corruption: costs and mitigation strategies€¦ · · 2017-04-09corruption: costs and mitigation...

TRANSCRIPT

Corruption: Costs and Mitigation Strategies

Presented by

Sanjeev GuptaDeputy Director

Fiscal Affairs Department

INTERNATIONAL MONETARY FUND

APRIL 12, 2017

Outline

Definitions and Manifestations

The economic and social costs of corruption

Corruption and Fiscal Policy

Strategies for addressing corruption based on IMF experience

Conclusions

2

Definitions and Manifestations“Abuse of public office for private gain”

Limited to public sector corruption (not private sector corruption)

Corruption can: Involve non-financial gain (e.g., conflicts of interest arising from family

interests)

Pervert the law making process (state capture/privatization of public policy)

If corruption becomes systemic (i.e. the norm), in the extreme it can affect all state functions and lead to a breakdown

3

The Economic and Social Costs of

Corruption

Potential Inclusive Growth

Fiscal

Corruption

Macro-FinancialStability

• Banking crises• External sector imbalances• Inflation• Fiscal unsustainability• Financial inclusion

Market Regulation

Monetary Policy

Financial Sector

Oversight

Public & PrivatePhysical Capital

• Inefficient public investment• Costly investment and production• Distorted composition of projects• Uncertainty• Distorted asset prices

Human Capital• Insufficient spending on

education/health• Poverty and inequality• Disincentives for skill

acquisition

TFP• Insufficient investment

(R&D)• Inefficiency• Distorted capital

allocation• Skills mismatch

PoliticalInstability

and Conflict

Public Order &

Enforcement

State Functions

5

… and can hinder sound monetary policy

Because of lower public revenues, countries tend to rely more on seignioragefinance

Fiscal dominance Inflation bias as shown in the figure

Corruption further weakens financial oversight and stability

Poor lending and regulatory practices Weak banking supervision

6

CPI Inflation and Corruption Perception Index 1/

(Average for 1995-2014)

Correlation= 0.426***

-40

-30

-20

-10

0

10

20

30

40-2 -1 0 1 2 3

Cor

rupt

ion

Perc

eptio

n In

dex

2/

CPI Inflation1/ Variables presented are deviations from values predicted by income level.2/ Larger numbers indicate lower perceived levels of public sector corruption. Asterisks from the correlation equation imply significance at 1%.

Corruption hampers market access…

Even market participants appear to factor in corruption into their lending decisions

7

Correlation = 0.488**

-40

-30

-20

-10

0

10

20

30

40-1.5 -1 -0.5 0 0.5 1 1.5

Cor

rupt

ion

Perc

eptio

n In

dex

2/

EM Yield Spread (Basis Points) 1/ Variables presented are deviations from values predicted by income level.2/ Larger numbers indicate lower perceived levels of public sector corruption. Asterisks from the correlation equation imply significance at 5%.

Emerging Market Sovereign Spreads and Corruption Perception Index 1/

(Average for 1995-2014)

