

Balance c/d 9,991

69,390 69,390

Stores Ledger Control A/c

To Balance b/d 8,750 By Work-in-progress Control A/c 56,501

General Ledger Adj. A/c 60,640 Production OH Control A/c 2,586

General Ledger Adj. A/c 312

Balance c/d 9,991

69,390 69,390

Wages Control A/c

To General Ledger Adj. A/c 59,153 By Work-in-progress C A/c 38,627

Production OH C A/c 9,543

AOH C A/c 6,731

Selling OH C A/c 4,252

59,153 59,153

Production OH Control A/c

To General Ledger Adj. A/c 10,432 By Work-in-progress C A/c 23,410

Stores Ledger C A/c 2,586

Wages C A/c 9,543

Costing P & L A/c (OA) 849

23,410 23,410

Work-in-progress Control A/c

To Balance b/d 4,280 By FG Control A/c 1,18,517

General Ledger Adj. A/c 1,950 Balance c/d 6,251

Stores Ledger Control A/c 56,501

Wages Control A/c 38,627

Production OH C A/c 23,410

1,24,768 1,24,768

Administration Overhead Control A/c

To General Ledger Adj. A/c 9,546 By FG Control A/c 15,150

Wages Control A/c 6,731 Costing P/L (UA) 1,127

Cost Accounting 4

16,277 16,277

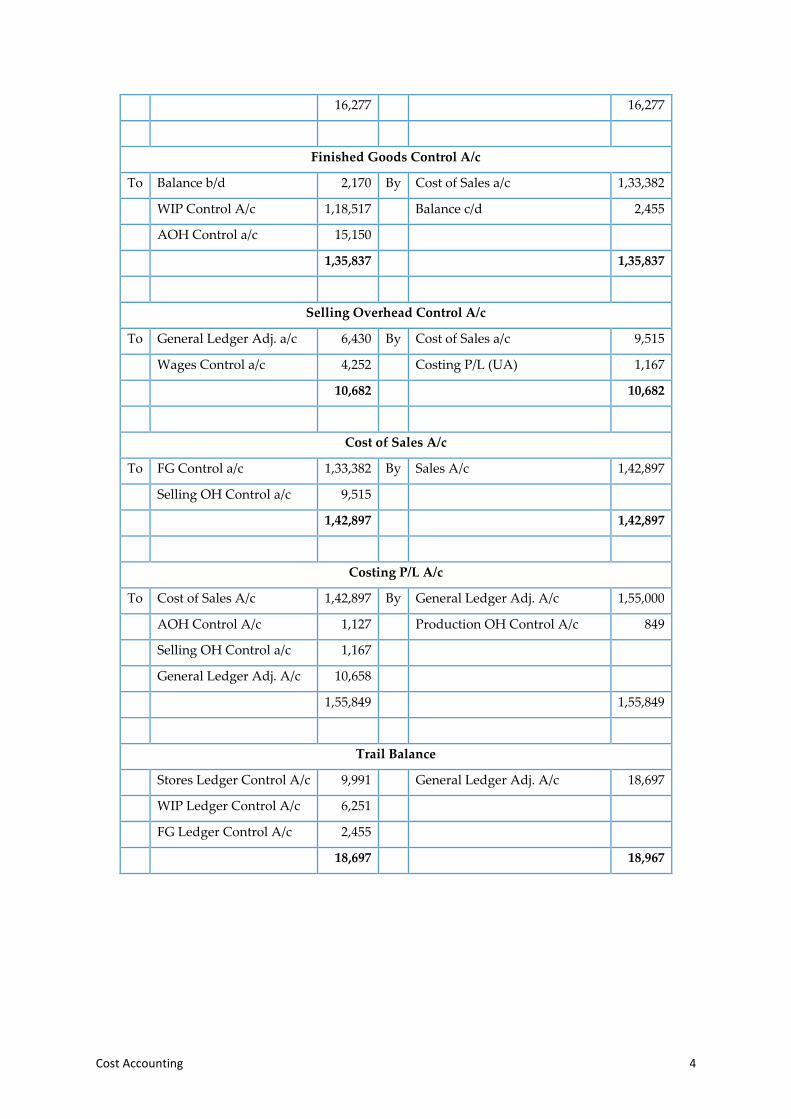

Finished Goods Control A/c

To Balance b/d 2,170 By Cost of Sales a/c 1,33,382

WIP Control A/c 1,18,517 Balance c/d 2,455

AOH Control a/c 15,150

1,35,837 1,35,837

Selling Overhead Control A/c

To General Ledger Adj. a/c 6,430 By Cost of Sales a/c 9,515

Wages Control a/c 4,252 Costing P/L (UA) 1,167

10,682 10,682

Cost of Sales A/c

To FG Control a/c 1,33,382 By Sales A/c 1,42,897

Selling OH Control a/c 9,515

1,42,897 1,42,897

Costing P/L A/c

To Cost of Sales A/c 1,42,897 By General Ledger Adj. A/c 1,55,000

AOH Control A/c 1,127 Production OH Control A/c 849

Selling OH Control a/c 1,167

General Ledger Adj. A/c 10,658

1,55,849 1,55,849

Trail Balance

Stores Ledger Control A/c 9,991 General Ledger Adj. A/c 18,697

WIP Ledger Control A/c 6,251

FG Ledger Control A/c 2,455

18,697 18,967

Cost Book Keeping 5

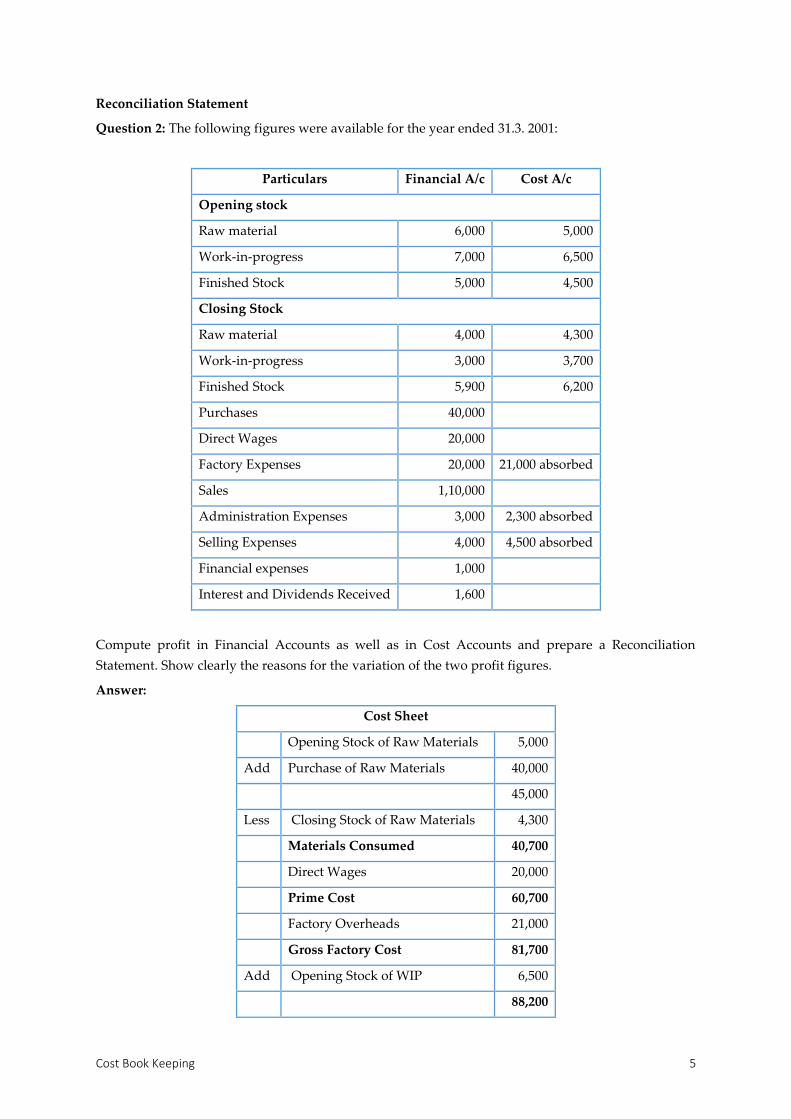

Reconciliation Statement

Question 2: The following figures were available for the year ended 31.3. 2001:

Particulars Financial A/c Cost A/c

Opening stock

Raw material 6,000 5,000

Work-in-progress 7,000 6,500

Finished Stock 5,000 4,500

Closing Stock

Raw material 4,000 4,300

Work-in-progress 3,000 3,700

Finished Stock 5,900 6,200

Purchases 40,000

Direct Wages 20,000

Factory Expenses 20,000 21,000 absorbed

Sales 1,10,000

Administration Expenses 3,000 2,300 absorbed

Selling Expenses 4,000 4,500 absorbed

Financial expenses 1,000

Interest and Dividends Received 1,600

Compute profit in Financial Accounts as well as in Cost Accounts and prepare a Reconciliation

Statement. Show clearly the reasons for the variation of the two profit figures.

Answer:

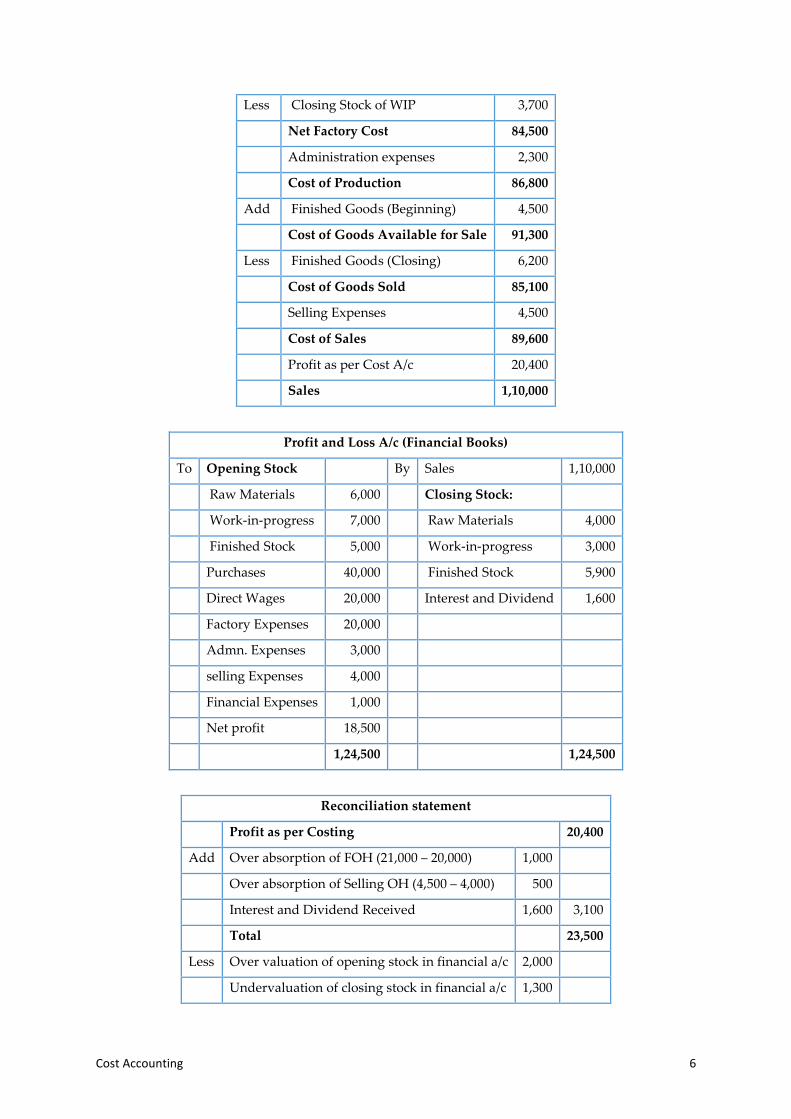

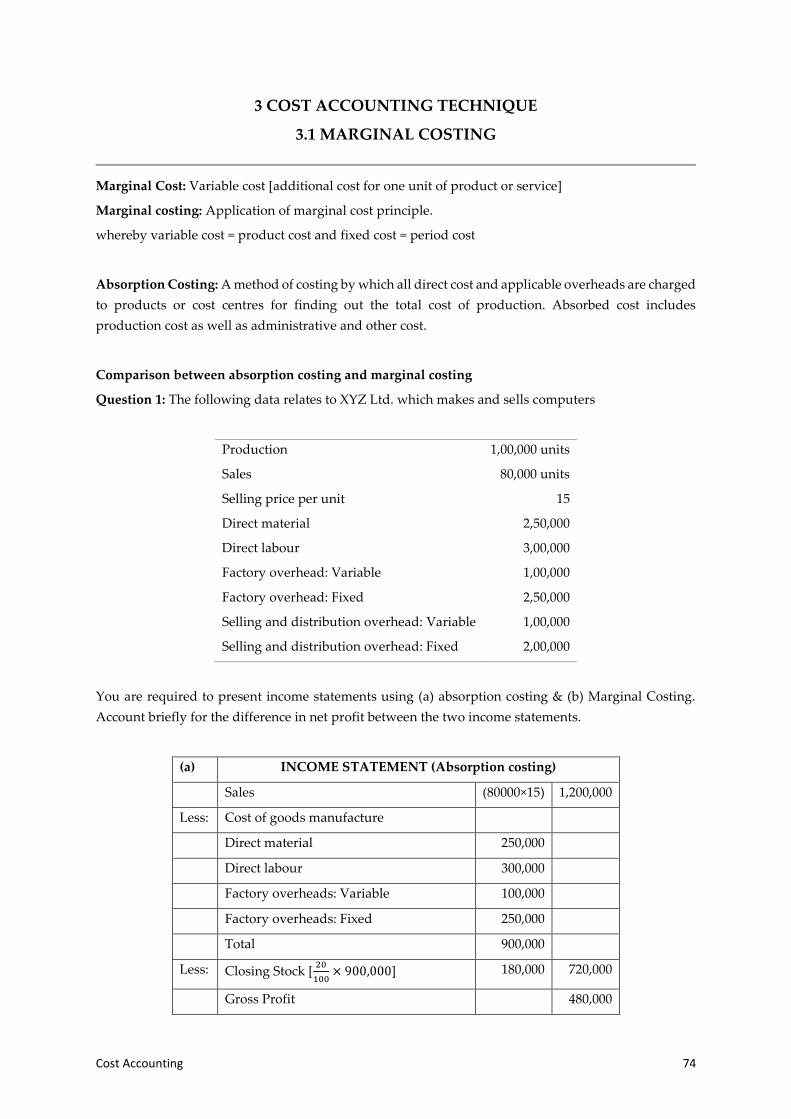

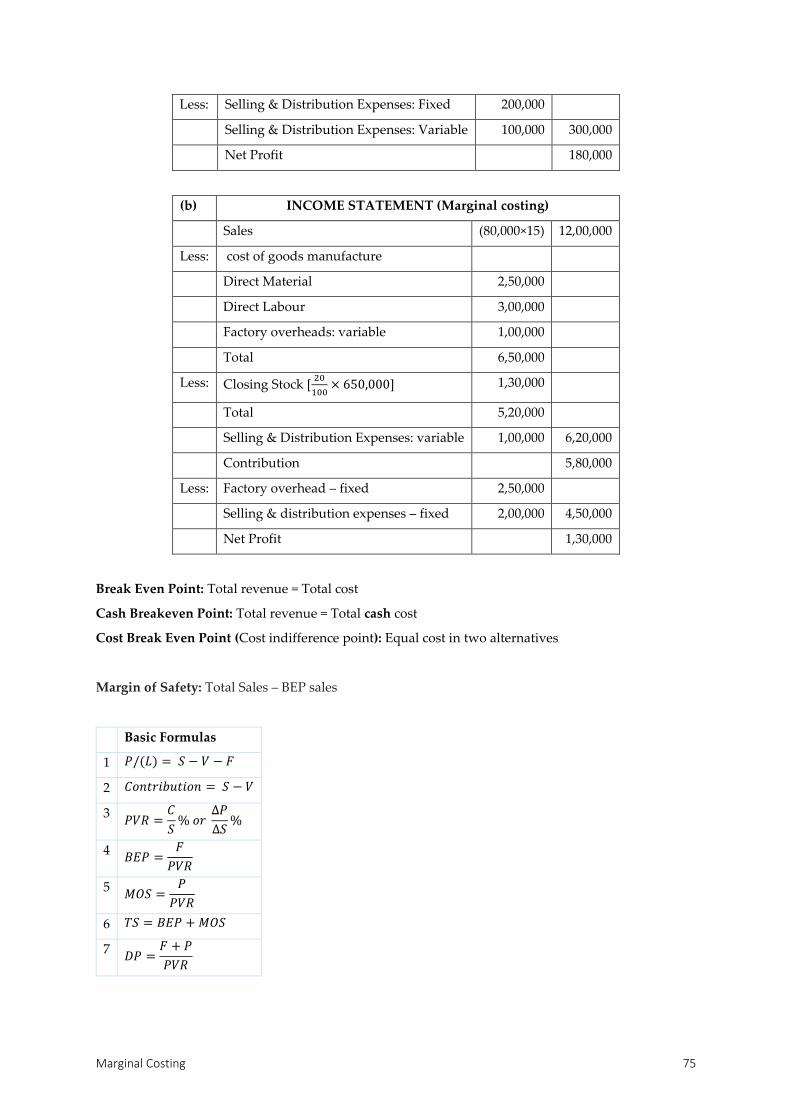

Cost Sheet

Opening Stock of Raw Materials 5,000

Add Purchase of Raw Materials 40,000

45,000

Less Closing Stock of Raw Materials 4,300

Materials Consumed 40,700

Direct Wages 20,000

Prime Cost 60,700

Factory Overheads 21,000

Gross Factory Cost 81,700

Add Opening Stock of WIP 6,500

88,200

Cost Accounting 6

Less Closing Stock of WIP 3,700

Net Factory Cost 84,500

Administration expenses 2,300

Cost of Production 86,800

Add Finished Goods (Beginning) 4,500

Cost of Goods Available for Sale 91,300

Less Finished Goods (Closing) 6,200

Cost of Goods Sold 85,100

Selling Expenses 4,500

Cost of Sales 89,600

Profit as per Cost A/c 20,400

Sales 1,10,000

Profit and Loss A/c (Financial Books)

To Opening Stock By Sales 1,10,000

Raw Materials 6,000 Closing Stock:

Work-in-progress 7,000 Raw Materials 4,000

Finished Stock 5,000 Work-in-progress 3,000

Purchases 40,000 Finished Stock 5,900

Direct Wages 20,000 Interest and Dividend 1,600

Factory Expenses 20,000

Admn. Expenses 3,000

selling Expenses 4,000

Financial Expenses 1,000

Net profit 18,500

1,24,500 1,24,500

Reconciliation statement

Profit as per Costing 20,400

Add Over absorption of FOH (21,000 – 20,000) 1,000

Over absorption of Selling OH (4,500 – 4,000) 500

Interest and Dividend Received 1,600 3,100

Total 23,500

Less Over valuation of opening stock in financial a/c 2,000

Undervaluation of closing stock in financial a/c 1,300

Cost Book Keeping 7

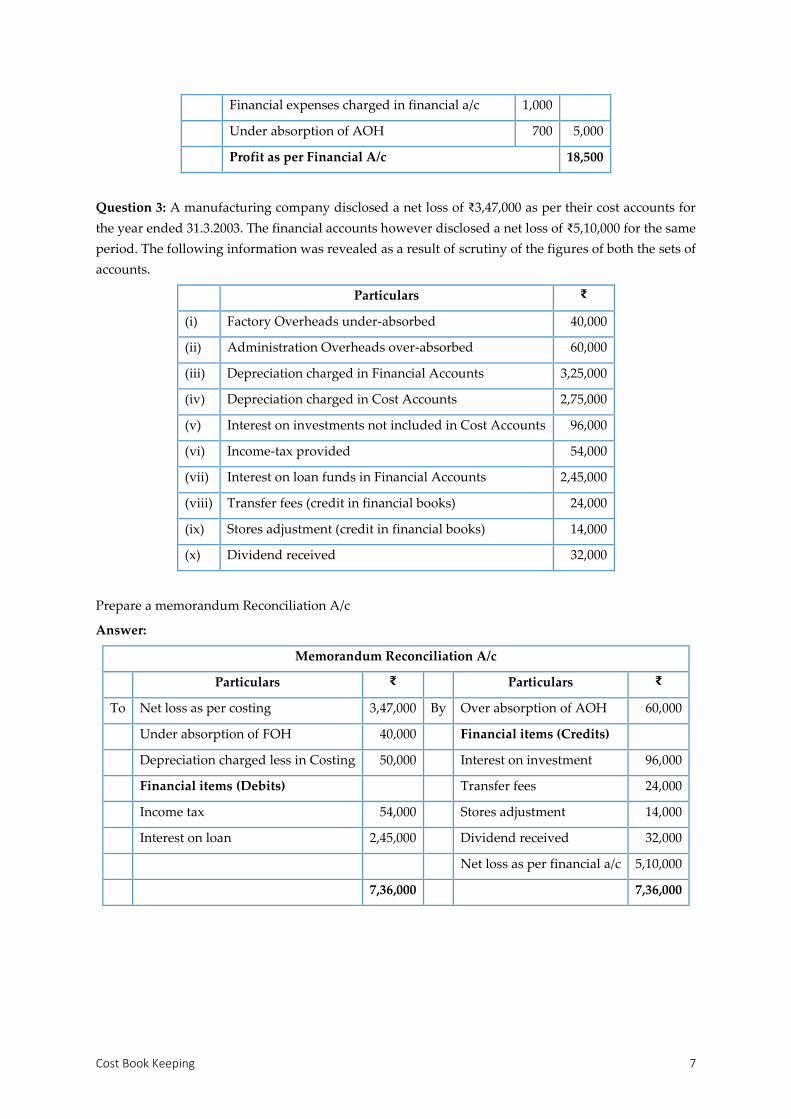

Financial expenses charged in financial a/c 1,000

Under absorption of AOH 700 5,000

Profit as per Financial A/c 18,500

Question 3: A manufacturing company disclosed a net loss of ₹3,47,000 as per their cost accounts for

the year ended 31.3.2003. The financial accounts however disclosed a net loss of ₹5,10,000 for the same

period. The following information was revealed as a result of scrutiny of the figures of both the sets of

accounts.

Particulars ₹

(i) Factory Overheads under-absorbed 40,000

(ii) Administration Overheads over-absorbed 60,000

(iii) Depreciation charged in Financial Accounts 3,25,000

(iv) Depreciation charged in Cost Accounts 2,75,000

(v) Interest on investments not included in Cost Accounts 96,000

(vi) Income-tax provided 54,000

(vii) Interest on loan funds in Financial Accounts 2,45,000

(viii) Transfer fees (credit in financial books) 24,000

(ix) Stores adjustment (credit in financial books) 14,000

(x) Dividend received 32,000

Prepare a memorandum Reconciliation A/c

Answer:

Memorandum Reconciliation A/c

Particulars ₹ Particulars ₹

To Net loss as per costing 3,47,000 By Over absorption of AOH 60,000

Under absorption of FOH 40,000 Financial items (Credits)

Depreciation charged less in Costing 50,000 Interest on investment 96,000

Financial items (Debits) Transfer fees 24,000

Income tax 54,000 Stores adjustment 14,000

Interest on loan 2,45,000 Dividend received 32,000

Net loss as per financial a/c 5,10,000

7,36,000 7,36,000

Cost Accounting 8

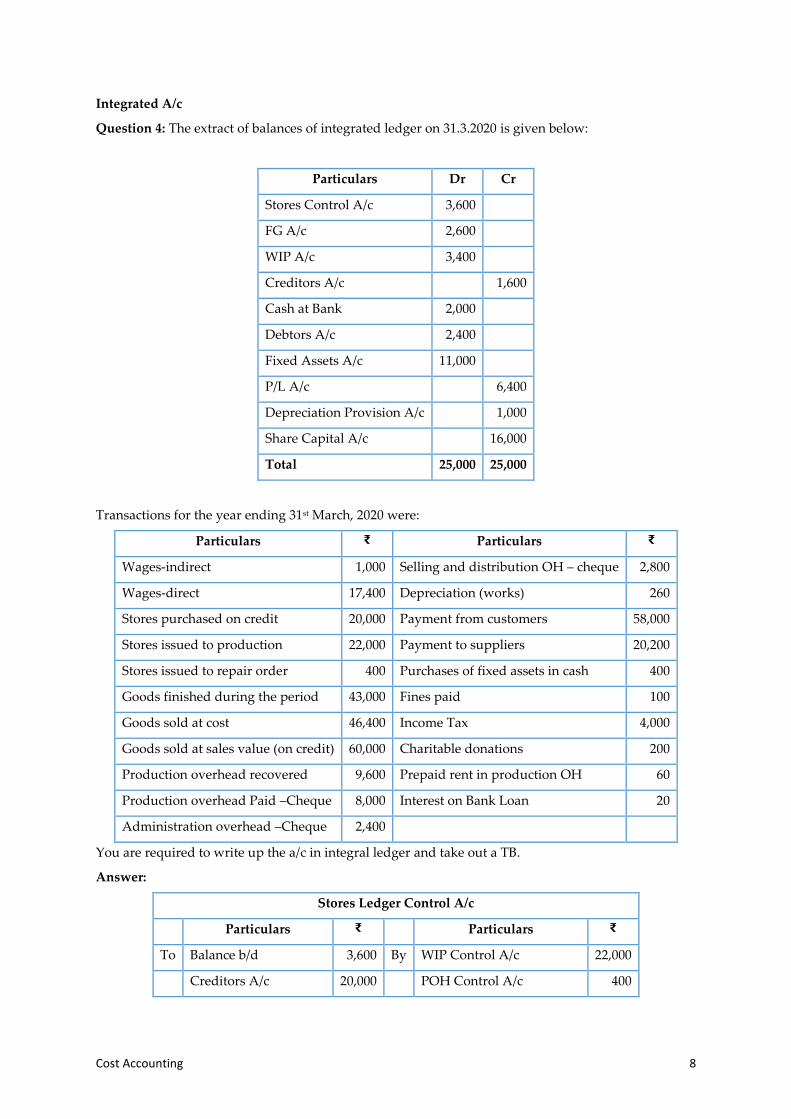

Integrated A/c

Question 4: The extract of balances of integrated ledger on 31.3.2020 is given below:

Particulars Dr Cr

Stores Control A/c 3,600

FG A/c 2,600

WIP A/c 3,400

Creditors A/c 1,600

Cash at Bank 2,000

Debtors A/c 2,400

Fixed Assets A/c 11,000

P/L A/c 6,400

Depreciation Provision A/c 1,000

Share Capital A/c 16,000

Total 25,000 25,000

Transactions for the year ending 31st March, 2020 were:

Particulars ₹ Particulars ₹

Wages-indirect 1,000 Selling and distribution OH – cheque 2,800

Wages-direct 17,400 Depreciation (works) 260

Stores purchased on credit 20,000 Payment from customers 58,000

Stores issued to production 22,000 Payment to suppliers 20,200

Stores issued to repair order 400 Purchases of fixed assets in cash 400

Goods finished during the period 43,000 Fines paid 100

Goods sold at cost 46,400 Income Tax 4,000

Goods sold at sales value (on credit) 60,000 Charitable donations 200

Production overhead recovered 9,600 Prepaid rent in production OH 60

Production overhead Paid –Cheque 8,000 Interest on Bank Loan 20

Administration overhead –Cheque 2,400

You are required to write up the a/c in integral ledger and take out a TB.