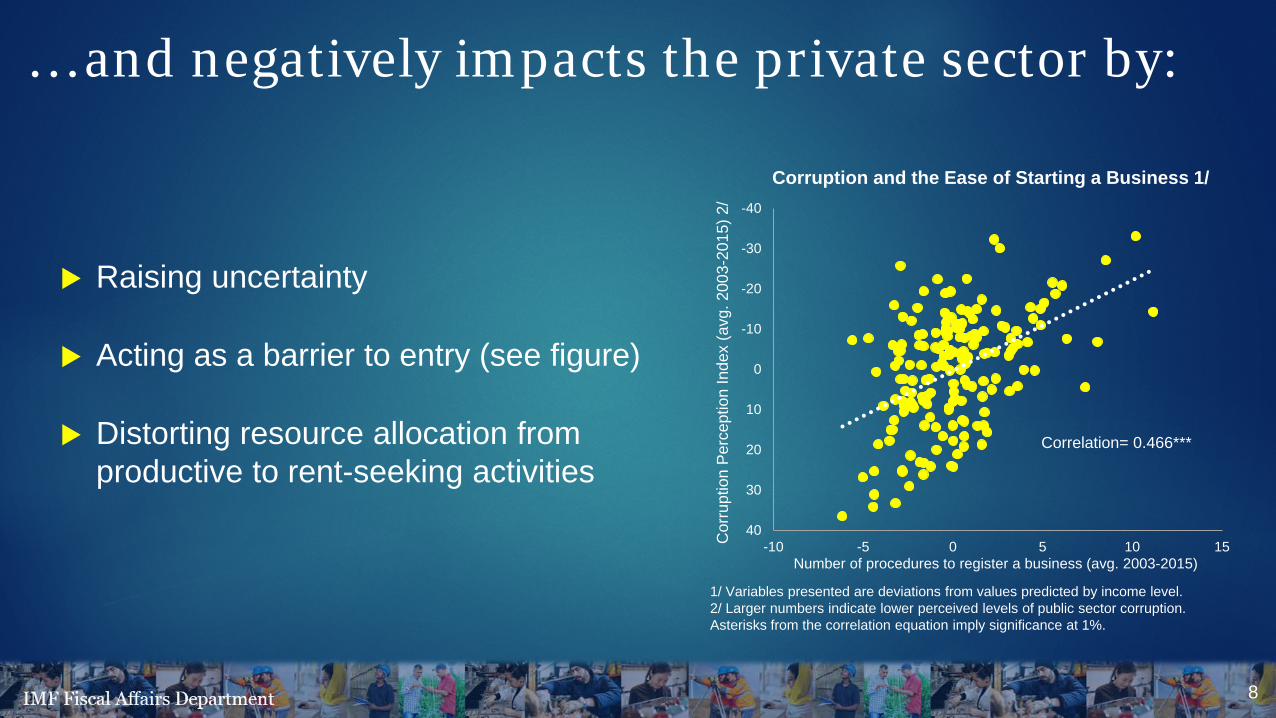

… and negatively impacts the private sector by:

Raising uncertainty

Acting as a barrier to entry (see figure)

Distorting resource allocation from productive to rent-seeking activities

8

Correlation= 0.466***

-40

-30

-20

-10

0

10

20

30

40-10 -5 0 5 10 15C

orru

ptio

n Pe

rcep

tion

Inde

x (a

vg. 2

003-

2015

) 2/

Number of procedures to register a business (avg. 2003-2015)

Corruption and the Ease of Starting a Business 1/

1/ Variables presented are deviations from values predicted by income level.2/ Larger numbers indicate lower perceived levels of public sector corruption. Asterisks from the correlation equation imply significance at 1%.

Corruption is linked to poor social and environmental outcomes

Limits build-up of human capital Through reduced allocations for social programs Compounded by leakages With potential consequences for equality and poverty

9

Studies show that child mortality rates are about one-third higher in countries with high corruption.Infant mortality rates and percent of low-birthweight babies are almost twice as high.

More pollution due to Weaker, poorly enforced environmental regulations Over extraction of natural resources

Political instability and conflict

10

► In the extreme, systemic corruption can lead to political instability and conflict

► It has been argued that natural resource abundance can accentuate the situation

Corruption and Fiscal Policy

Corruption and Expenditure: It undermines quantity and quality of public spending through…

Inflated public procurement costs Siphoning of funds through off-budget transactions Weak payroll controls and Weaknesses in computerized PFM systems

Distorts budget allocations Lower public investment and other priority

spending Lower efficiency of public investment (see figure)

12

Public Investment Efficiency and Corruption Perception Index

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

Corruption Perception Index (avg. 2004-15)

Note: The samples are grouped into high, medium and low corruption in equal numbers based on the Corruption Perception Index. The lines show the range of efficiency for each group. The green and red boxes are the second and third quartile (from the bottom) of the samples, thus the boxes cover 50 percent of the countries.

Publ

ic In

vest

men

t Effi

cien

cyIn

dex

(larg

er n

umbe

rs m

ean

high

er e

ffici

ency

, 0-1

)

High Corruption Medium Corruption Low Corruption

Corruption and taxationCorruption weakens the state’s capacity to raise revenue…

Harms the culture of compliance, increasing tax evasion

As a result, lower revenue limits the ability of the state to provide public services with consequences for growth

More empirical evidence needed…

Several papers document the negative effect of corruption on tax revenues (Friedman, Johnson, Kaufman, and Zoido-Lobaton (2000, JPE), Fjeldstad and Tungodden (2001), Fisman and Svenson (2002), Imam and Jacobs (2007, IMFWP), Besley and Persson (2014, JEP)).

Limited evidence on the transmission mechanisms and the composition effects ((Tanzi and Davoodi (1997), Imam and Jacobs (2007, IMFWP))

Here we report work on taxation and corruption…

Using recently compiled comprehensive dataset of 152 countries covering 1995-2015.

Assess the effects of corruption on tax revenues using disaggregated tax data.

Assess the effects of corruption on specific taxes using micro data derived from new IMF tools

13

Total Tax Revenue

14

0

5

10

15

20

25

30

35

40

0 20 40 60 80

Tax

Rev

enue

(% o

f GD

P)

TI Transparency Index

Total Tax: All Countries

Correlation -0.5175***

Note: Larger numbers on the x-axis indicate higher perceived levels of public sector corruption. Asterisks from the correlation equation imply significance at 1%.

0

5

10

15

20

25

30

35

40

0 20 40 60 80

Tax

Rev

enue

(% o

f GD

P)

TI Transparency Index

Total Tax: Advanced vs. Developing

AdvancedDeveloping

Correlation -0.4754***

Correlation -0.5266***

Taxes on Goods and Services

15

0

2

4

6

8

10

12

14

0 20 40 60 80

Tax

Rev

enue

(% o

f GD

P)

TI Perception Index

VAT Revenue

Correlation -0.3216***

Note:1. Larger numbers on the x-axis indicate higher perceived levels of public sector corruption. 2. Asterisks from the correlation equation imply significance at 1%.3. Data sourced from IMF’s FAD WoRLD Tax Database and Transparency International

0

0.2

0.4

0.6

0.8

1

1.2

0 20 40 60 80 100

C-E

ffici

ency

Rat

io

TI Perception Index

VAT C-Efficiency

Correlation -0.4668***

VAT Policy and compliance gaps

16

Note:1. Data sourced from IMF Revenue Administration’s Fiscal Information Tool (RA-FIT) and Gap program (RA-GAP), and Transparency

International2. Asterisks from the correlation equation imply significance at 1%.

0

1

2

3

4

5

6

7

8

0 20 40 60 80

Com

plia

nce

Gap

TI Perception Index

Correlation 0.5874***

Compliance Gap

0

10

20

30

40

50

60

70

80

0 20 40 60 80

VAT

Ref

und/

VAT

Gro

ss (%

)

TI Perception Index

VAT Refunds Correlation - 0.4301***

Income Tax Revenue

17

0

2

4

6

8

10

12

14

16

0 20 40 60 80

Tax

Rev

enue

(% o

f GD

P)

TI Perception Index

Individual Income Tax

0

1

2

3

4

5

6

7

8

0 20 40 60 80

Tax

Rev

enue

(% o

f GD

P)

TI Perception Index

Corporate Income Tax

Correlation -0.7452*** Correlation -0.0913

Note:1. Larger numbers on the x-axis indicate higher perceived levels of public sector corruption. 2. Asterisks from the correlation equation imply significance at 1%.3. Data sourced from IMF’s FAD WoRLD Tax Database and Transparency International

Other taxes: social security contributions and Trade Tax

18

0

2

4

6

8

10

12

14

16

18

0 50

Tax

Rev

enue

(% o

f GD

P)