Answer:

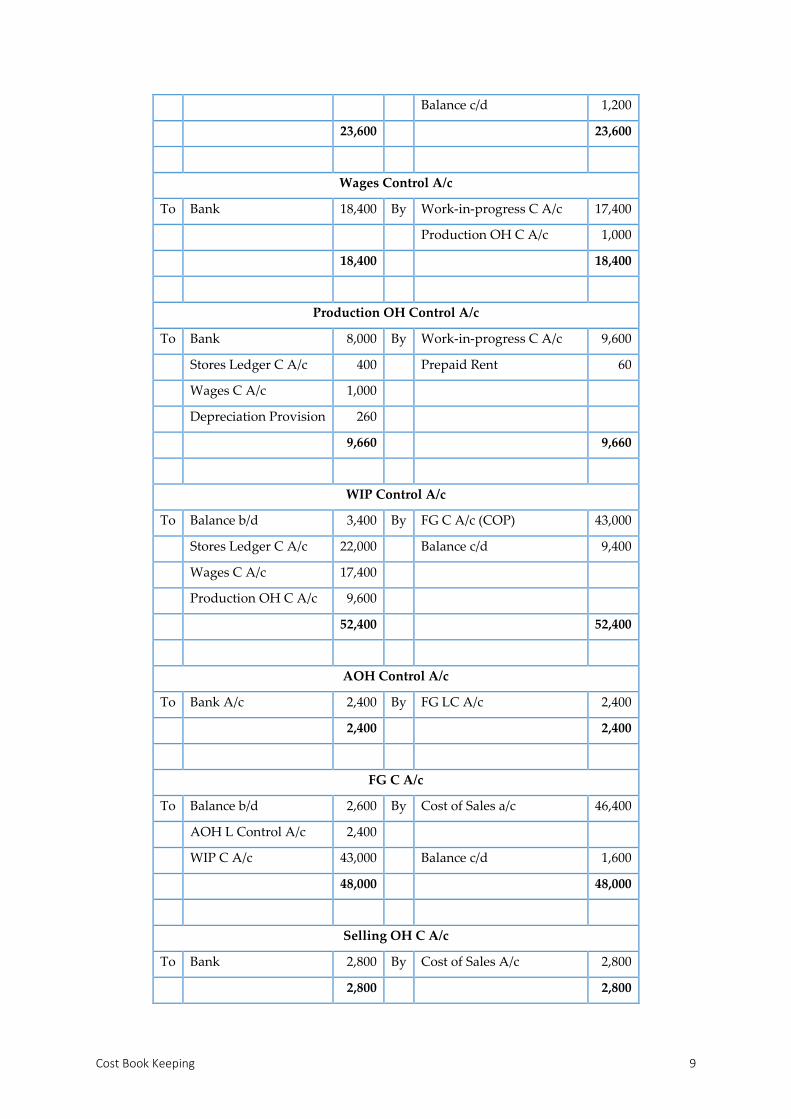

Stores Ledger Control A/c

Particulars ₹ Particulars ₹

To Balance b/d 3,600 By WIP Control A/c 22,000

Creditors A/c 20,000 POH Control A/c 400

Cost Book Keeping 9

Balance c/d 1,200

23,600 23,600

Wages Control A/c

To Bank 18,400 By Work-in-progress C A/c 17,400

Production OH C A/c 1,000

18,400 18,400

Production OH Control A/c

To Bank 8,000 By Work-in-progress C A/c 9,600

Stores Ledger C A/c 400 Prepaid Rent 60

Wages C A/c 1,000

Depreciation Provision 260

9,660 9,660

WIP Control A/c

To Balance b/d 3,400 By FG C A/c (COP) 43,000

Stores Ledger C A/c 22,000 Balance c/d 9,400

Wages C A/c 17,400

Production OH C A/c 9,600

52,400 52,400

AOH Control A/c

To Bank A/c 2,400 By FG LC A/c 2,400

2,400 2,400

FG C A/c

To Balance b/d 2,600 By Cost of Sales a/c 46,400

AOH L Control A/c 2,400

WIP C A/c 43,000 Balance c/d 1,600

48,000 48,000

Selling OH C A/c

To Bank 2,800 By Cost of Sales A/c 2,800

2,800 2,800

Cost Accounting 10

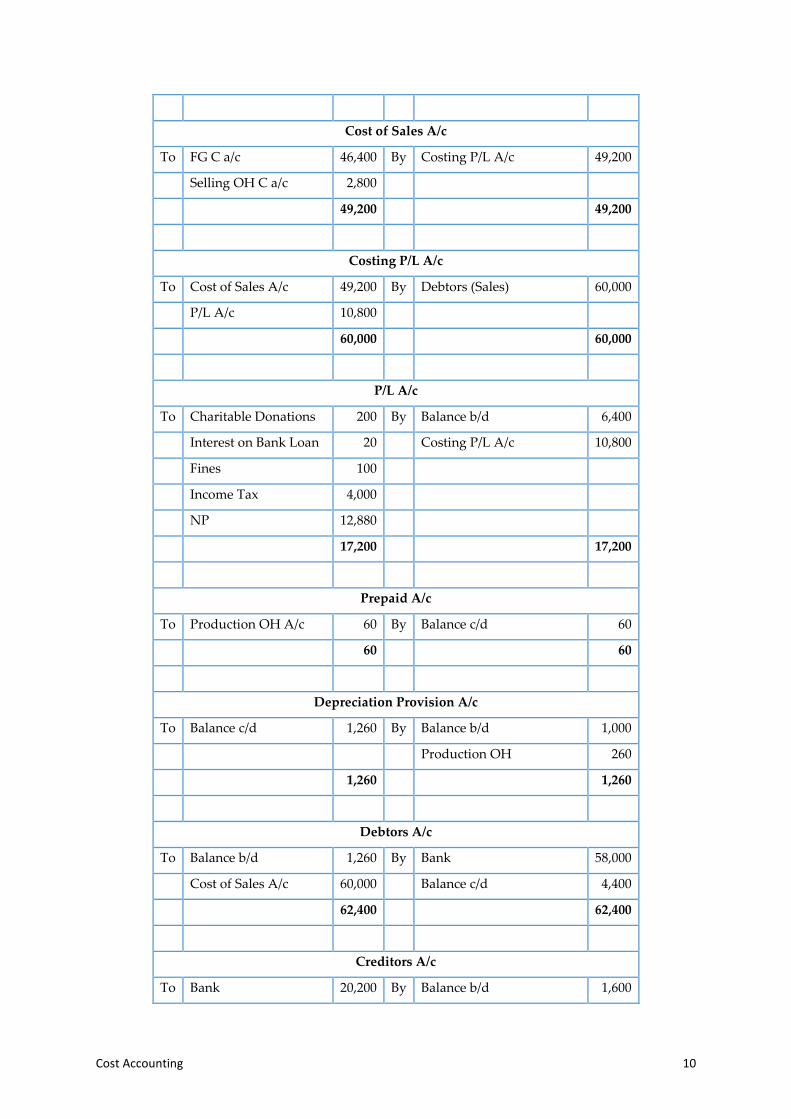

Cost of Sales A/c

To FG C a/c 46,400 By Costing P/L A/c 49,200

Selling OH C a/c 2,800

49,200 49,200

Costing P/L A/c

To Cost of Sales A/c 49,200 By Debtors (Sales) 60,000

P/L A/c 10,800

60,000 60,000

P/L A/c

To Charitable Donations 200 By Balance b/d 6,400

Interest on Bank Loan 20 Costing P/L A/c 10,800

Fines 100

Income Tax 4,000

NP 12,880

17,200 17,200

Prepaid A/c

To Production OH A/c 60 By Balance c/d 60

60 60

Depreciation Provision A/c

To Balance c/d 1,260 By Balance b/d 1,000

Production OH 260

1,260 1,260

Debtors A/c

To Balance b/d 1,260 By Bank 58,000

Cost of Sales A/c 60,000 Balance c/d 4,400

62,400 62,400

Creditors A/c

To Bank 20,200 By Balance b/d 1,600

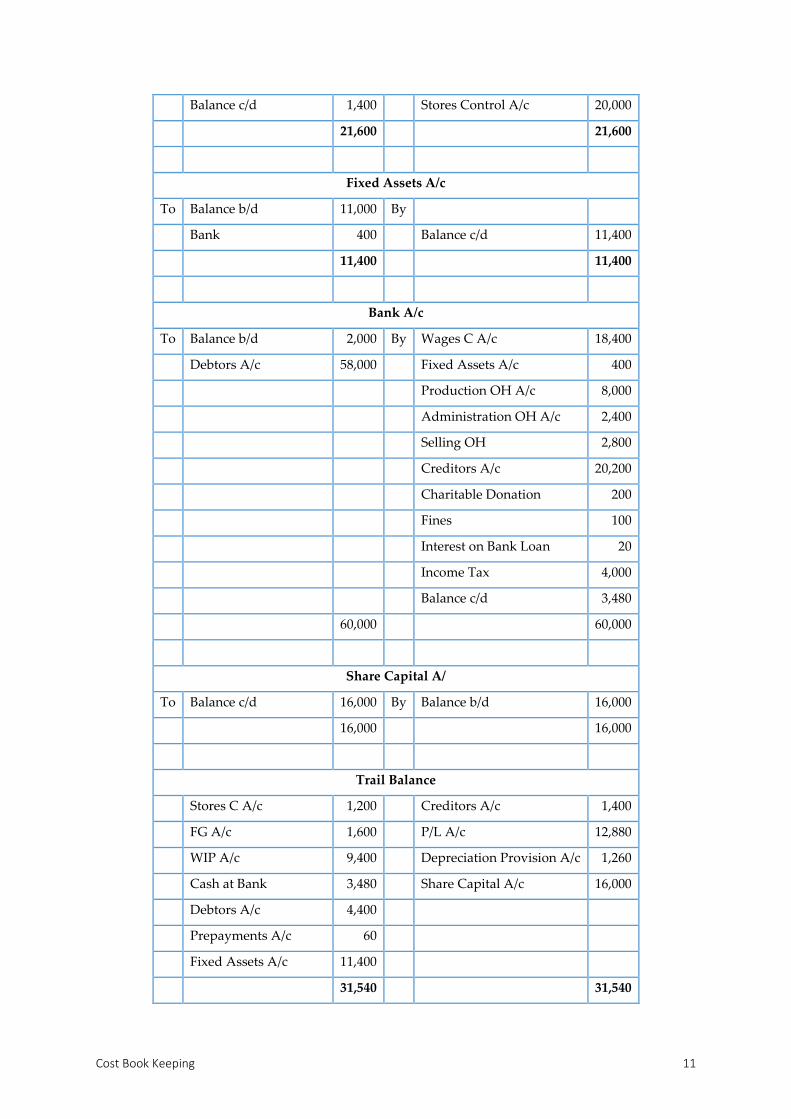

Cost Book Keeping 11

Balance c/d 1,400 Stores Control A/c 20,000

21,600 21,600

Fixed Assets A/c

To Balance b/d 11,000 By

Bank 400 Balance c/d 11,400

11,400 11,400

Bank A/c

To Balance b/d 2,000 By Wages C A/c 18,400

Debtors A/c 58,000 Fixed Assets A/c 400

Production OH A/c 8,000

Administration OH A/c 2,400

Selling OH 2,800

Creditors A/c 20,200

Charitable Donation 200

Fines 100

Interest on Bank Loan 20

Income Tax 4,000

Balance c/d 3,480

60,000 60,000

Share Capital A/

To Balance c/d 16,000 By Balance b/d 16,000

16,000 16,000

Trail Balance

Stores C A/c 1,200 Creditors A/c 1,400

FG A/c 1,600 P/L A/c 12,880

WIP A/c 9,400 Depreciation Provision A/c 1,260

Cash at Bank 3,480 Share Capital A/c 16,000

Debtors A/c 4,400

Prepayments A/c 60

Fixed Assets A/c 11,400

31,540 31,540

Cost Accounting 12

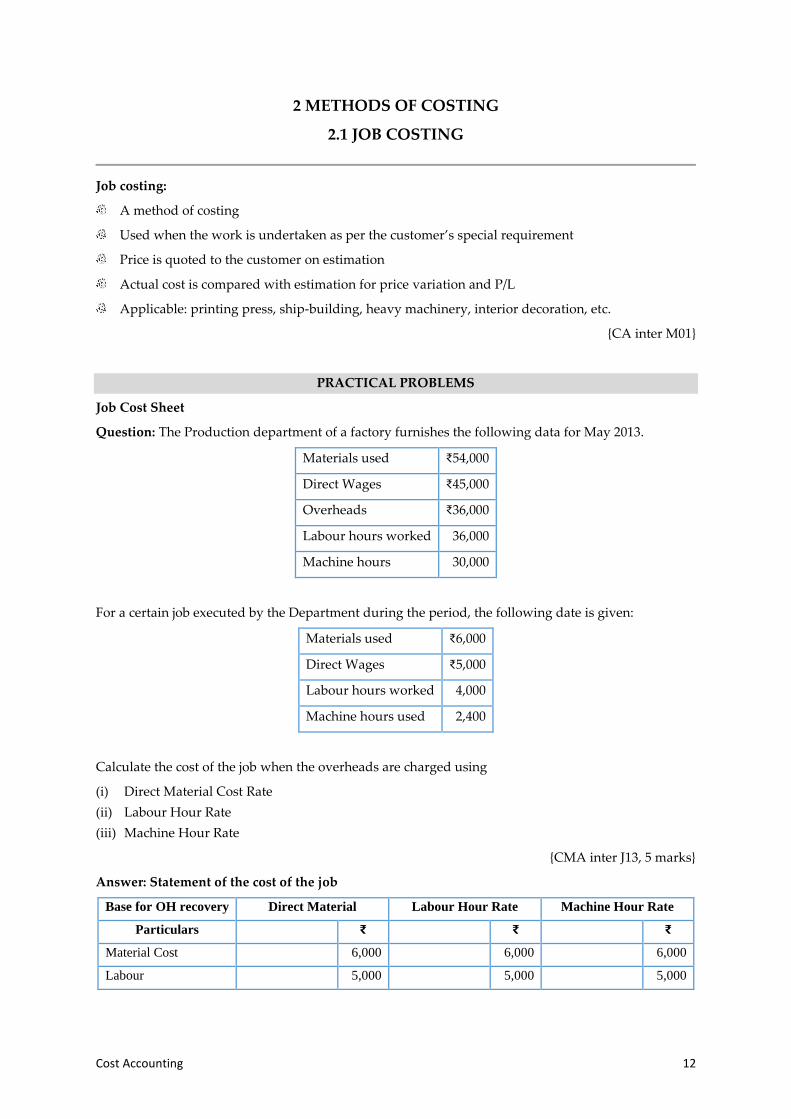

2 METHODS OF COSTING

2.1 JOB COSTING

Job costing:

A method of costing

Used when the work is undertaken as per the customer’s special requirement

Price is quoted to the customer on estimation

Actual cost is compared with estimation for price variation and P/L

Applicable: printing press, ship-building, heavy machinery, interior decoration, etc.

{CA inter M01}

PRACTICAL PROBLEMS

Job Cost Sheet

Question: The Production department of a factory furnishes the following data for May 2013.

Materials used ₹54,000

Direct Wages ₹45,000

Overheads ₹36,000

Labour hours worked 36,000

Machine hours 30,000

For a certain job executed by the Department during the period, the following date is given:

Materials used ₹6,000

Direct Wages ₹5,000

Labour hours worked 4,000

Machine hours used 2,400

Calculate the cost of the job when the overheads are charged using

(i) Direct Material Cost Rate

(ii) Labour Hour Rate

(iii) Machine Hour Rate

{CMA inter J13, 5 marks}

Answer: Statement of the cost of the job

Base for OH recovery Direct Material Labour Hour Rate Machine Hour Rate

Particulars ₹ ₹ ₹

Material Cost 6,000 6,000 6,000

Labour 5,000 5,000 5,000

Job Costing 13

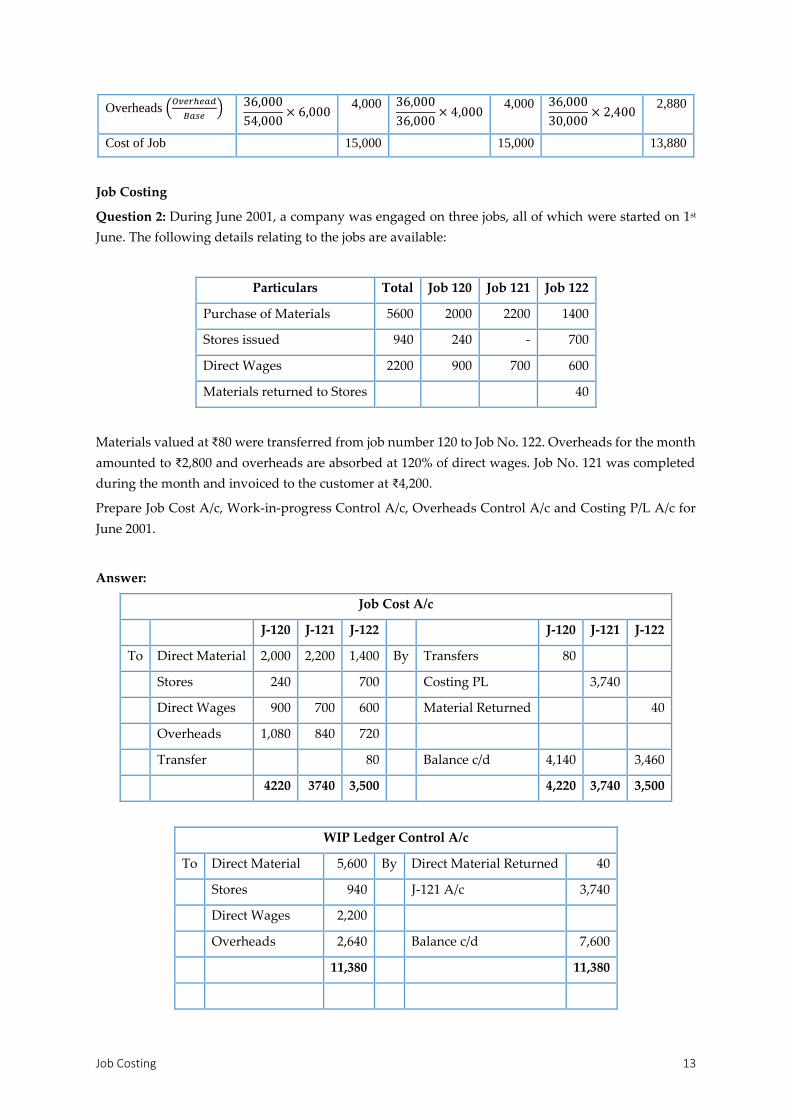

Overheads (𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑

𝐵𝑎𝑠𝑒)

36,000

54,000× 6,000

4,000 36,000

36,000× 4,000

4,000 36,000

30,000× 2,400

2,880

Cost of Job 15,000 15,000 13,880

Job Costing

Question 2: During June 2001, a company was engaged on three jobs, all of which were started on 1st

June. The following details relating to the jobs are available:

Particulars Total Job 120 Job 121 Job 122

Purchase of Materials 5600 2000 2200 1400

Stores issued 940 240 - 700

Direct Wages 2200 900 700 600

Materials returned to Stores 40

Materials valued at ₹80 were transferred from job number 120 to Job No. 122. Overheads for the month

amounted to ₹2,800 and overheads are absorbed at 120% of direct wages. Job No. 121 was completed

during the month and invoiced to the customer at ₹4,200.

Prepare Job Cost A/c, Work-in-progress Control A/c, Overheads Control A/c and Costing P/L A/c for

June 2001.

Answer:

Job Cost A/c

J-120 J-121 J-122 J-120 J-121 J-122

To Direct Material 2,000 2,200 1,400 By Transfers 80

Stores 240 700 Costing PL 3,740

Direct Wages 900 700 600 Material Returned 40

Overheads 1,080 840 720

Transfer 80 Balance c/d 4,140 3,460

4220 3740 3,500 4,220 3,740 3,500

WIP Ledger Control A/c

To Direct Material 5,600 By Direct Material Returned 40

Stores 940 J-121 A/c 3,740

Direct Wages 2,200

Overheads 2,640 Balance c/d 7,600

11,380 11,380

Cost Accounting 14

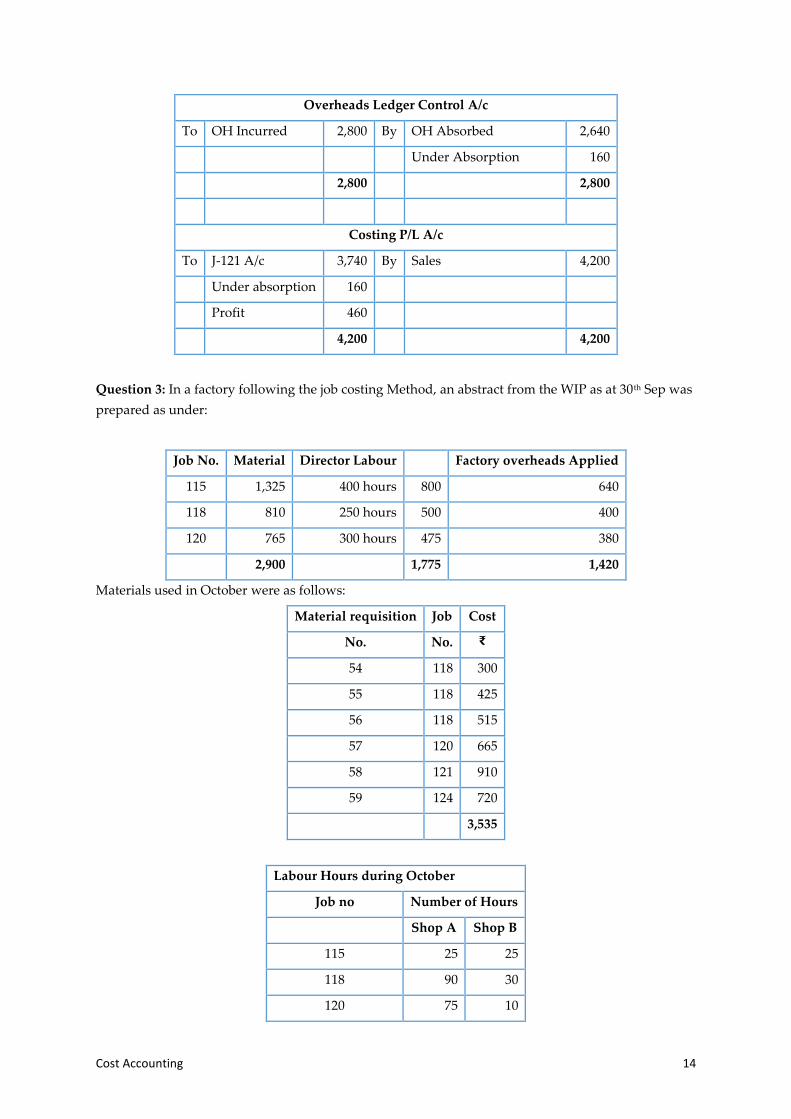

Overheads Ledger Control A/c

To OH Incurred 2,800 By OH Absorbed 2,640

Under Absorption 160

2,800 2,800

Costing P/L A/c

To J-121 A/c 3,740 By Sales 4,200

Under absorption 160

Profit 460

4,200 4,200

Question 3: In a factory following the job costing Method, an abstract from the WIP as at 30th Sep was

prepared as under:

Job No. Material Director Labour Factory overheads Applied

115 1,325 400 hours 800 640

118 810 250 hours 500 400

120 765 300 hours 475 380

2,900 1,775 1,420

Materials used in October were as follows:

Material requisition Job Cost

No. No. ₹

54 118 300

55 118 425

56 118 515

57 120 665

58 121 910

59 124 720

3,535

Labour Hours during October

Job no Number of Hours

Shop A Shop B

115 25 25

118 90 30

120 75 10

Job Costing 15

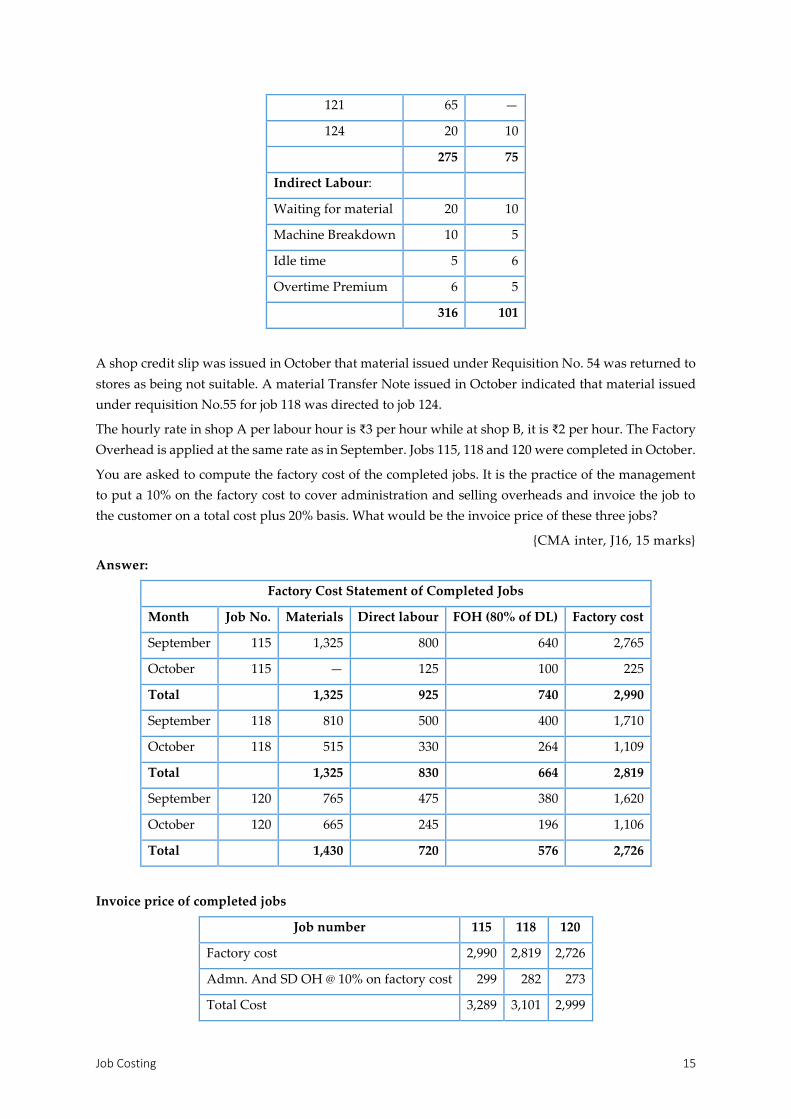

121 65 —

124 20 10

275 75

Indirect Labour:

Waiting for material 20 10

Machine Breakdown 10 5

Idle time 5 6

Overtime Premium 6 5

316 101

A shop credit slip was issued in October that material issued under Requisition No. 54 was returned to

stores as being not suitable. A material Transfer Note issued in October indicated that material issued

under requisition No.55 for job 118 was directed to job 124.

The hourly rate in shop A per labour hour is ₹3 per hour while at shop B, it is ₹2 per hour. The Factory

Overhead is applied at the same rate as in September. Jobs 115, 118 and 120 were completed in October.

You are asked to compute the factory cost of the completed jobs. It is the practice of the management

to put a 10% on the factory cost to cover administration and selling overheads and invoice the job to

the customer on a total cost plus 20% basis. What would be the invoice price of these three jobs?

{CMA inter, J16, 15 marks}

Answer:

Factory Cost Statement of Completed Jobs

Month Job No. Materials Direct labour FOH (80% of DL) Factory cost

September 115 1,325 800 640 2,765

October 115 — 125 100 225

Total 1,325 925 740 2,990

September 118 810 500 400 1,710

October 118 515 330 264 1,109

Total 1,325 830 664 2,819

September 120 765 475 380 1,620

October 120 665 245 196 1,106

Total 1,430 720 576 2,726

Invoice price of completed jobs

Job number 115 118 120

Factory cost 2,990 2,819 2,726

Admn. And SD OH @ 10% on factory cost 299 282 273

Total Cost 3,289 3,101 2,999

Cost Accounting 16

Profit (20% of Total cost) 658 620 600

Invoice price 3,947 3,721 3,599

Note: In the above solution it has been assumed that indirect labour costs have been included in the

factory overhead and they have been recovered as 80% of the labour cost.

Question 4: A factory incurred the following expenditure during the year 2007:

Particulars ₹ ₹

Direct material consumed 12,00,000

Manufacturing Wages 7,00,000

Manufacturing overhead: 19,00,000

Fixed 3,60,000

Variable 2,50,000 6,10,000

Cost of Production 25,10,000

In the year 2008, following changes are expected in production and cost of production.

1. Production will increase due to recruitment of 60% more workers in the factory.

2. Overall efficiency will decline by 10% on account of recruitment of new workers.

3. There will be an increase of 20% in Fixed overhead and 60% in Variable overhead.

4. The cost of direct material will be decreased by 6%.

5. The company desires to earn a profit of 10% on selling price.

Ascertain the cost of production and selling price.

{CA inter M08, 8 marks}

Answer:

Particulars ₹ ₹ Workings

Direct material consumed 12,00,000 16,24,320 12,00,000 ×

1441

100×

94

100

Manufacturing Wages 7,00,000 11,20,000 7,00,000 ×

160

100

Manufacturing overhead: 19,00,000 27,44,320

Fixed 3,60,000 4,32,000 3,60,000 ×

120

100

Variable 2,50,000 4,00,000 2,50,000 ×

160

100

Cost of Production 25,10,000 35,76,320 90

Profit 3,97,369 10

Sales 39,73,689 100

1 Production will increase by 60% but efficiency will decline by 10%. hence

160 – 10% of 160 = 144% so increase by 44%.

Job Costing 17

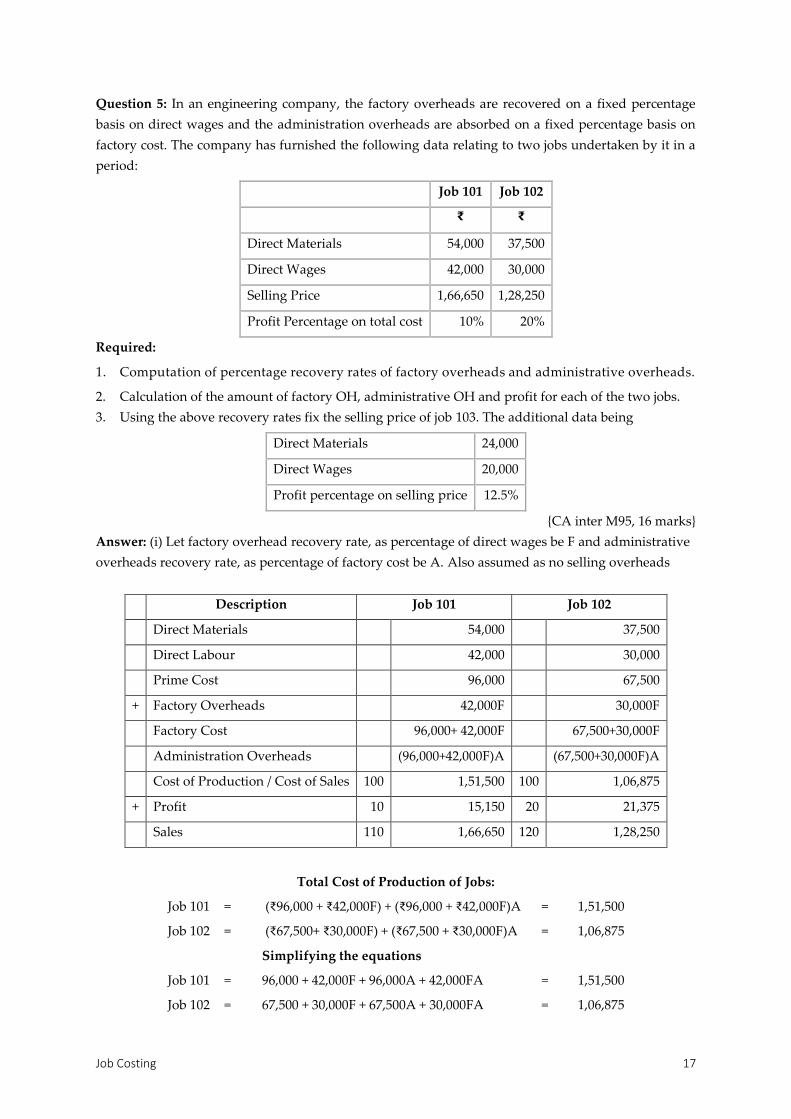

Question 5: In an engineering company, the factory overheads are recovered on a fixed percentage

basis on direct wages and the administration overheads are absorbed on a fixed percentage basis on

factory cost. The company has furnished the following data relating to two jobs undertaken by it in a

period:

Job 101 Job 102

₹ ₹

Direct Materials 54,000 37,500

Direct Wages 42,000 30,000

Selling Price 1,66,650 1,28,250

Profit Percentage on total cost 10% 20%

Required:

1. Computation of percentage recovery rates of factory overheads and administrative overheads.

2. Calculation of the amount of factory OH, administrative OH and profit for each of the two jobs.

3. Using the above recovery rates fix the selling price of job 103. The additional data being

Direct Materials 24,000

Direct Wages 20,000

Profit percentage on selling price 12.5%

{CA inter M95, 16 marks}

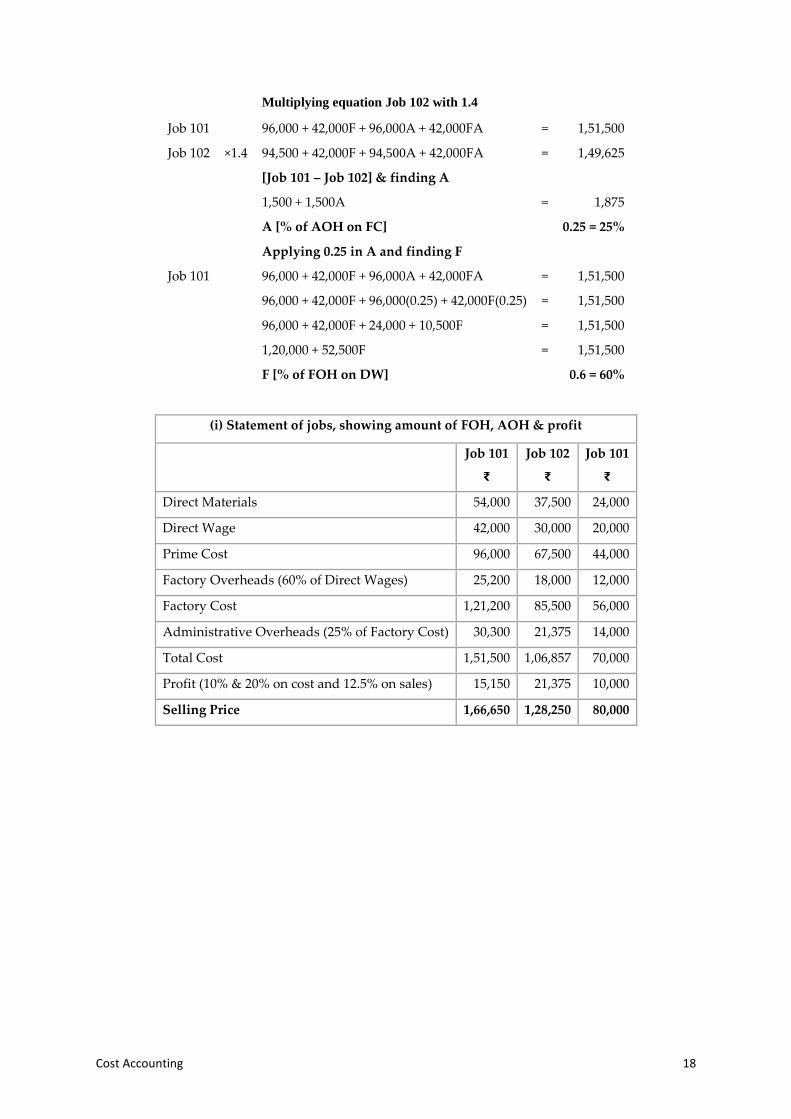

Answer: (i) Let factory overhead recovery rate, as percentage of direct wages be F and administrative

overheads recovery rate, as percentage of factory cost be A. Also assumed as no selling overheads

Description Job 101 Job 102

Direct Materials 54,000 37,500

Direct Labour 42,000 30,000

Prime Cost 96,000 67,500

+ Factory Overheads 42,000F 30,000F

Factory Cost 96,000+ 42,000F 67,500+30,000F

Administration Overheads (96,000+42,000F)A (67,500+30,000F)A

Cost of Production / Cost of Sales 100 1,51,500 100 1,06,875

+ Profit 10 15,150 20 21,375

Sales 110 1,66,650 120 1,28,250

Total Cost of Production of Jobs:

Job 101 = (₹96,000 + ₹42,000F) + (₹96,000 + ₹42,000F)A = 1,51,500

Job 102 = (₹67,500+ ₹30,000F) + (₹67,500 + ₹30,000F)A = 1,06,875

Simplifying the equations

Job 101 = 96,000 + 42,000F + 96,000A + 42,000FA = 1,51,500

Job 102 = 67,500 + 30,000F + 67,500A + 30,000FA = 1,06,875

Cost Accounting 18

Multiplying equation Job 102 with 1.4

Job 101 96,000 + 42,000F + 96,000A + 42,000FA = 1,51,500

Job 102 ×1.4 94,500 + 42,000F + 94,500A + 42,000FA = 1,49,625

[Job 101 – Job 102] & finding A

1,500 + 1,500A = 1,875

A [% of AOH on FC] 0.25 = 25%

Applying 0.25 in A and finding F

Job 101 96,000 + 42,000F + 96,000A + 42,000FA = 1,51,500

96,000 + 42,000F + 96,000(0.25) + 42,000F(0.25) = 1,51,500

96,000 + 42,000F + 24,000 + 10,500F = 1,51,500

1,20,000 + 52,500F = 1,51,500

F [% of FOH on DW] 0.6 = 60%

(i) Statement of jobs, showing amount of FOH, AOH & profit

Job 101

₹

Job 102

₹

Job 101

₹

Direct Materials 54,000 37,500 24,000

Direct Wage 42,000 30,000 20,000

Prime Cost 96,000 67,500 44,000

Factory Overheads (60% of Direct Wages) 25,200 18,000 12,000

Factory Cost 1,21,200 85,500 56,000

Administrative Overheads (25% of Factory Cost) 30,300 21,375 14,000

Total Cost 1,51,500 1,06,857 70,000

Profit (10% & 20% on cost and 12.5% on sales) 15,150 21,375 10,000

Selling Price 1,66,650 1,28,250 80,000

Batch Costing 19

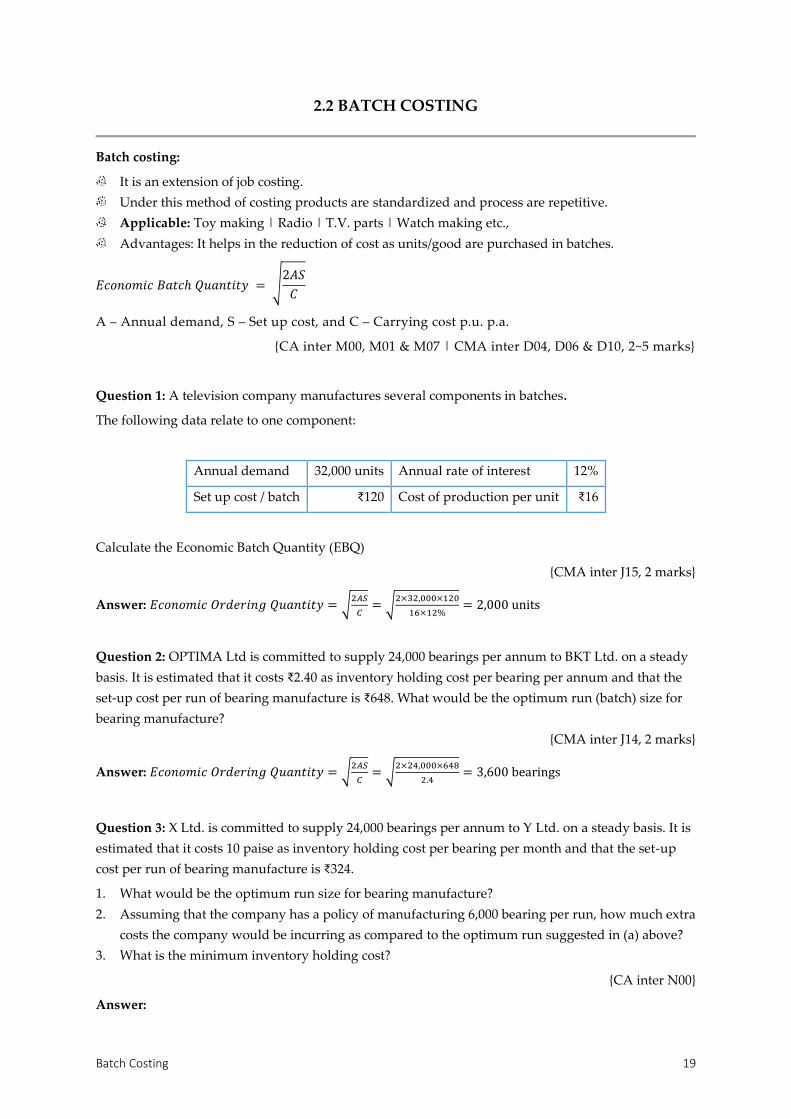

2.2 BATCH COSTING

Batch costing:

It is an extension of job costing.

Under this method of costing products are standardized and process are repetitive.

Applicable: Toy making | Radio | T.V. parts | Watch making etc.,

Advantages: It helps in the reduction of cost as units/good are purchased in batches.

𝐸𝑐𝑜𝑛𝑜𝑚𝑖𝑐 𝐵𝑎𝑡𝑐ℎ 𝑄𝑢𝑎𝑛𝑡𝑖𝑡𝑦 = √2𝐴𝑆

𝐶

A – Annual demand, S – Set up cost, and C – Carrying cost p.u. p.a.

{CA inter M00, M01 & M07 | CMA inter D04, D06 & D10, 2~5 marks}

Question 1: A television company manufactures several components in batches.

The following data relate to one component:

Annual demand 32,000 units Annual rate of interest 12%

Set up cost / batch ₹120 Cost of production per unit ₹16

Calculate the Economic Batch Quantity (EBQ)

{CMA inter J15, 2 marks}

Answer: 𝐸𝑐𝑜𝑛𝑜𝑚𝑖𝑐 𝑂𝑟𝑑𝑒𝑟𝑖𝑛𝑔 𝑄𝑢𝑎𝑛𝑡𝑖𝑡𝑦 = √2𝐴𝑆

𝐶= √

2×32,000×120

16×12%= 2,000 units

Question 2: OPTIMA Ltd is committed to supply 24,000 bearings per annum to BKT Ltd. on a steady

basis. It is estimated that it costs ₹2.40 as inventory holding cost per bearing per annum and that the

set-up cost per run of bearing manufacture is ₹648. What would be the optimum run (batch) size for

bearing manufacture?

{CMA inter J14, 2 marks}

Answer: 𝐸𝑐𝑜𝑛𝑜𝑚𝑖𝑐 𝑂𝑟𝑑𝑒𝑟𝑖𝑛𝑔 𝑄𝑢𝑎𝑛𝑡𝑖𝑡𝑦 = √2𝐴𝑆

𝐶= √

2×24,000×648

2.4= 3,600 bearings

Question 3: X Ltd. is committed to supply 24,000 bearings per annum to Y Ltd. on a steady basis. It is

estimated that it costs 10 paise as inventory holding cost per bearing per month and that the set-up

cost per run of bearing manufacture is ₹324.

1. What would be the optimum run size for bearing manufacture?

2. Assuming that the company has a policy of manufacturing 6,000 bearing per run, how much extra

costs the company would be incurring as compared to the optimum run suggested in (a) above?

3. What is the minimum inventory holding cost?

{CA inter N00}

Answer:

Cost Accounting 20

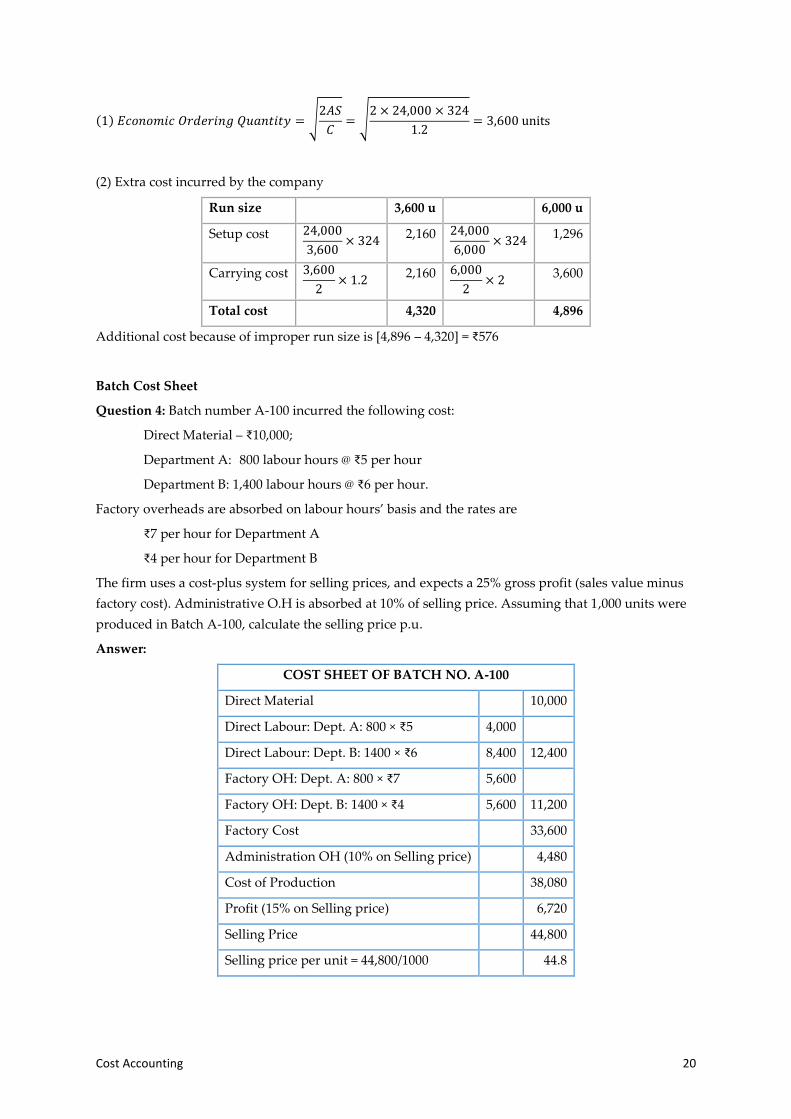

(1) 𝐸𝑐𝑜𝑛𝑜𝑚𝑖𝑐 𝑂𝑟𝑑𝑒𝑟𝑖𝑛𝑔 𝑄𝑢𝑎𝑛𝑡𝑖𝑡𝑦 = √2𝐴𝑆

𝐶= √

2 × 24,000 × 324

1.2= 3,600 units

(2) Extra cost incurred by the company

Run size 3,600 u 6,000 u

Setup cost 24,000

3,600× 324

2,160 24,000

6,000× 324

1,296

Carrying cost 3,600

2× 1.2

2,160 6,000

2× 2

3,600

Total cost 4,320 4,896

Additional cost because of improper run size is [4,896 – 4,320] = ₹576

Batch Cost Sheet

Question 4: Batch number A-100 incurred the following cost:

Direct Material – ₹10,000;

Department A: 800 labour hours @ ₹5 per hour

Department B: 1,400 labour hours @ ₹6 per hour.

Factory overheads are absorbed on labour hours’ basis and the rates are

₹7 per hour for Department A

₹4 per hour for Department B

The firm uses a cost-plus system for selling prices, and expects a 25% gross profit (sales value minus

factory cost). Administrative O.H is absorbed at 10% of selling price. Assuming that 1,000 units were

produced in Batch A-100, calculate the selling price p.u.

Answer:

COST SHEET OF BATCH NO. A-100

Direct Material 10,000

Direct Labour: Dept. A: 800 × ₹5 4,000

Direct Labour: Dept. B: 1400 × ₹6 8,400 12,400

Factory OH: Dept. A: 800 × ₹7 5,600

Factory OH: Dept. B: 1400 × ₹4 5,600 11,200

Factory Cost 33,600

Administration OH (10% on Selling price) 4,480

Cost of Production 38,080

Profit (15% on Selling price) 6,720

Selling Price 44,800

Selling price per unit = 44,800/1000 44.8

Contract Costing 21

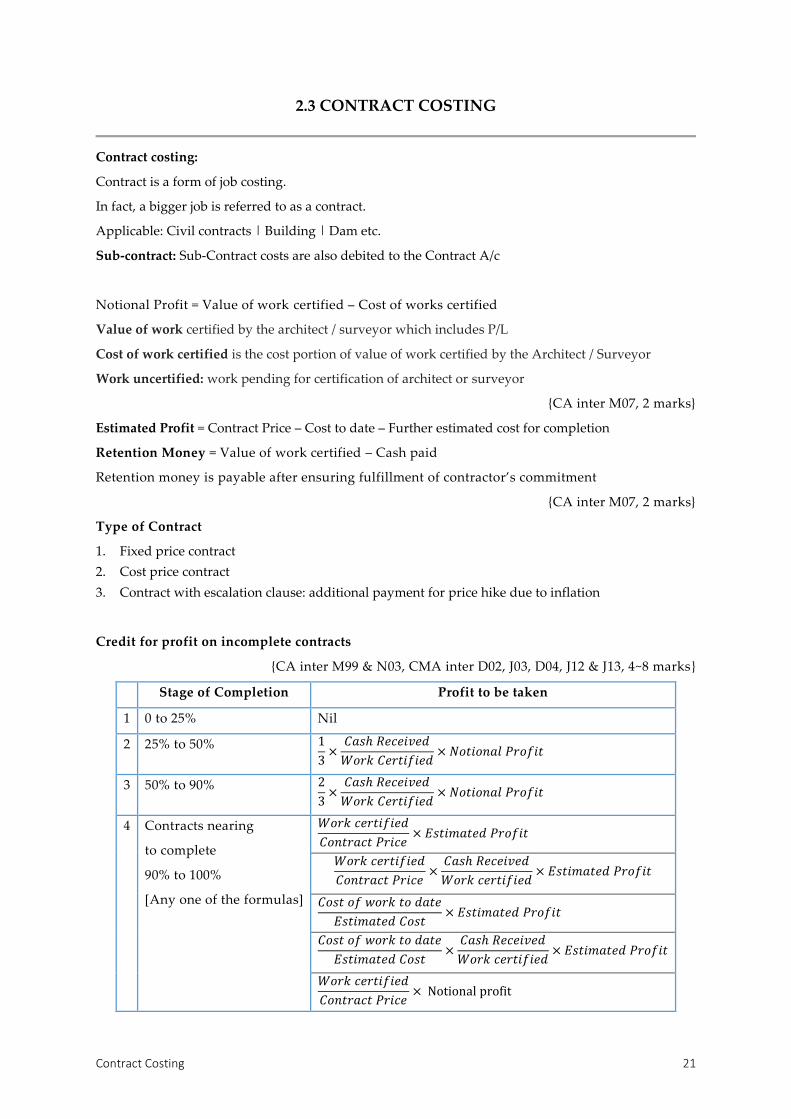

2.3 CONTRACT COSTING

Contract costing:

Contract is a form of job costing.

In fact, a bigger job is referred to as a contract.

Applicable: Civil contracts | Building | Dam etc.

Sub-contract: Sub-Contract costs are also debited to the Contract A/c

Notional Profit = Value of work certified – Cost of works certified

Value of work certified by the architect / surveyor which includes P/L

Cost of work certified is the cost portion of value of work certified by the Architect / Surveyor

Work uncertified: work pending for certification of architect or surveyor

{CA inter M07, 2 marks}

Estimated Profit = Contract Price – Cost to date – Further estimated cost for completion

Retention Money = Value of work certified – Cash paid

Retention money is payable after ensuring fulfillment of contractor’s commitment

{CA inter M07, 2 marks}

Type of Contract

1. Fixed price contract

2. Cost price contract

3. Contract with escalation clause: additional payment for price hike due to inflation

Credit for profit on incomplete contracts

{CA inter M99 & N03, CMA inter D02, J03, D04, J12 & J13, 4~8 marks}

Stage of Completion Profit to be taken

1 0 to 25% Nil

2 25% to 50% 1

3×

𝐶𝑎𝑠ℎ 𝑅𝑒𝑐𝑒𝑖𝑣𝑒𝑑

𝑊𝑜𝑟𝑘 𝐶𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑× 𝑁𝑜𝑡𝑖𝑜𝑛𝑎𝑙 𝑃𝑟𝑜𝑓𝑖𝑡

3 50% to 90% 2

3×

𝐶𝑎𝑠ℎ 𝑅𝑒𝑐𝑒𝑖𝑣𝑒𝑑

𝑊𝑜𝑟𝑘 𝐶𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑× 𝑁𝑜𝑡𝑖𝑜𝑛𝑎𝑙 𝑃𝑟𝑜𝑓𝑖𝑡

4 Contracts nearing

to complete

90% to 100%

[Any one of the formulas]

𝑊𝑜𝑟𝑘 𝑐𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑

𝐶𝑜𝑛𝑡𝑟𝑎𝑐𝑡 𝑃𝑟𝑖𝑐𝑒× 𝐸𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝑃𝑟𝑜𝑓𝑖𝑡

𝑊𝑜𝑟𝑘 𝑐𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑

𝐶𝑜𝑛𝑡𝑟𝑎𝑐𝑡 𝑃𝑟𝑖𝑐𝑒×

𝐶𝑎𝑠ℎ 𝑅𝑒𝑐𝑒𝑖𝑣𝑒𝑑

𝑊𝑜𝑟𝑘 𝑐𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑× 𝐸𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝑃𝑟𝑜𝑓𝑖𝑡

𝐶𝑜𝑠𝑡 𝑜𝑓 𝑤𝑜𝑟𝑘 𝑡𝑜 𝑑𝑎𝑡𝑒

𝐸𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝐶𝑜𝑠𝑡× 𝐸𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝑃𝑟𝑜𝑓𝑖𝑡

𝐶𝑜𝑠𝑡 𝑜𝑓 𝑤𝑜𝑟𝑘 𝑡𝑜 𝑑𝑎𝑡𝑒

𝐸𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝐶𝑜𝑠𝑡×

𝐶𝑎𝑠ℎ 𝑅𝑒𝑐𝑒𝑖𝑣𝑒𝑑

𝑊𝑜𝑟𝑘 𝑐𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑× 𝐸𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝑃𝑟𝑜𝑓𝑖𝑡

𝑊𝑜𝑟𝑘 𝑐𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑

𝐶𝑜𝑛𝑡𝑟𝑎𝑐𝑡 𝑃𝑟𝑖𝑐𝑒× Notional profit

Cost Accounting 22

PRACTICAL PROBLEMS

Concept Problem: Simple | Multiple Years | Multiple Contracts

Contract Nearing to Completion

Contract with Escalation Clause

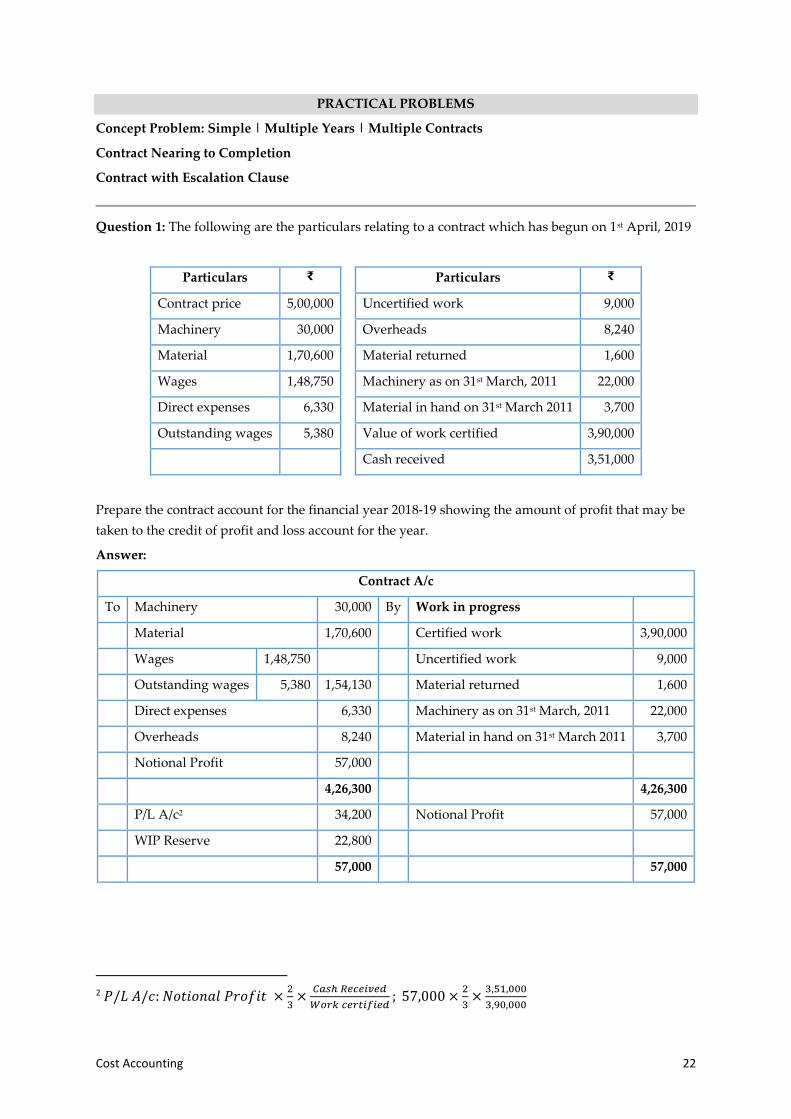

Question 1: The following are the particulars relating to a contract which has begun on 1st April, 2019

Particulars ₹ Particulars ₹

Contract price 5,00,000 Uncertified work 9,000

Machinery 30,000 Overheads 8,240

Material 1,70,600 Material returned 1,600

Wages 1,48,750 Machinery as on 31st March, 2011 22,000

Direct expenses 6,330 Material in hand on 31st March 2011 3,700

Outstanding wages 5,380 Value of work certified 3,90,000

Cash received 3,51,000

Prepare the contract account for the financial year 2018-19 showing the amount of profit that may be

taken to the credit of profit and loss account for the year.

Answer:

Contract A/c

To Machinery 30,000 By Work in progress

Material 1,70,600 Certified work 3,90,000

Wages 1,48,750 Uncertified work 9,000

Outstanding wages 5,380 1,54,130 Material returned 1,600

Direct expenses 6,330 Machinery as on 31st March, 2011 22,000

Overheads 8,240 Material in hand on 31st March 2011 3,700

Notional Profit 57,000

4,26,300 4,26,300

P/L A/c2 34,200 Notional Profit 57,000

WIP Reserve 22,800

57,000 57,000

2 𝑃/𝐿 𝐴/𝑐: 𝑁𝑜𝑡𝑖𝑜𝑛𝑎𝑙 𝑃𝑟𝑜𝑓𝑖𝑡 ×

2

3×

𝐶𝑎𝑠ℎ 𝑅𝑒𝑐𝑒𝑖𝑣𝑒𝑑

𝑊𝑜𝑟𝑘 𝑐𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑; 57,000 ×

2

3×

3,51,000

3,90,000

Contract Costing 23

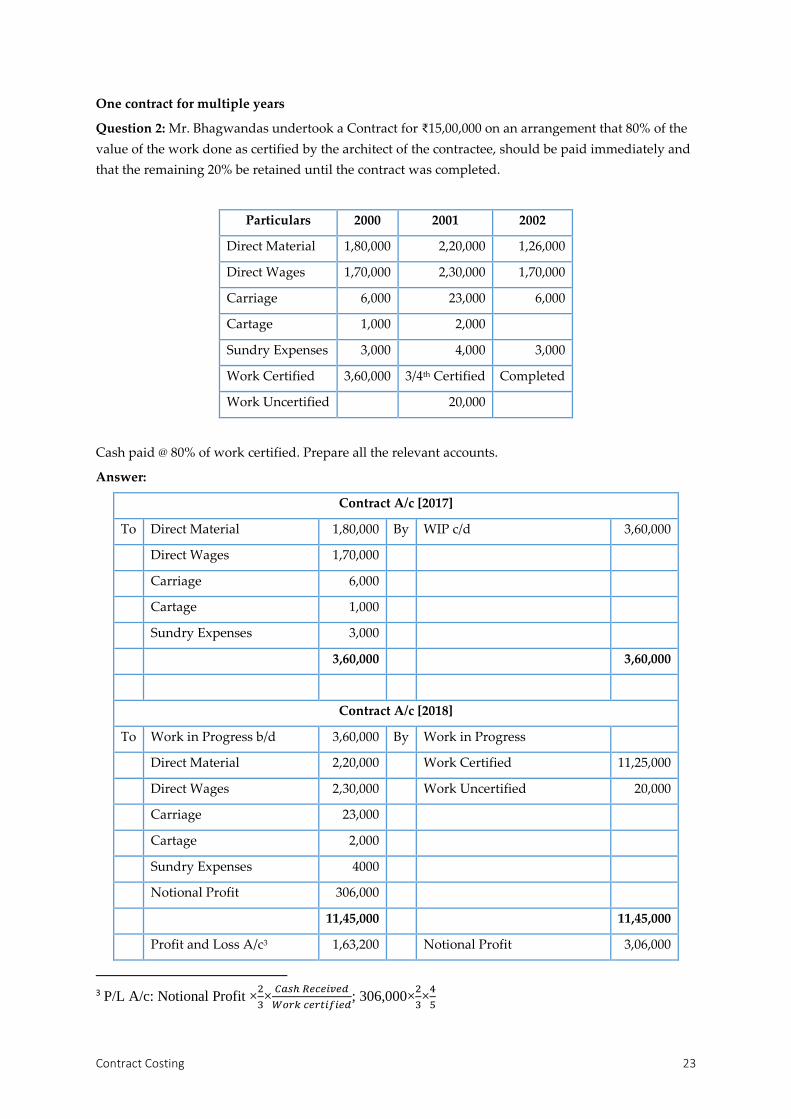

One contract for multiple years

Question 2: Mr. Bhagwandas undertook a Contract for ₹15,00,000 on an arrangement that 80% of the

value of the work done as certified by the architect of the contractee, should be paid immediately and

that the remaining 20% be retained until the contract was completed.