TI Perception Index

Social Security Contributions

Correlation -0.4193***

Note:1. Larger numbers on the x-axis indicate higher perceived levels of public sector corruption. 2. Asterisks from the correlation equation imply significance at 1%.3. Data sourced from IMF’s FAD WoRLD Tax Database and Transparency International

0

2

4

6

8

10

12

14

20 40 60 80 100

Tax

Rev

enue

(% o

f GD

P)

TI Perception Index

Trade Tax

Correlation -0.2100***

Trade Efficiency

19

0

5

10

15

20

25

30

35

10 30 50 70 90

Num

ber o

f Day

s

TI Perception Index

All Entry Points

Correlation 0.4217***

Note:1. Larger numbers on the x-axis indicate higher perceived levels of public sector corruption. 2. Asterisks from the correlation equation imply significance at 1%.3. Data sourced from IMF revenue Administration’s Fiscal Information Tool and Transparency International

0

20

40

60

80

100

Air Land Sea

Without Inspection

Low Corruption High Corruption

Air Land Sea

With Inspection

Low Corruption High Corruption

Days To Clear Imports Through Customs

Empirical methodology

Usual regression: 𝒚𝒚𝒊𝒊𝒊𝒊 = 𝜶𝜶 + 𝜷𝜷 ∗ 𝑪𝑪𝑪𝑪𝑪𝑪𝒊𝒊𝒊𝒊 + ∑𝒏𝒏𝒌𝒌 𝜽𝜽𝒌𝒌𝑿𝑿𝒊𝒊𝒊𝒊𝒌𝒌 + 𝜺𝜺𝒊𝒊𝒊𝒊

Data Tax data from IMF databases (WOrLD)

Corruption Perception Index (CPI) from Transparency International

Identification IV pool estimates (more data)

Instrumental variables: Index of ethnolinguistic fractionalization and religion fragmentation.

20

Total Tax Revenue

21

Note:1. Data sourced from IMF’s FAD WoRLD Tax Database and Transparency International2. Asterisks from the correlation equation imply significance at 1%.3. The line graph shows the change in average corruption perception index over time on the secondary axis

Corruption Index Over TimeTotal Tax Revenue

2.60

1.70

2.90 2.95

00.5

11.5

22.5

33.5

44.5

5

Overall 1995-2000 2003-2007 2008-2015Grouping by Time Period

***

***

*** ***

40

45

50

55

60

65

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Change in Revenue after 5 points increase in corruption index

Revenue composition

22

0.65 0.75

0.35

2.10

0.85

0

0.5

1

1.5

2

2.5

3

VAT Individual IncomeTax

Corporate IncomeTax

Social SecurityContributions

Trade Tax

Cha

nge

in T

ax R

even

ue

Tax Type

*** ******

***

***

Change in Revenue after 5 points increase in Corruption index

Note:1. Data sourced from IMF’s FAD WoRLD Tax Database and Transparency International2. Asterisks from the correlation equation imply significance at 1%.

Key messages on taxation and corruption Corruption is associated with weak revenue performance

The impact is felt more on VAT—the tax with most revenue potential. Corruption seems to be having a negative impact on its compliance and implementation

Personal income tax affected more than CIT—this has implications for the progressivity and the design of the tax system.

Surprisingly, social security contributions are strongly affected. More digging is needed to understand this result. This might be related to the extent of informality in the economy.

Trade taxes continue to be affected—as reflected in the delays at clearance points. While the importance of these taxes is declining for many developing countries, there are others such as fragile states where they will remain crucial sources of revenue.