Particulars 2000 2001 2002

Direct Material 1,80,000 2,20,000 1,26,000

Direct Wages 1,70,000 2,30,000 1,70,000

Carriage 6,000 23,000 6,000

Cartage 1,000 2,000

Sundry Expenses 3,000 4,000 3,000

Work Certified 3,60,000 3/4th Certified Completed

Work Uncertified 20,000

Cash paid @ 80% of work certified. Prepare all the relevant accounts.

Answer:

Contract A/c [2017]

To Direct Material 1,80,000 By WIP c/d 3,60,000

Direct Wages 1,70,000

Carriage 6,000

Cartage 1,000

Sundry Expenses 3,000

3,60,000 3,60,000

Contract A/c [2018]

To Work in Progress b/d 3,60,000 By Work in Progress

Direct Material 2,20,000 Work Certified 11,25,000

Direct Wages 2,30,000 Work Uncertified 20,000

Carriage 23,000

Cartage 2,000

Sundry Expenses 4000

Notional Profit 306,000

11,45,000 11,45,000

Profit and Loss A/c3 1,63,200 Notional Profit 3,06,000

3 P/L A/c: Notional Profit ×

2

3×

𝐶𝑎𝑠ℎ 𝑅𝑒𝑐𝑒𝑖𝑣𝑒𝑑

𝑊𝑜𝑟𝑘 𝑐𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑; 306,000×

2

3×

4

5

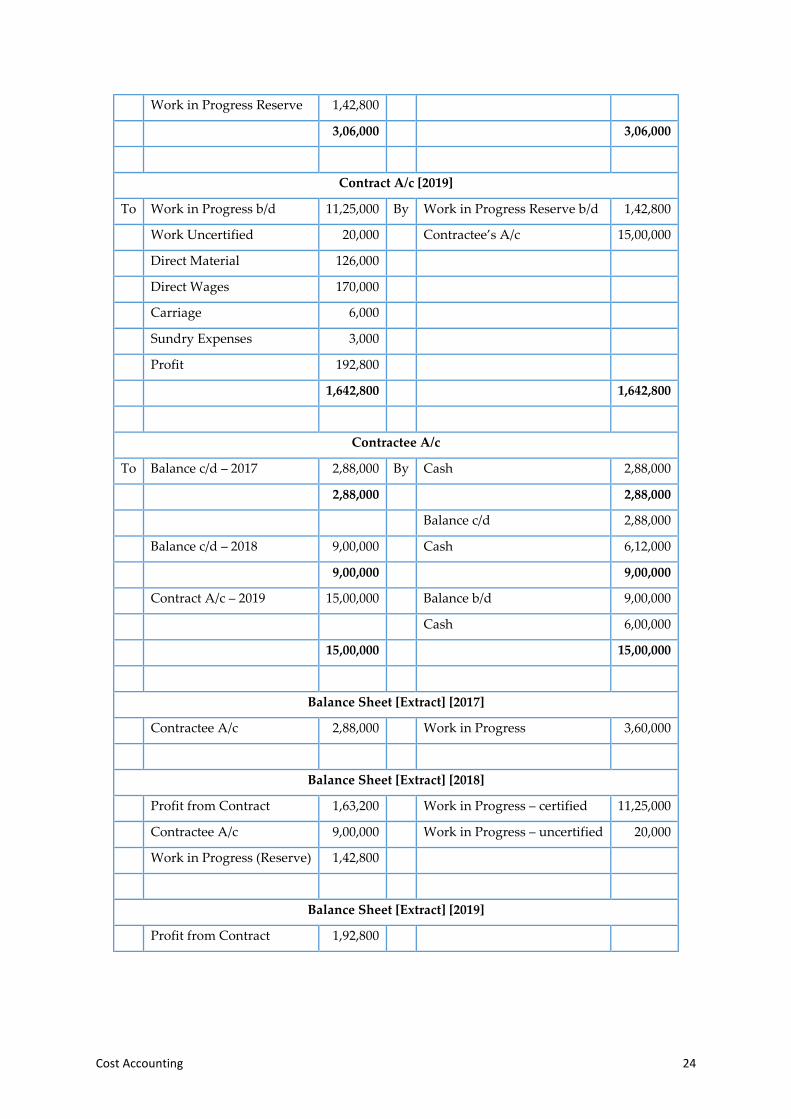

Cost Accounting 24

Work in Progress Reserve 1,42,800

3,06,000 3,06,000

Contract A/c [2019]

To Work in Progress b/d 11,25,000 By Work in Progress Reserve b/d 1,42,800

Work Uncertified 20,000 Contractee’s A/c 15,00,000

Direct Material 126,000

Direct Wages 170,000

Carriage 6,000

Sundry Expenses 3,000

Profit 192,800

1,642,800 1,642,800

Contractee A/c

To Balance c/d – 2017 2,88,000 By Cash 2,88,000

2,88,000 2,88,000

Balance c/d 2,88,000

Balance c/d – 2018 9,00,000 Cash 6,12,000

9,00,000 9,00,000

Contract A/c – 2019 15,00,000 Balance b/d 9,00,000

Cash 6,00,000

15,00,000 15,00,000

Balance Sheet [Extract] [2017]

Contractee A/c 2,88,000 Work in Progress 3,60,000

Balance Sheet [Extract] [2018]

Profit from Contract 1,63,200 Work in Progress – certified 11,25,000

Contractee A/c 9,00,000 Work in Progress – uncertified 20,000

Work in Progress (Reserve) 1,42,800

Balance Sheet [Extract] [2019]

Profit from Contract 1,92,800

Contract Costing 25

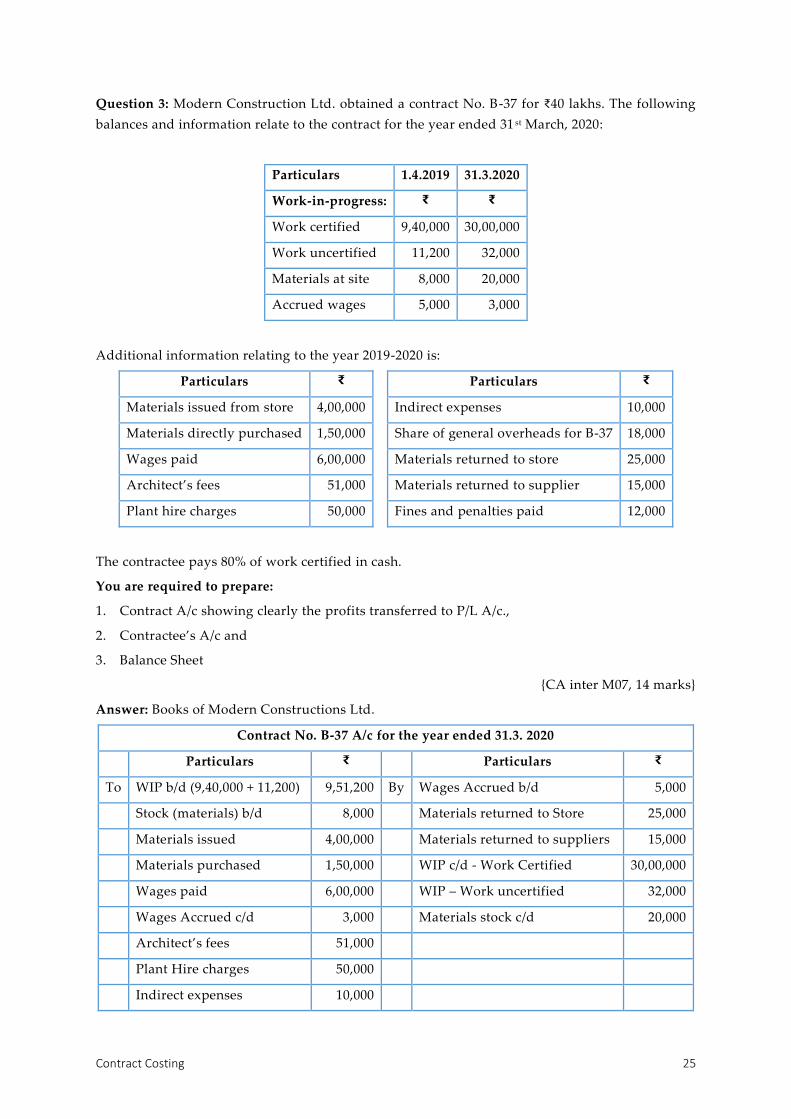

Question 3: Modern Construction Ltd. obtained a contract No. B-37 for ₹40 lakhs. The following

balances and information relate to the contract for the year ended 31 st March, 2020:

Particulars 1.4.2019 31.3.2020

Work-in-progress: ₹ ₹

Work certified 9,40,000 30,00,000

Work uncertified 11,200 32,000

Materials at site 8,000 20,000

Accrued wages 5,000 3,000

Additional information relating to the year 2019-2020 is:

Particulars ₹ Particulars ₹

Materials issued from store 4,00,000 Indirect expenses 10,000

Materials directly purchased 1,50,000 Share of general overheads for B-37 18,000

Wages paid 6,00,000 Materials returned to store 25,000

Architect’s fees 51,000 Materials returned to supplier 15,000

Plant hire charges 50,000 Fines and penalties paid 12,000

The contractee pays 80% of work certified in cash.

You are required to prepare:

1. Contract A/c showing clearly the profits transferred to P/L A/c.,

2. Contractee’s A/c and

3. Balance Sheet

{CA inter M07, 14 marks}

Answer: Books of Modern Constructions Ltd.

Contract No. B-37 A/c for the year ended 31.3. 2020

Particulars ₹ Particulars ₹

To WIP b/d (9,40,000 + 11,200) 9,51,200 By Wages Accrued b/d 5,000

Stock (materials) b/d 8,000 Materials returned to Store 25,000

Materials issued 4,00,000 Materials returned to suppliers 15,000

Materials purchased 1,50,000 WIP c/d - Work Certified 30,00,000

Wages paid 6,00,000 WIP – Work uncertified 32,000

Wages Accrued c/d 3,000 Materials stock c/d 20,000

Architect’s fees 51,000

Plant Hire charges 50,000

Indirect expenses 10,000

Cost Accounting 26

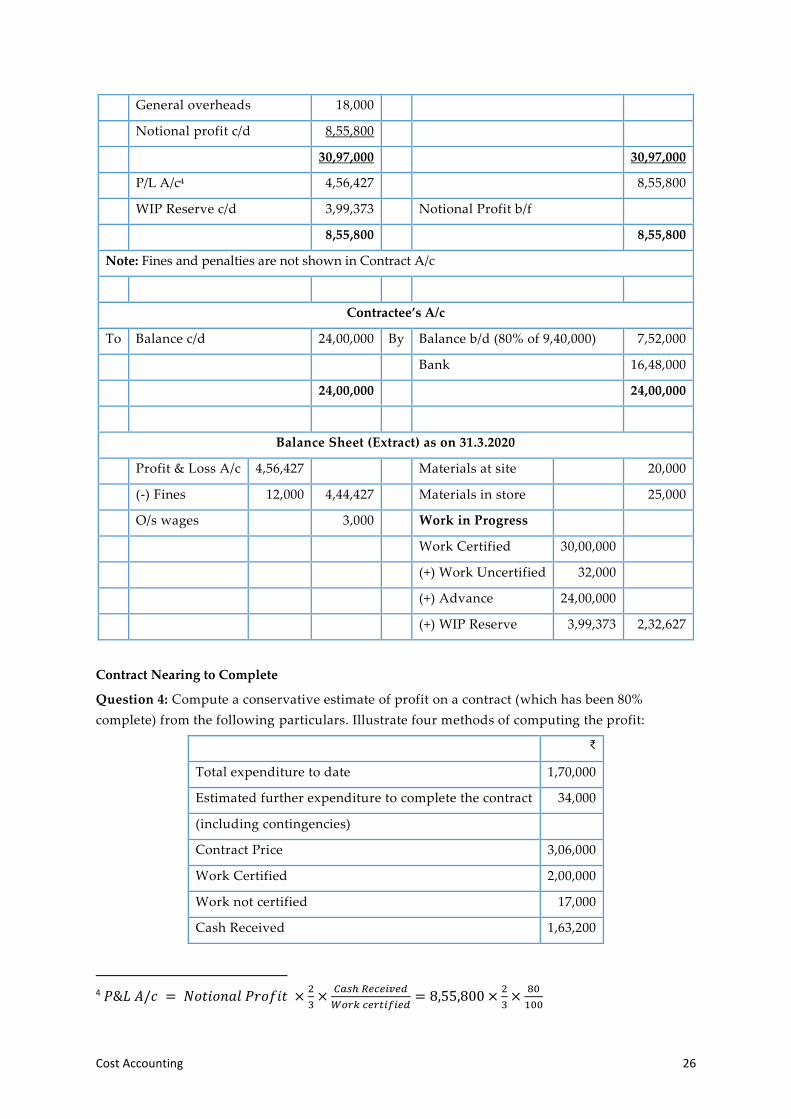

General overheads 18,000

Notional profit c/d 8,55,800

30,97,000 30,97,000

P/L A/c4 4,56,427 8,55,800

WIP Reserve c/d 3,99,373 Notional Profit b/f

8,55,800 8,55,800

Note: Fines and penalties are not shown in Contract A/c

Contractee’s A/c

To Balance c/d 24,00,000 By Balance b/d (80% of 9,40,000) 7,52,000

Bank 16,48,000

24,00,000 24,00,000

Balance Sheet (Extract) as on 31.3.2020

Profit & Loss A/c 4,56,427 Materials at site 20,000

(-) Fines 12,000 4,44,427 Materials in store 25,000

O/s wages 3,000 Work in Progress

Work Certified 30,00,000

(+) Work Uncertified 32,000

(+) Advance 24,00,000

(+) WIP Reserve 3,99,373 2,32,627

Contract Nearing to Complete

Question 4: Compute a conservative estimate of profit on a contract (which has been 80%

complete) from the following particulars. Illustrate four methods of computing the profit:

₹

Total expenditure to date 1,70,000

Estimated further expenditure to complete the contract 34,000

(including contingencies)

Contract Price 3,06,000

Work Certified 2,00,000

Work not certified 17,000

Cash Received 1,63,200

4 𝑃&𝐿 𝐴/𝑐 = 𝑁𝑜𝑡𝑖𝑜𝑛𝑎𝑙 𝑃𝑟𝑜𝑓𝑖𝑡 ×

2

3×

𝐶𝑎𝑠ℎ 𝑅𝑒𝑐𝑒𝑖𝑣𝑒𝑑

𝑊𝑜𝑟𝑘 𝑐𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑= 8,55,800 ×

2

3×

80

100

Contract Costing 27

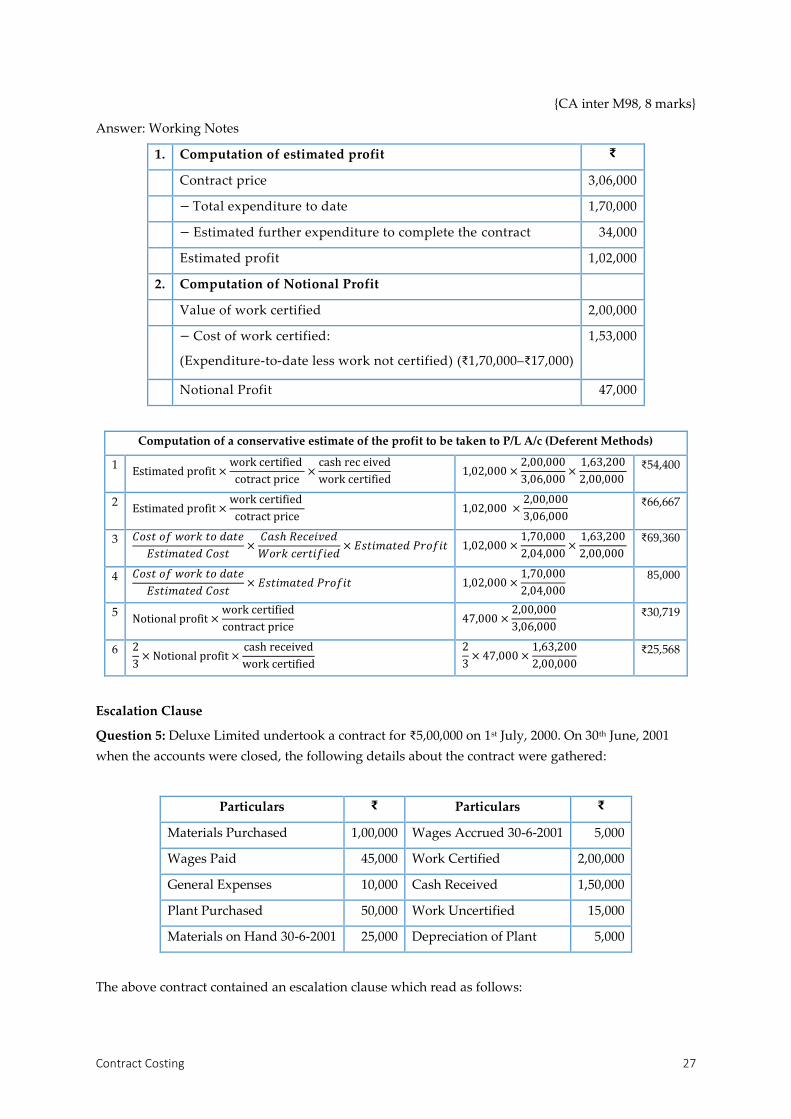

{CA inter M98, 8 marks}

Answer: Working Notes

1. Computation of estimated profit ₹

Contract price 3,06,000

− Total expenditure to date 1,70,000

− Estimated further expenditure to complete the contract 34,000

Estimated profit 1,02,000

2. Computation of Notional Profit

Value of work certified 2,00,000

− Cost of work certified:

(Expenditure-to-date less work not certified) (₹1,70,000–₹17,000)

1,53,000

Notional Profit 47,000

Computation of a conservative estimate of the profit to be taken to P/L A/c (Deferent Methods)

1 Estimated profit ×

work certified

cotract price×

cash rec eived

work certified 1,02,000 ×

2,00,000

3,06,000×

1,63,200

2,00,000

₹54,400

2 Estimated profit ×

work certified

cotract price 1,02,000 ×

2,00,000

3,06,000

₹66,667

3 𝐶𝑜𝑠𝑡 𝑜𝑓 𝑤𝑜𝑟𝑘 𝑡𝑜 𝑑𝑎𝑡𝑒

𝐸𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝐶𝑜𝑠𝑡×

𝐶𝑎𝑠ℎ 𝑅𝑒𝑐𝑒𝑖𝑣𝑒𝑑

𝑊𝑜𝑟𝑘 𝑐𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑× 𝐸𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝑃𝑟𝑜𝑓𝑖𝑡 1,02,000 ×

1,70,000

2,04,000×

1,63,200

2,00,000

₹69,360

4 𝐶𝑜𝑠𝑡 𝑜𝑓 𝑤𝑜𝑟𝑘 𝑡𝑜 𝑑𝑎𝑡𝑒

𝐸𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝐶𝑜𝑠𝑡× 𝐸𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝑃𝑟𝑜𝑓𝑖𝑡 1,02,000 ×

1,70,000

2,04,000

85,000

5 Notional profit ×

work certified

contract price 47,000 ×

2,00,000

3,06,000

₹30,719

6 2

3× Notional profit ×

cash received

work certified

2

3× 47,000 ×

1,63,200

2,00,000

₹25,568

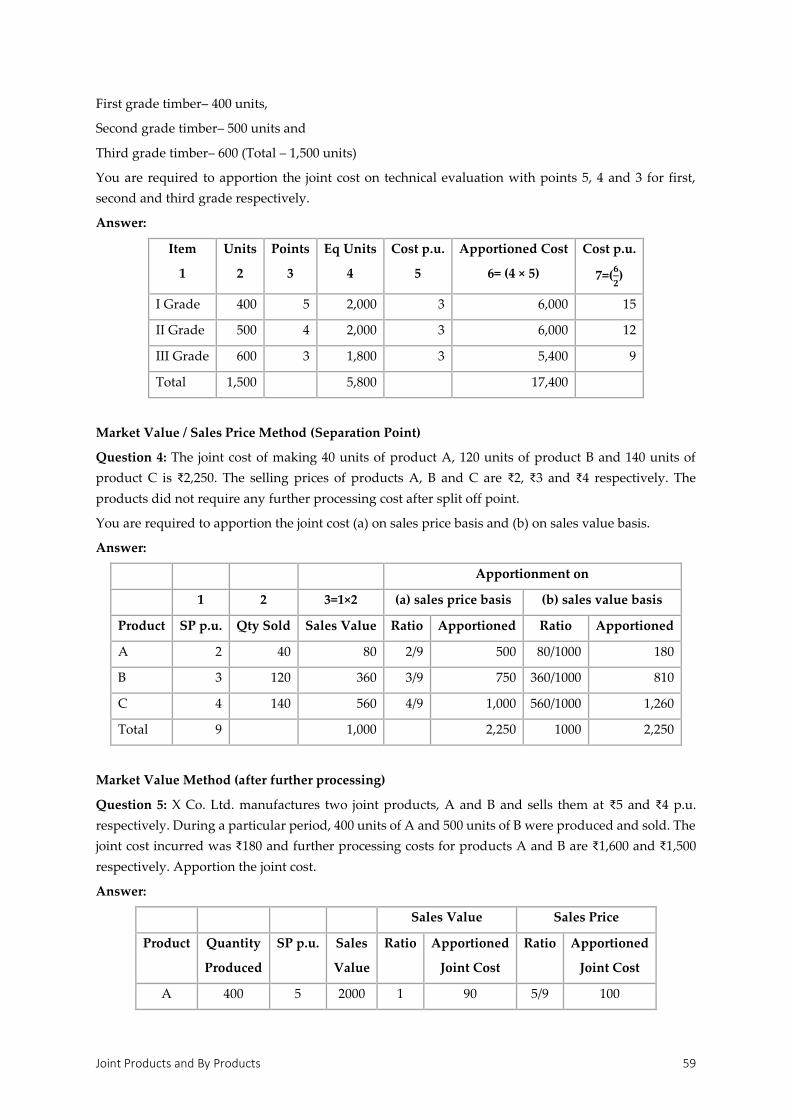

Escalation Clause

Question 5: Deluxe Limited undertook a contract for ₹5,00,000 on 1st July, 2000. On 30th June, 2001

when the accounts were closed, the following details about the contract were gathered:

Particulars ₹ Particulars ₹

Materials Purchased 1,00,000 Wages Accrued 30-6-2001 5,000

Wages Paid 45,000 Work Certified 2,00,000

General Expenses 10,000 Cash Received 1,50,000

Plant Purchased 50,000 Work Uncertified 15,000

Materials on Hand 30-6-2001 25,000 Depreciation of Plant 5,000

The above contract contained an escalation clause which read as follows:

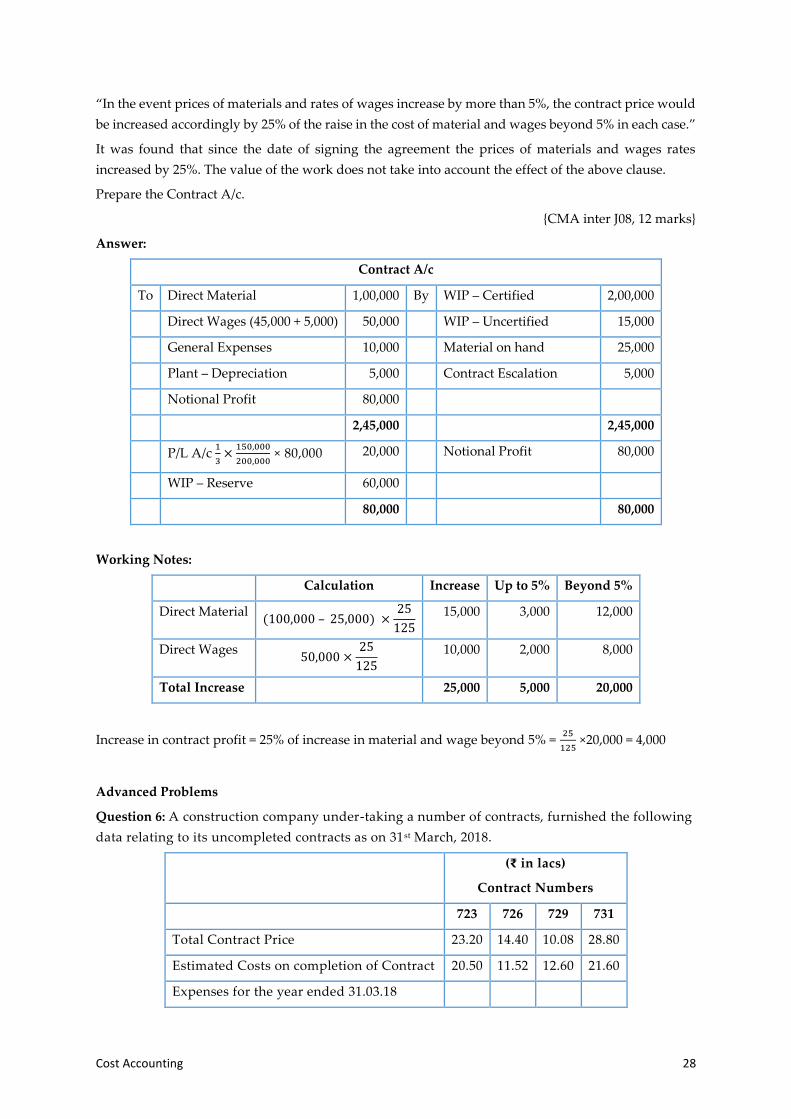

Cost Accounting 28

“In the event prices of materials and rates of wages increase by more than 5%, the contract price would

be increased accordingly by 25% of the raise in the cost of material and wages beyond 5% in each case.”

It was found that since the date of signing the agreement the prices of materials and wages rates

increased by 25%. The value of the work does not take into account the effect of the above clause.

Prepare the Contract A/c.

{CMA inter J08, 12 marks}

Answer:

Contract A/c

To Direct Material 1,00,000 By WIP – Certified 2,00,000

Direct Wages (45,000 + 5,000) 50,000 WIP – Uncertified 15,000

General Expenses 10,000 Material on hand 25,000

Plant – Depreciation 5,000 Contract Escalation 5,000

Notional Profit 80,000

2,45,000 2,45,000

P/L A/c 1

3×

150,000

200,000 × 80,000 20,000 Notional Profit 80,000

WIP – Reserve 60,000

80,000 80,000

Working Notes:

Calculation Increase Up to 5% Beyond 5%

Direct Material (100,000 – 25,000) ×

25

125

15,000 3,000 12,000

Direct Wages 50,000 ×

25

125

10,000 2,000 8,000

Total Increase 25,000 5,000 20,000

Increase in contract profit = 25% of increase in material and wage beyond 5% = 25

125 ×20,000 = 4,000

Advanced Problems

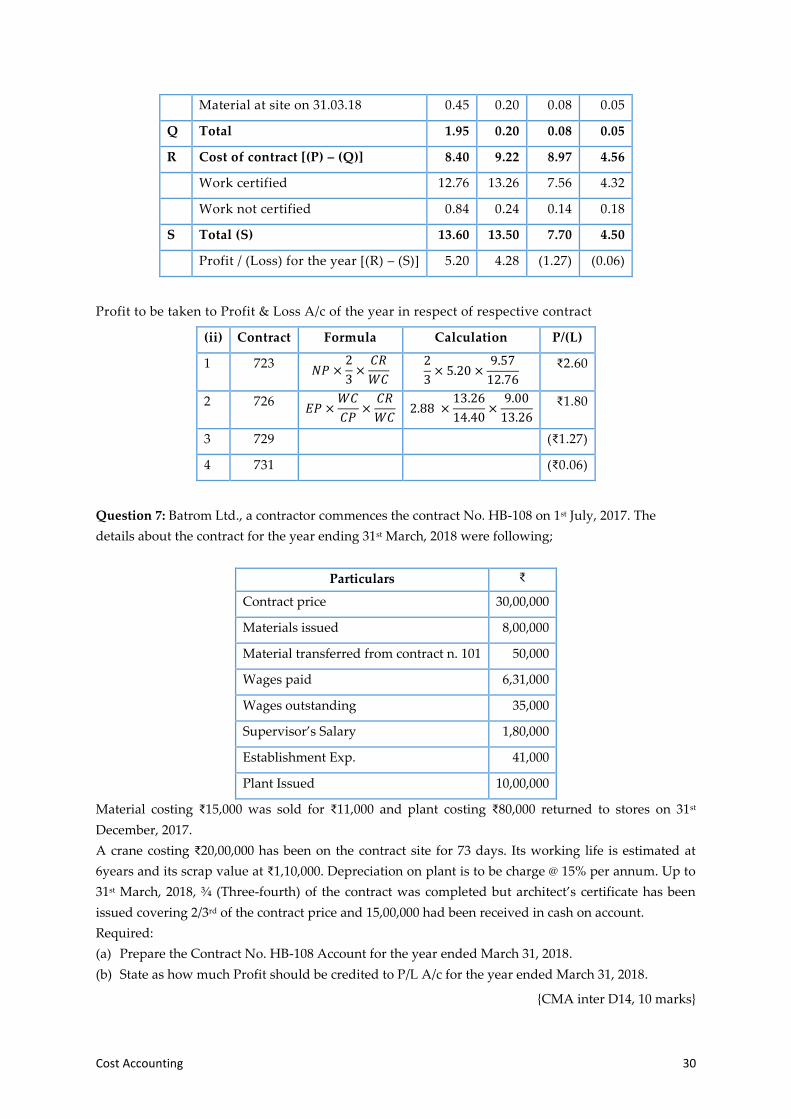

Question 6: A construction company under-taking a number of contracts, furnished the following

data relating to its uncompleted contracts as on 31st March, 2018.

(₹ in lacs)

Contract Numbers

723 726 729 731

Total Contract Price 23.20 14.40 10.08 28.80

Estimated Costs on completion of Contract 20.50 11.52 12.60 21.60

Expenses for the year ended 31.03.18

Contract Costing 29

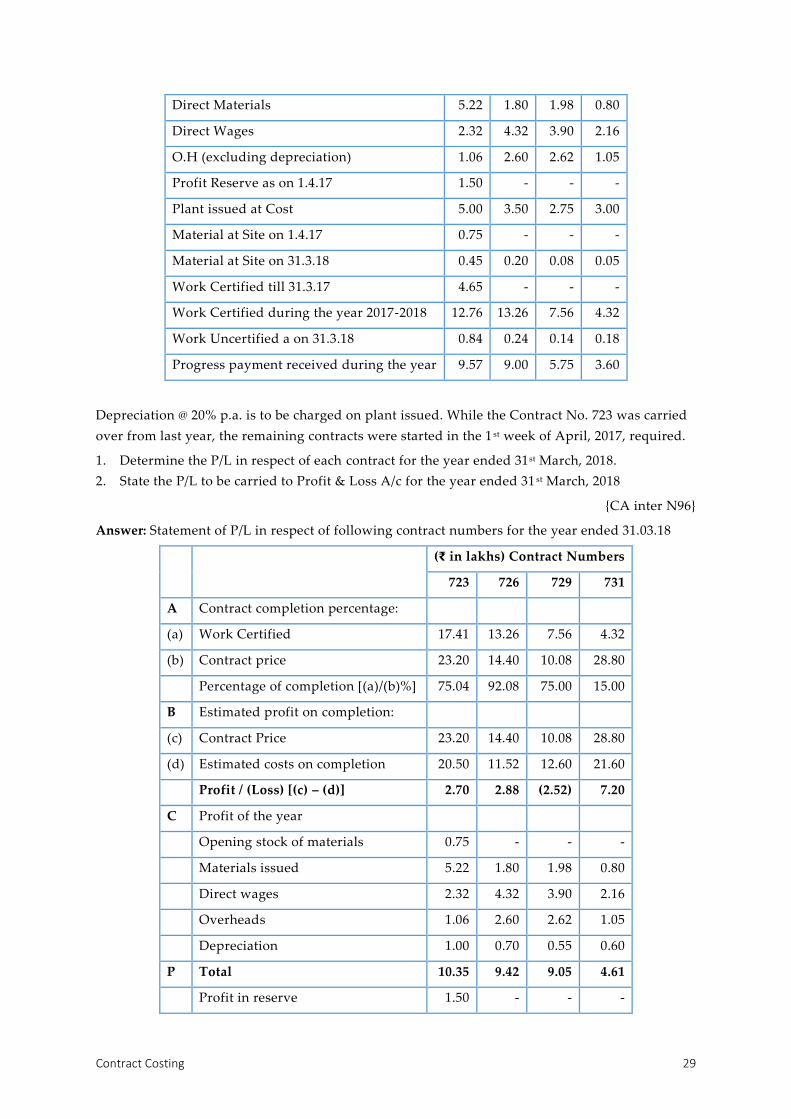

Direct Materials 5.22 1.80 1.98 0.80

Direct Wages 2.32 4.32 3.90 2.16

O.H (excluding depreciation) 1.06 2.60 2.62 1.05

Profit Reserve as on 1.4.17 1.50 - - -

Plant issued at Cost 5.00 3.50 2.75 3.00

Material at Site on 1.4.17 0.75 - - -

Material at Site on 31.3.18 0.45 0.20 0.08 0.05

Work Certified till 31.3.17 4.65 - - -

Work Certified during the year 2017-2018 12.76 13.26 7.56 4.32

Work Uncertified a on 31.3.18 0.84 0.24 0.14 0.18

Progress payment received during the year 9.57 9.00 5.75 3.60

Depreciation @ 20% p.a. is to be charged on plant issued. While the Contract No. 723 was carried

over from last year, the remaining contracts were started in the 1 st week of April, 2017, required.

1. Determine the P/L in respect of each contract for the year ended 31st March, 2018.

2. State the P/L to be carried to Profit & Loss A/c for the year ended 31 st March, 2018

{CA inter N96}

Answer: Statement of P/L in respect of following contract numbers for the year ended 31.03.18

(₹ in lakhs) Contract Numbers

723 726 729 731

A Contract completion percentage:

(a) Work Certified 17.41 13.26 7.56 4.32

(b) Contract price 23.20 14.40 10.08 28.80

Percentage of completion [(a)/(b)%] 75.04 92.08 75.00 15.00

B Estimated profit on completion:

(c) Contract Price 23.20 14.40 10.08 28.80

(d) Estimated costs on completion 20.50 11.52 12.60 21.60

Profit / (Loss) [(c) – (d)] 2.70 2.88 (2.52) 7.20

C Profit of the year

Opening stock of materials 0.75 - - -

Materials issued 5.22 1.80 1.98 0.80

Direct wages 2.32 4.32 3.90 2.16

Overheads 1.06 2.60 2.62 1.05

Depreciation 1.00 0.70 0.55 0.60

P Total 10.35 9.42 9.05 4.61

Profit in reserve 1.50 - - -

Cost Accounting 30

Material at site on 31.03.18 0.45 0.20 0.08 0.05

Q Total 1.95 0.20 0.08 0.05

R Cost of contract [(P) – (Q)] 8.40 9.22 8.97 4.56

Work certified 12.76 13.26 7.56 4.32

Work not certified 0.84 0.24 0.14 0.18

S Total (S) 13.60 13.50 7.70 4.50

Profit / (Loss) for the year [(R) – (S)] 5.20 4.28 (1.27) (0.06)

Profit to be taken to Profit & Loss A/c of the year in respect of respective contract

(ii) Contract Formula Calculation P/(L)

1 723 𝑁𝑃 ×

2

3×

𝐶𝑅

𝑊𝐶

2

3× 5.20 ×

9.57

12.76

₹2.60

2 726 𝐸𝑃 ×

𝑊𝐶

𝐶𝑃×

𝐶𝑅

𝑊𝐶 2.88 ×

13.26

14.40×

9.00

13.26

₹1.80

3 729 (₹1.27)

4 731 (₹0.06)

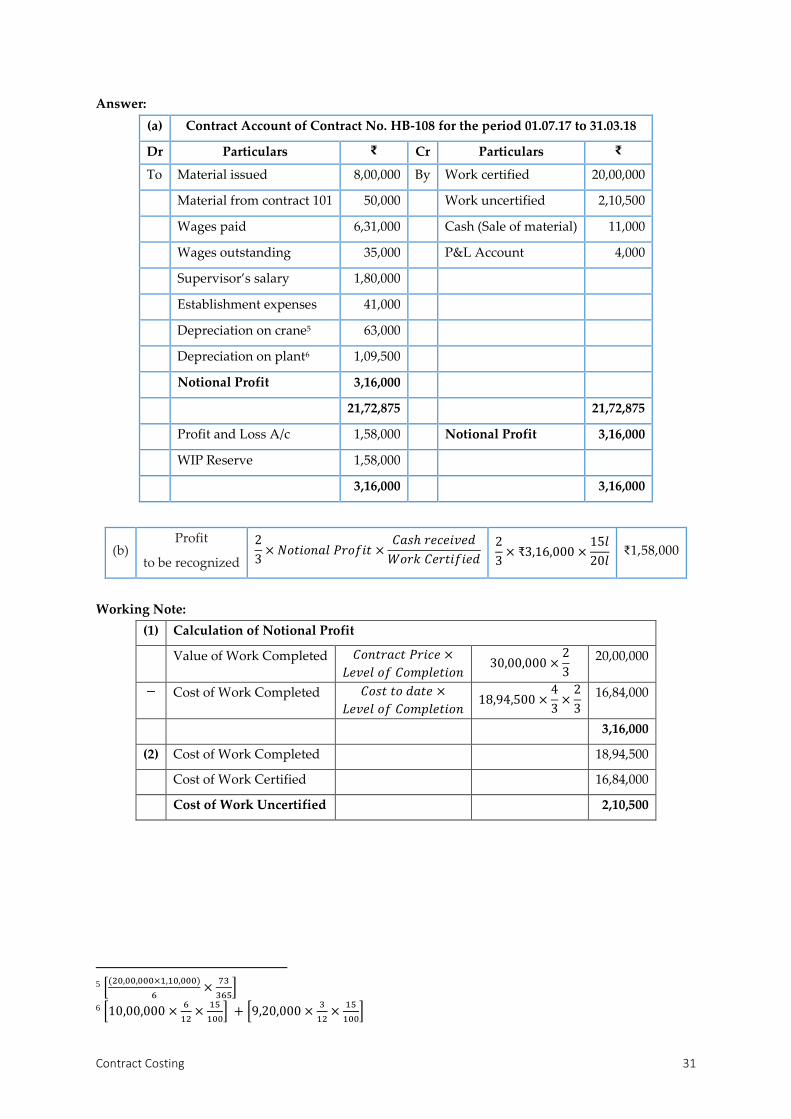

Question 7: Batrom Ltd., a contractor commences the contract No. HB-108 on 1st July, 2017. The

details about the contract for the year ending 31st March, 2018 were following;

Particulars ₹

Contract price 30,00,000

Materials issued 8,00,000

Material transferred from contract n. 101 50,000

Wages paid 6,31,000

Wages outstanding 35,000

Supervisor’s Salary 1,80,000

Establishment Exp. 41,000

Plant Issued 10,00,000

Material costing ₹15,000 was sold for ₹11,000 and plant costing ₹80,000 returned to stores on 31st

December, 2017.

A crane costing ₹20,00,000 has been on the contract site for 73 days. Its working life is estimated at

6years and its scrap value at ₹1,10,000. Depreciation on plant is to be charge @ 15% per annum. Up to

31st March, 2018, ¾ (Three-fourth) of the contract was completed but architect’s certificate has been

issued covering 2/3rd of the contract price and 15,00,000 had been received in cash on account.

Required:

(a) Prepare the Contract No. HB-108 Account for the year ended March 31, 2018.

(b) State as how much Profit should be credited to P/L A/c for the year ended March 31, 2018.

{CMA inter D14, 10 marks}

Contract Costing 31

Answer:

(a) Contract Account of Contract No. HB-108 for the period 01.07.17 to 31.03.18

Dr Particulars ₹ Cr Particulars ₹

To Material issued 8,00,000 By Work certified 20,00,000

Material from contract 101 50,000 Work uncertified 2,10,500

Wages paid 6,31,000 Cash (Sale of material) 11,000

Wages outstanding 35,000 P&L Account 4,000

Supervisor’s salary 1,80,000

Establishment expenses 41,000

Depreciation on crane5 63,000

Depreciation on plant6 1,09,500

Notional Profit 3,16,000

21,72,875 21,72,875

Profit and Loss A/c 1,58,000 Notional Profit 3,16,000

WIP Reserve 1,58,000

3,16,000 3,16,000

(b) Profit

to be recognized

2

3× 𝑁𝑜𝑡𝑖𝑜𝑛𝑎𝑙 𝑃𝑟𝑜𝑓𝑖𝑡 ×

𝐶𝑎𝑠ℎ 𝑟𝑒𝑐𝑒𝑖𝑣𝑒𝑑

𝑊𝑜𝑟𝑘 𝐶𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑

2

3× ₹3,16,000 ×

15𝑙

20𝑙 ₹1,58,000

Working Note:

(1) Calculation of Notional Profit

Value of Work Completed 𝐶𝑜𝑛𝑡𝑟𝑎𝑐𝑡 𝑃𝑟𝑖𝑐𝑒 ×

𝐿𝑒𝑣𝑒𝑙 𝑜𝑓 𝐶𝑜𝑚𝑝𝑙𝑒𝑡𝑖𝑜𝑛 30,00,000 ×

2

3

20,00,000

− Cost of Work Completed 𝐶𝑜𝑠𝑡 𝑡𝑜 𝑑𝑎𝑡𝑒 ×

𝐿𝑒𝑣𝑒𝑙 𝑜𝑓 𝐶𝑜𝑚𝑝𝑙𝑒𝑡𝑖𝑜𝑛 18,94,500 ×

4

3×

2

3

16,84,000

3,16,000

(2) Cost of Work Completed 18,94,500

Cost of Work Certified 16,84,000

Cost of Work Uncertified 2,10,500

5 [

(20,00,000×1,10,000)

6×

73

365]

6 [10,00,000 ×6

12×

15

100] + [9,20,000 ×

3

12×

15

100]

Cost Accounting 32

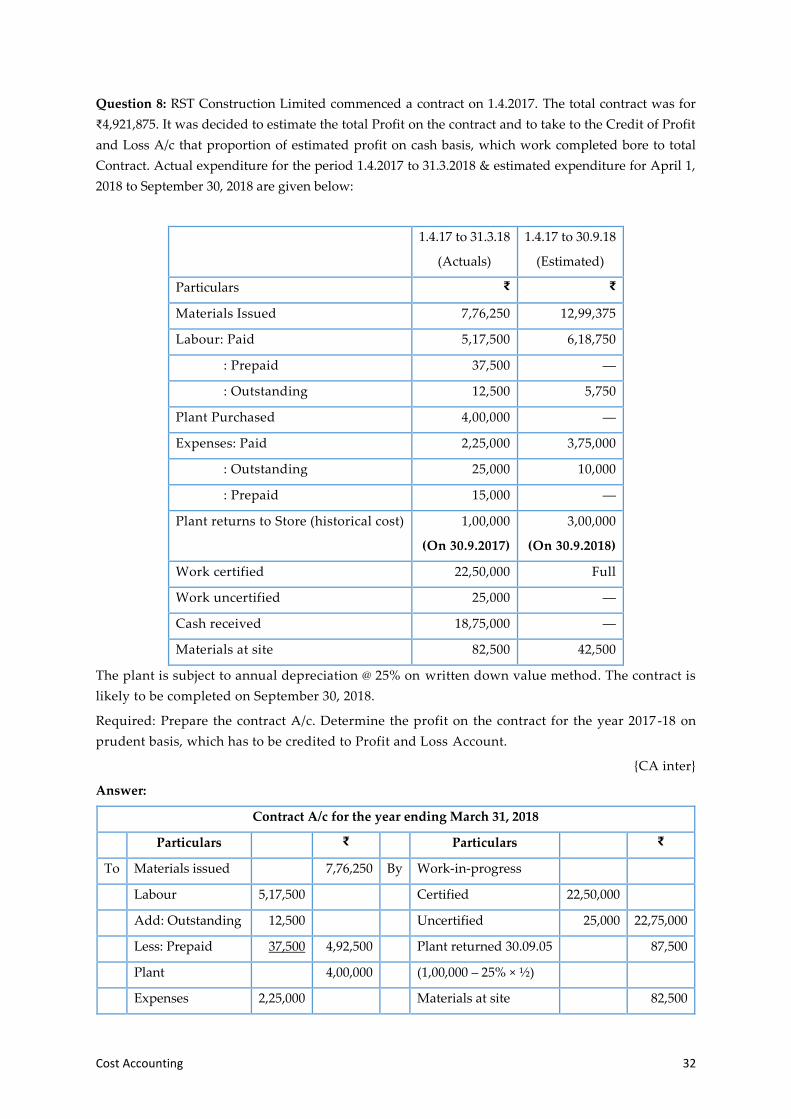

Question 8: RST Construction Limited commenced a contract on 1.4.2017. The total contract was for

₹4,921,875. It was decided to estimate the total Profit on the contract and to take to the Credit of Profit

and Loss A/c that proportion of estimated profit on cash basis, which work completed bore to total

Contract. Actual expenditure for the period 1.4.2017 to 31.3.2018 & estimated expenditure for April 1,

2018 to September 30, 2018 are given below:

1.4.17 to 31.3.18

(Actuals)

1.4.17 to 30.9.18

(Estimated)

Particulars ₹ ₹

Materials Issued 7,76,250 12,99,375

Labour: Paid 5,17,500 6,18,750

: Prepaid 37,500 ―

: Outstanding 12,500 5,750

Plant Purchased 4,00,000 ―

Expenses: Paid 2,25,000 3,75,000

: Outstanding 25,000 10,000

: Prepaid 15,000 ―

Plant returns to Store (historical cost) 1,00,000

(On 30.9.2017)

3,00,000

(On 30.9.2018)

Work certified 22,50,000 Full

Work uncertified 25,000 ―

Cash received 18,75,000 ―

Materials at site 82,500 42,500

The plant is subject to annual depreciation @ 25% on written down value method. The contract is

likely to be completed on September 30, 2018.

Required: Prepare the contract A/c. Determine the profit on the contract for the year 2017 -18 on

prudent basis, which has to be credited to Profit and Loss Account.

{CA inter}

Answer:

Contract A/c for the year ending March 31, 2018

Particulars ₹ Particulars ₹

To Materials issued 7,76,250 By Work-in-progress

Labour 5,17,500 Certified 22,50,000

Add: Outstanding 12,500 Uncertified 25,000 22,75,000

Less: Prepaid 37,500 4,92,500 Plant returned 30.09.05 87,500

Plant 4,00,000 (1,00,000 – 25% × ½)

Expenses 2,25,000 Materials at site 82,500

Contract Costing 33

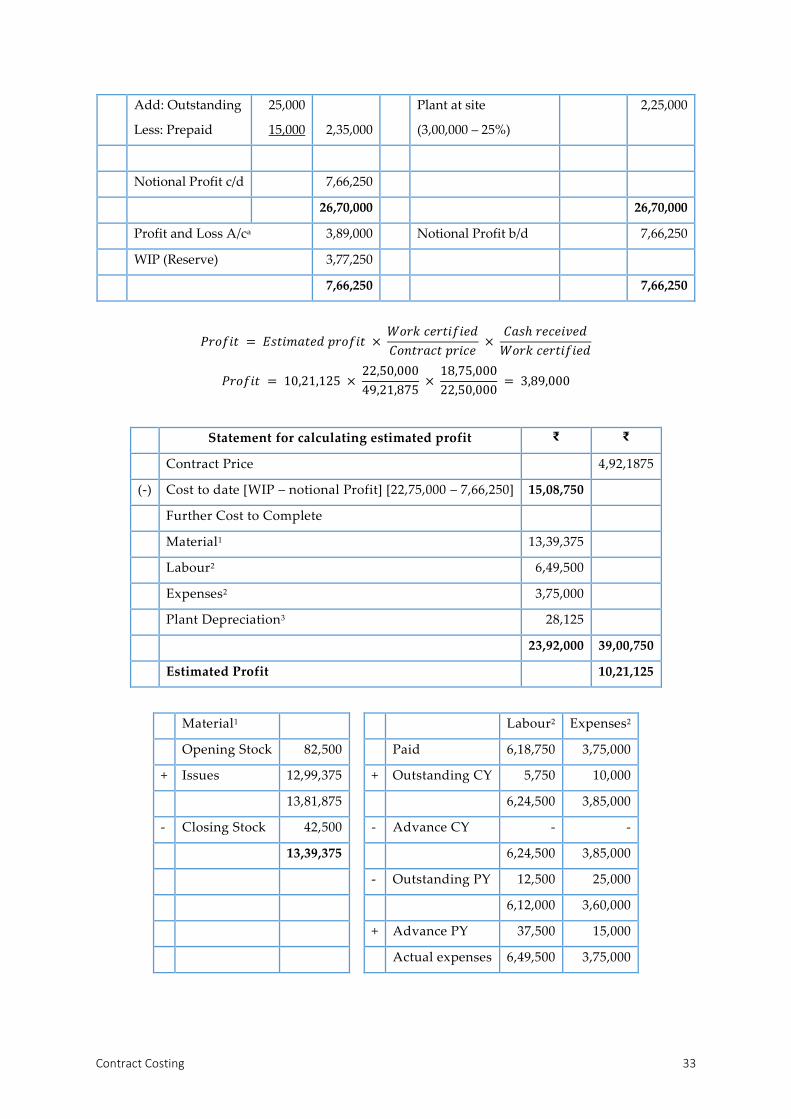

Add: Outstanding

Less: Prepaid

25,000

15,000

2,35,000

Plant at site

(3,00,000 – 25%)

2,25,000

Notional Profit c/d 7,66,250

26,70,000 26,70,000

Profit and Loss A/ca 3,89,000 Notional Profit b/d 7,66,250

WIP (Reserve) 3,77,250

7,66,250 7,66,250

𝑃𝑟𝑜𝑓𝑖𝑡 = 𝐸𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝑝𝑟𝑜𝑓𝑖𝑡 × 𝑊𝑜𝑟𝑘 𝑐𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑

𝐶𝑜𝑛𝑡𝑟𝑎𝑐𝑡 𝑝𝑟𝑖𝑐𝑒 ×

𝐶𝑎𝑠ℎ 𝑟𝑒𝑐𝑒𝑖𝑣𝑒𝑑

𝑊𝑜𝑟𝑘 𝑐𝑒𝑟𝑡𝑖𝑓𝑖𝑒𝑑

𝑃𝑟𝑜𝑓𝑖𝑡 = 10,21,125 × 22,50,000

49,21,875 ×

18,75,000

22,50,000 = 3,89,000

Statement for calculating estimated profit ₹ ₹

Contract Price 4,92,1875

(-) Cost to date [WIP – notional Profit] [22,75,000 – 7,66,250] 15,08,750

Further Cost to Complete

Material1 13,39,375

Labour2 6,49,500

Expenses2 3,75,000

Plant Depreciation3 28,125

23,92,000 39,00,750

Estimated Profit 10,21,125

Material1 Labour2 Expenses2

Opening Stock 82,500 Paid 6,18,750 3,75,000

+ Issues 12,99,375 + Outstanding CY 5,750 10,000

13,81,875 6,24,500 3,85,000

- Closing Stock 42,500 - Advance CY - -

13,39,375 6,24,500 3,85,000

- Outstanding PY 12,500 25,000

6,12,000 3,60,000

+ Advance PY 37,500 15,000

Actual expenses 6,49,500 3,75,000

Cost Accounting 34

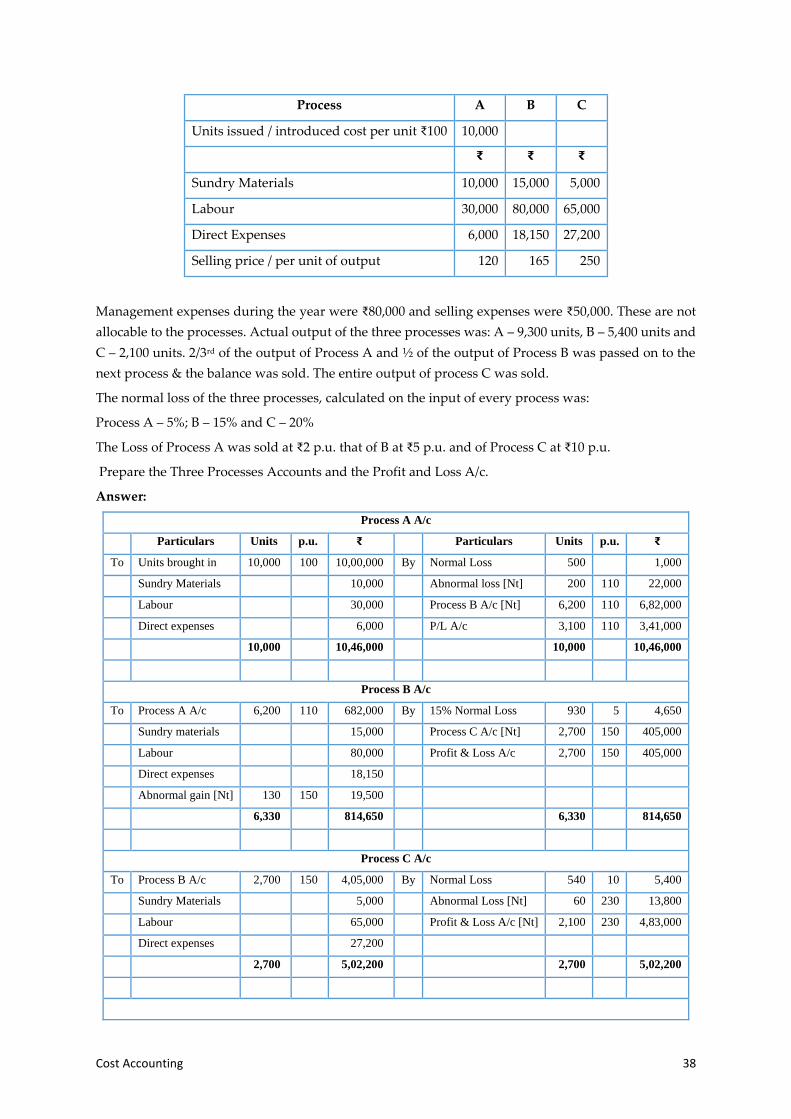

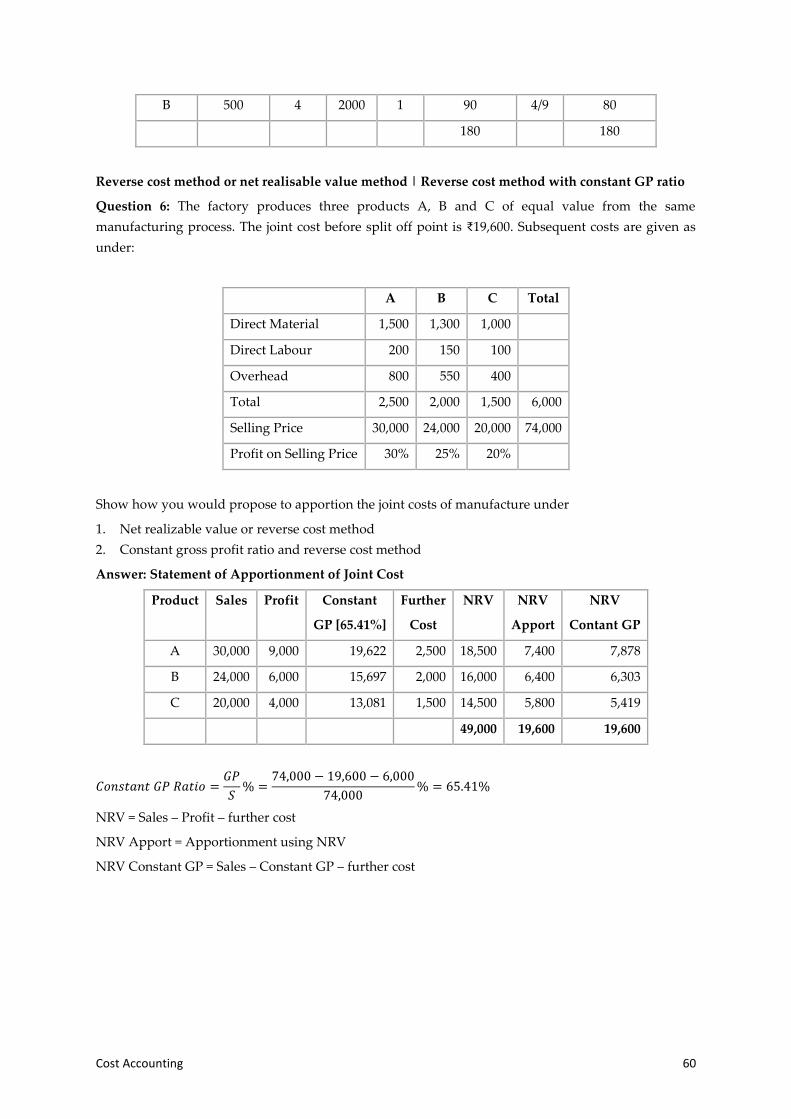

2.4 PROCESS COSTING

Process Costing: used in industries where the material has to pass through two or more processes for

being converted into a final product.

Operation Costing: It is the refinement of process costing. It is concerned with the determination of

the cost of each operation rather than the processes.