23

Strategies for Addressing CorruptionTransparency, Rule of Law, Economic

Reform and Regulation, Building Institutions

Fund Experience: four main areas

25

1. Transparency: providing public with access to information

2. Rule of Law: having a credible threat of prosecution

3. Economic Reform: eliminating excessive regulation

4. Building institutions: all depends on effective institutions

Transparency

GeneralTransparency is a pre-requisite for the proper functioning of the market

It can also be targeted on corruption Development of international standards on fiscal and financial transparency Transparency in extractive industries – these are important because of their

relative share in many economies Supporting international standards on transparent corporate ownership

26

Enhancing the Rule of Law

27

► There must be a credible threat of prosecution

► Sometimes new specialized institutions must be set up where existing ones are themselves corrupt

► An effective anti-money laundering framework must be in place to minimize the laundering of proceeds of corruption

► Enforcement must also target the private sector

Economic Reform

28

Eliminating Excessive Regulation

Excessive regulation is an important source of corruption (Anne Krueger: “rent seeking”)Elimination of excessive regulation and simplification are a cornerstone of anti-corruption strategy (i.e., Ukraine Caribbean, MENA countries).

However, it is important to have an adequate institutional framework in place first when transitioning from state controlled monopolistic markets. (i.e., emerging economies in Eastern Europe)

Building InstitutionsThe key issue is implementation, for which institutions are critical. Four building blocks for effective institutions.

A clear legal framework is requiredFor example: an independent central bank (mandate, oversight, operational and financial autonomy, appointment criteria, dismissal rules, legal protection of staff)

With adequate technical expertiseInstitutions cannot be effective without requisite technical competence

And the right incentive package for non-corrupt behaviorFor example: securing wage adequacy in combination with effective dismissal procedures

With a critical role of leadershipFor example: both setting a personal example and ensuring decisive action

29

Conclusion

Public sector corruption substantially impairs key channels influencing inclusive growth.

Fighting corruption calls for a long term and holistic strategy, albeit appropriately sequenced based on country-specific circumstances.

A crisis can be a catalyst for change; but a crisis setting generally does not permit for full resolution. Determined leadership over time is a key underlying factor.

30

Appendix Tables

31

32

First stageDpdt var.

(1) (2)

Ethno. Fraction. 46.5369*** 18.3044***(1.690) (1.421)

Religion Fragm. -11.0884*** -9.8781***(1.988) (1.320)

Openness -0.1159(0.590)

Log. of Inflation 3.0531***(0.310)

Share of Agric. 17.3537***(3.660)

Log. GDPpc PPP 64.8744***(3.947)

Log. GDPpc PPP 2̂ -4.1659***(0.226)

Constant 40.9355*** -179.5068***(1.123) (17.705)

Observations 1,934 1,934R-squared 0.262 0.672Standard errors in parentheses*** p<0.01, ** p<0.05, * p<0.1

AllCorr. percep. index

33

Corruption and TaxationDpdt var.

(1) (2) (3) (4)

Corr. percep. index -0.0052*** -0.0113*** -0.0005** -0.0005*(0.000) (0.001) (0.000) (0.000)

Corr. percep. indexAE -0.0034*** -0.0002(0.001) (0.000)

Openness 0.0045 0.0036 0.0211*** 0.0212***(0.006) (0.007) (0.008) (0.008)

Log. of Inflation 0.0142*** 0.0168*** -0.0005 -0.0005(0.003) (0.004) (0.001) (0.001)

Share of Agric. -0.1029*** 0.0642 -0.0499 -0.0498(0.032) (0.051) (0.044) (0.044)

Log. GDPpc PPP 0.3204*** 0.3395*** 0.2004*** 0.1993***(0.031) (0.050) (0.040) (0.041)

Log. GDPpc PPP 2̂ -0.0205*** -0.0220*** -0.0102*** -0.0101***(0.002) (0.003) (0.002) (0.002)

Constant -0.6494*** -0.3095* -0.7652*** -0.7538***(0.116) (0.166) (0.189) (0.192)

Observations 1,934 1,934 1,952 1,952R-squared 0.174 0.174AP 97.67 17.58PvalAP 0 0CD 101.2 15.83Standard errors in parentheses*** p<0.01, ** p<0.05, * p<0.1

Total Tax RevenueAll

IV Pool FE

34

Income and Geographical differencesDpdt var.

(1) (2) (3) (4) (5) (6)

Corr. percep. index -0.0113*** -0.0079*** -0.0045*** -0.0050*** -0.0053*** -0.0049***(0.001) (0.001) (0.000) (0.000) (0.000) (0.000)

Corr. percep. Index*AE -0.0034***(0.001)

Corr. percep. Index*DC 0.0034***(0.001)

Corr. percep. Index*CIS 0.0033***(0.000)

Corr. percep. Index*LAC -0.0008***(0.000)

Corr. percep. Index*MENA -0.0004*(0.000)

Corr. percep. Index*SSA 0.0002(0.000)

Constant -0.3095* -0.6448*** -0.3393*** -0.7679*** -0.6325*** -0.6553***(0.166) (0.176) (0.106) (0.114) (0.128) (0.115)

Observations 1,934 1,934 1,934 1,934 1,934 1,934AP 17.58 17.58 60.79 65.60 58.39 53.82PvalAP 0 0 0 0 0 0CD 15.83 15.83 66.28 55.22 46.70 59.17Standard errors in parentheses*** p<0.01, ** p<0.05, * p<0.1

Total Tax RevenueAll

35

Corruption and TaxationDpdt var.

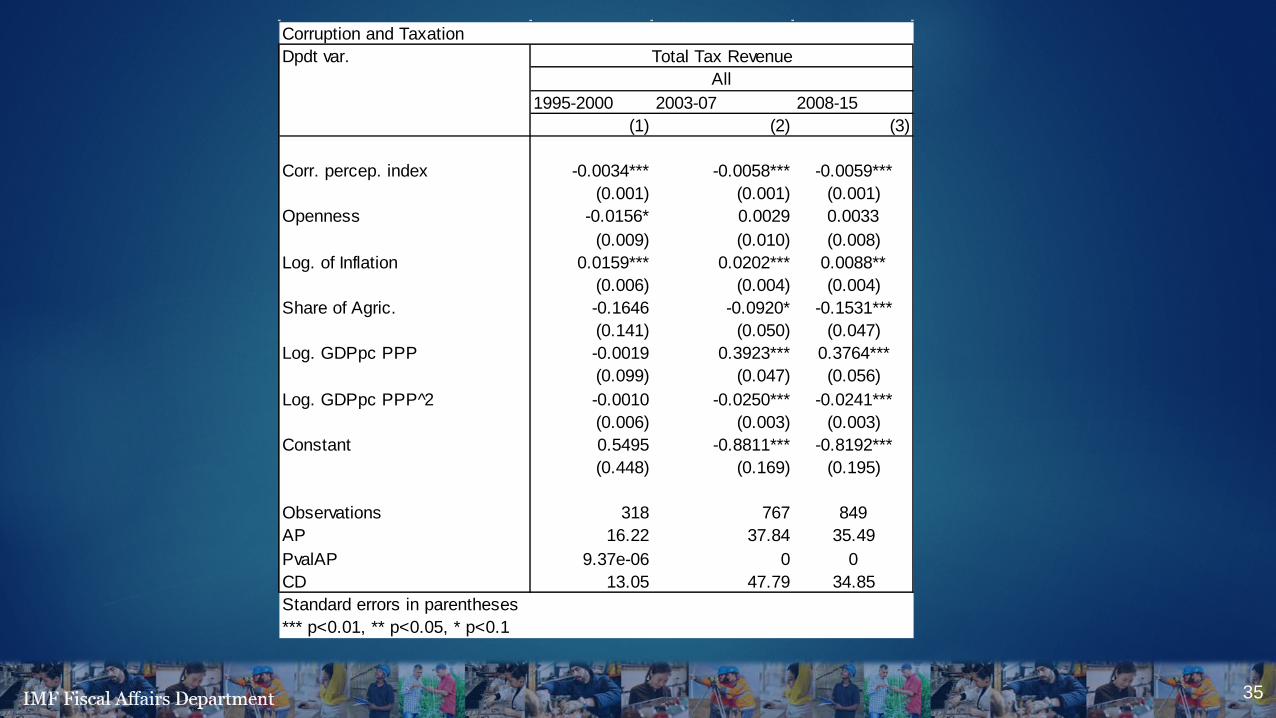

1995-2000 2003-07 2008-15(1) (2) (3)