PRACTICAL PROBLEM TYPE

1. Basic problems (Normal Loss, Abnormal Loss (Gain))

2. Problems with stocks (Equivalent Products): FIFO | Average Price

3. Inter Process Profit

4. Operation Costing

PRACTICAL PROBLEM

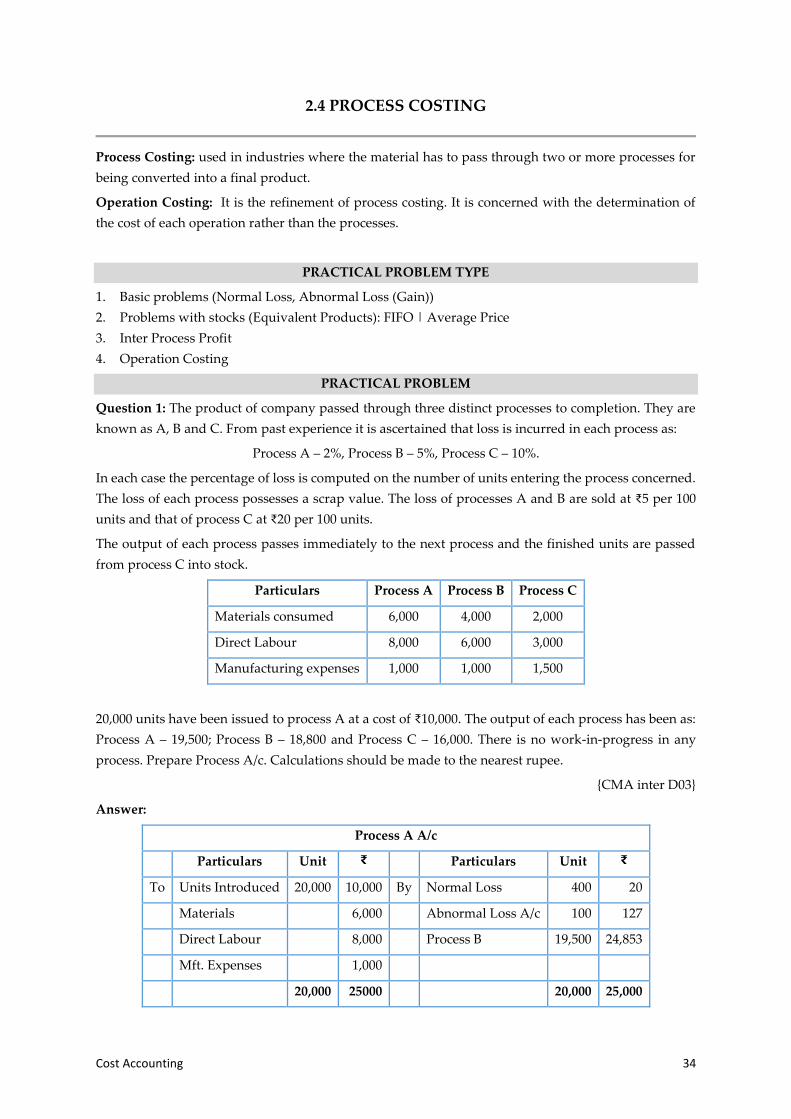

Question 1: The product of company passed through three distinct processes to completion. They are

known as A, B and C. From past experience it is ascertained that loss is incurred in each process as:

Process A – 2%, Process B – 5%, Process C – 10%.

In each case the percentage of loss is computed on the number of units entering the process concerned.

The loss of each process possesses a scrap value. The loss of processes A and B are sold at ₹5 per 100

units and that of process C at ₹20 per 100 units.

The output of each process passes immediately to the next process and the finished units are passed

from process C into stock.

Particulars Process A Process B Process C

Materials consumed 6,000 4,000 2,000

Direct Labour 8,000 6,000 3,000

Manufacturing expenses 1,000 1,000 1,500

20,000 units have been issued to process A at a cost of ₹10,000. The output of each process has been as:

Process A – 19,500; Process B – 18,800 and Process C – 16,000. There is no work-in-progress in any

process. Prepare Process A/c. Calculations should be made to the nearest rupee.

{CMA inter D03}

Answer:

Process A A/c

Particulars Unit ₹ Particulars Unit ₹

To Units Introduced 20,000 10,000 By Normal Loss 400 20

Materials 6,000 Abnormal Loss A/c 100 127

Direct Labour 8,000 Process B 19,500 24,853

Mft. Expenses 1,000

20,000 25000 20,000 25,000

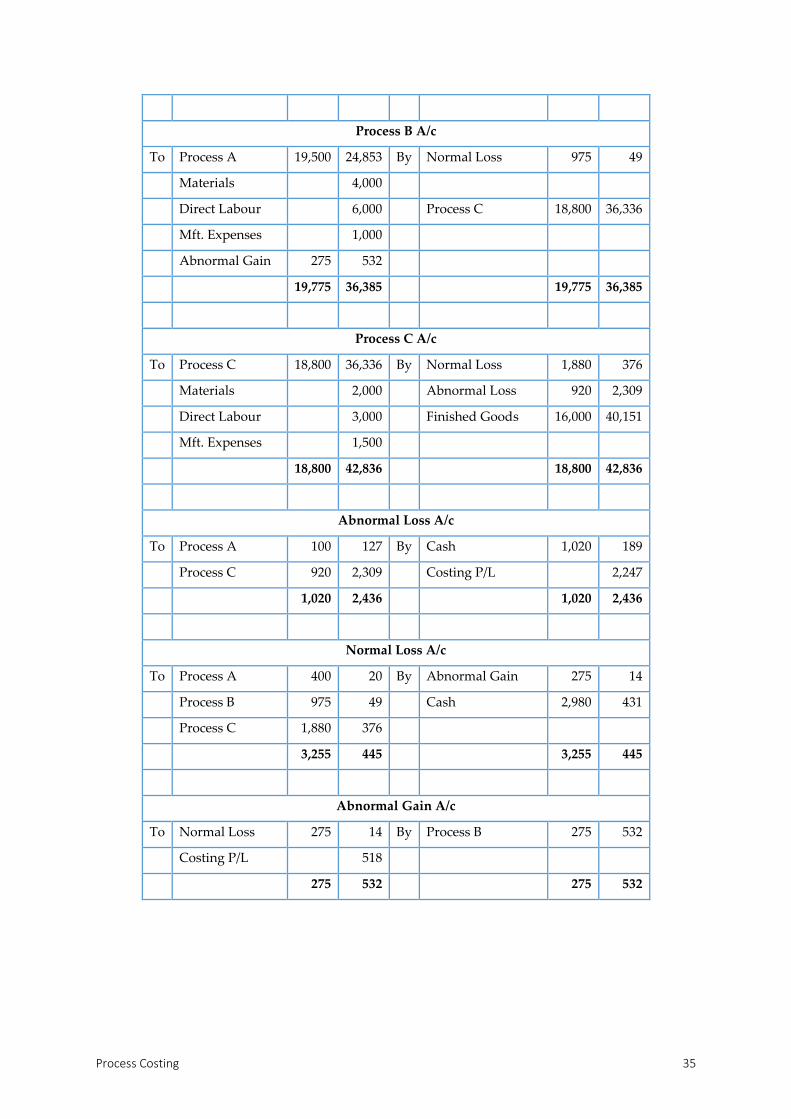

Process Costing 35

Process B A/c

To Process A 19,500 24,853 By Normal Loss 975 49

Materials 4,000

Direct Labour 6,000 Process C 18,800 36,336

Mft. Expenses 1,000

Abnormal Gain 275 532

19,775 36,385 19,775 36,385

Process C A/c

To Process C 18,800 36,336 By Normal Loss 1,880 376

Materials 2,000 Abnormal Loss 920 2,309

Direct Labour 3,000 Finished Goods 16,000 40,151

Mft. Expenses 1,500

18,800 42,836 18,800 42,836

Abnormal Loss A/c

To Process A 100 127 By Cash 1,020 189

Process C 920 2,309 Costing P/L 2,247

1,020 2,436 1,020 2,436

Normal Loss A/c

To Process A 400 20 By Abnormal Gain 275 14

Process B 975 49 Cash 2,980 431

Process C 1,880 376

3,255 445 3,255 445

Abnormal Gain A/c

To Normal Loss 275 14 By Process B 275 532

Costing P/L 518

275 532 275 532

Cost Accounting 36

Question 2: A product passes through three distinct processes I, II and III. The output of each process

is transferred to the next process and the output of process III is transferred to finished goods stock.

The normal wastage in each process and the realizable value of the same are given below:

Process Percentage of normal value

waste related to input

Realizable

per unit

I 5 ₹0.70

II 7 ₹0.80

III 10 ₹1.00

The details of cost data and output for a month are as follows:

Process

I II III

Material Consumed (₹) 1,20,000 40,000 40,000

Direct Labour Cost (₹) 80,000 60,000 60,000

Production expenses (₹) 40,000 40,000 28,000

Output (Units) 38,000 34,600 32,000

Process I was fed with 40,000 units of input costing ₹3,20,000. There were no opening and closing work-

in-progress. Prepare the process accounts for the month.

Answer:

Process I A/c

Particulars Units ₹ Particular Units ₹

To Raw material 40,000 3,20,000 By Normal loss 2,000 1,400

Direct Material 1,20,000 Process II a/c 38,000 5,58,600

Direct Labour 80,000

Production Exp. 40,000

40,000 5,60,000 40,000 5,60,000

Process II A/c

To Process I a/c 38,000 5,58,600 By Normal loss 2,660 2,128

Direct Material 40,000 Abnormal loss (WN1) 740 14,585

Direct Labour 60,000 Process III a/c 34,600 6,81,887

Production Exp. 40,000

38,000 6,98,600 38,000 6,98,600

Process Costing 37

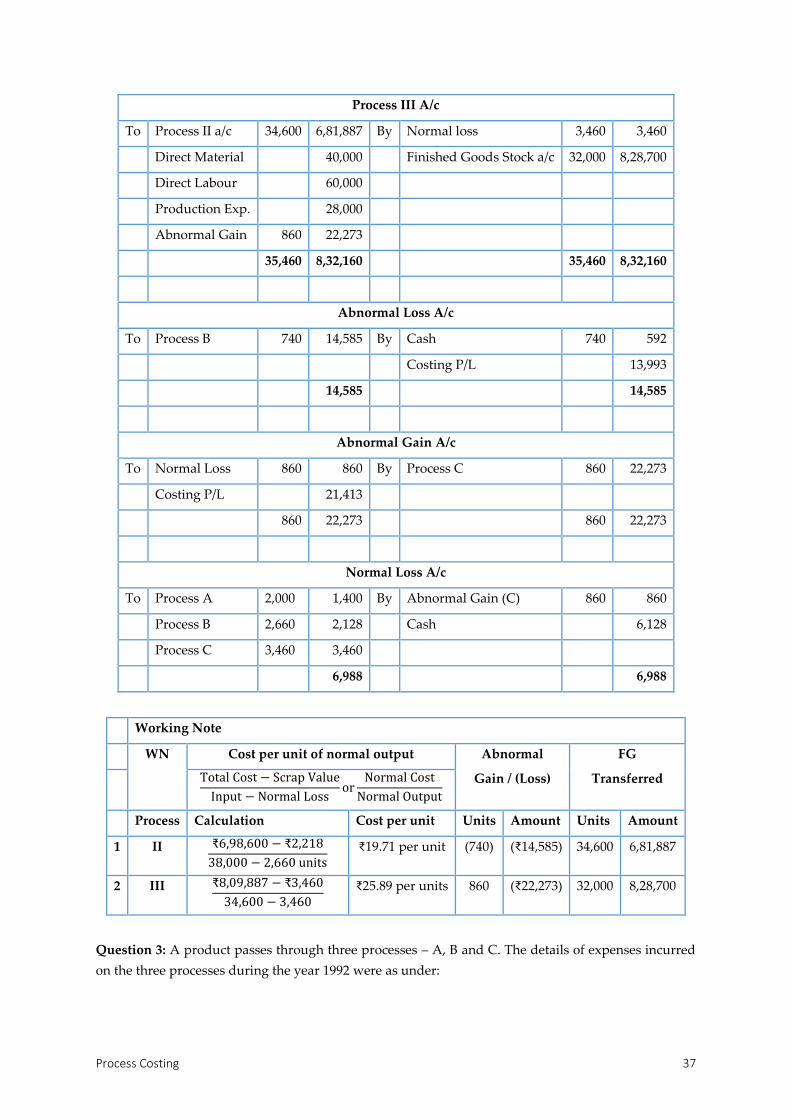

Process III A/c

To Process II a/c 34,600 6,81,887 By Normal loss 3,460 3,460

Direct Material 40,000 Finished Goods Stock a/c 32,000 8,28,700

Direct Labour 60,000

Production Exp. 28,000

Abnormal Gain 860 22,273

35,460 8,32,160 35,460 8,32,160

Abnormal Loss A/c

To Process B 740 14,585 By Cash 740 592

Costing P/L 13,993

14,585 14,585

Abnormal Gain A/c

To Normal Loss 860 860 By Process C 860 22,273

Costing P/L 21,413

860 22,273 860 22,273

Normal Loss A/c

To Process A 2,000 1,400 By Abnormal Gain (C) 860 860

Process B 2,660 2,128 Cash 6,128

Process C 3,460 3,460

6,988 6,988

Working Note

WN Cost per unit of normal output Abnormal

Gain / (Loss)

FG

Transferred Total Cost − Scrap Value

Input − Normal Lossor

Normal Cost

Normal Output

Process Calculation Cost per unit Units Amount Units Amount

1 II ₹6,98,600 − ₹2,218

38,000 − 2,660 units

₹19.71 per unit (740) (₹14,585) 34,600 6,81,887

2 III ₹8,09,887 − ₹3,460

34,600 − 3,460

₹25.89 per units 860 (₹22,273) 32,000 8,28,700

Question 3: A product passes through three processes – A, B and C. The details of expenses incurred

on the three processes during the year 1992 were as under:

Cost Accounting 38

Process A B C

Units issued / introduced cost per unit ₹100 10,000

₹ ₹ ₹

Sundry Materials 10,000 15,000 5,000

Labour 30,000 80,000 65,000

Direct Expenses 6,000 18,150 27,200

Selling price / per unit of output 120 165 250

Management expenses during the year were ₹80,000 and selling expenses were ₹50,000. These are not

allocable to the processes. Actual output of the three processes was: A – 9,300 units, B – 5,400 units and

C – 2,100 units. 2/3rd of the output of Process A and ½ of the output of Process B was passed on to the

next process & the balance was sold. The entire output of process C was sold.

The normal loss of the three processes, calculated on the input of every process was:

Process A – 5%; B – 15% and C – 20%

The Loss of Process A was sold at ₹2 p.u. that of B at ₹5 p.u. and of Process C at ₹10 p.u.

Prepare the Three Processes Accounts and the Profit and Loss A/c.

Answer:

Process A A/c

Particulars Units p.u. ₹ Particulars Units p.u. ₹

To Units brought in 10,000 100 10,00,000 By Normal Loss 500 1,000

Sundry Materials 10,000 Abnormal loss [Nt] 200 110 22,000

Labour 30,000 Process B A/c [Nt] 6,200 110 6,82,000

Direct expenses 6,000 P/L A/c 3,100 110 3,41,000

10,000 10,46,000 10,000 10,46,000

Process B A/c

To Process A A/c 6,200 110 682,000 By 15% Normal Loss 930 5 4,650

Sundry materials 15,000 Process C A/c [Nt] 2,700 150 405,000

Labour 80,000 Profit & Loss A/c 2,700 150 405,000

Direct expenses 18,150

Abnormal gain [Nt] 130 150 19,500

6,330 814,650 6,330 814,650

Process C A/c

To Process B A/c 2,700 150 4,05,000 By Normal Loss 540 10 5,400

Sundry Materials 5,000 Abnormal Loss [Nt] 60 230 13,800

Labour 65,000 Profit & Loss A/c [Nt] 2,100 230 4,83,000

Direct expenses 27,200

2,700 5,02,200 2,700 5,02,200

Process Costing 39

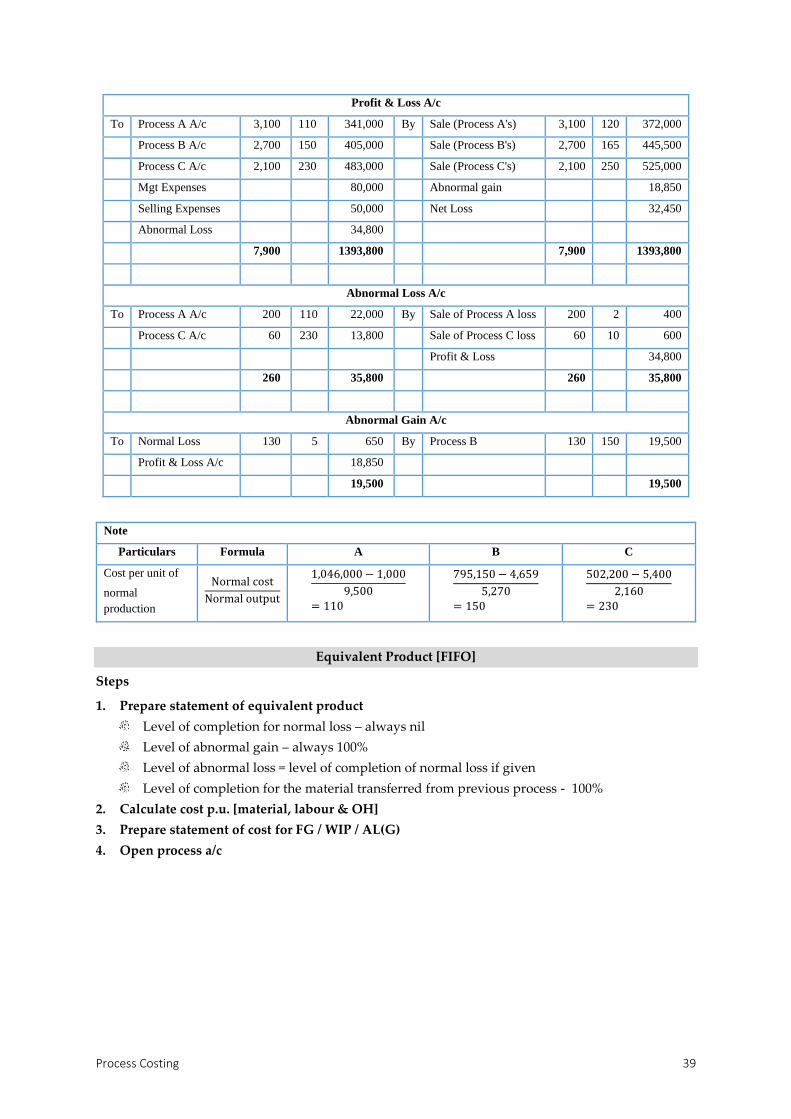

Profit & Loss A/c

To Process A A/c 3,100 110 341,000 By Sale (Process A's) 3,100 120 372,000

Process B A/c 2,700 150 405,000 Sale (Process B's) 2,700 165 445,500

Process C A/c 2,100 230 483,000 Sale (Process C's) 2,100 250 525,000

Mgt Expenses 80,000 Abnormal gain 18,850

Selling Expenses 50,000 Net Loss 32,450

Abnormal Loss 34,800

7,900 1393,800 7,900 1393,800

Abnormal Loss A/c

To Process A A/c 200 110 22,000 By Sale of Process A loss 200 2 400

Process C A/c 60 230 13,800 Sale of Process C loss 60 10 600

Profit & Loss 34,800

260 35,800 260 35,800

Abnormal Gain A/c

To Normal Loss 130 5 650 By Process B 130 150 19,500

Profit & Loss A/c 18,850

19,500 19,500

Note

Particulars Formula A B C

Cost per unit of

normal

production

Normal cost

Normal output

1,046,000 − 1,000

9,500= 110

795,150 − 4,659

5,270= 150

502,200 − 5,400

2,160= 230

Equivalent Product [FIFO]

Steps

1. Prepare statement of equivalent product

Level of completion for normal loss – always nil

Level of abnormal gain – always 100%

Level of abnormal loss = level of completion of normal loss if given

Level of completion for the material transferred from previous process - 100%

2. Calculate cost p.u. [material, labour & OH]

3. Prepare statement of cost for FG / WIP / AL(G)

4. Open process a/c

Cost Accounting 40

FIFO method

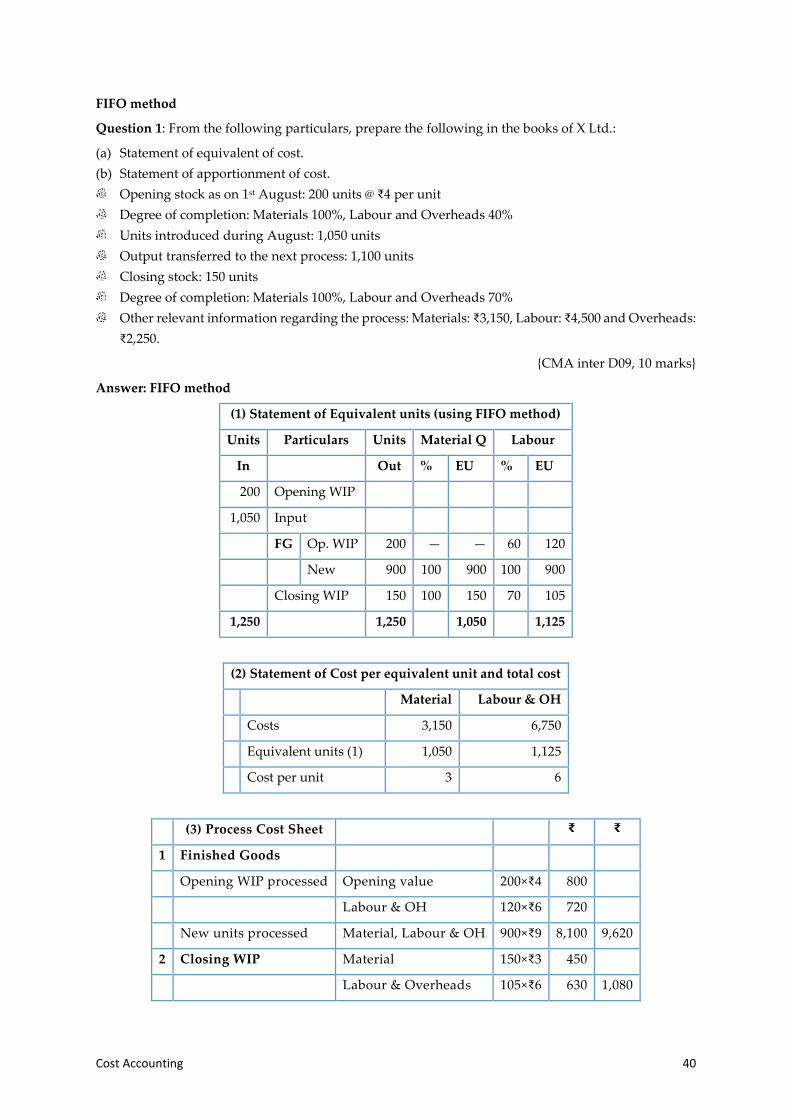

Question 1: From the following particulars, prepare the following in the books of X Ltd.:

(a) Statement of equivalent of cost.

(b) Statement of apportionment of cost.

Opening stock as on 1st August: 200 units @ ₹4 per unit

Degree of completion: Materials 100%, Labour and Overheads 40%

Units introduced during August: 1,050 units

Output transferred to the next process: 1,100 units

Closing stock: 150 units

Degree of completion: Materials 100%, Labour and Overheads 70%

Other relevant information regarding the process: Materials: ₹3,150, Labour: ₹4,500 and Overheads:

₹2,250.

{CMA inter D09, 10 marks}

Answer: FIFO method

(1) Statement of Equivalent units (using FIFO method)

Units Particulars Units Material Q Labour

In Out % EU % EU

200 Opening WIP

1,050 Input

FG Op. WIP 200 — — 60 120

New 900 100 900 100 900

Closing WIP 150 100 150 70 105

1,250 1,250 1,050 1,125

(2) Statement of Cost per equivalent unit and total cost

Material Labour & OH

Costs 3,150 6,750

Equivalent units (1) 1,050 1,125

Cost per unit 3 6

(3) Process Cost Sheet ₹ ₹

1 Finished Goods

Opening WIP processed Opening value 200×₹4 800

Labour & OH 120×₹6 720

New units processed Material, Labour & OH 900×₹9 8,100 9,620

2 Closing WIP Material 150×₹3 450

Labour & Overheads 105×₹6 630 1,080

Process Costing 41

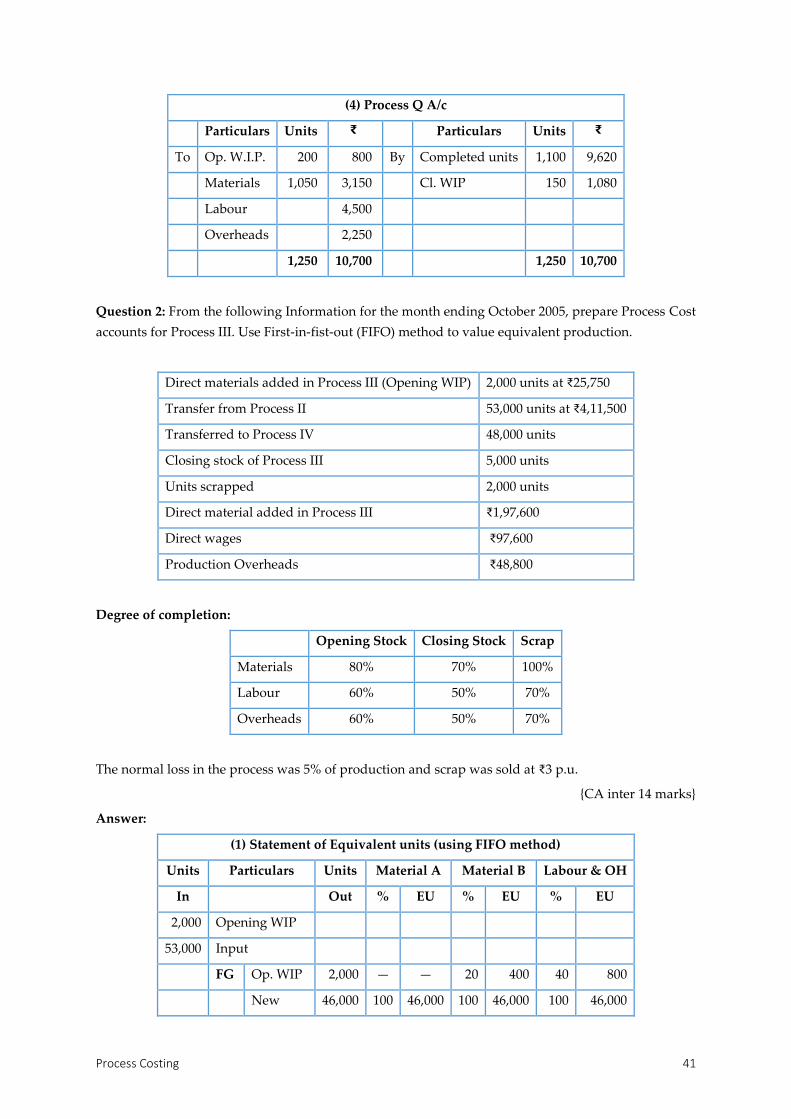

(4) Process Q A/c

Particulars Units ₹ Particulars Units ₹

To Op. W.I.P. 200 800 By Completed units 1,100 9,620

Materials 1,050 3,150 Cl. WIP 150 1,080

Labour 4,500

Overheads 2,250

1,250 10,700 1,250 10,700

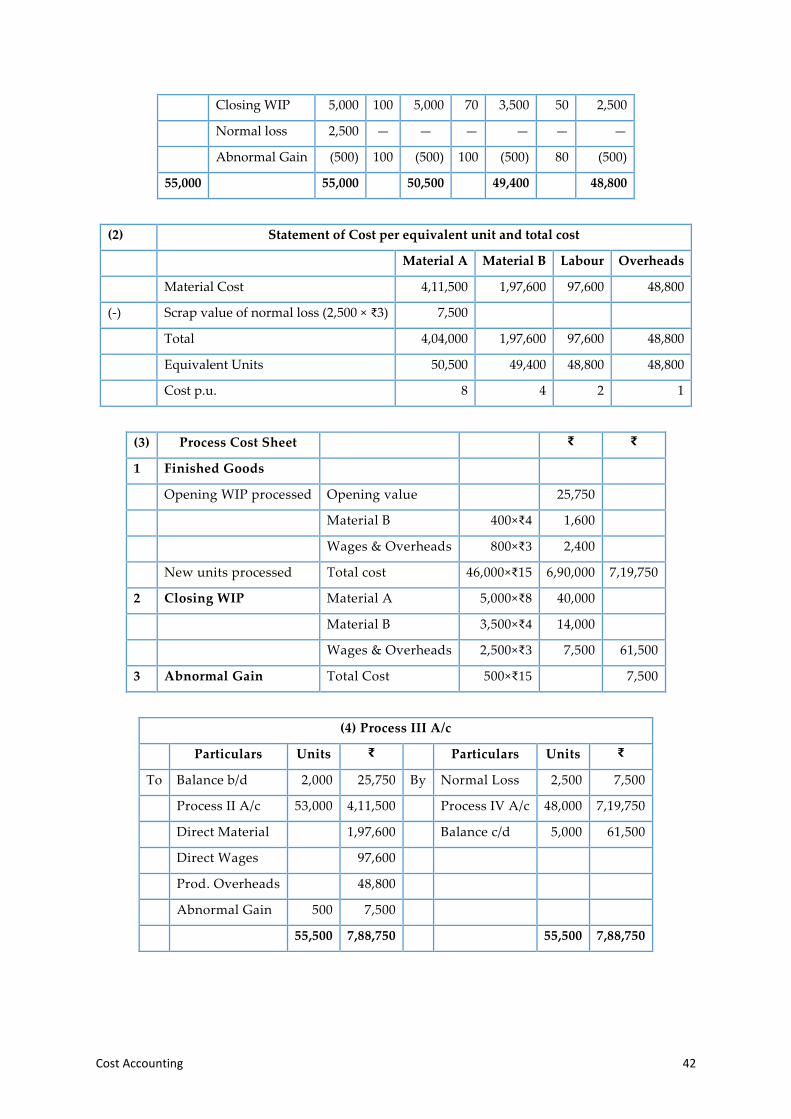

Question 2: From the following Information for the month ending October 2005, prepare Process Cost

accounts for Process III. Use First-in-fist-out (FIFO) method to value equivalent production.

Direct materials added in Process III (Opening WIP) 2,000 units at ₹25,750

Transfer from Process II 53,000 units at ₹4,11,500

Transferred to Process IV 48,000 units

Closing stock of Process III 5,000 units

Units scrapped 2,000 units

Direct material added in Process III ₹1,97,600

Direct wages ₹97,600

Production Overheads ₹48,800

Degree of completion:

Opening Stock Closing Stock Scrap

Materials 80% 70% 100%

Labour 60% 50% 70%

Overheads 60% 50% 70%

The normal loss in the process was 5% of production and scrap was sold at ₹3 p.u.