Corr. percep. index -0.0034*** -0.0058*** -0.0059***(0.001) (0.001) (0.001)

Openness -0.0156* 0.0029 0.0033(0.009) (0.010) (0.008)

Log. of Inflation 0.0159*** 0.0202*** 0.0088**(0.006) (0.004) (0.004)

Share of Agric. -0.1646 -0.0920* -0.1531***(0.141) (0.050) (0.047)

Log. GDPpc PPP -0.0019 0.3923*** 0.3764***(0.099) (0.047) (0.056)

Log. GDPpc PPP 2̂ -0.0010 -0.0250*** -0.0241***(0.006) (0.003) (0.003)

Constant 0.5495 -0.8811*** -0.8192***(0.448) (0.169) (0.195)

Observations 318 767 849AP 16.22 37.84 35.49PvalAP 9.37e-06 0 0CD 13.05 47.79 34.85Standard errors in parentheses*** p<0.01, ** p<0.05, * p<0.1

Total Tax RevenueAll

36

Corruption and Goods and Services taxesDpdt var. Goods and

Services TaxVAT Excise Tax VAT C-efficiency

(1) (2) (3) (4)

Corr. percep. index -0.0009*** -0.0013*** -0.0001 0.0030*(0.000) (0.000) (0.000) (0.002)

Openness 0.0008 0.0135*** 0.0013 0.0988***(0.002) (0.002) (0.001) (0.011)

Log. of Inflation 0.0019* 0.0021** -0.0002 -0.0086(0.001) (0.001) (0.001) (0.007)

Share of Agric. -0.0432*** 0.0065 0.0024 -0.1409(0.014) (0.016) (0.006) (0.106)

Log. GDPpc PPP 0.1448*** 0.1709*** 0.0284** 0.3489*(0.021) (0.023) (0.012) (0.204)

Log. GDPpc PPP 2̂ -0.0086*** -0.0103*** -0.0015* -0.0133(0.001) (0.001) (0.001) (0.012)

Constant -0.4754*** -0.5662*** -0.1067*** -1.8141**(0.078) (0.086) (0.040) (0.748)

Observations 1,654 1,388 1,574 1,091AP 48.80 48.28 50.19 41.05PvalAP 0 0 0 0.138CD 42.22 36.26 38.82 32.49Standard errors in parentheses*** p<0.01, ** p<0.05, * p<0.1

37

Corruption and Income TaxDpdt var. Income Tax Individual Income Tax Corporate Income Tax

(2) (3) (4)

Corr. percep. index -0.0009*** -0.0015*** 0.0007***(0.000) (0.000) (0.000)

Openness -0.0134*** -0.0125*** 0.0038***(0.002) (0.002) (0.001)

Log. of Inflation 0.0026** 0.0018* 0.0006(0.001) (0.001) (0.001)

Share of Agric. -0.0589*** -0.0404*** -0.0127(0.018) (0.013) (0.017)

Log. GDPpc PPP -0.1108*** -0.0751*** -0.0468**(0.026) (0.029) (0.021)

Log. GDPpc PPP 2̂ 0.0069*** 0.0041** 0.0035***(0.002) (0.002) (0.001)

Constant 0.5786*** 0.4865*** 0.1278(0.094) (0.094) (0.083)

Observations 1,684 1,432 1,508AP 49.95 28.60 42.79PvalAP 0.00812 1.04e-05 2.60e-05CD 40.70 19.50 31.02Standard errors in parentheses*** p<0.01, ** p<0.05, * p<0.1

38

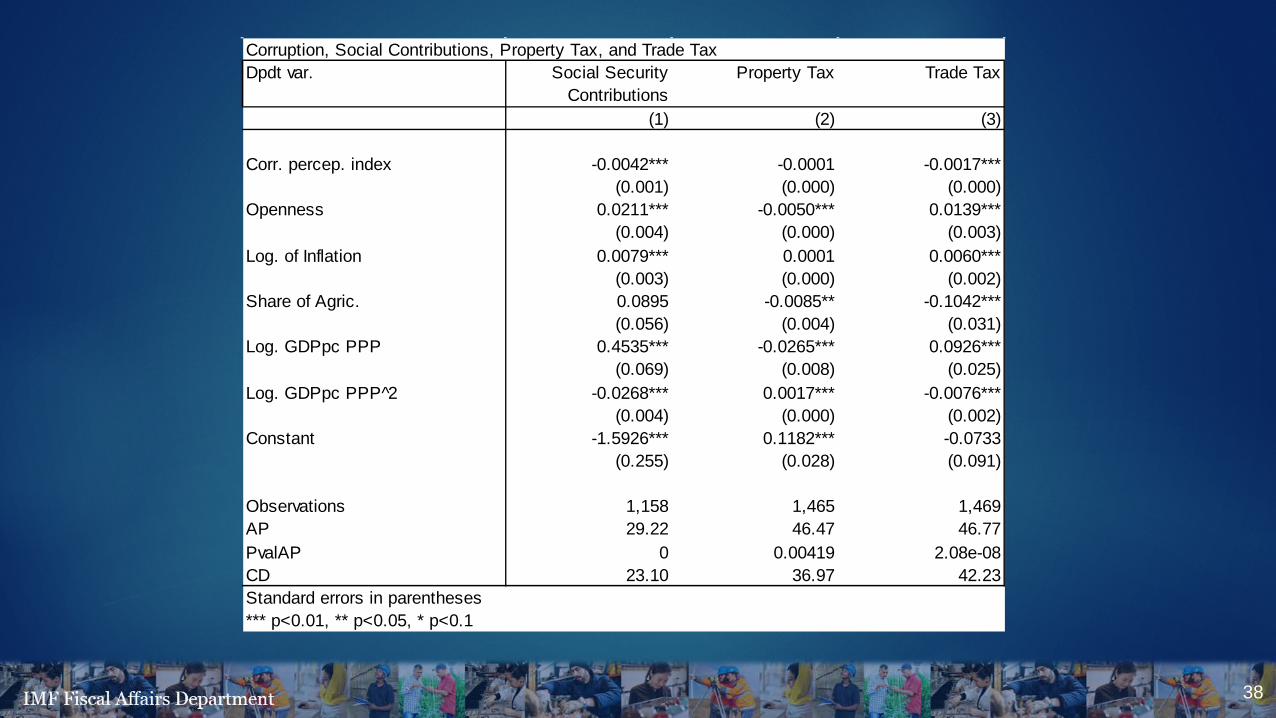

Corruption, Social Contributions, Property Tax, and Trade TaxDpdt var. Social Security

ContributionsProperty Tax Trade Tax

(1) (2) (3)

Corr. percep. index -0.0042*** -0.0001 -0.0017***(0.001) (0.000) (0.000)

Openness 0.0211*** -0.0050*** 0.0139***(0.004) (0.000) (0.003)

Log. of Inflation 0.0079*** 0.0001 0.0060***(0.003) (0.000) (0.002)

Share of Agric. 0.0895 -0.0085** -0.1042***(0.056) (0.004) (0.031)

Log. GDPpc PPP 0.4535*** -0.0265*** 0.0926***(0.069) (0.008) (0.025)

Log. GDPpc PPP 2̂ -0.0268*** 0.0017*** -0.0076***(0.004) (0.000) (0.002)

Constant -1.5926*** 0.1182*** -0.0733(0.255) (0.028) (0.091)

Observations 1,158 1,465 1,469AP 29.22 46.47 46.77PvalAP 0 0.00419 2.08e-08CD 23.10 36.97 42.23Standard errors in parentheses*** p<0.01, ** p<0.05, * p<0.1