{CA inter 14 marks}

Answer:

(1) Statement of Equivalent units (using FIFO method)

Units Particulars Units Material A Material B Labour & OH

In Out % EU % EU % EU

2,000 Opening WIP

53,000 Input

FG Op. WIP 2,000 — — 20 400 40 800

New 46,000 100 46,000 100 46,000 100 46,000

Cost Accounting 42

Closing WIP 5,000 100 5,000 70 3,500 50 2,500

Normal loss 2,500 — — — — — —

Abnormal Gain (500) 100 (500) 100 (500) 80 (500)

55,000 55,000 50,500 49,400 48,800

(2) Statement of Cost per equivalent unit and total cost

Material A Material B Labour Overheads

Material Cost 4,11,500 1,97,600 97,600 48,800

(-) Scrap value of normal loss (2,500 × ₹3) 7,500

Total 4,04,000 1,97,600 97,600 48,800

Equivalent Units 50,500 49,400 48,800 48,800

Cost p.u. 8 4 2 1

(3) Process Cost Sheet ₹ ₹

1 Finished Goods

Opening WIP processed Opening value 25,750

Material B 400×₹4 1,600

Wages & Overheads 800×₹3 2,400

New units processed Total cost 46,000×₹15 6,90,000 7,19,750

2 Closing WIP Material A 5,000×₹8 40,000

Material B 3,500×₹4 14,000

Wages & Overheads 2,500×₹3 7,500 61,500

3 Abnormal Gain Total Cost 500×₹15 7,500

(4) Process III A/c

Particulars Units ₹ Particulars Units ₹

To Balance b/d 2,000 25,750 By Normal Loss 2,500 7,500

Process II A/c 53,000 4,11,500 Process IV A/c 48,000 7,19,750

Direct Material 1,97,600 Balance c/d 5,000 61,500

Direct Wages 97,600

Prod. Overheads 48,800

Abnormal Gain 500 7,500

55,500 7,88,750 55,500 7,88,750

Process Costing 43

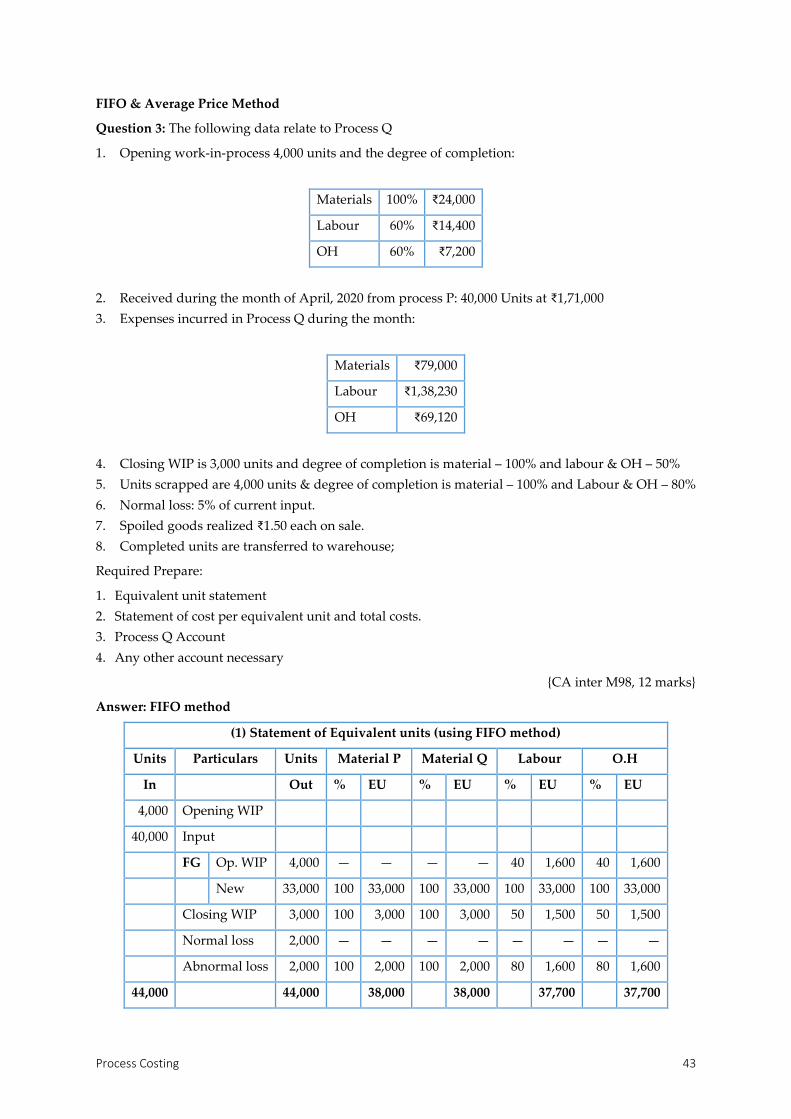

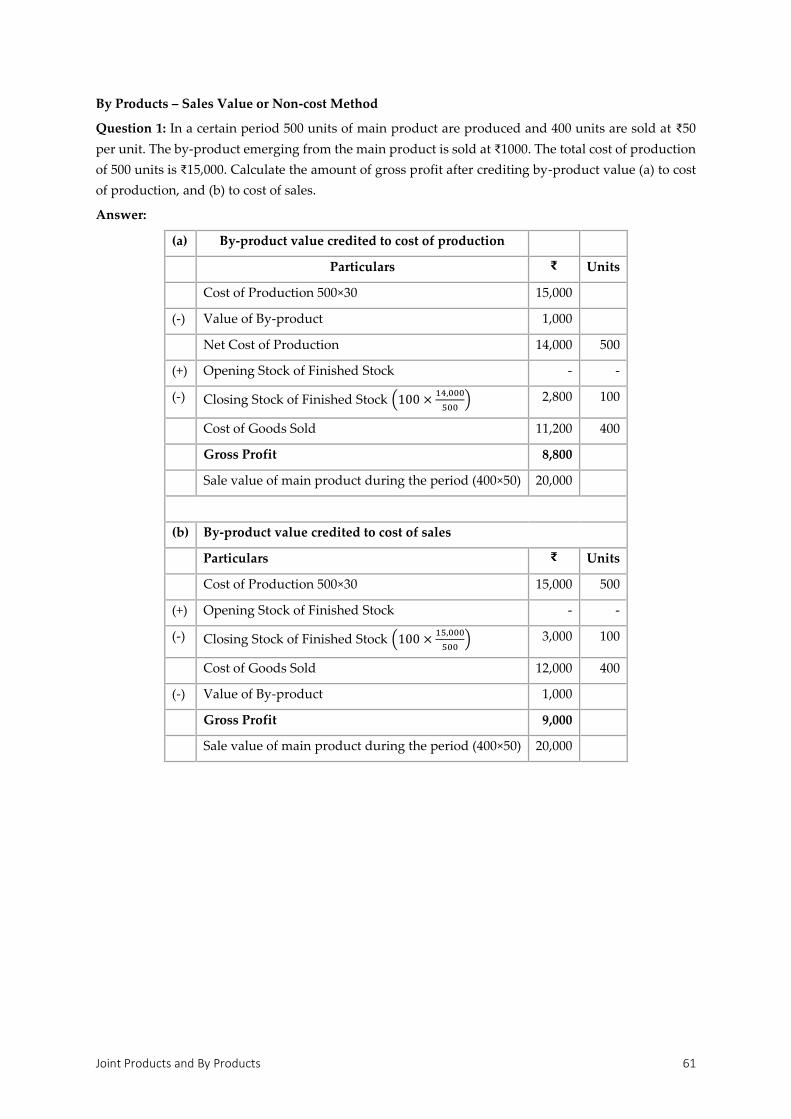

FIFO & Average Price Method

Question 3: The following data relate to Process Q

1. Opening work-in-process 4,000 units and the degree of completion:

Materials 100% ₹24,000

Labour 60% ₹14,400

OH 60% ₹7,200

2. Received during the month of April, 2020 from process P: 40,000 Units at ₹1,71,000

3. Expenses incurred in Process Q during the month:

Materials ₹79,000

Labour ₹1,38,230

OH ₹69,120

4. Closing WIP is 3,000 units and degree of completion is material – 100% and labour & OH – 50%

5. Units scrapped are 4,000 units & degree of completion is material – 100% and Labour & OH – 80%

6. Normal loss: 5% of current input.

7. Spoiled goods realized ₹1.50 each on sale.

8. Completed units are transferred to warehouse;

Required Prepare:

1. Equivalent unit statement

2. Statement of cost per equivalent unit and total costs.

3. Process Q Account

4. Any other account necessary

{CA inter M98, 12 marks}

Answer: FIFO method

(1) Statement of Equivalent units (using FIFO method)

Units Particulars Units Material P Material Q Labour O.H

In Out % EU % EU % EU % EU

4,000 Opening WIP

40,000 Input

FG Op. WIP 4,000 — — — — 40 1,600 40 1,600

New 33,000 100 33,000 100 33,000 100 33,000 100 33,000

Closing WIP 3,000 100 3,000 100 3,000 50 1,500 50 1,500

Normal loss 2,000 — — — — — — — —

Abnormal loss 2,000 100 2,000 100 2,000 80 1,600 80 1,600

44,000 44,000 38,000 38,000 37,700 37,700

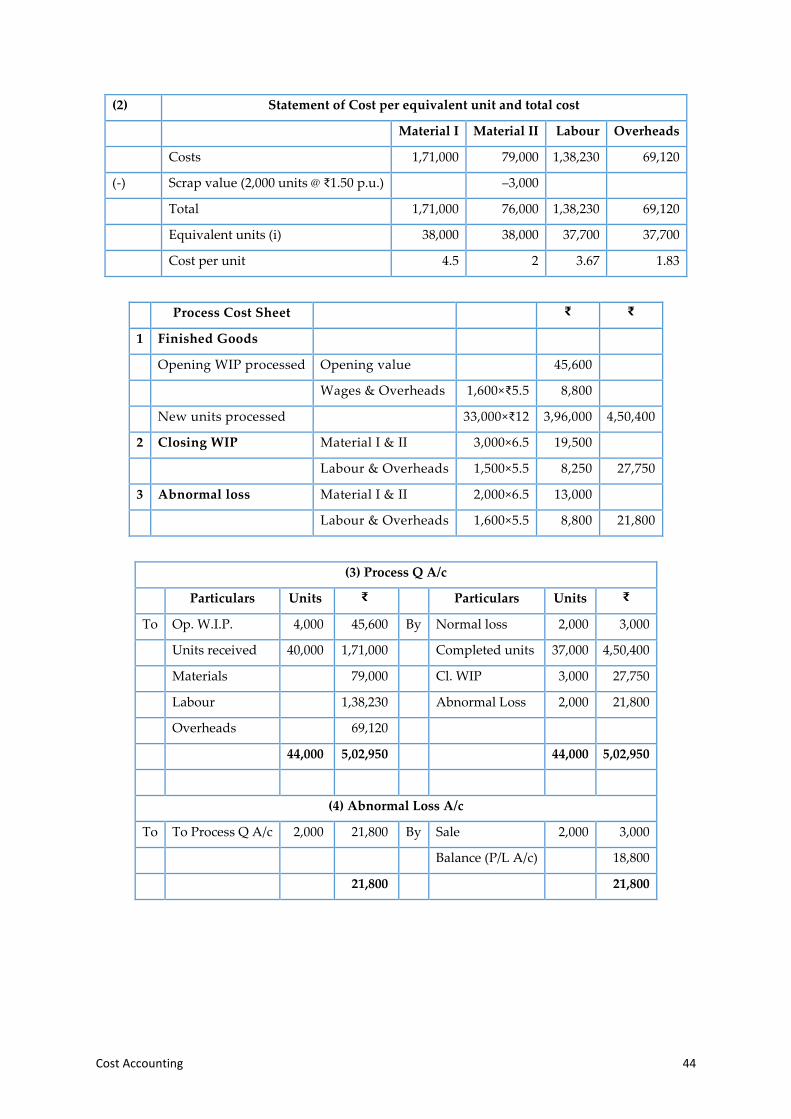

Cost Accounting 44

(2) Statement of Cost per equivalent unit and total cost

Material I Material II Labour Overheads

Costs 1,71,000 79,000 1,38,230 69,120

(-) Scrap value (2,000 units @ ₹1.50 p.u.) –3,000

Total 1,71,000 76,000 1,38,230 69,120

Equivalent units (i) 38,000 38,000 37,700 37,700

Cost per unit 4.5 2 3.67 1.83

Process Cost Sheet ₹ ₹

1 Finished Goods

Opening WIP processed Opening value 45,600

Wages & Overheads 1,600×₹5.5 8,800

New units processed 33,000×₹12 3,96,000 4,50,400

2 Closing WIP Material I & II 3,000×6.5 19,500

Labour & Overheads 1,500×5.5 8,250 27,750

3 Abnormal loss Material I & II 2,000×6.5 13,000

Labour & Overheads 1,600×5.5 8,800 21,800

(3) Process Q A/c

Particulars Units ₹ Particulars Units ₹

To Op. W.I.P. 4,000 45,600 By Normal loss 2,000 3,000

Units received 40,000 1,71,000 Completed units 37,000 4,50,400

Materials 79,000 Cl. WIP 3,000 27,750

Labour 1,38,230 Abnormal Loss 2,000 21,800

Overheads 69,120

44,000 5,02,950 44,000 5,02,950

(4) Abnormal Loss A/c

To To Process Q A/c 2,000 21,800 By Sale 2,000 3,000

Balance (P/L A/c) 18,800

21,800 21,800

Process Costing 45

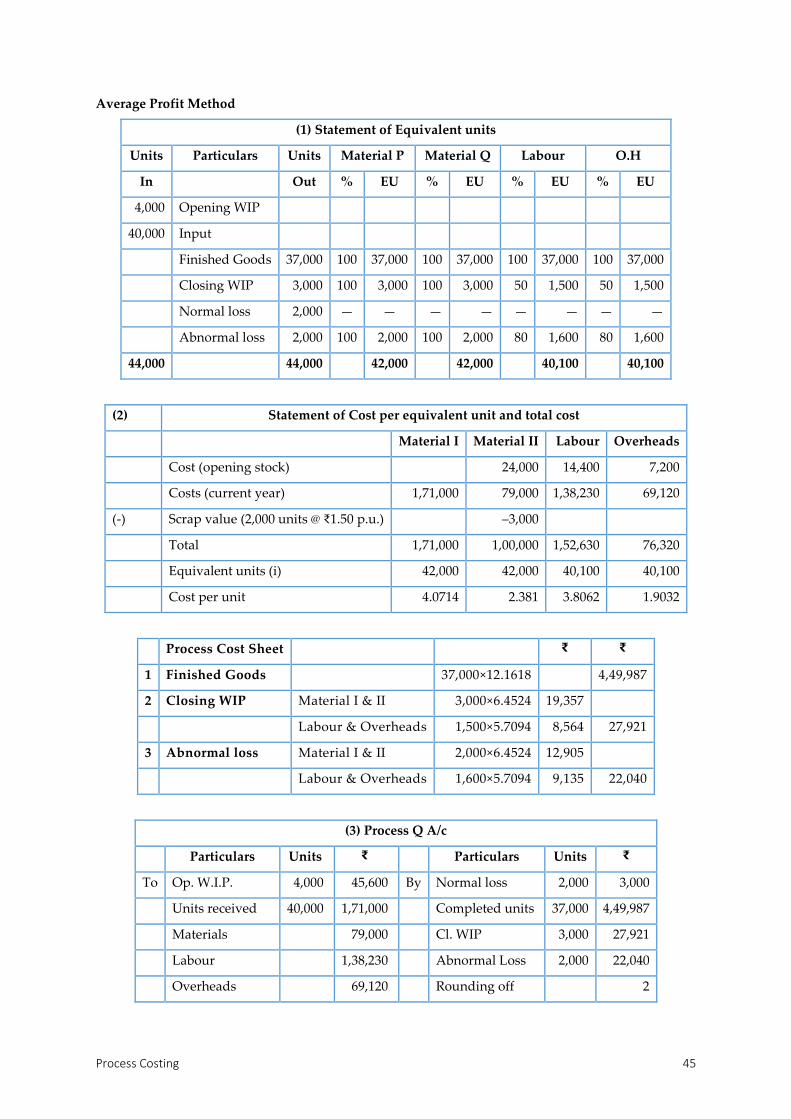

Average Profit Method

(1) Statement of Equivalent units

Units Particulars Units Material P Material Q Labour O.H

In Out % EU % EU % EU % EU

4,000 Opening WIP

40,000 Input

Finished Goods 37,000 100 37,000 100 37,000 100 37,000 100 37,000

Closing WIP 3,000 100 3,000 100 3,000 50 1,500 50 1,500

Normal loss 2,000 — — — — — — — —

Abnormal loss 2,000 100 2,000 100 2,000 80 1,600 80 1,600

44,000 44,000 42,000 42,000 40,100 40,100

(2) Statement of Cost per equivalent unit and total cost

Material I Material II Labour Overheads

Cost (opening stock) 24,000 14,400 7,200

Costs (current year) 1,71,000 79,000 1,38,230 69,120

(-) Scrap value (2,000 units @ ₹1.50 p.u.) –3,000

Total 1,71,000 1,00,000 1,52,630 76,320

Equivalent units (i) 42,000 42,000 40,100 40,100

Cost per unit 4.0714 2.381 3.8062 1.9032

Process Cost Sheet ₹ ₹

1 Finished Goods 37,000×12.1618 4,49,987

2 Closing WIP Material I & II 3,000×6.4524 19,357

Labour & Overheads 1,500×5.7094 8,564 27,921

3 Abnormal loss Material I & II 2,000×6.4524 12,905

Labour & Overheads 1,600×5.7094 9,135 22,040

(3) Process Q A/c

Particulars Units ₹ Particulars Units ₹

To Op. W.I.P. 4,000 45,600 By Normal loss 2,000 3,000

Units received 40,000 1,71,000 Completed units 37,000 4,49,987

Materials 79,000 Cl. WIP 3,000 27,921

Labour 1,38,230 Abnormal Loss 2,000 22,040

Overheads 69,120 Rounding off 2

Cost Accounting 46

44,000 5,02,950 44,000 5,02,950

(4) Abnormal Loss A/c

To To Process Q A/c 2,000 22,040 By Sale 2,000 3,000

Balance (P/L A/c) 19,040

22,040 22,040

Average Price Method

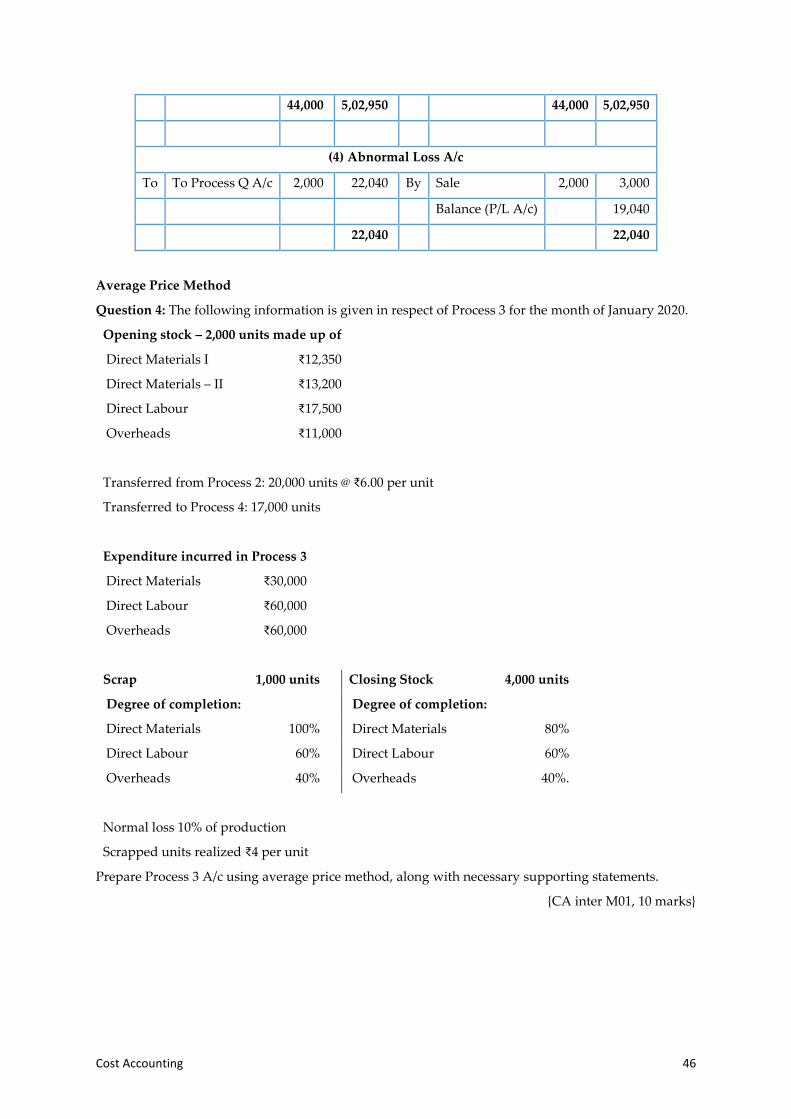

Question 4: The following information is given in respect of Process 3 for the month of January 2020.

Transferred from Process 2: 20,000 units @ ₹6.00 per unit

Transferred to Process 4: 17,000 units

Expenditure incurred in Process 3

Direct Materials ₹30,000

Direct Labour ₹60,000

Overheads ₹60,000

Scrap 1,000 units Closing Stock 4,000 units

Degree of completion: Degree of completion:

Direct Materials 100% Direct Materials 80%

Direct Labour 60% Direct Labour 60%

Overheads 40% Overheads 40%.

Normal loss 10% of production

Scrapped units realized ₹4 per unit

Prepare Process 3 A/c using average price method, along with necessary supporting statements.

{CA inter M01, 10 marks}

Opening stock – 2,000 units made up of

Direct Materials I ₹12,350

Direct Materials – II ₹13,200

Direct Labour ₹17,500

Overheads ₹11,000

Process Costing 47

Answer:

(1) Statement of Equivalent Production (Average cost method)

Particulars Total Unit Material I Material II Labour Overhead

% Units % Units % Units % Units

2,000 Opening WIP

20,000 Input

Units processed 17,000 100 17,000 100 17,000 100 17,000 100 17,000

Normal Loss1 1,800 — — — — — — — —

Abnormal gain (800) 100 (800) 100 (800) 100 (800) 100 (800)

Closing stock 4,000 100 4,000 80 3,200 60 2,400 40 1,600

22,000 20,200 19,400 18,600 17,800

(2) Statement of Cost per equivalent unit and total cost

Material I Material II Labour O.H

Opening Cost 12,350 13,200 17,500 11,000

Current year Costs (₹) 1,20,000 30,000 60,000 60,000

(-) Scrap value (1,800 units @ ₹4 p.u.) (₹) 7,200

Total 1,25,150 43,200 77,500 71,000

Equivalent units: 20,200 19,400 18,600 17,800

Cost per equivalent unit(₹) 6.1955 2.2268 4.1667 3.9888

Total cost p.u. 16.5778

(3) Process Cost Sheet ₹ ₹

1 Finished Goods 17,000×16.5778 2,81,822

2 Closing WIP Material I 4,000×6.1955 24,782

Material II 3,200×2.2268 7,126

Labour 2,400×4.1667 10,000

Overheads 1,600×3.9888 6,382 48,290

3 Abnormal gain 800×16.5778 13,262

(4) Process 3 A/c

Particulars Units ₹ Particulars Units ₹

To Opening WIP 2,000 54,050 By Normal Loss 1,800 7,200

Process 2 20,000 1,20,000 Finished goods units 17,000 2,81,822

1 10% of (2,000 units + 20,000 units – 4,000 units)

Cost Accounting 48

Direct Material II 30,000 Closing balance 4,000 48,290

Direct Labour 60,000

Overhead 60,000

Abnormal gain 800 13,262

22,800 3,37,312 22,800 3,37,312

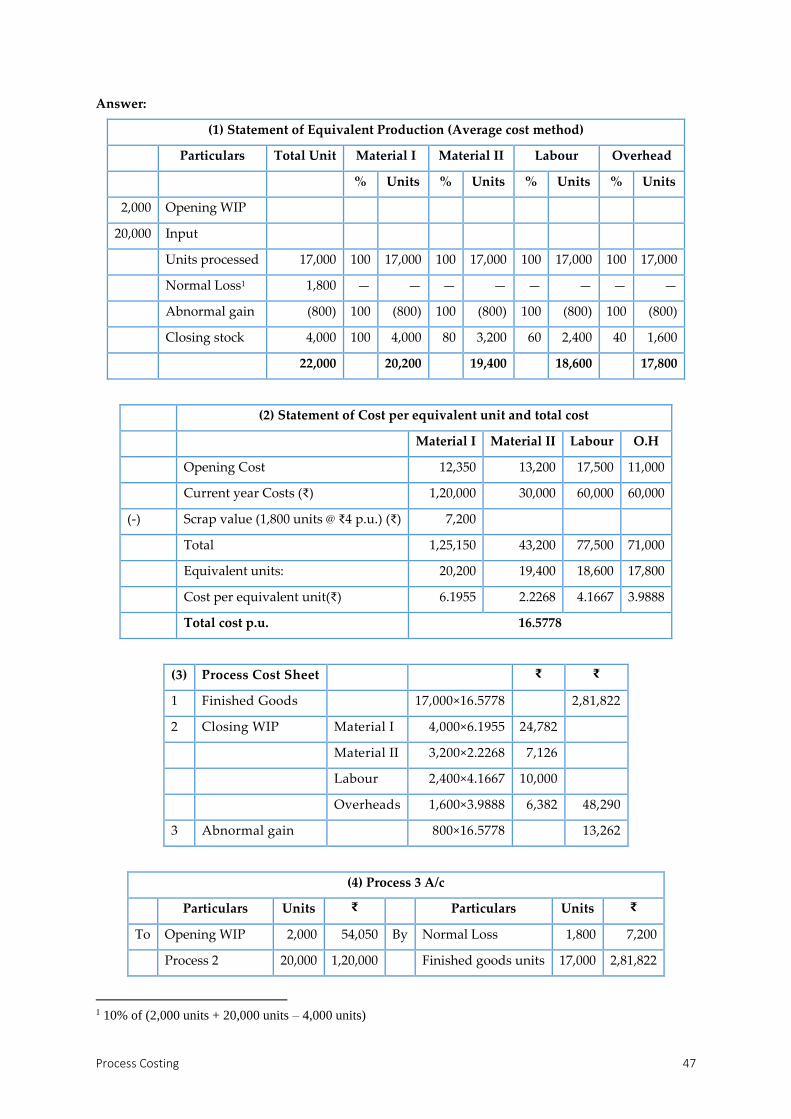

LIFO method

Question 5: From the following information relating to the month of January, 2020. Calculate the

equivalent production units and the value of finished production and WIP using LIFO method.

Opening WIP on 1st January 15,000 units; 50% complete.

Material: 18,000 Labour: 24,000 Overheads: 24,000 Total: 66,000

Units introduced in the process: 30,000 units

Material: 90,000 Labour: 157,500 Overheads: 210,000 Total: 457,500

During the period 22,500 units were completed and transferred to the next process. Closing work-in-

progress on 31st January: 22,500 units; 60% complete.

Answer: (1) Calculation of Equivalent Units

Units in Particulars Units Out % EU

15,000 Opening work in progress

30,000 Units introduced

Finished goods 22,500 100 22,500

Closing work in progress [new] 7,500 60 4,500

Closing work in progress [opening] 15,000 10 1,500

45,000 45,000 28,500

(2) 𝐶𝑜𝑠𝑡 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡 𝑜𝑓 𝑒𝑞𝑢𝑖𝑣𝑎𝑙𝑒𝑛𝑡 𝑝𝑟𝑜𝑑𝑢𝑐𝑡𝑖𝑜𝑛 = 𝑇𝑜𝑡𝑎𝑙 𝑐𝑜𝑠𝑡

𝐸𝑞𝑢𝑖𝑣𝑎𝑙𝑒𝑛𝑡 𝑈𝑛𝑖𝑡𝑠 =

457,500

28,500 = ₹16.0526

(3) Valuation of finished Production and WIP

1. 𝐹𝑖𝑛𝑖𝑠ℎ𝑒𝑑 𝑝𝑟𝑜𝑑𝑢𝑐𝑡𝑖𝑜𝑛𝑠 = 22,500 × ₹16.0526 = ₹3,61,184

2. 𝐶𝑙𝑜𝑠𝑖𝑛𝑔 𝑊𝐼𝑃 = ₹66,000 + (1,500 × 16.0526) + (4,500 × 16.0526) = ₹1,39,720.65

Process Costing 49

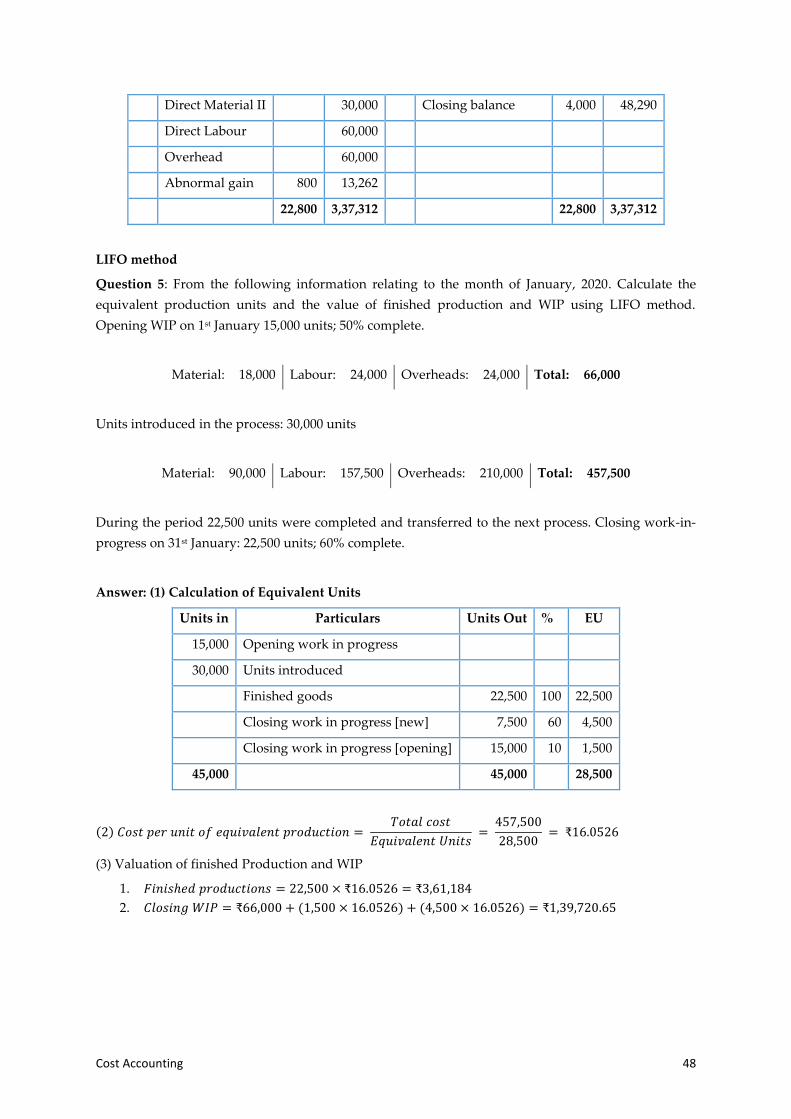

Inter Process Profit

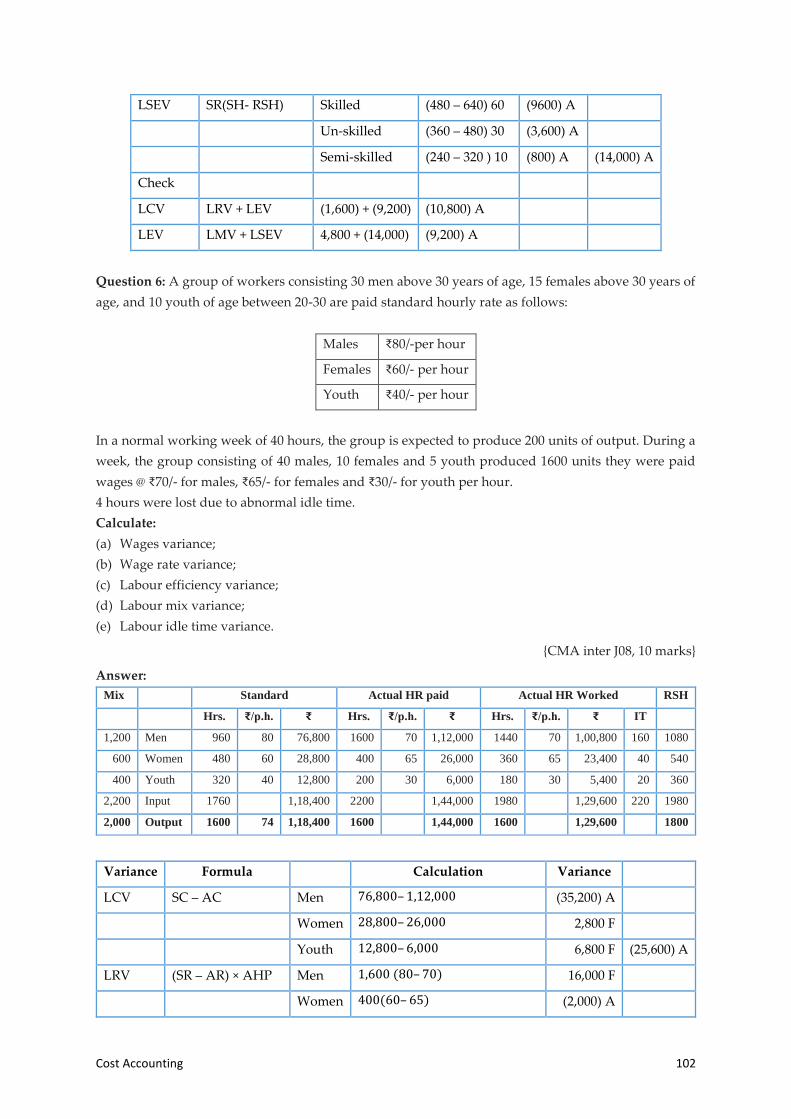

Question 1: A certain product passes through two processes desired before it is transferred to finished

stock. The following information is obtained for the month of January 2020.

Particulars P-I P-II FG

Opening Stock 7,500 9,000 22,500

Direct Material 15,000 15,750

Direct wages 11,200 11,250

Production overhead 10,500 4,500

Closing stock 3,700 4,500 11,250

Profit % on transfer price to the next Process 25% 20%

Inter-process profits for opening stock - 1,500 8,250

Stocks in processes are valued at prime cost and finished stock has been valued at the price at which it

was received from process II. Sales during the period were ₹140,000.

Prepare and compute

(a) process cost accounts showing profit element at each stage;

(b) actual realized profit; and

(c) stock valuation for balance sheet purposes.

Answer:

Process – I A/c

Particulars Total Cost Profit

To Opening Stock b/d 7,500 7,500 -

Direct Material 15,000 15,000 -

Direct Wages 11,200 11,200 -

Total 33,700 33,700 -

Less Closing Stock 3,700 3,700 -

Prime Cost 30,000 30,000 -

Factory overhead 10,500 10,500 -

Total Cost 40,500 40,500 -

Profit (1/3 of Cost) 13,500 - 13,500

Total 54,000 40,500 13,500

Process II

Particulars Total Cost Profit

To Opening Stock b/d 9,000 7,500 1,500

Cost Accounting 50

Process I transfer 54,000 40,500 13,500

Direct Material 15,750 15,750 -

Direct Wages 11,250 11,250 -

Total 90,000 75,000 15,000

(-) Closing Stock 4,500 3,750 750

Prime Cost 85,500 71,250 14,250

Factory overhead 4,500 4,500 -

Total Cost 90,000 75,750 14,250

Profit (1/4 of Cost) 22,500 - 22,500

Total 1,12,500 75,750 36,750

Finished Stock – II A/c

Particulars Total Cost Profit

To Opening Stock b/d 22,500 14,250 8,250

Process II transfer 1,12,500 75,750 36,750

Total 1,35,000 90,000 45,000

(-) Closing Stock 11,250 7,500 3,750

1,23,750 82,500 41,250

Gross profit 16,250 - 16,250

Sales 1,40,000 82,500 57,500

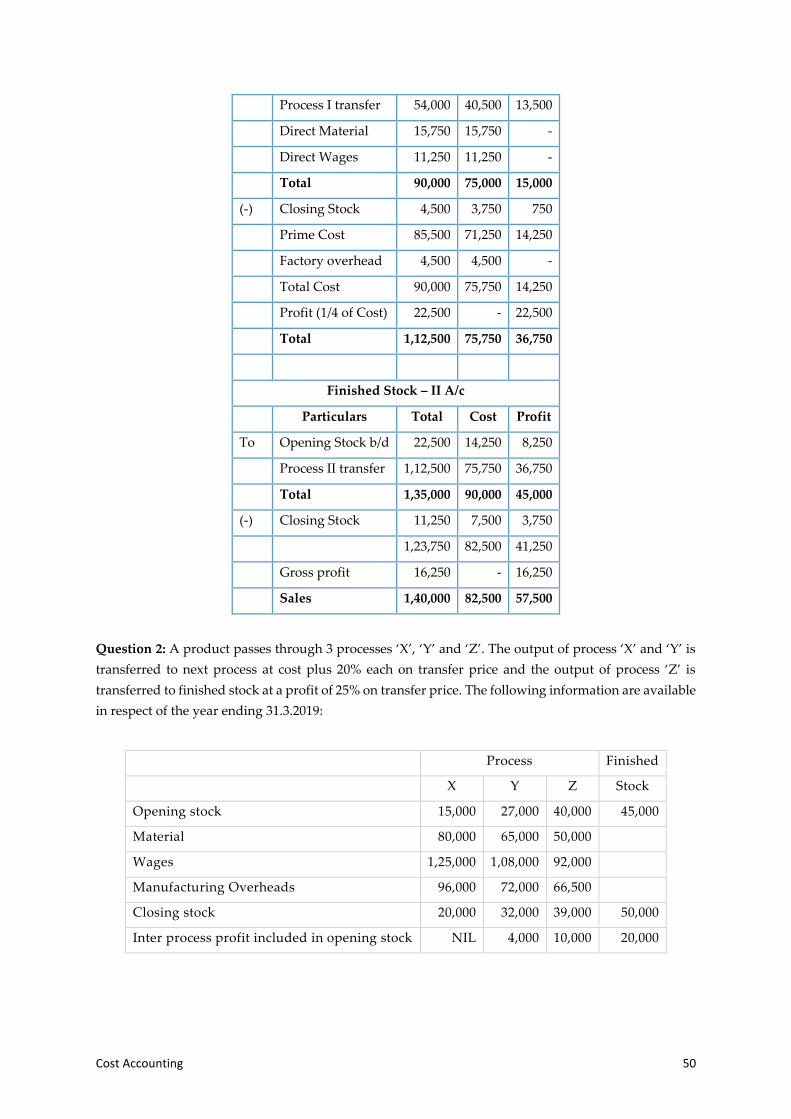

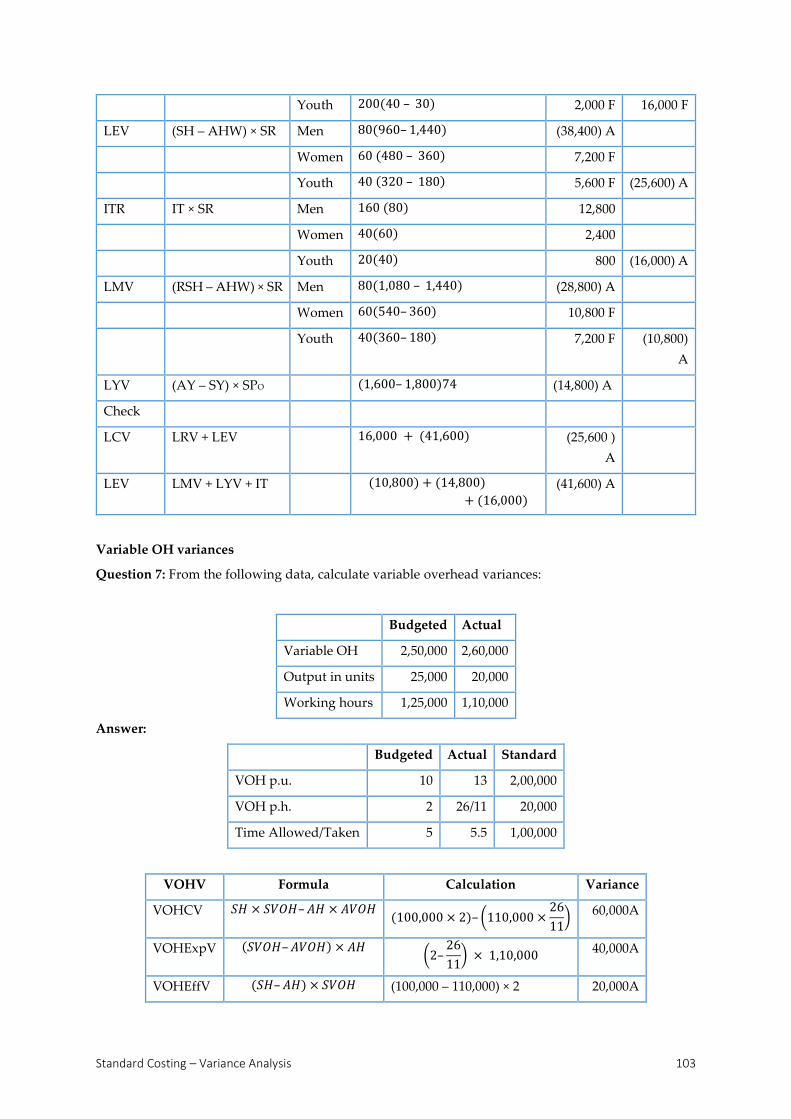

Question 2: A product passes through 3 processes ‘X’, ‘Y’ and ‘Z’. The output of process ‘X’ and ‘Y’ is

transferred to next process at cost plus 20% each on transfer price and the output of process ‘Z’ is

transferred to finished stock at a profit of 25% on transfer price. The following information are available

in respect of the year ending 31.3.2019:

Process Finished

X Y Z Stock

Opening stock 15,000 27,000 40,000 45,000

Material 80,000 65,000 50,000

Wages 1,25,000 1,08,000 92,000

Manufacturing Overheads 96,000 72,000 66,500

Closing stock 20,000 32,000 39,000 50,000

Inter process profit included in opening stock NIL 4,000 10,000 20,000

Process Costing 51

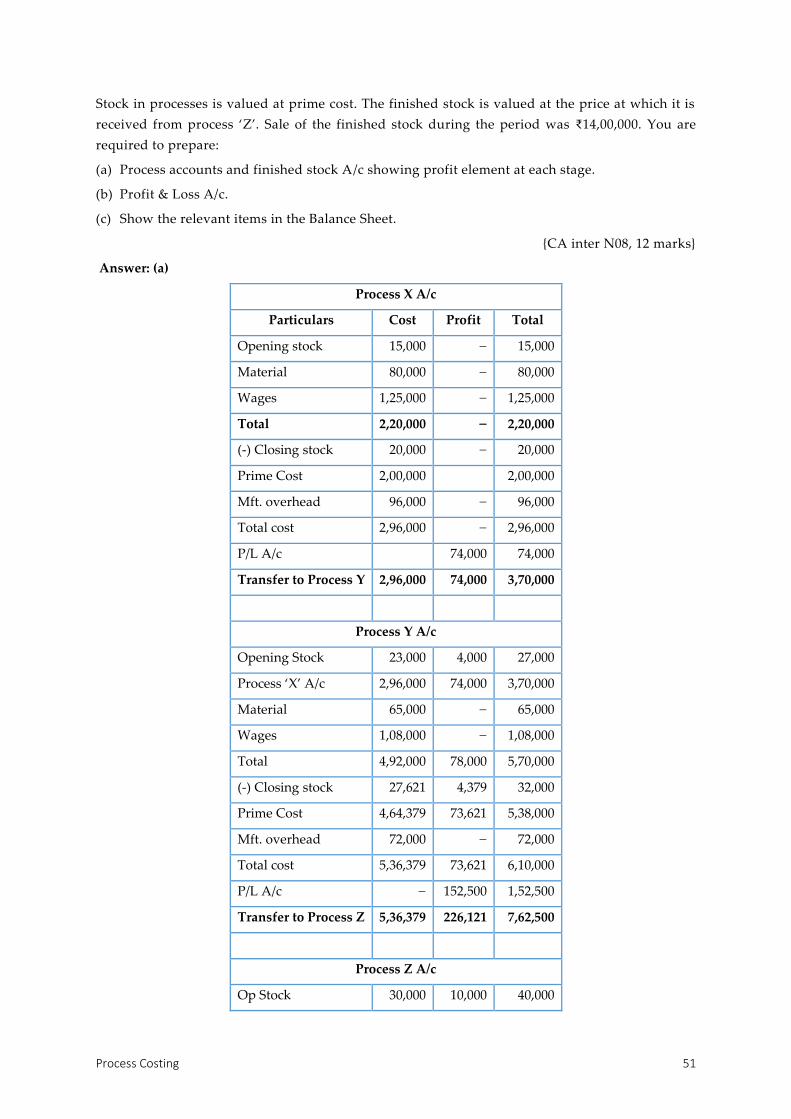

Stock in processes is valued at prime cost. The finished stock is valued at the price at which it is

received from process ‘Z’. Sale of the finished stock during the period was ₹14,00,000. You are

required to prepare:

(a) Process accounts and finished stock A/c showing profit element at each stage.

(b) Profit & Loss A/c.

(c) Show the relevant items in the Balance Sheet.

{CA inter N08, 12 marks}

Answer: (a)

Process X A/c

Particulars Cost Profit Total

Opening stock 15,000 − 15,000

Material 80,000 − 80,000

Wages 1,25,000 − 1,25,000

Total 2,20,000 − 2,20,000

(-) Closing stock 20,000 − 20,000

Prime Cost 2,00,000 2,00,000

Mft. overhead 96,000 − 96,000

Total cost 2,96,000 − 2,96,000

P/L A/c 74,000 74,000

Transfer to Process Y 2,96,000 74,000 3,70,000

Process Y A/c

Opening Stock 23,000 4,000 27,000

Process ‘X’ A/c 2,96,000 74,000 3,70,000

Material 65,000 − 65,000

Wages 1,08,000 − 1,08,000

Total 4,92,000 78,000 5,70,000

(-) Closing stock 27,621 4,379 32,000

Prime Cost 4,64,379 73,621 5,38,000

Mft. overhead 72,000 − 72,000

Total cost 5,36,379 73,621 6,10,000

P/L A/c − 152,500 1,52,500

Transfer to Process Z 5,36,379 226,121 7,62,500

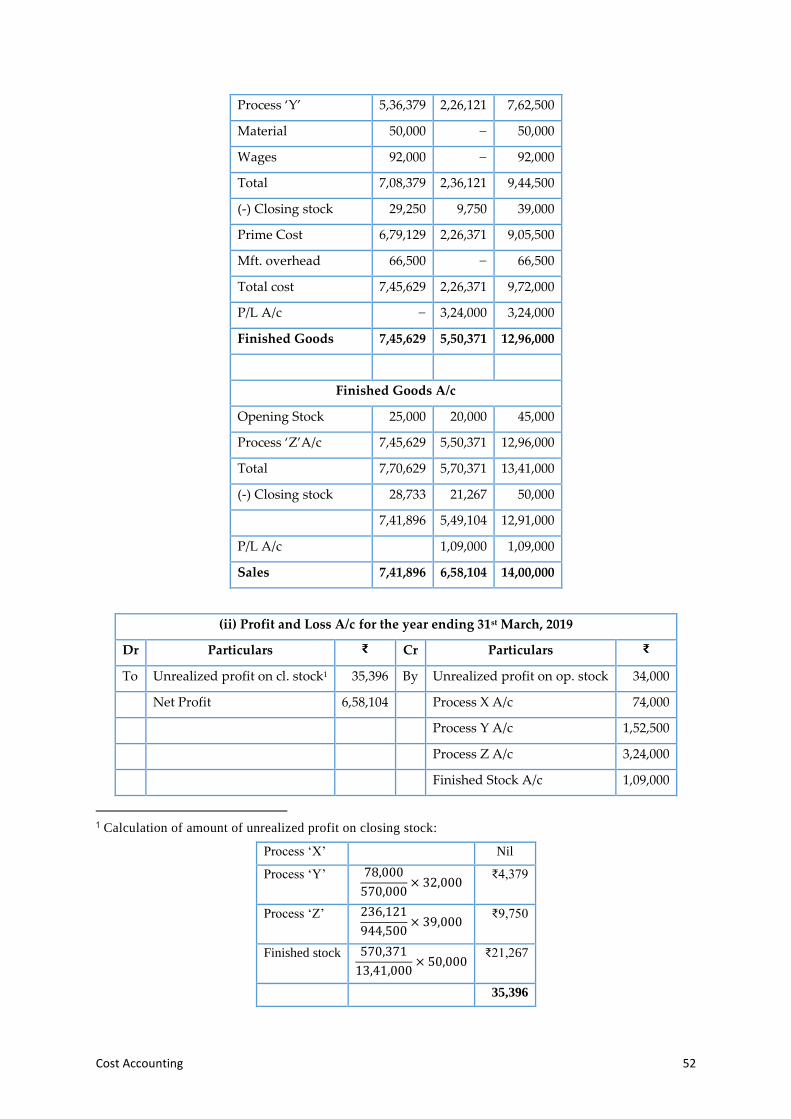

Process Z A/c

Op Stock 30,000 10,000 40,000

Cost Accounting 52

Process ‘Y’ 5,36,379 2,26,121 7,62,500

Material 50,000 − 50,000

Wages 92,000 − 92,000

Total 7,08,379 2,36,121 9,44,500

(-) Closing stock 29,250 9,750 39,000

Prime Cost 6,79,129 2,26,371 9,05,500

Mft. overhead 66,500 − 66,500

Total cost 7,45,629 2,26,371 9,72,000

P/L A/c − 3,24,000 3,24,000

Finished Goods 7,45,629 5,50,371 12,96,000

Finished Goods A/c

Opening Stock 25,000 20,000 45,000

Process ‘Z’A/c 7,45,629 5,50,371 12,96,000

Total 7,70,629 5,70,371 13,41,000

(-) Closing stock 28,733 21,267 50,000

7,41,896 5,49,104 12,91,000

P/L A/c 1,09,000 1,09,000

Sales 7,41,896 6,58,104 14,00,000

(ii) Profit and Loss A/c for the year ending 31st March, 2019

Dr Particulars ₹ Cr Particulars ₹

To Unrealized profit on cl. stock1 35,396 By Unrealized profit on op. stock 34,000

Net Profit 6,58,104 Process X A/c 74,000

Process Y A/c 1,52,500

Process Z A/c 3,24,000

Finished Stock A/c 1,09,000

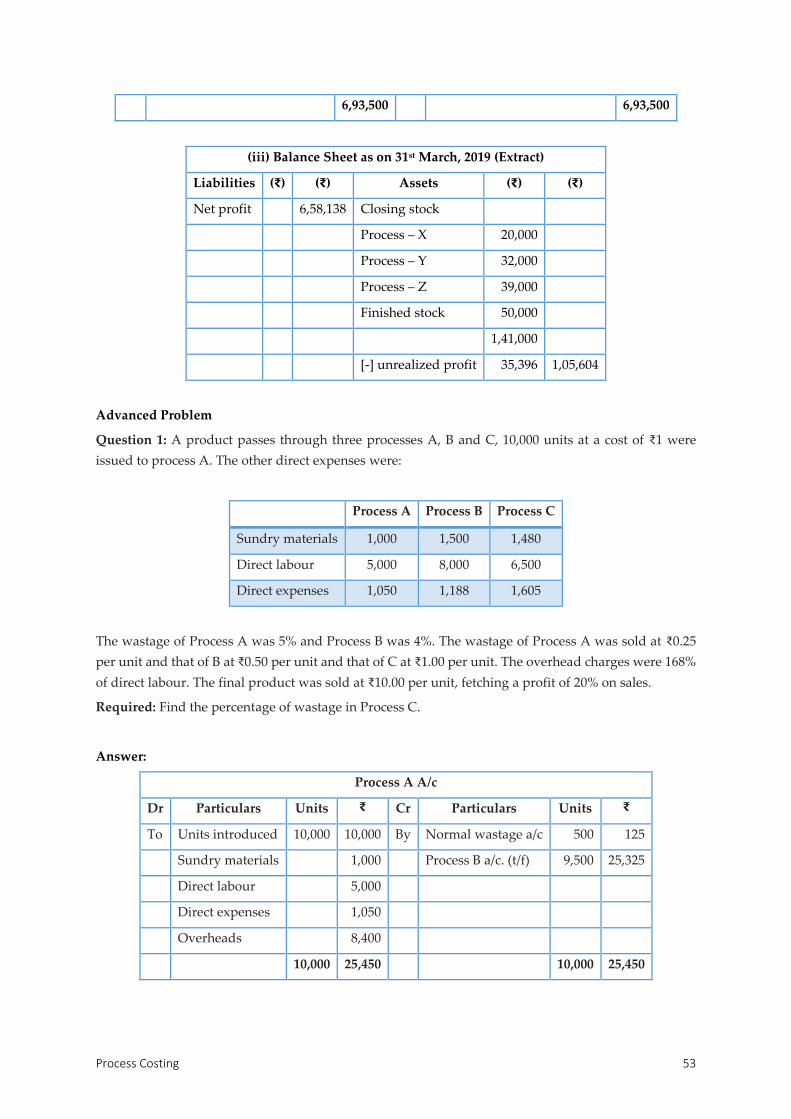

1 Calculation of amount of unrealized profit on closing stock:

Process ‘X’ Nil

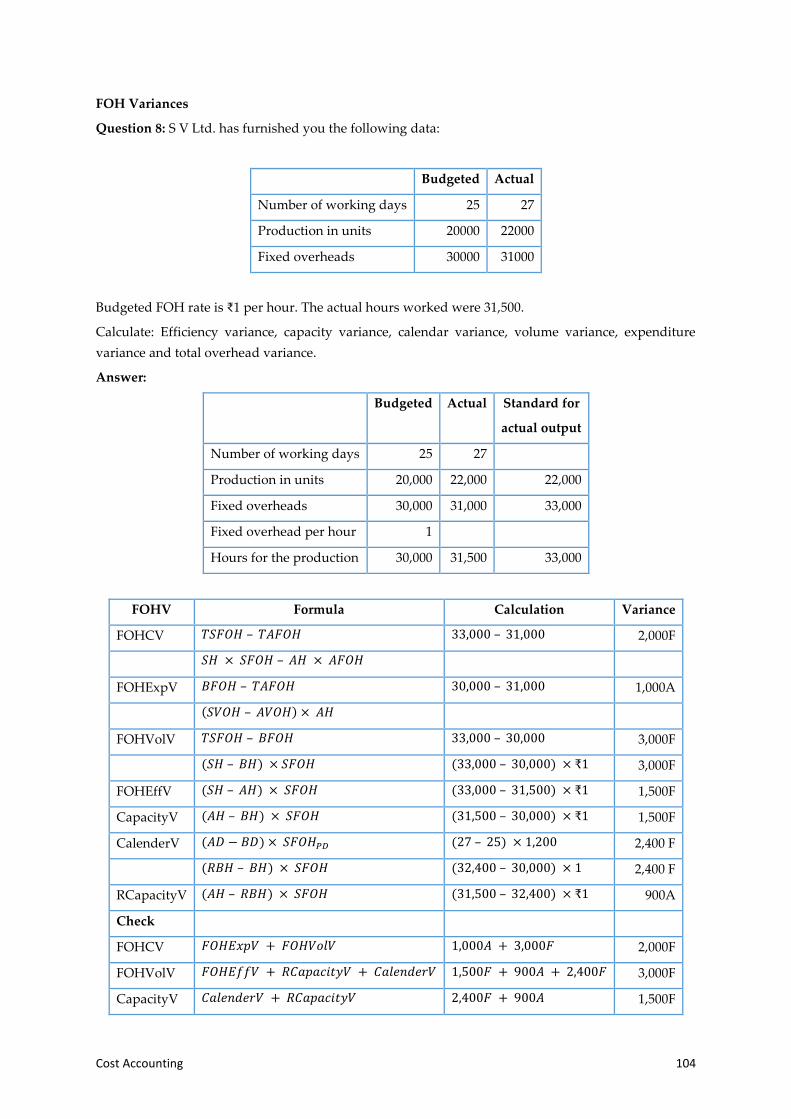

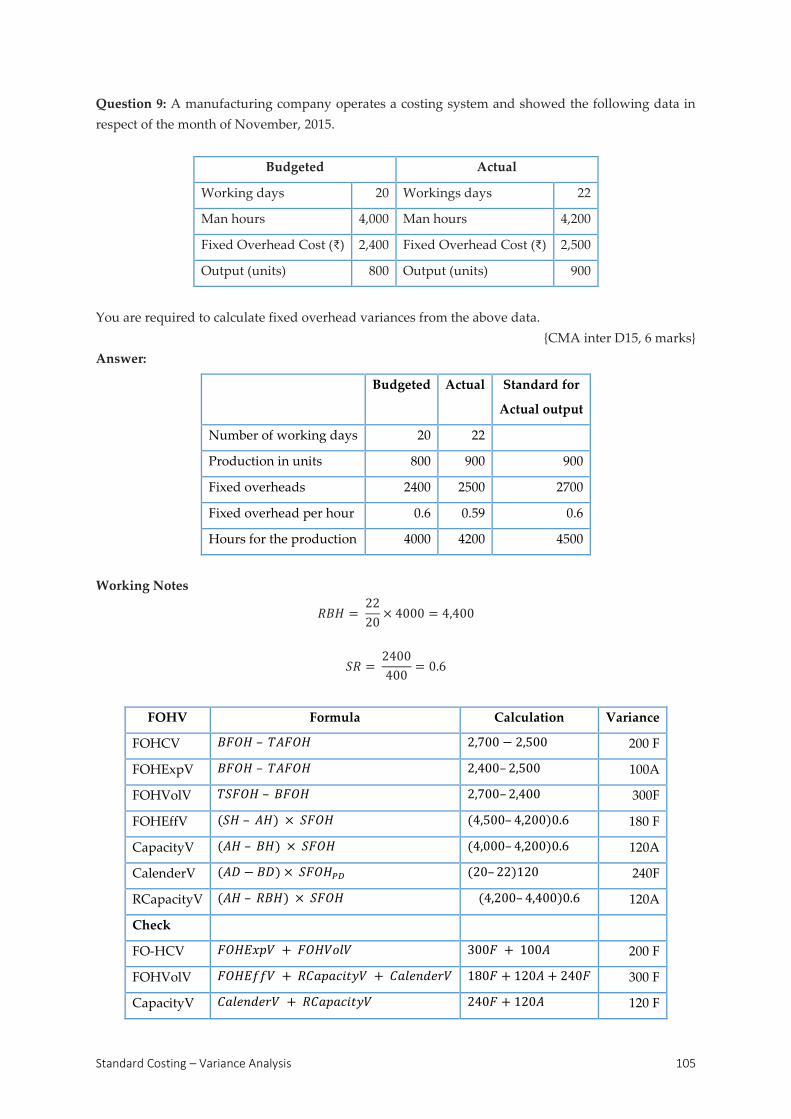

Process ‘Y’ 78,000